Embed Size (px)

Citation preview

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 132

EUROPEAN BANKING

Striking the right balance between risk and return

By Walter Sinn Rocco DrsquoAcunto and Andrea Oldrini

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 232

Copyright copy 2013 Bain amp Company Inc All rights reserved

Walter Sinn is a Bain amp Company partner based in the firmrsquos Frankfurt office

Rocco DrsquoAcunto is a partner based in Bainrsquos Milan office Andrea Oldrini is a

manager based in Milan They are all members of Bainrsquos European Financial

Services practice

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 332

European banking | Bain amp Company Inc

Page 1

Contents

European banking Striking the right balance between risk and return 2

1 Five years of RoRWA in Europe A bumpy landscape 7

2 Country and cluster league tables 17

3 Strategic perspectives and implications for management 23

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 432

European banking | Bain amp Company Inc

Page 2

European banking Striking the right balance between risk and return

Now that risk figures so prominently in European banking itrsquos time to raise the profile of a metric that has playeda minor role to date

This benchmarkmdashthe rate of return on risk-weighted assets or RoRWAmdashreliably integrates a balance-sheet-

management perspective with the revenue and cost side of the business Based on a comprehensive analysis of

121 banks across Europe by Bain amp Company RoRWA clearly emerges as the single most practical measure to

help senior bank executives manage their companiesrsquo performance and make savvy risk-reward decisions

Our analysis shows how and where the quality of management plays a major role in determining performance

Thatrsquos especially true in the core European countries where banks canrsquot rely on economic growth to lift their fortunes

Why does RoRWA deserve more respect now Five years since the global financial crisis bankers across Europe

still find themselves waging battle on many fronts Low interest rates a loss of customersrsquo trust stiff new targetcapital requirements and regulatory mandates have compounded the difficulty of operating in weak eurozone

economies On the cost side moreover banks are reconfiguring their distribution networks and streamlining

operations Yet even as revenue growth flattens and new digital technologies push up capital investments banks

are not making much headway on reining in costs

Indeed the banking industry is going through a major restructuring and only the fittest will survive this Darwinian

process The traditional tools that bankers have used to chart their competitive courses provide an inadequate map

for navigating treacherous new terrain With capital adequacy asset quality and broad macroeconomic trends

playing more prominent roles in shaping a bankrsquos financial performance it is the balance sheet not the profit-

and-loss statement which better captures the bankrsquos overall health and points to the areas that most need improvement

Todayrsquos environment of disruptive change calls for a holistic yet simple view of the returns that banks generate

on every unit of capital they commit to their businesses on a risk-adjusted basis

RoRWA fits the bill Other measures may be more precise in understanding risk theoretically but theyrsquore

impractical to use in managing the enterprise RoRWArsquos strength lies in using a well-understood measuremdash

risk-weighted assetsmdashas a denominator making it a good proxy for risk

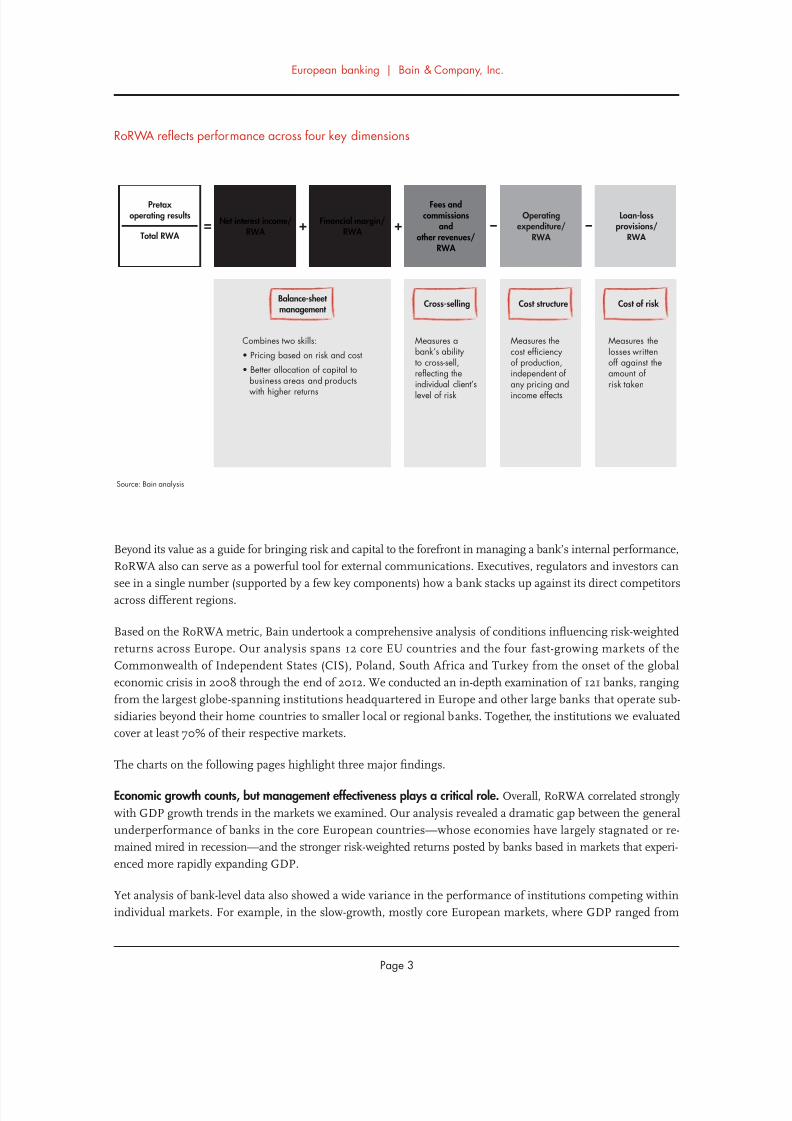

For business leaders RoRWA and the analysis of key components can provide practical guidance to optimize

bank performance across four dimensions

bull First RoRWA tracks how well a bank manages its balance sheet and appetite for risk Managers can see

whether they are properly pricing offerings to reflect their risk and cost and how well they are allocating

capital to business areas and products that generate higher returns

bull Second the benchmark guides decisions on how a bank factors in risk to its cross-selling opportunities that

bring in fees commissions and other revenues

bull Third on the cost side a RoRWA approach reveals the cost efficiency per unit of risk for the volume of

business a bank generates

bull Fourth RoRWA shines a light on the cost of risk by disclosing how well a bank is able to minimize its loan-loss

provisions on a risk-adjusted basis

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 532

European banking | Bain amp Company Inc

Page 3

Beyond its value as a guide for bringing risk and capital to the forefront in managing a bankrsquos internal performance

RoRWA also can serve as a powerful tool for external communications Executives regulators and investors can

see in a single number (supported by a few key components) how a bank stacks up against its direct competitorsacross different regions

Based on the RoRWA metric Bain undertook a comprehensive analysis of conditions influencing risk-weighted

returns across Europe Our analysis spans 12 core EU countries and the four fast-growing markets of the

Commonwealth of Independent States (CIS) Poland South Africa and Turkey from the onset of the global

economic crisis in 2008 through the end of 2012 We conducted an in-depth examination of 121 banks ranging

from the largest globe-spanning institutions headquartered in Europe and other large banks that operate sub-

sidiaries beyond their home countries to smaller local or regional banks Together the institutions we evaluated

cover at least 70 of their respective markets

The charts on the following pages highlight three major findings

Economic growth counts but management effectiveness plays a critical role Overall RoRWA correlated strongly

with GDP growth trends in the markets we examined Our analysis revealed a dramatic gap between the general

underperformance of banks in the core European countriesmdashwhose economies have largely stagnated or re-

mained mired in recessionmdashand the stronger risk-weighted returns posted by banks based in markets that experi-

enced more rapidly expanding GDP

Yet analysis of bank-level data also showed a wide variance in the performance of institutions competing within

individual markets For example in the slow-growth mostly core European markets where GDP ranged from

RoRWA reflects performance across four key dimensions

Source Bain analysis

= Net interest incomeRWA + + ndashndashFinancial margin

RWA

Fees andcommissions

andother revenues

RWA

Operatingexpenditure

RWA

Loan-lossprovisions

RWA

Measures abankrsquos abilityto cross-sellreflecting theindividual clientrsquos

level of risk

Cross-selling

Measures thecost efficiencyof productionindependent of any pricing and

income effects

Cost structure

Measures thelosses writtenoff against theamount ofrisk taken

Cost of risk

Combines two skills

bull Pricing based on risk and cost

bull Better allocation of capital to business areas and products

with higher returns

Balance-sheet management

Pretax operating results

Total RWA

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 632

European banking | Bain amp Company Inc

Page 4

negative 10 to 5 over the five-year period RoRWA by bank varied widely in every year Clearly for these

markets the quality of an individual bankrsquos management plays a major role in determining performance

In markets where GDP growth exceeded 5 by contrast we found considerably less variation in bank-level

RoRWA performance As the rising tide lifted all banks managementrsquos role in shaping returns appears to have

been more circumscribed

Most banks fail to earn their cost of capital Bain determined that the RoRWA required for banks to cover their

cost of capital fell within a range of 16 to 21 depending on a bankrsquos size and the country in which it is based

The RoRWA of most banks has failed to clear that cost-of-capital hurdle on average in any year since 2008

falling well short in every year except 2010 Once again however we found a wide variation between the bank

performance in the core European countries where RoRWA was consistently below the cost of capital and that

in the high-growth countries where RoRWA easily cleared the capital-cost bar

Looking at the banksrsquo underlying strengths and weaknesses by market we identified several major pain points

that pinched banksrsquo RoRWAs in the core European countries

The need to shed debt and rely on higher-cost equity to strengthen their balance sheets reduced these banksrsquo total

risk-weighted assets by nearly 8 between 2008 and 2012 Meanwhile their cost of risk increased sharply as

stagnant or shrinking economies forced them to boost their loan-loss provisions in the face of steeper write-offs

of bad credit Interest margins that remained at low levels shrinking fee incomes and higher operating costs also

added downward pressure to banksrsquo RoRWAs

Size matters Within core Europe the 10 biggest pan-European banks (by total assets and market capitalization)

fared best overall Helped by large increases in net interest income and strong improvements in financial margins

their RoRWAs came closest to earning their cost of capital

Other large European banks with subsidiaries outside their home countries reduced their operating costs partially

offsetting declines in risk-weighted fee income and higher loan-loss provisions But the RoRWAs for these

banks still failed to clear their cost-of-capital hurdle

Local banks in core Europe struggled weighed down by nonperforming loans and flat revenues Their RoRWAs

were negative in both 2008 and 2012 and did not come close to covering their cost of capital

Turning to country differences the four high-growth countries on the fringe of Europe the Middle East and Africa

have the wind at their backs Turkey ranked first in RoRWA for 2012 and it has jockeyed for top billing with

Poland and South Africa over the past five years

Countries in core Europersquos northern tier occupied the middle ranks of the national league tables with the Nordic

and Austrian banks showing the most consistent performance since 2008 Dutch Belgian and German banks

have been on an upswing since the financial crisis hit UK and French banks have been treading water although

Standard Chartered Bank and HSBC in the UK and BNP Paribas in France all ranked among the top 15 banks

in core European countries

Not surprisingly banks in Italy Portugal Spain and Irelandmdashall feeling the sting of the sovereign debt crisis and

deep economic recessionsmdashhave turned in the weakest RoRWAs

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 732

European banking | Bain amp Company Inc

Page 5

Illuminating the road ahead

While most European banks are moving in the right direction to meet Basel III requirements they could benefit

from using RoRWA to better anticipate and navigate the road ruts that lie ahead

Devising sustainable business models and bringing profitability back to attractive levelsmdashmeaning above the

cost of capitalmdashwill not be easy In the current market environment we expect continued pressure on interest

as well as on fee income For most banks managing the cost of risk will also be a challenge as stagnant economies

tend to drive up this cost

Getting a better grip on operating cost therefore will lead the agenda for most banks Structural costs can be

addressed using several means adopting new digital technologies and modernizing IT platforms optimizing

processes from end to end through such approaches as outsourcing and offshoring and expanding global pro-

curement initiatives

Local banks in core European countries face perhaps the stiffest challenges as restructuring will continue in the

face of stagnant economies and a higher cost of risk We expect to see further consolidation in this group For

the surviving institutions higher performance will hinge on better management of the deleveraging process

containment of the cost of raising new capital and more accurate factoring of risk into their price structures

