Embed Size (px)

Citation preview

Basic Law Department Metrics

Demonstrating the value of the departmentSession 602 | June 5, 2017

Introductions

Juanita Luna Sam Ranganathan Peter EilhauerDirector,

Legal OperationsSr. Director,

Legal OperationsDirector,

Legal Business Solutions

Agenda• The challenge for legal departments today• What is my ultimate goal?• What is my first step?• Where do I take that first step• How do you bring data together?• Examples• Takeaways

At the end of this session, you will….• Have a foundational understanding of the ‘what’ and ‘why’ of data

• Understand basic tools and techniques of data management

• Be able to draw from practical experiences of others to benefit your own metrics

Legal Departments Today…Many factors are contributing to a renewed focus by legal departments on data and reporting.

• Doing more with less

• Running legal like a business

• Understanding and owning new data sources

• Using technology to drive change

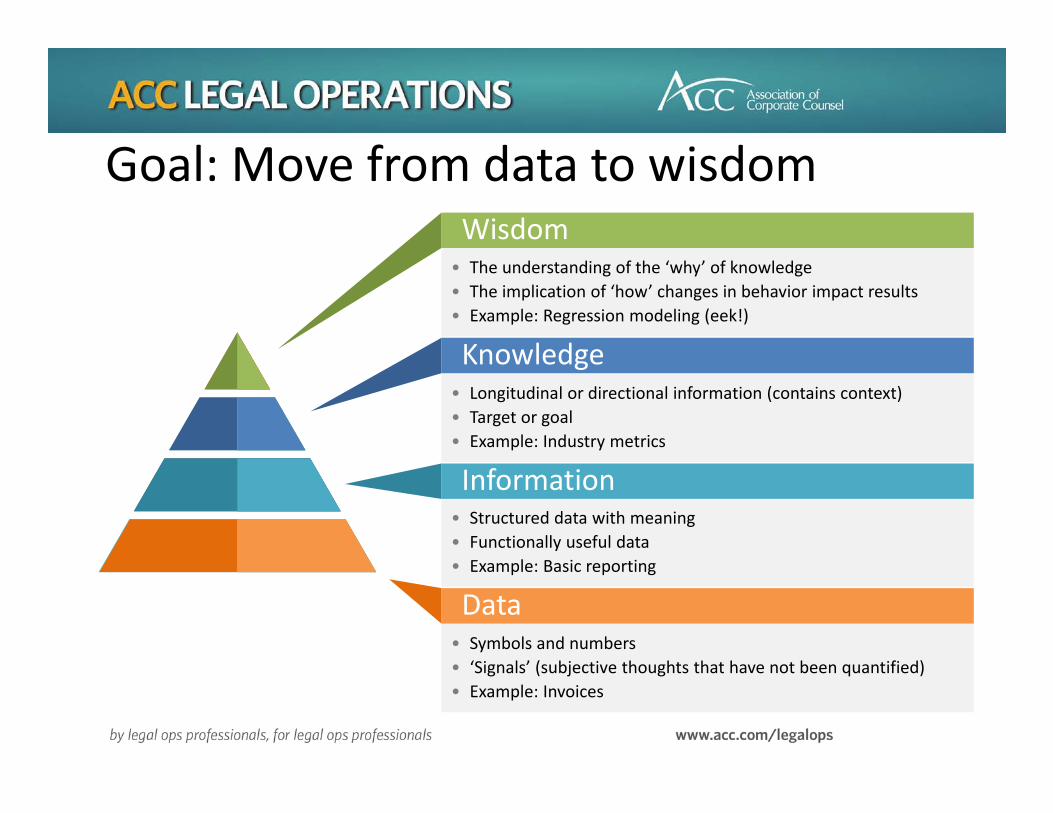

Goal: Move from data to wisdom

• The understanding of the ‘why’ of knowledge• The implication of ‘how’ changes in behavior impact results• Example: Regression modeling (eek!)

Wisdom

• Longitudinal or directional information (contains context)• Target or goal• Example: Industry metrics

Knowledge

• Structured data with meaning• Functionally useful data• Example: Basic reporting

Information

• Symbols and numbers• ‘Signals’ (subjective thoughts that have not been quantified)• Example: Invoices

Data

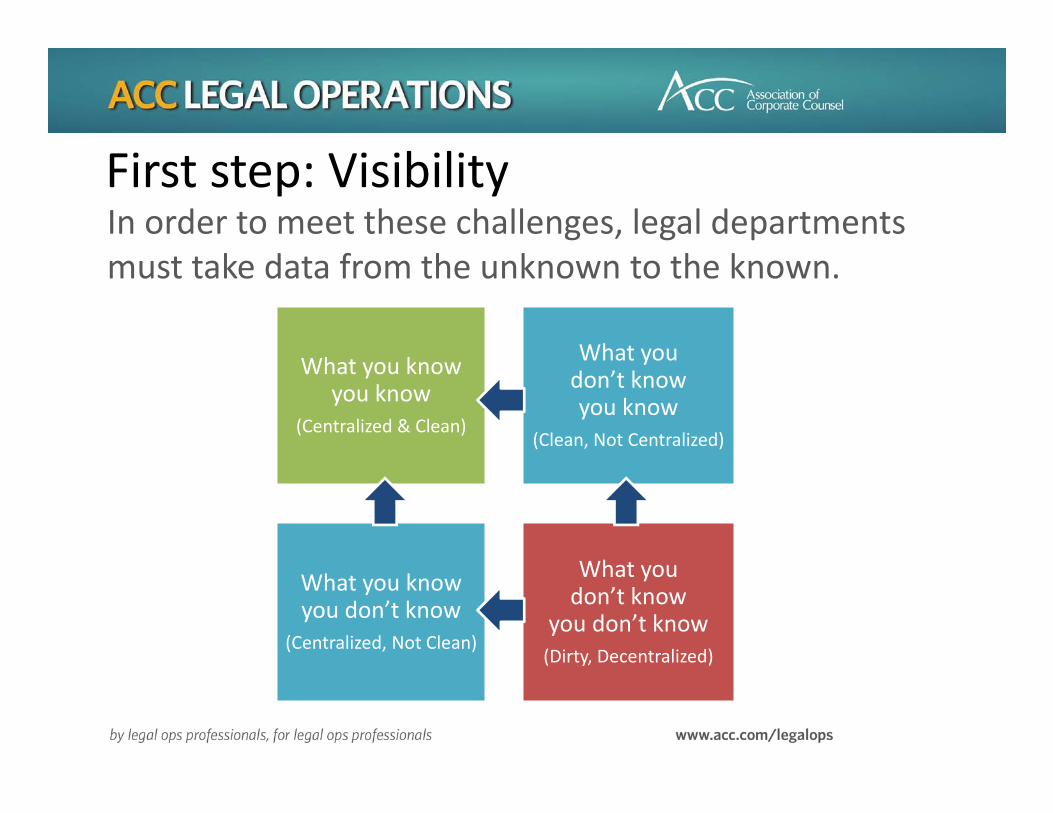

First step: VisibilityIn order to meet these challenges, legal departments must take data from the unknown to the known.

