Embed Size (px)

Citation preview

Bailouts Seminar, Winter, 2009

The Consumer Side of the Mortgage Industry

Darius Horton

Anush Yegyazarian

Eunjoe Ahn

Cleve Doty

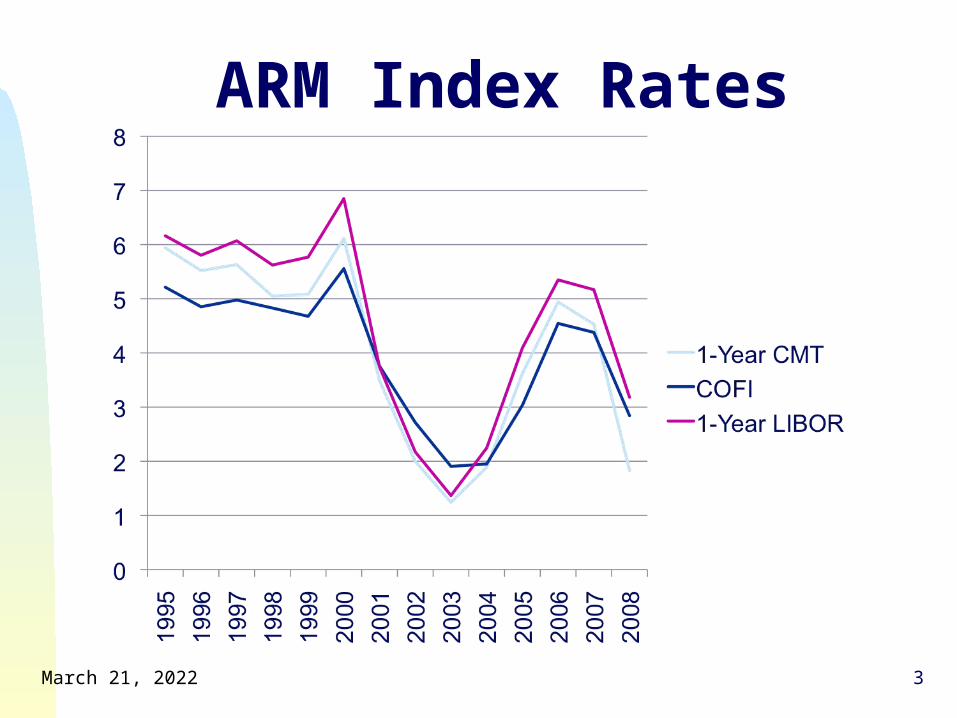

Adjustable Rate Mortgages (ARMs)

Start with a teaser rate, typically < 2%. Once the initial interest rate period expires, reset to an index +

fixed margin (for example, 2-3%) and adjust periodically, usually annually. Common indexes include:

The rates on 1-year constant-maturity Treasury (CMT) securities: estimated 1-year yields of recently auctioned Treasury bills and notes.

The Cost of Funds Index (COFI): weighted average of interest rates paid out on deposits, loans, etc. by financial institutions in the 11th District of the Federal Home Loan Bank (CA, NV, AZ).

The London Interbank Offered Rate (LIBOR): interest rate at which banks can borrow funds from other banks in the London interbank market.

Fully indexed rates are subject to both periodic and life-of-the-loan caps.

2April 18, 2023

ARM Index Rates

3April 18, 2023

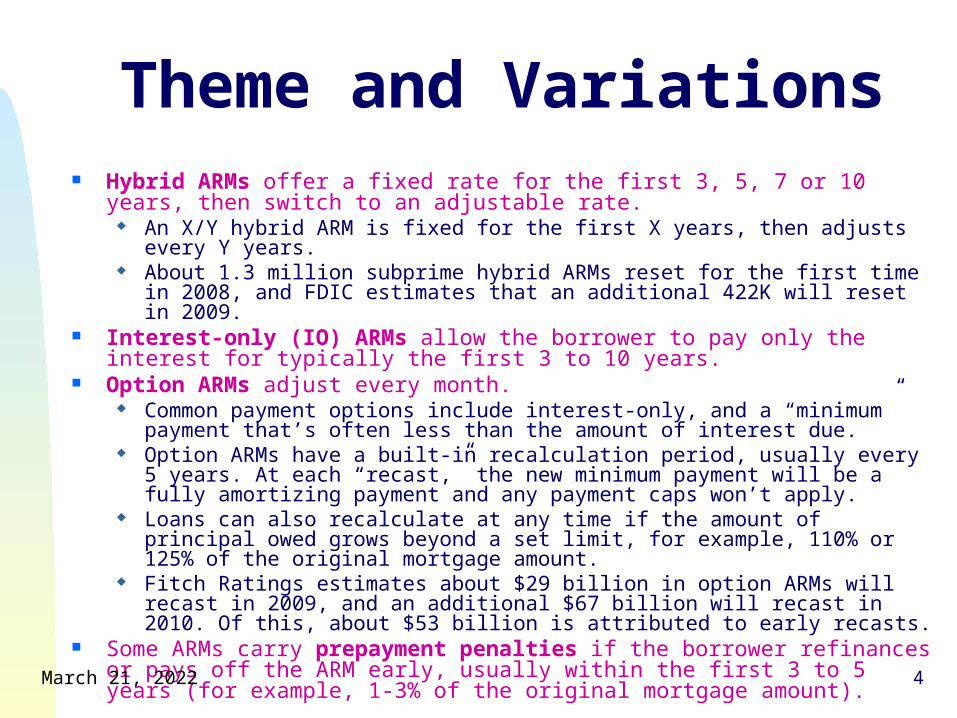

Theme and Variations Hybrid ARMs offer a fixed rate for the first 3, 5, 7 or 10 years, then switch to

an adjustable rate. An X/Y hybrid ARM is fixed for the first X years, then adjusts every Y years. About 1.3 million subprime hybrid ARMs reset for the first time in 2008, and

FDIC estimates that an additional 422K will reset in 2009. Interest-only (IO) ARMs allow the borrower to pay only the interest for

typically the first 3 to 10 years. Option ARMs adjust every month.

