Embed Size (px)

Citation preview

Bankruptcy Basics

Wendi FreemanFreeman | Wine, LLC

1040 eWall Street

Mt. Pleasant, SC 29464

843-849-1900

December 13, 2013

“How did you go bankrupt? Two ways. Gradually, then suddenly.”

-Ernest Hemingway, The Sun Also Rises

Types of Bankruptcy

• Chapter 7

• Chapter 13

• Chapter 11

• Chapter 12

• Chapter 9

• Chapter 15

Chapter 7 – Liquidation or Straight Bankruptcy

• Nationally more people file chapter 7 than any other type of bankruptcy.

• According to the Federal Judiciary, of the 1,410,653 bankruptcies filed in 2011, 992,332 were chapter 7 (70%).

• Chapter 7 provides for “liquidation” of a debtor’s non-exempt assets to pay a distribution to the creditors.– If assets are sold, unsecured creditors receive payment on a

pro-rata basis.

– In the majority of the cases filed, debtors do not have any nonexempt assets. There are called “no-asset cases.”

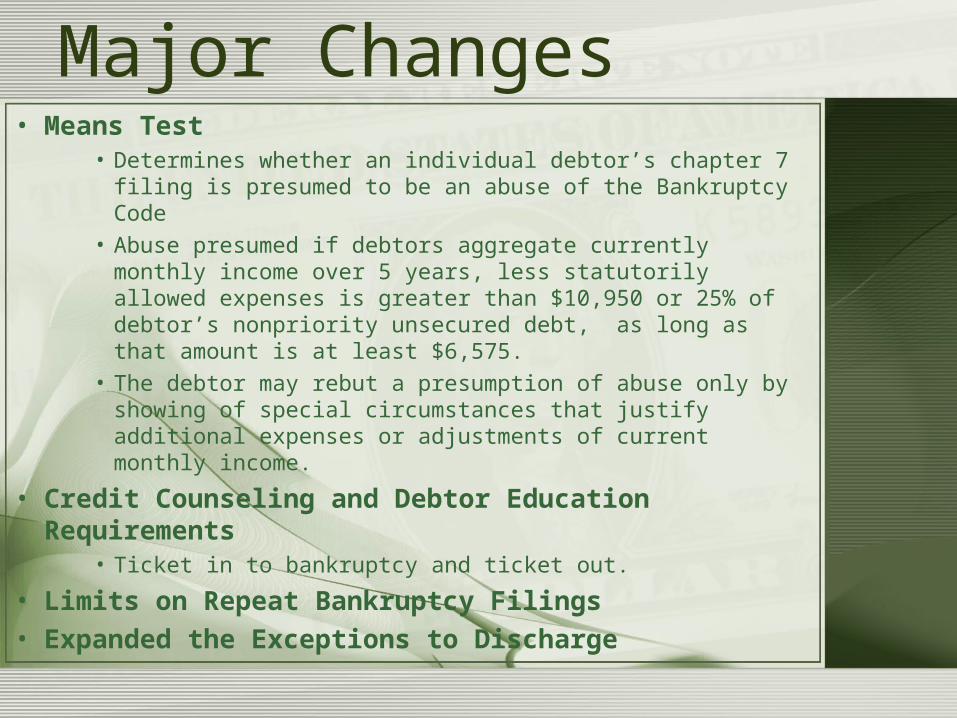

Major Changes• Means Test

• Determines whether an individual debtor’s chapter 7 filing is presumed to be an abuse of the Bankruptcy Code

• Abuse presumed if debtors aggregate currently monthly income over 5 years, less statutorily allowed expenses is greater than $10,950 or 25% of debtor’s nonpriority unsecured debt, as long as that amount is at least $6,575.

• The debtor may rebut a presumption of abuse only by showing of special circumstances that justify additional expenses or adjustments of current monthly income.

• Credit Counseling and Debtor Education Requirements• Ticket in to bankruptcy and ticket out.

