Embed Size (px)

Citation preview

CA Kinjesh Thakkar

Baroda Branch of ICAI

Impact of Ind AS on Corporate Taxation

Contents

1. Background and Applicability of Ind AS

2. Format of profit and loss under Ind AS

3. Conceptual and fundamental change

4. Interplay between Ind AS and Direct Tax

5. First time adoption of Ind AS

6. Practical Corporate Tax issues under Ind AS

CA Kinjesh Thakkar

Background and Applicability

CA Kinjesh Thakkar

Background

• Ind AS is the IFRS equivalent set of accounting standards with certain carve outs suitable for the Indian environment.

• Carve outs have been made to fill up the gap/differences in application of Accounting Principles Practices and economic conditions prevailing in India.

CA Kinjesh Thakkar

IFRSCarve-outs

Ind AS

IFRS Adoption

• Implementing IFRS into its legislation in exact form as issued by IASB

IFRS Convergence

• Implementing IFRS with certain change (carve-outs) to suit economic environment of country.

Applicability of Ind AS

2015-16

2016-17

2017-18

Voluntary and Early Adoption

All listed (Not on SME exchange) and unlisted companies with net worth of Rs.500 crores or more as at March 31, 2014

• All listed (Not on SME exchange) companies not covered above

• All unlisted companies with net worth of Rs.250 crores or more as at March 31, 2014

Notes:• Applies to Holding, subsidiaries, joint ventures and associate companies of above companies. • Applicable to both standalone and consolidated financial statements.• From 2018-19 onwards, when a company’s net worth becomes greater than Rs. 250 crores

CA Kinjesh Thakkar

Format of Profit & loss under Ind AS

CA Kinjesh Thakkar

Ind AS financials

A complete set of financial statements under Ind AS includes the following:

1. Balance sheet at the end of the period

2. Statement of profit and loss for the period

3. Statement of changes in equity for the period

4. Statement of cash flows for the period; notes, comprising a summary of significant accounting policies and other explanatory information.

5. Comparative financial information in respect of the preceding period as specified

6. Balance sheet as at the beginning of the preceding period when an entity applies an accounting policy retrospectively or makes a retrospective restatement of items in its financial statements, or when it reclassifies items in its financial statements having an impact on the balance sheet as at the beginning of the preceding period

CA Kinjesh Thakkar

Format of Ind AS Profit and loss account

Statement of Profit and loss account

Revenue

Revenue from Operations

Other income

Total Income from operations

Expenses

Cost of Materials consumed

Excise duty

Purchase of stock-in-trade

Changes in inventories of finished goods, stock-in-trade and work-in-progress

Employee Benefit expenses

Finance cost

Depreciation and Amortization expenses

Other expenses

Total Expenses

CA Kinjesh Thakkar

Format of Ind AS Profit and loss accountStatement of Profit and loss account (cont..)

Profit before tax

Tax expense (i) current tax(ii) Deferred tax

Profit (Loss) for the period from continuing operations

Profit/(loss) from discontinued operations

Tax expense of discontinued operations

Profit/(loss) from Discontinued operations(after tax)

Profit/(loss) for the period

Other comprehensive Income

A. (i) Items that will not be reclassified to profit or loss (revaluation, re-measurement of defined benefit plan etc.)

(ii) Income tax relating to items that will not be reclassified to profit or loss

B. (i) Items that will be reclassified to profit or loss (exchange difference in translation of financial statement of foreign operations)

(ii) Income tax relating to items that will be reclassified to profit or loss

Total comprehensive income for the period

CA Kinjesh Thakkar

Conceptual and Fundamental Change

CA Kinjesh Thakkar

Conceptual and fundamental change

IND AS

Substance over form

Extensive

Disclosures

Present value –time

value of money & Fair value

impact

More Principle based

rather than rule based

CA Kinjesh Thakkar

Interplay between Ind AS and Income Tax

CA Kinjesh Thakkar

Interplay between Ind AS and Income Tax

Accounting under Ind AS

Impact on MAT

Guidance under section 115JB

Specific adjustment as prescribed to

be made

Impact under normal

provision of Income tax Act

Treatment covered under ICDS or Act

Follow treatment as

per ICDS or Act

Treatment neither covered by ICDS nor Act

Interpret using Judicial

precedents

CA Kinjesh Thakkar

Interplay between Ind AS and Income Tax

Solution:

The SC vindicated this position in the case of C.I.T. v. Shoorji Vallabhdas & Co. holding as under –

“Income-tax is a levy on income. No doubt, the Income-tax Act takes into account two points of time at which the liability to tax is attracted, via. the accrual of the income or its receipt; but the substance of the matter is the income. If income does not result at all, there cannot be a tax, even though in book-keeping, an entry is made about a hypothetical income, which does not materialise. Where income has, in fact, been received and is subsequently given up in such circumstances that it remains the income of the recipient, even though given up, the tax may be payable. Where, however, the income can be said not to have resulted at all, there is obviously neither accrual nor receipt of income, even though an entry to that effect might, in certain circumstances, have been made in the books of account.“

Thus, based on above argument it is possible to say that Notional Income or notional expenses cannot be taxed or allowed under Income Tax.

CA Kinjesh Thakkar

Issue 1:

If Ind AS results in notional income or expenses to be recognized in statement of profit and loss account and there is no specific guidance under Act/ICDS what treatment to be adopted?

Interplay between Ind AS and Income Tax

Possible Views subject to ICDS specific adjustments:

View 1 : The assessee has option to choose ICAI AS for taxation purpose

View 2 : The assessee company has to mandatorily follow Ind AS for taxation purpose

CA Kinjesh Thakkar

Issue 2:Can assessee choose one method for accounting and a different method for tax purposes?

Analysis:

Under Income Tax Act, Section 44AA and 44AB takes care of requirement to maintain books of accounts and tax Audit.

Landmark Judgment of Supreme court in United commercial Bank vs CIT held that books of accounts prepared in statutory form may not be decisive and conclusive in

determining real income. Preparation of the balance sheet in accordance with the statutory provision would not

disentitle the assessee in submitting income tax return on the real taxable income.

Interplay between Ind AS and Income Tax

• Further, companies act cannot override taxability based on accounting.

• Thus, if real taxable income can be obtained from ICAI AS, one may opt for same.

Practical points for consideration:

• Separate set of ICAI AS needs to be prepared.

• Without Audited figures, it would be difficult to prove authenticity of accounts prepared as per ICAI AS when asked by tax authorities.

• Also, if tax authorities accept the books as per ICAI AS, reconciliation may be asked by tax authorities.

• Thus, better view is to follow Ind AS treatment in practical scenario.

CA Kinjesh Thakkar

Interplay between Ind AS and Income Tax

MAT

Business Income Computation

Presumptive basis Taxation

Proportion of Independence to Accounting adopted

Lowest Independence

Highest Independence

CA Kinjesh Thakkar

Ind AS and MAT

Ind AS and MAT

• Amendment in Finance Act, 2017

• Sub-section (2A) of section 115JB provides for following Ind AS adjustment to Book profit for person required to prepare accounts as per Ind AS.

• 1. Amount credited to OCI under the head “"Items that will not be re-classified to profit or loss“ except:

• -revaluation surplus as specified; or

• -gains or losses from equity instruments designated at FVTOCI as per Ind AS 109

• 2. One-fifth of the transition amount if positive for first 5 years of Ind AS

• 1. Amount debited to OCI under the head “"Items that will not be re-classified to profit or loss“

• 2. One-fifth of the transition amount if negative for first 5 years of Ind AS

CA Kinjesh Thakkar

Ind AS and MAT

Ind AS and MAT

• Calculation of Transition amount on convergence date:

Aggregate amount adjusted in other equity

capital reserve & securities premium

Transition Amount

Following shall not be included in transition amount:A) amount or aggregate of the amounts adjusted in the OCI on the convergence date which shall be subsequently re-classified to the profit or loss;(B) revaluation surplus for assets in accordance with the Ind AS 16 and Ind AS 38 adjusted on the convergence date;(C) gains or losses from investments in equity instruments designated at fair value through other comprehensive income in accordance with the Ind AS 109 adjusted on the convergence date;(D) adjustments relating to items of property, plant and equipment and intangible assets recorded at fair value as deemed cost in accordance with paragraphs D5 and D7 of the Ind AS 101 on the convergence date;(E) adjustments relating to investments in subsidiaries, joint ventures and associates recorded at fair value as deemed cost in accordance with paragraph D15 of the Ind AS 101 on the convergence date; and(F) adjustments relating to cumulative translation differences of a foreign operation in accordance with paragraph D13 of the Ind AS 101 on the convergence date.CA Kinjesh Thakkar

First time adoption of Ind AS

CA Kinjesh Thakkar

First Time Adoption of Ind AS

Transition Date

1st April 2015

Convergence date

1st April 201631st March 2017Previous

years

Transition period

Comparative

period

Current reporting period

First Ind AS reporting period for phase 1 companies

CA Kinjesh Thakkar

First Time Adoption of Ind AS

Issue 3

If financial year is different than tax year, example, Financial year is from June 2016 to May 2017 and Tax Year is from April 2016 to March 2017. How to compute following:

1. Income Tax under normal provision

2. Book profit for the purpose of MAT

CA Kinjesh Thakkar

Possible solutions for computing taxable income and book profit:

View 1: Adopt AS for whole tax year from April 16 to March 17

View 2: AS up till June ’16 and subsequently IND AS

View 3 : Adopt Ind AS for whole tax year from April ’16 till March ’17

First Time Adoption of Ind AS

Analysis for computing taxable Income under normal provision

• No express prohibition in the Act that separate records/accounts/statement for the purpose of compliance with other Acts cannot be maintained

• Landmark Judgment of Supreme court in United commercial Bank vs CIT (1999) 240 ITR 355 wherein concept of real income has been recognized.

• Any of the views may be followed. However, view 1 may result in additional preparation of books as per AS, thus this seems to be more burdensome.

Analysis for computing Book profit

• Book profit highly relies on accounting by corporates.

• Second proviso to section 115JB states that

“Provided further that where the company has adopted or adopts the financial year under the Companies Act, 2013 (18 of 2013), which is different from the previous year under this Act, the accounting policies; the accounting standards adopted for preparing such accounts including statement of profit and loss; the method and rates adopted for calculating the depreciation, shall correspond to the accounting policies, accounting standards and the method and rates for calculating the depreciation which have been adopted for preparing such accounts including statement of profit and loss for such financial year or part of such financial year falling within the relevant previous year”

Thus, view 2 seems to be permissible.

CA Kinjesh Thakkar

Practical Corporate Tax Issues under Ind AS

CA Kinjesh Thakkar

Practical Issues under Ind AS

In the books of Parent

Loan to Subsidiary account 100

To Bank account 100

In the books of Parent

Bank account 7

To Interest income 7

CA Kinjesh Thakkar

Issue 4 : Loan to Subsidiaries at less than market rate

IGAAP

Accounting of loan to subsidiaries as per AS

Accounting of interest income (yearly)

Practical Issues under Ind AS

Ind AS

Accounting of loan to subsidiaries as per

Loan given to subsidiaries is divided into two parts:

1. Loan amount i.e. fair value of loan as per market rate e.g. 90

2. Investment amount i.e. Differential value based on fair valuation on inception of loan e.g. 10

In the books of Parent

Loan to Subsidiary account 90

Investment in Subsidiary account 10

To Bank account 100

In the books of Parent

Loan to Subsidiary account 10

To Interest income 10

CA Kinjesh Thakkar

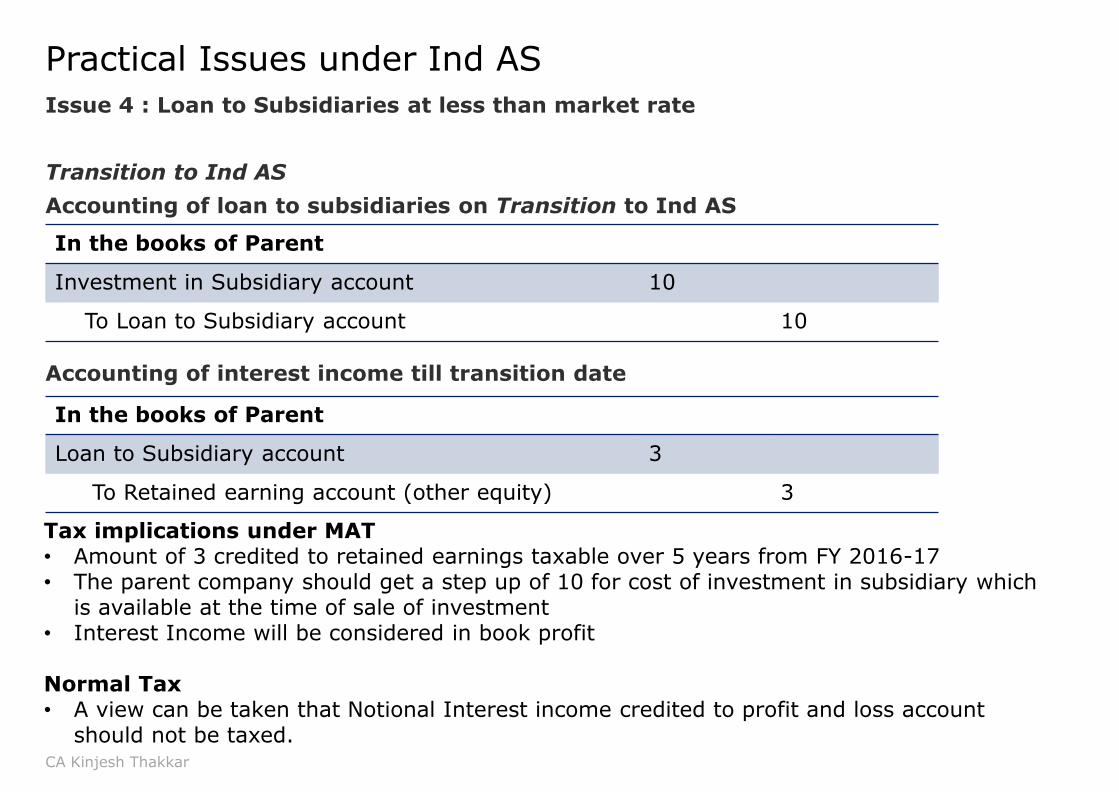

Issue 4 : Loan to Subsidiaries at less than market rate

Accounting of interest income (yearly)

Practical Issues under Ind AS

Transition to Ind AS

Accounting of loan to subsidiaries on Transition to Ind AS

Accounting of interest income till transition date

In the books of Parent

Investment in Subsidiary account 10

To Loan to Subsidiary account 10

In the books of Parent

Loan to Subsidiary account 3

To Retained earning account (other equity) 3

Tax implications under MAT• Amount of 3 credited to retained earnings taxable over 5 years from FY 2016-17• The parent company should get a step up of 10 for cost of investment in subsidiary which

is available at the time of sale of investment• Interest Income will be considered in book profit

Normal Tax• A view can be taken that Notional Interest income credited to profit and loss account

should not be taxed.CA Kinjesh Thakkar

Issue 4 : Loan to Subsidiaries at less than market rate

Practical Issues under Ind AS

Issue 5: Fair Value of Investment

MAT implications

Book profit includes year on year Gain of FVTPL items

1/5th of gain on transition amount included in book profit

FVTPLYear on year gain included in book profit in the year disposal

Gain on transition amount included in book profit in the year on disposal

FVTOCI

Normal Taxation

Taxed under the head Capital gains based on specific

treatment as per Act

CA Kinjesh Thakkar

Practical Issues under Ind AS

Issue 6: Free service on sales

Example:

Sale of Goods – INR 100,000

Free service on same – 4 services of INR 1000 each (cost for service is INR 800)

Accounting under IGAAP

Debtors account 100,000

To Sales revenue account 100,000

Accounting under Ind AS

Debtors account 100,000

To Sales revenue account 96,000

To Deferred revenue account 4,000

On date of free service claim, deferred revenue account will be debited and transferred to sales revenue account.