Common payment options include interest-only, and a “minimum” payment that’s often less than the amount of interest due.

Option ARMs have a built-in recalculation period, usually every 5 years. At each “recast,” the new minimum payment will be a fully amortizing payment and any payment caps won’t apply.

Loans can also recalculate at any time if the amount of principal owed grows beyond a set limit, for example, 110% or 125% of the original mortgage amount.

Fitch Ratings estimates about $29 billion in option ARMs will recast in 2009, and an additional $67 billion will recast in 2010. Of this, about $53 billion is attributed to early recasts.

Some ARMs carry prepayment penalties if the borrower refinances or pays off the ARM early, usually within the first 3 to 5 years (for example, 1-3% of the original mortgage amount).

4April 18, 2023

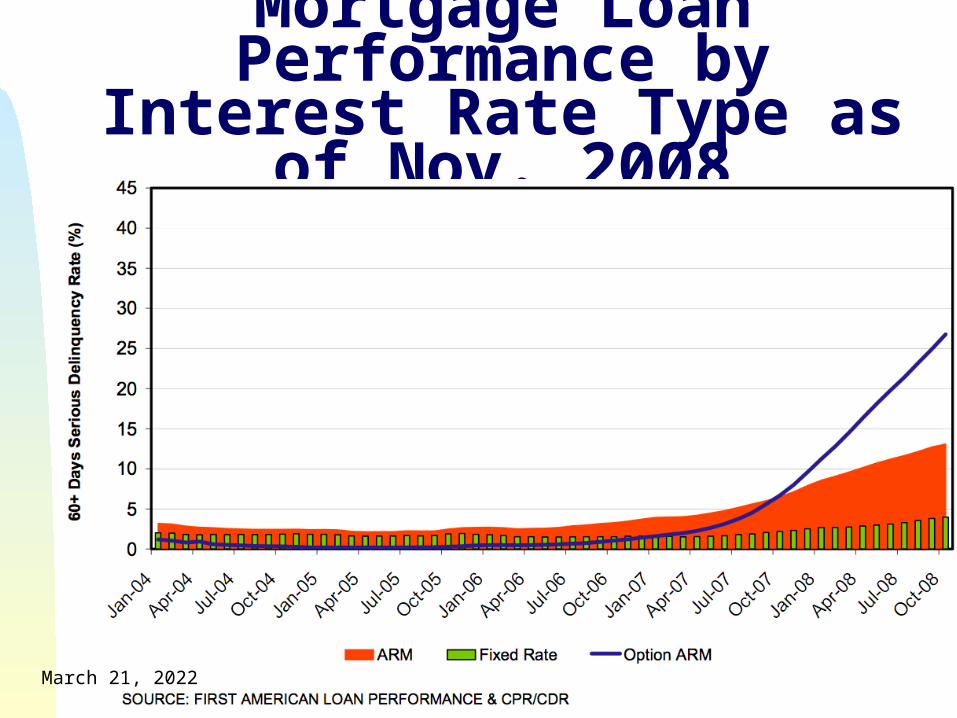

Mortgage Loan Performance by Interest

Rate Type as of Nov. 2008

5April 18, 2023

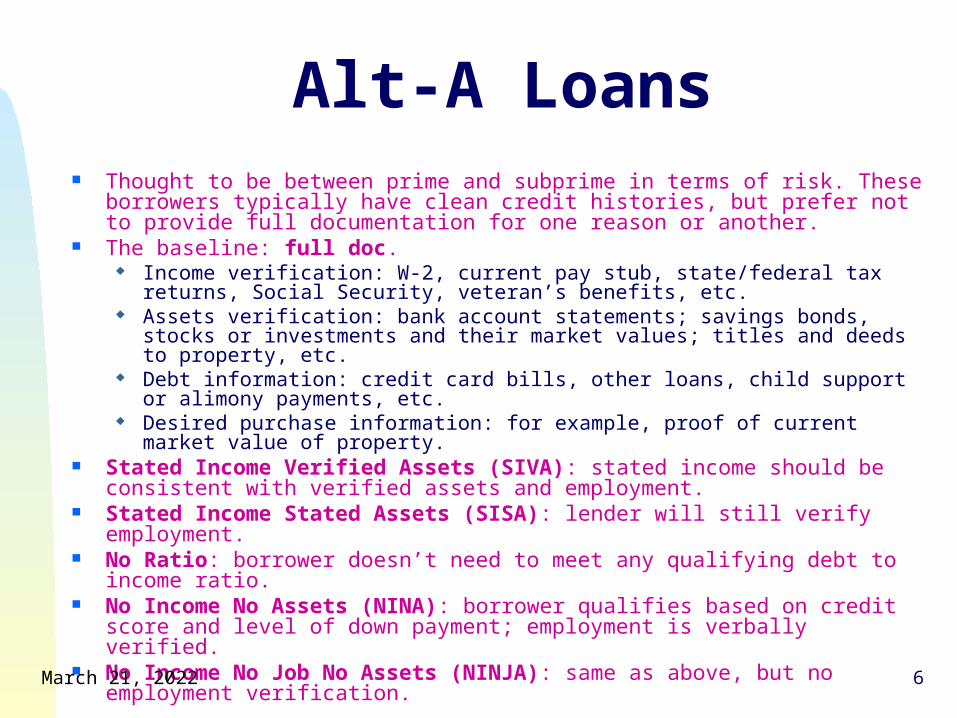

Alt-A Loans Thought to be between prime and subprime in terms of risk. These borrowers

typically have clean credit histories, but prefer not to provide full documentation for one reason or another.

