Embed Size (px)

Citation preview

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 1/32

LEDGER

When transactions are transferredinto concerned account the system iscalled ledger.

- To identify the amount of debtors

- To know the amount pay to supplier

- To know Good purchased during the period

- To know Amount of Revenue andexpenditure

Procedure of recording up the accounts is

known as Posting.

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 2/32

LEDGER

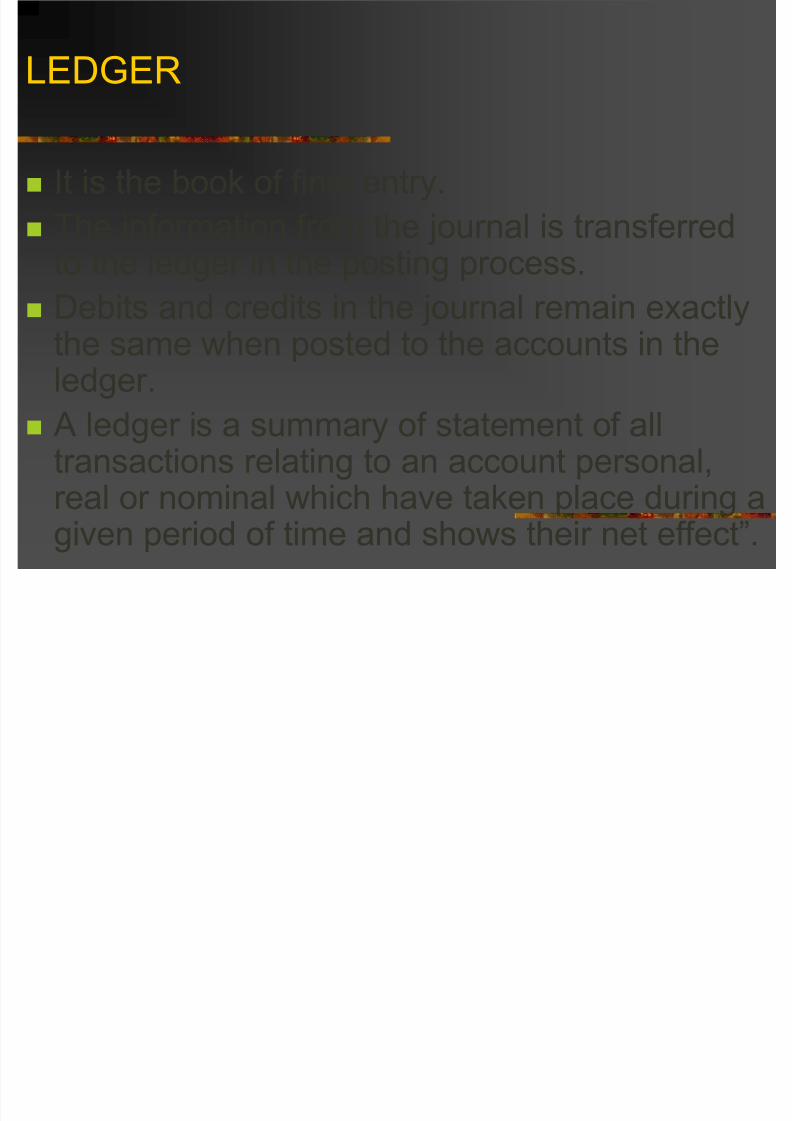

It is the book of final entry.

The information from the journal is transferred

to the ledger in the posting process. Debits and credits in the journal remain exactly

the same when posted to the accounts in theledger.

A ledger is a summary of statement of alltransactions relating to an account personal,real or nominal which have taken place during a

given period of time and shows their net effect”.

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 3/32

Ledger Account------------??

All the transactions pertaining to an account arecollected at one place in the ledger. This helps

to get clear idea of an account at a glance. Thetotal sales, Total purchases, amount due fromcustomer, amount due to customers, cash

balance, bank balance can be ascertained atany time from the ledgers. Ledgers help toprepare the Trial Balance and the final accounts

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 4/32

Ledger Format

1. T-Shaped Ledger Account

Traditional Approach

2. Horizontal Ledger Account With BalanceColumn

Mordern Approach

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 5/32

……………. A/c Cr.Dr.

Date Particulars J.F Amt. Date Particulars J.F Amt

To............... xxxx By ………… xxxx

xxxx xxxx

Ledger Format T-Shaped

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 6/32

Balancing the ledger Account:

Difference of total Dr & total Cr is Balancing Amount

If Total Dr > Total Cr, the balancing amount isappear in Cr side representing By balance c/d,called Debit balance.

If Total Cr > Total Dr, the balancing amount isappear in Dr side representing To balance c/d,called Credit balance.