CA Kinjesh Thakkar

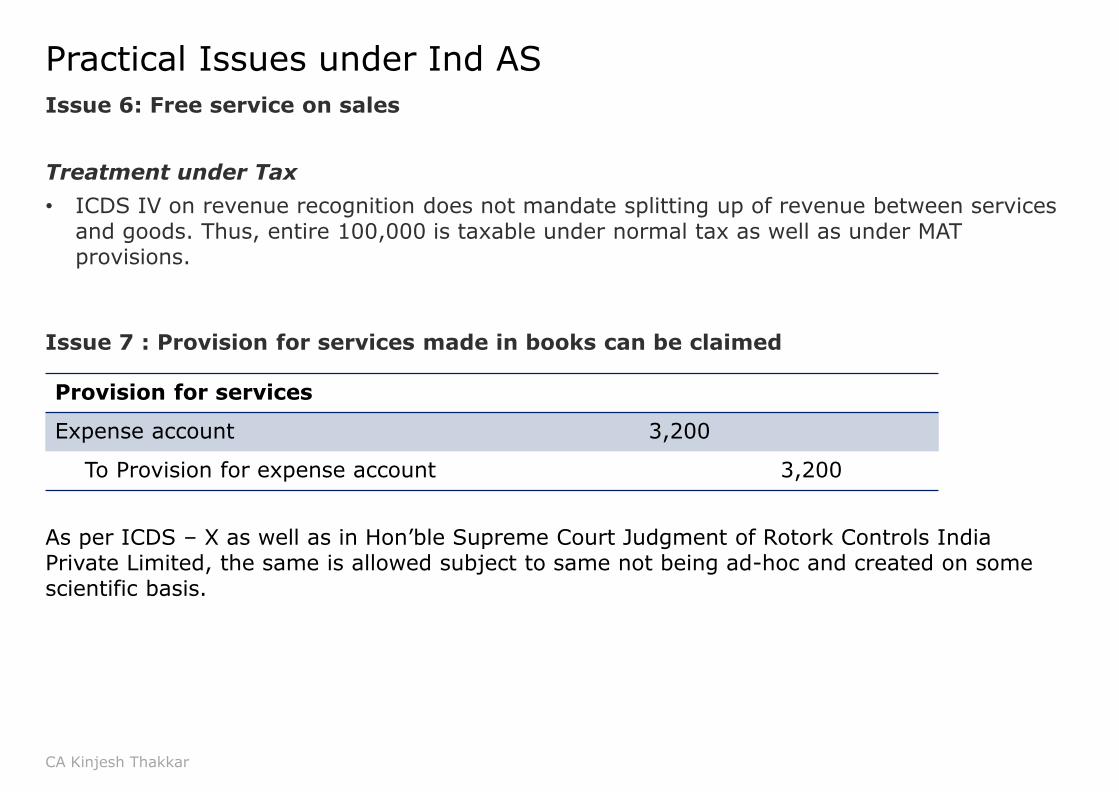

Practical Issues under Ind AS

Issue 6: Free service on sales

Treatment under Tax

• ICDS IV on revenue recognition does not mandate splitting up of revenue between services and goods. Thus, entire 100,000 is taxable under normal tax as well as under MAT provisions.

CA Kinjesh Thakkar

Issue 7 : Provision for services made in books can be claimed

Provision for services

Expense account 3,200

To Provision for expense account 3,200

As per ICDS – X as well as in Hon’ble Supreme Court Judgment of Rotork Controls India Private Limited, the same is allowed subject to same not being ad-hoc and created on some scientific basis.

