Embed Size (px)

Citation preview

1 December2011

Bangalore Branch of SIRCof the Institute of Chartered Accountants of India

2December2011

3 December2011

Bangalore Branch of SIRCof the Institute of Chartered Accountants of India

4December2011

5 December2011

Bangalore Branch of SIRCof the Institute of Chartered Accountants of India

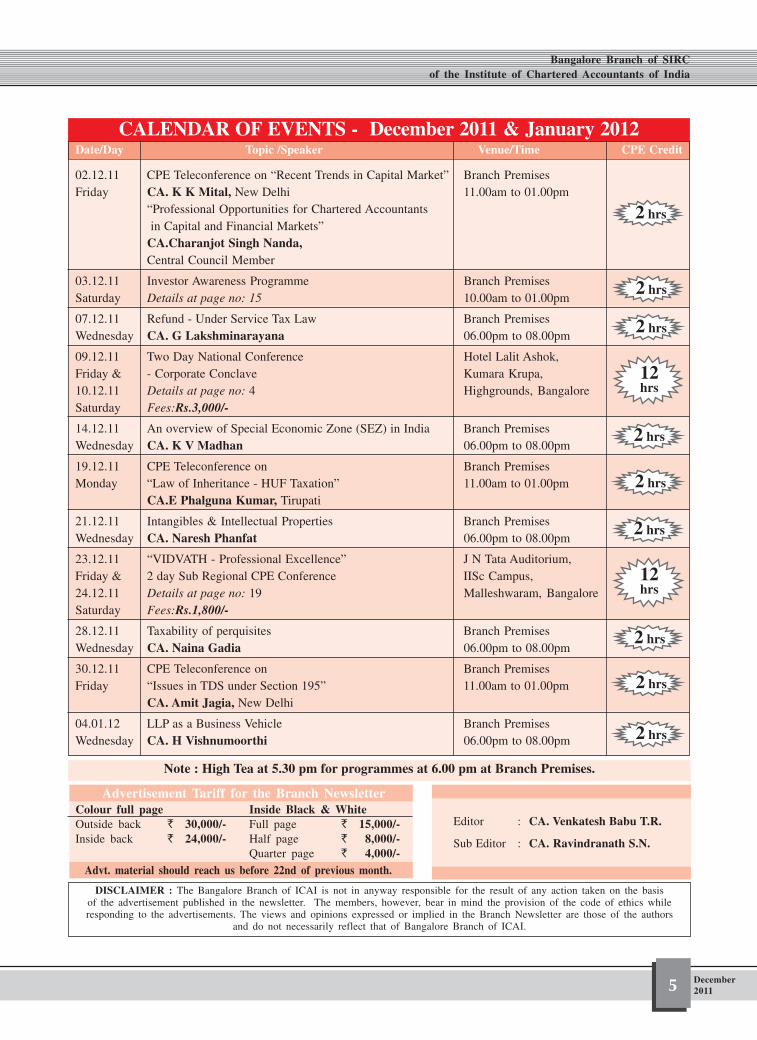

CALENDAR OF EVENTS - December 2011 & January 2012Date/Day Topic /Speaker Venue/Time CPE Credit

DISCLAIMER : The Bangalore Branch of ICAI is not in anyway responsible for the result of any action taken on the basisof the advertisement published in the newsletter. The members, however, bear in mind the provision of the code of ethics whileresponding to the advertisements. The views and opinions expressed or implied in the Branch Newsletter are those of the authors

and do not necessarily reflect that of Bangalore Branch of ICAI.

Note : High Tea at 5.30 pm for programmes at 6.00 pm at Branch Premises.

Advertisement Tariff for the Branch NewsletterColour full pageOutside back ` 30,000/-Inside back ` 24,000/-

Advt. material should reach us before 22nd of previous month.

Inside Black & WhiteFull page ` 15,000/-Half page ` 8,000/-Quarter page ` 4,000/-

Editor : CA. Venkatesh Babu T.R.

Sub Editor : CA. Ravindranath S.N.

02.12.11 CPE Teleconference on “Recent Trends in Capital Market” Branch PremisesFriday CA. K K Mital, New Delhi 11.00am to 01.00pm

“Professional Opportunities for Chartered Accountants in Capital and Financial Markets”CA.Charanjot Singh Nanda,Central Council Member

03.12.11 Investor Awareness Programme Branch PremisesSaturday Details at page no: 15 10.00am to 01.00pm

07.12.11 Refund - Under Service Tax Law Branch PremisesWednesday CA. G Lakshminarayana 06.00pm to 08.00pm

09.12.11 Two Day National Conference Hotel Lalit Ashok,Friday & - Corporate Conclave Kumara Krupa,10.12.11 Details at page no: 4 Highgrounds, BangaloreSaturday Fees:Rs.3,000/-

14.12.11 An overview of Special Economic Zone (SEZ) in India Branch PremisesWednesday CA. K V Madhan 06.00pm to 08.00pm

19.12.11 CPE Teleconference on Branch PremisesMonday “Law of Inheritance - HUF Taxation” 11.00am to 01.00pm

CA.E Phalguna Kumar, Tirupati

21.12.11 Intangibles & Intellectual Properties Branch PremisesWednesday CA. Naresh Phanfat 06.00pm to 08.00pm

23.12.11 “VIDVATH - Professional Excellence” J N Tata Auditorium,Friday & 2 day Sub Regional CPE Conference IISc Campus,24.12.11 Details at page no: 19 Malleshwaram, BangaloreSaturday Fees:Rs.1,800/-

28.12.11 Taxability of perquisites Branch PremisesWednesday CA. Naina Gadia 06.00pm to 08.00pm

30.12.11 CPE Teleconference on Branch PremisesFriday “Issues in TDS under Section 195” 11.00am to 01.00pm

CA. Amit Jagia, New Delhi

04.01.12 LLP as a Business Vehicle Branch PremisesWednesday CA. H Vishnumoorthi 06.00pm to 08.00pm

2 hrs

2 hrs

2 hrs

12hrs

2 hrs

2 hrs

2 hrs

12hrs

2 hrs

2 hrs

2 hrs

6December2011

TAX UPDATES OCTOBER 2011CA. Chythanya K.K., B.com, FCA, LL.B., Advocate

VAT, CST, ENTRY TAX,PROFESSIONAL TAXPARTS DIGESTED:

