Embed Size (px)

Citation preview

Banking Procedures and Services

© 2010 Pearson Education, Inc.All rights reserved

Chapter 12

Learning Objectives

• Explain the difference between different types of financial institutions

• Learn the basics of having a checking account, including how to balance an account

• Describe other available banking services

• Describe the two major federal insurers

• Explain the function and goals of the Federal Reserve

© 2010 Pearson Education, Inc. All rights reserved 0-2

Banks and Financial Institutions

• Banks and other financial institutions offer services such as providing personal loans and accepting deposits

• Most offer accounts that allow you to draft payments

• There are two major types of financial institutions: – Depository institutions

– Nondepository institutions

© 2010 Pearson Education, Inc. All rights reserved 0-3

Depository Institutions

• Depository institutions are financial institutions that provide traditional checking and savings account for individuals and business. They also provide loans

• Depository institutions take in and secure people’s money

• This money is loaned to people and businesses in the community

• Types of depository institutions include:– commercial banks

– savings banks

– credit unions

© 2010 Pearson Education, Inc. All rights reserved 0-4

Depository Institutions

• Depository institutions generally pay interest on the deposits people leave with them

• The deposits are used to make loans, on which they charge an even higher rate of interest

• They also make money by charging various fees for services, such as overdraft protection

© 2010 Pearson Education, Inc. All rights reserved 0-5

Nondepository Institutions

• Nondepository institutions consist of institutions that provide certain financial services but do not accept traditional deposits

• Nondepository institutions include:– insurance companies

– finance companies

– securities firms

– investment companies

© 2010 Pearson Education, Inc. All rights reserved 0-6

Choosing a Bank

• Automatic teller machines (ATMs) are machines where you take cash out from your bank account.

• Depository institutions can differ on fees charge, interest rates paid on deposits, and access to ATMs and branches

• There can be significant fees charged from ATMs that are not within your bank’s network

• Some internet banks pay a higher deposit rate, but they also provide limited access

© 2010 Pearson Education, Inc. All rights reserved 0-7

Check Your Financial IQ

• What are two types of financial institutions?

© 2010 Pearson Education, Inc. All rights reserved 0-8

Check Your Financial IQ

• Depository and nondepository institutions are financial institutions

© 2010 Pearson Education, Inc. All rights reserved 0-9

Banking Basics: Checking Accounts

• One of the more widely used banking services is the checking account

• It is also a service that can lead to trouble if not managed carefully

© 2010 Pearson Education, Inc. All rights reserved 0-10

How Checking Accounts Work

• Checking account is an account at a bank into which you deposit money and withdraw money by writing checks or using a debit card

• Check is a written order from you to your bank instructing it to pay money from your account to another party

• When you write a check for someone, that person “cashes” the check at your bank