High-growth countries still offer the most promising opportunities for the 10 biggest and other large pan-Euro-

pean players that aim to diversify their portfolios The best performers will be those banks that keep tight control

of the reins as they ride these booming economies

Regardless of a bankrsquos home country asset size or loan portfolio RoRWA analysis illuminates the ruts and holes

on the road ahead With just a few metrics senior managers can understand how their bank compares with its

peers and which factors to work on in order to create valuemdasha highly pragmatic means of improving the bankrsquos

risk-return profile

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 832

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 932

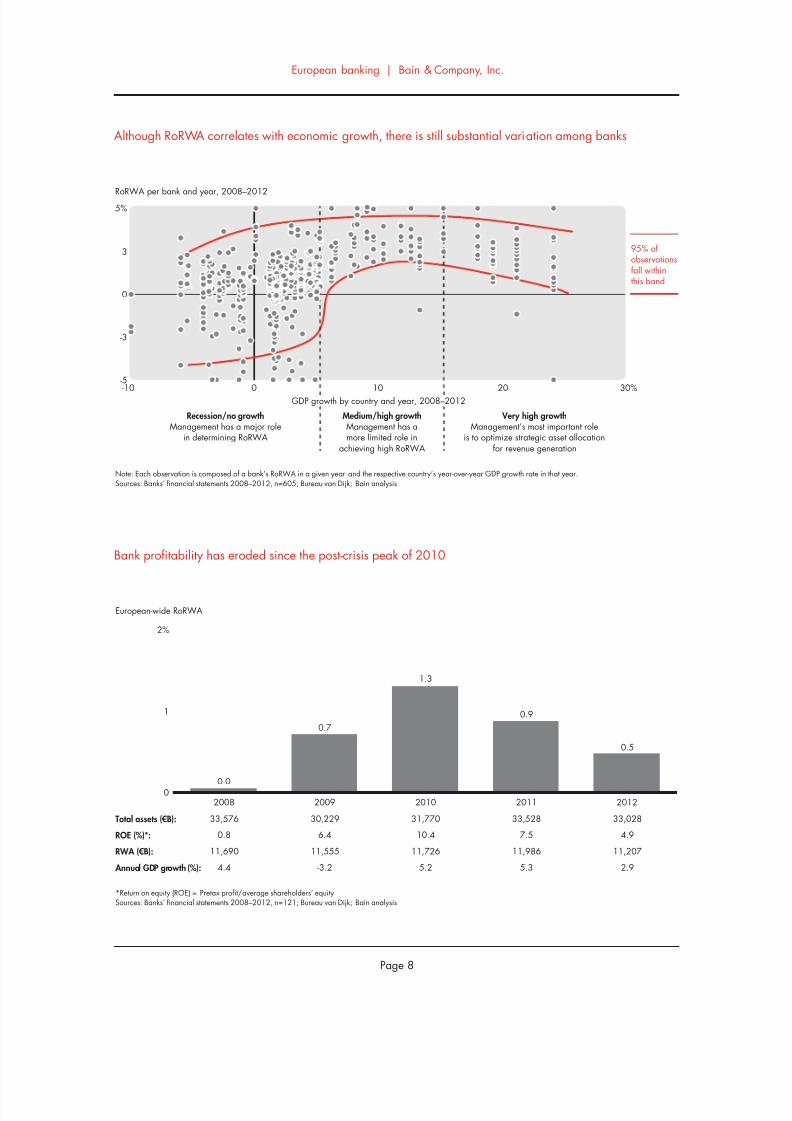

bull European banksrsquo return on risk recovered from the2008 financial crisis peaking in 2010 with an aver-age 13 RoRWA Since then however RoRWA

has declined to 05 on average This translatesto a level of profitability below the cost of capitalwhich means banks are destroying value

bull Looking beneath the average European banksrsquoRoRWAs correlated closely with economic growthover the past five years Banks in countries that sawstrong GDP growth like Turkey posted dramaticallyhigher performance and growth in both assetsand risk-weighted assets (RWA) than those in thecore European countries

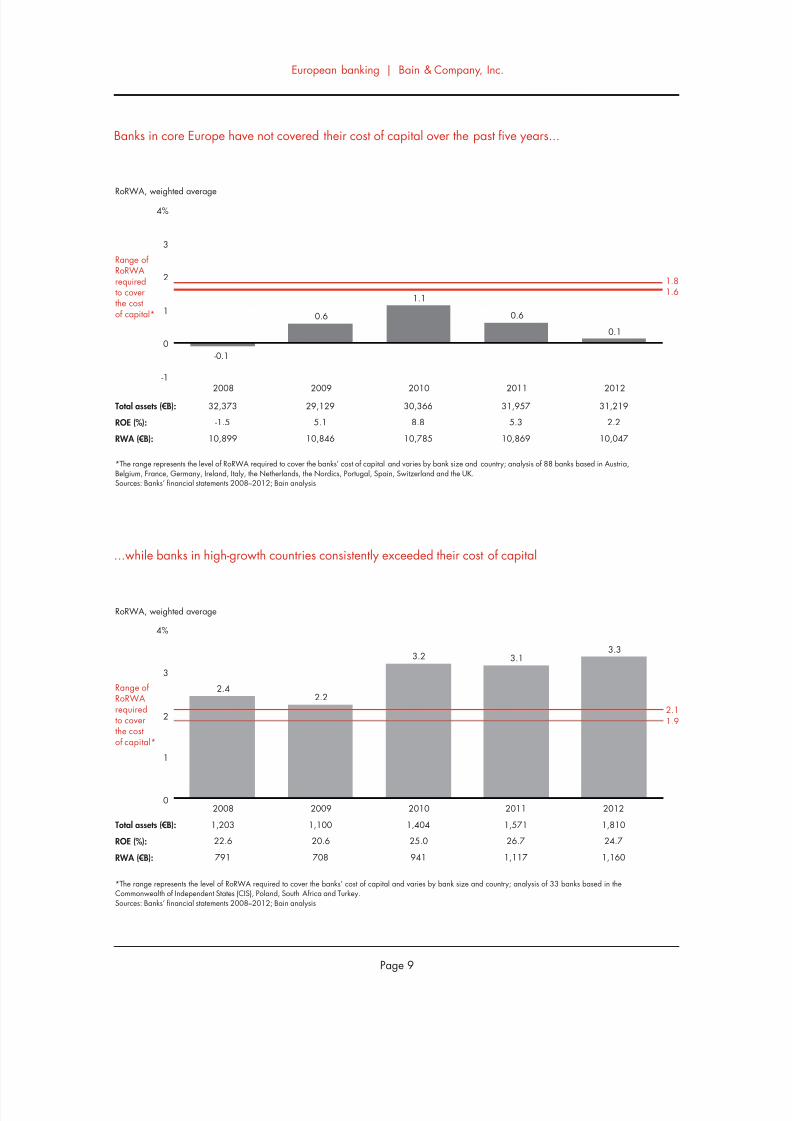

bull Banks in high-growth countries also consistently

exceeded their cost of capital whereas banks incore Europe have not covered their cost of capitalonly coming close to that bar in 2010 Core Europeexperienced a major amount of deleveragingdespite extraordinary initiatives such as theEuropean Central Bankrsquos long-term refinancingoperation (LTRO)

bull The quality of management plays a major role inindividual bank performance particularly in theslow-growth countries There was a wide rangeof RoRWAs among banks in those markets for each

of the five yearsbull In 2012 the biggest factors determining significant

value destruction were cost of risk as loan-lossprovisions rose and increased operating costwhich trended up as a percent of risk-weightedassets More active management of the balance sheethelped raise revenues but fees and commissionsprogressively declined

bull The larger the bank the better its performance onaverage The 10 biggest banks used their improve-

ments in financial margins and lower risk costs tocome close to earning their cost of capital

bull Other large regional banks managed to keep oper-ating costs lower than the 10 biggest but still fellwell short of their capital hurdle Smaller local banksfared the worst posting a negative RoRWA in 2012They have been forced to undertake a major de-leveraging of their balance sheets

1Five years of

RoRWA in Europe

A bumpy

landscape

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 1032

European banking | Bain amp Company Inc

Page 8

Although RoRWA correlates with economic growth there is still substantial variation among banks

Note Each observation is composed of a bankrsquos RoRWA in a given year and the respective countryrsquos year-over-year GDP growth rate in that yearSources Banksrsquo financial statements 2008ndash2012 n=605 Bureau van Dijk Bain analysis

RoRWA per bank and year 2008ndash2012

-5

-3

0

3

5

-10 0 10 20 30

95 ofobservationsfall withinthis band

Recessionno growthManagement has a major role

in determining RoRWA

Mediumhigh growthManagement has amore limited role in

achieving high RoRWA

Very high growthManagementrsquos most important role

is to optimize strategic asset allocationfor revenue generation

GDP growth by country and year 2008ndash2012

Bank profitability has eroded since the post-crisis peak of 2010

Return on equity (ROE) = Pretax profitaverage shareholdersrsquo equitySources Banksrsquo financial statements 2008ndash2012 n=121 Bureau van Dijk Bain analysis

European-wide RoRWA

0

1

2

200800

2009

07

2010 2011

09

2012

05

RWA (euroB)

33576

08

11690

44

30229

64

11555

-32

31770

104

11726

52

33528

75

11986

53

33028

49

11207

29

Total assets (euroB)

Annual GDP growth ()

ROE ()

13

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 1132

European banking | Bain amp Company Inc

Page 9

Banks in core Europe have not covered their cost of capital over the past five years

The range represents the level of RoRWA required to cover the banksrsquo cost of capital and varies by bank size and country analysis of 88 banks based in AustriaBelgium France Germany Ireland Italy the Netherlands the Nordics Portugal Spain Switzerland and the UKSources Banksrsquo financial statements 2008ndash2012 Bain analysis

RoRWA weighted average

RWA (euroB)

32373

-15

10899

29129

51

10846

30366

88

10785

31957

53

10869

31219

22

10047

Total assets (euroB)

ROE ()

2008

-01

2009

06

2010 2011

06

2012

01

Range ofRoRWArequiredto coverthe costof capital

11

-1

0

1

2

3

4

1816

while banks in high-growth countries consistently exceeded their cost of capital

The range represents the level of RoRWA required to cover the banksrsquo cost of capital and varies by bank size and country analysis of 33 banks based in theCommonwealth of Independent States (CIS) Poland South Africa and TurkeySources Banksrsquo financial statements 2008ndash2012 Bain analysis

RoRWA weighted average

RWA (euroB)

1203

226

791

1100

206

708

Total assets (euroB)

ROE ()

Range ofRoRWArequiredto coverthe costof capital

0

1

2

3

4

2008

24

2009

22

1404

250

941

2010

32

1571

267

1117

2011

31

1810

247

1160

2012

33

2119

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 1232

European banking | Bain amp Company Inc

Page 10

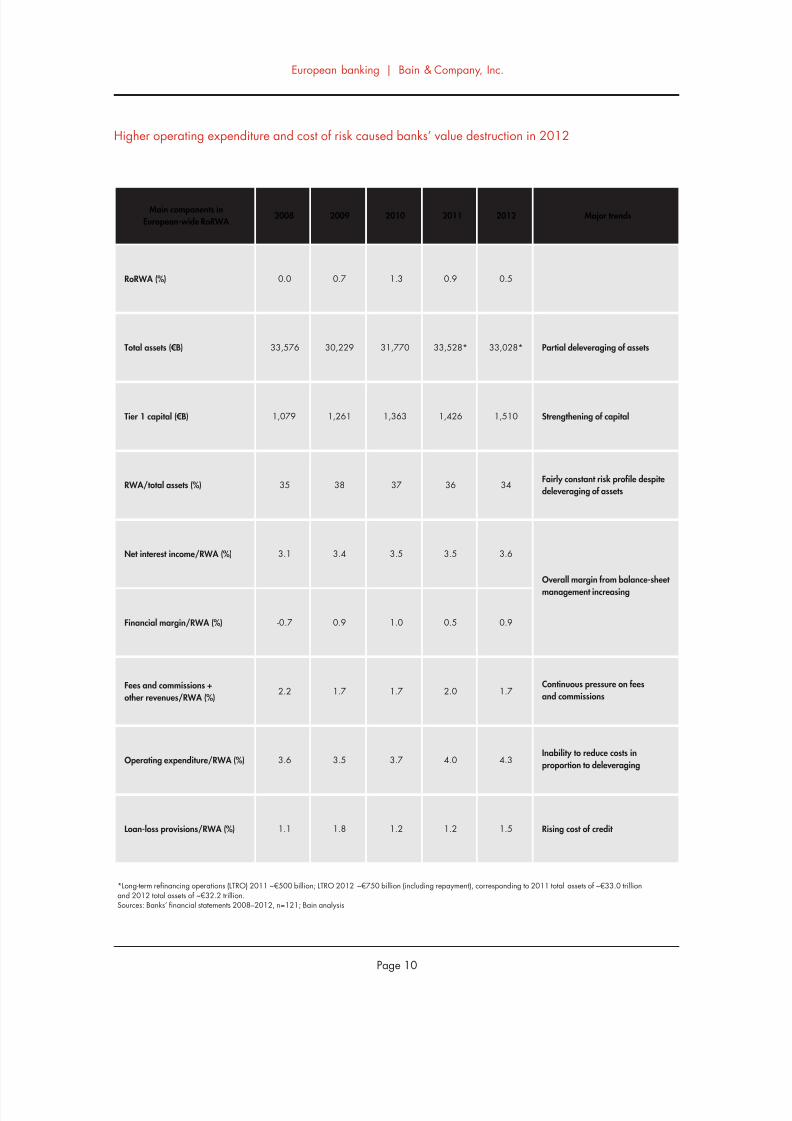

Higher operating expenditure and cost of risk caused banksrsquo value destruction in 2012

