Embed Size (px)

Citation preview

Bank and Capital MarketsNew Issue Review

28 July – 1 Aug 2014, week 30

Capital & Debt Advisory

ContentsSection 1 Market backdrop 2

Section 2 Bank loan market 3

Section 3 USD public bond market 7

Section 4 GBP public bond market 9

Section 5 EUR public bond market 11

Section 6 US Private Placement market 12

ContactsUnited KingdomLuke ReeveTel: +44 20 7951 6548Email: [email protected]

Chris LoweTel: +44 20 7951 0826Email: [email protected]

Gary DavisonTel: +44 161 333 2767Email: [email protected]

EuropeOlivier CatonnetTel: +33 1 5561 0535Email: [email protected]

Jonathan H.M. HarfieldTel: +420 731 627 155Email: [email protected]

Britta BeckerTel: +49 40 36132 20781Email: [email protected]

AsiaGaurav AhujaTel: +65 6309 8276Email: [email protected]

US & CanadaK.C. BrechnitzTel: +1 704 335 4211Email: [email protected]

Tony IanniTel: +1 416 943 3476Email: [email protected]

AustraliaSebastian PaphitisTel: +61 2 9248 4773Email: [email protected]

Jason LoweTel: +61 3 8650 7600Email: [email protected]

Section 7 Credit ratings 14

Section 8 Glossary 15

@EY_UKI

EY Capital and Debt Advisory - New Issue Review 2

Market backdropSlowing growth in the UK economy however outlook remains positive

► Disappointing economic data in the UK was released during the week, in contrast to the more positivedata noted throughout the past 12 to 18 months. The UK economy has outgrown the majority of itspeers over recent times and even following this latest release of data, performance remains above that ofmost of the G7 advanced economies. A senior economic adviser to the EY Item Club suggested slowergrowth would mean “less chance of the economy running into bottlenecks, and will aid the sustainabilityof the expansion”.

► UK manufacturing growth slowed in July, with the Markit purchasing managers’ index falling from 57.2in June to 55.4 in July. Although this is the lowest value in the past 12 months, it is still well above 50which illustrates an expansion in activity. The PMI release did highlight positive news in that job creation,output and new orders all increased in July, however at a slower pace than the first half of 2014.

► The EU and US presented a more united front this week, agreeing to more stringent sanctions againstRussia. The EU imposed restrictions on Russia’s largest state owned banks from issuing stocks or bondsin European markets. These sanctions are targeting Russia’s financial, energy and defence sectors.Similar restrictions were announced by the US, with President Obama suggesting these sanctions havealready “made a weak Russian economy even weaker”. The EU measures includes a complete armsembargo however certain carve outs are included for existing contracts. The impact of these sanctions isalready taking effect, with BP, the UK oil giant, that owns a fifth of Rosneft, the oil group controlled bythe Russian government, likely to be affected by the restrictions.

► Argentina suffered their second default in 13 years on Wednesday as credit ratings agency S&P placedthe sovereign’s bonds into “selective default”. Argentina missed the Wednesday deadline to pay US$539million of interest. Yields on Argentinian government dollar denominated bonds, maturing in 2033, rosefollowing the announcement from 8.8 per cent to 9.7 per cent on Thursday morning, however thisremains below the 12 per cent reached in June.

Section 1: Market backdrop

Tenor 3yr 5yr 7yr 10yr 30yr

UK swap rate 1.69 2.13 2.40 2.67 3.07

Gilt rate 1.16 1.94 2.24 2.55 3.24

Tenor 3yr 5yr 7yr 10yr 30yr

US swap rate 1.13 1.81 2.23 2.63 3.26

UST rate 0.92 1.67 2.15 2.49 3.28

Source: Bloomberg

Source: Bloomberg Source: Bloomberg

Source: Bloomberg

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2014 2016 2018 2020 2022 2024

Rat

e(%

)

3 month UK LIBOR forward rates

Current forward 3m UK LIBOR (-1 wk) fwd 3m UK LIBOR

2yr

3yr 4yr

5yr7yr

10yr

(5)

(4)

(3)

(2)

(1)

0

1

Rat

e(b

ps)

Weekly change in UK SWAP

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Yie

ld(%

)