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 7/32

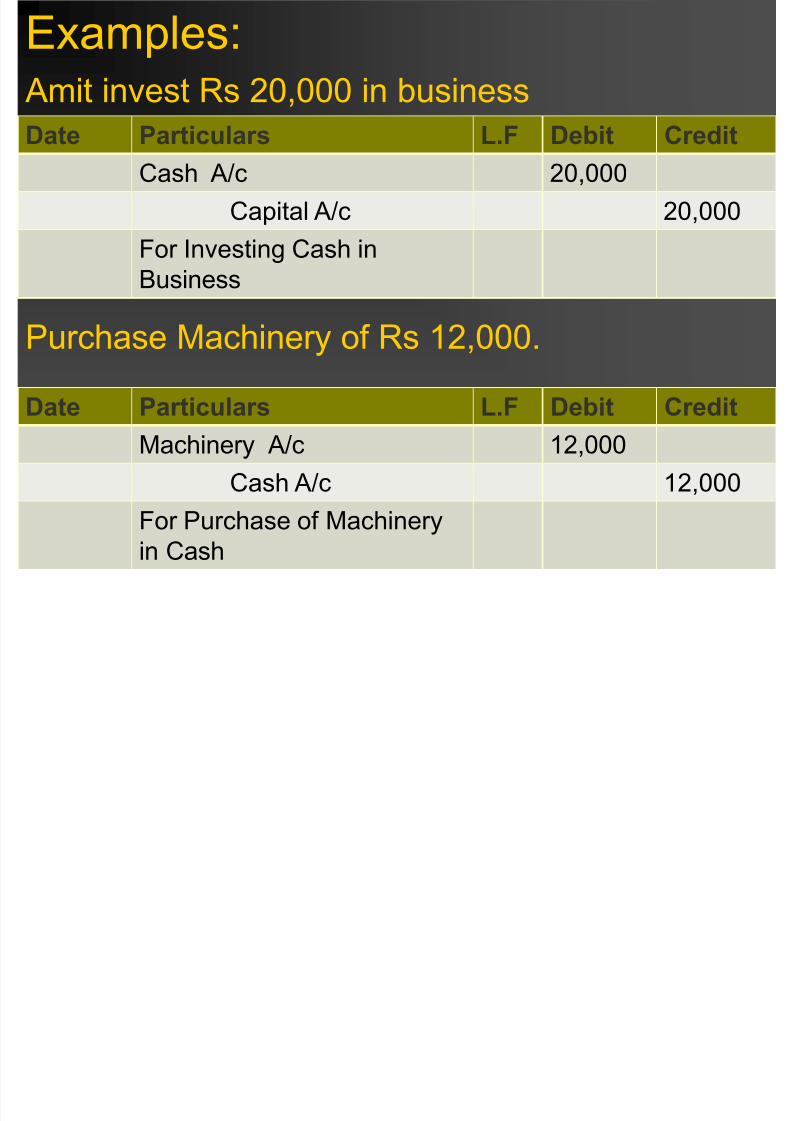

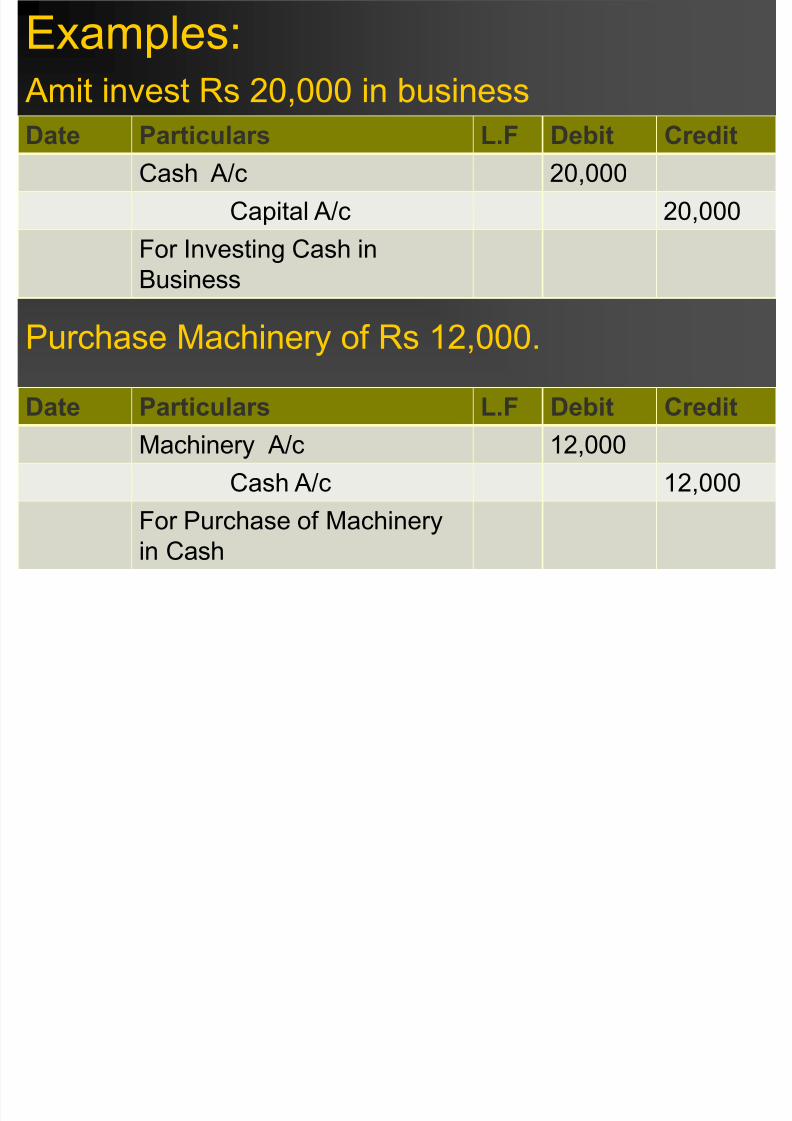

Examples:Amit invest Rs 20,000 in business

Date Particulars L.F Debit CreditCash A/c 20,000

Capital A/c 20,000

For Investing Cash inBusiness

Purchase Machinery of Rs 12,000.

Date Particulars L.F Debit Credit

Machinery A/c 12,000

Cash A/c 12,000

For Purchase of Machineryin Cash

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 8/32

Balancing the ledger Account:

date Particulars J.

F

Amt date Particulars J.

F

Amt

To Capital 20,000 By Machinery 12,000

By balancec/d 8,000

20,000 20,000

Cash A/c Cr.Dr.

Difference of total Dr & total Cr is Balancing Amount:

Here, Total Dr – Total Cr = Balancing Amount20,000 – 12,000 = 8,000

Also, Total Dr > Total Cr, the balancing amount isappear in Cr side representing By balance c/d, called

Debit balance.

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 9/32

Balancing the ledger Account:

date Particulars J.

F

Amt date Particulars J.

F

Amt

To balance

c/d

20,000 By Cash 20,000

20,000 20,000

Capital A/c Cr.Dr.

Difference of total Dr & total Cr is Balancing Amount:

Here, Total Cr – Total Dr = Balancing Amount20,000 – 0 = 20,000

Also, Total Cr > Total Dr, the balancing amount isappear in Dr side representing To balance c/d, called

Credit balance.

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 10/32

Horizontal Ledger Account WithBalance Column

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 11/32

Examples:Amit invest Rs 20,000 in business

Date Particulars L.F Debit CreditCash A/c 20,000

Capital A/c 20,000

For Investing Cash inBusiness

Purchase Machinery of Rs 12,000.

