Embed Size (px)

Citation preview

8/3/2019 Balance Sheet Recession Basics

http://slidepdf.com/reader/full/balance-sheet-recession-basics 1/15

Balance Sheet Recession Basics – Not Your Father’s Economic Cycle

The Situation

Europe, UK and the US are all currently mired in a Balance Sheet Recession (BSR).A term for the current “rare disease” the global economy is suffering from coined byRichard Koo in his seminal book “The Holy Grail of Macroeconomics” where heprovides a blueprint for our current malaise and provides what I think is the mostcomprehensive solution to date. This is my attempt to use his template, laid out in thebook, to look at our world today. I am not an economist, for that I am grateful, but if I’m wrong on anything please do correct me!

The length of time it takes for the various countries to emerge from their BSR willdepend on the policy responses enacted in each economic zone. One precedent is

provided by the Great Depression where it took 30 years, from 1929 to 1959 beforeinterest rates returned to their average level of the 1920s. These are once in ageneration events and we have never had one affecting such a large bloc of GlobalGDP simultaneously.

What is a Balance Sheet Recession?

“To understand the Great Depression was the Holy Grail of Macroeconomics” BenBernanke

A Balance Sheet Recession comes to pass when a plunge in asset prices damagesprivate sector balance sheets so badly as to bring about a shift in the mindset andpriorities of the asset owners; from profit maximisation to debt minimisation; andfrom forward looking to backward looking. When the value of assets like equities andreal estate falls but the loans used to purchase them remain, borrowers findthemselves with a negative net worth and in a struggle to survive.

As with the asset bubbles that precede them, Balance Sheet Recessions are rare andprolonged events. When they do happen, they render useless the standard economicpolicy responses taught in universities and practiced by Investment Bankers andCentral Bankers globally.

In Japan, as today in the US, UK and Europe, we have a situation where manycorporate and personal balance sheets are underwater but “core operations” for mostcompanies and families remain reasonably robust – profits are healthy and cashflow/incomes are solid. In this situation, any rational actor will commit

themselves to diligently repaying their debt and adding low risk assets to repair

their balance sheet as quickly as possible.

A nationwide plunge in asset prices eviscerates the asset side of the balance sheet butleaves the liabilities intact. The entire economy experiences a “fallacy of

composition” which means an action that is most appropriate for each individual

becomes ruinous if everyone engages in it at once. In this example, we mean repairingbalance sheets.

8/3/2019 Balance Sheet Recession Basics

http://slidepdf.com/reader/full/balance-sheet-recession-basics 2/15

Koo’s example is as follows – a household earns $1,000 and spends $900, saving$100. The $900 spent becomes someone else’s income and circulates in the economy,the $100 goes to a bank where it is then lent out to individuals or corporates whichwould then spend or invest it, circulating it back into the economy. Thereforespending and savings both continue to circulate – keeping the $1,000 “in play”. If

there are no willing borrowers for the $100 then the banks will lower the interest ratethey charge until the demand is created.

But in Japan and in the Great Depression, and to some extent now, there is no demandfor the $100 despite interest rates at 300 year lows.

The $100 just sits in the bank being neither borrowed nor spent. Only $900 is spent inthe economy and the next household receives only that $900 of which it saves 10% tothe bank, which again cannot lend that $90 because there is no loan demand so it stays

as reserves. The next household receives only $810 in income and so on. This is adeflationary spiral which would serve only to exacerbate falls in asset prices makingbalance sheets worse rather than better.

Add to this simple model the additional problem of corporates also in balance sheetrepair mode and you have an idea of the problem faced. The economy loses demand

equivalent to the sum of net household savings and net corporate debt

repayment each year.

This is exactly what happened in the Great Depression taking Gross National Productdown by almost 50% in 4 years.

According to Koo, the only solution for this problem is for sustained fiscal policysupport via direct government borrowing and spending on real projects to keep theeconomy afloat whilst private sector balance sheets are fully repaired.

How do we know we are in a Balance Sheet Recession?

1. Private Sector is Paying Down Debt

2. Monetary Policy is Impotent3. Quantitative Easing Doesn’t Work 4. Silent and Invisible5. Debt Rejection Syndrome

1. Private Sector is Paying Down Debt

Now, as in Japan, it was argued by many that the banking sector was primarilyresponsible for the recession. It is believed that a struggling banking sector is choking

off the flow of money to the economy – we see this in politicians jawboning about“forcing banks to lend to businesses so they can invest” and so on.

