Embed Size (px)

Citation preview

Bangladesh Institute of Bank ManagementS e c t i o n N o. - 2, M i r p u r, D h a k a -1216

B W2012ANK-REVIE

BANK-REVIEW 2012

Advisor & Editor

Dr. Toufic Ahmad Choudhury

Report PreparationTeam

Team LeaderDr. Shah Md. Ahsan Habib

MembersMd. Mohiuddin Siddique

Md. Nehal AhmedAtul Chandra Pandit

Editorial AssociatesDr. Bandana Saha

Abed Ali

Bangladesh Institute of Bank ManagementPlot # 4, Main Road # 1(South), Section # 2, Mirpur, Dhaka-1216

PABX: 9003031-5, 9003051-2, Fax: 88-02-9006756Email: [email protected], Web: www.bibm.org.bd

FOREWORDS

III

Preparation of 'Bank-Review 2012' is a collective endeavour of the team members that drews on

support of the faculty colleagues and other staffs of BIBM. This is the second annual issue of the

publication. This time 'the year' with the title of the publication is adjusted. The first issue of the

publication is titled as 'Bank Review 2010’, however this is named as 'Bank Review 2012' considering

the fact that the published data for 2011 can only be made available in mid-2012. In the process of

preparing this report, BIBM library, administration and publication wing have played a proactive role.

The preparation team received immense help and cooperation at the data collection stage from

a good number of executives working in the Bangladesh Bank and in the member banks of BIBM.

In this context, we would like to register our deep appreciation for the support received from the

officials of DOS, BRPD, SME and Statistics Departments of Bangladesh Bank. We are especially grateful

to Mr. Shahriar Siddiqui, Deputy Director, DOS, BB for his continuous support at the stage of data

gathering. We are also grateful to all the officials of relevant desks of commercial banks for their

cooperation. The preparation team is obliged to the faculty members for their suggestions and

support. Finally, we are indebted to the Advisor and Editor of the publication Dr. Toufic Ahmad Choudhury

for his continuous mentoring.

Dr. Shah Md. Ahsan Habib

Md. Mohiuddin Siddique

Md. Nehal Ahmed

Atul Chandra Pandit

V

MESSAGE FROM THE DIRECTOR GENERAL

Bangladesh Institute of Bank Management (BIBM) presents its second issue of the bank review titled

'Bank-Review 2012' - a publication started from the year 2011 that basically seeks to present a unique

way of assessing the strengths and weaknesses of the banking sector institutions of Bangladesh.

The study covers mainly the data of the banks for the calender year 2011.

In the Banking market of Bangladesh, the banks and financial institutions are operating in an intense

competitive environment where they need to locate their market niche so that they can craft and put

into use appropriate financial and marketing strategy. We hope the banks and financial institutions

would be benefited by the analysis contained in the Bank-Review. We, at the BIBM, envision the

Review to be our flagship publication and would welcome comments and suggestions from potential

users to improve upon our presentation.

(Dr. Toufic Ahmad Choudhury)

Director General

VII

CONTENTSAbbreviation IXChapter One: Background & Methodology 1 Background of the Report 3Methodology of the Report 5Limitations of the Report 11Organization of the Report 11

Chapter Two: Governance, Activities and Operations of Banks 13

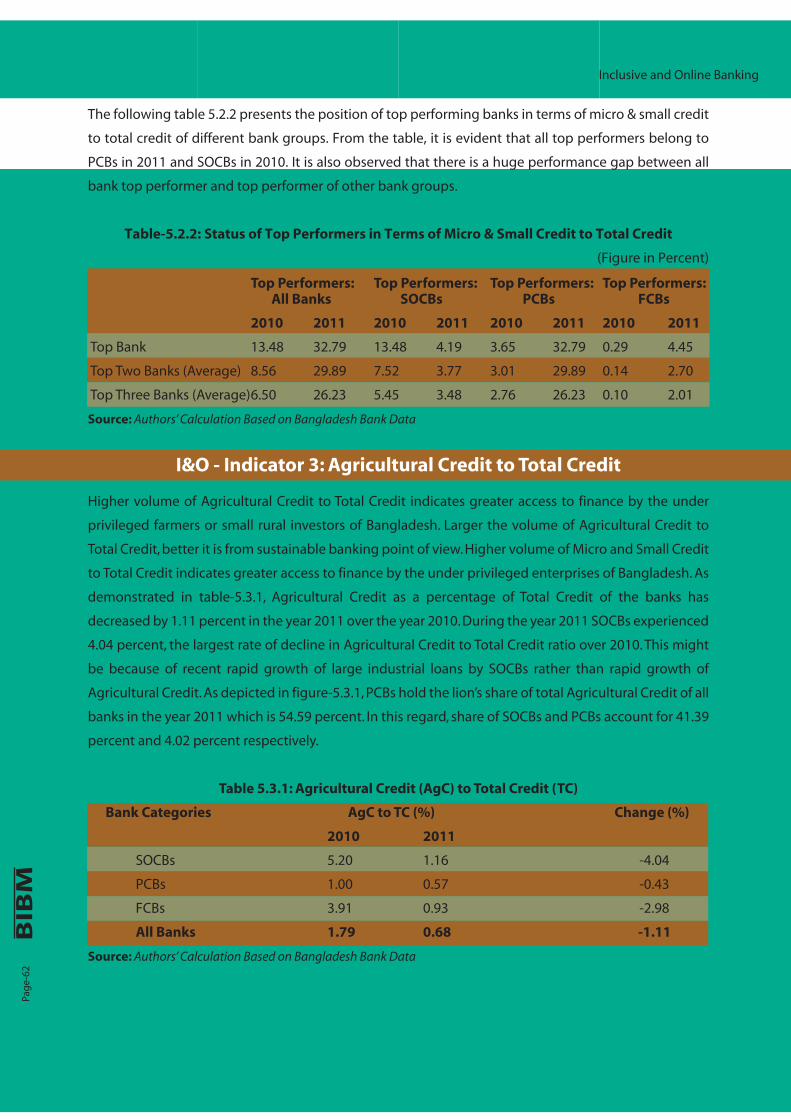

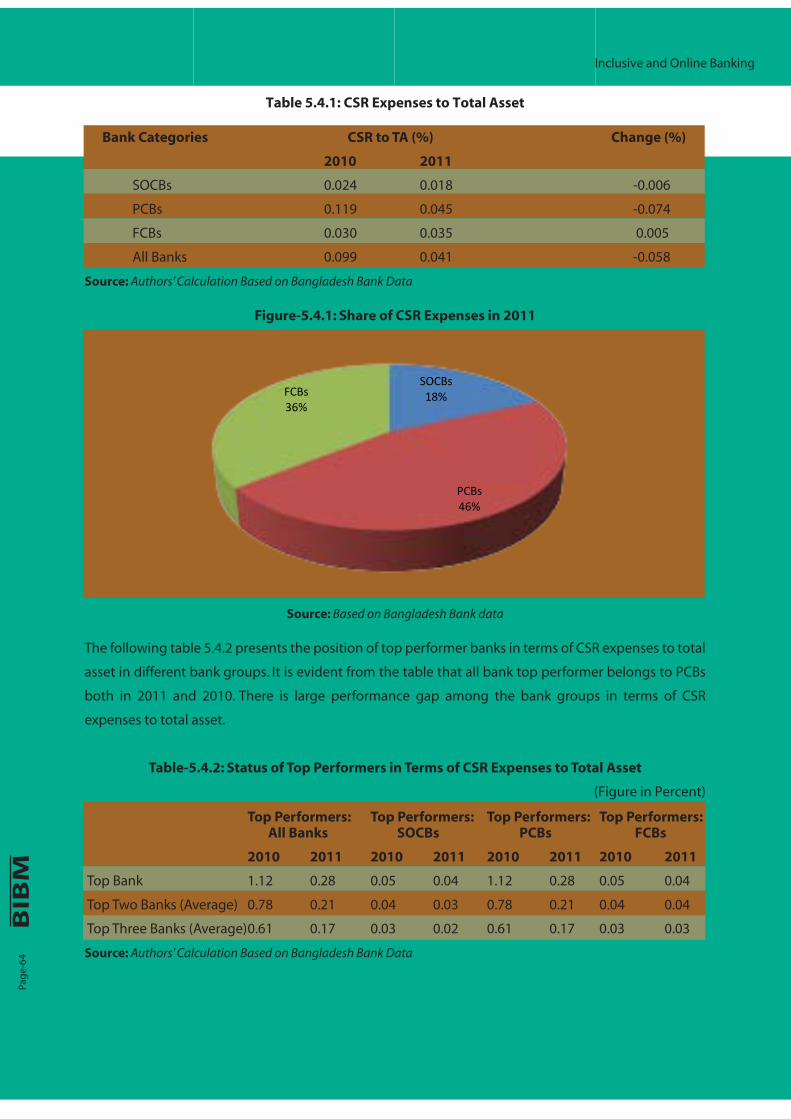

Chapter Three: Health Report of the Banking Sector of Bangladesh 25 Performance Evaluation Criteria 27Strength and Soundness 28Size and Growth (S&G) 35Profitability and Efficiency (P&E) 48Asset Quality 54Inclusive and Online Banking 59

Chapter Four: Observations and Concluding Remarks 67Observations and Concluding Remarks 69Appendix One: A Short Review of the Specialized Banks of Bangladesh 74

List of TablesTable-1.1.1: Change in Capital Adequacy Ratio in between CY 2010 and CY 2011 30Table-1.1.2: Status of Top Performers in Terms of Capital Adequacy Ratio 30Table-1.2.1: NPL Net of Provision to Total Equity Ratio of Banks [Average] 31Table-1.2.2: Status of Top Performers in Terms of NPL to Equity Ratio 31Table-1.3.1: Liquid Assets to Short Term Liabilities of Banks [Average] 32Table-1.3.2: Status of Top Performers in Terms of Liquid Asset to Short Term Liability 32Table-1.4.1: Borrowing liability to Total Liability of Banks [Average] 33Table-1.4.2: Status of Top Performers in Terms of Liquid Asset to Short Term Liability 33Table-1.5.1: Advance Deposit (AD) Ratio of Banks [Average] 34Table-1.5.2: Status of Top Performers in Terms of Advance Deposit Ratio 34Table-2.1.1: Number of Deposit Account of Banks 36Table-2.1.2: Overall Performance of Banks in Terms of Number of Deposit Account (Average) 37Table-2.1.3: Status of Top Performers in Terms of Number of Deposit Account (Average) 37Table-2.2.1: Number of Branch of Banks 38Table-2.2.2: Overall Performance of Banks in Terms of Number of Branch (Average) 39Table-2.2.3: Status of Top Performers in Terms of Number of Branch (Average) 39Table-2.3.1: Total Revenue of Banks 40Table-2.3.2: Overall Performance of Banks in Terms of Number of Branch [Average] 40Table-2.3.3: Status of Top Performers in Terms of Total Revenue 41Table-2.4.1: Total Assets of Banks 41Table-2.4.2: Overall Performance of Banks in Terms of Total Asset [Average] 42Table-2.4.3: Status of Top Performers in Terms of Total Asset 42Table-2.5.1: Average Deposit Growth of Banks (%) 43Table-2.5.2: Status of Top Performers in Terms of Total Deposit Growth 43Table-2.6.1: Average Loan and Advance Growth of Banks(%) 44Table-2.6.2: Status of Top Performers in Terms of Total Loan and Advance Growth 45Table-2.7.1: Average Net Interest Income Growth of Banks (%) 45Table-2.7.2: Status of Top Performers in Terms of Net Interest Income Growth 46Table-2.8.1: Average Net Interest Income Growth of Banks (%) 46

