Embed Size (px)

Citation preview

SUBJECT: BUSINESS LAWS

B.COM 3rd

Year (2014)

UNIT – I

Elements of Law Relating to Contract under Indian Contract Act, 1872

Indian Contract Act, 1872

The Indian Contract Act, 1872 is one of the oldest in the Indian law regime, passed by the

legislature of pre-independence India; it received its assent on 25th April 1872. The statute

contains essential principles for formation of contract along with law relating to indemnity,

guarantee, bailment, pledge and agency.

Meaning of a valid Contract:

An agreement involves an offer or proposal by one person and acceptance of such offer or

proposal by another person. If the agreement is capable of being enforced by law then it is a

contract. Section 2[h] of Indian Contract Act, 1872 defines the term contract as “an agreement

enforceable by law”.

According to the terms of Section 10 of the Act, an agreement is a valid contract if it is made by

the free consent of the parties competent to contract, for a lawful consideration and with a lawful

object and are not expressly declared to be void.

Essential Elements of a valid Contract

In order to be a valid contract, in the first place there must be an offer and the said offer must

have been accepted. Such offer and acceptance should create legal obligations between parties.

This should result in a moral duty on the person who promises or offers to do something.

Similarly this should also give a right to the promisee to claim its fulfillment. Such duties and

rights should be legal and not merely moral. These elements can be summarized as follows:

1. Intention to create legal obligation through offer and acceptance:

In the first place, there must be an offer and the said offer must have been accepted. Such offer

and acceptance should create legal obligations between parties. This should result in a moral

duty on the person who promises or offers to do something. Similarly this should also give a

right to the promisee to claim its fulfillment. Such duties and rights should be legal and not

merely moral.

2. Free consent of the parties:

The second element is the ‘consent’ of the parties. ‘Consent’ means ‘knowledge and approval’ of

the parties concerned. This can also be understood as identity of minds in understanding the term

viz consensus ad idem. Further such consent must be free. Consent would be considered as free

consent if it is not vitiated by coercion, undue influence, fraud, misrepresentation or mistake.

Wherever the consent of any party is not free, the contract is voidable at the option of that party.

3. Competency or capacity to enter into contract:

Capacity or incapacity of a person could be decided only after reckoning various factors. Section

11 of the Indian Contract Act, 1872 elaborates on the issue by providing that a person who-

a) has not attained the age of majority,

b) is of unsound mind and

c) is disqualified from entering into a contract by any law to which he is subject,

should be considered as not competent to enter into any contract. Therefore, law prohibits

(a) Minors (b) persons of unsound mind and (c) person who are otherwise disqualified like an

alien enemy, insolvents, convicts etc from entering into any contract.

4. Lawful consideration:

‘Consideration’ would generally mean ‘compensation’ for doing or omitting to do an act or deed.

It is also referred to as ‘quid pro quo’ viz ‘something’ in return for another thing’. Such a

consideration should be a lawful consideration.

5. Lawful object:

The last element to clinch a contract is that the agreement entered into for this purpose must not

be which the law declares to be either illegal or void. An illegal agreement is an agreement

expressly or impliedly prohibited by law. A void agreement is one without any legal effects. For

Example: Threat to commit murder or making/publishing defamatory statements or entering into

agreements which are opposed to public policy are illegal in nature.

Types of Contracts:

The following are the main types of contracts:

1. Void Contract

A void contract is one which cannot be enforced by a court of law. As per Section 2 (j) “A

contract which ceases to be enforceable by law becomes void”. For example, a contract becomes

void when any of the following happens:

a. Where both parties to an agreement are under a mistake of fact [Section 20]

b. When the consideration or object of an agreement is unlawful [Section 23],

c. An agreement without consideration [Section 25],

d. An agreement in restraint of marriage [Section 26], trade [Section 27], legal

proceedings [Section 28] and agreement by way of wager [Section 30] are instances of

void contract. 2. Voidable Contract

A voidable contract is one where one of the parties to the agreement is in a position or is legally

entitled or authorized to avoid performing his part. Such a right might arise from the fact that the

contract may have been brought about by one of the parties by coercion, undue influence, fraud

or misrepresentation and hence the other party has a right to treat it as a voidable contract.

Section 2[i] defines a voidable agreement which is enforceable by law at the option of one or

more parties but not at the option of the other or others.

3. Illegal Contracts

Illegal contracts are those that are forbidden by law. All illegal contracts are hence void also.

Because of the illegality of their nature they cannot be enforced by any court of law. Thus,

contracts which are opposed to public policy or immoral are illegal. Similarly contracts to

commit crime like supari contracts are illegal contracts.

4. Express Contracts

A contract would be an express contract if the terms are expressed by words or in writing.

Section 9 of the Act provides that if a proposal or acceptance of any promise is made in words

the promise is said to be express.

5. Implied Contracts

Implied contracts come into existence by implication which is mostly by law and or by action.

Section 9 of the Act contemplates such implied contracts when it lays down that in so far as such

proposal or acceptance is made otherwise than in words, the promise is said to be implied. For

instance ‘A’ delivers goods by mistake at the warehouse of ‘B’ instead of that of ‘C’. Here ‘B’

not being entitled to receive the goods is obliged to return the goods to ‘A’ although there was no

such contract to that effect.

6. Tacit Contracts

Tacit contracts are those that are inferred through the conduct of parties. An example of tacit

contract is where a contract is assumed to have been entered when a sale is given effect to at the

fall of hammer in an auction sale.

7. Executed Contract

The consideration in a given contract could be an act or forbearance. When the act is done or

executed or the forbearance is brought on record, then the contract is an executed contract.

8. Executory Contract

In an executory contract, the consideration is reciprocal promise or obligation. Such

consideration is to be performed in future only and therefore these contracts are described as

executory contracts.

9. Unilateral Contract

Unilateral contracts is a one sided contract in which only one party has to perform his duty or

obligation.

10. Bilateral Conracts

A Bilateral contract is one where the obligation or promise is outstanding on the part of both the

parties.

Performance of Contracts

Performance by all the parties of the respective obligations is the natural and normal mode of

termination or discharging of a contract. Section 37 of the Contract Act, states that the parties to

a contract must either perform or offer to perform their respective promise under the contract. In

case of performance involving personal skill, taste, credit etc., the promisor himself must

perform the contract. In case of contract of impersonal nature, the promisor himself or his agent

must perform the contract, but in case of death of the promisor before the performance, the

liability of performance falls on his legal representative. Section 41 states that if the promisee

accepts the performance of the promise from a third party, he cannot afterwards enforce it

against the promisor.

By Whom a Contract may be Performed

The promise under a contract can be performed by any one of the following:

I. Promisor himself: Invariably the promise has to be performed by the promisor where

the contracts are entered into for performance of personal skills, or diligence or

personal confidence, it becomes absolutely necessary that the promisor performs it

himself.

II. Agent: Where personal consideration is not the foundation of a contract, the

promisor or his representative can employ a competent person to perform it.

III. Representatives: Generally upon the death of promisor, the legal representatives of

the deceased are bound by the promise unless it is a promise for performance

involving personal skill or ability of the promisor.

IV. Third Person: Where a promisee accepts performance from a third party he cannot

afterwards enforce it against the promisor. Such a performance, where accepted by

the promisor has the effect of discharging the promisor though he has neither

authorized nor ratified the act of the third party.

V. Joint promisors: Where two or more persons jointly promise, the promise must be

performed jointly unless a contrary intention appears from the contract.

Termination and Discharge of Contracts

Discharge of a contract implies termination of the contractual relationship between the parties.