The baseline: full doc. Income verification: W-2, current pay stub, state/federal tax returns, Social

Security, veteran’s benefits, etc. Assets verification: bank account statements; savings bonds, stocks or

investments and their market values; titles and deeds to property, etc. Debt information: credit card bills, other loans, child support or alimony

payments, etc. Desired purchase information: for example, proof of current market value of

property. Stated Income Verified Assets (SIVA): stated income should be consistent

with verified assets and employment. Stated Income Stated Assets (SISA): lender will still verify employment. No Ratio: borrower doesn’t need to meet any qualifying debt to income ratio. No Income No Assets (NINA): borrower qualifies based on credit score and

level of down payment; employment is verbally verified. No Income No Job No Assets (NINJA): same as above, but no employment

verification. 6April 18, 2023

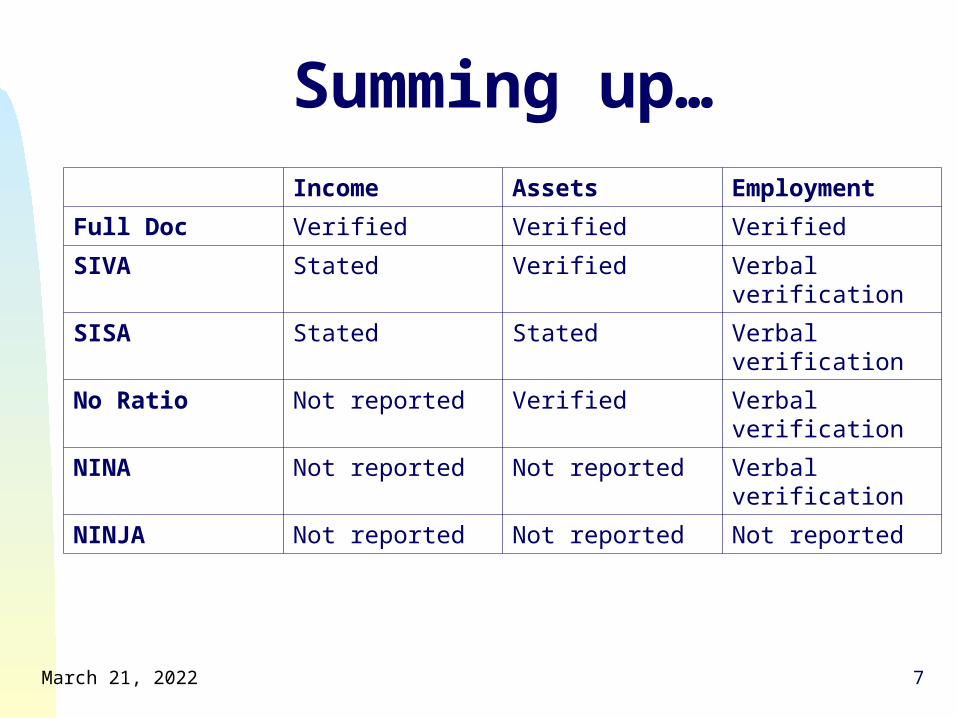

Summing up…Income Assets Employment

Full Doc Verified Verified Verified

SIVA Stated Verified Verbal verification

SISA Stated Stated Verbal verification

No Ratio Not reported Verified Verbal verification

NINA Not reported Not reported Verbal verification

NINJA Not reported Not reported Not reported

7April 18, 2023

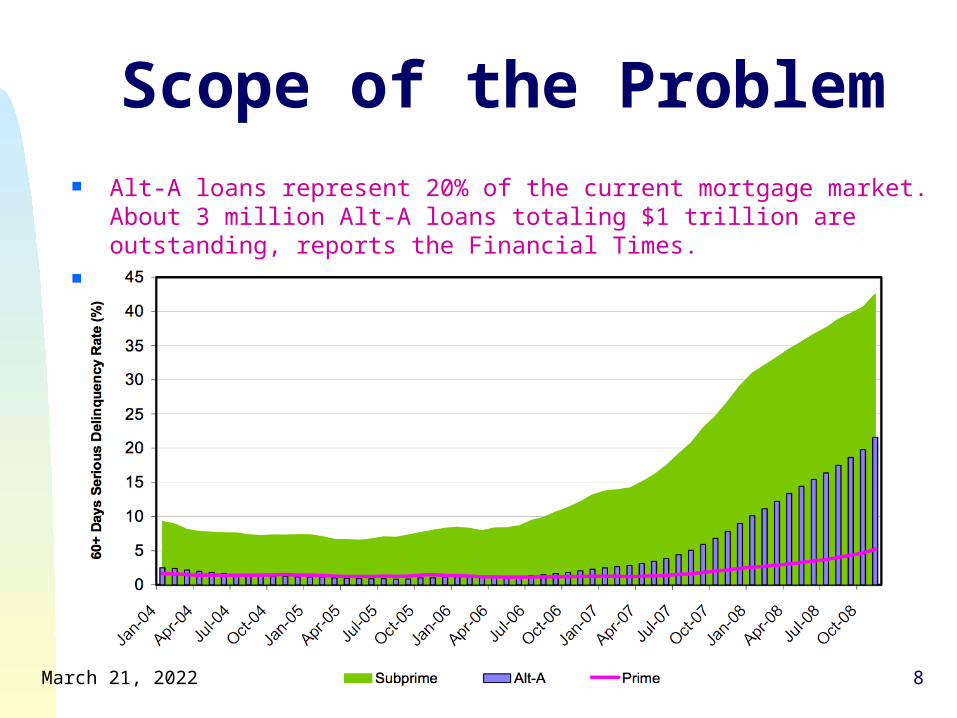

Scope of the Problem Alt-A loans represent 20% of the current mortgage market. About 3 million Alt-

