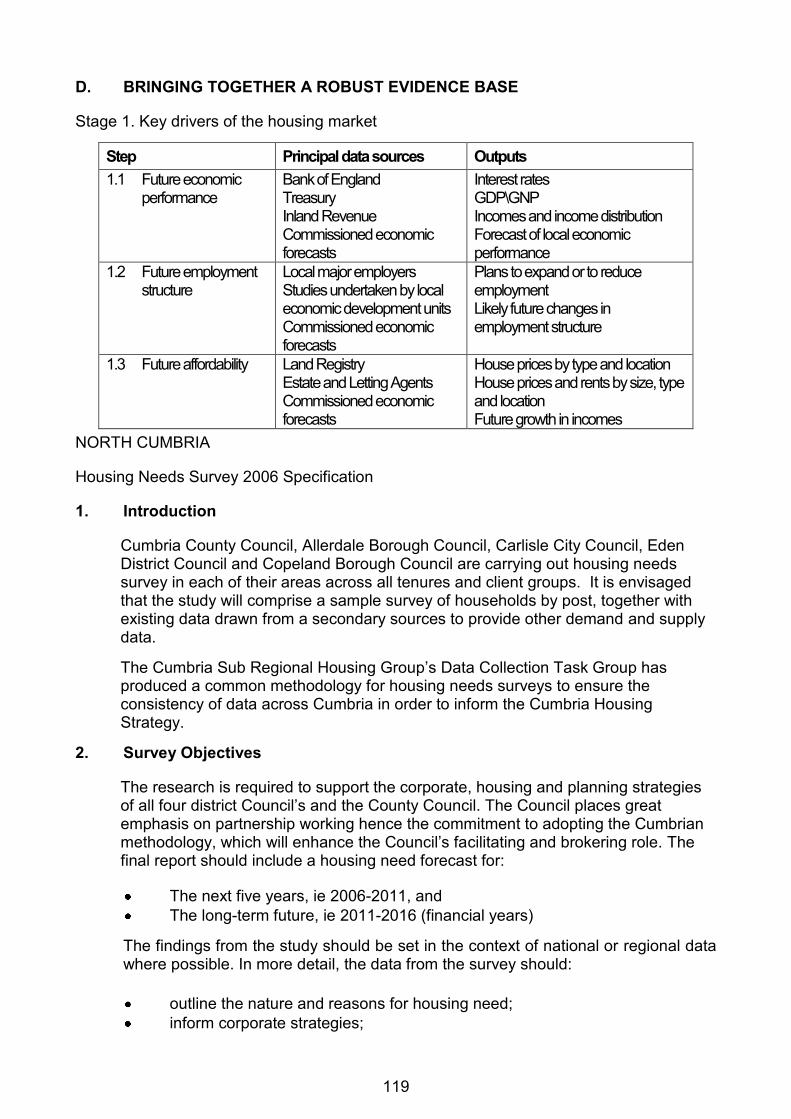

Embed Size (px)

Citation preview

Based on Ordnance Survey map material with the permission of the Controller of Her Majesty's Stationary Office. Crown Copyright. Unauthorised reproduction infringes Crown Copyright and may lead to prosecution or civil proceedings.

Cumbria County Council. Licence No LA076546. 2006.

2

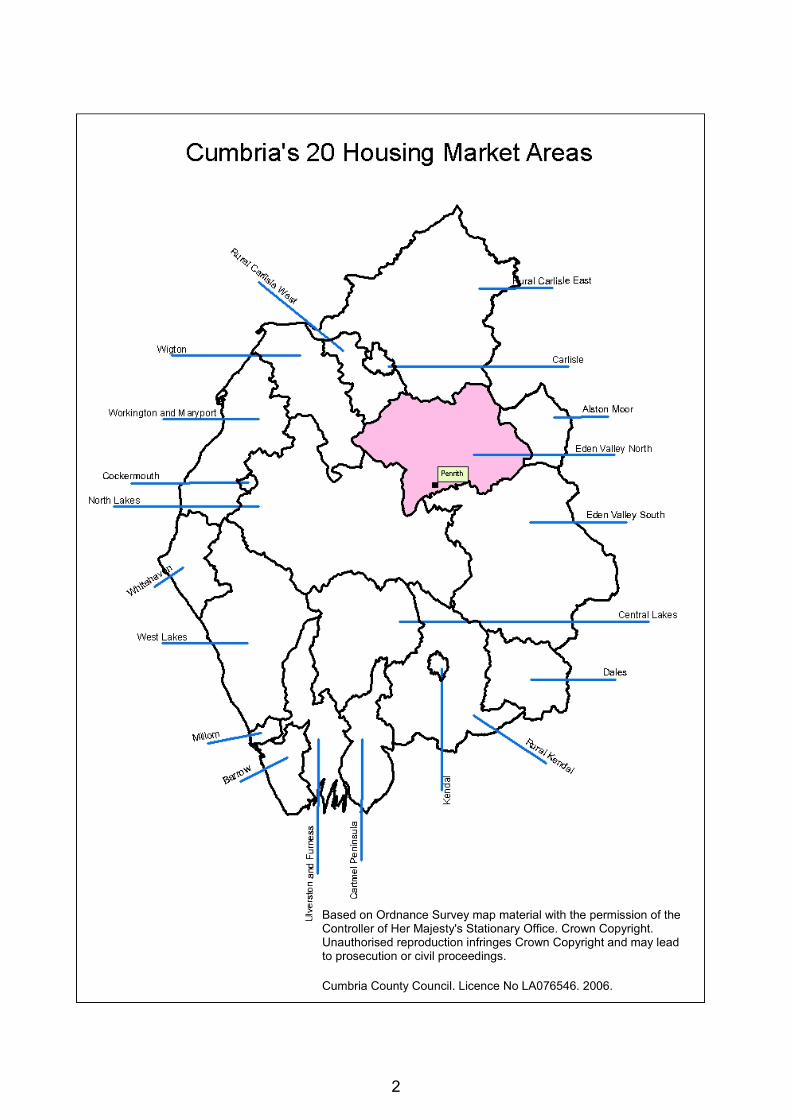

Based on Ordnance Survey map material with the permission of the Controller of Her Majesty's Stationary Office. Crown Copyright. Unauthorised reproduction infringes Crown Copyright and may lead to prosecution or civil proceedings.

Cumbria County Council. Licence No LA076546. 2006.

3

Eden Valley North Strategic Housing Market Assessment

List of Abbreviations ............................................................................................... 5

Current Market Profile ............................................................................................. 6

Headline Findings ...................................................................................................... 6

Targets ...................................................................................................................... 6

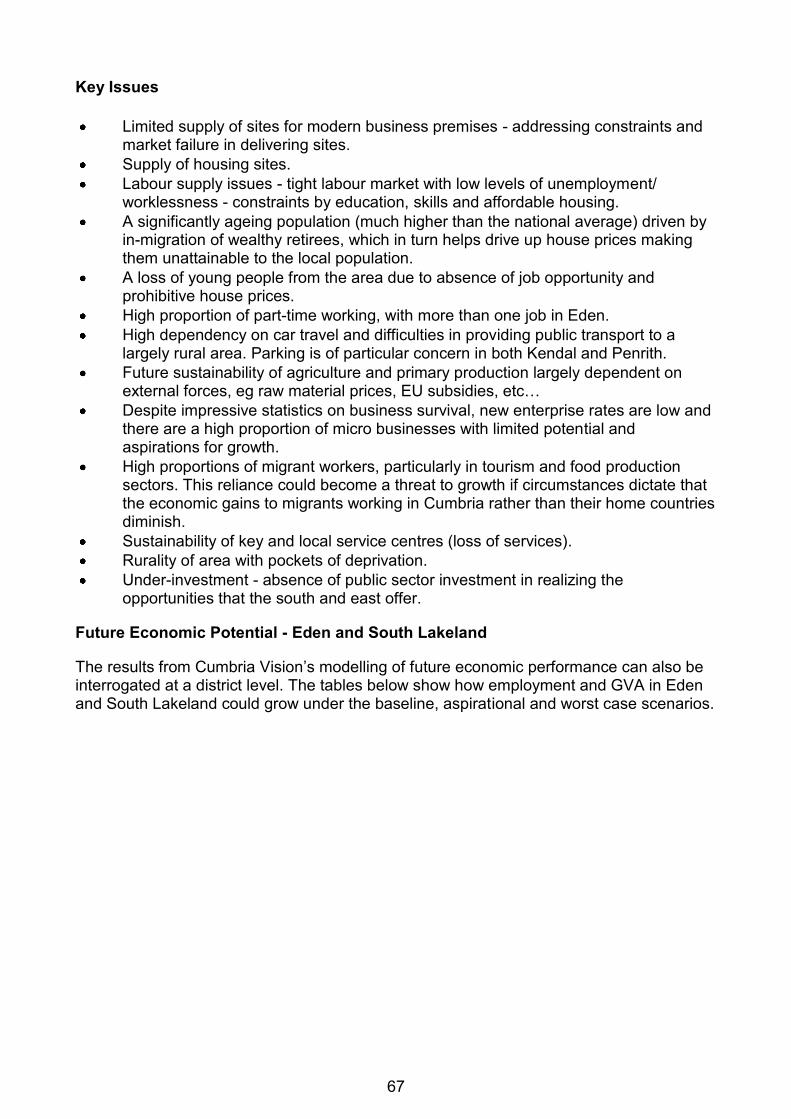

Key Issues ................................................................................................................. 7

Balanced Housing Market Indicators .................................................................... 9

The Current Housing Market ................................................................................ 10

Stage 1: The Demographic and Economic Context ................................................. 10

1.1 Demography and Household Types ......................................................... 10

1.2 National and Regional Economic Policy ................................................... 12

1.3 Employment Levels and Structure ............................................................ 20

1.4 Incomes and Earnings .............................................................................. 35

Stage 2: The Housing Stock .................................................................................... 41

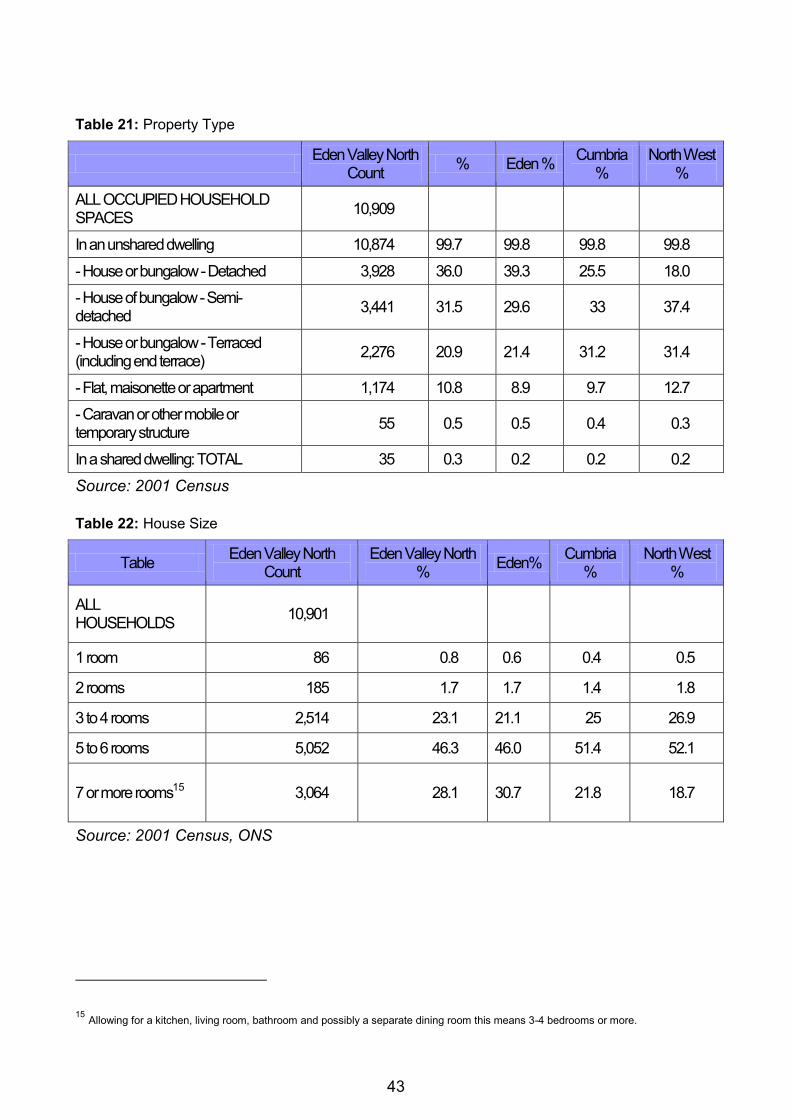

2.1 The Dwelling Profile .................................................................................. 41

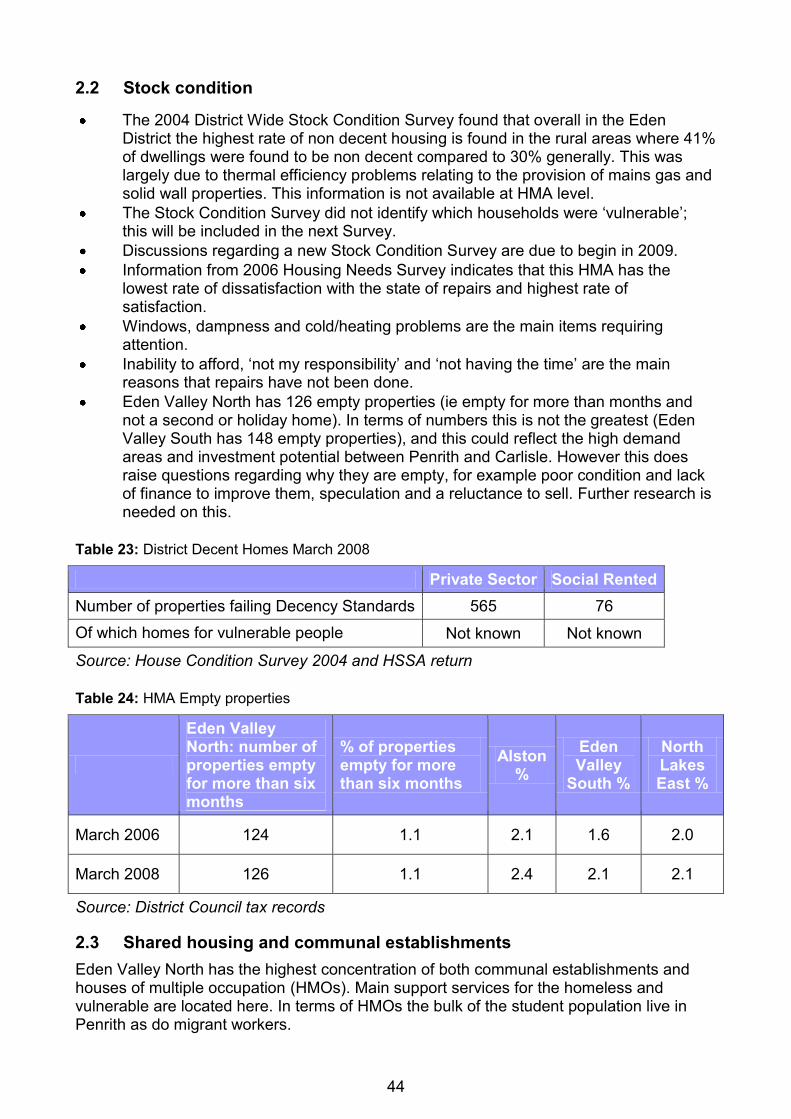

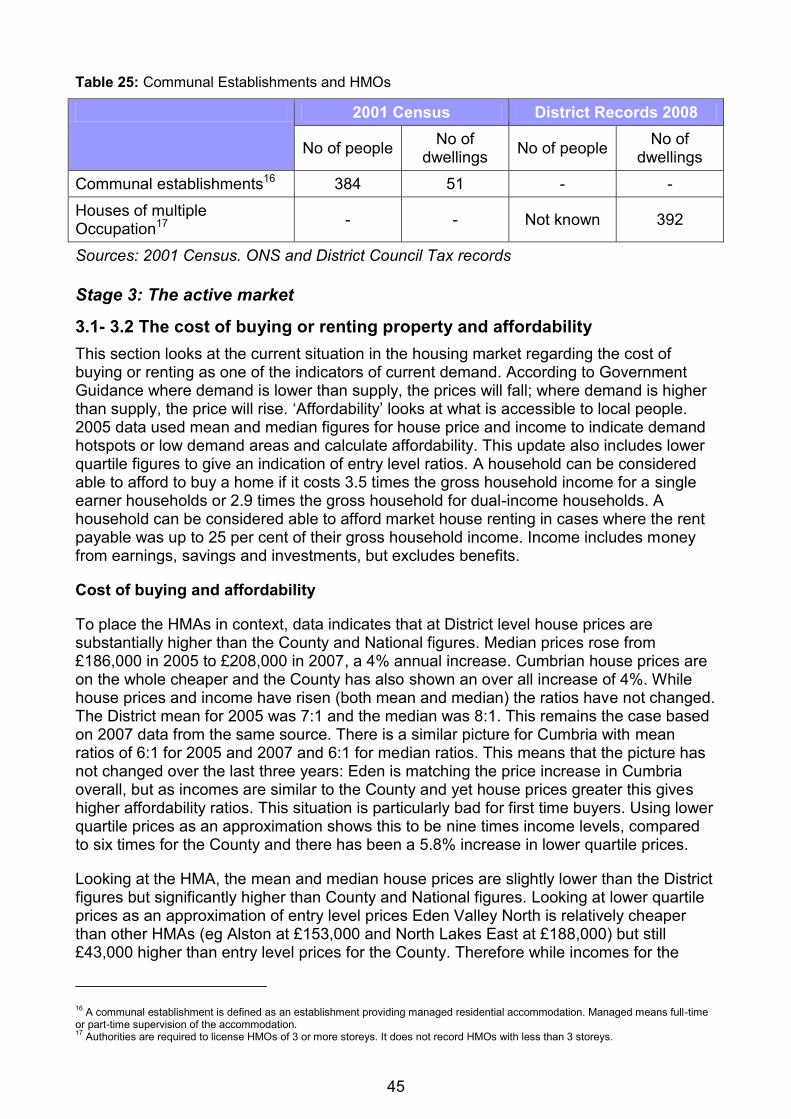

2.2 Stock Condition ........................................................................................ 44

2.3 Shared Housing and Communal Establishments ..................................... 44

Stage 3: The Active Market ..................................................................................... 45

3.1-3.2 The cost of buying or renting a property and affordability ......................... 45

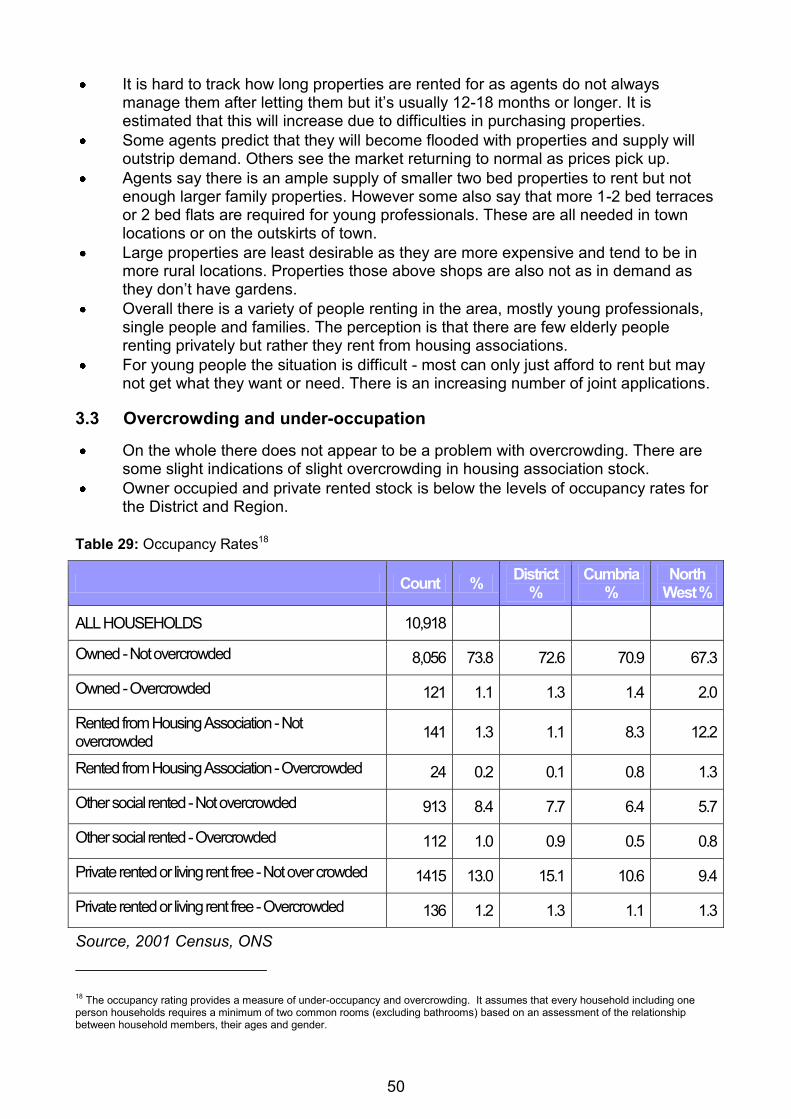

3.3 Overcrowding and under-occupation ........................................................ 50

3.4 Vacancies, available supply and turnover by tenure................................. 51

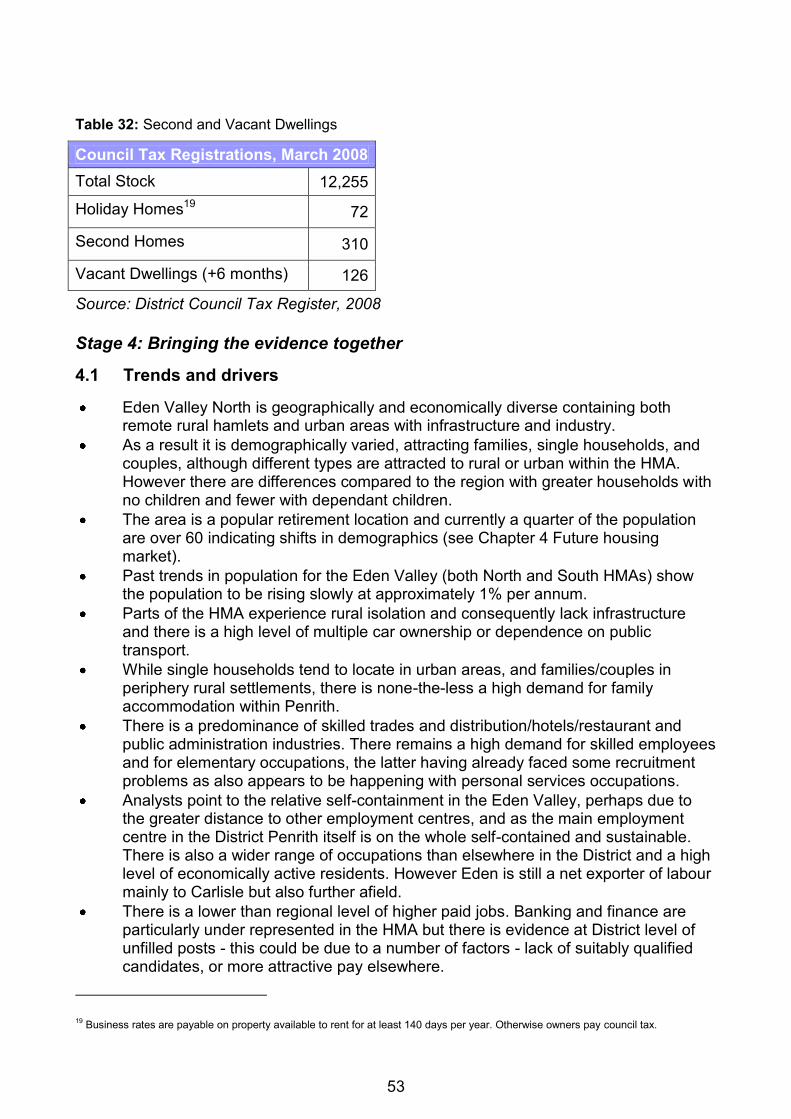

3.5 Second Homes and Vacant Dwellings ...................................................... 52

Stage 4: Bringing the Evidence Together ................................................................ 53

4.1 Trends and Drivers ................................................................................... 53

4.2 Issues for Future Policy/ Strategy ............................................................. 54

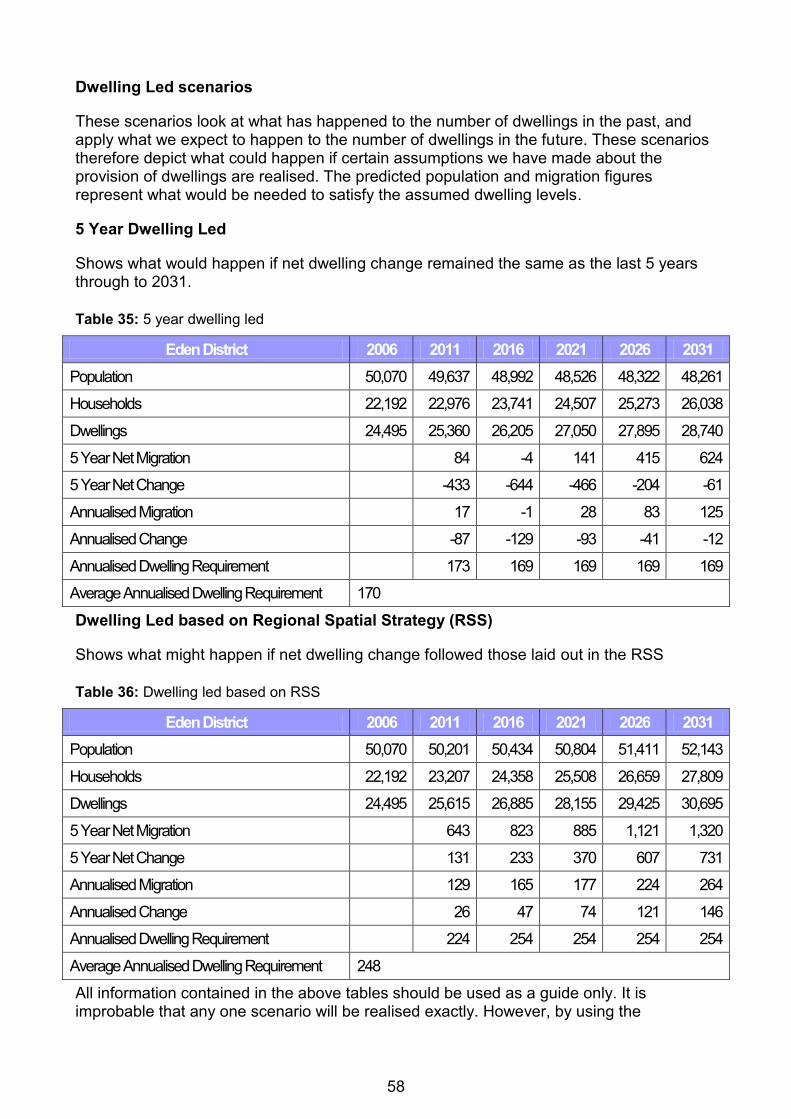

The Future Housing Market .................................................................................. 56

