Embed Size (px)

DESCRIPTION

banking service

Citation preview

INTRODUCTION: - SERVICE TAX

Service tax is a tax levied by Central Government of India on services provided or to be provided excluding services covered under negative list and considering the Place of Provision of Services Rules, 2012 and collected as per Point of Taxation Rules, 2011 from the person liable to pay service tax. Person liable to pay service tax is governed by Service Tax Rules, 1994 he may be service provider or service receiver or any other person made so liable. It is an indirect tax wherein the service provider collects the tax on services from service receiver and pays the same to government of India.[1] Few services are presently exempt in public interest via Mega Exemption Notification 25/2012-ST as amended up to date & few services are charged service tax at abated rate as per Notification No. 26/2012-ST as amended up to date. Presently from 1 June 2015, service tax rate has been increased to consolidated rate @ 14% of value of services provided or to be provided. The service tax rate now is consolidated rate as education cess & secondary higher education cess are subsumed with 2% of "Swachh Bharat Cess(0.50%)" has been notified by the Government

From 15 November 2015, the effective rate of service tax plus Swachh Bharat Cess, post introduction of Swachh Bharat Cess, will be 14.5%.

HISTORY OF SERVICE TAX

Dr. Raja Chelliah Committee on tax reforms recommended the introduction of service tax. Service tax had been first levied at a rate of five per cent flat from 1 July 1994 till 13 May 2003, at the rate of eight percent flat w.e.f 1 plus an education cess of 2% thereon w.e.f 10 September 2004 on the services provided by service providers. The rate of service tax was enhanced to 12% by Finance Act, 2006 w.e.f 18.4.2006. Finance Act, 2007 has imposed a new secondary and higher education cess of one percent on the service tax w.e.f 11.5.2007, increasing the total education cess to three percent and a total levy of 12.36 percent. The revenue from the service tax to the Government of Indiahave shown a steady rise since its inception in 1994. The tax collections have grown substantially since 1994-95 i.e. from 410₹ crore (US$61 million) in 1994-95 to 132518₹ crore (US$20 billion) in 2012-13. The total number of Taxable services also increased from 3 in 1994 to 119 in 2012. However, from 1 July 2012 the concept of taxation on services was changed from a 'Selected service approach' to a 'Negative List regime'. This changed the taxation system of services from tax on some Selected services to tax being levied on the every service other than services mentioned in Negative list.

Rates

While presenting the 2015 Union budget of India, the FM had increased the Service Tax Rate from 12.36% to 14%. This new rate of Service Tax @ 14% was applicable from 1st June 2015. Moreover from 15th Nov 2015, Swachh Bharat Cess @ 0.5% also got applicable. Therefore the effective rate of Service Tax is currently at 14.5% with effect from 15th Nov 2015.[3] 2016 Union budget of India has proposed to impose a Cess, called the Krishi Kalyan Cess, @ 0.5% on all taxable services effective from 1 June 2016. The new effective service tax could henceforth be 15%.

Service Tax Return, Records & Invoices

Records

According to Rule 5 of Service Tax Rules, 1994, records include computerized data and means the record as maintained by an assessee in accordance with the various laws in force from time to time. Records maintained as such shall be acceptable to Central Excise Officer. Every assessee is required to furnish to the Central Excise Officer at the time of filing his return for the first time a list of all accounts maintained by the assessee in relation to Service Tax including memoranda received from his branch offices. This intimation may be sent along with a covering letter while filing the service tax return for the first time

Invoice

Rule 4A prescribes that taxable services shall be provided and input credit shall be distributed only on the basis of a bill, invoice or challan. Such bill, invoice or challan will also include documents used by service providers of banking services (such as pay-in-slip, debit credit advice etc.) and consignment note issued by goods transport agencies. Rule 4B provides for issuance of a consignment note to a customer by the service provider in respect of goods transport booking services.

RECENT CHANGES

Budget 2016 Update: Finance Minister while presenting the Budget 2016 introduced a new Cess called the Krishi Kalyan Cess. This Cess would be levied on all taxable services and would be levied @ 0.5% of the total value of service. This Cess would be levied over and above the Service Tax and the Swachh Bharat Cess.

This Cess would be applicable from 1st June 2016. Before 1st June 2016 – only Service Tax @ 14% and Swachh Bharat Cess @ 0.5% would be applicable but from 1st June 2016 – Krishi

Kalyan Cess would also be applicable and then the effective rate of tax would become 15%. Before, 1st June – it is 14.5%.

What is Service Tax?It is a tax which is payable on services provided by the service provider. Just like Excise duty is payable on goods which are manufactured, similarly Service Tax is payable on Services provided.

This Tax is payable by the provider of Service to the Govt. of India. However, the Service Provider can collect this Tax from the Consumer of Service (also referred to as Recipient of Service) and deposit the same with the Govt.

