Embed Size (px)

Citation preview

Bank Ownership and Expansion of the Financial System in

Thailand

Juliano Assunção∗

Sergey Mityakov⊥

Robert Townsend⊕

Abstract

This paper studies bank ownership and different aspects of the financial

expansion in Thailand through a dynamic spatial competition model. Data

suggest that ownership matters. BAAC, a government development bank in

Thailand, expands into poorer and less populated villages and villages more

distant from the markets, while commercial banks' entry has positive

correlation with wealth/population and proximity to markets. Assuming

that commercial banks maximize profits and BAAC maximizes total access to

finance, the model not only matches the profile of bank expansion in data,

but also explains key characteristics of the interaction between BAAC and

commercial banks – the existence of commercial banks affect the behavior of

the BAAC, and commercial banks locate in clusters while BAAC doesn’t.

(VERY PRELIMINARY – PLEASE DO NOT QUOTE)

∗ PUC-‐Rio, Department of Economics, [email protected]‐rio.br ⊥ Clemson University, The John E. Walker Department of Economics, [email protected] ⊕ University of Chicago and MIT, Department of Economics, [email protected]

1 Introduction

Does bank ownership affect the expansion of the financial system? How do private banks

change the behavior of government development banks?

Government ownership of banks is a common phenomenon around the world -‐ on average,

42 percent of the equity of the 10 largest banks in 92 countries was owned by the

government in 1995 (La Porta, López-‐de-‐Silanes and Shleifer 2002). The literature on the

consequences of government ownership of banks is still thin and primarily focused on the

influence of political objectives in the determination of lending policies of state-‐owned

banks (Sapienza 2004; Khwaja and Mian 2005; Dinç 2005; Micco, Panizza and Yañes 2007).

This paper studies geographical location as another potential channel through which

government ownership matters. The analysis is based on the comparison between the

behavior of a government development bank (BAAC) and that of commercial banks in a

period of financial expansion in Thailand. We assume that the locations of both BAAC and

commercial banks are endogenous. We build a structural model to investigate the

geographical expansion of BAAC and commercial banks. The model is a dynamic sequential

entry game between BAAC and commercial bank(s), where the players compete by opening

offices in different locations. We explicitly incorporate geography in the model by assuming

that villages constitute a weighted graph with weights reflecting village characteristics

influencing profits of the banks (e.g. wealth, population, etc).

The model interacts with the data in different aspects of the main assumptions adopted and

the empirical implications derived.

First, the model incorporates the evidence that BAAC and commercial banks are aiming at

different tasks. Commercial banks’ access is positively correlated with wealth and

proximity to markets, evidence that lead us to assume that commercial banks are

maximizing profits. BAAC, on the other hand, expands into poorer villages and villages that

are more distant from the markets. Even controlling for (per capita) wealth and other

village characteristics, BAAC tends to expand into less populated areas. Thus, data make it

difficult to consider that BAAC is maximizing profits or targeting poverty. We then assume

that BAAC maximizes the total access to finance in the model -‐ an assumption which is

compatible with the observed patterns.

Second, the model matches the empirical pattern of change in the behavior of BAAC when

facing commercial banks. Data show that the presence of BAAC is positively correlated

with population in provinces with low penetration of commercial banks. This correlation

decreases according to the presence of commercial banks. The model generates this

pattern. In an economy without commercial banks, BAAC expands first into the more

populated areas. This behavior changes substantially when commercial banks are present.

If the BAAC puts enough weight on the future, BAAC has an incentive not to serve the best

markets first, since it anticipates these markets are quickly attended by commercial banks.

The behavior of commercial banks, on the other hand, is less affected by the presence of

BAAC. With or without BAAC, commercial banks serve first the best locations. BAAC is

treated as a competitor that prefers to attend the less profitable locations first and do not

affect the choices of commercial banks in the first stages of interaction.

Third, the model also explains the differences we observe in the pattern of spatial

distribution of BAAC and commercial banks. We approximate the reaction functions of the

model based on a spatial regression approach suggested by Chen and Conley (2001). We

show that BAAC expansion in each village is correlated with changes in villages at a wide

range of distances, while commercial banks changes are correlated only with changes in

nearby villages. Commercial banks seem to be clustered and BAAC is distributed more

uniformly across Thailand. This evidence is compatible with some key examples derived

from the model, where commercial banks are clustered around large markets while BAAC

goes to more isolated areas.

Our paper is also related to the literature of dynamic spatial competition that studies

similar questions though in different contexts.

Chan, Padmanabhan, and Seetharaman (2006) use geographical location model to estimate

the spatial interaction between different gasoline stations in Singapore. However, they do

not model location choice per se: gas stations locations are chosen by the benevolent

government. Contrary to that in our paper we take demand for financial services and

structure of bank competition as given and try to explain the location choice of BAAC and

commercial bank offices. In this sense this paper is complementary to ours. Aguirregabiria,

and Vicentini (2006) employs multiperiod simultaneous move game to analyze location

choice of multistore firms.

Holmes (2005) looks at the expansion of Wal-‐Mart through the lens of a dynamic model.

The author estimates economies of density which he argues is an important determinant of

Wal-‐Mart's choice of new stores locations. However, in that paper there is only one player

(Wal-‐Mart) and its competition with other chains is not modeled explicitly. Whereas in our

paper competition between commercial banks and BAAC is crucial in explaining BAAC

behavior.

Paper by Schmidt-‐Dengler (2006) is the closest reference to our model. The author also

studies a dynamic sequential move game to analyze new technology (MRI) adoption by the

US hospitals taking hospital payoff structure as exogenous. However, there is rather

important difference: players in his paper have the same objective (profit maximization). In

our paper on the contrary we are trying to reconcile observed differences in behavior

between BAAC and commercial banks by assuming that objective functions of these banks

are different. In particular, we assume that commercial banks maximize profits, and then

choose objective function for BAAC trying to match observed empirical patterns.

