Embed Size (px)

Citation preview

BDB India Private Limited

BDB India Private Limited

Impact of electric vehicles on the automotive ecosystem

India is poised to soar, higher than many fast-growing large economies over the next decade. At

the same time, automotive original equipment manufacturers (OEMs) and component

manufacturers in the country aspire to achieve global eminence.

The future of the auto OEM and auto component industry is being shaped by multiple trends,

policies and discontinuities.

The Indian automotive OEM industry is already in a strong position. Globally, it is at the forefront

of many segments—leading in two-wheelers, segment A cars, and tractors. The industry aspires to

nearly triple vehicle sales by 2026, from 26 mn to 76 mn vehicles in 2026, across segments. India

is renowned as a global hub for frugal and scalable engineering.

Busy automotive clusters across India drive the industry— especially the three major clusters of

Mumbai–Pune–Nasik–Aurangabad in the West, Chennai–Bangalore–Hosur in the South, and

Delhi–Gurgaon–Faridabad in the North,14 as well as upcoming areas like Sri City, Anantapur and

Sanand.

These could be definitive tailwinds for the Indian automotive components industry, which has

ambitions of its own by 2026—to double the contribution to manufacturing GDP with a four-fold

growth in size and a six-fold growth in exports.

The auto component industry’s turnover increased from ₹ 1.1 lakh cr (US$ 24 bn) in FY 2009, to ₹

3.5 lakh cr (US$ 51.2 bn) in FY 2018. While industry turnover has more than tripled (in Rupee

terms) in the past decade, India’s contribution to global turnover is approximately 3%.

Autonomous vehicles, connected vehicles, Electrification and Shared Mobility (ACES) are very

real, disruptive and technology-driven trends that could change the future of the mobility industry.

India already has more than 50 startups working on innovative ACES technologies across cars,

two-wheelers and commercial vehicles.

These technologies are gaining ground due to increasing customer acceptance, stricter emission

regulations, lower battery costs and more widely available charging infrastructure.

By 2030, various estimates expect that the share of EVs in global markets could be upwards of

30% of all new vehicle sales, edging into the market share of traditional vehicles. By that time,

shared mobility and connected vehicles could contribute US$ 1,575 bn to automotive revenues, a

critical chunk of overall revenues of US$ 6,600 bn.

A leading shared mobility company took more than eight years to complete its first 5 bn rides, and

then in just over one year, doubled the number of rides. In India, shared mobility providers saw a

four-fold rise in ride volumes between 2015 and 2016. With EVs likely to make these services

cheaper, the figures are only expected to increase.

Impact of Electric Vehicles on the Automotive Ecosystem

Automakers are

realizing that surge is arriving sooner

than expected paving the way for new internal power

centers and external

partnerships

Automakers

The dealer business model will undergo changes as electric

vehicle maintenance costs are expected to be lower than those of conventional cars