On the termination of such relationship, the parties are released from their obligations in the

contract. In this way the contract comes to an end. In other words, a contract is said to be

discharged when the rights and obligations created by the contract are terminated. The contract

may be discharged in any one of the following ways which are known as modes of discharging

contract.

Modes of Discharge of Contract:

A contract can be discharged in the following ways:

1. By performance

2. By mutual agreement

3. By supervening impossibility

4. By operation of law

5. By lapse of time

6. By material alteration

7. By breach of contract

1. Discharge of Contract by Performance:

This is the most popular and usual way of discharging the contract. Performance means

accomplishing of that which is required by a contract. This may be of two types:

i. Actual performance: When both the parties do what they have promised to

do, the contract is said to be performed. In this way both parties get

released from their obligations in that contract, and the contract comes to

an end.

ii. Attempted performance: when the promisor is ready and willing to

perform his promise, but the promisee refuses to accept the performance,

it is known as attempted performance. An attempted performance, to be

legally valid, must have the following requirements:

a. It must be unconditional

b. It must be made at reasonable place and time.

c. Reasonable opportunity to ascertain capability.

d. Reasonable opportunity for inspection of goods.

e. It must have been made to the promisee or proper person.

2. Discharge of contract by Mutual agreement:

A contract is formed when the parties mutually agree on a matter. In the same way both the

parties of a contract may by mutual agreement discharge the contract.

3. Discharge of contract by supervening impossibility:

A contract is discharged due to supervening impossibility under the following situations:

i. Destruction of subject matter of contract

ii. Non existence or non occurrence of a particular state of things

iii. Change of law or stepping in of a person with statutory authority.

iv. Death or personal incapacity of the party.

v. Declaration of war.

4. Discharge of contract by operation of law

A contract may also be discharged by the operation of the law. In these cases, the law comes

into force and the parties are released from their obligations in the contract. Following are the

instances where the contract is discharged by an operation of law:

i. Death of promisor

ii. Insolvency

iii. Merger

iv. Loss of evidence

5. Discharge of contract by lapse of time

The contract must be performed within a stipulated period of time or a reasonable period of

time. If not, the contract will be discharged. Provisions regarding the time factor are provided

in the Indian Limitation Act.

6. Discharge of contract by material alterations

A contract is also discharged when the promisee or his agent makes any material alteration,

without the consent of the other party, in the document containing the contract and its terms

and conditions.

7. Discharge of contract by breach of contract

Breach of contract means refusal of performance on the part of the parties. That means

failure of a party to perform his or her obligation under a contract.

Bailment

Sections 148 to 181 of the Indian Contract Act, 1872 (Chapter IX) deal with contracts of

bailment and pledge. Bailment is the change of possession of goods from one person to another

for some specific purpose. It is defined by Section 148, as the delivery of goods by one person to

another for some purpose, upon a contract that they shall, when the purpose is accomplished, be

returned or otherwise disposed off according to the direction of the person delivering them. The

person delivering the goods is called the ‘“Bailor” and the person to whom the goods are

delivered is called the “Bailee”. For example, if A delivers his car to B, a mechanic for repairs,

then there is a contract of bailment between A and B. Here A is the bailor and B is the bailee.

Characteristics of Bailment

A contract of bailment has the following characteristics:

1. Delivery of goods

2. Agreement

3. Purpose

4. Return of goods

Pledge

Section 72 defines a pledge as ‘the bailment of goods as security for payment of debt or

performance of a promise’. The person who delivers the goods as security is called pledgor

(pawnor) and the person to whom the goods are so delivered is called pledge (pawnee). The

ownership of the goods remains with the pledgor. It is only a qualified property that passes to the

pledge. For example, if A borrows Rs. 25000 from B and keeps his gold ornaments as security, a

contract of pledge arises. Here, A is the pledgor and B is the pledge. Pledges are a form of

security to assure that a person will repay a debt or perform an act under a contract. In a contract

of pledge, one person temporarily gives possession of his property to another party.

Contract of Indemnity

In ordinary parlance, the term indemnity means to make good any loss or to compensate any

person who has suffered some loss. Section 124 of the Act defined a contract of indemnity as a

contract by which one party promises to save the other from a loss caused to him by the conduct

of the promisor himself, or the conduct of any other person. The person who makes the promise

to make good the loss is called the indemnifier. The person whose loss is to be made good is

called indemnity holder.

A contract of indemnity is entered into for compensating losses of the other party that may or

may not occur in future. As such, a contact of indemnity is a type of contingent contract. The

performance of the contract is dependent on happening or non happening of a contingency which

may cause losses to another party.

Contract of Guarantee

A contract of guarantee is a contract to perform the promise made or discharge liability incurred

by a third person in case of his default. The contract of guarantee is made to ensure performance

of a contact or discharge of obligation by the promisor. In case he fails to do so, the person

giving assurance or guarantee becomes liable for such performance or discharge. In a contract of

guarantee there are three parties, namely, the principal debtor, creditor and surety. The principal

debtor is primarily liable to pay and the surety is the person who gives the guarantee.

Characteristics of contract of guarantee

The following the characteristics of a contract of guarantee:-

1. Essentials of a valid contract: It must possess all the essentials of a valid contract.

2. Concurrence of the party: To be legally valid, there must be concurrence of all the

parties (three, principal debtor, creditor and surety) to a contract of guarantee and to

its terms and conditions.

3. Consideration: It must be supported by a lawful consideration.

4. Primary liability: In a contract of guarantee there is a primary liability on the

principal debtor to repay or to discharge the obligation.

5. Implied Indemnity: In every contract of guarantee, there is an implied indemnity.

6. Disclosure of facts: It is duty of the creditor that he must disclose to the surety all

those facts likely to affect the degree of his responsibility.

7. Form of a contract: According to Section 126 of the Act, the contract of guarantee

may be made in writing or by the words of mouth.

Law of Agency

The contract of agency is a part of the Indian Contract Act, 1872. The terms ‘agent’ and

‘principal’ are defined in Section 182 of the Act. According to this section, an agent is a person

employed to do any act for another or to represent another in dealings with third persons. The

person for whom such act is done, or who is represented is called the principal. The contract

which creates the relationship of principal and agent is called ‘agency’. If A appoints B to act on

behalf of him in a situation, there is a contract of agency. Here, A is the principal and B is the

agent. The definition given by the Act is very wide and includes servant, employee etc.

Essentials of a Contract of Agency

To constitute a contract of agency, the following essentials are required:

I. Agreement: An agreement between the principal and the agent is the first requirement of

a contract of agency.

II. Competency of principal: Section 183 of the Act states that any person who is of the age

of majority and of sound mind can employ an agent.

III. Consideration not necessary: No consideration is required to create an agency (Section

185). The agent is remunerated by way of commission for his services rendered.

Termination of Agency

Section 201 provides the circumstances under which an agency can be terminated. According to

this, an agency is terminated by the principal revoking his authority, or by the agent renouncing

the business of the agency being completed, or by either the principal or the agent dying or

becoming of unsound mind, or by the principal being adjudicated an insolvent.

Finder of lost goods and his position

In terms of Section 71 ‘A person who finds goods belonging to another and takes them into his

custody is subject to same responsibility as if he were a bailee’.

Thus a finder of lost goods has:

I. To take proper care of the property as men of ordinary prudence would take

II. No right to appropriate the goods and

III. To restore the goods if the owner is found.

Rights and Duties of Finder of Goods

A ‘finder of lost goods’ is as good as a bailee and he enjoys all the rights and carries all the

responsibilities of a bailee.

