Embed Size (px)

Citation preview

Baja Ca l i forn ia’ s Economy,

Secur i ty , and Why I t Matters

San Diego Regional Economic Development Corporation

Board Meeting • March 13, 2013

…Some (Possibly)

Surprising Manufacturing

& Trade Numbers

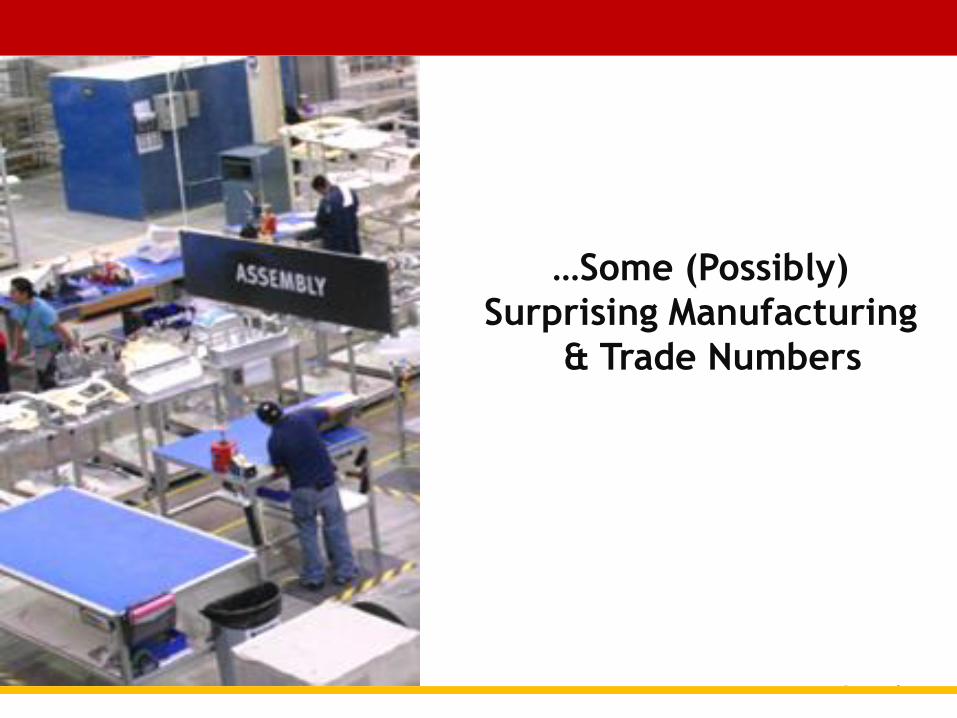

• Trade in the combined NAFTA marketplace of 454

million consumers is still increasing…

• US$1.2+ trillion in trade between NAFTA

partners in 2011

• $460 billion in trade between US & Mexico (12.5% of total US)