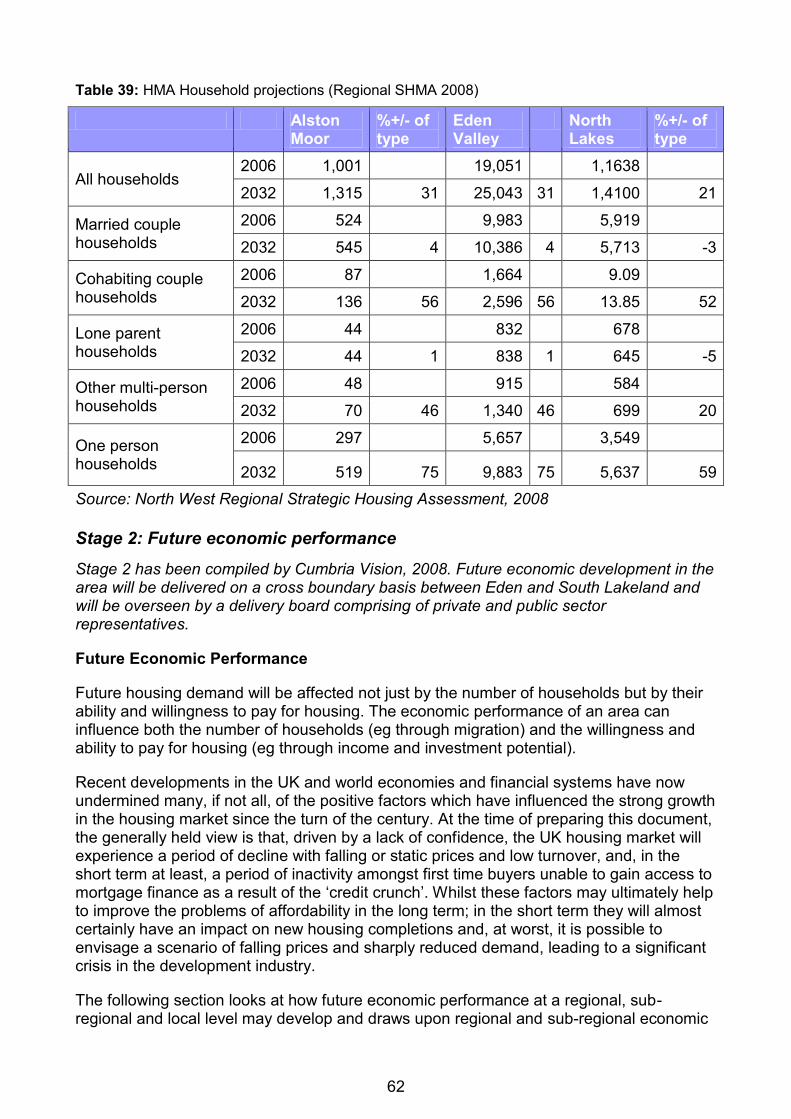

Stage 1: Projecting changes in future numbers of households ................................ 56

Stage 2: Future Economic Performance .................................................................. 62

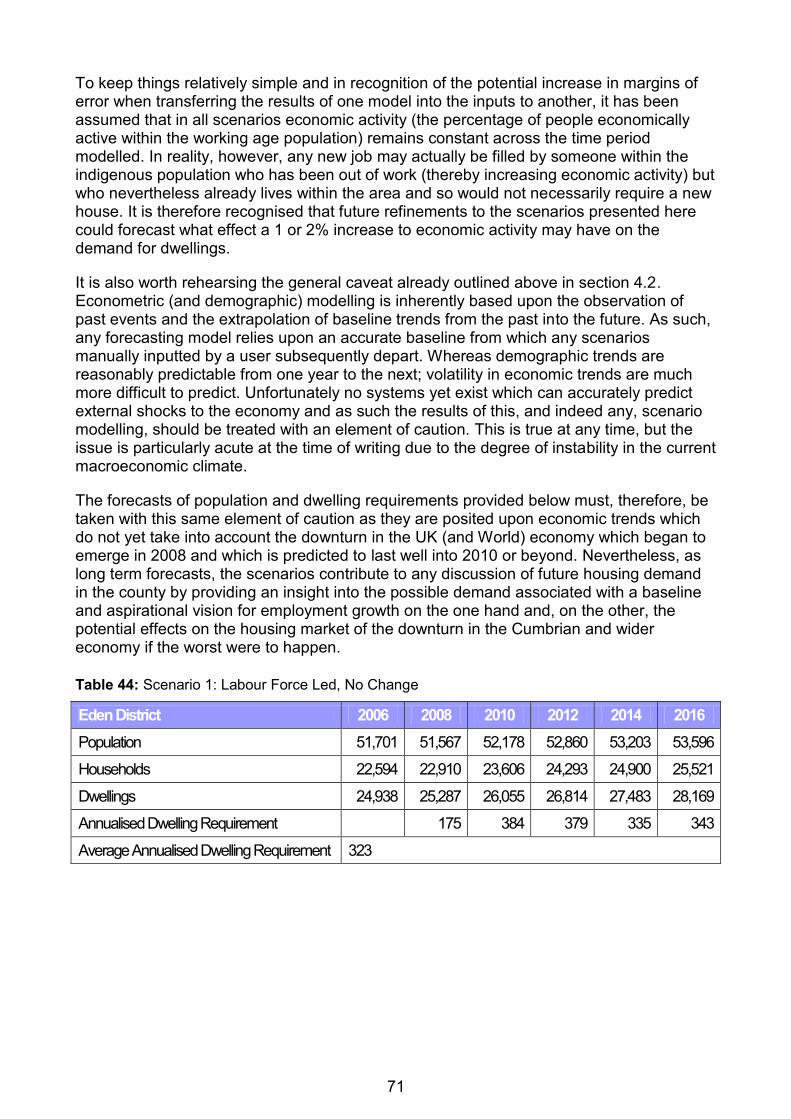

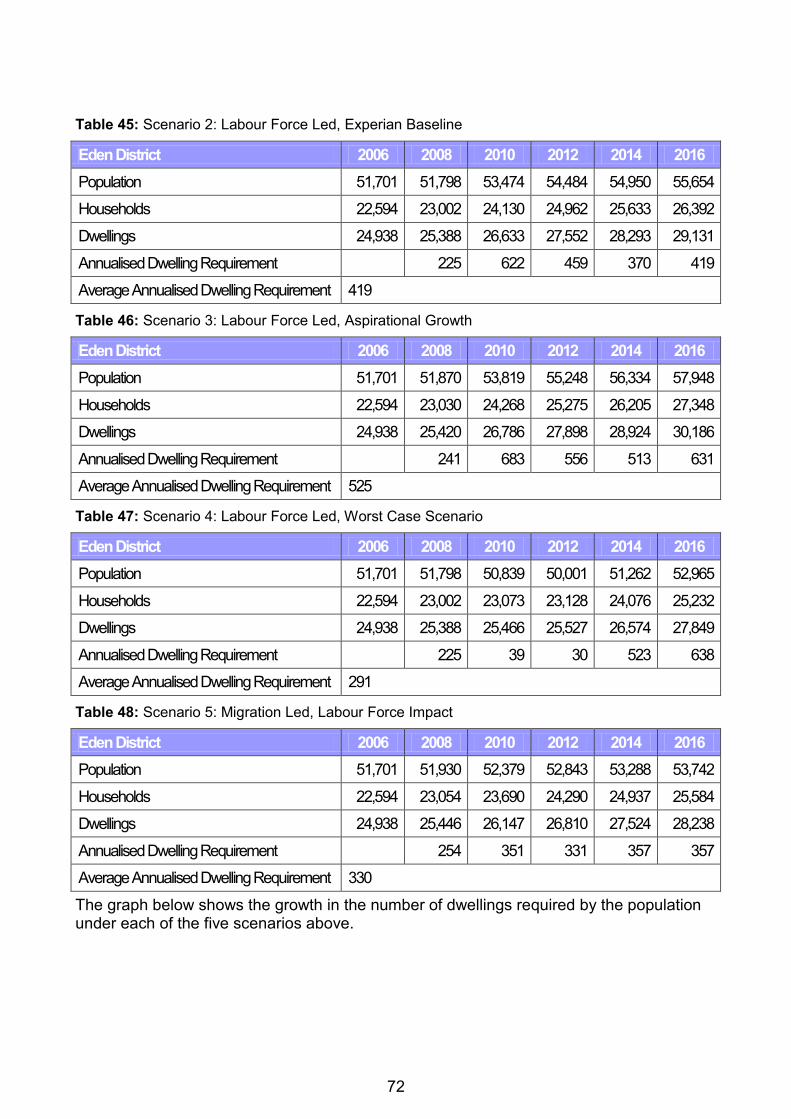

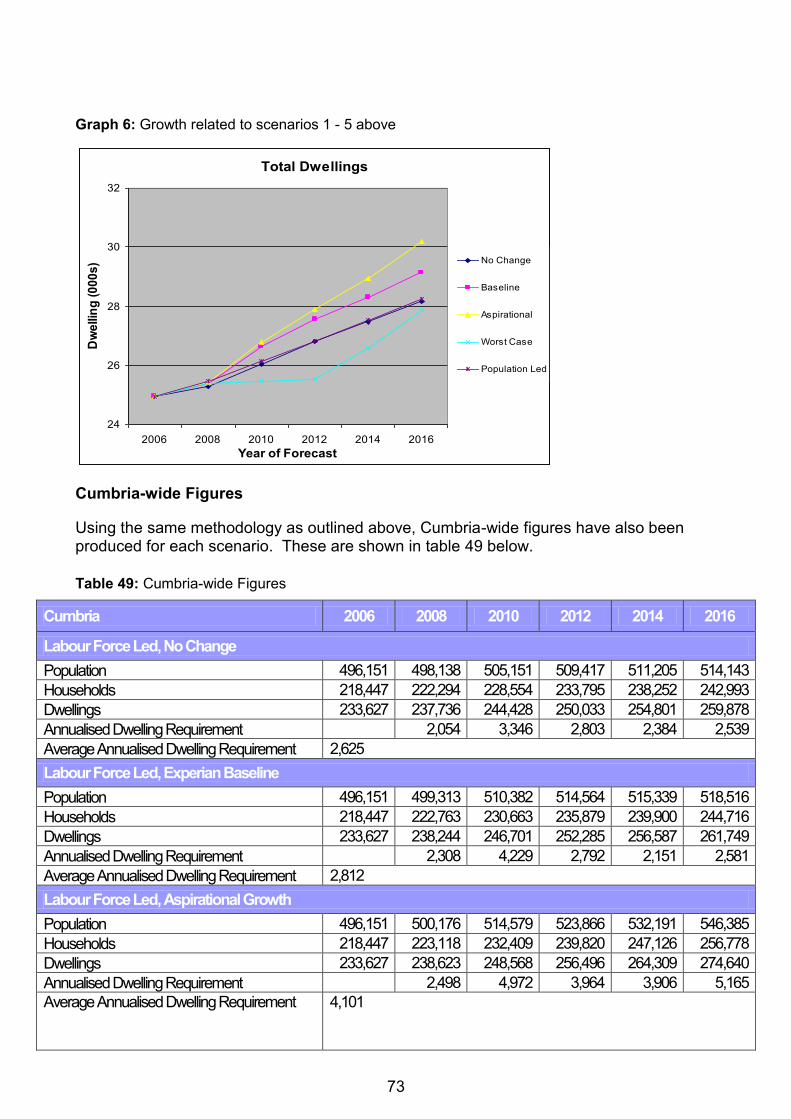

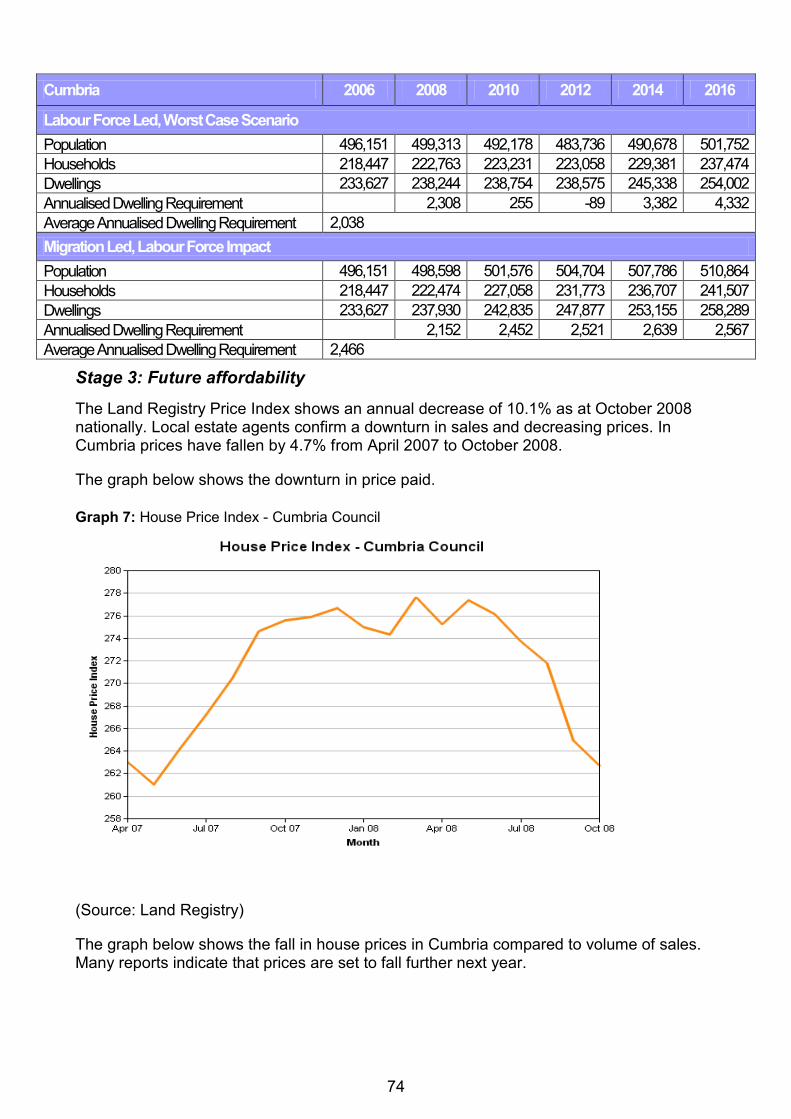

Stage 3: Future Affordability .................................................................................... 74

Stage 4: Bringing the Evidence Together ................................................................ 77

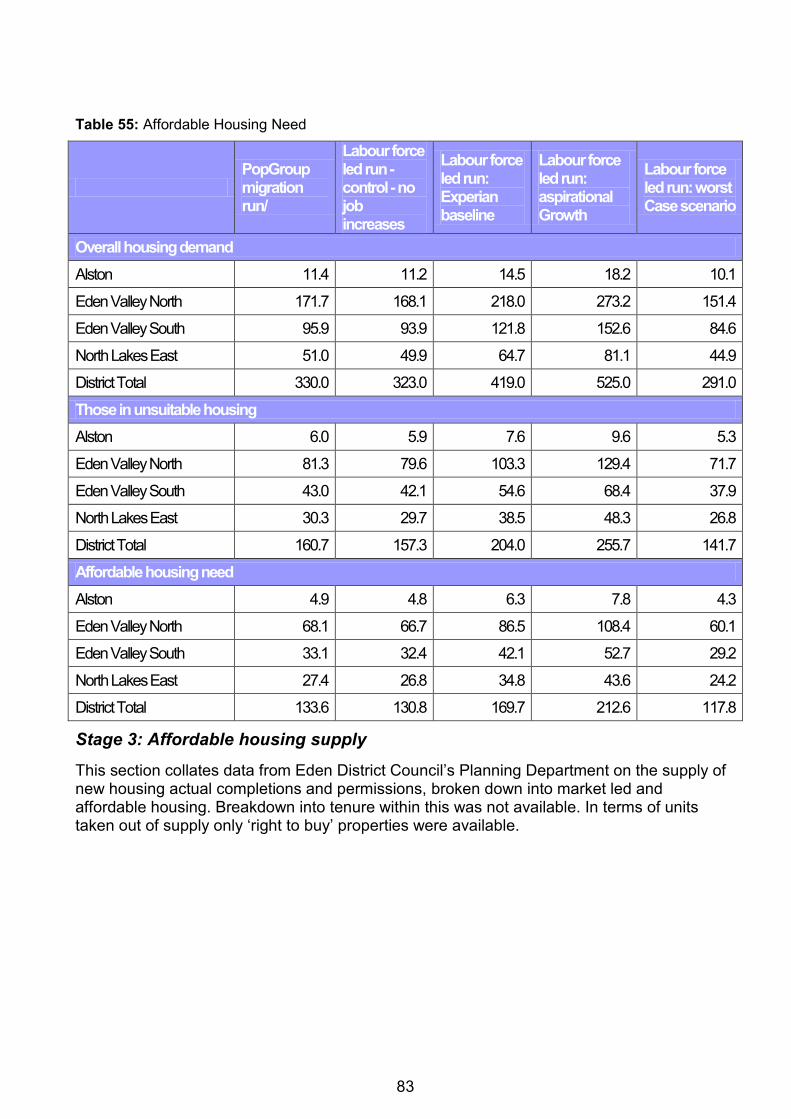

Housing Need (affordable housing) ..................................................................... 78

Stage 1: Current Housing Need ............................................................................... 78

Stage 2: Future Housing Need ................................................................................ 78

Stage 3: Affordable Housing Supply ........................................................................ 83

4

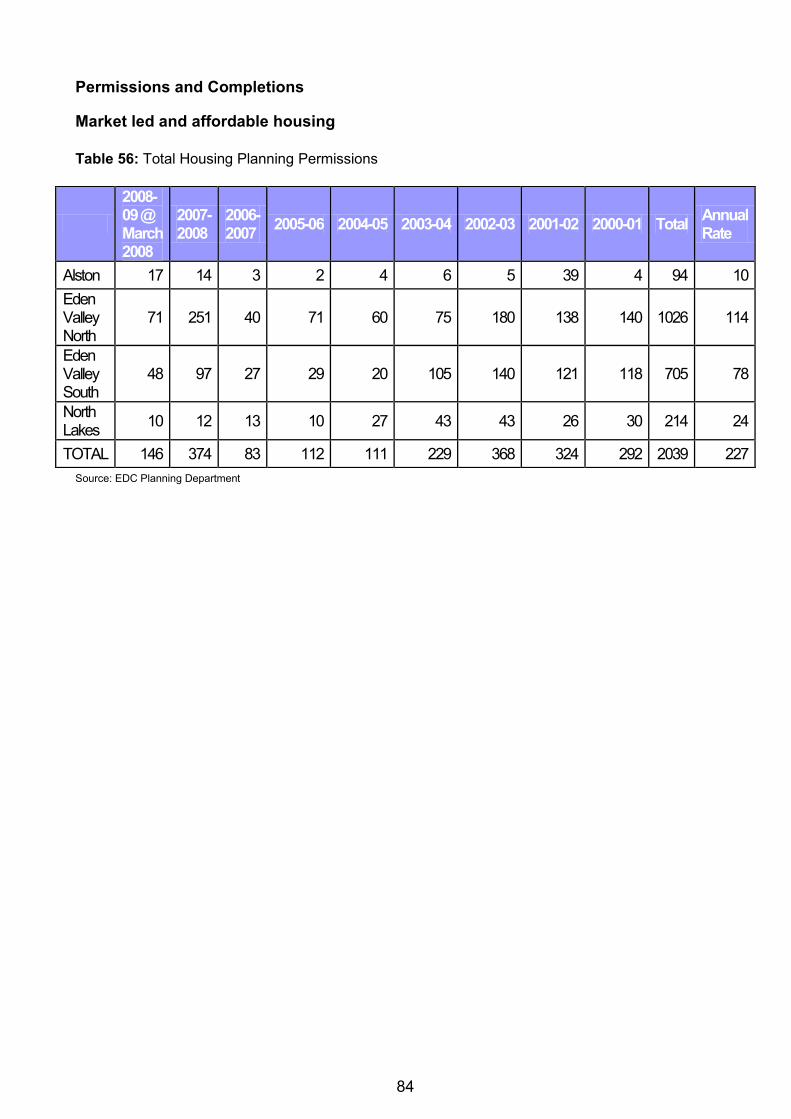

Permissions and Completions .................................................................... 84

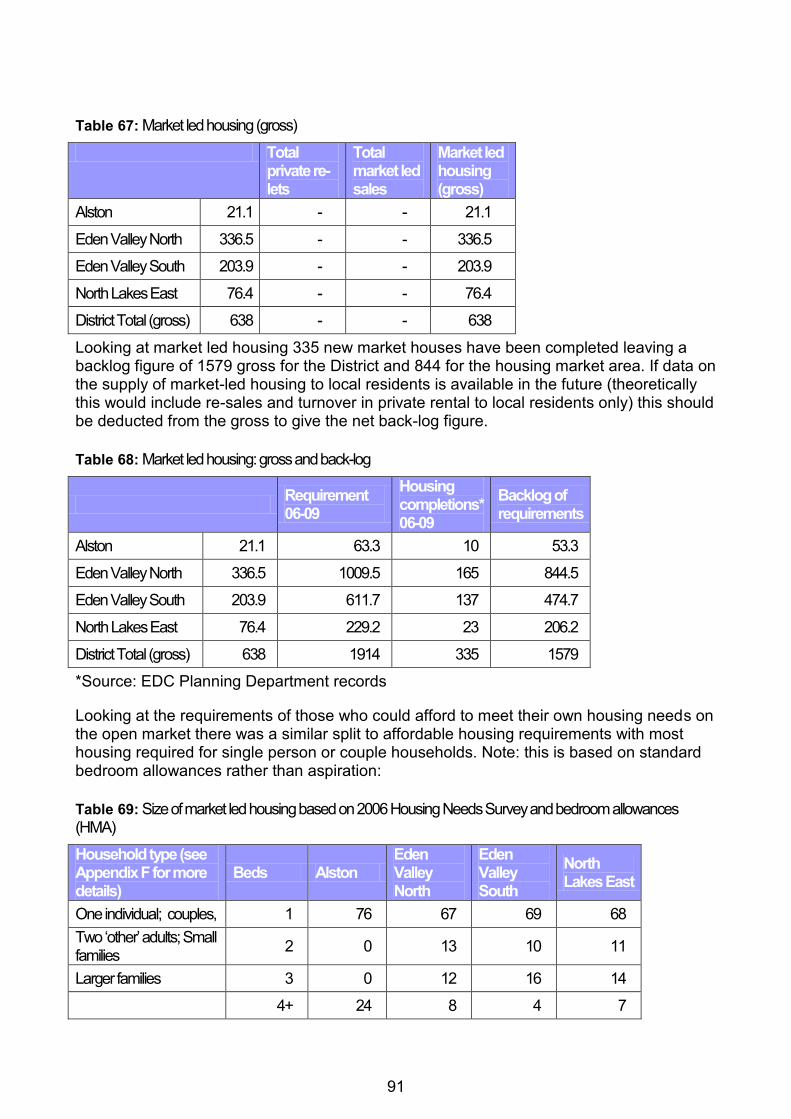

Market led and affordable housing ..................................................................................... 84

Affordable housing only- permissions and completions ..................................................... 85

Stage 4: Housing Requirements of Households in Need ......................................... 86