a) 44 VST – 3 to 5

b) 45 VST - 1

c) 7 GSTC – Part 2

d) 10 GSTR – Part 8

e) 16 KCTJ – Part 7

f) 71 KLJ – Part 9 & 10

Reference / Description

2011-12 (16) KCTJ 201 : The ACCTv. Pink City & others- In the instantcase, the assessee had not filed thereturn and had failed to pay the tax.The department levied penalty underSection 72(1) of the KVAT Actwithout issuing show-cause notice.The assessee contended that penaltywas imposed without giving anyshow-cause notice and hence thesame was against the natural justice.The department counsel contendedthat there is no provision in Section72(1) of the KVAT which provides forissue of show-cause notice beforeimposing penalty and also contendedthat even if the show-cause notice wasissued and the assessee was heard,that does not change the position asto levy penalty or not.In view of theabove fact, the Honourable KarnatakaHigh Court observed that sub-sections other than sub-section (1) ofSection 72 of the KVAT Act expresslyprovide for issue of a show-causenotice and to hear the assessee beforeimposing the penalty, but suchprovision is conspicuously missing inSection 72(1) of the KVAT Act. In thisregard, the Court held that though thesaid Section does not provide for such

provision, it also has not expresslyexcluded the same. Therefore, as aprinciple of natural justice, show-cause notice has to be issued andassessee’s has to be heard. Furtheranswering to the contention of thedepartment counsel that mere issue ofshow-cause does not change theposition as to levy penalty or not, theCourt held that imposition of penaltywould be automatic in which event,following the principles of naturaljustice would be a mere emptyformality. Merely because nodiscretion was left with the authoritiesunder the aforesaid provision inimposing the penalty once thecondition prescribed for imposingpenalty was satisfied, that would notrender the said provisionunconstitutional. But at the same timeif the rule of ‘audit alterm partern’ hadto be meaningful and in a genuine casewhere the non-compliance of thestatutory requirement was beyond thecontrol of the assessee and was notintentional, the authority who wasvested with the power to imposepenalty should have the power and thediscretion not to impose penalty. Infact the reason why such a discretionwas not left with the authority was,that the experience shows, that sucha power and discretion was notproperly exercised and in many casesabused, rendering the provisionimposing the penalty otiose. When theobject of introducing this provisionfor penalty in the KVAT Act was toenforce strict compliance of thestatutory provisions, the legislature inits wisdom had not conferred anydiscretion on the authority concerned.

That would not by itself denude thepower of the authority to reduce orwaive penalty in a genuine deservingcase. Further, the Court also stated thecircumstances under which such abenefit could be given to the assesseewhich reads as under:-

1. Death of the proprietor/proprietrix.

2. Death or incapacitation of anyperson authorized to file returns in thecase of tax payers who are firms orcompanies.

3. Natural calamities including fireaccidents.

4. Seizure of books of accounts andother documents of the tax payer byany statutory authority.

5. Sealing or closure of businesspremises of the tax payer by anystatutory authority.

6. Non-issue of TDS certificate byGovernment departments and otherauthorities to the tax payers who areworks contractors

7. Transfer of the tax payer’s life fromthe jurisdiction to another authoritywithout prior intimation to the taxpayer8. If in law they are not liableto file return or not liable to pay taxunder the Act.

Thus, the Court concluded that whenonce there is a non-compliance withthe statutory requirements of notfurnishing returns within thestipulated time or after furnishing thereturns, non-payment of tax alongwith the returns, the penalty shouldfollow as a rule. However, only inexceptional cases falling under theaforesaid circumstances, theauthority may in its discretion forreasons to be recorded in writing,showing the application of mind by

7 December2011

Bangalore Branch of SIRCof the Institute of Chartered Accountants of India

them and their satisfaction, exercisethat discretion and waive the penaltyeither fully or partially.

2011 (71) Kar. L.J. 341 (Tri.) (DB):Centum Industries Pvt. Ltd. v. Stateof Karnataka- In the instant case, theappellant had purchased certain goodsfrom SACPL (seller) in the month ofJuly 2006 for Rs. 21,87,822 includingVAT of Rs. 2,43,306/-. The appellantfailed to claim input tax on the saidpurchase in the respective period butclaimed the same in the month ofFebruary 2007 (i.e. after six months).The seller had not remitted toGovernment, the tax so collected andhad been deregistered. The claim ofthe appellant was rejected by theDepartment despite the appellanthaving produced valid tax invoice.Inview of the above facts, the Tribunalheld that if a dealer establishes hisclaim for input tax by furnishing avalid tax invoice issued by aregistered dealer indicating the VATcollected in it, he would bedischarging the liability cast upon himunder Section 70(1) of the KVAT Actand merely because the dealer whosells goods and collects tax from himhad not complied with the provisionsof the KVAT Act, the dealer buyingthe goods from such seller cannot beheld responsible for it and it wasresponsibility of the authoritiesconcerned for taking appropriateaction under the law against the non-complaint dealer.Further, the Tribunalheld that the law does not stipulatethat dealer would forfeit input taxcredit if the dealer had failed to utilisethe same in the month succeedingmonth in which input tax was paid onpurchase made. The Tribunal relyingon the principle in its own judgmentin the case of M/s. Texport OverseasPvt. Ltd. v. State, in STA No. 1831 of2008, dated 22.09.2010 that ‘whenonce tax has been paid, the party

should not be asked to pay the taxagain’ by denying the input tax, heldthat the department was not justifiedin denying the input tax credit.

INCOME TAX

PARTS DIGESTED:

a) 336 ITR – Part 4

b) 337 ITR – Part 4 & 5

c) 338 ITR – Part 1 to 3

d) 201 Taxman – Part 5 & 6

e) 202 Taxman – Part 1 to 4

f) 71 KLJ – Part 9 & 10

g) 11 ITR (Trib) – Part 3, 4, 6 to 9

h) 12 ITR (Trib) – Part 1

i) 132 ITD – Part 5 to 8

j) 5 International Taxation –Part 4

Reference / Description[2011] 337 ITR 389 (Delhi – HC):CIT v. Madhya Bharat EnergyCorporation Ltd.- In the instant case,the Delhi High Court dealing with theaspect of non-issuance of notice underSection 143(2) of the IT Act in respectof re-assessment proceedings, heldthat the IT Act does not specificallyprovide that the assessment madeunder Section 147 of the IT Actshould be made after the issue ofnotice under Section 143(2) of the ITAct.With due respect, the hon. HighCourt’s decision requiresreconsideration as the proviso tosection 148, which brings out theneed of issue of notice under section143(2), was not noticed by the Hon.High Court.

[2011] 337 ITR 399 (Delhi –HC):Ashok Chaddha v. ITO - In theinstant case, the Assessing Officerduring the assessment under Section153A of the IT Act had not issuednotice under Section 143(2) of the ITAct calling for details. The Delhi HighCourt observed that the Assessing

Officer had issued notice underSection 153A and questionnairescalling for details. Further, the Courtobserved that Section 153A nowhereprescribes issuance of notice underSection 143(2) and the words ‘so faras may be’ used in Section 153A(1)(a)cannot be interpreted to mean that theissue of notice under Section 143(2)is mandatory in the case of anassessment under Section 153A of theIT Act. Thus, the Court held thatnotice under Section 143(2) was notnecessary during the assessmentunder Section 153A.Ironically, theHon. High Court did not notice thatthe phrase “ so far as may be” wasinterpreted by the Supreme Court inthe case of Hotel Blue Moon 321 ITR362 while holding that issue of noticeu/s 143(2) is mandatory for carryingout block assessment.

