Embed Size (px)

Citation preview

ASLI DEMIRGUC-KUNT

ENRICA DETRAGIACHE

OUARDA MERROUCHE

Bank Capital: Lessons from the Financial Crisis

Using a multicountry panel of banks, we study whether better capitalizedbanks experienced higher stock returns during the financial crisis. We differ-entiate among various types of capital ratios: the Basel risk-adjusted ratio,the leverage ratio, the Tier 1 and Tier 2 ratios, and the tangible equity ra-tio. We find several results: (i) before the crisis, differences in capital didnot have much impact on stock returns; (ii) during the crisis, a strongercapital position was associated with better stock market performance, mostmarkedly for larger banks; (iii) the relationship between stock returns andcapital is stronger when capital is measured by the leverage ratio rather thanthe risk-adjusted capital ratio; (iv) higher quality forms of capital, such asTier 1 capital and tangible common equity, were more relevant.

JEL codes: G21, G28Keywords: bank capital, financial crisis, Basel capital accord.

SINCE THE FIRST BASEL capital accord in 1988, the prevailingapproach to bank regulation has put capital at front and center: more capital shouldmake banks better able to absorb losses with their own resources, without becominginsolvent or necessitating a bailout with public funds. In addition, by forcing bankowners to have some “skin in the game,” minimum capital requirements shouldcurb incentives for excessive risk taking created by limited liability and amplifiedby deposit insurance and bailout expectations. Over the last 20 years, regulatorycapital requirements have been refined and broadened to cover various types of risk,differentiate among asset classes of different risk, and allow for a menu of approachesto determine the risk weights to be applied to each asset category. In the process,

The views expressed in this paper are those of the authors, and should not be attributed to the WorldBank, the International Monetary Fund, or the European Securities and Markets Authority. We thank StijnClaessens, Martin Hellwig, Noel Sacasa, and seminar participants at Williams College, Chicago FederalReserve Bank Structure Conference, and the IMF Institute for useful comments.

ASLI DEMIRGUC-KUNT is Director of Research, the World Bank (E-mail: [email protected]). ENRICA DETRAGIACHE is Senior Advisor, European Department at the IMF (E-mail:[email protected]). OUARDA MERROUCHE is Program Manager, Graduate Institute of International andDevelopment Studies, Geneva (E-mail: [email protected]).

Received October 20, 2011; and accepted in revised form April 19, 2012.

Journal of Money, Credit and Banking, Vol. 45, No. 6 (September 2013)C© 2013 World Bank

1148 : MONEY, CREDIT AND BANKING

the rules have become increasingly elaborate, reflecting the growing complexity ofmodern banking, but also the need to address ongoing efforts by regulated entities tocircumvent the requirements through financial innovation.1

While regulatory consensus has viewed capital as an essential tool to limit riskin banking, there has been less agreement among economic theorists. A number oftheoretical models bear out the relationship posited by regulators that minimum cap-ital requirements ameliorate the moral hazard created by deposit insurance (Furlongand Keeley 1989, Keeley and Furlong 1990, Rochet 1992), but others find that suchrequirements, by reducing the charter value of banks, have the opposite effect (Koehnand Santomero 1980, Kim and Santomero 1988). Calem and Rob (1999) reconcilesthese different views: in a dynamic model in which banks build up capital throughretained earnings, this paper shows that when capital is low relative to the regulatoryminimum banks choose a very risky loan portfolio to maximize the option value ofdeposit insurance. As capital increases and future insolvency becomes less likely, onthe other hand, incentives to take on risk are curbed by the desire to preserve thebank’s charter value. When banks are so well capitalized that insolvency is remote,an additional increase in capital induces banks to take on more risk to benefit from theupside. In this model, the relationship between bank capital and risk is U-shaped.2

The recent financial crisis undoubtedly demonstrated that existing capital regula-tion, in its design or implementation, was inadequate to prevent a panic in the financialsector, and once again governments around the world had to step in with emergencysupport to prevent a collapse.3 Many of the banks that were rescued appeared to bein compliance with minimum capital requirements shortly before and even duringthe crisis. In the ensuing debate over how to strengthen regulation, capital continuesto play an important role. A consensus is being forged around a new set of capitalstandards (Basel III), with the goal of making capital requirements more stringent.4

In this paper we evaluate the effectiveness of current capital regulations andtest existing theories that motivate the use of capital regulation to curb bank risktaking. If bank capital truly helps curbing bank risk-taking incentives and absorbing

1. See Caprio and Honohan (1999) for a discussion.2. Diamond and Rajan (2000) presents a theory of bank capital in a framework that also explains why

financial intermediaries exist. In this theory, capital helps bank deal with unexpected withdrawals fromdepositors, but increases ex post rent extraction from borrowers, which is undesirable ex ante. For a reviewof the literature on bank capital, see for instance Santos (2001).

3. See, for instance, Vinals et al. (2010), Caprio, Demirguc-Kunt, and Kane (2010), Demirguc-Kuntand Serven (2010), Hellwig (2010), and Merrouche and Nier (2010).

4. In July 2010, the Basel Committee agreed to introduce a Tier 1 leverage ratio of 3% on a trialbasis, and later on, in September 2010, it formulated new, strengthened risk-adjusted capital requirements.Specifically, the common equity ratio will increase from 2% to 4.5%, with an additional countercyclicalbuffer of 0–2.5% at the discretion of country supervisors. In addition, banks will be required to hold a“capital conservation” buffer of an additional 2.5% of common equity, bringing the total to 7%. The Tier1 capital requirement will increase to 6% from 4%, while the total risk-adjusted capital requirement willremain unchanged at the existing 8% level. Banks will be able to meet the difference between the totalcapital requirement and the Tier 1 requirement with Tier 2 capital. Definitions of various forms of capitalhave also become more stringent. Particularly, there will be stronger limits on the amount of intangiblecapital (mortgage servicing rights, deferred tax assets, minority interests). All changes will be phased ingradually, and the transition will have to be completed by 2019.

ASLI DEMIRGUC-KUNT, ENRICA DETRAGIACHE, AND OUARDA MERROUCHE : 1149

losses, we would expect that, when a large, unexpected negative shock to bankvalue materializes—as was the case with the financial crisis that began in August2007—equity market participants would judge better-capitalized banks to be in abetter position to withstand the shock, and the stock price of these banks would notfall as much as that of poorly capitalized banks.

