Embed Size (px)

Citation preview

1

Basel II Pillar 2Supervisory Review Process

Simon ToppingHong Kong Monetary Authority

2

Outline of Presentation

• Rationale for Pillar 2• Key principles• Banks’ internal capital adequacy assessment process• Supervisory review process• Requiring capital above minimum levels• Risks covered under Pillar 2• Hong Kong approach to implementation

3

Pillar 2:Pillar 2:Supervisory Review of Supervisory Review of

Capital AdequacyCapital Adequacy

Three pillars

approach

Minimumcapital

requirements

Supervisory review of

capitaladequacy

Marketdiscipline

4

Rationale for Pillar 2Rationale for Pillar 2

• Encourage banks to utilise better risk management techniques• Ensure banks have adequate capital to support all risks• Focus on internal, not regulatory, capital• Accommodate differences between banks

5

Supervisory Review of Supervisory Review of Capital AdequacyCapital Adequacy

Pillar 2 is based on four key principles:

• Banks' Own Assessment of Capital Adequacy • Supervisory Review Process • Capital Above Regulatory Minima• Supervisory Intervention

Foundation = existing supervisory guidance, especially Core Principles for Effective Banking Supervision

6

Banks’ Own Assessment of Risk and Banks’ Own Assessment of Risk and Capital AdequacyCapital Adequacy

Principle 1• Banks should have a process for assessing their overall

capital adequacy in relation to their risk profile and a strategy for maintaining their capital levels.

7

Banks’ Own Assessment of Risk and Banks’ Own Assessment of Risk and Capital AdequacyCapital Adequacy

• The level and sophistication of the capital adequacy assessment process should be tailored to the bank’s activities and the risks involved in these activities

• There is no “best practice” with regard to the design and implementation of such a process (no “one size fits all”)

• However, there are some key features that should be included in every bank’s process

8

Banks’ Own Assessment of Risk and Banks’ Own Assessment of Risk and Capital AdequacyCapital Adequacy

• Board and senior management oversight• Policies and procedures designed to ensure that the bank identifies,

measures, monitors and controls all material risks• A systematic, disciplined process:

– that relates capital to the level of risk– that states capital adequacy goals vis-à-vis risk, considering the

bank’s strategic focus and business plan– of internal controls, reviews, and audit to ensure the integrity of

the overall management process

9

Banks’ Own Assessment of Risk and Banks’ Own Assessment of Risk and Capital AdequacyCapital Adequacy

• Have an assessment process• Which is the firm’s responsibility• Proportionate• Formal, documented and management’s responsibility• Integrated into the management process and decision-making culture• Reviewed regularly• Risk based• Comprehensive• Forward-looking• Fit for purpose• Produce a reasonable outcome

10

Banks’ Own Assessment of Risk and Banks’ Own Assessment of Risk and Capital AdequacyCapital Adequacy

What factors should management consider?• Regulatory ratios and requirements• Peer comparisons• Expectations of counterparties and rating agencies• Business cycle effects• Forward-looking stress tests• Concentrations of credit and other risks• Other qualitative and subjective factors• Formal modelling and risk analysis• Building value for shareholders

11

Supervisory Review ProcessSupervisory Review Process

Principle 2• Supervisors should review and evaluate banks’ internal capital

adequacy assessments and strategies, as well as their ability tomonitor and ensure their compliance with regulatory capital ratios. Supervisors should take appropriate supervisory action if they are not satisfied with the result of this process.

12

Supervisory Review ProcessSupervisory Review Process

Traditional methods for monitoring compliance withminimum regulatory capital ratios:• On-site examinations• Off-site surveillance • Meetings with bank management • Periodic reporting• Review of work of internal and external auditors

13

Supervisory Review ProcessSupervisory Review Process

Renewed focus on supervisors’ evaluation of process to determine:• that target levels of capital chosen are comprehensive and

relevant to the current operating environment;• that these levels are properly monitored and reviewed by senior

management; and• that the composition of capital is appropriate for the nature and

scale of the bank’s business.