• The bank takes the money out of your account and gives it to the person

• This process often happens electronically

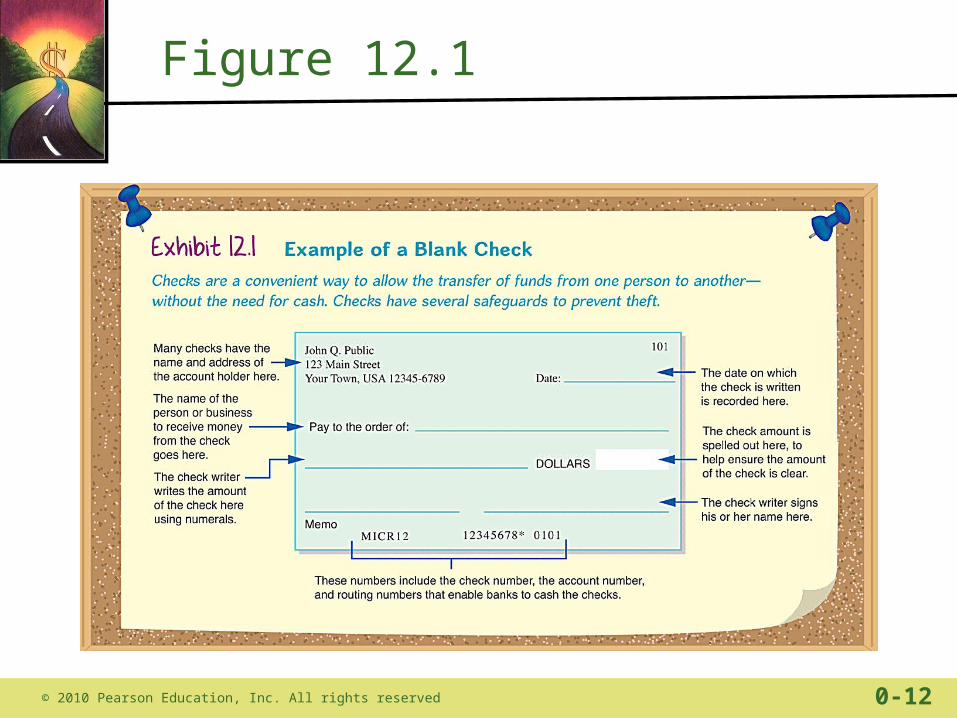

• See figure 12.1 to see a sample check and an explanation of its parts

© 2010 Pearson Education, Inc. All rights reserved 0-11

Figure 12.1

© 2010 Pearson Education, Inc. All rights reserved 0-12

How Checking Accounts Work

• We open checking accounts because it allows us to have an accurate payment record

• It also allows us to carry less cash

• Checks also make it safer to send payment via the mail

• Checks can only be cashed by the person it is written out to

© 2010 Pearson Education, Inc. All rights reserved 0-13

Math for Personal Finance

• Jim’s checking account balance was $541.39 at the beginning of the month. He deposited a $50 check he earned form mowing lawn and wrote a check for $28.32. His monthly service fee was $8.

• What is Jim’s new account balance?

© 2010 Pearson Education, Inc. All rights reserved 0-14

Math for Personal Finance

• Solution: $541.39 + $50 - $28.32 - $8 = $555.07

© 2010 Pearson Education, Inc. All rights reserved 0-15

NOW Accounts

• Negotiable order of withdrawal (NOW) accounts function much like checking accounts except they pay a small amount of interest on money in the account

• Money kept in ordinary checking accounts do not usually earn interest

• You can earn interest on NOW accounts

• NOW accounts require you to maintain a minimum balance in order to earn interest

© 2010 Pearson Education, Inc. All rights reserved 0-16

Debit Cards

• Debit card enables you to withdraw cash from your account at ATMs, or to pay directly for goods or services at businesses

• Many banks provide debit cards to their account holders

• A debit card looks like a credit card, but works differently

• There is no credit involved• The amount of money is

withdrawn immediately from your account

© 2010 Pearson Education, Inc. All rights reserved 0-17

Debit Cards

• Personal identification number (PIN) are usually four-digit numbers that you need to memorize in order to be able to use your debit card

• Debit cards are convenient but can make it easy to spend money

• Record debit card withdrawals and purchases in your check register

• Debit cards require you to use a personal identification number (PIN)

• Be careful with your PIN. No one should know it but you.

© 2010 Pearson Education, Inc. All rights reserved 0-18

Math for Personal Finance

• Tucker used his debit card to withdraw $40 cash from his account. However, he used an out-of=network ATM that charged him $2.50, and his own bank charged another $2 for the out-of-network withdrawal.

• How much will his account be charged in total?

© 2010 Pearson Education, Inc. All rights reserved 0-19

Math for Personal Finance

• Solution: That was an expensive withdrawal for Tucker. His account will be reduced by $40 + $2.50 + $2 = $44.50

© 2010 Pearson Education, Inc. All rights reserved 0-20

Using Your Checking Account

• Check register is a small ledger the bank will provide you for keeping track of your account balance

• The amount you open an account with is your balance

• Record that amount in your check register

• Record all checks and debit card purchases/withdrawals in the register.

