Embed Size (px)

Citation preview

© 2014 Husch Blackwell LLP. All Rights Reserved.

© Husch Blackwell LLP

Bankruptcy’s Impact On Your and Other Creditors’ Business:How to Make the Bad News Better

Ben Mann John Cruciani

© Husch Blackwell LLP

An Overview of Business Bankruptcy & Creditors’ Rights Issues

June 26, 2014 12-1pm CDT

Benjamin F. Mann Partner – Kansas City

John J. Cruciani Partner – Kansas City

© 2014 Husch Blackwell LLP. All Rights Reserved.

An Overview of Chapters 11, 9 and 7 of the Bankruptcy Code

Chapter 11

• Debtor remains in possession – DIP (no trustee‐usually)

• Business operation continues

• Debtor reorganizes or sells business

• Unsecured Creditors Committee is involved in larger cases

Operation of Business in Chapter 11

Debtor-in-Possession (DIP) Free to buy, sell and use property in ordinary course of

business without court approval (§§ 1107 and 363(c)(1)) Use of cash collateral (§ 363(c)(2)) Must provide adequate protection or get secured creditor’s

consent

Borrow post-petition (§ 364) “DIP financing”

Critical payments and vendors (no statutory authority; court made rule)

All of above usually occur in context of “1st-day" motions and hearings)

© 2014 Husch Blackwell LLP. All Rights Reserved.

Operation of Business in Chapter 11

Creditors’ Committee Appointment by U.S. Trustee

Representative of all unsecured creditors

Whether to serve

Sale of Assets (§ 363) Out of ordinary course – requires Court

Approval

Subject to higher bids at hearing

Can be done without Plan or any vote of creditors

Can be free and clear of liens and claims

Chapter 11 Plans & Confirmation

Debtor has the exclusive right to propose plan for 120 days (§ 1121). This Deadline is often extended, maximum is 18 months.

Plan & Disclosure Statement filed (§§ 1123-25) Debtor creates classes of creditors and proposes how to

pay claims per class)

Creditors vote on Plan by Class (§ 1126) 2/3 in $ amount of those voting

More than ½ in number of creditors of those voting

Standards for Confirmation (§ 1129(a)) 13 separate requirements

© 2014 Husch Blackwell LLP. All Rights Reserved.

Chapter 11 Plans & Confirmation

Major Requirements Pay all administrative expense and priority creditors in full Liquidation equivalent to each creditor At least one “impaired” class votes to accept Plan is feasible

Cramdown (§ 1129(b)) Plan can be confirmed without all classes accepting if:

Secured creditors receive payments equal to value of liens Unsecured creditors – 100% of claims or pro rata payment

and no distribution to any junior claims or interest (the “absolute priority” rule)

An Overview of Chapters 11, 9 and 7 of the Bankruptcy Code

Chapter 9

• Adjustment of debts of a Municipality (e.g. cities, counties, water/sewer districts, etc.)

• States themselves are not eligible (i.e. California can’t file, but Orange County can)

• Debtor remains in possession, no trustee ever appointed

© 2014 Husch Blackwell LLP. All Rights Reserved.

An Overview of Chapters 11, 9 and 7 of the Bankruptcy Code

Unlike all other Chapters, Debtor must be insolvent (fail to pay debts as they come due or inability to pay in future)

Chapter 9 Eligibility Requirements

Must Meet the Definition of Municipality

Must Have State Authorization to File

Municipality Must Be Insolvent

Municipality Must Desire to put Together a Plan to Adjust its Debts

© 2014 Husch Blackwell LLP. All Rights Reserved.

General Requirements to Confirm a Chapter 9 Plan of Adjustment

Must be proposed in good faith

Must meet the best interests of creditors’ test: creditors must get at least what they would get if the case

were dismissed and they could pursue whatever rights or remedies they had under state law

The plan must be feasible

Plan treatment must be fair and equitable to the non-accepting classes

An Overview of Chapters 11, 9 and 7 of the Bankruptcy Code

Chapter 7

• Trustee appointed

• Immediate cessation of business (absent rare order, debtor should not be operating)

• Liquidation of all assets by a trustee or secured creditors

© 2014 Husch Blackwell LLP. All Rights Reserved.