A loans totaling $1 trillion are outstanding, reports the Financial Times. Mortgage Loan Performance by Borrower Type as of Nov. 2008:

8April 18, 2023

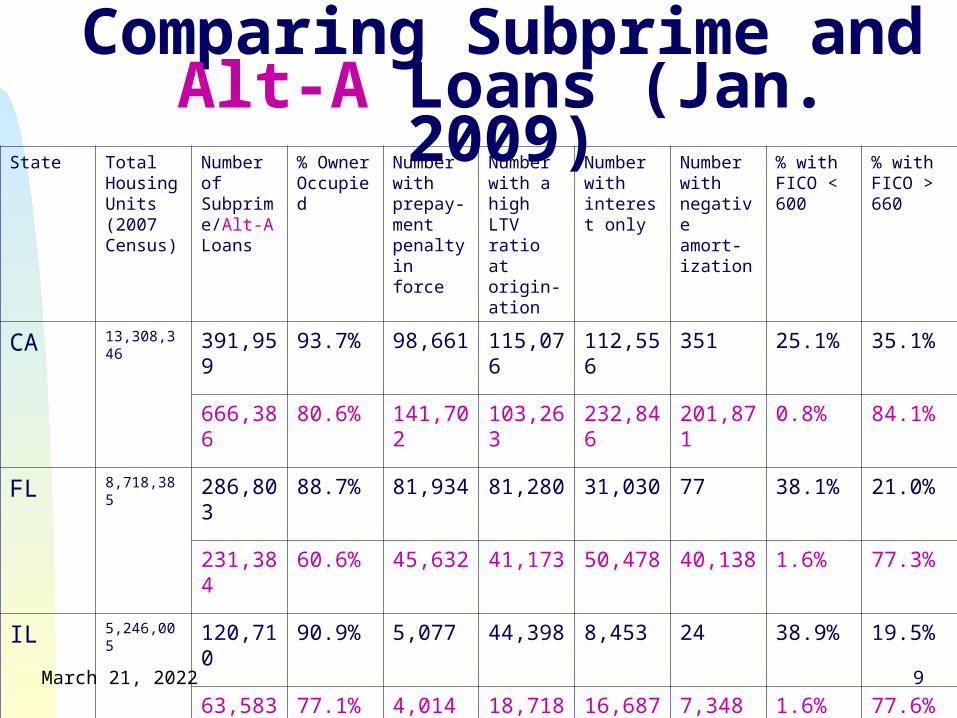

Comparing Subprime and Alt-A Loans (Jan. 2009)

9

State Total Housing Units (2007 Census)

Number of Subprime/Alt-A Loans

% Owner Occupied

Number with prepay-ment penalty in force

Number with a high LTV ratio at origin-ation

Number with interest only

Number with negative amort-ization

% with FICO < 600

% with FICO > 660

CA 13,308,346 391,959 93.7% 98,661 115,076 112,556 351 25.1% 35.1%

666,386 80.6% 141,702 103,263 232,846 201,871 0.8% 84.1%

FL 8,718,385 286,803 88.7% 81,934 81,280 31,030 77 38.1% 21.0%

231,384 60.6% 45,632 41,173 50,478 40,138 1.6% 77.3%

IL 5,246,005 120,710 90.9% 5,077 44,398 8,453 24 38.9% 19.5%

63,583 77.1% 4,014 18,718 16,687 7,348 1.6% 77.6%April 18, 2023

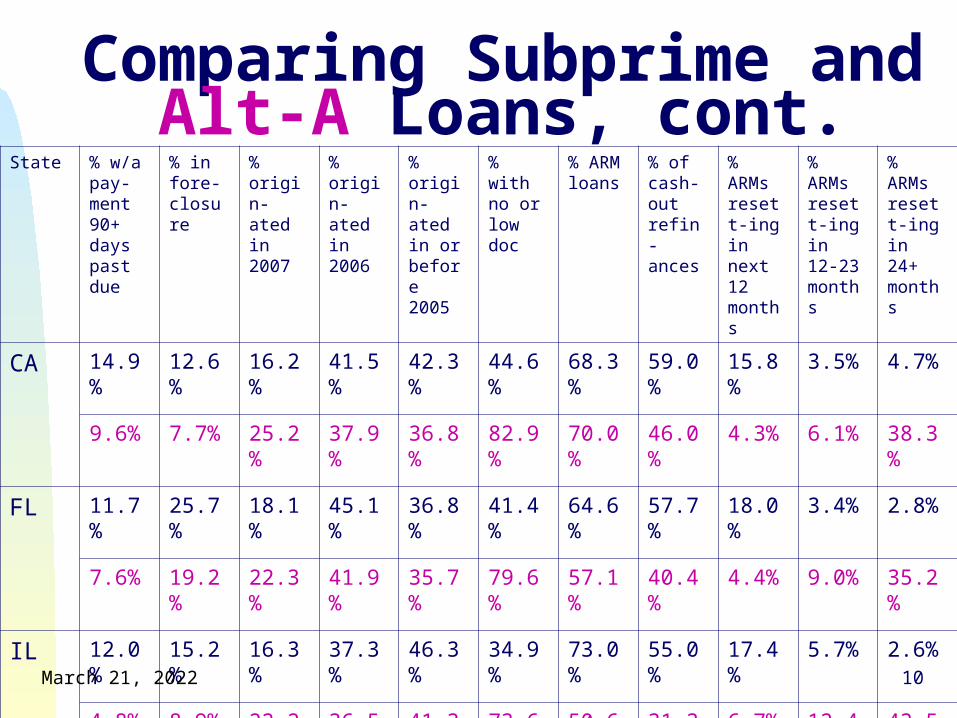

Comparing Subprime and Alt-A Loans, cont.