Dealers

Powertrain-related suppliers will need

to reinvent themselves to be relevant in the

future

Suppliers

Customers prefer vehicles that are fun to drive and

packed with latest technology and

features

End Customers

Governments may

bank on electric vehicles to meet

their climate change goals

Government Regulations

BDB India Private Limited

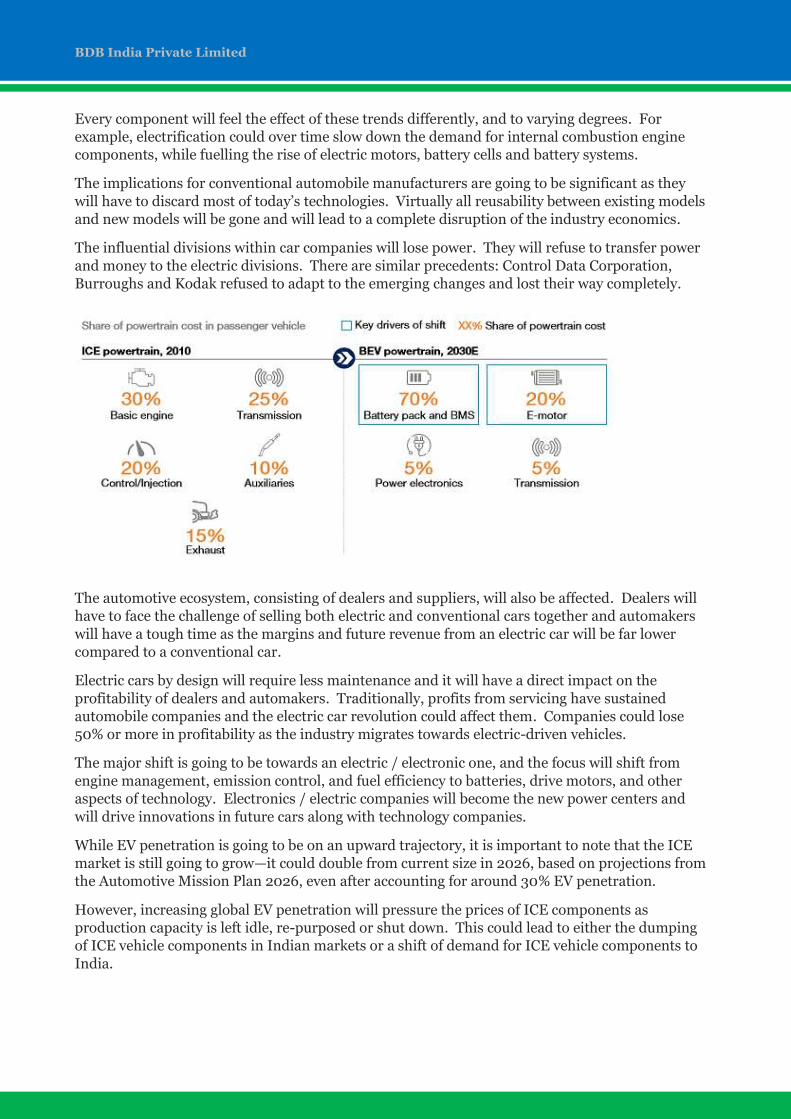

Every component will feel the effect of these trends differently, and to varying degrees. For

example, electrification could over time slow down the demand for internal combustion engine

components, while fuelling the rise of electric motors, battery cells and battery systems.

The implications for conventional automobile manufacturers are going to be significant as they

will have to discard most of today’s technologies. Virtually all reusability between existing models

and new models will be gone and will lead to a complete disruption of the industry economics.

The influential divisions within car companies will lose power. They will refuse to transfer power

and money to the electric divisions. There are similar precedents: Control Data Corporation,

Burroughs and Kodak refused to adapt to the emerging changes and lost their way completely.

The automotive ecosystem, consisting of dealers and suppliers, will also be affected. Dealers will

have to face the challenge of selling both electric and conventional cars together and automakers

will have a tough time as the margins and future revenue from an electric car will be far lower

compared to a conventional car.

Electric cars by design will require less maintenance and it will have a direct impact on the

profitability of dealers and automakers. Traditionally, profits from servicing have sustained

automobile companies and the electric car revolution could affect them. Companies could lose

50% or more in profitability as the industry migrates towards electric-driven vehicles.

The major shift is going to be towards an electric / electronic one, and the focus will shift from

engine management, emission control, and fuel efficiency to batteries, drive motors, and other

aspects of technology. Electronics / electric companies will become the new power centers and

will drive innovations in future cars along with technology companies.

While EV penetration is going to be on an upward trajectory, it is important to note that the ICE

market is still going to grow—it could double from current size in 2026, based on projections from

the Automotive Mission Plan 2026, even after accounting for around 30% EV penetration.

However, increasing global EV penetration will pressure the prices of ICE components as

production capacity is left idle, re-purposed or shut down. This could lead to either the dumping

of ICE vehicle components in Indian markets or a shift of demand for ICE vehicle components to

India.

BDB India Private Limited

Electric vehicles will be able to innovate faster

Compared to internal combustion engine vehicles, electric vehicles have a significant advantage -

battery technology developments are faster than those of the engine technology on gasoline-based

vehicles.

In addition, the trend of packing electronics in today’s automobiles shows that innovations in

electronics will outpace other innovations. The amount of electronics in an electric vehicle is high

compared to conventional vehicles. It offers opportunities for more innovations. The electric car of

the future will be a true computer on wheels and will change the character of the automobile.

