Embed Size (px)

Citation preview

Bajaj Allianz Micro Insurance Initiative - India Case Study

9th International Micro Insurance Conference 2013 14th November 2013, Jakarta

Presented by - Yogesh Gupta Senior Vice President & Head Business Procurement, Micro & Mass Market

Opportunity: Lower middle income group

2

Emerging Trend: Opportunity at the ' forgotten’ Middle of the Pyramid

“9th International Microinsurance Conference 2013, Jakarta”

Only 5% of the Indian population is covered with some

sort of insurance cover

In India, Social Security Is virtually non existent

This means that Close to 800 million

People in Rural India have no insurance

access

There is an urgent need to provide insurance

protection to these individuals

India: Economic Snapshot

This segment of the country largely has no access to the financial services.

--------------------------------------- Large part of this population,

which is below poverty line are without savings, credit or insurance services.

Our company operates in a country where 32.7% of the population fall below the international poverty line of US$ 1.25 per day while 68.7% live on less than US$ 2 per day.

Source: UNDP, World Bank 2010 Report

• Limited availability of documents to determine health, age & primary education levels.

Documentation

• Erratic and seasonal income hence lapsation trends can be higher than normal

Income Patterns

• Efficient mechanisms for collecting premiums as little as US$ 1 per month against yearly premium

Small Ticket Sizes

• Simple to understand as the target audience is largely financially illiterate

• Low awareness

Customer Profile

Challenges : Product Design - Rural Market

“9th International Microinsurance Conference 2013, Jakarta”

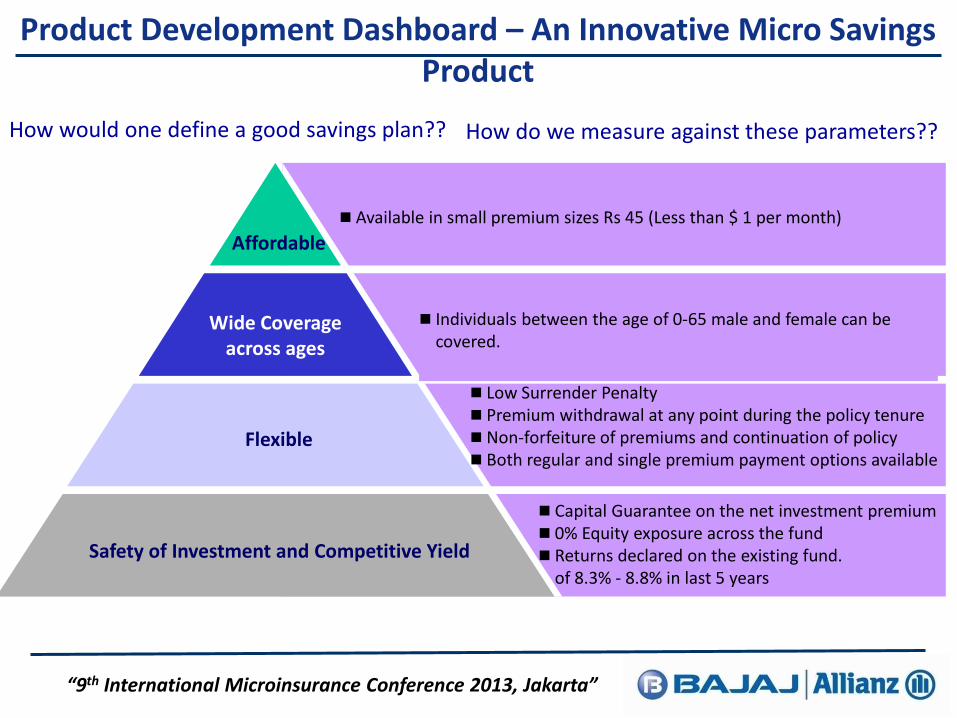

How do we measure against these parameters??

Product Development Dashboard – An Innovative Micro Savings Product

Affordable

Wide Coverage across ages

Flexible

Minimal documentation for enrollment and claims

Safety of Investment and competitive yield

Individuals between the age of 0-65 male and female can be covered.

Available in small premium sizes Rs 45 (Less than $ 1 per month)

Low Surrender Penalty Premium withdrawal at any point during the policy tenure Non-forfeiture of premiums and continuation of policy Both regular and single premium payment options available

Affordable

Wide Coverage across ages

Flexible

Safety of Investment and Competitive Yield

Capital Guarantee on the net investment premium 0% Equity exposure across the fund Returns declared on the existing fund. of 8.3% - 8.8% in last 5 years

“9th International Microinsurance Conference 2013, Jakarta”

How would one define a good savings plan??