The bailee has the following rights:

I. To claim compensation for any loss arising from non-disclosure of known defects in the

goods.

II. To claim indemnification for any loss or damage as a result of defective title.

III. To deliver back the goods to joint bailers according to the agreement or directions

IV. To deliver the goods back to the bailor whether or not the bailor has the right to the --

goods

V. To exercise his ‘right of lien’. This right of lien is a right to retain the goods and is

exercisable where charges due in respect of goods retained have not been paid. The right

of lien is a particular lien for the reason that the bailee can retain only these goods for

which the bailee has to receive his fees/remuneration.

VI. To take action against third parties if that party wrongfully denies the bailee of his right

to use the goods.

Apart from the above, the ‘finder of lost goods’ can ask for reimbursement for expenditure

incurred for preserving the goods but also for searching the true owner. If the real owner refuses

to pay compensation, the ‘finder’ cannot sue but retain the goods so found. Further where the

real owner has announced any reward, the finder is entitled to receive the reward. The right to

collect the reward is a primary and a superior right even more than the right to seek

reimbursement of expenditure. Lastly the finder though has no right to sell the goods found in

the normal course, he may sell the goods if the real owner cannot be found with reasonable

efforts or if the owner refuses to pay the lawful charges subject to the following conditions.

a. When the article is in danger of perishing and losing the greater part of the value or

b. When the lawful charges of the finder amounts to two-third or more of the value of the

article found.

UNIT – II

Elements of Law Relating to Sale of Goods under Sale of Goods Act, 1930

Elements of the Sale of Goods Act, 1930

The law relating to sale of goods is contained in the Sale of Goods Act, 1930. The Act came into

force on 1st July, 1930. Provisions pertaining to the sale of goods were earlier contained in

Chapter VII of the Indian Contract Act, 1872. The Act of 1930 extends to whole of India, except

Jammu and Kashmir. It deals with provisions relating to passing of ownership of the goods from

seller to buyer, duties of seller and buyer, rights of unpaid seller, remedies available to buyer if

the goods are not delivered to him etc.

Contract of Sale

The term contract of sale is a generic term and it includes both sale and agreement to sell. Where,

under a contract of sale, the property in goods is transferred from seller to the buyer, it is called

‘Sale’ but where the transfer of property in goods is to take place at a future time or subject to

some conditions thereafter to be fulfilled, the contract is called ‘ agreement to sell’. Section 4 (1)

of the Act defines a contract of sale of goods as a contract whereby the seller transfers or agrees

to transfer the property in goods to the buyer for price.

Essentials of Contract of Sale

The following are the essentials of contract of sale:

1. Two parties: There are two distinct parties in a contract of sale – seller and buyer.

2. Transfer of general property: ‘Property’ means the general property in goods and not

merely a special property [Section 2 (11)].

3. Goods: Goods form the subject matter of the contract and must be movable. Goods mean

every kind of movable property other than actionable claims and money and include

stock and shares, growing crops, grass and things attached to or forming part of land

which are agreed to be severed sale or under the contract of sale.

4. Price: The consideration for the contract of sale must be in the form of money and is

called price.

5. All essentials of a valid contract: All the essential elements of a valid contract like

agreement, free consent, consideration, etc. must be present in a contract of sale of goods.

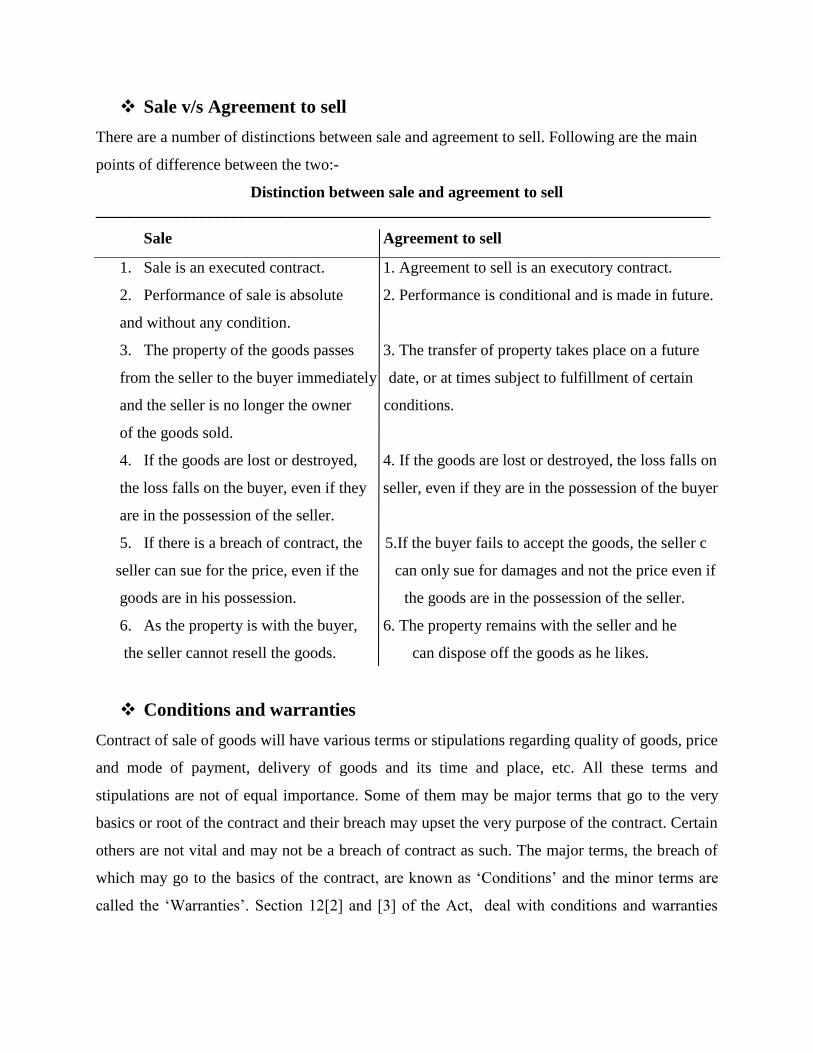

Sale v/s Agreement to sell

There are a number of distinctions between sale and agreement to sell. Following are the main

points of difference between the two:-

Distinction between sale and agreement to sell

_____________________________________________________________________________

Sale Agreement to sell

1. Sale is an executed contract. 1. Agreement to sell is an executory contract.

2. Performance of sale is absolute 2. Performance is conditional and is made in future.

and without any condition.

3. The property of the goods passes 3. The transfer of property takes place on a future

from the seller to the buyer immediately date, or at times subject to fulfillment of certain

and the seller is no longer the owner conditions.

of the goods sold.

4. If the goods are lost or destroyed, 4. If the goods are lost or destroyed, the loss falls on

the loss falls on the buyer, even if they seller, even if they are in the possession of the buyer

are in the possession of the seller.

5. If there is a breach of contract, the 5.If the buyer fails to accept the goods, the seller c

seller can sue for the price, even if the can only sue for damages and not the price even if

goods are in his possession. the goods are in the possession of the seller.

6. As the property is with the buyer, 6. The property remains with the seller and he

the seller cannot resell the goods. can dispose off the goods as he likes.

Conditions and warranties

Contract of sale of goods will have various terms or stipulations regarding quality of goods, price

and mode of payment, delivery of goods and its time and place, etc. All these terms and

stipulations are not of equal importance. Some of them may be major terms that go to the very

basics or root of the contract and their breach may upset the very purpose of the contract. Certain

others are not vital and may not be a breach of contract as such. The major terms, the breach of

which may go to the basics of the contract, are known as ‘Conditions’ and the minor terms are

called the ‘Warranties’. Section 12[2] and [3] of the Act, deal with conditions and warranties

respectively. While conditions are the very basis of a contract of sale, warranty is only of

secondary importance.