Practical Issues under Ind AS

• Ind AS 37 mandates creation of provision considering time value of money.

• Discounting of provisions is required in such a scenario.

Accounting under IGAAP

Expense account 100

To Provision account 100

Accounting under Ind AS for creation of provision

Expense account 90

To Provision account 90

Accounting under Ind AS for interest charge YoY

Interest account 4

To Provision account 4

CA Kinjesh Thakkar

Whether for tax computation, provision to be considered at discounted value or at the original value (i.e. Without considering the discounted factor)

Issue 8: Provisions under Ind AS

Practical Issues under Ind AS

Issue 8: Provisions under Ind AS

Possible solution

ICDS X provides that provision should not be discounted

Hon’ble SC Judgment of Rotork Controls India Private Limited read with ICDS X shall be allowed

Normal Tax Discounted value

will be allowed on creation of provision for ascertained liabilities

Interest charge debited YoY shall be allowed in said year

MAT

CA Kinjesh Thakkar

Practical Issues under Ind AS

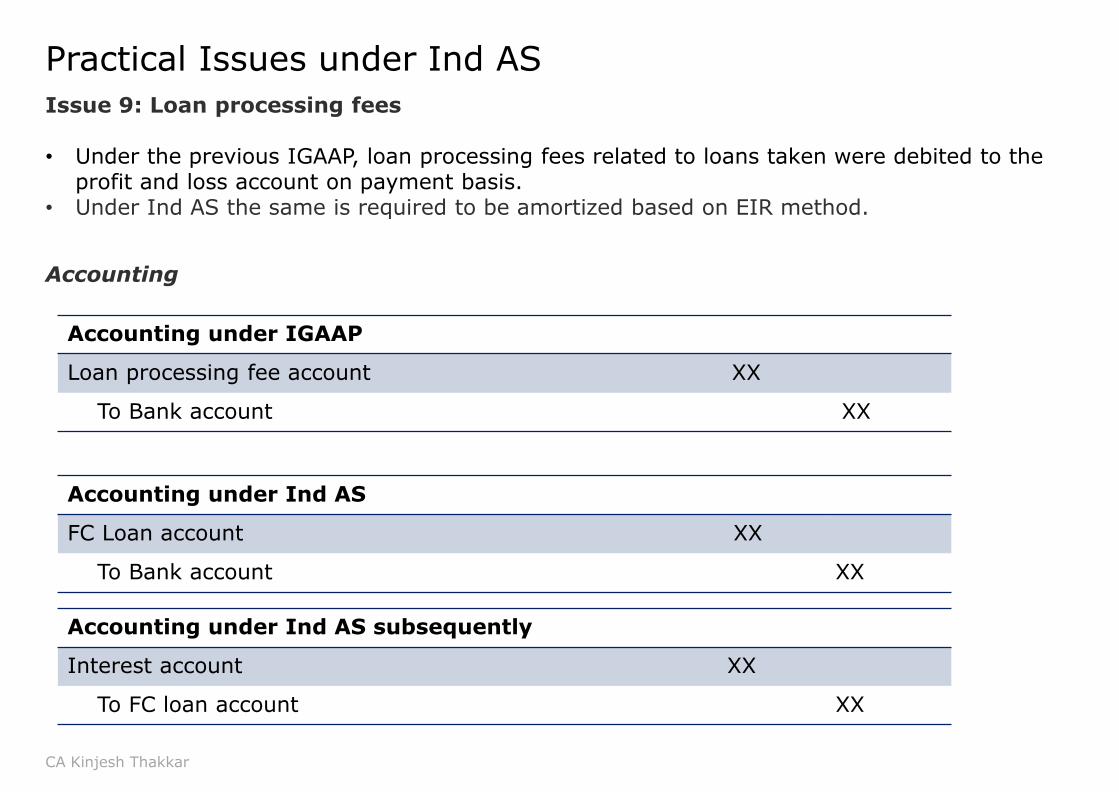

Issue 9: Loan processing fees

• Under the previous IGAAP, loan processing fees related to loans taken were debited to the profit and loss account on payment basis.