List of TablesTable-2.8.2: Status of Top Performers in Terms of Net Interest Income Growth 47Table-3.1.1: Overall Performance of Banks in Terms of Return on Asset [Average] 49Table-3.1.2: Status of Top Performers in Terms of Return on Asset 50Table-3.2.1: Overall Performance of Banks in Terms of Return on Equity [Average] 51Table-3.2.2: Status of Top Performers in Terms of Return on Equity 51Table-3.3.1: Total Expense to Total Revenue of Banks 51Table-3.3.2: Status of Top Performers in Terms of Total Expense to Total Revenue 52Table-3.4.1: Profit Per Employee of Banks 53Table-3.4.2: Status of Top Performers in Terms of Profit per Employee of Banks 53Table-4.1.1: Growth in Gross NPL of Banks 55Table-4.1.2: Status of Top Performers in Terms of Growth in Gross NPL 55Table-4.2.1: Gross NPL to Total Loans & Advances 56Table-4.2.2: Status of Top Performers in Terms of Gross NPL to Total Loans & Advance 56Table-4.3.1: Credit Concentration 57Table-4.3.2: Status of Top Performers in Terms of Credit Concentration 58Table-4.4.1: Division Wise Share of Total Advances 58Table 5.1.1: Rural Branch (RB) to Total Branch (RB) 60Table-5.1.2: Status of Top Performers in Terms of Credit Concentration 61Table-5.2.1: Micro & Small Credit (MSC) to Total Credit (TC) (%) 61Table-5.2.2: Status of Top Performers in Terms of Micro & Small Credit to Total Credit 62Table 5.3.1: Agricultural Credit (AgC) to Total Credit (TC) 62Table-5.3.2: Status of Top Performers in Terms of Agricultural Credit to Total Credit 63Table-5.4.1: CSR Expenses to Total Asset 64Table-5.4.2: Status of Top Performers in Terms of CSR Expenses to Total Asset 64Table-5.5.1: Number of ATM Booth 56Table-5.5.2: Status of Top Performers in Terms of Number of ATM Booth 66Table-5.6.1: Number of Any Branch Banking Branch to Total Branch 66Appendix Table 1.1: Status of Deposits, Loans, Branches and Employees for the Year 2010 76Appendix Table 1.2: Status of Deposits, Loans, Branches and Employees for the Year 2011 77Appendix Table 1.3: Selected Growth Indicators of Specialized Banks 77

List of GraphsFigure-1.1.1 Capital to Risk Weighted Assets Ratio of Banks [Average] 29Figure-2.1.1: Share of Deposit Account of Banks in 2011 36Figure-2.2.1: Share of Number of Branch of Banks in 2011 38Figure-2.3.1: Share of Total Revenue in 2011 40Figure-2.4.1: Share of Total Assets of Banks in 2011 41Figure-2.5.1: Average Deposit Growth of Banks 43Figure-2.6.1: Average Loan and Advance Growth of Banks 44Figure-2.7.1: Average Net Profit/Net Income of Banks 45Figure-2.8.1: Average Net Profit/Net Income Growth of Banks 47Figure-3.1.1: Average Return on Asset of Banks 49Figure-3.2.1: Average Return on Equity of Banks 50Figure-4.3.1: Credit Concentration of Banks 57Figure-5.1.1: Share of Rural Branch in 2011 60Figure-5.2.1: Share of Micro & Small Credit in 2011 61Figure-5.3.1: Share of Agricultural Credit in 2011 63Figure-5.4.1: Share of CSR Expenses in 2011 64Figure-5.5.1: Share of ATM Booth 65Appendix Figure-1.1: Market Share of Specialized Banks in Advances, Deposits, Assets and Branches 75Appendix Figure-1.2: Average Growth Rates of Selected Expansion Indicators of the Specialized Banks 75Appendix Figure-1.3: Average Growth Rates of Selected Performance Indicators of the Specialized Banks 76

VIII

ABBREVIATION

IX

AAIBL Al-Arafah Islami Bank Limited

ABBL AB Bank Limited

ABL Agrani Bank Limited

ACH Automated Clearing House

AD Advance Deposit

AD Authorised Dealer

ALS Assured Liquidity Support

AQ Asset Quality

ATM Automated Teller Machine

BAL Bank Asia Limited

BASIC BASIC Bank Limited

BB Bangladesh Bank

BCBL Bangladesh Commerce Bank Limited

BCBS Basel Committee on Banking Supervision

BDBL Bangladesh Development Bank Limited

BDT Bangladesh Taka

BIBM Bangladesh Institute of Bank Management

BKB Bangladesh Krishi Bank

BRAC BRAC Bank Limited

BRPD Banking Regulation & Policy Department

BSB Bangladesh Shilpa Bank

BSEC Bangladesh Securities & Exchange Commission

BSRS Bangladesh Shilpa Rin Sangstha

BTRC Bangladesh Telecommunication Regulatory Commission

CAR Capital Adequacy Ratio

CBC Commercial Bank of Ceylon PLC

CDCS Certified Documentary Credit Specialist

CEO Chief Executive Officer

CIB Credit Information Bureau

Citi Citibank, N.A.

City The City Bank Limited

CL Classified Loan

CPD Centre for Policy Dialogue

CRM Credit Risk Management

CSR Corporate Social Responsibility

CY Calendar Year

DA Documents against Acceptance

DBBL Dutch-Bangla Bank Limited

DBL Dhaka Bank Limited

DOE Department of Environment

DOS Department of Off-site Supervision

DP Documents against Payment

ABBREVIATION

X

DSE Dhaka Stock Exchange

EBL Eastern Bank Limited

ECC Export Cash Credit

EDF Export Development Fund

EFT Electronic Fund Transfer

EIA Environmental Impact Assessment

EPZ Export Processing Zone

ERQ Exporters Retention Quota

ETP Effluent Treatment Plant

EXIM Export Import Bank of Bangladesh Limited

FCB Foreign Commercial Bank

FDBP Foreign Documentary Bills Purchased

FE Foreign Exchange

FSIBL First Security Islami Bank Limited

FY Fiscal Year

GDP Gross Domestic Product

GRI Global Reporting Initiative

HBL Habib Bank Limited

HHK Hybrid Hoffman Kiln

HRM Human Resource Management

HSBC The Hongkong and Shanghai Banking Corporation Limited

IBBL Islami Bank Bangladesh Limited

ICC Internal Control and Compliance

ICT Information and Communication Technology

IDRA Insurance Development and Regulatory Authority

IFIC IFIC Bank Limited

IPO Initial Public Offer

I & O Inclusive & Online Banking

JBL Janata Bank Limited

KSA Kingdom of Saudi Arabia

LC Letter of Credit

LIM Loan against Imported Merchandise

LTR Loan against Trust Receipt

MFI Micro Finance Institution

MICR Magnetic Ink Character Recognition

MTBL Mutual Trust Bank Limited

MTO Money Transfer Organization

MOF Ministry of Finance

MRA Micro-credit Regulatory Authority

NBL National Bank Limited

NBFI Non-bank Financial Institutions

NCCBL National Credit and Commerce Bank Limited

ABBREVIATION

XI

NPL Non Performing Loan

NRB Non-Resident Bangladeshi

ONE ONE Bank Limited

PBL Pubali Bank Limited

PC Packing Credit

PCB Private Commercial Bank

PD Primary Dealer

PEC Performance Evaluation Criteria

POST Point of Sale Terminal

PSTN Public Switched Telecommunication Network

P & E Profitability & Efficiency

RAKUB Rajshahi Krishi Unnayan Bank

RBL Rupali Bank Limited

RMU Risk Management Unit

ROA Return on Asset

ROE Return on Equity

SBL Sonali Bank Limited

SBI State Bank of India

SCB Standard Chartered Bank

SEBL Southeast Bank Limited

SEC Securities and Exchange Commission

SIBL Social Islami Bank Limited

SJIBL Shahjalal Islami Bank Limited

StBL Standard Bank Limited

SME Small & Medium Enterprise

SOCB State-owned Commercial Bank

SOD Secured Overdraft

SPCB Specialized Bank

SWIFT Society for Worldwide Interbank Financial Telecommunication

S & G Size & Growth

S & S Strength & Soundness

ST Short Term

TMSS Thengamara Samabay Samity

TT Telegraphic Transfer

UBL Uttara Bank Limited

UCBL United Commercial Bank Limited

UCP Uniform Customs and Practice

UCPDC Uniform Customs and Practice for Documentary Credits

URC Uniform Rules for Collection

URR Uniform Rules for Bank-to-Bank Reimbursements

URDG Uniform Rules For Demand Guarantees

Chapter One

Background & Methodology

Pag

e-03

Banks are the most significant of the financial intermediaries that play very useful roles in the

economic life of every modern state. In Bangladesh, banking sector is the core component of the

financial system engaged mainly in mobilizing funds and offering lending services. Banks lend to

businesses, consumers, and governments and thus contribute to production, innovation,

infrastructure development, job creation and overall prosperity. It is well recognised that sustainable

performance of banking sector and real sector development go hand in hand. To ensure sustainable

operation, banks are expected to contribute to both economic and social development of the country.

The financial system of Bangladesh mainly comprises of banks, NBFIs, MFIs and their regulatory

bodies. Most of the institutions in the financial sector are characterized by a mix of public and private

ownership. Of these broad sub-sectors, banks are dominant that hold significant market share of the

financial sector of Bangladesh. While the Bangladesh Bank has regulatory and supervisory jurisdiction

over the entire banking subsector as well as the NBFIs (excluding insurance companies), the

Bangladesh Securities and Exchange Commission (BSEC) exercises similar functions for the stock

exchanges and the merchant banks. Insurance companies and MFIs are regulated by IDRA and MRA

respectively.

The growth and evolution of the banking system of Bangladesh can be viewed in different broad

phases. Banking sector of Bangladesh performed poorly following independence, offering a narrow

range of products and inefficient delivery of financial instruments, and was largely non-competitive in

structure. To rectify weaknesses of the banking sector and to take forward the development, reforms

commenced in the early 1980s. The period from independence to the early 1980s was marked by the

expansion of bank branches by the government controlled banks. The period from early 1980s to early

1990s was the period of privatization of banks that allowed new banks in the private sector to

augment competition in the banking sector. The period from early 1990s is the period of financial

reforms and consolidation. Improving performances of the banking sector received priority mainly

since 1990 when government launched financial sector reform programs. The program pursued a

series of legal, policy, and institutional reforms to improve the process of financial intermediation to

ensure more efficient allocation of financial resources and to improve the competitiveness of the

private sector. Over the years, performance of the banking industry has improved by increasing their

scope of activities, improving service quality, engaging technology, and introducing social

connectivity through CSR practices. The changes have brought greater competition in the industry;

and the intensive and continuously increasing competition in the banking sector has created a need

for access to information for evaluating commercial banks operating in this market.

Background of the Report

Pag

e-04

Background & Methodology

Remarkable changes have taken place in the banking sector of Bangladesh in terms of size, market

structure, activities and performances over the years. The reforms injected more players in the

banking sector, with most banks increasing the range and diversity of their products and services.

Nevertheless, a few government controlled big banks still dominate the sector. In regard to the

change in governance, the enactment of the new banking laws and prudential regulations brought

discipline in the banking sector. As a whole, changes have taken place in terms of efficiency,

soundness, complexities and challenges. To cope with the growing changes and decision making,

reliable information is crucial.

In Bangladesh, different published sources1 capture comparative information on the performances of

broad groups of banks (SOCB, PCB, FCB, SPCB). This report is another effort to compare the different

broad groups of banks following different methodology. The main aim of the independent review is

to highlight performance and development in the banking sector and thus to contribut to the

country’s reliable business and economic information. In the report, a comparison of bank groups

would help identifying status of different bank groups as per selected performance indicators.

It would also have a comparison of the performances of the banking sector for the year 2010 and

2011. It is expected that this kind of publication would complement the existing disclosure system in

the banking sector of the country. This report might also help internal control team of a bank in

preparing annual report on the health of the bank that is required to be submitted to the MD and the

Audit Committee of the Board for onward submission to the Board of Directors – as suggested by the

Bangladesh Bank2.

1 Ministry of Finance, Bangladesh Bank etc.

2 In the guideline ‘Managing Core Risk in Banking: Internal Control and Compliance’ Bangladesh bank suggested a reporting structure for the internal control team of a bank according to which the

team would prepare an annual report on the health of the bank to be submitted to the MD and the Audit Committee of the Board for onward submission to the Board of Drectors.