An Overview of Chapters 11, 9 and 7 of the Bankruptcy Code

Chapter 7

• The Trustee is the decision maker, subject to court approval

• Debtor does not normally have authority to resolve pre‐petition suits

• The majority of Chapter 7 cases (90%) are no‐asset cases

Other Bankruptcy Chapters

Chapter 12 Exclusively for Debtors that are family farmers (similar to

Chapter 13)

Chapter 13 An individual debt readjustment bankruptcy (Debtors make

monthly payments for 36-60 months)

Chapter 15 Ancillary Proceedings for non-US bankruptcy proceedings

for US assets

© 2014 Husch Blackwell LLP. All Rights Reserved.

Action to Take Upon Knowledge of Bankruptcy Filing

Insure compliance with Automatic Stay

Evaluate 20 Day Claims and Reclamation Claims

File Request for Notices

Review Debtor’s Schedules

File Proof of Claim

Review Status of Any Executory Contracts

Preliminary assessment of preferential exposure and retain records

Section 362 -- The Automatic StayCreditors are prohibited from the following automatically upon the bankruptcy filing Any act to collect debt

Any act to foreclose or seize assets

Any commencement or continuation of lawsuit

Termination of contract

Exercise of setoff rights

There are exceptions to the automatic stay (e.g. criminal proceedings, state regulatory proceedings, certain financial contracts)

© 2014 Husch Blackwell LLP. All Rights Reserved.

Section 362 -- The Automatic Stay

Relief from Stay To obtain your property or collateral

No equity

Not necessary for reorganization

To obtain other relief

For cause

Lack of adequate protection

Executory Contracts in Bankruptcy

Governed by § 365 of the Bankruptcy Code

• Includes contracts (including purchase orders) where performance is remaining on both sides (if only payment by Debtor remains – not executory)

• Also includes unexpired leases

© 2014 Husch Blackwell LLP. All Rights Reserved.

Executory Contracts in Bankruptcy

Debtor’s Options: Assume

Assume & Assign

Reject

Executory Contracts in Bankruptcy

Assumption – Heaven Pay cure costs

Continue performance

Assignment:

Must assume first

Can assign even if prohibited by contract

But assignee must show ability to perform

© 2014 Husch Blackwell LLP. All Rights Reserved.

Executory Contracts in Bankruptcy

• Not a termination – but an authorized breach

• Damages caused by breach – pre‐petition unsecured claim

Rejection:

(a/k/a Hell)

Executory Contracts in Bankruptcy

Deadline on Debtor to Assume or Reject

At time of Confirmation Hearing

Post-Petition/Pre-Assumption or Rejection PURGATORY

Creditor must keep performing but Debtor cannot be compelled to perform

© 2014 Husch Blackwell LLP. All Rights Reserved.

Executory Contracts in Bankruptcy

No protection in bankruptcy law

But UCC § 2-609

Demand for adequate assurance of performance

Remember:

Every supplier relationship can be an executory contract to some extent

Outstanding P.O.s that have been accepted are executory contracts and cannot be unilaterally cancelled or credit terms changed

Special Rules Regarding Intellectual Property

If the Debtor is the licensor and the IP contract is rejected, the licensee can either treat the contract as terminated or retain its rights under the contract.

Proofs of Claim

What Is It: A form (and supporting attachments) that puts the trustee, the court and the debtor on notice that a creditor is asserting it is owed some obligation by the bankruptcy estate

© 2014 Husch Blackwell LLP. All Rights Reserved.

Proofs of Claim

Many larger cases will send out customized proof of claim forms to creditors

While most of the form is self-explanatory, it is important that it be filled out completely

If the debtor is one of several jointly administered cases, be sure to file your proof of claim in the actual case for the debtor(s) that is obligated to you

Attach or Summarize Documentation

Many factors affect whether and how secured and priority creditors file proofs of claim

Proofs of Claim When: (Chapters 7, 12 and 13) Most

creditors must file a proof of claim within 90 days of the § 341 meeting of creditors or such other separate notice that is mailed to all creditors

When: (Chapters 11 and 9) A motion to establish a proof of claim deadline is filed and served

Sometimes referred to as a claims bar date

Creditors receive a copy of the notice of bar date

© 2014 Husch Blackwell LLP. All Rights Reserved.