A second question that we address in the paper is which concept of capital was morerelevant to stock valuation during the crisis. Existing capital requirements are set as aproportion of risk exposure; but if the risk exposure calculation under Basel rules didnot reflect actual risk, capital measures based on cruder risk-exposure proxies, suchas total assets, may have been considered as more meaningful by equity traders (Blum2007). The flaws of Basel I risk weights included the 50% risk weight for loans securedby mortgages, the zero risk weights on sovereign debt, and incentives to engage inregulatory arbitrage caused by the lack of differentiation among commercial loansof different quality. Critics of Basel II questioned the increased reliance on creditrating agencies to determine risk weights (given that rating agencies are paid bythe rated parties) and the reliance on banks’ own (internal) models, which are nottransparent and create problems of consistency between banks. Hellwig (2010) arguesthat Basel II risk calibrations, in particular under the model-based approach appliedby large banks, led to excessive indebtedness and maturity transformation through:(i) insufficient accounting of risks arising from correlations of credit risks betweenmortgage assets and derivatives and correlations between counterparty credit risks andunderlying risks in derivatives and other hedge contracts; and (ii) a poorly designedempirical basis for risk modeling that uses short times series, which exhibit substantialnonstationarity and does not account for the endogeneity of the risks involved. A thirdissue is the types of instrument that are counted as capital for regulatory purposes. Asrecognized by the Basel Committee on Banking Supervision (2009), under currentstandards some banks were able to show strong capitalization while holding a limitedamount of tangible common equity, which is the component of capital that is availableto absorb losses while the bank remains a going concern. In our regressions, we testwhether banks with higher quality capital were viewed more positively by equitymarket participants.

Because we use a panel of banks from several countries, in our tests we canuse country–time dummy variables to control for all country and time-specific fac-tors potentially affecting stock returns, including differences in interest rates andother macroeconomic variables, the severity of the financial crisis and its economicrepercussions across countries, different policy responses by the authorities, differ-ent quality of bank regulation and supervision, and differences in accounting andregulatory standards. This approach greatly reduces concerns about possible omittedvariables.

We find support for the hypothesis that better-capitalized banks experienced asmaller decline in their equity value during the crisis. However, the effect is large androbust only for a subsample comprising the larger banks. For this group, we also findthat stock returns during the crisis were more sensitive to the leverage ratio than tothe risk-adjusted Basel ratio, an indication that market participants may have viewed

1150 : MONEY, CREDIT AND BANKING

the risk-adjustment under Basel as uninformative during the crisis.5 Finally, we alsofind some evidence that Tier 1 capital was seen as the more relevant notion of capital,especially in the sample of larger banks.

Our paper is related to work by Estrella, Park, and Peristiani (2000) that tests howalternative capital ratios fared in predicting U.S. bank failures in the early 1990s,and finds that a leverage ratio performs just as well as a risk-adjusted measure ofcapital. Berger and Bouwman (2009) explore the relationship between bank capitaland different aspects of banks’ performance in crises and tranquil times for U.S.banks. Crises include both banking crises and stock market crashes. Among thetests is a comparison of excess stock returns on a portfolio of well-capitalized banksand one of poorly capitalized banks during the recession of the early 1990s andduring the recent subprime crisis. According to this study, better capitalized banksdid significantly better in the early 1990s, but not in the recent crisis. The study doesnot explore the potentially different role of alternative concepts of bank capital.

The paper is structured as follows. The next section presents the data and theempirical model. Section 2 contains the main results. Section 3 concludes.

1. SAMPLE SELECTION, DATA DESCRIPTION, AND EMPIRICAL MODEL

1.1 Sample Selection

We start with all the banks in the Bankscope database that are listed and hence havea stock price. We then exclude banks for which no information is available on capital.In addition, since we rely on intracountry variation to identify the relationships ofinterest, we exclude from the sample countries/dates for which we have less thanfive banks in the sample. The baseline sample includes a total of 381 banks in 12economies during the period Q1/2005–Q1.2009. Not all banks enter the sample inevery quarter, so the sample is unbalanced. The sample size in each quarter variesbetween 273 and 313.6 All the countries in the sample are advanced countries,7 andU.S. and Japanese banks dominate the sample. Note that the United States has beenslower to implement Basel II capital requirements than the other countries in oursample. In fact, in the United States the implementation of Basel II is still ongoingwhile in other countries implementation started at the end of 2006 for the simplermethodologies and completed at the end of 2007 for the advanced methodologies(Financial Stability Institute 2010).

The ratio of total assets of the banks in our sample to GDP varies between about144% (Hong Kong) and 18% (United States), with an average of 45% of GDP.

5. Throughout the paper we use interchangeably the terms “Basel ratio” and “risk-weighted capitalratio.”

6. Only two banks in our sample were closed down during our sample period (both of them U.S.banks), so attrition bias should not be a serious concern.

7. The sample comprises Canada, Denmark, France, Germany, Greece, Hong Kong, Italy, Japan,Norway, United Kingdom, and the United States.

ASLI DEMIRGUC-KUNT, ENRICA DETRAGIACHE, AND OUARDA MERROUCHE : 1151

Throughout the paper, we also show estimation results for a subsample includingonly very large banks, that is, banks with assets above US$50 billion. This sampleincludes a total of 91 banks from eight countries (with sample size in each quarterbetween 58 and 66 banks). It accounts for about 20% of the number of banks and65% of total assets of the full sample. The rationale for focusing on the largest banksis that typically these are the more sophisticated institutions that operate on a globalscale with complex balance sheets. Thus, these may be the banks with more opaqueassets and in a better position to skirt capital regulation through regulatory arbitrage.In addition, large banks are key to the stability of the system as a whole.

1.2 The Empirical Model

We estimate various version of the following basic equation:

yi j t =∑

j t

α j t d jt + β1(dnoncrisis ∗ ki j t−1) + γ 1(dnoncrisis ∗ Xi jt−1)

+β2(dcrisis ∗ ki j t−1) + γ 2(dcrisis ∗ Xi jt−1) + ui jt ,

where yijt is the bank’s stock return between the end of quarter t – 1, and the end ofquarter t calculated as log[RI(t)/RI(t – 1)], where RI is the Datastream return index:

RIt = RIt−1 ∗ P It

P It−1∗

(1 + DY

100 ∗ n

),

where PI is the price index, DY is the dividend yield of the price index, and n is thenumber of days in financial year. The αs, βs, and γ s are coefficients to be estimated;djt is a matrix of country/time dummy variables; kijt–1 is lagged bank capital, thevariables we are mostly interested in; and Xijt–1, is a matrix of bank-level controlvariables.8 Note that dnoncrisis is a dummy variable taking the value of 1 for thequarters preceding the financial crisis, that is, Q1.2006–Q2.2007, while dcrisis is adummy variable for quarters during which the financial crisis was unfolding, namely,Q3.2007–Q1.2009. Finally, uijt is a disturbance term.9 Through the interaction termwith the crisis dummy we allow the effect of the various explanatory variables onstock returns to differ during the crisis period.

The country/year dummy variables control for any possible omitted effect thatoperates at the country level, such as macroeconomic shocks, the systemic componentof the shock to bank equity prices, the policy response to the crisis, differences inaccounting and regulatory definition of capital across countries, and so on. In otherwords, what our model seeks to explain is just the cross-sectional, within-countrydispersion in stock returns in each quarter.

8. The test of serial correlation in the error term (as described in Drukker 2003) fails to reject the nullhypothesis of no serial correlation (p-value = 0.95).

9. For a similar empirical model relating stock returns during the financial crisis to firm characteristics,see Tong and Wei (2010).