Date Particulars L.F Debit Credit

Machinery A/c 12,000

Cash A/c 12,000

For Purchase of Machineryin Cash

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 12/32

Horizontal Ledger Account WithBalance Column

Date Transaction Debit Credit Balance

Opening Balance 0

Investing in Cash 20,000 20,000

Purchase of machinery 12,000 8,000

Cash A/c

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 13/32

© Mary Low

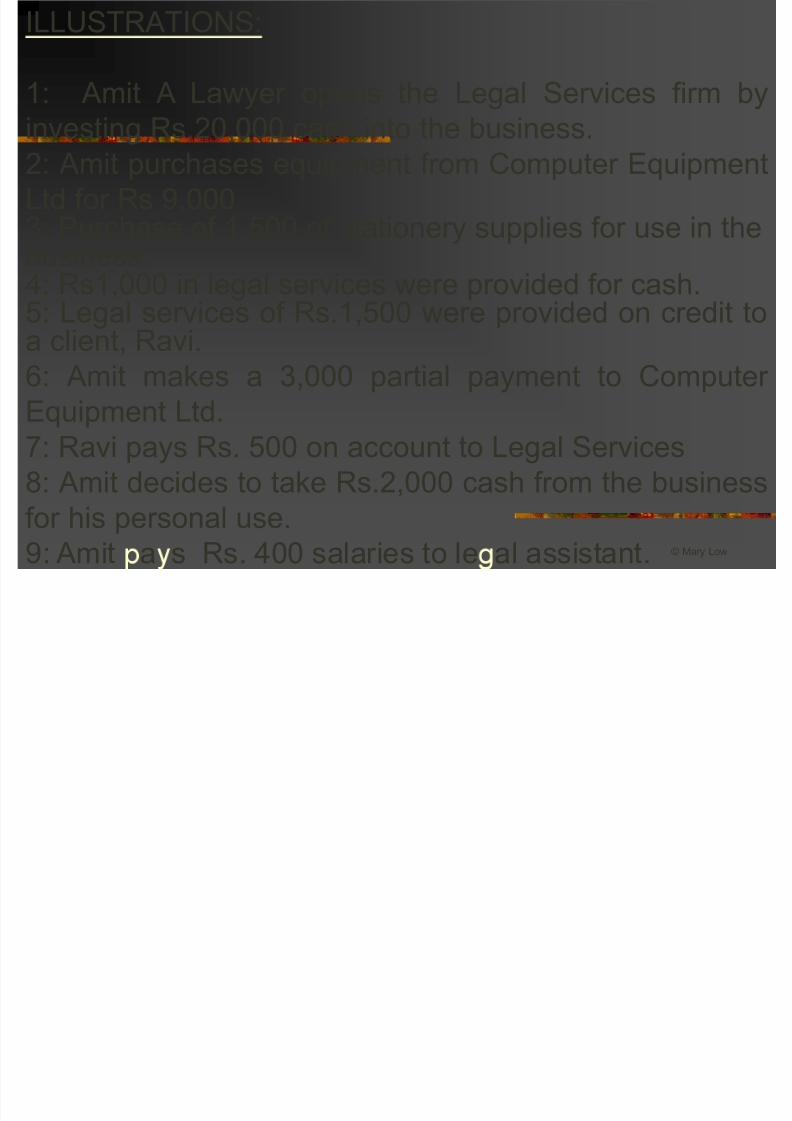

ILLUSTRATIONS:

1: Amit A Lawyer opens the Legal Services firm by

investing Rs.20,000 cash into the business.2: Amit purchases equipment from Computer EquipmentLtd for Rs 9,0003: Purchase of 1,500 of stationery supplies for use in the

business.4: Rs1,000 in legal services were provided for cash.5: Legal services of Rs.1,500 were provided on credit toa client, Ravi.6: Amit makes a 3,000 partial payment to Computer

Equipment Ltd.7: Ravi pays Rs. 500 on account to Legal Services8: Amit decides to take Rs.2,000 cash from the businessfor his personal use.9: Amit a s Rs. 400 salaries to le al assistant.