© 2010 Pearson Education, Inc. All rights reserved 0-21

Using Your Checking Accounts

• Keeping an accurate balance is essential

• Some checking accounts have overdraft protection

• The bank will cash up to a certain amount even if you do not have money in your account

• You will have to pay back the bank and pay a fee

© 2010 Pearson Education, Inc. All rights reserved 0-22

Using Your Checking Accounts

• Some checking accounts do not have overdraft protection

• If you overdraw such an account, the bank will not cash any checks

• They will charge you a fee for overdrawing your account

• Most businesses will also charge you a fee for writing them a bad check

© 2010 Pearson Education, Inc. All rights reserved 0-23

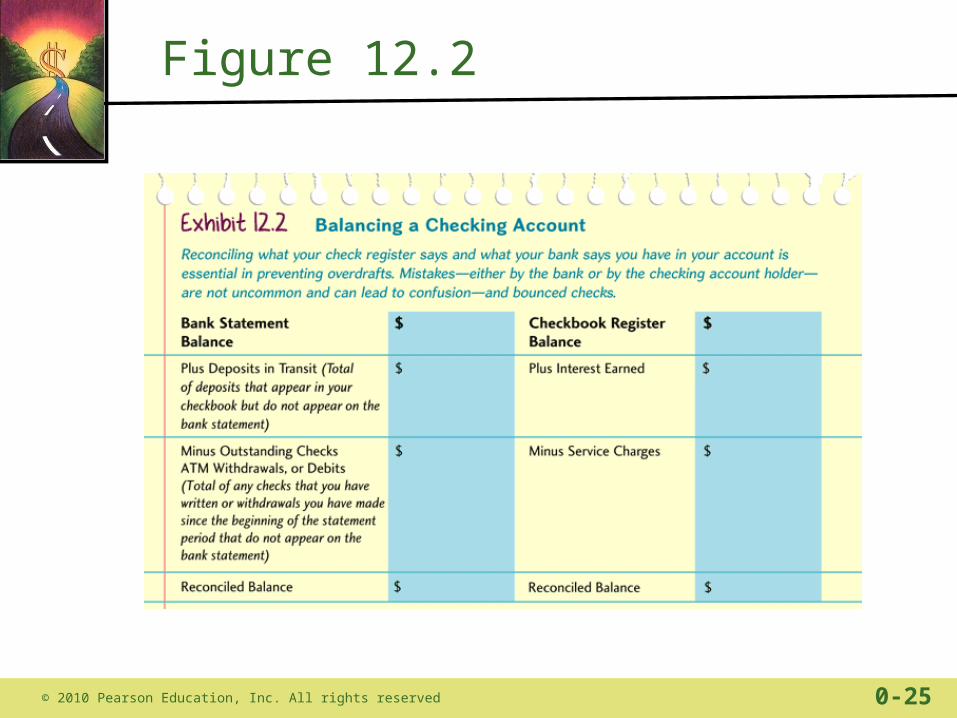

Balancing Your Account

• It is possible for errors—yours or the bank’s—to occur.

• You should regularly compare your records to the bank’s. (see figure 12.2)

• At the end of each month the bank will send you a bank statement

• This lists the bank’s records of all the deposits and checks written against your account

© 2010 Pearson Education, Inc. All rights reserved 0-24

Figure 12.2

© 2010 Pearson Education, Inc. All rights reserved 0-25

Math for Personal Finance

• Mary Beth’s checking account balance on her bank statement shows $184.32. However, she wrote checks for $41.78 and $12.10 that have not cleared the bank yet.

• How much do Mary Beth’s outstanding checks total?

© 2010 Pearson Education, Inc. All rights reserved 0-26

Math for Personal Finance

• Solution: Outstanding checks are checks that have not cleared the bank so the total is $41.78 +$12.10 = $53.88

© 2010 Pearson Education, Inc. All rights reserved 0-27

Check Your Financial IQ

• Why are checking accounts useful?

© 2010 Pearson Education, Inc. All rights reserved 0-28

Check Your Financial IQ

• They enable you to carry less cash, keep records, and mail payments securely

© 2010 Pearson Education, Inc. All rights reserved 0-29

Other Banking Services

• Banks offer a variety of different services besides checking and savings accounts

• A few of them are discussed on the following slides

• Become familiar with these services as they can help with your financial planning

© 2010 Pearson Education, Inc. All rights reserved 0-30

Safety Deposit Box

• Safety deposit boxes are small containers located inside the bank vault and are used to store valuable documents

• Safety deposit boxes are usually available for rent at most banks

• Safety deposit boxes usually contain wills and small objects such as jewelry, rare coins, and legal documents