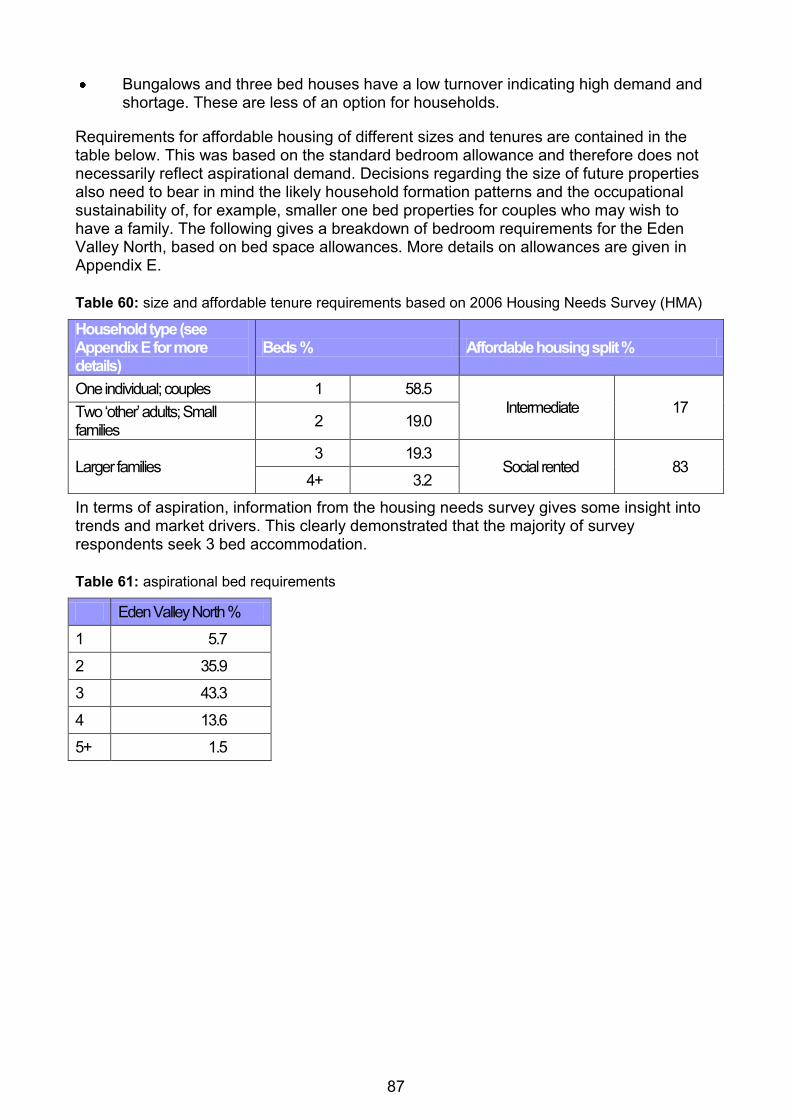

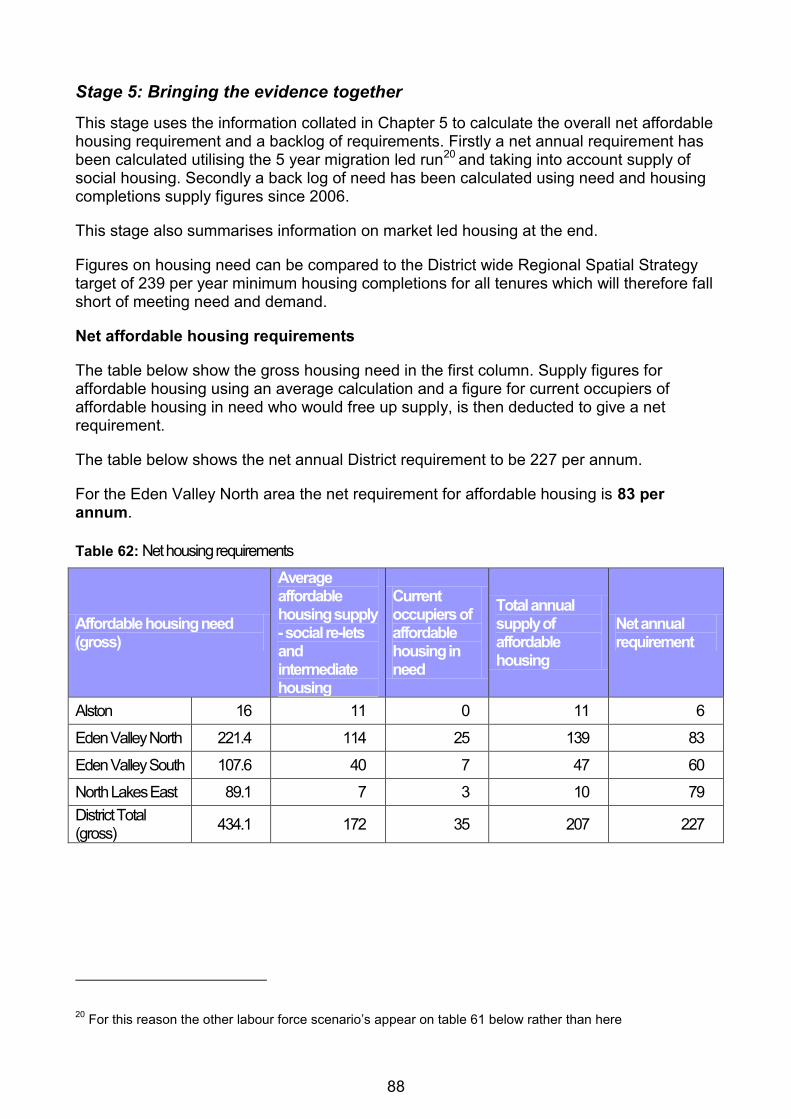

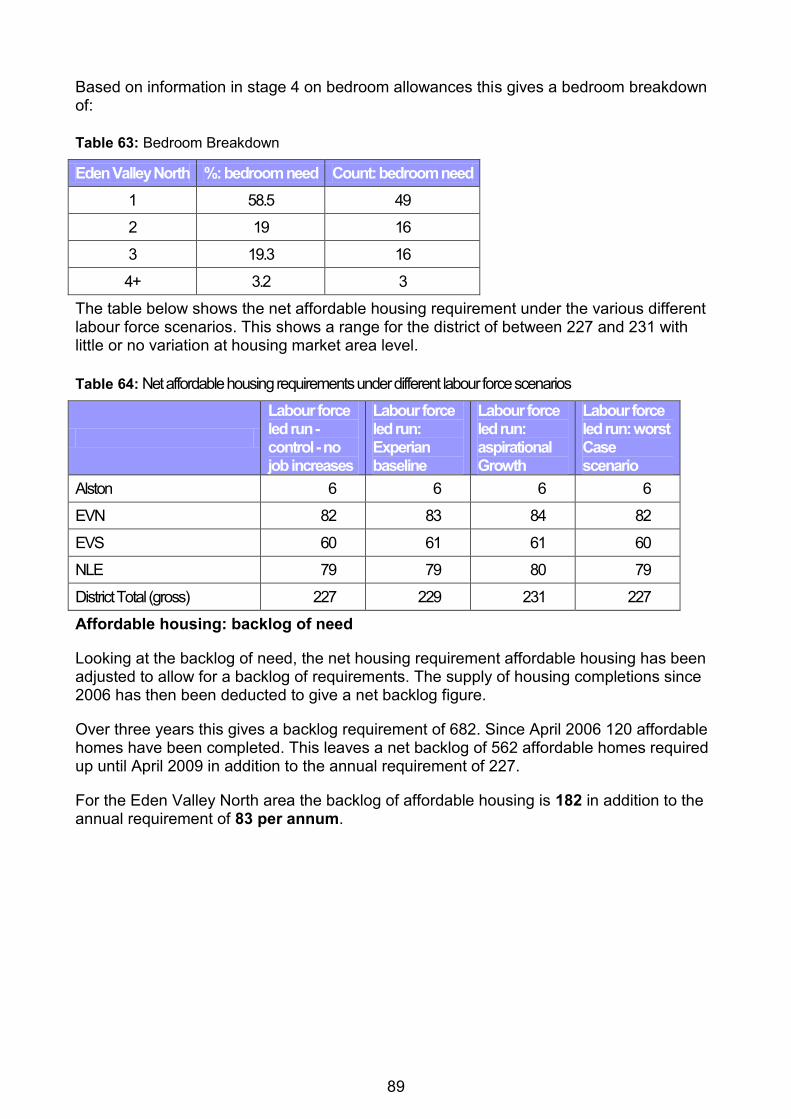

Stage 5: Bringing the Evidence Together ................................................................ 87

Updated estimate of net annual housing need ................................................................... 87

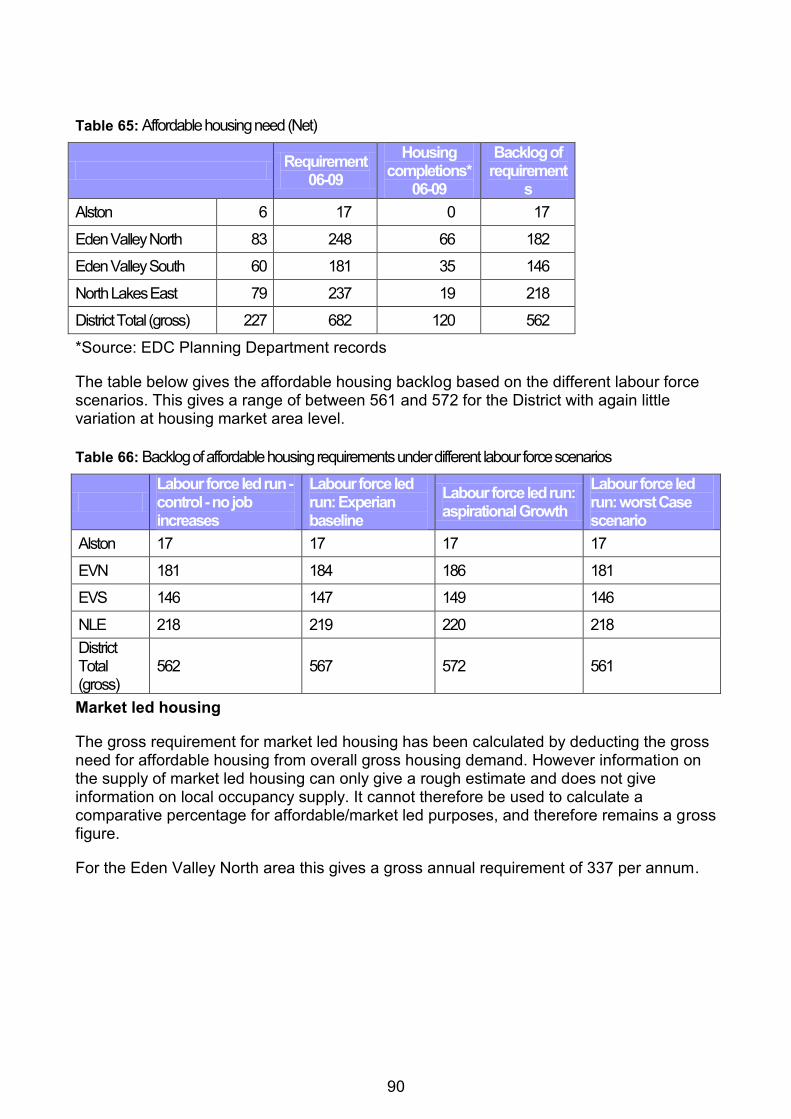

Key issues for future policy/ strategy ................................................................................. 92

Housing Requirements of Specific Household Groups..................................... 93

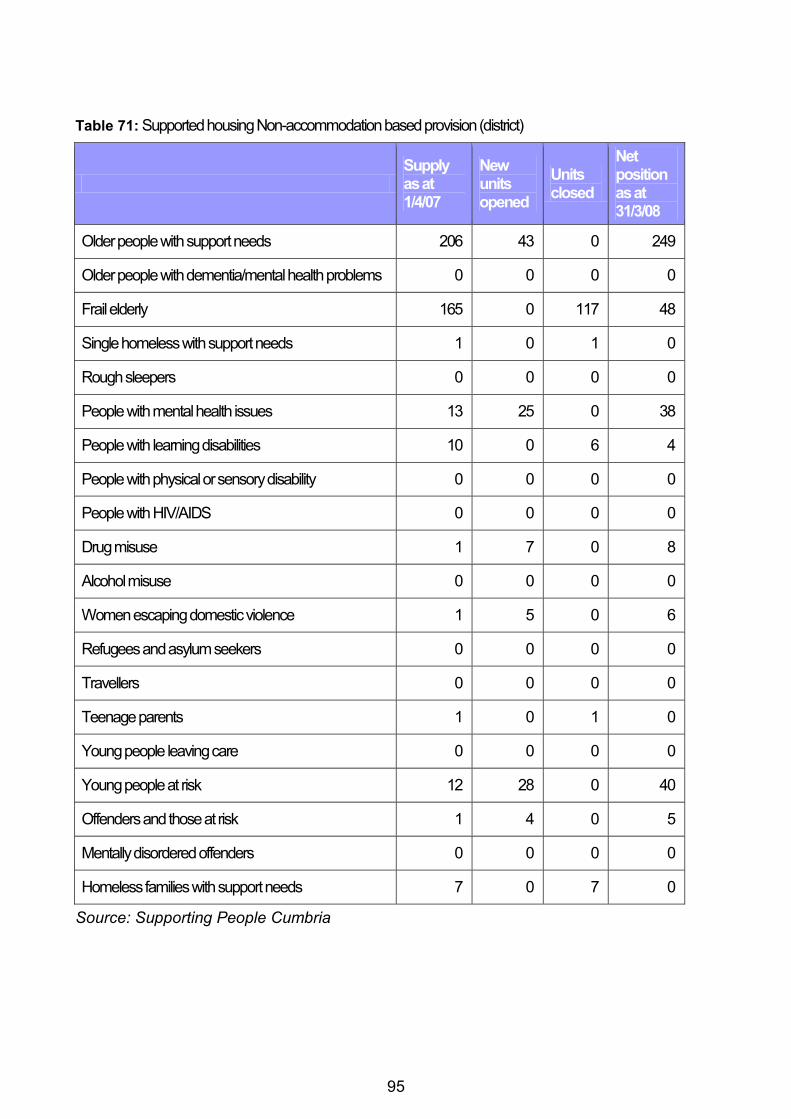

Supported Housing .................................................................................................. 93

Older People ............................................................................................................ 96

Gypsy and Travellers ............................................................................................... 97

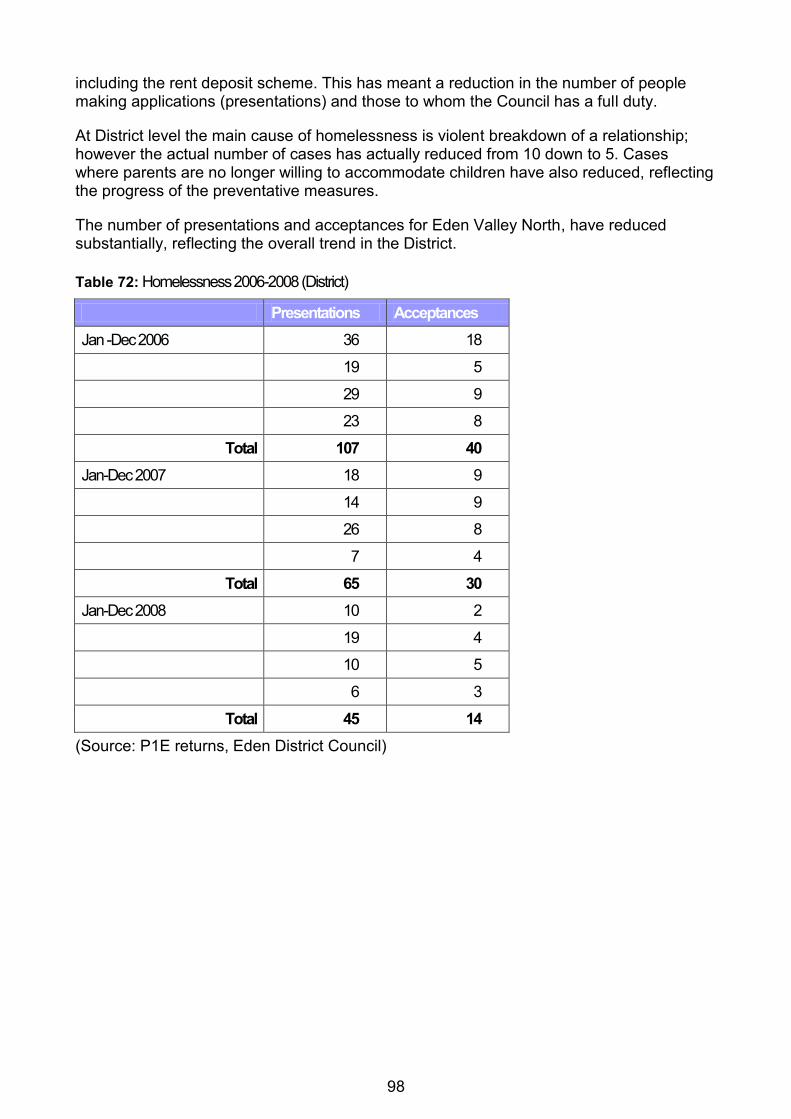

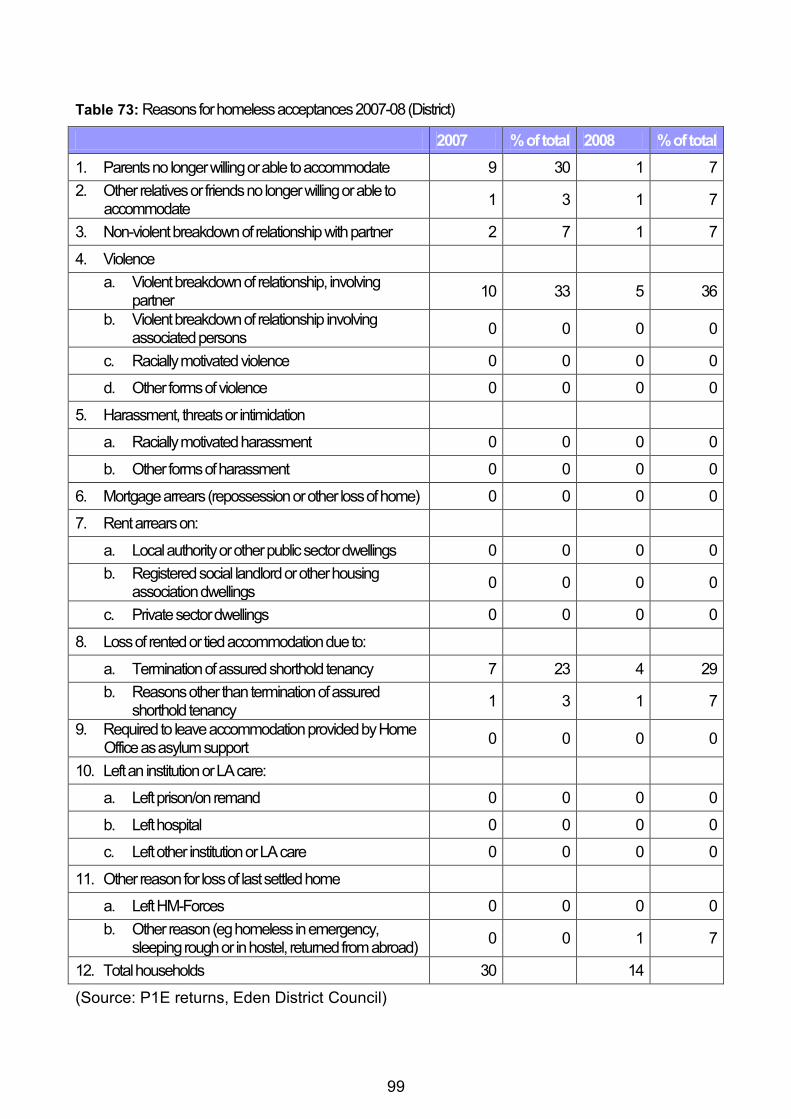

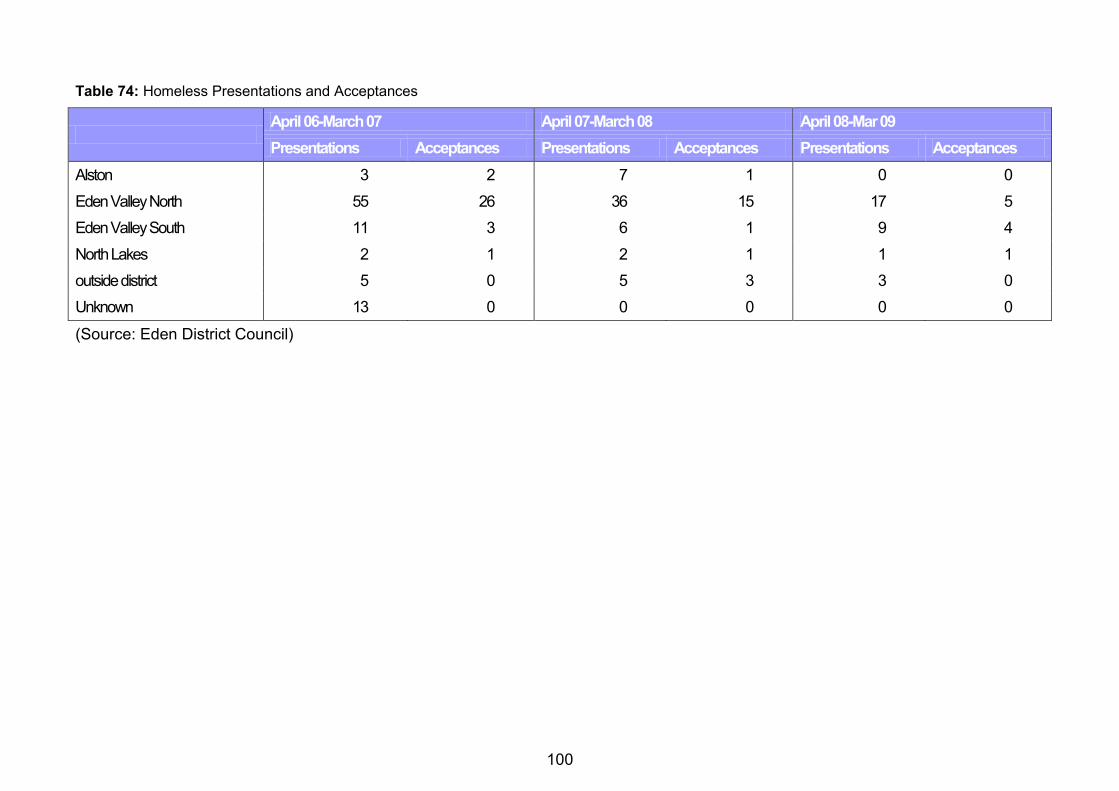

Homelessness ......................................................................................................... 97

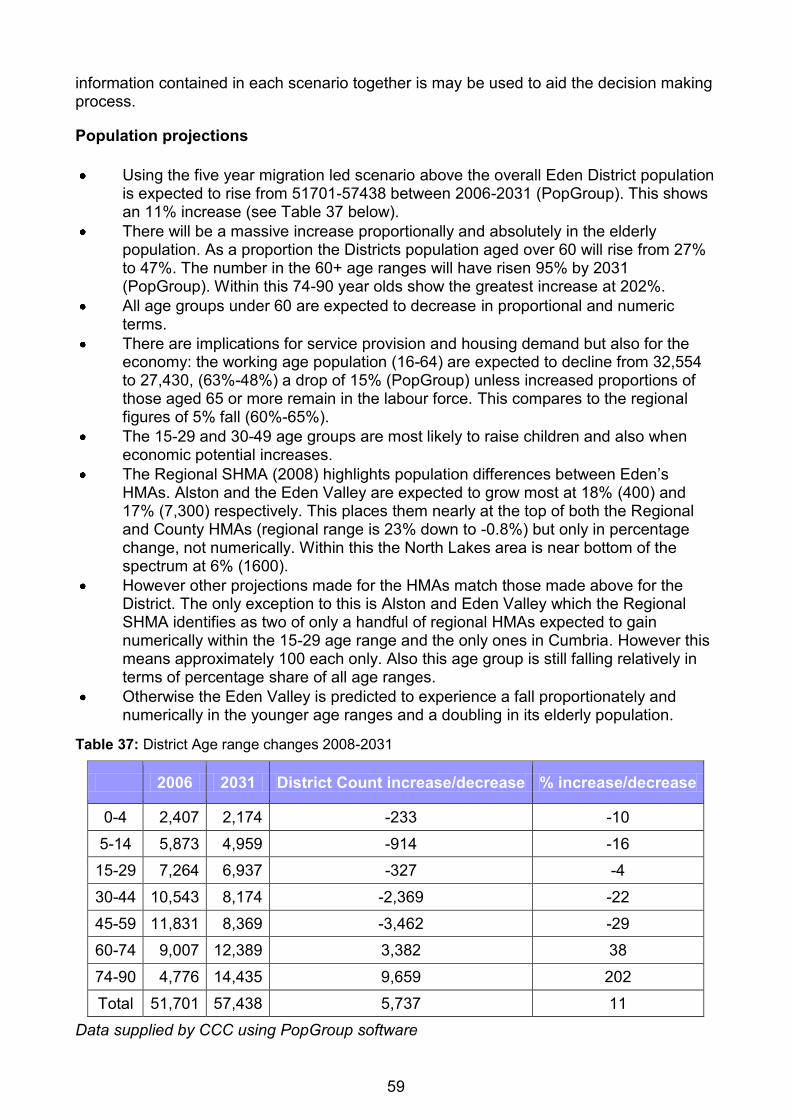

Report Conclusions - Bringing the Evidence Together ..................................... 98

Bibliography ..................................................................................................................... 103

List of Tables........................................................................................................ 104

List of Graphs ...................................................................................................... 106

Appendices .................................................................................................................... 107

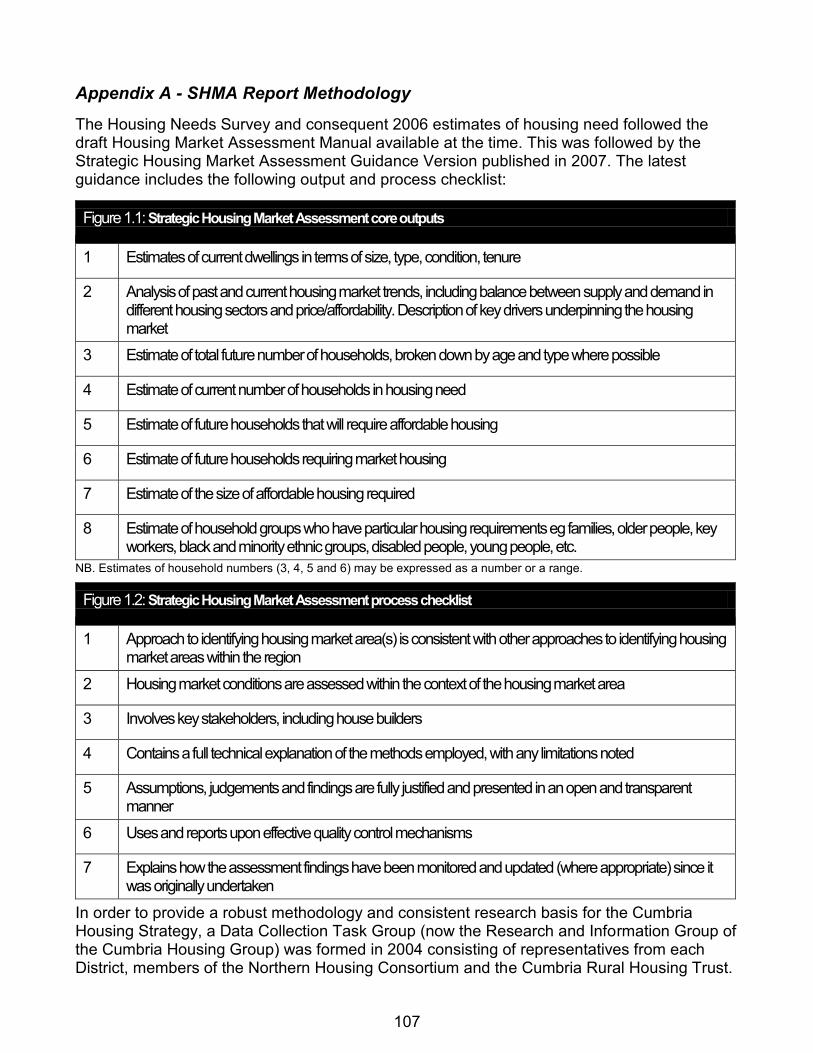

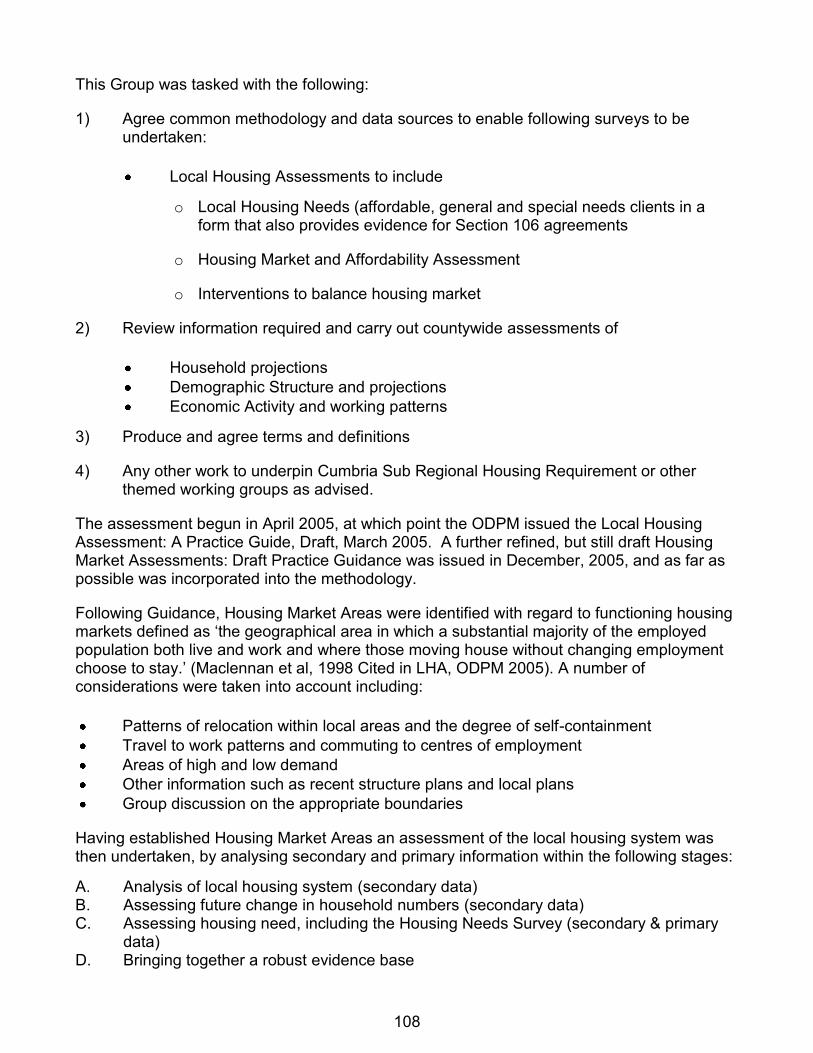

Appendix A - SHMA Report Methodology ............................................................. 107