14

Capital Above Regulatory Minimum Ratios

Principle 3• Supervisors should expect banks to operate above the

minimum regulatory capital ratios and should have the ability to require banks to hold capital in excess of the minimum.

15

Capital Above Regulatory Minimum Ratios

• Pillar 1 requirements include a buffer for uncertainties that affect the banking population as a whole

• All banks are expected to operate ABOVE the minimum requirement (i.e. not just at 8%!)

• Supervisors will need to consider whether the particular features of their banks/markets are adequately covered

16

Capital Capital Above Regulatory Regulatory Minimum RatiosMinimum Ratios

Means to ensure banks are operating with adequate capital levels:• Reliance on a bank’s internal capital assessment• Establishment of “trigger” and “target” ratios• Establishment of defined capital categories above minimum

ratios (e.g. “Prompt Corrective Action”)• Higher requirements for outliers

17

Supervisory Intervention

Principle 4• Supervisors should seek to intervene at an early stage to

prevent capital from falling below the minimum levels required to support the risk characteristics of a particular bank and should require rapid remedial action if capital is not maintained or restored.

18

Supervisory Intervention

Objective • Identify as early as possible the potential for serious

erosion of the bank’s capital position in order to limit risk to depositors and financial system

19

Supervisory Intervention

Intervening Actions• Determined by law, national policies, case-by-case

analysis• Moral suasion to encourage banks to improve their capital

positions• Capital ratios may represent triggers for supervisory

action, up to and including the closure of the bank

20

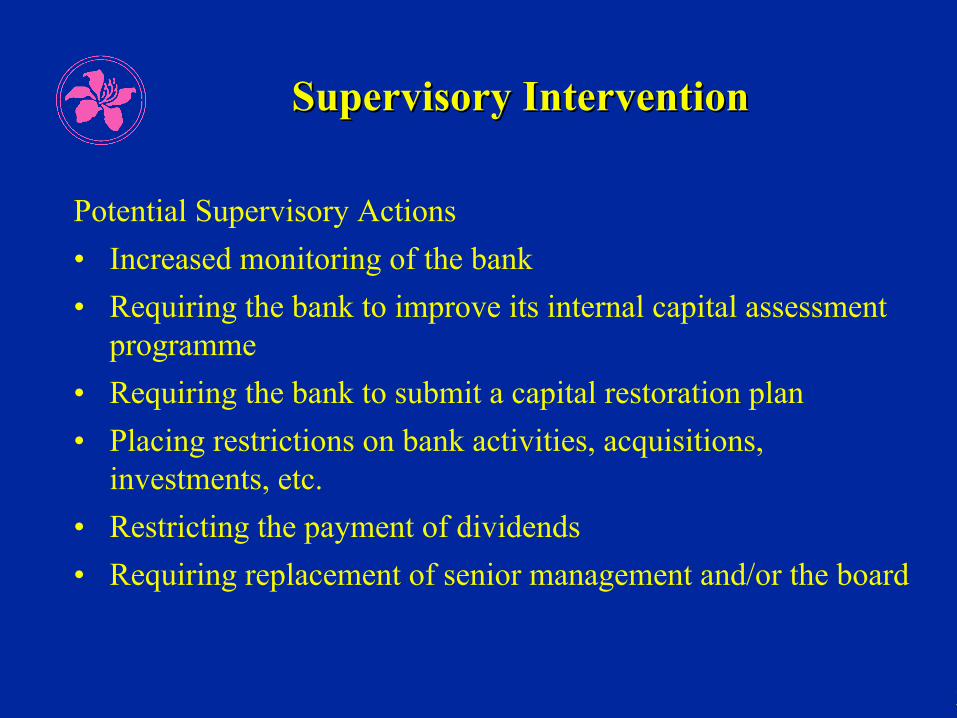

Supervisory InterventionSupervisory Intervention

Potential Supervisory Actions• Increased monitoring of the bank• Requiring the bank to improve its internal capital assessment

programme• Requiring the bank to submit a capital restoration plan• Placing restrictions on bank activities, acquisitions,

investments, etc.• Restricting the payment of dividends• Requiring replacement of senior management and/or the board

