Embed Size (px)

Citation preview

Basics of Private Equity Taxation Steven D. Bortnick Partner, Pepper Hamilton LLP

Presented to The Wharton Private Equity and Venture Capital Club | January 17, 2012

#15411207v.1

2

The Essentials-What We’ll Cover

• Corporate Acquisitions − When can a transaction be tax-free − When taxable transactions are preferred over tax-free

transactions − Examples of certain tax-free transactions − Stock sales versus asset sales

3

The Essentials – What We’ll Cover

• Partnership Investments − Tax efficiency − Basis step up − Special issues for tax-exempt investors (UBTI)

4

The Essentials-What We’ll Cover

• Financing Issues − Various rules that may limit deductibility of interest in the

US

5

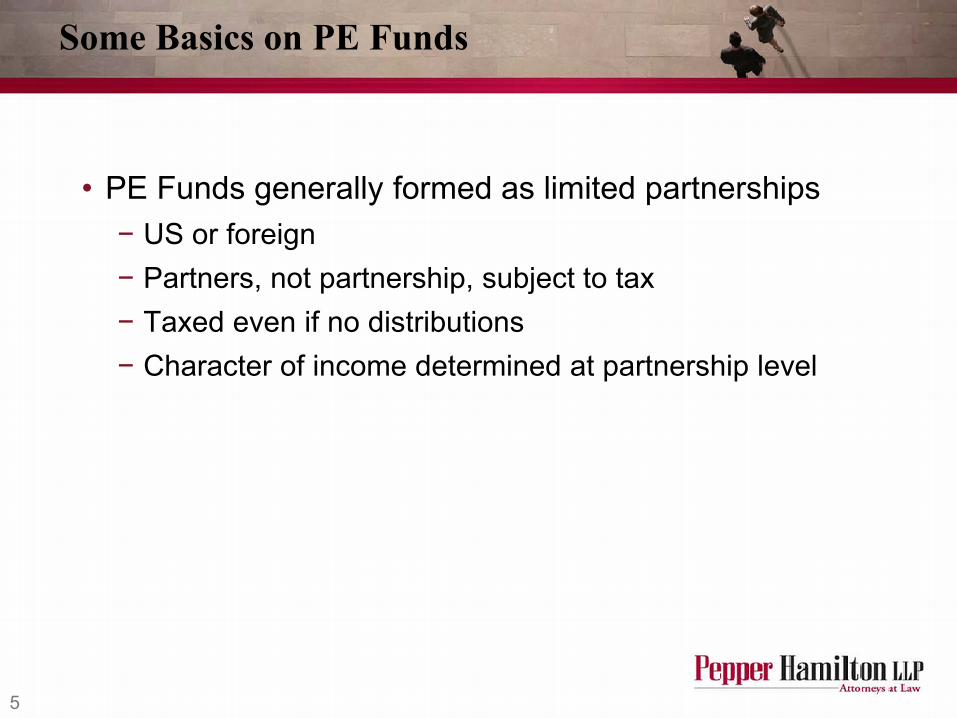

Some Basics on PE Funds

• PE Funds generally formed as limited partnerships − US or foreign − Partners, not partnership, subject to tax − Taxed even if no distributions − Character of income determined at partnership level

6

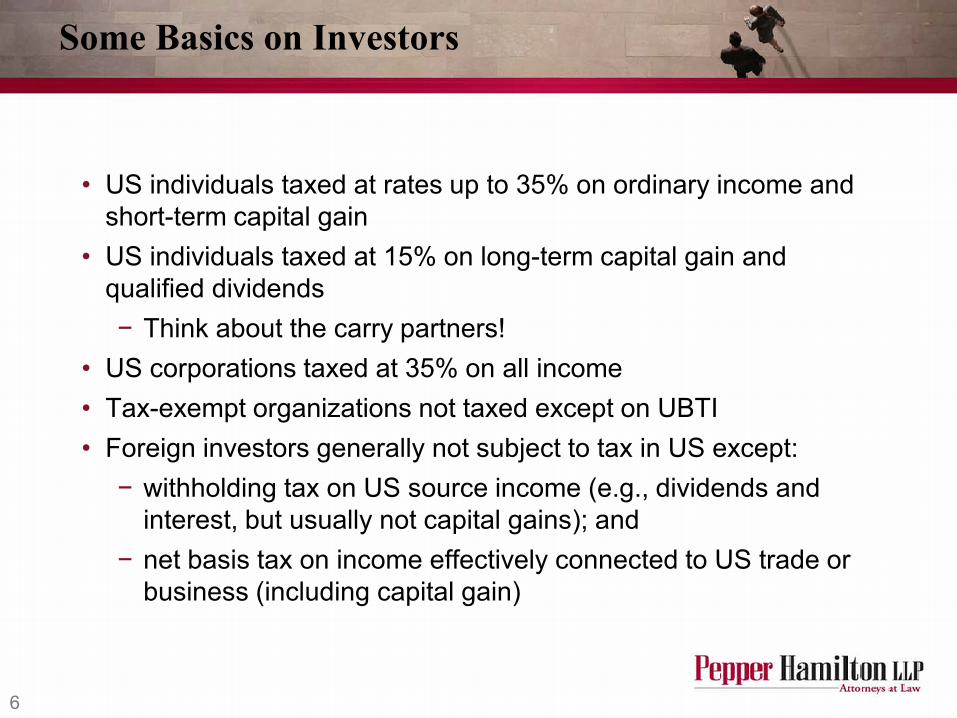

Some Basics on Investors

• US individuals taxed at rates up to 35% on ordinary income and short-term capital gain

• US individuals taxed at 15% on long-term capital gain and qualified dividends − Think about the carry partners!

• US corporations taxed at 35% on all income • Tax-exempt organizations not taxed except on UBTI • Foreign investors generally not subject to tax in US except:

− withholding tax on US source income (e.g., dividends and interest, but usually not capital gains); and

− net basis tax on income effectively connected to US trade or business (including capital gain)