Applicability of Service Tax

This tax came into effect in 1994 and was introduced by the then Finance Minister Dr. Manmohan Singh. Earlier Service Tax was payable only on a specified list of services but Pranab Mukherjee while delivering his budget speech on 16th March 2012 announced that this Tax would be applicable on all services except the negative list of services. From 1st July 2012 onwards, all services (except those specified in the negative list of services by the Govt) are now liable for service tax.

However, there are some services which are composite services. For eg: Food being served inRestaurant. Although VAT is levied on Food, but we don’t go to a Restaurant only to have Food but also to avail the services of the waiters, kitchen staff etc. Therefore, Service Tax is also leviedon Food served in Restaurant. In such cases, it is practically impossible to segregate how much the customer has paid for the food and how much he has paid for the services.

Such services are popularly known as Composite Services and in such cases an abatement scheme is announced by the govt under which Service Tax is only levied only on a specified portion of the Total Bill.

Service Tax On Cash Basis

Earlier Service Tax was charged on cash basis for every service provider. Currently, it is charged on cash basis for Individual service providers and for companies it is being charged on accrual basis i.e companies liability to deposit tax arises as soon as services are provided irrespective of the collection of funds on the same.

However Individual Service Providers have to deposit this Tax with the Govt only when the Invoice Amount has been collected. Service Tax Payment is deposited by the Service Provider with the Govt. quarterly in case of Individuals/Partnership and Monthly in all other cases.

Moreover, every Service Provider is now required to apply for Service Tax Registration if the Value of Services provided by him during a Financial Year is more than Rs. 9 Lakhs, but the Tax would be payable only when the Value of Services provided is more than Rs. 10 Lakhs.

All service providers in India, except those in the state of Jammu and Kashmir, are required to pay this tax in India. Service Tax is not levied on the persons residing in Jammu & Kashmir.

Service Tax Rate

The Service Tax Rate applicable from 1st June 2015 is 14%. This rate is an inclusive rate and SHEC and Education Cess is not required to be charged above this.

This Tax is required to be deposited on a Monthly/Quarterly basis. It can be paid either by manually depositing in the Bank or through Online Payment of Service Tax. In case, of excess payment of Tax by the Service Provider with the Governement, the Service Provider can either adjust the excess amount paid or can claim Refund of the Excess Tax deposited. Refer: Service Tax Refund

Case Study

Let’s understand via simple case, If a Chartered Accountant, provides services in the capacity of auditor to ABC Ltd. and the audit fees is Rs. 1,00,000 then the service tax chargeable will be 14.5% on Rs. 1,00,000 i.e. INR 14,000. Hence, the total billing to be done by CA to ABC Ltd will be INR 1, 14,500.

The segregation of Value of Service Provided (i.e. Rs. 1,00,000) and the Tax payable thereon (i.e. Rs. 14,500) shall be separately showing on the Invoice.

In case, no tax is separately charged in Invoice or the service receiver makes partial payment then the service tax shall be proportionately taken to be amount as on the gross amount received by the service provider for the taxable service provided or to be provided by him.

INTRODUCTION: - SERVICE TAX IN BANKING

Banking and financial services are subject to levy of Service Tax in more than one form. While only specific services were taxed prior to 1.7.2012, all such services are taxable now barring those which are in negative list.

W.e.f.1.07.2012, all services, other than services specified in the negative list, provided or agreed to be provided in the taxable territory by a person to another would be taxed under section 66B. Service' has been defined in clause (44) of the new section 65B and means -

any activity for consideration carried out by a person for another and includes a declared service.

In short, service means -

any activity carried out by a person for another for consideration includes declared service but does not include

o transfer in title of goods or immovable propertyo transaction in money or actionable claimo provisions of service by employee to employero deemed sale of goodso duties performed by MP/MLA/Members of Municipal Corporation, Panchayats or

Local authorities person holding constitutional posts.

Since all banking companies including cooperative banks satisfy all the conditions of 'service', their services shall be taxable, subject to provisions of the Service Tax law.

Negative List of Services

Meaning of Negative List (Clause 34 of Section 65B/Section 66D)

Negative list has been defined under clause 34 of section 65B and such services are specified in section 66D of theFinance Act, 1994, as introduced by the Finance Act, 2012. Negative list of services would mean the services specified in section 66D which specifies seventeen broad categories of services. Only the following negative list entry is relevant for bank -

i. extending deposits, loans or advances in so far as the consideration is represented by way of interest or discount;

ii. inter se sale or purchase of foreign currency amongst banks or authorised dealers of foreign exchange or amongst banks and such dealers.

Interest

Interest has been defined in section 65B(30) of the Finance Act, 1994 as under-

‘interest’ means interest payable in any manner in respect of any money borrowed or debt incurred (including a deposit, claim or other similar right or obligation) but does not include any service fee or other charge in respect of the moneys borrowed or debt incurred or in respect of any credit facility which has not been utilized.