• Limits on Repeat Bankruptcy Filings

• Expanded the Exceptions to Discharge

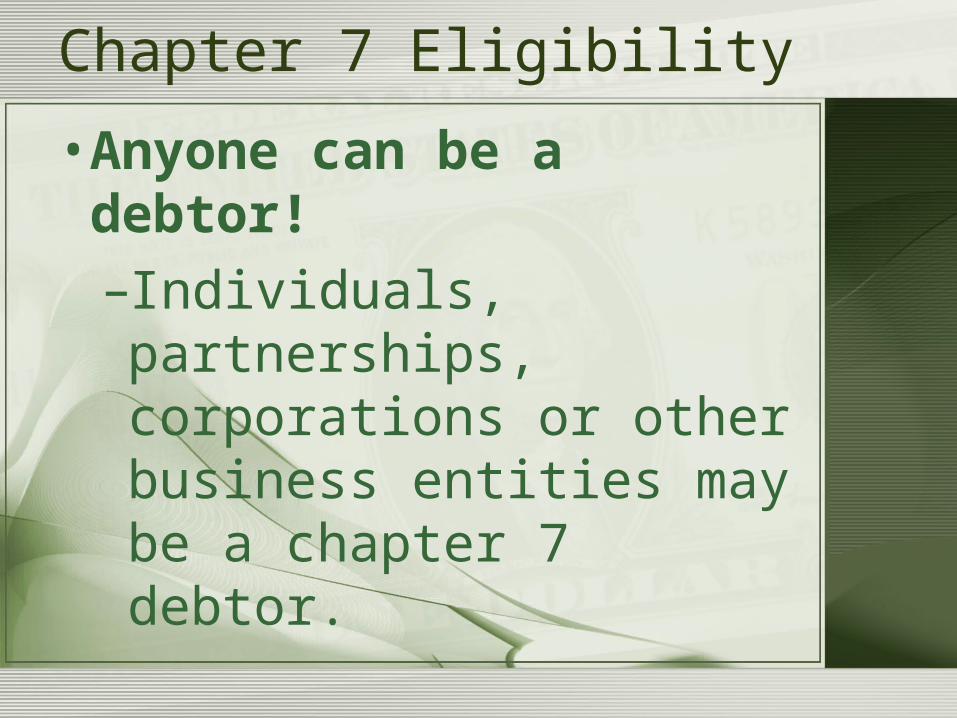

Chapter 7 Eligibility

• Anyone can be a debtor!

–Individuals, partnerships, corporations or other business entities may be a chapter 7 debtor.

