Embed Size (px)

Citation preview

© 2014 Ipsos. All rights reserved.

Contains Ipsos' Confidential and Proprietary information and may not be disclosed or reproduced without the prior written consent of Ipsos.

2013 FULL YEAR RESULTSBACK TO GROWTH

NOW THE PACE ACCELERATES

27 February 2014

AGENDA

HIGHLIGHTS OF THE YEAR

2013 RESULTS

MARKET OVERVIEW

OUTLOOK

2

1

3

5

IPSOS4

2013 Full Year Results – 27 February 2014

HIGHLIGHTSOF THE YEAR

2013 Full Year Results – 27 February 2014

REVENUE €1,712.4M

OPERATING MARGIN 10.6%

NET PROFIT ATTRIBUTABLE TO THE GROUP €121.0M

HIGHLIGHTS OF THE YEAR

CARBON DISCLOSURE PROJECT AWARD ON SOCIALAND ENVIRONMENTAL TRANSPARENCY

4

NEGATIVE IMPACT OF FOREIGN EXCHANGE -4.4%

2013 RESULTS

2013 Full Year Results – 27 February 2014

OPERATING MARGIN OF 10.6%

In millions of euros 2013 2012 Variation

2013/2012

Revenue 1,712.4 1,789.5 -4.3%

Gross profit 1,097.8 1,147.2 -4.3%

Gross profit/Revenue 64.1% 64.1%

Operating margin 182.1 178.5 +2.1%

Operating margin/Revenue 10.6% 10%

Other operating income and expense (18.2) (36.6) -

Net impact of Remeasurements relating to the Synovate transaction

post allocation period(71.3) - -

Finance costs (23.4) (23.9) -2.2%

Income tax (33.5) (27.3) +22.8%

Net profit (attrib. to the Group) 17.4 74.1 -76.5%

Net income Group share (excluding net impact of Remeasurements

relating to the Synovate transaction post allocation period)88.7 74.1 +19.8%

Adjusted net profit* (attrib. to the Group) 121.0 118.5 +2.1%

6

* Adjusted net profit is calculated before non-cash items linked to IFRS 2 (share-based payments), amortisation of acquisition-related intangible assets

(client relationships), deferred tax liabilities related to goodwill on which amortisation is tax-deductible in certain countries and the impact net of tax of other

non-recurring income and expenses and before the net impact of Remeasurements relating to the Synovate transaction post allocation period

2013 Full Year Results – 27 February 2014

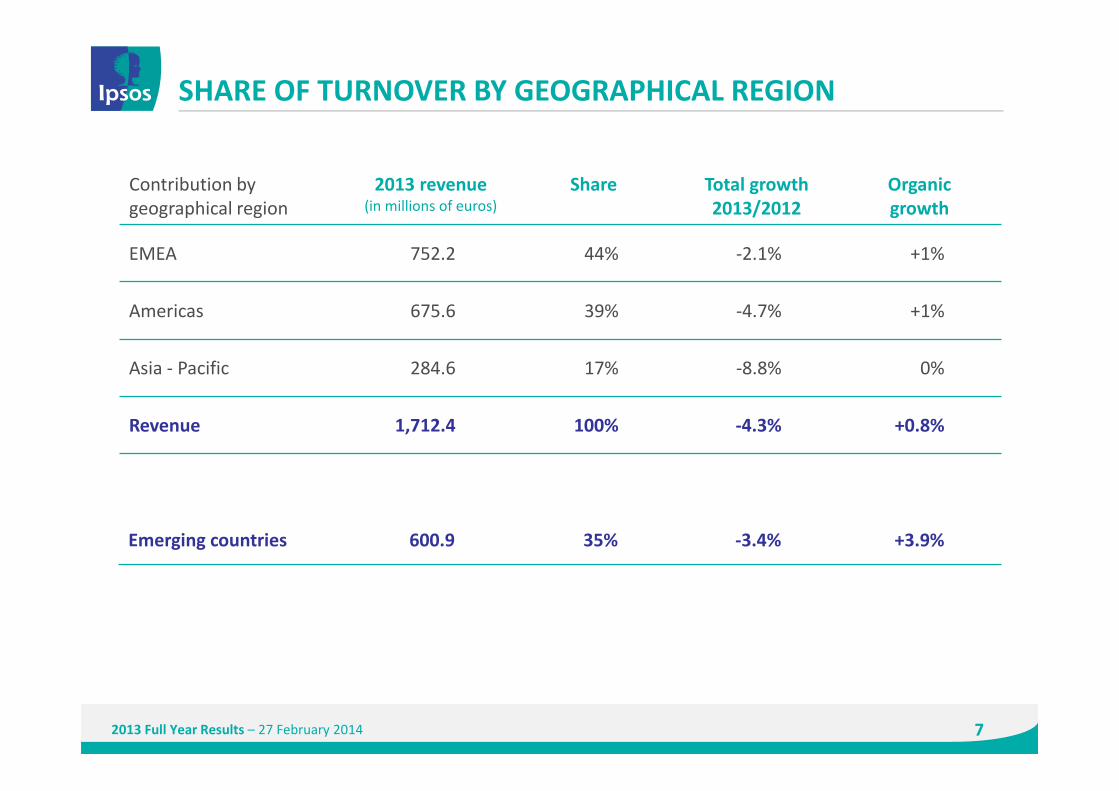

SHARE OF TURNOVER BY GEOGRAPHICAL REGION

Contribution by

geographical region

2013 revenue(in millions of euros)