10

State % w/a pay-ment 90+ days past due

% in fore-closure

% origin-ated in 2007

% origin-ated in 2006

% origin-ated in or before 2005

% with no or low doc

% ARM loans

% of cash-out refin-ances

% ARMs resett-ing in next 12 months

% ARMs resett-ing in 12-23 months

% ARMs resett-ing in 24+ months

CA 14.9% 12.6% 16.2% 41.5% 42.3% 44.6% 68.3% 59.0% 15.8% 3.5% 4.7%

9.6% 7.7% 25.2% 37.9% 36.8% 82.9% 70.0% 46.0% 4.3% 6.1% 38.3%

FL 11.7% 25.7% 18.1% 45.1% 36.8% 41.4% 64.6% 57.7% 18.0% 3.4% 2.8%

7.6% 19.2% 22.3% 41.9% 35.7% 79.6% 57.1% 40.4% 4.4% 9.0% 35.2%

IL 12.0% 15.2% 16.3% 37.3% 46.3% 34.9% 73.0% 55.0% 17.4% 5.7% 2.6%

4.8% 8.9% 22.2% 36.5% 41.3% 73.6% 50.6% 31.3% 6.7% 12.4% 43.5%April 18, 2023

JUMBO Loans Mortgages exceeding the conforming loan limits set by the

Office of Federal Housing Enterprise Oversight, and thus not eligible to be purchased, guaranteed or securitized by Fannie or Freddie.

Conforming loans top out at $417K in most parts of the country. The stimulus package raised the limit from $625K to $729,750 in high-cost areas such as parts of CA, NY and HI. The median home price in San Francisco and NYC is $600K.

About 4% of all borrowers have non-conforming loans, estimates First American CoreLogic. That %age rises in states like CA, at 17%, and NY, at 8%.

Since 2007, the interest rate difference between conforming and JUMBO loans has been about 1-2%. Before that, it averaged about 0.2%.

Last month, “about 2.57% of prime borrowers who took out jumbo loans last year were at least 60 days delinquent. They got to that level within 10 months, the fastest rate since at least 1992.” —Bloomberg

11April 18, 2023

April 18, 2023 12

Who regulates? Mortgage lending in the United States is subject to a

diverse patchwork of regulations. Most regulations are found in state law, or the common

law Federal regulatory agencies operate on top of state law :

The Federal Reserve The FDIC The Office of Comptroller of the Currency The Office of Thrift Supervision The Federal Financial Institutions Examination Council

April 18, 2023 13

The Truth in Lending Act Also known as Regulation Z Its purpose is to “promote the informed use of consumer

credit by requiring disclosure about its terms and costs.” Requires disclosures about the loan’s APR, fees, points,

term and pre-payment options. Prohibits refinancing a mortgage within 1 year, unless “the

refinancing is in the borrower’s interests.” Prohibits lending without regard to the consumer’s ability

to repay. There is a presumption that the Act has been violated if

the lender engages in a “pattern or practice” without verifying and documenting the borrower’s income.

April 18, 2023 14

The Homeownership and Equity Protection Act

Passed in 1994, this amends the TILA for certain high-cost loans. It applies to:

Any first lien with an interest rate 8 points (10 points for second liens) higher than a comparable treasury bill.

Or any mortgage with fees higher than $583 or 8% of the loan amount.

It prohibits: Balloon payments for loans with less than 5 year terms. Negative amortization Most pre-payment penalties. Disguising high-cost loans as home equity loans.

It does NOT prohibit steering borrowers into more expensive loans. As high as 61% of sub-prime borrowers would have qualified for

prime loans.

April 18, 2023 15

The Community Reinvestment Act

Passed in 1997, its purpose is to encourage banks to “meet the credit needs of the local communities” while maintaining “safe and sound operations.”

In practice, this amounts to a prohibition on “red lining.” Banks would draw lines on the map around neighborhoods where

they would not lend. The Act requires banks to meet the needs of “low-and-moderate

income neighborhoods.” As well as the needs of women and minorities.

Only applies to deposit-taking institutions. That means the CRA did not apply to many of the largest sub-prime

mortgage originators, such as Countrywide and Ameriquest.

April 18, 2023 16

The Financial Benefits Worksheet

Designed to ensure compliance with the TILA’s prohibition on loans that are not in the borrower’s interests.

Add points for benefits such as: Reducing monthly payment. Reducing interest rate. Cash out exceeds points and fees by more than 2 to 1.

Lose points for harms such as: Points and fees exceed cash out. Re-financing loan within 1 year.

Could not approve loan with a score below 3, but in practice, scores of 1 and 2 were quite common.