7

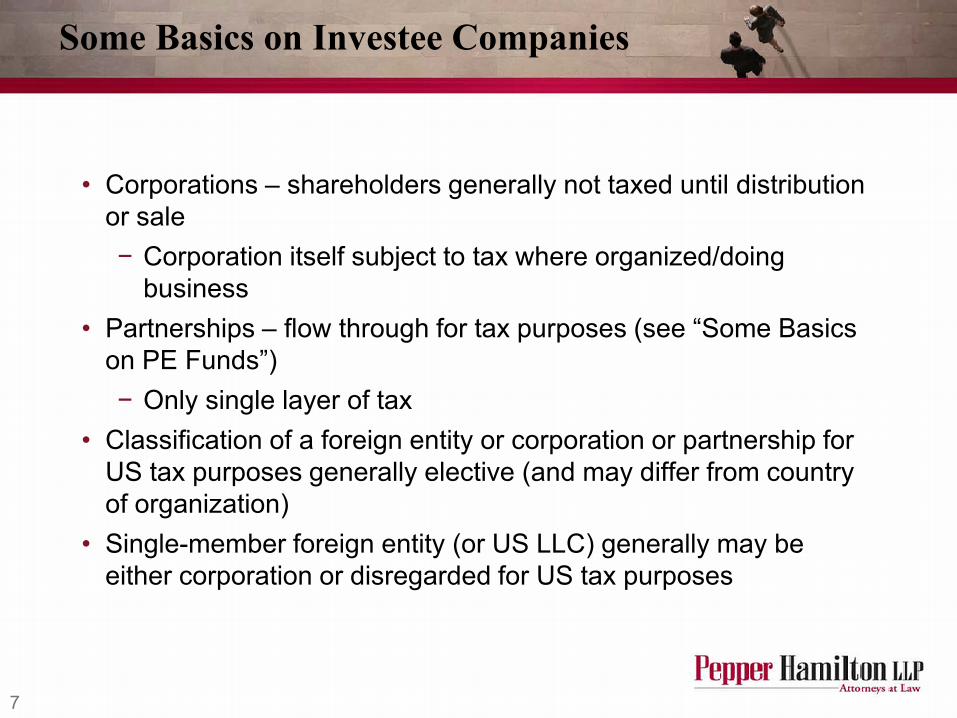

Some Basics on Investee Companies

• Corporations – shareholders generally not taxed until distribution or sale − Corporation itself subject to tax where organized/doing

business • Partnerships – flow through for tax purposes (see “Some Basics

on PE Funds”) − Only single layer of tax

• Classification of a foreign entity or corporation or partnership for US tax purposes generally elective (and may differ from country of organization)

• Single-member foreign entity (or US LLC) generally may be either corporation or disregarded for US tax purposes

8

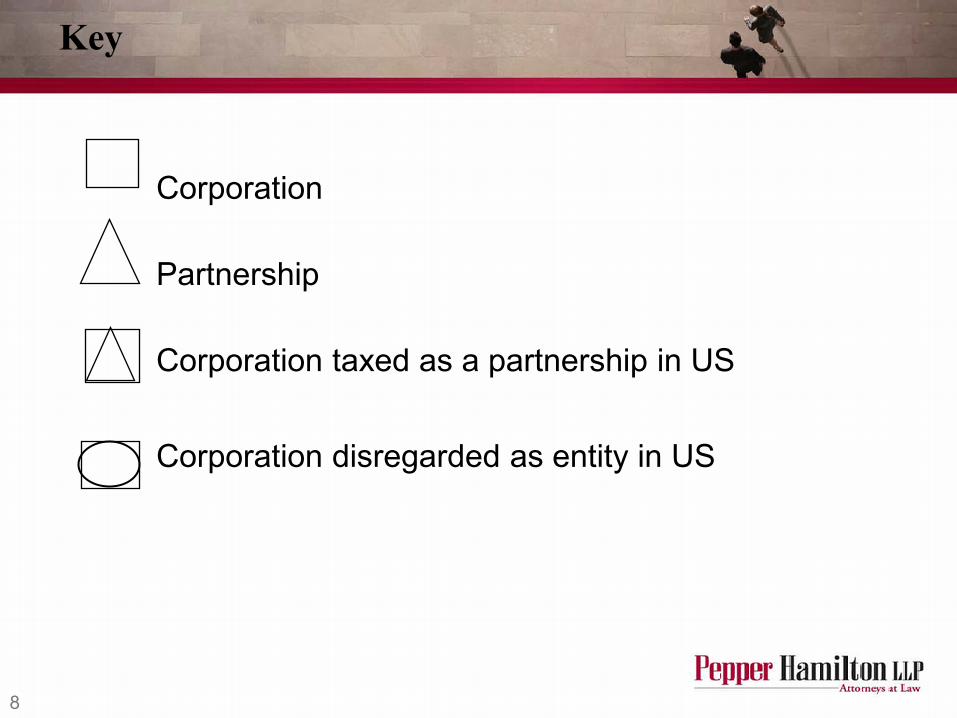

Key

Corporation

Partnership

Corporation taxed as a partnership in US Corporation disregarded as entity in US

9

Corporate Acquisitions

10

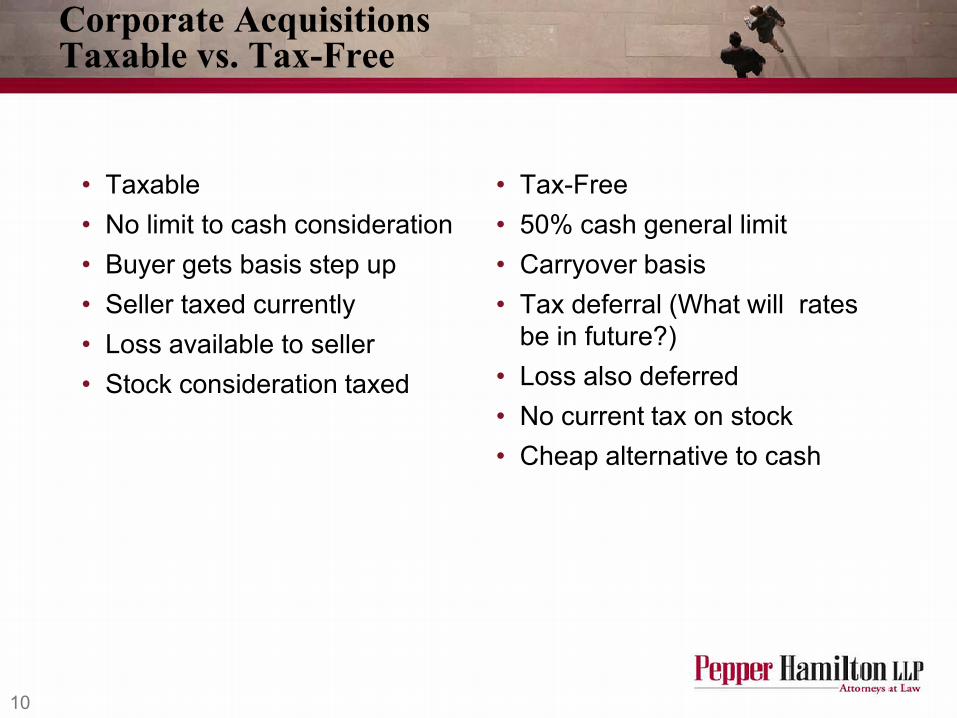

Corporate Acquisitions Taxable vs. Tax-Free

• Taxable • No limit to cash consideration • Buyer gets basis step up • Seller taxed currently • Loss available to seller • Stock consideration taxed

• Tax-Free • 50% cash general limit • Carryover basis • Tax deferral (What will rates

be in future?) • Loss also deferred • No current tax on stock • Cheap alternative to cash