What you knowyou know

(Centralized & Clean)

What you don’t knowyou know

(Clean, Not Centralized)

What you know you don’t know

(Centralized, Not Clean)

What youdon’t know

you don’t know(Dirty, Decentralized)

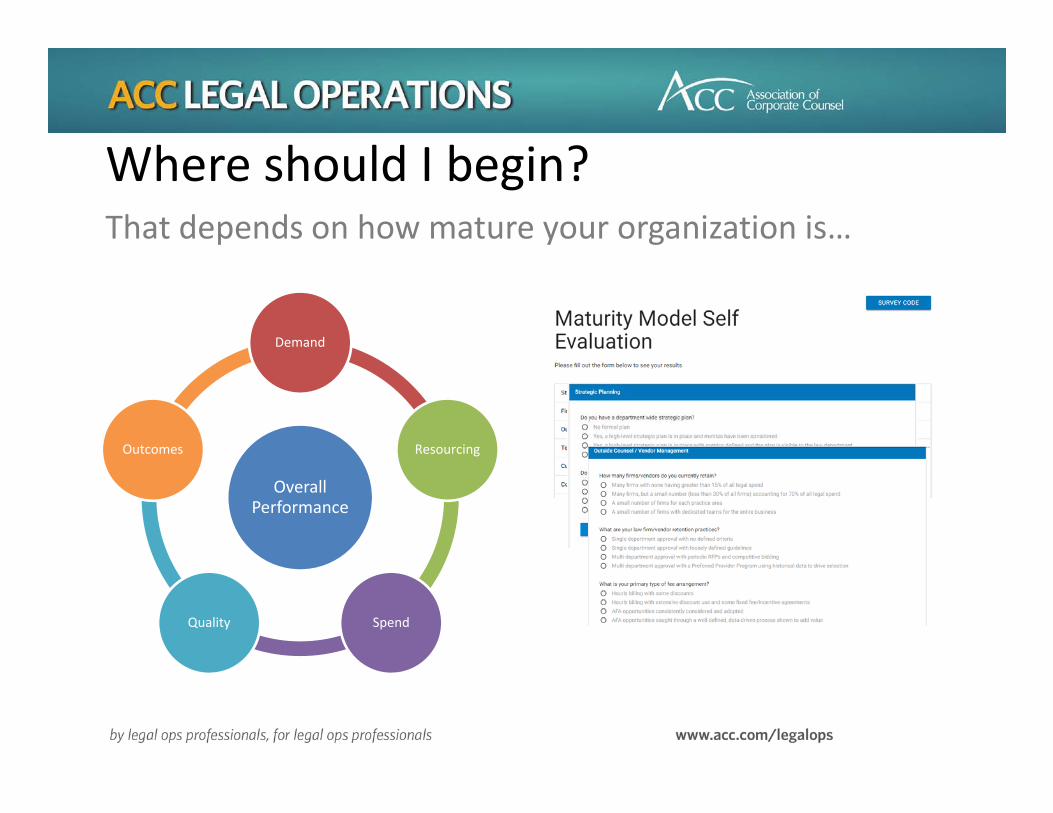

Where should I begin?That depends on how mature your organization is…

Overall Performance

Demand

Resourcing

SpendQuality

Outcomes

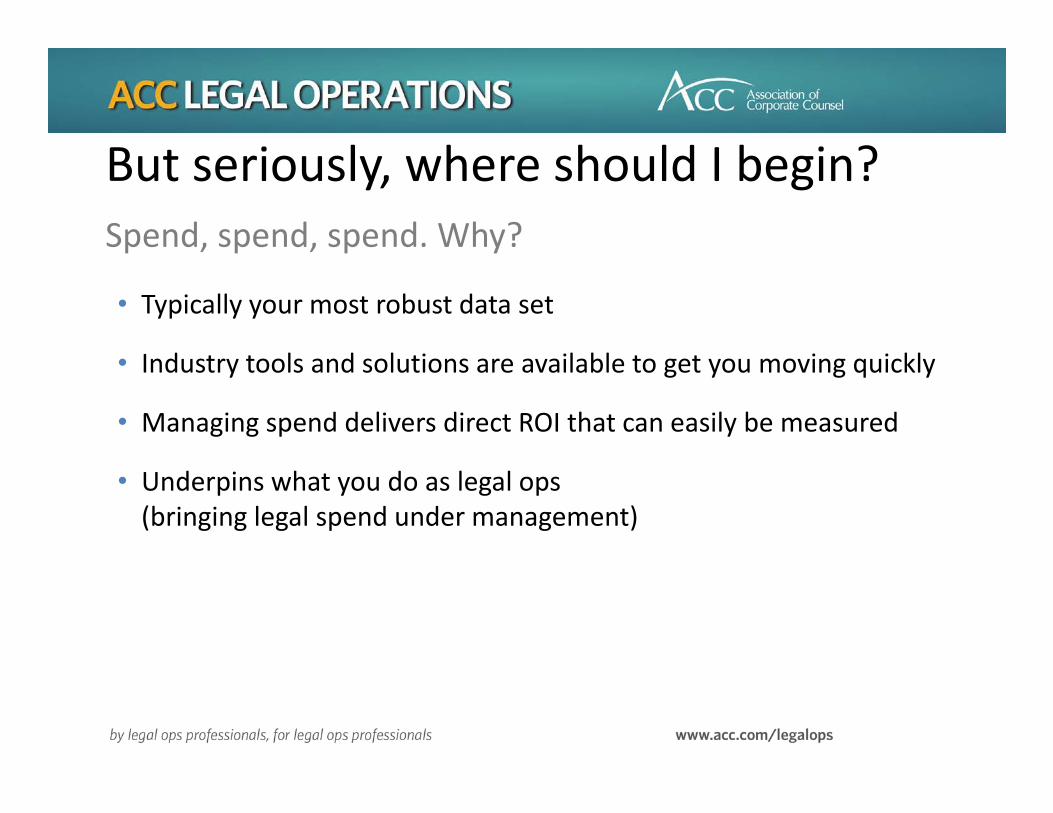

But seriously, where should I begin?Spend, spend, spend. Why?

• Typically your most robust data set

• Industry tools and solutions are available to get you moving quickly

• Managing spend delivers direct ROI that can easily be measured

• Underpins what you do as legal ops (bringing legal spend under management)

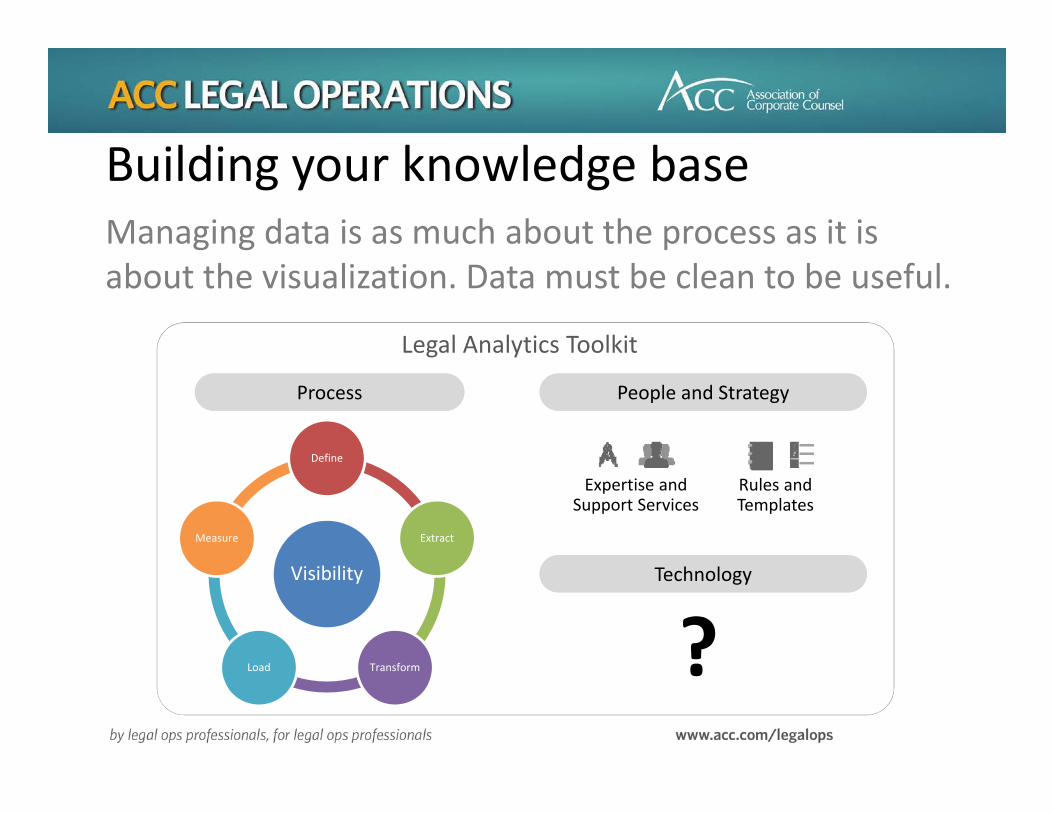

Building your knowledge baseManaging data is as much about the process as it is about the visualization. Data must be clean to be useful.