Pag

e-05

Background & Methodology

Performance of 36 Banks are Evaluated

A total of 36 banks are considered for performance evaluation in this study. Banks with less than 1 per

cent market share (total volume of assets of a bank expressed as a percentage of total volume of

assets of the banking industry) are excluded3. For some of these banks, data were also not available.

Four specialized banks (BKB, RAKUB, BASIC and BDBL) have been excluded considering their different

nature of operations or non-availability of required/comparable data. Morever, reporting time line of

BKB and RAKUB is different from that of the other banks; and required consolidated data on BDBL

(formed by merging BSRS and BSB) are not available.

Bangladesh Bank and Annual Reports are Main Sources of Data

Annual Reports of the selected banks were collected to gather relevant information. Morever, data

from different departments of Bangladesh Bank like Banking Regulation and Policy Department

(BRPD), Department of Off-site Supervision (DOS), Statistics Department have been collected.

Published information sources of MOF are also used. A number of individual banks were contacted for

data validation.

Performances of the CY 2011 are considered

The data of mainly for the calender year 2011 of the selected banks are considered to evaluate the

performances of banks. A comparison has also been made between CY 2010 and CY 2011. Write-up on

‘Governance, Activities and Operation’ covers some additional recent information.

Bank groups are evaluated on Five Broad Performance Evaluation Criteria

Five broad Performance Evaluation Criteria (PEC) have been set up to evaluate banks’ performance:

Strength and Soundness; Size and Growth; Profitability and Efficiency; Asset Quality; and Inclusive and

Online Banking. Each broad criterion is allocated 20 percent weight and a few logically selected ratios

(indicators) have been complied . Five broad PECs are discussed along with their selected indicators as

follows.

3 Bank Alfalah, BCBL, Habib Bank, ICB Islamic Bank, National Bank of Pakistan, State Bank of India, Woori Bank.

Methodology of the Report

Pag

e-06

Background & Methodology

PEC 1: Strength and Soundness

The strength and soundness of a bank reflects the ability of a bank to absorb different shocks and

survive in an economic downturn. A financially sound bank can more easily achieve the confidence of

the customers than others. Financial Soundness and strength indicators are calculated and

disseminated to be used in macro prudential analysis, which comprises of assessment and control

over strengths and vulnerabilities of financial systems with a view to increasing financial soundness as

well as reducing probability of financial system bankruptcy. Five indicators have been used for

assessing the strength and soundness of banks:

PEC 1- Indicator 1: Capital Adequacy Ratio: Capital Adequacy Ratio (CAR) is a ratio of banks

Capital to Risk Weighted Assets. It is a ratio that regulators in the banking system use to watch bank's

health, specifically bank's capital to its risk. Higher ratio indicates better performance. The indicator is

computed as:

Capital to Risk Weighted Assets = [Total Eligible Capital ÷ Risk Weighted Assets] ×100

PEC 1- Indicator 2: NPL to Equity Ratio: Higher NPL is a recognized indicator of lack of

strength and soundness. The complete title of the ratio should be NPL net of provisions to total equity.

Like CAR, the ratio indicates a bank’s capacity to absorb credit risk. Lower ratio indicates better

performance. The indicator is computed as:

NPL to Equity Ratio = [(Classified Loan – Provision against Classified Loan) ÷Total Equity] ×100

PEC 1- Indicator 3: Liquid Assets to Short term Liabilities: To banks, liquidity is the

ability to meet obligations when they become due without incurring unacceptable losses. Here the

Liquid Assets are the sum of Cash, Balance with other banks and Financial Institutions, Money at call

and Short Notice and Investment. Short-term Liabilities are the sum of Borrowed Liabilities and Total

Deposits less Fixed Deposits. The ratio measures a bank’s ability to meet its short-term obligations

with its most liquid assets. Higher the ratio, better the performance. The indicator is computed as:

Liquid Assets to ST Liabilities = [Liquid Asset ÷ Short Term Liabilities] ×100

PEC 1- Indicator 4: Borrowing liability to Total Liability: Banks should mainly rely on

deposit liabilities as a source of fund to create their assets. Higher borrowing liabilities indicate greater

dependency on money market and lack of strength and soundness required to attract adequate

deposits. The indicator shows the proportion of borrowing liability of the total liabilities of a bank.

Lower ratio indicates better performance. The indicator is computed as:

Borrowing Liability to Total Liability = [Borrowed Liability ÷Total Liability] × 100

PEC 1- Indicator 5: Advance Deposit Ratio: Banks should maintain a balance between the

volume of advances and deposit. Advance deposit ratio is used to measure the degree of balance

between advance and deposit. High value of this ratio may increase bank income but may increase

liquidity risk and vice-versa.

Advance Deposit Ratio = [Total Advances ÷ Total Deposit] ×100

Pag

e-07

Background & Methodology

PEC 2: Size and Growth

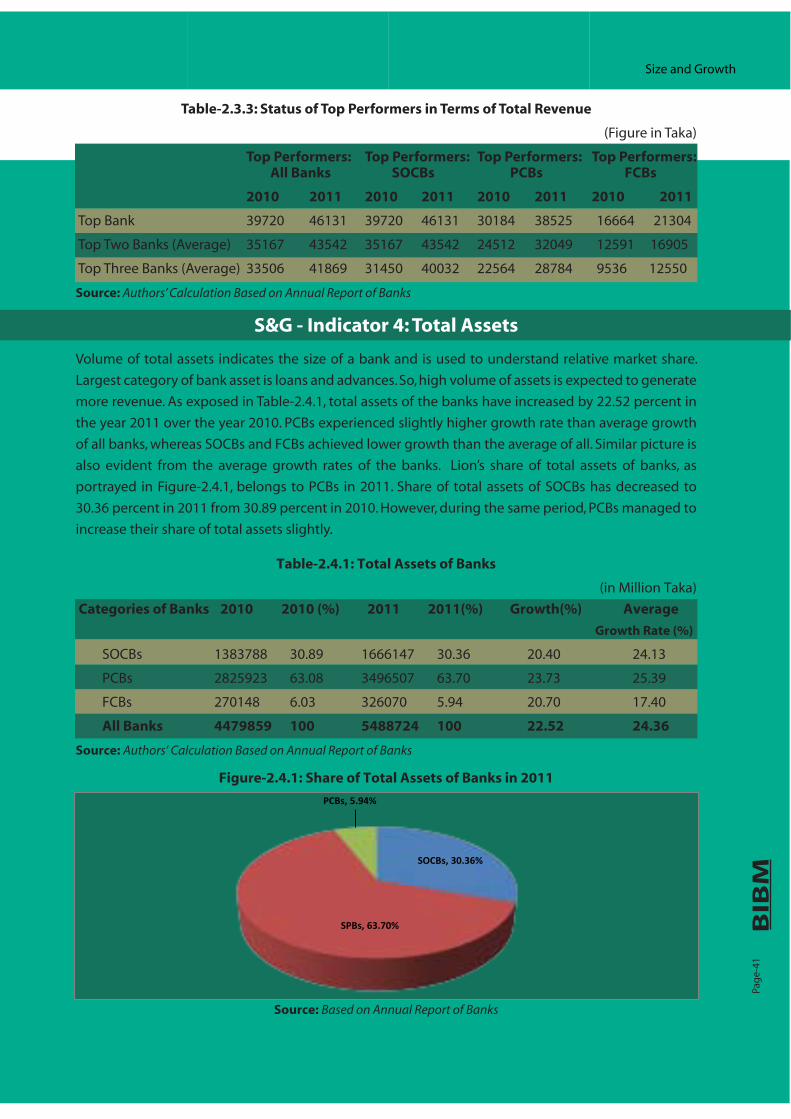

Bank size affects profits of banks and ensures greater financial access. Relatively big banks have

greater opportunity to minimize risks and may enjoy economies of scale. Growth is recognized as one

of the prime indicators of the performance of any institution. Under this head, four indicators related

to size and four indicators related to growth are considered to assess the performances of banks.

PEC 2 - Indicator 1: Number of Deposit Account: Higher number of deposit account

indicates greater market share and bigger size of the bank. Absolute number of deposit accounts has

been used to assess the banks in terms of size. Larger the number of deposit accounts, better the

performance.

PEC 2 - Indicator 2: Number of Branch: Higher number of branches indicates greater market

share and bigger size of the bank. Absolute number of branches has been used to assess the banks in

terms of size. Larger the number of branches, better the performance.

PEC 2 - Indicator 3: Total Revenue: Higher volume of total revenue indicates greater volume

of activities and bigger size. Absolute volume of total revenue has been used to evaluate the banks in

terms of size. Higher the volume of total revenue, better the performance.

PEC 2 - Indicator 4: Total Asset: Higher volume of total assets indicates greater market share.

Absolute volume of total assets has been used to assess the banks in terms of size. Higher the volume

of total assets, better the performance.

PEC 2 - Indicator 5: Total Deposit Growth: Deposit growth indicates increase in sources of

funds by banks. Higher the growth rate of deposits, better the performance. The indicator is

computed as:

Deposit Growth = [(Current Year Deposit – Previous Year Deposit) ÷ Previous Year Deposit] ×100

PEC 2 - Indicator 6: Total Advance growth: Advance growth indicates increase in uses of

funds by banks. Higher the growth rate of advances, better the performance. The indicator is

computed as:

Advance Growth = [(Current Year Advance–Previous Year Advance)÷Previous Year Advance] ×100

PEC 2 - Indicator 7: Net Profit Growth: Growth in Net Profit is the most crucial indicator to

evaluate growth performance of any commercial institution. Higher the growth rate of net profits,

better the performance. The indicator is computed as:

Profit Growth = [(Current Year Profit – Previous Year Profit) ÷ Previous Year Profit] ×100

PEC 2 - Indicator 8: Net Interest Income Growth: Net Interest Income is generally the major

income of banks. Higher the growth rate of net interest income, better the performance. The indicator

is computed as:

Net Interest Income Growth = [(Current Year NII – Previous Year NII) ÷ Previous Year NII] ×100

Background & Methodology

PEC 3: Profitability and Efficiency

Profitability and Efficiency analyses are essential for the evaluation of performances of any

commercially run organization. Profitability is a concept associate with the objective of assessing a

bank's results from efficiency point of view for entire activities. It represents the modality to achieve

the major goal of bank's activity. The profitability and efficiency analyses are based on the following

four indicators to rank the banking performances.

PEC 3 - Indicator 1: Return on Assets (ROA): This indicator is also known as profit to assets

and measures the management capacity to use the financial and real resources of a bank in order to

generate profit. Higher the ratio, better the performance. The indicator is computed as:

Return on Assets: (Net Income after Tax ÷ Total Assets) × 100

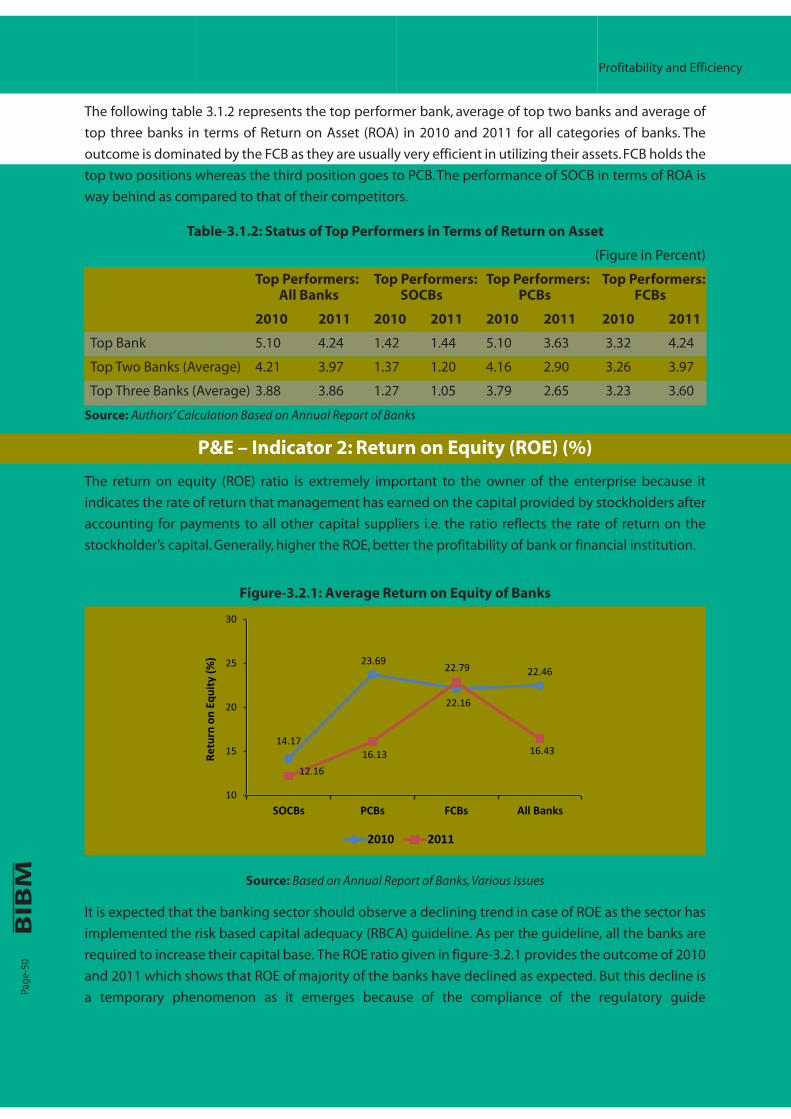

PEC 3 - Indicator 2: Return on Equity (ROE): Return on Equity or profit to equity is a

recognized indicator of profitability which is used to measure the management efficiency in all its

dimensions. Higher the ratio, better the performance. The indicator is computed as:

Return on Equity: [Net Income after Tax ÷ Total Equity] × 100

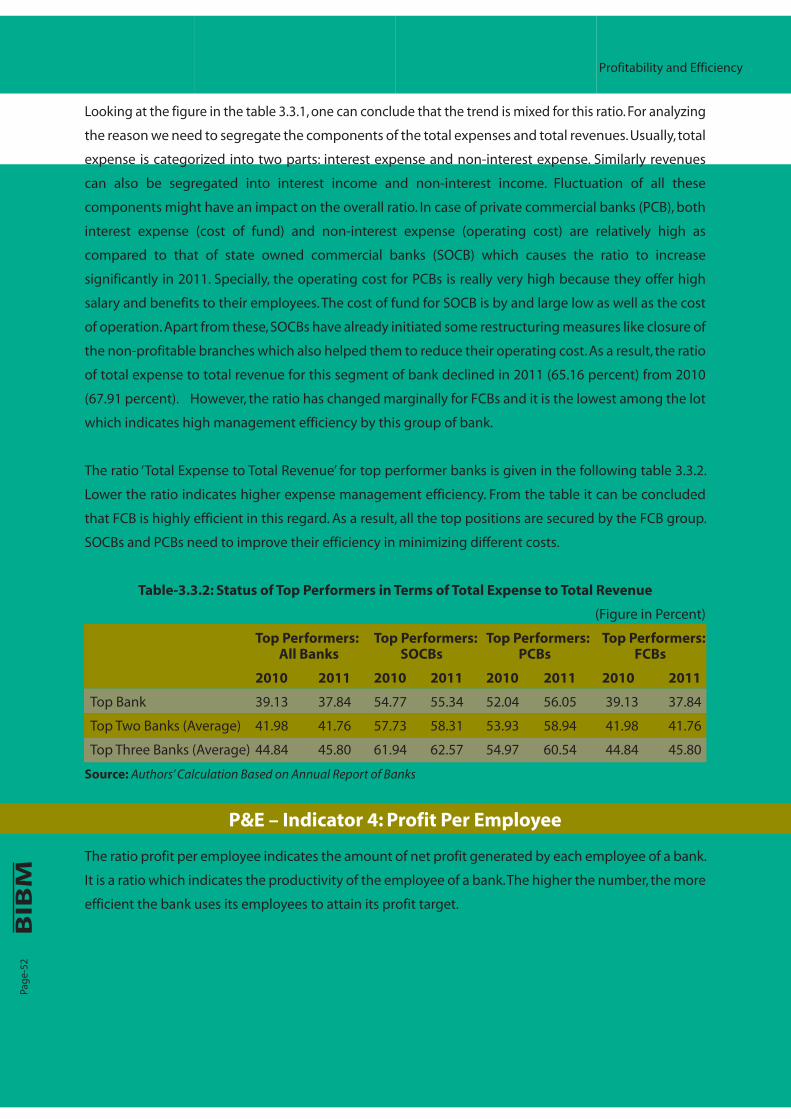

PEC 3 - Indicator 3: Total Expense to Total Revenue: A measure of the total expenses

associated with earning of revenue by banks. It indicates efficient use of scarce resources by banks to

attain their goals. Lower the ratio, better the performance. The indicator is computed as:

Total Expense to Total Revenue = [Total Expenses ÷ Total Revenue] × 100

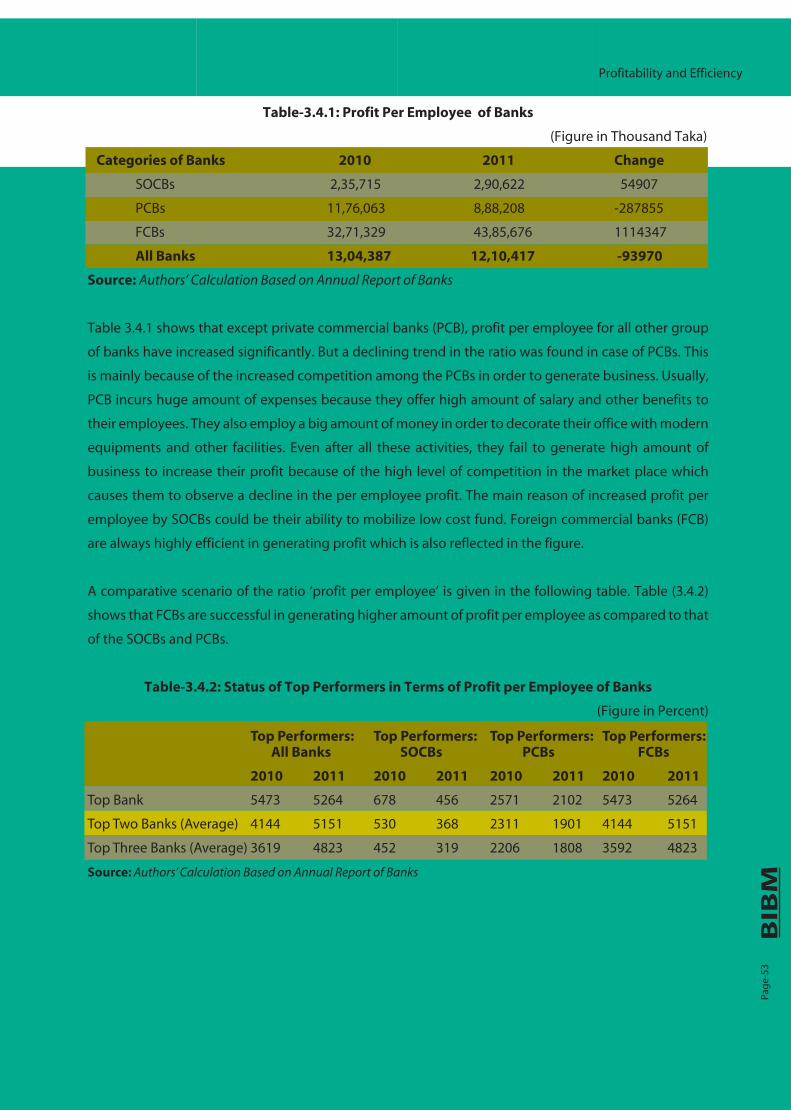

PEC 3 - Indicator 4: Profit per Employee: It is a ratio which indicates the productivity of the

employee of a bank. The higher the number, the more efficient the bank uses its employees to attain

its goal. Higher the ratio, better the performance. The indicator is computed as:

Profit per Employee = [Net Income after Tax ÷ Total Employees]

Pag

e-08

PEC 4: Asset Quality

Assets are the sources of earning for any organization. If the quality of assets deteriorates, it adversely

affects the earning potentials which eventually reduce the value of the firm. The largest category of

earning assets of a bank is loans and advances. So the consideration of the quality of loans is necessary

while performing the ranking. In evaluating asset quality, evaluators look at the existing and potential

loss exposure, primarily in the loan portfolio. Under this head, four indicators related to asset qualities

are considered to rank performances of banks.

PEC 4 - Indicator 1: Growth in Gross NPL: Growth in gross NPL indicates the change in the

performance of a bank in terms of asset quality. Lower the growth rate of Gross NPL, better the

performance. The indicator is computed as:

Gross NPL Growth = [(Current Year CL – Previous Year CL) ÷ Previous Year CL] ×100

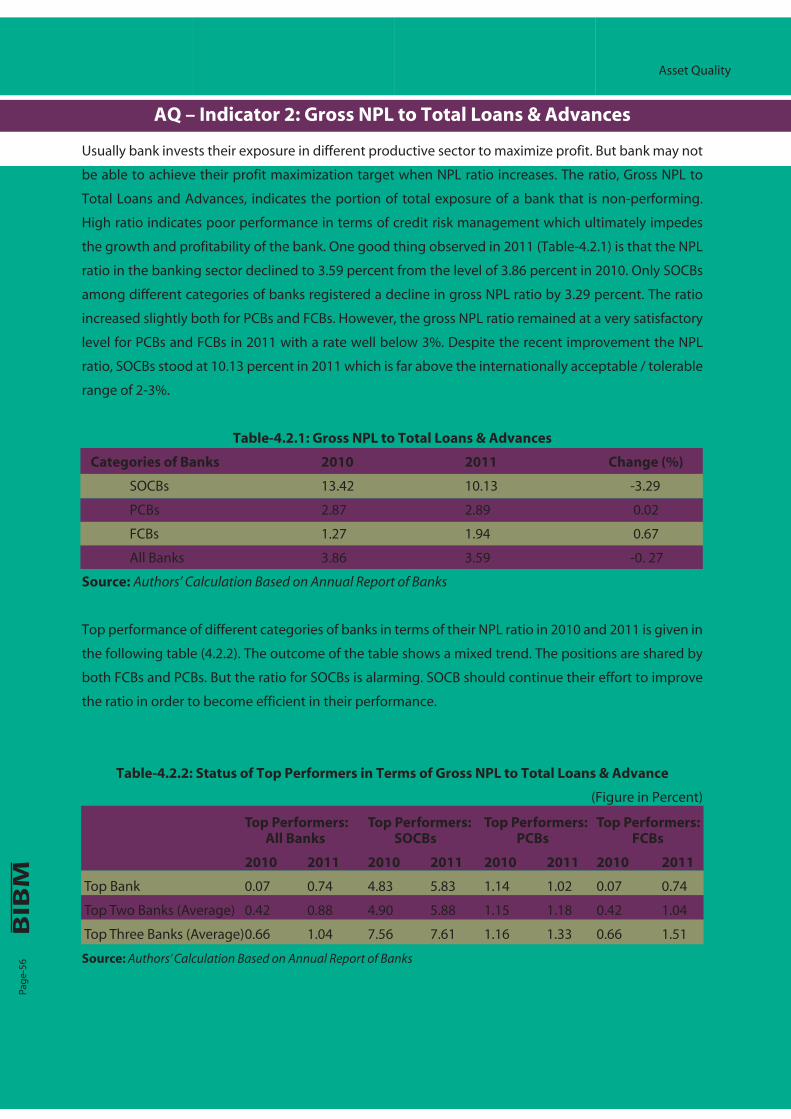

PEC 4 - Indicator 2: Gross NPL to Total Advances: The ratio, Gross NPL to Total Loans and Advances,

indicates the portion of total advances that are non-performing. Lower the Gross NPL to Total

Advances, better the performance. The indicator is computed as:

Gross NPL to Total Advances = [Classified Loan ÷ Total Loan and Advances] ×100

PEC 4 - Indicator 3: Credit Concentration by Loan Size: Credit concentration has been measured in

terms of large loans. A loan has been considered as large loan if the outstanding loan amount is more

than 10% of its capital. Lower the Large Loan to Total Loans and Advances, better the performance.