Long-term refinancing operations (LTRO) 2011 ~euro500 billion LTRO 2012 ~euro750 billion (including repayment) corresponding to 2011 total assets of ~euro330 trillionand 2012 total assets of ~euro322 trillionSources Banksrsquo financial statements 2008ndash2012 n=121 Bain analysis

20122010 2011

RoRWA ()

Total assets (euroB)

Tier 1 capital (euroB)

RWAtotal assets ()

Net interest incomeRWA ()

Financial marginRWA ()

Fees and commissions +

other revenuesRWA ()

Operating expenditureRWA ()

Loan-loss provisionsRWA ()

05

33028

1510

34

36

09

17

43

15

13

31770

1363

37

35

10

17

37

12

09

33528

1426

36

35

05

20

40

12

2009

07

30229

1261

38

34

09

17

35

18

00

33576

1079

35

31

-07

22

36

11

2008Main components in

European-wide RoRWA Major trends

Partial deleveraging of assets

Strengthening of capital

Fairly constant risk profile despite

deleveraging of assets

Overall margin from balance-sheet

management increasing

Continuous pressure on fees

and commissions

Inability to reduce costs in

proportion to deleveraging

Rising cost of credit

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 1332

European banking | Bain amp Company Inc

Page 11

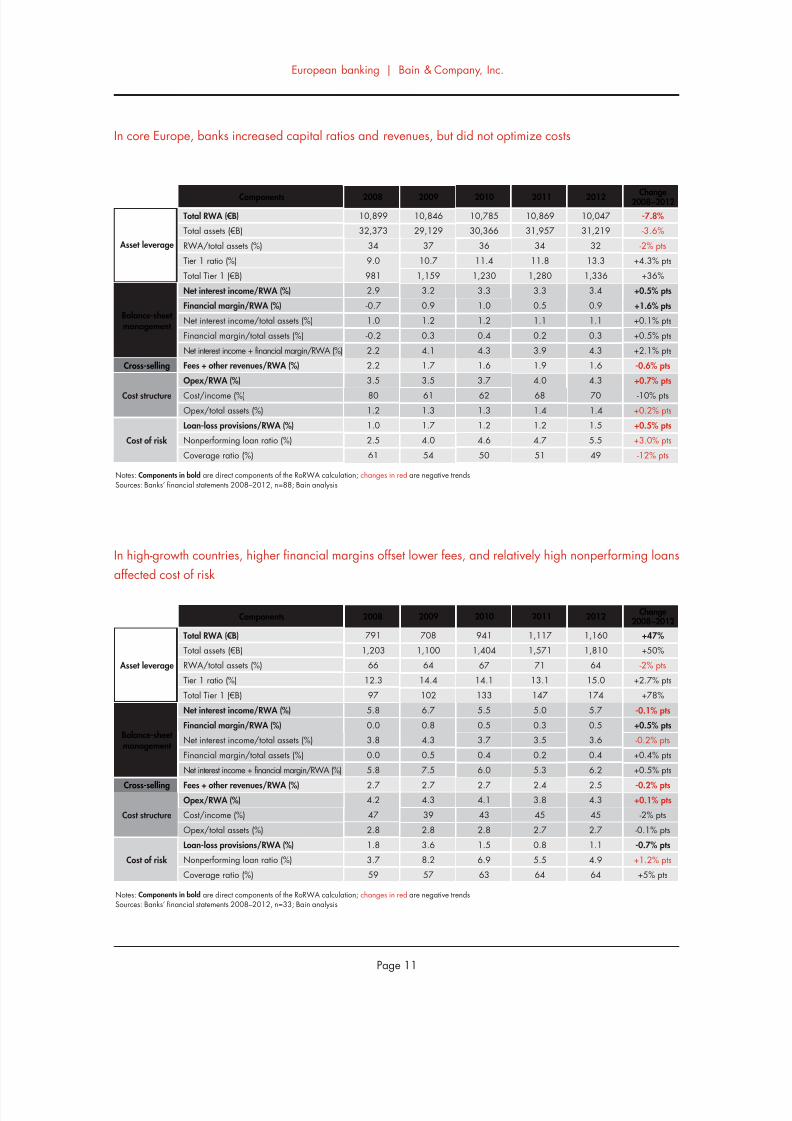

In core Europe banks increased capital ratios and revenues but did not optimize costs

Notes Components in bold are direct components of the RoRWA calculation changes in red are negative trendsSources Banksrsquo financial statements 2008ndash2012 n=88 Bain analysis

2012 Change2008minus20122010 2011

Total RWA (euroB)

Total assets (euroB)

RWAtotal assets ()

Tier 1 ratio ()

Total Tier 1 (euroB)

Net interest incomeRWA ()

Financial marginRWA ()

Net interest incometotal assets ()

Financial margintotal assets ()

Net interest income + financial marginRWA ()

Fees + other revenuesRWA ()

OpexRWA ()

Costincome ()

Loan-loss provisionsRWA ()

Nonperforming loan ratio ()

Coverage ratio ()

10047

31219

32

133

1336

34

09

11

03

43

16

43

70

15

55

49

-78

-36

-2 pts

+43 pts

+36

+05 pts

+16 pts

+01 pts

+05 pts

+21 pts

-06 pts

+07 pts

-10 pts

+05 pts

+30 pts

-12 pts

10785

30366

36

114

1230

33

10

12

04

43

16

37

62

12

46

50

10869

31957

34

118

1280

33

05

11

02

39

19

40

68

12

47

51

2009

10846

29129

37

107

1159

32

09

12

03

41

17

35

61

17

40

54

10899

32373

34

90

981

29

-07

10

-02

22

22

35

80Opextotal assets () 14 +02 pts13 141312

10

25

61

Cross-selling

Asset leverage

Balance-sheet management

Cost structure

Cost of risk

2008Components

In high-growth countries higher financial margins offset lower fees and relatively high nonperforming loans

affected cost of risk

Notes Components in bold are direct components of the RoRWA calculation changes in red are negative trendsSources Banksrsquo financial statements 2008ndash2012 n=33 Bain analysis

2012 Change2008minus2012

2010 2011

Total RWA (euroB)

Total assets (euroB)

RWAtotal assets ()

Tier 1 ratio ()

Total Tier 1 (euroB)

Net interest incomeRWA ()

Financial marginRWA ()

Net interest incometotal assets ()

Financial margintotal assets ()

Net interest income + financial marginRWA ()

Fees + other revenuesRWA ()OpexRWA ()

Costincome ()

Opextotal assets ()

Loan-loss provisionsRWA ()

Nonperforming loan ratio ()

Coverage ratio ()

1160

1810

64

150

174

57

05

36

04

62

2543

45

27

11

49

64

+47

+50

-2 pts

+27 pts

+78

-01 pts

+05 pts

-02 pts

+04 pts

+05 pts

-02 pts+01 pts

-2 pts

-01 pts

-07 pts

+12 pts

+5 pts

941

1404

67

141

133

55

05

37

04

60

2741

43

28

15

69

63

1117

1571

71

131

147

50

03

35

02

53

2438

45

27

08

55

64

2009

708

1100

64

144

102

67

08

43

05

75

2743

39

28

36

82

57

791

1203

66

123

97

58

00

38

00

58

2742

47

28

18

37

59

Cross-selling

Asset leverage

Balance-sheet management

Cost structure

Cost of risk

2008Components

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 1432

European banking | Bain amp Company Inc

Page 12

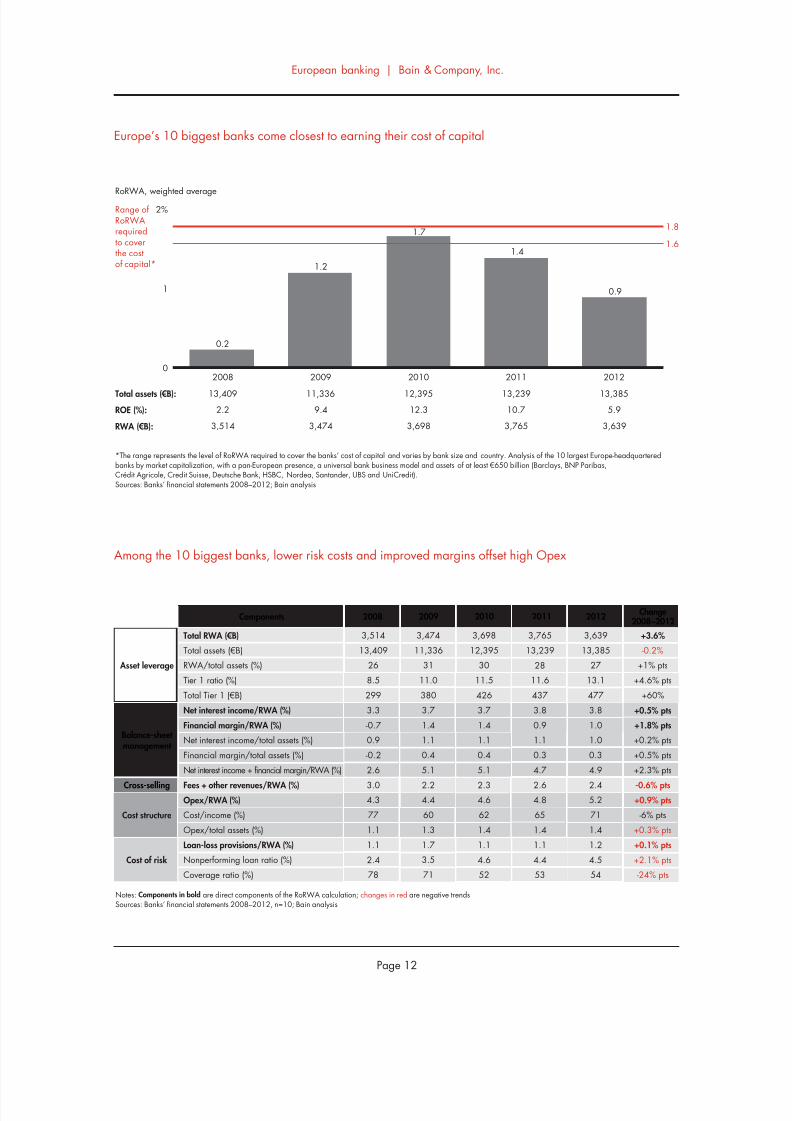

Europersquos 10 biggest banks come closest to earning their cost of capital

The range represents the level of RoRWA required to cover the banksrsquo cost of capital and varies by bank size and country Analysis of the 10 largest Europe-headquarteredbanks by market capitalization with a pan-European presence a universal bank business model and assets of at least euro650 billion (Barclays BNP ParibasCreacutedit Agricole Credit Suisse Deutsche Bank HSBC Nordea Santander UBS and UniCredit)Sources Banksrsquo financial statements 2008ndash2012 Bain analysis

RoRWA weighted average

RWA (euroB)

1340922

3514

1133694

3474

Total assets (euroB)

ROE ()

Range ofRoRWArequiredto coverthe costof capital

12395123

3698

13239107

3765

1338559

3639

2008

02

2009 2010

17

2011

14

2012

09

12

0

1

2

18

16

Among the 10 biggest banks lower risk costs and improved margins offset high Opex