10-year Benchmark yields

10yr UST 10yr Gilt 10yr Bund

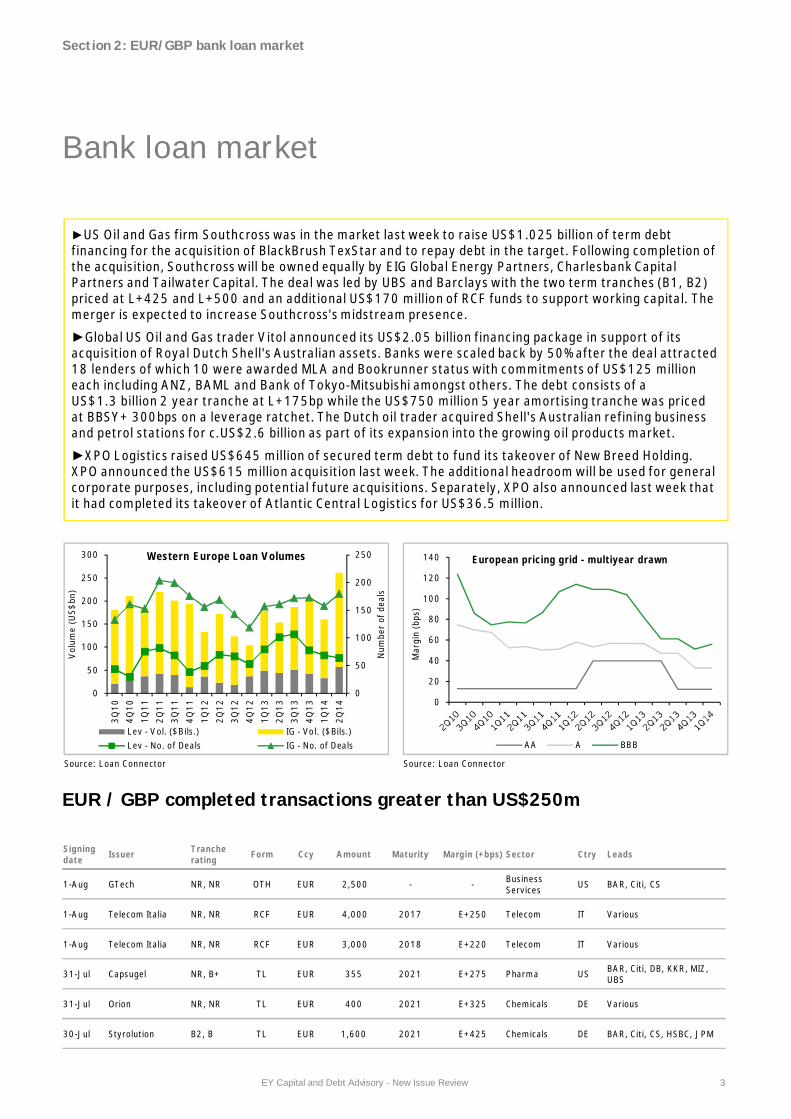

Bank loan market

EUR / GBP completed transactions greater than US$250m

EY Capital and Debt Advisory - New Issue Review 3

►US Oil and Gas firm Southcross was in the market last week to raise US$1.025 billion of term debtfinancing for the acquisition of BlackBrush TexStar and to repay debt in the target. Following completion ofthe acquisition, Southcross will be owned equally by EIG Global Energy Partners, Charlesbank CapitalPartners and Tailwater Capital. The deal was led by UBS and Barclays with the two term tranches (B1, B2)priced at L+425 and L+500 and an additional US$170 million of RCF funds to support working capital. Themerger is expected to increase Southcross's midstream presence.

►Global US Oil and Gas trader Vitol announced its US$2.05 billion financing package in support of itsacquisition of Royal Dutch Shell's Australian assets. Banks were scaled back by 50% after the deal attracted18 lenders of which 10 were awarded MLA and Bookrunner status with commitments of US$125 millioneach including ANZ, BAML and Bank of Tokyo-Mitsubishi amongst others. The debt consists of aUS$1.3 billion 2 year tranche at L+175bp while the US$750 million 5 year amortising tranche was pricedat BBSY+ 300bps on a leverage ratchet. The Dutch oil trader acquired Shell's Australian refining businessand petrol stations for c.US$2.6 billion as part of its expansion into the growing oil products market.

►XPO Logistics raised US$645 million of secured term debt to fund its takeover of New Breed Holding.XPO announced the US$615 million acquisition last week. The additional headroom will be used for generalcorporate purposes, including potential future acquisitions. Separately, XPO also announced last week thatit had completed its takeover of Atlantic Central Logistics for US$36.5 million.

Section 2: EUR/GBP bank loan market

Source: Loan Connector Source: Loan Connector

0

20

40

60

80

100

120

140

Mar

gin

(bps

)

European pricing grid - multiyear drawn

AA A BBB

0

50

100

150

200

250

0

50

100

150

200

250

300

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

Num

ber

ofde

als

Vol

ume

(US$

bn)

Western Europe Loan Volumes

Lev - Vol. ($Bils.) IG - Vol. ($Bils.)Lev - No. of Deals IG - No. of Deals

Signingdate Issuer Tranche

rating Form Ccy Amount Maturity Margin (+bps) Sector Ctry Leads

1-Aug GTech NR, NR OTH EUR 2,500 - - BusinessServices US BAR, Citi, CS

1-Aug Telecom Italia NR, NR RCF EUR 4,000 2017 E+250 Telecom IT Various

1-Aug Telecom Italia NR, NR RCF EUR 3,000 2018 E+220 Telecom IT Various

31-Jul Capsugel NR, B+ TL EUR 355 2021 E+275 Pharma US BAR, Citi, DB, KKR, MIZ,UBS

31-Jul Orion NR, NR TL EUR 400 2021 E+325 Chemicals DE Various

30-Jul Styrolution B2, B TL EUR 1,600 2021 E+425 Chemicals DE BAR, Citi, CS, HSBC, JPM

Bank loan marketEUR / GBP completed transactions greater than US$250m (cont.)

EY Capital and Debt Advisory - New Issue Review 4

Section 2: Bank loan market

Signingdate Issuer Tranche

rating Form Ccy Amount Maturity Margin (+bps) Sector Ctry Leads

29-Jul Endemol NR, B RCF EUR 65 - - Media NL CS, DB, JPM, NOM

29-Jul Endemol NR, B TL EUR 700 2021 L+525 Media NL CS, DB, JPM, NOM

29-Jul Endemol NR, CCC+ TL EUR 335 2022 L+875 Media NL CS, DB, JPM, NOM

29-Jul Legrand NR, NR RCF EUR 900 2021 - Manufacturing FR BNP, CM-CIC, CA, NAT,RBS, SG