2 Background

We study the behavior of commercial banks and the Bank for Agriculture and Agricultural

Cooperative (BAAC).

BAAC is a State Enterprise created in 1966 to finance agricultural activities of farmers and

farmer institutions. BAAC is organized in a three tier structure comprising head office,

branch offices and field offices. The head office is located in Bangkok. Branch offices are

located in the provincial centers and district towns. And field offices, which are the bank’s

front line of contact with the farming communities, are located in towns.

The operation of BAAC is decentralized. Each field office has an average of three to five

officers, each one responding for around 700 client farmers. Field officers are supervised

by a field office chief, who reports directly to the respective branch manager.

BAAC offer a package of services that includes savings, credit, and payment and transfers of

funds. Credit conditions and requirements are flexible, accepting different kinds of

collateral -‐ land titles, government securities, saving deposits or joint liability agreements

(Tambunlertchai 2004).

We analyzed the period from 1986 to 1996, which was characterized by a substantial

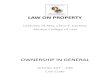

financial expansion. Figure 1 shows a sharp increase in the number of branches, especially

for the case of BAAC. Number of branches for BAAC has increased from 79 to 502 in the

whole country, while the ratio population per BAAC branch decreased from 462 thousand

individuals per branch to 67 thousand individuals per branch. Commercial banks opened

more than 2,000 branches in the same period.

[Figure 1 -‐ Number of branches and Outreach]

Data depicted in figure 1 shows an increase in the number of bank branches. There is a

monotonic increase in the number of branches of both BAAC and commercial banks, which

have determined a substantial reduction in the population to branch ratio. Although this

clearly shows the expansion of the financial system in Thailand, the information on bank

branches represents only one dimension of the supply of financial services in the period.

Branches are concentrated in some areas – for example, 27% of the branches are located in

5 provinces (out of 53 provinces in the country). Population in Thailand is relatively

dispersed in approximately 50,000 villages and, consequently, there is another aspect of

the provision of financial services through credit officers.

In order to better characterize the change in the access to financial services, we also use

data from the Thai Community Development Department (CDD) survey that is presented in

the following section. This data indicate that the fraction of villages without access to BAAC

decreased from 20% in 1986 to 5% in 1996. For the case of commercial banks, the same

indicator decreased from 73% to 56%. Both the branch and credit use perspectives show a

significant financial expansion in the period from 1986 to 1996.

The comparison between the branch data and the CDD survey also illustrates how

important field officers are for the BAAC operation. Even with a lower number of branches,

BAAC attends a substantial higher number of villages.

3 Data description

As mentioned above, we have data from two main sources. The first one is a list of all bank

branches in Thailand with address, date of entry and exits, obtained from the Bank of

Thailand. This data comprise all branches opened from 1943. All branches were geo-‐

located.

[Table 1 -‐ Descriptive statistics -‐ CDD data]

The second data source is the Thai Community Development Department (CDD) survey,

conducted every two year from 1986 to 1996. Table 1 depicts summary statistics for the

1986 and 1996 years. There are binary variables indicating the use of financial providers

(BAAC and commercial banks). We also have information on population, education, a

wealth index based on the number motorcycles, pick-‐up trucks and flush toilets per 1000

villagers, and distance to the market.

[Figure 2 -‐ Thai regions and provinces]

[Figure 3 -‐ CDD selected villages and amphoe district center locations]

CDD data are organized in samples with two levels of aggregation -‐ amphoe-‐level data and

village-‐level data. The amphoe-‐level sample comprises the whole country, with 704 geo-‐

located observations. The village-‐level data consists in two samples. The full sample covers

villages from the whole country for which we have data -‐ more than 24,000 villages. But

this full sample is not geo-‐located. In order to characterize the geographical patterns at the

village-‐level, we use a restricted sample of villages from four chosen provinces, out of

Thailand's 73 provinces as shown in figure 2. The selected provinces are presented in

figure 3 and were chosen to represent the strong regional economic and environmental

variation exhibited in Thailand. We have a total of 3,391 geo-‐located villages -‐ 1,300

villages in Sisaket, 1,230 in Buriram, 419 in Lop Buri and 442 in Chachoengsao.

4 The profile of financial expansion for BAAC and commercial banks

This section characterizes the profile of financial expansion in Thailand. We start showing a

comparison between our two main data sources. Table 2 presents regressions of the credit

use, as measure in CDD data, on the respective number of branches on that category, at the

amphoe-‐level of aggregation, for levels and changes of 1986 and 1996. The main conclusion

of table 2 is that CDD data and branches are capturing different aspects of the financial

services in Thailand. The R-‐squared are negligible and the only two out of the six

coefficients are significant, with one of them negative. The point estimates for the

regressions of the 1996 levels and the change between 1986 and 1996 are all negative. One

possible explanation for this discrepancy is that lending activities are provided by other

distribution channels, as credit officers for example. We thus consider the CDD data as a

better characterization of the location of financial provision in Thailand.

[Table 2 – Branch data vs CDD data]

We now show evidence that ownership may matter – there are visible differences in the

profile of the expansion of BAAC and commercial banks. Table 3 presents the profile of the

changes for the period from 1986 to 1996. Columns (1) to (4) are based on the CDD sample,

while column (5) depict similar results for the branch data.

[Table 3 – Change in access to financial providers from 1986 to 1996]

In the following regressions, we interpret data as if market conditions (population, per

capita wealth, education and distance to markets) are exogenous to the location of financial

providers. Although this assumption may be too strong for the empirical analysis, it allows

us to characterize overall patterns that are incorporated in the model of the following

section. We consider specification in which the dependent variables are changes for the

1986-‐1996 period and independent variables are changes in the other provider plus a set

of variables characterizing initial market conditions. The objective is to characterize how

market conditions are correlated with the subsequent expansion of BAAC and commercial

banks. The analysis is focused on the cross-‐section variation of markets at both village and

amphoe levels of aggregation. This is why we do not consider fixed-‐effects panel data

models.