NAFTA: INTEGRATION STILL INCREASING…

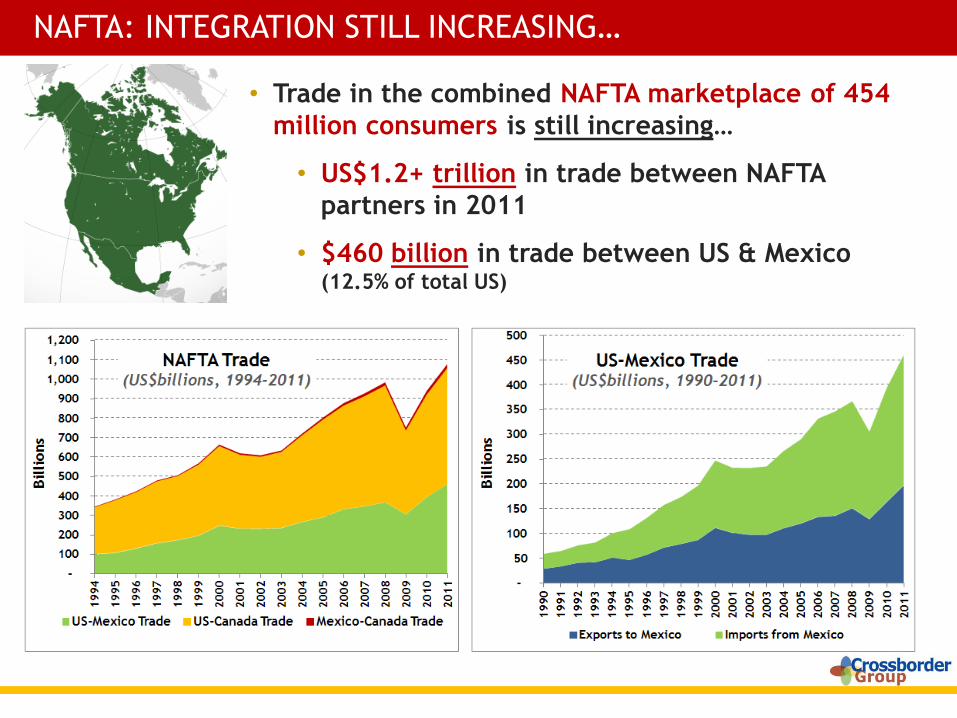

• Otay Mesa is typically #2 Land Port along US-Mexico border…

• Over 62,000 trucks cross northbound (and south) each month…

• Over US$38.2 billion in imports and exports at Otay Mesa in 2011

• …Nearly$2.8 billion/month in trade in 1H-2012

MUCH OF THAT TRADE AT OTAY MESA PORT OF ENTRY

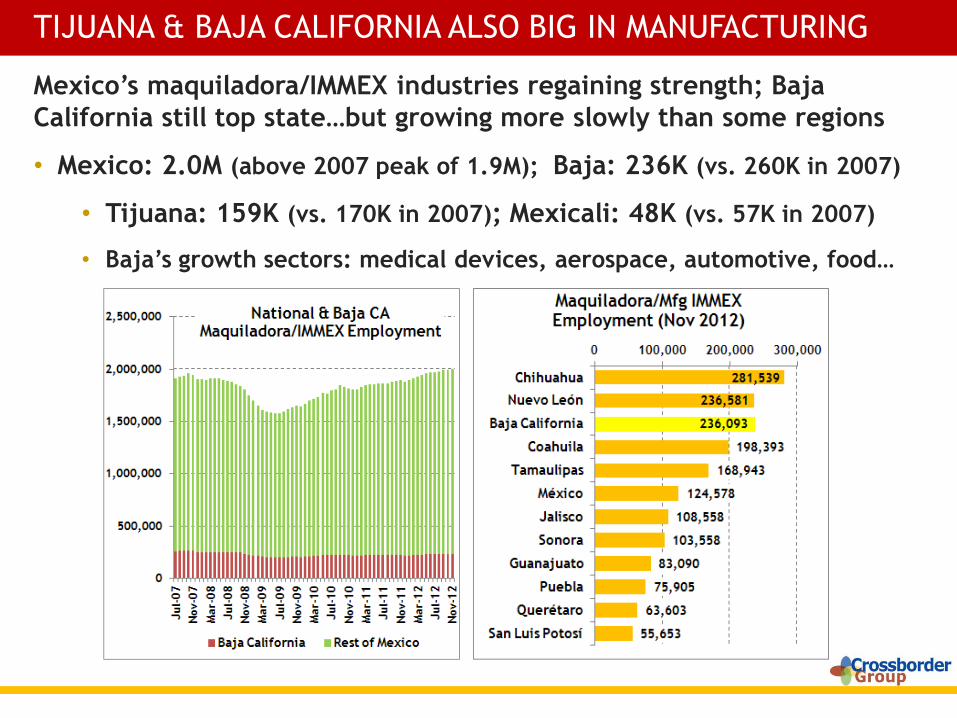

Mexico’s maquiladora/IMMEX industries regaining strength; Baja

California still top state…but growing more slowly than some regions

• Mexico: 2.0M (above 2007 peak of 1.9M); Baja: 236K (vs. 260K in 2007)

• Tijuana: 159K (vs. 170K in 2007); Mexicali: 48K (vs. 57K in 2007)