It should only be in the form of interest and does not include any service charge, fee or other charge, by whatever name called. For example, processing charges, pre-payment fee, late fee, cheque bounce charges etc. will not be called interest.

Such ‘interest’ has to be paid or received in relation to -

Money borrowed Debt incurred Deposit Claim or other similar right or obligation

Any charges or amounts collected over and above the interest or discount amounts would represent taxable consideration. Invoice discounting or cheque discounting or any similar form of discounting is covered only to the extent consideration is represented by way of discount as such discounting is nothing else but a manner of extending a credit facility or a loan.

The negative list entry covers any such service wherein moneys due are allowed to be used or retained on payment of interest or on a discount. The words used are ‘deposits, loans or advances and have to be taken in the generic sense. They would cover any facility by which an amount of money is lent or allowed to be used or retained on payment of what is commonly called the time value of money which could be in the form of an interest or a discount. This entry would not cover investments by way of equity or any other manner where the investor is entitled to a share of profit.

Illustrations of services covered in negative list could be as follows -

Fixed deposits or saving deposits or any other such deposits in a bank for which return is received by way of interest.

Providing a loan or over draft facility or a credit limit facility in consideration for payment of interest.

Mortgages or loans with a collateral security to the extent that the consideration for advancing such loans or advances are represented by way of interest.

Corporate deposits to the extent that the consideration for advancing such loans or advances are represented by way of interest or discount.

Repos / Reverse Repos

Repos and reverse repos are financial instruments of short term call money market that are normally used by banks to borrow from or lend money to RBI. The margins, called the repo rate or reverse repo rate in such transactions are nothing but interest charged for lending or borrowing of money. Thus, they have the characteristics of loans and deposits for interest. However, they are more appropriately excluded from the definition of service itself being the sale and purchase of securities, which are goods.

Commercial Paper (‘CP’) and Certificate of Deposit (‘CD’)

Commercial paper (‘CP’) and Certificate of Deposit (‘CD’) are instruments for lending or borrowing money where in consideration is represented by way of a discount issue or subscription to CPs or CDs would be covered in the negative list entry relating to ‘services by way of extending deposits, loans or advances insofar as consideration is represented by way of interest or discount’. It may also be borne in mind that promissory note is included in the definition of money in the Act as given in clause (33) of section 65B.

However, if some service charges or service fees or documentation fees or broking charges or such like fees or charges are charged, the same would be considerations for provision of service and chargeable to service tax.

Credit Cards

In case of a credit card, issuing entity allows the facility of payment of the purchases made by the card holder within a specified period failing which some charges are levied. The question that arises is whether the credit so extended for this payment is in the nature of a loan or advance for interest.

Interest for delayed payment of any consideration for the sale of goods or provision of service has been specifically excluded from value by rule 6 of valuation rules. Thus ordinarily any interest charged for delayed payment of consideration would be outside the gambit of service tax. However in the case of credit cards the credit extended is not for the delayed payment of consideration for the provision of services. The services in the case of the credit card are by way of levy of issuing charges or the commission charged from merchants etc. The interest in this case is not for the consideration for the use of the card. Thus the benefit under the valuation rules will not be available to credit card companies.

The other question is whether such credit extended will amount to loans or advances. Loans and advances are meant to signify amounts contractually negotiated as such (loan or advance) and not merely failure to pay an amount at the due date. The exorbitant charges have also no relationship with the prevailing interest for the same class of creditworthiness and are in the nature of consideration for the services rendered for using the convenience of using the services by way of a credit card and hence taxable.

