Embed Size (px)

Citation preview

Balancing Your BudgetBalancing Your Budget

Paying For College

• Financial Aid• FAFSA: pay attention to

deadlines!– Usually due by end of June– Priority– Numerous types of loans/grants

• Loans: must pay back, accrue interest

• Grants: don’t have to pay back

Paying For College

Scholarships• NIU Scholarship Office

– Help find scholarships (NIU & private)

– Provides computers and assistance

• Find you own!

• Not Financial Aid

Paying For College

• Parents/Relatives

• Private Loans

• Employment

• Last options: consider less hours or take semester off

What is a Budget?

• A budget is itemizing your income against your expenses for a given period.

• A budget allows you to better visualize your financial picture.

How does a Budget Help Me?

• Stay out of debt• Save for the future• Attain goals• Trim spending• Relieve Stress• Lifelong money management

skills

BUDGETING 101

The first step is to know how much money is coming in so you know how much money you can spend.

Budgeting Basics

• Determine WANTS vs. NEEDS

• Determine your goals– Short term– Long term

• Do the Math

Budgeting: Easy as 123

Step 1: Add up all of your income

Step 2: Add up all of your expenses

Step 3: Calculate the difference

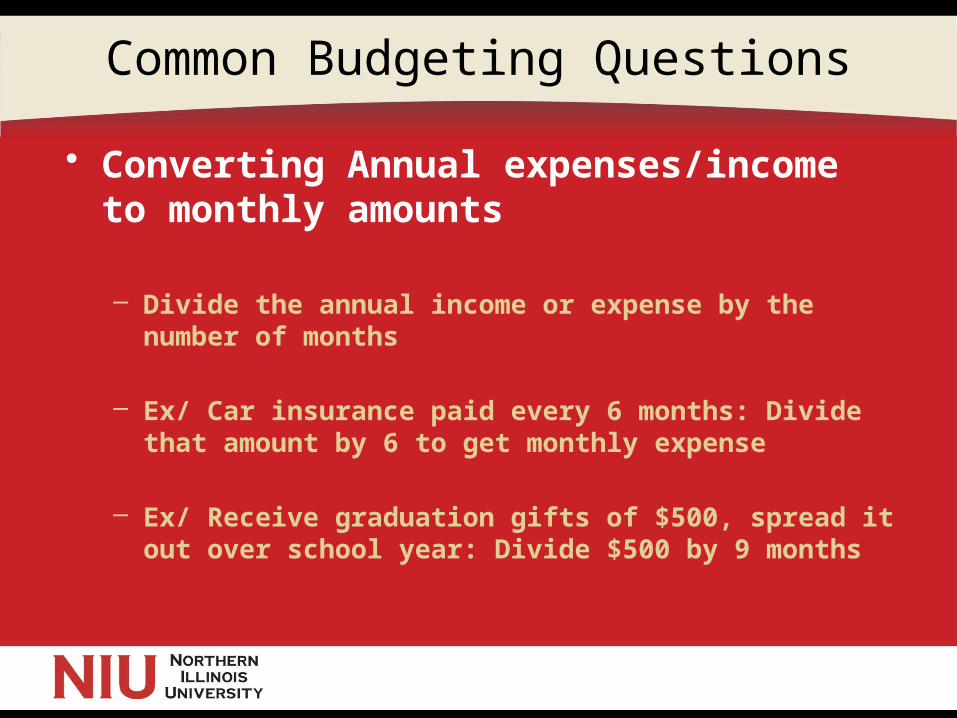

Common Budgeting Questions

• Converting Annual expenses/income to monthly amounts

– Divide the annual income or expense by the number of months

– Ex/ Car insurance paid every 6 months: Divide that amount by 6 to get monthly expense

– Ex/ Receive graduation gifts of $500, spread it out over school year: Divide $500 by 9 months