1152 : MONEY, CREDIT AND BANKING

To isolate the effect of capital on this dispersion, we control for other bank-specificcharacteristics that may affect stock returns. Specifically, we control for bank liquidityusing liquid assets/assets; the bank’s reliance on deposits for funding (deposits/totalassets), asset quality (loans loss provisions/total assets), the banks’ business model(net loans/assets), and the bank size (log of total assets). Also, following standardasset pricing models, we include in the regression the stock’s beta (computed as the5-year covariance between the bank’s monthly stock return and the country stockmarket return) and the market-to-book value of equity.10 The price–earnings ratio(P/E) measure possible mispricing of bank equity during the boom.

Explanatory variables computed from bank balance sheet information, includingthe variables measuring bank capital, are available on a yearly basis rather than aquarterly basis, while our dependent variable is quarterly. For these variables, we usethe last available (but not contemporaneous) observation. For example, stock returnsduring each of the four quarters of 2007 are regressed on balance sheet variables atthe end of 2006. The model is estimated with ordinary least squares (OLS) estimates,and standard errors are clustered at the bank level to take into account possibleautocorrelation in the residuals.11

1.3 Overview of the Data

Table 1 shows summary statistics for the distribution of stock returns during thesample period for the full sample and for the sample of larger banks. Median quarterlystock returns are positive in the precrisis period and, as expected, become negative inthe third quarter of 2007, with a median quarterly decline of 2.6% in the full sampleand 3.5% in the sample of larger banks. Returns are also much more dispersed duringthe crisis than in tranquil times, with the standard deviation more than doubling. Thepost-Lehman quarters show even more negative stock returns and somewhat higherdispersion.

The main variable of interest is bank capital. As discussed in the Introduction,we use a number of alternative definitions of capital: (i) the risk-adjusted regulatorycapital ratio, calculated according to Basel rules—this is calculated as the sum of Tier1 and Tier 2 capital divided by risk-adjusted assets and off-balance sheet exposures;(ii) the Tier 1 regulatory ratio, which excludes Tier 2 capital from the numerator; (iii)the leverage ratio (defined as regulatory capital divided by total assets); (iv) the Tier1 ratio and Tier 2 leverage ratio; and (v) the tangible common equity ratio (definedas tangible equity divided by tangible assets). Tier 1 capital comprises shareholderfunds and perpetual, noncumulative preference shares. Tier 2 capital comprises hybridcapital, subordinated debt, loan loss reserves, and valuation reserves.

10. For a discussion of why it is desirable to include these variables directly in the regressions as firmcharacteristics rather than going through a factor model, see Tong and Wei (2010) and Whited and Wu(2006).

11. In unreported tests, we checked that clustering at the country level or by quarter (or both) does notchange the standard errors substantially.

ASLI DEMIRGUC-KUNT, ENRICA DETRAGIACHE, AND OUARDA MERROUCHE : 1153

TAB

LE

1

SUM

MA

RY

STA

TIS

TIC

S:C

API

TAL

RA

TIO

SA

ND

CO

NT

RO

LV

AR

IAB

LE

S

No.

ofob

serv

atio

nsM

ean

Std.

dev.

25th

perc

entil

e50

thpe

rcen

tile

75th

perc

entil

e95

thpe

rcen

tile

Full

sam

ple

Stoc

kre

turn

prec

risi

sQ

1.20

06–Q

2.20

071,

875

0.4

3.6

−1.

60.

32.

26.

1St

ock

retu

rncr

isis

Q3.

2007

–Q1.

2009

2,34

4−

3.5

7.8

−6.

7−

2.6

0.8

6.8

Stoc

kre

turn

post

-Leh

man

Q3.

2008

–Q1.

2009

1,01

3−

5.3

9.8

−10

.0−

4.8

0.4

8.9

RW

Rt

4,25

412

.62.

810

.711

.913

.719

.5R

WR

t14,

073

10.2

2.8

8.1

9.7

11.6

16.5

RW

Rt2

4,04

92.

31.

51.

22.

43.

14.

9L

Rt

3,77

98.

12.

55.

97.

89.

813

.0L

Rt1

3,81

46.

72.

44.

76.

38.

311

.4L

Rt2

3,72

61.

41.

10.

71.

31.

93.

4C

omm

oneq

uity

/RW

A3,

655

9.6

5.5

6.3

9.1

11.9

19.5

Com

mon

equi

ty/T

A5,

381

7.1

4.5

3.8

6.2

9.5

16.8

Oth

erca

pita

l/RW

A3,

654

1.2

3.3

−0.

60.

22.

28.

6O

ther

capi

tal/T

A3,

700

0.8

2.3

−0.

40.

11.

46.

0Ta

ngib

leeq

uity

/tang

ible

asse

ts5,

495

8.1

5.2

5.0

6.7

9.2

18.1

Mar

kett

obo

okva

lue

ofeq

uity

(PB

)4,

152

1.35

27.

897

1.01

71.

440

1.98

03.

078

Pric

e–ea

rnin

gsra

tio(P

E)

3,95

424

.537

149.

932

12.8

2515

.833

21.0

0038

.600

Bet

a4,

186

0.54

01.

090

0.24

30.

477

0.79

71.

487

Loa

nlo

sspr

ovis

ions

/TA

4,18

10.

234

0.24

50.

059

0.15

40.

329

0.86

3L

iqui

das

sets

/TA

4,15

67.

761

10.6

130.

118

2.84

310

.399

34.3

07To

tald

epos

its/T

A4,

195

73.3

6915

.359

63.7

0777

.242

87.2

7389

.929

Net

loan

s/TA

4,21

564

.289

14.4

8557

.830

66.8

4073

.940

83.4

30L

og(T

A)

4,21

916

.021

1.87

914

.561

16.2

6317

.429

18.6

59L

arge

bank

ssa

mpl

eSt

ock

retu

rnpr

ecri

sis

Q1.

2006

–Q2.

2007

340

0.8

3.0

−1.

20.

82.

46.

0St

ock

retu

rncr

isis

Q3.

2007

–Q1.

2009

480

−4.

78.

0−

8.0

−3.

50.

06.

7St

ock

retu

rnpo

st-L

ehm

anQ

3.20

08–Q

1.20

0921

1−

6.7

10.3

−11

.6−

5.8

−1.

08.

7R

WR

t88

712

.22.

410

.611

.713

.119

.5R

WR

t182

78.

61.

97.

28.

29.

512

.7R

WR

t282

73.

21.

52.

73.

34.

05.

2

(Con

tinue

d)

1154 : MONEY, CREDIT AND BANKING

TAB

LE

1

CO

NT

INU

ED

No.

ofob

serv

atio

nsM

ean

Std.

dev.

25th

perc

entil

e50

thpe

rcen

tile

75th

perc

entil

e95

thpe

rcen

tile

LR

t74

17.

22.

25.

46.

58.

512

.4L

Rt1

769

5.1

1.7

3.7

4.6

6.0

8.8

LR

t273

62.

01.

01.

31.

92.

83.

8C

omm

oneq

uity

/RW

A74

57.

23.

93.

47.