CDD data (columns 1 to 4) suggest that commercial banks expansion is positively

correlated to population and wealth, while these correlations are negative for BAAC, when

significant. For the case of distance to markets, table 3 shows that the changes in access to

commercial banks are higher in villages closer to markets. BAAC, again, shows the opposite,

going to more distant villages.

The comparison between columns (3) and (4) also reveals differences in the profile of the

expansion within and across amphoes. This comparison may shed light on the way BAAC is

reaching the poor, less populated and more isolated areas. In column (4), the increase in

BAAC access is higher for poor amphoes and not related to population, or average distance

to markets. Thus, it seems that BAAC concentrates on poorer amphoes and, within these

amphoes, focuses on the less populated and more isolated villages.

Column (5) presents the same exercise considering the branch data. First, there is a

difference with the patterns depicted by the CDD data, although they are not incompatible.

Second, we also see a difference between the profile of changes in branches of commercial

banks and BAAC. Changes in BAAC are negatively related to education, while changes in

commercial banks are positively related to population.

We thus end up in a situation where commercial banks and BAAC seem to aim at different

targets. While commercial banks seem to maximize profits in the choice of locations, data

make it difficult to reconcile BAAC with profit maximization or targeting poverty – BAAC is

negatively correlated with population even conditioning on wealth. Next section tries to

rationalize this difference assuming that commercial banks maximizes profits and BAAC

maximizes the population access to financial services.

5 Model

We now present a dynamic spatial model that incorporates the patterns we observe in

data. In particular, we assume that BAAC behaves in order to maximize the population

access to financial services over time, while commercial banks maximize intertemporal

profits.

5.1 Demand for financial services

Consider a finite number

�

M of markets for financial services (villages). Each village can

have a bank office open in it. Each village

�

i = 1,...,M is characterized by the population size

�

ni and potential profits per person

�

pi (denote

�

π i = ni pi the total potential profit from

village

�

i). We consider

�

ni and

�

pi as exogenous variables.

Villages are connected by roads, which are represented by

�

R = rij( ) , where

�

rij = 1 if and only

if villages

�

i and

�

j are directly connected by a road and

�

rij = 0 otherwise. Notice that

�

R is a

symmetric matrix.

If there is a bank branch in village

�

i then people from any directly connected village

�

k can

travel to get access to financial services, bringing profits

�

pk to village

�

i . We assume that

travel is costly and that only a fraction

�

τ −1 (with

�

τ > 1) of people from such villages can

travel. If village

�

k has no bank office but is directly connected to several villages with

banks’ offices then the travelers

�

τ −1 split equally between those banks.

5.2 Supply of financial services

For the sake of simplicity, we assume there are two banks, which we name BAAC and

commercial bank. These banks compete by opening branches in different villages. Each

village can have at most one office of any bank. Banks move sequentially by opening offices

in villages without banks.

We summarize their interaction in the form of the following multi-‐period game:

1. New period begins.

2. Nature selects which bank will move in the current period. We call this bank

“active” in this period.

3. “Active” bank selects a village to open a new branch in.

4. All banks receive profits from the people who come to their branches to get

access to financial services, according to the profit and road structure

�

π i{ },R( ) . 5. Current period ends. If there are empty villages the game continues from stage

1. If all villages are occupied the game ends.

We do not allow banks to close their branches. Since there are a finite number of villages, it

is clear that banks will stop opening branches. After that, all banks receive the same profits

over time. This focus on entries not only simplifies the analysis but it is also compatible

with the investigated period in Thailand, as described in section 2.

The state of access to finance in the economy is characterized by the set of existing bank

offices in each period – access to financial services is represented by the vectors

�

F1,F2 ∈RM

(

�

M is the number of villages). The state variable of the economy is represented by

�

F = Fk{ }k=1,2 . Each vector

�

Fk has

�

M components which are zeros or ones, with ones

corresponding to the villages where bank

�

k has offices and zeros for the other villages.

More formally,

�

Fk = fk1,..., fk

M( ) , where

�

fki = 1 if bank

�

k has an office in village

�

i and

�

fki = 0

otherwise.

We denote

�

G F( ) = F1 + F2 the vector of aggregate access to banking services. Also,

�

Gi F( ) shows whether village

�

i has access to banking services at all in state

�

F .

Since people are allowed to travel between adjacent villages (i.e. villages connected by

roads) to get access to financial services, it is useful for each village

�

i to count the number

of banking options residents of that village have if they decide to travel. For each village

�

i ,

we denote

�

N i F( ) the number of adjacent locations with banks’ offices in them when the

state of the economy is

�

F , i.e.

�

N i F( ) =# j : j = 1,...,M, j ≠ i,Ri, j = 1, f1j + f2

j = 1{ } . We assume that people who travel from village

�

i to get access to finance in adjacent locations spread

equally among those

�

N i F( ) available options.

Banks are interested in how much profits traveling people would bring to their respective

offices. For each village

�

i , we define

�

N i k,F( ) as the number of adjacent locations with bank

�

k offices, i.e.

�

N i F( ) =# j : j = 1,...,M, j ≠ i,Ri, j = 1, fkj = 1{ }. Evidently, we have that

�

N i F( ) = N i 1,F( ) + N i 2,F( ) . Thus, from any village

�

i , which residents travel outside to get

access to banking services, bank’s

�

k payoff will be:

�

1τπ iN i k,F( )N i F( ) .

Thus, we can write the profit of bank

�

k in a given period as:

�

Π k,F( ) = π ii: fk

i F( ) =1∑ +

1τ

π iN i k,F( )N i F( )i:Gi F( ) =0

∑ . (1)

The first term captures profits obtained by bank

�

k in villages it has offices in. The second

term represents what is obtained from the directly connected villages.