29-Jul Springer B2, B TL EUR 250 2020 E+375 Media DE GS, JPM

29-Jul Springer B2, B TL EUR 606 2020 E+375 Media DE BAR, CS, GS, JPM, NOM,UBS

29-Jul Telefonica NR, NR TL EUR 700 2017 E+200 Telecom ES Various

29-Jul Telefonica NR, NR TL EUR 700 2018 E+210 Telecom ES Various

28-Jul Amaya Caa1, BB TL EUR 200 - L+425 Leisure CA BAR, DB, Macquarie

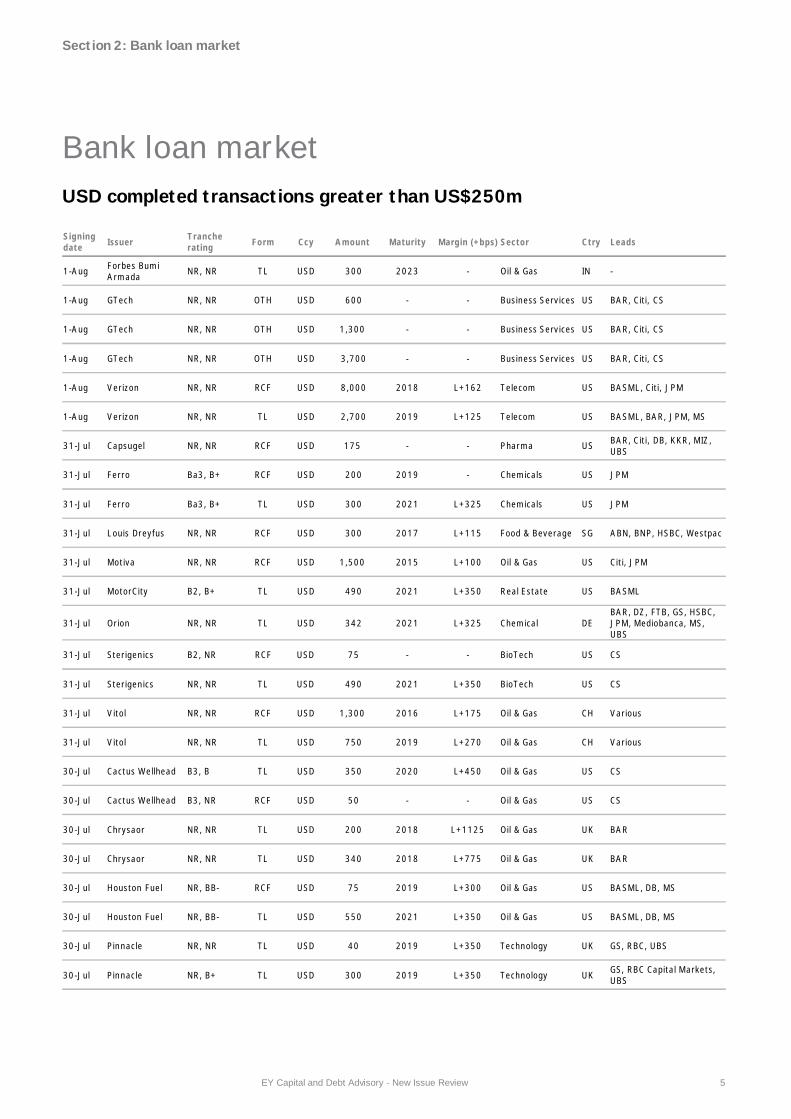

Bank loan marketUSD completed transactions greater than US$250m

EY Capital and Debt Advisory - New Issue Review 5

Section 2: Bank loan market

Signingdate Issuer Tranche

rating Form Ccy Amount Maturity Margin (+bps) Sector Ctry Leads

1-Aug Forbes BumiArmada NR, NR TL USD 300 2023 - Oil & Gas IN -

1-Aug GTech NR, NR OTH USD 600 - - Business Services US BAR, Citi, CS

1-Aug GTech NR, NR OTH USD 1,300 - - Business Services US BAR, Citi, CS

1-Aug GTech NR, NR OTH USD 3,700 - - Business Services US BAR, Citi, CS

1-Aug Verizon NR, NR RCF USD 8,000 2018 L+162 Telecom US BASML, Citi, JPM

1-Aug Verizon NR, NR TL USD 2,700 2019 L+125 Telecom US BASML, BAR, JPM, MS

31-Jul Capsugel NR, NR RCF USD 175 - - Pharma US BAR, Citi, DB, KKR, MIZ,UBS

31-Jul Ferro Ba3, B+ RCF USD 200 2019 - Chemicals US JPM

31-Jul Ferro Ba3, B+ TL USD 300 2021 L+325 Chemicals US JPM

31-Jul Louis Dreyfus NR, NR RCF USD 300 2017 L+115 Food & Beverage SG ABN, BNP, HSBC, Westpac

31-Jul Motiva NR, NR RCF USD 1,500 2015 L+100 Oil & Gas US Citi, JPM

31-Jul MotorCity B2, B+ TL USD 490 2021 L+350 Real Estate US BASML

31-Jul Orion NR, NR TL USD 342 2021 L+325 Chemical DEBAR, DZ, FTB, GS, HSBC,JPM, Mediobanca, MS,UBS

31-Jul Sterigenics B2, NR RCF USD 75 - - BioTech US CS

31-Jul Sterigenics NR, NR TL USD 490 2021 L+350 BioTech US CS

31-Jul Vitol NR, NR RCF USD 1,300 2016 L+175 Oil & Gas CH Various

31-Jul Vitol NR, NR TL USD 750 2019 L+270 Oil & Gas CH Various

30-Jul Cactus Wellhead B3, B TL USD 350 2020 L+450 Oil & Gas US CS

30-Jul Cactus Wellhead B3, NR RCF USD 50 - - Oil & Gas US CS

30-Jul Chrysaor NR, NR TL USD 200 2018 L+1125 Oil & Gas UK BAR

30-Jul Chrysaor NR, NR TL USD 340 2018 L+775 Oil & Gas UK BAR

30-Jul Houston Fuel NR, BB- RCF USD 75 2019 L+300 Oil & Gas US BASML, DB, MS

30-Jul Houston Fuel NR, BB- TL USD 550 2021 L+350 Oil & Gas US BASML, DB, MS

30-Jul Pinnacle NR, NR TL USD 40 2019 L+350 Technology UK GS, RBC, UBS

30-Jul Pinnacle NR, B+ TL USD 300 2019 L+350 Technology UK GS, RBC Capital Markets,UBS

Bank loan marketUSD completed transactions greater than US$250m (cont.)