11

Corporate Taxable Acquisitions

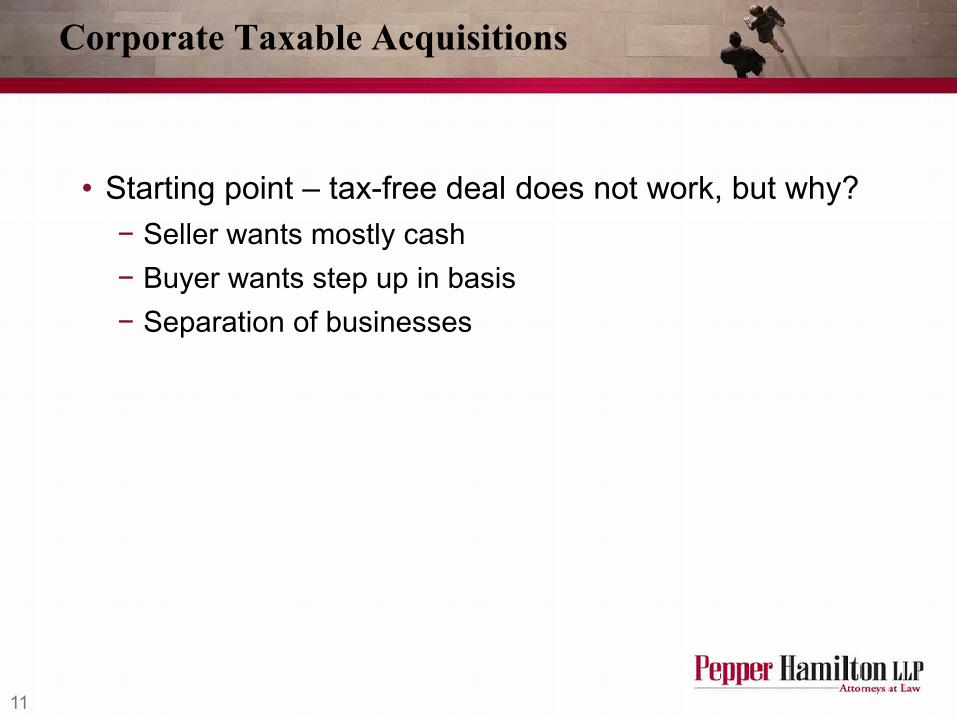

• Starting point – tax-free deal does not work, but why? − Seller wants mostly cash − Buyer wants step up in basis − Separation of businesses

12

Buyer’s Perspective

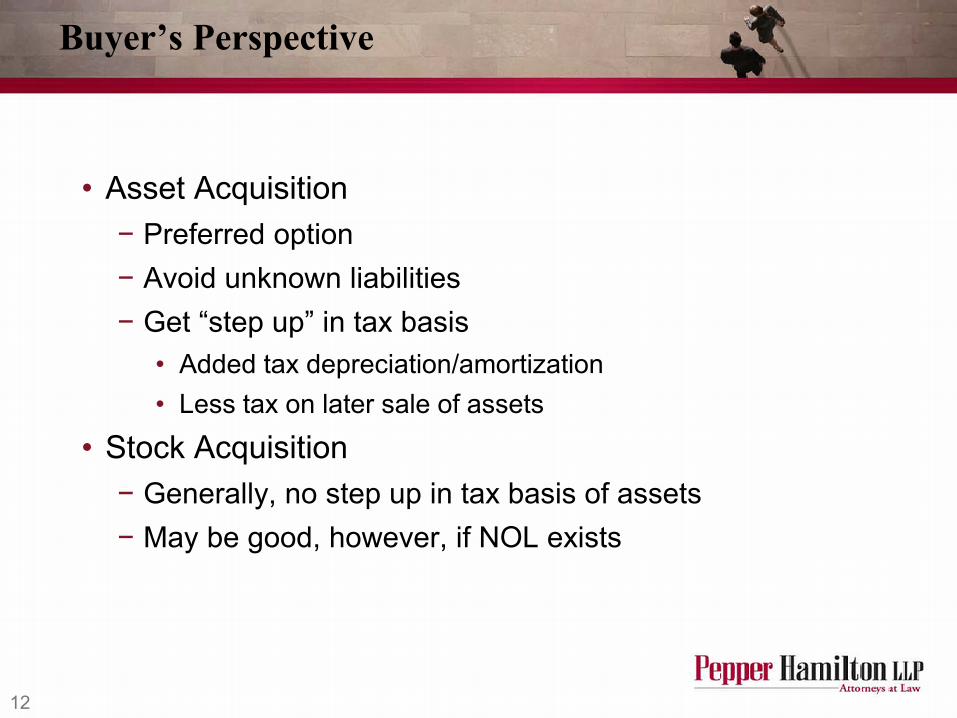

• Asset Acquisition − Preferred option − Avoid unknown liabilities − Get “step up” in tax basis

• Added tax depreciation/amortization • Less tax on later sale of assets

• Stock Acquisition − Generally, no step up in tax basis of assets − May be good, however, if NOL exists

13

Seller’s Perspective

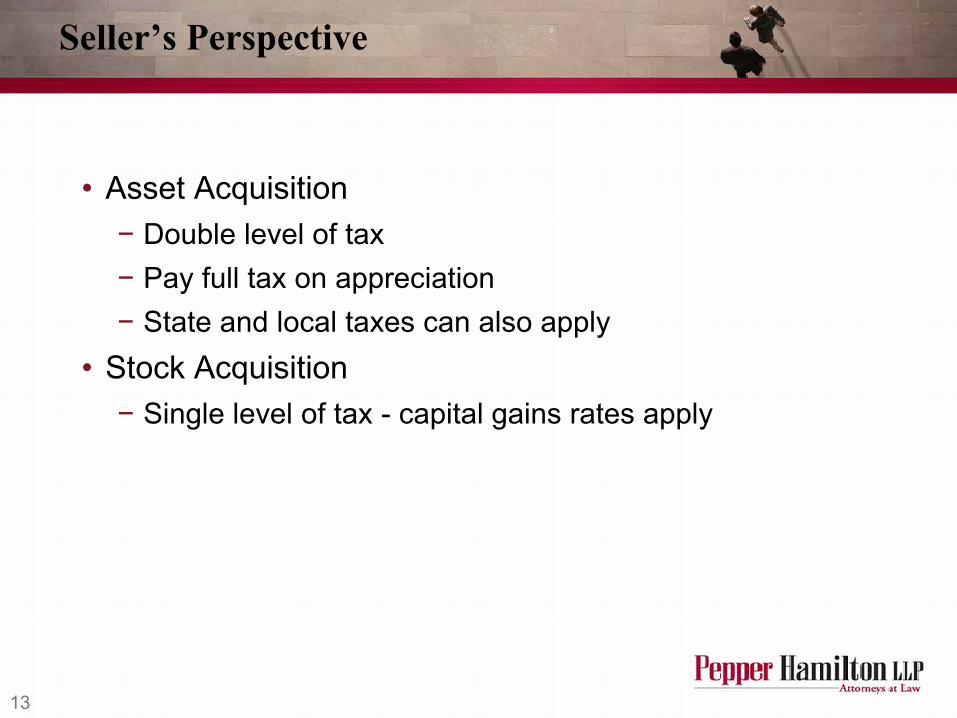

• Asset Acquisition − Double level of tax − Pay full tax on appreciation − State and local taxes can also apply