[2011] 337 ITR 498 (Delhi – HC):Mitsubishi Corporation v. CIT andanother-The Delhi High Courtdealing with the expression ‘salary’under Section 17 of the IT Act readwith Rule 3 of the IT Rules observedthat the said expression is an inclusiveone and is not restricted to what isincluded in the definition. Therefore,the Court held that the tax paid byemployer on behalf of employeeforms part of ‘salary’ for the purposevaluation of perquisite under rule 3.

[2011] 337 ITR 511 (All. – HC):Shyama Charan Gupta v. CIT- In theinstant case, assessee was themanaging director of a Company,received advances of salary andcommission on profits. The AssessingOfficer treated the same as deemeddividend under Section 2(22)(e) of theIT Act.The Allahabad High Court inrespect to advance received towardssalary held that the same cannot betreated as deemed dividend as thesalary was due to the assessee and wascredited to his account every month.

8December2011

In respect to advance receivedtowards commission the Courtobserved that the advance ofcommission on profits was over andabove the amount drawn during thecourse of the years before the profitswere determined and accrued to theassessee, therefore, the Court treatedthe same as deemed dividend.TheHon. Court missed the point that theterm salary under sec 17(1) includescommission and hence differentialtreatment could not have beenaccorded to commission.

[2011] 338 ITR 95 (Bom. – HC):DIT v. Dun & BradstreetInformation Services India P. Ltd.-In the instant case the assessee hadimported business information reportsfrom its subsidiary non-residentCompany and had made remittanceswithout deducting tax at source. TheAssessing Officer held that theassessee was liable to deduct tax atsource. The Tribunal relying on therulings of the Authority of AdvanceRuling, ruled that the payment forbusiness information reports to itssubsidiaries does not attract tax underthe provisions of Section 195 of theIT Act and assessee was not liable todeduct tax. The Bombay High Courtobserved that though the ruling of theauthority was not binding in thepresent case, the ruling of Authoritywas related to the very same businessinformation reports imported by theassessee and therefore, held that theruling of Authority of AdvanceRulings can be relied or followedwhen there are similar facts in respectof same subject-matter and thus, heldthat the assessee was not liable todeduct tax.

[2011] 202 Taxman 318 (P&H –HC)14 taxmann.com 45 (P&H - HC)CIT v. Director, Delhi Public School-

In the instant case, the assessee wasrunning a public school and was liableto deduct tax at source from salary andremuneration paid to its teaching staff.It had been providing free/concessional educational facilities tothe wards of teachers and other staffmembers of the school. Whilecalculating the amount of perquisitetaxable in the hands of teachers/staffqua free/concessional educationalfacilities provided to their wards, theassessee had been allowing adeduction of Rs. 1,000 per month perchild from the total amount ofeducational facilities provided free ofcost to them. The Assessing Officerheld that the assessee had wronglyallowed a deduction of Rs. 1,000/- permonth per child while calculating theamount of taxable perquisite andadded an amount of Rs. 12,000 perannum per child to the value ofperquisites on account of freeeducational facilities provided to thewards of the employees/staff of theschool and therefore, the AssessingOfficer calculated short deduction tothat extent and treated the assessee tobe in default and also charged interestunder Section 201(1A) of the ITAct.The Punjab & Haryana HighCourt observed that on plain readingof sub-rule (5) of Rule 3 of the ITRules, it emerges that where the valueof the perquisite of free/concessionaleducational facility arises to anemployee and the valuation thereofexceeds Rs. 1,000/- per month, thenthe entire amount is added and isliable to be taxed in the hands of therecipient. However, an exception hasbeen carved out in the provisoattached to the said sub-rulewhereunder the sub-rule has noapplicability in a situation where thecost of such education or value ofsuch benefit per child does not exceed

Rs. 1,000 per month. The Court heldthat the said sub-rule nowhereprovided that while determining thevalue of the perquisite wherever itexceeds Rs. 1,000 per month then theamount of Rs. 1,000 per month hadto reduced from the value of suchperquisite. The Court further held thatonce the value of the perquisiteexceeded Rs. 1,000 per month,proviso to Rule 3(5) had noapplicability. Thus, the Courtconcluded that the value of the benefitof free education to the wards of theemployees shall be quantified as thevalue of the perquisite in the handsof the employer without any reductionof Rs. 1,000 per month per child.

[2011] 202 Taxman 327 (Delhi -HC); 14 taxmann.com 14 (Delhi -HC) CIT v. National TravelServices- In the instant case, theassessee-firm took loan of certainamount through its partners from aCompany, in which the assessee-firmheld 48.18 per cent equity shares. TheAssessing Officer treated the same asdeemed dividend under Section2(22)(e) of the IT Act. The assesseecontended that the assessee-firm wasnot a ‘registered shareholder’ of theCompany.The Delhi High Court heldthat the expression ‘being a personas a beneficial owner of shares’qualifies the word ‘shareholder’ andthus, to attract provisions of section2(22)(e), person to whom loan oradvance is made should be a‘shareholder’ as well as ‘beneficialowner’. The High Court however heldthat in case of partnership firm havingpurchased shares through its partnersin a Company, which has paid loansis to be treated as a ‘shareholder’ andit was not necessary that it has to be‘registered shareholder’ of aCompany.

9 December2011

Bangalore Branch of SIRCof the Institute of Chartered Accountants of India

RECENT JUDICIALPRONOUNCEMENTS ININDIRECT TAXESN.R. Badrinath, Grad C.W.A., F.C.A.Madhur Harlalka, B. Com., F.C.A

VAT/CST:

Software Development Services arenot works contract: The appellantwas engaged in the business ofsoftware development and providingsoftware services. A notice was issuedfor re-assessment and the assessingauthority after hearing the contentionsof the appellant concluded that theactivity of software developmentattracted ‘works contract tax’(‘WCT’) under Section 4(1)(C) ofKVAT Act. Aggrieved by this order,the appellant preferred a Writ Petitionbefore the Karnataka High Court. TheSingle Judge Bench of the High Courtdismissed the Writ Petition by holdingthat the question of whether thecontracts were service contracts orworks contracts was to be carefullyexamined and this was possible onlythrough a statutory appeal providedto the appellant against the orderpassed by the assessing authority.Against the order of the Single Judge,the appellant filed the Writ Appealsbefore the Division Bench. Afterhearing the rival submissions, theHigh Court framed the followingpoint for its consideration:

“Whether the contract fordevelopment of a software falls withinthe mischief of a “works contract”,and when the software so developedvests with the customer from day oneand does it amount to deemed saleunder Article 366(29-A)(b) of theConstitution of India?”