Condition is defined in Section 12 [2] as a stipulation essential to the main purpose of the

contract, the breach of which gives the aggrieved party a right to reject the contract itself. In

addition, action for damages for losses suffered, if any, due to breach of condition can also be

made.

Warranty is defined in Section 12 [3] as stipulation collateral to the main purpose of the

contract, the breach of which gives the aggrieved party a right to sue for damages and not to void

the contract itself.

Express and Implied conditions and warranties

Conditions may be express or implied. They are express when, at the will of the parties, they are

inserted in the contract. They are said to be implied when the law presumes their existence in the

contract, even though it has not been put into it in express words. According to Section 62,

implied conditions and warranties may be varied by express agreement or by the course of

dealing between the parties, or by usage of trade.

Doctrine of Caveat Emptor

The doctrine of caveat emptor means ‘let the buyer beware’. According to this doctrine , it is the

duty of the buyer to be careful while purchasing goods. In the absence of any enquiry from the

buyer , the seller is not bound to disclose the defects in the goods. It is the buyer who must

examine the goods thoroughly and must see that the goods that he buys are suitable for the

purpose of which he want them. If the goods turn out to be defective, the buyer cannot sue the

seller, as there is no implied undertaking by the seller that he shall supply goods to suit the

buyer’s purpose.

Exceptions to caveat emptor

The doctrine of caveat emptor does not apply in the following situations:

a. When the seller makes a representation of fact, whether innocent or fraudulent,

regarding the product.

b. When the seller actively conceals a defect in the goods which could not be revealed

by ordinary examination.

c. Where goods are supplied by description and they do not correspond with the

description given by the seller.

d. Where goods are supplied by description and they are not of merchantable quality.

Performance of contract of sale

The performance of a contract of sale implies delivery of goods by the seller and the acceptance

of the delivery of goods and payment for them by the buyer, in accordance with the contract. The

parties are free to provide any terms they like in their contract about the time, place and manner

of delivery of goods, acceptance thereof and payment of the price. But if the parties are silent

and do not provide anything regarding these matters in the contract them the rules contained in

the Sale of Goods Act are applicable.

Delivery

Delivery of goods means voluntary transfer of possession of goods from one person to another

[Sec. 2(2)]. If transfer of possession of goods is not voluntary, that is, possession is obtained

under pistol point or by theft, there is no delivery.

Rights of unpaid seller

A seller of the goods is deemed to be an unpaid seller when the whole of the price has not been

paid or tendered or a bill of exchange or other negotiable instrument has been received as

conditional payment. The unpaid seller has the following rights:

a) Against the goods: Against the goods , the unpaid seller has the right of lien, the right of

stoppage of goods in transit, and the right of resale. The right of lien can be exercised

only for non – payment of the price and not for any other charges. The right of stoppage

of goods in transit means the right of stoppage of goods while they are in transit to regain

the possession and to retain them till the full price is paid. The right to resale gives the

seller the right to resell the goods in the following cases:

I. When the goods are perishable.

II. When the right is expressly reserved in the contract.

III. When despite the seller giving a notice to the buyer of the intention to resell, the

buyer does not pay or tender the price within a reasonable time.

b) Against the buyer personally: the unpaid seller can file a suit for price, as well as file a

suit for damages for non – acceptance.

UNIT – III

Elements of Law Relating to Negotiable Instruments under Negotiable

Instruments Act, 1881

In India, the law relating to negotiable instruments is contained in the Negotiable Instruments

Act, 1881. It deals with Promissory Notes, Bills of Exchange and Cheques, the three kinds of

negotiable instruments in most common use. The Act applies to the whole of India and to all

persons resident in India, whether foreigners or Indians. The act also applies to ‘hundis’, other

documents such as treasury bills, dividend warrants, bearer debentures, etc. These instruments

are also recognised as negotiable instruments, either by mercantile customs or under other act

like the Companies Act, 1956.

Definition of Negotiable Instruments

The word meaning of ‘negotiable’ is being transferable by delivery, and the word ‘instrument’

means a written document by which a right is created in favour of some person. Thus, negotiable

instrument means a written document transferable by delivery. According to Section 13 of the

Act, a negotiable instrument means ‘a promissory note, bill of exchange or cheque payable either

to order or to bearer’. The two main aspects of a negotiable instrument thus are that it is payable

to order and is payable to bearer.

1. Payable to order: According to this, a note, bill or cheque is payable to order which is

expressed to be ‘payable to a particular person or his order’. A document that

contains express words prohibiting negotiability is a valid document but they are

considered as negotiable instruments since they cannot be negotiated further.

However, a cheque is an exception to this. A cheque crossed ‘account payee only’ is

considered negotiable.

2. Payable to bearer: This means ‘payable to any person whosoever bears it’. A note

,bill or cheque is payable to a bearer which is expressed to be so payable.

Elements of Negotiable Instruments

The essential elements of a negotiable instrument are as under:

1. Negotiability: The instruments are transferable from one person to another without

any further formality.

2. Transferee can sue in his own name without giving notice: A bill, note or a cheque

represents a debt and implies the right of the creditor to recover it from his debtor.

The creditor has the right to either recover this amount himself or he can transfer this

right to another person.

3. Better title to a bonafide transferee for value: A bonafide transferee of a negotiable

instrument gets the instrument free from all defects. He is not affected by any defect

of title of the transferor or any prior party.

4. Presumptions: There are certain presumptions that apply to all negotiable

instruments, which are contained in Sections 118 and 119. Some of the presumptions

are as follows:

a) Every negotiable instrument was made, drawn, accepted, indorsed or

transferred for consideration.

b) A negotiable instrument bearing a date was made or drawn on the date

mentioned.

c) Every bill of exchange was made and accepted at a reasonable time and before

its maturity.

d) That the holder of a negotiable instrument is a holder in due course.

Types of Negotiable Instruments

The following are the main types of Negotiable instruments:

1. Promissory Notes: Section 4 of the Act defines a promissory note as an instrument

in writing (not being a bank note or a currency note) containing an unconditional

undertaking signed by the maker, to pay a certain sum of money only to or to the

order of a certain person or to the bearer of the instrument. Any promissory note

will have two parties, the maker who makes the promissory note and the payee to

whom the payment is to be made. Based on the definition, the essential features of

promissory note include the following:

I. It must be in writing.

II. It must contain a promise or undertaking to pay.

III. The promise to pay must be unconditional.

IV. The maker must be a certain person.

V. They payee must be certain.

VI. The sum payable must be certain.

2. Bills of Exchange

A bill of exchange is an instrument in writing containing an unconditional order signed by the

maker directing a certain person to pay a certain sum of money only to , or to the order of, a

certain person or to the bearer of the instrument.

Parties to a Bill of Exchange

A bill of exchange will have three parties – the drawer, drawee and payee. The person who

makes the bill is called the ‘drawer’. The person who is directed to pay is called the ‘drawee’ and

the person to whom the payment is to be made is called the ‘payee’. If the bill is endorsed to

another person, the endorsee who is in possession of the bill is called the ‘holder’. The holder

must present the bill to the drawee for his acceptance. When the drawee accepts the bill, by

writing the word ‘accepted’ and then signing it, he is called the ‘acceptor’.