© 2010 Pearson Education, Inc. All rights reserved 0-31

Cashier’s Checks, Money Orders, and Travelers Checks

• Cashier’s check is a type of check that is written to a specific payee but charged against the bank instead of your account

• Banks are also a source of cashier’s checks

• When you buys a cashier’s check, the bank takes the money out of your account immediately

• These types of checks are accepted in situations when a personal check is not

© 2010 Pearson Education, Inc. All rights reserved 0-32

Cashier’s Checks, Money Orders, and Travelers Checks

• Money orders are purchased for cash so that the recipient can trust that they are worth what they say they are

• Money orders function similar to cashier’s checks

• The US Postal Service sells money orders for a fee

• Money orders are also common when you buys something online.

• The seller does not have to wait for your check to clear when using a money order.

© 2010 Pearson Education, Inc. All rights reserved 0-33

Cashier’s Checks, Money Orders, and Travelers Checks

• Travelers checks are checks written by a large financial institution with no payee specified

• People pay for travelers checks in advance

• The recipient can be confident that the check will be cashed

• Travelers checks are accepted around the world

• Travelers who lost travelers checks can usually replace them

© 2010 Pearson Education, Inc. All rights reserved 0-34

Arrangements for Credit Payments

• Bank drafts occur when you authorize someone to take money out of your bank account automatically to satisfy some financial obligation

• Bank drafts are used to make car and house payments, and to pay utility bills

• People use bank drafts to contribute to retirement accounts and other investments

• Bank drafts help you pay off borrowed money in a timely manner

© 2010 Pearson Education, Inc. All rights reserved 0-35

Arrangements for Credit Payment

• Electronic funds transfer is whenever you authorize someone to access your bank account for payment or for deposit

• Bank drafts are an example of electronic funds transfer

• A bank draft authorization will set a specific date on which the money is taken from your account

• With bank drafts, you do not have to write a check every month

• Make sure to record all bank drafts and transfers in your check register

© 2010 Pearson Education, Inc. All rights reserved 0-36

Other Online Services

• Most banks now offer a variety of online services, such as: – having payments drafted directly out of your

account– utilize online bill payment services– transfer funds between checking and savings

accounts– make loan applications– check your bank statements

© 2010 Pearson Education, Inc. All rights reserved 0-37

Check Your Financial IQ

• Besides checking account, what services are typically offered by banks?

© 2010 Pearson Education, Inc. All rights reserved 0-38

Check Your Financial IQ

• Services include safety deposit boxes, cashier’s checks, money orders, and travelers checks

© 2010 Pearson Education, Inc. All rights reserved 0-39

Deposit Insurance

• One of the reasons to put money in the bank is to keep it safe

• If the institution went bankrupt, you would want your money to be protected

• Most financial institutions have deposit insurance on the first $250,000 you have on deposit.

• The major federal insurers are:

• Federal Deposit Insurance Corporation (FDIC)

• National Credit Union Savings Insurance Fund (NCUSIF)

© 2010 Pearson Education, Inc. All rights reserved 0-40

FDIC

• The federal government created the FDIC in 1933 during the Great Depression

• The bank failures caused people to take their money out of even healthy institutions

• This reaction hurt the banks and reduced the amount of money available for borrowing

• The government needed a way to restore faith in the banking system

© 2010 Pearson Education, Inc. All rights reserved 0-41

FDIC

• Saving money is critical to economic growth

• If there is no money deposited in the banks, businesses cannot borrow

• Currently, the FDIC provides deposit insurance on the first $250,000 of deposits at insured institutions

• FDIC insurance covers checking accounts, savings accounts, NOW accounts, and certificates of deposit

© 2010 Pearson Education, Inc. All rights reserved 0-42

NCUSIF

• Credit unions functions similarly to a bank, but unlike a bank, a credit union has nonprofit status and is owned by its members

• The National Credit Union Association (NCUA) supervises credit unions

• It provides deposit insurance with the same limits as FDIC insured deposits

• This program is also backed by the federal government

© 2010 Pearson Education, Inc. All rights reserved 0-43

Check Your Financial IQ

• Why is it important to give people confidence in the safety of their deposits?

