BAJAJ ELECTRICALS LTD.INSPIRING TRUSTINTRODUCTION:Bajaj

Electricals Ltd (BEL) (BSE:500031) is an Indian consumer electrical

Equipments manufacturing company based in Mumbai, Maharashtra. It

is a part of the 380 billion (US$6.2billion) Bajaj Group. It has

diversified with interests in lighting, luminaries, appliances,

fans, LPG based Generators, engineering and projects. Its main

domains are lighting, consumer durables, engineering and projects

.Some notable project includes lighting works at the Commonwealth

Games stadium and the Bandra Worli Sea LinkIt has 19 branch offices

spread in different parts of the country with a chain of about 1000

distributors, 4000 authorised dealers, over 400,000 retail outlets

and over 282 Customer Care centres.HISTORY:July 1938- It was

incorporated in 14 July 1938 as Radio Lamp Works Limited under the

Indian Companies Act, 1913 as a Public company limitedOctober 1960-

On 1 October 1960 it was renamed to Bajaj Electrical

Limited1993-1994- Bajaj Electricals entered into a joint venture

with Black & Decker Corporation, United States, for the

manufacture and marketing of power tools, household appliances, and

related accessories, through a separate company named Black &

Decker Bajaj Private Limited2000-2001- The Company set-up our

manufacturing facilities including a fabrication unit and a

galvanizing plant at Ranjangaon, near Pune for the manufacture of

high masts, lattice towers, and related products, and the said

manufacturing facilities commenced commercial production with

effect from April 1, 2001.November 2002-Our Company entered into a

technical collaboration and brand licensing agreement with Morphy

Richards, United Kingdom, for the sales and marketing of electrical

appliances under the brand name of "Morphy Richards" in India.Year

2005-the year 2005 the company entered into a Distribution

agreement with Trilux Lenze of Germany for high end technical

lightingYear 2007-In the year 2007, the company acquired 32% of the

share capital of Starlite Lighting Limited, a company engaged in

the manufacture of Compact Fluorescent Lamps ("CFLs").2012-2013 -In

2012-2013, they have completely divested our stake and association

with Black & Decker Corporation, USA.

PRODUCT RANGE :Its main domains are lighting, consumer durables,

engineering and projects. Lighting includes lamps, tubes and

luminaires. Consumer durables include appliances and fans.

Engineering and projects -The Company provides engineering and

projects services consisting of mast lighting, mobile light tower,

flag mast; street furniture projects, including hot dip galvanized

poles, cast iron ornamental lamp posts, and glass reinforces

polymer composite poles; specialty projects, such as stadium

lighting, rural electrification, and transmission line towers.

Luminaires includes industrial lighting, roadway lighting, area

lighting, urban architecture and accessories fluorescent lamps,

fluorescent tube lights, LED lights; power solutions, including

home UPS, inverters, and generators. Others include die casting,

wind energy & solar energy

Leverage ratios :Debt/Equity ratio= (Short term debt + Long term

debt)/Equity(CONSIDER ANNEXURE 2)for the year ending march

2010:=151.84/494.38=0.30for the year ending march

2011:=116.47/611.11=0.19for the year ending march

2012:=187.16/699.86=0.26for the year ending march

2013:=159.99/728.64=0.21

interpretation:Companies with less debt equity ratio are less

risky than the companies having a high ratio. It is important for a

share holder to look at the financial ratios in order to invest in

it.company was having least debt equity ratio in the year 2011 and

is trying to maintain it by having debt equity ratio as 0.21 in the

year ending march 2013.

interest coverage ratio:(CONSIDER ANNEXURE 1)

interest coverage =opearting income/interest expense

for the year ending march 2010: = 240.03/38.21 = 6.28

for

the year ending march 2011:= 255.45/37.68 = 6.77

for the year ending march 2012: = 238.83/62.31 = 3.83

for the year ending march 2013:= 110.75/68.97= 1.60

interpretation:If a company borrows money in the form of debt,

it most likely incurs interest charges on it. The interest coverage

ratio measures a company's ability to meet its interest obligations

with income earned from the firm's primary source of business.

Again, higher interest coverage ratios are typically better, and

interest coverage close to or less than one means the company has

some serious difficulty paying its interest.

Interest coverage ratio indicates the comfort with which the

company may be able to service the interest expense (i.e. finance

charges) on its outstanding debt. Higher interest coverage ratio

indicates that the company can easily meet the interest expense

pertaining to its debt obligations. In our view, interest coverage

ratio of below 1.5 should raise doubts about the companys ability

to meet the expenses on its borrowings. Interest coverage ratio

below 1 indicates that the company is just not generating enough to

service its debt obligations.Bajajelecs average interest coverage

ratio over the last 5 financial years has been 4.62 times which

indicates that the Company can meet its debt obligations without

any difficulty.

long term debt to equity ratio(CONSIDER ANNEXURE 2)=long term

borrowings /equityfor the year ending 31 march 2010=

151.83/494.37=0.30for the year ending 31 march

2011=45.10/611.11=0.07for the year ending 31 march

2012=40.45/699.86=0.06for the year ending 31 march 2013=

34.54/728.64=0.05interpretation:Companies operating with high long

term debt to equity on their balance sheets are vulnerable to

economic cycles. In times of slowdown in economy, companies with

high levels of debt find it increasingly difficult to service the

interest on their borrowings as profit margins decline. We believe

that long term debt to equity ratio higher than 0.6 - 0.8 could

affect the business of a company and its results of

operations.Bajajelec's average long term debt to equity ratio over

the last 4 financial years has been 0.12 times which indicates that

the Company operates with close to zero debt and is placed well to

withstand economic slowdowns

BAJAJ ELECTRICALS SHAREHOLDINGS PATTERN.