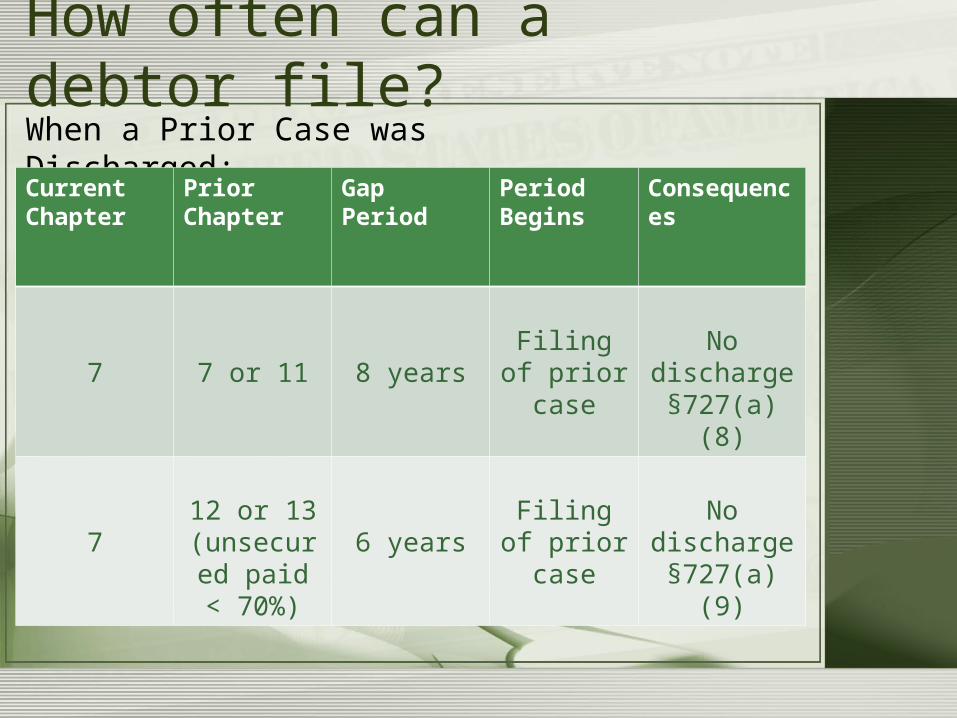

How often can a debtor file?When a Prior Case was Discharged:

Current Chapter

PriorChapter

GapPeriod

PeriodBegins

Consequences

7 7 or 11 8 yearsFiling of prior case

No discharge §727(a)(8)

712 or 13

(unsecured paid < 70%)

6 yearsFiling of prior case

No discharge§727(a)(9)

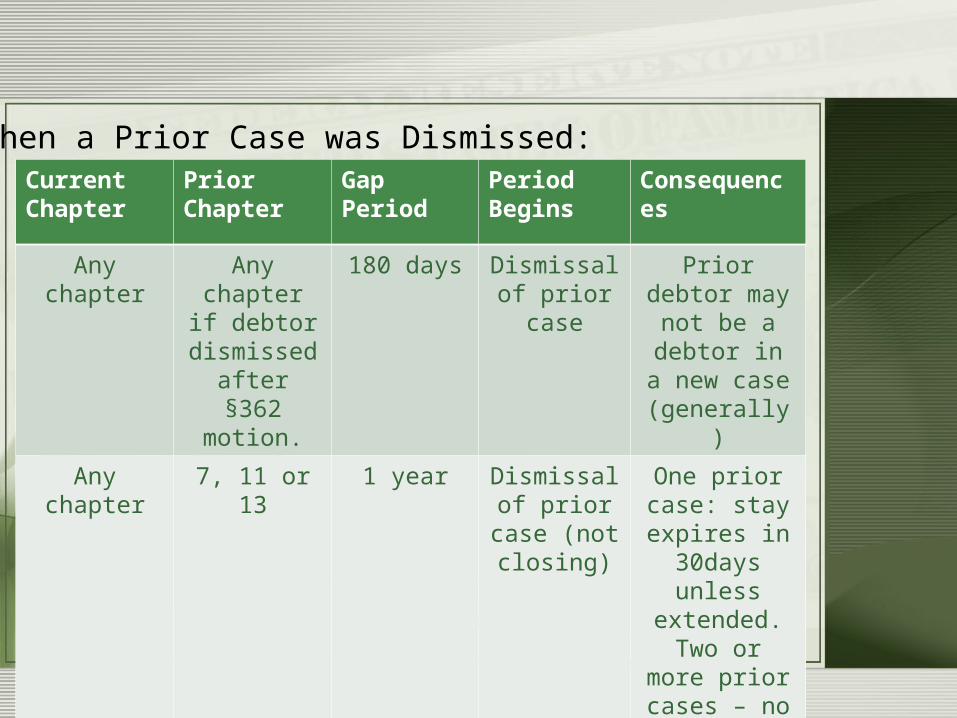

CurrentChapter

PriorChapter

GapPeriod

PeriodBegins

Consequences

Any chapter Any chapter if debtor

dismissed after §362

motion.