© 2010 Pearson Education, Inc. All rights reserved 0-44

Check Your Financial IQ

• If people lose confidence in the safety of their deposits, they may withdraw money in panic and that can damage even healthy banks

© 2010 Pearson Education, Inc. All rights reserved 0-45

The Federal Reserve and Banking System

• The bank is part of a larger system that plays a central role in the nation’s economy

• At the heart of that banking system is the Federal Reserve System

• The Fed, as it is known, helps regulate our banking system and our whole economy

© 2010 Pearson Education, Inc. All rights reserved 0-46

Multiple Roles

• Federal Reserve System serves as the central bank of the United States

• The Federal Reserve Act of 1913 created the Federal Reserve System

• The Fed regulates banks and carries out the nation’s economic policies

• The Fed’s major economic goals are to create ongoing economic growth, encourage full employment, and promote price stability

• The Fed uses monetary policy in order to achieve these goals

© 2010 Pearson Education, Inc. All rights reserved 0-47

Price Stability

• Price level stability means making sure that we don’t have inflation (or deflation)

• Inflation is defined as a sustained increase in the general level of prices

• The main goal of Fed policy is price level stability

• Inflation means the prices of goods and services are going up

• Inflation is considered problematic to the government and the Fed because it harms businesses and individuals in our economy

© 2010 Pearson Education, Inc. All rights reserved 0-48

Monetary Policy

• Monetary policy involves the raising or lowering of the money supply to achieve some goal

• Fiat money has value not because the coins and bills have some value in their own right, but because the government orders that it be accepted as payment

• The Fed uses monetary policy as its primary tool to fight inflation and promote a healthy economy

• The money we currently use in the United States is known as fiat money

• With fiat money, a five-dollar bill is worth five dollars because the government says it is

© 2010 Pearson Education, Inc. All rights reserved 0-49

Monetary Policy

• The government must control how much of that paper and coin is circulating in the economy

• The United States Treasury is in charge of printing money and minting coins

• The Fed is the agency in charge of determining how much money is in circulation

© 2010 Pearson Education, Inc. All rights reserved 0-50

Monetary Policy

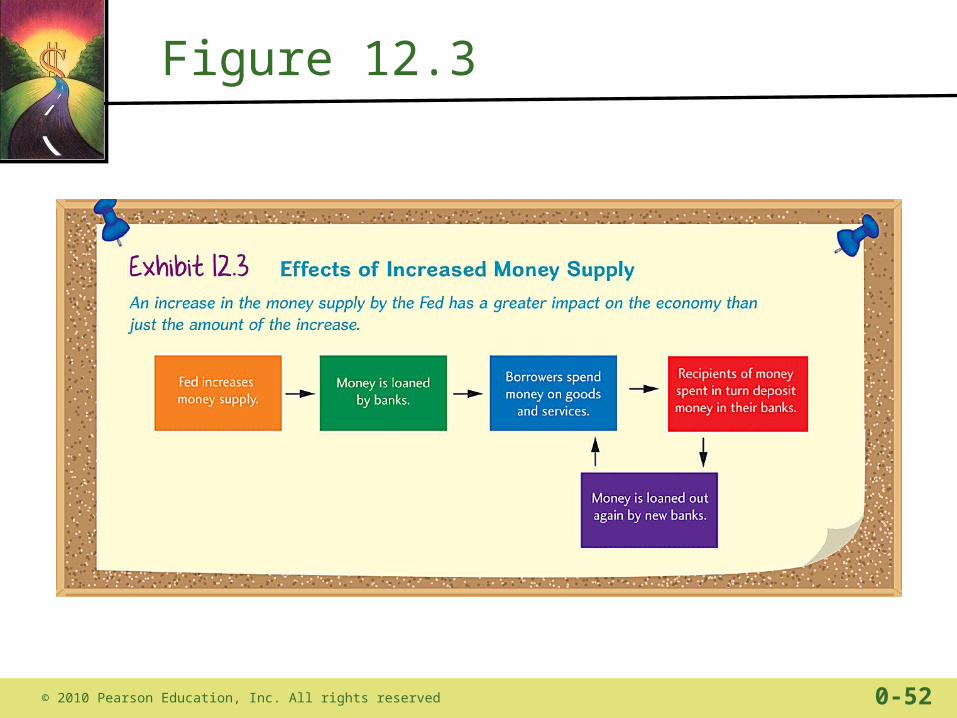

• Physical money in circulation is the most visible part of the money supply

• There is a lot of electronic money that we never see

• As the economy grows and more people need money to make purchases, the Fed expands the money supply