We are now ready to write the objective functions of BAAC and commercial banks. In each

period, each bank can be called to open a new office. We denote this bank as active in

period

�

t . If bank

�

1 is active, bank

�

0 is non-active, and vice-‐versa. We assume a simple

Markov structure for transition of the banks between active and non-active states. Namely,

we denote by

�

PA |Ak and

�

PNA |Ak the probabilities that an active bank

�

k in a given period is

active and non-‐active, respectively. Similarly,

�

PA |NAk and

�

PNA |NAk represent the probability of a

non-‐active bank

�

k be active or not in the following period.

We start with the problem of the active commercial bank, for which

�

k = 1. Denote

�

VA1 F( )

the value function of commercial bank conditional on the fact that it is active in this period

and the aggregate financial access state is

�

F . In this case, commercial bank is called to open

an office in any of the empty locations. The state of financial access, after the choice,

changes from

�

F = F1,F2( ) to a feasible

�

F '= ′ F 1,F2( ) , where

�

F1 and

�

′ F 1 differ only in one

component

�

i0 indicating the empty village in state

�

F where commercial bank opens a new

office. We formally define the set of feasible moves for bank

�

k in state

�

F as

�

Ωk F( ) = ′ F k :∀i0 = 1,...,M, ′ F ki0 − Fk

i0 = 1⇒ Gi0 F( ) = 0{ }. Then, the problem of an active commercial bank can be written as:

�

VA1 F( ) = max

′ F 1∈Ω1 F( )Π 1, ′ F ( ) + β VS

1 ′ F 1,F2( )PS |A1

S∈ A ,NA{ }∑

⎡

⎣ ⎢

⎤

⎦ ⎥ , (2)

where

�

β ∈ 0,1[ ] is the discount factor. Commercial bank choose where to open the new office maximizing its current period payoff

�

Π 1, ′ F ( ) plus the discounted expected continuation value.

Let us now define the value function of commercial bank when it is non-‐active. If

commercial bank is not active, BAAC choose the next state

�

′ F F( ) = F1, ′ F 2 F( )( ), where

�

′ F 2 F( )

is the optimal choice of BAAC when facing state

�

F . The value function for the non-active

commercial bank is given by:

�

VNA1 F( ) = Π 1, ′ F F( )( ) + β VS

1 F1, ′ F 2 F( )( )PS |NA1

S∈ A ,NA{ }∑

⎡

⎣ ⎢

⎤

⎦ ⎥ . (3)

We assume that, different from the profit-‐maximizing commercial bank, BAAC (the bank

labeled as 2) cares about the total financial access of people to finance services no matter

which bank is provider. The simplest way to incorporate this behavior in the model is to

assume that BAAC current period payoff includes payoffs from all customers getting access

to finance in offices of both BAAC and commercial bank. In fact, if the profit per person is

uniform across villages (which implies in

�

π i = pni), maximizing total profits is equivalent to

maximize the number of customers with access to financial services. Thus, we can write the

value function for the active BAAC as:

�

VA2 F( ) = max

′ F 2∈Ω2 F( )Π k, ′ F ( )

k =1,2∑ + β VS

2 F1, ′ F 2( )PS |A2

S∈ A ,NA{ }∑

⎡

⎣ ⎢

⎤

⎦ ⎥ , (4)

where

�

′ F = F1, ′ F 2( ) . We have an analogous value function for the non-active BAAC, given by:

�

VNA2 F( ) = Π k, ′ F F( )( )

k =1,2∑ + β VS

2 ′ F 1 F( ),F2( )PS |NA2

S∈ A ,NA{ }∑

⎡

⎣ ⎢

⎤

⎦ ⎥ . (5)

The only difference between the objective functions of commercial bank and BAAC is the

sum of payoffs in the first term of (4) and (5). Will such change be enough to induce BAAC

to go to worse and more distant locations as observed in the data?

It appears that there are two effects at work. On the one hand, since all locations occupied

(and customers served) by the commercial bank in the current period are treated by BAAC

as its own locations (customers), BAAC acts as a big commercial bank owning all these

locations. In particular it tries not to interfere with its current market and tries to open new

branches in locations with are far from both its own and commercial bank existing offices.

On the other hand, there is also an effect related to the anticipation of future expansion of

commercial banks. If BAAC for some reason knows that some (more profitable) market will

be served by commercial banks in the near future, it does not open a branch there today

going to less lucrative markets instead. If BAAC were to go to the (next) best market in the

current period (even if this does not interfere with the current markets of commercial

banks) then in the future commercial banks would come to this market as well. Since each

additional $ received by commercial banks expanding into this market would mean only a

fraction of a $ to BAAC, this would be not optimal from viewpoint of maximization of the

total access to financial services. That's why this effect might push BAAC to go into distant

and less profitable/populated locations even if there are no commercial banks currently in

better locations in the current period.

5.3 Equilibrium

The model described above has an equilibrium that is almost always unique. This result can

be demonstrated by backward induction. Consider the last stage of the game played by the

banks. After this stage banks will be receiving constant profits over time. Then the game is

trivial the bank which is active fills the last village, which has no bank office in it.

Consider the point before uncertainty about who moves last is realized (the stage before

the last one). This uncertainty would give expected continuation payoffs to the bank that is

active in the last but one stage. Now each active bank has two choices. Assume that profits

for each location are such that for any final node of the game resulting continuation profits

are different. Consider the set of parameters of the game

�

π i( ) such that the active bank is indifferent between locations in at least one of the final nodes. Define this set as

�

Q M −1( ) , where

�

M is total number of villages/periods in the game, and denote the number of final

nodes of the game

�

x . Notice that

�

x < ∞ .

We can represent

�

Q M −1( ) as the union of

�

x sets

�

Qx M −1( ) , where

�

Qx M −1( ) is the set of parameters for which the player active in node

�

x is indifferent between its two possible

actions. Then,

�

Qx places only one linear restriction on

�

π i( ) and, therefore, it is a set of zero measure. Consequently,

�

Q is also a set of zero measure.