SHAREHOLDING PATTERN (% OF SHARES HELD)ShareholdingMarch

2010March 2011March 2012March 2013December 2013

Promoter65.7165.2065.9866.0866.22

FIIs3.858.855.4711.5015.40

DIIs16.2711.2810.064.482.90

Others14.1714.6718.4917.9415.48

(CONSIDER ANNEXURE 1)THE OPERATING PROFIT OF BAJAJ ELECTRICALS

HAS GONE DOWN FROM 255.45 IN YEAR 2011 TO 238.83 IN THE YEAR 2012

AND FINALLY 110.75 IN THE YEAR 2013. The reason for the poor show

on bourses is the EPC business, which has been a drag for the

company: it wiped out 53% of the total operating profit in FY13 and

66% in the first half FY14. Cost overruns and execution delays in

the EPC business have resulted in the poor performance. The segment

also led to a rise in working capital, which impacted the return on

capital. But now the company is trying to set things in order. "We

have become very selective about the projects we choose and will

take the ones only with high margins. We have also set up a new ERP

system and a new team for the EPC business and our focus will only

be on execution. The uncertain future surrounding its Engineering

& Projects division (E&P) has made investors jittery,

causing the market cap to lose substantial value.Creating value for

shareholders: Over the years, the company has not only strengthened

its financial position but has also created a great deal of

shareholder value. The same has been the result of the company's

continuous improvement in product and processes, widening of

product range and entering new categories and geographies. Few

initiatives to name are innovative launches in fan division (Disney

fans for kids), launching new models in appliances segment

(consumer durables like ovens, heaters, iron, etc.), tie-ups with

leading international brands like Morphy Richards, acquiring stake

in Starlite Lightning Ltd - manufactures compact fluorescent lamps

and technology tie ups in the lightening segment (Abacus and

Trilux, Delta and Securiton). Its efforts to boost earnings, lower

expenses, efficient use of assets and expanding reach through

dealer distributor network led to improvement in ROIC (return on

capital employed). ROIC improved from merely 1.7% in FY03 to 25% in

FY11). There has been a marginal dip in ROIC in FY12. The same is

on account of poor macroeconomic environment surrounding its

E&P business. Economic revival and increase in infrastructure

spend is likely to result in better utilization of assets and

higher earnings. The changing revenue mix and lower finance cost is

likely to give a further boost to profitability. Despite working

capital needs remaining the same, improved earnings is expected to

boost ROIC. BALANCE SHEET STRENGTH: With increase in profitability

and consequently cash flows, the company's debt servicing

capability has improved. The same is highlighted by consistently

declining gearing ratio (debt to equity ratio- D/E) and improving

interest coverage ratio. D/E ratio has come down from 2.6 times in

FY03 to 0.3 in FY12. Going forward, we expect the company to

further lower its debt burden and maintain the debt to equity

around similar level (well below 1x). As the company's

profitability improved and obligations declined, its interest

coverage ratio improved from 0.4 in FY03 to 8.4 in FY11. Although

interest coverage fell substantially to around 4x in FY12, we

believe that this is only a temporary phenomenon and expect the

coverage to go back to FY11 levels.

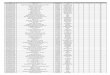

ANNEXURE 1:Operating Profit110.75238.83255.45240.03187.98

PBDIT152.39247.98267.30248.15188.74

Interest68.9762.3137.6838.2142.20

PBDT83.42185.67229.62209.94146.54

Depreciation14.4512.5210.769.208.55

Other Written Off0.000.000.000.000.00

Profit Before Tax68.97173.15218.86200.74137.99

Extra-ordinary items0.002.80-1.07-8.182.48

PBT (Post Extra-ord Items)68.97175.95217.79192.56140.47

Tax17.7758.0773.9975.3550.67

Reported Net Profit51.21117.88144.86117.1089.13

ANNEXURE 2:Sources Of Funds MAR13 MAR12 MAR11 MAR10

Total Share Capital19.95 19.9319.7719.51

Equity Share Capital19.95 19.9319.7719.51

Share Application Money0.00 0.000.020.00

Preference Share Capital0.00 0.000.000.00

Reserves708.69 671.11582465.52

Revaluation Reserves0.00 8.829.089.35

Networth728.64 699.86611494.38

Secured Loans51.02 76.6648.2668.39

Unsecured Loans108.97 110.5068.2183.45

Total Debt159.99 187.16116151.84

Total Liabilities888.63 887.02727646.22

9BAJAJ ELECTRICALS LTD.