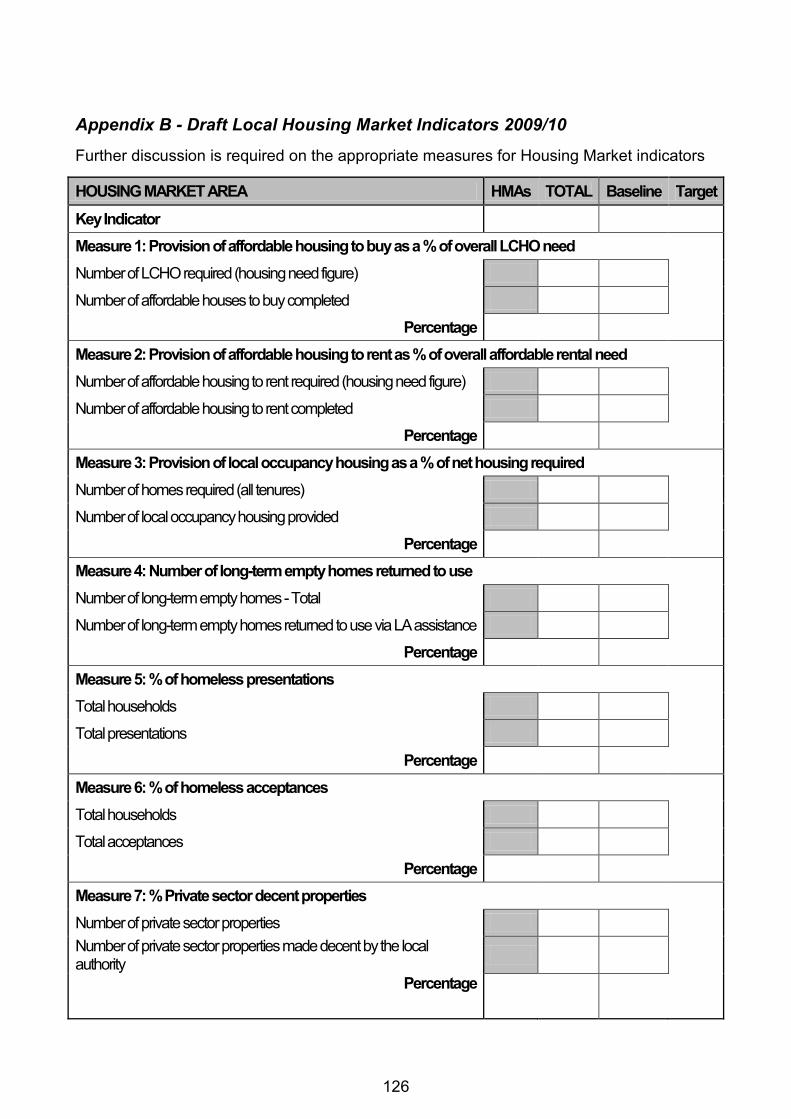

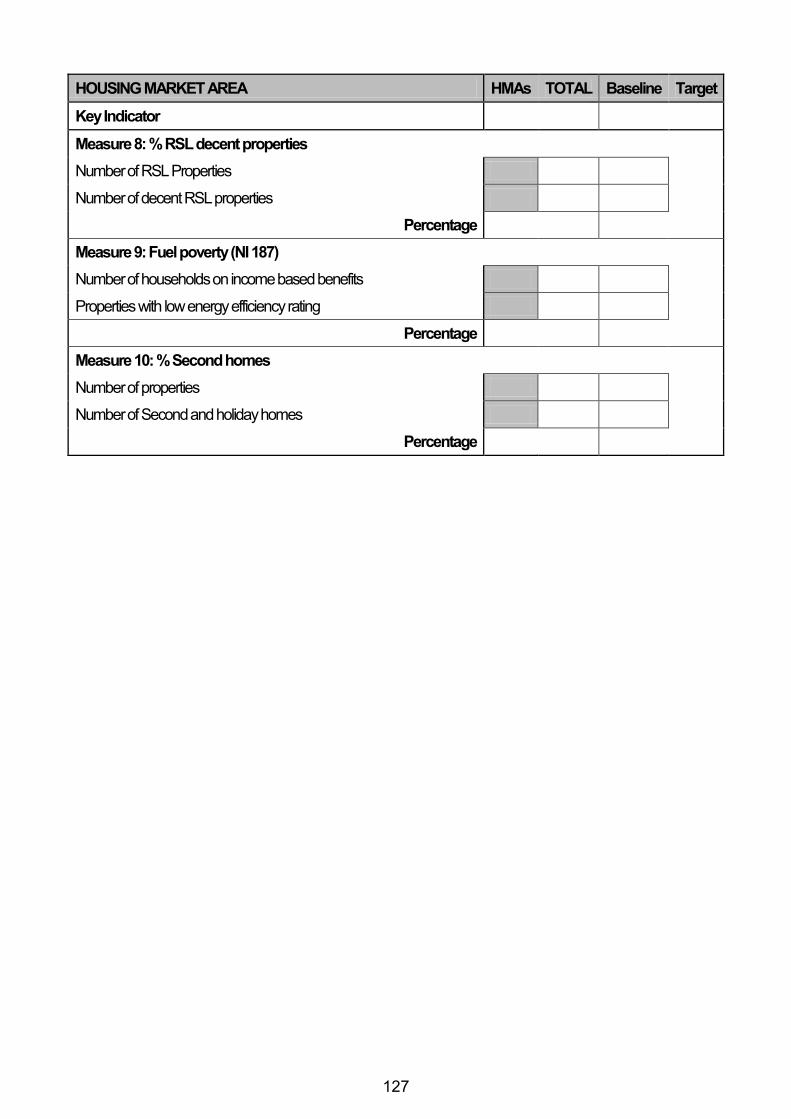

Appendix B - Draft Local Housing Market Indicators 2009-10 ............................... 125

Appendix C - Additional Tables ............................................................................. 127

Appendix D - Definition and types of affordable housing ....................................... 129

Appendix E - Key Aspirational Scenario Assumptions .......................................... 132

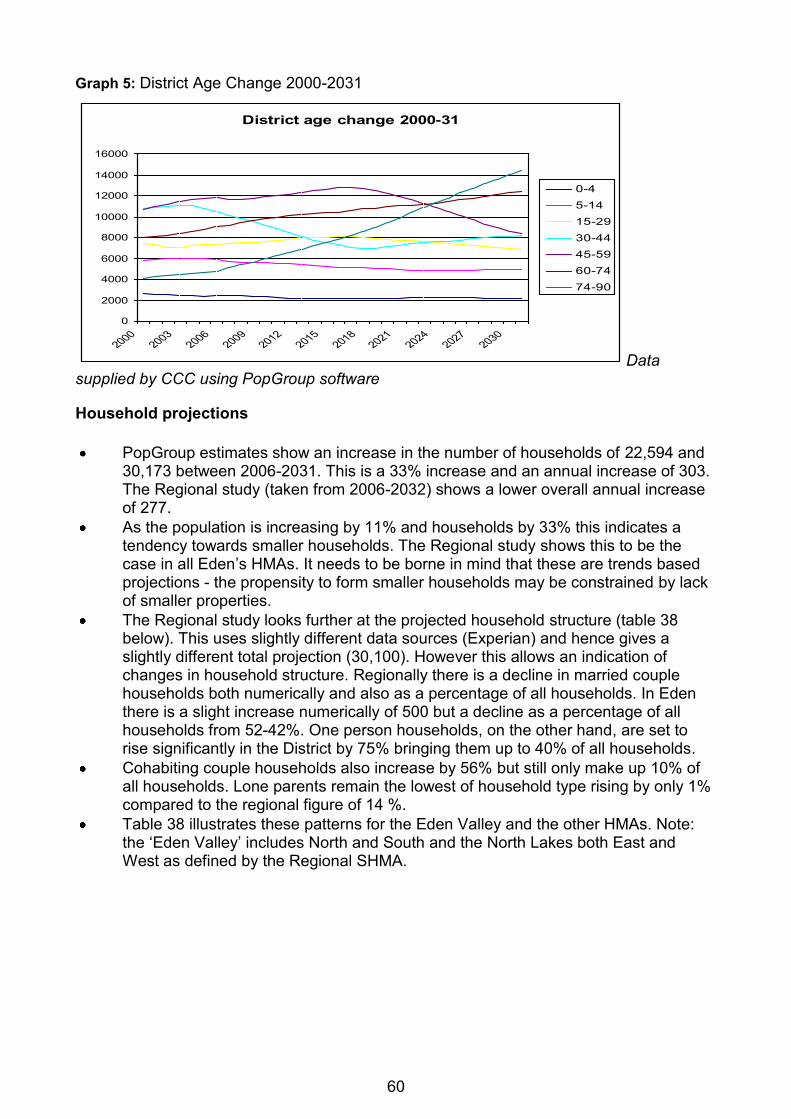

Appendix F - Bed Space Allowances used for the 2006 Housing Needs Survey .. 134

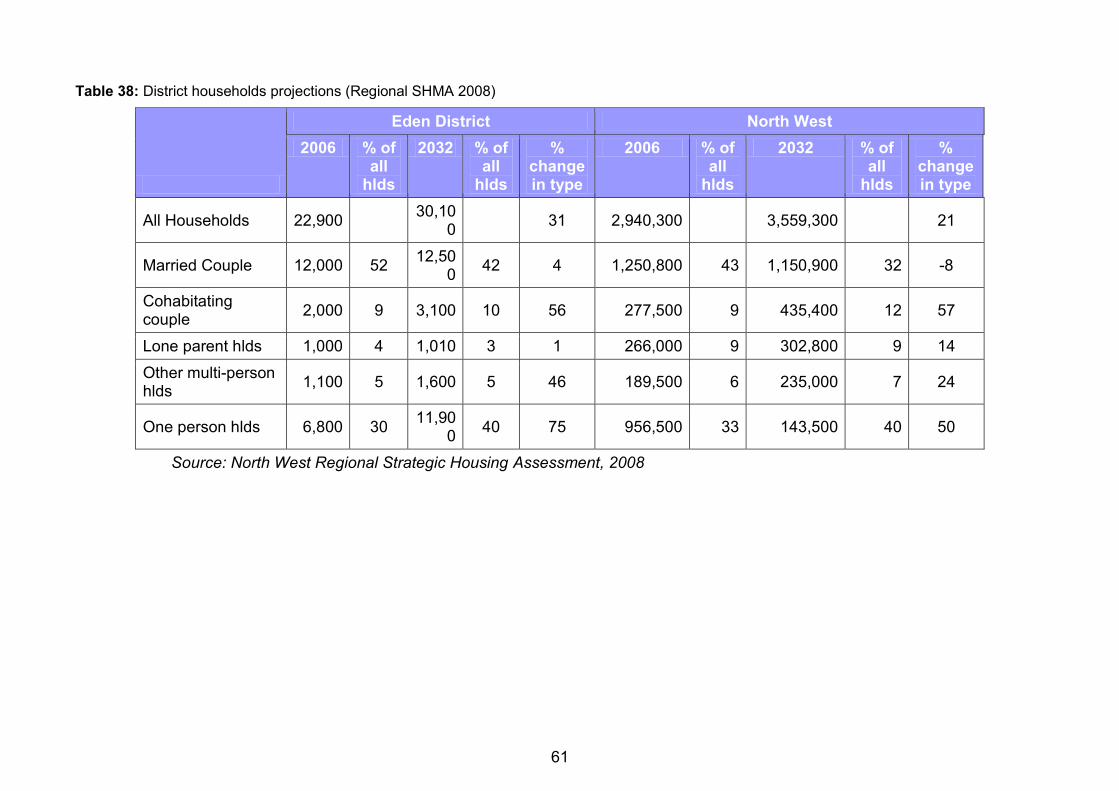

5

Acknowledgements

Paula Kennerley, Cumbria County Council

Stuart Frank, Cumbria Vision

Note to the Strategic Housing Market Assessment

The SHMA documents have been prepared jointly by each Cumbria district in consultation with local and county stakeholders and have been compiled using the Governments‟ Strategic Housing Market Assessments Practice Guidance Version 2, August 2007. The documents are not intended to provide definitive estimates of housing need, demand and market conditions. However they aim to provide insights into how housing markets operate both now and in the future. They are intended to allow an evidence base upon which to develop planning and housing policies by considering the characteristics of the housing market, how key factors work together and the probable scale of change in future housing needs and demand (SHMA Guidance, 2007, pp7-9).

To allow ease of reference each stage of the assessment follows the same order as the Guidance. Data sources occasionally differ from those recommended in the Guidance where they have been unavailable or where more robust up to date information has been accessed. The following analysis looks at the housing market area and provides information on the wider District and Cumbrian level where this adds contextual information. For a full methodology and checklist of core outputs and process please see appendix A.

Abbreviations

EDC Eden District Council

HMA Housing market area

LDNP/A Lake District National Park/Authority

SHMA Strategic housing market assessment

TTWs Travel to work areas

6

1. Current Market Profile

This diverse Housing Market Area is strongly influenced both by Carlisle, lying at its northern boundary and the Lake District National Park to the south west, in addition to the Districts main service centre of Penrith in the south of the HMA.

There are strong commuting and migration connections within the radius of Penrith with many who live in the town and its hinterland also working there, and it has been noted that Penrith is a sustainable market town with a high degree of self-containment1. Penrith is both a base for industry and commuters with road and rail links running directly through it. A high proportion of Service industries are based in the area, with distribution, hotels and restaurants making up 28% of all industries in addition to the high proportion of public administration, education and health services. There are a number of attractive rural settlements within commuter distance from Penrith and Carlisle, and with comparatively lower house prices to the Lakes National Park this has made it a popular location for home owners. However house price to income ratios are generally high and affordability remains a problem for many local people.

Headline Findings

Penrith is a sustainable market town with the majority of migration and travel to work patterns falling within a 30km radius of the town.

There is a skilled workforce but in poorly paid jobs within the District and also professional people who can afford to live here but choose to commute to work.

To ensure continued sustainability and economic development there is a requirement for social housing and intermediate housing, particularly „family‟ homes for current residents, to support a balance housing market.

Housing Needs Survey indicates a decline in demand for large properties in outlying villages and an affordable need for smaller two-three bed houses.

Targets

The following targets have been devised for this market area. In order to achieve these appropriate actions from the Cumbria Housing Strategy Action Plan will be applied.

50 units of affordable housing per year for the next two years to be reviewed thereafter.

A target relating to floating support will be identified during the Supporting People review of Floating Support.

A target relating to move on accommodation will be identified within the Cumbria Move On Strategy, 2007/08.

100% of all social housing decent by 2010.

70% of private sector housing providing homes for vulnerable people to meet Decent Homes Standard by 2010.

At least one empty property returned to use through empty property grants per year.

1 Penrith Housing Study, Land Use Consultants and Jacqueline Blenkinship, March 2006

7

Key Issues to be amended following consultation

Affordable Housing

Higher number of flats, terraces and right-to-buy properties in Penrith than outlying rural areas. Therefore:

Lowest entry level house price to income ratio for the District but wide variations in outlying rural settlements.

The overall ratio for this Housing Market Area remains high at 7x median income and 9x lower quartile income (2007) and unaffordable to those wishing to move up the property ladder

Lack of affordable social rented and intermediate housing particularly „family‟ housing.

Additional bottom rung affordable housing is required to support people in lower level jobs but affordable starter and move up accommodation is required for those living here and trapped on the bottom rung of the housing ladder.

Homelessness

Greatest number of homeless acceptances within the Eden District, mainly due to loss of rented accommodation.

Supported Housing

Support and lack of services within walking distance may become an increasing issue for the elderly within rural areas. With younger people finding it increasingly difficult to remain in villages the elderly may become more isolated.

Eden District wide issues include need for move-on accommodation to enable people to live independently and free up space in supported housing schemes across various client groups such as mental health.

General need for increased floating support.

Increased costs involved in providing services to rural areas - a particular concern due to the sparse rural nature of many areas in the Eden District.

Decent Homes

Plans in place to make 70% social housing decent by 2010.

Regeneration

New Squares/Southend Road development in Penrith town centre is currently under discussion.

Employment Needs amending following input from Economic Development:

The District as a whole has low unemployment and is a net exporter of labour.

Predominance of skilled trades and distribution/hotels/restaurant and public administration industries.

High demand for skilled and elementary occupations.

Evidence of higher paid professional commuting out of the District.

There are fewer „transport and communications‟ employers (6.5%) than would be expected given the main commuter routes running through the area.

8

Impact of Proposed Development

The majority of new affordable developments focus on local and key service centres.

Turnover in social rented stock and new permissions given for affordable new build are expected to supply 102 units.

New Squares/Southend Road development is currently under review. Currently twelve flats for social rent are due to begin February 2009 and further talks area underway regarding the rest of the site.

Whist the majority of need is within Penrith the size and type of units built need to be balanced to allow residents to meet their needs across a range of size, type and tenures.

Market Drivers

Large number of lower paid industries. Management positions are likely to be in the lower paid hotel and catering sector.

General perceptions, central location and proximity to the Lake District National Park make this market area an attractive location for both residents and businesses wishing to be based near access routes.

There is a good range of facilities (schools, health care, shops etc) in the main service town but a dependence on car ownership in rural areas

Housing affordability is an issue for newly forming households and families

9

2. Balanced Housing Market Indicators

A set of local housing market indicators are in the process of being developed to assess the extent to which a housing market is balanced. Proposed indicators are contained in appendix B. Further work is needed to ensure the indicators can be monitored regularly and the information collected consistently across Cumbria. This will need the co-operation of social registered landlords, strategy and planning departments in collecting the data at housing market level.

10

3. The Current Housing Market

Stage 1: The demographic and economic context

The aim of this chapter is to assess the current housing situation to see what is driving the housing system. This involves interpreting a wide range of data and trends to produce a picture of the housing situation and covers demographics, the policy context, labour force structure, characteristics of the housing stock, incomes and house prices.

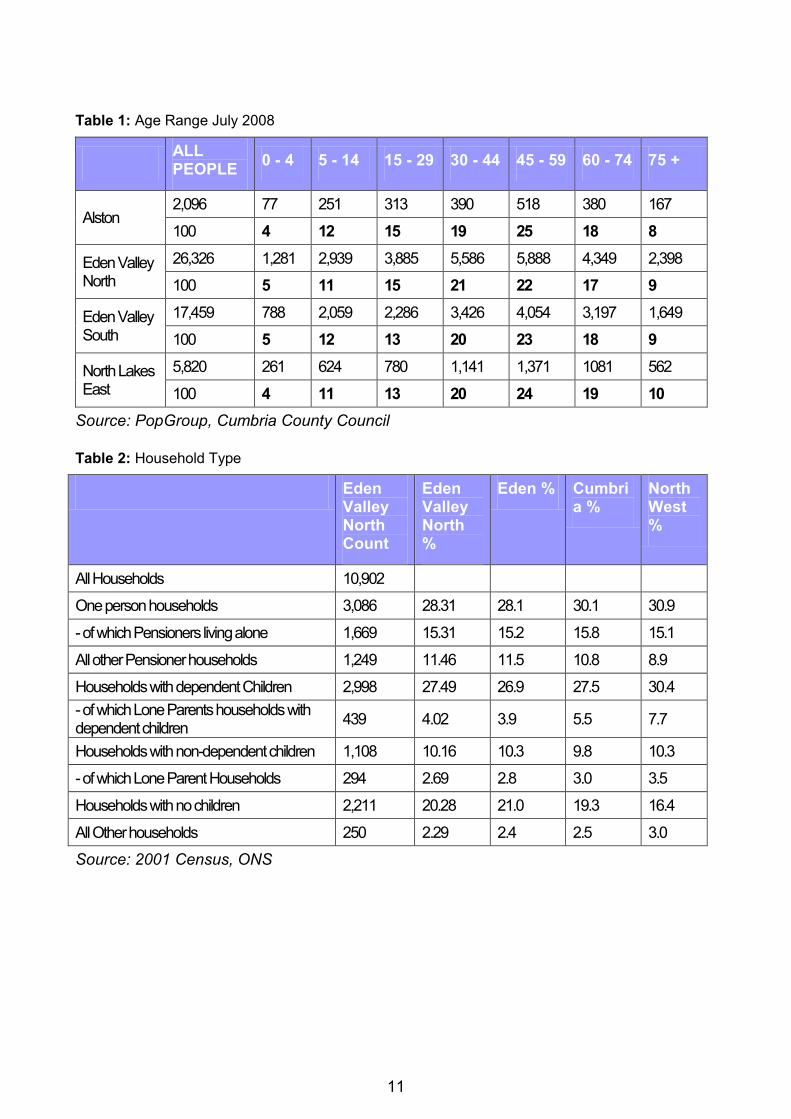

1.1 Demography and household types

The population in the District overall has been growing slowly: on average since 1991 there has been an increase of 0.74% per year which compares to the regional growth of 1.2% (PopGroup).

Eden Valley North contains the highest population of the Districts four housing market areas.

Currently the spread of age groups is skewed towards the middle aged and elderly with 69% aged over 30. The largest age group is 45-59.

The population aged over 60 currently stands at 26% compared to the regional figure of 24%.

The highest household type is one person households of which half are pensioners living alone.

The second highest household type is households with children. Within this the level of lone parent households is similar to Eden and Cumbria as a whole and remains lower than the regional average.

Households with no children are also higher than the regional average and similar to patterns for the Eden District and Council as a whole. There are also a higher number in the 15-29 age bracket than other HMAs which indicates that these are newly forming households who will require „first time‟ homes.

There are a greater proportion of ethnic groups in this HMA than the average for the Eden District; however it is likely that this is due to the influence of Penrith and Carlisle, and remains significantly lower than regionally or nationally - there are 11% fewer non-white British groups than the national figure.