EY Capital and Debt Advisory - New Issue Review 6

Section 2: Bank loan market

Signingdate Issuer Tranche

rating Form Ccy Amount Maturity Margin (+bps) Sector Ctry Leads

30-Jul Reynolds NR, NR OTH USD 9,000 2015 L+150 Food & Beverage US Citi, JPM

30-Jul Sterigenics B2, NR TL USD 490 2021 L+350 BioTech US CS

29-Jul ALM NR, B+ RCF USD 23 2020 - Media US Macquarie

29-Jul ALM NR, B+ TL USD 215 2020 L+450 Media US Macquarie

29-Jul ALM NR, CCC+ TL USD 50 2021 L+800 Media US Macquarie

29-Jul Chief Exploration NR, NR TL USD 350 - - Oil & Gas US -

29-Jul Mallinckrodt Ba2, BB+ TL USD 700 2021 L+300 Pharma IE BAR, Citi, DB, Wells

29-Jul Orbotech NR, B+ TL USD 300 2020 L+375 Technology US JPM

29-Jul Southcross NR, NR RCF USD 50 - - Oil & Gas US BAR, UBS

29-Jul Southcross NR, NR RCF USD 120 - - Oil & Gas US Wells

29-Jul Southcross B1, NR TL USD 450 - L+425 Oil & Gas US Wells

29-Jul Southcross B2, NR TL USD 575 2021 L+500 Oil & Gas US BAR, UBS

29-Jul Springer B2, B TL USD 1,250 2020 L+375 Media DE BAR, CS, GS, JPM, NOM,UBS

29-Jul United Site B1, B RCF USD 50 - - Business Services US GE

29-Jul United Site B1, B TL USD 40 - L+425 Business Services US GE

29-Jul United Site B1, B TL USD 175 - L+425 Business Services US GE

29-Jul XPO NR, NR TL USD 645 - - Transport US Citi, CS, DB, MS

28-Jul Amaya B1, BB RCF USD 100 2019 - Leisure CA BAR, DB, Macquarie

28-Jul Amaya B1, BB TL USD 1,750 2021 L+400 Leisure CA BAR, DB, Macquarie

28-Jul Amaya NR, B TL USD 800 2022 L+700 Leisure CA BAR, DB, Macquarie

28-Jul inVentiv B2, B- TL USD 446 2018 L+625 BioTech US Citi

28-Jul MD America Caa2, CCC+ TL USD 525 2019 L+850 Oil & Gas US BASML

USD public bond market

EY Capital and Debt Advisory - New Issue Review 7

► Monthly issuance volumes in the USD bond market slumped to a three-year low in July, with a markedreduction in both domestic and cross-border names coming to the market. Activity was clustered early inthe week, ahead of a broad sell-off in high-yield credit towards the end of the week.

► Many investors cited the combination of geopolitical uncertainty, earnings blackout periods and a wait onlatest economic data as convincing many issuers to hold off new issuance. Latest developments inArgentina and a raft of weak earnings results from US corporates are likely to ensure that August seesonly modest issuance volumes, ahead of the traditional pick-up in market activity in September.

► Air Products & Chemicals (A2, A, NR) priced US$400 million of 10-year notes flat to initial guidance ofT+90bps, with a coupon of 3.4%, and was seen marginally wider in secondary trading at the end of theweek.

► Tyco Electronics Group (Baa1, A-, A-) attracted an order book in excess of US$5 billion to price an18-month US$500 million floater at L+20bps alongside US$250 million 5-year and US$250 million 10-year bonds priced at T+65bps and T+100bps respectively; some 20-25bps inside initial price guidance

Domestic

Section 3: USD public bond market

Source: Reuters Source: Reuters

0

50

100

150

200

250

Spre

ad(b

ps)

USD secondary public bond spread 10-year

Avg. AA USD 10yr spreads Avg. A USD 10yr spreads

Avg. BBB USD 10yr spreads

0

50

100

150

200

0

20

40

60

80

100

Num

ber

issu

ed

Vol

ume

(US$

bn)

Monthy US$ bond volumes

Domestic volume (US$) Cross-border volume (US$)Cross-border number issued Domestic number issued

Signingdate Issuer Tranche rating

(M,S&P,F) Form Amount(US$m) Coupon Maturity Spread

(T+bps) Sector Ctry Leads

31-Jul CDW B3, B, NR SN 600 6.000% 2022 +363 Business Services US MS, BAR

31-Jul WLH PNW B3, B-, NR SN 300 7.000% 2022 +462 Real Estate US JPM, Citi, CS

30-Jul Kilroy Baa3, BBB-, NR SN 400 4.250% 2029 +180 Real Estate US Wells, BASML, JPM

30-Jul PaperWorks B3, B-, NR SSN 275 9.500% 2019 - Paper US Jefferies, Macquarie

29-Jul Compressco B2, B, NR SN 350 7.250% 2022 +522 Oil & Gas US BASML, BAR, CS, JPM,RBC, Wells