8/3/2019 Balance Sheet Recession Basics

http://slidepdf.com/reader/full/balance-sheet-recession-basics 3/15

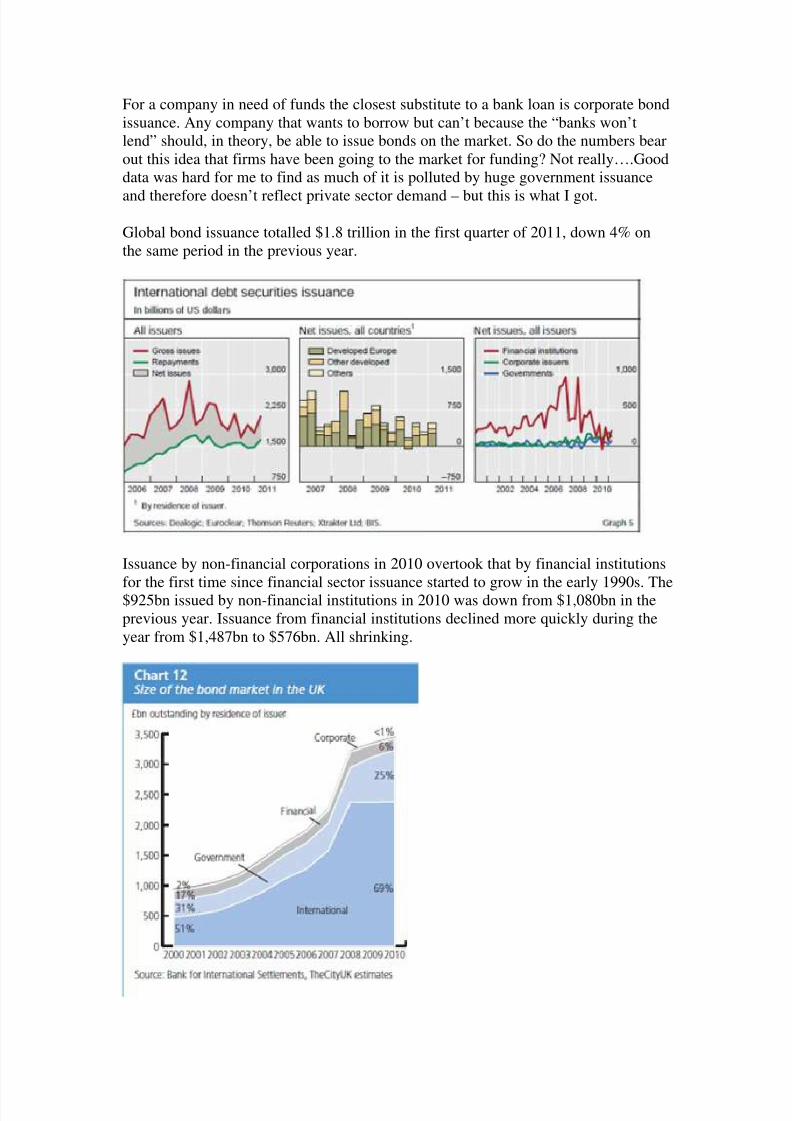

For a company in need of funds the closest substitute to a bank loan is corporate bondissuance. Any company that wants to borrow but can’t because the “banks won’tlend” should, in theory, be able to issue bonds on the market. So do the numbers bearout this idea that firms have been going to the market for funding? Not really….Gooddata was hard for me to find as much of it is polluted by huge government issuance

and therefore doesn’t reflect private sector demand – but this is what I got.

Global bond issuance totalled $1.8 trillion in the first quarter of 2011, down 4% onthe same period in the previous year.

Issuance by non-financial corporations in 2010 overtook that by financial institutions

for the first time since financial sector issuance started to grow in the early 1990s. The$925bn issued by non-financial institutions in 2010 was down from $1,080bn in theprevious year. Issuance from financial institutions declined more quickly during theyear from $1,487bn to $576bn. All shrinking.

8/3/2019 Balance Sheet Recession Basics

http://slidepdf.com/reader/full/balance-sheet-recession-basics 4/15

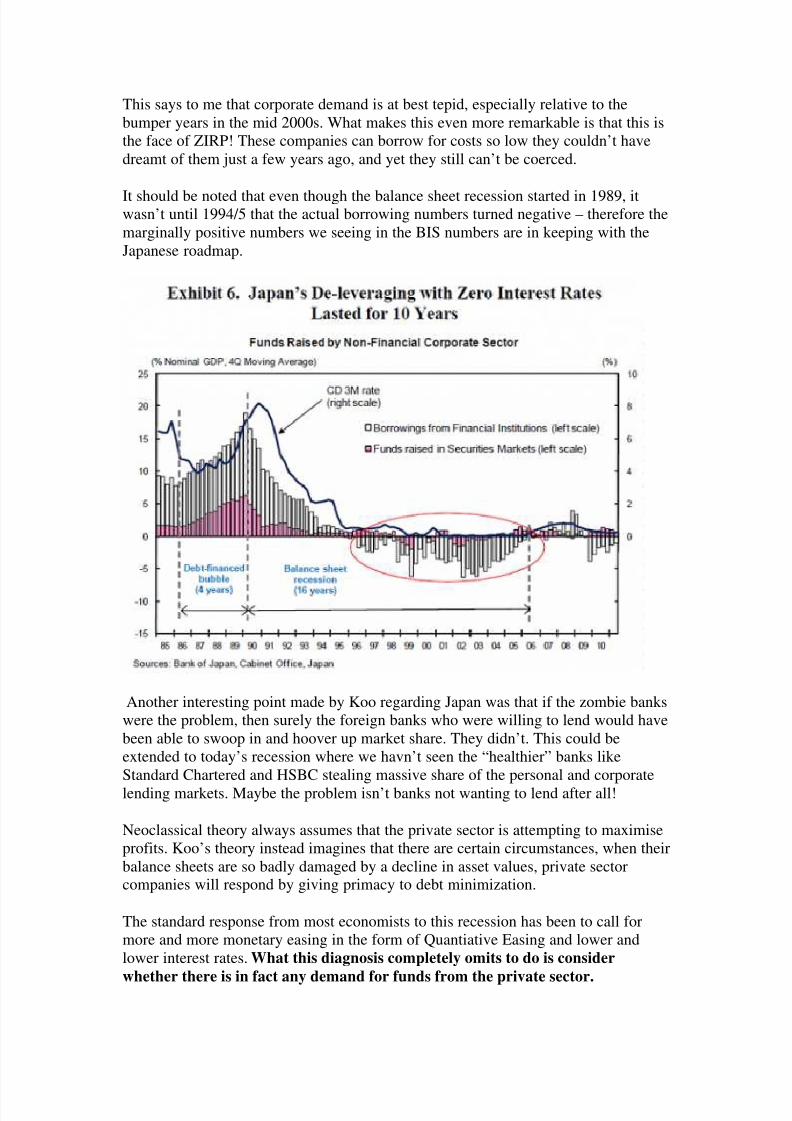

This says to me that corporate demand is at best tepid, especially relative to thebumper years in the mid 2000s. What makes this even more remarkable is that this isthe face of ZIRP! These companies can borrow for costs so low they couldn’t havedreamt of them just a few years ago, and yet they still can’t be coerced.

It should be noted that even though the balance sheet recession started in 1989, itwasn’t until 1994/5 that the actual borrowing numbers turned negative – therefore themarginally positive numbers we seeing in the BIS numbers are in keeping with theJapanese roadmap.

Another interesting point made by Koo regarding Japan was that if the zombie bankswere the problem, then surely the foreign banks who were willing to lend would havebeen able to swoop in and hoover up market share. They didn’t. This could beextended to today’s recession where we havn’t seen the “healthier” banks likeStandard Chartered and HSBC stealing massive share of the personal and corporatelending markets. Maybe the problem isn’t banks not wanting to lend after all!

Neoclassical theory always assumes that the private sector is attempting to maximiseprofits. Koo’s theory instead imagines that there are certain circumstances, when theirbalance sheets are so badly damaged by a decline in asset values, private sectorcompanies will respond by giving primacy to debt minimization.

The standard response from most economists to this recession has been to call formore and more monetary easing in the form of Quantiative Easing and lower andlower interest rates. What this diagnosis completely omits to do is consider

whether there is in fact any demand for funds from the private sector.

8/3/2019 Balance Sheet Recession Basics

http://slidepdf.com/reader/full/balance-sheet-recession-basics 5/15

A recession as prolonged and pronounced as the one we are currently in can only becompared with Japan since 1989 and the Great Depression. Unfortunately, the samplesize is small because this “condition” is extremely rare.