§ 503(b)(9) Claims (20-Day Claims)

Grants administrative expense priority for the value of any goods received by the debtor within 20 days before the

commencement of the case if goods sold in the ordinary

course of business

New provision added by the 2005 BAPCPA amendments

Provides administrative expense priority to certain pre‐petition

claims

Supplants reclamation rights except for claims between 45‐21

days before filing

Unlike reclamation, no notice requirement

Unlike reclamation, not subject to senior secured lender claims

§ 503(b)(9) Claims (20-Day Claims)

Scope of §503(b)(9) Applies to goods, not services Combination of goods and services

Majority and minority views

Goods must be received by debtor within 20 days before bankruptcy filing

Value presumptively the invoice or purchase price

Ordinary course

© 2014 Husch Blackwell LLP. All Rights Reserved.

§ 503(b)(9) Claims (20-Day Claims)

Manner of asserting a § 503(b)(9) claim No bankruptcy code provision or rule

When – as set by Court – could be separate bar date or same bar date as for regular proofs of claim

How to assert – Proof of Claim (with or without section for § 503(b)(9) claims)

Separate form

File application

§ 503(b)(9) Claims (20-Day Claims)

Payment on claim

• Generally not entitled to immediate payment

• But must be paid upon confirmation of Chapter 11 plan

© 2014 Husch Blackwell LLP. All Rights Reserved.

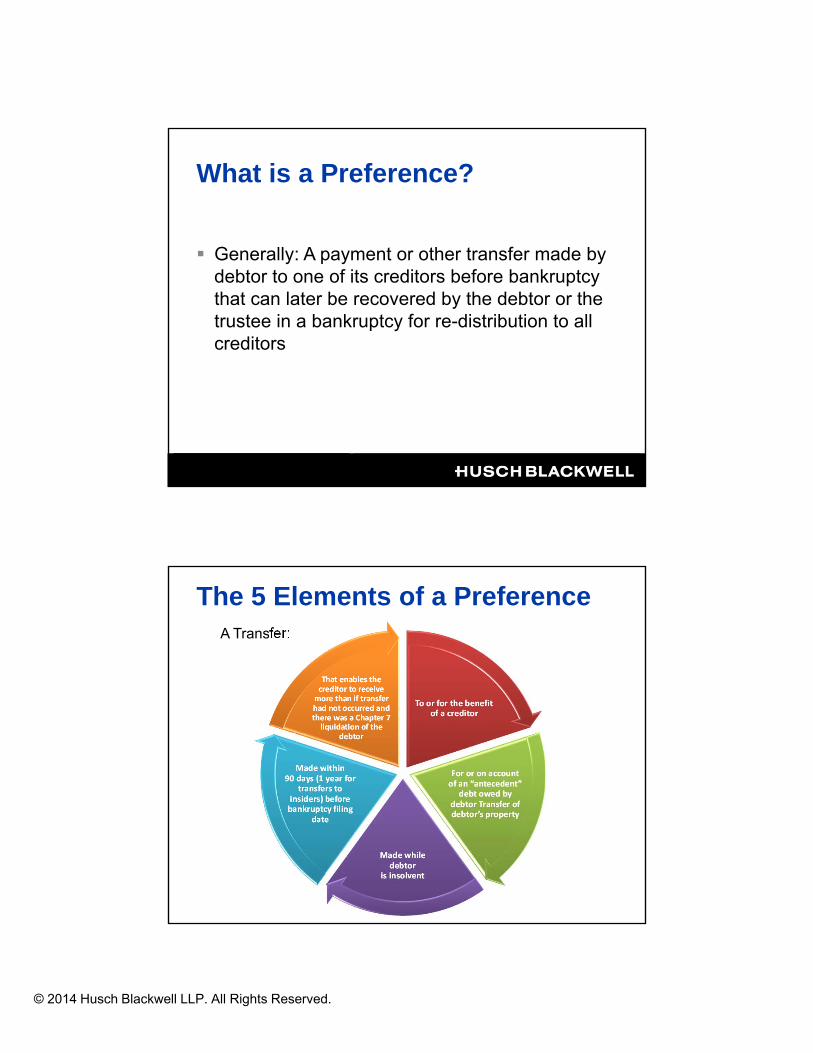

What is a Preference?