29-Jul CONSOL B1, BB, NR SN 1,850 5.875% 2022 +341 Oil & Gas US GS

29-Jul EQT Midstream Ba1, BBB-, BBB- SN 500 4.000% 2024 +160 Oil & Gas US DB, GS, JPM, MIS, BNP,SunTrust, US Bancorp

29-Jul Level 3 B3, B, BB SN 1,000 5.375% 2022 +324 Telecom US Citi, BASML, MS, BAR,GS, Jefferies, JPM

29-Jul Universal Health Ba1, BB+, BBB- SSN 300 3.750% 2019 +206 Healthcare US Various

29-Jul Universal Health Ba1, BB+, BBB- SSN 300 4.750% 2022 +247 Healthcare US Various

USD public bond market

EY Capital and Debt Advisory - New Issue Review 8

Section 3: USD public bond market

Domestic (cont.)

Cross-border

Signingdate Issuer Tranche rating

(M,S&P,F) Form Amount(US$m) Coupon Maturity Spread

(T+bps) Sector Ctry Leads

28-Jul Air Products A2, A, NR SN 400 3.350% 2024 +90 Industrial US BAR, RBS, Wells

28-Jul Harland Clarke Caa1, B-, NR SN 715 9.250% 2021 +704 Business Services US CS, BASML

28-Jul NRG Yield Ba1, BB+, NR SN 500 5.375% 2024 - Utilities US BASML, Citi, GS, RBC

28-Jul United Airlines NR, BB+, BB+ OTH 238 4.625% 2022 - Aviation US CS, MS, DB, GS, Citi, BAR,BNP, CA

28-Jul United Airlines NR, A-, A OTH 823 3.750% 2026 +125 Aviation US CS, MS, DB, GS, Citi, BAR,BNP, CA

Signingdate Issuer Tranche rating

(M,S&P,F) Form Amount(US$m) Coupon Maturity Spread

(T+bps) Sector Ctry Leads

1-Aug Greeland HongKong Ba1, BB+, BBB- SN 500 4.375% 2017 - Real Estate CN CS, HSBC, MS, BOC, JPM

1-Aug Jingrui B3, NR, B SN 150 13.625% 2019 - Real Estate CN HIC, UBS, BOC, CLSA,Guotai Junan

31-Jul HudBay B3, B-, NR SN 170 9.500% 2020 - Metal & Mining CA RBC

30-Jul KWG B1, B+, NR SN 400 8.250% 2019 - Real Estate CN GS, HSBC, MS, STA, UBS

30-Jul Mallinckrodt B2, B, NR SN 900 5.750% 2022 - Pharma IE BAR, DB, Citi, Wells

29-Jul Olam NR, NR, NR SN 300 4.500% 2020 +295 Food & Beverage SG ANZ, BAR, JPM, STA

28-Jul Tyco Baa1, A-, A- SN 250 Float 2016 - Manufacturing CH Citi, JPM, BASML, BNP,DB

28-Jul Tyco Baa1, A-, A- SN 250 2.350% 2019 +65 Manufacturing CH Citi, JPM, BASML, BNP,DB

28-Jul Tyco Baa1, A-, A- SN 250 3.450% 2024 +100 Manufacturing CH Citi, JPM, BASML, BNP,DB

GBP public bond market

EY Capital and Debt Advisory - New Issue Review 9

► It was a quiet week for Sterling investors, with no significant corporate issuance to report. With limitednames currently in the pipeline, it is anticipated the Sterling market will have a quiet August beforerenewed activity as participants return from summer holidays in September.

Section 4: GBP public bond market

Domestic

Cross-border

Signingdate Issuer Tranche rating

(M,S&P,F) Form Amount(GBPm) Coupon Maturity Spread

(G+bps) Sector Ctry Leads

No significant issuance in the week

Signingdate Issuer Tranche rating

(M,S&P,F) Form Amount(GBPm) Coupon Maturity Spread

(G+bps) Sector Ctry Leads

31-Ju; Grainger NR, NR , NR SSN 75 5.000% 2020 - Real Estate UK SANT, BAR, HSBC, LBG,RBS

Source: Reuters Source: Reuters

0

50

100

150

200

Spre

ad(b

ps)

GBP secondary public bond spread 10-year

Avg. AA GBP 10yr spreads Avg. A GBP 10yr spreads

Avg. BBB GBP 10yr spreads

0

1

2

3

4

5

6

7

01122334455

Num

ber

issu

ed

Vol

ume

(GBP

m)

