Embed Size (px)

Citation preview

SERVING COMMUNITY BANKS SINCE 1968

CHICAGO RALEIGH SAN FRANCISCO TAMPA

Private and Confidential

FINAL BASEL III CAPITAL RULES:WHAT DOES IT MEAN TO YOU?

IMPACT ON COMMUNITY BANKS

September 2013

Private and Confidential

Monroe Financial Partners, Inc. - 2 -

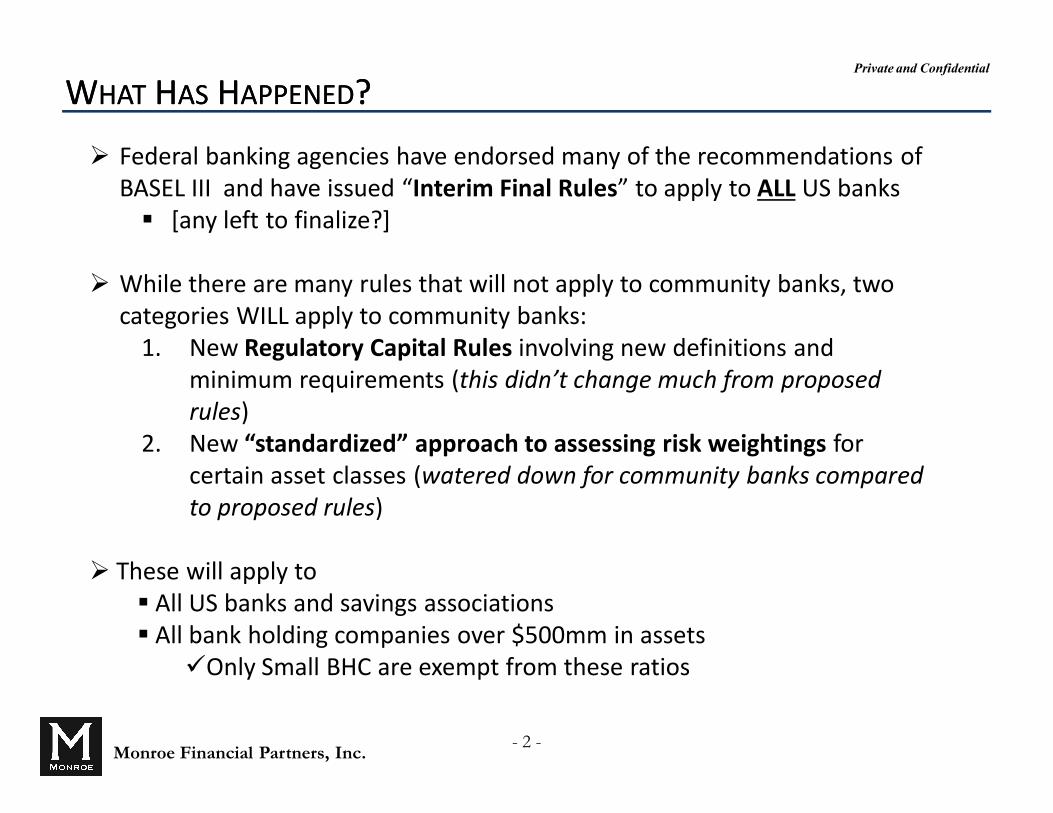

WHAT HAS HAPPENED?WHAT HAS HAPPENED?

Ø Federal banking agencies have endorsed many of the recommendations of BASEL III and have issued “Interim Final Rules” to apply to ALL US banks§ [any left to finalize?]

Ø While there are many rules that will not apply to community banks, two categories WILL apply to community banks:

1. New Regulatory Capital Rules involving new definitions and minimum requirements (this didn’t change much from proposed rules)

2. New “standardized” approach to assessing risk weightings for certain asset classes (watered down for community banks compared to proposed rules)

Ø These will apply to § All US banks and savings associations§ All bank holding companies over $500mm in assetsüOnly Small BHC are exempt from these ratios

Private and Confidential

Monroe Financial Partners, Inc. - 3 -

WHY DO YOU CARE?WHY DO YOU CARE?

Ø These new rules are more complex, require more data from the banks and will be more difficult to administer

Ø Primary observations on what will change:1. Higher overall minimum capital ratios2. Increased common equity requirements, including a new key ratio

(“Common Equity Tier 1 Capital/Total RBC”)3. Higher risk weightings for commercial RE and many securitiesü More complexity around calculations

4. New constraints on dividends, buybacks and executive compensationü Limited by new concept of “capital buffer” above minimal ratiosü Currently includes tax distributions for Sub-S banks [research]

Ø New Effective Date: January 2015

Private and Confidential

Monroe Financial Partners, Inc. - 4 -

WHY DO YOU CARE?WHY DO YOU CARE?

Fundamental Question:What will the long-term impact on the industry be for attracting

the new capital that will be required to fund these new rules?

Old RuleCAPITAL IS KING

New RuleCOMMON

EQUITYIS KING

Private and Confidential

Monroe Financial Partners, Inc. - 5 -

DEFINITION OF CAPITAL: FINAL COMPARISON TO PROPOSALSDEFINITION OF CAPITAL: FINAL COMPARISON TO PROPOSALS

Proposed Rules Interim Final RulesAccumulated Other Comprehensive Income Recognized in Common Equity Tier 1 Capital

Provides Banks (Other than Advanced Approaches Banks) a One-time AOCI Opt-out to Retain Current

AOCI Treatment

Holding Company-issued TruPSTo be Phased Out of Tier 1 Capital

Permits Certain TruPS in Tier 1 Capital per the Dodd-Frank Act [research]

Retained Mortgage Servicing Rights Fair Value Haircut Removes Mortgage Servicing Rights Fair Value Haircut

Certain ESOP Shares Did Not Qualify as Capital Waives Certain Qualifying Criteria for Limited ESOP Shares