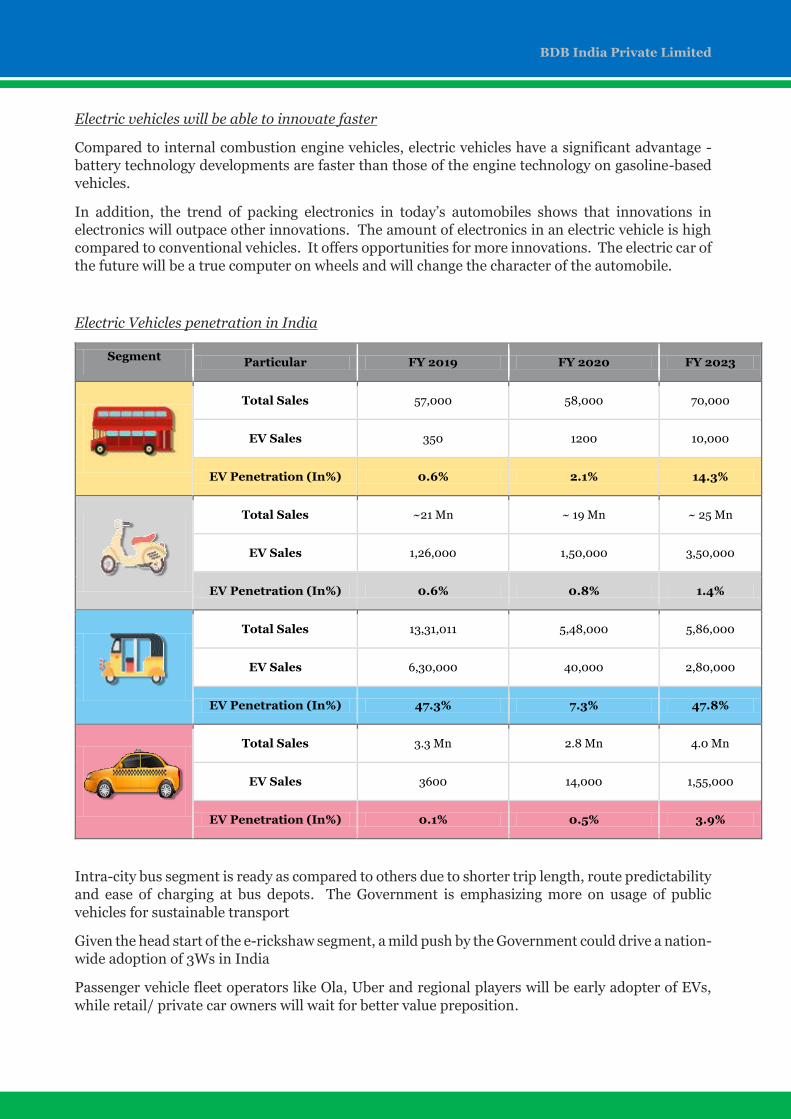

Electric Vehicles penetration in India

Intra-city bus segment is ready as compared to others due to shorter trip length, route predictability

and ease of charging at bus depots. The Government is emphasizing more on usage of public

vehicles for sustainable transport

Given the head start of the e-rickshaw segment, a mild push by the Government could drive a nation-

wide adoption of 3Ws in India

Passenger vehicle fleet operators like Ola, Uber and regional players will be early adopter of EVs,

while retail/ private car owners will wait for better value preposition.