The indicator is computed as:

Credit Concentration = [Total Large Loan ÷ Total Loan and Advances] ×100

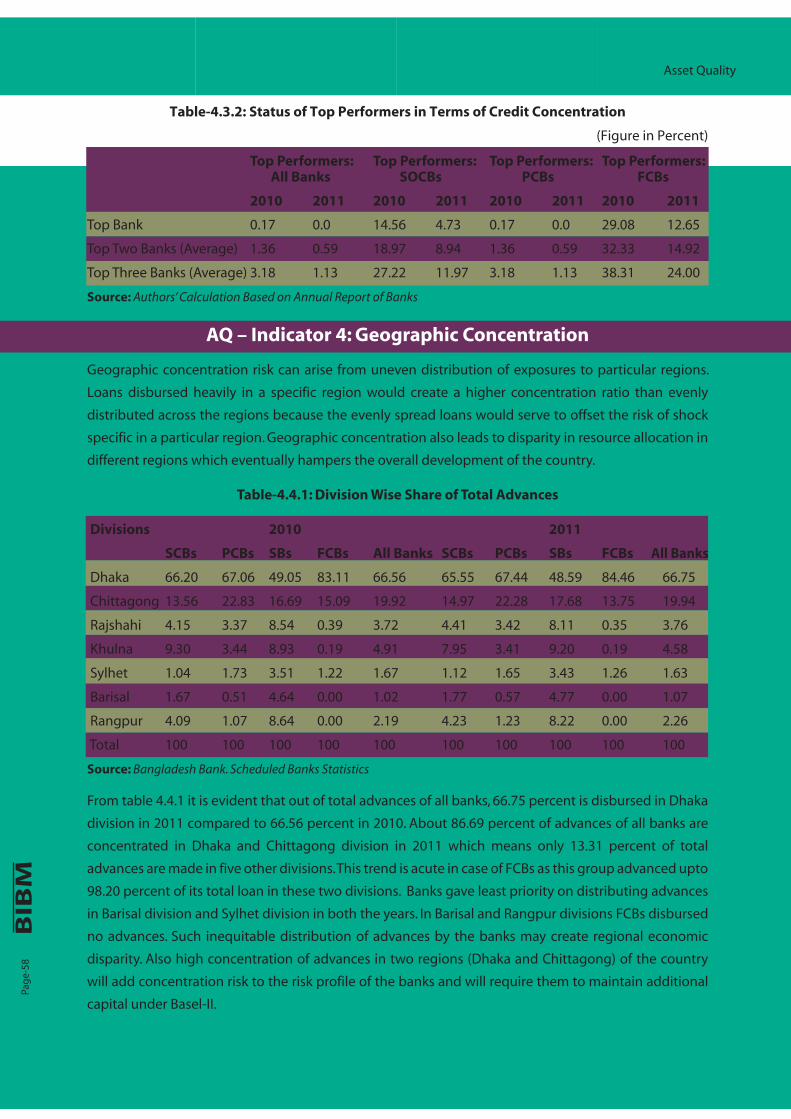

PEC 4 - Indicator 4: Credit Concentration by Division: A good credit portfolio is one that is well

diversified in terms of allocation of advances or credit. High credit concentration increases credit

portfolio risk and vice versa. High concentration of bank advances to a particular division or region

may endanger a bank if that division or region is affected by natural calamity or other external event.

Credit Concentration = [Total Loans to a Division ÷ Total Loan and advances] ×100Pa

ge-

09

Background & Methodology

PEC-5: Inclusive and Online Banking

Inclusive banking is concerned with sustainable or ethical banking and is part of a larger societal

movement toward more social responsibility. This movement should include ethical investment and

distribution of resources and corporate social responsibility. In Bangladesh, inclusive operation of

banks should be connected with the distribution of banks resources to rural economy, the agricultural

sector, and micro and small enterprise sector. Online banking operation is another sustainable way of

offering quality banking services. It is said that online banking is the starting point of green or

environmental banking. Under this head, six indicators related to inclusive and online banking are

considered to rank performances of banks.

PEC 5 - Indicator 1: Rural Bank Branch to Total Branch: Higher number of Rural Bank Branch

indicates greater access to finance by the under privileged people. However, small banks have

limitation of setting up greater number of bank branches. Therefore, performance based on absolute

number of bank branches would be biased towards big banks. Thus two indicators have been used:

ranks based on absolute number of branches (higher the number of branches, better the

performance) and ranks based on the ratio of Rural Branch to Total Branch (higher the ratio, better the

performance).

PEC 5 - Indicator 2: Micro and Small Credit to Total Loans: Higher volume of Micro and Small Credit

to Total Credit indicates greater access to finance by the under served enterprises of Bangladesh.

Larger the volume of Micro and Small Credit to Total Loans and Advances, better the performance.

Micro and Small Credit to Total Loans = [Micro and small credit ÷ Total Loan and advances] ×100

PEC 5 - Indicator 3: Agricultural Credit to Total Loans: Higher volume of Agricultural Credit to Total

Loans and Advances indicates greater access to finance by the under privileged farmers or small rural

investors of Bangladesh. Larger the volume of Agricultural Credit to Total Loans, better the

performance.

Agricultural Credit to Total Loans = [Agricultural Credit ÷ Total Loan and advances] ×100

PEC 5 - Indicator 4: CSR Expense to Total Asset: Higher volume of CSR Expenditure to Total Assets

indicates greater contribution of a bank to community development and environmental activities.

Larger the ratio, better the performance.

PEC 5 - Indicator 5: Number of ATM Booth: Greater number of ATM booths indicates greater and

easier access of banking activities by the clients. Larger the number of ATM booth, better the

performance.

PEC 5 - Indicator 6: Number of Any Branch Bank to Total Bank: Greater number of branches under

Any Branch Banking indicates better status and networking of banks. Larger the number of branches

under Any Branch Banking, better the performance.

Pag

e-10

Background & Methodology

Limitations of the Report

The report is based on 36 banks. A few commercial banks and specialized banks have been excluded

from the study mainly because of non-availability of required data or different nature of operations.

Selection of right indicators could always be a matter of debate. For assessing the performances of

banks, a total number of 30 indicators have been identified under five broad Performance Evaluation

Indicators (PECs). This is not an exhaustive list.

Organization of the Report

The report is organized into four chapters. Chapter 1 discusses background and methodological

issues. Chapter 2 discusses the governance, activities, and operations of banks. Health of the banking

sector is examined based on some indicators in chapter 3. Chapter 4 summarizes the observations of

the report and offers concluding remarks. A general assessment of the specialized banks of the

country is attached as appendix to the report.

Pag

e-11

Background & Methodology

Chapter Two

Governance, Activities and Operations of Banks

Governance, Activities and Operations of Banks

Pag

e-15

The banking sector of Bangladesh comprises of 4 state-owned commercial banks (SOCBs)4,

4 specialized banks (SPB)5, 30 domestic private commercial banks (PCBs)6, and 9 foreign commercial

banks (FCBs)7. The FCBs are operating in Bangladesh as the branches of the banks which are in

operation abroad. PCBs can be categorized into conventional PCBs (28 conventional PCBs) that

perform the banking functions in conventional fashion i.e interest based operations; and Islamic

Shariah based PCBs (7 Islamic Shariah based PCBs) that execute banking activities according to Islamic

Shariah based principles. Other than these, there are nine newly licensed banks8. Of these, three have

already started operations and others are preparing to launch their operations. Other than these

scheduled banks9, there are 4 non-scheduled10 banks in the country. Over the years, the competitive

structure of the banks has changed; however, the operational and competitive environment of all

categories of banks is not the same. Full commercially motivated operational environment is mainly

enjoyed by the PCBs and FCBs. Government directed expansion of credit and some other relevant

services are performed by SOCBs and specialized banks of the country. In recent time though the

government has corporatized SOCBs and made them more autonomous to operate under better

commercial environment, no visible impact is observed.

As the regulatory and supervisory authority of the banking sector in Bangladesh, Bangladesh Bank

discharges its responsibility through a regulatory and supervisory framework. In regard to governance

framework, the ‘Prudential Regulations for Banks’11 published by the Bangladesh Bank is

a comprehensive and crucial document. It covers policies, rules, guidelines and requirements of the

governance of banks like capital adequacy, loan classification, core risk management; responsibilities

of chief executive officers, board of directors; disclosure requirements etc. In connection with

regulatory and supervisory changes, some recent initiatives of the Bangladesh Bank are remarkable.

Bangladesh Bank adopted financial sector regulatory and supervisory frameworks with sharper risk

and systemic stability focus in line with post-global crisis revisions of international best practice

standards. The more stringent loan classification norms formulated by the Bangladesh Bank are being

implemented in the country. Currently the central bank is implementing Basel II capital regime, and

preparations are on for phasing in Basel III capital and liquidity standards. Bangladesh Bank sharpened

its supervisory vigilance for improving corporate governance, risk management and disclosure

4 SBL, JBL, ABL, RBL

5 BASIC, BDBL, BKB, RAKUB

6 AAIBL, ABBL, BAL, BCBL, BRAC, City, DBBL, Dhaka, EBL, EXIM, FSIBL, IBBL, ICB Islamic Bank, IFIC, Jamuna, Mercantile, MTBL, NBL, NCCBL, ONE, PBL, Premier, Prime, SEBL, SIBL, SJIBL, StBL, Trust, UBL, UCBL.

7 Bank Alfalah, CBC, Citi, HBL, HSBC, National Bank of Pakistan, SBI, SCB, Woori Bank.

8 In April, 2012 Bangladesh Bank approved licensing of nine new commercial banks (three with NRB and six with indigenous sponsors).

9 The banks which get license to operate under Bank Company Act.

10 Ansar VDP Unnayan Bank, Karmashangosthan Bank, Probashi Kollyan Bank and Jubilee Bank that are established for special and definite objective and operate under the acts that are enacted

for meeting up those objectives, are termed as Non-Scheduled Banks. These banks cannot perform all functions of scheduled banks.11

Last published (updated version till September 2011).

Pag

e-16

Governance, Activities and Operations of Banks

practices in the financial sector. Bangladesh Bank started publishing Financial Stability Reports since

2011 to identify the risks that could affect individual bank, financial sector, and/or the economy.

Scheduled banks were instructed to establish a separate Risk Management Unit to develop risk

management capacity among them to manage the risks that can cause systemic threats and

jeopardize the stability of the entire financial system. Periodical stress testing has also been made

mandatory to bring out vulnerabilities of banks and financial institutions. Initiatives are also

undertaken to upgrade BB’s regulatory and supervisory capabilities continually to meet the emerging

new challenges. In addition to enacting and amending various prudential measures with the existing

acts, Bangladesh Bank examines the activities of the banks on a continuous basis with the ultimate

objective of establishing and maintaining a high level of professionalism in the banking sector.

The supervision by Bangladesh bank takes two forms- off site and on site. While off-site supervision is

carried through the report and statements submitted by the banks- on site goes the other way i.e.

examining or assessing the financial condition and compliance with the laid down rules and

regulations through directly visiting and observing the operations of the banks. These two

approaches are complementary to each other and if properly synchronized reduces the possibility of

large scale banking irregularities. To support the strengthening of prudential controls and increase

the effectiveness of supervision, BB adopted a new organizational structure in May 2012 aimed at

consolidating management of on-site and off-site supervision activities. In Bangladesh, Bangladesh

Bank is the true supervisor of the private sector and foreign banks only. Traditionally, Bangladesh

Bank does not have enough supervisory grips over the state owned commercial banks. That is a grey

area in our system and one of the major obstacles to ensure the proper functioning of the state

owned banks. The recently finalized draft of 'The Bank Company (Amendment) Act, 2013', with a view

to strengthening the country's banking system is a notable initiative. The amendment of the act is

aimed at bringing about 'discipline' in the management of banks. The previous act did not mention

the number of board of directors and the new version mentioned the number of bank directors not to

exceed 20. And out of them four directors will be independent. The tenure of the directors will be for

three years and none of them can be director for two consecutive terms. As per the new version, the

CEO can be removed by the Bangladesh Bank. The amendment is expected to bring positive changes

in improving regulatory and governance environment of banks.