• Baja’s growth sectors: medical devices, aerospace, automotive, food…

TIJUANA & BAJA CALIFORNIA ALSO BIG IN MANUFACTURING

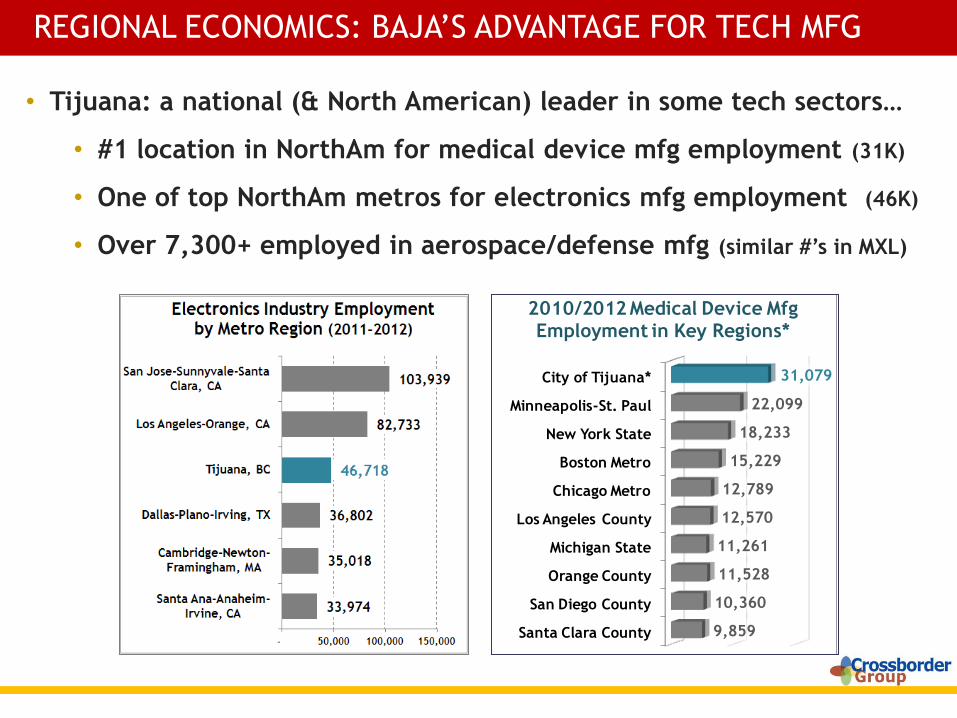

• Tijuana: a national (& North American) leader in some tech sectors…

• #1 location in NorthAm for medical device mfg employment (31K)

• One of top NorthAm metros for electronics mfg employment (46K)

• Over 7,300+ employed in aerospace/defense mfg (similar #’s in MXL)