Effective Date: January 1, 2013 Effective Date: January 1, 2015(for non-Advanced Approaches Banks)

Private and Confidential

Monroe Financial Partners, Inc. - 6 -

RISK-WEIGHTED ASSETS: FINAL COMPARISON TO PROPOSALSRISK-WEIGHTED ASSETS: FINAL COMPARISON TO PROPOSALS

Proposed Rules1-4 Family Risk Weights to Increase,

Varying from 35% to 200%

No Recognition of PMI

Eliminate 120 Day Safe Harbor Provision for Mortgage Loan Sales

HVCRE Definition Potentially Included Farmland and Community Development Projects

Foreign Government, Bank, & Public Sector Entity Risk Weight Depends on

Country Risk Classification (CRC) Assessment

No Provision for Bank Owned Life Insurance

Interim Final RulesNo Changes to Existing 50% and 100% Risk Weightings

for 1-4 Family Residential Loans (Including Interest Only and Balloons)

Recognition of PMI

Retains Safe Harbor Provision

HVCRE Excludes Farmland and Community Development Projects

If No CRC Assessment, Weighting Depends on Organization for Economic Co-operation & Development

(OECD) Membership

Look-through to Risk Weight of Underlying Assets or Guarantor

Private and Confidential

Monroe Financial Partners, Inc. - 7 -

BASEL III REGULATORY CAPITAL RULES

BASEL III REGULATORY CAPITAL RULES

Private and Confidential

Monroe Financial Partners, Inc. - 8 -

NEW REGULATORY CAPITAL CHANGESNEW REGULATORY CAPITAL CHANGES

The new rules will:

1. Revise the definitions of regulatory capital components and related calculations.

ü Create two types of Tier 1 Capitalü Add a new “Common Equity Tier 1 Risk-Based Capital” ratio.

2. Incorporate the revised regulatory capital requirements into the Prompt Corrective Action (PCA) framework.

3. Implement a new Capital Conservation Buffer that limits certain capital actions, such as paying dividends, repurchasing stock and paying bonuses to employees.

4. Provide a transition period for several aspects of the proposed rules.

RegulatoryCapital

Private and Confidential

Monroe Financial Partners, Inc. - 9 -

Tier 2

Additional Tier 1

Common Equity Tier 1

NEW CAPITAL DEFINITIONS: THREE COMPONENTSNEW CAPITAL DEFINITIONS: THREE COMPONENTSRegulatory

Capital

All capital ratio calculations will use the new capital definitions

Private and Confidential

Monroe Financial Partners, Inc. - 10 -

NEW CAPITAL RATIO: COMMON EQUITY TIER 1 CAPITALNEW CAPITAL RATIO: COMMON EQUITY TIER 1 CAPITALRegulatory

Capital

Common Stock +

Retained Earnings

Accumulated Other

Comprehensive Income

Qualifying Minority Interest

Adjustments & Deductions

Common Equity Tier 1

Accumulated OtherComprehensive Income

Net unrealized gains/losses on available-for-sale securities

§ Current treatment: available-for-sale equity securities losses included in Tier 1 and portion of gains included in Tier 2.

§ New rule treatment: net unrealized gains/losses on available-for-sale debt and equity securities included in Common Equity Tier 1.

The Final Rule permits you to choose to accept the new AOCI treatment:

Private and Confidential

Monroe Financial Partners, Inc. - 11 -

NEW CAPITAL RATIO: COMMON EQUITY TIER 1 CAPITALNEW CAPITAL RATIO: COMMON EQUITY TIER 1 CAPITALRegulatory

Capital

Common Stock +

Retained Earnings

LimitedAOCI Items

Qualifying Minority Interest

Adjustment & Deductions

Common Equity Tier 1

Permanent AOCI Opt-Out Election

§ Opt-Out: same AOCI treatment as today.

§ Election: the March 31, 2015 Call Report and FR Y-9C (if applicable)

Adjustments &

Deductions

§Detailed on next page

The Final Rule also permits you to Opt-Out of including AOCI

New Standards

for Qualification

§Detailed on following pages

Private and Confidential

Monroe Financial Partners, Inc. - 12 -

DEFINITION: ADJUSTMENTS AND DEDUCTIONSDEFINITION: ADJUSTMENTS AND DEDUCTIONSRegulatory

CapitalAdjustments & Deductions to CET1

Deductions§ Goodwill

§ Deferred Tax Assets (Carryforwards)

§ Other Intangibles (except for mortgage servicing assets)

§ Gain on Sale of Securitization Exposure

§ Non-significant (<10%) investments in another financial institution’s capital instruments exceeding a threshold

Adjustments§ Subtract unrealized gains/ add unrealized losses on cash flow hedges

Threshold Deductions

Deduct Amounts > 10%(individually) or > 15% (aggregate)of Common Equity Tier 1 Capital:

§ Mortgage Servicing Assets

§ Deferred Tax Assets related to temporary timing differences

§ Significant (>10%) investments in another unconsolidated financial institution’s common stock

Amounts not deducted are generally subject to 250% Risk Weight

Private and Confidential

Monroe Financial Partners, Inc. - 13 -

DEFINITION: ADJUSTMENTS AND DEDUCTIONSDEFINITION: ADJUSTMENTS AND DEDUCTIONSRegulatory

CapitalInvestments in Unconsolidated FI’s Capital InstrumentsIs your investment in an unconsolidated financial institution’s

capital instruments non-significant or significant?

If the bank owns 10% or less of the other financial institution’s common shares

If the bank owns over 10% of the other financial institution’s common shares

All investments in the financial institution are considered non-significant

All investments in the financial institution are considered significant

Please refer to the interim final rule for additional information on this topic.