Generally: A payment or other transfer made by debtor to one of its creditors before bankruptcy that can later be recovered by the debtor or the trustee in a bankruptcy for re-distribution to all creditors

The 5 Elements of a PreferenceA Transfer:

To or for the benefit of a creditor

For or on account of an “antecedent”

debt owed by debtor Transfer of debtor’s property

Made while debtor

is insolvent

Made within 90 days (1 year for

transfers to insiders) before bankruptcy filing

date

That enables the creditor to receive

more than if transfer had not occurred and there was a Chapter 7 liquidation of the

debtor

© 2014 Husch Blackwell LLP. All Rights Reserved.

Preferences

Preferences asserted 1½-2 years after bankruptcy filing After creditor takes hit on lost pre-petition amounts and

maybe rejection of its executory contract The Debtor or Trustee must generally bring suit to

recover a preference within 2 years of the bankruptcy filing date (but service may be delayed)

Preferences

Steps to minimize exposure when customer is a “bankruptcy risk” Convert to prepayments

If reaching agreement to pay down old debt, reaffirm new sales will be paid according to terms and apply all payments first to current payables

Avoid changing terms or practice that has existed for long period

© 2014 Husch Blackwell LLP. All Rights Reserved.

Preferences

What to do when bankruptcy is filed Determine preference exposure

Maintain and secure payment history records and backup documents for two-year period before bankruptcy

Make sure “write-offs” for bankruptcy are not reflected as paid

Challenging Preference Claims

There are several possible defenses to defeat some or all of a preference claim including, among others: Subsequent new value

Ordinary course of business

Contemporaneous exchange

© 2014 Husch Blackwell LLP. All Rights Reserved.

Avoidance Powers

A Trustee and DIP have same powers Strong-Arm Clause (§ 544) power to avoid transaction

which could be avoided by hypothetical lien creditor e.g. unperfected security interests and state law UFTA claims

Invalidate certain statutory liens (§ 545) Rent

Which arise upon Debtor’s insolvency

Fraudulent Transfers & Obligations (§ 548)

Fraudulent Conveyances (§ 548)

Avoid transfers or obligations by Debtor if within 2 years of bankruptcy if Done with actual intent to “hinder, delay or defraud”

present or future creditors OR

In exchange for “less than reasonably equivalent value” and Debtor was insolvent in any of 3 ways Balance sheet

Undercapitalized

Unable to pay as come due

© 2014 Husch Blackwell LLP. All Rights Reserved.

Setoffs (§ 553) Common law rights preserved but exercise of

rights stayed by automatic stay Limitations

Mutuality Contractual Parties Strictly Construed Debtor affiliates Creditor affiliates

Pre/Post Bankruptcy Distinction Other Limitations

Acquiring claims to create setoffs within 90 days Setoffs done within 90 days if there is net improvement

Recoupments

Recoupment is not a bankruptcy concept, but rather common law. It requires that the claims arose out of the same transaction,

without the timing requirements of setoff. Recoupment does not require that both claims arise before the petition date.

Courts have often classified recoupment as a defense to payment by allowing one party to a transaction to withhold funds due to another party sufficient to recover an obligation owed by that other party and which arises from the same transaction

© 2014 Husch Blackwell LLP. All Rights Reserved.

How to Improve the Plight of the

Unsecured Creditor in Bankruptcy

1. Security Interest

2. Other Credit Enhancementsa. Guaranties

b. Letters of Credit

c. Mechanics (or other statutory) liens

3. Credit Insurance

© 2014 Husch Blackwell LLP. All Rights Reserved.

Advantages / Disadvantages in Bankruptcy for Secured Creditor

Advantages:

Potential for relief from stay to foreclose

Each secured creditor is in separate class

Interest and attorneys’ fees recoverable if creditor is oversecured

Disadvantages:

Existing blanket lienholder has negative pledge

Second lien position may have no value

Delays in filing can create preferences

Advantages / Disadvantages in Bankruptcy for Secured Creditor

© 2014 Husch Blackwell LLP. All Rights Reserved.