The High Court held that it is settledthat there is no prohibition in law toimpose a tax both by Parliament andState Legislature on different aspectsi.e. Parliament can levy tax onservices and State Legislature haspower to levy tax on sale of goods. Ifcomputer programming andproviding of computer softwareinvolves two aspects (i.e. workscontract), one falling within the powerof the Parliament and the other fallingwithin the power of the StateLegislature to enact the law, the lawso enacted cannot be found fault with.But this distinctiveness of twotransactions has to be ascertainedfrom the terms of composite contract.If such an intention is not discerniblefrom the terms of the contract then thepith and substance of the contract i.e.the true nature and character of thecontract has to be ascertained. If onan examination of the contract as awhole, it is not possible to discern thatthe contract involves sale of goods butis essentially an agreement to renderservice, neither the concept of a workscontract nor the concept of aspecttheory is attracted.

Further, the test for compositecontracts other than those mentionedin Article 366(29A) continues to beas to what the parties had in mind orintended and the separate rightsarising out of the transaction. It isnecessary to look into the terms of thecontract carefully to ascertain the trueintent and nature of the contract, viz.,

what is the nature of activity, what theparties intended, what is agreed uponand what is the consideration paid. Inthe instant case, it is abundantly clearthat the parties have entered into anagreement whereby the appellantrenders services to clients fordevelopment of software i.e. forsoftware development and otherservices. All patentable andunpatentable inventions, discoveriesand ideas which are made orconceived as a direct or indirect resultof the programming or other servicesperformed under the agreement shallbe considered as works made for hireand shall remain exclusive propertyof the client and the appellant shallhave no ownership interest therein.Since, even before rendering services,appellant has given up his rights tothe software to be developed, thecontract in question is not ‘workscontracts’ but ‘contracts for servicesimplicitor’. They are not compositecontracts consisting of ‘contract ofservice’ and ‘contract for sale ofgoods’ but an ‘indivisible contract forservice’ only. [SaskenCommunication Technologies LtdVs Joint Commissioner ofCommercial Taxes, Bangalore,2011-TIOL-707-HC-KAR-ST]

SERVICE TAX:

Business Auxiliary Services –marketing services: In the presentcase, Microsoft Corporation IndiaPrivate Limited, the appellant, isproviding marketing services,technical support services includingmarketing of Microsoft products inIndia to its parent company, MicrosoftOperations PTE Limited. Theappellant has claimed the aboveservices as Export of Services underthe category of “Business AuxiliaryServices”. However, the service tax

10December2011

department has levied service tax onthe ground that services wereprovided in India and don’t qualifyas export of services. Being aggrievedwith the order of adjudicationauthority, the appellant preferred anAppeal before the Tribunal.

In this regard, the Member (J) andMember (T) have separately held asfollows:

MEMBER (J) - Law relating toservice tax has been laid down byApex Court in All India Federationof Tax Practitioners. Applying theprinciple of equivalence, there is nodifference between manufacture ofmarketable excisable goods andproviding of marketable / saleableservices in the form of an activityundertaken by the service provider forconsideration, which correspondinglystands consumed by the servicereceiver. The Article 286(1)(b) of theConstitution of India explains what“export” means and such concept inthis regard is “taking out of India to aplace outside India”. This is arecognized test to hold an activity tobe export under the Customs Act,1962. Activity relating to goods beingequal to the activity relating toservice, following “Principles ofEquivalence”, meaning of the term“export” recognized by Constitutionalprovision and tested by law relatingto Central Sales Tax, Customs,Central Excise and Export and ImportPolicy of the government leaves nodoubt to construe meaning of the saidterm in the context of export ofservice under the provisions ofFinance Act, 1994 read with Exportof Service Rules, 2005. There shouldbe two termini for export of service.Service generated in one termini iftravels outside that termini for endingthereat, export can be said to havebeen made.

The activity of promotion of goodsended in India upon identification ofcustomers and nothing travelledabroad to end there. There is noambiguity that legislature in terms ofExport of Service Rules, 2005intended that service consumedoutside India shall be export. In thepresent case when marketing serviceswere provided by the Appellant tobring Microsoft products andtechnical support into India in termsof the agreement, ultimateconsumption of service was made inIndia and the appellant as agent of theforeign principal acted on its behalfin India. The circulars issued byCBE&C subscribe to the concept of“export” as is stated in theConstitution and finds support fromdecisions of Apex Court on thesubject of export. It appears that theBoard has clear perception of suchterm having gained vast experiencefrom law of Customs and CentralExcise as well as Export & ImportPolicy. Identification of customers inIndia brings an end to the promotionof marketing handicapping suchpromotion to travel abroad. Circularsdo not appear to have made anyapproach contrary to suchproposition.

MEMBER (T): What constitutesexport of services is an issue wherethere are reasons for differentunderstanding in the matter. Theactivities for promotion and the salesconsequent to the promotion takeplace substantially in India related toproducts belonging to a personlocated outside India. Therefore, it isto be considered that the impugnedservice was delivered outside India.The clarification issued on 13-05-2011 gives the impression that thematter is to be decided with referenceto “the accrual of benefit “. This

expression is not used in the Rulesthough it was used in the earliercircular dated 24-02-2009. Thecircular does not give any clarity tothe issue. If a person does marketpromotion for a manufacturer locatedoutside India for selling the goods inIndia after its import, the goods willbe considered to be imported but themarketing services will be consideredto be exported. It may prima facieappear to be contradictory. But this isthe outcome of the Rules as it existsnow and this was the position clarifiedby CBEC vide Circular No.111/05/2009-ST dated 24-02-2009.

Though there is equivalence betweengoods and services in certain aspectsfor taxing the two, there is afundamental difference between themin the matter that the former istangible while the latter is not tangiblein most cases though its effect oroutcome may be tangible. It isdifficult to conceive of taking theservice and crossing the border. Theword “export” in Article 286 in theConstitution is used with reference togoods. So is the case with definitionof “export” in section 2 (18) of theCustoms Act, 1962. It will obviouslyneed some dovetailing in the contextof export of service which issue hascome up only after 1994. It is thisdovetailing that is being achievedthrough Export of Service Rules,2005 and the criteria laid down in theRules are neither arbitrary norinconsistent with any provision in theConstitution. The consumer of theservice is the person paying for theservice and not any person who mayalso benefit from the activity. It is notpossible to achieve exact equivalencebetween taxation on goods andservices and especially so in thematter of criteria for deciding thequestion whether service is exported.

11 December2011

Bangalore Branch of SIRCof the Institute of Chartered Accountants of India

The Apex Court has not ruled in theabove decisions that tax on servicesand duties on goods are on identicalfooting in all respects.