Share Total growth

2013/2012

Organic

growth

EMEA 752.2 44% -2.1% +1%

Americas 675.6 39% -4.7% +1%

Asia - Pacific 284.6 17% -8.8% 0%

Revenue 1,712.4 100% -4.3% +0.8%

Emerging countries 600.9 35% -3.4% +3.9%

7

2013 Full Year Results – 27 February 2014

SHARE OF TURNOVER BY SPECIALISATION

Contribution by

specialisation

2013 revenue(in millions of euros)

Share Total growth

2013/2012

Organic

growth

Advertising Research 274.5 16% -3.3% -1%

Marketing Research 891.0 52% -6% +1%

Media Research 169.7 10% +0.7% +3%

Opinion & Social

Research152.0 9% -3.7% -1%

Client/Employee

Relationship

Management Research

225.2 13% -2.7% +0.5%

Revenue 1,712.4 100% -4.3% +0.8%

8

2013 Full Year Results – 27 February 2014

48.2 49.0

130.3

133.1178.5

2012H1 2012 H2 2012H1 2013 H2 2013 2013

182.1

14.7%

10.6%

10.0%

13.7%

5.8% 6.1%

MARGINS IMPROVE SEMESTER AFTER SEMESTER

9

2013 Full Year Results – 27 February 2014

COMPONENTS OF CHANGE IN OPERATING MARGIN

10

- 0,20

2012 Variable

remuneration

Investment

in the Client

Organisation and

product offer

2013Benefits of the

combination

(GE and payroll)

10.0%

-0.10

+0.90

10.6%

-0.20

THE OPERATING MARGIN PROGRESSES THANKSTO THE BENEFITS OF THE COMBINATION

TRIPLING OF NET CASH GENERATION

In millions of euros 2013 2012 Variation

Gross Operating Cash flow 196.3 169.7 +16%

Change in WCR (54.1) (66.3)

Tax and interest expense (49.8) (51.9)

Purchases of PP&E and intangible assets (18.0) (28.4)

Free Cash flow 74.4 23.1 +222%

Acquisitions 9.4 (28.4)

Capital increase/(decrease) 0.2 1.6

Share repurchase (3.9) (6.1)

Net change in debt (25.4) 10.5

Dividends (29.9) (29.8)

Cash at end of period 148.7 132.3 +12%

2013 Full Year Results – 27 February 2014 11

2013 Full Year Results – 27 February 2014

BALANCE SHEET STRUCTURE IMPROVED

12

In millions of euros 2013 30 June 2013 2012

Shareholders’ equity 852 804 928

Net debt 545 634 623

Gearing 63.9% 78.8% 67.2%

Net debt/EBITDA x 2.5 x 2.9 x 2.9

Interest cover

(operating margin/interest expense)x 8.2 x 3.8 x 7.5

39

59

127

92

209

146

22

31/12/2013 2014 2015 2016 2017 2018 2020 2022

694

Gross Debt

(€M)

2013 Full Year Results – 27 February 2014

LONG-TERM FINANCIAL RESOURCES

13

31 December 2013: Ipsos has 148.7 million euros of cash and 184 million euros of credit lines enabling itto meet its obligations after the success of its refinancing on better terms than previously:- August 2, 2013: Syndicated loan of 150 million euros to 5 years in fine.- November 7, 2013: Schuldschein of 109 million euros with 3, 5 and 7-year tranches.

SPLIT BY DATE OF MATURITY

PROPOSED DIVIDEND OF 70 CENTIMES (+9%)

2013 Full Year Results – 27 February 2014 14

2013 2012

Dividend per share 0.70 0.64

Earnings per share 0.38 1.64

Adjusted earnings per share 2.67 2.62

Adjusted earnings per share distributed 26.2% 24.4%

TANGIBLE COMMITMENT TO SOCIAL RESPONSIBILITY

15

2013: IPSOS WINS PRESTIGIOUS CARBON DISCLOSURE PROJECT

AWARD AS THE FRENCH COMPANY WITH THE MOST IMPROVED

CDP DISCLOSURE SCORE

� CDP is an international, not-for-profit organisation providing the only global system for companies to measure, disclose, manage and share vital environmental information

Key milestones of Ipsos Corporate Social Responsibility

20132012201120102008/2009

� Launch of TAKING RESPONSIBILITY initiativeIpsos becomes first global market research company to join United Nations Global Compact

� First annual global TAKING RESPONSIBILITY Survey of Corporate Responsibility initiatives undertaken