Monthy GBP bond volumes

Volume (GBP) Number issued

ORB retail bond market

EY Capital and Debt Advisory - New Issue Review 10

In the market

Recent Issues

Date Issuer Ratings (M,S&P,F) Form Amount(GBPm) Coupon Maturity Sector Country

15-Jul Retail Charity NR, NR, NR SN 11 4.475% 2021 Real Estate UK

9-Jun Ladbrokes NR, BB, BB SN 100 5.13% 2022 Leisure UK

30-Jan Paragon NR, NR, NR SN 125 6.13% 2022 Finance UK

6-Dec Premier Oil NR, NR, NR SN 150 5.00% 2020 Oil & Gas UK

21-Oct A2Dominion NR, NR, AA- SN 150 4.75% 2022 Real Estate UK

25-Jul Bruntwood NR, NR, NR SSN 50 6.00% 2020 Real Estate UK

25-Jun Helical Bar NR, NR, NR SN 80 6.00% 2020 Real Estate UK

8-May International PersonalFinance NR, NR, BB+ SN 70 6.13% 2020 Finance UK

21-Mar Provident NR, NR, BBB SN 65 6.00% 2021 Finance UK

05-Mar Paragon NR, NR, NR SN 60 6.00% 2020 Finance UK

15-Feb EnQuest NR, NR, NR SN 145 5.50% 2022 Oil & Gas UK

19-Dec Alpha Plus NR, NR, NR SSN 49 5.75% 2019 Education UK

12-Dec UNITE NR, NR, NR SN 90 6.13% 2020 Real Estate UK

Date Issuer Ratings (M,S&P,F) Form Amount(GBPm) Coupon Maturity Sector Country

30-Jul Buford NR, NR, NR SN - 6.50% 2022 Finance UK

Section 4: ORB retail bond market

EUR public bond market

EY Capital and Debt Advisory - New Issue Review 11

► The Eurobond market has seen a strong increase in high-yield issuance during the first half of the year,with sub-investment grade bonds accounting for over 25% of total issuance in the year to date. Manyattribute this increase to investors clamouring to maximise yield amidst near record-low benchmarkinterest rates. Overall year-to-date volumes have increased c. 20% vs. 2013 equivalent issuance levels,though investors will likely be thankful with the prospect of a quiet summer ahead.

► French supermarket giant Casino Guichard-Perrachon (NR, NR, BBB-) took advantage of limited volumesin the week, attracting a €2.6 billion order book in support of its €900 million 12-year bond, allowingfinal pricing to be tightened from initial guidance of +135bps to a final print at MS+125bps. The newissue pricing was seen as broadly flat to the company’s existing issuer curve, further demonstrating theappetite from investors to secure strong allocations in an increasingly selective market.

Section 5: EUR public bond market

Source: Reuters

Source: Reuters Source: Reuters

Domestic

Cross-borderSigningdate Issuer Tranche rating

(M,S&P,F) Form Amount(GBPm) Coupon Maturity Spread

(G+bps) Sector Ctry Leads

No significant issuance in the week

0

50

100

150

200Sp

read

(bps

)EUR secondary public bond spread 10-year

Avg. AA EUR 10yr spreads Avg. A EUR 10yr spreads

Avg. BBB EUR 10yr spreads

0

10

20

30

40

50

60

70

0

5

10

15

20

25

Num

ber

issu

ed

Vol

ume

(EU

Rm

)

Monthy EUR bond volumes

Volume (EUR) Number issued

Signingdate Issuer Tranche rating

(M,S&P,F) Form Amount(EURm) Coupon Maturity Spread

(+bps) Sector Ctry Leads

31-Jul HomeVi B3, B, NR SSN 355 6.875% 2021 +626 Healthcare FR GS, DG, NAT

30-Jul Casino Guichard-Perrachon NR, BBB-, BBB- SN 900 2.798% 2026 - Retail FR CA, GS, JPM, MIZ, RBS,

SANT, UBS

30-Jul Play Caa1, CCC+, NR SN 415 7.750% 2020 +758 Telecom PL JPM, BASML, Citi, CS

Private Placement market

EY Capital and Debt Advisory - New Issue Review 12

► The US Private Placement market saw activity pick up through the second half of July, with a number ofissuers pricing deals ahead of the traditional summer break.

► In the Power & Utilities sector, Cross Texas Transmission – viewed as an NAIC-1 (A-) issuer – priced amulti-tranche US$265 million offering split across 5-30 year maturities. The Amarillo, Texas-basedelectricity transmission construction and maintenance company held the offering at original launch size,pricing its benchmark US$60 million 10-year notes at T+80bps (3.28% coupon), US$45 million 20-yearnotes at T+90bps (3.79% coupon) and US$65 million 30-year notes at T+95bps (4.21% coupon).

► Cogeco Cable, the Montreal-based cable company – viewed as an NAIC-2 (BBB-) issuer – pricedUS$175 million of senior-secured notes, split as US$25 million of 10-year notes at T+155bps andUS$150 million of 12-year notes at T+170bps. This compared favourably to the issuers June 2013offering of 12-year senior-secured notes that then priced at T+220bps.

► Grainger plc. – the UK’s largest listed residential property manager (viewed as NAIC-3; BB+) has tappedits existing £200 million 5.0% senior secured 7-year notes originally issued in November 2013. The new£75 million offering, due to mature in December 2020, was priced to yield 4.792%.

Section 6: US Private Placement market

Source: Private Placement Monitor Source: Bloomberg

Source: Private Placement Monitor Source: Private Placement Monitor

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Am

ount

(US$

b)

US Private Placement volumes

2011 2012 2013 2014

050

100150200250300350400450500

Spre

adto

US

Trea

sury

/bps

NAIC-1 US Private Placement spreads (bps)

10yr High 10yr Low

050

100150200250300350400450500

Spre

adto

US

Trea

sury

/bps

NAIC-2 US Private Placement spreads (bps)

10yr High 10yr Low

0.00.51.01.52.02.53.03.54.04.5

Yie

ld(%

)

US Treasury benchmark yields

5yr UST 7yr UST 10yr UST 30yr UST

Date Issuer Ratings Form Amount(US$m) Coupon Maturity Spread

(T+bps) Sector Ctry

Aug-14 Fonterra Cooperative NAIC-1 SN 250 - 12yr15yr - Food & Beverage NZ

Date Issuer Ratings Form Amount(US$m) Coupon Maturity Spread

(T+bps) Sector Ctry

Aug-14 Cross TexasTransmission NAIC-1 (A-) SSN

4560504565

2.46%3.28%3.58%3.79%4.21%

5yr10yr15yr20yr30yr

+80+80

+110/10yr+90/Icur

+95

Utilities US

Jul-14 Idexx Laboratories NAIC-1 SN507575

3.32%3.76%3.72%

7yr10yr12yr

- Business services US

Jul-14 Southern LightsPipeline NAIC-1 (A) - 1,000

C$352 3.98% 26f/12avg +150/10yr Oil & Gas US

Jul-14 Virginia InternationalGateway NAIC-1 (A-) - 450 3.93% 16f/13avg +135/Icur Port US