Our Flagship Micro Insurance Product Innovation

“Sarve Shakti Suraksha”

which stands for…

“Securing & Empowering Everyone”

Launched - April’2008

Nos of Lives Covered – More than 7 Million

“9th International Microinsurance Conference 2013, Jakarta”

6

Key Product Features

Non Forfeiture of Premiums SSS (Sarve Shakti Suraksha ) – Over the

Counter Solution( OTC) Risk coverage with savings options Minimum Sum Assured per annum: Rs

2500 Minimum product term: 5 years Eligibility- Between 0-65 years Low Premium: Rs 45 (Less than $1per

month) Minimal documentation at the time of

product enrollment & Claims. Rider Available – ADB & ADDB

Incase of Death of the member- Sum Assured plus the account value of the customers investment

On Maturity Value - The account value subject to the minimum maturity guarantee,

Sarve Shakti Suraksha - Simplistic & Customer Centric

“9th International Microinsurance Conference 2013, Jakarta”

Low Surrender Penalty

Easy Revival without Penalty

Loan Against Policy

Non Medical Underwriting

Easy Enrollment by just filling One Pager form with on the spot “Welcome Letter”

“Over the Counter (OTC) Solution”

“Standard Premium Across all Ages”

Yet Another “Hit” in Micro Insurance & Financial Inclusion

Group Term Life Product

“9th International Microinsurance Conference 2013, Jakarta”

• Depending on the group, underwriting rate is set by the company ’ s underwriter • Varies based on group demographics

• Sum Insured: Minimum INR 1000, no limit on maximum coverage • Risks covered: Natural and accidental death • Disability rider is optional (but rarely implemented in microfin ance context) • MFIs deduct the outstanding loan balance (if any) from the sum i nsured

• Group Insurance

• An insurance product designed to provide risk protection against natural death to the end customer

• Other benefits include an accidental death & disability rider

• Non - bank Microfinance Institutions (MFIs) & Common Service Centers

• India

• Pure Risk Insurance coverage for a period of one year

• Group Term Life

Group or individual product

Covered risks & benefits / sum insured

Premium range (min, max)

Country

Distribution partner type (e.g. MFIs, banks, coops, retailers)

1 - sentence product description

Product type (e.g. credit life, endowment, motorcycle)

Product name (generic or marketing name)

• Depending on the group, underwriting rate is set by the company’s underwriter ’ • Varies based on group demographics

• Sum Insured: Minimum INR 1000, no limit on maximum coverage • Risks covered: Natural and accidental death • Disability rider is optional (but rarely implemented in microfinance context • MFIs deduct the outstanding loan balance (if any) from the sum insured

• Group Insurance

• An insurance product designed to provide risk protection against natural death to the end customer

• Other benefits include an accidental death & disability rider

• Non - bank Microfinance Institutions (MFIs) & Common Service Centers

• India

• Pure Risk Insurance coverage for a period of one year

• Group Term Life

Group or individual product

Covered risks & benefits / sum insured

Premium range (min, max)

Country

Distribution partner type (e.g. MFIs, banks, coops, retailers)

1 - sentence product description

Product type (e.g. credit life, endowment, motorcycle)

Product name (generic or marketing name)

Nos of Lives Covered – More than 30 Million in last 5 years

• Willing to get associated with service support and policy administration/servcing

• Support the insurer in intimation and resolution of claims and other requirements

Have a service orientation

• Promote financial literacy and insurance awareness through specially designed tools

Promote insurance awareness

• Have a firmly established operation across specified core businesses

• Insurance cant be the sole business activity • Help in buildling Low cost of distribution

Existing distributors of products/services

• Associate with partners operating across these segments

• Have sound knowledge, understanding and access to captive customer databases

• Proper Infrastructure

Collaborate with strategic partners

Product Distribution Approach – Rural Market

“9th International Microinsurance Conference 2013, Jakarta”

Distribution – Our Rural Business Model

Rural Business

Micro Finance

Institutions

Dairy Federation

National E-governance

Plan

Boards & Associations

Credit/ Non Credit

Co-operative Societies

Rural Banks

Business Correspondents

Others

“9th International Microinsurance Conference 2013, Jakarta”

70 Micro Finance Institutions

200 Rural Banks

7 NeGP Players with 60,000 CSCs

10 Key BC Players with target reach to 20 million people

More than 600 Co-op Scocities

We have piloted with 4 key Dairy Boards in Indian

Exploring Coffee/Tea/Sugar Board etc

NGOs, Organisation with Rural Presence such a “Rural Retail”

Rural & Micro Insurance Achievements (As on Sept’13)

“9th International Microinsurance Conference 2013, Jakarta”

Total Nos of Lives Covered in last 5 years : 3.61 Million

Figures are on Financial Yea Wise i.e. 1st April – 31stMarch

Figures as on September’13

1.700.00

1.70 1.370.311.69

0.331.04

1.37

0.814.27

5.08

2.21

15.61

17.81

0.61

7.908.51

7.02

29.14

36.16

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

Live

s Co

vere

d (in

Mill

ions

)