• Stock Acquisition − Single level of tax - capital gains rates apply

14

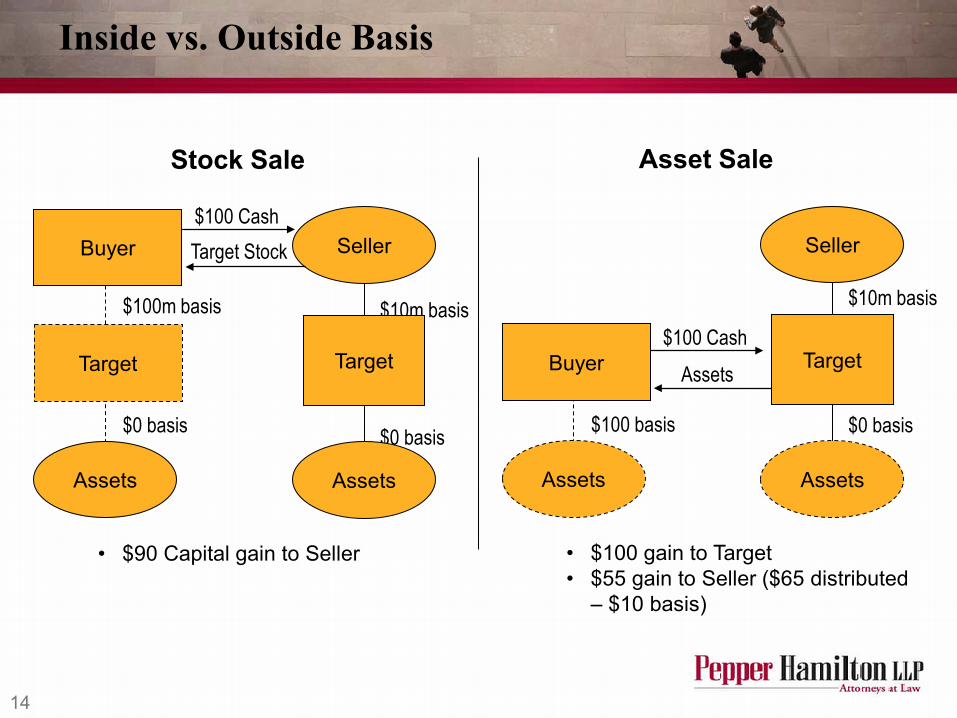

Inside vs. Outside Basis

$10m basis

$0 basis

Buyer

Target

Assets

Target

Assets

Seller $100 Cash Target Stock

$100m basis

$0 basis

• $90 Capital gain to Seller

Stock Sale

Buyer

Assets

Target

Assets

Seller

$100 Cash Assets

$10m basis

$0 basis $100 basis

• $100 gain to Target • $55 gain to Seller ($65 distributed

– $10 basis)

Asset Sale

15

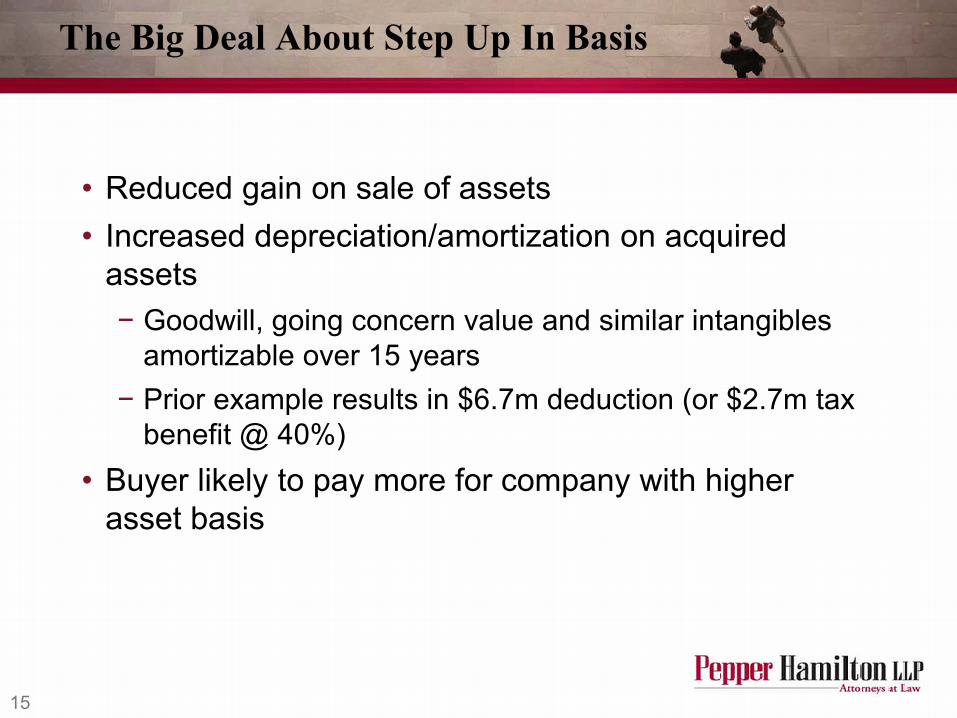

The Big Deal About Step Up In Basis

• Reduced gain on sale of assets • Increased depreciation/amortization on acquired

assets − Goodwill, going concern value and similar intangibles

amortizable over 15 years − Prior example results in $6.7m deduction (or $2.7m tax

benefit @ 40%) • Buyer likely to pay more for company with higher

asset basis

16

A Cross Between Stock and Asset Deals

• 338 Election − Treats a stock deal like an asset deal − Purchaser must be a corporation − Must acquire 80% of target “by purchase”

• Fully taxable • Watch out for tax-free rollovers

− Corporate and Shareholder taxation − Tax is on 100% even if bought only 80%

17

338 – S Corps and Consolidated Subs.

• Target is S Corporation or subsidiary that files consolidated return with seller

• Joint 338(h)(10) election is made • Treated as asset sale • Selling shareholders (in S Corp) or selling consolidated group

pay tax • Single tax with full basis step up!!

− Higher tax if outside basis greater than inside basis and Target C corp. sub.