Japanese companies have spent the last 15 years paying down debt at a time when

interest rates are at zero. From the perspective of an IMF economist, Treasury Policyadvisor or a investment bank economist, this makes no sense. As loan rates fall,demand for loans is not increasing. This is madness!

If you are profit maximising, as the private sector is always assumed to be, then theonly reason you would pay down debt at zero interest rates is if you have nopossibility of making a positive return on your investments – if that’s the case, are youa going concern?

What this persistent paying down of debt in the face of their education andeconomist’s expectations demonstrates is that the private sector no longer has “profit

maximisation” as its main goal – now the goal is debt minimisation. It’s a massive,secular swing in mindset.

Loans to private businesses in Europe grew at just a 1.7% rate in November, a

plunge from October’s 2.7% and missing expectations of 2.6% by a wide margin.Corporate credit is being turned off. This has happened even as the ECB’s balancesheet has risen from EUR 1.9 trillion to EUR 2.7 trillion in 6 months is trulyremarkable.

Reuters said “Loans to private sector firms in the euro zone fell in November while

growth in lending to households slowed, European Central Bank data showed on

Thursday, adding to the case for an interest rate cut. The drop in funding to

companies increased fears that the region faces a looming credit crunch, an issue

of growing concern for the ECB as the worsening sovereign crisis makes firms and

households increasingly wary about taking on debt, weighing on the economic outlook.

In an attempt to kick-start loan activity, the 17-country bloc’s central bank conducted

last week its first-ever three-year funding operation, which saw banks take up almost

half a trillion Euros.”

2. Monetary Policy is Impotent

Governments are supposed to manage economies with monetary and fiscal policy butone of the key characteristics of these rare balance sheet recessions is that monetarypolicy becomes useless. The Bank of Japan kept interest rates at near zero from 1995to 2005 but yet the economy did not recover and stock markets did not rally.

The reason for this is one of the key assumptions of monetary policy is not applicablein a balance sheet recession. The assumption that the private sector always has willing

8/3/2019 Balance Sheet Recession Basics

http://slidepdf.com/reader/full/balance-sheet-recession-basics 6/15

borrowers that will respond to a change in the price of credit. Lower interest rates andthe number of borrowers will increase and economic activity will pick up. When thereare no borrowers the bank is powerless.

As explained above, if the mechanism of recycling savings back into the economy isbroken then the government must do something to stop the vicious cycle. Thegovernment must do the opposite of the private sector, it must borrow andspend/invest the savings that the private sector is no long demanding to use as loans(the $100 in our example.).

Japan has avoided depression like conditions because the government has, on thewhole, borrowed and spent what the private sector would not have. When the privatesector is paying down debt, only public sector borrowing and spending can prevent acontraction.

When firms and households are minimizing debt the government is the only netborrower left in the economy and therefore the money supply will contract unlessfiscal policy is expansionary.

3. Quantitative Easing Doesn’t Work

Because today’s economists are all trained to think the same way, to assume privatesector profit maximisation, they assume that if interest rates are low enough then theywill borrow and invest. This clearly isn’t happening. In today’s world we keephearing that corporate balance sheets are awash with cash (no-one ever mentions theliabilities on the other side.) but this is a reflection of fear and uncertainty on the partof company management – they are not investing and they are certainly not borrowingto invest.

“Imagine a patient who takes a drug prescribed by her doctor but does not react as

the doctor expected, and more importantly does not get better. When she reports back,

he tells her to double the dosage, but this does not help either. So he orders her to

take four times, eight times, and finally a hundred times the original dosage. All to no

avail. Any normal human being would come to the conclusion that the originaldiagnosis was wrong and the patients suffered from a different disease.” Page 74

4. Silent & Invisible

No-one wants to talk about a BSR. Those with the closest knowledge of the situationare incentivised to keep quiet about it. Corporate CEOs and indebted households donot want to draw attention to their underwater balance sheets because this might maketheir situation worse as investors or creditors attempt to call in loans and bring a slowburning situation to a resolution.

On the other side, banks do not want to draw attention to their decimated loan books,their technically insolvent borrowers or mortgages that are in negative equity. If the

8/3/2019 Balance Sheet Recession Basics

http://slidepdf.com/reader/full/balance-sheet-recession-basics 7/15

payments are being met and the borrowers remain cash flow positive then both partiescan “mark to make believe” and “extend & pretend”. Of course ZIRP helps ease thisprocess too.

5. Debt Rejection Syndrome

The generation that survived the Depression has a reputation for a life time of debtrepudiation. Those who have been indebted and then suffered through years of hardwork to repair their balance sheets are left with a revulsion of debt even after theirbalance sheets have been returned to health. I believe it will take a great deal of timebefore the Anglo Saxon economies become as comfortable with debt, especially debtused for consumption, as they were in the last few years.

How do we fix The Balance Sheet Recession and why?

“That’s all it takes, really. Pressure, and time.” Red in Shawshank Redemption

Time, low interest rates and not having to mark assets to market help, but theeconomy needs more support than these things which are usually enough to restore acyclical recession to growth.