Mar. 5, 2009Consumer-side Fraud

17

Appraisals

Governed by Federal and State law: Financial Institution Rescue, Recovery, and

Enforcement Act (FIRREA, 1989) Title XI: Real Estate Appraisal Reform

Amendments• Created Appraisal Subcommittee, which set

national appraiser standards matching those created by USPAP (an ad hoc group made up of appraisal professionals organizations)

• States still have a lot of leeway

Mar. 5, 2009 Consumer-side Fraud 18

Certification and Licensing Required States set the specifics

Training varies from 75 to 165 hours Tests may be state-run or given through

qualified organizations Different categories of appraisers based on

training and experience Appraisers must renew their certification

every two years Guidelines require use of comparable

property nearby to help set values, plus home inspection, written report

Mar. 5, 2009 Consumer-side Fraud 19

Fraud Easy to Do, Hard to Catch Skewed incentives

Lenders and mortgage brokers often required buyers and owners looking to refinance to use one of their appraisers

Appraisers paid per eval, need to keep lenders happy to keep business

In competitive market, consumers and lenders wanted high valuations

Fines for violations, but little oversight Complaint required for investigation

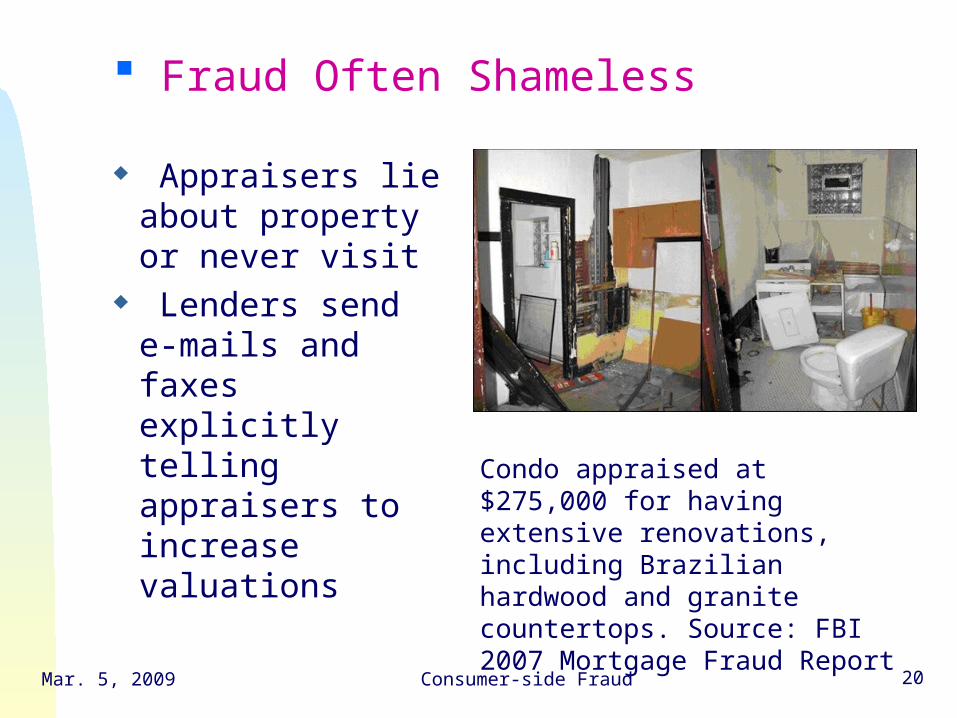

Appraisers lie about property or never visit

Lenders send e-mails and faxes explicitly telling appraisers to increase valuations

Mar. 5, 2009 Consumer-side Fraud 20

Condo appraised at $275,000 for having extensive renovations, including Brazilian hardwood and granite countertops. Source: FBI 2007 Mortgage Fraud Report

Fraud Often Shameless

Mar. 5, 2009 Consumer-side Fraud 21

Recent (Dubious) Reform: Home Valuation Code of Conduct, Effective May 1, 2009 Required for business with Fannie and

Freddie Championed by Andrew Cuomo after NY

investigations into WaMu, others Sought to lessen lender influence over

appraisers Problem: Empowers intermediaries called

Appraisal Management Cos. that have skewed incentives and little oversight

Mar. 5, 2009 Consumer-side Fraud 22

Dubious Reform (continued) Some of the same subprime players are now

AMCs NovaStar Financial, disciplined in 3 states, now

an AMC called StreetLinks National Appraisal Service (BusinessWeek, Feb. 5, 2009)

Some banks run their own AMCs Bank of America, Wells Fargo, for example,

have their own AMCs (BW, Feb. 5, 2009)

The Consumer Side of the Sub-Prime Mortgage

MarketFraudulent Practices

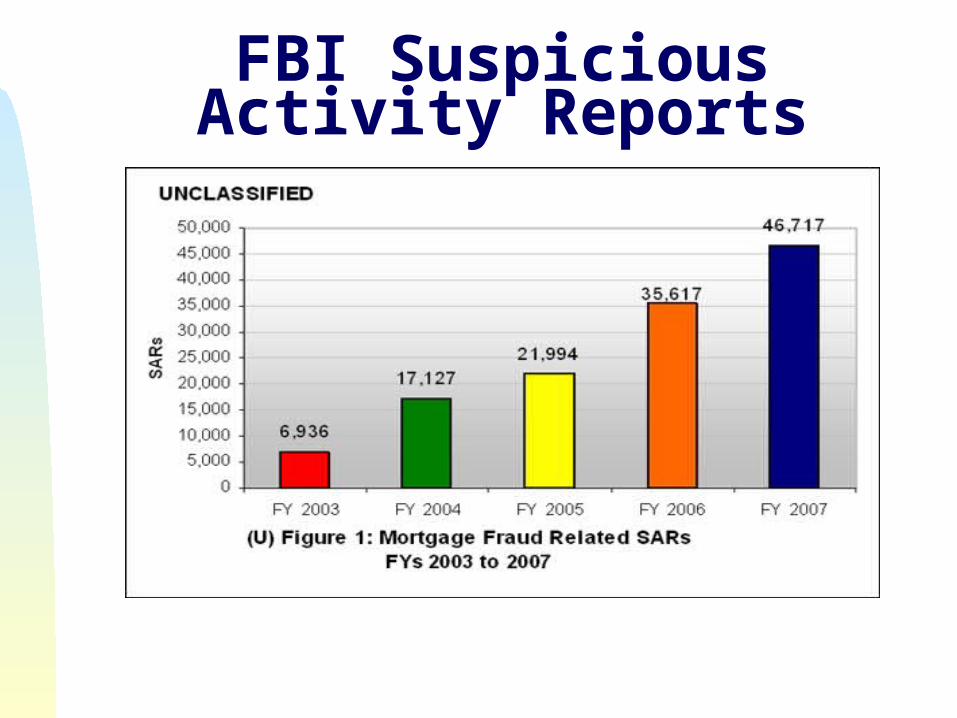

FBI Suspicious Activity Reports

FBI SARs

Up 31% from 2006 to 2007. (2008 numbers unavailable)