Segment Particular FY 2019 FY 2020 FY 2023

Total Sales 57,000 58,000 70,000

EV Sales 350 1200 10,000

EV Penetration (In%) 0.6% 2.1% 14.3%

Total Sales ~21 Mn ~ 19 Mn ~ 25 Mn

EV Sales 1,26,000 1,50,000 3,50,000

EV Penetration (In%) 0.6% 0.8% 1.4%

Total Sales 13,31,011 5,48,000 5,86,000

EV Sales 6,30,000 40,000 2,80,000

EV Penetration (In%) 47.3% 7.3% 47.8%

Total Sales 3.3 Mn 2.8 Mn 4.0 Mn

EV Sales 3600 14,000 1,55,000

EV Penetration (In%) 0.1% 0.5% 3.9%

BDB India Private Limited

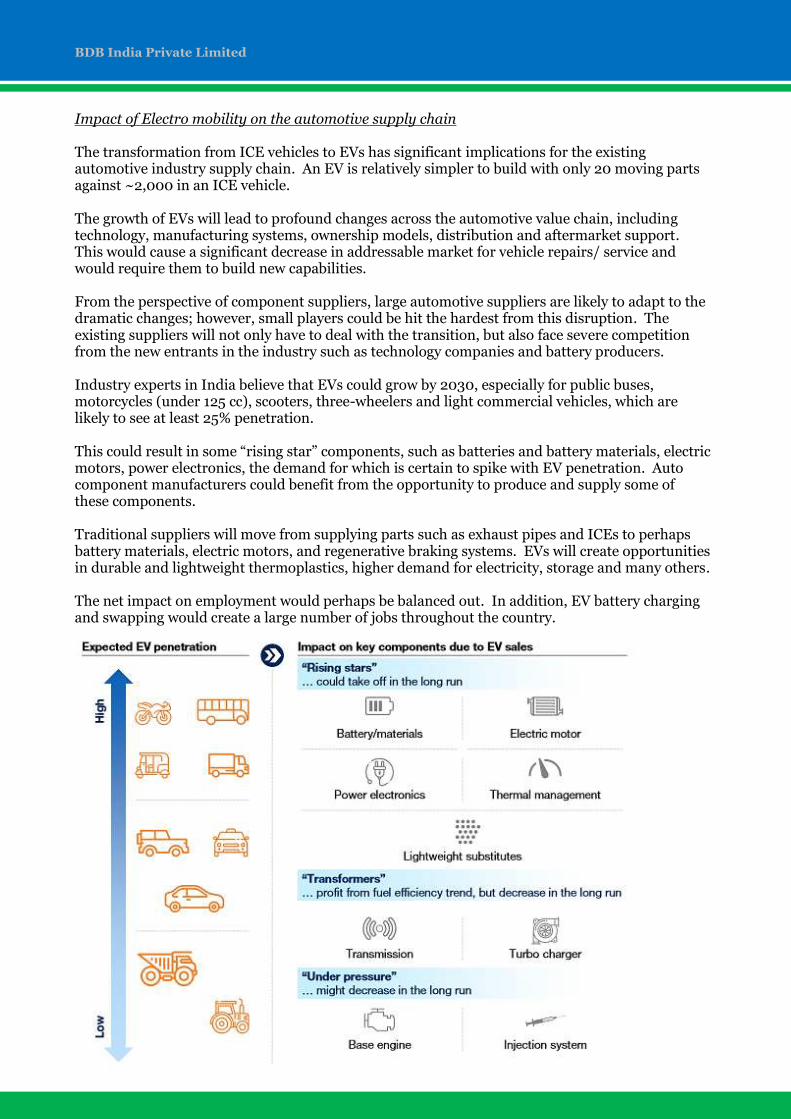

Impact of Electro mobility on the automotive supply chain The transformation from ICE vehicles to EVs has significant implications for the existing automotive industry supply chain. An EV is relatively simpler to build with only 20 moving parts against ~2,000 in an ICE vehicle. The growth of EVs will lead to profound changes across the automotive value chain, including technology, manufacturing systems, ownership models, distribution and aftermarket support. This would cause a significant decrease in addressable market for vehicle repairs/ service and would require them to build new capabilities. From the perspective of component suppliers, large automotive suppliers are likely to adapt to the dramatic changes; however, small players could be hit the hardest from this disruption. The existing suppliers will not only have to deal with the transition, but also face severe competition from the new entrants in the industry such as technology companies and battery producers. Industry experts in India believe that EVs could grow by 2030, especially for public buses, motorcycles (under 125 cc), scooters, three-wheelers and light commercial vehicles, which are likely to see at least 25% penetration. This could result in some “rising star” components, such as batteries and battery materials, electric motors, power electronics, the demand for which is certain to spike with EV penetration. Auto component manufacturers could benefit from the opportunity to produce and supply some of these components. Traditional suppliers will move from supplying parts such as exhaust pipes and ICEs to perhaps battery materials, electric motors, and regenerative braking systems. EVs will create opportunities in durable and lightweight thermoplastics, higher demand for electricity, storage and many others. The net impact on employment would perhaps be balanced out. In addition, EV battery charging and swapping would create a large number of jobs throughout the country.