Private and Confidential

Monroe Financial Partners, Inc. - 14 -

SIGNIFICANT/NON-SIGNIFICANT INVESTMENT DEDUCTIONSSIGNIFICANT/NON-SIGNIFICANT INVESTMENT DEDUCTIONS

Deduct from the tier of capital the instrument would qualify for:

If your bank’s investment is in an instrument that qualifies as:

Any required deductions would be:

Tier 2 Capital

Additional Tier 1 Capital

Common Equity Tier 1 Capital

Deducted from your Tier 2 Capital

Deducted from your Additional Tier 1 Capital

Deducted from your Common Equity Tier 1 Capital

RegulatoryCapital

Private and Confidential

Monroe Financial Partners, Inc. - 15 -

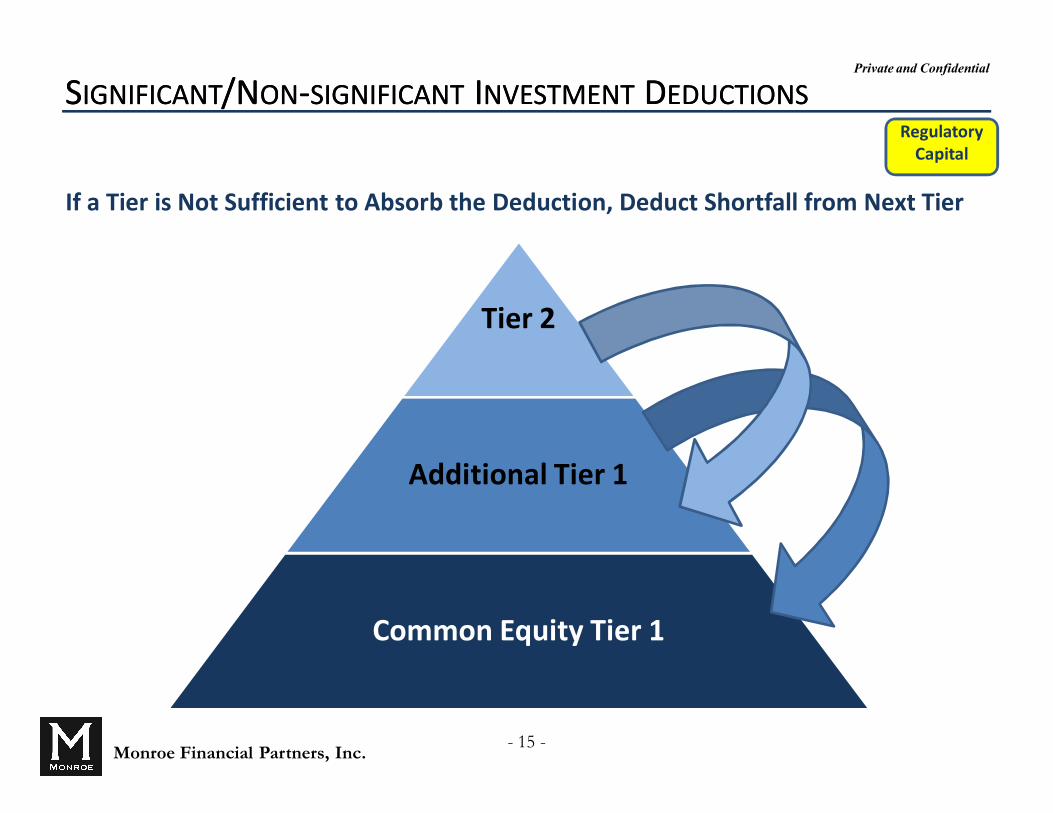

SIGNIFICANT/NON-SIGNIFICANT INVESTMENT DEDUCTIONSSIGNIFICANT/NON-SIGNIFICANT INVESTMENT DEDUCTIONS

If a Tier is Not Sufficient to Absorb the Deduction, Deduct Shortfall from Next Tier

Tier 2

Additional Tier 1

Common Equity Tier 1

RegulatoryCapital

Private and Confidential

Monroe Financial Partners, Inc. - 16 -

QUALIFYING MINORITY INTERESTQUALIFYING MINORITY INTEREST

§ A limited amount of minority interest may qualify for each tier of capital• Refer to the rule for the specific calculation method for the limit that will apply for your bank

§ Common Equity Tier 1 Minority Interest• Subsidiary must be a depository institution

§ Additional Tier 1 and Total Capital Minority Interest• Subsidiary is not required to be a depository institution

§ The capital instruments issued by the subsidiary must meet all criteria for the respective tier of capital

RegulatoryCapital

Private and Confidential

Monroe Financial Partners, Inc. - 17 -

Qualifying Tier 1 Minority Interest

SBLF & TARP* (Bank Issued)

Noncumulative Perpetual Preferred

Stock, including surplus

Certain Investments in Financial Institutions

DEFINITION: ADDITIONAL TIER 1 CAPITAL

Additional Tier 1

Capital

Additional Tier 1

*Only if original bank issuance qualified as Tier 1 Capital.

Less

RegulatoryCapital

Private and Confidential

Monroe Financial Partners, Inc. - 18 -

Tier 2 Preferred Stock &

Subordinated Debt*

Limited Allowance for

Loan and Lease Losses

Qualifying Tier 2 Minority Interest

Tier 2 Capital

DEFINITION: TIER 2 CAPITALDEFINITION: TIER 2 CAPITAL

Eliminated Limits on:§ Subordinated debt§ Limited-life preferred stock§ Amount of Tier 2 Capital included in Total Capital

Less Tier 2 Investments in Financial Institutions

*Includes bank-issued SBLF and TARP instruments that currently qualify as Tier 2 Capital.

RegulatoryCapital

Private and Confidential

Monroe Financial Partners, Inc. - 19 -

COMMON EQUITY TIER 1 RBC RATIOCOMMON EQUITY TIER 1 RBC RATIO

Common Equity Tier 1

Capital

Total Risk-weighted Assets

CommonEquity Tier

1 RBC Ratio

§ Creates a new risk-based capital measure.

§ Purpose: To ensure institutions “hold high-quality regulatory capital that is available to absorb losses.”