21

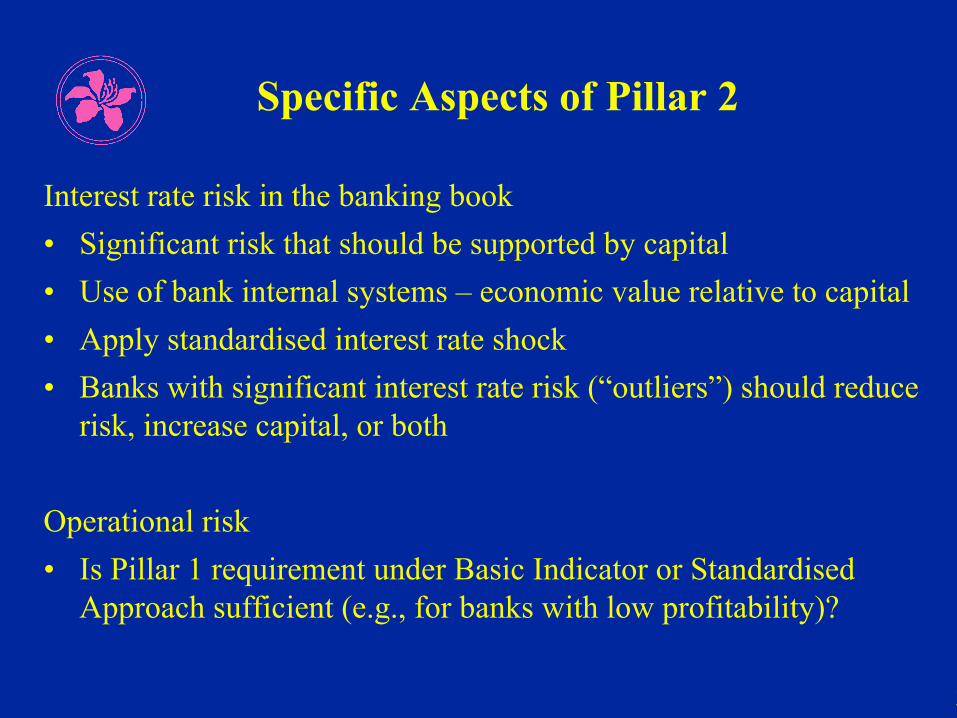

Specific Aspects of Pillar 2

Interest rate risk in the banking book• Significant risk that should be supported by capital• Use of bank internal systems – economic value relative to capital• Apply standardised interest rate shock• Banks with significant interest rate risk (“outliers”) should reduce

risk, increase capital, or both

Operational risk• Is Pillar 1 requirement under Basic Indicator or Standardised

Approach sufficient (e.g., for banks with low profitability)?