Reports from financial institutions only. The FBI suspects that lax lending standards

led to increased fraud. Total annual estimated losses: $4 billion to

$6 billion (estimated by The Prieston Group)

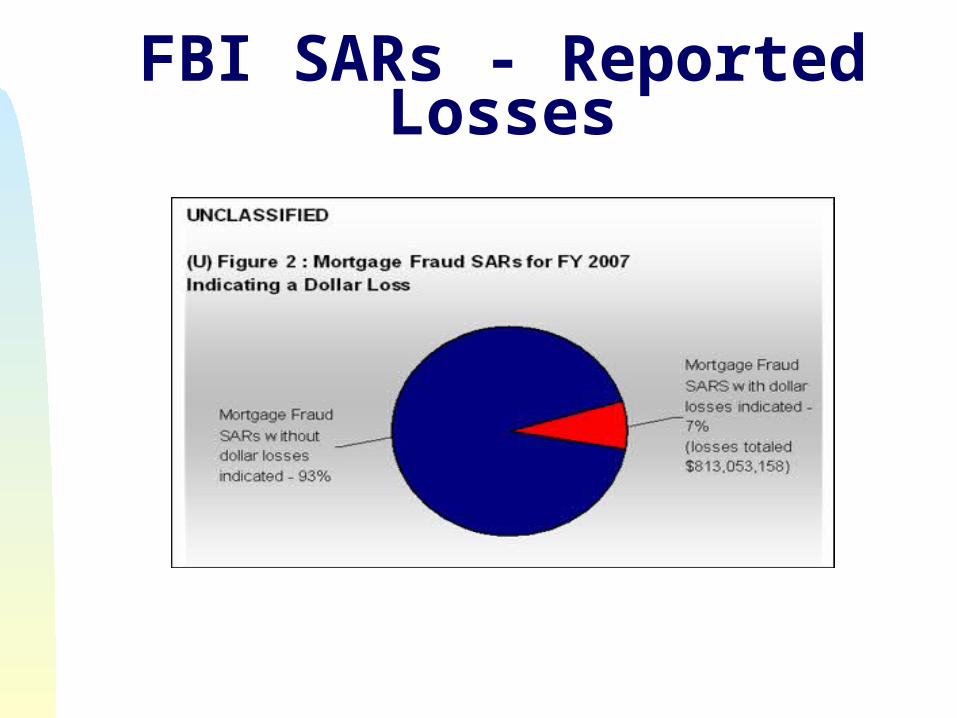

FBI SARs - Reported Losses

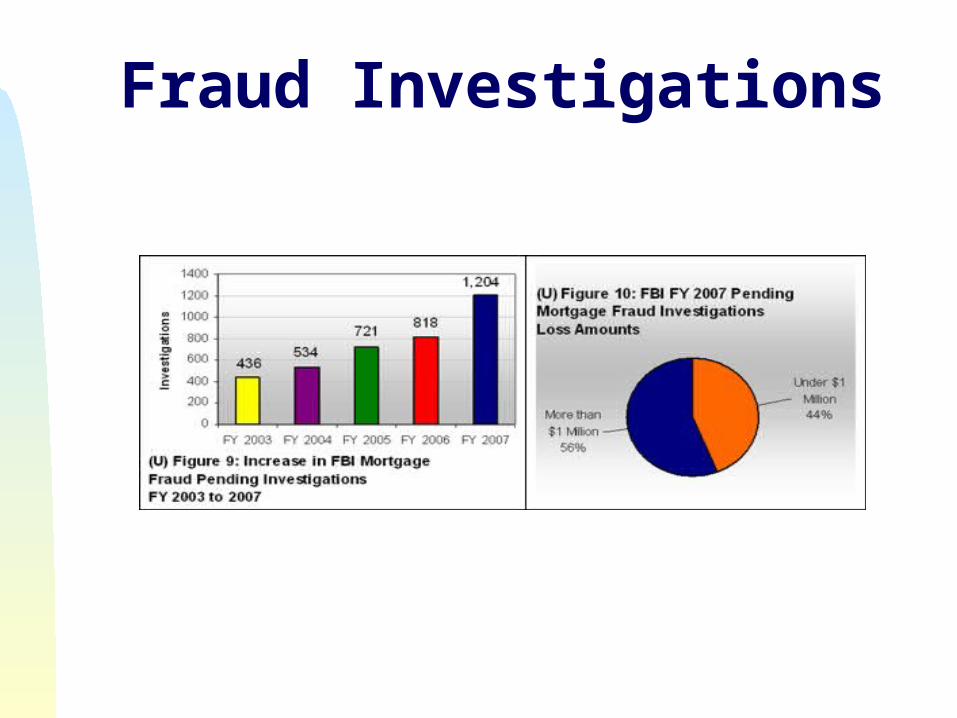

Fraud Investigations

Fraud Investigations

FBI mortgage fraud investigations at the end of FY 2007: a 47% increase from FY 2006 and a 176%

increase from FY 2003. 56% of 2007 investigations involved dollar

losses of more than $1M. L.A. led the nation for mortgage fraud SARs

(more than 2x as much as the next worst city, Miami)