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 14/32

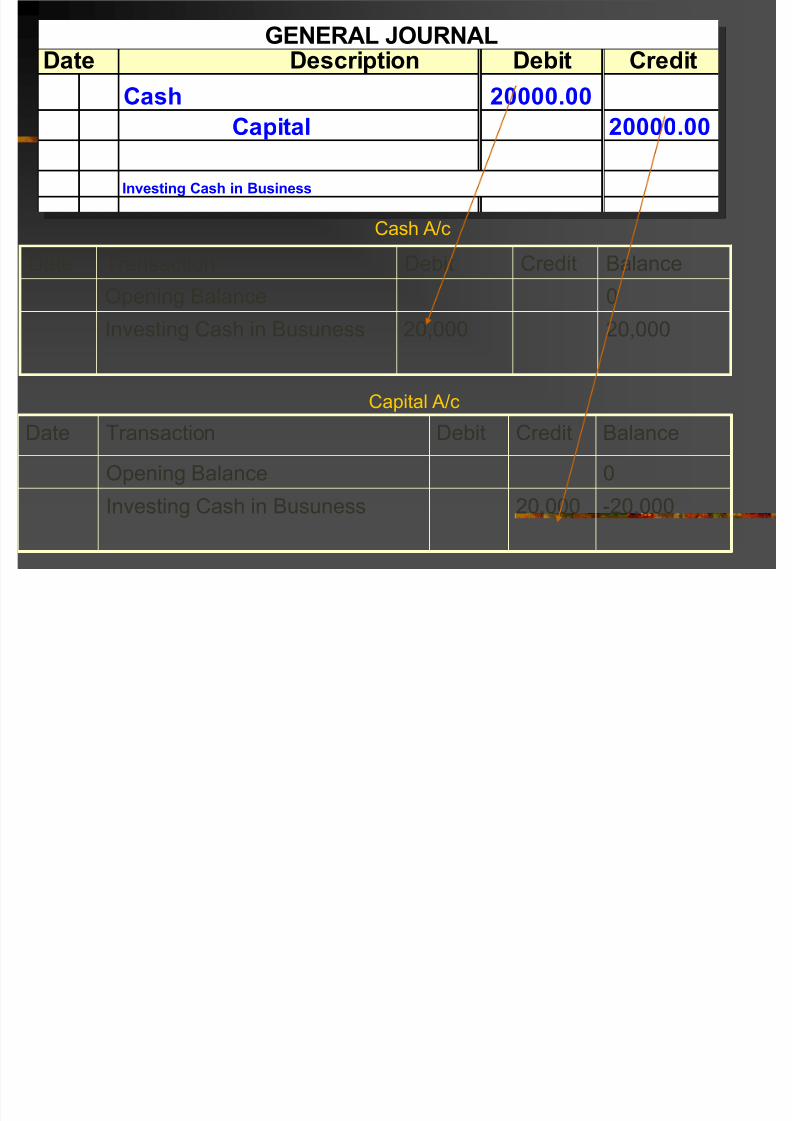

Journal 1

Date Description Debit Credit

Cash 20000.00

Capital 20000.00

GENERAL JOURNAL

Investing Cash in Business

Date Transaction Debit Credit Balance

Opening Balance 0

Investing Cash in Busuness 20,000 -20,000

Date Transaction Debit Credit BalanceOpening Balance 0

Investing Cash in Busuness 20,000 20,000

Cash A/c

Capital A/c

GENERAL JOURNAL

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 15/32

Date Description Debit Credit

Computer Equipment A/c 9000.00

Com. Equ. Ltd 9000.00

GENERAL JOURNAL

Purchase of Equipment on Credit

Date Transaction Debit Credit Balance

Opening Balance 0

Purchase Of Equipment onCredit

9,000 9,000

Date Transaction Debit Credit Balance

Opening Balance 0

Purchase Of Equipment on Credit 9,000 -9,000

Com. Equ. Ltd A/c

Computer Equipment A/c

GENERAL JOURNAL

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 16/32

Date Description Debit Credit

Supplies A/c 1500.00

Cash 1500.00

GENERAL JOURNAL

Purchase Of Suplies in Cash

Date Transaction Debit Credit Balance

Opening Balance 0

Purchase Of Supplies in Cash 1,500 1,500

Date Transaction Debit Credit Balance

Opening Balance 0

Investing Cash in Business 20,000 20,000

Purchase Of Supplies in Cash 1,500 18,500

Cash A/c

Supplies A/c

GENERAL JOURNAL

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 17/32

Date Description Debit Credit

Cash A/c 1000.00

Service Revenue A/c 1000.00

GENERAL JOURNAL

Legal Service revenue earned in cash

Date Transaction Debit Credit Balance

Opening Balance 0

1 Investing in Cash 20,000 20,000

2 Purchase Of Supplies in Cash 1,500 18,500

3 Service Revenue earned in Cash 1,000 19,500

Date Transaction Debit Credit BalanceOpening Balance 0

Service Revenue earned in Cash 1,000 -1,000

Cash A/c

Service Revenue A/c

GENERAL JOURNAL

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 18/32

Date Description Debit Credit

Ravi A/c 2500.00

Service Revenue 2500.00

GENERAL JOURNAL

Legal Service Revenue earned in Credit

Date Transaction Debit Credit Balance

Opening Balance 0

Service Revenue earned in credit 1,500 1,500

Date Transaction Debit Credit Balance

Opening Balance 0Service Revenue earned in Cash 1,000 -1,000

Service Revenue earned in credit 2,500 -3,500

Service Revenue A/c

Ravi A/c

GENERAL JOURNAL

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 19/32

Date Description Debit Credit

Com.Equ. Ltd A/c 3000.00

Cash A/c 3000.00

GENERAL JOURNAL

Paid Cash to Computer Equipment Ltd.