Notes Components in bold are direct components of the RoRWA calculation changes in red are negative trendsSources Banksrsquo financial statements 2008ndash2012 n=10 Bain analysis

2012 Change2008minus2012

2010 2011

Total RWA (euroB)

Total assets (euroB)

RWAtotal assets ()

Tier 1 ratio ()

Total Tier 1 (euroB)

Net interest incomeRWA ()

Financial marginRWA ()

Net interest incometotal assets ()

Financial margintotal assets ()

Net interest income + financial marginRWA ()

Fees + other revenuesRWA ()OpexRWA ()

Costincome ()

Opextotal assets ()

Loan-loss provisionsRWA ()

Nonperforming loan ratio ()

Coverage ratio ()

3639

13385

27

131

477

38

10

10

03

49

2452

71

14

12

45

54

+36

-02

+1 pts

+46 pts

+60

+05 pts

+18 pts

+02 pts

+05 pts

+23 pts

-06 pts+09 pts

-6 pts

+03 pts

+01 pts

+21 pts

-24 pts

3698

12395

30

115

426

37

14

11

04

51

2346

62

14

11

46

52

3765

13239

28

116

437

38

09

11

03

47

2648

65

14

11

44

53

2009

3474

11336

31

110

380

37

14

11

04

51

2244

60

13

17

35

71

3514

13409

26

85

299

33

-07

09

-02

26

3043

77

11

11

24

78

Cross-selling

Asset leverage

Balance-sheet management

Cost structure

Cost of risk

2008Components

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 1532

European banking | Bain amp Company Inc

Page 13

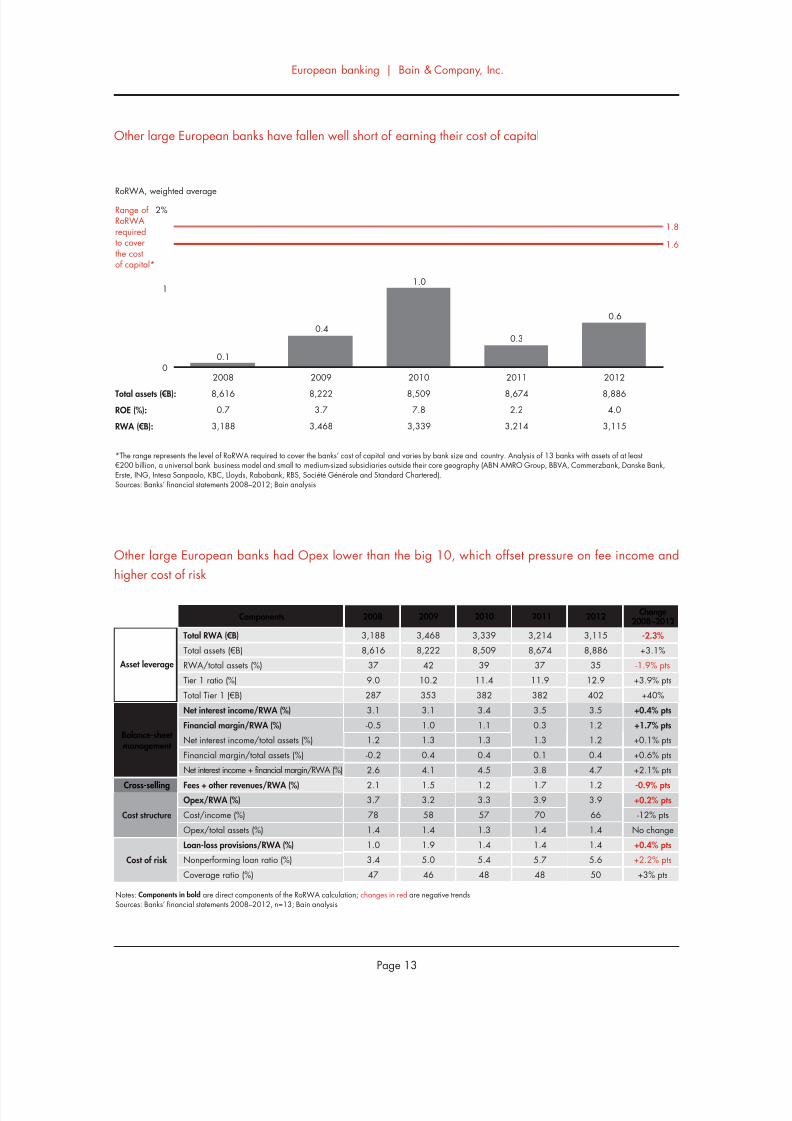

Other large European banks have fallen well short of earning their cost of capital

The range represents the level of RoRWA required to cover the banksrsquo cost of capital and varies by bank size and country Analysis of 13 banks with assets of at leasteuro200 billion a universal bank business model and small to medium-sized subsidiaries outside their core geography (ABN AMRO Group BBVA Commerzbank Danske BankErste ING Intesa Sanpaolo KBC Lloyds Rabobank RBS Socieacuteteacute Geacuteneacuterale and Standard Chartered)Sources Banksrsquo financial statements 2008ndash2012 Bain analysis

RoRWA weighted average

RWA (euroB)

Total assets (euroB)

ROE ()

Range ofRoRWArequiredto coverthe costof capital

861607

3188

2008

01

822237

3468

2009

04

850978

3339

2010

867422

3214

2011

03

888640

3115

2012

06

10

0

1

2

18

16

Other large European banks had Opex lower than the big 10 which offset pressure on fee income and

higher cost of risk

Notes Components in bold are direct components of the RoRWA calculation changes in red are negative trendsSources Banksrsquo financial statements 2008ndash2012 n=13 Bain analysis

2012 Change2008minus2012

2010 2011

Total RWA (euroB)

Total assets (euroB)

RWAtotal assets ()

Tier 1 ratio ()

Total Tier 1 (euroB)

Net interest incomeRWA ()

Financial marginRWA ()

Net interest incometotal assets ()

Financial margintotal assets ()

Net interest income + financial marginRWA ()

Fees + other revenuesRWA ()OpexRWA ()

Costincome ()

Opextotal assets ()

Loan-loss provisionsRWA ()

Nonperforming loan ratio ()

Coverage ratio ()

3115

8886

35

129

402

35

12

12

04

47

1239

66

14

14

56

50

-23

+31

-19 pts

+39 pts

+40

+04 pts

+17 pts

+01 pts

+06 pts

+21 pts

-09 pts+02 pts

-12 pts

No change

+04 pts

+22 pts

+3 pts

3339

8509

39

114

382

34

11

13

04

45

1233

57

13

14

54

48

3214

8674

37

119

382

35

03

13

01

38

1739

70

14

14

57

48

2009

3468

8222

42

102

353

31

10

13

04

41

1532

58

14

19

50

46

3188

8616

37

90

287

31

-05

12

-02

26

2137

78

14

10

34

47

Cross-selling

Asset leverage

Balance-sheet management

Cost structure

Cost of risk

2008Components

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 1632

European banking | Bain amp Company Inc

Page 14

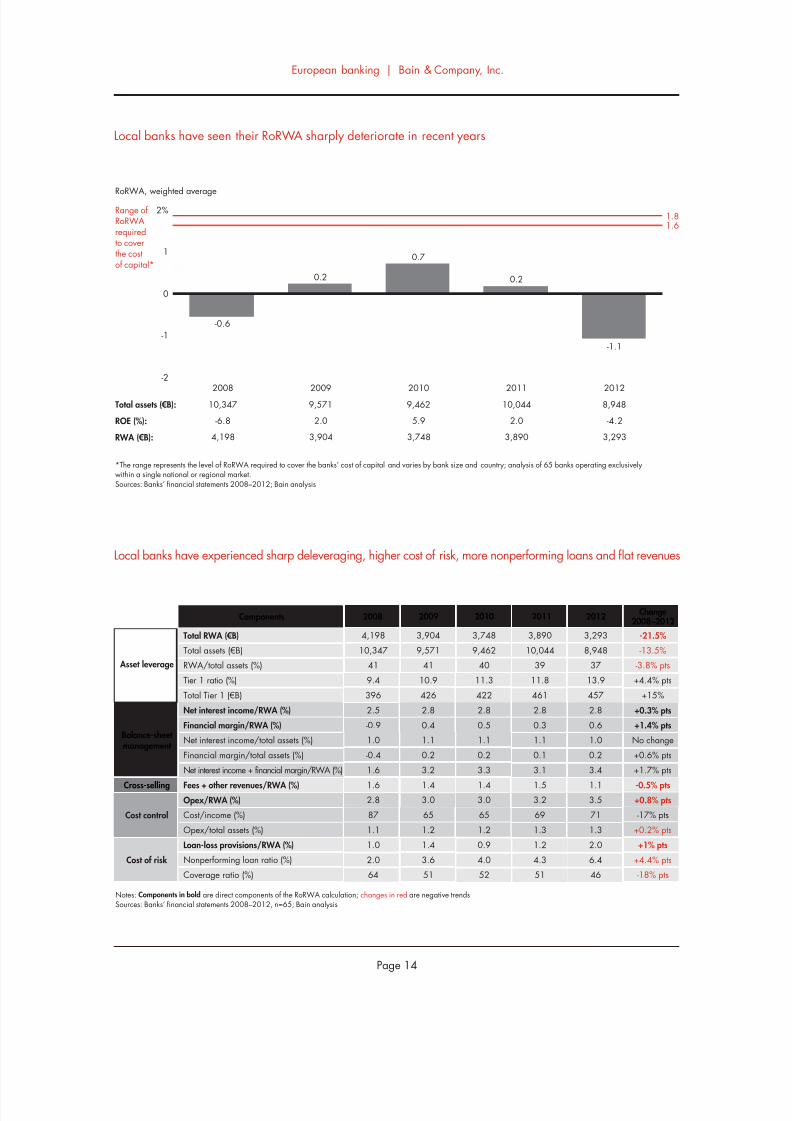

Local banks have seen their RoRWA sharply deteriorate in recent years

The range represents the level of RoRWA required to cover the banksrsquo cost of capital and varies by bank size and country analysis of 65 banks operating exclusivelywithin a single national or regional marketSources Banksrsquo financial statements 2008ndash2012 Bain analysis

RoRWA weighted average

RWA (euroB)

Total assets (euroB)

ROE ()

Range ofRoRWArequiredto coverthe costof capital

10347

-68

4198

9571

20

3904

9462

59

3748

10044

20

3890

8948

-42

3293

2008

-06

2009

02

2010

07

2011

02

2012

-11

-2

-1

0

1

21816

Local banks have experienced sharp deleveraging higher cost of risk more nonperforming loans and flat revenues

Notes Components in bold are direct components of the RoRWA calculation changes in red are negative trendsSources Banksrsquo financial statements 2008ndash2012 n=65 Bain analysis

2012 Change2008minus2012

2010 2011

Total RWA (euroB)

Total assets (euroB)

RWAtotal assets ()

Tier 1 ratio ()

Total Tier 1 (euroB)

Net interest incomeRWA ()

Financial marginRWA ()

Net interest incometotal assets ()

Financial margintotal assets ()

Net interest income + financial marginRWA ()

Fees + other revenuesRWA ()OpexRWA ()

Costincome ()

Opextotal assets ()

Loan-loss provisionsRWA ()

Nonperforming loan ratio ()

Coverage ratio ()