REGIONAL ECONOMICS: BAJA’S ADVANTAGE FOR TECH MFG

Santa Clara County

San Diego County

Orange County

Michigan State

Los Angeles County

Chicago Metro

Boston Metro

New York State

Minneapolis-St. Paul

City of Tijuana*

9,859

10,360

11,528

11,261

12,570

12,789

15,229

18,233

22,099

31,079

2010/2012 Medical Device Mfg Employment in Key Regions*

*data for Q2-2012 *see endnotes for estimation methodology used

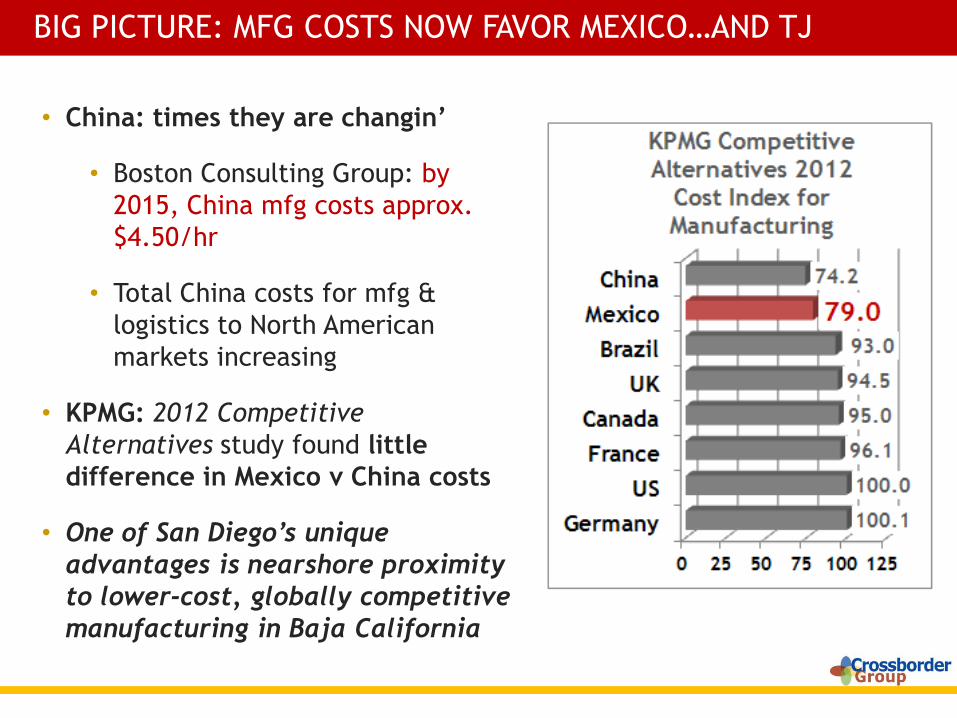

WHY IS MEXICO’S MANUFACTURING GROWING?

There has been persistent trend for manufacturing labor cost

increases in rest of North America…and many other markets

• Labors costs for Mexico manufacturing have relatively flat (in US$)

• Costs higher in Brazil – and (possibly) soon China

• China: times they are changin’

• Boston Consulting Group: by

2015, China mfg costs approx.