Cash A/c

Com. Equ. Ltd A/c

Date Transaction Debit Credit Balance

Opening Balance 0

1 Investing in Cash 20,000 20,000

2 Purchase Of Supplies in Cash 1,500 18,500

3 Service Revenue earned in Cash 1,000 19,500

4 Paid cash to computer equipment ltd. 3,000 16,500

Date Transaction Debit Credit Balance

Opening Balance 0

Purchase Of Equipment on Credit 9,000 -9,000

Paid cash to computer equipment ltd. 3,000 -6,000

GENERAL JOURNAL

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 20/32

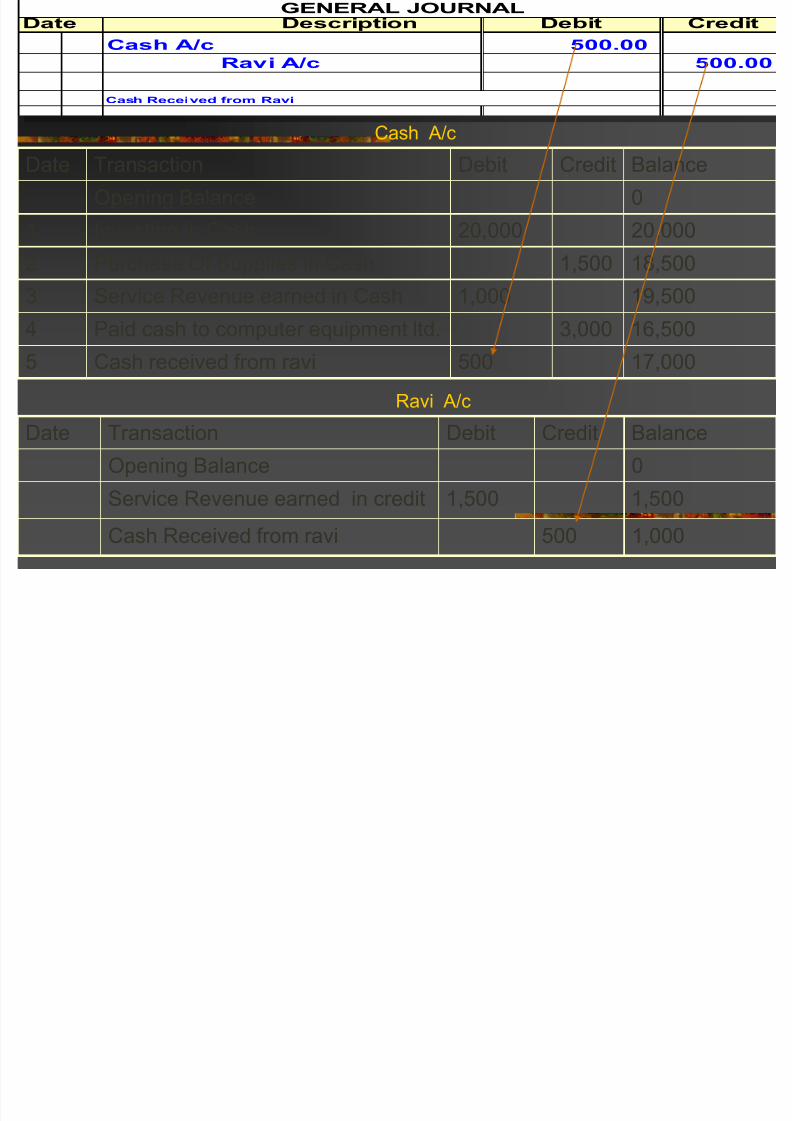

Date Description Debit Credit

Cash A/c 500.00

Ravi A/c 500.00

GENERAL JOURNAL

Cash Received from Ravi

Date Transaction Debit Credit Balance

Opening Balance 0

1 Investing in Cash 20,000 20,000

2 Purchase Of Supplies in Cash 1,500 18,5003 Service Revenue earned in Cash 1,000 19,500

4 Paid cash to computer equipment ltd. 3,000 16,500

5 Cash received from ravi 500 17,000

Date Transaction Debit Credit Balance

Opening Balance 0

Service Revenue earned in credit 1,500 1,500

Cash Received from ravi 500 1,000

Cash A/c

Ravi A/c

Date Description Debit Credit

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 21/32

© Mary Low

Date Description Debit Credit

Drawing A/c 2000.00

Cash A/c 2000.00

Cash Drawing for personal use

Date Transaction Debit Credit Balance

Opening Balance 0

1 Investing in Cash 20,000 20,0002 Purchase Of Supplies in Cash 1,500 18,500

3 Service Revenue earned in Cash 1,000 19,500

4 Paid cash to computer equipment ltd. 3,000 16,500

5 Cash received from ravi 500 17,000

6 Cash Drawing for personal use 2,000 15,000

Drawing A/c

Cash A/c

Date Transaction Debit Credit Balance

Opening Balance 0

1 Cash Drawing for personal use 2,000 2,000

GENERAL JOURNAL

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 22/32

© Mary Low

Date Description Debit Credit

Salary A/c 400.00

Cash A/c 400.00

GENERAL JOURNAL

Salary Paid to Legal assistant

Date Transaction Debit Credit Balance

Opening Balance 0

Salary Paid to legal assistant 400 400

Date Transaction Debit Credit Balance

Opening Balance 0

1 Investing in Cash 20,000 20,000

2 Purchase Of Supplies in Cash 1,500 18,5003 Service Revenue earned in Cash 1,000 19,500

4 Paid cash to computer equipment ltd. 3,000 16,500

5 Cash received from ravi 500 17,000

6 Cash Drawing for personal use 2,000 15,0007 Salar Paid to le al assistant 400 14 600

Cash A/c

Salary A/c

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 23/32

T-Ledger Account

Date Particulars J.F Amount Date Particulars J.F Amount

To Capital A/c 20,000 By Supplies A/c 1,500

To Service revenue 1,000 By A/P (Com. Equ.ltd) 3,000

To A/R (Ravi) 5,00 By Drawing 2,000

By Salary 400

By Balance c/d 14600

21,500 21,500

Cash A/c Cr.Dr.