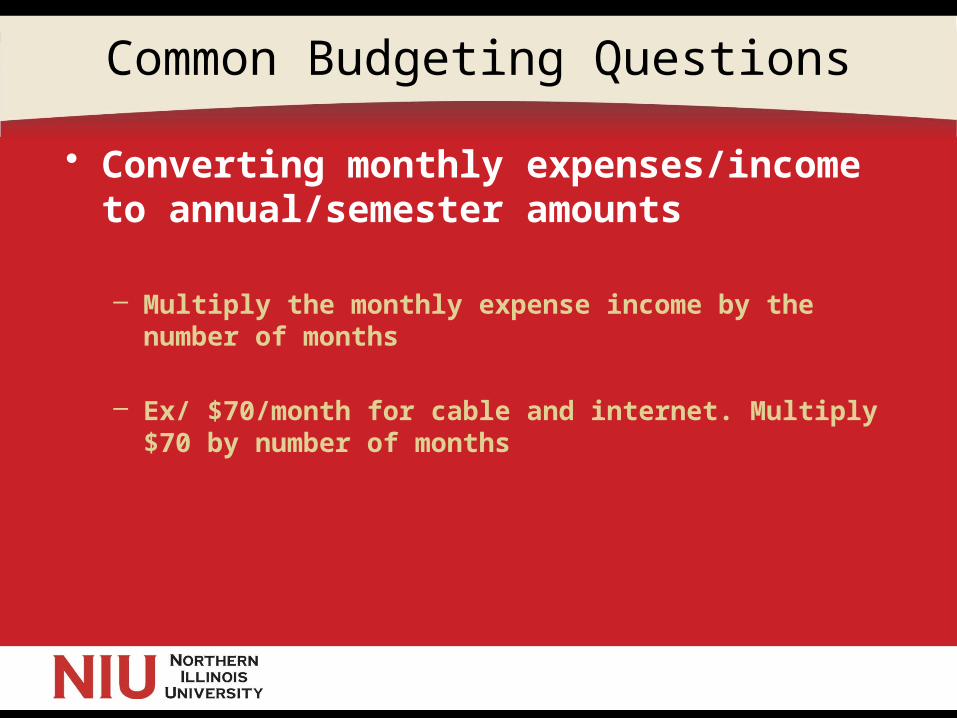

Common Budgeting Questions

• Converting monthly expenses/income to annual/semester amounts

– Multiply the monthly expense income by the number of months

– Ex/ $70/month for cable and internet. Multiply $70 by number of months

Common Budgeting Questions

• Income and Expenses change during the summer– Create a separate summer budget– Spread out savings from summer job throughout

the school year• Ex/ Save up $3000 during the summer: Divide

by 9 months to get monthly budget– When calculating yearly budget, don’t multiply

monthly expenses by 12 if you will not have those expenses year round• Ex/ $70/month for cable and internet, but

cancelling for summer months: only multiply $70 by 9 months

Budgeting Tips

• Everyone’s budget is going to be unique, so add, remove, or change any of the budget categories

• Be conservative with your estimatesWhen in doubt:

» Overestimate expenses» Underestimate income

• Start an emergency fund

Assess Goals and Expenditures

• Do your expenses exceed your income?– Bridge the gap by trimming down your

spending– Pick up a part-time job– Take out more loans– Use credit card to cover any short term gaps

• Do you have money left over after covering your expenditures?– Attain goals faster, make new goals– Start paying off student loans, invest for the

future, save for a summer trip

Money Munchers

ATM Fees Computerware Home Parties CosmeticsOnline Services Beauty Parlor Over the limit fees

Cell phones Dating Ice Cream Parking Fees

Gifts Overage Fees Bottled Water Bounced ChecksClubs

Cigarettes Greeting Cards Tanning Haircuts Movies

Cable TV Late Payment Fees Dinners Out Bar Night

Books Fast Food Attacks Dry Cleaning Car WashLottery Tickets Magazines Movie RentalsSportsLunches Out Gambling CD’s/Music Downloads

Prescriptions

Household Items Pet Costs Licenses Speeding Tickets

Cash Advance Fees Munchies Gifts Souvenirs

Track Spending

• Track your spending each month

• Compare to budgeted amounts

Importance of Saving Money

• Short-Term: – Emergency cushion: experts recommend 3-6

months worth of living expenses– Short Term goals: trips/vacations,

household purchases, new clothes, etc.