22

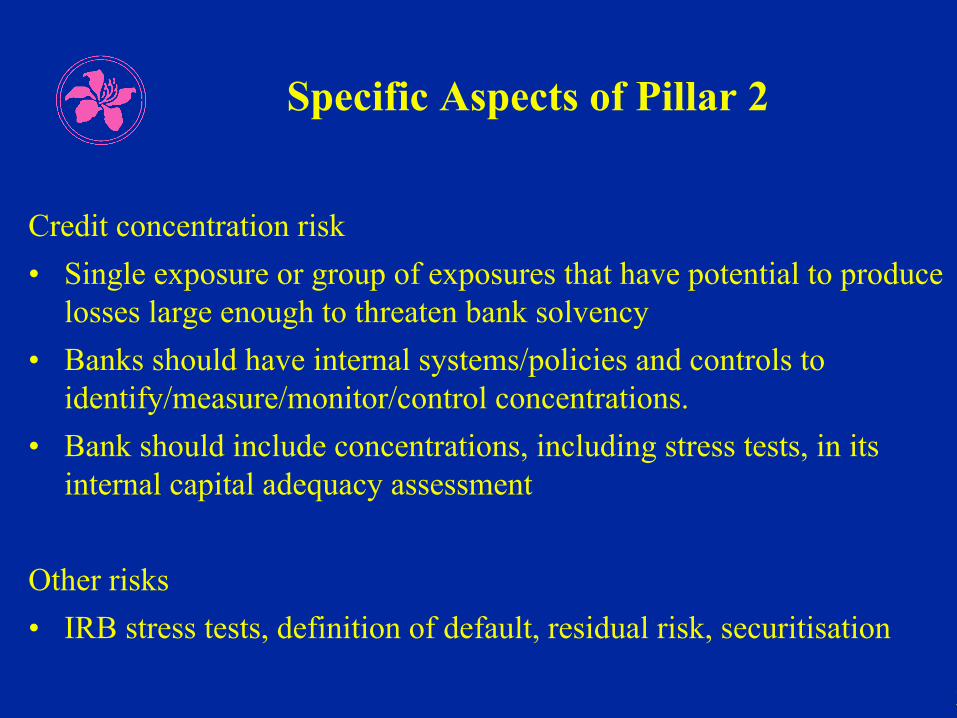

Specific Aspects of Pillar 2

Credit concentration risk• Single exposure or group of exposures that have potential to produce

losses large enough to threaten bank solvency• Banks should have internal systems/policies and controls to

identify/measure/monitor/control concentrations.• Bank should include concentrations, including stress tests, in its

internal capital adequacy assessment

Other risks• IRB stress tests, definition of default, residual risk, securitisation

23

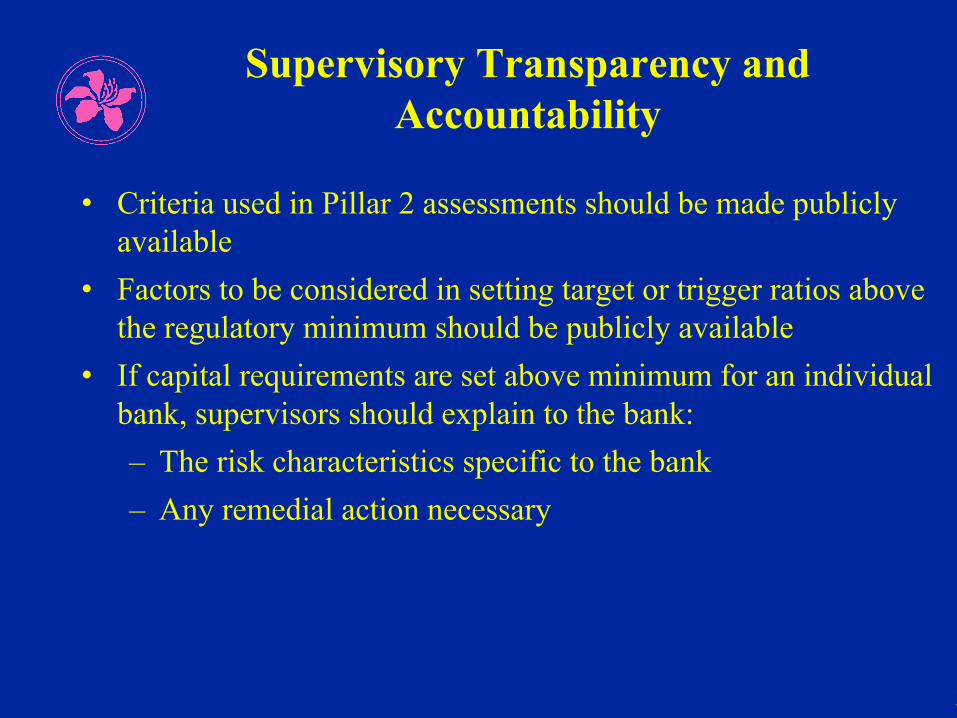

Supervisory Transparency and Accountability

• Criteria used in Pillar 2 assessments should be made publicly available

• Factors to be considered in setting target or trigger ratios above the regulatory minimum should be publicly available

• If capital requirements are set above minimum for an individual bank, supervisors should explain to the bank:– The risk characteristics specific to the bank– Any remedial action necessary