RegulatoryCapital

Private and Confidential

Monroe Financial Partners, Inc. - 20 -

REVISED REGULATORY CAPITAL MINIMUM RATIOSREVISED REGULATORY CAPITAL MINIMUM RATIOS

Regulatory Capital Minimum Ratios (%)Current Rule Interim Final Rule

Tier 1 Leverage Capital 3.0/4.0 4.0Common Equity Tier 1 Risk-based Capital

n/a 4.5

Tier 1 Risk-based Capital 4.0 6.0Total Risk-based Capital 8.0 8.0

Effective on January 1, 2015, for all banks

RegulatoryCapital

Private and Confidential

Monroe Financial Partners, Inc. - 21 -

NEW CAPITAL CONSERVATION BUFFER: ABOVE MINIMUMS

Maximum Payout Amount as % of Eligible Retained Income

60%

40%

20%

0%

No Buffer Limit

Size of BufferAbove Minimum

Capital Levels

Greater than 2.5%

> 1.875% to 2.500%

> 1.250% to 1.875%

> 0.625% to 1.250%

< 0.625%

§ Certain payments will be restricted if a bank does not exceed minimal capital requirements: “Capital Conservation Buffer”

ü Dividendsü Share buybacksü Discretionary payments on Tier 1

instrumentsü Discretionary bonus payments to senior

management

§ Eligible Retained Income: Would be defined as the most recent four quarters of net income less any capital distributions and certain discretionary payments.

§ Agencies maintain the supervisory authority to impose further restrictions and/or require capital commensurate with the bank’s risk profile.

RegulatoryCapital

Private and Confidential

Monroe Financial Partners, Inc. - 22 -

RESTRICTIONS WILL APPLY UPON LOWEST MEASUREMENTRESTRICTIONS WILL APPLY UPON LOWEST MEASUREMENT

Common Equity Tier 1 Risk-Based

Ratio

Tier 1 Risk-Based Ratio

Total Risk-Based Ratio

4.5%

6.0%

8.0%

Bank’s Conservation

Buffer=

Lowest of the Three Amounts

Bank’s Capital RatiosLess:

Minimum Capital

RegulatoryCapital

Private and Confidential

Monroe Financial Partners, Inc. - 23 -

CAPITAL CONSERVATION BUFFER: EXAMPLECAPITAL CONSERVATION BUFFER: EXAMPLE

Example Bank Ratios

%

Basel III Minimum

Ratios %

Calculated Buffer

Measure %

Maximum Payout

Amount %

Common Equity Tier 1 Risk-Based Capital Ratio

7.50 4.50 3.00 None

Tier 1 Risk-Based Capital Ratio 8.50 6.00 2.50 60

Total Risk-Based Capital Ratio 9.00 8.00 1.00 20

Conservation Buffer Example

Determination of Buffer and Limit

1. Determine bank risk-based capital ratios.

2. Subtract Basel III minimum ratios.

3. Determine calculated buffer for each ratio.4. Apply the maximum payout limit of eligible retained

income that is consistent with the lowest buffer.

Payout Limit:

20% of LTM Earnings

RegulatoryCapital

Private and Confidential

Monroe Financial Partners, Inc. - 24 -

TIMELINE AND TRANSITION PERIODTIMELINE AND TRANSITION PERIOD

Phase-in Schedule

Capital Ratio 2015 (%) 2016 (%) 2017 (%) 2018 (%) 2019 (%)

Minimum Tier 1 Leverage Capital Ratio 4.0

Minimum Common Equity Tier 1 Risk-based Capital Ratio 4.5

Minimum Tier 1 Risk-based Capital Ratio 6.0

Minimum Total Risk-based Capital Ratio 8.0

Buffer Calculation

Capital Conservation Buffer 0.625 1.25 1.875 2.50

Minimum Common Equity Tier 1 Plus Capital Conservation Buffer 4.5 5.125 5.75 6.375 7.00

Minimum Tier 1 Capital Plus Capital Conservation Buffer 6.0 6.625 7.25 7.875 8.50

Minimum Total Capital Plus Conservation Buffer 8.0 8.625 9.25 9.875 10.50

Deductions/Adjustments

Phase-in of certain deductions and adjustments 40 60 80 100

RegulatoryCapital

Private and Confidential

Monroe Financial Partners, Inc. - 25 -

PROMPT CORRECTIVE ACTION (PCA)PROMPT CORRECTIVE ACTION (PCA)

PCA Categories Tier 1 Leverage (%)

Common Equity Tier 1 RBC (%)

Tier 1 RBC

Total RBCCurrent (%) Interim Final

Rule (%)

Well Capitalized > 5.0 > 6.5 > 6.0 > 8.0 > 10.0

Adequately Capitalized > 4.0 > 4.5 > 4.0 > 6.0 > 8.0

Undercapitalized < 4.0 < 4.5 < 4.0 < 6.0 < 8.0

Significantly Undercapitalized < 3.0 < 3.0 < 3.0 < 4.0 < 6.0

Critically Undercapitalized Tangible Equity/ Total Assets < 2%

§ Revised PCA ratios are effective on January 1, 2015, for all banks

§ Tangible Equity equals the revised Tier 1 Capital plus outstanding non-Tier 1 perpetual preferred stock

RegulatoryCapital

Private and Confidential

Monroe Financial Partners, Inc. - 26 -

“STANDARDIZED APPROACH” TO RISK WEIGHTING ASSETS

“STANDARDIZED APPROACH” TO RISK WEIGHTING ASSETS

Private and Confidential

Monroe Financial Partners, Inc. - 27 -

NEW ASSET RISK WEIGHTING RULESNEW ASSET RISK WEIGHTING RULES

1. Revised Risk-weighting Methodology – On-Balance Sheet Assets:

§ 1-4 Family Residential Real Estate Loans§ “High Volatility” Commercial Real Estate§ Past Due Assets§ Structured Securities§ Equity Holdings

2. Revised Risk-weighting Methodology – Off-Balance Sheet Items.

3. Allows for substitution of a wider range of financial collateral and eligible guarantors for calculating risk-weighted assets.