Consider now a stage where the active bank has

�

z possible options. Then, analogously to

the case above, we have

�

z linear restrictions on a corresponding set

�

Q M − z +1( ) . This set is defined by the indifference of the active bank at least between two options. The set

�

Q M − z +1( ) can also be written as a finite union of the sets

�

Q M − z +1( )i, j defined by linear

restrictions representing the indifference of the active bank going to village

�

i or village

�

j .

Therefore,

�

Q M − z +1( )i, j has zero measure and, consequently,

�

Q M − z +1( ) is also a set of

zero measure.

Thus, the (finite) union of all sets

�

Q M − z +1( ) with respect to all possible values of

�

z is also

a set of zero measure and the game has a unique equilibrium for almost all values of

parameters

�

π i( ) .

5.4 Discussion

We make two restrictive assumptions to make our game solvable.

First, we assume that banks are called to choose locations sequentially and exogenously.

We do not adopt simultaneous move game to avoid multiple equilibria. Sequential game we

analyze here has an advantage that equilibrium is almost always unique, as showed in the

previous sections.

Second, we also assume that banks cannot open offices in the same location. We make this

assumption for computational reasons, because it reduces the number of nodes in the game

tree. The (unique) equilibrium of the game described above can easily be found using the

algorithm of backward induction. Unfortunately, computing this equilibrium could become

rather difficult computation task because of dimensionality curse. For example, considering

a deterministic version of the model where the BAAC and the commercial bank alternate

choosing locations, the game tree of a game with

�

M villages has

�

M! possible paths.

The computational burden is of order of

�

M!. In practice, computing game even for 9 villages on a workstation could take several minutes. Computing it for 12-‐15 nodes requires several

days. That's why in our analysis below we have to severely restrict the number of villages

(6-‐7 nodes) to make the problem solvable in reasonable time. This is also the reason why

we do not allow several banks to open branches in the same village because this essentially

means adding more nodes to the game making it intractable computationally.

6 Some key examples

This section solves the model for a set of artificial examples in order to shed some light on

the differences in the behavior of BAAC and commercial banks and the role of key

parameters.

Consider a particular configuration of villages on a map. Namely, assume that there are six

villages having coordinates (0,0), (1,1), (2,2), (3,3), (3,4), (4,4). Further assume that there is

a road going through villages (1,1), (2,2), (3,3), (3,4), whereas villages (0,0) and (4,4) are

not connected to any village at all. Figure 4 depicts this economy.

[Figure 4 – Example economy]

We populate villages by people with the assumption that more central locations have more

people, which is consistent with empirical patterns we observe in the data. We also

consider

�

τ = 2, a parameter that determines that 50% of the population of each village is

able to travel.

Finally, we consider a deterministic version of the model where each bank alternate in

choosing locations. This allows us to build more informative examples in a computationally

feasible number of villages.

6.1 Basic intuition of the model

Let's see how the BAAC and the commercial bank enter into this economy. We start

considering

�

β = 1, a parameter representing that both providers are forward looking.

Figure 5 shows expansion paths of two banks: red and green dots shows the locations of

offices of commercial bank and BAAC at any period, respectively.

[Figure 5 – Commercial bank (red) x BAAC (green)

�

β = 1,τ = 2( ) ]

In this case, commercial bank immediately occupies the best location (2,2). BAAC, on the

other hand, chooses first the least profitable and more isolated village. BAAC anticipates

future entry of commercial bank in location (3,3) in the next period, which also serves part

of location (3,4). Instead of going to the most populated available villages, it prefers to go to

places that will not be occupied by commercial bank in the immediate future (isolated

locations (0,0) and (4,4)).

In

�

T = 3, when BAAC is called to play, the location that maximizes the current payoff is the

location (3,3), which brings $4.15 in profits ($2.8 from its market plus $1.35 from the

travelers of location (3,4)). On the other hand, half of the population of location (3,3) was

already with access to financial services travelling to location (2,2). Thus, the net gain of

locating in (3,3) is reduced from $4.15 to $2.65. Contrary to that expanding into either

location (0,0) or (4,4) would bring $2 every period on top of the expansion by the

commercial bank into location (3,3). Thus, when discount rate is sufficiently high, BAAC

prefers going into those isolated and poorer locations instead. In the last period, we see

commercial bank clustered in the most populated villages, while BAAC scattered in less

populated and more isolated villages.

In order to better illustrate this argument, figure 6 shows the same exercise but

considering

�

β = 0 . Both providers now only concern about the current profits in each

period.

[Figure 6 – Commercial bank (red) x BAAC (green)

�

β = 0,τ = 2( )]

Commercial bank immediately occupies the best location (location (2,2)) as in the previous

example. But now, BAAC opens a branch right next to the commercial bank in location

(3,3). Remember that in figure 5 BAAC goes to (0,0) because it incorporates the benefits of

waiting for commercial banks to attend the most populated villages. Here, this effect does

not exist because BAAC is totally myopic. The only thing that matters is the current payoff.

Opening a branch in (3,3) provides access to its own market (half of which was not

attended by commercial bank in (2,2)) plus part of the market of village (3,4). In this case,

we see a quite different pattern in the last period. Cross section data from this example

would show commercial bank and BAAC operating in villages with the same average

population, with quite similar geographical distribution.

The comparison between these two simple examples indicates that the differences in the

behavior of the two providers increase with the discount factor. In particular, for

�

β

sufficiently high, we might observe BAAC going to less populated and more isolated areas,

anticipating the profit maximizing behavior of the commercial bank.

These patterns help to interpret the differences in the behavior of BAAC and commercial

banks in Thailand from 1986 to 1996, as described in section 4.

6.2 Interaction between BAAC and commercial bank

We now study the interaction between BAAC and commercial bank. We would like to

develop the intuition about how the behavior of BAAC changes in the presence of

commercial banks. Applying the argument developed above to a higher level of

aggregation, we might expect BAAC going first to less populated provinces and start to

operate alone in villages from these provinces. As time goes by, with the increasing

penetration of financial services, commercial bank arrives in later periods. The question we

would like to investigate is whether the behavior of BAAC changes or not at this moment,

when commercial banks start to play in these provinces.