24

Pillar 2 Issues

Potentially Significant Obstacles• Legal and regulatory impediments• Resources (personnel, training, etc) necessary for

effective supervisory review• Level playing field• Transparency• Ability to exercise supervisory judgment

25

Hong Kong Approach: CAAP

• Each bank should establish a CAAP to fit its own circumstances and needs, having regard to the risk profile and level of sophistication of its operations

• The CAAP should be risk-based, forward-looking and form an integral part of the bank’s management / decision-making process

• The HKMA would not expect all banks necessarily to have a well-developed CAAP by 1 Jan 2007, but they should initiate efforts to put in place the basic elements of the CAAP and make steady progress towards enhancing the process over time

• Foreign bank subsidiaries may adopt group CAAP which is subject to comparable supervisory standards

26

Hong Kong Approach: SRP

Main objectives of the SRP :• Ensure banks have adequate capital to support all material risks

in their businesses• Encourage banks to develop and use better risk management

techniques for monitoring and controlling their risks• Encourage banks to engage in active capital management,

including strategic and capital planning• Foster an active dialogue between banks and supervisors

regarding fulfilment of capital adequacy and risk management standards

27

Hong Kong Approach: Setting Minimum CARs

• Legislation gives the MA the power to set minimum CARs on a bank-by-bank basis, in the range of 8 - 16% (i.e. with a maximum “add-on” of 8%)

• Current practice is to require a minimum “add-on” of 2%, principally to cover operational risk and business cycle risk

• In the past the process by which individual CARs are set has not very transparent, nor entirely rigorous; in practice, the ratio required was largely a function of the bank’s CAMEL rating and its size

28

Hong Kong Approach: New SRP

• We have developed and tested a new “scoring system” based around our existing risk-based supervisory system

• Banks are assessed on 8 risk areas – credit, market, interest rate, liquidity, operational, legal, reputation and strategic

• Their score depends on both the risk level and the quality of their risk management

29

Hong Kong Approach: New SRP

• The process begins with an assessment of the common factors (via the 13 supporting templates) using a combination of techniques and tools, including quantitative and qualitative assessments, scoring of key indicators and trends, statistical and sensitivity analyses, stress and scenario tests, benchmarking against industry performance and peer group comparison

• Scores (up to a total of 100) will be allocated to common factors included in the 13 supporting templates

30

Hong Kong Approach: New SRP

• The total score will be translated into a minimum CAR (up to 16%) according to a mapping table

• The portion above 8% is the capital add-on reflecting the HKMA’s assessment of the AI’s overall risk profile and extent of Pillar 2 risks

• Before arriving at the appropriate minimum CAR, need to assess any AI-specific factors not covered under the scoring system

31

Hong Kong Approach: New SRP

• The results of the SRP will be discussed with the bank, and willdetermine both the minimum CAR for the bank and our supervisory priorities

• The results can also be aggregated across the sector to provide a picture of sectoral risks

• Banks’ own CAAPs will be reviewed as part of the SRP, but setting of their minimum CAR will, for the time being, remain driven by supervisory assessment

• In effect, this approach attempts to apply the same degree of rigour to the Pillar 2 risks as has been applied to the Pillar 1risks