4. Rules begin January 1, 2015

Standardized Approach on

RiskMain Impact on Community Banks

Private and Confidential

Monroe Financial Partners, Inc. - 28 -

INTERIM FINAL RULE: RISK-WEIGHTED ASSETSINTERIM FINAL RULE: RISK-WEIGHTED ASSETSStandardized Approach on

Risk

What Has Changed From Current RulesOn-balance Sheet

High Volatility Commercial Real Estate Claims on Securities Brokerage Firms

Past-due Asset Exposures Cleared Transactions

Securitizations (Structured Investments) Unsettled Transactions

Equity Exposures Foreign Government Exposures

Equity Exposures to Investment Funds Foreign Bank Exposures

Off-balance Sheet

Certain Credit Conversion Factors Certain Repo-style Transactions

Risk-weighting Substitution

Collateralized Exposures Guaranteed Exposures

Private and Confidential

Monroe Financial Partners, Inc. - 29 -

1-4 FAMILY RISK WEIGHTS: NO CHANGES1-4 FAMILY RISK WEIGHTS: NO CHANGESStandardized Approach on

RiskNo Changes From Current Rules

Banks Should Continue To:§ Use 50% & 100% risk weights

§ Recognize Private Mortgage Insurance (PMI)

§ Combine first & junior liens and treat as a single exposure (with no intervening lien)

No Change for “balloon” and “interest only” mortgages

No Change for loans sold• 120 day safe harbor rule remains

Private and Confidential

Monroe Financial Partners, Inc. - 30 -

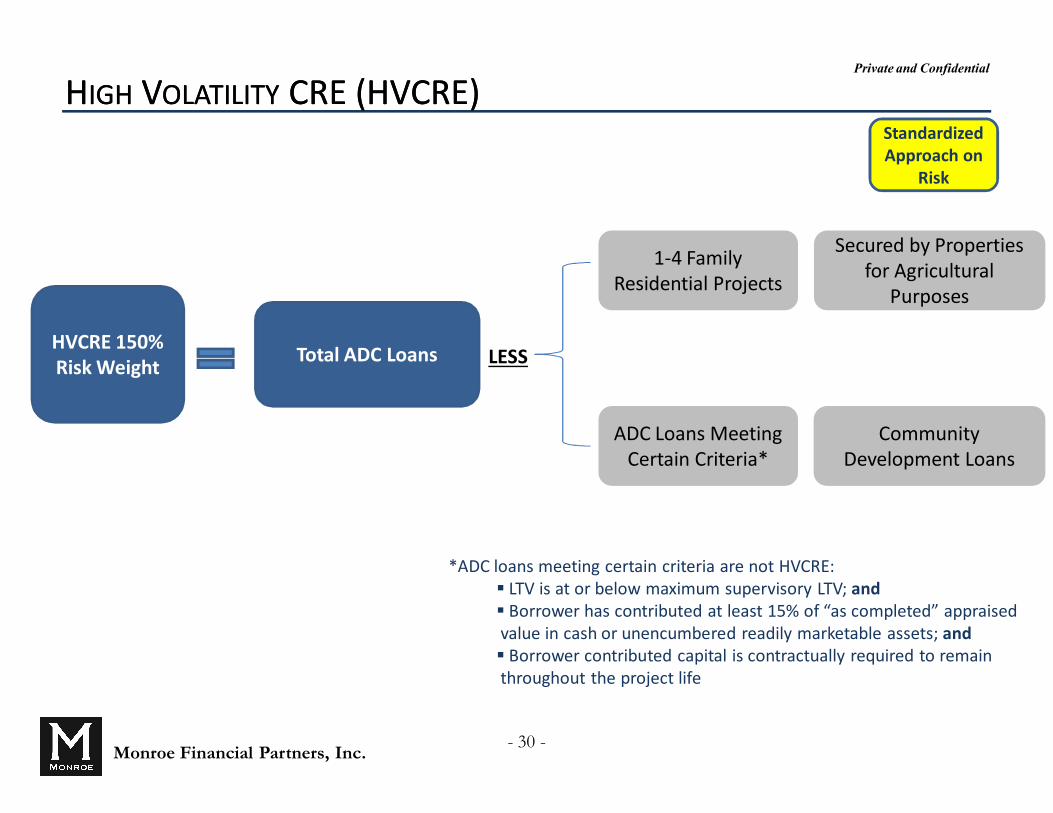

HIGH VOLATILITY CRE (HVCRE)HIGH VOLATILITY CRE (HVCRE)Standardized Approach on

Risk

HVCRE 150% Risk Weight Total ADC Loans LESS

1-4 Family Residential Projects

Secured by Properties for Agricultural

Purposes

ADC Loans Meeting Certain Criteria*

Community Development Loans

*ADC loans meeting certain criteria are not HVCRE:§ LTV is at or below maximum supervisory LTV; and§ Borrower has contributed at least 15% of “as completed” appraised value in cash or unencumbered readily marketable assets; and§ Borrower contributed capital is contractually required to remain throughout the project life

Private and Confidential

Monroe Financial Partners, Inc. - 31 -

IS IT HVCRE?IS IT HVCRE?Standardized Approach on

Risk

Not HVCRE HVCRE1-4 Family ADC project ADC loan on shopping center with LTV above

supervisory maximum

Loan to finance Farmland and valued as such ADC loan to construct office building where borrower has not contributed qualifying capital

Community Development ADC project ADC loan to construct hotel where borrower-contributed capital is not held for life of project

Private and Confidential

Monroe Financial Partners, Inc. - 32 -

APPROACHES FOR RISK-WEIGHTING STRUCTURED SECURITIES & SECURITIZATIONSAPPROACHES FOR RISK-WEIGHTING STRUCTURED SECURITIES & SECURITIZATIONSStandardized Approach on

Risk

Must Choose One… …or Bank May Use 1,250% Risk Weighting

Gross Up Method Simplified Supervisory Formula Approach- the New Option* 1,250% Risk Weight

§ Similar to current rules

§ Capital required for subordinated tranches is based on the amount of the tranche held by the bank plus the pro-rata support provided to senior tranches

§ Key clarification: use weighted average risk weight of underlying collateral

§ Assigns a risk weight based on several criteria:

§Weighted average risk weight of underlying collateral

§ Relative size & seniority of a particular security in structure

§ Delinquency level of underlying collateral

§ A bank may apply a 1,250% risk weight to any of its securitization exposures

*A securitization can not be assigned a risk weight of less than 20%.