Jul-14 Alaska Electric Lightand Power NAIC-1 - 75 - 30yr 125 Utilities US

Jul-14 New Mexico Gas NAIC-2 SN50

15070

2.71%3.64%3.54%

5yr10yr12yr

+105+115

+105/10yrOil & Gas US

Jul-14 Prime Property Fund NAIC-2 (Baa2/A-) AN 120120

3.88%3.98%

10yr12yr

+140+150/10yr Real Estate US

Jul-14 Black Hills Corp - FMB 8575

4.43%4.53%

30yr30yr

-- Energy & Power US

Date Issuer Ratings Form Amount(US$m) Coupon Maturity Spread

(T+bps) Sector Ctry

Aug-14 Cogeco Cable NAIC-2 (BBB-) SSN 25150 - 10yr

12yr+155

+170/10yr Telecoms CA

Aug-14 Mullen Group NAIC-2 SN CAD$ 400 3.95% 10yr12yr

+135+145 Business Services CA

Jul-14 Auckland InternationalAirport NAIC-1 (A-) SN 250 3.61% 12yr +110/10yr Aviation NZ

Jul-14 Adani Abbot PointTerminal

NAIC-2(Baa3/BBB-) SSN 150 - 7yr

10yr+225+225 Port IN

Jul-14 Attero NAIC-2 SSN 125.6 equiv

3.55%4.30%2.87%3.27%

3yr (EUR)5yr (USD)5yr (EUR)7yr (EUR)

- Energy & Power NL

Jul-14 ADLER Real Estate - - EUR50 6.00% 5yr - Real Estate DE

Jul-14 Jersey Electric - - STG30 --

20yr25yr

-- Energy & Power JE

Private Placement marketDomestic: In the market

EY Capital and Debt Advisory - New Issue Review 13

Domestic: Issued

Cross Border: In the market

Cross Border: Issued

Section 6: US Private Placement market

Date Issuer Ratings Form Amount(US$m) Coupon Maturity Spread

(T+bps) Sector Ctry

Aug-14 Peoples Gas Light NAIC-1 - - - - - Utilities US

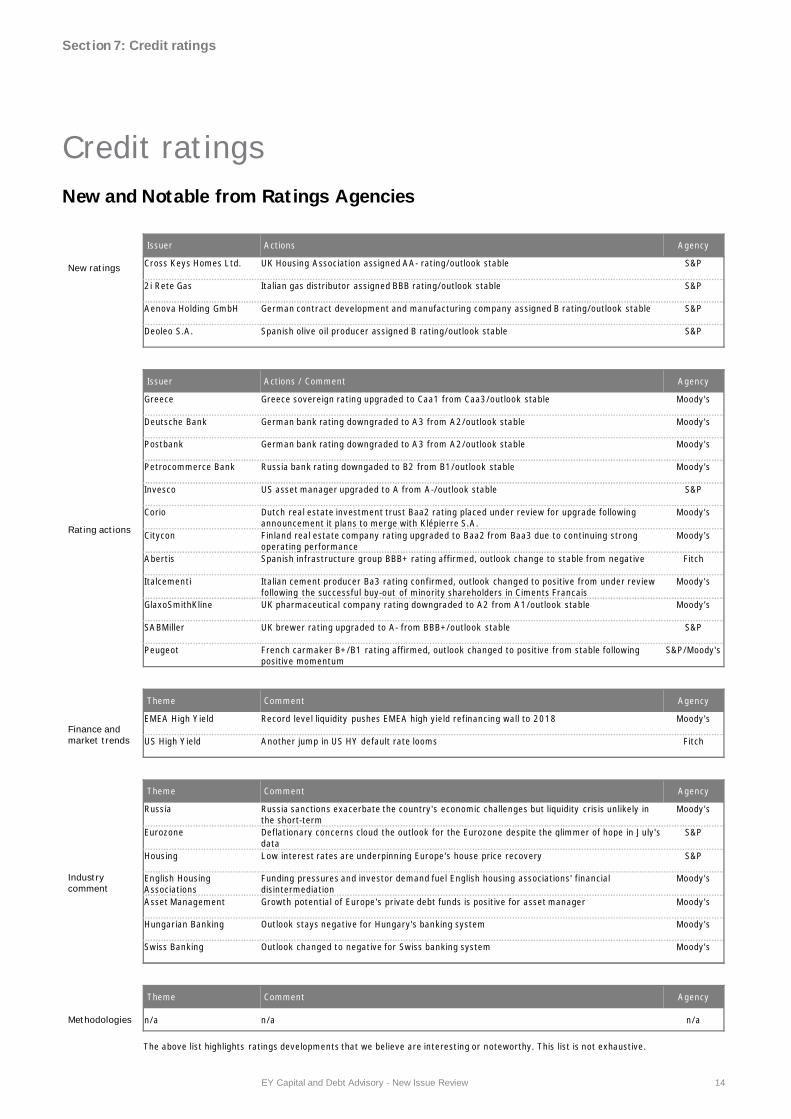

Credit ratingsNew and Notable from Ratings Agencies

EY Capital and Debt Advisory - New Issue Review 14

Issuer Actions Agency

New ratings Cross Keys Homes Ltd. UK Housing Association assigned AA- rating/outlook stable S&P