− May convert some capital gain to ordinary income − Beware the S Corporation that was a C Corporation in past 10

years

18

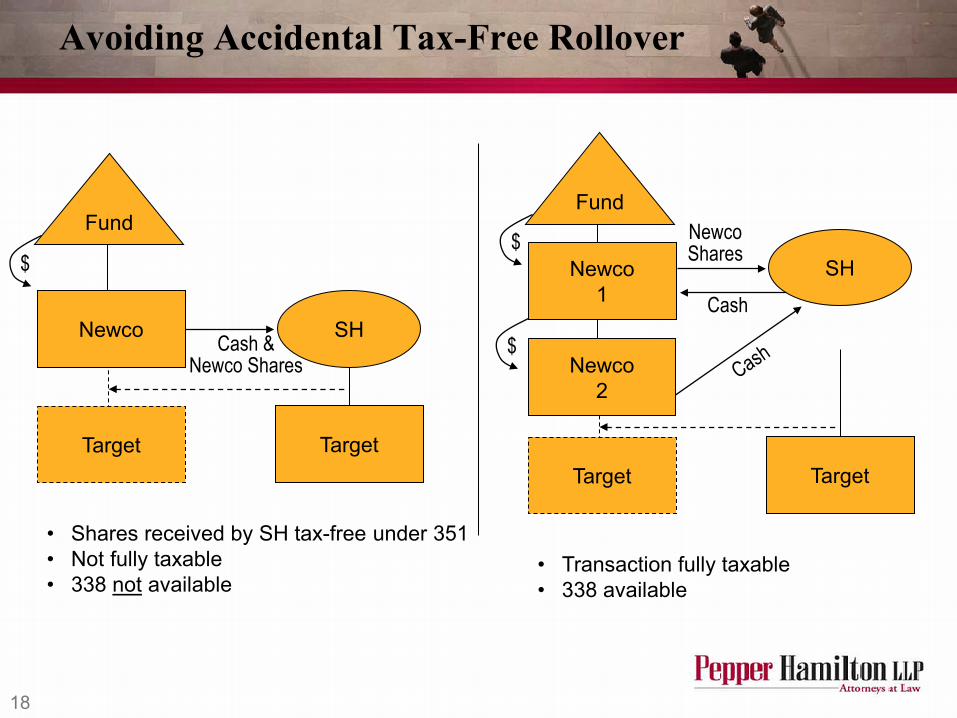

Avoiding Accidental Tax-Free Rollover

Newco

Target

SH Cash & Newco Shares

$

• Shares received by SH tax-free under 351 • Not fully taxable • 338 not available