BDB India Private Limited

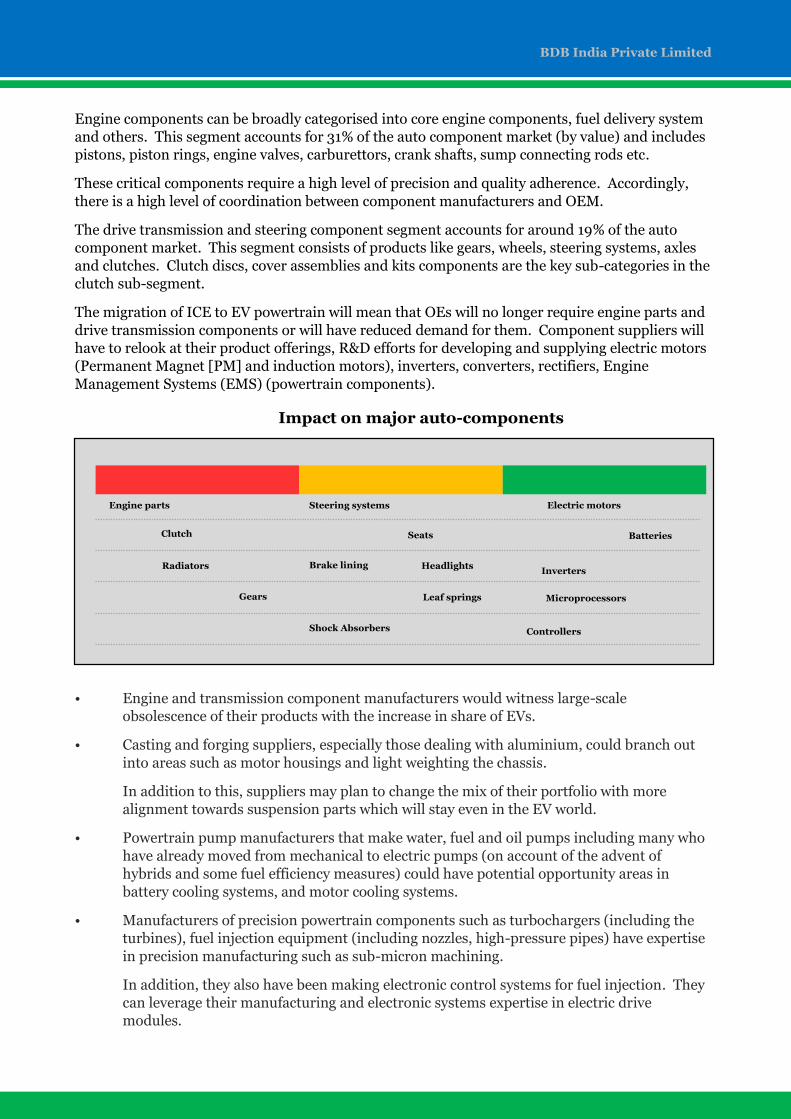

Engine components can be broadly categorised into core engine components, fuel delivery system

and others. This segment accounts for 31% of the auto component market (by value) and includes

pistons, piston rings, engine valves, carburettors, crank shafts, sump connecting rods etc.

These critical components require a high level of precision and quality adherence. Accordingly,

there is a high level of coordination between component manufacturers and OEM.

The drive transmission and steering component segment accounts for around 19% of the auto

component market. This segment consists of products like gears, wheels, steering systems, axles

and clutches. Clutch discs, cover assemblies and kits components are the key sub-categories in the

clutch sub-segment.

The migration of ICE to EV powertrain will mean that OEs will no longer require engine parts and

drive transmission components or will have reduced demand for them. Component suppliers will

have to relook at their product offerings, R&D efforts for developing and supplying electric motors

(Permanent Magnet [PM] and induction motors), inverters, converters, rectifiers, Engine

Management Systems (EMS) (powertrain components).