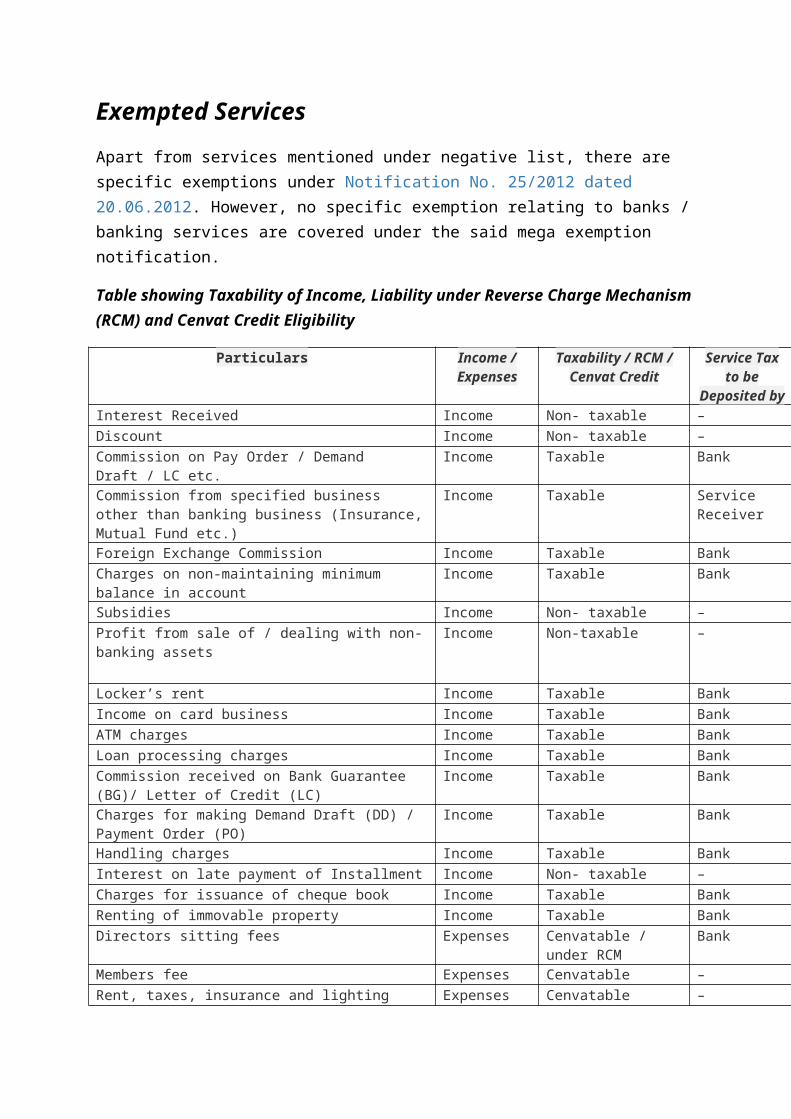

Exempted Services

Apart from services mentioned under negative list, there are specific exemptions under Notification No. 25/2012 dated 20.06.2012. However, no specific exemption relating to banks / banking services are covered under the said mega exemption notification.

Table showing Taxability of Income, Liability under Reverse Charge Mechanism (RCM) and Cenvat Credit Eligibility

Particulars Income / Expenses

Taxability / RCM / Cenvat Credit

Service Tax to be

Deposited byInterest Received Income Non- taxable –Discount Income Non- taxable –Commission on Pay Order / Demand Draft / LC etc. Income Taxable BankCommission from specified business other than banking business (Insurance, Mutual Fund etc.)

Income Taxable Service Receiver

Foreign Exchange Commission Income Taxable BankCharges on non-maintaining minimum balance in account

Income Taxable Bank

Subsidies Income Non- taxable –Profit from sale of / dealing with non-banking assets Income Non-taxable –

Locker’s rent Income Taxable BankIncome on card business Income Taxable BankATM charges Income Taxable BankLoan processing charges Income Taxable BankCommission received on Bank Guarantee (BG)/ Letter of Credit (LC)

Income Taxable Bank

Charges for making Demand Draft (DD) / Payment Order (PO)

Income Taxable Bank

Handling charges Income Taxable BankInterest on late payment of Installment Income Non- taxable –Charges for issuance of cheque book Income Taxable BankRenting of immovable property Income Taxable BankDirectors sitting fees Expenses Cenvatable / under

RCMBank

Members fee Expenses Cenvatable –Rent, taxes, insurance and lighting expenses Expenses Cenvatable –Security Expenses Expenses Cenvatable –Law charges Expenses Cenvatable / under

RCMBank

Postage and Telegram Expenses Expenses Cenvatable –Telephone charges Expenses Cenvatable –Auditor’s fees Expenses Cenvatable –Repair and maintenance of premises / ATM machines

Expenses Cenvatable –

Revenue Stamps Expenses – –Sweeping and cleaning charges Expenses – –Loss from sale of or dealing with non-banking assets Expenses Cenvatable –Advertisement Expenses Cenvatable –Recovery Agent fees / commission Expenses Cenvatable / under

RCMBank

Service Tax charged by Banks on Interest/ Finance Charges charged on delayed Credit Card Payments

It has come to my notice that several banks are charging service tax on interest and finance charges on credit card payments. In certain cases although the nomenclature is clearly mentioned as "Interest" still the bank has charged service tax. In this case when I protested about this issue by sending an email to the bank I got an immediate reply reversing the Interest and service tax.

Although I considered myself fortunate to have saved some money in the bargain, I think this situation needs serious correction. The crux of the matter is that most Banks have an unwritten policy to charge service tax on almost all services which they provide probably to be on the safe side to avoid entering into litigation with the department. They end up charging the customer who rarely has the time or in most cases the know-how to question these charges and when someone question they hastily refund the amount.