180 days Dismissal of prior case

Prior debtor may not be a

debtor in a new case (generally)

Any chapter 7, 11 or 13 1 year Dismissal of prior case

(not closing)

One prior case: stay expires in 30days unless extended. Two or more prior

cases – no stay unless imposed

§362(c)(4)

When a Prior Case was Dismissed:

Chapter 7 Trustee• The United States Trustee Program is part of the

Department of Justice responsible for overseeing the administration of bankruptcy cases and private trustees under 28 U.S.C. §586 and 11 U.S.C. §101, et seq.– The regional USTP appoints case trustees to manage chapter 7

cases. • 2 chapter 7 trustees in the Charleston district.

– Preside over §341 hearings

– Question debtors under oath about assets, debts, income, expenses and financial transactions

– Determine whether there are nonexempt assets that can be liquidated.

• If nonexempt assets exist, the trustee will notify creditors to file proofs of claims. The trustee then sells the assets and pays the unsecured creditors on a pro-rata basis.

Chapter 7 Discharge• In a chapter 7 case, an individual debtor discharges or

eliminates personal liability for most unsecured debts and keeps all nonexempt property.

• Examples of unsecured debt:

– Credit Cards

– Medical Bills

– Personal Loans

• Corporations, partnerships and other business entities are not entitled to a discharge.

There have been 7,136 bankruptcy cases filed in South Carolina as of December 1, 2013.

Chapter 13 – Wage Earner’s Plan

• Allows individuals with regular income to adjust their debt.

• Adjustment is done through a “plan” proposed by the debtor and approved by the court to repay all or some debt over 3 to 5 years.

• In South Carolina, 7,936 bankruptcy cases were filed in 2012. Of those bankruptcies, approximately 56% were chapter 13s.

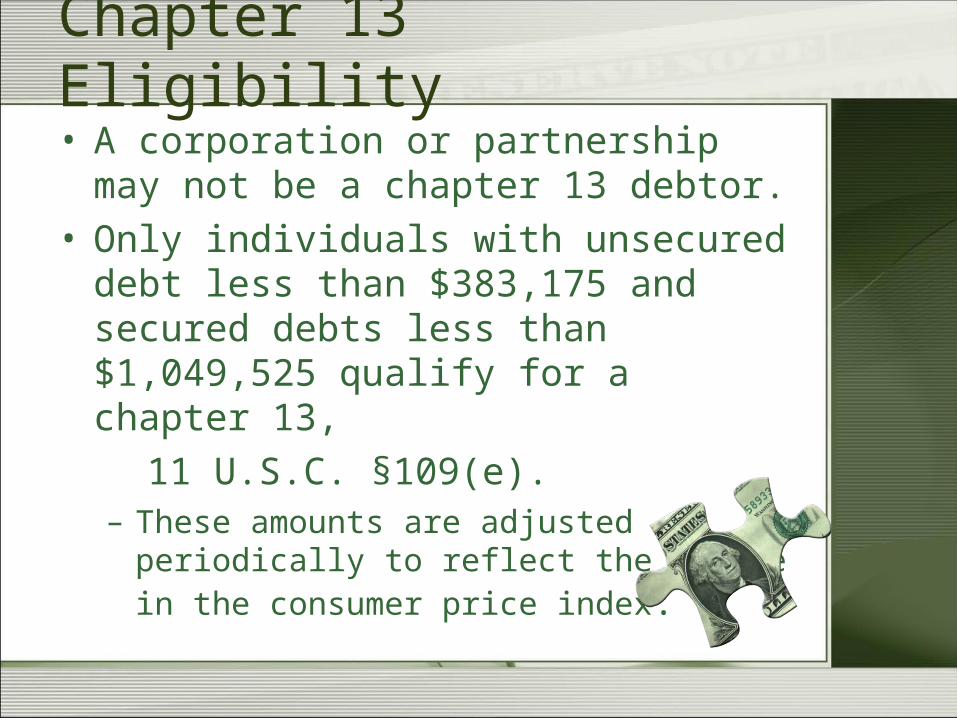

Chapter 13 Eligibility• A corporation or partnership may not be a

chapter 13 debtor.• Only individuals with unsecured debt less than

$383,175 and secured debts less than $1,049,525 qualify for a chapter 13,

11 U.S.C. §109(e).– These amounts are adjusted periodically to reflect

the change in the consumer price index.