• Engine and transmission component manufacturers would witness large-scale

obsolescence of their products with the increase in share of EVs.

• Casting and forging suppliers, especially those dealing with aluminium, could branch out

into areas such as motor housings and light weighting the chassis.

In addition to this, suppliers may plan to change the mix of their portfolio with more

alignment towards suspension parts which will stay even in the EV world.

• Powertrain pump manufacturers that make water, fuel and oil pumps including many who

have already moved from mechanical to electric pumps (on account of the advent of

hybrids and some fuel efficiency measures) could have potential opportunity areas in

battery cooling systems, and motor cooling systems.

• Manufacturers of precision powertrain components such as turbochargers (including the

turbines), fuel injection equipment (including nozzles, high-pressure pipes) have expertise

in precision manufacturing such as sub-micron machining.

In addition, they also have been making electronic control systems for fuel injection. They

can leverage their manufacturing and electronic systems expertise in electric drive

modules.

Wiring harnesses

Negative impact Neutral Positive impact

Engine parts

Clutch

Radiators

Gears

Steering systems

Seats

Brake lining Headlights

Leaf springs

Shock Absorbers

Electric motors

Batteries

Inverters

Microprocessors

Controllers

Impact on major auto-components

BDB India Private Limited

• Electrical component makers including those supplying wire harnesses and switches could

see a huge opportunity as the length of the wire harness in an EV is three times as much as

in a conventional ICE vehicle.

This, coupled with the fact that wire harness manufacturing is relatively labour-intensive,

could certainly hold tremendous opportunities for players in India.

• Cooling system manufacturers engaged in the manufacture of heat exchangers/radiators

could see an upside in battery/motor cooling areas.

Thermal management of battery and motor/electronics is very crucial in EVs as the

performance of the battery is totally dependent on the operating temperature.

• After-treatment system manufacturers, the majority of whom cater to canning part of the

after-treatment value chain, could use competencies in sheet metal fabrication,

electroplating and mechatronics in EVs as well.

The ability to apply a thin layer of metal can be used in EV wirings as they are a little

different from conventional vehicles.

• Manufacturers of fuel tanks, most of which have become plastic, could use their

competencies in heat, impact-resistant plastics for developing tanks for housing cooling

fluid in the battery cooling circuit, especially since they have competencies to make tanks

in various shapes for packaging in the limited space available.

• HVAC system manufacturers would see a shift in the need for thermal management in a

vehicle. The conventional heaters may need to be upgraded especially since the large heat

source in the form of an IC engine would not be available.

This will require separate electric heaters. The AC functionality is expected to remain

same.

Likely scenario in case significant of EV adoption in India

1. OEMs likely to lose some control in the EV value chain:

EVs are less complex to manufacture as compared to ICE vehicles with far fewer moving

components and the battery constituting more than 50% of the value of vehicle. This

would result in a dilution of control for the OEMs.

2. Significant changes in component manufacturers’ portfolios:

Existing powertrain-related suppliers would lose markets, making them significantly

smaller in an all-EV scenario. Whereas new opportunities lie in EV parts such as battery,

motors, controllers and microprocessors.

3. Lack of battery manufacturing capabilities in the country to lead to more partnerships and

collaborations:

As EVs gain traction in India, OEMs need to look to secure access to Li-ion reserves and

R&D capabilities to manufacture batteries indigenously. Hence, a number of foreign

collaborations, partnerships and consortiums between OEMs, battery producers and

suppliers could be expected.

BDB India Private Limited

Key implications to current automotive players:

1. OEMs need to reinvent their business to focus on building relationships with battery and

electric/electronics component suppliers and also explore opportunities for in-house

battery manufacturing.

2. Given the ease of manufacturing of EVs combined with a larger trend of increased vehicle

sharing, there is a risk of vehicles getting commoditized and thus an increased focus on

OEM brand differentiation would be required.

3. Component manufacturers need to re-align their product portfolios as the industry

transitions to EVs. Given EVs are a cross-sector play, new sources of value creation will

need to be discovered and the pecking order of the industry participants will get redrawn

Impact on automotive dealers

The average ratio of car sales to car service in India is 1:15, which means that for every 1 car sold,

15 cars are serviced. Aftersales and servicing is crucial for dealer profitability as they bring

footfalls and significant revenues.