Essential Characteristics of a Bill of Exchange

An instrument to be considered a valid bill of exchange should comply with the following

conditions:

I. It must be in writing.

II. It must be definite and should contain an unconditional order to pay.

III. It must be signed by the drawer.

IV. All the parties must be certain.

V. The sum payable on the instrument must be certain.

VI. It must contain an order to pay money only.

VII. It must also comply with the formalities with respect to date, consideration,

stamps etc.

3. Cheque

A cheque is defined as ‘a bill of exchange drawn on a specified banker and not expressed to be

payable otherwise than on demand and it includes the electronic image of a truncated cheque and

a cheque in the electronic form’. From the definition it can be seen that a cheque is a bill of

exchange with two distinctive features:

1. It is always drawn on a bank.

2. It is always payable on demand.

Crossing of Cheques

Cheques may be open cheques or crossed cheques. An open cheque is one that is payable across

the counter of a bank. Crossing helps in preventing any probable loss that may occur, in the

event of an open cheque getting into the hands of a wrong person. Crossing is a unique feature

associated with a cheque that affects a certain obligation of the paying banker and also its

negotiable character. Crossing of a cheque is effected by drawing two parallel transverse lines

with or without the words ‘and company’ or any abbreviation. If a cheque bears across its face

and addition of the words ‘and company’ or any abbreviation between two parallel transverse

lines or transverse lines simply, either with or without the words ‘not negotiable’ that shall be

deemed a crossing and the cheque shall be deemed to be crossed. Since the payment cannot be

claimed across the counter on a crossed cheque, crossing of cheques serves as a measure of

safety against theft or loss of cheques in transit.

According to Section 126 of the Act, a cheque can be crossed by any of the following persons:

1. The drawer of a cheque

2. The holder of the cheque

3. The banker

Parties to Negotiable Instruments

Holder:

The ‘holder’ of a negotiable instrument means any person entitled to the possession of the

instrument in his own name and to receive or recover the amount due thereon from the parties

liable thereto (Sec.8). Thus, in order to be called a ‘holder’ a person must satisfy the following

two conditions:

I. He must be entitled to the possession of the instrument in his own name.

II. He must be entitled to receive or recover the amount due thereon from the parties

liable thereto.

Holder in due course

The ‘holder in due course’ means any person who for consideration becomes the possessor of a

negotiable instrument if payable to bearer, or the payee or indorsee thereof if payable to order,

before the amount mentioned in it became payable, and without sufficient cause to believe that

any defect existed in the title of the person from whom he derived his title (Sec. 9). Thus, in

order to be called a ‘holder in due course’ a person must possess the following specifications:

1. He must be a ‘holder’. i.e., he must be entitled to the possession of the instrument in

his own name under a legal title and to recover the amount thereof from the parties

liable thereto.

2. He must be a holder of valuable consideration, i.e., there must be some consideration

to which law attaches value. The consideration, however, need not be adequate.

3. He must have become the holder of the negotiable instrument before its maturity.

4. He must take the negotiable instrument complete and regular on the face of it.

5. He must have become holder in good faith.

Liabilities of parties to Negotiable Instruments

The provisions of law regarding the liability of parties to negotiable instruments are as follows:

1. Liability of drawer: The drawer of a bill of exchange or cheque is bound, in case of

dishonor by the drawee or acceptor thereof, to compensate the holder, provided due

notice of dishonor has been given to, or received by, the drawer as hereinafter

provided (Sec.30). Thus, the drawer of a bill or cheque is liable to the holder only of

(i) the instrument has been dishonored, and (ii) due notice of dishonor has been given

to him.

2. Liability of drawee of cheque (Sec. 31): The drawee of the cheque (i.e., the paying

banker) must pay the cheque when duly presented for payment provided he has

sufficient funds to the drawer applicable to the payment of such cheque. If the drawee

banker wrongfully dishonors the cheque he can be made liable to pay exemplary

damages to the drawer. Notice that when the banker makes a default he is liable not

towards the payee or the holder but towards the drawer. This is so because there is no

privity of contract between the holder and the banker. The holder has a remedy

against the drawer and not against the banker.

3. Liability of ‘maker’ of bill and ‘acceptor’ of bill (Sec.32): The maker of a

promissory note and the acceptor of a bill of exchange are the principle debtors and

hence they are primarily liable for the amount due on the instrument according to its

apparent tenor, in the absence of a contract to the contrary. There may be a contract to

the contrary, for instance, in the case of an ‘accommodation bill’ the acceptor may be

exempt from liability as per contract.

4. Liability of endorser (Sec. 35): When an endorser endorses and delivers a negotiable

instrument before maturity he impliedly undertakes to be liable to every subsequent

holder for the loss caused to him if the instrument is dishonoured by the party

primarily liable thereon. Thus, the endorser stands in the position of a ‘drawer’ to all

the subsequent holders.

Liabilities of paying banker

The paying banker (drawee of the cheque) must pay the cheque when duly presented for

payment provided he has sufficient funds to the drawer applicable to the payment of such

cheque. If the drawee banker wrongfully dishonors the cheque he can be made liable to pay

exemplary damages to the drawer. Notice that when the banker makes a default he is liable

not towards the payee or the holder but towards the drawer. This is so because there is no

privity of contract between the holder and the banker. The holder has a remedy against the

drawer and not against the banker.

Dishonor of instruments

A negotiable instrument may be dishonored by (i) non – acceptance or (ii) non – payment. As

presentment for acceptance is required only in case of bills of exchange, it is only the bills of

exchange which may be dishonored by non – acceptance. Of course any type of negotiable

instrument – promissory note, bill of exchange or cheque – may be dishonored by non –

payment.

1. Dishonor by Non – acceptance : A bill of exchange is said to be dishonored by non –

payment in the following cases:

a. When the drawee or one of several drawees (not being partners) makes default in

acceptance upon being duly required to accept the bill.

b. Where the presentment for acceptance is excused and the bill is not accepted, i.e.,

remains unaccepted.

c. Where the drawee is incompetent to contract.

d. Where the drawee makes the acceptance qualified.

e. If the drawee is a fictitious person or after reasonable search cannot be found.

2. Dishonor by Non – payment

A promissory note, bill of exchange or cheque is said to be dishonored by non – payment when

the maker of the note, acceptor of the bill or drawee of the cheque makes default in payment

upon being duly required to pay the same (Sec. 92). Also, a promissory note or bill of exchange

is dishonored by non – payment when presentment for payment is excused expressly by the

maker of the note or acceptor of the bill and the note or bill remains unpaid at or after maturity

(Sec. 76).

UNIT – IV

Elements of Company Law – I under Indian Companies Act, 1956

Meaning of Company: Company as defined by Section 3(1) of the Companies Act, 1956 :

“Company means a company formed and registered under this Act or an existing company”. A

company as described in the Act, denotes an ‘association of persons who have associated

together to conduct or carry on a business for gain.’ The persons so associate will contribute

money for the conduct of the business. The amount so contributed will be used as the share

capital of the company.

Nature of Company: A company is an association of persons formed for a common purpose,

with capital divisible into parts, known as shares, and with a limited liability. It is a creation of

law and is known as artificial person. It has perpetual succession and a common seal. The nature

of company may be summed up in the following points:

1. Incorporated Association: A company must be incorporated or registered under the

Companies Act. In the case of a public company, the minimum number of persons

required is 7 and for a private company, it is 2.

2. Artificial Person: A company is created with the sanction of law and it itself is not a

human being, and hence an artificial person clothed with certain rights and

obligations.

Features/Characteristics of a Company: The characteristics of a company as brought out by

various definitions are as under:

1. Separate Legal Entity: When a company is registered, a new legal person will be

born and thereafter, the company will be regarded as an entity separate from its

members. A company on registration, the association of persons incorporated

becomes a body corporate by the name contained in the memorandum. A company is

an entirely different person, from its members. It can act only through human agency.