I trust that most of my intellectually enlightened brethren would agree that as much as we all believe that "We should give Caesar what is due to him" we should also believe that "We should not give Caesar what is not due to him".

In line with this policy, I emailed the relevant banks saying that charging service tax on interest/ finance charges is not in order and it does not matter whether you refund my interest or not, the very basis of the charge is defective due to reasons which I have explained below. In my case, in the case of two banks service tax has been charged on interest and finance charges for which I had sent my objections to them. The replies received from these banks were unsatisfactory and virtually stated that these charges are done as per the "Service Tax Provisions" none of which was quoted in the letter.

To clarify the position as per Service tax law, the relevant provisions are listed as follows:

* As per Section 65(105)(zzzw) of Finance Act, 1994, "credit card or other payment card services" are "services provided or to be provided to any person, by any other person, in relation to credit card, debit card, charge card or other payment card service, in any manner." The value for the taxable service will be the gross amount charged by the service provider for such services. The basic element of taxability under this head is that the transaction should amount to "Service", which is not satisfied in the case of Interest charged on delayed payments.

* There is another head which is relevant to this discussion i.e. "Banking and Other Financial Services". As perSection 65(105)(zm) introduced in the Finance Act, 1994, "Banking and Other Financial Services" are "Services provided or to be provided to a customer by a banking company or a financial institution, including a non-banking financial company, or any other body corporate or any other person in relation to banking and other financial services."

* In terms of Section 65(12) of the Act, banking and financial services specifically include lending of money.

* Any loan given by a bank, even though it is a short term loan under a credit card is lending by a bank and as such this service will be more appropriately be covered under the head "Banking and other Financial Services".

* Finally, for calculating the taxable value of the services, as per clause (iv) Rule 6(2) of Service Tax (Determination of Value) Rules 2006, any "interest" charged on the loans advanced cannot be included.

Under such circumstances, the bank cannot charge any service tax either on the repayment amounts or the interest charged on the principal amounts.

Service tax can only be charged on the amounts collected as their charges for providing the loan , under heads such as `administrative expenses', `commissions', `service charges', processing fees etc.

I feel this situation needs to be addressed and corrected and someone needs to start the process and hence this article so that when you are making your credit card payments please make sure that you are not paying service tax on interest charged on delayed payments.

I am sure that if you protest the bank will end up reversing the interest charged also.

Service tax finds several banking services taxable on scrutiny

The Department of Service tax has found several banking services taxable on scrutiny following the negative list of services.

According to officials close to the development, some of the contentious issues are availing tax credit for payment of premium for insuring deposits, services rendered on behalf of the Reserve Bank of India (RBI) and commission on foreign exchange business. At present the banks treat most of these services exempt but they are not as per the department, sources said

The Department of Service Tax has also issued show cause notices to several banks in raising demand.

Explaining this, an official source said the banks pay premium to Deposit Insurance and Credit Guarantee Corporation (DICGC) for insuring their deposit (fixed deposits, saving banks deposits and current account) and pay 12% of the total amount paid premium as

service tax.

Then these banks take credit for the service tax paid on these items for payment of taxes on other taxable services. The credit is availed by the banks for paying the service tax on insuring these items (various deposits) as according to banks these deposits are output services as per service tax rules.

However the Department is of the view that as per the rule 6 of the Cenvat Credit rules 2004, these deposits form part of negative services and not output services. Cenvat rules make it obligatory to get credit for payment of taxes on output services and not negative services as per the negative list. An output service is defined as any taxable service within taxable territory of India but does not include negative services as per cenvat credit rules and reverse charge payments.

While the department has found several omissions by the banks on this account in its scrutiny amounting to a lapse of around Rs 2,000-2,500 crore across the banking sector, this issue is still is under deliberation, said sources Similarly, the RBI pays commission to the banks for collecting government taxes – customs, service tax, income tax etc. These are services rendered by the banks on behalf of the RBI. While department contends that banks should pay service tax on the commission received, banks at present do no pay service taxes.

Kerala Bench of CESTAT (Customs, Excise and Service Tax Appellate Tribunal) held that banks will not pay services tax on commission received from RBI on these services.

The department is of the view that as per the negative list, services rendered by RBI are exempt from service but services to RBI and services undertaken on behalf of the RBI are taxable as these are rendered free. These banks receive commission for these services discharged on behalf of the RBI and hence should pay service tax.

To this effect, a total demand has been firmed up to the tune of Rs 80-100 crore and show cause notices have been issued to banks.

BANKING SERVICES UNDER FINANCE ACT, 1994

The service provided by banking company will be covered under the definition of service under section 65B (44) ofFinance Act, 1994.