• Long-Term: Attain Financial Goals– Financing a college education– Buying a house– Buying a car– Retirement

Saving Money and Investing

• Always consult with a professional financial planner to determine your investing goals

• The value of your savings/investments is determined by 3 basic factors:– Amount of money you put in– Interest Rate– Time

• Hard to control interest rate on your investments, so focus on the amount of money you are putting in and start investing for your future early

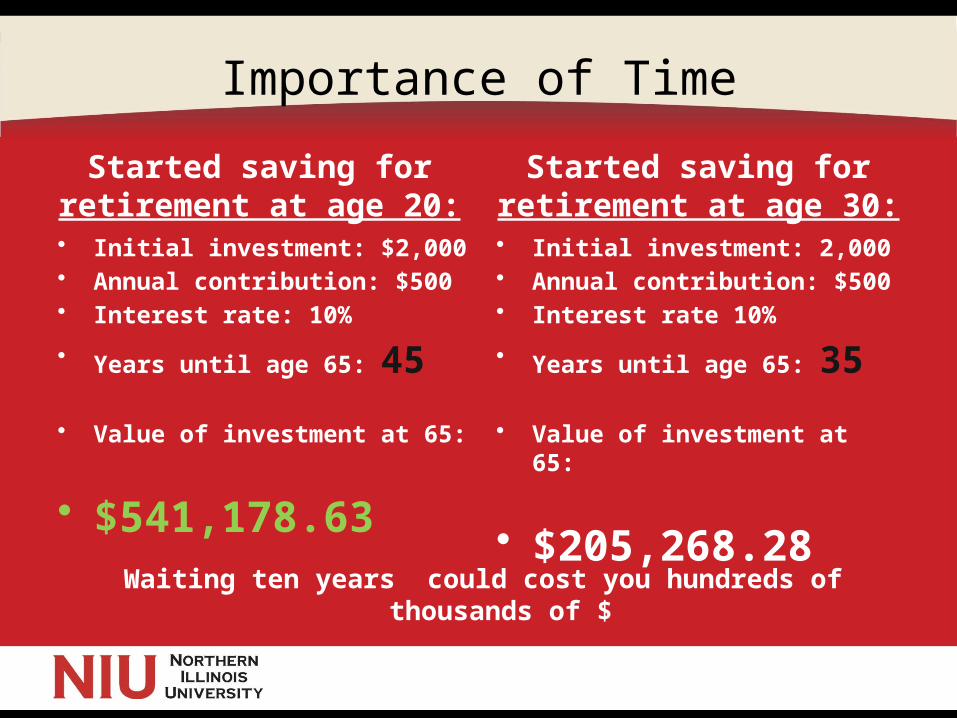

Importance of Time

Started saving for retirement at age 20:• Initial investment: $2,000• Annual contribution: $500• Interest rate: 10%

• Years until age 65: 45

• Value of investment at 65:

• $541,178.63Waiting ten years could cost you hundreds of

thousands of $

Started saving for retirement at age 30:• Initial investment: 2,000• Annual contribution: $500• Interest rate 10%

• Years until age 65: 35

• Value of investment at 65:

• $205,268.28

Saving Money

• First – Make a goal

• Understand the sacrifices needed to attain that goal

• Develop a timeframe

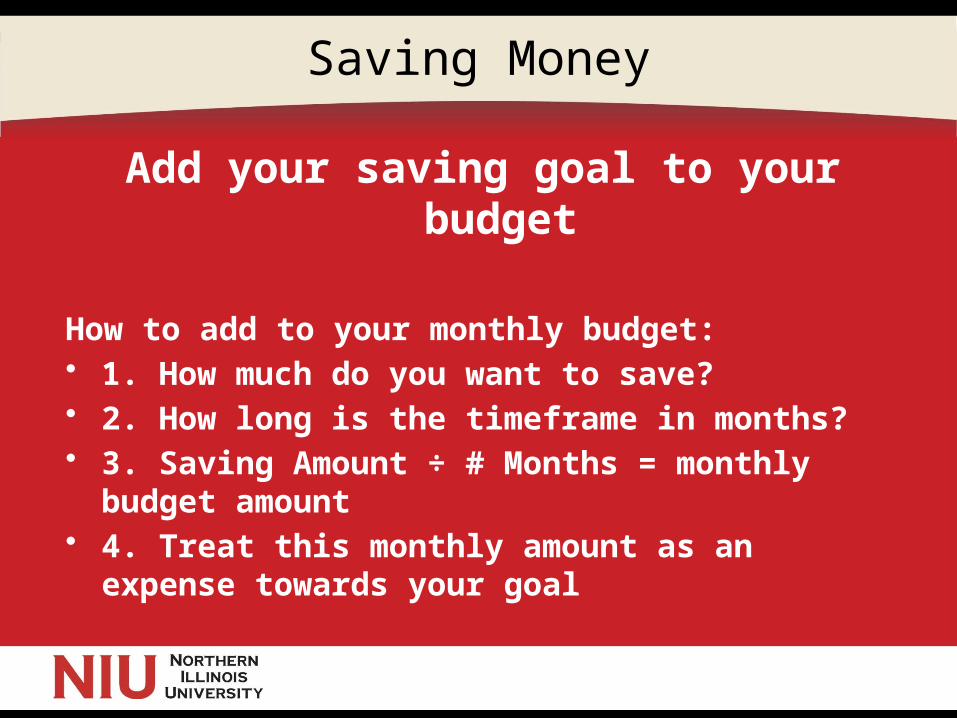

Saving Money

Add your saving goal to your budget

How to add to your monthly budget:• 1. How much do you want to save?• 2. How long is the timeframe in months?• 3. Saving Amount ÷ # Months = monthly

budget amount• 4. Treat this monthly amount as an expense

towards your goal

Money Saving Tips

• Try generic brands

• Master the ten second rule

• Take public transportation

• Go to a matinee

• Make your own coffee

• Save your coins!

• Start emergency fund

• Use ebay/craigslist/freecycle

Credit

WHAT IS CREDIT?$ It is a loan

$ It is an agreement

$ It comes with fees, interests& other

charges

Credit is a debt; it is NOT income!!!

Build Your Credit

• Credit is called “your second resume”

• Information stays on your credit report for seven years

• Your credit rating is your reputation

FICO Score

FICO Scores are calculated from a lot of different credit data in your credit report. This data can be grouped into five categories as outlined below. The percentages in the chart reflect how important each of the categories is in determining your FICO score.

FICO Score / Credit Score

Like your GPA, the higher your FICO score, the better!

• FICO Scores range from 300-850

– 680 and higher = prime borrower

– 550 and below = lots of work to do!

Getting a Good Credit Score

• Keep account balances well below 50% of your available credit

• Think twice about co-signing

• Avoid Excessive inquiries

• Pay your bills on time

A good FICO score of 750+ can mean your interest rate on a home loan will be 4 percentage points lower than somebody with a 500 score. This can mean over $200,000 in saved interest on a house.

Debit Cards

• Allow access to checking account via ATMs

• Amount is deducted from checking account

• Not a charge card, must have the funds available NOW

Charge cards vs Credit Cards

Charge Cards• must be paid in full every month (AMEX)• provides convenience of not having to pay

for purchases with cash, but balance may not be carried over month-to-month

Credit Cards• operate on a credit limit and revolving

basis• if not paid-in-full within grace period,

interest is charged on the remaining balance

Paper or Plastic?

Credit Cards

• Interest rate fees--17% - 21% for students

• Annual fee

• Over the limit fees

• Late payment fees

• Transaction fees

Adding it all up…

Table 1: Minimum Repayment Schedule on a $2,000 Credit Card Loan at 19 Percent Monthly minimum payment amount

Number of months to repay

Total interest payment

$40 100 $1,994

$50 64 $1,193

$75 35 $619

$100 25 $424

Source: Credit Card Minimum Payment Interest Calculator, Daniel C. Peterson, www.webwinder.com

Interest savings between lowest/highest payment = $1,570;time saved = 75 months or 6.25 years!

Signs of High Risk Credit Card Use

• Average credit card balances over $1,000

• Owning four or more credit cards

• Carrying a balance each month

• Using credit cards to charge tuition or fees

Credit Card Don’ts

• Don’t get more than one

• Don’t use them for cash advances

• Don’t use them to pay for basics: rent, groceries, etc.