Balancing the ledger Account:Difference of total Dr & total Cr is Balancing Amount

If Total Dr > Total Cr, the balancing amount is appear in Cr siderepresenting By balance c/d, called Debit balance.If Total Cr > Total Dr, the balancing amount is appear in Dr siderepresenting To balance c/d, called Credit balance.

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 24/32

T-Ledger Account

Date Particulars J.F Amount Date Particulars J.F Amount

To Balance c/d 20,000 By Cash A/c 20,000

20,000 20,000

Capital A/c Cr.Dr.

Balancing the ledger Account:Difference of total Dr & total Cr is Balancing Amount

If Total Dr > Total Cr, the balancing amount is appear in Cr siderepresenting By balance c/d, called Debit balance.If Total Cr > Total Dr, the balancing amount is appear in Dr siderepresenting To balance c/d, called Credit balance.

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 25/32

T-Ledger Account

Date Particulars J.F Amount Date Particulars J.F Amount

To A/P (Comp.

Equip. ltd)

9,000 By balance c/d 9,000

9,000 9,000

Computer Equipment A/c Cr.Dr.

Balancing the ledger Account:Difference of total Dr & total Cr is Balancing Amount

If Total Dr > Total Cr, the balancing amount is appear in Cr siderepresenting By balance c/d, called Debit balance.If Total Cr > Total Dr, the balancing amount is appear in Dr siderepresenting To balance c/d, called Credit balance.

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 26/32

T-Ledger Account

Date Particulars J.F Amount Date Particulars J.F Amount

To Cash 3,000 By Computer

Equipment A/c

9,000

To Balance c/d 6,000

9,000 9,000

A/P(Computer Equipment ltd) A/c Cr.Dr.

Balancing the ledger Account:Difference of total Dr & total Cr is Balancing Amount

If Total Dr > Total Cr, the balancing amount is appear in Cr siderepresenting By balance c/d, called Debit balance.If Total Cr > Total Dr, the balancing amount is appear in Dr siderepresenting To balance c/d, called Credit balance.

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 27/32

© Mary Low

Some more Examples

Start a business with Rs. 5000 cash and a buildingworth Rs. 10000Purchase goods worth Rs. 2000, out of which 1200 oncredit from RamPurchase Machinery of Rs. 2500, Rs 500 paid in Cash

& remaining Through Bank LoanSold goods for Rs. 600, including Rs. 400 to ShyamReceived Rs. 380 from shyam in full settlement of hisaccount

Paid Rs. 100 for wages & salary Rs. 50Paid Rs 1150 for Ram for his full claimWithdraw Rs. 400 from his business, out of which 50%is for personal purpose & remaining for businesspromotion