Collection of deposits and offering credit are the core activities of banks. With the passage of time,

banks are facing growing competition in mobilising their expected volume of deposits and thus

effective marketing of deposit products is receiving increasing importance in banks as part of their

operational strategies. As of end February 2012, the total volume of deposits of all banks was close to

Pag

e-17

Governance, Activities and Operations of Banks

BDT 4500 billion of which 80 percent were time deposits (MOF, 2012)12 . Private sector is the prime

source of deposits and rural economy contributes around 13 percent of total deposits. Credit is the

main asset component of banks. According to a recent BIBM Review study (2012)13 , credit and

investment assets of scheduled banks amounted to a minuscule Taka 7.07 billion in December 1972

which stood 654 fold higher at over BDT4625 billion as of December 2011. And the total volume of

domestic credit of the country stood at around BDT 5548 billion as of February 2013 . According to BB

(2013)14 data on a year-on-year basis, the domestic credit recorded 13.37 percent growth at the end of

February 2013 of which 13.96 percent growth was in the private sector and 11.33 percent in the

private sector.

After running through a number of reform programs related to credit operation of banks, the banking

activities have reached a stage of reliability. Banks have been given almost full freedom for their own

credit operation. Selection of borrowers and appraisal of projects/economic activities are crucial

components of the credit operations of banks. In this connection, CRM is used by the banks for

handling credit risks in their lending operations. In addition, availability of different tools like online

Credit Information Bureau (CIB), legal support both for credit operation and loan recovery,

accessibility to tailored software and, most importantly, injection of a pool of talented bankers in the

banking sector truly upgraded the credit operation of commercial banks. Availability of these do not

only help a bank in the process of creating good quality loans but also help to maintain the quality of

the loans through proper monitoring, close supervision and frequent follow up. One indicator may be

the status of classified loan that came down to around 7 percent (of total outstanding loans) in June

2012 as compared to 27 percent in 1990. It is to be mentioned here that the improvement may even

be considered greater as over the years the loan-classification norms have been made more and more

stringent. The increase in the classified loans of the banking sector in 2013 is attributed mainly to the

implementation of the new classification norms (implemented from end December 2012) of the

central bank. Increase in risk taking activities is also evident in some instances. Different types of credit

concentration (such as urban concentration, trade concentration, etc.) are evident from the BIBM

review study (2012). Such inequitable distribution of advance by banks are not only creating

12 MOF (2012) Activities of Banks, Non-Bank Financial Instituations and Insurance Companies 2012, Ministry of Finance Government of Bangladesh.

13 BIBM (2012) Banking Review Series- an annual publication of BIBM, Dhaka, Bangladesh.

14 BB (2013) Bangaladesh Bank Quarterly, Vol-X, No-3, Bangladesh Bank.

Pag

e-18

Governance, Activities and Operations of Banks

economic disparity, but also adding credit concentration risk to the risk profile of the banks, requiring

additional capital under Basel-II. Slow recovery has been observed in the real estate, RMG and

commodity sector since mid 2011, compelling the entrepreneurs to reschedule their repayment. In

many instances, there are evidences of the compromise of loan quality in an atmosphere of ambitious

profit and intense competition. Moreover, some operational difficulty in connection with the effective

use of CRM is observed. As per the CRM guideline, a bank needs to have its own credit policy, risk

rating model, data base and checklists. Though CRM requires updating of the lending guidelines at

least annually, but a number of banks do not follow it meticulously. Banks use CRG scoring for all

types of lending other than consumer financing, small enterprise financing, short term agricultural

credit and micro credit. The banks are not maintaining any electronic database of the CRG score of the

borrowers although it is required by the CRM. Maintaining data base can help banks in developing

more rigorous internal risk rating model as required by Basel-II for switching over to advance

approach. Though required by the CRM, in some of the banks, effective segregation among

relationship management, credit administration and approval function has not been found (BIBM

Review 2012).

In regard to the sectoral distribution, the disbursement and recovery status of agricultural and rural

credit marked some improvement in recent period. According to the BB (2013) data, both

disbursement and recovery of the agricultural credit by the banking sector increased by over 15

percent during July 2012- February 2013 (relative to the same period of the previous year). In spite of

the improvement, the credit exposure of banks to the agricultural sector and rural economy remained

very limited. The contribution of agriculture sector to GDP is almost 20 percent but the flow of credit

to this sector in Bangladesh was only around 5.59 percent of total advance as of end 2011. To ensure

greater credit flows to the agricultural sector, Bangladesh Bank has made it mandatory for all banks to

disburse at least 2 percent of their total loans to the agricultural sector. About industrial credit, it is

well known that medium and large industrial units have been the main targets of the banks.

According to BB statistics (as of end 2011), of the industrial credit, over 85 percent goes to the large

and medium industries. Small enterprises get relatively less importance. However, though slowly, the

situation is improving over the years. According to BB (2003) update, outstanding position of SME

loans stood at BDT 1008 billion as of end December 2012. The specialized banks and private sector

banks have attained notable growth in the sector in recent period. Bangladesh Bank has undertaken

notable initiatives and introduced refinancing facilities to promote greater credit flows to the SME

sectors. The BB data show that small and cottage industries accounts for less than 5 percent and flows

of banks credits to the rural areas remained very limited.

Pag

e-19

Governance, Activities and Operations of Banks

In the area of international banking, banks offer trade payment, trade finance and foreign exchange

services. Trade payment is at the heart of international banking activities of banks in Bangladesh.

Letter of Credit (LC) is the most widely used method of payment both in import and export

transactions mainly because of the regulatory restrictions. According to BIBM Review Studies (2012

and 2013), in 2011 (January-December), 97 percent (number of cases) import payments from the

country were made through LC that has gone down to 86 percent in 2012. In case of export the figure

was 66 percent in 2011 that decreased to 60 percent in 2012. In spite of the change, documentary

credit remains the most widely used international trade payment methods in the country.

Documentary collection is the second most popular method. In contrast to most global economies,

the use of open account is very low. Cash in advance is used in a very limited number of cases both in

imports and exports. However, the use of documentary collection and open account is significantly

higher within EPZs of the country where the restrictions of the trade policies of the county are not

applicable. In regard to facilitation of trade payment, ‘delay in payment’ has been found as a common

practice by the trade service providing banks, which do not only harm institutional reputations of

banks but also the country’s image. As the LC is the most commonly used method of payment, UCPDC

is particularly relevant and important for the practitioners. Bangladesh Bank accepted UCP 600 as the

regulatory framework for LC operation for cross border trade in 2007. However, there has so far been

no such circular about URR725 or URC522. No guideline is there for ISP98 and URDG758. Sometimes it

creates confusion among practitioners. As mentioned earlier, banks offer financing facilities to the

exporters and importers. Though generally interest rate is not regulated by the Bangladesh Bank, in

export financing banks interest rates cannot exceed 7 percent. Back-to-back is a very popular trade

financing technique used by the banks to support garments exporters of the country. It is well known

that the regulatory provisions related to trade services in the EPZs are different. The trade payment

related restrictions of the trade policies are not applicable for EPZs of the country. Practically, there are

confusions among bankers about the provisions applicable for the EPZs. Instead of scattered and

piecemeal directives, a comprehensive master guideline on trade service practices of EPZ might help

bankers to act uniformly and correctly. Some other common procedural difficulties faced by the banks

are related to the timely receipt of bill of entry (from customs) and delay in the disbursement of EDF

fund. Several instances of non-repatriation of export proceeds, non-reporting, and malpractices in

trade services are concerns of the regulatory authority of the banking system. However, the cases of

non-payment of the accepted bills in local LCs became a grave concern for all quarters.

As observed by the BIBM Review (2012), remarkable changes may be observed in the operational

efficiency of the trade services departments of banks. Information technology is rapidly changing

the nature of international trade services in the country. ICT based activities like internet banking on

trade services, online reporting to BB, and new avenues for remittance can be identified as adaptation

of advanced ICT by the banking sector. Basically, it has enabled them to go for faster decision making,

prompt documentation and processing. Internally, quite a few banks are fully relying on software

based operations. It is a remarkable achievement that almost all executives working in the trade

services departments of different banks have training exposures. A considerable number of

employees of the concerned departments have received training from BIBM. A remarkable

improvement in connection with the development of professional bankers in the trade services area

reflects the growing number of Certified Documentary Credit Specialist (CDCS) in the banking sector

of the country. The number of CDCS holders in the country was only 1 till 2008, which increased to

over 100 by the end of 2011.

Treasury management function of banks received importance in the country only in recent years.

Liberalization of interest rates, exchange rates, and currency convertibility necessitate establishment

of treasury management unit in the commercial banks of the country. Considering the paramount

importance of the treasury operations, Bangladesh Bank has issued a guideline to establish a separate

treasury department in each bank. In Bangladesh money market is still very thin, because of lack of

diversified market participants and market instruments. Foreign exchange market is basically the spot

market. Very limited transactions take place in the market. Though, commodity swap has been

permitted to facilitate exporter to handle price risk, the product is hardly in use. Absence of secondary

market forces the bond market to stay at a budding stage. As a result, banks especially PD banks were

suffering from liquidity problem. To overcome the situation, the dealer banks were seeking immediate

operational and policy supports from the central bank. Bangladesh Bank was very active throughout

the year (2011) for managing the liquidity pressure of banks. BB has allowed PDs to enjoy assured

liquidity support (ALS) for a period of 75 days against their holdings of T-bills and T-bonds. The

illiquidity of financial markets may also be attributed to heavy government borrowing, huge L/C

payments of BPC by SOCBs and over lending by the banks, especially PCBs. Very recently (April 2013),

Bangladesh Bank has moved to introduce a new system to help commercial banks that face a liquidity

problem by adjusting the shortfall with another bank having surplus funds with the central bank.

Under the system, BB will be allowed to adjust a bank’s shortage in the cash reserve requirement

(CRR) and statutory liquidity ratio (SLR) with another bank with surplus funds with BB. Primary dealer

banks that have an obligation to invest in government securities and bonds may handle their CRR

shortfall using the provisions.

Pag

e-20

Governance, Activities and Operations of Banks

Pag

e-21

Banking sector in Bangladesh has started giving due emphasis on HR only in the recent years.

According to BIBM survey (2012), the banks have their individual HR policy but in many cases these

are not up to date and fully implemented. Two broad areas of HR, training and career development,

are getting growing importance in a good number of banks. The survey also shows that about

two-third of the banks have their separate training institute; others operate their training activity with

having a training cell along with other job. However, for training activities most banks heavily rely on

BIBM and external trainers. Major challenges for many banks are to develop the core competencies

and skills for different operational areas like credit appraisal, risk management and handling trade and

treasury activities. Even for most of the banks, there is no scientific method of selection of trainees.

Though performance appraisal is done jointly in many banks, yet in reality subordinates hardly

contradict bosses. Compensation discrepancies, and recruitment and retention of qualified

employees are other HRM challenges of the banks.

Notable improvement has taken place in the country in regard to e-banking services in Bangladesh.

Bangladesh Bank has been playing an active role to maintain and promote smooth and secured

e-banking operations. Banks have been allowed to make online money transactions, payment of

utility bills, transfer of funds, payments for trading goods and services through e-channels like

Internet, ATM, Mobile phone, etc. BB has issued Mobile Banking guidelines to facilitate and oversee

these initiatives in the financial sector. Considering the importance of information systems security in

banks BB has issued ICT security guidelines for banking and financial institutions. In regard to the use

of ICT in the banking operation, online access to Credit Information Bureau (CIB), installation of

Bangladesh Automated Clearing House (BACH), introducing MICR cheques and EFT are remarkable

events. As a part of stepping towards online banking, the FCBs have played the pioneer role with the

adoption of modern technology in retail banking since the early 1990s, whereas the SOCBs and PCBs

came forward with such services on a limited scale since the late 1990s. At present, several PCBs and

FCBs of the country offer limited Tele banking, Internet banking, and M-banking services.