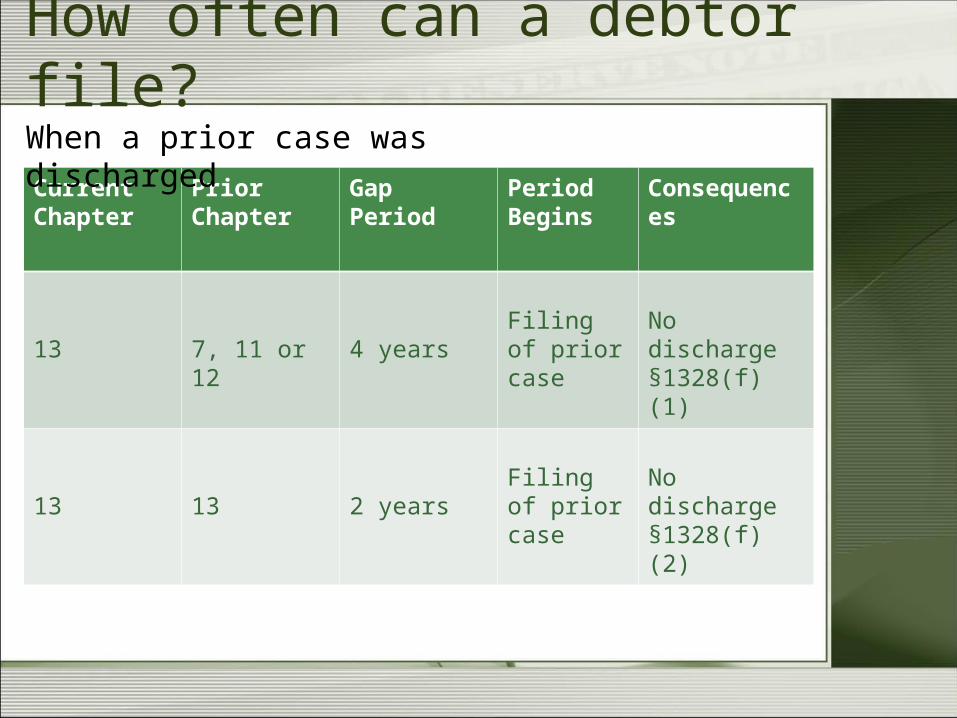

How often can a debtor file?

CurrentChapter

PriorChapter

GapPeriod

PeriodBegins

Consequences

13 7, 11 or 12 4 yearsFiling of prior case

No discharge §1328(f)(1)

13 13 2 yearsFiling of prior case

No discharge§1328(f)(2)

When a prior case was discharged

Chapter 20 (13+7=20)• The filing of a chapter 13 shortly after

discharging a majority of a debtor’s liabilities in a chapter 7.

• While a debtor is not able to receive a discharge in the chapter 13, it can be useful to pay nondischargable debt or mortgage arrearage.

Chapter 13 Trustee• Does not liquidate a debtor’s assets.

• Evaluates the debtor’s financial affairs and makes recommendations to the court.

• Reviews the bankruptcy petition and schedules.

• Assures that income calculations are accurate and expenses are reasonable.

• May object to bankruptcy plan.

• Responsible for obtaining the greatest return to unsecured creditors.

• Accepts monthly payments from debtors

to pay the proofs of claims filed in a case.

Why File a Chapter 13?• May allow a debtor to keep nonexempt assets.

• May stop a foreclosure and allow debtors to repay past mortgage balances.