2i Rete Gas Italian gas distributor assigned BBB rating/outlook stable S&P

Aenova Holding GmbH German contract development and manufacturing company assigned B rating/outlook stable S&P

Deoleo S.A. Spanish olive oil producer assigned B rating/outlook stable S&P

Issuer Actions / Comment Agency

Rating actions

Greece Greece sovereign rating upgraded to Caa1 from Caa3/outlook stable Moody's

Deutsche Bank German bank rating downgraded to A3 from A2/outlook stable Moody's

Postbank German bank rating downgraded to A3 from A2/outlook stable Moody's

Petrocommerce Bank Russia bank rating downgaded to B2 from B1/outlook stable Moody's

Invesco US asset manager upgraded to A from A-/outlook stable S&P

Corio Dutch real estate investment trust Baa2 rating placed under review for upgrade followingannouncement it plans to merge with Klépierre S.A.

Moody's

Citycon Finland real estate company rating upgraded to Baa2 from Baa3 due to continuing strongoperating performance

Moody's

Abertis Spanish infrastructure group BBB+ rating affirmed, outlook change to stable from negative Fitch

Italcementi Italian cement producer Ba3 rating confirmed, outlook changed to positive from under reviewfollowing the successful buy-out of minority shareholders in Ciments Francais

Moody's

GlaxoSmithKline UK pharmaceutical company rating downgraded to A2 from A1/outlook stable Moody's

SABMiller UK brewer rating upgraded to A- from BBB+/outlook stable S&P

Peugeot French carmaker B+/B1 rating affirmed, outlook changed to positive from stable followingpositive momentum

S&P/Moody's

Theme Comment Agency

Finance andmarket trends

EMEA High Yield Record level liquidity pushes EMEA high yield refinancing wall to 2018 Moody's

US High Yield Another jump in US HY default rate looms Fitch

Theme Comment Agency

Industrycomment

Russia Russia sanctions exacerbate the country's economic challenges but liquidity crisis unlikely inthe short-term

Moody's

Eurozone Deflationary concerns cloud the outlook for the Eurozone despite the glimmer of hope in July'sdata

S&P

Housing Low interest rates are underpinning Europe's house price recovery S&P

English HousingAssociations

Funding pressures and investor demand fuel English housing associations' financialdisintermediation

Moody's

Asset Management Growth potential of Europe's private debt funds is positive for asset manager Moody's

Hungarian Banking Outlook stays negative for Hungary's banking system Moody's

Swiss Banking Outlook changed to negative for Swiss banking system Moody's

Theme Comment Agency

Methodologies n/a n/a n/a

The above list highlights ratings developments that we believe are interesting or noteworthy. This list is not exhaustive.

Section 7: Credit ratings

Asset-backed securitization ABS Not rated NR

Commercial mortgage-backed securitization CMBS Other loan OTH

Credit tenant lease CTL Project bond (non-recourse) PB

Deep discount bond DDB Revolving credit facility RCF

Energy savings performance contract ESPC Senior note SN

First mortgage bonds FMB Senior secured note SSN

London interbank offered rate LIBOR Subordinated note SUB

Medium-term note MTN Term loan TL

ABN Amro ABN JP Morgan JPM

Bank of America Merrill Lynch BASML KBC Capital Markets KBC

Bank of Tokyo Mitsubishi UFJ BOTM Landesbank Baden-Wuerttemberg LBBW

Banco Santander SA SANT Lloyds Capital Services Ltd LCS

Bank of New York BNY Lloyds Banking Group LBG

Bank of Nova Scotia BNS Banca March MAR

Barclays Bank BAR Mitsubishi UFJ Financial MIS

Barclays Capital Barcap Mizuho Financial Group Inc MIZ

BayernLB BLB Morgan Stanley MS

BMO Capital Markets BMO Natixis NAT

BNP Paribas Group BNP Norddeutsche Landesbank GZ NLB

Calyon CAL Nomura NOM

Citi Citi PNC Capital Markets PNC

Commonwealth Bank of Australia CBA Rabobank RAB

Commerzbank AG CZB RBC Capital Markets RBC

Crédit Agricole CA RBS RBS

Credit Suisse CS Société Générale SG

Deutsche Bank DB Scotia Capital Inc SCA

DnB NORD DnB Standard Bank Plc SB

European Investment Group EIG Standard Chartered Bank STA

Fortis Securities Inc FOR SRM Robinson Humphrey SRH

Goldman Sachs & Co GS Sumitomo SUM

HSBC HSBC UBS UBS

ING Groep NV ING UniCredit Group UNI

Intesa Sanpaolo SA ISP U.S. Bancorp USB

Incapital LLC INC Wells Fargo Wells

Banca IMI IMI WestLB WLB

GlossaryTechnical abbreviations

Financial institution abbreviations

EY | Assurance | Tax | Transactions | Advisory

Ernst & Young LLP

© Ernst & Young LLP. Published in the UK.All Rights Reserved.

The UK firm Ernst & Young LLP is a limited liability partnership registered in England and Waleswith registered number OC300001 and is a member firm of Ernst & Young Global Limited.

Ernst & Young LLP, 1 More London Place, London, SE1 2AF.

Information in this publication is intended to provide only a general outline of the subjects covered. Itshould neither be regarded as comprehensive nor sufficient for making decisions, nor should it beused in place of professional advice. Ernst & Young LLP accepts no responsibility for any loss arisingfrom any action taken or not taken by anyone using this material.

ey.com