Legal Analytics Toolkit

Technology

Expertise and Support Services

Rules and Templates

People and Strategy

Visibility

Define

Extract

TransformLoad

Measure

Process

?

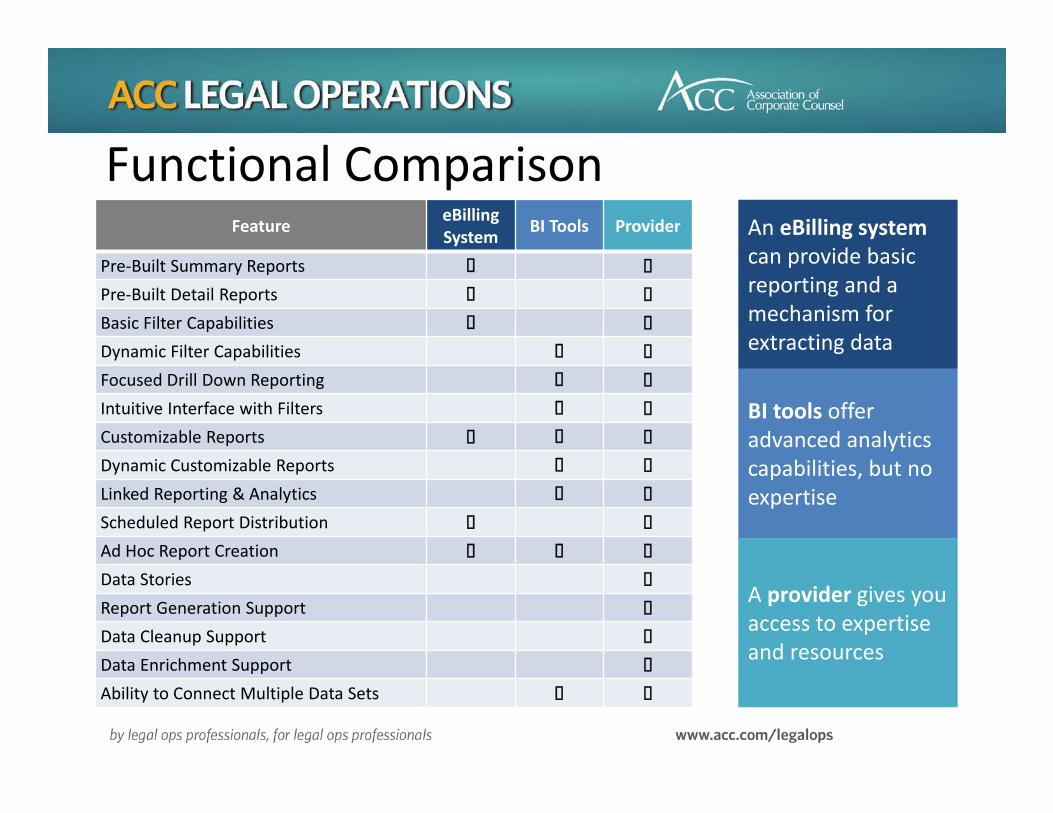

What are my technology options?Making vs. Building vs. Buying Expertise

Basic reporting in Excel Feed eBilling data into a BI Tool

Hire provider to develop your dashboards

by

Functional ComparisonFeature eBilling

System BI Tools Provider

Pre‐Built Summary ReportsPre‐Built Detail ReportsBasic Filter CapabilitiesDynamic Filter CapabilitiesFocused Drill Down ReportingIntuitive Interface with FiltersCustomizable ReportsDynamic Customizable ReportsLinked Reporting & AnalyticsScheduled Report DistributionAd Hoc Report CreationData StoriesReport Generation SupportData Cleanup SupportData Enrichment SupportAbility to Connect Multiple Data Sets

An eBilling system can provide basic reporting and a mechanism for extracting data