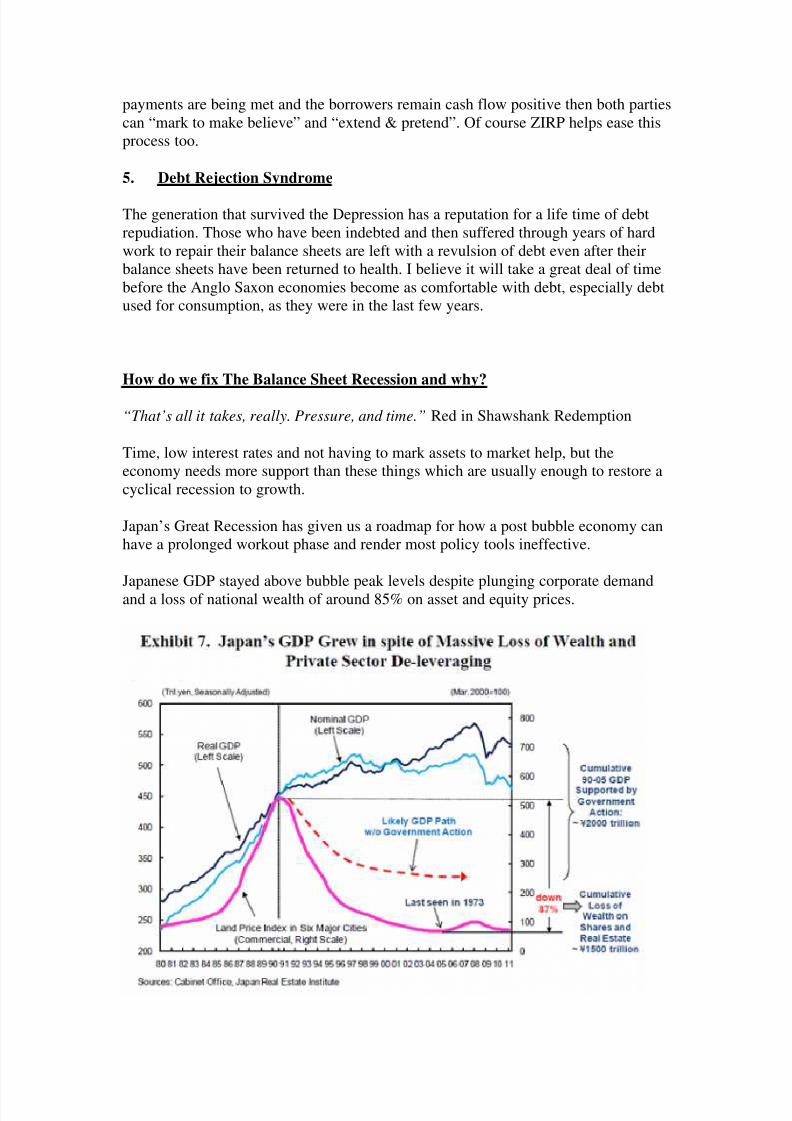

Japan’s Great Recession has given us a roadmap for how a post bubble economy canhave a prolonged workout phase and render most policy tools ineffective.

Japanese GDP stayed above bubble peak levels despite plunging corporate demandand a loss of national wealth of around 85% on asset and equity prices.

8/3/2019 Balance Sheet Recession Basics

http://slidepdf.com/reader/full/balance-sheet-recession-basics 8/15

Here we have to imagine the counter-factual, which is never easy. The fact that GDPgrew in the face of such precipitous asset declines may be viewed as a success. Koosays

“In a Hollywood world, the hero is the one who saves hundreds of lives after the

crisis has erupted and thousands have died.

But if a wise individual recognizes the danger in advance and successfully acts to

avert the calamity, there is no story, no hero and no movie…..Japan successfully

avoided economic apocalypse for fifteen years. But from the perspective of the media,

which has never grasped the essence of the problem, the government spent 140

trillion yen and nothing happened. So they twisted the story to imply the government

wasted the money.”

So Koo is saying it was only because the government engaged in fiscal stimulus to theextent that it did that stopped a collapse in Japan’s GDP and in its standard of living.

Imagine if the S&P 500 or FTSE 100 fell 80% from its current level over the next 15years and the average home price was circa $20,000 – do you think we’d have hadpositive GDP growth!?

If this is the case, and the Japanese government more or less did a great job, then doesthat mean that a Japanese scenario is close to our best case scenario too? A scarythought indeed.

“A balance sheet recession is characterised by a deflationary gap equal to household