$4.50/hr

• Total China costs for mfg &

logistics to North American

markets increasing

• KPMG: 2012 Competitive

Alternatives study found little

difference in Mexico v China costs

• One of San Diego’s unique

advantages is nearshore proximity

to lower-cost, globally competitive

manufacturing in Baja California

BIG PICTURE: MFG COSTS NOW FAVOR MEXICO…AND TJ

Tijuana: Size, Security

and Borders Waits…

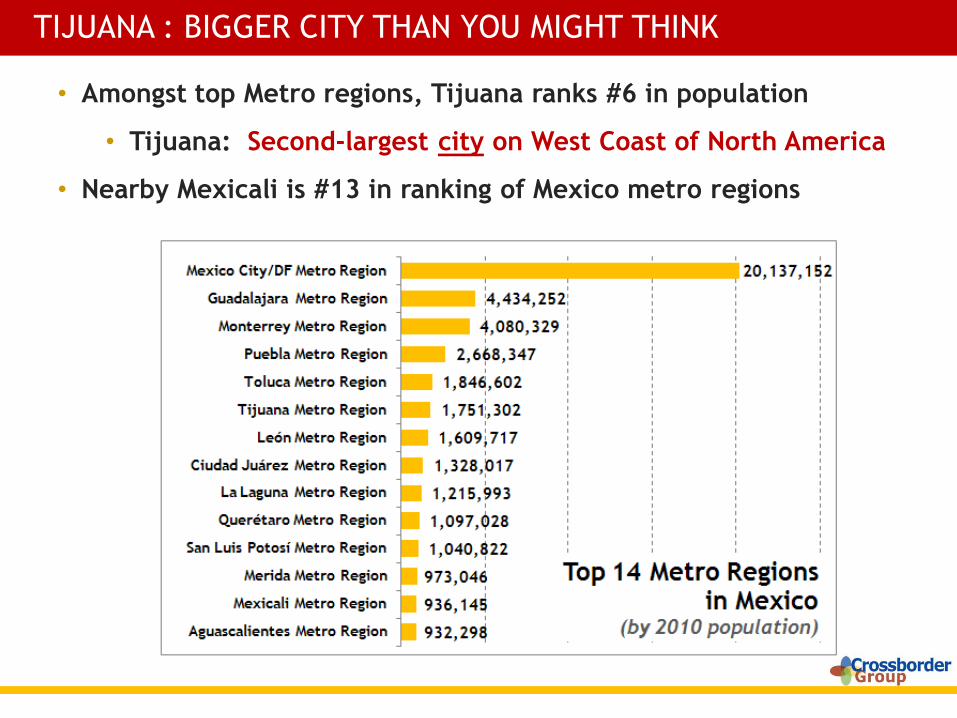

• Amongst top Metro regions, Tijuana ranks #6 in population

• Tijuana: Second-largest city on West Coast of North America

• Nearby Mexicali is #13 in ranking of Mexico metro regions

TIJUANA : BIGGER CITY THAN YOU MIGHT THINK

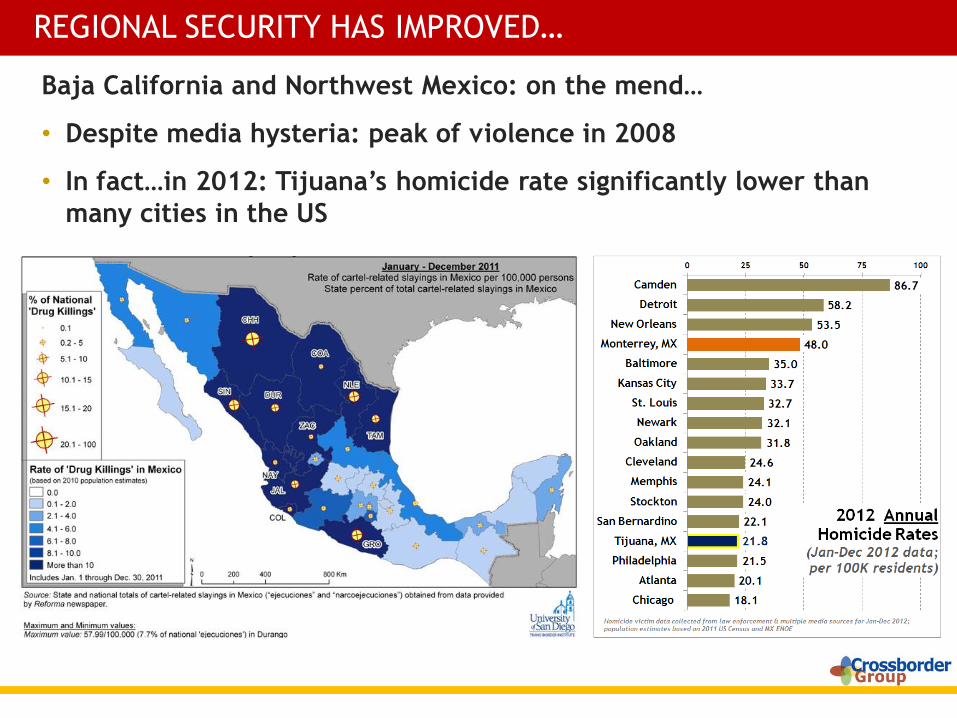

Baja California and Northwest Mexico: on the mend…

• Despite media hysteria: peak of violence in 2008