[Figure 7 – BAAC (red) x BAAC (green)

�

β = 1,τ = 2( ) ]

Figure 7 shows a situation in which BAAC is playing alone (against itself), considering a

discount factor

�

β = 1. In this case, different from what we see in figure 5. BAAC starts

choosing the most populated and central village (location (2,2)). At this point, the cross

section variation of access to financial services depicts a positive correlation between

population and access to BAAC. Then, after assuring that the most populated villages are at

least partially attended, BAAC starts to operate in isolated villages.

[Table 4 – Interaction between BAAC and commercial banks]

The change in the behavior of BAAC when facing or not commercial banks is also

compatible with our data, as shown in table 4. We focus on the year of 1986, when the

penetration of commercial banks was particularly low. The main idea is to test whether the

profile of BAAC changes with the penetration of commercial banks at the province level.

For each village, we compute the percentage of villages with commercial bank access in the

respective province. This is a way of characterizing the presence of commercial banks at

the province level, when considering the village-‐level regressions.

Table 4 show a positive and statistically significant coefficient for population. This suggests

that, in provinces where the percentage of villages with commercial banks access is zero,

the presence of BAAC is positively correlated to the population. The coefficient related to

the interaction between population and the penetration of commercial banks at the

province level is negative and statistically significant. As we move from provinces with low

to those with high penetration of commercial banks, the presence of BAAC becomes less

related to population. The coefficients of both level and the interaction of the per capita

wealth are not significant, suggesting that BAAC behavior is more sensible to population

than to wealth.

Thus, not only the profile of BAAC is different from that of commercial bank, as showed in

section 4, but also it changes with the presence of commercial banks, as suggested by the

model.

7 Simulation (to be done)

This section is devoted to simulation exercises from the model. The idea is to draw random

samples of 6 to 8 villages from our data, compute the equilibrium, and analyze the profile of

the outcomes, comparing BAAC with the commercial bank.

8 Estimation (to be done)

This section aims at proposing an algorithm to estimate the parameters of the model

β,τ ,λ( ) , based on the approach of Bajari, Benkard and Levin (Econometrica, 2007).

9 Empirical approximations of the reaction function of BAAC and commercial

banks

The model outlined in section 5 determines optimal entry policies for BAAC and

commercial banks. As already mentioned, solving the model is a computationally too costly

for larger economies. In particular, it is not feasible to solve the model for the number of

villages we observe in data, even restricting the analysis to a specific province.

This section considers reduced-‐form approximations for the optimal policy functions of

BAAC and commercial banks, based on a semi-‐parametric spatial econometric approach

developed by Chen and Conley (2001). This approach allows us to identify geographical

patterns of the observed expansion of BAAC and commercial banks.

The optimal policy function of bank

�

k can be represented by:

Fk* t +1( ) = σ k ,t Fk

* t( ),F−k* t( ) R, π i( ),β,τ( ) , (6)

where

�

F * 0( ) = 0 . We take a quasi-‐linear and stationary approximation for the village-‐level

version of equation (6), considering the following specification:

fki t +1( ) = wk

i, j fkj t( )

j=1

M

∑ + w−ki, j f−k

j t( )j=1

M

∑ + γ R, π i( ),β,τ( ) + εki t +1( ) , (7)

where εki t +1( ) is an approximation error and γ ⋅( ) is any (potentially non-‐linear) function.

Notice that the weights wkj and w−k

j do not vary according to the time periods. Stationarity

is a strong assumption in our case, since we focus exclusively on entries in a finite number

of markets. However, this assumption is less strong for our data, where we are quite far

apart from the end of the game. Still, this exercise shows us another dimensions of the

differences we observe in the behavior of BAAC and commercial banks.

Considering equation (7) for the periods t +1 and T +1, where T > t , we can write:

Δfki T( ) = wk

i, jΔfkj T( )

j=1

M

∑ + w−ki, jΔf−k

j T( )j=1

M

∑ + Δεki T( ) , (8)

where we also take that Δfki T +1( ) ≈ Δfk

i T( ) , since they differ only in one component. Actually, the error from this approximation tends to be smaller the greater is the difference

between t and T . Equation (8) represents how the changes in the presence of bank k in

village i is related to the changes in other villages and to the changes in the presence of the

other provider.

In principle, we would like to estimate (8) and compare the estimated weights of BAAC and

commercial bank. Unfortunately, coefficients of the regression related to (8) cannot be

identified – there are more coefficients than observations. Thus, we need to impose

restrictions on the weights wki, j and w−k

i, j . We thus take the approach of Chen and Conley

(2001) and consider weights structured according to a spatial distance matrix, with

wki, j = gk Di, j( ) and w−k

i, j = g−k Di, j( ) , where Di, j is the distance between villages i and j .

Error! Reference source not found.Error! Reference source not found.Error!

Reference source not found.Error! Reference source not found.

Therefore, we consider two different specifications to for equation (8), for the period from

1986 to 1996. In order to focus on the variation observed in the period, we focus on

specifications related to the changes in access as following:

Δfki T( ) = gk Di, j( )Δfkj T( )

j=1

M

∑ +αΔf−kj T( ) + Δεk

i T( ) , (9)

and

Δfki T( ) = αΔfkj T( ) + g−k Di, j( )Δf−kj T( )

j=1

M

∑ + Δεki T( ) . (10)

The models are straightforward adaptations of the methodology presented in Chen and

Conley (2001). Notice that the only difference between (9) and (10) is related to the term

in the summation. In the first case, the function gk D( ) represents how changes in access at village

�

i are correlated with changes at village

�

j for a given provider k (geographical own-‐

effects). In the second case, the function g−k D( ) shows how changes in one provider at village

�

i are related to changes of the other provider at village

�

j (geographical cross-‐

effects). The differences in the behavior of BAAC and commercial banks can be captured by

the comparison of functions gk and g−k .