11

Table 1: Age Range July 2008

ALL PEOPLE

0 - 4 5 - 14 15 - 29 30 - 44 45 - 59 60 - 74 75 +

Alston 2,096 77 251 313 390 518 380 167

100 4 12 15 19 25 18 8

Eden Valley North

26,326 1,281 2,939 3,885 5,586 5,888 4,349 2,398

100 5 11 15 21 22 17 9

Eden Valley South

17,459 788 2,059 2,286 3,426 4,054 3,197 1,649

100 5 12 13 20 23 18 9

North Lakes East

5,820 261 624 780 1,141 1,371 1081 562

100 4 11 13 20 24 19 10

Source: PopGroup, Cumbria County Council

Table 2: Household Type

Eden Valley North Count

Eden Valley North %

Eden % Cumbria %

North West %

All Households 10,902

One person households 3,086 28.31 28.1 30.1 30.9

- of which Pensioners living alone 1,669 15.31 15.2 15.8 15.1

All other Pensioner households 1,249 11.46 11.5 10.8 8.9

Households with dependent Children 2,998 27.49 26.9 27.5 30.4

- of which Lone Parents households with dependent children

439 4.02 3.9 5.5 7.7

Households with non-dependent children 1,108 10.16 10.3 9.8 10.3

- of which Lone Parent Households 294 2.69 2.8 3.0 3.5

Households with no children 2,211 20.28 21.0 19.3 16.4

All Other households 250 2.29 2.4 2.5 3.0

Source: 2001 Census, ONS

12

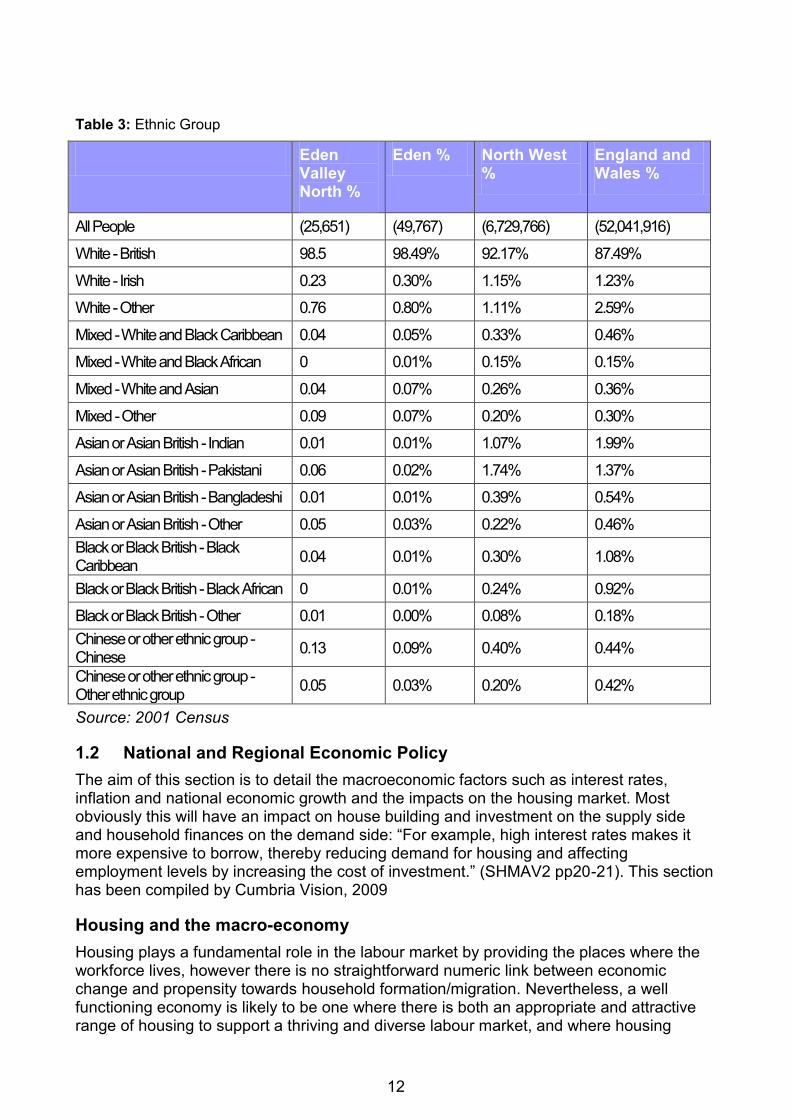

Table 3: Ethnic Group

Eden Valley North %

Eden % North West %

England and Wales %

All People (25,651) (49,767) (6,729,766) (52,041,916)

White - British 98.5 98.49% 92.17% 87.49%

White - Irish 0.23 0.30% 1.15% 1.23%

White - Other 0.76 0.80% 1.11% 2.59%

Mixed - White and Black Caribbean 0.04 0.05% 0.33% 0.46%

Mixed - White and Black African 0 0.01% 0.15% 0.15%

Mixed - White and Asian 0.04 0.07% 0.26% 0.36%

Mixed - Other 0.09 0.07% 0.20% 0.30%

Asian or Asian British - Indian 0.01 0.01% 1.07% 1.99%

Asian or Asian British - Pakistani 0.06 0.02% 1.74% 1.37%

Asian or Asian British - Bangladeshi 0.01 0.01% 0.39% 0.54%

Asian or Asian British - Other 0.05 0.03% 0.22% 0.46%

Black or Black British - Black Caribbean

0.04 0.01% 0.30% 1.08%

Black or Black British - Black African 0 0.01% 0.24% 0.92%

Black or Black British - Other 0.01 0.00% 0.08% 0.18%

Chinese or other ethnic group - Chinese

0.13 0.09% 0.40% 0.44%

Chinese or other ethnic group - Other ethnic group

0.05 0.03% 0.20% 0.42%

Source: 2001 Census

1.2 National and Regional Economic Policy

The aim of this section is to detail the macroeconomic factors such as interest rates, inflation and national economic growth and the impacts on the housing market. Most obviously this will have an impact on house building and investment on the supply side and household finances on the demand side: “For example, high interest rates makes it more expensive to borrow, thereby reducing demand for housing and affecting employment levels by increasing the cost of investment.” (SHMAV2 pp20-21). This section has been compiled by Cumbria Vision, 2009

Housing and the macro-economy

Housing plays a fundamental role in the labour market by providing the places where the workforce lives, however there is no straightforward numeric link between economic change and propensity towards household formation/migration. Nevertheless, a well functioning economy is likely to be one where there is both an appropriate and attractive range of housing to support a thriving and diverse labour market, and where housing

13

provision responds to changes in economic structure and performance. With this in mind, economic strategies and planning policy in the North West and across the UK now routinely highlight the impact that issues such as high prices, inadequate supply and poor quality housing might have on the capacity of an area to attract and retain a viable labour force.

National Context

Despite strong economic growth and broad stability since 1994/1995, current economic indications suggest that this position has changed significantly, brought about by high oil, utility and food costs, combined with a continued restriction on the availability of new mortgages brought on by the international „credit crunch‟ stemming from the USA, and the resultant loss of global business confidence. Most economists now agree that the UK economy will enter a recession in the forthcoming months, which could lead to increased levels of unemployment. As at September 2008, predictions are that average house prices will fall by up to 25%, and it will be 2010 before there may be signs of a recovery (Nationwide, September 2008). Other signals within the UK economy show that manufacturing output is declining as a further sign that the UK economy is entering a recession.

Recent news headlines would suggest that, with developers reducing staffing levels, the more alarming effects of the credit crunch, such as widespread job losses and large falls in land value are already being felt by the house building industry. Should a recession occur, it is likely that there would be further reductions in demand for housing, with resultant falls in house prices, until such time as a new equilibrium is reached between demand and supply and stability is achieved in the international markets. However, aside from the lending practices of major lenders, the underlying reasons behind the high house price inflation in recent years, is the fact that there has been insufficient housing provision to meet needs across the UK. Some economists predict that once the economy picks up again, there could be a further surge in house price inflation, which may be as serious as had been experienced in recent years. There is a need therefore to continue to build new houses in order to respond to underlying housing needs.

Monetary Policy

Interest rates reflect the effective cost of borrowing money and in the UK the base interest rate is set by the Bank of England‟s, Monetary Policy Committee (MPC). The Bank usually sets interest rates in order to try and meet an inflation target which is based on the Consumer Price Index (CPI) being equal to 2.0% ± 1. If inflation is forecast to rise above the target, the Bank is likely to raise interest rates in order to reduce spending in the economy, and therefore moderate inflationary pressures.

Following some significant price rises in the food and energy sectors over the last year, the CPI has soared above its target value peaking, in September, at 5.2%. However the CPI has now begun to fall back with the most recent data for January showing inflation at 3.1% (still well above the target value). Due largely to a recent fall in oil prices related to falling demand linked to declines in global production levels, inflation is currently expected to fall rapidly over the coming months.

Rather than responding impulsively in the short term, the Bank‟s overarching aim is to ensure inflation returns to target in the medium to long term. Thus principally as a result of the MPC‟s forecast that the currently high level of inflation is a temporary phenomenon, interest rates have remained low and below the 10 year average of 5.2%. Unsurprisingly, there are also a number of other factors which play an important role in the balancing act

14

between inflation and interest rates such as consumer confidence; time lags between rate changes and their effects on demand; the differential between the two rates and the ratio of fixed rate vs. variable rate mortgages (and in particular the proportion of sub-prime mortgages, where borrowers are paying a high proportion of their disposal income on repayments).

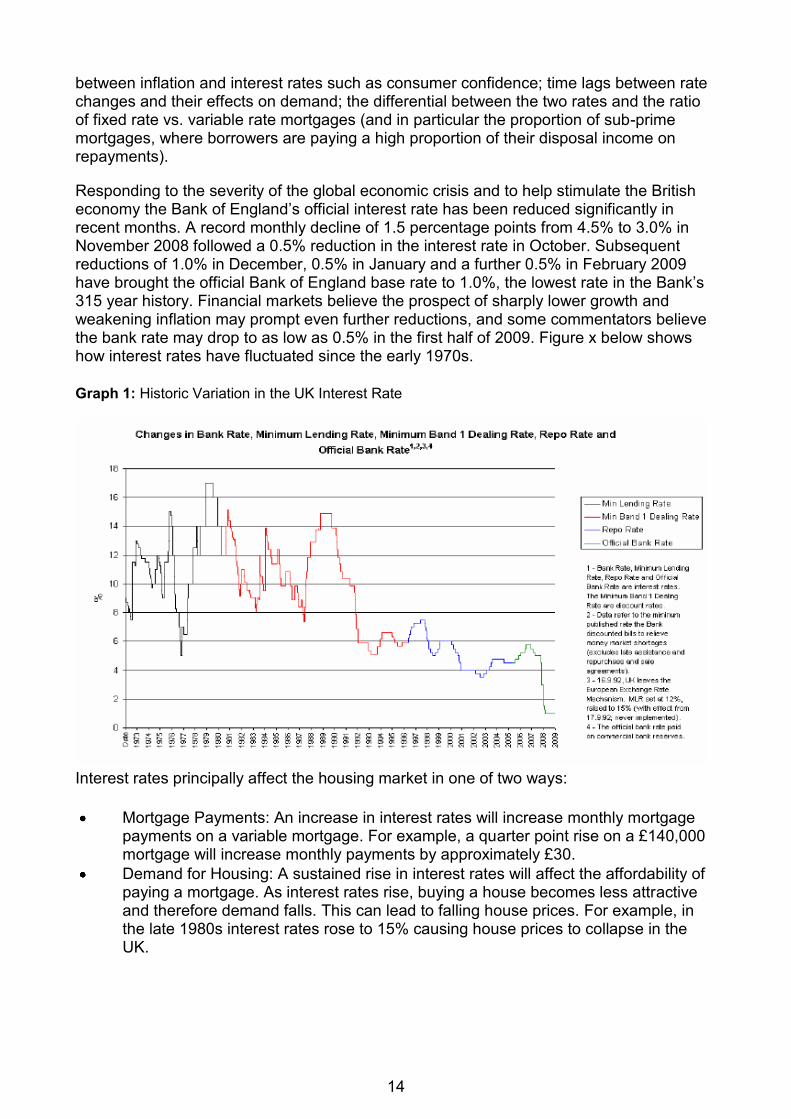

Responding to the severity of the global economic crisis and to help stimulate the British economy the Bank of England‟s official interest rate has been reduced significantly in recent months. A record monthly decline of 1.5 percentage points from 4.5% to 3.0% in November 2008 followed a 0.5% reduction in the interest rate in October. Subsequent reductions of 1.0% in December, 0.5% in January and a further 0.5% in February 2009 have brought the official Bank of England base rate to 1.0%, the lowest rate in the Bank‟s 315 year history. Financial markets believe the prospect of sharply lower growth and weakening inflation may prompt even further reductions, and some commentators believe the bank rate may drop to as low as 0.5% in the first half of 2009. Figure x below shows how interest rates have fluctuated since the early 1970s.

Graph 1: Historic Variation in the UK Interest Rate

Interest rates principally affect the housing market in one of two ways:

Mortgage Payments: An increase in interest rates will increase monthly mortgage payments on a variable mortgage. For example, a quarter point rise on a £140,000 mortgage will increase monthly payments by approximately £30.

Demand for Housing: A sustained rise in interest rates will affect the affordability of paying a mortgage. As interest rates rise, buying a house becomes less attractive and therefore demand falls. This can lead to falling house prices. For example, in the late 1980s interest rates rose to 15% causing house prices to collapse in the UK.

15

North West Regional Context

(Source: Northwest Regional Economic Forecasting Panel, Spring 2008)

The recent history of the regional economy includes a period of:

Very rapid jobs growth, especially between 2001 and 2004. This may be exceptional and unlikely to be seen again. It followed marked recent increases in public spending such that a third of the region‟s jobs are now in the public sector; and it also included the out-sourcing of jobs in financial and business services from higher cost places in the South, following a downturn in international financial markets in 2001.

Net migration shift, which explain why the region‟s population began to grow again from 2001. This also appears to have been closely related to this exceptional period of growth in job opportunities. While the growth in participation amongst men has remained low, a significant increase of the participation of women in the region‟s labour force appears to have been a further response to this same peak in job opportunities. Nevertheless, the underlying trend in the growth of jobs in the North West has still been running on average around 0.1 percentage points a year below that in the UK.

A fall in productivity, which accompanied the recent peak in jobs growth in the North West. Services now represent the bulk of jobs, and productivity levels in all broad service sectors in the region fell relative to the UK between 1995 and 2005. Also, there is little left of an advantage the region once enjoyed in the productivity stakes because of its once considerable concentration of employment in manufacturing, in which labour productivity, is generally higher than in services.

The relative decline in the region‟s productivity in services is attributed to:

A gradual fall in its price level relative to the UK, which is bound to have had a general effect on relative wages.

A shift in the balance between lower and higher level jobs in favour of the UK, and a widening disparity between earnings in higher-level jobs between London and other major cities, including Manchester and Liverpool. This effect has been particularly marked in top-end jobs in financial and business services, a sector that now provides almost half of GVA in London as against less than a fifth in the North West.

The output gap between the region and the UK has generally grown faster than the North West. The main influence has been the performance of London as a global city and as an international provider of high level services, together with consequential growth in the „super city region‟ around London. Its direct influence now expands into parts of the East Midlands, the West Midlands, and the South West, as well as into Eastern England and much of the South East.

16

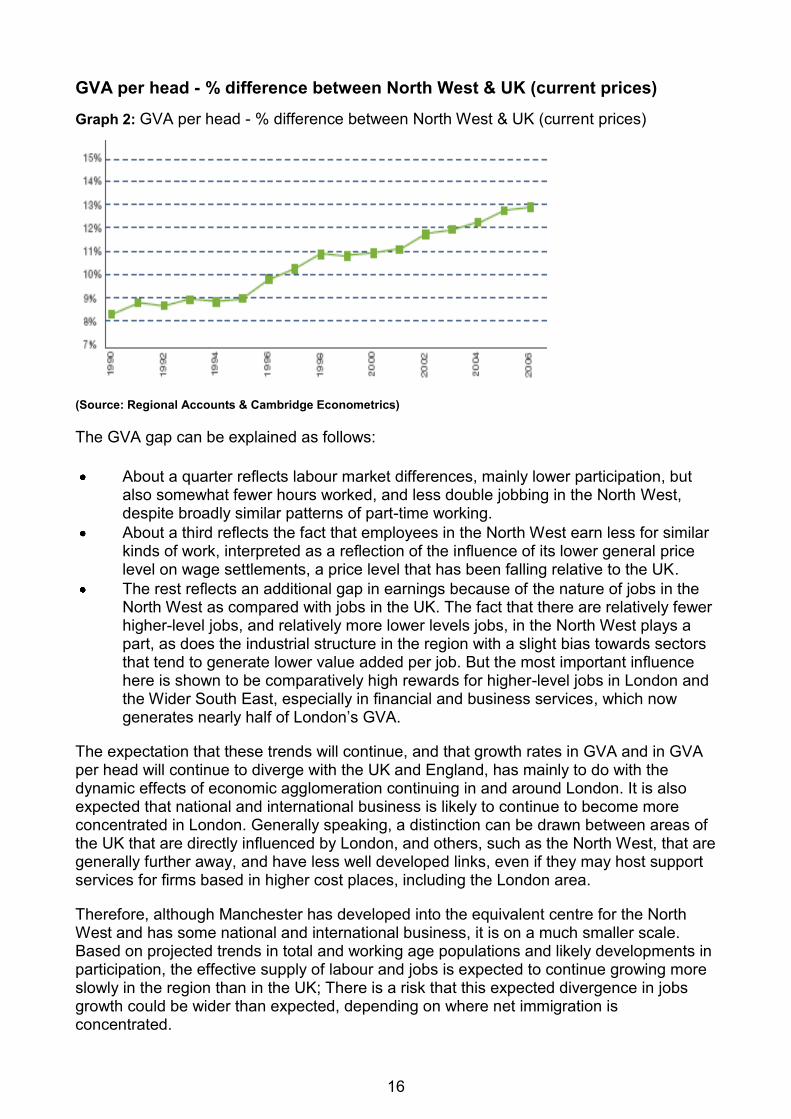

GVA per head - % difference between North West & UK (current prices)

Graph 2: GVA per head - % difference between North West & UK (current prices)

(Source: Regional Accounts & Cambridge Econometrics)

The GVA gap can be explained as follows:

About a quarter reflects labour market differences, mainly lower participation, but also somewhat fewer hours worked, and less double jobbing in the North West, despite broadly similar patterns of part-time working.

About a third reflects the fact that employees in the North West earn less for similar kinds of work, interpreted as a reflection of the influence of its lower general price level on wage settlements, a price level that has been falling relative to the UK.

The rest reflects an additional gap in earnings because of the nature of jobs in the North West as compared with jobs in the UK. The fact that there are relatively fewer higher-level jobs, and relatively more lower levels jobs, in the North West plays a part, as does the industrial structure in the region with a slight bias towards sectors that tend to generate lower value added per job. But the most important influence here is shown to be comparatively high rewards for higher-level jobs in London and the Wider South East, especially in financial and business services, which now generates nearly half of London‟s GVA.

The expectation that these trends will continue, and that growth rates in GVA and in GVA per head will continue to diverge with the UK and England, has mainly to do with the dynamic effects of economic agglomeration continuing in and around London. It is also expected that national and international business is likely to continue to become more concentrated in London. Generally speaking, a distinction can be drawn between areas of the UK that are directly influenced by London, and others, such as the North West, that are generally further away, and have less well developed links, even if they may host support services for firms based in higher cost places, including the London area.

Therefore, although Manchester has developed into the equivalent centre for the North West and has some national and international business, it is on a much smaller scale. Based on projected trends in total and working age populations and likely developments in participation, the effective supply of labour and jobs is expected to continue growing more slowly in the region than in the UK; There is a risk that this expected divergence in jobs growth could be wider than expected, depending on where net immigration is concentrated.

17

The central forecast of the most likely gap in GVA growth between the North West and the UK over the next twenty years is an average of 0.4 percentage points per annum, or a little more. The results of public policy initiatives are implicit in these trends and the Forecasting Panel think change is unlikely mainly because many programmes are similar to those that have been in place for some time and economic performance seems to have been driven mainly by structural change responding to market forces. This may change if firms and other bodies in the region take increased advantage of strategic opportunities in which the region has strengths (for instance in nuclear, energy, and environment-related industries) and if we saw public policy concentrating an increased proportion of resources on growth, especially on accommodating and underpinning agglomeration through appropriate policies, such as transport and housing.

It is nonetheless implicit in this view that the North West‟s economy will continue to grow more rapidly than in the 1990s, and also that living standards in the region will continue to improve on average even if the gap in GVA per head is expected to widen. Although the North West‟s growth corridor may flourish, and its influence will spread geographically, especially given effective transport and spatial policies, the corridor is simply different in character and scale, and less of an integrated whole at present, than is London and its surroundings.

Construction and Housing

Since the first quarter of 2007 the rate of increase in house prices in the region has declined, while in the final quarter of the year house price inflation in the UK declined for the first time in two years. Along with a fall in the numbers of housing transactions, this confirms that the housing market is weakening. The most recent national data to September 2008 shows that the annual rate at which house prices are falling continued to accelerate to hit a new record of 5.1 per cent. However, homes lost only 0.1 per cent of their value during September itself, well down on August's drop of 2.7 per cent.

Construction: Growth in 2007 was sustained by private commercial orders

Construction orders in the North West increased through the first half of 2007, but have since fallen back. In 2007 private sector new housing orders declined to below 2005 levels. However, the level of infrastructure and other public orders increased. Private industrial orders remained relatively unchanged from 2006; growth in private commercial orders was much more marked in the first half of the year, although they have since fallen back.

The value of construction output in 2007 was 12.8% higher than in 2006, due primarily to new public housing and other private sector repair and maintenance. Private commercial and industrial output growth more than offset a decline in infrastructure output.

GVA growth in construction was weak in 2006 at 1.0% but is estimated to have strengthened to 2.1% in 2007, although this was weaker than in the UK as a whole. Weaker growth is expected in 2008; 1.5% for the North West and 1.0% for the UK. GVA is then expected to fall in 2009 in response to the impact of the credit crisis and the weakening housing market, before recovering in 2010 and 2011.

18

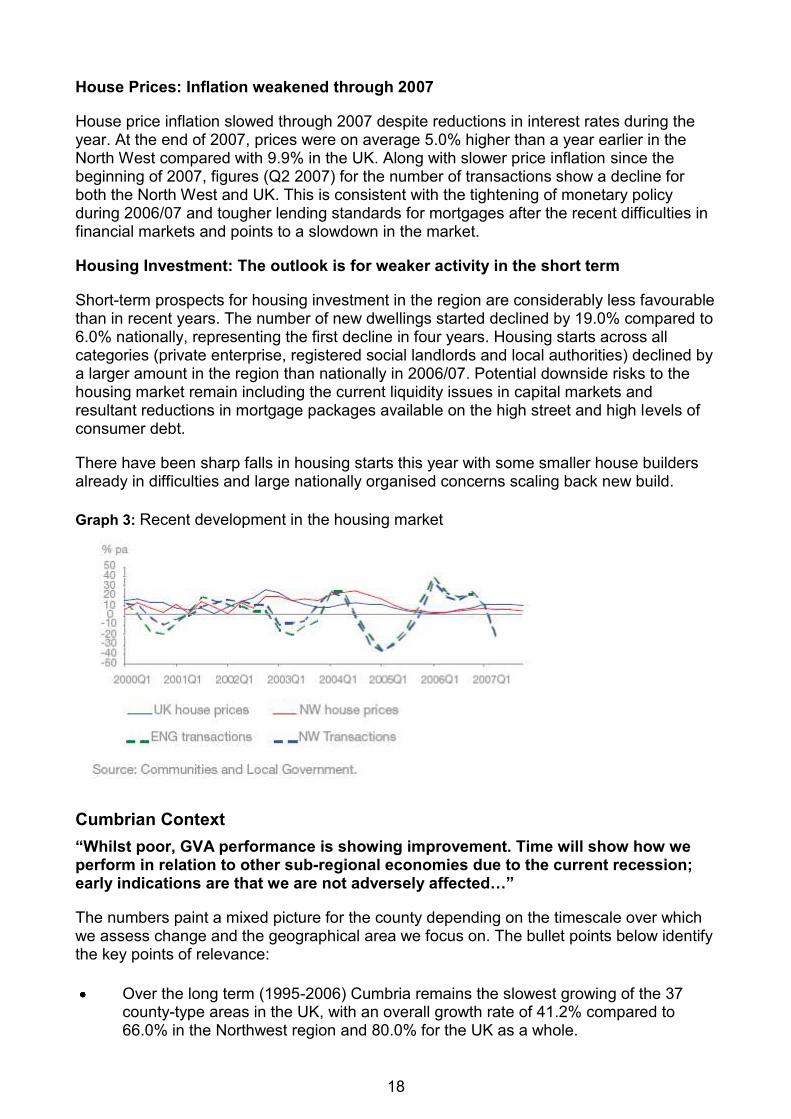

House Prices: Inflation weakened through 2007

House price inflation slowed through 2007 despite reductions in interest rates during the year. At the end of 2007, prices were on average 5.0% higher than a year earlier in the North West compared with 9.9% in the UK. Along with slower price inflation since the beginning of 2007, figures (Q2 2007) for the number of transactions show a decline for both the North West and UK. This is consistent with the tightening of monetary policy during 2006/07 and tougher lending standards for mortgages after the recent difficulties in financial markets and points to a slowdown in the market.

Housing Investment: The outlook is for weaker activity in the short term

Short-term prospects for housing investment in the region are considerably less favourable than in recent years. The number of new dwellings started declined by 19.0% compared to 6.0% nationally, representing the first decline in four years. Housing starts across all categories (private enterprise, registered social landlords and local authorities) declined by a larger amount in the region than nationally in 2006/07. Potential downside risks to the housing market remain including the current liquidity issues in capital markets and resultant reductions in mortgage packages available on the high street and high levels of consumer debt.

There have been sharp falls in housing starts this year with some smaller house builders already in difficulties and large nationally organised concerns scaling back new build.

Graph 3: Recent development in the housing market

Cumbrian Context

“Whilst poor, GVA performance is showing improvement. Time will show how we perform in relation to other sub-regional economies due to the current recession; early indications are that we are not adversely affected…”

The numbers paint a mixed picture for the county depending on the timescale over which we assess change and the geographical area we focus on. The bullet points below identify the key points of relevance:

Over the long term (1995-2006) Cumbria remains the slowest growing of the 37 county-type areas in the UK, with an overall growth rate of 41.2% compared to 66.0% in the Northwest region and 80.0% for the UK as a whole.

19

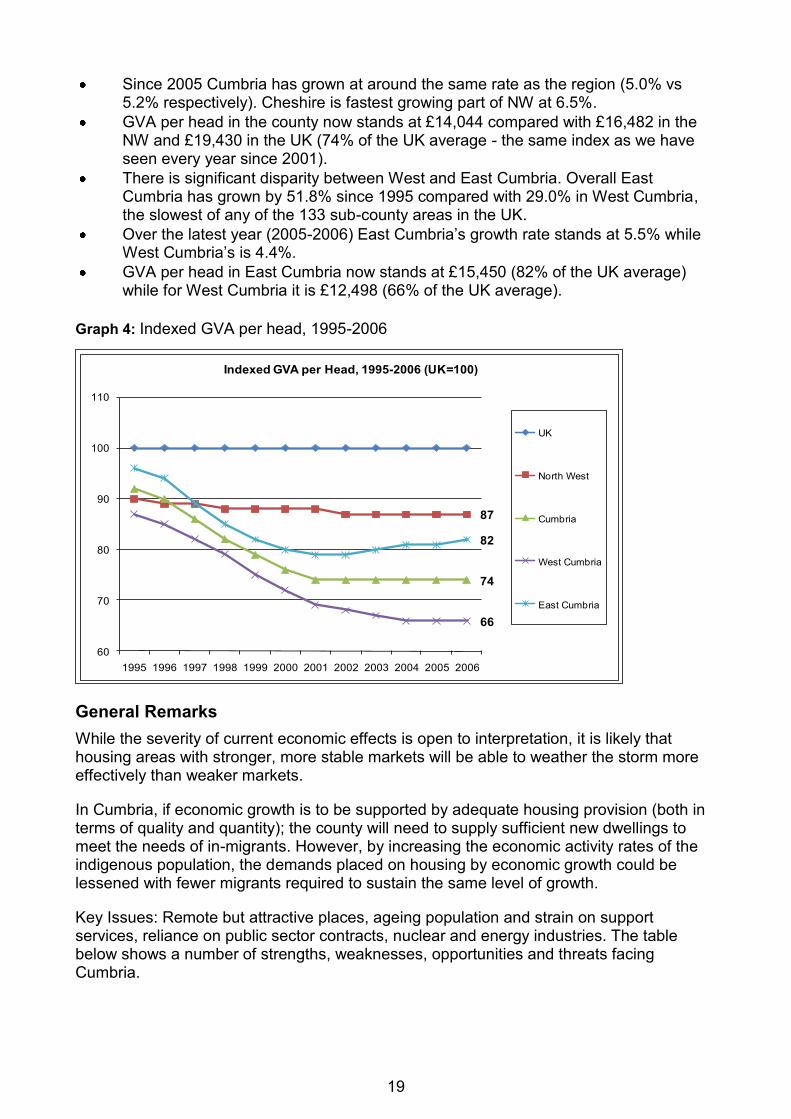

Since 2005 Cumbria has grown at around the same rate as the region (5.0% vs 5.2% respectively). Cheshire is fastest growing part of NW at 6.5%.