2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 Total

Year

No of Lives CoveredSSS GTL Total

Rural & Micro Insurance Achievements (As on Sept’13)

“9th International Microinsurance Conference 2013, Jakarta”

Total New Business Premium Collected in last 5 years : US $ 163.24 Mn Total Corpus under Micro Insurance in last 5 years : US $ 272.67 Mn

1 USD = INR Rs. 60 Figures are on Financial Yea Wise i.e. 1st April – 31stMarch

Figures as on September’13

160.01

16.10

34.720.26

34.98

21.68 1.39

23.07

20.34 5.4125.75

27.57 16.03

43.60

10.249.51 19.75

130.6332.61

163.24

0

50

100

150

200

Prem

ium

( in

USD

Mill

ion)

2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 Total

Year

Micro Insurance New BusinessSSS GTL Total

12

Micro Saving Solution – Sarve Shakti Suraksha

• Nos of Claims Received - 27,418 • Nos of Claims Settled - 26,536 • Claims Settlement Ratio (NOP) -96.78% • Claim Received (Amount) -Rs. 174.65 or US $ 29.11 Mn • Claims Settled (Amount) – Rs. 169.10 or US $ 28.18 Mn • Claim Settlement Ratio (NOP) – 96.78% • Claim Settlement Ratio (Amount) – 96.81%

Claim Settlement : The Moment of Truth

“9th International Microinsurance Conference 2013, Jakarta”

Micro Saving Solution – Group Term Life

• Nos of Claims Received - 1,74,197 • Nos of Claims Settled - 1,70,413 • Claims Settlement Ratio (NOP) – 97.83% • Claims Settlement Amount (Sum Assured)

• Rs. 227.56 Crores or US $ 37.92 Mn

Total Nos. Claims Settled under Micro Insurance Initiative – 1,96,949 Total Claims Settled (Amount) – Rs. 396.66 Crores or US $ 66.11 Mn

Overall Claim Settlement Ratio (NOP) – 97.31%

1 USD = INR Rs. 60

Claim Story…

Claim Settlement : The Moment of Truth

Our Cost Effective Strategy

14

“9th International Microinsurance Conference 2013, Jakarta”

• Spread the risk • Mutual basis – premium / claim sharing

• Speedy settlement of Claims • A marketing opportunity

• Keep it simple • Lack of data can be a hurdle, so price as per experience • Customized to the needs of the target segment

• Issue Master Policy • Constant Interaction through community workers • Process re-engineering to keep policy issuance cost less

• Less Documentation • Less Premium • Less Operational Cost

More Emphasis on Less

Service Delivery

Products

Claims

Underwriting

Aggregators RO’s/ Branches Bajaj Allianz Life & Aggregators

Microinsurance Business model: Large customer aggregator driven Mass Market Approach

Member & the Aggregator Activity: Example Product development Marketing & sales Purchase of policy

In 2008, research conducted by partner on savings needs of its microcredit customers.

Data collected as part of survey formed basis of product development approach.

Mass awareness campaigns in villages,

Product information disseminated through well organized daily center meetings

Center meets serve as effective customer contact points.

A typical client …lives on less than 2$ a day Lives In rural areas or Slums …generates income from activities

such as agriculture, livestock, trade, production & services

…only members allowed

Bajaj Allianz Life & Aggregator Bajaj Allianz Life & Aggregator Bajaj Allianz Life & Aggregator

Claims … Claims documentation Damage / Risk

… Verification and payments issuance Cheques issued by Bajaj Allianz Payment issued in partner

branches or in center meetings

Limited paperwork requirements Assessment of the claims

received Verify and certify documentation Cancel out exclusions

Death due to natural reasons, illnesses or accidents such as drowning, snake bites which occur in rural areas

Example:

Special Initiatives in Micro Insurance

“9th International Microinsurance Conference 2013, Jakarta”

17

Easy and simple to understand products Simplified products, minimal documentation for enrollment and claims

settlement, non forfeiture in case of premium non payment, 2 years for

reinstating policy at no interest charges

It’s an essential requirement – Financial Inclusion The segment is vulnerable and exposed to different sorts of risks which can

impact livelihood, Insurance performs the role of a efficient risk protection and

social security tool.

Financial Literacy and Insurance Awareness Cascading key messages on insurance concepts as well as product details

using easy to explain simple tools

Important tool to ensure portfolio quality, as members are aware and well informed

about the key attributes of the scheme

Ensures long term value creation and customer satisfaction.

To Summarize...

“9th International Microinsurance Conference 2013, Jakarta”

Microinsurance is a

Social Business Opportunity…

Thank You For Your Attention!!!