2. Perpetual Succession: A company is a legal person with perpetual succession.

Perpetual succession means that the membership of a company may change from time

to time but that will not affect the continuity of the company. The members may

come and go, but the company can go on forever until dissolved by the process of

law.

3. Limited Liability: A company may be incorporated with limited liability. The

liability may be limited by shares or by guarantee. The liability of the members will

only be to the extent of the face value of the shares which are held by them or the

amount guaranteed by them.

4. Separate Property: A company is a legal person. It can acquire, own, enjoy or

dispose of properties, in its own name. Although the capital of the company is

contributed by its shareholders, they are not joint owners of the company’s property.

5. Transferability of Shares: The shares of a public company are freely transferable. A

shareholder can sell his shares of a public company in the open market. The only

restriction is that it needs to be done in the manner provided in the Articles of the

Company.

6. Common Seal: A company has no physical existence. It can enter into contracts only

through human beings under the seal of the company. The seal of the company

represents the official signature of the company.

7. Capacity to sue: A company being a legal person can sue and be sued in its own

corporate name.

8. Application of doctrine of ultra vires: In the case of a company, the application of

ultra vires doctrine is essential feature. It cannot go beyond the ‘Object Clause’ of the

Memorandum of Association.

9. Winding up: The winding up procedure of a company, by which the functioning of

the company is terminated, is prescribed by law. The company will cease to be in

existence only by it compliance.

10. Legal Restrictions: The formation, working and winding up of company are strictly

governed by the act incorporated for this, i.e., the Companies Act, 1956. Any actions

which is contrary to the provisions of the Companies Act or any law in force will be

declared illegal.

Types of Companies:

Companies may generally be classified as follows:

1. Based on incorporation

2. Based on liability

3. Based on number of members

4. Based on control

5. Based on ownership

Classification of Companies Based on Incorporation

Based on incorporation the companies can be divided into Statutory, Registered and Chartered

Companies:

1. Statutory Companies: Statutory Companies are those which are incorporated under a

special act passed either by the parliament or by the state legislature. In India, these

companies can be found in the fields of public enterprise or public utility services. The

Reserve Bank of India, State Bank of India, Industrial Finance Corporation etc. are

examples of such companies in India.

2. Registered Companies: These companies are formed and registered under the

Companies Act of 1956, or were registered under any of the earlier Companies Acts.

3. Chartered Companies: These companies are those which are incorporated by the Royal

Charter. The companies like East India Company were formed by the Royal Charter. The

scope of activities of such companies is laid down in the charter of incorporation. These

type of companies do not exist in India.

Classification of Companies Based on Liability:

Based on liability the companies can be divided into limited liability companies and unlimited

liability companies:

1. Limited Liability Companies: The companies limited by liability are classified into

companies limited by shares, companies limited by guarantee and the hybrid form.

a) Companies limited by shares: A limited company is one in which the

liability of the members is limited by its Memorandum of Association, to the

amount, if any, unpaid on the shares held by them. The shareholders cannot be

called upon to pay more than the amount remaining unpaid on his shares. His

personal assets cannot be called upon for the payment of the liabilities of the

company.

b) Companies limited by guarantee: In a company limited by guarantee the

liability of the members is limited by the Memorandum to such an amount as

the members respectively undertake to contribute to the assets of the company

in the event of it being wound up.

c) Companies limited by shares as well as guarantee: This is a hybrid form of

company which combined elements of the guarantee and share of the

company. Every member of such a company is subject to a twofold liability,

i.e., the guarantee which may become effective from the winding up of the

company and the liability to pay up the nominal amount of his share which

may become effective during the lifetime of the company or at the time of

winding up.

2. Unlimited Companies: The liability of the shareholders of these types of companies

is unlimited, in the sense that the members of the companies are liable to the full

extent to meet the obligations of the company. However, it is to be noted that the

company being a separate entity is only liable, not the members, to its creditors. In the

event of winding up, the liquidator may call upon the members to contribute to the

assets of the company without limitation of their liability for the payment of the

company.

Classification of Companies Based on Number of Members

Based on the number of members companies can be divided into private and public companies:

1. Private Company: A private limited company as defined by the Companies Act is a

company which is having a minimum paid – up capital of Rs. 1 lakh or such higher

paid – up capital as prescribed by its Articles, and which:

a) Restricts the right to transfer it shares, if any.

b) Limits the members to 50 (200 as per Companies Act, 2013).

c) Prohibits any invitation to the public to subscribe for any shares or

debentures of the company.

A private company is one which can be formed by a minimum of two members.

2. Public Company: The main characteristics of a public company are :

a) One which is not a private company.

b) In which the number of shareholders is not restricted.

c) Which can invite the public to subscribe its shares and where the

shares are freely transferable.

d) Has a minimum paid – up capital of Rs. 5 lakh or such higher paid –

up capital as may be prescribed.

Classification of Companies Based on Ownership

Based on ownership, companies can be classified as under:

1. Government Company: These are companies in which the central or the state

government holds not less than 51 per cent of the share capital.

2. Foreign Company: The Companies Act defines a foreign company as one which is

incorporated outside India and has established a place of business within India by itself or

through electronic, mode and conducts any business activity in India in any other manner.

3. One – person Company: ‘One – person Company’ [OPC] means a company which has

only one person as a member. It is registered as a private company with one member and

at least one director. Adequate safeguards in case of death/disability of the sole person

should be provided through appointment of another individual as nominee director.

Classification of Companies Based on Control

Based on control, companies can be classified as under:

1. Holding Company: A holding company is a company which holds more than 50%

of issued share capital, or more than 50% of the voting power, or has power to

appoint or control the composition of directors of other company. The other company

is known as subsidiary company.

2. Subsidiary Company: A company is deemed to be subsidiary of another in the

following cases:

a) If the holding company controls the composition of its Board of Directors.

The composition of a company’s Board of Directors will be considered to

be controlled by another company, if that other company by exercise of its

power, appoint or remove all or majority of the directors.

b) That the other company exercises or controls more than half of the total

voting power and holds more than half of the nominal value of its equity

share capital.

c) If it is a subsidiary of a third company which itself is a subsidiary of the

controlling company.

Promotion of a Company:

Promotion is a term denoting the preliminary steps taken for the purpose of registration and

floatation of the company. The persons who assume the task of promotion are called promoters.

The word ‘promoter’ was not defined under the Companies Act, 1956, now the Section 2 (69) of

Companies Act, 2013 defines it as a person who has been named as such in a prospectus or is

identified by the company in the annual return or who has control over the affairs of the

company, directly or indirectly whether as a shareholder, director or otherwise.

Incorporation and commencement of business of companies:

For registration of a company the required documents are to be filed with the Registrar. The

documents include the Memorandum of Association, Articles of Association and the agreement,

which the company proposes to enter into any individual for appointment as its Managing

Director or Manager. Along with this, a declaration known as ‘Statutory Declaration of

Compliance’, which certifies that all the requirements of the Companies Act and Rules, in

respect of registration have been complied with, has also to be filed. On satisfactorily meeting all

the statutory requirements, the Registrar of Companies will issue a ‘Certificate of Incorporation’.

By issuing this certificate the Registrar certifies under that the company is incorporated, and in

the case of a limited company that the company is limited. Such a certificate given by the

Registrar is conclusive evidence that all the requirements of the Companies Act have been

complied with, in respect of registration. Once the company is registered after issuing the

certificate of incorporation, it becomes a distinct legal entity, with perpetual succession and with

all the other characteristics of a registered company.