3293

8948

37

139

457

28

06

10

02

34

1135

71

13

20

64

46

-215

-135

-38 pts

+44 pts

+15

+03 pts

+14 pts

No change

+06 pts

+17 pts

-05 pts+08 pts

-17 pts

+02 pts

+1 pts

+44 pts

-18 pts

3748

9462

40

113

422

28

05

11

02

33

1430

65

12

09

40

52

3890

10044

39

118

461

28

03

11

01

31

1532

69

13

12

43

51

2009

3904

9571

41

109

426

28

04

11

02

32

1430

65

12

14

36

51

4198

10347

41

94

396

25

-09

10

-04

16

1628

87

11

10

20

64

Cross-selling

Asset leverage

Balance-sheet management

Cost control

Cost of risk

2008Components

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 1732

European banking | Bain amp Company Inc

Page 15

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 1832

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 1932

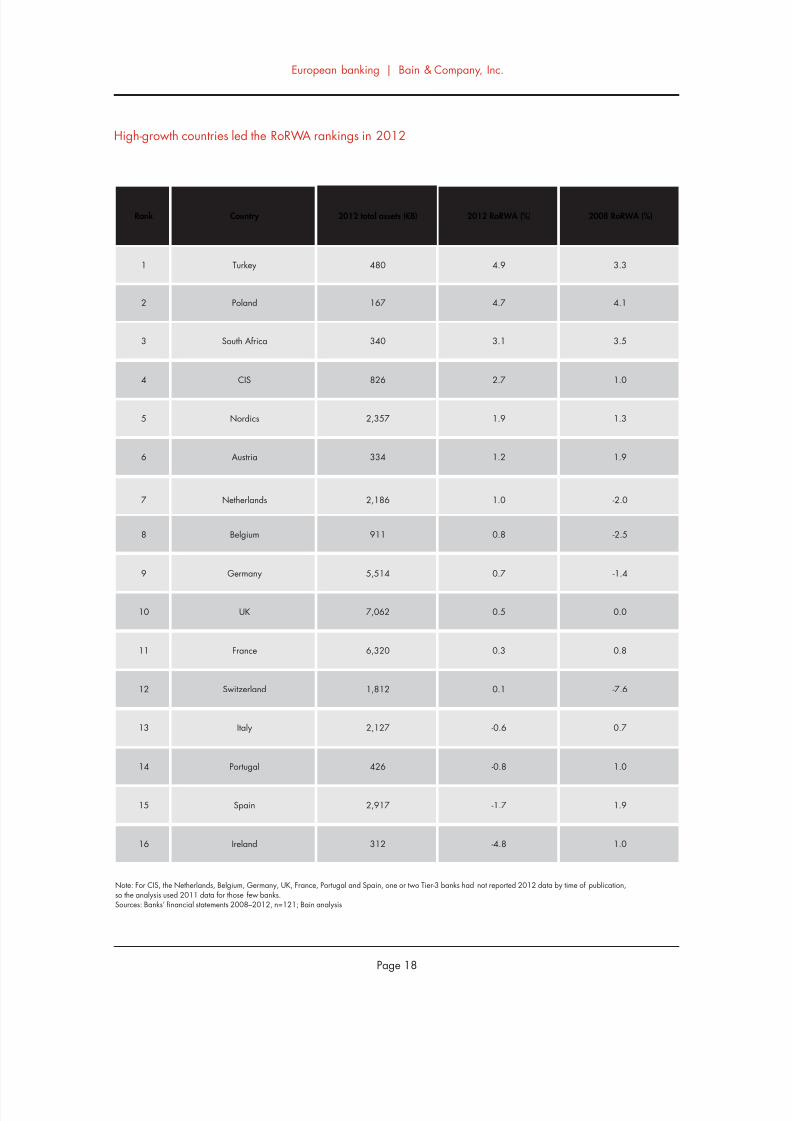

bull Countries with strong economic growth led the2012 RoRWA rankings Turkey took pole positionwith a 49 RoRWA In core Europe the Nordic

countries posed the strongest performance witha 19 RoRWA followed by Austria and theNetherlands The largest economies of Germanythe UK and France trailed behind

bull Banks in Italy Portugal Spain and Ireland whichhave been mired in the sovereign debt crisis anddeep economic recessions turned in the weakestRoRWA performances

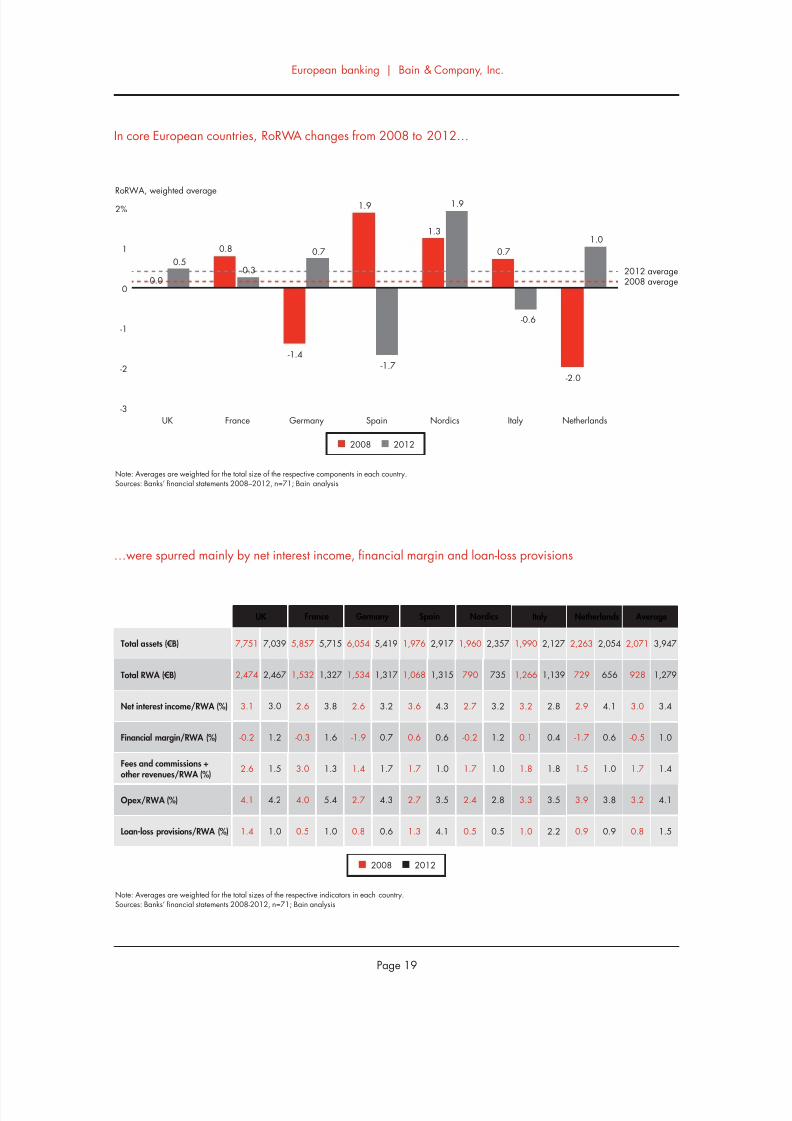

bull Among the core European countries changes inRoRWAs from 2008 to 2012 stemmed mainly

from changes in three components net interestincome financial margin and loan-loss provisions

bull Countries that posted large positive changesmdashincluding Germany the Netherlands the Nordiccountries and the UKmdashbenefited from higherfinancial margins more control of operatingexpenditure and lower cost of risk Countries withlarge drops in RoRWAs were hurt by infl exiblecost structures which prevented them from shrinkingtheir production costs and a cost of risk that was

almost double the averagebull Northern Europe dominated the league tables

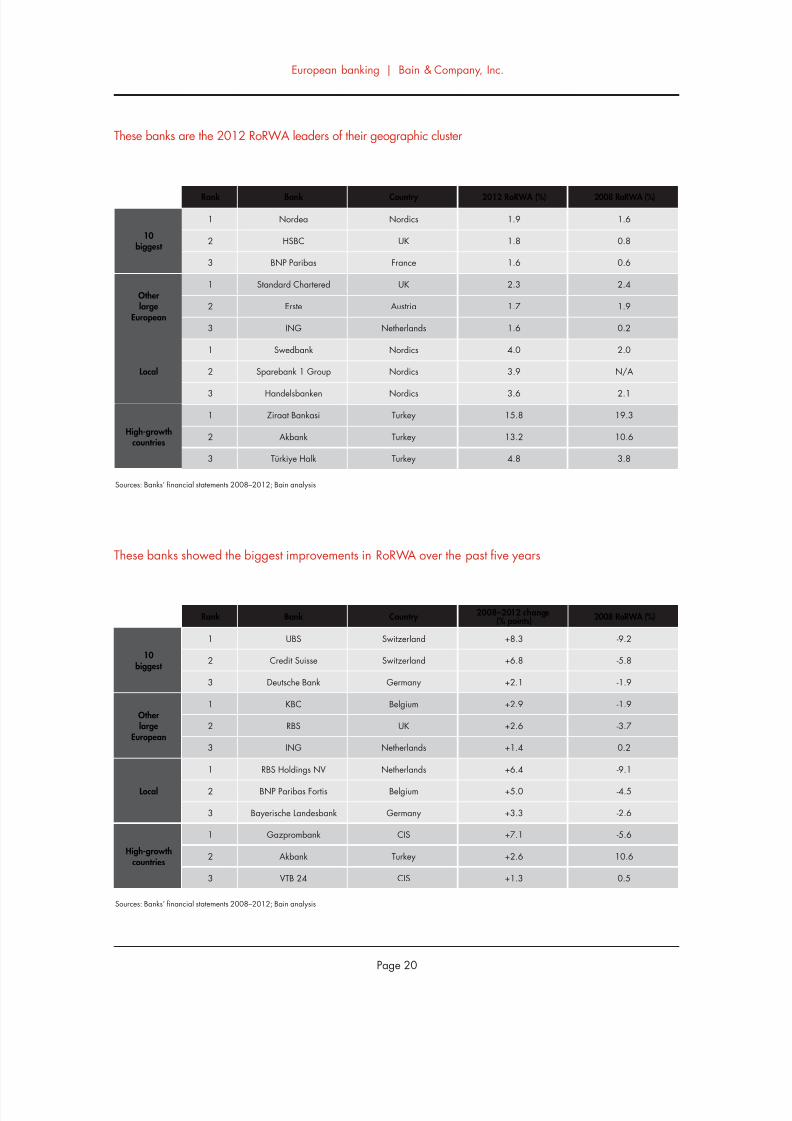

whether one looks at the 2012 leaders or themost improved banks For example the RoRWAleaders among both local and the 10 biggestbanks included banks in the Nordic countriesfollowed by those in the UK France Austria andthe Netherlands

bull In the most improved group banks in Switzer-land the Netherlands and Germany made a

strong showing

bull In high-growth countries Turkey and the Common-wealth of Independent States (CIS) took leadingpositions for the most improved banks and Turkeyfor the 2012 leaders

2Country and cluster

league tables

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 2032

European banking | Bain amp Company Inc

Page 18

High-growth countries led the RoRWA rankings in 2012

Note For CIS the Netherlands Belgium Germany UK France Portugal and Spain one or two Tier-3 banks had not reported 2012 data by time of publicationso the analysis used 2011 data for those few banksSources Banksrsquo financial statements 2008ndash2012 n=121 Bain analysis

Rank 2012 RoRWA ()

Turkey

Poland

South Africa

CIS

Nordics

Austria

Netherlands

Belgium

Germany

UK

France

Switzerland

Italy

Portugal

Spain

Ireland

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

49

47

31

27

19

12

10

08

07

05

03

01

-06

-08

-17

-48

480

167

340

826

2357

334

2186

911

5514

7062

6320

1812

2127

426

2917

312

2012 total assets (euroB)Country 2008 RoRWA ()

33

41

35

10

13

19

-20

-25

-14

00

08

-76

07

10

19

10

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 2132

European banking | Bain amp Company Inc

Page 19

In core European countries RoRWA changes from 2008 to 2012hellip

Note Averages are weighted for the total size of the respective components in each countrySources Banksrsquo financial statements 2008ndash2012 n=71 Bain analysis

RoRWA weighted average

-3

-2

-1

0

1

2

2008 average2012 average

UK

05

France

08

Germany

-14

07

Spain

19

-17

Nordics

13

19

Italy

07

-06

Netherlands

-20

10

2008 2012

0003

hellipwere spurred mainly by net interest income financial margin and loan-loss provisions

Note Averages are weighted for the total sizes of the respective indicators in each countrySources Banksrsquo financial statements 2008-2012 n=71 Bain analysis

NordicsGermany Spain

Total assets (euroB)

Total RWA (euroB)

Net interest incomeRWA ()

Financial marginRWA ()

Fees and commissions +other revenuesRWA ()

OpexRWA ()

Loan-loss provisionsRWA ()

France

7751

UK

2008 2012

AverageItaly Netherlands

7039

2474 2467

31 30

-02 12

26 15

41 42

14 10

5857 5715

1532 1327

26 38

-03 16

30 13

40 54

05 10

6054 5419

1534 1317

26 32

-19 07

14 17

27 43

08 06

1976 2917

1068 1315

36 43

06 06

17 10

27 35

13 41

1960 2357

790 735

27 32

-02 12

17 10

24 28

05 05

1990 2127

1266 1139

32 28

01 04

18 18

33 35

10 22

2263 2054

729 656

29 41

-17 06

15 10

39 38

09 09

2071 3947

928 1279

30 34

-05 10

17 14

32 41

08 15

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 2232

European banking | Bain amp Company Inc

Page 20

These banks are the 2012 RoRWA leaders of their geographic cluster

Sources Banksrsquo financial statements 2008ndash2012 Bain analysis

Rank 2012 RoRWA ()