Private and Confidential

Monroe Financial Partners, Inc. - 33 -

COLLATERALIZED TRANSACTIONSCOLLATERALIZED TRANSACTIONSStandardized Approach on

Risk§ Collateralized transactions include loans and repurchase agreements

§May substitute the risk weight of an exposure that is secured by financial collateral, consisting of:

§Cash on deposit§ Gold bullion§ U.S. Government securities§ Certain other investment grade securities§ Publicly traded equities & convertible bonds§Money market fund shares (if quoted daily)

§ Available methods for recognizing collateral§ Simple approach (similar to current capital rules)§Collateral haircut approach

Private and Confidential

Monroe Financial Partners, Inc. - 34 -

TREATMENT OF GUARANTEESTREATMENT OF GUARANTEES

A bank may substitute the risk weight of an eligibleguarantor for the risk weight of the exposure

Eligible Guarantors Include

Eligible Guarantees Must

§ Depository institution or holding company

§ Federal Home Loan Banks

§ Farmer Mac

§ Entities with investment grade debt

§ Be written and either:

§ Unconditional§ A contingent obligation of the U.S. Government or its agencies

§ Also meet other requirements of the rule

Standardized Approach on

Risk

Private and Confidential

Monroe Financial Partners, Inc. - 35 -

HIGH VOLATILITY COMMERCIAL REAL ESTATEHIGH VOLATILITY COMMERCIAL REAL ESTATE

Other CRE

Includes HVCRE

High Volatility CRE (HVCRE) Represents a Small Subset of the Industry’s CRE Portfolio

HVCRE means Acquisition, Development, or Construction Financing except:

§ 1-4 family residential properties§Projects in which:

1. The loan-to value ratio <maximum supervisory loan-to-value, and

2. Borrower contributed at least 15% of “as completed” appraised value, and

3. Borrower contributed the capital before the bank advances funds, and the capital is contractually required to remain throughout the project life.

The NPR would assign HVCRE loans a risk weight of 150%.

Standardized Approach on

Risk

Private and Confidential

Monroe Financial Partners, Inc. - 36 -

CRE RISK WEIGHTS - EXAMPLESCRE RISK WEIGHTS - EXAMPLES

100% 150%

Owner-Occupied Office Building

Non Owner-Occupied Office Building

Manufacturing/Industrial Building

Acquisition, Development, and Construction: 1-4 family residential properties

Acquisition, Development, and Construction: non-1-4 family residential properties and LTV is 90%

Risk WeightsCommercial Real Estate

Standardized Approach on

Risk

Private and Confidential

Monroe Financial Partners, Inc. - 37 -

PAST DUE ASSETS RISK WEIGHTSPAST DUE ASSETS RISK WEIGHTS

50% 100% 150%

Revenue Bond

Multifamily Loan

Consumer Loan

Commercial and Industrial

Non-Farm Non-Residential

Agricultural

Assets > 90 days past due or nonaccrual

Risk Weights

Does not apply to:§ 1-4 family residential exposures§ HVCRE (already risk-weighted 150%)§Portion of loan balances with eligible guarantees or collateral (risk weight varies)

Standardized Approach on

Risk

Private and Confidential

Monroe Financial Partners, Inc. - 38 -

STRUCTURED SECURITIESSTRUCTURED SECURITIES

Examples include:Private Label Mortgage-Backed Securities

Trust Preferred Collateralized Debt Obligations (TruPS)Asset-Backed Securities

Three Approaches

§ Risk weight based on one of the following:

1. Weighted average of underlying collateral (Gross UP)

2. 2. Formula based on subordination position and delinquencies (Simplified Supervisory Formula Approach –SSFA)

3. 1,250%

§Eliminates Ratings-Based Approach.

Other Requirements/Options

§Must apply approach selected consistently.§1,250% option may be used regardless of approach selected.§Requirement for comprehensive understanding and due diligence

ü Understand complexity & materialityü Understand performance featuresü Conduct initial and ongoing written analysis

— If not met, 1,250% will apply

Standardized Approach on

Risk

Private and Confidential

Monroe Financial Partners, Inc. - 39 -

EQUITY RISK WEIGHTSEQUITY RISK WEIGHTS

0% 20% 100% 250% 300% 400% 600%

Federal Reserve Bank stock

Federal Home Loan Bank stock

CDFI and community development equity exposures

An investment of common stock in an unconsolidated financial institution (unless already deducted)*

A publicly traded equity exposure*

An equity exposure that is not publicly traded*

An equity exposure to a hedge fund or any investment firm that has greater than immaterial leverage*

Risk WeightsEquity Exposures

* To the extent that the aggregate adjusted carrying value of certain equity exposures do not exceed 10% of the bank’s total capital, a 100% risk weight may be applied.