• This includes more electronic money, paper money, and coins (see figure 12.3)

© 2010 Pearson Education, Inc. All rights reserved 0-51

Figure 12.3

© 2010 Pearson Education, Inc. All rights reserved 0-52

Monetary Policy

• The Fed uses monetary policy to change interest rates and impact buying behavior

• If the Fed wants to encourage people to spend more money, it increases the money supply

• When more money is available, it drives interest rates down and encourages spending

• When the Fed reduces the money supply, interest rates go up

© 2010 Pearson Education, Inc. All rights reserved 0-53

Monetary Policy

• If the Fed shrinks the money supply, people will compete for an item (money) that’s in limited supply

• The price of that money (interest rates) will go up

• If the Fed is concerned about inflation, it will shrink the money supply

• This will drive up the price of money and discourage spending, which should slow inflation

© 2010 Pearson Education, Inc. All rights reserved 0-54

Monetary Policy

• A Discount rate occurs when the Fed changes the interest rate it charges to the banks when it loans them money

• The Fed uses the money supply to impact interest rates

• Banks use the option of borrowing money from the Fed only on occasion

• Either of these actions are designed to slow the economy or stimulate the economy

© 2010 Pearson Education, Inc. All rights reserved 0-55

Monetary Policy

• The Fed has to maintain a balance

• It wants enough money in the economy to encourage economic growth, but not too much because to cause inflation

• Keep the Fed’s overall goals in mind: stable prices, economic growth, and full employment

© 2010 Pearson Education, Inc. All rights reserved 0-56

Check Your Financial IQ

• What is the main tool the Fed uses to influence the economy?

© 2010 Pearson Education, Inc. All rights reserved 0-57

Check Your Financial IQ

• The Fed changes the money supply

© 2010 Pearson Education, Inc. All rights reserved 0-58

Summary

• Banks and other financial institutions offer individual services such as:– making personal loans– accepting deposits– providing accounts that allow you to draft payments

• There are two types of institutions: – Depository institutions– Nondepository institutions

© 2010 Pearson Education, Inc. All rights reserved 0-59

Summary

• One of the most widely used banking services is the checking account

• Checking accounts allow us to have an accurate record of our payments and to carry less check

• Many banks provide debit cards to their checking account holders

• A debit card enables you to withdraw cash from your checking account

© 2010 Pearson Education, Inc. All rights reserved 0-60

Summary

• Other services provided by banking institutions are the following:– Safety deposit boxes– Cashier’s checks– Money orders– Travelers checks

• Banks also offer services for credit payment

© 2010 Pearson Education, Inc. All rights reserved 0-61

Summary

• The FDIC and NCUSIF are two major insurers for most financial institutions

• Most financial institutions have deposit insurance to protect your money up to some maximum amount

© 2010 Pearson Education, Inc. All rights reserved 0-62

Summary

• The Fed is the heart of the banking system and regulates banking and the whole economy

• The Fed’s major economic goals are to:– create ongoing economic growth– encourage full employment– promote price stability

• The Fed uses monetary policy to help accomplish these goals

© 2010 Pearson Education, Inc. All rights reserved 0-63

Key Terms and Vocabulary

• Automatic Teller Machine (ATM)• Bank draft• Cashier’s check• Check• Check register• Checking account• Credit union• Debit card• Depository institutions• Discount rate• Electronic funds transfer• Federal Deposit Insurance

Corporation( FDIC)• Federal Reserve System

• Fiat money• Inflation• Monetary policy• Money orders• National Credit Union Savings

Insurance Fund (NCUSIF)• Negotiable order of withdrawal

(NOW) accounts• Nondepository institutions• Personal identification number

(PIN)• Price level stability• Safety deposit boxes• Travelers checks

© 2010 Pearson Education, Inc. All rights reserved 0-64

Websites

• www.bls.gov

• Dir.yahoo.com/

• www.fdic.gov

• www.federalreserveeducation.org

• www.federalreserve.gov

© 2010 Pearson Education, Inc. All rights reserved 0-65