Nordics

UK

France

UK

Austria

Netherlands

Nordics

Nordics

Nordics

Turkey

Turkey

Turkey

1

2

3

1

2

3

1

2

3

1

2

3

19

18

16

23

17

16

40

39

36

158

132

48

Nordea

HSBC

BNP Paribas

Standard Chartered

Erste

ING

Swedbank

Sparebank 1 Group

Handelsbanken

Ziraat Bankasi

Akbank

Tuumlrkiye Halk

Bank Country 2008 RoRWA ()

16

08

06

24

19

02

20

NA

21

193

106

38

10biggest

Otherlarge

European

Local

High-growthcountries

These banks showed the biggest improvements in RoRWA over the past five years

Sources Banksrsquo financial statements 2008ndash2012 Bain analysis

Rank 2008ndash2012 change( points)

Switzerland

Switzerland

Germany

Belgium

UK

Netherlands

Netherlands

Belgium

Germany

CIS

Turkey

CIS

1

2

3

1

2

3

1

2

3

1

2

3

+83

+68

+21

+29

+26

+14

+64

+50

+33

+71

+26

+13

UBS

Credit Suisse

Deutsche Bank

KBC

RBS

ING

RBS Holdings NV

BNP Paribas Fortis

Bayerische Landesbank

Gazprombank

Akbank

VTB 24

Bank Country 2008 RoRWA ()

-92

-58

-19

-19

-37

02

-91

-45

-26

-56

106

05

10biggest

Otherlarge

European

Local

High-growthcountries

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 2332

European banking | Bain amp Company Inc

Page 21

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 2432

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 2532

bull Europersquos environment continues to be volatile andinvestors are seeking better information about abankrsquos stability asset quality and key factors that

generate value RoRWA plays a useful role hereby focusing on the balance sheetmdashwhich enablescomparison between a bank and its peersmdashand byidentifying the factors influencing bank performance

bull Banks still need to address challenges along eachdimension of RoRWA in order to lift their profit-ability levels above the cost of capital In recent

years the profitability of lending assets has beensustained mainly by the fi nancial componentsincluding a boost from LTRO To raise asset prof-itability banks will have to better manage their

capital allocations and risk profilesbull The pressure on fee income will continue To offset

that trend banks should turn to their close clientrelationships for new sources of revenues

bull Lowering operating costs is the dimension thatwarrants managementrsquos attention at any bankregardless of size or location Initiatives that havethe greatest potential for tackling structural costsinclude adopting digital technologies and modern-izing IT platforms optimizing processes from endto end through outsourcing offshoring and other

means and expanding global procurement Suchinitiatives are essential for survival in an industrygoing through discontinuous change

bull Deleveraging the loan portfolio for riskier clients isa pressing issue which still poses significant threatsfor local banks In countries with a higher cost ofrisk and stagnant or negative GDP growth rateslocal banks may face further painful restructuring

bull Astute management of the cost of risk includingtaking a portfolio perspective offers opportunities

for most banksmdashin part to meet the new require-ments of Basel III and reassure rating agencies

bull Further consolidation of the local and other largebanks over the coming years will likely benefitthe 10 biggest banks and those in high-growthcountries These high-growth countries offer thegreatest opportunities for RoRWA growth for largeand pan-European players looking to diversifytheir portfolios

3Strategic

perspectives and

implications for

management

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 2632

European banking | Bain amp Company Inc

Page 24

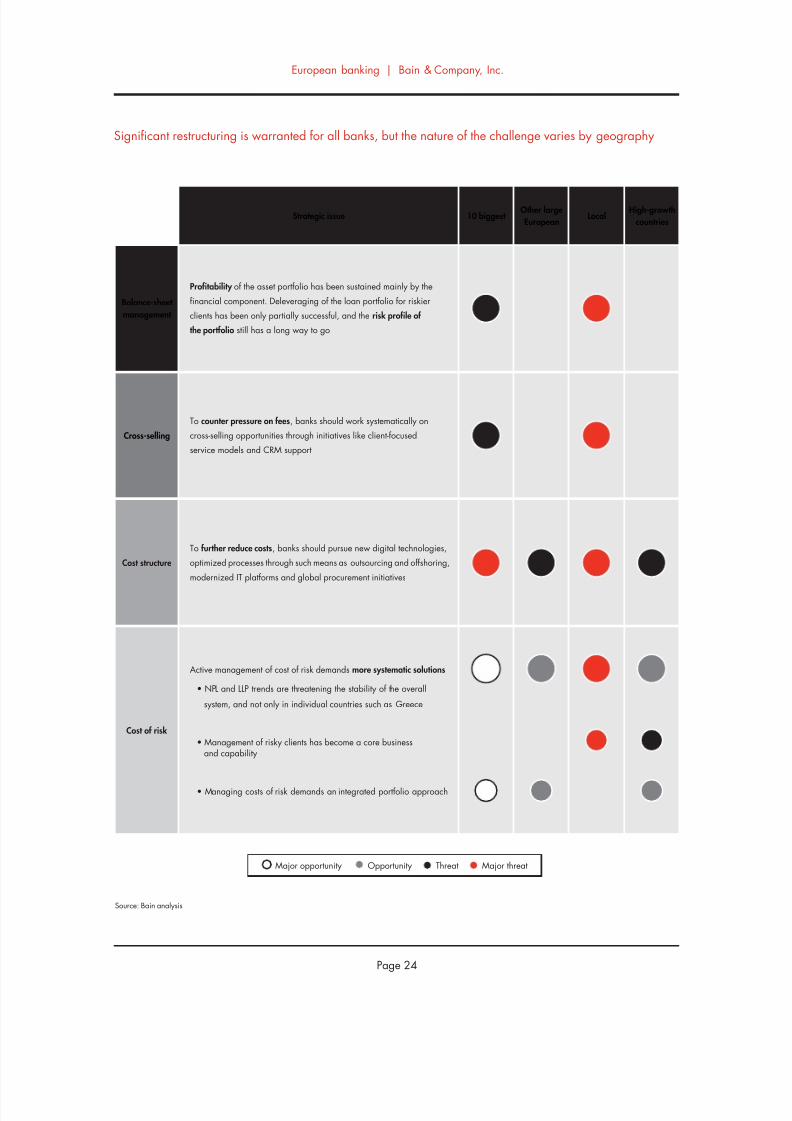

Significant restructuring is warranted for all banks but the nature of the challenge varies by geography

Source Bain analysis

10 biggest Strategic issueHigh-growth

countries

Other large

EuropeanLocal

Cross-selling

Balance-sheet

management

Cost structure

Cost of risk

Major threatThreatOpportunityMajor opportunity

Profitability of the asset portfolio has been sustained mainly by the

financial component Deleveraging of the loan portfolio for riskier

clients has been only partially successful and the risk profile of

the portfolio still has a long way to go

To counter pressure on fees banks should work systematically on

cross-selling opportunities through initiatives like client-focused

service models and CRM support

To further reduce costs banks should pursue new digital technologies

optimized processes through such means as outsourcing and offshoring

modernized IT platforms and global procurement initiatives

Active management of cost of risk demands more systematic solutions

bull NPL and LLP trends are threatening the stability of the overall

system and not only in individual countries such as Greece

bull Management of risky clients has become a core business and capability

bull Managing costs of risk demands an integrated portfolio approach

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 2732

European banking | Bain amp Company Inc

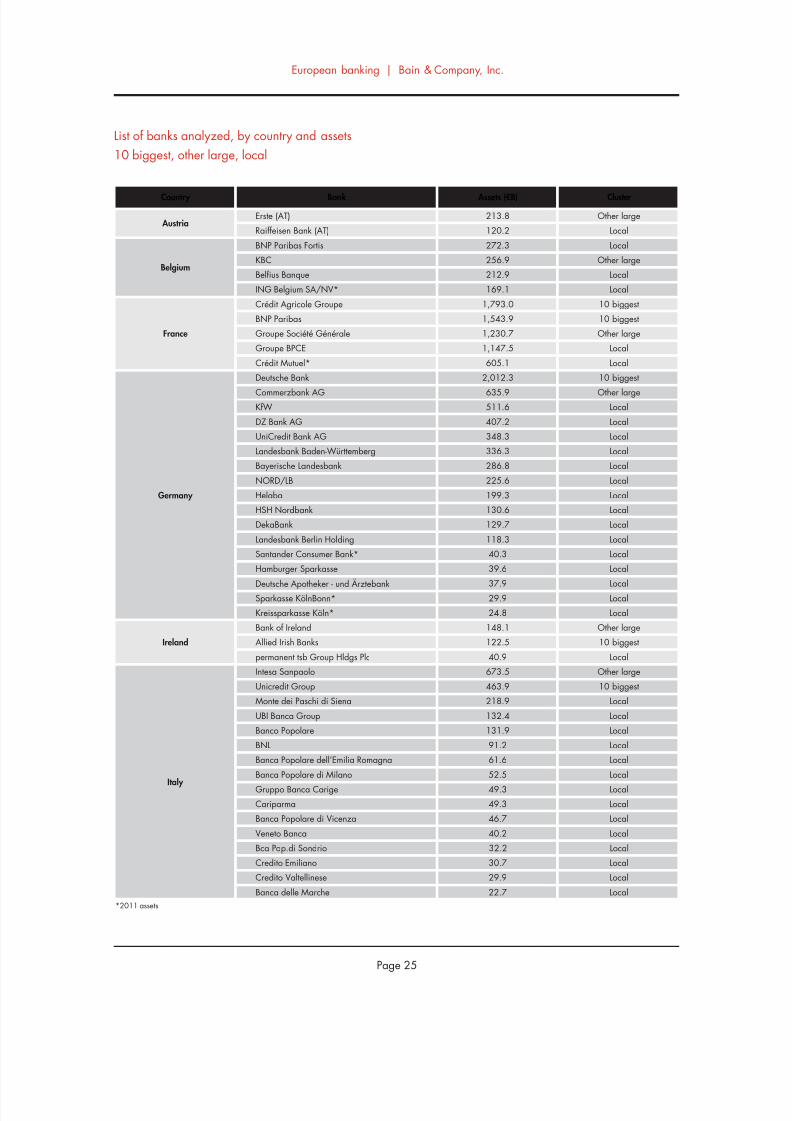

Page 25

Assets (euroB)

Erste (AT)

Raiffeisen Bank (AT)