Equations (9) and (10) are estimated for two samples for which we have geo-‐located

observations. We consider the amphoe-‐level data for the whole country and the village-‐

level data for the four selected provinces. Results are depicted in figures 8 and 9.

In all cases, we get flat

�

g functions for BAAC and decaying

�

g functions for commercial

banks. The presence of BAAC in a given village (amphoe) is connected with the presence of

BAAC at a wider range of distances. The presence of commercial banks in a given village

(amphoe), on the other hand, is related only with the presence of commercial banks in

nearby villages (amphoes).

In the case of the specification with geographical cross-‐effects, we study how the changes in

BAAC for village

�

i are affected by the changes in commercial bank in village

�

j and vice-‐

versa. We focus now on the geographical interaction across different banks rather than

self-‐related geographical interaction of each bank.

At the amphoe-‐level, each provider interacts with the other in the same way it interacts to

itself. BAAC presents a flat pattern with respect to commercial banks, while commercial

banks depict decaying patterns with respect to BAAC. For the village-‐level data, the results

change for the case of commercial banks, as shown in figure 9(ii). Commercial bank

expansion in a given village is not affected by the changes of BAAC in other villages. The

pattern for the BAAC is similar to that obtained with the amphoe-‐level data. The changes in

the access to BAAC in a given village are affected by the change in the access to commercial

banks in villages located at a wide range of distances.

The comparison between these two patterns reveals interesting features about the

underlying decision-‐making choices compatible with the data. The profitability of a given

village in this environment, conditional on the location of the nearby competitors (which

completely define the market size), is independent from what happen in the other (farer)

villages. In this example we are closer to a decaying g function. For the flat pattern case,

we can take a country-‐level mandate as an example. If BAAC (as we assume in the model)

maximizes the total financial access of the population, the access of a given village might

become related to the access in all other villages in the country.

10 Conclusion

This paper studies location as another channel through which bank ownership may matter.

We build a spatial dynamic entry model where the government development bank (BAAC)

maximizes total access to finance irrespective of which bank provides it, while the private

bank (commercial bank) maximizes profits. If the discount factor is high enough, we see

BAAC anticipating that commercial bank has incentive to attend the most profitable villages

first and go to more isolated and less populated ones, as suggested by our data. In addition,

we show that the behavior of BAAC changes whether playing against commercial banks or

not and that the geographical location patterns of BAAC and commercial banks are

different.

References

Ackerberg, Daniel A. and Gautam Gowrisankaran (2006) “Quantifying equilibrium network

externalities in the ACH banking industry”. NBER Working Papers 12488.

Chan, Tat Y.; V. Paddy Padmanabhan and P. B. Seethu Seetharaman (2007) “An Econometric

Model of Location and Pricing in the Gasoline Market”. Journal of Marketing Research,

44(November): 622-‐635.

Chen, X. and T. G. Conley (2001) “A new semiparametric spatial model for panel time

series”. Journal of Econometrics, 105: 59-‐83.

Holmes, Thomas J. (2008) “The Diffusion of Wal-‐Mart and Economies of Density”. NBER

Working Paper 13783.

Micco, Alejandro; Ugo Panizza and Monica Yañez (2007) “Bank ownership and

performance. Does politics matter?”. Journal of Banking & Finance, 31(1): 219-‐241.

Panle, Jia (2008) “What Happens When Wal-‐Mart Comes to Town: An Empirical Analysis of

the Discount Retailing Industry”. Econometrica, forthcoming.

Sapienza, Paola (2004) “The effects of government ownership on bank lending”. Journal of

Financial Economics, 72(2): 357-‐384.

Schmidt-‐Dengler, Philipp (2006) “The Timing of New Technology Adoption: The Case of

MRI”. Mimeo.

Figure 1 -‐ Number of branches and Outreach

198619881990199219941996

!"#$%&'(")*++,*++, ,"--./0(&%1*&)23,"--./0(&%1*&)23 4"'&%

!"#$%&'(")*/&)05.3

!"#$%&'(")6*/&)05.3 */&)05.3

!"#$%&'(")6*/&)05.3 */&)05.3

!"#$%&#'!% '( &"%#!!) *#")) %*#"!) *#'"'!&#)!'#%'% )% &%&#)&$ *#(&( *'#)'& %#+!*!&#&"(#++* *%& %''#('" %#%"' *$#%+$ %#!(*!%#&"&#$(& %*+ *$&#$(! %#$(+ *%#$!$ %#)++!%#(%)#*%$ !!% ((#*)* !#+!& *+#)$! !#!""!!#'"+#!"! $+% "'#%$% !#!(+ (#($( !#)(%

!

"#!

$!!

%#!

&!!

"'(& "'(( "''! "'') "''% "''&

!

")#*!!!

)#!*!!!

$+#*!!!

#!!*!!!!""#

,-./0123-45.67587149: 87149:6;

!

"!!!

)!!!

$!!!

%!!!

"'(& "'(( "''! "'') "''% "''&

,-./0123-45.67587149: 87149:6;

198619881990199219941996

!"#$%&'(")*++,*++, ,"--./0(&%1*&)23,"--./0(&%1*&)23 4"'&%

!"#$%&'(")*/&)05.3

!"#$%&'(")6*/&)05.3 */&)05.3

!"#$%&'(")6*/&)05.3 */&)05.3

!"#$%&#'!% '( &"%#!!) *#")) %*#"!) *#'"'!&#)!'#%'% )% &%&#)&$ *#(&( *'#)'& %#+!*!&#&"(#++* *%& %''#('" %#%"' *$#%+$ %#!(*!%#&"&#$(& %*+ *$&#$(! %#$(+ *%#$!$ %#)++!%#(%)#*%$ !!% ((#*)* !#+!& *+#)$! !#!""!!#'"+#!"! $+% "'#%$% !#!(+ (#($( !#)(%

!

"#!

$!!

%#!

&!!

"'(& "'(( "''! "'') "''% "''&

*+,-./01+23,45365/278 65/27849

!

"!!!

)!!!

$!!!

%!!!