Target

Fund

Newco 2

Target

SH

• Transaction fully taxable • 338 available

Target

Fund

$ Newco

1

$

Newco Shares

Cash

19

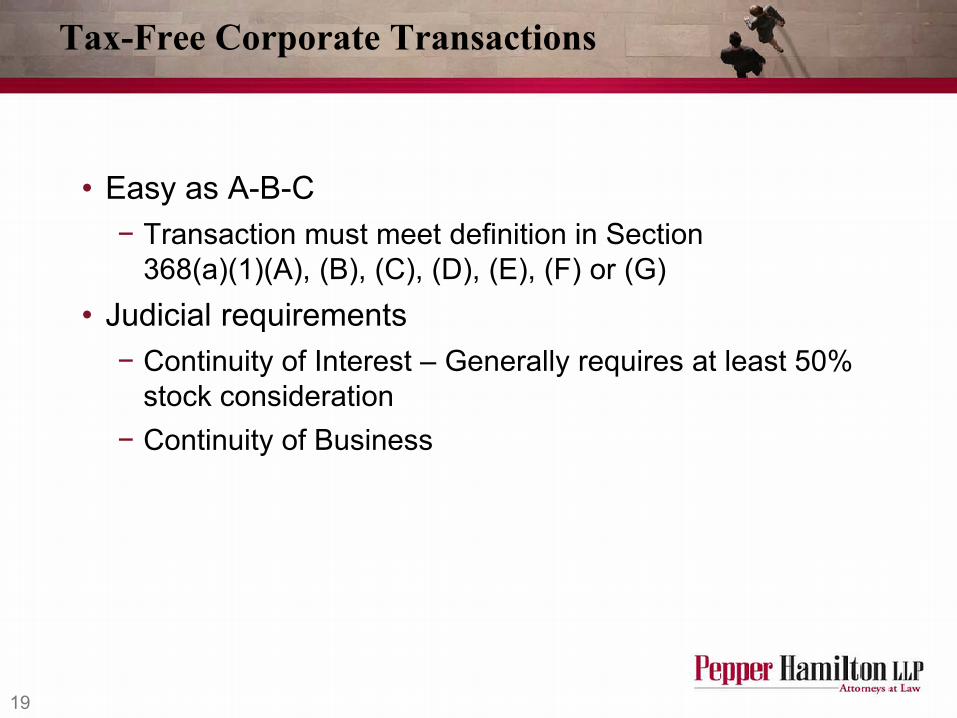

Tax-Free Corporate Transactions

• Easy as A-B-C − Transaction must meet definition in Section

368(a)(1)(A), (B), (C), (D), (E), (F) or (G) • Judicial requirements

− Continuity of Interest – Generally requires at least 50% stock consideration

− Continuity of Business

20

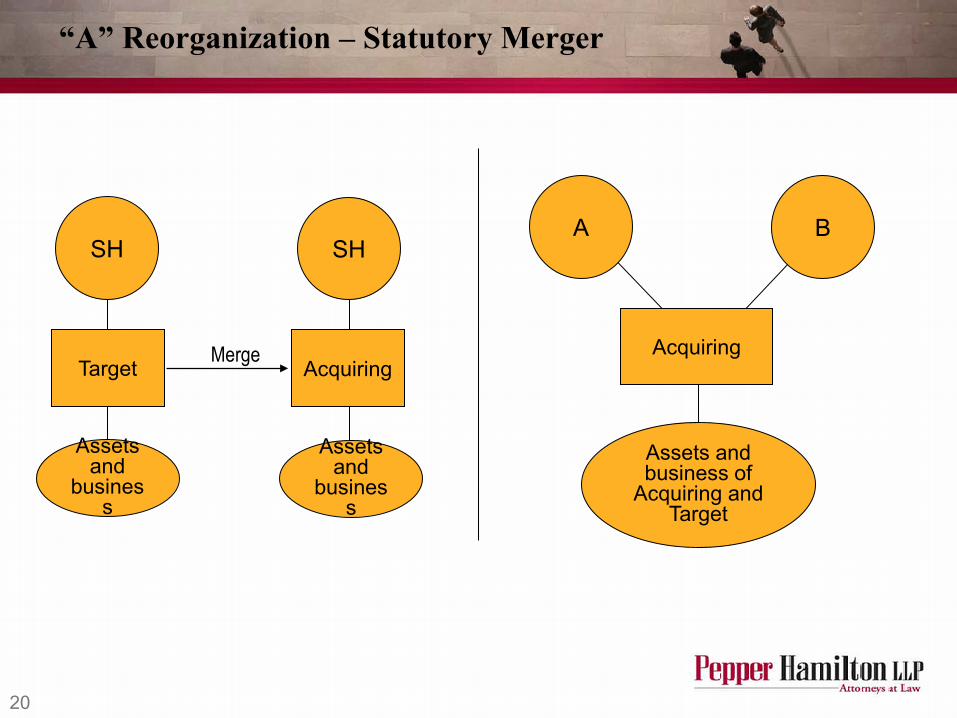

“A” Reorganization – Statutory Merger

Target Merge

Assets and

business

Assets and

business

Acquiring

SH SH A B

Assets and business of

Acquiring and Target

Acquiring

21

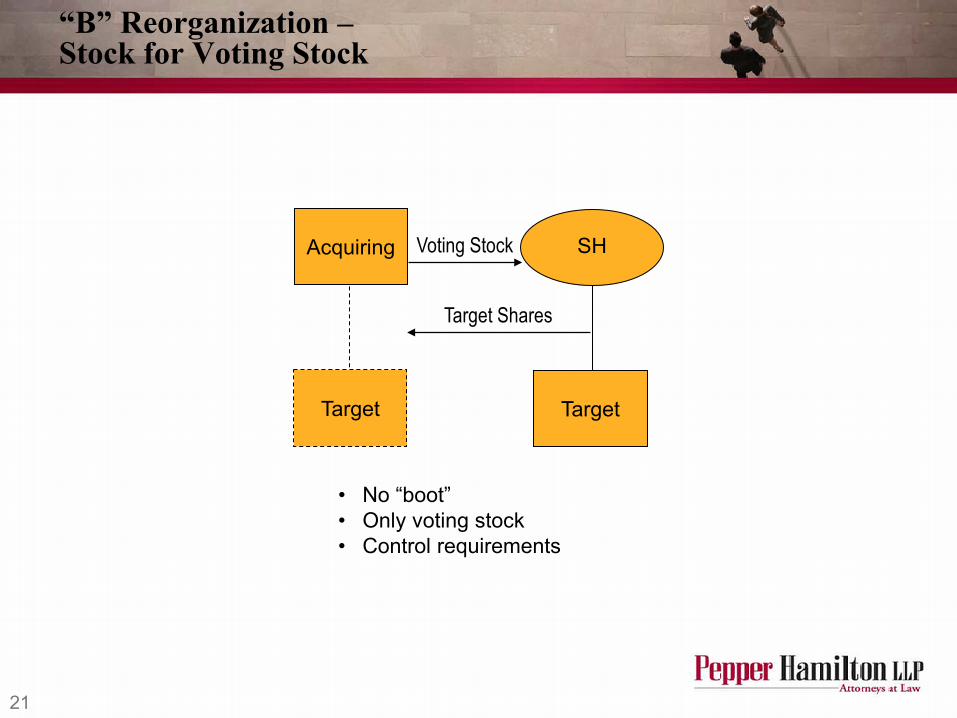

“B” Reorganization – Stock for Voting Stock

Target

Voting Stock SH

Target

Acquiring

Target Shares

• No “boot” • Only voting stock • Control requirements

22

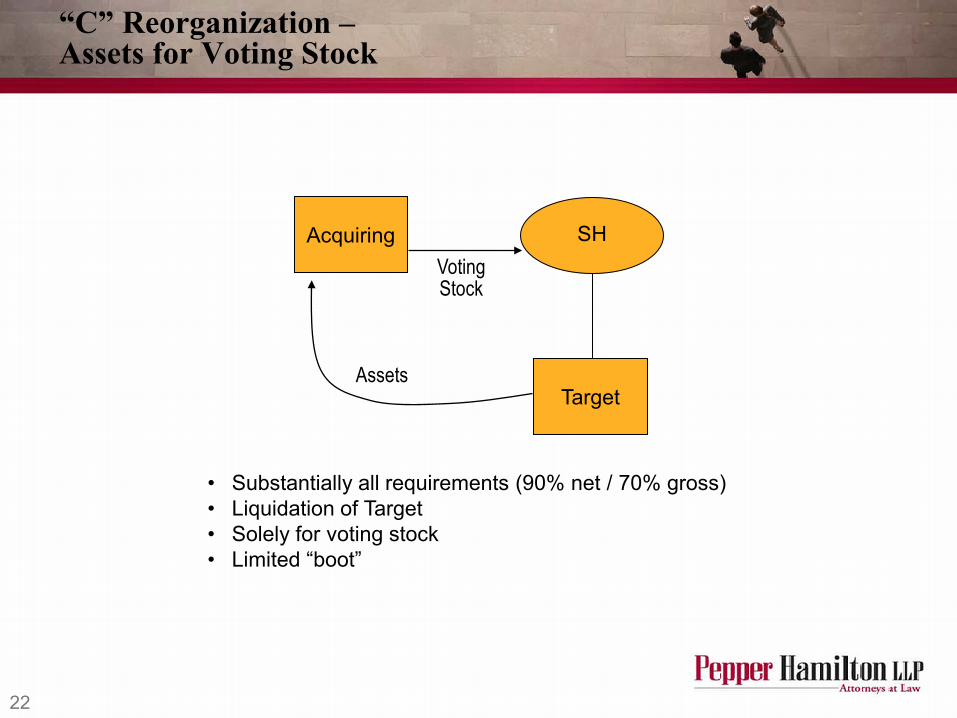

“C” Reorganization – Assets for Voting Stock

Voting Stock

SH

Target

Acquiring

• Substantially all requirements (90% net / 70% gross) • Liquidation of Target • Solely for voting stock • Limited “boot”