• In fact…in 2012: Tijuana’s homicide rate significantly lower than

many cities in the US

REGIONAL SECURITY HAS IMPROVED…

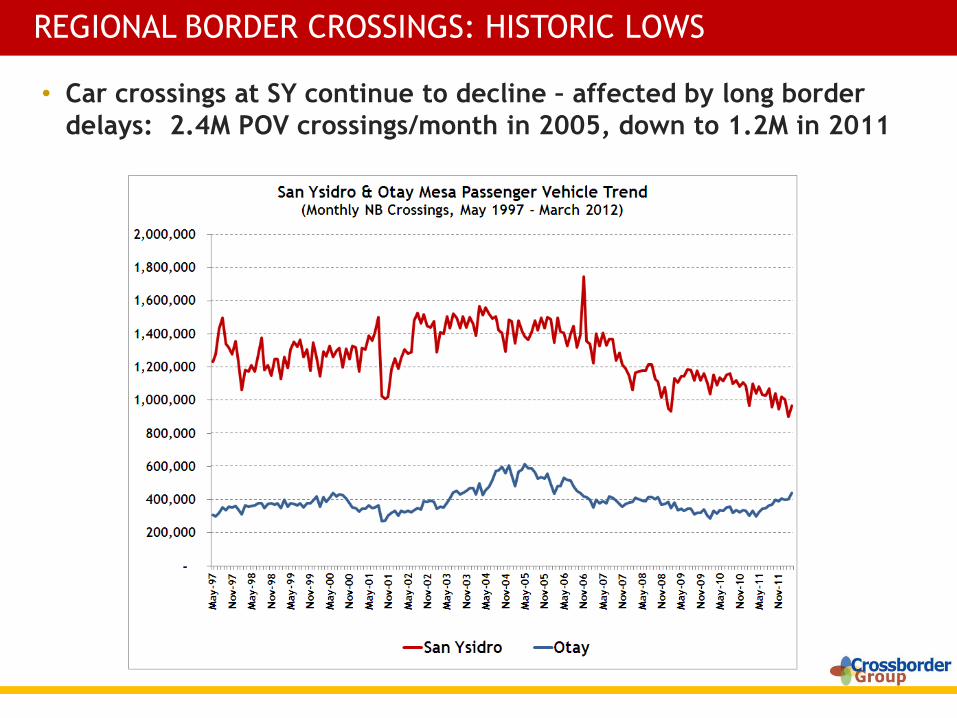

• Car crossings at SY continue to decline – affected by long border

delays: 2.4M POV crossings/month in 2005, down to 1.2M in 2011

REGIONAL BORDER CROSSINGS: HISTORIC LOWS

• To-date, very few efforts to accurately measure border wait times

at San Ysidro and Otay Mesa…

• SANDAG & Caltrans changing that: border wait time study

underway (with a bit of help from Crossborder Group)

LITTLE BORDER DELAY DATA…SO FAR

• Yet: too-little (+ delayed) funds for POEs (SY, Otay & Otay East)

• Around $2-3 billion needed just for California-Baja CA POEs

BORDER CROSSINGS – PLANNED…BUT NOT ENOUGH $$

Why better

infrastructure?