Other Credit Enhancements

1. Guaranty by Third PartyAdvantage: Not subject to automatic stay

Disadvantage: Still subject to collection risks and costs

2. Letter of CreditAdvantage: Not subject to automatic stay

Virtually no collection risks or costs

Disadvantage: Debtor reluctant to give because it costs money

3. Mechanics and Other Statutory LiensKey is to anticipate and complete filing steps

Credit Insurance

What is Credit Insurance? A contract with a third party that provides for

payment to you in the event your customer doesn't pay or goes bankrupt

Not as common in the U.S. as in other parts of the world, but it is becoming more popular

© 2014 Husch Blackwell LLP. All Rights Reserved.

Credit Insurance

Two major types of insurance Insurance for some or all of your A/R portfolio

Insurance specific to a certain customer

Advantages of credit insurance Provide a guaranty of payment

Not normally dependent on amount of bankruptcy distribution

Hedges some of your credit risk

Don't have to insure all of your potential exposure

Peace of mind for a troublesome customer

Credit Insurance

© 2014 Husch Blackwell LLP. All Rights Reserved.

Disadvantages of credit insurance Can be extremely expensive

Fully earned/non-refundable premiums

If your claim is for goods with § 503(b)(9) treatment, may not put you in a better position

There are additional steps/items required compared to a typical bankruptcy

You may not have purchased enough insurance

Credit Insurance

Non-Bankruptcy Proceedings

Receiverships ABCsState Law Insolvency Proceedings

© 2014 Husch Blackwell LLP. All Rights Reserved.

Receiverships

Receiverships Receiverships can be broadly or narrowly tailored to

preserve and protect particular property interests

Multiple possible parties involved: Lender may need a receiver for its collateral

Subordinate party who has an interest

Property owner that is the subject of the receivership

Unsecured creditor

ABCs

Assignments for the Benefits of Creditors (ABCs) It is the voluntary state court equivalent to a Chapter 7

(liquidation) bankruptcy.

An “assignee” is appointed. The assignee is assigned all assets of the debtor, and the assignee marshals and liquidates these assets for the collective benefit of the debtor’s creditors.

Typically only those creditors that assent receive distributions.

© 2014 Husch Blackwell LLP. All Rights Reserved.

State Law Insolvency Proceedings

Minority of states have statutory proceedings including preference recovery provisions

Some have other bankruptcy‐type provisions (cash collateral usage and free and clear sales) e.g. Wisconsin and California

Sole Source Suppliers

Many times, a particular customer will be the only producer of a critical part or component for a product

Financial distress or bankruptcy can interrupt the supply of this good or part

© 2014 Husch Blackwell LLP. All Rights Reserved.

Alternatives may be available to attempt to keep the flow of goods uninterrupted Purchasing raw materials directly, prepaying for goods

or other accommodations

Important to try to recognize these situations as early as possible

Often it is time-consuming to get another supplier approved and operational Particularly true for precision products

Sole Source Suppliers

You may provide proprietary tooling or dies to customers who manufacture parts for us

Important to look at any written agreement regarding ownership of tooling or dies

Tooling/Dies/Goods in Possession of our Customers

© 2014 Husch Blackwell LLP. All Rights Reserved.

Tolling/Dies/Goods in Possession of our Customers

UCC 9-505 allows a financing statement to be filed as a "precautionary filing" to put the world on notice of our ownership rights

Enter into bailment agreements to set forth the parties’ rights and obligations Better to do this when the relationship is good

If a customer files bankruptcy may want to seek relief from automatic stay to recover property.

Also, important to monitor for asset sales to make sure they don’t try to sell our tooling, dies or other proprietary products

Tolling/Dies/Goods in Possession of our Customers

© 2014 Husch Blackwell LLP. All Rights Reserved.

Questions?

John CrucianiPartner

Kansas City, MO

816.983.8197

Ben MannPartner

Kansas City, MO

816.983.8126

Thank You!

![Bankruptcy's 5 Most Pressing Questions: [FAQ] Answered](https://img.pdfslide.us/doc/110x75/587d561d1a28abee158b5a23/bankruptcys-5-most-pressing-questions-faq-answered.jpg)