BI tools offer advanced analytics capabilities, but no expertise

A provider gives you access to expertise and resources

CASE STUDIES

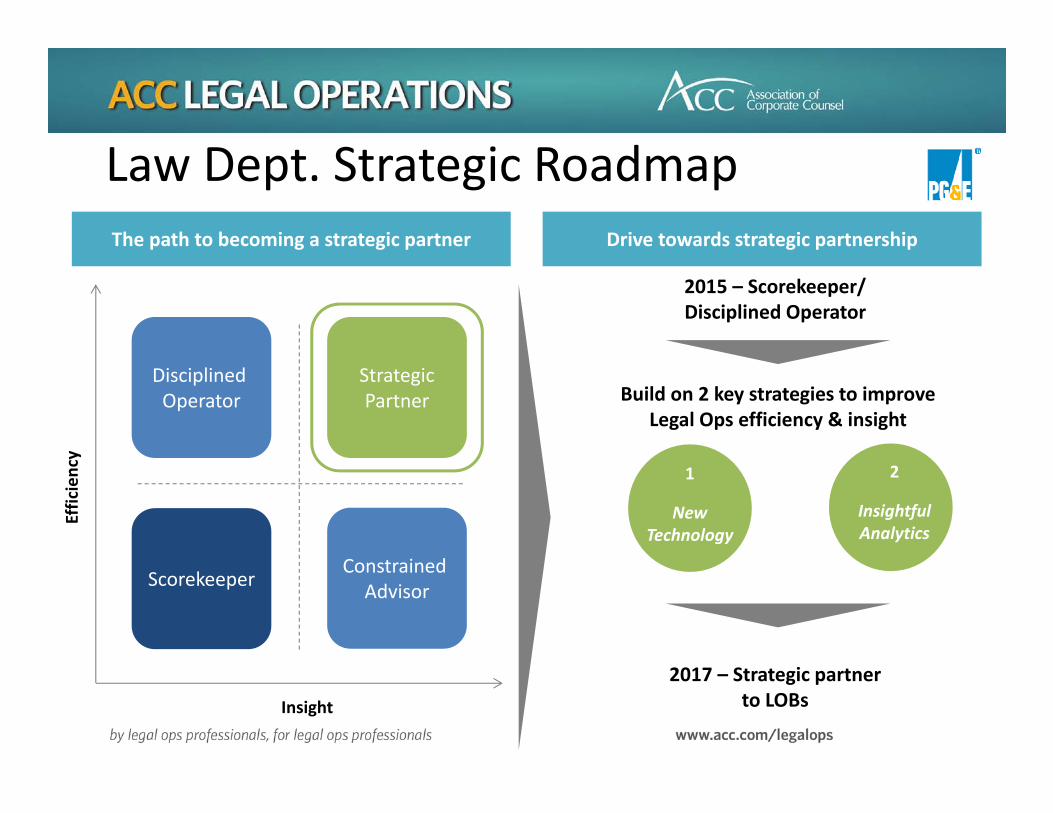

Law Dept. Strategic RoadmapThe path to becoming a strategic partner

Effic

iency

Insight

Disciplined Operator

StrategicPartner

Scorekeeper Constrained Advisor

Drive towards strategic partnership

2015 – Scorekeeper/Disciplined Operator

2017 – Strategic partner to LOBs

Build on 2 key strategies to improve Legal Ops efficiency & insight

2

Insightful Analytics

1

New Technology

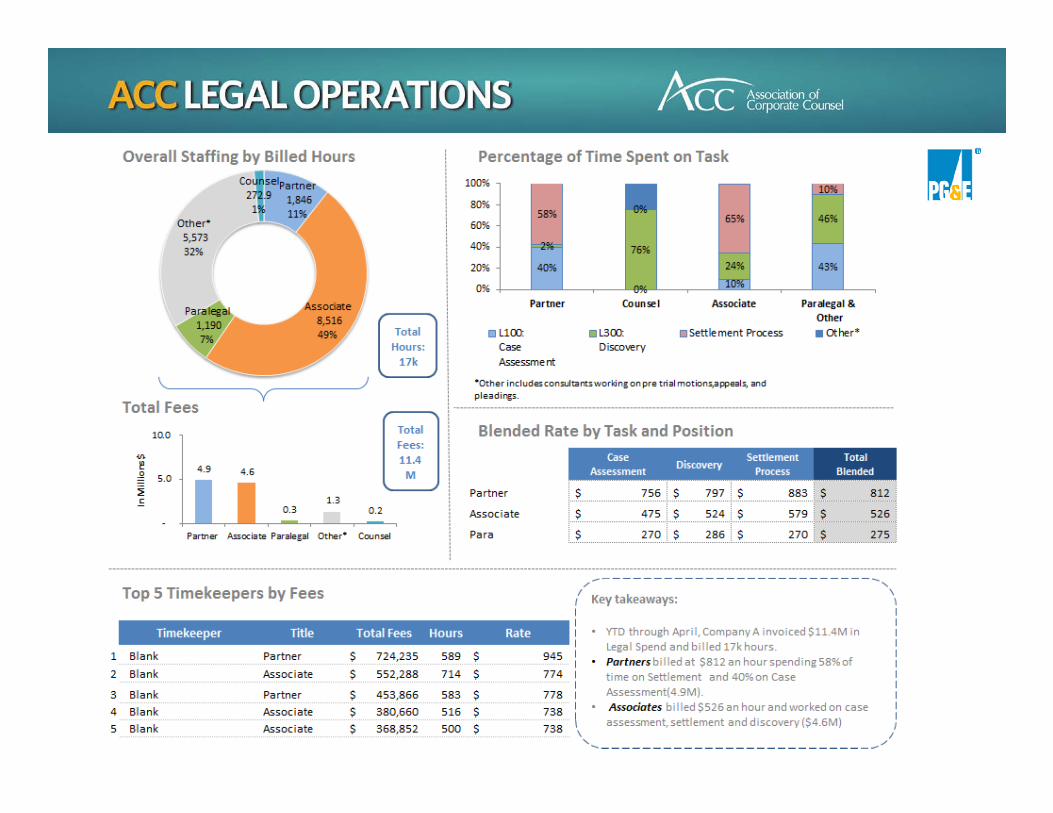