However, the powertrain migration from ICE to electric will have a significant impact on the

serviceability of the platforms as there will be fewer moving parts.

The country’s top two OEMs, Maruti Suzuki and Hyundai Motor India, together service over

66,000 cars daily. There will be significant downsizing of technicians in the coming years as the

viability of dealerships will be questioned

BDB India Private Limited

Automotive players in India could expand their play in these times of disruption through the

following focus areas:

Change the mix in the ecosystem: The entry of EVs in the automotive landscape could change the

balance of the industry. OEMs and suppliers may need to start competing for new sources of value

addition to maintain their profit pools.

Many unconventional partnerships are emerging, such as the foray of global tier-1 auto suppliers

into the EV battery business via joint ventures with cell makers. Many EV startups have also

mushroomed in the recent past, inspired to replicate the success of a few players.

OEMs and component players in India need to figure out opportunities to protect and expand

their market share. There are early signs of resilience across segments—a leading two-wheeler

manufacturer has invested in a start-up to manufacture affordable electric two-wheelers. A

hardware startup has developed a premium scooter that uses an in-house lithium-ion battery and

can charge to 80% in under an hour. Similar innovations are needed across the EV ecosystem.

As an example, in China, incumbents and new attackers are expanding their play across the EV

supply chain—from developing batteries to offering services like charging. Interestingly, the

established players and EV specialists are trying to develop a presence across most parts of the

value chain, while emerging players are selective about their role—venturing into areas like design

and engineering, marketing and sales, distribution and charging services.

Build new competencies: As EVs take off in India, most automotive players may need greater

access to new technical talent not only in software and power electronics but also across

commercial and supply chain functions.

In addition, there could be a need to build new technology assets like testing facilities, rapid

prototyping, and product/ UI design capabilities. Automotive players in India need to assess such

needs and find ways to build EV competencies in their existing talent pool or acquire from outside.

Improve performance: This could include reducing battery cost and charging time, and increasing

EV driving range. Globally, battery prices are dropping due to technology and scale

improvements—this could affect battery prices in India as well.

Additionally, automotive players in India could explore ways to make charging as convenient as

refuelling. Battery swapping could be a solution, especially for public transport vehicles like buses

and three-wheelers, where product standardization is easier (subject to charging time, ease of

swapping, scheduling and routing of vehicles).

Build scale: Battery and EV component manufacturers in India need to figure out strategies to

develop scale and to make local manufacturing feasible. Leading battery manufacturers have a

different point of view on scale.

According to one estimate, approximately 3 GWh of cell production facility is needed to gain

economies of scale in battery cell production. Another global battery manufacturer puts the figure

at a minimum of 10 GWh. Going with the conservative estimate of 10 GWh, approximately

200,000 to 500,000 four wheelers (10-20 kWh) and 1.5 million to 2 million two wheelers (3 kWh)

sold in a year need to be electric to create the required scale. This seems achievable even excluding

the replacement battery demand.

BDB India Private Limited

The road ahead for auto component manufacturers

There is no denying that e-mobility is here and now, and that its growth could impact auto

component manufacturers in India in a big way. It is imperative for auto component

manufacturers to start preparing for the ensuing disruption. They could consider a three step

roadmap to smoothly transition into the EV way:

Acknowledge and move fast: While three-wheelers and buses are expected to be electrified in the

first wave, the second wave will see scooters, taxis and small and light commercial vehicles going

the EV way. This will eventually be followed by private cars and other vehicle segments.

As a result, there could be a gradual transition away from ICE vehicles across various segments

giving auto component suppliers some time to transition to a different product mix. However, as

the supply–demand balance shifts, auto component manufacturers need to brace for significantly

lean operations in ICE vehicle components.

Re-invent the business, including collaborating with OEMs/other manufacturers across the global

industry: It might be a big challenge for an individual player to take control of the EV market.

Auto component manufacturers could benefit by collaborating among themselves and with OEMs

to chart out their EV path, and accordingly define individual strategies.

It might be timely to get started on this, as the prudent players have already started forming

partnerships. As automotive players in India seek the best business model, it is important to

remember that models that have worked in the past and in other geographies may not necessarily

be the best solution for markets in India.