210

.513

.4C

omm

oneq

uity

/TA

973

4.8

3.3

1.9

4.1

7.5

10.7

Oth

erca

pita

l/RW

A74

51.

43.

3−

1.1

0.8

3.5

7.3

Oth

erca

pita

l/TA

748

0.7

2.0

−0.

60.

51.

94.

3Ta

ngib

leeq

uity

/tang

ible

asse

ts97

64.

52.

02.

94.

15.

98.

6M

arke

tto

book

valu

eof

equi

ty80

71.

601

2.31

91.

297

1.67

02.

157

2.93

9Pr

ice–

earn

ings

ratio

800

31.6

6929

5.39

911

.767

14.1

6717

.992

31.3

03B

eta

819

0.86

00.

488

0.49

20.

797

1.15

01.

850

Loa

nlo

sspr

ovis

ions

/TA

820

0.23

40.

213

0.07

30.

177

0.33

80.

679

Liq

uid

asse

ts/T

A82

09.

586

11.1

000.

779

4.35

516

.489

34.2

66To

tald

epos

its/T

A79

662

.089

17.2

8849

.131

62.6

0676

.183

88.8

89N

etlo

ans/

TA82

053

.105

16.1

2643

.873

54.6

3066

.195

74.2

10L

og(T

A)

820

18.4

290.

318

18.1

7418

.659

18.6

5918

.659

NO

TE

S:B

anks

inou

rsam

ple

oper

ate

in12

diff

eren

tOE

CD

coun

trie

s.T

hesa

mpl

epe

riod

fort

hem

easu

res

ofca

pita

l(la

gged

one

peri

odin

the

regr

essi

on)i

s20

05–2

008.

The

year

lyda

taar

eob

tain

edfr

omB

anks

cope

.RW

Rt

isth

eto

talc

apita

lade

quac

yra

tioun

der

the

Bas

leru

les.

Itm

easu

res

regu

lato

ryca

pita

ldiv

ided

byri

sk-w

eigh

ted

asse

tsan

dof

fba

lanc

esh

eetr

isks

.RW

Rt1

isth

eT

ier

1ri

sk-w

eigh

ted

capi

talr

atio

,defi

ned

assh

areh

olde

rfu

nds

plus

perp

etua

l,no

ncum

ulat

ive

pref

eren

cesh

ares

plus

reta

ined

earn

ings

,as

ape

rcen

tage

ofri

sk-w

eigh

ted

asse

tsan

dof

fba

lanc

esh

eetr

isks

mea

sure

dun

der

Bas

elru

les.

RW

Rt2

isth

eT

ier

2ca

pita

lrat

io,d

efine

das

subo

rdin

ated

debt

,hyb

rid

capi

tal,

loan

loss

rese

rves

,and

valu

atio

nre

serv

esdi

vide

dby

risk

-wei

ghte

das

sets

and

off

bala

nce

shee

tris

ksm

easu

red

unde

rB

asle

rule

s.L

Rti

sth

ele

vera

gera

tiode

fined

asre

gula

tory

capi

tal

divi

ded

byto

tala

sset

s.L

Rt1

isth

eT

ier

1le

vera

gera

tioan

dL

Rt2

isth

eT

ier

2le

vera

gera

tio.O

ther

capi

tali

sal

lcap

itale

xclu

ding

com

mon

equi

ty.T

angi

ble

com

mon

equi

tyis

shar

ehol

der

fund

sm

inus

inta

ngib

leca

pita

l.T

hem

arke

tvar

iabl

es(s

tock

retu

rn,p

rice

–ear

ning

sra

tio,B

eta,

mar

ket-

to-b

ook

valu

eof

equi

ty)a

requ

arte

rly

fort

hepe

riod

Q1.

2005

–Q1.

2008

.The

sour

ceis

Dat

astr

eam

.The

beta

isde

fined

asth

em

easu

reof

anas

set’s

risk

inre

latio

nto

the

mar

ket;

itis

calc

ulat

edov

era

5-ye

arpe

riod

usin

gm

onth

lyob

serv

atio

ns.L

iqui

dity

incl

udes

trad

ing

asse

ts,a

ndlo

ans

and

adva

nces

with

am

atur

ityof

less

than

3m

onth

s.To

tald

epos

itsin

clud

esa

ving

san

dde

man

dde

posi

ts.T

Ast

ands

for

tota

lass

ets.

Sum

mar

yst

atis

tics

are

repo

rted

for

the

who

lesa

mpl

ean

dth

esa

mpl

eof

larg

eba

nks.

Lar

geba

nks

are

defin

edas

bank

sw

ithto

tala

sset

sab

ove

$50

billi

on(t

he20

thpe

rcen

tile

ofas

sets

).

ASLI DEMIRGUC-KUNT, ENRICA DETRAGIACHE, AND OUARDA MERROUCHE : 1155

Table 1 shows summary statistics on bank capital in our samples and sum-mary statistics for the other explanatory variables. For the full sample, the medianrisk-adjusted capital asset ratio was 11.9%, comfortably above the minimum Baselrequirement of 8%, with a standard deviation of 2.8%. Interestingly, larger banks hadlower capital than the full sample as measured by the tangible equity ratio (a medianof just 4.1%), the leverage ratio (a median of 6.5%), or the Tier 1 risk-adjusted ratio(8.2%). Thus, larger banks were relying more heavily on lower quality capital andhad larger “risk adjustments” of assets than smaller banks.

2. THE RESULTS

2.1 Results from the Baseline Model

Table 2 contains estimation results for the baseline model for the full sample and thesample of larger banks. The model allows the coefficient of all explanatory variablesto differ among the precrisis and crisis periods, and the table also reports tests for theequality of the crisis and precrisis coefficients.

Before the crisis, several of the explanatory variables appeared to significantlyaffect stock returns: banks with lower loan loss provisions, a higher market-to-bookratio, and a lower P/E ratio had higher stock returns. Also, among large banks moreliquidity was associated with higher returns. As for capital, there is some evidencethat higher capital (measured by the leverage ratio) resulted in higher stock returns inthe full sample, but the coefficient is small and the statistical significance is marginal.

During the crisis, the relationship between stock returns and bank characteristicschanged markedly. More reliance on deposit funding was rewarded by the stock mar-ket, not surprisingly given the disruptions in wholesale funding markets throughoutthe crisis. On the other hand, the standard liquidity ratio has a negative and significantcoefficient in one specification. Perhaps this reflects the fact that liquid assets wereassociated with holdings of mortgage-backed securities that were at the center of theasset quality deterioration and quickly became illiquid once the crisis started (BaselCommittee on Bank Supervision 2009). Also, liquidity during a crisis may capturethe extent of liquidity support by the Central Bank, a signal of trouble. The coefficientof loan loss provisions becomes much larger in the full sample, although it remainsinsignificant for the larger banks. The market-to-book ratio is no longer significantin the full sample.