GVA per head in the county now stands at £14,044 compared with £16,482 in the NW and £19,430 in the UK (74% of the UK average - the same index as we have seen every year since 2001).

There is significant disparity between West and East Cumbria. Overall East Cumbria has grown by 51.8% since 1995 compared with 29.0% in West Cumbria, the slowest of any of the 133 sub-county areas in the UK.

Over the latest year (2005-2006) East Cumbria‟s growth rate stands at 5.5% while West Cumbria‟s is 4.4%.

GVA per head in East Cumbria now stands at £15,450 (82% of the UK average) while for West Cumbria it is £12,498 (66% of the UK average).

Graph 4: Indexed GVA per head, 1995-2006

87

74

66

82

60

70

80

90

100

110

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Indexed GVA per Head, 1995-2006 (UK=100)

UK

North West

Cumbria

West Cumbria

East Cumbria

General Remarks

While the severity of current economic effects is open to interpretation, it is likely that housing areas with stronger, more stable markets will be able to weather the storm more effectively than weaker markets.

In Cumbria, if economic growth is to be supported by adequate housing provision (both in terms of quality and quantity); the county will need to supply sufficient new dwellings to meet the needs of in-migrants. However, by increasing the economic activity rates of the indigenous population, the demands placed on housing by economic growth could be lessened with fewer migrants required to sustain the same level of growth.

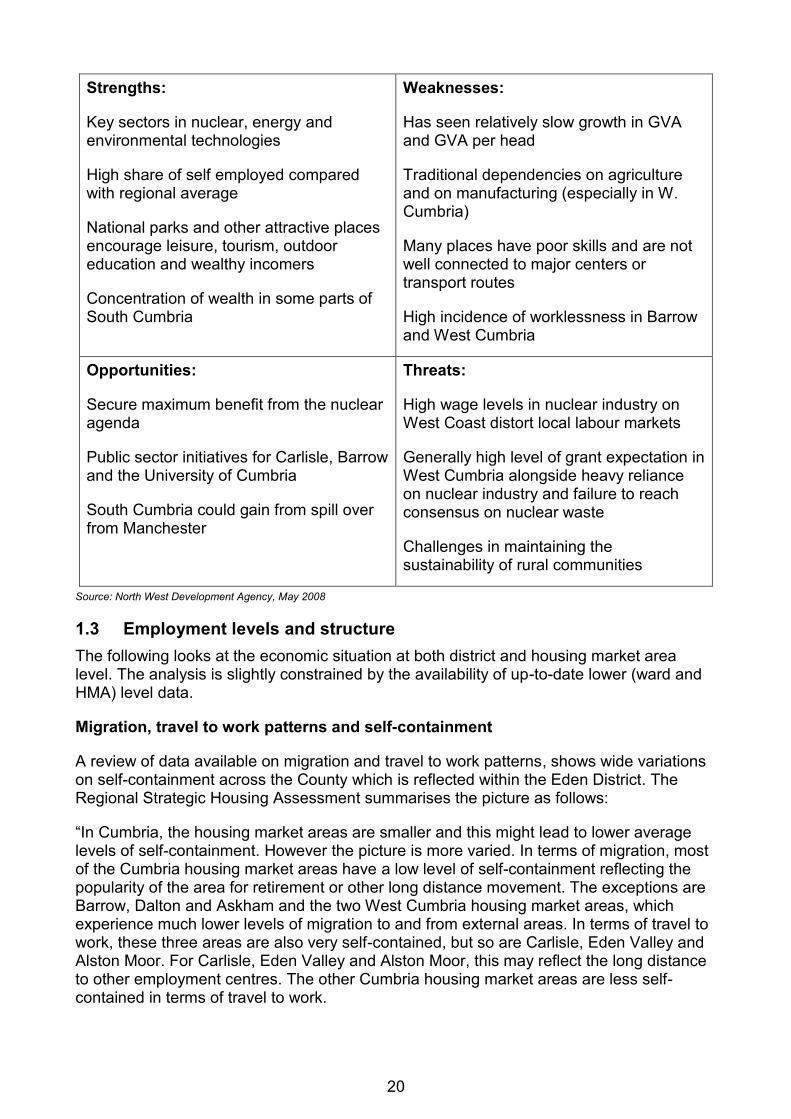

Key Issues: Remote but attractive places, ageing population and strain on support services, reliance on public sector contracts, nuclear and energy industries. The table below shows a number of strengths, weaknesses, opportunities and threats facing Cumbria.

20

Strengths:

Key sectors in nuclear, energy and environmental technologies

High share of self employed compared with regional average

National parks and other attractive places encourage leisure, tourism, outdoor education and wealthy incomers

Concentration of wealth in some parts of South Cumbria

Weaknesses:

Has seen relatively slow growth in GVA and GVA per head

Traditional dependencies on agriculture and on manufacturing (especially in W. Cumbria)

Many places have poor skills and are not well connected to major centers or transport routes

High incidence of worklessness in Barrow and West Cumbria

Opportunities:

Secure maximum benefit from the nuclear agenda

Public sector initiatives for Carlisle, Barrow and the University of Cumbria

South Cumbria could gain from spill over from Manchester

Threats:

High wage levels in nuclear industry on West Coast distort local labour markets

Generally high level of grant expectation in West Cumbria alongside heavy reliance on nuclear industry and failure to reach consensus on nuclear waste

Challenges in maintaining the sustainability of rural communities

Source: North West Development Agency, May 2008

1.3 Employment levels and structure

The following looks at the economic situation at both district and housing market area level. The analysis is slightly constrained by the availability of up-to-date lower (ward and HMA) level data.

Migration, travel to work patterns and self-containment

A review of data available on migration and travel to work patterns, shows wide variations on self-containment across the County which is reflected within the Eden District. The Regional Strategic Housing Assessment summarises the picture as follows:

“In Cumbria, the housing market areas are smaller and this might lead to lower average levels of self-containment. However the picture is more varied. In terms of migration, most of the Cumbria housing market areas have a low level of self-containment reflecting the popularity of the area for retirement or other long distance movement. The exceptions are Barrow, Dalton and Askham and the two West Cumbria housing market areas, which experience much lower levels of migration to and from external areas. In terms of travel to work, these three areas are also very self-contained, but so are Carlisle, Eden Valley and Alston Moor. For Carlisle, Eden Valley and Alston Moor, this may reflect the long distance to other employment centres. The other Cumbria housing market areas are less self-contained in terms of travel to work.

21

“In terms of linkages with other areas, because of its geographic position, Barrow, Dalton and Askham have strong links only with Ulverston/Cartmel. The West Cumbria housing market areas tend to have links with one another, and to some extent with Carlisle. For the remainder of Cumbria, there is a north-south split, with stronger links between Central Lakes, Dales/Rural Kendal and outside the sub region Lancaster, and a separate grouping of Eden Valley, North Lakes, Alston Moor and Carlisle.” (RSHA p32).

This self-containment is also present in migration patterns across the county:

“Geographical patterns of migration in Cumbria exhibit similar characteristics to that which we might expect; namely, most moves are of short distance and there is an inverse relationship between the magnitude of individual flows and the distance travelled…. Of the 814 flows involving Cumbria and/or other parts of the North West, 799 were moves within Cumbria, six were from Cumbria to Lancashire, five were from Lancashire to Cumbria and four were from Greater Manchester to Cumbria. Within Cumbria itself, there is a clear „geometry‟ of migration centred on key locations such as Carlisle, Penrith, Workington and Maryport, Whitehaven, Barrow-in-Furness, Windermere, and Kendal. Overall, the data suggests that there is a high degree of „self-containment‟ whereby these locations function as relatively independent housing market areas.” (Cumbria Economic Bulletin, 2007)

Analysis in March 2008 at county and district level tends to confirm “spatially coincident housing and labour market…. with a high degree of home to work trip self-containment” (Stephen Hincks, Cumbria Economic Bulletin, 2008). However the same analysis also showed that Cumbria also has longer distance commuting (ie over 30km in length), of which Eden has a relatively high share. This might reflect the fact that some residents in Cumbria need to travel greater distances to access employment opportunities and the connections between Penrith and Carlisle for the Eden District.

There are strong commuting and migration connections within the radius of Penrith with many who live in the town and its hinterland also working there, and it has been noted that Penrith is a sustainable market town with a high degree of self-containment2. However the picture is clearly varied with higher degrees of migration and travel to work depending on the specific area‟s attractiveness and availability of suitable employment. Further evidence derived from the 2001 Census showed that overall Eden is a net exporter of labour, with 827 more employed residents than workforce compared to Carlisle which in a net importer of labour of 5,801 (Cumbria Economic Bulletin, Sept 2004). This may have policy implications if we wish to look at expanding our economy, cut commuting patterns and encourage people to both live and work in the district.

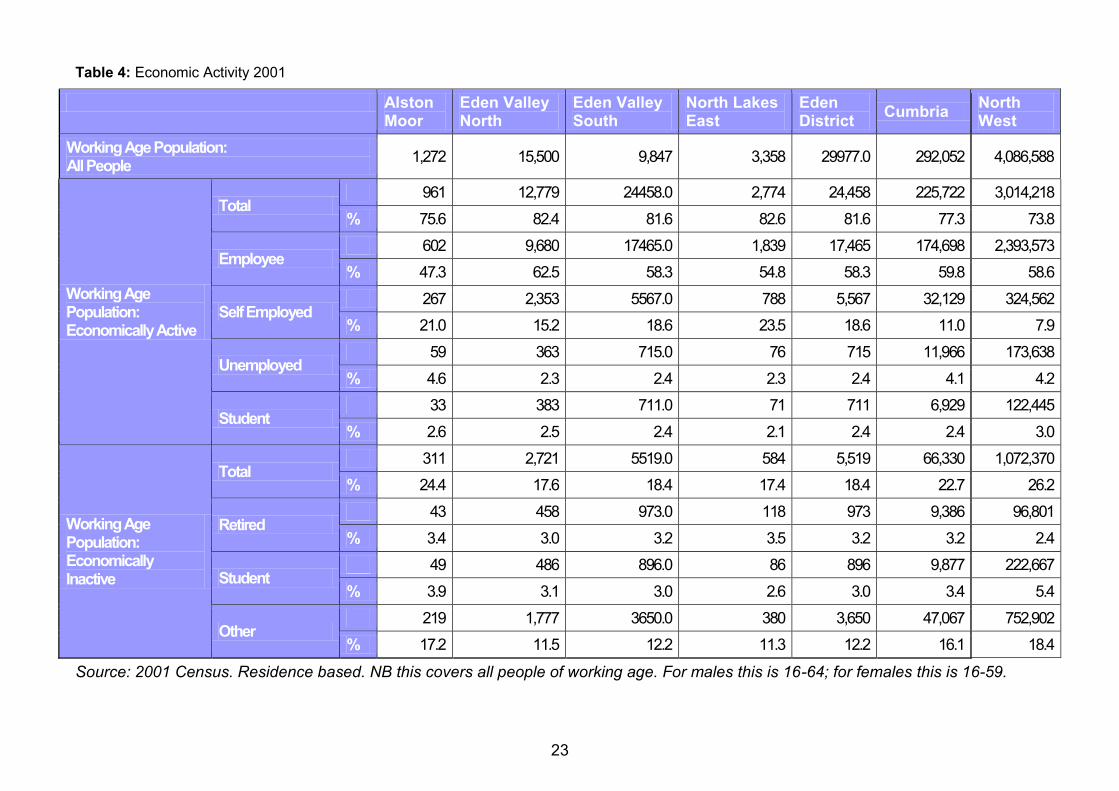

Economic Activity3

Data from 2001 (table 4) showed Eden District to have a higher than county and regional figures for the total working age population economically active and living in the district. While there was a slightly lower percent of employees, there is a much higher percentage of self-employed.

Looking at economic activity at HMA level, 2001 data (Census) showed that Eden Valley North had a higher percentage of economically active residents (total) than both county

2 Penrith Housing Study, Land Use Consultants and Jacqueline Blenkinship, March 2006

3 „Economic Activity‟ is available up to 2006-07 through the Labour Force Survey at district level only, however the sample was too

low to be reliable, while housing market level data is only available for 2001 and from the Census.

22

and regional levels. This was the second highest percentage in the District and the area contained by far the highest number of working age residents (15,500), reflecting both larger population and the ability to commute to the main employment hubs of Penrith and Carlisle. Conversely the area contained the second lowest percentage of economically inactive residents and the lowest percentage of retired people (of working age) in the District. Economically inactive includes those looking after a house, those in retirement but also includes those without work who are not actively seeking or available for employment. The HMA contains the highest number of self-employed people but this was still the lowest percentage in the District, and highlights Eden‟s overall higher than Regional and County levels. Unemployment was typical of the District and lower than the County and Regional percentages. Containing Newton Rigg University campus and the higher number of buy-to-let properties in Penrith this area also contained the concentration of students in the District. This figure is set to increase with the forthcoming expansion of the University (see chapter 6 „Requirements of Specific Household Groups‟).

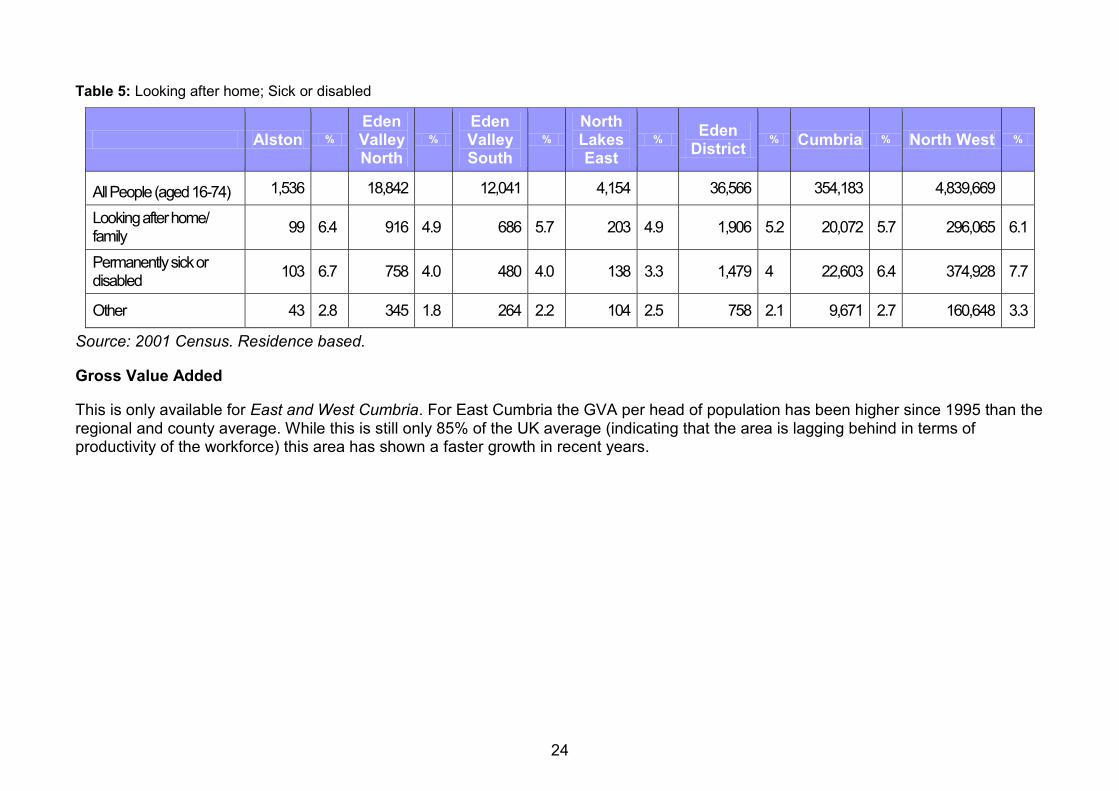

Looking specifically at those looking after the home or sick/disabled (table 5) there were a lower percentage of this group than County and Regional levels, although this was similar to the District picture.

23

Table 4: Economic Activity 2001

Alston Moor

Eden Valley North

Eden Valley South

North Lakes East

Eden District

Cumbria North West

Working Age Population: All People

1,272 15,500 9,847 3,358 29977.0 292,052 4,086,588

Working Age Population: Economically Active

Total 961 12,779 24458.0 2,774 24,458 225,722 3,014,218

% 75.6 82.4 81.6 82.6 81.6 77.3 73.8

Employee 602 9,680 17465.0 1,839 17,465 174,698 2,393,573

% 47.3 62.5 58.3 54.8 58.3 59.8 58.6

Self Employed 267 2,353 5567.0 788 5,567 32,129 324,562

% 21.0 15.2 18.6 23.5 18.6 11.0 7.9

Unemployed 59 363 715.0 76 715 11,966 173,638

% 4.6 2.3 2.4 2.3 2.4 4.1 4.2

Student 33 383 711.0 71 711 6,929 122,445

% 2.6 2.5 2.4 2.1 2.4 2.4 3.0

Working Age Population: Economically Inactive

Total 311 2,721 5519.0 584 5,519 66,330 1,072,370

% 24.4 17.6 18.4 17.4 18.4 22.7 26.2

Retired 43 458 973.0 118 973 9,386 96,801

% 3.4 3.0 3.2 3.5 3.2 3.2 2.4

Student 49 486 896.0 86 896 9,877 222,667

% 3.9 3.1 3.0 2.6 3.0 3.4 5.4

Other 219 1,777 3650.0 380 3,650 47,067 752,902

% 17.2 11.5 12.2 11.3 12.2 16.1 18.4

Source: 2001 Census. Residence based. NB this covers all people of working age. For males this is 16-64; for females this is 16-59.

24

Table 5: Looking after home; Sick or disabled

Alston % Eden Valley North

% Eden Valley South

% North Lakes East

% Eden District

% Cumbria % North West %

All People (aged 16-74) 1,536 18,842 12,041 4,154 36,566 354,183 4,839,669

Looking after home/ family

99 6.4 916 4.9 686 5.7 203 4.9 1,906 5.2 20,072 5.7 296,065 6.1

Permanently sick or disabled

103 6.7 758 4.0 480 4.0 138 3.3 1,479 4 22,603 6.4 374,928 7.7

Other 43 2.8 345 1.8 264 2.2 104 2.5 758 2.1 9,671 2.7 160,648 3.3

Source: 2001 Census. Residence based.

Gross Value Added

This is only available for East and West Cumbria. For East Cumbria the GVA per head of population has been higher since 1995 than the regional and county average. While this is still only 85% of the UK average (indicating that the area is lagging behind in terms of productivity of the workforce) this area has shown a faster growth in recent years.

25

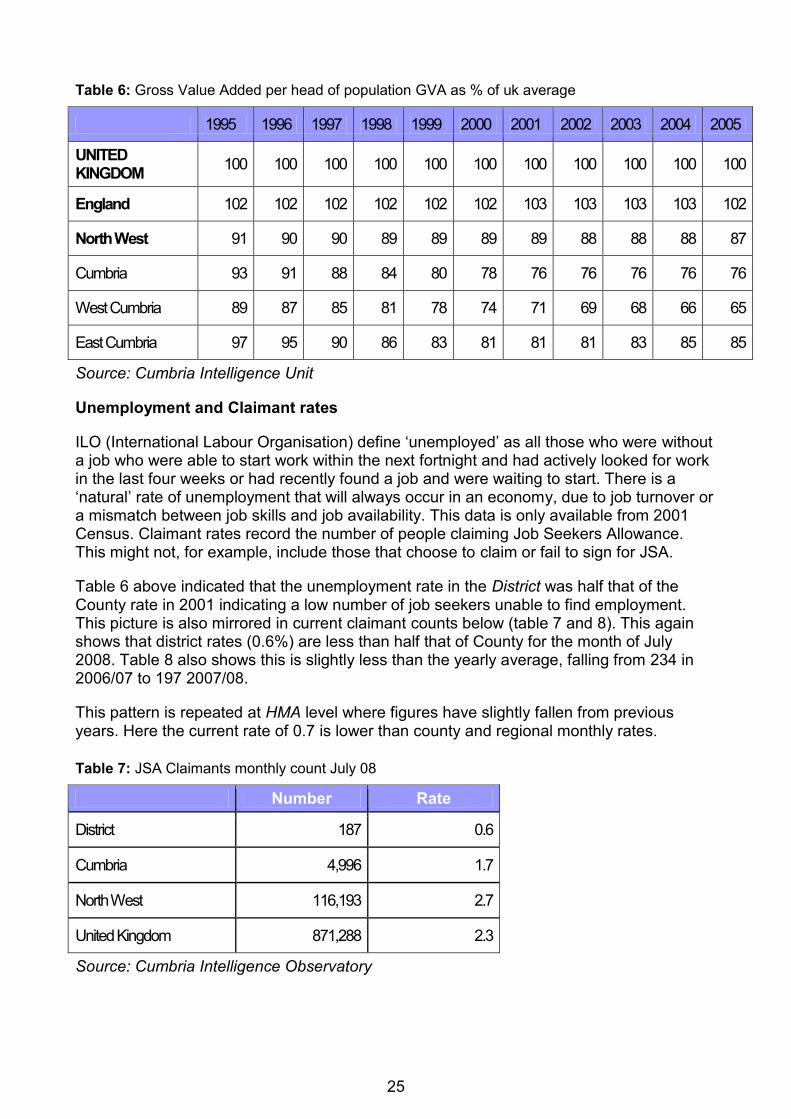

Table 6: Gross Value Added per head of population GVA as % of uk average

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

UNITED KINGDOM

100 100 100 100 100 100 100 100 100 100 100

England 102 102 102 102 102 102 103 103 103 103 102

North West 91 90 90 89 89 89 89 88 88 88 87

Cumbria 93 91 88 84 80 78 76 76 76 76 76

West Cumbria 89 87 85 81 78 74 71 69 68 66 65

East Cumbria 97 95 90 86 83 81 81 81 83 85 85

Source: Cumbria Intelligence Unit

Unemployment and Claimant rates

ILO (International Labour Organisation) define „unemployed‟ as all those who were without a job who were able to start work within the next fortnight and had actively looked for work in the last four weeks or had recently found a job and were waiting to start. There is a „natural‟ rate of unemployment that will always occur in an economy, due to job turnover or a mismatch between job skills and job availability. This data is only available from 2001 Census. Claimant rates record the number of people claiming Job Seekers Allowance. This might not, for example, include those that choose to claim or fail to sign for JSA.

Table 6 above indicated that the unemployment rate in the District was half that of the County rate in 2001 indicating a low number of job seekers unable to find employment. This picture is also mirrored in current claimant counts below (table 7 and 8). This again shows that district rates (0.6%) are less than half that of County for the month of July 2008. Table 8 also shows this is slightly less than the yearly average, falling from 234 in 2006/07 to 197 2007/08.

This pattern is repeated at HMA level where figures have slightly fallen from previous years. Here the current rate of 0.7 is lower than county and regional monthly rates.