Build the right assets and skills to serve the needs of the new age industry: Auto component

manufacturers could need access to new assets (e.g., new prototyping and testing facilities) and

skills (across diverse functions like engineering, sourcing, marketing, investments/M&A) in order

to thrive in the new ecosystem. It is imperative that they think about it and chart out detailed

plans to build or acquire such assets and skills.

BDB India Private Limited

About BDB

BDB India Private Limited is a business consulting and market research company headquartered in Pune, India. We have been working with customer driven and market oriented organizations over the last 30 years. Our consulting and research experience includes every major vertical in the B2B Industrial sector; Healthcare and the Agricultural sector. BDB has time and again displayed exceptional ability to map patterns and trends through our customized studies and developed winning strategies for entering and succeeding in markets such as South Asia, South East Asia, the Middle East & Far East (Japan, South Korea, Taiwan) and Africa Regions. BDB recommends specific products (and systems) to promote, geographical regions to start within, point of sale models, pricing, recommends specifications if customization is necessary and aftermarket support. The marketplace is the interface between product and consumer. All market and customer driven business enterprises therefore tailor their strategy, based on the marketplace. As commercial enterprises have to be market and customer driven, BDB's cutting edge inputs to our clients have always resulted in their meeting or exceeding their growth targets and market-leadership aims. Business research and Strategy is an intricate, involved and specialised subject and specialization cannot be mass produced. Every specialization needs expertise, dedication, commitment and enthusiasm. And at BDB, we pursue our specialization with a passion. We have constituted a fine team, whose talent and honesty of purpose is beyond compare. Researching the market thoroughly, profiling existing customers and potential customers, analysis of product differentiation, technology evaluation, re-evaluating customer needs and creating new markets are important steps towards success. Conversion of these needs into demand and creating an appropriate market interface can lead to sales growth and larger market share. The best result oriented strategy specifically tailored for our clients and for specific product range, requires intricate market research and intimate knowledge about the working of the market place. Our methodology of studying the markets in-depth involves primary research of the stakeholders – buyers, end users, OEMs, consultants, channel partners, competitors, and EPC contractors – the entire value chain. The findings are then analysed leveraging our years of experience. Thanks to the faith entrusted in us by many globally leading multinational companies as well as Indian business groups over quarter of a century; today BDB can carry out in-depth market analysis to map potential opportunities. BDB, an ISO certified company is uniquely qualified, experienced and equipped to design a failsafe growth plan that will achieve business growth. BDB's unique strategy developing expertise, based on in house market research, includes

sectors such as electrical industry, process industry, automotive industry, machine tool

industry, metallurgical industry, plastics and composites industry, HVAC industry,

construction machinery industry, farm equipment industry, industrial chemical sector,

agrochemical industry, pharmaceutical & healthcare sector, domestic appliances market,

international markets as well as qualitative studies involving customer satisfaction

measurement and monitoring in the industrial eco-system.

BDB India Private Limited

BDB's Business Divisions

Industrial

Automotive

Building Management Services

Food processing equipment Construction Equipment

Industrial Consumables Electrical power

Industrial Automation & Electronics and Telecommunication

Instrumentation General Engineering

Machinery & Machine Tools Industrial Chemicals

Metallurgy Marine

HVAC Process Equipment

Oil & Gas Renewable Energy

Plastics & Composites

BDB's Services

MARKET

STAKEHOLDER

MARKETING

CENTRIC

CENTRIC

CENTRIC

• Market Sizing & Potential • Customer Satisfaction & • Direct Marketing

Assessment Monitoring

- Creating Awareness

• Market Entry Strategy

• Vendor Satisfaction

- Credibility Establishment

• Price Sensitivity

• Techno Economic Feasibility • Brand Image - Lead Generation

• Bench Marking Analysis - Sales Connect

(Product, Price, Technology)

• Raw Material & Location

Evaluation

• Partner Identification &

Evaluation

• Export Potential

Healthcare

Medical consumables Medical devices Medical equipment Hospital equipment Hospitals

Agriculture and allied

Farm machinery Fertilizers

Insecticides Micro irrigation Micro nutrients

Pesticides Food and

beverages