Fraud Schemes

Illegal property flipping Builder-bailout schemes Seller assistance scams Short-sale schemes Foreclosure rescue scams (the new fad) Mortgage fraud ponzi schemes Other lending practices at financial firms

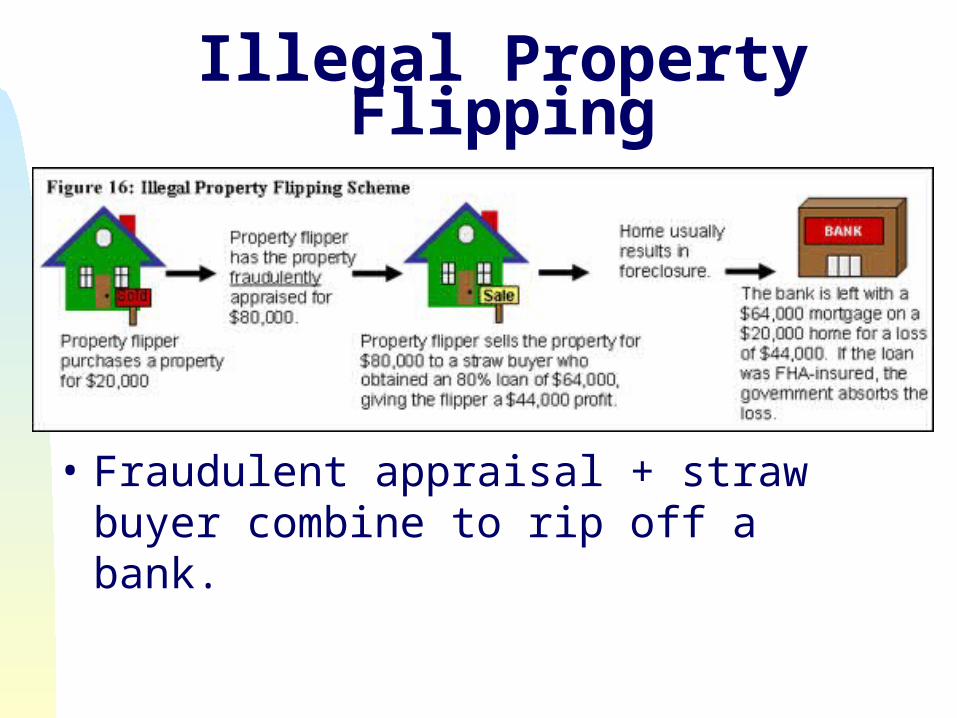

Illegal Property Flipping

• Fraudulent appraisal + straw buyer combine to rip off a bank.

Builder-bailout Schemes Builders fraudulently unload property in a distressed

market. Example: builder has difficulty selling property, so he offers

incentives that are not on the loan paperwork. He inflates the value of a $200,000 home to $240,000. The bank gives a mortgage for $200,000, thinking that the lender paid the builder $40,000, creating home equity.

The builder then “forgives” the home owner’s $40,000 down payment and keeps any profits.

The lender has no equity in the home, so it must pay foreclosure expenses.

Seller Assistance Scams Perpetrators find an anxious seller and offer to find a buyer. Perpetrator finds out how much seller will take. Perpetrator finds appraiser to inflate home’s value, and

negotiates a sale (with mortgage) to a buyer recruited by perpetrator.

Seller receives asking price for home, and perpetrator receives “servicing fee” = difference between seller’s WTA and inflated value.

When the mortgage defaults, the lender is stuck with home that can’t be sold at inflated value.

Fraudulent Short Sale Perpetrator recruits a straw buyer to purchase a property. Straw buyer secures mortgage for 100% of home’s value.

Straw buyer may refinance and obtain $30,000 for repairs. Perpetrator pockets the $30,000. Mortgage goes into default. Straw buyer informs lender of default, and recommends

perpetrator as a potential buyer in a short sale. Perpetrator purchases home before foreclosure in a short sale. Perpetrator sells property at actual value for a profit, or

artificially inflates the value to create an illegal property flip.

Foreclosure Rescue Scams

Perpetrators contact individuals in danger of foreclosure, promising help.

Perpetrators secure deed through promise of help and sometimes a series of forged deeds.

Perpetrators strip home of equity or sell the home, pocketing profit.

Mortgage Fraud Ponzi Schemes

• Claims to have originated $810M in fraudulent MBS.• Involved in $100M ponzi scheme at Loomis Wealth

Solutions.• “Apprehended At Border With $70,000 In Cowboy

Boots, $1M In Swiss Bank Certificates” (see links)

• Meet Christopher Warren, age 27.

• Confessed to large-scale mortgage fraud before fleeing the country.

Ameriquest

Nation’s largest subprime lender. Supported many political campaigns; Deval Patrick

was on its board. Ameriquest customers filed more complaints with

the Federal Trade Commission from 2000 through 2004 than did those of two of its biggest competitors combined, the agency said – 466 compared with 101 for Full Spectrum Lending (Countrywide’s sub-prime unit) and 51 for New Century Financial Corp.

Ameriquest

Ameriquest employees “forged documents, hyped customers’ creditworthiness and “juiced” mortgages with hidden rates and fees.”

Settlement: $325 million nationwide, $21M in Texas.

Ameriquest In court documents and interviews, 32 former employees

across the country say they witnessed or participated in improper practices, including: “deceiving borrowers about the terms of their loans, forging documents, falsifying appraisals and fabricating borrowers’ income to qualify them for loans they couldn't afford.”

“Whatever you had to do to close a loan, that’s what was done,” said Brien Hanley, a former loan agent at the company’s Leawood, Kan., branch. “If you had to state somebody’s income at $8,000 a month and they were a day-care provider, who's to say it wasn’t?”