Turning to capital, the Basel ratio is positive and (marginally) significant in thefull sample during the crisis. Based on our estimates, an increase in this ratio by1 percentage point increases quarterly stock returns by 11 basis points, a relativelysmall effect. The leverage ratio is not significant in the full sample. Among the largestbanks, on the other hand, the leverage ratio has a positive and strongly significantcoefficient in the crisis while the Basel ratio is insignificant. As to the magnitudeof the effect, for the large banks increasing the leverage ratio by 1 percentage pointwould have resulted in an additional 55 basis points in stock returns per quarter, or12% of the median quarterly decline of 4.7%.

1156 : MONEY, CREDIT AND BANKING

TABLE 2

STOCK MARKET PERFORMANCE AND BANK CAPITAL OVER THE FINANCIAL CYCLE

Full sample Large banks

RWR LR RWR LR(1) (2) (3) (4)

Precrisis periodCapital*PreCrisis 0.023 0.078* − 0.155 − 0.046

[0.036] [0.046] [0.102] [0.089]Liquidity*PreCrisis 0.016* 0.012 0.047** 0.041

[0.008] [0.010] [0.022] [0.026]Deposits*PreCrisis 0.013 0.017 0.013 0.014

[0.009] [0.012] [0.014] [0.013]Net Loans*PreCrisis 0.001 − 0.001 − 0.020* − 0.012

[0.007] [0.008] [0.012] [0.012]Provisions*PreCrisis − 1.204*** − 1.043** − 1.333* − 1.402

[0.374] [0.428] [0.760] [0.886]Size*PreCrisis 0.053 0.07 − 0.698 − 0.209

[0.070] [0.078] [0.839] [0.736]PB*PreCrisis 0.018*** 0.015** 0.108 0.093

[0.005] [0.006] [0.072] [0.075]PE*PreCrisis 0.000 − 0.001*** − 0.009*** − 0.009***

[0.000] [0.000] [0.003] [0.003]Beta*PreCrisis − 0.233 − 0.082 − 0.239 − 0.338

[0.242] [0.257] [0.293] [0.349]Crisis period

Capital*Crisis 0.114* 0.124 0.207 0.553***[0.063] [0.096] [0.143] [0.194](0.079) (0.597) (0.004) (0.002)

Liquidity*Crisis − 0.037** − 0.037 0.098* 0.094[0.017] [0.022] [0.056] [0.066](0.002) (0.015) (0.308) (0.334)

Deposits*Crisis 0.036** 0.038* 0.074*** 0.102***[0.016] [0.020] [0.022] [0.030](0.125) (0.180) (0.022) (0.011)

Net Loans*Crisis − 0.030* − 0.031* − 0.032 − 0.073**[0.016] [0.018] [0.028] [0.028](0.020) (0.080) (0.694) (0.043)

Provisions*Crisis − 3.014*** − 3.644*** − 2.947 − 2.927[0.995] [1.076] [2.373] [3.246](0.068) (0.017) (0.497) (0.637)

Size*Crisis − 0.038 0.043 − 1.265 − 0.73[0.088] [0.090] [0.830] [0.730](0.180) (0.691) (0.005) (0.010)

PB*Crisis 0.027 0.006 0.043 0.024[0.064] [0.062] [0.070] [0.042](0.885) (0.893) (0.582) (0.465)

PE*Crisis − 0.001*** − 0.001*** − 0.001*** − 0.001***[0.000] [0.000] [0.000] [0.000](0.267) (0.837) (0.015) (0.008)

Beta*Crisis − 0.594* − 0.754** − 0.105 0.014[0.350] [0.358] [0.506] [0.658](0.333) (0.084) (0.800) (0.585)

(Continued)

ASLI DEMIRGUC-KUNT, ENRICA DETRAGIACHE, AND OUARDA MERROUCHE : 1157

TABLE 2

CONTINUED

Full sample Large banks

RWR LR RWR LR(1) (2) (3) (4)

Country*Year FE Yes Yes Yes YesNumber of observations 4,254 3,779 887 741R2 0.23 0.23 0.31 0.32

NOTES: The estimated model is:

yi j t = ∑j t

α j t d j t + β1(dnoncrisis ∗ ki j t−1) + γ 1(dnocrisis ∗ Xi jt−1) + β2(dcrisis ∗ ki j t−1) + γ 2(dcrisis ∗ Xi jt−1) + ui j t ,

where yijt is the bank’s stock returns in quarter t; the αs, βs, and γ s are coefficients to be estimated; djt is a matrix of coun-try*time dummy variables; kijt–1 is bank capital, the variables we are mostly interested in; Xijt–1, is a matrix of bank-level control variables;dcrisis is a dummy variable for quarters during which the financial crisis was unfolding; and uijt is a disturbance term. The stock return(including dividends) is calculated as ln(RI(t)/RI(t – 1)), where RI is the Datastream total return index. The sample period for the stock returnis Q1.2006–Q1.2009. Crisis is a dummy that takes value 1 from Q3.2007–Q1.2009. Capital is measured either as total regulatory capital(Tier 1 + Tier 2) scaled by Basel risk-weighted assets (RWR) or total regulatory capital scaled by total unweighted assets (leverage ratio,LR). See Table 1 for a detailed definition of the control variables. Liquidity stands for liquid assets, deposits for total deposits (includingdemand and saving deposits), provisions for loan loss provisions, and size is the logarithm of total assets. Liquidity, deposits, net loans, andloan loss provisions are all in percentage of total assets. PB stands for market-to-book value of equity and PE for price–earnings ratio. Allexplanatory variables are lagged 1 year. We report estimates for the whole sample and the sample of large banks. Large banks are defined asbanks with total assets above $50 billion. We report standard errors clustered by bank in brackets and the p-value for the test of significantdifference between the precrisis and crisis coefficients in parentheses. *, **, and *** stand for statistically significant at the 10%, 5%, and1% levels, respectively. Robust standard errors clustered by bank are reported in brackets. In parentheses we report the p-value for the test ofequality of effects during crisis and precrisis.

The finding that the leverage ratio is significant while the regulatory ratio is notfor large banks may suggest that market participants did not view the risk adjustmentunder Basel as informative in capturing the true risk in bank portfolios during thecrisis. This also suggests that the differences in stock returns among large banks withdifferent capital levels did not just reflect expectations about actions by regulators(such as decisions to close or merge undercapitalized banks, or demand additionalcapital), as such decisions would presumably have been taken on the basis of shortfallsin regulatory capital. Rather, capital mattered because of its ability to absorb lossesas well as its possible role as a signal of bank asset quality.

When we split capital into Tier 1 and Tier 2 (Table 3), it is Tier 1 leveragethat remains significant, suggesting that market participants focused more on thecomponent of capital that is available to absorb losses while the bank continues as agoing concern. In the last four columns of Table 3, we measure capital using the ratioof tangible common equity to tangible capital. When we do this, for the full samplecapital is significant both before the crisis and during the crisis, but the coefficient issmall. For the large bank sample, the coefficient is significant and large in magnitudeduring the crisis, consistent with the results for Tier 1 leverage.