Considering the two different viewsof the Member (T) and Member (J)of the bench of the Tribunal, pointsof difference was referred to a ThirdMember. Whether the impugnedBusiness Auxiliary Service ofpromotion of market in India forforeign principal made in terms theAgreement, promotion of marketingservices were delivered outside India,governed by the principles ofequivalence and destination basedconsumption tax and amounts toexport of service considering Article286(1)(b) of the Constitution of Indiaread with Apex decisions, theprovisions of Export Service Rules,2005 as well as Circulars. [MicrosoftCorporation India Private Limited VsCST, New Delhi, 2011-TIOL-1508-CESTAT-DEL]

CENTRAL EXCISE:

Sale of Scrap Generated during therepair and maintenance of CapitalGoods: In the present case questionbefore the Hon’ble Supreme Court iswhether scrap or waste arising fromrepair and maintenance of plant andmachinery (i.e. capital goods)installed in cement factory, is liableto excise duty. The Hon’ble SupremeCourt held that it is clear that theprocess of repair and maintenance ofthe machinery of the cementmanufacturing plant, in which M.S.Scrap and iron scrap arise has nocontribution or effect on the processof manufacturing of the cement. Therepairing activity in any possiblemanner can’t be called as a part ofmanufacturing activity in relation toproduction of end product. Therefore,the M.S. Scrap and iron scrap can’tbe said to be a by-product of the final

product. The metals scrap and wastearising out of the repair andmaintenance work of the machineryused in manufacturing of cement, byno stretch of imagination, can betreated as subsidiary product to thecement which is the main product.The metal scrap and waste arise onlywhen the assessee undertakesrepairing and maintenance work ofthe capital goods and, therefore don’tarise regularly and continuously in thecourse of a manufacturing business ofcement. Manufacture in terms ofSection 2(f) of Central Excise Act,1944 includes any process incidentalor ancillary to the completion of themanufactured product. This “anyprocess” can be a process in themanufacture or process in relation tomanufacture of the end product,which involves bringing some kindchange to the raw materials at variousstages by different operations. Theprocess in manufacture must have theeffect of bringing change ortransformation in the raw materialsand this should lead to creation of anynew or distinct and excisable product.The process in relation to manufacturemeans a process which is so integrallyconnected to the manufacturing of theend product without which, themanufacture of the end product wouldbe impossible or commerciallyinexpedient. The repair activity in anypossible manner can’t be called as apart of manufacturing activity inrelation to production of end product.Therefore, the M.S. Scrap and IronScrap can’t be said to be by productof the final product. At the best, it isby-product of the repairing processwhich uses welding electrodes, mildsteel, cutting tools, M.S. Angles, M.S.Channels, M.S. Beans etc.

The metal scrap and waste specifiedunder heading 74.02 of the Central

Excise Tariff Act and Section 8(a) toSection XV of the Act has verylimited purpose of existing coverageto the particular item to the duty, thisnote can’t be constructed to have anydeeming effect in relation to theprocess of the manufacturing ascontemplated by Section 2(f) of theCentral Excise Act, 1944. Therefore,the scrap is not exigible to excise dutymerely because of their specificationin particular tariff entry. Scrap is notexcisable unless they aremanufactured in terms of Section 2(f)of the Act. [Grasim Industries LimitedVs. Union of India, 2011 (273) E.L.T10 (S.C)]

Excise Duty Exemptions: Theappellant has three productionfacilities in Faridabad for manufactureof tractor and tractors parts. Thetractors parts manufactured in UnitNo 1 are being sent to Unit 2 and Unit3 for use in the manufacture oftractors. Unit I is geographically at adistance of about 1.5 km from UnitNo. II and III and Unit II and Unit IIIwere adjacent to each other. Theseunits initially had separateregistrations. The appellant obtainedone common PAN based CentralExcise Registration in respect of allthese units. The tractors wereexempted from central excise duty interms of Notification No. 6/02-CE dt.01.03.2002 as amended byNotification No. 23/2004-CE dt.09.07.2004. Accordingly, theappellants have claimed exemptionunder the above notification for allthree units. However, subsequently,the common central exciseregistration was cancelled on theground that Unit I is geographicallyat a distance of about 1.5 km fromUnits No. II and III and also that UnitNo. II & III are separated by anotherunit. Further, excise duty was levied

12December2011

on clearances of goods from Unit I toUnit II & III. Further, that the Unit IIand III are not interlinked since thefinal goods manufactured in one Unitare not inputs / intermediate productsfor the other units and the clearancesmade from Unit II to Unit III are notexempt under Notification No. 6/02-CE dt. 01.03.2002 (S. No. 296) andlater under Notification No. 6/06-CE01.03.2006 (S. No. 92) in respect ofclearances of goods not used withinthe same factory of production.

On appeals, the Tribunal held thatnormally different manufacturingunits of any manufacturers arerequired to take separate registrationsin terms of the conditions, safeguardsand procedures prescribed inNotification No. 35/2001 dated21.06.2001. However, NotificationNo. 36/2001 provides for relaxationsand in certain cases registration istotally exempted and in certain casescommon registration is provided for.The Board has given the aboveguidelines as to circumstances inwhich two premises can be treated aspart of the same factory. The facilityof common registration can beextended at the discretion of theCommissioner taking into account therelevant factors. It is settled law thatthe authority which has power to grantcertain permission / facility has thepower to withdraw the same.However, withdrawing the saidfacility retrospectively, in the givenfacts and when the permission wasgranted based on applications by theappellants and after due verificationof the details is not appropriate. It isnot a case of the department that theappellants have given any falseparticulars and obtained the facility.The Commissioner has power torevoke the common registrationgranted, in case he found the

guidelines issued by the Board do notpermit common registration.However, the Commissioner was notjustified in withdrawing the facilityof common registrationretrospectively. Further, the term‘used in the factory of production’stands interpreted by the SupremeCourt as use not in any other factory.Accordingly, the appeal was allowedby setting aside the demand. [EscortsLtd Vs CCE, Delhi 2011-TIOL-1514-CESTAT-DEL]

CENVAT Credit:

Export of exempted goods andCENVAT credit refund: Theappellants are engaged in themanufacture of stainless steel utensils,aluminium utensils and cutlery and allsuch goods are exempted frompayment of excise duty. Theappellants filed unutilized CENVATcredit refund claims under Rule 5 ofthe CENVAT Credit Rules, 2004 inrespect of service tax paid on the inputservices used in or in relation to themanufacture of final product.However, the adjudicating authoritynoting that the final export productwas exempted from payment ofcentral excise duty the claims wereconsidered under the provisions ofNotification No. 41/2007-ST dated06.10.2007 and rejected the refundclaim. The Commissioner (Appeals)also upheld the impugned order.