32

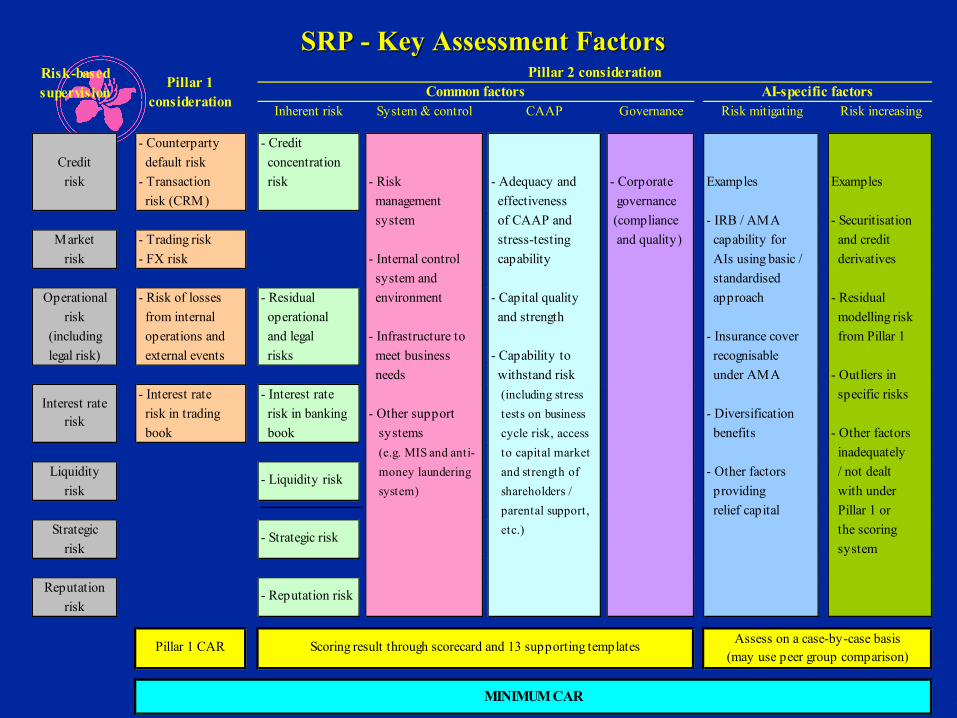

SRP SRP -- Key Assessment FactorsKey Assessment FactorsRisk-basedsupervision

Inherent risk System & control CAAP Governance Risk mitigating Risk increasing

- Counterparty - CreditCredit default risk concentrationrisk - Transaction risk - Risk - Adequacy and - Corporate Examples Examples

risk (CRM) management effectiveness governance system of CAAP and (compliance - IRB / AMA - Securitisation

Market - Trading risk stress-testing and quality) capability for and creditrisk - FX risk - Internal control capability AIs using basic / derivatives

system and standardisedOperational - Risk of losses - Residual environment - Capital quality approach - Residual

risk from internal operational and strength modelling risk(including operations and and legal - Infrastructure to - Insurance cover from Pillar 1legal risk) external events risks meet business - Capability to recognisable

needs withstand risk under AMA - Outliers in- Interest rate - Interest rate (including stress specific risks risk in trading risk in banking - Other support tests on business - Diversification book book systems cycle risk, access benefits - Other factors

(e.g. MIS and anti- to capital market inadequatelyLiquidity money laundering and strength of - Other factors / not dealt

risk system) shareholders / providing with under parental support, relief capital Pillar 1 or

Strategic etc.) the scoringrisk system

Reputationrisk

Pillar 2 consideration

Interest raterisk

Pillar 1 CAR Scoring result through scorecard and 13 supporting templates

- Liquidity risk

- Strategic risk

- Reputation risk

Pillar 1consideration

Common factors

MINIMUM CAR

Assess on a case-by-case basis(may use peer group comparison)