2017 ACC Metrics 16

The

story

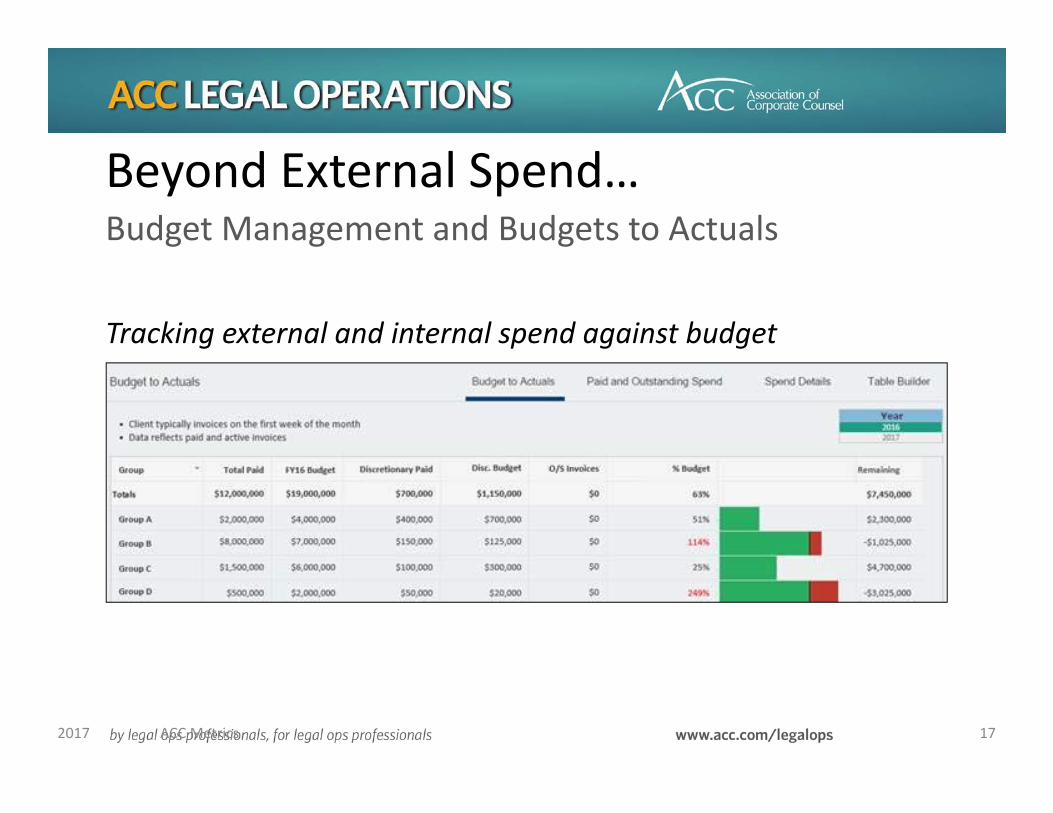

Beyond External Spend…Budget Management and Budgets to Actuals

2017 ACC Metrics 17

Tracking external and internal spend against budget

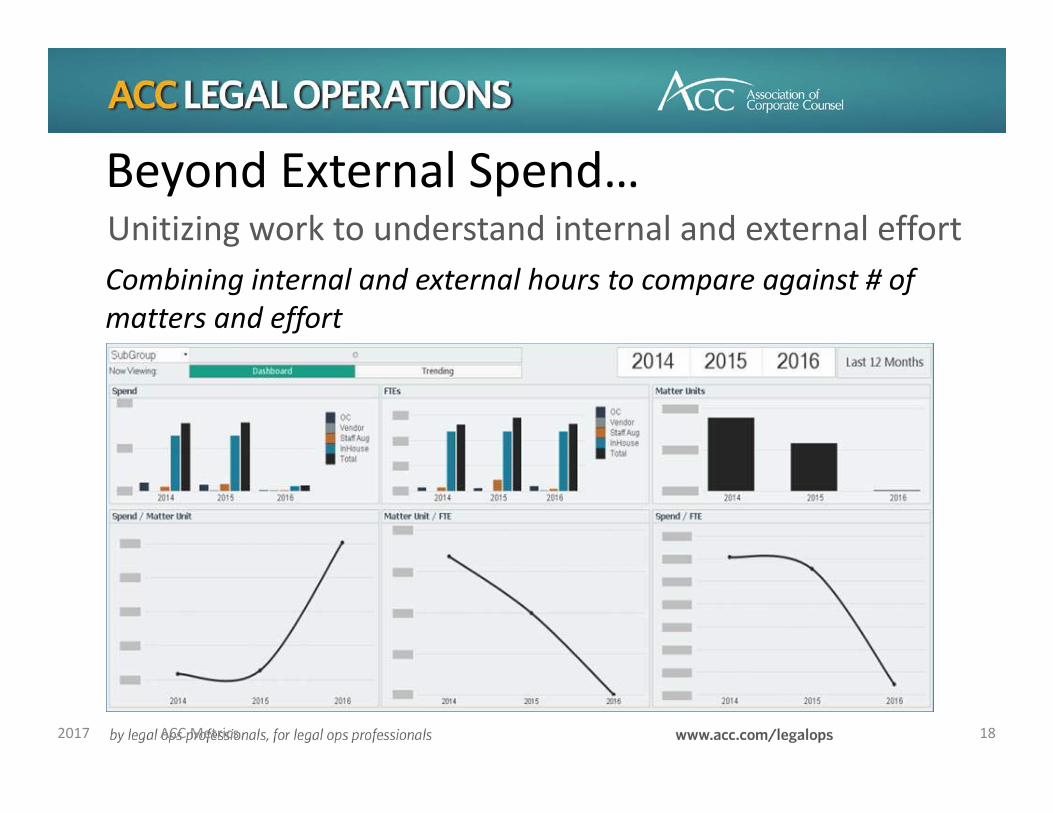

Beyond External Spend…Unitizing work to understand internal and external effort

2017 ACC Metrics 18

Combining internal and external hours to compare against # of matters and effort

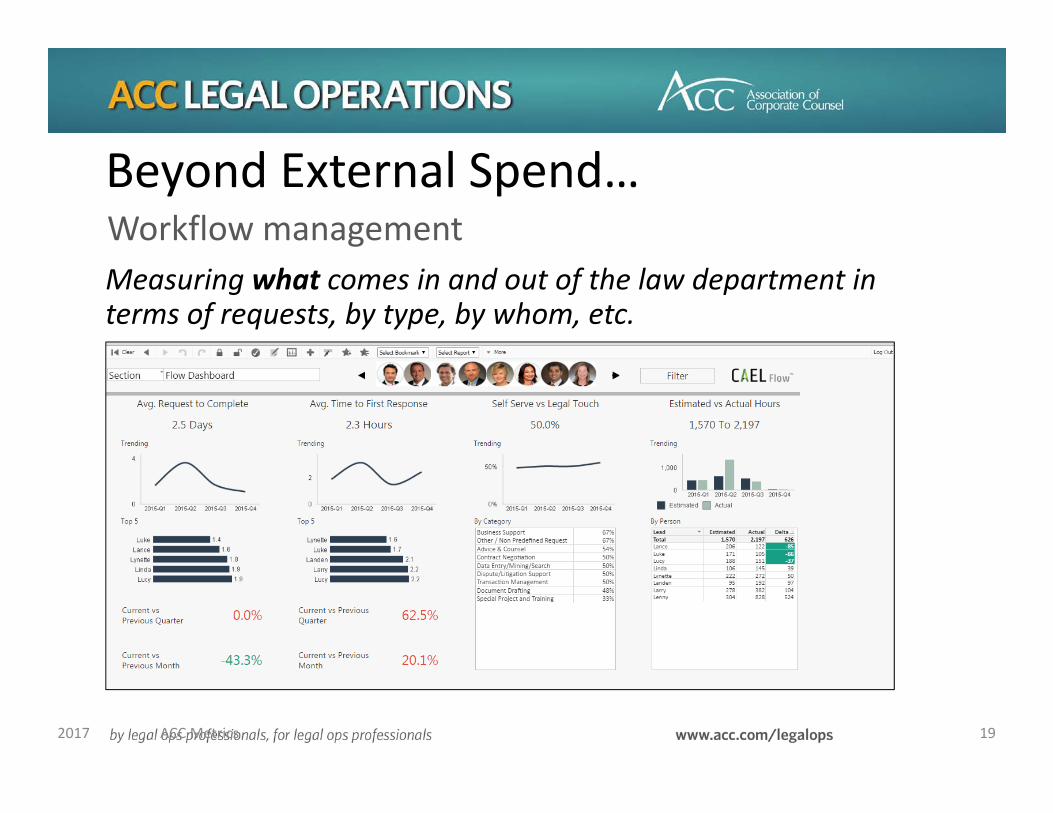

Beyond External Spend…Workflow managementMeasuring what comes in and out of the law department in terms of requests, by type, by whom, etc.