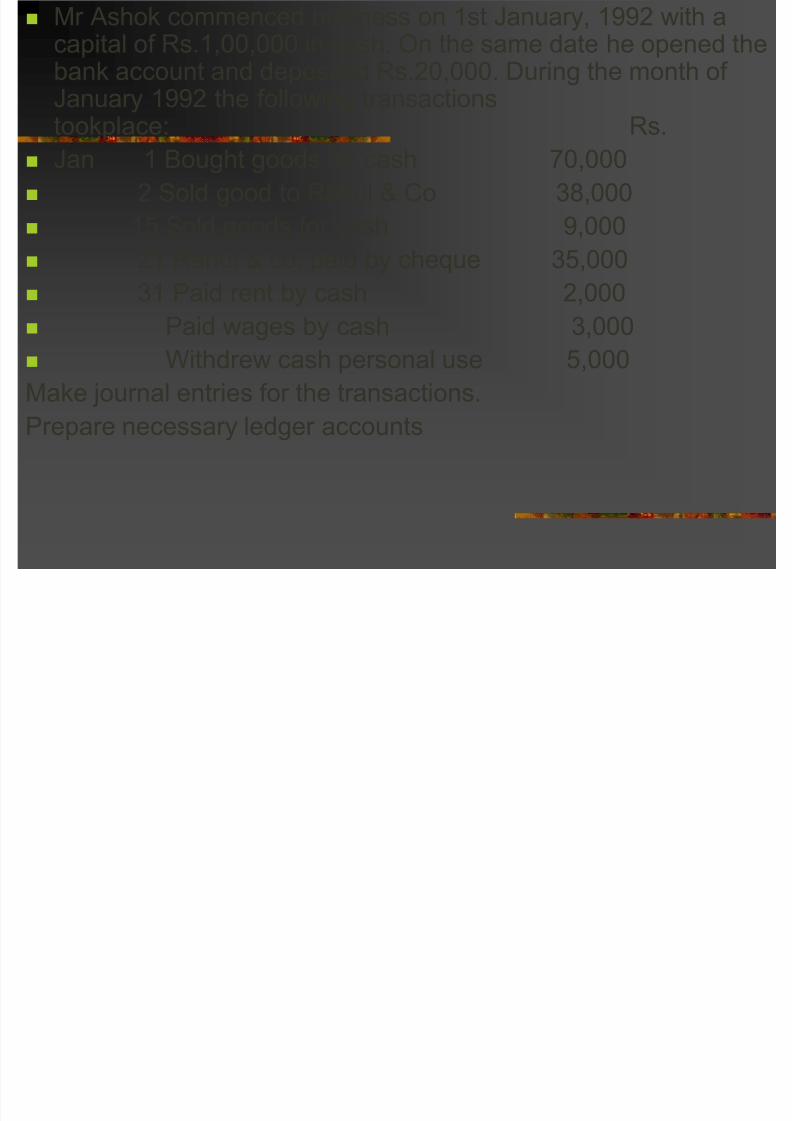

Mr Ashok commenced business on 1st January 1992 with a

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 28/32

Mr Ashok commenced business on 1st January, 1992 with acapital of Rs.1,00,000 in cash. On the same date he opened thebank account and deposited Rs.20,000. During the month ofJanuary 1992 the following transactions

tookplace: Rs. Jan 1 Bought goods for cash 70,000

2 Sold good to Rahul & Co 38,000

15 Sold goods for cash 9,000

21 Rahul & co. paid by cheque 35,000 31 Paid rent by cash 2,000

Paid wages by cash 3,000

Withdrew cash personal use 5,000

Make journal entries for the transactions.Prepare necessary ledger accounts

1)Mr A deposited into bank Rs 50 000 to start a business

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 29/32

1)Mr.A deposited into bank Rs.50,000 to start a business

2) Paid rent for three months at Rs.2500 per month

3) Bought office equipment from B&Co. for Rs. 10000, paid tothem Rs.3000 and promised to pay the balance after two

months. 4) Rendered services to clients and received cash Rs. 5000

5) Purchase supplies for cash Rs. 400

6) Paid salaries to staff Rs. 5400

7) Bought furniture for Rs. 3200,paid to K&Co. Rs.1200 andpromised to pay balance after one month

8) Withdrew cash for personal use Rs. 3000

9) Billed to Nasir for services rendered Rs. 12500

10) Received from Nasir Rs.5000INSTRUCTION

A: Prepare journal entries

B: Post to ledger accounts

(Considering All payments through Bank)

Prepare Jornal entries and make necessary ledger

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 30/32

Prepare Jornal entries and make necessary ledgeraccounts from the following transactions

1. Mr. Ahmed invested cash Rs. 125,000

2. Bought merchandise for cash Rs.200003. Paid rent for the month Rs.50004. Purchase office supplies for Rs.15005. Sold goods for cash Rs.5000

6. Purchase goods on credit from Nasir Ali Rs.100007. Paid salaries to office staff Rs. 125008. Paid to Nasir Ali Rs.35009. Sold goods on credit to Abid Rs.1500010. Merchandise return to Nasir Ali Rs.25011. Goods were returned by Abid Rs.75012. Withdrew cash for personal use Rs.1000

13. Sold old machine at Rs 500

In July 2005 Nasir Jamal started business and

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 31/32

In July 2005, Nasir Jamal started business andcompleted following transactions.

July 1 He deposited $ 165,000 cash in a business

July 2 Purchased equipment for $ 55,000 from ABC Co.paid $20,000 and balance will be paid after threemonth.

July 7 Paid rent for three months $ 1500

July 12 Purchase goods on credit from Khan & Co. $1200

July 17 Paid salaries to staff $ 2500

July 20 Paid to Khan & Co.$ 700

July 23 Paid insurance $ 400

July 27 Nasir withdrew $ 1500 cash from the businessfor personal use

Prepare journal entries and Ledger accounts.

Khalid invested in business cash Rs 40000 office

8/10/2019 BBA Ledger Account

http://slidepdf.com/reader/full/bba-ledger-account 32/32

. Khalid invested in business cash Rs.40000, officeequipment Rs.60,0002. Purchase merchandise for cash Rs. 60003. Purchase goods on credit from Zahid Rs.10000

4. Sold merchandise on credit to Amir Rs.100005. Paid rent expense Rs.6006. Sold merchandise for cash Rs. 35007. Earned commission Rs. 10000

8. Purchase supplies on credit from Aleem Rs. 8009. Paid traveling expense Rs. 65010. Sold merchandise to Mr. Kareem Rs. 4000 oncredit.

11. Khalid withdrew cash for personal use Rs. 300012. Rendered services to client and receivedcommission Rs. 200013. Paid insurance for the month Rs. 500

Prepare journal entries and Ledger accounts