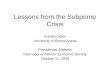

To gain a better understanding of the timing of the effects under consideration,we have estimated our empirical model separately for each quarter and plotted theestimated regression coefficients of capital and their 10% confidence interval inFigure 1. We do this exercise for the two concepts of capital (regulatory ratio andleverage ratio) and for the two samples (full sample and large banks only). The chartsshow that the “sensitivity” of stock returns to bank capital was negligible before thecrisis, and it became stronger as the crisis progressed, until the third quarter of 2008.

1158 : MONEY, CREDIT AND BANKING

TAB

LE

3

TIE

R1

AN

DT

IER

2C

API

TAL

AN

DTA

NG

IBL

EC

OM

MO

NE

QU

ITY

Full

sam

ple

Lar

geba

nks

Full

sam

ple

Lar

geba

nks

RW

RL

RR

WR

LR

RW

RL

RR

WR

LR

Full

sam

ple

Lar

geba

nks

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

Tie

r1*

PreC

risi

s0.

024

0.11

0*−

0.09

20.

061

[0.0

46]

[0.0

61]

[0.1

29]

[0.1

49]

Tie

r2*

PreC

risi

s0.

074

0.00

6−

0.10

6−

0.25

2[0

.055

][0

.072

][0

.145

][0

.178

]T

ier

1*C

risi

s0.

117

0.15

40.

264

0.60

3***

[0.0

80]

[0.1

08]

[0.1

86]

[0.2

10]

Tie

r2*

Cri

sis

0.05

10.

058

0.13

10.

415

[0.0

98]

[0.1

88]

[0.2

57]

[0.3

50]

Com

mon

equi

ty*P

reC

risi

s0.

015

0.04

8−

0.00

5−

0.00

3[0

.018

][0

.034

][0

.089

][0

.143

]O

ther

capi

tal*

PreC

risi

s−

0.09

7***

−0.

079

−0.

053

−0.

214*

[0.0

34]

[0.0

59]

[0.0

83]

[0.1

12]

Com

mon

equi

ty*C

risi

s0.

114*

*0.

165*

*0.

283*

*0.

617*

*[0

.044

][0

.067

][0

.126

][0

.278

]O

ther

capi

tal*

Cri

sis

−0.

015

0.00

20.

324*

*0.

561*

[0.0

76]

[0.1

02]

[0.1

44]

[0.2

93]

Tang

ible

equi

ty*P

reC

risi

s0.

038*

*0.

086

[0.0

19]

[0.0

77]

Tang

ible

equi

ty*C

risi

s0.

095*

**0.

532*

**[0

.031

][0

.168

]C

ontr

ols*

Cri

sis

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Con

trol

s*Pr

eCri

sis

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Cou

ntry

*Yea

rFE

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Num

ber

ofob

serv

atio

ns4,

049

3,72

682

773

63,

654

3,70

074

574

85,

495

976

R2

0.23

0.23

0.32

0.33

0.23

0.23

0.32

0.32

0.22

0.30

NO

TE

S:T

hede

pend

entv

aria

ble

isth

equ

arte

rly

stoc

kre

turn

.The

stoc

kre

turn

(inc

ludi

ngdi

vide

nds)

isca

lcul

ated

asln

(RI(

t)/R

I(t–

1)),

whe

reR

Iis

the

Dat

astr

eam

tota

lret

urn

inde

x.Se

eTa

ble

2fo

ra

deta

iled

desc

ript

ion

ofth

ees

timat

edm

odel

.The

sam

ple

peri

odfo

rth

est

ock

retu

rnis

Q1.

2006

–Q1.

2009

.All

cont

rolv

aria

bles

are

lagg

ed1

year

.Cri

sis

isa

dum

my

vari

able

that

take

sva

lue

1fr

omQ

3.20

07to

Q1.

2009

.Tie

r1

(Tie

r2)

isT

ier

1(T

ier2

)cap

itals

cale

dei

ther

byri

sk-w

eigh

ted

asse

ts(R

WR

)ort

otal

unw

eigh

ted

asse

ts(L

R).

Tie

r1ca

pita

linc

lude

ssh

areh

olde

rfun

dspl

uspe

rpet

ual,

nonc

umul

ativ

epr

efer

ence

shar

es,p

lus

reta

ined

earn

ings

.Tie

r2ca

pita

lin

clud

essu

bord

inat

edde

bt,h

ybri

dca

pita

l,lo

anlo

ssre

serv

es,a

ndva

luat

ion

rese

rves

.Tan

gibl

eco

mm

oneq

uity

issh

areh

olde

rsfu

ndm

inus

inta

ngib

leca

pita

ldi

vide

dby

tota

lta

ngib

leas

sets

.We

repo

rtes

timat

esfo

rth

ew

hole

sam

ple

and

the

sam

ple

ofla

rge

bank

s.L

arge

bank

sar

ede

fined

asba

nks

with

tota

lass

ets

abov

eU

S$50

billi

on.S

tand

ard

erro

rscl

uste

red

byba

nkar

ere

port

edin

brac

kets

and

the

p-va

lues

for

the

test

ofsi

gnifi

cant

diff

eren

cebe

twee

nth

epr

ecri

sis

and

cris

isco

effic

ient

sar

ere

port

edin

pare

nthe

ses.

*,**

,and

***

stan

dfo

rst

atis

tical

lysi

gnifi

cant

atth

e10

%,5

%,a

nd1%

leve

l,re

spec

tivel

y.R

obus

tsta

ndar

der

rors

clus

tere

dby

bank

are

repo

rted

inbr

acke

ts.

ASLI DEMIRGUC-KUNT, ENRICA DETRAGIACHE, AND OUARDA MERROUCHE : 1159-1

01

2-1

01

2

20

06

q2

20

06

q3

20

06

q4

20

07

q1

20

07

q2

20

07

q3

20

07

q4

20

08

q1

20

08

q2

20

08

q3

20

08

q4

20

06

q2

20

06

q3

20

06

q4

20

07

q1

20

07

q2

20

07

q3

20

07

q4

20

08

q1

20

08

q2

20

08

q3

20

08

q4

LR Full sample LR Large banks

RWR Full sample RWR Large banks

Graphs by Type

FIG. 1. Response of Bank Stock Returns to Lagged Bank Capital before and during the Financial Crisis.

The strongest effect is for the leverage ratio during the period Q4.2007–Q2.2008 inthe sample of large banks.

In Table 4 we estimate a slightly different version of the baseline regressions as arobustness test. Instead of carrying out the estimation for the full sample period andtwo separate samples (all banks and large banks), we estimate the model separatelyfor the precrisis and crisis periods, and interact the coefficients of the explanatoryvariables with a large-bank dummy and a small-bank dummy (with the dummyswitching value for banks with asset size above $50 billion). In an additional exercise,we run a regression for the period following the Lehman bankruptcy only, to testwhether the effect of capital on stock returns differed during the most acute phase ofthe financial crisis. The results tend to confirm our earlier findings: capital becomesmore important during the crisis, and the strongest effect is that of the Tier 1 leverageratio on stock returns of large banks. During the post-Lehman quarter, the coefficientof Tier 1 leverage for large banks is larger than in the full crisis period, suggestingthat capital was affecting stock returns particularly strongly during this period.