• Under Ind AS the same is required to be amortized based on EIR method.

Accounting

Accounting under IGAAP

Loan processing fee account XX

To Bank account XX

Accounting under Ind AS

FC Loan account XX

To Bank account XX

Accounting under Ind AS subsequently

Interest account XX

To FC loan account XX

CA Kinjesh Thakkar

Practical Issues under Ind AS

Issue 9: Loan processing fees

If amount has already been debited till transition date. Then entry in books for unamortized portion shall be:

Accounting on transition date

FC loan account XX

To retained earning account XX

Normal Tax

•Loan processing fees can be considered allowable considering section 2(28A) read with section 36(1)(iii)

•Consider treatment of ICDS-IX

•Once taken as allowable in year of incurrence, amortization should be disallowed.

•Reduction in liability of FC loan won’t impact. However, if tax department adds the said amount, the same can be claimed in year of amortization.

MAT

• Increase in Retained earning on transition shall be included in book profit by 1/5th of amount.

•Year on year charge of interest shall be allowed as deduction in book profit.

•No implication on reduction of FC loan as it does not impact profit and loss account

CA Kinjesh Thakkar

Practical Issues under Ind AS

Issue 10: Defined benefit plan

Actuarial gain/loss on defined benefit plan

Treatment in IGAAP Amount

Current service cost 50

Actuarial (gain)/loss 50

Net debited to profit and loss account 100

Treatment in Ind AS Amount

Items routed through profit and loss

Current service cost 50

Items routed through OCI that will never be re-classified to profit and loss

Actuarial (gain)/loss 50

• Allowed as deduction under MAT

• Allowed under normal tax subject to section 43B and relevant section governing such cost.

• For transition amount, as the same would already have been taken as deduction earlier, it should not be taken in computation of same else it will result in double deduction.

CA Kinjesh Thakkar

Practical Issues under Ind AS

Issue 11: Proposed Dividend

• As per Ind AS, proposed dividend up to transition period is to be reversed since dividend as per Ind AS is recognized in the year of payment of dividend as compared to declaration of dividend under IGAAP.

• On transition to Ind AS, following entry to be passed:

Accounting on transition date

Proposed Dividend XX

To retained earning account (other equity) XX

Normal Tax

•Dividend is not allowed as deduction

•This is post tax item, entails DDT for domestic company.

MAT

•Dividend is not allowed as deduction in computing book profit.

•However, the amount of proposed dividend in year of transition shall be included in other equity as a part of transition amount.

•Thus, without any specific exclusion under 115JB it need to be offered to tax.

Representation has been made to CBDT and clarification is awaited.

CA Kinjesh Thakkar

Issue/Topic ICDS AS Ind AS

Issue 12: Inventories –deferred settlement terms.

Not specifically covered under ICDS.

Not covered specifically Difference between normal purchase price and deferred settlement purchase price is recognized as Interest.

Issue 13: Inventories –allocationof fixed productionOverheads

Allocation of fixed production overheads is based on normal capacity.The actual level of production should be used, if it approximates normal capacity.

The actual level of production may be used, if it approximates normal capacity.

Same as AS

Issue 14: Interest Income

Interest shall accrue on time basis.

Interest accrues, in mostcircumstances, on the time Basis.

Interest shall be calculated by using the effective interest rate method (EIR).

Issue15: Property, Plant and Equipment –estimatedcosts of dismantling, removing or restoring

Not covered by ICDS. No such requirement. The initial estimate of the costs of dismantling and removing the item and restoring the site on which it is located is required to be included in the cost of the respective item of property, plant and equipment.

Practical Issues under Ind AS

CA Kinjesh Thakkar

Questions ???

38CA Kinjesh Thakkar

39

Thank You

CA, CS, M.comContact No: +91 9662255337E-mail ID: [email protected]

Kinjesh Thakkar

Kinjesh Thakkar

The views presented in PPT are personal and subject to changes in law from time to time. It is advisable to consult the consultant before taking any action.