• Don’t charge more than you can pay off in a month

• Don’t let banks increase you credit limit

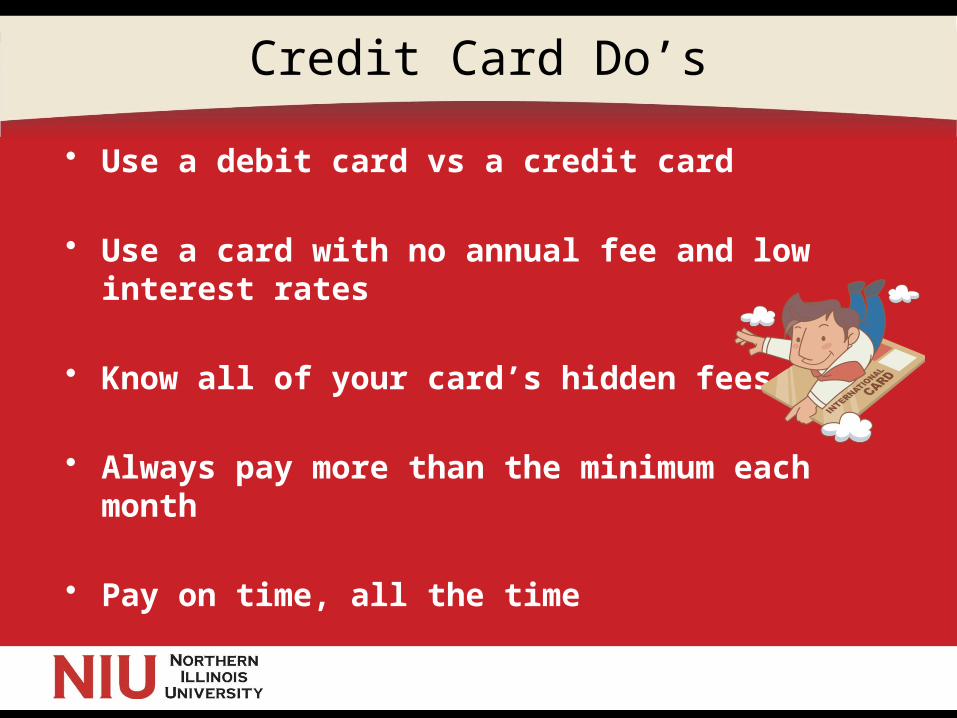

Credit Card Do’s

• Use a debit card vs a credit card

• Use a card with no annual fee and low interest rates

• Know all of your card’s hidden fees

• Always pay more than the minimum each month

• Pay on time, all the time

Good vs Bad Debt

Good debt is debt that returns something of long term value

Bad debt is often categorized as short-term “feel good” debt and may be unwise purchases that you can’t afford and don’t really

need.

Debt Warning Signs

• Living from paycheck to paycheck• Making late, minimum, or skipping

payments• Having credit cards at or near your credit

limit• Arguing with family or friends over your

spending habits• Being unsure of how much you really owe• Using cash advances to pay your bills• Having your credit card declined• Having increasingly more of your income

paying for debts each month

Relationship-Secured Support

FAMILY & FRIENDS

• Keep open lines of communication

• Treat family members and financial members w/ great respect

bankruptcy

• Goes on your record for 10 years

• May hurt parent’s credit rating if co-signed

• Can keep you from getting a mortgage for a house, credit at reasonable rates, a

job, or from being promoted

It does not discharge student loans, child support, secured debt, or income taxes

Solutions

• Develop a budget & live within your means

• Redefine the good life your own way

• List your short-term financial obligations and goals for each month, for the year, and future 5 years

• Focus on paying on the balance with the highest

interest rate

• Lose the credit cards

• Consolidate student loans

Become a Peer educator!

• What is Financial Cents?

• Opportunities to Get Involved-Marketing Team, Collaboration Team, Junior

Achievement

• Why Get Involved?– Enhance your leadership skills– Build teamwork– Build your resume– Help the NIU community