savings plus net corporate debt repayment.” page 67

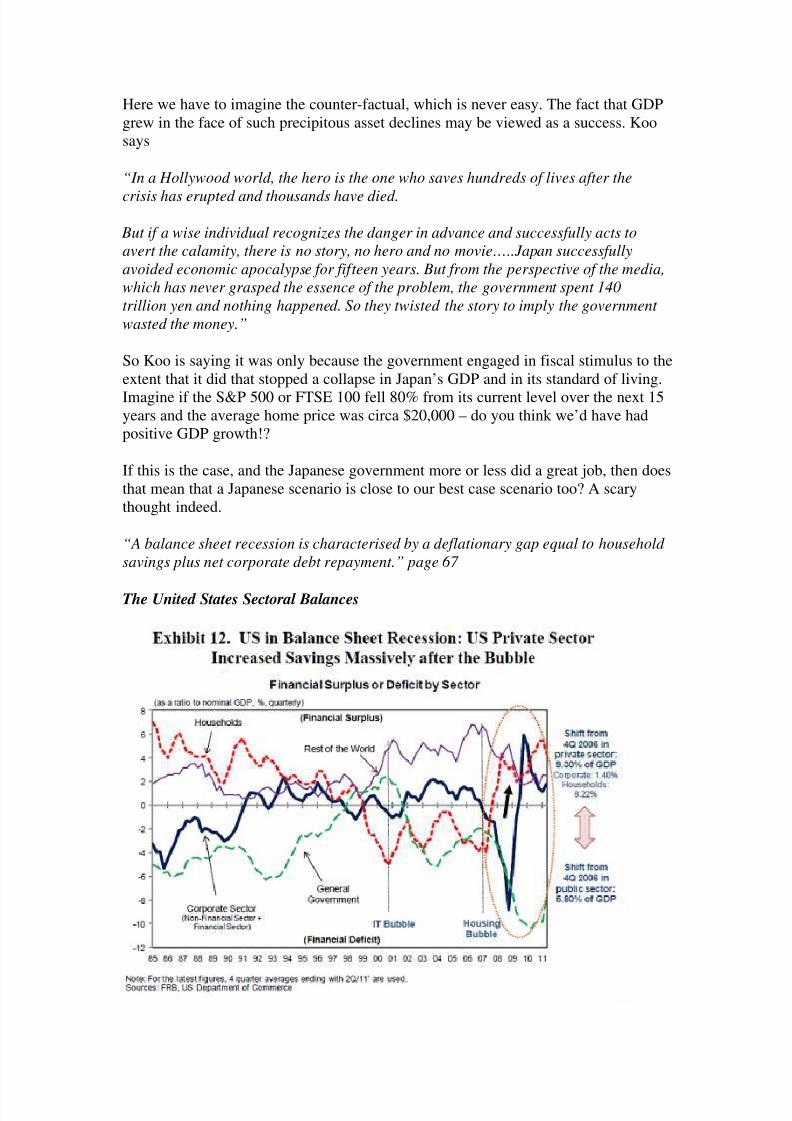

The United States Sectoral Balances

8/3/2019 Balance Sheet Recession Basics

http://slidepdf.com/reader/full/balance-sheet-recession-basics 9/15

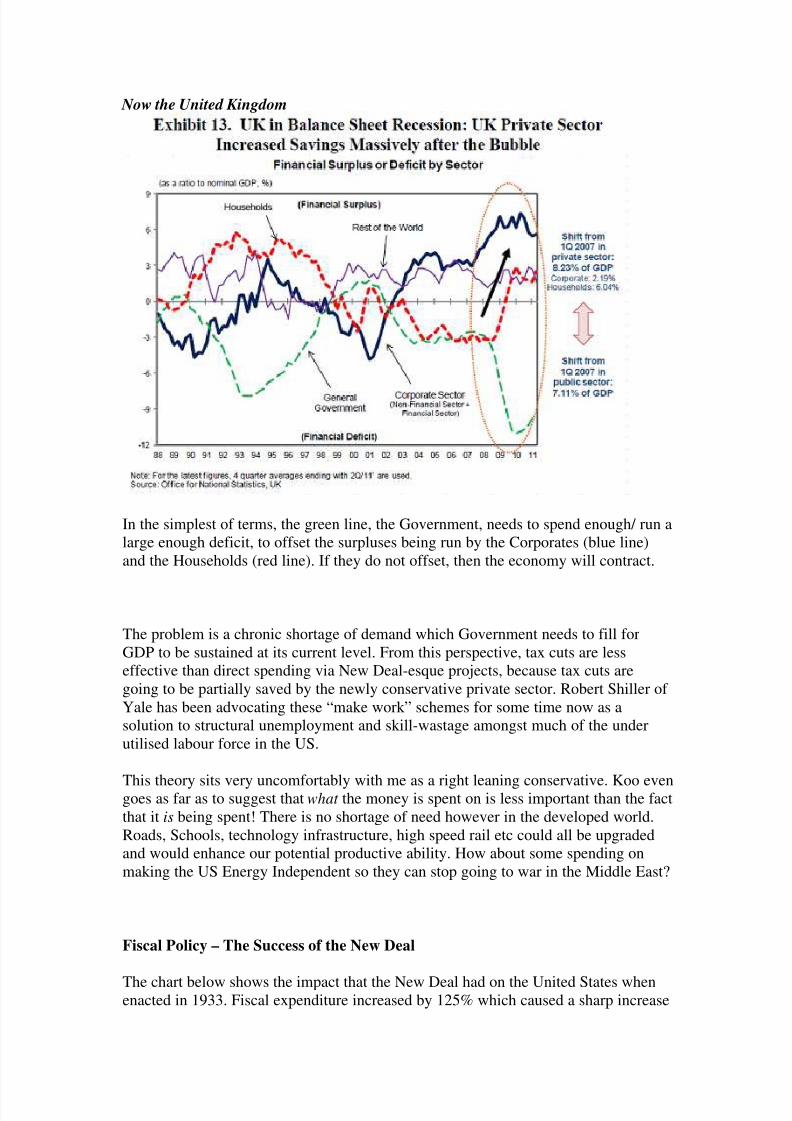

Now the United Kingdom

In the simplest of terms, the green line, the Government, needs to spend enough/ run alarge enough deficit, to offset the surpluses being run by the Corporates (blue line)and the Households (red line). If they do not offset, then the economy will contract.

The problem is a chronic shortage of demand which Government needs to fill forGDP to be sustained at its current level. From this perspective, tax cuts are lesseffective than direct spending via New Deal-esque projects, because tax cuts aregoing to be partially saved by the newly conservative private sector. Robert Shiller of Yale has been advocating these “make work” schemes for some time now as asolution to structural unemployment and skill-wastage amongst much of the underutilised labour force in the US.

This theory sits very uncomfortably with me as a right leaning conservative. Koo evengoes as far as to suggest that what the money is spent on is less important than the factthat it is being spent! There is no shortage of need however in the developed world.Roads, Schools, technology infrastructure, high speed rail etc could all be upgradedand would enhance our potential productive ability. How about some spending onmaking the US Energy Independent so they can stop going to war in the Middle East?

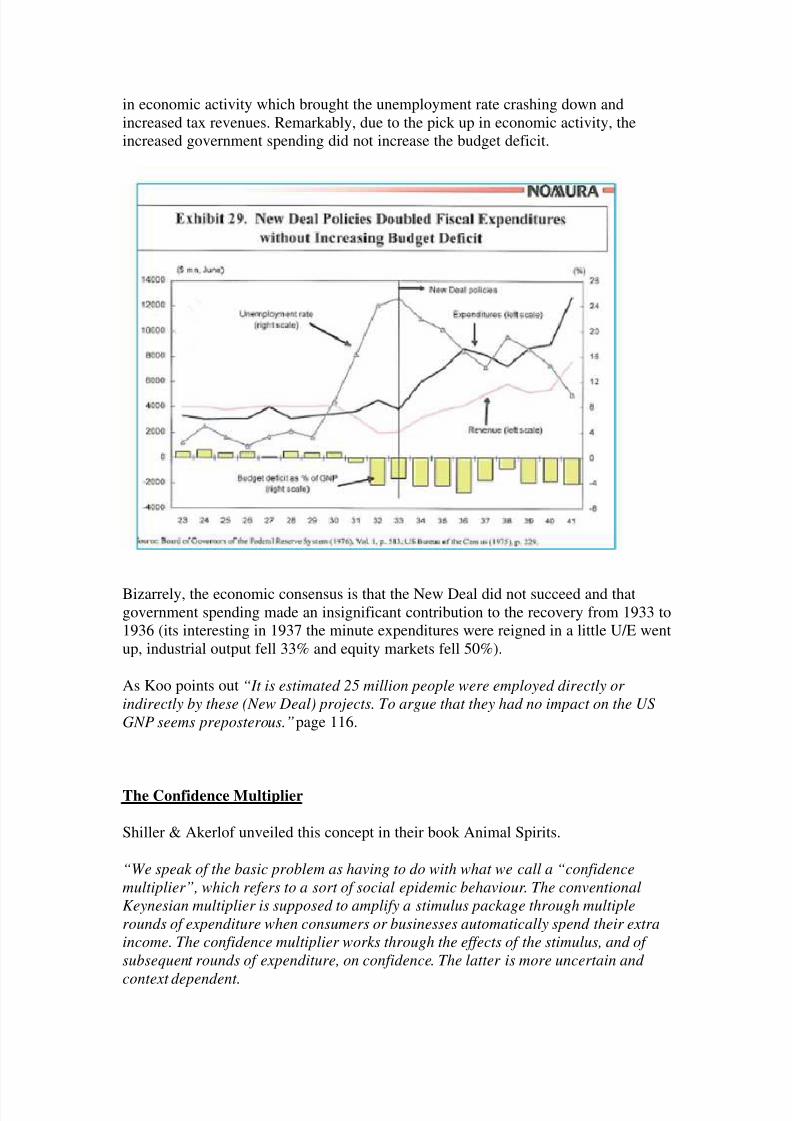

Fiscal Policy – The Success of the New Deal

The chart below shows the impact that the New Deal had on the United States whenenacted in 1933. Fiscal expenditure increased by 125% which caused a sharp increase

8/3/2019 Balance Sheet Recession Basics

http://slidepdf.com/reader/full/balance-sheet-recession-basics 10/15

in economic activity which brought the unemployment rate crashing down andincreased tax revenues. Remarkably, due to the pick up in economic activity, theincreased government spending did not increase the budget deficit.