Table 7: JSA Claimants monthly count July 08

Number Rate

District 187 0.6

Cumbria 4,996 1.7

North West 116,193 2.7

United Kingdom 871,288 2.3

Source: Cumbria Intelligence Observatory

26

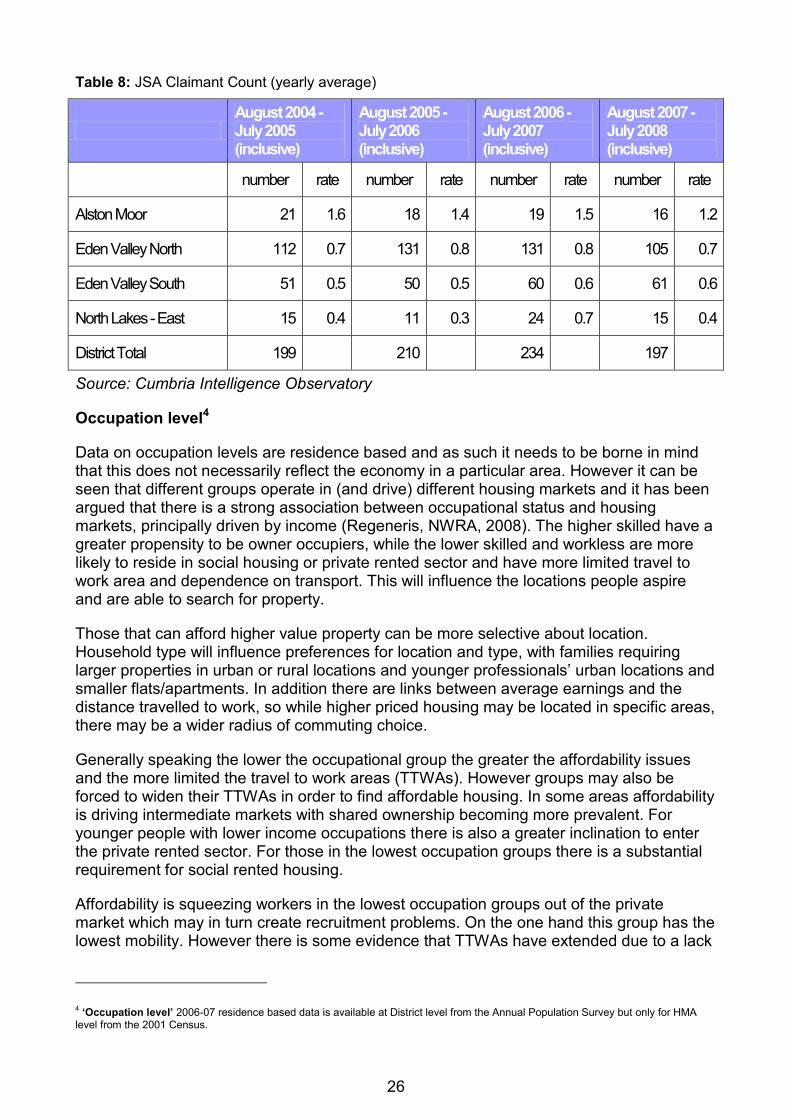

Table 8: JSA Claimant Count (yearly average)

August 2004 - July 2005 (inclusive)

August 2005 - July 2006 (inclusive)

August 2006 - July 2007 (inclusive)

August 2007 - July 2008 (inclusive)

number rate number rate number rate number rate

Alston Moor 21 1.6 18 1.4 19 1.5 16 1.2

Eden Valley North 112 0.7 131 0.8 131 0.8 105 0.7

Eden Valley South 51 0.5 50 0.5 60 0.6 61 0.6

North Lakes - East 15 0.4 11 0.3 24 0.7 15 0.4

District Total 199 210 234 197

Source: Cumbria Intelligence Observatory

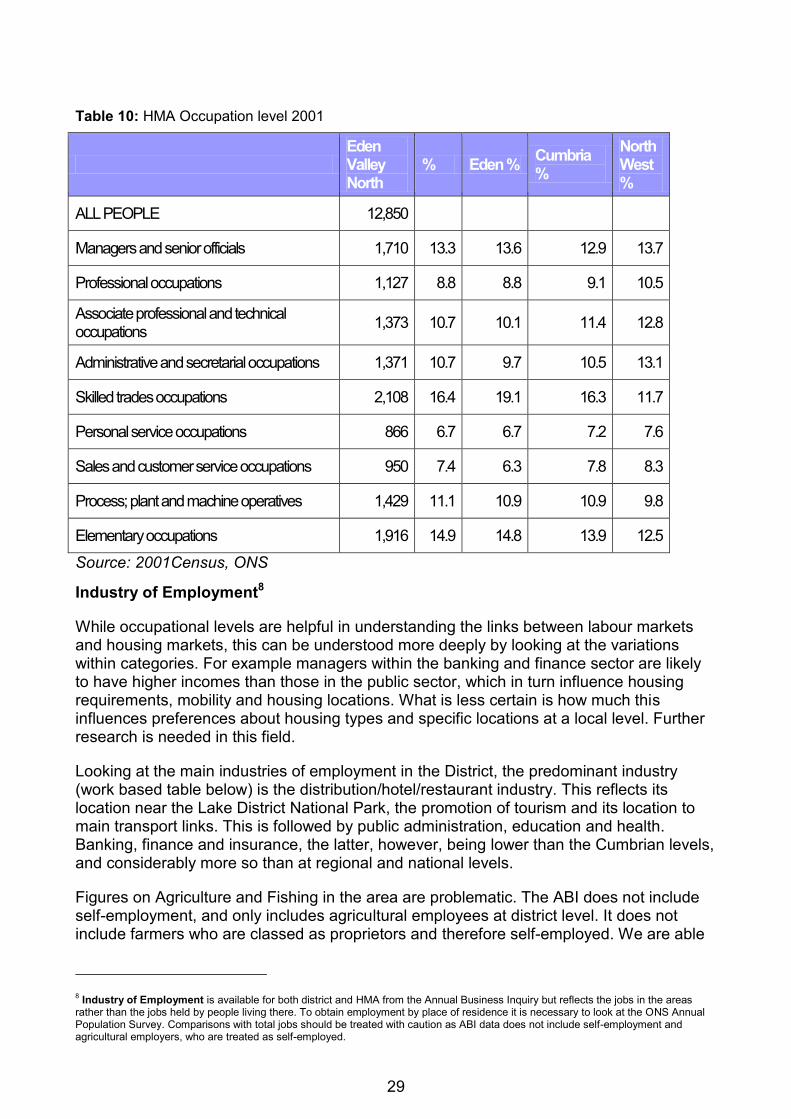

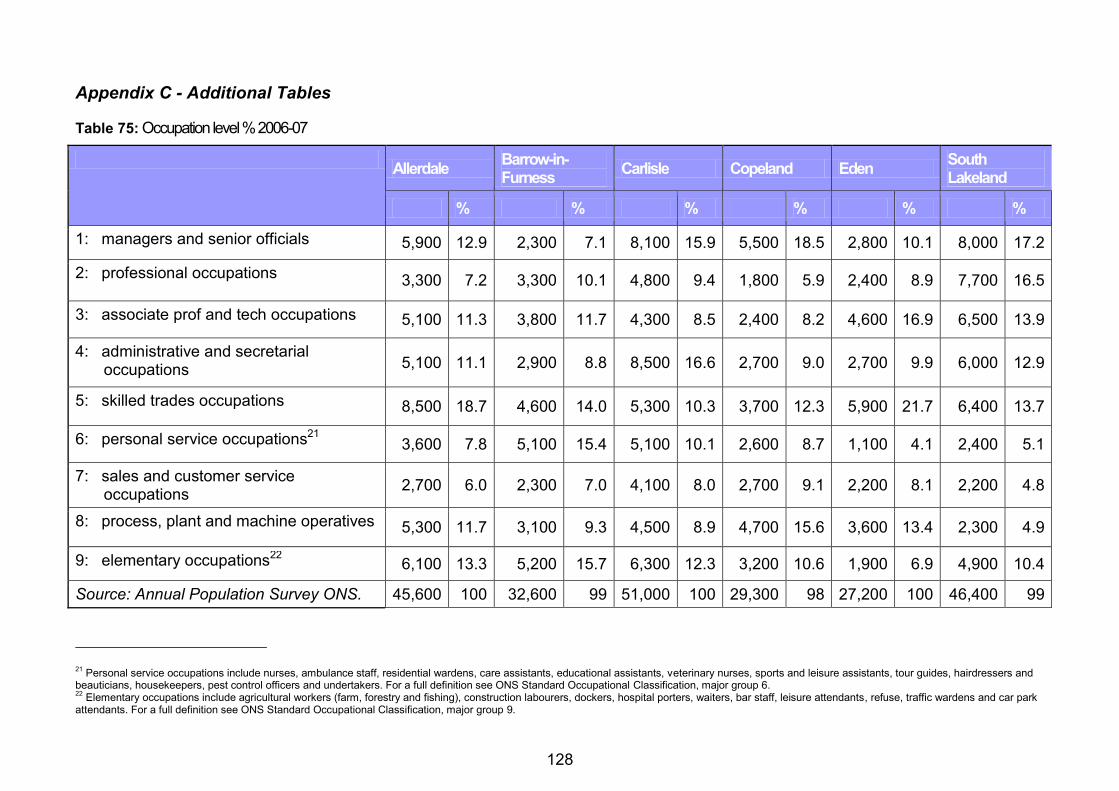

Occupation level4

Data on occupation levels are residence based and as such it needs to be borne in mind that this does not necessarily reflect the economy in a particular area. However it can be seen that different groups operate in (and drive) different housing markets and it has been argued that there is a strong association between occupational status and housing markets, principally driven by income (Regeneris, NWRA, 2008). The higher skilled have a greater propensity to be owner occupiers, while the lower skilled and workless are more likely to reside in social housing or private rented sector and have more limited travel to work area and dependence on transport. This will influence the locations people aspire and are able to search for property.

Those that can afford higher value property can be more selective about location. Household type will influence preferences for location and type, with families requiring larger properties in urban or rural locations and younger professionals‟ urban locations and smaller flats/apartments. In addition there are links between average earnings and the distance travelled to work, so while higher priced housing may be located in specific areas, there may be a wider radius of commuting choice.

Generally speaking the lower the occupational group the greater the affordability issues and the more limited the travel to work areas (TTWAs). However groups may also be forced to widen their TTWAs in order to find affordable housing. In some areas affordability is driving intermediate markets with shared ownership becoming more prevalent. For younger people with lower income occupations there is also a greater inclination to enter the private rented sector. For those in the lowest occupation groups there is a substantial requirement for social rented housing.

Affordability is squeezing workers in the lowest occupation groups out of the private market which may in turn create recruitment problems. On the one hand this group has the lowest mobility. However there is some evidence that TTWAs have extended due to a lack

4 „Occupation level‟ 2006-07 residence based data is available at District level from the Annual Population Survey but only for HMA

level from the 2001 Census.

27

of affordable housing near their place of work. Some employers, for example, may need to provide transport for lower skilled employees. For these groups shared ownership may not be an option.

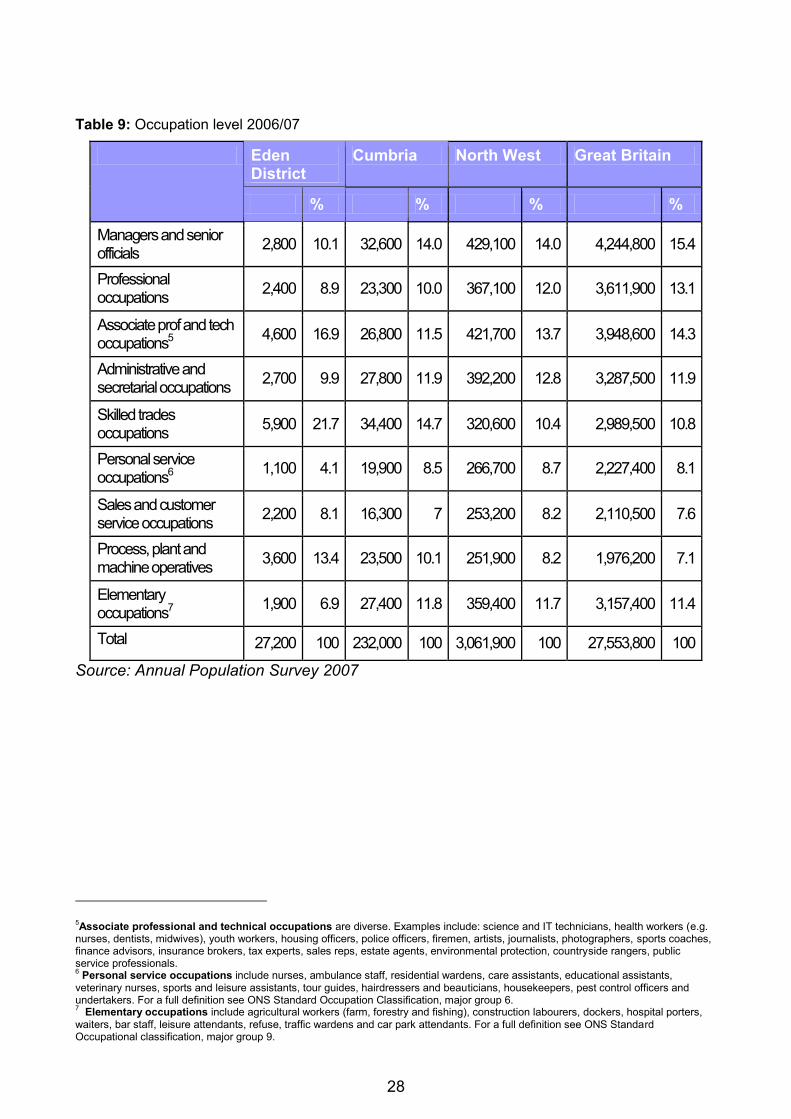

The Eden District and Cumbria has a lower proportion of its workforce in overall higher paid levels (professional, managerial and associated technical occupations) than the North West which in turn has less than the British percentage. There is a much higher incidence of skilled occupations, possibly low paid, in Cumbria than the North West and England and this is particularly so in the Eden District.

However comparing APS data and 2001 Census data also gives some indication that total overall upper level professions are increasing in Cumbria and the District. Within these upper professions there are differences in growth rates. Since 2001 there has been a District wide reduction in the proportion of manager/senior officer occupation levels from 14% to 10%. This fall in managers/senior officers in Eden does not match the figures for Cumbria and the North West, where this sector has shown an increase, and this could have implications for high value property demand, indicating a slow down in this end of the market for the Eden District. Along side this there has been a reduction in elementary occupations of 8% and a reduction in personal service occupations of 3%. Other occupations have remained the same or risen (typically by 2-3%), with associate professional and technical occupations showing the most significant increase of 7% up to 17%.

Eden has outstripped Cumbria and the North West in the proportional rise of these professional/technical occupations at the same time as seeing greater growth in the proportion of skilled trades occupations. Outside Eden there has been a reduction in these skilled trades but less growth in professional/technical occupations (see also Additional Tables, appendix C). This means the District now has a very slightly higher than county level of overall higher paid occupations. The District is catching up albeit due to rising associate professional/technical occupations rather than senior occupations, which could nonetheless signal a greater overall degree of mobility; People are able to work greater distances from their homes, and can afford to choose more affluent areas to live, which may also have fuelled house prices. A similar situation exists, for example, in South Lakeland, which has the highest percentage of residents with higher occupation levels and has some of the highest prices properties in Cumbria.

Census 2001 data showed the HMA had a predominance of residence with skilled trades although this was slightly lower than the District percentage. This was followed by elementary occupations, which may now have reduced if the area follows district trends. Overall the level of managers/senior officials, professional, associate professional mirrored the District and was at this point significantly lower than the region. However the District pattern indicates that whole still lower than regionally it may be catching up as commuting extends and people are willing to live further from work. This has been reflected in the income levels which were higher than district and Cumbrian levels in 2005 and remained so in 2007 (see 1.4 Income and earnings).

28

Table 9: Occupation level 2006/07

Eden District

Cumbria North West Great Britain

% % % %

Managers and senior officials

2,800 10.1 32,600 14.0 429,100 14.0 4,244,800 15.4

Professional occupations

2,400 8.9 23,300 10.0 367,100 12.0 3,611,900 13.1

Associate prof and tech occupations5

4,600 16.9 26,800 11.5 421,700 13.7 3,948,600 14.3

Administrative and secretarial occupations

2,700 9.9 27,800 11.9 392,200 12.8 3,287,500 11.9

Skilled trades occupations

5,900 21.7 34,400 14.7 320,600 10.4 2,989,500 10.8

Personal service occupations6

1,100 4.1 19,900 8.5 266,700 8.7 2,227,400 8.1

Sales and customer service occupations

2,200 8.1 16,300 7 253,200 8.2 2,110,500 7.6

Process, plant and machine operatives

3,600 13.4 23,500 10.1 251,900 8.2 1,976,200 7.1

Elementary occupations7

1,900 6.9 27,400 11.8 359,400 11.7 3,157,400 11.4

Total 27,200 100 232,000 100 3,061,900 100 27,553,800 100

Source: Annual Population Survey 2007

5Associate professional and technical occupations are diverse. Examples include: science and IT technicians, health workers (e.g.

nurses, dentists, midwives), youth workers, housing officers, police officers, firemen, artists, journalists, photographers, sports coaches, finance advisors, insurance brokers, tax experts, sales reps, estate agents, environmental protection, countryside rangers, public service professionals. 6 Personal service occupations include nurses, ambulance staff, residential wardens, care assistants, educational assistants,

veterinary nurses, sports and leisure assistants, tour guides, hairdressers and beauticians, housekeepers, pest control officers and undertakers. For a full definition see ONS Standard Occupation Classification, major group 6. 7 Elementary occupations include agricultural workers (farm, forestry and fishing), construction labourers, dockers, hospital porters,

waiters, bar staff, leisure attendants, refuse, traffic wardens and car park attendants. For a full definition see ONS Standard Occupational classification, major group 9.

29

Table 10: HMA Occupation level 2001

Eden Valley North

% Eden % Cumbria %

North West %

ALL PEOPLE 12,850

Managers and senior officials 1,710 13.3 13.6 12.9 13.7

Professional occupations 1,127 8.8 8.8 9.1 10.5

Associate professional and technical occupations

1,373 10.7 10.1 11.4 12.8

Administrative and secretarial occupations 1,371 10.7 9.7 10.5 13.1

Skilled trades occupations 2,108 16.4 19.1 16.3 11.7

Personal service occupations 866 6.7 6.7 7.2 7.6

Sales and customer service occupations 950 7.4 6.3 7.8 8.3

Process; plant and machine operatives 1,429 11.1 10.9 10.9 9.8

Elementary occupations 1,916 14.9 14.8 13.9 12.5

Source: 2001Census, ONS

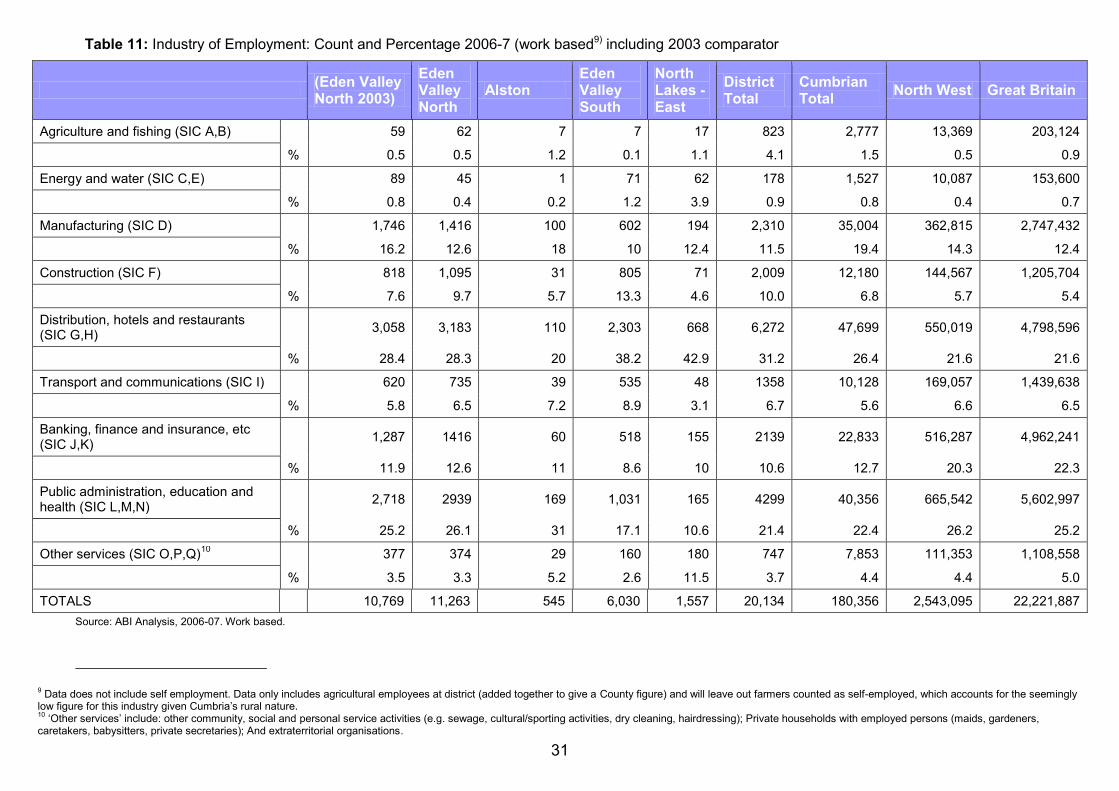

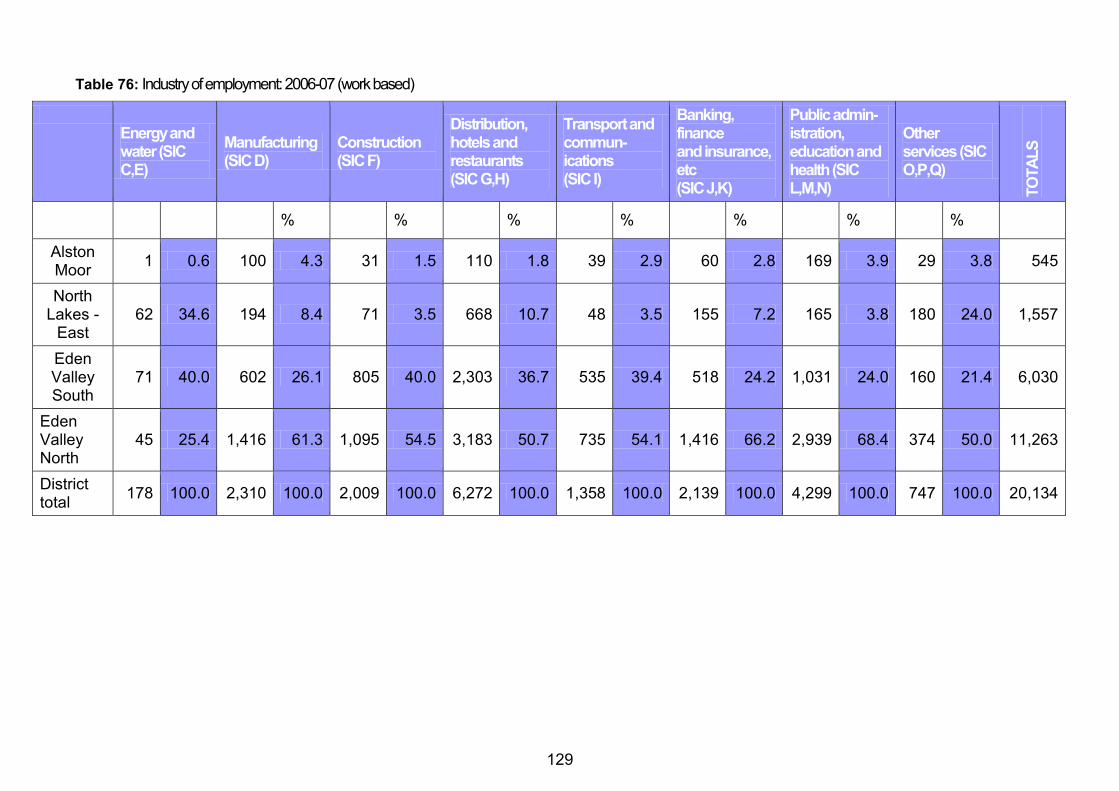

Industry of Employment8

While occupational levels are helpful in understanding the links between labour markets and housing markets, this can be understood more deeply by looking at the variations within categories. For example managers within the banking and finance sector are likely to have higher incomes than those in the public sector, which in turn influence housing requirements, mobility and housing locations. What is less certain is how much this influences preferences about housing types and specific locations at a local level. Further research is needed in this field.

Looking at the main industries of employment in the District, the predominant industry (work based table below) is the distribution/hotel/restaurant industry. This reflects its location near the Lake District National Park, the promotion of tourism and its location to main transport links. This is followed by public administration, education and health. Banking, finance and insurance, the latter, however, being lower than the Cumbrian levels, and considerably more so than at regional and national levels.

Figures on Agriculture and Fishing in the area are problematic. The ABI does not include self-employment, and only includes agricultural employees at district level. It does not include farmers who are classed as proprietors and therefore self-employed. We are able

8 Industry of Employment is available for both district and HMA from the Annual Business Inquiry but reflects the jobs in the areas

rather than the jobs held by people living there. To obtain employment by place of residence it is necessary to look at the ONS Annual Population Survey. Comparisons with total jobs should be treated with caution as ABI data does not include self-employment and agricultural employers, who are treated as self-employed.

30

to say that for the district there is twice the Cumbrian percentage and four times the regional and national percentage of agricultural employees but not the extent of this industry for housing market areas from this source.

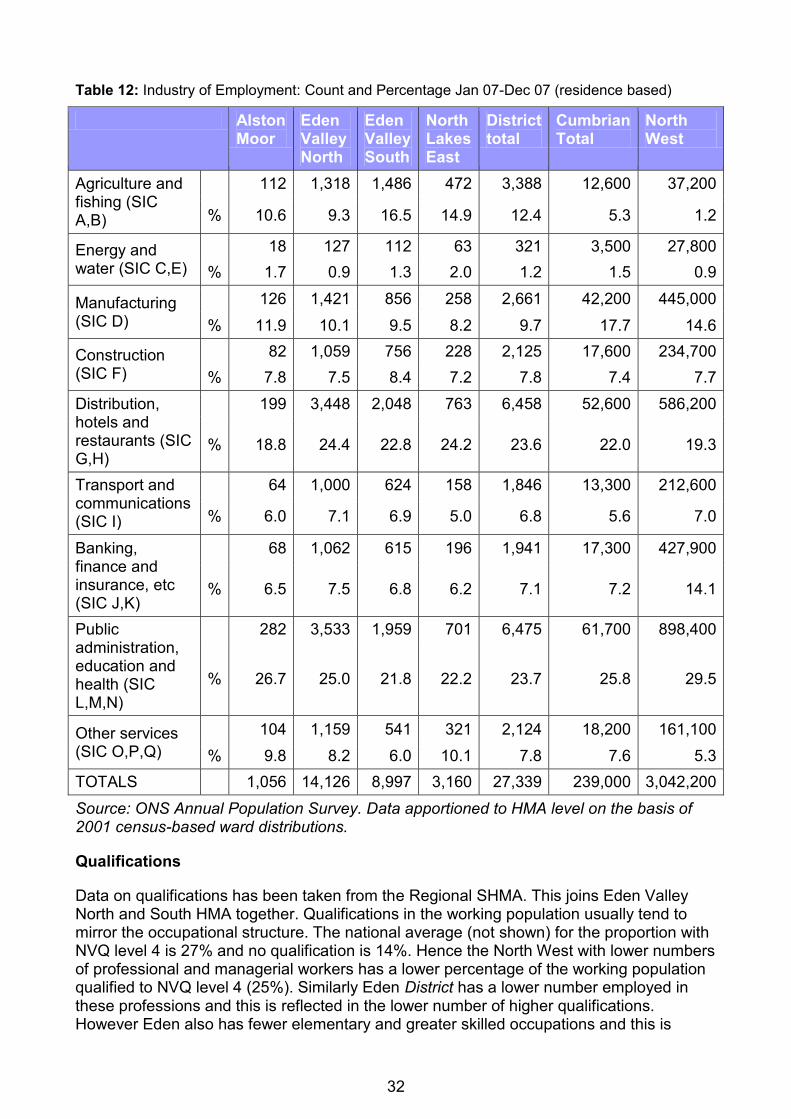

Residence based information (table 12) shows the jobs held by people living in the District. The highest proportion is in public administration, followed by the distribution/hotel/restaurants. This data also gives an indication of those residents working in agriculture, 3,388, the third largest industry, and it would seem reasonable to assume that many farmers and farm workers don‟t commute from outside the district to get to work and therefore these are also jobs based within the District.

At HMA level, Eden Valley North provides 11,263 jobs (not including farm owners) and 2,353 residence based self-employed (see Economic Activity table). At least 50% of all Eden‟s industries are based in this area, except for water and energy industries (see Additional tables) and is the District banking and public administration base. While it is not possible to say how many of these posts are filled by HMA residents, the information on travel to work areas indicates a degree of self containment in and around Penrith, and towards Carlisle. Further research into the level of industries in rural areas at a more local level is needed.

The highest level of industry within the area is distribution/hotels/restaurants with approximately 82% based in Penrith (based on 2003 ABI work based figures not shown). Further work is needed to break this category down further, although it is likely that the majority of this industry will be hotels and restaurants. This is followed by public administration/education/health; manufacturing; and banking/finance/insurance, with approximately 73% of the latter based in Penrith (2003 figures). Comparing this to the situation in 2003 shows a roughly similar pattern with slight rises in construction, transport, banking, public administration and other services.

Looking the type of industry in which the residents of the area work the patterns are very similar to the Districts, with the largest sector being public administration, followed by distribution/hotels/restaurants. While not the main industry for residence in the area, the highest number and percent of residents working in banking/finance/insurance in the District also lives here. Comparing this with 2001 Census data on occupational levels indicates that the levels are likely to be a higher scale overall than elsewhere in the District.

Comparing this with the data on occupation indicates that while there may be a relatively good level of managerial/professional levels these may not be in the highest paid sectors, but are rather hotel/catering and agriculture managers. Also while there was a high level of skilled trades, this includes agriculture workers and chefs/cooks, which are not necessarily the highest paid trades.