1160 : MONEY, CREDIT AND BANKING

TABLE 4

STOCK MARKET PERFORMANCE AND BANK LEVERAGE: SEPARATE PRECRISIS AND CRISIS REGRESSIONS

Precrisis Crisis Post-Lehman

RWR LR RWR LR RWR LR(1) (2) (3) (4) (5) (6)

Tier 1*Large − 0.034 0.088 0.165 0.536*** 0.123 0.720**[0.090] [0.093] [0.154] [0.181] [0.257] [0.323]

Tier 1*Small 0.036 0.036 0.08 0.151 0.033 0.141[0.045] [0.066] [0.114] [0.148] [0.158] [0.214]

Tier 2*Large 0.039 − 0.053 0.103 0.357 0.008 0.269[0.101] [0.158] [0.189] [0.283] [0.295] [0.388]

Tier 2*Small 0.08 − 0.052 0.049 0.161 − 0.126 0.28[0.060] [0.076] [0.130] [0.214] [0.248] [0.369]

Controls*Large Yes Yes Yes Yes Yes YesControls*Small Yes Yes Yes Yes Yes YesCountry*Year FE Yes Yes Yes Yes Yes YesNumber of observations 1,820 1,650 2,229 2,076 949 897R2 0.23 0.23 0.15 0.16 0.22 0.23

NOTES: The dependent variable is quarterly bank stock returns. The stock return (including dividends) is calculated as ln(RI(t)/RI(t – 1)),where RI is the Datastream total return index. See Table 2 for a detailed description of the estimated model. In this table report estimates forthree separate sample period: (i) the precrisis period Q1.2006–Q2.2007; (ii) the crisis period Q3.2007–Q1.2009; and (iii) the period followingLehman bankruptcy Q3.2008–Q1.2009. We also allow all coefficients to vary by bank size. Large is a dummy variable that takes value 1 ifthe bank has total assets above U.S. $50 billion and small a dummy that takes value one for all other banks. Tier 1 (Tier 2) is Tier 1 (Tier 2)capital scaled either by risk-weighted assets (RWR) or total unweighted assets (LR). Tier 1 capital includes shareholder funds plus perpetual,noncumulative preference shares, plus retained earnings. Tier 2 capital includes subordinated debt, hybrid capital, loan loss reserves, andvaluation reserves. Standard errors clustered by bank are reported in brackets. *, **, and *** stand for statistically significant at the 10%, 5%,and 1% level, respectively. Robust standard errors clustered by bank reported in brackets.

We conducted a battery of robustness checks, which we do not report for sakeof brevity.12 These tests include: an alternative definition of large banks based onoperating income; an alternative specification in which capital is measured by theleverage ratio and the ratio of risk-adjusted assets to total assets is introduced asan additional regressor; alternative estimation techniques;13 alternative measures ofliquidity; including a measure of lagged profitability (return on assets); an alterna-tive sample including countries with less than five banks (but at least two banks);alternative specifications in which we control for either market to book ratio or priceearnings ratio, but not both;14 and a specification where we include a dummy variablethat takes the value of 1 if a bank has been recapitalized with government funds in agiven quarter. Our findings are robust to all these tests.

2.2 Why Does Capital Affect Stock Returns Only among Large Banks?

These results raise the question of why the leverage ratio matters for equity pricesespecially in the sample of larger banks. One possible interpretation is that larger

12. All these results are available upon request.13. We used weighted least squares to address possible problems with the sample composition being

uneven. We also clustered standard errors by country rather than bank, by quarter, and by both countryand quarter; baseline results were not changed.

14. Fama and French (1996) showed that market to book value and price earnings ratio may containsimilar information about expected stock returns.

ASLI DEMIRGUC-KUNT, ENRICA DETRAGIACHE, AND OUARDA MERROUCHE : 1161

TABLE 5

SAMPLE SPLIT BY INITIAL CAPITAL LEVELS

High capital in 2006 Low capital in 2006

RWR LR RWR LR(1) (2) (3) (4)

Tier 1*PreCrisis − 0.006 0.111 0.294* 0.180[0.079] [0.125] [0.162] [0.126]

Tier 2*PreCrisis 0.12 − 0.044 0.177 0.061[0.105] [0.123] [0.137] [0.134]

Tier 1*Crisis 0.018 − 0.048 0.496*** 0.498**[0.108] [0.163] [0.182] [0.198](0.792) (0.126) (0.092) (0.054)

Tier 2*Crisis − 0.023 − 0.455* 0.390* 0.579*[0.187] [0.268] [0.204] [0.316](0.432) (0.129) (0.210) (0.160)

Controls*Crisis Yes Yes Yes YesControls*PreCrisis Yes Yes Yes YesCountry*Year FE Yes Yes Yes YesNumber of observations 1,857 1,795 2,192 1,931R2 0.26 0.26 0.22 0.23

NOTES: The dependent variable is the quarterly stock return. The stock return (including dividends) is calculated as ln(RI(t)/RI(t − 1)), whereRI is the Datastream total return index. See Table 2 for a detailed description of the estimated model. The sample period for the stock return isQ1.2006–Q1.2009. All control variables are lagged 1 year. Crisis is a dummy that takes value one from Q3.2007 to Q1.2009. Tier 1 (Tier 2) isTier 1 (Tier 2) capital scaled either by risk-weighted assets (RWR) or total unweighted assets (LR). Tier 1 capital includes shareholder fundsplus perpetual, noncumulative preference shares, plus retained earnings. Tier 2 capital includes subordinated debt, hybrid capital, loan lossreserves, and valuation reserves. Common equity is shareholders fund and other capital total regulatory capital minus common equity. RWRstands for risk-weighted capital ratio and LR for leverage ratio. In this table we report separate estimates for the subsamples of initially welland poorly capitalized banks. The high capital subsample includes banks with capital above the sample median in 2006, while the low capitalsample includes banks with capital below the sample median in 2006. In order to keep a reasonable number of countries in each subsample(at least 7 countries) we lower our threshold number of banks by country to 3 banks that is we obtain samples with at least 48 observationsper country (12 observations per year). Standard errors clustered by bank are reported in brackets and the p-values for the test of significantdifference between the precrisis and crisis coefficients are reported in parentheses. *, **, and *** stand for statistically significant at the 10%,5%, and 1% level, respectively. Robust standard errors clustered by bank are reported in brackets. In parentheses we report the p-values forthe test of equality of effects during crisis and precrisis.

banks with complex operations have more opportunities to take advantage of “regu-latory arbitrage” and distort the risk exposure measure used by regulators to computecapital adequacy. Also, capital’s role as a signal of a bank’s exposure to toxic assetsmay have been more important in the case of large banks, whose balance sheets aremore opaque than those of small banks.