Assets

23

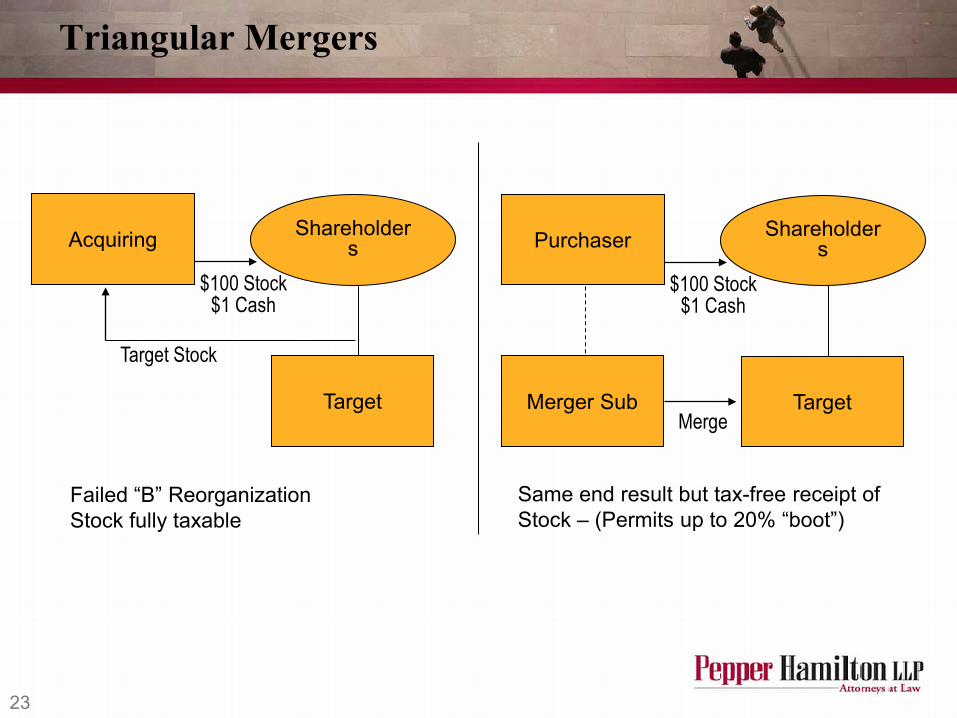

Triangular Mergers

Merger Sub

$100 Stock $1 Cash

Shareholders

Target

Purchaser

Merge

Failed “B” Reorganization Stock fully taxable

$100 Stock $1 Cash

Shareholders

Target

Acquiring

Target Stock

Same end result but tax-free receipt of Stock – (Permits up to 20% “boot”)

24

Foreign Mergers Get Equal Treatment

• 2006 change in regulations allows mergers involving foreign corporations to qualify as ‘A’ reorganizations

• Changes over 70 years of contrary regulatory treatment

• Substantially eases ability to do tax-free cross-border deal

• Must run the 367 obstacle course

25

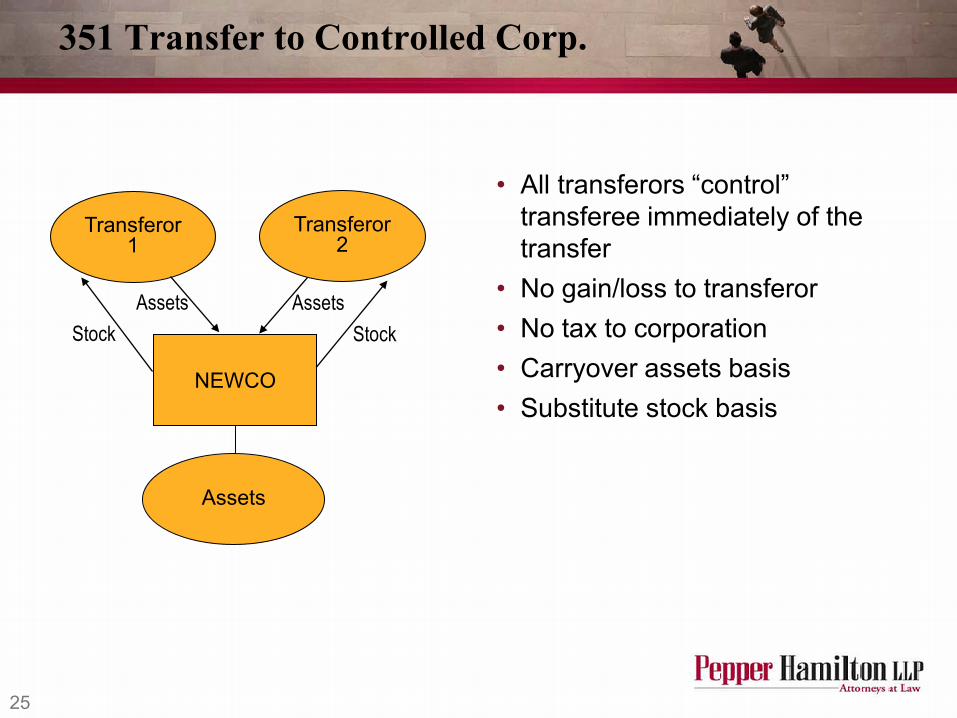

351 Transfer to Controlled Corp.

• All transferors “control” transferee immediately of the transfer

• No gain/loss to transferor • No tax to corporation • Carryover assets basis • Substitute stock basis

Assets

NEWCO

Stock

Transferor 1

Transferor 2

Assets Stock

Assets

26

Partnership Acquisitions

27

Partnership Acquisitions

• Partnerships • Single level of tax (partners) • Capital gain on sale except for

“hot assets” • Flow-through income character • Distributions first tax-free return

on capital • UBTI & ECI flow through • Can transfer assets to

partnership tax free (investments company exception)

• Corporations • Double (or more) tax (corporation

and shareholder) • Capital gain on sale (PFIC and

CFC exceptions • Character determined under

distribution rules • Distributions-dividends to extent

of E&P, then return of basis, then as capital gain

• Blocks UBTI & ECI • Can transfer assets to

corporation tax free and transferors control (investment company exception)

28

Partnership Acquisitions

• Partnerships • Tax free receipt of profits

interests

• Corporations • Receipt of stock for service

taxable

29

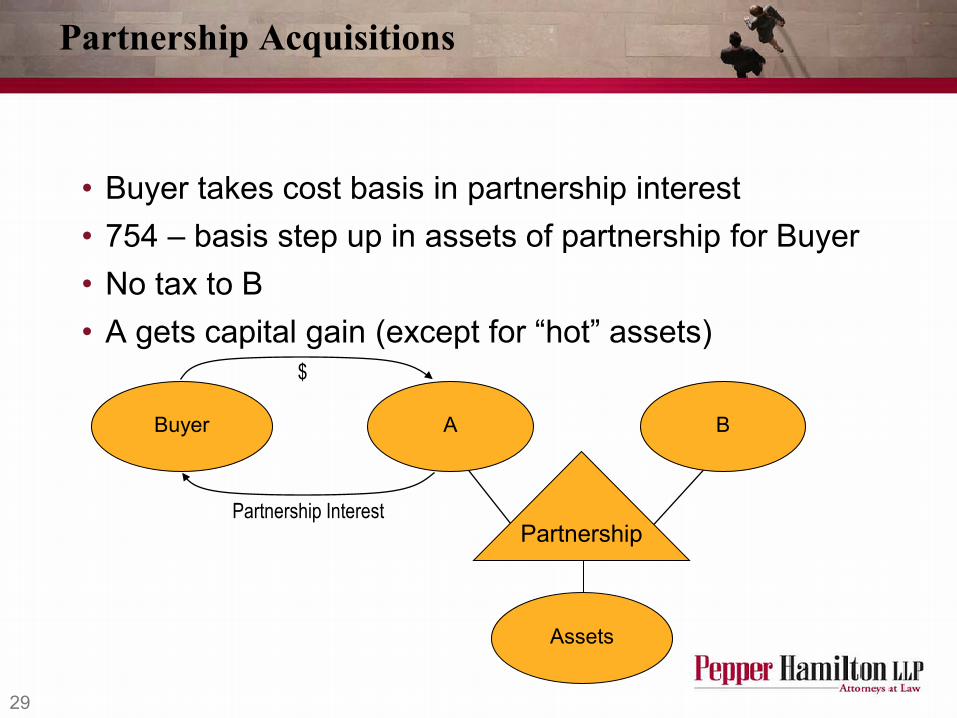

Partnership Acquisitions

• Buyer takes cost basis in partnership interest • 754 – basis step up in assets of partnership for Buyer • No tax to B • A gets capital gain (except for “hot” assets)