On further appeal, the Tribunal heldthat a manufacturer is entitled to availcredit in respect of duty paid on inputsused in the manufacture of goodscleared on payment of duty as well asexempted goods. The service tax paidon input services also can be availedas input credit. Rule 6 of the CENVATCredit Rules provides that in casecommon inputs or input services areused in the manufacture of exempted

or duty paid goods, the manufacturerhas to maintain separate records andin the absence of separate records, themanufacturer has to pay 10% of theprice of the exempted goods. TheRule further provides that theprovisions of sub - Rules (1), (2), (3)and (4) shall not be applicable in casethe excisable goods removed withoutpayment of duty and are cleared forexport under bond in terms of theprovisions of Central Excise Rules.This Rule is interpreted by theHon’ble High Courts in the case ofRepro India Ltd. and in the case ofDrish Shoes Ltd. The Hon’ble HighCourts held that input credit isavailable in respect of the inputs usedin the manufacture of final productbeing exported irrespective of the factthat the final product is otherwiseexempted. In view of the abovedecisions, the rejection of the refundclaims filed under Rule 5 of theCENAT Credit Rules is notsustainable and therefore refundshould be granted. [King Metal WorksVs. CCE, Mumbai-IV, 2011-TIOL-1477-CESTAT-MUM]

CA. G.V. Krishna

(M No. : 028109)

is nominated as Director of

The Karnataka State

Co-oprative Apex Bank Ltd.,

Bangalore

Congratulation

13 December2011

Bangalore Branch of SIRCof the Institute of Chartered Accountants of India

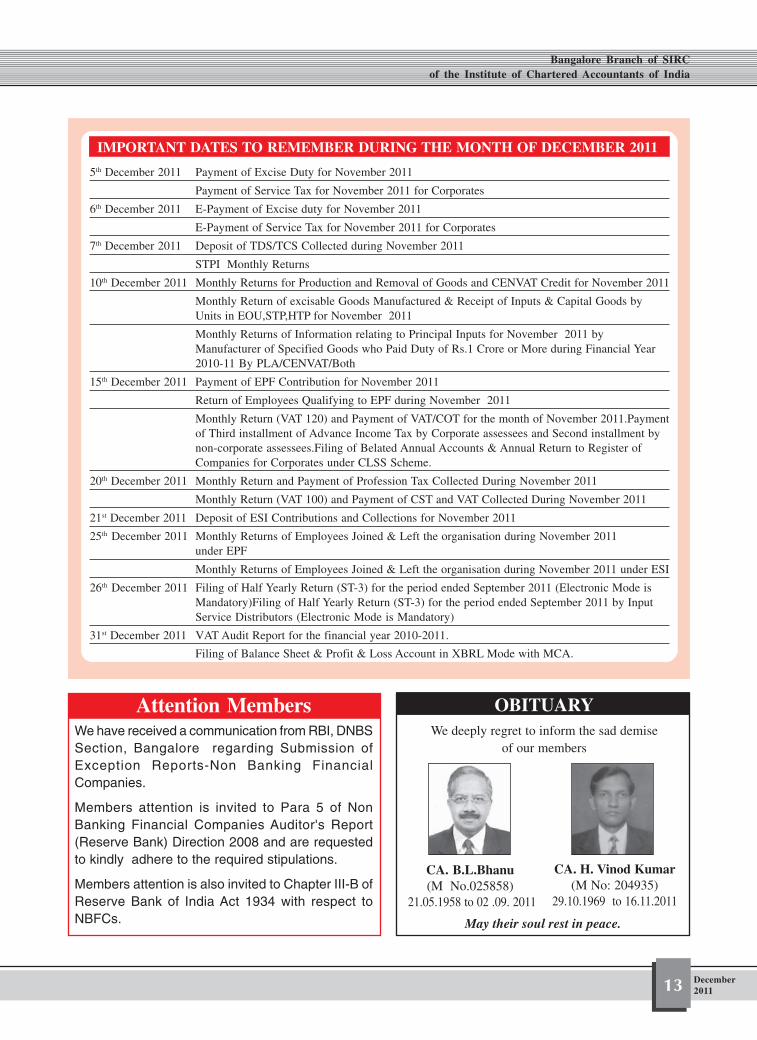

IMPORTANT DATES TO REMEMBER DURING THE MONTH OF DECEMBER 2011

5th December 2011 Payment of Excise Duty for November 2011

Payment of Service Tax for November 2011 for Corporates

6th December 2011 E-Payment of Excise duty for November 2011

E-Payment of Service Tax for November 2011 for Corporates

7th December 2011 Deposit of TDS/TCS Collected during November 2011

STPI Monthly Returns

10th December 2011 Monthly Returns for Production and Removal of Goods and CENVAT Credit for November 2011

Monthly Return of excisable Goods Manufactured & Receipt of Inputs & Capital Goods byUnits in EOU,STP,HTP for November 2011

Monthly Returns of Information relating to Principal Inputs for November 2011 byManufacturer of Specified Goods who Paid Duty of Rs.1 Crore or More during Financial Year2010-11 By PLA/CENVAT/Both

15th December 2011 Payment of EPF Contribution for November 2011

Return of Employees Qualifying to EPF during November 2011

Monthly Return (VAT 120) and Payment of VAT/COT for the month of November 2011.Paymentof Third installment of Advance Income Tax by Corporate assessees and Second installment bynon-corporate assessees.Filing of Belated Annual Accounts & Annual Return to Register ofCompanies for Corporates under CLSS Scheme.

20th December 2011 Monthly Return and Payment of Profession Tax Collected During November 2011

Monthly Return (VAT 100) and Payment of CST and VAT Collected During November 2011

21st December 2011 Deposit of ESI Contributions and Collections for November 2011

25th December 2011 Monthly Returns of Employees Joined & Left the organisation during November 2011under EPF

Monthly Returns of Employees Joined & Left the organisation during November 2011 under ESI

26th December 2011 Filing of Half Yearly Return (ST-3) for the period ended September 2011 (Electronic Mode isMandatory)Filing of Half Yearly Return (ST-3) for the period ended September 2011 by InputService Distributors (Electronic Mode is Mandatory)

31st December 2011 VAT Audit Report for the financial year 2010-2011.

Filing of Balance Sheet & Profit & Loss Account in XBRL Mode with MCA.

CA. B.L.Bhanu(M No.025858)

21.05.1958 to 02 .09. 2011

We deeply regret to inform the sad demiseof our members

May their soul rest in peace.

CA. H. Vinod Kumar(M No: 204935)

29.10.1969 to 16.11.2011

OBITUARYAttention MembersWe have received a communication from RBI, DNBSSection, Bangalore regarding Submission ofException Reports-Non Banking FinancialCompanies.

Members attention is invited to Para 5 of NonBanking Financial Companies Auditor's Report(Reserve Bank) Direction 2008 and are requestedto kindly adhere to the required stipulations.

Members attention is also invited to Chapter III-B ofReserve Bank of India Act 1934 with respect toNBFCs.

OBITUARY

14December2011

Adv

t.

Adv

t.A

dvt.