Expansion of CSR and inclusive banking activities is a notable change in the banking sector in recent

years. Bangladesh Bank has been guiding banks and financial institutions into mainstreaming

Corporate Social Responsibility (CSR) in their institutional goals and objectives in line with inclusive

growth objectives of the country. The basic target is to engage the entire financial sector in

a sustained financial inclusion campaign to reach out to the unserved and underserved population. In

response to these, the expenditure of banks on CSR activities increased by over four times in the last

three years. As part of inclusion campaign, priority attention of the Bangladesh Bank has been

directed to adequacy of credit flows to agriculture, SMEs, renewable energy generation and women

Governance, Activities and Operations of Banks

Pag

e-22

entrepreneurship. Currently, banks may sanction loan of BDT 2.5 million to women entrepreneurs

without collateral but against personal guarantee under refinance facilities by BB if the borrower is

a women entrepreneur or if 51 percent shareholders of the borrowing enterprise are women. In order

to include large number of women micro entrepreneurs in the SME credit facilities, a policy of group

based lending of up to BDT 50,000 or above has been adopted. In response to the inclusion campaign

SOCBs have by now opened over ten million new bank accounts in favor of small farmers and other

low income groups with a nominal Taka ten initial deposits, enabling them to receive government

agricultural input subsidies/social safety net payments in these accounts, besides making other

transactions.

Banking sector of Bangladesh initiated green banking activities in recent period as part of their social

and environmental responsibilities. To foster green banking practices in the country, BB formulated

the ‘Green Banking Policy and Strategy framework’ and ‘Environmental Risk Management Guidelines’

in a consultative manner. Many banks are now financing environmental friendly projects. BB has also

introduced a refinance scheme worth BDT 2 billion refinance loans for effluent treatment plants

(ETPs), solar panels, bio-gas plants and HHK technology in brick making industry at a 5 percent

interest rate provided by banks. It is to be noted that banking sector of Bangladesh responded

remarkably by undertaking a number of initiatives in regard to in-house environment management,

environmental risk management and environmental reporting. Recently, honorable Governor of BB

has been adorned as ‘Green Governor’ in recognition of the green initiatives undertaken by the

central bank in the Doha Climate Change Conference.

The Internal Control & Compliance (ICC) department of banks is responsible for risk identification of

various activities of a bank. ICC is to recognize and assess all of the material risks that could adversely

affect the achievement of the bank’s goals. As narrated in the BIBM review study (2012), the head of

the internal control is responsible for the both compliance and control related tasks which include

compliance with laws and regulation, audits and inspection, monitoring activities and risk assessment.

The head of internal control unit should have a reporting line with the bank’s board. The audit

committee of the board can be the contact point for the internal control unit. This unit must also have

a reporting line with the Managing Director (MD) of the bank. Generally, the ICC of banks comprises

the following three units-Internal Audit & Inspection Unit, Monitoring Unit and Compliance Unit. The

audit team of the ICC assesses the effectiveness of the internal control system of the bank through

periodic internal audit. The monitoring unit is responsible to monitor the operational performance of

various branches. The compliance unit of ICC is to ensure that bank complies with all regulatory

requirements while conducting its business. BIBM review (2012) reveals that in spite of rapid changes

Governance, Activities and Operations of Banks

in banking operations due to technological developments, ICC manuals of individual banks are not

reviewed regularly. Even some of the banks have not yet introduced risk based audit plan. The

personnel of ICC department actually do not have the freedom to take corrective actions. The review

also finds that most of the banks have Risk Management Units (RMU) which is separate from ICC.

However, in reality, a close cooperation between ICC and RMU is supposed to improve risk

management capacity of a bank. Some of recent experiences and cases of unethical practices and

irregularities reassert the importance of the ICC in the context of the banking sector of the country.

The frequency and magnitude of such fraudulent activities inflicted huge burden on the banking

sector and has impacted the public confidence and reputation of the banking sector- a sector which

has shown significant growth, strength and discipline for a long period of time. The occurrence of

fund embezzlement also raised serious doubt in the minds of the depositors, regulators and other

stakeholders of the banking sectors about the financial discipline and operational standards. It is

generally recognized that such types of unscrupulous activity cannot take place without the active

collaboration or passive approval of the concerned bankers. Practically, the incidences reflect the

importance as well as failure of internal control mechanism of banks.

Success of the banking operation and performance of the banking sector heavily depend upon the

enabling and supportive environment to handle the growing complexity and challenges in the

banking sector. Enforcement of the prudential guidelines and effective risk based supervision is the

need of the time. Having a set of prudent regulatory measures, effective supervision depends upon

adequate power, sufficient resources and independence to foster good supervision. Central bank

needs strong support from the government to enforce its authority and supervisory power. Recent

evidences of irregularities demonstrate that Bangladesh Bank is not in a position to take corrective

measures on its own. Incidentally, Bangladesh Bank does not have enough supervisory grips over the

state controlled commercial banks. The way out of the fund misappropriation that is observed in

recent times in the banking sector rests upon a comprehensive and risk focused internal control and

internal audit in banks, sufficient autonomy of Bangladesh Bank, and zero tolerance by the

government and the central bank against any major violations of the banking norms. Only these can

offer an enabling environment where a risk based supervision approach by Bangladesh Bank with

a set of skilled central bankers can truly deliver. This is a necessity for improving the performance and

ensuring a sustainable banking sector of the country.

Pag

e-23

Governance, Activities and Operations of Banks

Chapter Three

Health Report of the Banking Sector of Bangladesh

Strength

&

Soundness

Size&

Grow

th

PerformanceEvaluation

Criteria

Profit

ability

&Effi

ciency

Asset Quality

Inclu

sive &O

nlin

eB

ankin

g

Performance Evaluation Criteria

Pag

e-27

PEC

-5

PEC-4

PEC-3

PEC-1

PEC-2

Strength&

Soundness

Performance Evaluation Criteria (PEC) -1: Strength & Soundness

Indicator-1:Capital Adequacy Ratio

Ind

icat

or-

2:

NP

L to

Equ

ity

Rat

io

Indicator-3:

Liquid Assets

to

Short - term

Liabilities

Indic

ator 5

:

Advance

Deposit (

AD)

Ratio (%

)

Pag

e-28

A strong and sound financial system is very much essential for ensuring the long-run financial stability

of a country. Bank is a highly leveraged financial institution which greatly depends on public’s money

for their business. Because of the nature of the banking business it is highly dependent on the trust of

the customer. To ensure the customer’s confidence, a financially strong and sound banking system is

very important. The indicator ‘strength and soundness’ is very crucial to measure the shock absorbtion

capacity of a bank under any adverse economic scenario. The strength of a bank means the capacity to

withstand against all types of odds which is measured by the capital of a bank. Bank capital stands as

a protection against loss for bank customers, creditors, and shareholders. Regulators place a high

degree of importance upon assessments of capital and assign regulatory benchmarks. The soundness

is a major determinant of the viability of any banking institution. A bank can be considered as sound

when it follows all the rules, regulations and norms set by the regulators. By assuring the high level of

compliance to the regulation, a bank can not only ensure the increased financial soundness but it also

reduces the probability of bankruptcy. Five indicators have been considered for assessing the strength

and soundness of banks: (1) Capital Adequacy Ratio, (2) NPL net of provisions to Total Equity, (3) Liquid

Asset to Short-term Liabilities, (4) Borrowing Liability to Total Liability and (5) Advance to Deposit Ratio.

Indicator-4:

Borrowing

Liability to

Total

Liability

Pag

e-29

S&S – Indicator 1: Capital Adequacy Ratio (%)

Figure-1.1.1 Capital to Risk Weighted Assets Ratio of Banks [Average]

Strength & Soundness

Banks operating in Bangladesh are maintaining capital since 1996 on the basis of risk-weighted assets

in line with BCBS capital framework published in 1988. To cope with the international best practices

and to make the bank’s capital more risk sensitive as well as more shock resilient, ‘Guidelines on Risk

Based Capital Adequacy (RBCA) for Banks’ (Revised regulatory capital framework in line with Basel II)

have been introduced by BB from 2009. Subsequently, a revised guideline was suggested by central

bank during August and December 2010. Since then banks are required to maintain Capital Adequacy

Ratio (CAR) of not less than 10.0 percent with at least 5.0 percent in core capital.

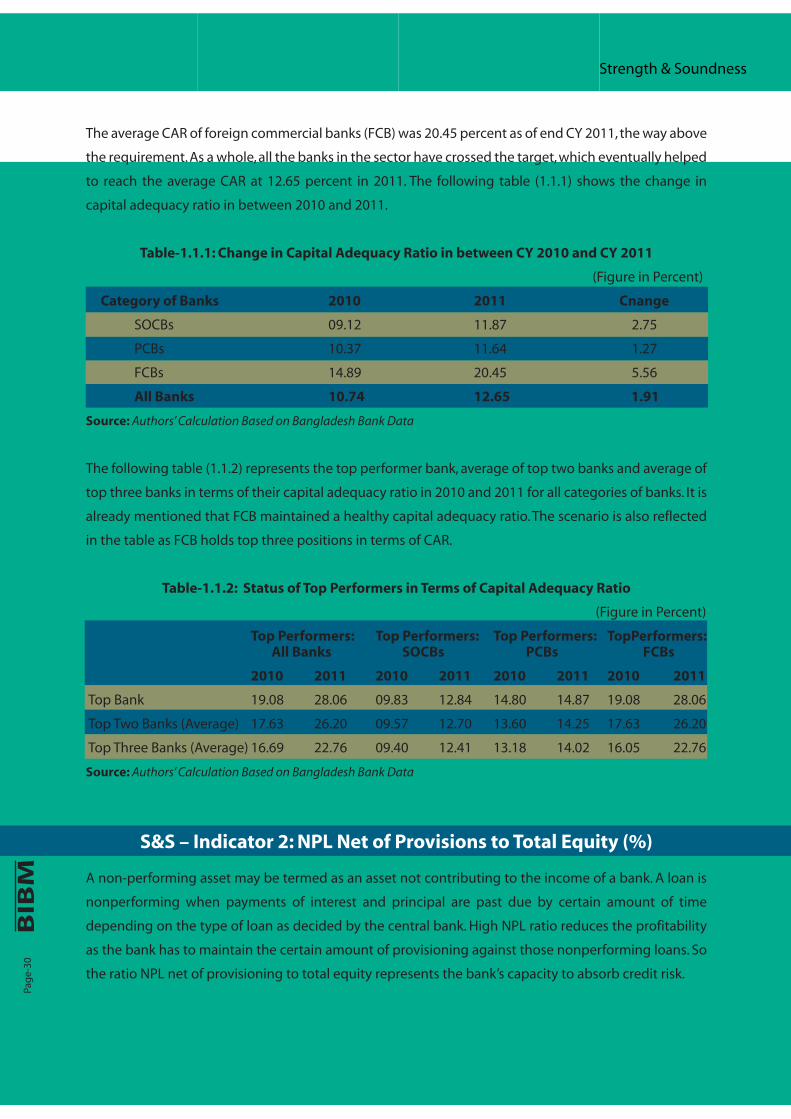

Source: Authors’ Calculation Based on Bangladesh Bank Data

The average CAR for banks improved in between CY 2010 and CY 2011. Figure 1.1.1 shows that as of

December 2010, the SOCBs, PCBs and FCBs maintained CAR of 9.12, 10.37 and 14.90 percent respectively,

which increased to 11.87, 11.64 and 20.45 percent respectively in December 2011 for 3 different

categories of banks.

Looking at the group-wise CAR position, it is evident that all categories of banks are successful in

maintaining required CAR of 10 percent in 2011. The state-owned commercial banks achieved

significant improvement in terms of their capital adequacy ratio in 2011 as compared to that of 2010.

All the private commercial banks have attained their target level. Although both SOCBs and PCBs are

successful in maintaining the minimum capital requirement set by the central bank, more needs to be

accomplished by these banks. By fulfilling the CAR of 10 percent, banks are only maintaining the

minimum capital as prescribed in Pillar-I of Basel-II. Now it is time to concentrate to increase their

capital base further to fulfill the additional capital requirement as per Pillar-II of Basel-II.