Another interpretation is based on the Calem–Rob model. If we measure capi-talization based on “high-quality” capital such as the Tier 1 ratio or the tangiblecommon equity ratio, the larger banks in our sample were less well capitalized thanthe smaller banks, as pointed out in the previous section.15 The Calem–Rob modelpredicts that at low levels of capitalization, bank risk taking is a decreasing functionof capital, while for strongly capitalized banks the relationship has the opposite sign.If we take the size of the decline in stock prices during the crisis as a measure of themarket’s view of how much risk a bank had taken during the good times, then theCaleb–Rob model would predict a positive relationship between capital and stock

15. For instance, the median common equity ratio is 6.2% in the full sample but only 4.1% in thelarge-bank sample.

1162 : MONEY, CREDIT AND BANKING

returns for less well capitalized banks but not for better capitalized banks, which iswhat we find.

To explore this interpretation further, in Table 5 we rerun the baseline regressionssplitting the sample based on the level of capitalization at the end of 2006. Interest-ingly, for banks with capital above the median, higher capital did not translate intobetter stock performance during the crisis. On the other hand, for less well capitalizedbanks, higher capital did result in a higher stock returns during the crisis. For thissample split, we do not see a distinction between the Basel ratio and the leverage ratioor between Tier 1 and Tier 2 capital. All in all, these findings are consistent with theimplications of the Caleb–Rob model, namely, that a negative relationship betweenrisk and capital should appear only for weakly capitalized banks.

3. CONCLUSIONS

The recent global financial crisis has led to widespread calls to reform bankregulation and supervision. Changes in bank capital regulation have been at the heartof the policy discussions. In redesigning prudential standards to incorporate lessonsfrom the recent turmoil, the Basel committee of supervisors has grappled with twoimportant questions among others: What type of capital should banks hold to ensurethat they can better withstand periods of economic and financial stress? And shoulda simple leverage ratio be introduced to reduce regulatory arbitrage and improvetransparency?

We find that before the crisis, differences in initial capital—whether risk adjustedor not, however defined—did not consistently affect subsequent bank stock returns.The importance of capital, on the other hand, becomes evident during the crisisperiod, particularly for the largest banks in our sample. These are the banks of greatersystemic importance, as well as those holding lesser quality capital at the inceptionof the crisis. Our results also show that during the crisis stock returns of large bankswere more sensitive to the leverage ratio than the risk-adjusted capital ratio. Thismay be because market participants viewed the risk adjustment under Basel rulesas subject to manipulation or in any case not reflective of true risk in the case oflarge banks. Finally, we also find that the positive association with subsequent stockreturns is stronger for higher quality capital (Tier 1 leverage and tangible commonequity).

Our results have potential policy implications for the current process of regulatoryreform. First, we find support for the view that a stronger capital position is animportant asset during a systemic crisis, suggesting that the current emphasis onstrengthening capital requirements is broadly appropriate. Second, our results indicatethat the introduction of a minimum leverage ratio to supplement minimum risk-adjusted capital requirements is important, as properly measuring risk exposure isvery difficult especially for large and complex financial organizations. Finally, ourstudy indicates that greater emphasis on “higher quality capital” in the form of Tier1 capital or tangible equity is justified.

ASLI DEMIRGUC-KUNT, ENRICA DETRAGIACHE, AND OUARDA MERROUCHE : 1163

LITERATURE CITED

Basel Committee on Banking Supervision. (2009) “Consultative Proposals to Strengthen theResilience of the Banking Sector.” Bank of International Settlements, http://www.bis.org/press/p091217.htm.

Berger, Allen N., and Christa H.S. Bouwman. (2009) “Bank Capital, Performance, and Survivalaround Financial Crises.” Unpublished manuscript.

Blum, M. Jurg. (2007) “Why Basel II May Need a Leverage Ratio Restriction.” Swiss NationalBank Working Paper 2007–4.

Calem, Paul, and Rafael Rob. (1999) “The Impact of Capital-Based Regulation on BankRisk-Taking.” Journal of Financial Intermediation, 8, 317–52.

Caprio, Gerard, and Patrick Honohan. (1999) “Beyond Capital Ideas: Restoring BankingStability.” World Bank Policy Research Working Paper No. 2235.

Caprio, Gerard, Asli Demirguc-Kunt, and Edward Kane. (2010) “The 2007 Meltdown in Struc-tured Securitization: Searching for Lessons, Not Scapegoats.” The World Bank ResearchObserver, 25, 125–55.

Demirguc-Kunt, Asli, and Luis Serven. (2010) “Are All Sacred Cows Dead? Implications ofthe Financial Crisis for Macro and Financial Policies.” The World Bank Research Observer,25, 91–124.

Diamond, Douglas W., and Raghuram Rajan. (2000) “A Theory of Bank Capital.” Journal ofFinance, 55, 2431–65.

Drukker, David M. (2003) “Testing for Serial Correlation in Linear Panel Data Models.” StataJournal, 2, 168–77.

Estrella, Arturo, Sangkyun Park, and Stavros Peristiani. (2000) “Capital Ratios as Predictorsof Bank Failure.” Economic Policy Review, Federal Reserve Bank of New York, July, 33–52.

Fama, Eugene F., and Kenneth R. French. (1996) “Multifactor Explanations of Asset PricingAnomalies.” Journal of Finance, 51, 55–84.

Financial Stability Institute. (2010) “Survey on the Implementation of the New Capital Ade-quacy Framework.” Occasional Paper No. 9.

Furlong, Frederick, and Michael Keeley. (1989) “Capital Regulation and Bank Risk-Taking:A Note.” Journal of Banking and Finance, 13, 883–91.

Furlong, Frederick, and Michael Keeley. (1990) “A Re-examination of the Mean-VarianceAnalysis of Bank Capital Regulation.” Journal of Banking and Finance, 15, 69–84.

Hellwig, Martin. (2010) “Capital Regulation after the Crisis: Business as Usual?” Max PlanckInstitute Working Paper.

Kim, Daesik, and Anthony Santomero. (1988) “Risk in Banking and Capital Regulation.”Journal of Finance, 43, 1219–33.

Koehn, Michael, and Anthony M. Santomero. (1980) “Regulation of Bank Capital and PortfolioRisk.” Journal of Finance, 35, 1235–44.

Merrouche, Ouarda, and Erland Nier. (2010) “What Caused the Global Financial Cri-sis? Evidence on Drivers of Financial Imbalances 1999–2007.” IMF Working Paper10/265.

Rochet, Jean-Charles. (1992) “Capital Requirements and the Behaviour of Commercial banks.”European Economic Review, 36, 1137–78.

1164 : MONEY, CREDIT AND BANKING

Santos, Joao A.C. (2001) “Bank Capital Regulation in Contemporary Banking Theory: AReview of the Literature.” Financial Markets, Institutions, and Instruments, 10, 41–84.

Tong, Hui, and Shang-Jin Wei. (2010) “The Composition Matters: Capital Inflows and LiquidityCrunch during a Global Economic Crisis.” Review of Financial Studies, 24, 2023–52.

Vinals, Jose, Jonathan Fiechter, Ceyla Pazarbasioglu, Laura Kodres, Aditya Narain, and MarinaMoretti. (2010) “Shaping the New Financial System.” IMF Staff Position Note, 10/15.

Whited, Toni M., and Guojun Wu. (2006) “Financial Constraints Risk.” Review of FinancialStudies, 19, 531–59.