Assets

Partnership Interest

A B

Partnership

Buyer

$

30

US Financing Issues

31

Financing

• Debt financing tax issues − PIK Debt − HYDO − Earnings Stripping − Payable in Equity − Withholding Tax Concerns − Other Concerns

32

PIK Debt

• Payable in kind − You can be taxed even if do not get cash − Original Issue Discount or OID − Market Discount Rules

• Is it good debt for tax purposes?

33

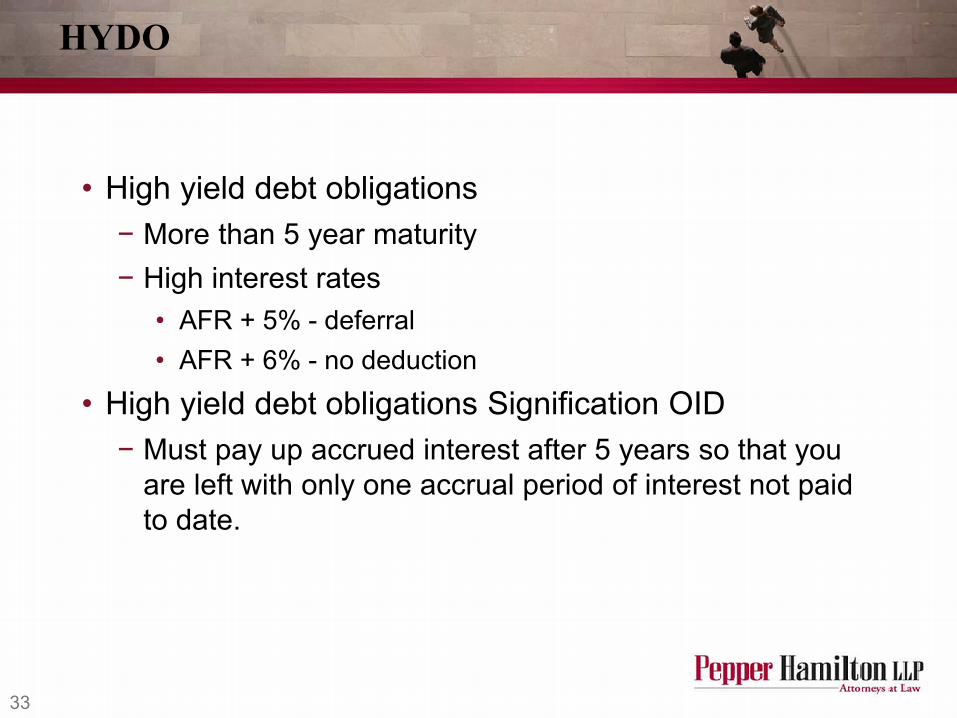

HYDO

• High yield debt obligations − More than 5 year maturity − High interest rates

• AFR + 5% - deferral • AFR + 6% - no deduction

• High yield debt obligations Signification OID − Must pay up accrued interest after 5 years so that you

are left with only one accrual period of interest not paid to date.

34

Earnings Stripping Rules

• No Deduction for Disqualified Interest Expense but only to extent of Excess Interest Expense and Only if Debt-Equity Ratio is greater than 1.5:1

35

Debt Payable in Equity

• If substantial portion of principal or interest may be paid in equity, then no deduction even if pay the interest in cash.

36

Other Concerns

• Section 279-Deduction lost for: • Debt incurred to buy stock or equity if (i)

insubordination, (ii) convertible & (iii) 2:1 or greater debt equity ratio.

37

Steven D. Bortnick

• Partner in Tax Practice Group of Pepper Hamilton LLP • Resident in the Princeton and New York offices • Focuses practice on domestic and international tax and private

equity matters • Handles broad range of cross-disciplinary transactions

including asset, stock, cross-border and domestic acquisitions, tax-free spinoffs, recapitalizations and reorganizations

• Experienced in structuring of domestic and international private equity transactions from tax and venture capital operating company standpoints

• Worked with pooled investment vehicles • Counsels corporate entities on tax issues • Advises U.S. citizens and corporations in overseas investment • Involved in formation of private equity and hedge funds

609.951.4117 212.808.2715 [email protected]

38

BERWYN 400 Berwyn Park 899 Cassatt Road

Berwyn, PA 19312-1183 610.640.7800

FAX 610.640.7835

BOSTON Suite 1010

101 Federal Street Boston, MA 02110-1817

617.956.4350 FAX: 617.956.4351

DETROIT Suite 3600

100 Renaissance Center Detroit, MI 48243-1157

313.259.7110 FAX 313.259.7926

HARRISBURG Suite 200

100 Market Street P.O. Box 1181

Harrisburg, PA 17108-1181 717.255.1155

FAX 717.238.0575

NEW YORK The New York Times Building 37th Floor, 620 Eighth Avenue

New York, NY 10018-1405 212.808.2700

FAX: 212.286.9806

ORANGE COUNTY Suite 1700

5 Park Plaza Irvine, CA 92614-8503

949.567.3500 FAX 949.863.0151

PHILADELPHIA 3000 Two Logan Square

Eighteenth and Arch Streets Philadelphia, PA 19103-2799

215.981.4000 FAX 215.981.4750

PITTSBURGH 50th Floor

500 Grant Street Pittsburgh, PA 15219-2502

412.454.5000 FAX 412.281.0717

PRINCETON Suite 400

301 Carnegie Center Princeton, NJ 08543-5276

609.452.0808 FAX 609.452.1147

WASHINGTON Hamilton Square

600 Fourteenth Street, N.W. Washington, DC 20005-2004

202.220.1200 FAX 202.220.1665

WILMINGTON Hercules Plaza, Suite 5100

1313 Market Street P.O. Box 1709

Wilmington, DE 19899-1709 302.777.6500

FAX 302.421.8390

Pepper Hamilton LLP Offices

39

Pepper has expanded from its Philadelphia origins to 11 locations.

Detroit, MI Pittsburgh, PA

New York, NY

Wilmington, DE

Philadelphia, PA

Berwyn, PA

Harrisburg, PA

Washington, DC

Princeton, NJ

Orange County, CA

Boston, MA

Pepper Locations