9.12

11.87 10.37

11.64

14.9

20.45

10.74 12.65

0

5

10

15

20

25

2010 2011

CA

R (%

)

SOCBs PCBs FCBs All Banks

Strength & Soundness

Pag

e-30

The average CAR of foreign commercial banks (FCB) was 20.45 percent as of end CY 2011, the way above

the requirement. As a whole, all the banks in the sector have crossed the target, which eventually helped

to reach the average CAR at 12.65 percent in 2011. The following table (1.1.1) shows the change in

capital adequacy ratio in between 2010 and 2011.

Table-1.1.1: Change in Capital Adequacy Ratio in between CY 2010 and CY 2011

(Figure in Percent)

Category of Banks 2010 2011 Cnange

SOCBs 09.12 11.87 2.75

PCBs 10.37 11.64 1.27

FCBs 14.89 20.45 5.56

All Banks 10.74 12.65 1.91

Source: Authors’ Calculation Based on Bangladesh Bank Data

The following table (1.1.2) represents the top performer bank, average of top two banks and average of

top three banks in terms of their capital adequacy ratio in 2010 and 2011 for all categories of banks. It is

already mentioned that FCB maintained a healthy capital adequacy ratio. The scenario is also reflected

in the table as FCB holds top three positions in terms of CAR.

Table-1.1.2: Status of Top Performers in Terms of Capital Adequacy Ratio

(Figure in Percent)

Top Performers: Top Performers: Top Performers: TopPerformers: All Banks SOCBs PCBs FCBs

2010 2011 2010 2011 2010 2011 2010 2011

Top Bank 19.08 28.06 09.83 12.84 14.80 14.87 19.08 28.06

Top Two Banks (Average) 17.63 26.20 09.57 12.70 13.60 14.25 17.63 26.20

Top Three Banks (Average) 16.69 22.76 09.40 12.41 13.18 14.02 16.05 22.76

Source: Authors’ Calculation Based on Bangladesh Bank Data

S&S – Indicator 2: NPL Net of Provisions to Total Equity (%)

A non-performing asset may be termed as an asset not contributing to the income of a bank. A loan is

nonperforming when payments of interest and principal are past due by certain amount of time

depending on the type of loan as decided by the central bank. High NPL ratio reduces the profitability

as the bank has to maintain the certain amount of provisioning against those nonperforming loans. So

the ratio NPL net of provisioning to total equity represents the bank’s capacity to absorb credit risk.

Strength & Soundness

Pag

e-31

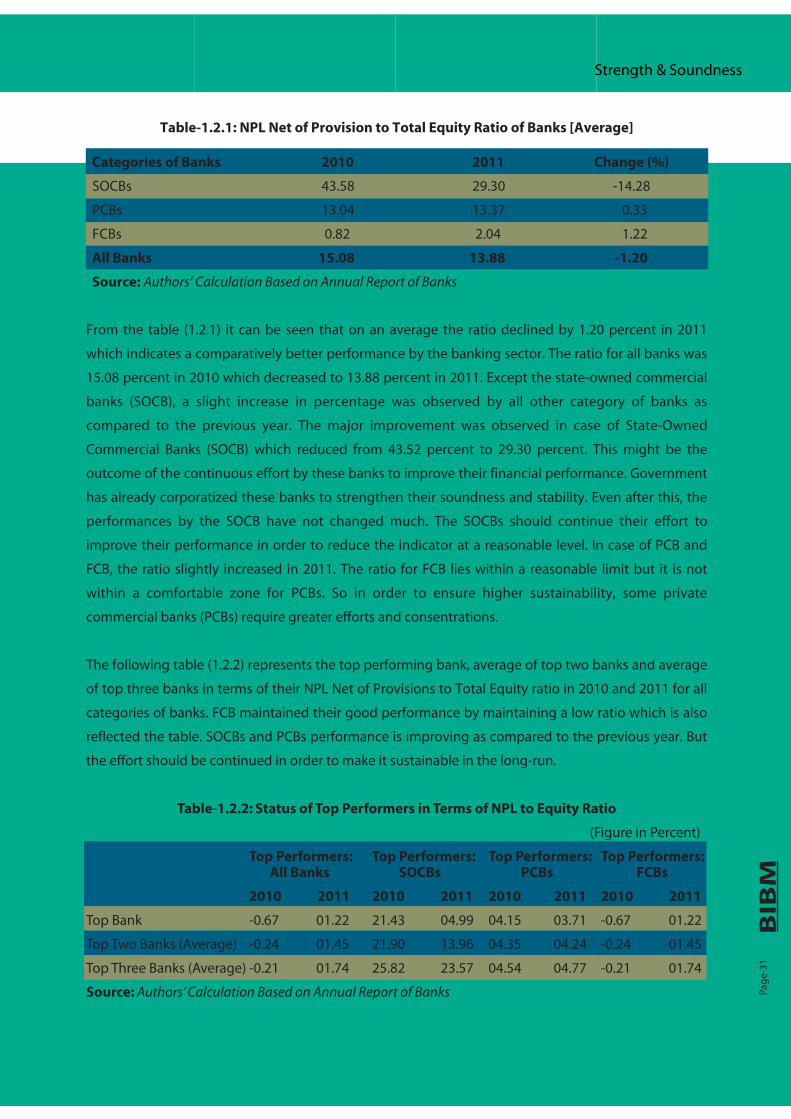

Table-1.2.1: NPL Net of Provision to Total Equity Ratio of Banks [Average]

Categories of Banks 2010 2011 Change (%)

SOCBs 43.58 29.30 -14.28

PCBs 13.04 13.37 0.33

FCBs 0.82 2.04 1.22

All Banks 15.08 13.88 -1.20

Source: Authors’ Calculation Based on Annual Report of Banks

From the table (1.2.1) it can be seen that on an average the ratio declined by 1.20 percent in 2011

which indicates a comparatively better performance by the banking sector. The ratio for all banks was

15.08 percent in 2010 which decreased to 13.88 percent in 2011. Except the state-owned commercial

banks (SOCB), a slight increase in percentage was observed by all other category of banks as

compared to the previous year. The major improvement was observed in case of State-Owned

Commercial Banks (SOCB) which reduced from 43.52 percent to 29.30 percent. This might be the

outcome of the continuous effort by these banks to improve their financial performance. Government

has already corporatized these banks to strengthen their soundness and stability. Even after this, the

performances by the SOCB have not changed much. The SOCBs should continue their effort to

improve their performance in order to reduce the indicator at a reasonable level. In case of PCB and

FCB, the ratio slightly increased in 2011. The ratio for FCB lies within a reasonable limit but it is not

within a comfortable zone for PCBs. So in order to ensure higher sustainability, some private

commercial banks (PCBs) require greater efforts and consentrations.

The following table (1.2.2) represents the top performing bank, average of top two banks and average

of top three banks in terms of their NPL Net of Provisions to Total Equity ratio in 2010 and 2011 for all

categories of banks. FCB maintained their good performance by maintaining a low ratio which is also

reflected the table. SOCBs and PCBs performance is improving as compared to the previous year. But

the effort should be continued in order to make it sustainable in the long-run.

Table-1.2.2: Status of Top Performers in Terms of NPL to Equity Ratio

(Figure in Percent)

Top Performers: Top Performers: Top Performers: Top Performers: All Banks SOCBs PCBs FCBs

2010 2011 2010 2011 2010 2011 2010 2011

Top Bank -0.67 01.22 21.43 04.99 04.15 03.71 -0.67 01.22

Top Two Banks (Average) -0.24 01.45 21.90 13.96 04.35 04.24 -0.24 01.45

Top Three Banks (Average) -0.21 01.74 25.82 23.57 04.54 04.77 -0.21 01.74

Source: Authors’ Calculation Based on Annual Report of Banks

Strength & Soundness

Pag

e-32

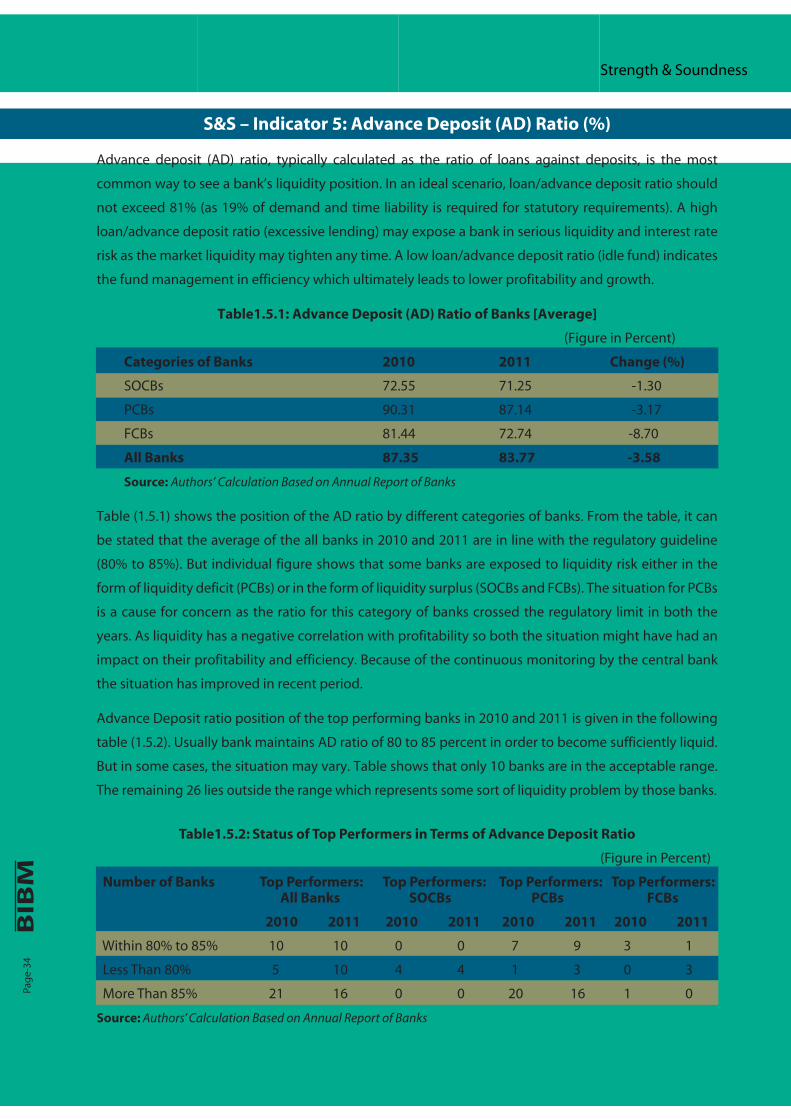

S&S – Indicator 3: Liquid Assets to Short Term Liabilities (%)

Bank usually mobilizes fund from the depositor and invest the amount in different business entity. They

always create a mismatch by doing this which sometimes put them in liquidity crisis. Liquidity is the

ability to meet obligations when they come due without incurring significant losses. For mitigating this

scenario, bank sometimes borrow from the call money market and other sources for a very short period

of time. The ratio measures a bank’s ability to meet its short-term obligations with its most liquid assets.

Higher ratio of liquid assets to short-term liabilities indicates the high ability of the bank to meet its

obligations which in turn indicates stability and soundness of the bank.

Table-1.3.1: Liquid Assets to Short Term Liabilities of Banks [Average]

Categories of Banks 2010 2011

SOCBs 58.99 73.67

PCBs 69.86 76.31

FCBs 69.19 89.66

All Banks 68.58 77.50

Source: Authors’ Calculation Based on Annual Report of Banks

From the table (1.3.1) it is evident that the ratio has improved significantly for all categories of banks.

As a result, the aggregate has also increased in 2011 from the previous year. The reason behind the

outcome is pretty simple. The banking sector has observed a severe liquidity crisis in 2010 in the history

of Bangladesh. The call money rate reached to highest ever in December 2010 (to 33.54 percent against

3.33 percent in July 2010) due to increase in demand for fresh fund in the inter-bank market following

the increase in CRR in mid-December 2010. Bangladesh Bank raised both CRR and SLR in mid-December

2010 to contain inflationary pressure. The weighted average call money rate declined after December,

2010 and the market remained stable at a tolerable level because of the timely intervention by the

Bangladesh Bank in the market. The liquidity pressure gradually eased in 2011 which helped all types of

banks to improve their ratio significantly.

Performance of top bank, average of top two banks and average of top three banks in terms of their