2017 ACC Metrics 19

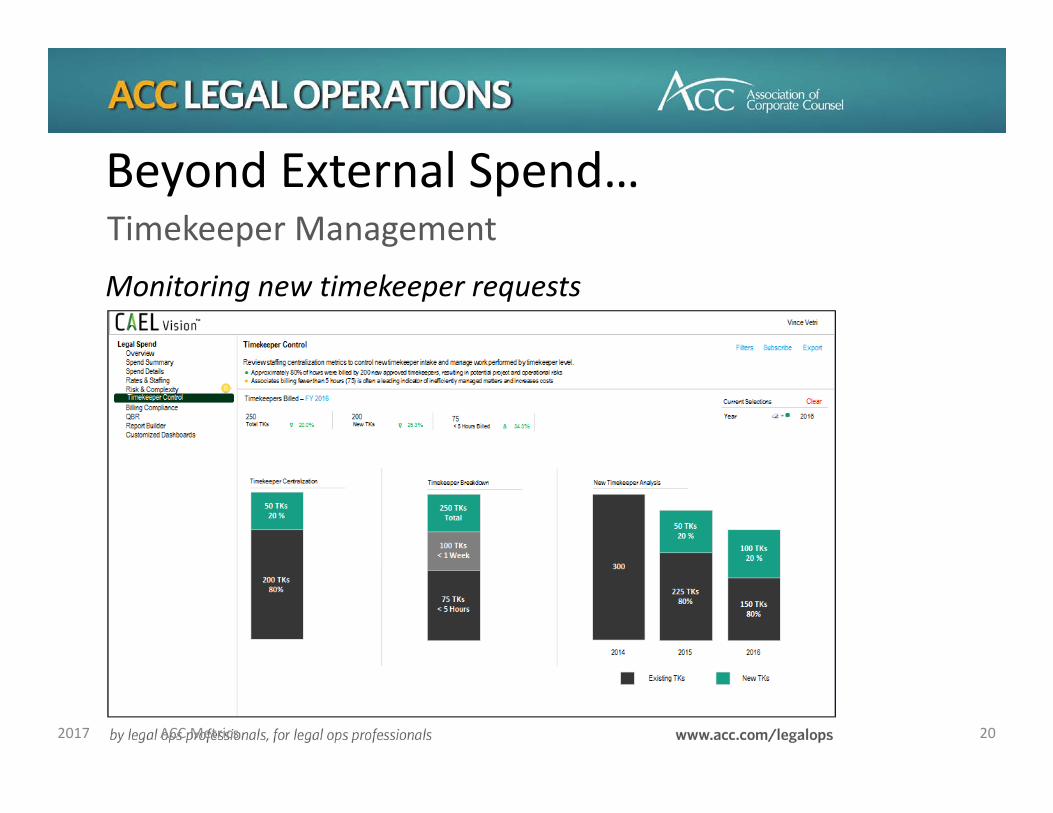

Beyond External Spend…Timekeeper ManagementMonitoring new timekeeper requests

2017 ACC Metrics 20

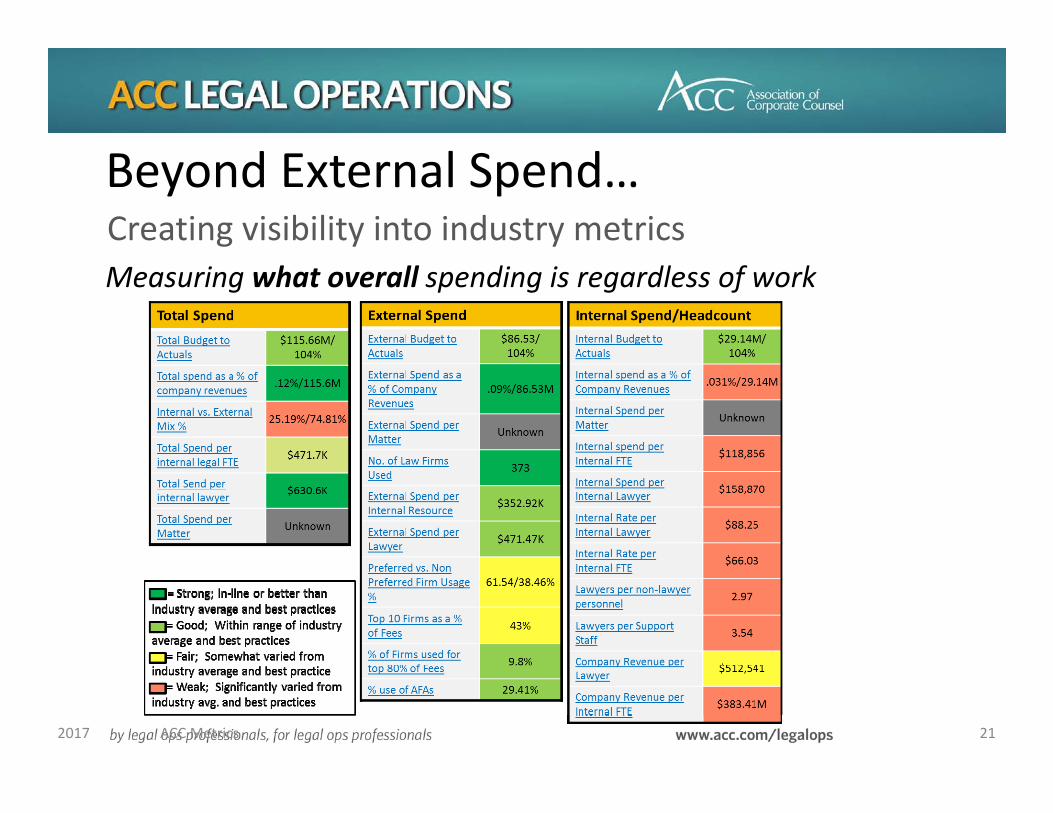

Beyond External Spend…Creating visibility into industry metricsMeasuring what overall spending is regardless of work

2017 ACC Metrics 21

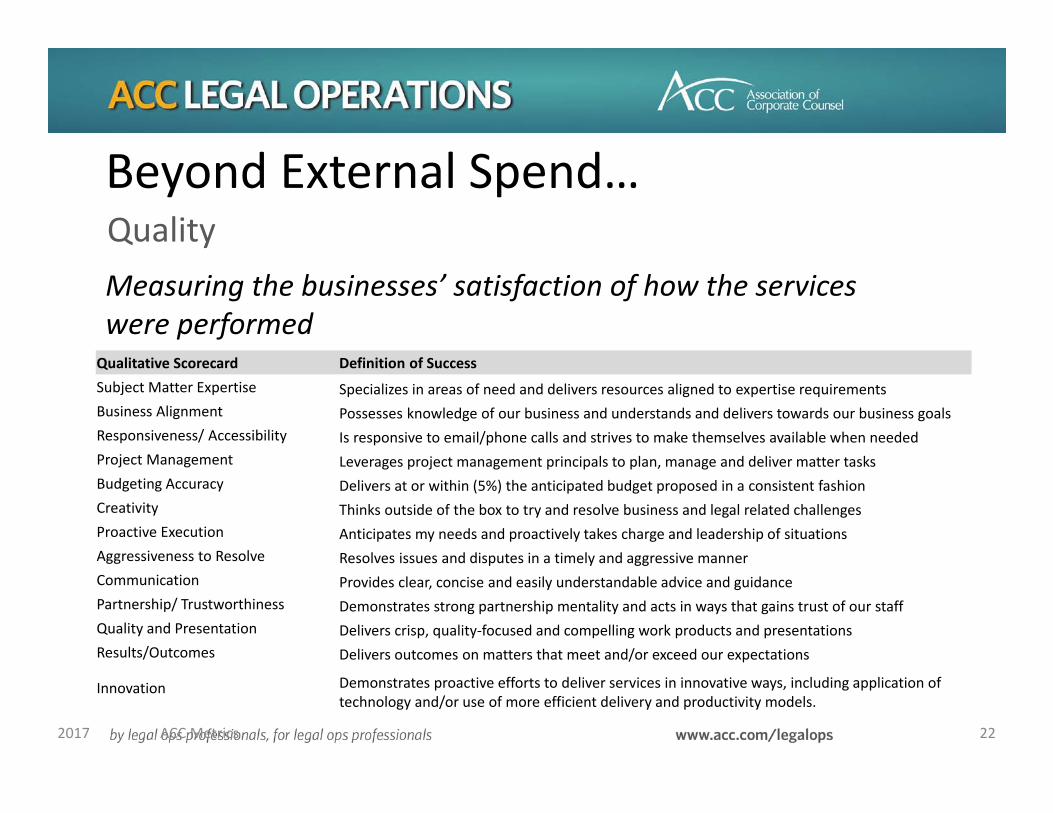

Measuring the businesses’ satisfaction of how the services were performed

QualityBeyond External Spend…

2017 ACC Metrics 22

Qualitative Scorecard Definition of SuccessSubject Matter Expertise Specializes in areas of need and delivers resources aligned to expertise requirementsBusiness Alignment Possesses knowledge of our business and understands and delivers towards our business goalsResponsiveness/ Accessibility Is responsive to email/phone calls and strives to make themselves available when neededProject Management Leverages project management principals to plan, manage and deliver matter tasks Budgeting Accuracy Delivers at or within (5%) the anticipated budget proposed in a consistent fashionCreativity Thinks outside of the box to try and resolve business and legal related challengesProactive Execution Anticipates my needs and proactively takes charge and leadership of situations Aggressiveness to Resolve Resolves issues and disputes in a timely and aggressive mannerCommunication Provides clear, concise and easily understandable advice and guidancePartnership/ Trustworthiness Demonstrates strong partnership mentality and acts in ways that gains trust of our staffQuality and Presentation Delivers crisp, quality‐focused and compelling work products and presentationsResults/Outcomes Delivers outcomes on matters that meet and/or exceed our expectations

Innovation Demonstrates proactive efforts to deliver services in innovative ways, including application of technology and/or use of more efficient delivery and productivity models.