Bizarrely, the economic consensus is that the New Deal did not succeed and thatgovernment spending made an insignificant contribution to the recovery from 1933 to1936 (its interesting in 1937 the minute expenditures were reigned in a little U/E wentup, industrial output fell 33% and equity markets fell 50%).

As Koo points out “It is estimated 25 million people were employed directly or

indirectly by these (New Deal) projects. To argue that they had no impact on the US

GNP seems preposterous.”page 116.

The Confidence Multiplier

Shiller & Akerlof unveiled this concept in their book Animal Spirits.

“We speak of the basic problem as having to do with what we call a “confidence

multiplier”, which refers to a sort of social epidemic behaviour. The conventional

Keynesian multiplier is supposed to amplify a stimulus package through multiple

rounds of expenditure when consumers or businesses automatically spend their extra

income. The confidence multiplier works through the effects of the stimulus, and of

subsequent rounds of expenditure, on confidence. The latter is more uncertain and

context dependent.

8/3/2019 Balance Sheet Recession Basics

http://slidepdf.com/reader/full/balance-sheet-recession-basics 11/15

These other considerations highlight the difficulties that governments will have in

changing this wait-and-see behaviour (current poor sentiment/debt minimisation), and suggest different concerns about just how to structure a stimulus package.

Different kinds of stimulus have different effects on confidence, depending on how

they are viewed and interpreted by the public. The focus has to get off of “what

fraction of this stimulus will be spent” to “how does this stimulus affect confidence”.

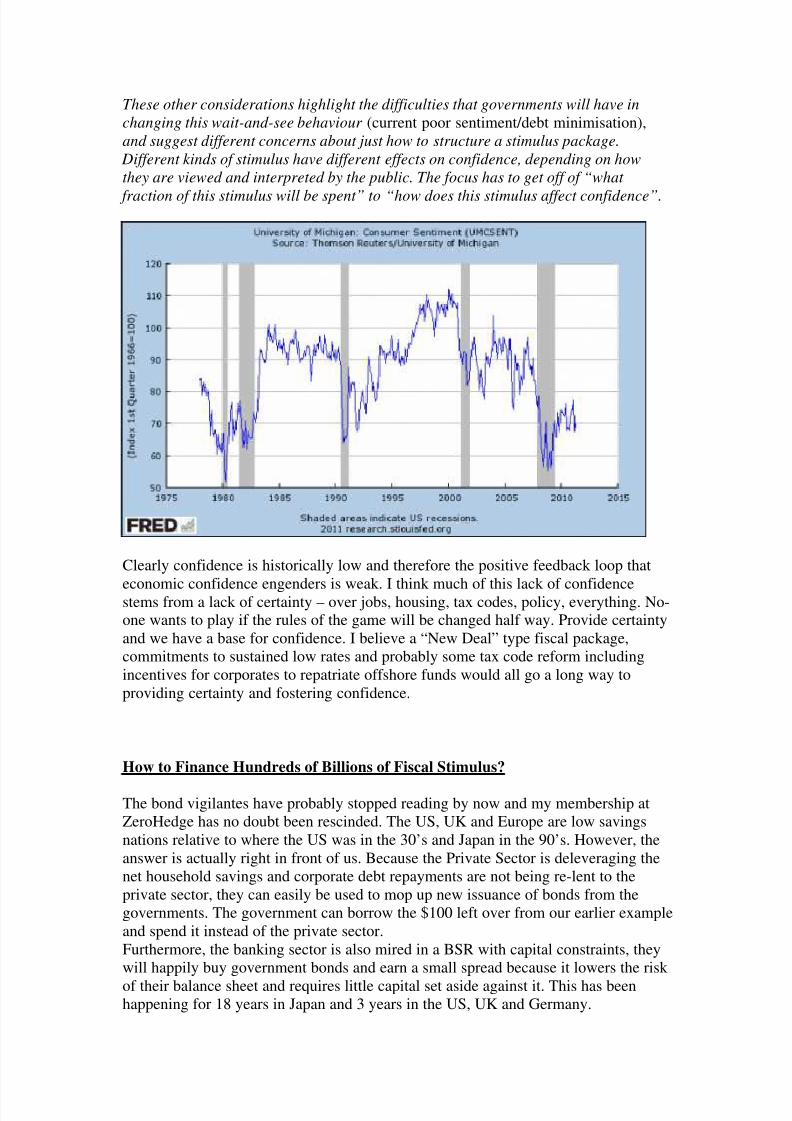

Clearly confidence is historically low and therefore the positive feedback loop that

economic confidence engenders is weak. I think much of this lack of confidencestems from a lack of certainty – over jobs, housing, tax codes, policy, everything. No-one wants to play if the rules of the game will be changed half way. Provide certaintyand we have a base for confidence. I believe a “New Deal” type fiscal package,commitments to sustained low rates and probably some tax code reform includingincentives for corporates to repatriate offshore funds would all go a long way toproviding certainty and fostering confidence.

How to Finance Hundreds of Billions of Fiscal Stimulus?

The bond vigilantes have probably stopped reading by now and my membership atZeroHedge has no doubt been rescinded. The US, UK and Europe are low savingsnations relative to where the US was in the 30’s and Japan in the 90’s. However, theanswer is actually right in front of us. Because the Private Sector is deleveraging thenet household savings and corporate debt repayments are not being re-lent to theprivate sector, they can easily be used to mop up new issuance of bonds from thegovernments. The government can borrow the $100 left over from our earlier exampleand spend it instead of the private sector.Furthermore, the banking sector is also mired in a BSR with capital constraints, theywill happily buy government bonds and earn a small spread because it lowers the risk

of their balance sheet and requires little capital set aside against it. This has beenhappening for 18 years in Japan and 3 years in the US, UK and Germany.

8/3/2019 Balance Sheet Recession Basics

http://slidepdf.com/reader/full/balance-sheet-recession-basics 12/15

Koo adds a further insight….

“The low yields on government debt are also the market’s way of telling the

government that if there is anything to be done with taxpayer’s money, now is the time

to do it…The market is imploring governments to undertake such projects NOW for

the sake of both the economy and taxpayers.” Page 267

Why can’t we have inflation?