The high level of agriculture, hotel/catering, added to the high level of self-employment and skilled trades could just as easily indicate a high level of farming, bed and breakfast industries and smaller catering concerns as it could residents in well paid, high powered, highly mobile positions.

31

Table 11: Industry of Employment: Count and Percentage 2006-7 (work based9) including 2003 comparator

(Eden Valley North 2003)

Eden Valley North

Alston Eden Valley South

North Lakes - East

District Total

Cumbrian Total

North West Great Britain

Agriculture and fishing (SIC A,B) 59 62 7 7 17 823 2,777 13,369 203,124

% 0.5 0.5 1.2 0.1 1.1 4.1 1.5 0.5 0.9

Energy and water (SIC C,E) 89 45 1 71 62 178 1,527 10,087 153,600

% 0.8 0.4 0.2 1.2 3.9 0.9 0.8 0.4 0.7

Manufacturing (SIC D) 1,746 1,416 100 602 194 2,310 35,004 362,815 2,747,432

% 16.2 12.6 18 10 12.4 11.5 19.4 14.3 12.4

Construction (SIC F) 818 1,095 31 805 71 2,009 12,180 144,567 1,205,704

% 7.6 9.7 5.7 13.3 4.6 10.0 6.8 5.7 5.4

Distribution, hotels and restaurants (SIC G,H)

3,058 3,183 110 2,303 668 6,272 47,699 550,019 4,798,596

% 28.4 28.3 20 38.2 42.9 31.2 26.4 21.6 21.6

Transport and communications (SIC I) 620 735 39 535 48 1358 10,128 169,057 1,439,638

% 5.8 6.5 7.2 8.9 3.1 6.7 5.6 6.6 6.5

Banking, finance and insurance, etc (SIC J,K)

1,287 1416 60 518 155 2139 22,833 516,287 4,962,241

% 11.9 12.6 11 8.6 10 10.6 12.7 20.3 22.3

Public administration, education and health (SIC L,M,N)

2,718 2939 169 1,031 165 4299 40,356 665,542 5,602,997

% 25.2 26.1 31 17.1 10.6 21.4 22.4 26.2 25.2

Other services (SIC O,P,Q)10

377 374 29 160 180 747 7,853 111,353 1,108,558

% 3.5 3.3 5.2 2.6 11.5 3.7 4.4 4.4 5.0

TOTALS 10,769 11,263 545 6,030 1,557 20,134 180,356 2,543,095 22,221,887

Source: ABI Analysis, 2006-07. Work based.

9 Data does not include self employment. Data only includes agricultural employees at district (added together to give a County figure) and will leave out farmers counted as self-employed, which accounts for the seemingly

low figure for this industry given Cumbria‟s rural nature. 10

„Other services‟ include: other community, social and personal service activities (e.g. sewage, cultural/sporting activities, dry cleaning, hairdressing); Private households with employed persons (maids, gardeners, caretakers, babysitters, private secretaries); And extraterritorial organisations.

32

Table 12: Industry of Employment: Count and Percentage Jan 07-Dec 07 (residence based)

Alston Moor

Eden Valley North

Eden Valley South

North Lakes East

District total

Cumbrian Total

North West

Agriculture and fishing (SIC A,B)

112 1,318 1,486 472 3,388 12,600 37,200

% 10.6 9.3 16.5 14.9 12.4 5.3 1.2

Energy and water (SIC C,E)

18 127 112 63 321 3,500 27,800

% 1.7 0.9 1.3 2.0 1.2 1.5 0.9

Manufacturing (SIC D)

126 1,421 856 258 2,661 42,200 445,000

% 11.9 10.1 9.5 8.2 9.7 17.7 14.6

Construction (SIC F)

82 1,059 756 228 2,125 17,600 234,700

% 7.8 7.5 8.4 7.2 7.8 7.4 7.7

Distribution, hotels and restaurants (SIC G,H)

199 3,448 2,048 763 6,458 52,600 586,200

% 18.8 24.4 22.8 24.2 23.6 22.0 19.3

Transport and communications (SIC I)

64 1,000 624 158 1,846 13,300 212,600

% 6.0 7.1 6.9 5.0 6.8 5.6 7.0

Banking, finance and insurance, etc (SIC J,K)

68 1,062 615 196 1,941 17,300 427,900

% 6.5 7.5 6.8 6.2 7.1 7.2 14.1

Public administration, education and health (SIC L,M,N)

282 3,533 1,959 701 6,475 61,700 898,400

% 26.7 25.0 21.8 22.2 23.7 25.8 29.5

Other services (SIC O,P,Q)

104 1,159 541 321 2,124 18,200 161,100

% 9.8 8.2 6.0 10.1 7.8 7.6 5.3

TOTALS 1,056 14,126 8,997 3,160 27,339 239,000 3,042,200

Source: ONS Annual Population Survey. Data apportioned to HMA level on the basis of 2001 census-based ward distributions.

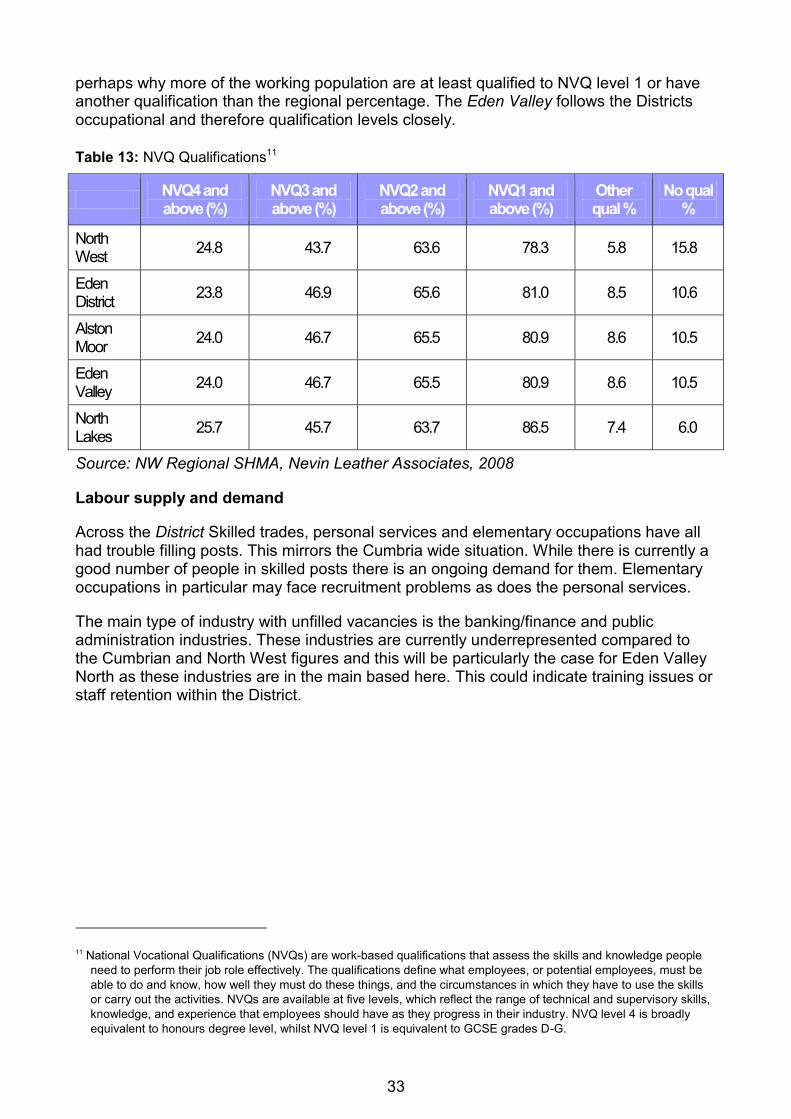

Qualifications

Data on qualifications has been taken from the Regional SHMA. This joins Eden Valley North and South HMA together. Qualifications in the working population usually tend to mirror the occupational structure. The national average (not shown) for the proportion with NVQ level 4 is 27% and no qualification is 14%. Hence the North West with lower numbers of professional and managerial workers has a lower percentage of the working population qualified to NVQ level 4 (25%). Similarly Eden District has a lower number employed in these professions and this is reflected in the lower number of higher qualifications. However Eden also has fewer elementary and greater skilled occupations and this is

33

perhaps why more of the working population are at least qualified to NVQ level 1 or have another qualification than the regional percentage. The Eden Valley follows the Districts occupational and therefore qualification levels closely.

Table 13: NVQ Qualifications11

NVQ4 and above (%)

NVQ3 and above (%)

NVQ2 and above (%)

NVQ1 and above (%)

Other qual %

No qual %

North West

24.8 43.7 63.6 78.3 5.8 15.8

Eden District

23.8 46.9 65.6 81.0 8.5 10.6

Alston Moor

24.0 46.7 65.5 80.9 8.6 10.5

Eden Valley

24.0 46.7 65.5 80.9 8.6 10.5

North Lakes

25.7 45.7 63.7 86.5 7.4 6.0

Source: NW Regional SHMA, Nevin Leather Associates, 2008

Labour supply and demand

Across the District Skilled trades, personal services and elementary occupations have all had trouble filling posts. This mirrors the Cumbria wide situation. While there is currently a good number of people in skilled posts there is an ongoing demand for them. Elementary occupations in particular may face recruitment problems as does the personal services.

The main type of industry with unfilled vacancies is the banking/finance and public administration industries. These industries are currently underrepresented compared to the Cumbrian and North West figures and this will be particularly the case for Eden Valley North as these industries are in the main based here. This could indicate training issues or staff retention within the District.

11 National Vocational Qualifications (NVQs) are work-based qualifications that assess the skills and knowledge people

need to perform their job role effectively. The qualifications define what employees, or potential employees, must be

able to do and know, how well they must do these things, and the circumstances in which they have to use the skills

or carry out the activities. NVQs are available at five levels, which reflect the range of technical and supervisory skills,

knowledge, and experience that employees should have as they progress in their industry. NVQ level 4 is broadly

equivalent to honours degree level, whilst NVQ level 1 is equivalent to GCSE grades D-G.

34

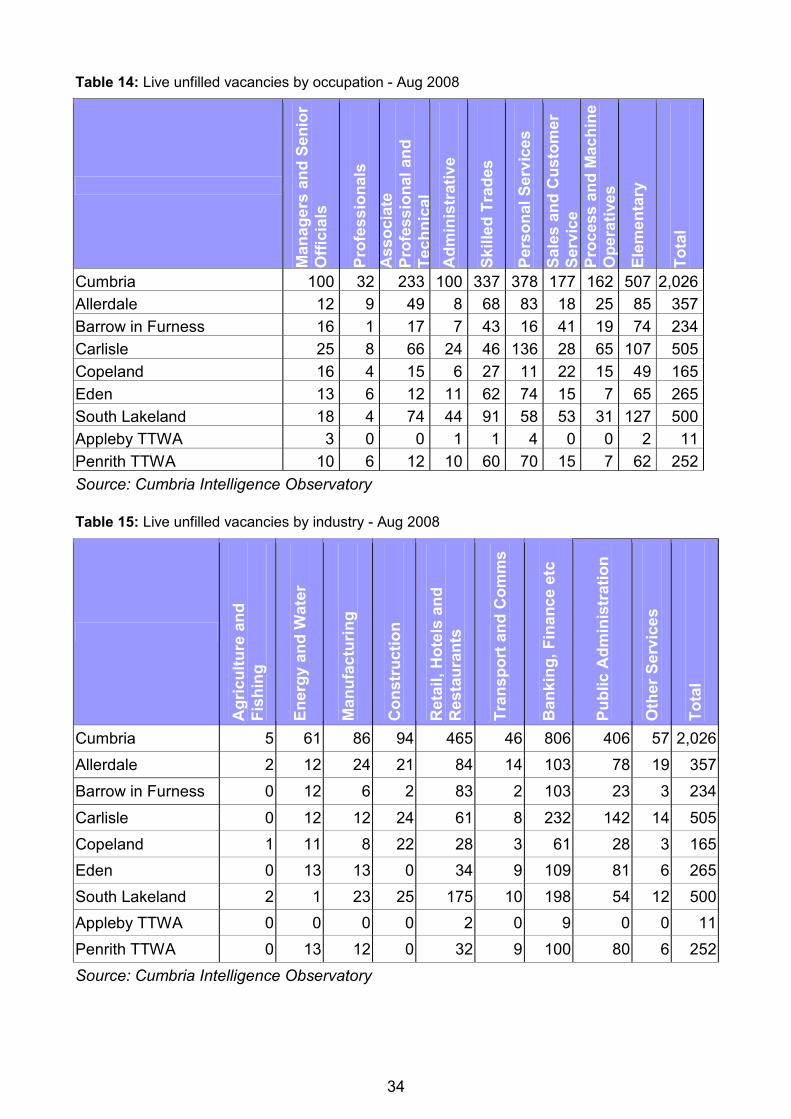

Table 14: Live unfilled vacancies by occupation - Aug 2008

Ma

nag

ers

an

d S

en

ior

Off

icia

ls

Pro

fes

sio

na

ls

Ass

ocia

te

Pro

fes

sio

na

l a

nd

Tec

hn

ical

Ad

min

istr

ati

ve

Sk

ille

d T

rad

es

Pe

rso

nal

Serv

ice

s

Sa

les

an

d C

usto

me

r

Se

rvic

e

Pro

ce

ss

an

d M

ac

hin

e

Op

era

tive

s

Ele

me

nta

ry

To

tal

Cumbria 100 32 233 100 337 378 177 162 507 2,026

Allerdale 12 9 49 8 68 83 18 25 85 357

Barrow in Furness 16 1 17 7 43 16 41 19 74 234

Carlisle 25 8 66 24 46 136 28 65 107 505

Copeland 16 4 15 6 27 11 22 15 49 165

Eden 13 6 12 11 62 74 15 7 65 265

South Lakeland 18 4 74 44 91 58 53 31 127 500

Appleby TTWA 3 0 0 1 1 4 0 0 2 11

Penrith TTWA 10 6 12 10 60 70 15 7 62 252

Source: Cumbria Intelligence Observatory

Table 15: Live unfilled vacancies by industry - Aug 2008

Ag

ric

ult

ure

an

d

Fis

hin

g

En

erg

y a

nd

Wa

ter

Ma

nu

fac

turi

ng

Co

ns

tru

cti

on

Reta

il,

Ho

tels

an

d

Res

tau

ran

ts

Tra

nsp

ort

an

d C

om

ms

Ban

kin

g,

Fin

an

ce

etc

Pu

blic

Ad

min

istr

ati

on

Oth

er

Se

rvic

es

To

tal

Cumbria 5 61 86 94 465 46 806 406 57 2,026

Allerdale 2 12 24 21 84 14 103 78 19 357

Barrow in Furness 0 12 6 2 83 2 103 23 3 234

Carlisle 0 12 12 24 61 8 232 142 14 505

Copeland 1 11 8 22 28 3 61 28 3 165

Eden 0 13 13 0 34 9 109 81 6 265

South Lakeland 2 1 23 25 175 10 198 54 12 500

Appleby TTWA 0 0 0 0 2 0 9 0 0 11

Penrith TTWA 0 13 12 0 32 9 100 80 6 252

Source: Cumbria Intelligence Observatory

35

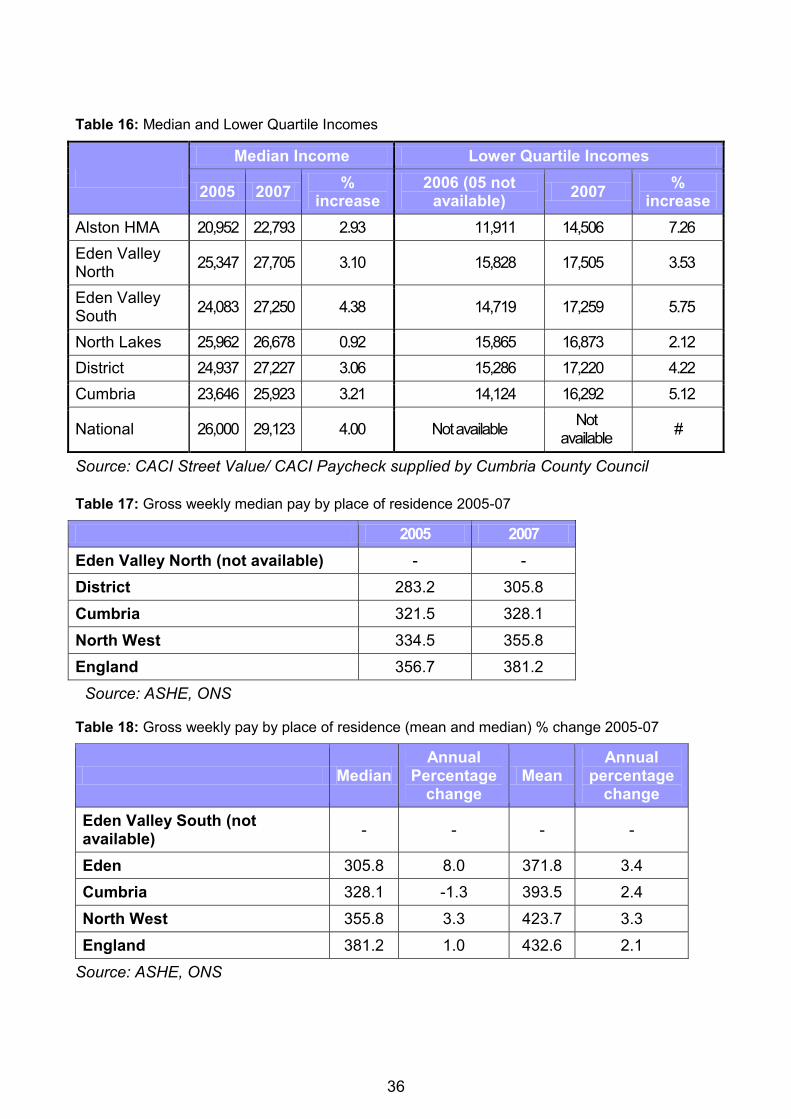

1.4 Incomes and earnings12

Government Guidance suggests that incomes and earnings are key drivers of demand. Studies suggest that households spend more on housing as incomes increase, though at a rate less than their growth in income, and as incomes rise demand for neighbourhood quality increases together with house size. In 2005 the median income for Eden District and Cumbria was lower than the National level, and this situation has not improved - in fact the gap has increase with the national levels increasing 4% and district and county 3%.

Within this Eden Valley North‟s median income was higher than the District and Cumbria‟s in 2005 but still lower than the National figure. This pattern had not changed by 2008. Looking at lower quartile incomes (from 2006) this was and still is higher than the District average and Cumbria. Also the area contains the widest gap between lower quartile and median income figures, indicating a wide range of marginally higher incomes. However while this has seen an annual increase of 3.53% in lower quartile incomes this growth is not as marked an increase as County‟s and is below growth in other parts of the District

It is not possible to say what proportion of this income is earned income and what may be from investments and pensions, though it is likely that the slightly higher income is influenced by employment in Carlisle. While the area contains the highest lower quartile incomes this does not necessarily mean that it has fewer numbers of people on lower incomes. As the area has the largest number of people it follows that within its bottom 25% there may be an equal or even greater number of people on £14,506 or below than in Alston with its lower population.

While the District wide unemployment rate may be low the gross weekly pay is lower than the median for Cumbria, the North West and England, and although the area has experienced increases earnings are still lower by between £22 and £75 per week. Therefore there are more people working in lower paid jobs despite the overall rise in upper occupational levels (see above). Earnings data is not available at HMA level.

12 Information on incomes is derived from CACI Paycheck. This utilises Census data and does not therefore householders if their

property is a second/holiday home. „Income‟ includes income from savings, investments, certain benefits and earnings. Earnings are salary only.

36

Table 16: Median and Lower Quartile Incomes

Median Income Lower Quartile Incomes

2005 2007 %

increase 2006 (05 not

available) 2007

% increase

Alston HMA 20,952 22,793 2.93 11,911 14,506 7.26

Eden Valley North

25,347 27,705 3.10 15,828 17,505 3.53

Eden Valley South

24,083 27,250 4.38 14,719 17,259 5.75

North Lakes 25,962 26,678 0.92 15,865 16,873 2.12

District 24,937 27,227 3.06 15,286 17,220 4.22

Cumbria 23,646 25,923 3.21 14,124 16,292 5.12

National 26,000 29,123 4.00 Not available Not

available #

Source: CACI Street Value/ CACI Paycheck supplied by Cumbria County Council

Table 17: Gross weekly median pay by place of residence 2005-07

2005 2007

Eden Valley North (not available) - -

District 283.2 305.8

Cumbria 321.5 328.1

North West 334.5 355.8

England 356.7 381.2

Source: ASHE, ONS

Table 18: Gross weekly pay by place of residence (mean and median) % change 2005-07

Median Annual

Percentage change

Mean Annual

percentage change

Eden Valley South (not available)

- - - -

Eden 305.8 8.0 371.8 3.4

Cumbria 328.1 -1.3 393.5 2.4

North West 355.8 3.3 423.7 3.3

England 381.2 1.0 432.6 2.1

Source: ASHE, ONS

37

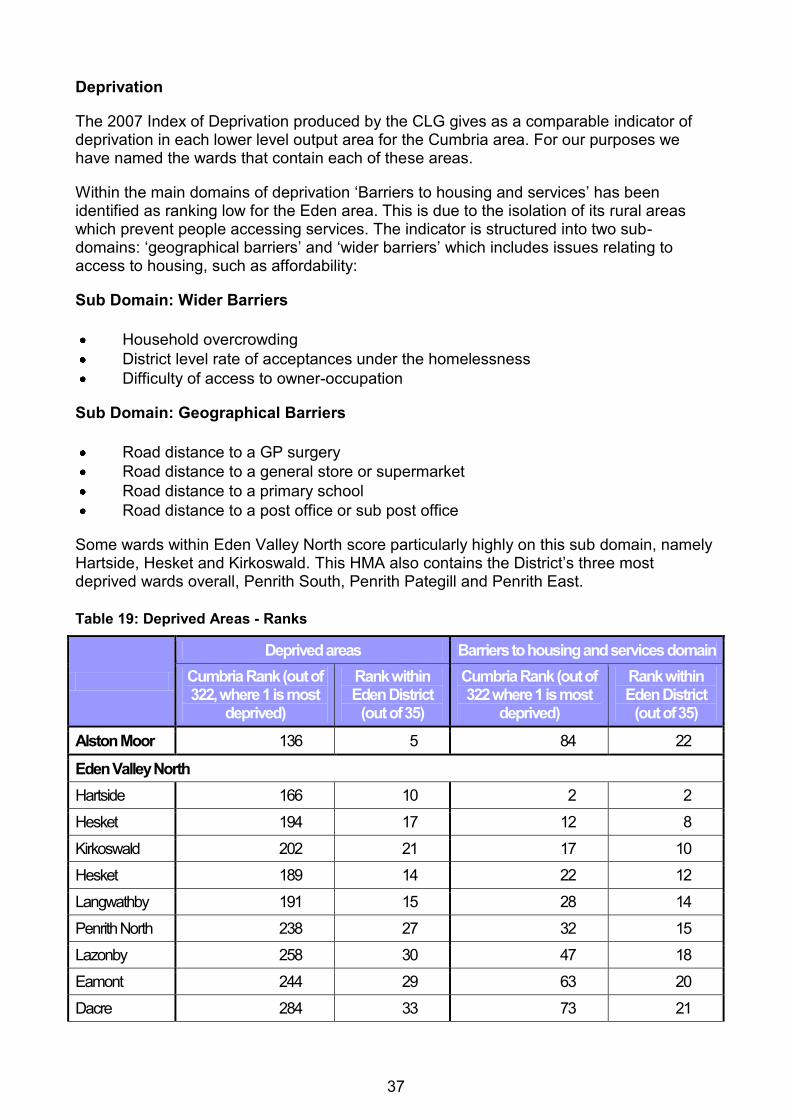

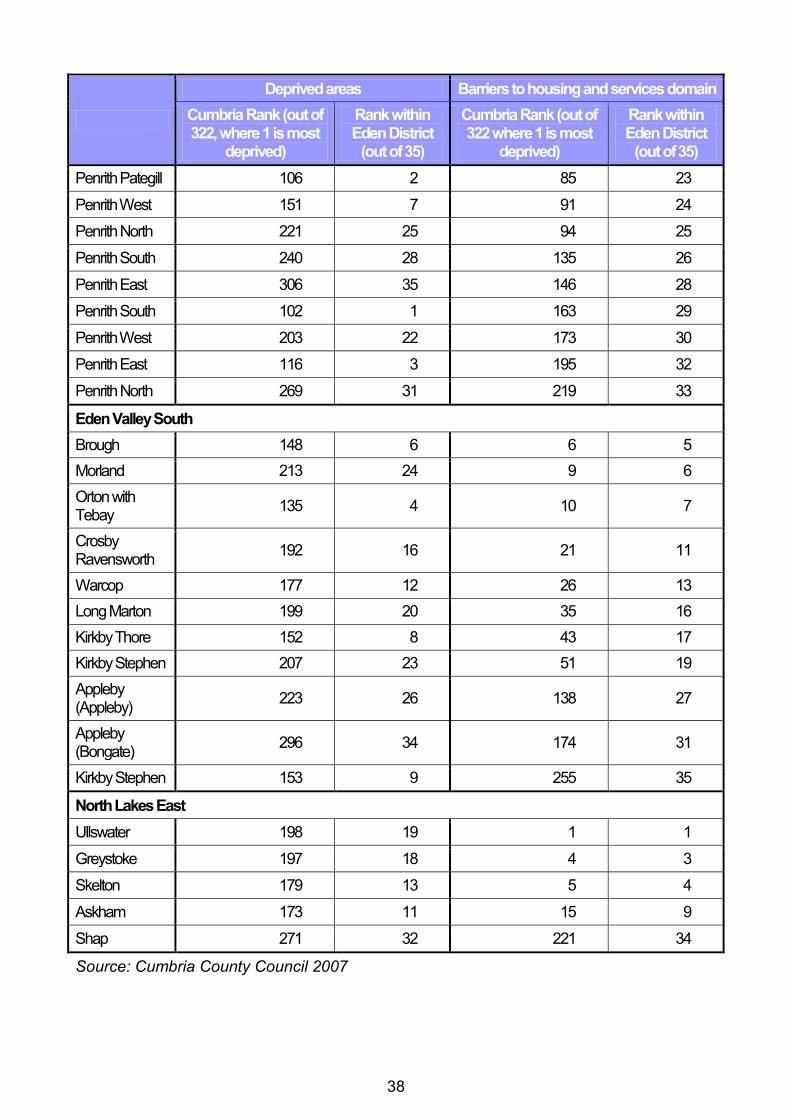

Deprivation