AI-specific factors

33

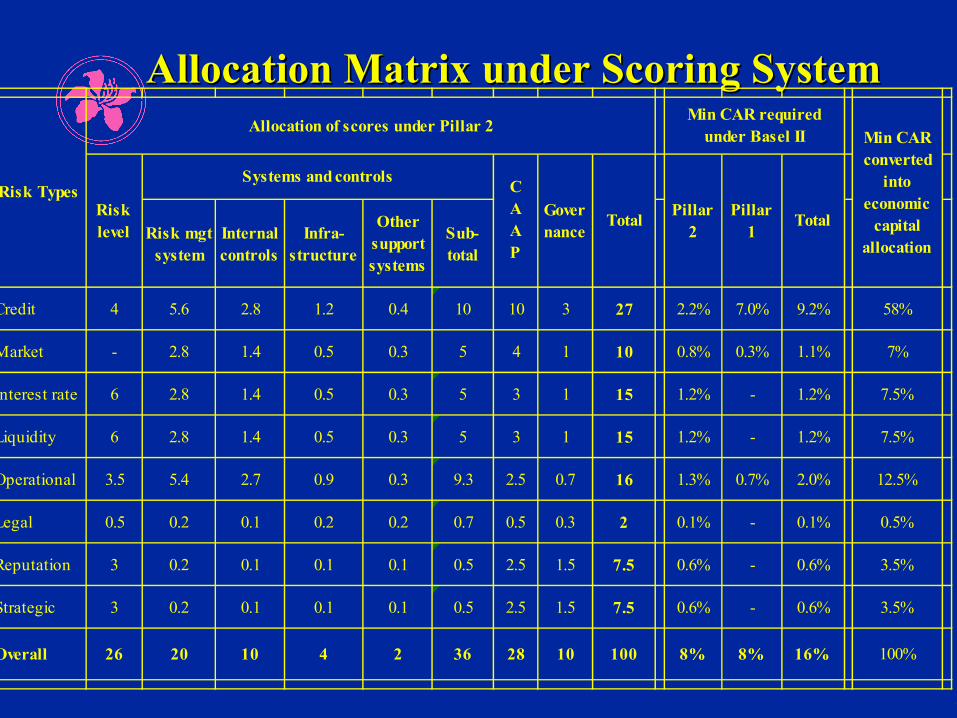

Allocation Matrix under Scoring SystemAllocation Matrix under Scoring System

Risk mgtsystem

Internalcontrols

Infra-structure

Othersupportsystems

Sub-total

Credit 4 5.6 2.8 1.2 0.4 10 10 3 27 2.2% 7.0% 9.2% 58%

Market - 2.8 1.4 0.5 0.3 5 4 1 10 0.8% 0.3% 1.1% 7%

Interest rate 6 2.8 1.4 0.5 0.3 5 3 1 15 1.2% - 1.2% 7.5%

Liquidity 6 2.8 1.4 0.5 0.3 5 3 1 15 1.2% - 1.2% 7.5%

Operational 3.5 5.4 2.7 0.9 0.3 9.3 2.5 0.7 16 1.3% 0.7% 2.0% 12.5%

Legal 0.5 0.2 0.1 0.2 0.2 0.7 0.5 0.3 2 0.1% - 0.1% 0.5%

Reputation 3 0.2 0.1 0.1 0.1 0.5 2.5 1.5 7.5 0.6% - 0.6% 3.5%

Strategic 3 0.2 0.1 0.1 0.1 0.5 2.5 1.5 7.5 0.6% - 0.6% 3.5%

Overall 26 20 10 4 2 36 28 10 100 8% 8% 16% 100%

Min CARconverted

intoeconomic

capitalallocation

Allocation of scores under Pillar 2

Total

Min CAR requiredunder Basel II

Pillar1

Pillar2

TotalGovernance

Risklevel

Systems and controlsRisk Types C

AAP

34

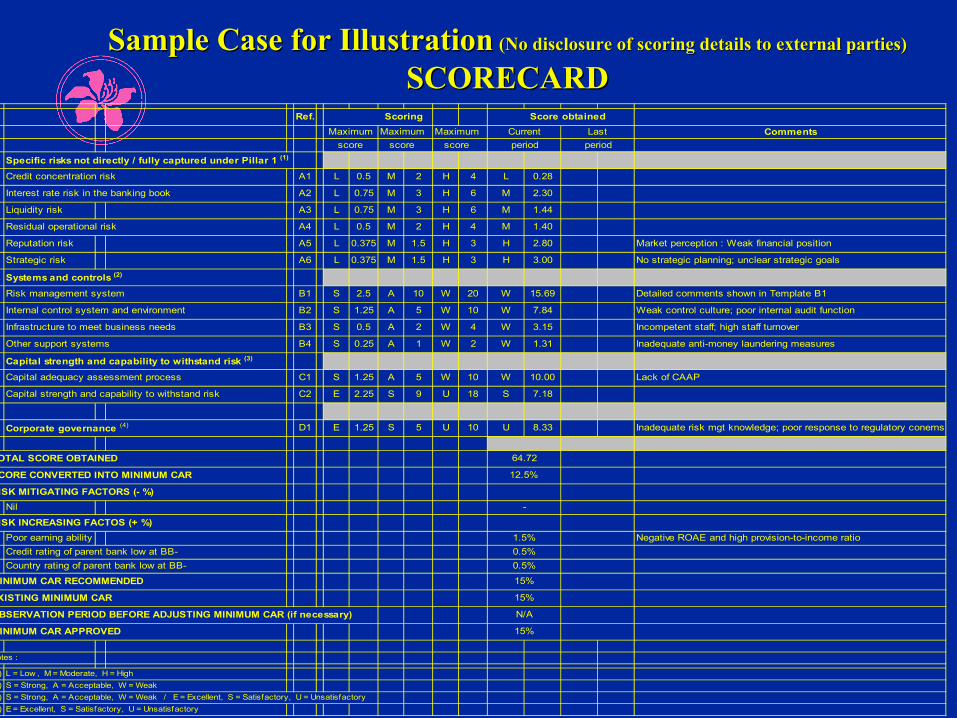

Sample Case for IllustrationSample Case for Illustration (No disclosure of scoring details to external parties)(No disclosure of scoring details to external parties)

SCORECARDSCORECARDRef. Scoring Score obtained

Maximum Maximum Maximum Current Last Comments score score score period period

A. Specific risks not directly / fully captured under Pillar 1 (1)

Credit concentration risk A1 L 0.5 M 2 H 4 L 0.28

Interest rate risk in the banking book A2 L 0.75 M 3 H 6 M 2.30

Liquidity risk A3 L 0.75 M 3 H 6 M 1.44

Residual operational risk A4 L 0.5 M 2 H 4 M 1.40

Reputation risk A5 L 0.375 M 1.5 H 3 H 2.80 Market perception : Weak financial position

Strategic risk A6 L 0.375 M 1.5 H 3 H 3.00 No strategic planning; unclear strategic goals

B. Systems and controls (2)

Risk management system B1 S 2.5 A 10 W 20 W 15.69 Detailed comments shown in Template B1