Quantitative Easing improves the liquidity sloshing around the banking system, itdoes not improve the solvency of the institutions.

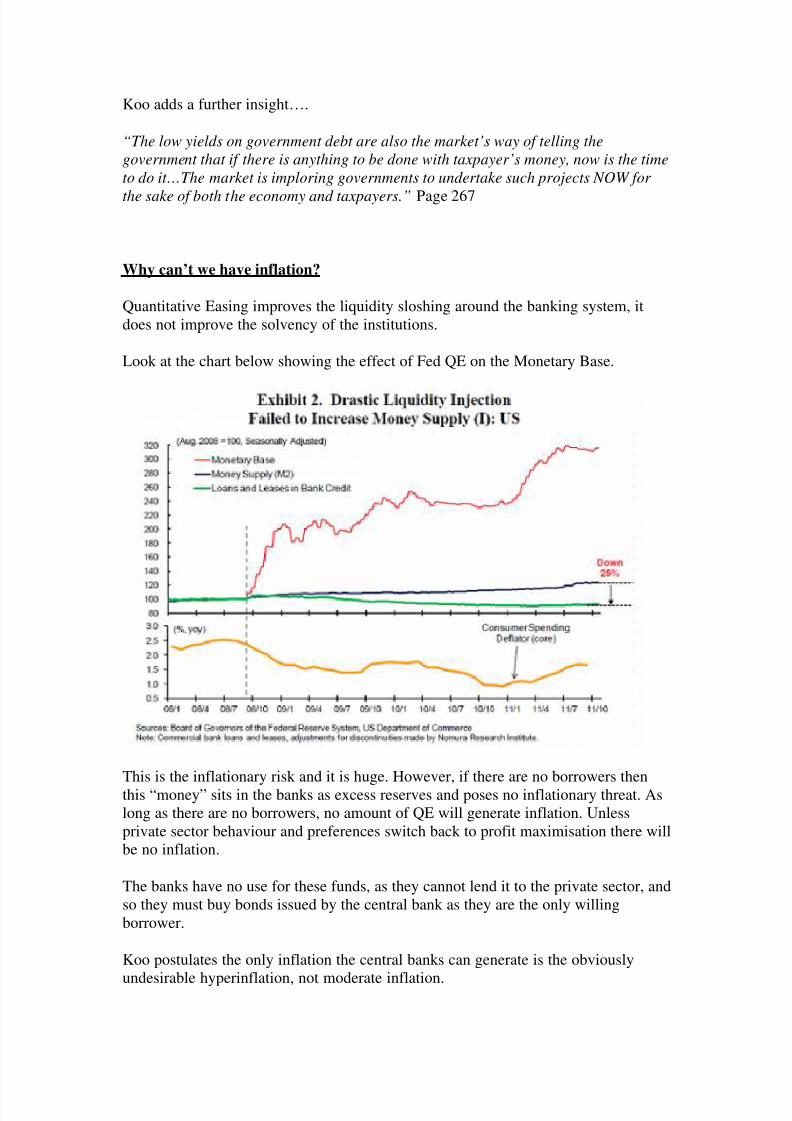

Look at the chart below showing the effect of Fed QE on the Monetary Base.

This is the inflationary risk and it is huge. However, if there are no borrowers thenthis “money” sits in the banks as excess reserves and poses no inflationary threat. Aslong as there are no borrowers, no amount of QE will generate inflation. Unlessprivate sector behaviour and preferences switch back to profit maximisation there willbe no inflation.

The banks have no use for these funds, as they cannot lend it to the private sector, andso they must buy bonds issued by the central bank as they are the only willingborrower.

Koo postulates the only inflation the central banks can generate is the obviously

undesirable hyperinflation, not moderate inflation.

8/3/2019 Balance Sheet Recession Basics

http://slidepdf.com/reader/full/balance-sheet-recession-basics 13/15

“Although a central bank can always generate hyperinflation by acting so as to lose

the public’s trust, its ability to induce modest inflation depends on whether private

businesses are in profit maximisation mode or not.” Page 137

Again, we come back to the chart above, without borrowers of the excess reserves,

there can be no credit growth and no inflation.

“The failure of the Bank of Japan’s five year experiment with QE to generate either

inflation or growth in the money supply is proof that trust in the central bank remains

intact. As long as it does, nothing will happen to inflation, because people have no

reason to abandon the correct and responsible course of paying down debt.” Page

137

QE Related Price Boosts

Investors become much more focused on dividends and DCF as a guage of value after

a bubble collapse. It seems unlikely that they will view price rises brought about bycentral bank asset purchases as anything more than transient unless they are certainthe price is backed by future cash flows. This means there is not likely to be anyinflationary consequences to these asset price increases.

“Central Bank purchases of government debt invariably imply an injection of

reserves into the banking system. Even though additional reserves will have no

inflationary consequences as long as there is no demand for funds from the private

sector, once demand returns, the central bank will face the risk of a massive credit

expansion based on excess reserves already present in the system.” Page 138

Central Bank purchases of debt do not create inflation. The resumption of borrowing/spending/investing by a private sector borrowing from a banking sectorawash with liquidity does.

Helicopter Money

“Money is distilled work” Little House on the Prairie

Helicopter Money is a cure that is significantly worse than the disease. Because fiatmoney is no longer backed by gold and instead only by faith in central banks it mustbe treated carefully. When Bernanke threatens to drop money out of Helicopters heonly thinks of the demand side of the equation, people would pick up the money andgo spend it. However, he overlooks the fact that any rational shopkeeper upon seeingthis would automatically close their stores as they have no way of knowing the valueof the money they are receiving. The economy would collapse to barter.

The Differences between today and Japan/Great Depression?