Section 65B (44) of Finance Act, 1994 reads as below:

“Service means any activity carried out by a person for another for consideration, and includes declared services,

but does not include (i)….. (ii) ….. (iii) a transaction in money or actionable claim”.And further clause (n) of section 66D “Negative List of Services” specifies certain services related to banking services as non taxable which reads as follows

“Services by way of:

1. Extending deposits, loans and advances in so far as the consideration is represented by way of interest and discounts.

2. Inter se sale or purchase of foreign currency amongst banks or authorized dealers of foreign exchange or amongst banks and such dealers”

By the virtue of above read sections all the income earned by bank will fall under service tax net except income in the nature of interest or discounts and sale and purchase of foreign currency amongst banks and financial institutions.

DEPOSITS, LOANS OR ADVANCES

The meaning of deposits, loans or advances as explained in CBEC’s Education Guide are replicated below:

a. Fixed deposits or saving deposits or any other such deposits in a bank or a financial institution for which return is received by way of interest.

b. Providing a loan or overdraft facility or a credit limit facility in consideration for payment of interest or discountc. Mortgages or loan with a collateral security to the extent that the consideration for advancing such loans or advances is represented by way of interest or discounts.

d. Corporate deposits to the extent that the consideration for advancing such loans or advances are represented by way of interest or discount.

INTEREST OR DISCOUNT

The word ‘interest’ has been defined under section 65B (30) as:

”Interest means interest payable in any manner in respect of any moneys borrowed or debt incurred (including a deposit, claim or similar rights or obligations) but does not include any service fee or other charges in respect of money’s borrowed or debt incurred or in respect of any credit facility which has not been utilized”

And further clause (iv) of rule 6 (2) [rule 6 of service tax (determination of values) Rules 2006] which specifies the inclusion and exclusion of value of taxable services specifically exclude ‘Interest on delayed payment’ from value of taxable services. The said rule reads as follows

“Interest on delayed payment of any consideration for the provision of service or sales of property, whether movable or immovable”

In the light of the above read provision and rules, it is clarified that interest payable on deposit, loans or advances and interest on delayed payment are fall outside the gambit of service tax and no tax is payable on such services.

However service fee or any other charges in respect of money borrowed or debt incurred or any part of unutilized credit facility does not comes under the meaning of interest. Hence on such charges or fees service tax is payable.

SALE OR PURCHASE OF FOREIGN CURRENCY

Clause (n) (ii) of section 66D excludes sale or purchase of foreign currency from leviability of service tax, if such sale or purchase takes place:

a. Amongst banks

b. Amongst authorized dealers

c. Amongst banks and such dealers

Service tax is not leviable in sale or purchase of foreign currency only when such service takes place amongst the persons authorized to deal in foreign currency. The tax is payable when sales or purchases takes place to/from the final consumers of foreign currency.

As per rule 2B of service tax (determination of value) Rules, 2006 value of purchase and sales of foreign currency including money changing provided by banks shall be determined by the service provider as follows:

SERVICES PROVIDED BY THE RBI

Services provided by the RBI are non taxable services as the same specified under ‘Negative List of Services’. Clause (b) of section 66D reads as follows:

“Services by the Reserve Bank of India” Only the service provided by RBI is non-taxable service but not:

a. Any services provided to RBI

b. Services provided by any other subsidiary banks of the RBI.

c. When similar services provided by other banks authorized by the RBI

There are some services where the service recipient is liable to pay service tax. If any such services are received by the RBI, then it will be liable to pay service tax under reverse charges.

Banking and financial service

Definition:

Finance act, 1994 has stated following definition relating to banking and financial services:

As per section 2(14) of the act "authorised dealer of foreign exchange" shall have the meaning assigned to "authorised person" in clause (c) of section 2 of the Foreign Exchange Management Act, 1999

As per section 2(30) of the act, "interest" has the meaning assigned to it in clause (28A) of section 2 of the Income-tax Act, 1961

As per section 2(33) of the act, "money" means legal tender, cheque, promissory note, bill of exchange, letter of credit, draft, pay order, traveller cheque, money order, postal or electronic remittance or any similar instrument but shall not include any currency that is held for its numismatic value;

As per section 2(42) of the act, "Reserve Bank of India" means the bank established under section 3 of the Reserve Bank of India Act, 1934.

As per section 2(43) of the act, "securities"(1) has the meaning assigned to it in clause (h) of section 2 of the Securities Contract (Regulation) Act, 1956;

Mega exemption notification no. 25/2012-ST, dated 20th June, 2012, “banking company” has the meaning assigned to it in clause (a) of section 45A of the Reserve Bank of India Act, 1934.

As per notification no - 26/2012, Service Tax, 20th June, 2012 - “chit” means a transaction whether called chit, chit fund, chitty, kuri, or by whatever name by or under which a person enters into an agreement with a specified number of persons that every one of them shall subscribe a certain sum of money (or a certain quantity of grain instead) by way of periodical installments over a definite period and that each subscriber shall, in his turn, as determined by lot or by auction or by tender or in such other manner as may be specified in the chit agreement, be entitled to a prize amount.