15 December2011

Bangalore Branch of SIRCof the Institute of Chartered Accountants of India

NoDelegate

FeeCPE2 hrs

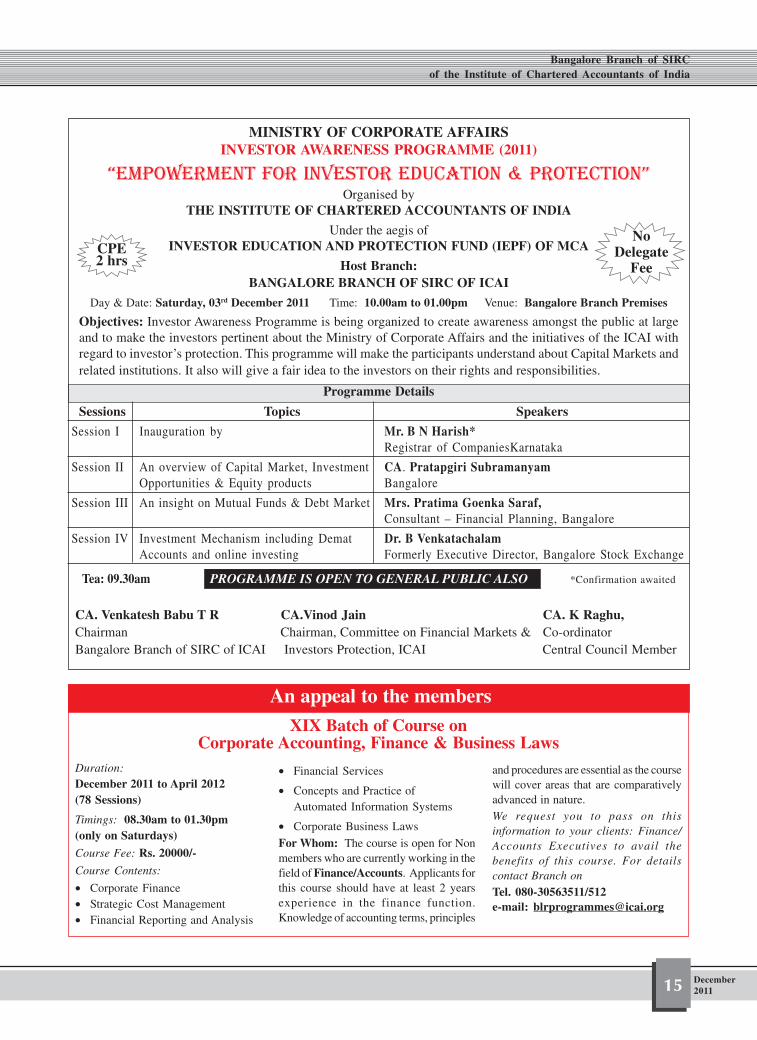

MINISTRY OF CORPORATE AFFAIRSINVESTOR AWARENESS PROGRAMME (2011)

“EMPOWERMENT FOR INVESTOR EDUCATION & PROTECTION”Organised by

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

Under the aegis ofINVESTOR EDUCATION AND PROTECTION FUND (IEPF) OF MCA

Host Branch:BANGALORE BRANCH OF SIRC OF ICAI

Day & Date: Saturday, 03rd December 2011 Time: 10.00am to 01.00pm Venue: Bangalore Branch Premises

Objectives: Investor Awareness Programme is being organized to create awareness amongst the public at largeand to make the investors pertinent about the Ministry of Corporate Affairs and the initiatives of the ICAI withregard to investor’s protection. This programme will make the participants understand about Capital Markets andrelated institutions. It also will give a fair idea to the investors on their rights and responsibilities.

Programme Details

Sessions Topics Speakers

Session I Inauguration by Mr. B N Harish*Registrar of CompaniesKarnataka

Session II An overview of Capital Market, Investment CA. Pratapgiri SubramanyamOpportunities & Equity products Bangalore

Session III An insight on Mutual Funds & Debt Market Mrs. Pratima Goenka Saraf,Consultant – Financial Planning, Bangalore

Session IV Investment Mechanism including Demat Dr. B VenkatachalamAccounts and online investing Formerly Executive Director, Bangalore Stock Exchange

Tea: 09.30am PROGRAMME IS OPEN TO GENERAL PUBLIC ALSO *Confirmation awaited

CA. Venkatesh Babu T R CA.Vinod Jain CA. K Raghu,Chairman Chairman, Committee on Financial Markets & Co-ordinatorBangalore Branch of SIRC of ICAI Investors Protection, ICAI Central Council Member

An appeal to the membersXIX Batch of Course on

Corporate Accounting, Finance & Business LawsDuration:December 2011 to April 2012(78 Sessions)

Timings: 08.30am to 01.30pm(only on Saturdays)

Course Fee: Rs. 20000/-

Course Contents:

• Corporate Finance• Strategic Cost Management• Financial Reporting and Analysis

• Financial Services

• Concepts and Practice ofAutomated Information Systems

• Corporate Business Laws

For Whom: The course is open for Nonmembers who are currently working in thefield of Finance/Accounts. Applicants forthis course should have at least 2 yearsexperience in the finance function.Knowledge of accounting terms, principles

and procedures are essential as the coursewill cover areas that are comparativelyadvanced in nature.We request you to pass on thisinformation to your clients: Finance/Accounts Executives to avail thebenefits of this course. For detailscontact Branch onTel. 080-30563511/512e-mail: [email protected]