Floatation / commencement of business:

A company after having been registered, and having received its certificate of incorporation, is

ready for ‘floatation’. This means that it can go ahead with raising capital sufficient to

commence business and to carry it on satisfactorily. However, in the case of private companies,

they are prohibited from inviting public to subscribe to the share. A company having share

capital that is both private and public limited company should not commence business or

exercise any borrowing powers unless a declaration is filed with Registrar by a director verified

in the manner prescribed. This declaration should state that every subscriber to the memorandum

has paid the value of the shares agreed to be taken by him, paid – up capital is not less than Rs. 5

lakhs in the case of public company and Rs. 1 lakh in case of private company. Registered office

details have been filed with the Registrar for verification.

Memorandum of Association

Memorandum of Association is the fundamental document of a company. It is considered the

charter, defines the reason of the existence of the company, and is of supreme importance. The

Memorandum of Association contains those conditions on the basis of which the company is

incorporated. A company cannot be incorporated without it.

Memorandum of Association is the document which contains the rules regarding the constitution

and activities or objects. It gives protection to the shareholders since it contains the purpose to

which their money is put to use. Since it contains the powers of the company, it provides

protection to persons who deal with it. Any person who deals with the company will be able to

know the objects of the company, and whether the contractual relations to which the person is

indenting to enter into is within the objective of the company.

The Memorandum of Association tells us about the objects of the company’s formation and the

utmost possible scope of its operation, beyond which its actions cannot go. That is, it defines as

well as confines the power of the company. If the company does anything beyond the objects and

powers conferred on it by the Memorandum of Association, it will be considered ultra vires

(beyond the powers of) the company and hence void.

Contents of Memorandum of Association

The compulsory clauses to be contained in the Memorandum of Association are as follows:

1. Name clause: The name of the company establishes its identity and is the

symbol of its existence. The Companies Act specifies that the name must end

with ‘Limited’ in the case of a public company, and ‘Private Limited’ in the

case of a private company. Subject to this the promoters are free to choose any

suitable name provided it does not violate the necessary provisions with respect

to selecting the name as contained in the act like, it should not resemble name

by which a company is already registered and so on.

2. Registered office clause [or domicile clause or situation clause]: The

Companies Act specifies that a company shall, on and from the 15th

day of its

incorporation has to have a registered office capable of receiving and

acknowledging communications and notices as may be addressed to it.

3. Objects clause: The objects clause is a very important clause as it defines the

sphere of its activities, the aims it seeks to achieve and the activities or business

it proposes to conduct. A company cannot do anything beyond or outside the

objects and any act done beyond them will be ultra vires and void. Earlier under

the Companies Act, 1956, the objects clause in the Memorandum of Association

has to state the main objects , ancillary or incidental objects and other objects.

Now, under the amended Companies Act, 2013 , Memorandum of Association

need to contain only the objects for which the company is proposed to be

incorporated and any matter which is considered necessary.

4. Liabilities clause: Liabilities clause states about the nature of liability of the

members. In the absence of liability clause in the Memorandum, it means that

the liability of the members is unlimited.

5. Capital clause: This clause states the amount of share capital with which the

company is registered and mode of its division into shares. This is known as the

authorized or nominal capital of the company.

6. Association or subscription clause: It is in this clause that the subscribers

declare that they desire to be formed into a company and agree to take shares

stated against their names. As per this clause, at the end of the Memorandum of

every company, there shall be an association or declaration of association which

reads, We, the several persons whose names and addresses and occupation are

subscribed, are desirous of being formed into a company in pursuance of this

Memorandum of Association, and we respectively agree to take the number of

shares in the capital of the company set opposite our respective name.

Alteration of Memorandum of Association

The Memorandum of Association, being a principal document of any company, is not easy to

change. The Companies Act recognizes the unalterable character of the Memorandum and

provides for alteration in exceptional cases [Section 13] and with certain laid down procedures.

1. Alteration of the Name Clause

A company registered with a name, which in the opinion of the Central Government is

identical or resembles with the name of existing company, shall change its name by passing

an ordinary resolution within three months from the date of direction given by the Central

Government. The change in the name clause shall be effective from the date of the issue of

the fresh Certificate of Incorporation.

2. Alteration of domicile clause

The domicile is the place of its registered office. Change in the place if the registered office

will require change in the domicile clause of the Memorandum of Association. A company

may change its domicile:

I. From one place to another within the state: When the office is shifted from one

locality to another in the same city, no special resolution is needed.

II. From one state to another state: When a company shifts its office from one

state to another state, it has to pass a special resolution. The change shall take

effect only when it is confirmed by the Company Law Tribunal.

3. Alteration of objects clause

The objects clause of the company being an important clause in the Memorandum of

Association, the change if any would amount to a change in the nature of the company as a

whole. A company can alter its object if such an alteration enables it:

I. To carry on its business more economically and more effectively.

II. To attain its main object or purpose by new or improved means.

III. To enlarge its local area of operation.

IV. To restrict or abandon any of the object or purpose specified in the Memorandum.

V. To sell or dispose off the whole or any part of the undertaking of the company.

VI. To amalgamate with any other company or body of persons.

VII. To carry on some business which under existing circumstances may be

conveniently combined with the business of the company.

For alteration in the object clause, the company is required to pass a resolution and seek

permission of the Company Law Tribunal.

Alteration of Capital Clause

A company limited with share capital, if permitted by its Articles of Association, may alter its

capital clause for the following reasons:

I. To increase the share capital,

II. To consolidate its share capital into shares of higher denominations,

III. To subdivide the share capital into shares of lower denominations,

IV. To convert shares to stock,

V. To cancel the unissued capita, and

VI. To reduce its share capital.

In cases other than reducing share capital, only ordinary resolution need to be passed, and no

confirmation of the tribunal is required.

Alteration of the liability clause

The liability of the members of a limited company or a guarantee company cannot be made

unlimited without their consent in writing. However, the liability of the Directors, Managing

Director or Manager can be made unlimited by passing a special resolution, if the Articles so

permit, and with the consent of the officer in writing. Information regarding this should be given

to the Registrar within 30 days of passing the resolution.

Articles of Association

The Articles of Association, next in importance to the Memorandum, are the bye – laws , rules

and regulations that govern the management of the internal affairs as well as the conduct of the

business. The Articles define a host of things which include duties, rights, powers and authority

of the shareholders, the directors in their respective capacities and of the company in general. It

also states the mode and form in which the business of the company is to be carried out. The

Articles of a company have a contractual force between the company and it members and also

between the members in relation to their rights as members.

Alteration of Articles of Association

Companies have been given wide powers to alter their Articles, and any clause in the Articles

that prohibits alteration of Articles is invalid. A company may, by means of special resolution,

alter its Articles at any time and a copy of the resolution altering the Articles has to be filed with

the Registrar within 30 days of passing it. The alteration of the Articles of Association is subject

to certain limitations and those limitations are discussed below:

1. The alteration must not be inconsistent with the provisions of the Companies Act.

2. The alteration must not be in conflict with the Memorandum of Association.

3. The alteration must not sanction anything which is illegal.

4. The alteration must not constitute a fraud on the minority shareholders.

5. The alteration must not increase the liability of existing shareholders.

6. The alteration must not cause a breach of contract.

7. The alteration must be made in good faith and for the benefit of the company as a

whole

8. Alteration of Articles when a public company is converted into a private company is

converted into a private company requires the approval of the Central Government.