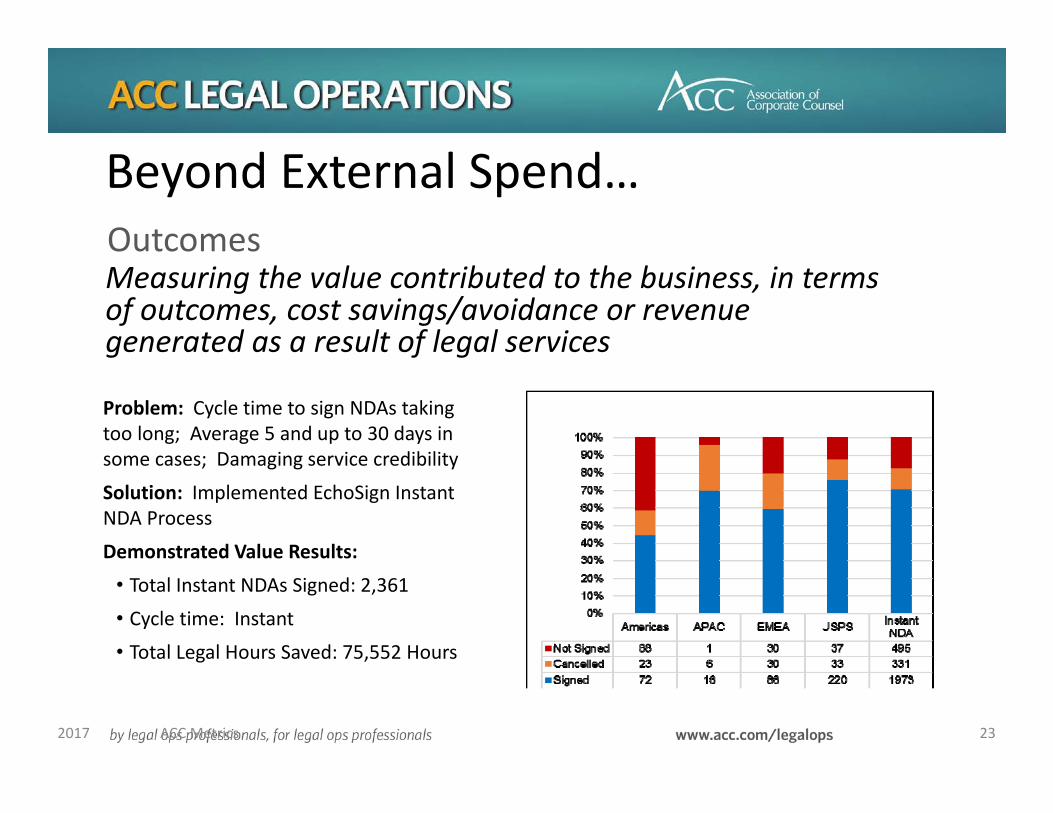

Measuring the value contributed to the business, in terms of outcomes, cost savings/avoidance or revenue generated as a result of legal services

Outcomes

Beyond External Spend…

2017 ACC Metrics 23

Problem: Cycle time to sign NDAs taking too long; Average 5 and up to 30 days in some cases; Damaging service credibility

Solution: Implemented EchoSign Instant NDA Process

Demonstrated Value Results:

• Total Instant NDAs Signed: 2,361• Cycle time: Instant

• Total Legal Hours Saved: 75,552 Hours

TAKEAWAY

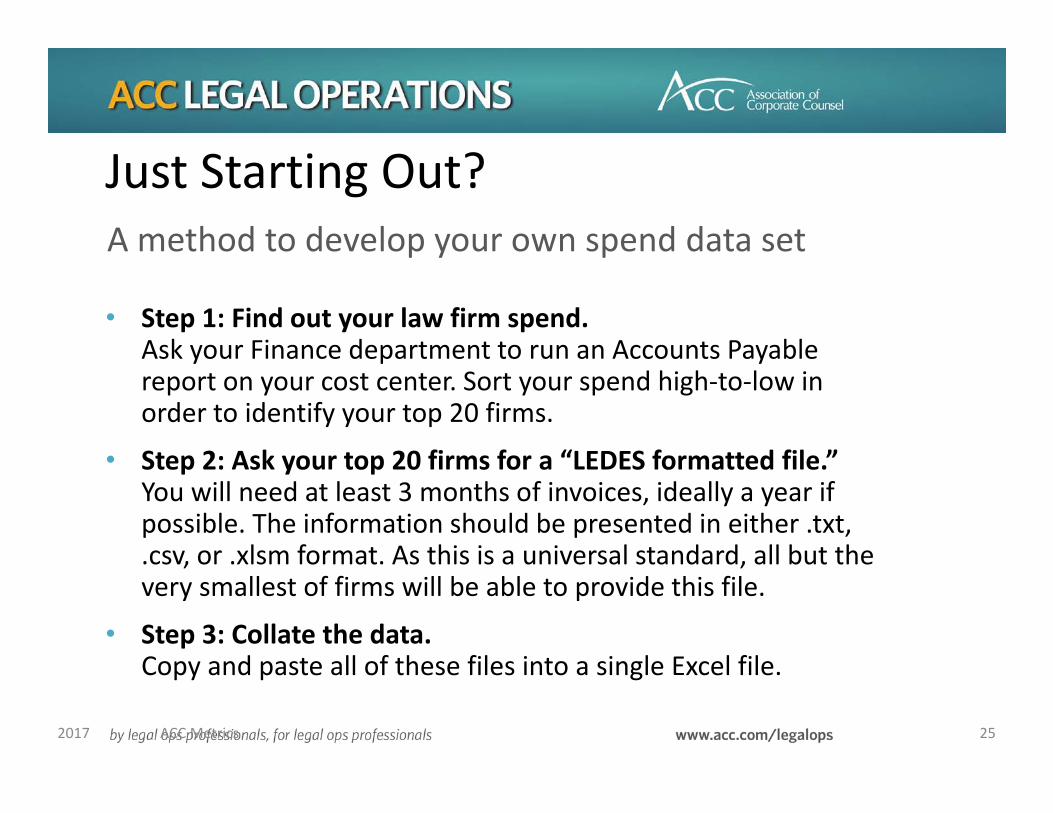

• Step 1: Find out your law firm spend. Ask your Finance department to run an Accounts Payable report on your cost center. Sort your spend high‐to‐low in order to identify your top 20 firms.

• Step 2: Ask your top 20 firms for a “LEDES formatted file.” You will need at least 3 months of invoices, ideally a year if possible. The information should be presented in either .txt, .csv, or .xlsm format. As this is a universal standard, all but the very smallest of firms will be able to provide this file.

• Step 3: Collate the data. Copy and paste all of these files into a single Excel file.

A method to develop your own spend data set

Just Starting Out?