Internal control system and environment B2 S 1.25 A 5 W 10 W 7.84 Weak control culture; poor internal audit function

Infrastructure to meet business needs B3 S 0.5 A 2 W 4 W 3.15 Incompetent staff; high staff turnover

Other support systems B4 S 0.25 A 1 W 2 W 1.31 Inadequate anti-money laundering measures

C. Capital strength and capability to withstand risk (3)

Capital adequacy assessment process C1 S 1.25 A 5 W 10 W 10.00 Lack of CAAP

Capital strength and capability to withstand risk C2 E 2.25 S 9 U 18 S 7.18

D. Corporate governance (4) D1 E 1.25 S 5 U 10 U 8.33 Inadequate risk mgt knowledge; poor response to regulatory conerns

TOTAL SCORE OBTAINED

SCORE CONVERTED INTO MINIMUM CAR

RISK MITIGATING FACTORS (- %)- Nil

RISK INCREASING FACTOS (+ %)- Poor earning ability Negative ROAE and high provision-to-income ratio- Credit rating of parent bank low at BB-- Country rating of parent bank low at BB-

MINIMUM CAR RECOMMENDED

EXISTING MINIMUM CAR

OBSERVATION PERIOD BEFORE ADJUSTING MINIMUM CAR (if necessary)

MINIMUM CAR APPROVED

Notes :

(1) L = Low , M = Moderate, H = High(2) S = Strong, A = Acceptable, W = Weak(3) S = Strong, A = Acceptable, W = Weak / E = Excellent, S = Satisfactory, U = Unsatisfactory(4) E = Excellent, S = Satisfactory, U = Unsatisfactory

0.5%

64.72

12.5%

-

15%

1.5%

0.5%

15%

15%

N/A

35

Conclusions

• The three pillars together are intended to achieve a level of capital commensurate with a bank’s overall risk profile

• Starting point and emphasis is bank’s assessment• Sophistication of capital assessment should depend on size,

complexity, and risk profile of the bank• Pillar 2 does not require specific, formal, across-the-board capital

add-on requirements - a range of approaches is possible• Intention is to drive

– better bank risk management and– more risk-focused supervision