"'(& "'(( "''! "'') "''% "''&

!

:;#!!

"#;!!!

));#!!

$!;!!!!"##$%&'()*+(,-.

*+,-./01+23,45365/278 65/27849

Figure 2 -‐ Thai regions and provinces

Figure 3 -‐ CDD selected villages and amphoe district centers

Figure 4 – Example economy

Figure 5 – Commercial bank (red) x BAAC (green)

�

β = 1,τ = 2( )

Figure 6 – Commercial bank (red) x BAAC (green)

�

β = 0,τ = 2( )

Figure 7 – BAAC (red) x BAAC (green)

�

β = 1,τ = 2( )

Figure 8 – Geographical pattern of policy functions (amphoe-‐level data)

(i) specification with geographical own-‐effects

(ii) specification with geographical cross-‐effects

Figure 9 – Geographical pattern of policy functions (village-‐level data)

(i) specification with geographical own-‐effects

(ii) specification with geographical cross-‐effects

Table 1 -‐ Descriptive statistics -‐ CDD Data

obs. mean std. dev. min max

1986

access to BAAC 44513 0.8 0.4 0 1

access to commercial banks 44175 0.3 0.4 0 1

population (thousands) 44652 603.7 420.2 11 9864

per capita wealth 29235 0.5 0.3 0.0 8.9

% population with advanced

secondary school 35918 0.0 0.3 0.0 52.0

time to the market (in

minutes) 42762 35.0 30.6 1 998

1996

access to BAAC 44536 0.9 0.2 0 1

access to commercial banks 44280 0.4 0.5 0 1

population (thousands) 44649 606.2 421.1 3 9788

per capita wealth 43515 1.2 0.5 0.0 23.2

% population with advanced

secondary school 44281 0.0 0.0 0.0 4.9

Table 2 – Branch data vs CDD Data

CDD Data 1996 1986 Change (1986-‐1996) BAAC Commercial

Bank BAAC Commercial

Bank BAAC Commercial

Bank (1) (2) (3) (4) (5) Branch data -‐0.003 -‐0.001 0.061*** 0.002 -‐0.005 -‐0.004** (0.530) (0.600) (3.250) (0.920) (0.540) (2.360) Constant 0.944*** 0.467*** 0.804*** 0.285*** 0.135*** 0.183*** (169.650) (45.200) (89.730) (30.140) (16.150) (19.830) observations 705 705 705 705 705 705 R-‐squared 0.00 0.00 0.01 0.00 0.00 0.00

Table 3 – Change in access to financial providers from 1986 to 1996

Panel (i): Change in Access to BAAC 1986-‐1996

Village Level Amphoe Level

Branch Data (Amphoes)

(1) (2) (3) (4) (5) -‐0.867*** -‐0.871*** -‐0.915*** -‐0.666*** -‐0.058 access in 1986 (0.006) (0.006) (0.004) (0.019) (0.790)

0.052*** 0.047*** 0.073*** -‐0.012 change in access to commercial banks in 1986-‐96 (0.003) (0.003) (0.020) (1.560)

0.056*** 0.049*** 0.028 0.001 access to commercial banks in 1986 (0.004) (0.004) (0.021) (0.120)

-‐0.005* -‐0.011*** -‐0.007*** 0.001 -‐0.030 ln(population in 1986) (0.003) (0.003) (0.002) (0.006) (0.830) -‐0.038*** -‐0.053*** -‐0.011** -‐0.084*** -‐0.091 per capita wealth in 1986 (0.005) (0.005) (0.005) (0.022) (0.670) -‐0.003 -‐0.002 -‐0.001 0.005 -‐0.254*** % population with advanced

secondary school in 1986 (0.003) (0.003) (0.004) (0.049) (5.050) 0.003* 0.005** 0.006*** 0.008 -‐0.102 ln(distance (minutes) to the

market in 1986) (0.002) (0.002) (0.002) (0.011) (1.400)

amphoe-‐level fixed effects no no yes observations 24498 24202 24202 704 704 R-‐squared 0.70 0.70 0.75 0.68 0.01 Panel (ii): Change in Access to Commercial Banks 1986-‐1996 (1) (2) (3) (4) (5)

-‐0.823*** -‐0.832*** -‐0.924*** -‐0.485*** -‐1.159*** access in 1986 (0.007) (0.007) (0.007) (0.035) (2.580) 0.288*** 0.266*** 0.253*** -‐0.18 change in access to BAAC in 1986-‐

96 (0.013) (0.015) (0.070) (1.640) 0.294*** 0.274*** 0.220*** 0.730*** access to BAAC in 1986 (0.014) (0.017) (0.058) (6.320) 0.099*** 0.099*** 0.095*** 0.018* 0.336** ln(population in 1986) (0.005) (0.005) (0.006) (0.010) (2.370) 0.214*** 0.228*** 0.120*** 0.194*** 0.05 per capita wealth in 1986 (0.010) (0.010) (0.012) (0.040) (0.110) -‐0.011*** -‐0.010*** -‐0.01 -‐0.072 0.232 % population with advanced

secondary school in 1986 (0.001) (0.001) (0.009) (0.091) (0.740) -‐0.029*** -‐0.030*** -‐0.031*** -‐0.049** 0.491 ln(distance (minutes) to the

market in 1986) (0.004) (0.004) (0.004) (0.020) (1.240)

amphoe-‐level fixed effects no no yes observations 24221 24202 24202 704 704 R-‐squared 0.39 0.40 0.49 0.25 0.58

Table 4 – Interaction between commercial banks and BAAC in 1986

Access to BAAC in

1986

0.083*** ln(population in 1986) (0.008)

0.017 per capita wealth in 1986 (0.016)

-‐0.096*** ln(population in 1986) * % villages with access to commercial banks in the province (0.025)

-‐0.074 per capita wealth in 1986 * % villages with access to commercial banks in the province (0.048)

0.123*** access to commercial banks in 1986 (0.005)

Observations 28970

R-‐squared 0.09