2017 ACC Metrics 25

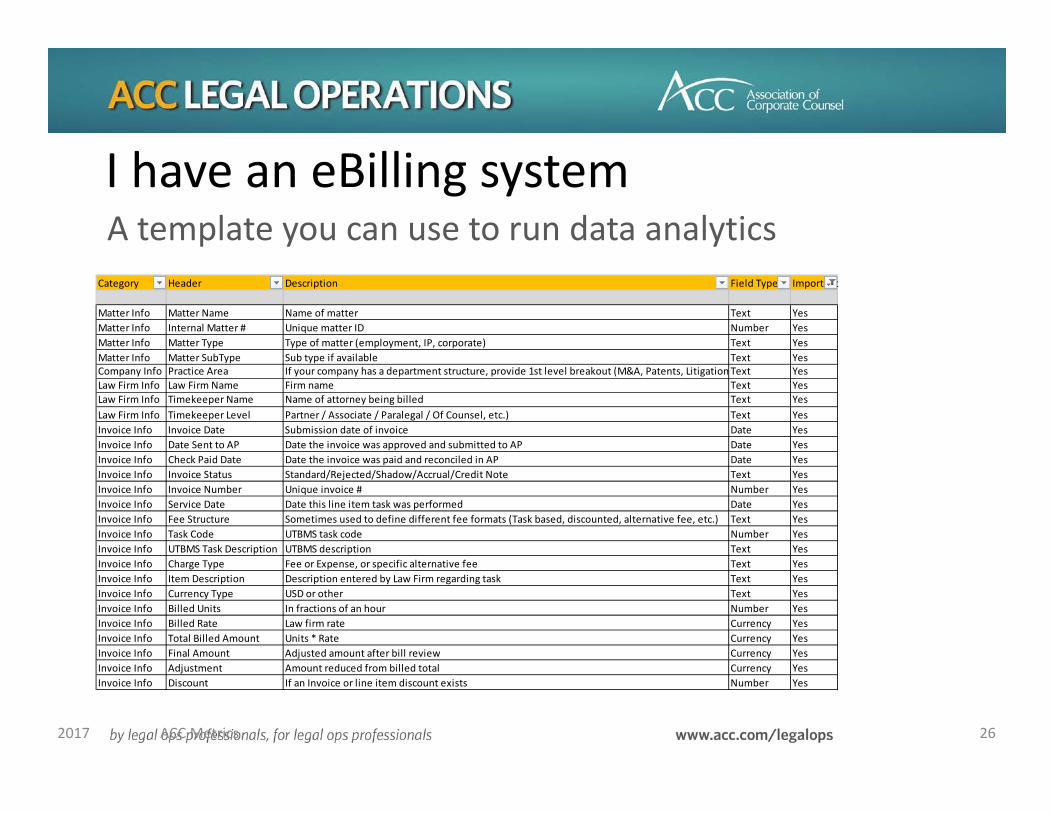

I have an eBilling systemA template you can use to run data analytics

2017 ACC Metrics 26

Category Header Description Field Type Important

Matter Info Matter Name Name of matter Text YesMatter Info Internal Matter # Unique matter ID Number YesMatter Info Matter Type Type of matter (employment, IP, corporate) Text YesMatter Info Matter SubType Sub type if available Text YesCompany Info Practice Area If your company has a department structure, provide 1st level breakout (M&A, Patents, LitigationText YesLaw Firm Info Law Firm Name Firm name Text YesLaw Firm Info Timekeeper Name Name of attorney being billed Text YesLaw Firm Info Timekeeper Level Partner / Associate / Paralegal / Of Counsel, etc.) Text YesInvoice Info Invoice Date Submission date of invoice Date YesInvoice Info Date Sent to AP Date the invoice was approved and submitted to AP Date YesInvoice Info Check Paid Date Date the invoice was paid and reconciled in AP Date YesInvoice Info Invoice Status Standard/Rejected/Shadow/Accrual/Credit Note Text YesInvoice Info Invoice Number Unique invoice # Number YesInvoice Info Service Date Date this line item task was performed Date YesInvoice Info Fee Structure Sometimes used to define different fee formats (Task based, discounted, alternative fee, etc.) Text YesInvoice Info Task Code UTBMS task code Number YesInvoice Info UTBMS Task Description UTBMS description Text YesInvoice Info Charge Type Fee or Expense, or specific alternative fee Text YesInvoice Info Item Description Description entered by Law Firm regarding task Text YesInvoice Info Currency Type USD or other Text YesInvoice Info Billed Units In fractions of an hour Number YesInvoice Info Billed Rate Law firm rate Currency YesInvoice Info Total Billed Amount Units * Rate Currency YesInvoice Info Final Amount Adjusted amount after bill review Currency YesInvoice Info Adjustment Amount reduced from billed total Currency YesInvoice Info Discount If an Invoice or line item discount exists Number Yes

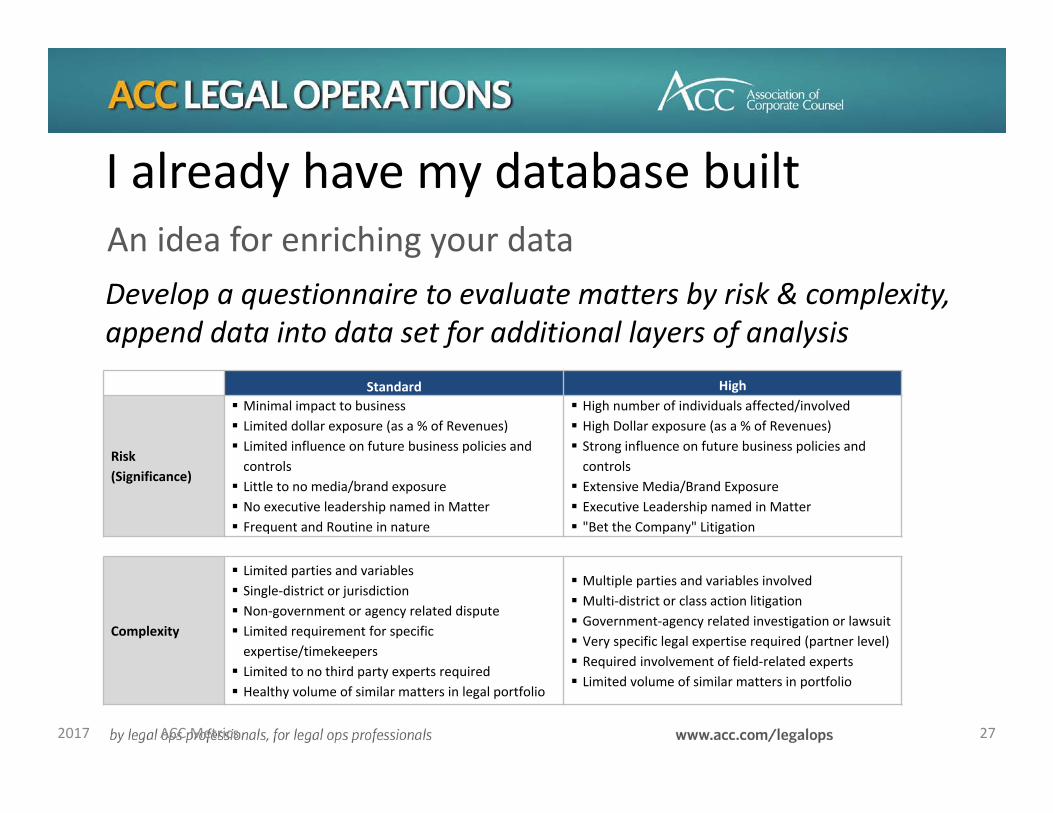

Develop a questionnaire to evaluate matters by risk & complexity, append data into data set for additional layers of analysis

An idea for enriching your data

I already have my database built

2017 ACC Metrics 27

Standard High

Risk (Significance)

Minimal impact to business Limited dollar exposure (as a % of Revenues) Limited influence on future business policies and controls Little to no media/brand exposure No executive leadership named in Matter Frequent and Routine in nature

High number of individuals affected/involved High Dollar exposure (as a % of Revenues) Strong influence on future business policies and controls Extensive Media/Brand Exposure Executive Leadership named in Matter "Bet the Company" Litigation

Complexity

Limited parties and variables Single‐district or jurisdiction Non‐government or agency related dispute Limited requirement for specific expertise/timekeepers Limited to no third party experts required Healthy volume of similar matters in legal portfolio

Multiple parties and variables involved Multi‐district or class action litigation Government‐agency related investigation or lawsuit Very specific legal expertise required (partner level) Required involvement of field‐related experts Limited volume of similar matters in portfolio

Discussion