BNP Paribas Fortis

KBC

Belfius Banque

ING Belgium SANV

Creacutedit Agricole Groupe

BNP Paribas

Groupe Socieacuteteacute Geacuteneacuterale

Groupe BPCE

Creacutedit Mutuel

Deutsche Bank

Commerzbank AGKfW

DZ Bank AG

UniCredit Bank AG

2138

1202

2723

2569

2129

1691

17930

15439

12307

11475

6051

20123

63595116

4072

3483

Austria

Belgium

France

Germany

Country Bank Cluster

Other large

Local

Local

Other large

Local

Local

10 biggest

10 biggest

Other large

Local

Local

10 biggest

Other largeLocal

Local

Local

Ireland

Landesbank Baden-Wuumlrttemberg

Bayerische Landesbank

NORDLB

Helaba

HSH Nordbank

DekaBank

Landesbank Berlin Holding

Santander Consumer Bank

Hamburger Sparkasse

Deutsche Apotheker - und Aumlrztebank

Sparkasse KoumllnBonn

Kreissparkasse Koumlln

Bank of Ireland

Allied Irish Banks

permanent tsb Group Hldgs Plc

Intesa Sanpaolo

3363

2868

2256

1993

1306

1297

1183

403

396

379

299

248

1481

1225

409

6735

Local

Local

Local

Local

Local

Local

Local

Local

Local

Local

Local

Local

Other large

10 biggest

Local

Other large

Unicredit Group

Monte dei Paschi di Siena

4639

2189

10 biggest

Local

UBI Banca Group

Banco Popolare

BNL

Banca Popolare dellrsquoEmilia Romagna

Banca Popolare di Milano

Gruppo Banca Carige

Cariparma

Banca Popolare di Vicenza

Veneto Banca

1324

1319

912

616

525

493

493

467

402

Local

Local

Local

Local

Local

Local

Local

Local

Local

Italy

2011 assets

Bca Popdi Sondrio 322 Local

Credito Emiliano

Credito Valtellinese

Banca delle Marche

307

299

227

Local

Local

Local

List of banks analyzed by country and assets

10 biggest other large local

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 2832

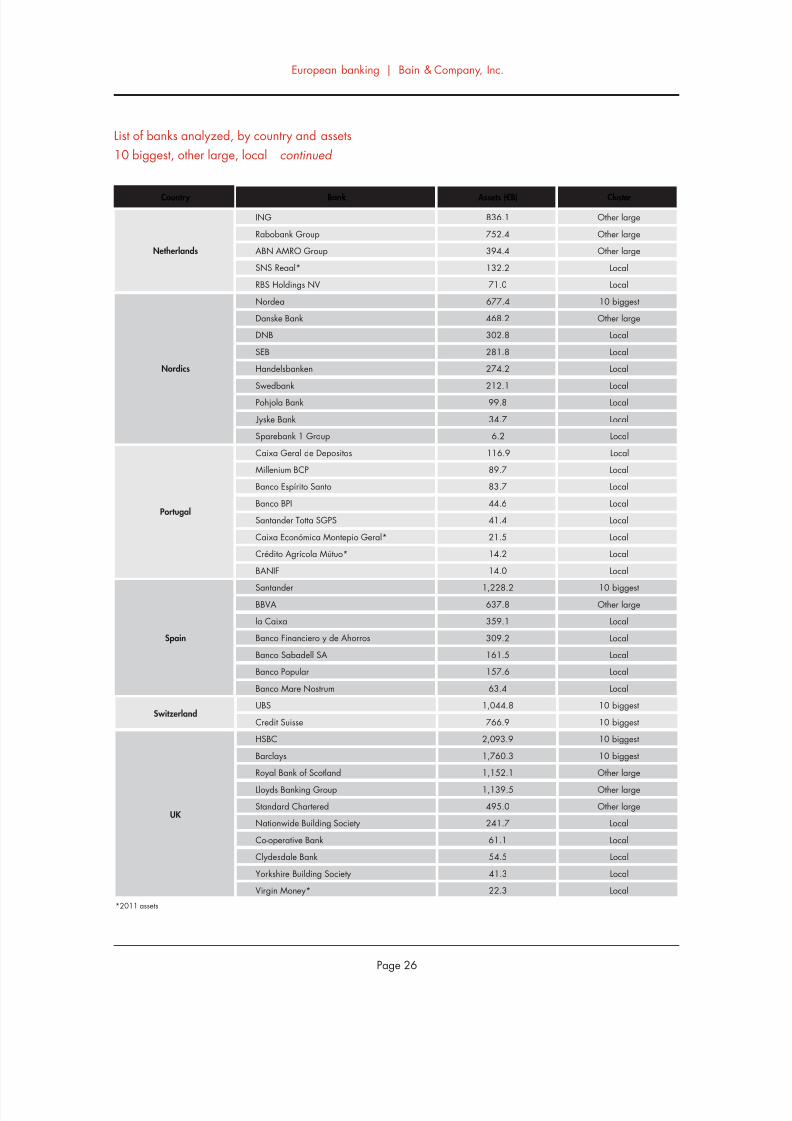

European banking | Bain amp Company Inc

Page 26

Assets (euroB)Country Bank Cluster

ING

Rabobank Group

ABN AMRO Group

SNS Reaal

RBS Holdings NV

8361

7524

3944

1322

710

Netherlands

Other large

Other large

Other large

Local

Local

Nordea 6774 10 biggest

Danske Bank

DNB

4682

3028

Other large

Local

SEB

Handelsbanken

Swedbank

Pohjola Bank

2818

2742

2121

998

Local

Local

Local

Local

Nordics

Jyske Bank 347 Local

Sparebank 1 Group 62 Local

Caixa Geral de Depositos 1169 Local

Millenium BCP

Banco Espiacuterito Santo

897

837

Local

Local

Banco BPI

Santander Totta SGPS

Caixa Econoacutemica Montepio Geral

Creacutedito Agriacutecola Muacutetuo

446

414

215

142

Local

Local

Local

Local

Portugal

BANIF 140 Local

SantanderBBVA

la Caixa

Banco Financiero y de Ahorros

Banco Sabadell SA

122826378

3591

3092

1615

Spain

10 biggestOther large

Local

Local

Local

Banco Popular

Banco Mare Nostrum

1576

634

Local

Local

UBS

Credit Suisse

10448

7669Switzerland

10 biggest

10 biggest

HSBC 20939 10 biggest

Barclays

Royal Bank of Scotland

17603

11521

10 biggest

Other large

Lloyds Banking Group

Standard Chartered

Nationwide Building Society

Co-operative Bank

11395

4950

2417

611

Other large

Other large

Local

Local

UK

Clydesdale Bank 545 Local

Yorkshire Building Society 413 Local

Virgin Money 223 Local

2011 assets

List of banks analyzed by country and assets

10 biggest other large localmdashcontinued

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 2932

European banking | Bain amp Company Inc

Page 27

Assets (euroB)

Sberbank

VTB 24

PKO BP

Bank Pekao

BRE Bank

ING Bank Slaski

Standard Bank

Absa

FirstRand

Nedbank

Investec

Tuumlrkiye İş Bankası

Tuumlrkiye Garanti

Ziraat Bankasi

Akbank

Yapı ve Kredi

3781

1857

463

361

244

187

928

766

729

647

330

869

777

708

706

568

CIS

Poland

South Africa

Turkey

Country Bank

Tuumlrkiye Halk Bankasi

Tuumlrkiye Vakıflar

Finansbank

471

467

239

Gazprombank

Russian Agricultural Bank

Alfa-Bank

Nomos-Bank

UniCredit Bank Russia

712

358

357

225

218

AKB Rosbank

Promsvyazbank

ZAO Raiffeisenbank

URALSIB Bank

Russian Standard Bank

AKB Probusinessbank

200

173

160

113

74

35

2011 assets

Bank Zachodni WBK + Kredyt Bank

Getin NobleBank

Bank Millennium

143

141

126

List of banks analyzed by country and assets

High-growth countries

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 3032

European banking | Bain amp Company Inc

Page 28

Key contacts in Bainrsquos European Financial Services practice

Franco Baronio in Milan (francobaroniobaincom)Rocco DrsquoAcunto in Milan (roccodacuntobaincom)

Ada Di Marzo in Paris (adadimarzobaincom)

Bertrand Facq in Warsaw (bertrandfacqbaincom)

Fabrice Franzen in Johannesburg (fabricefranzenbaincom)

Thomas Herbeck in Frankfurt (thomasherbeckbaincom)

Karaca Kestelli in Istanbul (karacakestellibaincom)

Nicolaacutes Lopez in Madrid (nicolaslopezbaincom)

Niels Peder Nielsen in Copenhagen (nielspedernielsenbaincom)

Andrea Oldrini in Milan (andreaoldrinibaincom)

Mathijs Robbens in Amsterdam (mathijsrobbensbaincom)

Visar Sala in Moscow (visarsalabaincom)

Walter Sinn in Frankfurt (waltersinnbaincom)Joatildeo Soares in London (joaosoaresbaincom)

Acknowledgments

The authors would like to thank the following Bain colleagues for their valuable support in producing this report

Sonal Chawla Christian Duus Franccedilois Fastrez Farsan Ghassim and Shikha Mahato

See these related Bain perspectives at wwwbaincom

bull Managing risk and capital

bull How Europersquos banks can return to health

bull The digital challenge to retail banks

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 3132

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 3232

For more information visit wwwbaincom

Share983140 983105m983138io983150 Tru Rs983157983148ts

Bain amp Company is the management consulting firm that the worldrsquos business leaders come to whenthey want results

Bain advises clients on strategy operations technology organization private equity and mergers and acquisitions We develop

practical customized insights that clients act on and transfer skills that make change stick Founded in 1973 Bain has

48 offices in 31 countries and our deep expertise and client roster cross every industry and economic sector Our clients

have outperformed the stock market 4 to 1

What sets us apart

We believe a consulting firm should be more than an adviser So we put ourselves in our clientsrsquo shoes selling outcomes not

projects We align our incentives with our clientsrsquo by linking our fees to their results and collaborate to unlock the full potential

of their business Our Results Deliveryreg process builds our clientsrsquo capabilities and our True North values mean we do theright thing for our clients people and communitiesmdashalways

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 232

Copyright copy 2013 Bain amp Company Inc All rights reserved

Walter Sinn is a Bain amp Company partner based in the firmrsquos Frankfurt office

Rocco DrsquoAcunto is a partner based in Bainrsquos Milan office Andrea Oldrini is a

manager based in Milan They are all members of Bainrsquos European Financial

Services practice

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 332

European banking | Bain amp Company Inc

Page 1

Contents

European banking Striking the right balance between risk and return 2

1 Five years of RoRWA in Europe A bumpy landscape 7

2 Country and cluster league tables 17

3 Strategic perspectives and implications for management 23

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 432

European banking | Bain amp Company Inc

Page 2

European banking Striking the right balance between risk and return

Now that risk figures so prominently in European banking itrsquos time to raise the profile of a metric that has playeda minor role to date

This benchmarkmdashthe rate of return on risk-weighted assets or RoRWAmdashreliably integrates a balance-sheet-

management perspective with the revenue and cost side of the business Based on a comprehensive analysis of

121 banks across Europe by Bain amp Company RoRWA clearly emerges as the single most practical measure to

help senior bank executives manage their companiesrsquo performance and make savvy risk-reward decisions

Our analysis shows how and where the quality of management plays a major role in determining performance

Thatrsquos especially true in the core European countries where banks canrsquot rely on economic growth to lift their fortunes

Why does RoRWA deserve more respect now Five years since the global financial crisis bankers across Europe

still find themselves waging battle on many fronts Low interest rates a loss of customersrsquo trust stiff new targetcapital requirements and regulatory mandates have compounded the difficulty of operating in weak eurozone

economies On the cost side moreover banks are reconfiguring their distribution networks and streamlining

operations Yet even as revenue growth flattens and new digital technologies push up capital investments banks

are not making much headway on reining in costs

Indeed the banking industry is going through a major restructuring and only the fittest will survive this Darwinian

process The traditional tools that bankers have used to chart their competitive courses provide an inadequate map

for navigating treacherous new terrain With capital adequacy asset quality and broad macroeconomic trends

playing more prominent roles in shaping a bankrsquos financial performance it is the balance sheet not the profit-

and-loss statement which better captures the bankrsquos overall health and points to the areas that most need improvement

Todayrsquos environment of disruptive change calls for a holistic yet simple view of the returns that banks generate

on every unit of capital they commit to their businesses on a risk-adjusted basis

RoRWA fits the bill Other measures may be more precise in understanding risk theoretically but theyrsquore

impractical to use in managing the enterprise RoRWArsquos strength lies in using a well-understood measuremdash

risk-weighted assetsmdashas a denominator making it a good proxy for risk

For business leaders RoRWA and the analysis of key components can provide practical guidance to optimize

bank performance across four dimensions

bull First RoRWA tracks how well a bank manages its balance sheet and appetite for risk Managers can see

whether they are properly pricing offerings to reflect their risk and cost and how well they are allocating

capital to business areas and products that generate higher returns

bull Second the benchmark guides decisions on how a bank factors in risk to its cross-selling opportunities that

bring in fees commissions and other revenues

bull Third on the cost side a RoRWA approach reveals the cost efficiency per unit of risk for the volume of

business a bank generates

bull Fourth RoRWA shines a light on the cost of risk by disclosing how well a bank is able to minimize its loan-loss

provisions on a risk-adjusted basis

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 532

European banking | Bain amp Company Inc

Page 3

Beyond its value as a guide for bringing risk and capital to the forefront in managing a bankrsquos internal performance

RoRWA also can serve as a powerful tool for external communications Executives regulators and investors can

see in a single number (supported by a few key components) how a bank stacks up against its direct competitorsacross different regions

Based on the RoRWA metric Bain undertook a comprehensive analysis of conditions influencing risk-weighted

returns across Europe Our analysis spans 12 core EU countries and the four fast-growing markets of the