As per Place of provisions of rule, 2012, "non-banking financial company" means-

(i) a financial institution which is a company; or

(ii) a non-banking institution which is a company and which has as its principal business the receiving of deposits, under any scheme or arrangement or in any other manner, or lending in any manner; or

(iii) such other non-banking institution or class of such institutions, as the Reserve Bank of India may, with the previous approval of the Central Government and by notification in the Official Gazette specify

1.2. Exemption on transaction relating to banking and financial service:

As per section 66D(b) negative list of services, services provided by Reserve Bank of India would be exempt from service tax.

As per section 66D(n) –negative list of services, following activities would be exempt from service tax: services by way of-

(i) extending deposits, loans or advances in so far as the consideration is represented by way of interest or discount;

(ii) inter se sale or purchase of foreign currency amongst banks or authorized dealers of foreign exchange or amongst banks and such dealers.

Examples on the above negative services are:

· Fixed deposits or saving deposits or any other such deposits in a bank or a financial institution for which return is received by way of interest.

· Providing a loan or overdraft facility or a credit limit facility in consideration for payment of interest.

· Mortgages or loans with a collateral security to the extent that the consideration for advancing such loans or advances are represented by way of interest.

· Corporate deposits to the extent that the consideration for advancing such loans or advances are represented by way of interest or discount.

Further, as per entry no. 29 of mega exemption notification 25/2012-ST, dated 20th June, 2012, services provided by a business facilitator or a business correspondent to banking company or an insurance company, in a rural area would be exempt from service tax. (“business facilitator or business correspondent” means an intermediary appointed under the business facilitator model or the business correspondent model by a banking company or an insurance company under the guidelines issued by Reserve Bank of India)

1.3. Valuation of service

Options for determination of service tax on sale and purchase of foreign exchange to others:

Option1 : Service tax on value of service: As per Rule 2B of service tax (Determination of Value) Rules, 2011 and text of Guidance notes on service tax issued by CBEC on 20th June, 2012 valuation would be done in following manner:

· Manner of determination of value of service in relation to money changing including sale and purchase of foreign currency: If a currency is exchanged from or to Indian Rupees then, as per Rule 2B of the Valuation Rules, the value of taxable service shall be equal to the difference in the buying rate or the selling rate, as the case may be, and the RBI reference rate for that currency. For example if US$ 1000 are sold by a customer @ Rs55 per US$ and RBI reference rate for US$ is Rs.55.73 then the taxable value shall be Rs.730 (1000 x 0.73).

· Manner to determine value if the RBI reference rate for a currency is not available: As per the first proviso to Rule 2B in case RBI reference rate for a currency is not available the value shall be 1% of the gross amount of Indian Rupees provided or received by the person changing the money.

· Manner to determine value of taxable service if foreign currency is exchanged for another foreign currency: These situations are dealt with in second proviso to Rule 2B as per which in such situations the value of taxable service shall be equal to 1% of the lesser of the two amounts the person changing the money would have received by converting one of the currencies into Indian Rupees on that day at the reference rate provided by RBI.

Option 2: Composition scheme: As per Rule (7B) of service tax Rules, person liable to pay service tax has option to pay service tax at following rates, instead of full rate of service tax:

· 0.12 percent of the gross amount of currency exchanged for an amount upto rupees 100,000 subject to the minimum amount of rupees 30; and

· Rupees 120 and 0.06 per cent. of the gross amount of currency exchanged for an amount of rupees exceeding rupees 100,000 and upto rupees 10,00,000; and

· Rupees 660 and 0.012 per cent. of the gross amount of currency exchanged for an amount of rupees exceeding 10,00,000, subject to maximum amount of rupees 6000

The person providing the service shall exercise above option for a financial year and such option shall not be withdrawn during the remaining part of that financial year.

Service tax on services provided in relation to Chit funds: As per notification no. 26/2012-ST dated 10-6-2012, service tax would be payable on 70% of amount charged subject to Cenvat credit on input, input services and capital goods is not availed.

1.4. Place of provision of service

As per rule 9 of place of provisions rules, 2012, place of provision of services in case of Services provided by a banking company, or a financial institution, or a non-banking financial company, to account holders shall be the location of the service provider.

CBEC has provided following clarification in Text of Guidance notes on service tax issued by CBEC on 20th June, 2012:

Meaning of “account holder”: “Account” has been defined in the rules to mean an account which bears an interest to the depositor. Services provided to holders of demand deposits, term deposits, NRE (non-resident external) accounts and NRO (non-resident ordinary) accounts will be covered under this rule.

Banking services provided to persons other than account holders will be covered under the main rule (Rule 3- location of receiver).