8/3/2019 Balance Sheet Recession Basics

http://slidepdf.com/reader/full/balance-sheet-recession-basics 14/15

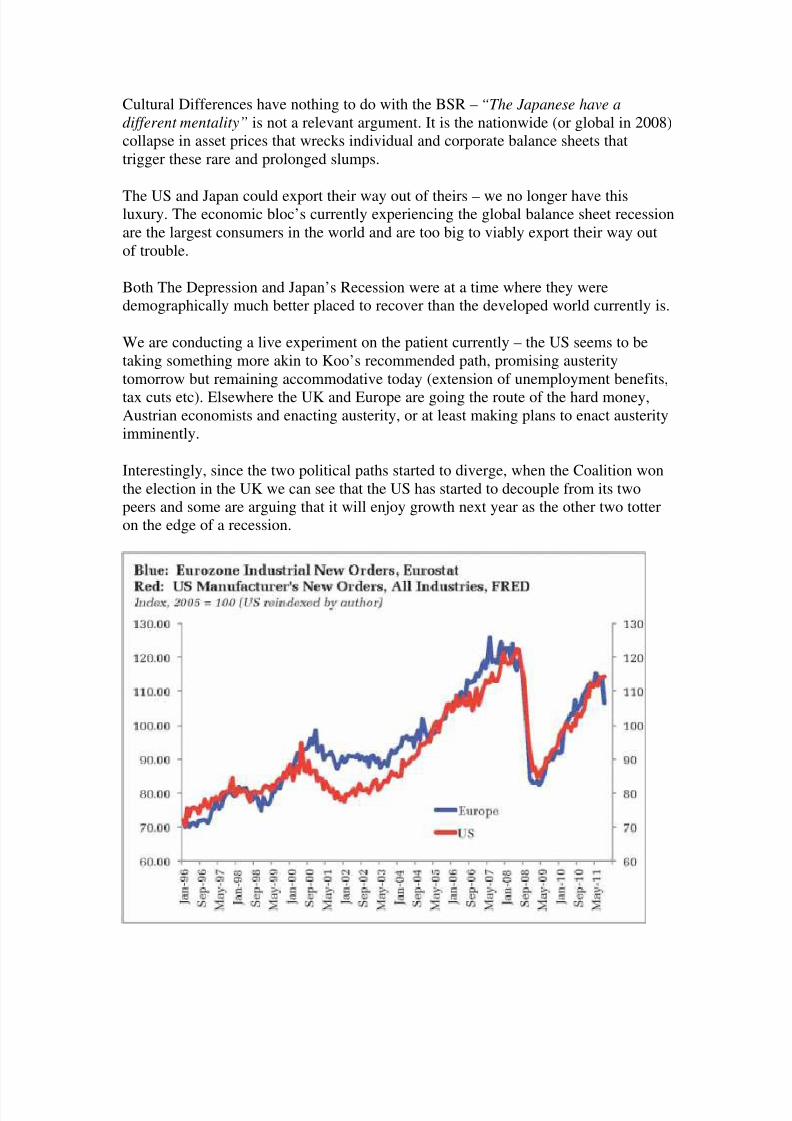

Cultural Differences have nothing to do with the BSR – “The Japanese have a

different mentality” is not a relevant argument. It is the nationwide (or global in 2008)collapse in asset prices that wrecks individual and corporate balance sheets thattrigger these rare and prolonged slumps.

The US and Japan could export their way out of theirs – we no longer have thisluxury. The economic bloc’s currently experiencing the global balance sheet recessionare the largest consumers in the world and are too big to viably export their way outof trouble.

Both The Depression and Japan’s Recession were at a time where they weredemographically much better placed to recover than the developed world currently is.

We are conducting a live experiment on the patient currently – the US seems to betaking something more akin to Koo’s recommended path, promising austeritytomorrow but remaining accommodative today (extension of unemployment benefits,

tax cuts etc). Elsewhere the UK and Europe are going the route of the hard money,Austrian economists and enacting austerity, or at least making plans to enact austerityimminently.

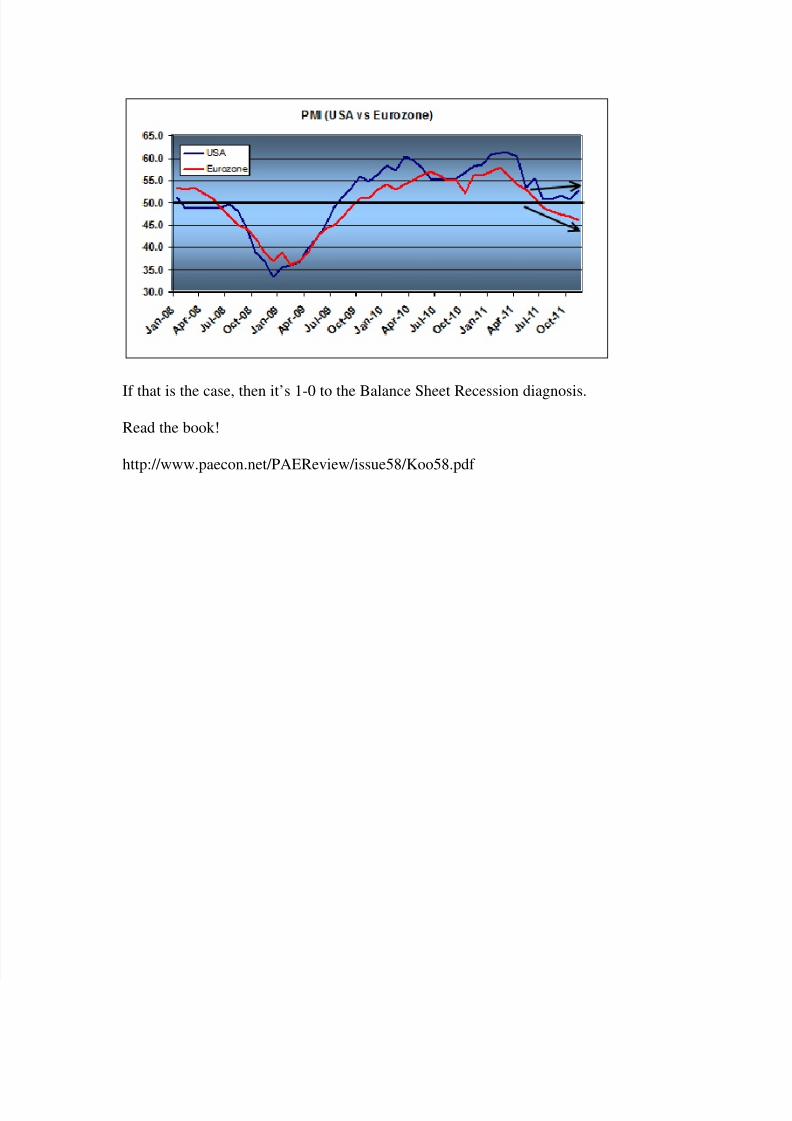

Interestingly, since the two political paths started to diverge, when the Coalition wonthe election in the UK we can see that the US has started to decouple from its twopeers and some are arguing that it will enjoy growth next year as the other two totteron the edge of a recession.

8/3/2019 Balance Sheet Recession Basics

http://slidepdf.com/reader/full/balance-sheet-recession-basics 15/15

If that is the case, then it’s 1-0 to the Balance Sheet Recession diagnosis.

Read the book!

http://www.paecon.net/PAEReview/issue58/Koo58.pdf