Effects of Memorandum and Articles of Association to Outsiders

Two doctrines, namely, the doctrine of constructive notice and the doctrine of indoor

management, deal with the provisions related with the dealings of outsiders with the

company. The principles related with both these doctrines are discussed below.

Doctrine of Constructive notice

Constructive notice means the notice which is assumed under law. Every person dealing with

the company is deemed to a have constructive notice of the contents of the Memorandum and

Articles of the company. Any outsider dealing with the company is presumed to have read

the contents of the registered documents of the company. There is a further presumption that

the documents have been understood fully in the proper sense. Thus, the doctrine or rule of

constructive notice is a presumption operating in favour of the company against the outsider.

Doctrine of Indoor Management

The doctrine of indoor management is an exception to the rule of constructive notice. It

imposes an important limitation on the doctrine of constructive notice. According to this

doctrine, persons dealing with the company are entitled to presume that the internal

requirements prescribed in the Memorandum and Articles have been properly observed. A

transaction has two aspects, namely, substantive and procedural. An outsider dealing with the

company can only find out the substantive aspect by reading the Memorandum and Articles.

Even though he may find the procedural aspect, he cannot find out whether the procedure has

been followed or not.

UNIT – V

Elements of Company Law – II under Indian Companies Act, 1956

Director

The Companies Act, 1956 defines a ‘director’ as any person occupying the position of director

by whatever name called. A body corporate, association or firm, cannot be appointed as a

director. Though the Act makes it obligatory for all the companies to have directors, it does not

provide guidelines as to who can be appointed as directors.

Type of Directors

Directors could be broadly classified into two types:

1. Inside directors: Inside directors are those directors who are in the whole – time

employment of a company. This category includes managing director, whole – time

director, technical director executive director, etc.

2. Outside directors: Directors, who are not in the whole – time employment of the

company and as such are not associated with its day – to – day working, are outside

directors. They include professional directors, nominated directors and statutory

directors.

Number of Directors

The minimum number of directors in case of a public company is three and that of a private

company is two. Under the Companies Act, 1956 the maximum number directors was 12, but

now it has been raised to 15, and more can be appointed by passing a special resolution,

Companies Act, 2103 (Section 149).

Appointment of Directors

The first directors of a company may be named in its Articles of Association. First director is one

who assumes the office from the incorporation of the company. Directors, other than first are

appointed in the general meeting. Additional directors are appointed by the Board of Directors of

a company. An independent director may be selected from a data bank containing the names,

addresses and qualifications of persons who are eligible and willing to act as independent

directors.

Remuneration of Directors

Managerial remuneration can take the form of monthly payments which includes salary or a

specified percentage of net profit or a commission/ or fee for attending each meeting of the board

called sitting fees. In the absence of a specific agreement, directors are not entitled to

remuneration for their services. The remuneration payable to the directors of the company is

determined either by the Articles or by a resolution passed in the general meeting. Maximum

limit of 11% of net profit in the case of public limited companies is applicable. For companies

with no profits or inadequate profits remuneration shall be payable in accordance with new

Schedule (Schedule V) of Remuneration and in case a company is not able to comply with the

Schedule V, approval of Central Government would be necessary.

Appointment of Key Managerial Personnel and Tenure

An important new provision incorporated under the Companies Act, 2013 is the definition given

to ‘key managerial personnel (KMP)’ and their appointment. KMP, according to section 2 [51]

means the Chief Executive Officer or the managing director, the Chief Financial Officer; and

such other officer as may be prescribed. Every company belonging to such class or classes of

companies as may be prescribed shall have the whole time KMP. Unless the Articles of a

company provide otherwise or the company does not carry multiple businesses, an individual

shall not be the chairperson of the company as well as the managing director or Chief Executive

Officer at the same time. This is not applicable to such class of companies engaged in multiple

businesses and which has appointed one or more Chief Executive Officers for each such

business. The company secretary can be appointed as whole – time KMP by a resolution of the

Board which stipulating the terms and conditions of appointment including the remuneration. If

the office of any whole – time KMP is vacated, it can be filled up by the Board at a meeting of

the Board within a period of six months from the date of such vacancy. If a company does not

appoint a KMP, the penalty proposed under the Act is Rs. 1,00,000 which may extend to Rs.

5,00,000, Rs. 50,000 and Rs. 1,000 per day if contravention continues on every director or key

managerial position.

Powers of the Board

The Board enjoys the following powers:

1. Power exercisable only at board meetings: The Board of Directors of a company shall

exercise the following powers on behalf of the company at the meeting of the board:

a) Power to make calls on shares in respect of money unpaid on their shares,

b) Power to authorize the buy – back ,

c) Power to issue debentures,

d) Power to borrow moneys otherwise than on debentures,

e) Power to invest the funds of the company and

f) Power to make loans.

2. Powers exercisable only with the consent of the company in general meeting: The

BoD of a public company, or of a private company which is subsidiary of a public

company, shall do the following only with the consent of a general meeting:

a) Sell, lease or otherwise dispose off the whole undertaking of the company.

b) Remit or give time for the repayment of any debt due by a director except

in the case of renewal or continuance of an advance made by a banking

company to its director.

c) Invest, otherwise than in trust securities, the amount of compensation

received by the company in respect of compulsory acquisition, etc.

d) Borrow money, where the money is to be borrowed, together with the

money already borrowed by the company.

e) Contribute to charitable and other funds not directly relating to the

business of the company or welfare of its employees.

Liabilities of Directors

The liabilities of directors are the following:

1. Liability towards the company: A director is liable to the company due to breach of

fiduciary duty, acts which are ultra vires the Memorandum and Articles of

Association, negligence, breach of trust and misfeasance.

2. Liability to third parties: The directors are personally liable to third parties for

misstatement of facts in prospectus, irregular allotment etc.

3. Liability for breach of statutory duties: Directors are bound to comply with the

statutory duties. Any default in compliance of these duties attracts penal

consequences.

4. Liability for acts of co – directors : A director is an agent only of the company and

not of the other members of the board. So any action done by the board does not

impose any form of liability on the director who did not participate in their action or

did not have any knowledge of it.

5. Criminal liability: Actions on the part of directors such as filing of prospectus or

statement in lieu of prospectus containing untrue statement, failure to repay deposits

within the prescribed limit, knowingly making a false or misleading statement thereby

inducing persons to invest money, fraudulently renewing share certificates or issuing

a duplicate certificate, failure to submit balance sheet, profit and loss account at the

annual general meeting, etc. will invite criminal liability to the directors.

Prospectus and Allotment of Securities

Prospectus means any document described or issued as a prospectus includes any notice,

circular, advertisement or other document inviting deposits from the public or inviting offers

from the public for the subscription or purchase of any shares in, or debentures of a body

corporate.

Prospectus has the following characteristics:

1. It must be an invitation to the public.\

2. The invitation must be made by, or on behalf of, the company, or in relation to an

intended company.

3. The invitation must be to subscribe must be to subscribe or purchase shares or

debentures or such other instrument.

Statement in lieu of Prospectus

As per the Act, all public companies are required to either issue a prospectus or file a statement

in lieu of prospectus with the Registrar. A private company is not required to have either of the

above documents. However, when a private company converts itself into a public company it

must either file a prospectus or file a statement in lieu of prospectus.

Issue of Shares

Shares can be issued in any of the following ways:

I. Issue at par: Shares are deemed to have been issued at par when subscribers are

required to pay only the amount equivalent to the nominal or face value of the

shares issued.

II. Issue at premium: If the buyers of shares are required to pay more than the face

value of the share, then that share is said to be issued or sold at a premium.

III. Issue at discount: Prior to the enactment of Companies Act, 2013 issue of shares