Services that are provided by a banking company to an account holder (holder of an account bearing interest to the depositor)

Following are examples of services that are provided by a banking company or financial institution to an “account holder”, in the ordinary course of business:-

i) services linked to or requiring opening and operation of bank accounts such as lending, deposits, safe deposit locker etc;

ii) transfer of money including telegraphic transfer, mail transfer, electronic transfer etc.

Services that are not provided by a banking company or financial institution to an account holder, in the ordinary course of business, and consequently not to be covered under this Rule:

Following are examples of services that are generally NOT provided by a banking company or financial institution to an account holder (holder of a deposit account bearing interest), in the ordinary course of business:-

i) financial leasing services including equipment leasing and hire-purchase;

ii) merchant banking services;

iii) Securities and foreign exchange (forex) broking, and purchase or sale of foreign currency, including money changing;

iv) asset management including portfolio management, all forms of fund management, pension fund management, custodial, depository and trust services;

v) advisory and other auxiliary financial services including investment and portfolio research and advice, advice on mergers and acquisitions and advice on corporate restructuring and strategy;

vi) banker to an issue service.

In the case of any service which does not qualify as a service provided to an account holder, the place of provision will be determined under the default rule i.e. the Main Rule 3. Thus, it

will be the location of the service receiver where it is known (ascertainable in the ordinary course of business), and the location of the service provider otherwise.

1.5. Cenvat credit restriction

As per rule 6(3B) of Cenvat credit rule, 2004, a banking company and a financial institution including a non-banking financial company, engaged in providing services by way of extending deposits, loans or advances, shall pay for every month an amount equal to fifty per cent. of the CENVAT credit availed on inputs and input services in that month.

1.6. Records of banking and financial institutions

As per rule 4A of service tax rule, 1994, if provider of taxable service is a banking company or a financial institution including a non-banking financial company providing service to any person, then:-

· Within 45 days the invoice, bill or challan, as the case may be, is to be issued

· an invoice, a bill or, as the case may be, challan shall include any document, by whatever name called, whether or not serially numbered, and whether or not containing address of the person receiving taxable service.

1.7. Relevant notifications and circulars:

Taxability on transaction relating banking and financial services clarified in CEBEC’s Taxation of service: An Education Guide issued on 20th June, 2012:

· Transaction in Commercial Paper (CP) or Certification of Deposit (CD): Transaction like Issue, subscription or trading in CP and CD would be outside ambit of definition of ‘Service’.

· Invoice discounting or cheque discounting or any other similar form of discounting: Such discounting would be exempt from service tax only to the extent consideration is represented by way of discount.

· Transaction in Repos and reverse repos: Such transaction would be outside ambit of definition of ‘service’.

· Transaction in forward contracts in commodities and currencies or future contracts: Such transaction would be outside ambit of definition of ‘service’.

· Charges for making drafts, letter of credit issuance charges relating to CP/ CDs: Such charges would be chargeable to service tax subject to other element of taxability are present.

· Service charges or administration charges received in addition of interest on a loan, advance or a deposit: Such charges would be chargeable to service tax subject to other element of taxability are present.

· Service charges, service fees, documentation fees, broking fees or such like fees or charges charged on forward contract, future contracts, repos/reverse repos, CD, CPs: Such charges would be chargeable to service tax subject to other element of taxability are present.

· Late payment of dues on credit card outstanding: Charges for late payment of dues on credit card outstanding would be chargeable to service tax. Further, credit extended after due date of payment on credit card will not amount to loans and advances but the same would be considered in nature of consideration for the services rendered for using the convenience of using the services by way of a credit card and hence taxable.

· Pre-closer charges, commitment charges, fore-closer charges, charges for pre-payment of loan, reset or restructuring loan charges: Such charges would be chargeable to service tax subject to other element of taxability are present.

· Sale and purchase of foreign exchange: sale and purchase of foreign exchange between banks or authorized dealers of foreign exchange or between banks and such dealers would be exempt from service tax. However, services provided by banks or authorized dealers of foreign exchange by way of sale of foreign exchange to general public would not be exempt under negative list of services.

1.8. Judgments

· Madhav Nagrik Sahkari Bank v. CCE (2012) 35 STT 154 (CESTAT) - Cooperative banks are subject to service tax.

· Punjab national Bank v. CCE, Chandigarh (2009) 14 STR 465 (Cestat, New delhi) service of MICR (magnetic ink character recognition) for cheque clearing was held as taxable service.

· State bank of India v. CST, Kolkata (2009) 16 STR 640 (Cestat, Kolkata) – cheque processing services are liable to service tax.

· Housing Development Finance corporation ltd v. CST, Ahmedabad (2012) 34 STT 129 (Cestat, Ahmedabad) - reset charges and pre-payment charges can be considered as cost incurred by borrow and the same were liable to service tax.