Commonwealth of Independent States (CIS) Poland South Africa and Turkey from the onset of the global

economic crisis in 2008 through the end of 2012 We conducted an in-depth examination of 121 banks ranging

from the largest globe-spanning institutions headquartered in Europe and other large banks that operate sub-

sidiaries beyond their home countries to smaller local or regional banks Together the institutions we evaluated

cover at least 70 of their respective markets

The charts on the following pages highlight three major findings

Economic growth counts but management effectiveness plays a critical role Overall RoRWA correlated strongly

with GDP growth trends in the markets we examined Our analysis revealed a dramatic gap between the general

underperformance of banks in the core European countriesmdashwhose economies have largely stagnated or re-

mained mired in recessionmdashand the stronger risk-weighted returns posted by banks based in markets that experi-

enced more rapidly expanding GDP

Yet analysis of bank-level data also showed a wide variance in the performance of institutions competing within

individual markets For example in the slow-growth mostly core European markets where GDP ranged from

RoRWA reflects performance across four key dimensions

Source Bain analysis

= Net interest incomeRWA + + ndashndashFinancial margin

RWA

Fees andcommissions

andother revenues

RWA

Operatingexpenditure

RWA

Loan-lossprovisions

RWA

Measures abankrsquos abilityto cross-sellreflecting theindividual clientrsquos

level of risk

Cross-selling

Measures thecost efficiencyof productionindependent of any pricing and

income effects

Cost structure

Measures thelosses writtenoff against theamount ofrisk taken

Cost of risk

Combines two skills

bull Pricing based on risk and cost

bull Better allocation of capital to business areas and products

with higher returns

Balance-sheet management

Pretax operating results

Total RWA

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 632

European banking | Bain amp Company Inc

Page 4

negative 10 to 5 over the five-year period RoRWA by bank varied widely in every year Clearly for these

markets the quality of an individual bankrsquos management plays a major role in determining performance

In markets where GDP growth exceeded 5 by contrast we found considerably less variation in bank-level

RoRWA performance As the rising tide lifted all banks managementrsquos role in shaping returns appears to have

been more circumscribed

Most banks fail to earn their cost of capital Bain determined that the RoRWA required for banks to cover their

cost of capital fell within a range of 16 to 21 depending on a bankrsquos size and the country in which it is based

The RoRWA of most banks has failed to clear that cost-of-capital hurdle on average in any year since 2008

falling well short in every year except 2010 Once again however we found a wide variation between the bank

performance in the core European countries where RoRWA was consistently below the cost of capital and that

in the high-growth countries where RoRWA easily cleared the capital-cost bar

Looking at the banksrsquo underlying strengths and weaknesses by market we identified several major pain points

that pinched banksrsquo RoRWAs in the core European countries

The need to shed debt and rely on higher-cost equity to strengthen their balance sheets reduced these banksrsquo total

risk-weighted assets by nearly 8 between 2008 and 2012 Meanwhile their cost of risk increased sharply as

stagnant or shrinking economies forced them to boost their loan-loss provisions in the face of steeper write-offs

of bad credit Interest margins that remained at low levels shrinking fee incomes and higher operating costs also

added downward pressure to banksrsquo RoRWAs

Size matters Within core Europe the 10 biggest pan-European banks (by total assets and market capitalization)

fared best overall Helped by large increases in net interest income and strong improvements in financial margins

their RoRWAs came closest to earning their cost of capital

Other large European banks with subsidiaries outside their home countries reduced their operating costs partially

offsetting declines in risk-weighted fee income and higher loan-loss provisions But the RoRWAs for these

banks still failed to clear their cost-of-capital hurdle

Local banks in core Europe struggled weighed down by nonperforming loans and flat revenues Their RoRWAs

were negative in both 2008 and 2012 and did not come close to covering their cost of capital

Turning to country differences the four high-growth countries on the fringe of Europe the Middle East and Africa

have the wind at their backs Turkey ranked first in RoRWA for 2012 and it has jockeyed for top billing with

Poland and South Africa over the past five years

Countries in core Europersquos northern tier occupied the middle ranks of the national league tables with the Nordic

and Austrian banks showing the most consistent performance since 2008 Dutch Belgian and German banks

have been on an upswing since the financial crisis hit UK and French banks have been treading water although

Standard Chartered Bank and HSBC in the UK and BNP Paribas in France all ranked among the top 15 banks

in core European countries

Not surprisingly banks in Italy Portugal Spain and Irelandmdashall feeling the sting of the sovereign debt crisis and

deep economic recessionsmdashhave turned in the weakest RoRWAs

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 732

European banking | Bain amp Company Inc

Page 5

Illuminating the road ahead

While most European banks are moving in the right direction to meet Basel III requirements they could benefit

from using RoRWA to better anticipate and navigate the road ruts that lie ahead

Devising sustainable business models and bringing profitability back to attractive levelsmdashmeaning above the

cost of capitalmdashwill not be easy In the current market environment we expect continued pressure on interest

as well as on fee income For most banks managing the cost of risk will also be a challenge as stagnant economies

tend to drive up this cost

Getting a better grip on operating cost therefore will lead the agenda for most banks Structural costs can be

addressed using several means adopting new digital technologies and modernizing IT platforms optimizing

processes from end to end through such approaches as outsourcing and offshoring and expanding global pro-

curement initiatives

Local banks in core European countries face perhaps the stiffest challenges as restructuring will continue in the

face of stagnant economies and a higher cost of risk We expect to see further consolidation in this group For

the surviving institutions higher performance will hinge on better management of the deleveraging process

containment of the cost of raising new capital and more accurate factoring of risk into their price structures

High-growth countries still offer the most promising opportunities for the 10 biggest and other large pan-Euro-

pean players that aim to diversify their portfolios The best performers will be those banks that keep tight control

of the reins as they ride these booming economies

Regardless of a bankrsquos home country asset size or loan portfolio RoRWA analysis illuminates the ruts and holes

on the road ahead With just a few metrics senior managers can understand how their bank compares with its

peers and which factors to work on in order to create valuemdasha highly pragmatic means of improving the bankrsquos

risk-return profile

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 832

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 932

bull European banksrsquo return on risk recovered from the2008 financial crisis peaking in 2010 with an aver-age 13 RoRWA Since then however RoRWA

has declined to 05 on average This translatesto a level of profitability below the cost of capitalwhich means banks are destroying value

bull Looking beneath the average European banksrsquoRoRWAs correlated closely with economic growthover the past five years Banks in countries that sawstrong GDP growth like Turkey posted dramaticallyhigher performance and growth in both assetsand risk-weighted assets (RWA) than those in thecore European countries

bull Banks in high-growth countries also consistently

exceeded their cost of capital whereas banks incore Europe have not covered their cost of capitalonly coming close to that bar in 2010 Core Europeexperienced a major amount of deleveragingdespite extraordinary initiatives such as theEuropean Central Bankrsquos long-term refinancingoperation (LTRO)

bull The quality of management plays a major role inindividual bank performance particularly in theslow-growth countries There was a wide rangeof RoRWAs among banks in those markets for each

of the five yearsbull In 2012 the biggest factors determining significant

value destruction were cost of risk as loan-lossprovisions rose and increased operating costwhich trended up as a percent of risk-weightedassets More active management of the balance sheethelped raise revenues but fees and commissionsprogressively declined

bull The larger the bank the better its performance onaverage The 10 biggest banks used their improve-

ments in financial margins and lower risk costs tocome close to earning their cost of capital

bull Other large regional banks managed to keep oper-ating costs lower than the 10 biggest but still fellwell short of their capital hurdle Smaller local banksfared the worst posting a negative RoRWA in 2012They have been forced to undertake a major de-leveraging of their balance sheets

1Five years of

RoRWA in Europe

A bumpy

landscape

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 1032

European banking | Bain amp Company Inc

Page 8

Although RoRWA correlates with economic growth there is still substantial variation among banks

Note Each observation is composed of a bankrsquos RoRWA in a given year and the respective countryrsquos year-over-year GDP growth rate in that yearSources Banksrsquo financial statements 2008ndash2012 n=605 Bureau van Dijk Bain analysis

RoRWA per bank and year 2008ndash2012

-5

-3

0

3

5

-10 0 10 20 30

95 ofobservationsfall withinthis band

Recessionno growthManagement has a major role

in determining RoRWA

Mediumhigh growthManagement has amore limited role in

achieving high RoRWA

Very high growthManagementrsquos most important role

is to optimize strategic asset allocationfor revenue generation

GDP growth by country and year 2008ndash2012

Bank profitability has eroded since the post-crisis peak of 2010

Return on equity (ROE) = Pretax profitaverage shareholdersrsquo equitySources Banksrsquo financial statements 2008ndash2012 n=121 Bureau van Dijk Bain analysis

European-wide RoRWA

0

1

2

200800

2009

07

2010 2011

09

2012

05

RWA (euroB)

33576

08

11690

44

30229

64

11555

-32

31770

104

11726

52

33528

75

11986

53

33028

49

11207

29

Total assets (euroB)

Annual GDP growth ()

ROE ()

13

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 1132

European banking | Bain amp Company Inc

Page 9

Banks in core Europe have not covered their cost of capital over the past five years

The range represents the level of RoRWA required to cover the banksrsquo cost of capital and varies by bank size and country analysis of 88 banks based in AustriaBelgium France Germany Ireland Italy the Netherlands the Nordics Portugal Spain Switzerland and the UKSources Banksrsquo financial statements 2008ndash2012 Bain analysis

RoRWA weighted average

RWA (euroB)

32373

-15

10899

29129

51

10846

30366

88

10785

31957

53

10869

31219

22

10047

Total assets (euroB)

ROE ()

2008

-01

2009

06

2010 2011

06

2012

01

Range ofRoRWArequiredto coverthe costof capital

11

-1

0

1

2

3

4

1816

while banks in high-growth countries consistently exceeded their cost of capital

The range represents the level of RoRWA required to cover the banksrsquo cost of capital and varies by bank size and country analysis of 33 banks based in theCommonwealth of Independent States (CIS) Poland South Africa and TurkeySources Banksrsquo financial statements 2008ndash2012 Bain analysis

RoRWA weighted average

RWA (euroB)

1203

226

791

1100

206

708

Total assets (euroB)

ROE ()

Range ofRoRWArequiredto coverthe costof capital

0

1

2

3

4

2008

24

2009

22

1404

250

941

2010

32

1571

267

1117

2011

31

1810

247

1160

2012

33

2119

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 1232

European banking | Bain amp Company Inc

Page 10

Higher operating expenditure and cost of risk caused banksrsquo value destruction in 2012

Long-term refinancing operations (LTRO) 2011 ~euro500 billion LTRO 2012 ~euro750 billion (including repayment) corresponding to 2011 total assets of ~euro330 trillionand 2012 total assets of ~euro322 trillionSources Banksrsquo financial statements 2008ndash2012 n=121 Bain analysis

20122010 2011

RoRWA ()

Total assets (euroB)

Tier 1 capital (euroB)

RWAtotal assets ()

Net interest incomeRWA ()

Financial marginRWA ()

Fees and commissions +

other revenuesRWA ()

Operating expenditureRWA ()

Loan-loss provisionsRWA ()

05

33028

1510

34

36

09

17

43

15

13

31770

1363

37

35

10

17

37

12

09

33528

1426

36

35

05

20

40

12

2009

07

30229

1261

38

34

09

17

35

18

00

33576

1079

35

31

-07

22

36

11

2008Main components in

European-wide RoRWA Major trends

Partial deleveraging of assets

Strengthening of capital

Fairly constant risk profile despite

deleveraging of assets

Overall margin from balance-sheet

management increasing

Continuous pressure on fees

and commissions

Inability to reduce costs in

proportion to deleveraging

Rising cost of credit

7222019 Bain amp Co- European Banking Report

httpslidepdfcomreaderfullbain-co-european-banking-report 1332

European banking | Bain amp Company Inc

Page 11

In core Europe banks increased capital ratios and revenues but did not optimize costs

Notes Components in bold are direct components of the RoRWA calculation changes in red are negative trendsSources Banksrsquo financial statements 2008ndash2012 n=88 Bain analysis

2012 Change2008minus20122010 2011

Total RWA (euroB)

Total assets (euroB)

RWAtotal assets ()

Tier 1 ratio ()

Total Tier 1 (euroB)

Net interest incomeRWA ()

Financial marginRWA ()

Net interest incometotal assets ()

Financial margintotal assets ()

Net interest income + financial marginRWA ()

Fees + other revenuesRWA ()

OpexRWA ()

Costincome ()

Loan-loss provisionsRWA ()

Nonperforming loan ratio ()

Coverage ratio ()

10047

31219

32

133

1336

34

09

11

03

43

16

43

70

15

55