• Lengthens the term of a some secured debt.

• Reduces the interest rate on a loans secured by personal property.

• Can wipe out judgment liens.

• Eliminates second or third mortgages when the real estate is worth less than the first mortgage balance.

• Restructures tax debt.

• Debtors are permitted to modify the rights

of many secured creditors to pay only the

value of the security interest (11 U.S.C. §1322).

Valuation Rules• 910-Day Rule

– In order to prevent people from buying a new car and cramming down the loan soon after driving it off the lot, the debtor must have purchased the car at least 910 days prior to the bankruptcy filing.

• One-Year Rule– Similar to the 910-day rule for cars, but applies to all other

personal property. It requires that the goods be purchased at least one year prior to the bankruptcy before a cram down is allowed.

Determining the amount unsecured creditors receive

• Debtor’s disposable income.

• Means Test

• Nonexempt Assets.– Hypothetical liquidation test

Chapter 11

• Called Reorganizations

• Can file if debt exceeds chapter 13 limits

• Ordinarily used by commercial entities seeking to continue operating the business and repay creditors through a court-approved plan of reorganization.

• Can reduce debt, prepay a portion of a debtor’s obligation and discharge.

• Able to terminate burdensome contracts and leases, recover asset and reorganize to become profitable.

Chapter 12

• Adjusts the debts of family farmers or fishermen with regular annual income.

• Similar to a chapter 13 in which the debtor proposes a plan to repay debts over 3 to 5 years.

Chapter 9

• Permits municipalities to adjust their debt.

• A prime example of a chapter 9 is Detroit’s bankruptcy filing.

• Largest municipality in US history to enter Chapter 9 bankruptcy.

Chapter 15

• Allows authorized foreign representatives to obtain relief from a U.S. Bankruptcy Court to aid in the administration of a foreign insolvency proceeding.

• Debtors must have its “center of main interests” (COMI) in a foreign country.