Standardized Approach on

Risk

Private and Confidential

Monroe Financial Partners, Inc. - 40 -

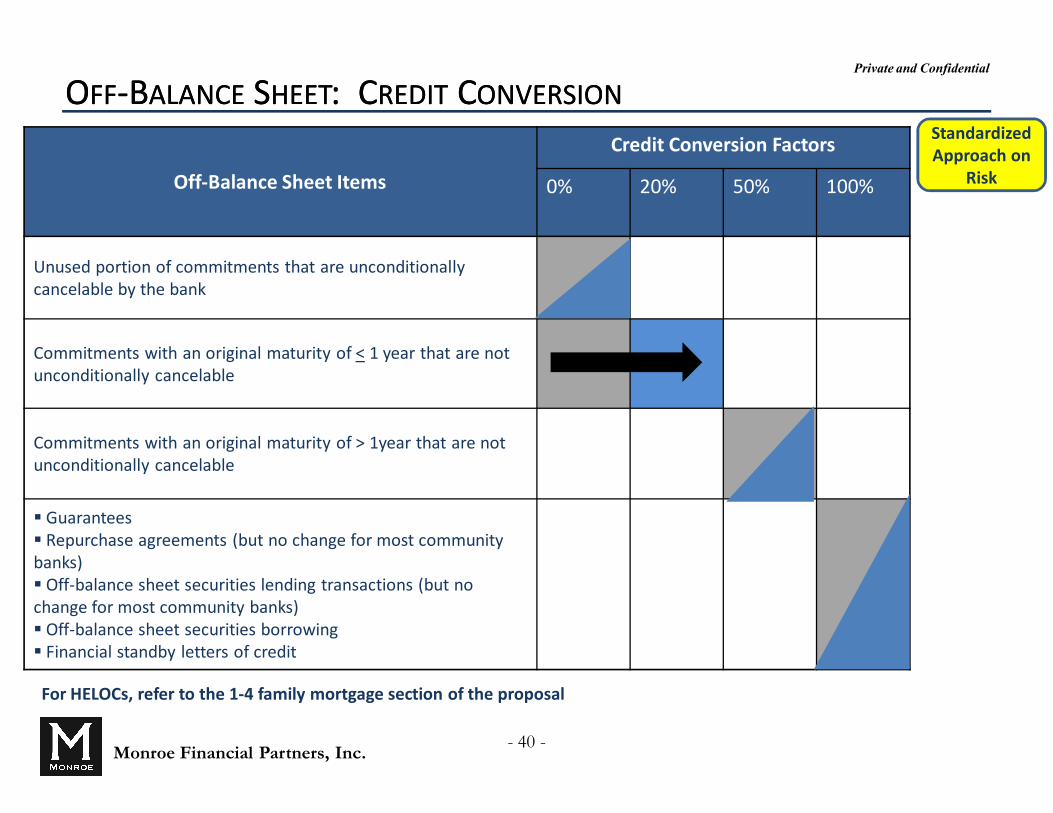

OFF-BALANCE SHEET: CREDIT CONVERSIONOFF-BALANCE SHEET: CREDIT CONVERSION

For HELOCs, refer to the 1-4 family mortgage section of the proposal

Off-Balance Sheet Items

Credit Conversion Factors

0% 20% 50% 100%

Unused portion of commitments that are unconditionally cancelable by the bank

Commitments with an original maturity of < 1 year that are not unconditionally cancelable

Commitments with an original maturity of > 1year that are not unconditionally cancelable

§ Guarantees§ Repurchase agreements (but no change for most community banks)§ Off-balance sheet securities lending transactions (but no change for most community banks)§ Off-balance sheet securities borrowing§ Financial standby letters of credit

Standardized Approach on

Risk

Private and Confidential

Monroe Financial Partners, Inc. - 41 -

OFF-BALANCE SHEET: MORTGAGE BANKINGOFF-BALANCE SHEET: MORTGAGE BANKING

1-4 Family Mortgage Loans Sold§ Credit-Enhancing Representations and Warranties on Assets Sold:

— Early Payment Default—Premium Refund Clause

§ Existing Treatment:— Provides exclusion for early payment default or premium refund clauses that are for a period of 120 days or less.

§ Proposed Treatment:— Eliminates existing 120-day exclusion.—All early payment default and premium refund clauses are treated as off-balance sheet guarantees for the duration of the enhancement.

§ Proposed Risk Weight:— Credit Conversion Factor: 100%— Risk Weight: 35% to 200% based on Category 1 or Category 2 and loan to value.

Standardized Approach on

Risk

Private and Confidential

Monroe Financial Partners, Inc. - 42 -

COLLATERALIZED TRANSACTIONS EXAMPLESCOLLATERALIZED TRANSACTIONS EXAMPLESUnder the proposal, a bank may substitute the

asset’s risk weight with the collateral’s risk weight.

0% 20% 50% 100%Cash on deposit at the bank or third party custodian*US Government Securities (proposed: must discount market value by 20%)*

Government Sponsored Entity securities

Money market funds

"Investment grade" securities (examples):

General Obligation Municipal

Revenue Municipal

Corporate

Risk Weights

Risk Weight Varies

“Investment grade” means that “the entity to which the bank is exposed through a loan or security, or the reference entity with respect to a credit derivative, has adequate capacity to meet financial commitments for the projected life of the asset or exposure.”

*Current risk weight for state nonmember banks. Current risk weight may differ for national and state member banks.

Standardized Approach on

Risk

Private and Confidential

Monroe Financial Partners, Inc. - 43 -

TREATMENT OF GUARANTEESTREATMENT OF GUARANTEES

Under the proposal, a bank may substitute the risk weight of an eligible guarantor for the risk weight of the exposure.