It’s a benefit for the

economy on both sides

of the border…

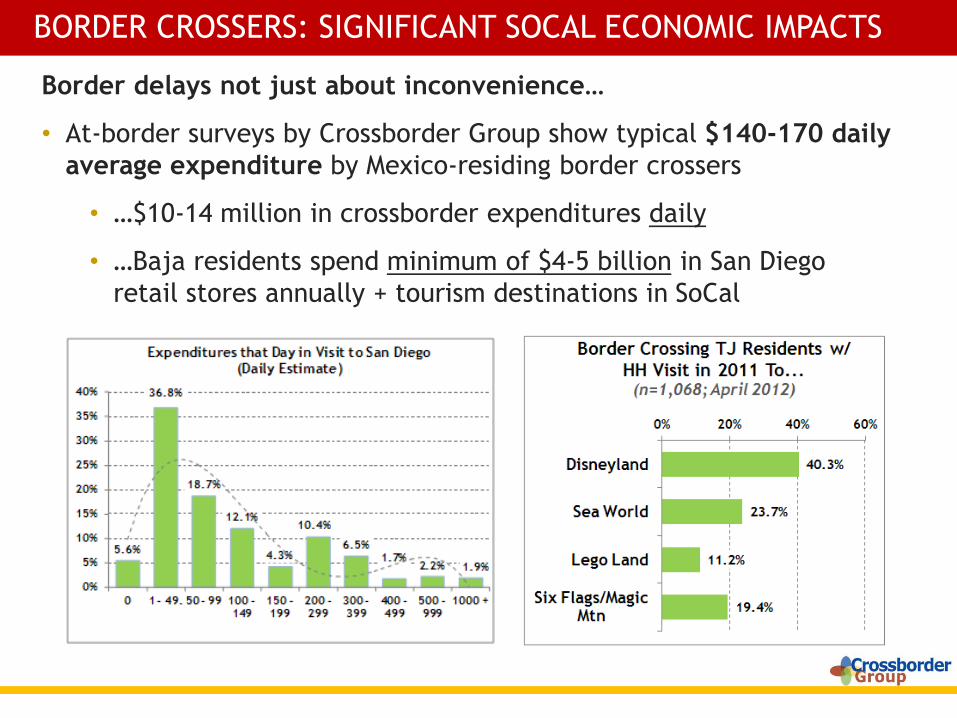

Border delays not just about inconvenience…

• At-border surveys by Crossborder Group show typical $140-170 daily

average expenditure by Mexico-residing border crossers

• …$10-14 million in crossborder expenditures daily

• …Baja residents spend minimum of $4-5 billion in San Diego

retail stores annually + tourism destinations in SoCal

BORDER CROSSERS: SIGNIFICANT SOCAL ECONOMIC IMPACTS

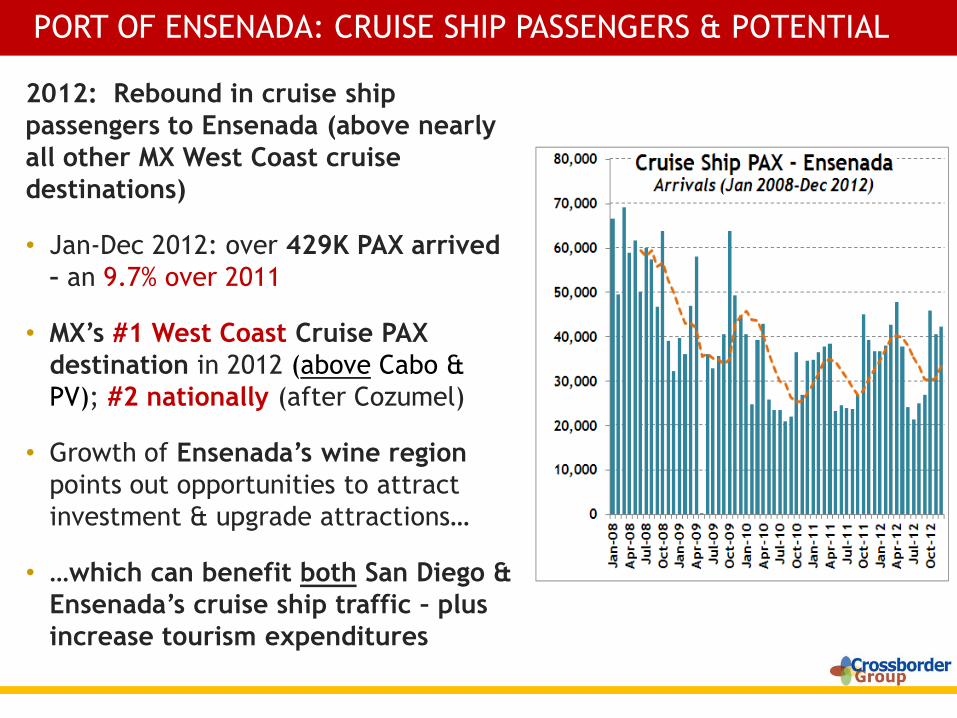

2012: Rebound in cruise ship

passengers to Ensenada (above nearly

all other MX West Coast cruise

destinations)

• Jan-Dec 2012: over 429K PAX arrived

– an 9.7% over 2011

• MX’s #1 West Coast Cruise PAX

destination in 2012 (above Cabo &

PV); #2 nationally (after Cozumel)

• Growth of Ensenada’s wine region

points out opportunities to attract

investment & upgrade attractions…

• …which can benefit both San Diego &

Ensenada’s cruise ship traffic – plus

increase tourism expenditures

PORT OF ENSENADA: CRUISE SHIP PASSENGERS & POTENTIAL

SOMETHING UNIQUE: THE “CALI-BAJA” MEGA REGION

Tried to give a sense of “why it matters”…

• San Diego Regional EDC blog, March 4:

“…Let’s make sure it’s really the year of cross-border progress.”

¡Gracias! ¿Preguntas?

Kenn Morris, President/CEO of Crossborder Group

Email: Kenn @CrossborderBusiness.com

San Diego: 619-710-8120 • Tijuana: 664-380-6151

![[Please list the analysis conducted] - Baja SAE Baja SAE Redesign Comparison... · Web view2016 Baja SAE Design Comparison Document 2016 Baja SAE Design Comparison Document 2016 Baja](https://img.pdfslide.us/doc/110x75/5ab1e61b7f8b9a284c8d112e/please-list-the-analysis-conducted-baja-baja-sae-redesign-comparisonweb-view2016.jpg)