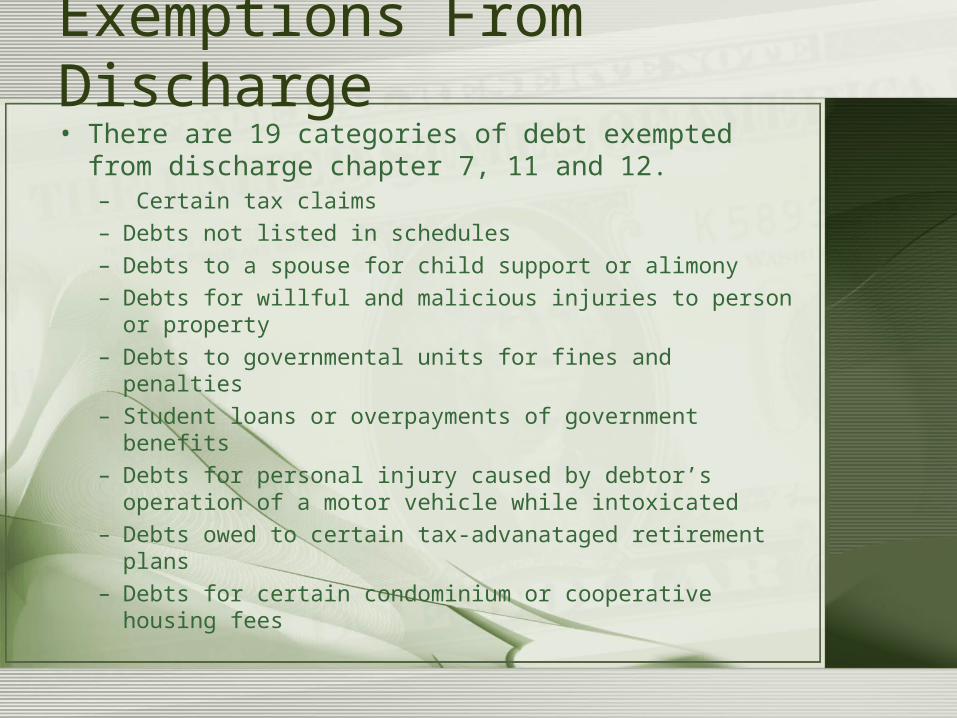

Exemptions From Discharge• There are 19 categories of debt exempted from

discharge chapter 7, 11 and 12.– Certain tax claims

– Debts not listed in schedules

– Debts to a spouse for child support or alimony

– Debts for willful and malicious injuries to person or property

– Debts to governmental units for fines and penalties

– Student loans or overpayments of government benefits

– Debts for personal injury caused by debtor’s operation of a motor vehicle while intoxicated

– Debts owed to certain tax-advanataged retirement plans

– Debts for certain condominium or cooperative housing fees

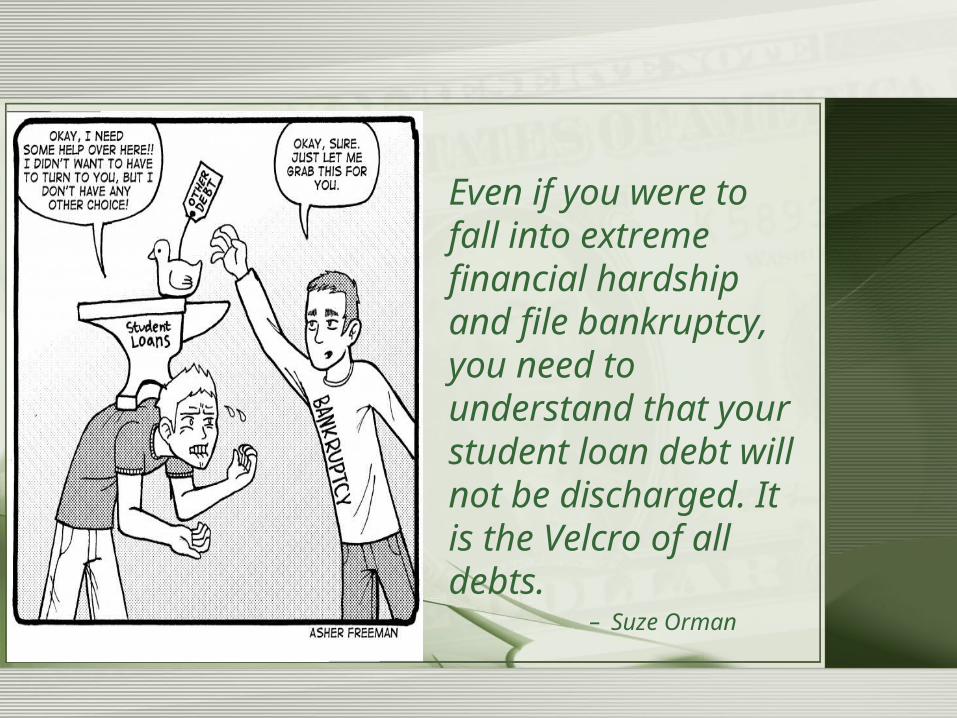

Even if you were to fall into extreme financial hardship and file bankruptcy, you need to understand that your student loan debt will not be discharged. It is the Velcro of all debts.

– Suze Orman

![Design Pattern 1 [Eric Freeman & Elisabeth Freeman 1 – 5 ]](https://img.pdfslide.us/doc/110x75/56649cf15503460f949c07c5/design-pattern-1-eric-freeman-elisabeth-freeman-1-5-.jpg)

![[Gordon R. Freeman and Phyllis J. Freeman] Stonehenge Archeology](https://img.pdfslide.us/doc/110x75/5571f81e49795991698cacea/gordon-r-freeman-and-phyllis-j-freeman-stonehenge-archeology.jpg)