Eligible Guarantors Include:

§ Depository institution or holding company

§Federal Home Loan Banks

§Farmer Mac

§Entity that has “investment grade” debt

Eligible Guarantees Must:

§ Be written and either:— Unconditional, or

—A contingent obligation of the U.S. government or its agencies

§Also meet other requirements

Standardized Approach on

Risk

Private and Confidential

Monroe Financial Partners, Inc. - 44 -

Region SoutheastTotal Assets ($000) $394,806

Loans/ Deposits 82% NPA + 90/Assets 6.80%Total 1-4 Fam. Loans/ Loans 54% Nonaccrual+ 90 PD/ Loans 6.10%Total CRE Loans/Loans (1) 30%

Old Risk Weighted Assets 245,274 247,115 Excess ALLL 1,237 1-4 Family Risk Adj. (2) 38,037 CRE High Volatility Adj. (3) 5,782 Past Due Loans Adj. 4,102 Other Adj. 316 New Risk Weighted Assets 294,115

Difference 48,841 % Difference 19.9%

Old Calculation New Calculation Basel III MinimumLeverage Ratio 6.61% 6.55% 5.00%Common Equity Tier 1 Ratio (5) NA 8.69% 7.00%Tier 1 Capital Ratio 10.51% 8.69% 8.50%Total Capital Ratio 11.77% 9.95% 10.50%

Company Information

Loan Mix and Asset Quality (%)

Risk Weighted Assets Calculation ($000)

Capital Ratios

Region MidwestTotal Assets ($000) $228,536

Loans/ Deposits 80% NPA + 90/Assets 1.23%Total 1-4 Fam. Loans/ Loans 64% Nonaccrual+ 90 PD/ Loans 0.67%Total CRE Loans/Loans (1) 22%

Old Risk Weighted Assets 138,249 138,249 Excess ALLL - 1-4 Family Risk Adj. (2) 29,752 CRE High Volatility Adj. (3) 2,805 Past Due Loans Adj. 376 Other Adj. - New Risk Weighted Assets 171,181

Difference 32,932 % Difference 23.8%

Old Calculation New Calculation Basel III MinimumLeverage Ratio 6.17% 6.17% 5.00%Common Equity Tier 1 Ratio NA 8.18% 7.00%Tier 1 Capital Ratio 10.13% 8.18% 8.50%Total Capital Ratio 11.12% 8.98% 10.50%

Company Information

Loan Mix and Asset Quality (%)

Risk Weighted Assets Calculation ($000)

Capital Ratios

COMMUNITY BANKS WITH HIGH MORTGAGE LOAN EXPOSURECOMMUNITY BANKS WITH HIGH MORTGAGE LOAN EXPOSURE

(1). CRE Loans are defined as other construction and development, farm, multifamily and commercial real estate loans.(2). Assumes 90% of 1-4 family 1st lien loans fall under category 1. LTV breakdowns are based on the avg. LTV breakdowns found in the 10-Ks of publicly traded banks.(3). Assumes 15% of the CRE loans are highly volatile.

Community banks with high mortgage loan exposure may find themselves struggling to meet the new capital requirements under Basel III.

Private and Confidential

Monroe Financial Partners, Inc. - 45 -

Region WestTotal Assets ($000) $137,164

Loans/ Deposits 87% NPA + 90/Assets 6.58%Total 1-4 Fam. Loans/ Loans 7% Nonaccrual+ 90 PD/ Loans 5.71%Total CRE Loans/Loans (1) 80%

Old Risk Weighted Assets 102,497 104,103 Excess ALLL 1,500 1-4 Family Risk Adj. (2) 1,745 CRE High Volatility Adj. (3) 5,788 Past Due Loans Adj. 2,718 Other Adj. - New Risk Weighted Assets 112,854

Difference 10,357 % Difference 10.1%

Old Calculation New Calculation Basel III MinimumLeverage Ratio 7.39% 7.44% 5.00%Common Equity Tier 1 Ratio NA 5.47% 7.00%Tier 1 Capital Ratio 10.00% 9.13% 8.50%Total Capital Ratio 11.27% 10.40% 10.50%

Company Information

Loan Mix and Asset Quality (%)

Risk Weighted Assets Calculation ($000)

Capital Ratios

COMMUNITY BANKS WITH HIGH COMMERCIAL LOAN EXPOSURECOMMUNITY BANKS WITH HIGH COMMERCIAL LOAN EXPOSURE

(1). CRE Loans are defined as other construction and development, farm, multifamily and commercial real estate loans.(2). Assumes 90% of 1-4 family 1st lien loans fall under category 1. LTV breakdowns are based on the avg. LTV breakdowns found in the 10-Ks of publicly traded banks.(3). Assumes 15% of the CRE loans are highly volatile.

Basel III’s new capital requirements will also affect banks with high commercial loan exposure.

Region Mid AtlanticTotal Assets ($000) $340,928

Loans/ Deposits 98% NPA + 90/Assets 0.02%Total 1-4 Fam. Loans/ Loans 34% Nonaccrual+ 90 PD/ Loans 0.00%Total CRE Loans/Loans (1) 56%

Old Risk Weighted Assets 281,667 281,770 Excess ALLL - 1-4 Family Risk Adj. (2) 36,069 CRE High Volatility Adj. (3) 11,962 Past Due Loans Adj. - Other Adj. 1,300 New Risk Weighted Assets 331,101

Difference 49,434 % Difference 17.6%

Old Calculation New Calculation Basel III MinimumLeverage Ratio 8.94% 9.18% 5.00%Common Equity Tier 1 Ratio NA 8.60% 7.00%Tier 1 Capital Ratio 9.85% 8.60% 8.50%Total Capital Ratio 11.08% 9.68% 10.50%

Company Information

Loan Mix and Asset Quality (%)

Risk Weighted Assets Calculation ($000)

Capital Ratios

Private and Confidential

Monroe Financial Partners, Inc. - 46 -

CONCLUSION: QUANTITY & QUALITY OF CAPITALCONCLUSION: QUANTITY & QUALITY OF CAPITAL

Ø The new rules as proposed present a dramatically more conservative posture around capital requirements

§ Higher overall levels of capital required

§ Higher proportion of common equity requiredü Creative Tier 1 instruments are being legislated out of existence

§ Much more restrictive rules around shareholder distributions, buybacks and bonuses, all limited by capital levels

§ More detailed approach and conservative to weighting the risk of assets

Standardized Approach on

Risk