16December2011

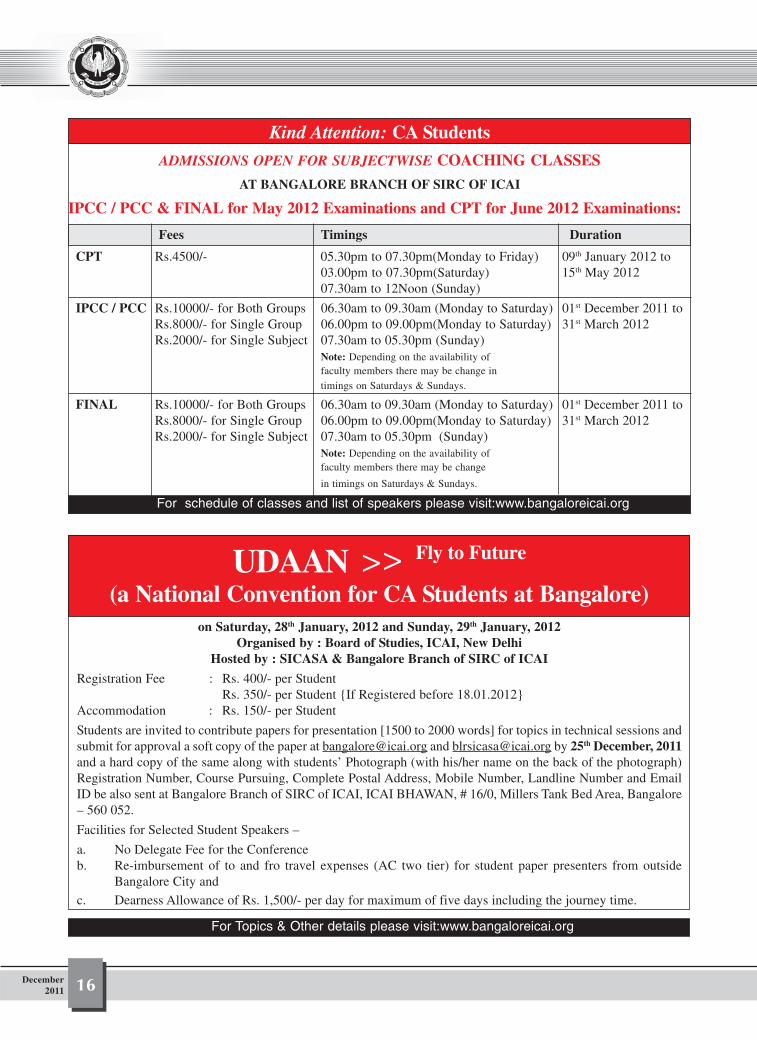

UDAAN Fly to Future

(a National Convention for CA Students at Bangalore)on Saturday, 28th January, 2012 and Sunday, 29th January, 2012

Organised by : Board of Studies, ICAI, New DelhiHosted by : SICASA & Bangalore Branch of SIRC of ICAI

Registration Fee : Rs. 400/- per StudentRs. 350/- per Student {If Registered before 18.01.2012}

Accommodation : Rs. 150/- per Student

Students are invited to contribute papers for presentation [1500 to 2000 words] for topics in technical sessions andsubmit for approval a soft copy of the paper at [email protected] and [email protected] by 25th December, 2011and a hard copy of the same along with students’ Photograph (with his/her name on the back of the photograph)Registration Number, Course Pursuing, Complete Postal Address, Mobile Number, Landline Number and EmailID be also sent at Bangalore Branch of SIRC of ICAI, ICAI BHAWAN, # 16/0, Millers Tank Bed Area, Bangalore– 560 052.

Facilities for Selected Student Speakers –

a. No Delegate Fee for the Conferenceb. Re-imbursement of to and fro travel expenses (AC two tier) for student paper presenters from outside

Bangalore City and

c. Dearness Allowance of Rs. 1,500/- per day for maximum of five days including the journey time.

Kind Attention: CA Students

ADMISSIONS OPEN FOR SUBJECTWISE COACHING CLASSES

AT BANGALORE BRANCH OF SIRC OF ICAI

IPCC / PCC & FINAL for May 2012 Examinations and CPT for June 2012 Examinations:

Fees Timings Duration

CPT Rs.4500/- 05.30pm to 07.30pm(Monday to Friday) 09th January 2012 to03.00pm to 07.30pm(Saturday) 15th May 201207.30am to 12Noon (Sunday)

IPCC / PCC Rs.10000/- for Both Groups 06.30am to 09.30am (Monday to Saturday) 01st December 2011 toRs.8000/- for Single Group 06.00pm to 09.00pm(Monday to Saturday) 31st March 2012Rs.2000/- for Single Subject 07.30am to 05.30pm (Sunday)

Note: Depending on the availability offaculty members there may be change in

timings on Saturdays & Sundays.

FINAL Rs.10000/- for Both Groups 06.30am to 09.30am (Monday to Saturday) 01st December 2011 toRs.8000/- for Single Group 06.00pm to 09.00pm(Monday to Saturday) 31st March 2012Rs.2000/- for Single Subject 07.30am to 05.30pm (Sunday)

Note: Depending on the availability offaculty members there may be change

in timings on Saturdays & Sundays.

For schedule of classes and list of speakers please visit:www.bangaloreicai.org

>>

For Topics & Other details please visit:www.bangaloreicai.org

17 December2011

Bangalore Branch of SIRCof the Institute of Chartered Accountants of India

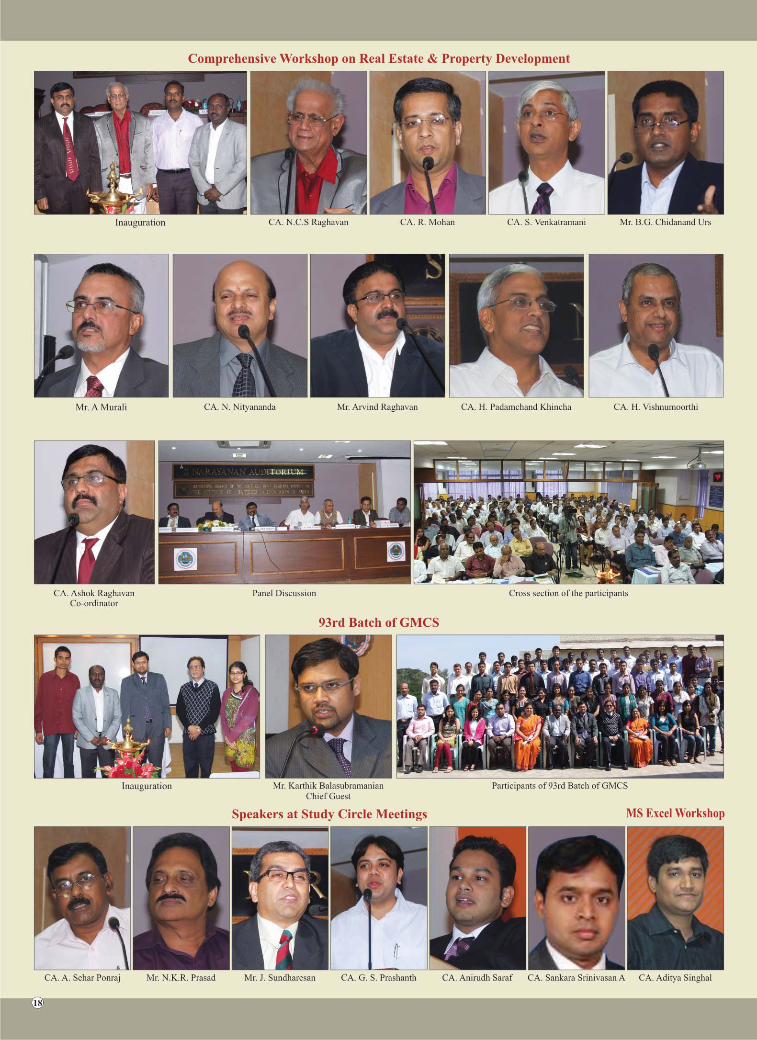

18December2011

19 December2011

Bangalore Branch of SIRCof the Institute of Chartered Accountants of India

20December2011