� First reporting of its environmental information to the Carbon DisclosureProject (CDP)

� Greenhouse Gas (GHG) measurement initiative piloted across 17 countries (c. 70% of our business)

� Ipsos granted ‘Active Status’ by UN Global Compact

� Corporate Responsibility highlighted as a specific disclosure in the Annual Report

� Ipsos’ Global Corporate Responsibility policy launched

� GHG measurement project extended to over 80% of our business

� Ipsos Corporate Responsibility measurement initiatives subject to external audit for the first time

2013 Full Year Results – 27 February 2014

MARKET OVERVIEW

EVEN IF… BASED ON…

� Developing countriesare slowing down

� The differences in performance from one country to another are marked

� A good momentum in Anglo-Saxon countries

� An orderly transitionof China to its new development mode

2014: A POSITIVE ENVIRONMENT, WITH CHALLENGES

2013 Full Year Results – 27 February 2014

� In the short term, the United States, the United Kingdom and Germany are/become key markets again due to their size and their ability to generate innovations, global programs and growth

� In the longer term, large developing countries will remain key drivers of growth, despite their inevitable volatility

THE WORLD ECONOMY IS STILL GROWING

THE SOCIAL AND MARKET RESEARCH INDUSTRY REGAINS STRENGH

17

MARKET RESEARCH ENTERS A NEW PHASE

� The range of new services will increase

� The ability of Anglo-Saxon markets to innovate and grow will be decisive

2009 WAS A PIVOTAL YEAR

2014 WILL BE A PIVOTAL YEAR

2005/2008 2008/2012

� Strong annual growth � Weak annual growth

� Development of panel-based activities

2005 USD 2008 USDAverage annual

change 2005/2008(in current dollars)

2012 USD*Average annual

change 2008/2012(in current dollars)

Size of the Market 23,193 31,857 11.2% 33,331 1.1%

Emerging countries 3,307 5,205 16.3% 6,998 7.7%

Developed countries 19,886 26,652 10.3% 26,333 -0.3%

UK + US + Germany 12,318 16,354 9.9% 16,709 0.5%

Panels 6,494 7,327 4.1% 9,734 7.4%

« Big 4 » (excl. IMS) 7,051 11,429 13.2% 13,017 3.3%

Globalisation: the « Big 4 » move from 30% to 40% of the market share

2013 Full Year Results – 27 February 2014 18

*Restated of scope change made by Esomar

THE WORLD IS CHANGING, THE MARKET IS MOVING

Digital marketing is part of brand building

Let’s celebrate the end of digital marketing.

Let’s focus on creating the great ideas that move people and build

great brands. And let’s leverage the tools, platforms and technology

to make them bigger and engage with people like never before.

“”

Unilever will […] slash its product variants by 30 per cent and focus

predominantly on brands […].

The company is now more inclined to favour fewer global advertising

concepts over multiple local ideas.

Advertising concepts become more global

Paul Polman, Unilever Chief ExecutiveUnilever Investor Day, December 2013, London

Marc Pritchard, P&G’s Global Brand Building Officer

Digital Marketing Exposition & Conference, September 2013, Düsseldorf

2013 Full Year Results – 27 February 2014 19

COMPANIES ARE EVOLVING THEIR BUSINESS MODELS

This necessitates the deployment of global infrastructures and proceduresGLOBAL

To deny differences between countries is to limit proper understandingLOCAL

To be used, information must be understandableSIMPLICITY

The source of many new services, including but not solely Big DataSCIENCE & TECHNOLOGY

Ipsos does not lack these as information on society,people and markets is at the heart of decision-makingCURIOSITY, CONFIDENCE & INTENSITY

ACCURACY The knowledge of statistics and models is the reason for our industry

SPECIALISATIONSThe cornerstone of Ipsos’ differentiation strategy is based on the developmentand co-existence in the same company of specific expertise

SPEED Necessary in terms of what is required from information

MOBILES & CLOUD The tools of transformation for today and for tomorrow

SOCIAL Networks that change the behaviour and feelings of people, and therefore the art of convincing

KEY WORDS

2013 Full Year Results – 27 February 2014 20

IPSOSGrowth levers

NEW SERVICES

SUCCESS WITH BIG CLIENTS

ONE IPSOS

FOCUS ON FLOURISHING MARKETS

TALENTED TEAMS

22

ONE IPSOS

Global Coverageover 4.5 millionof panelists in 46 countries(5 continents, growthin emerging markets)

Common platform for collecting, processingand storing data

Next*WorkbenchWorkflow system establishing a framework of collaboration betweenresearchers and Operations

30/30 initiative

Shorter questionnaires, more actionablepresentations

Copy Testing

Delivery time reduction

= 50%

Cost reduction = 25%

TrackingCentralisationof operating model

Ipsos Training Center

Consistent standards and global training withthe roll-out of the Ipsos Training Centre accross83 countries (+5):- 303 classes available

online (+57) - 7,170 Ipsos

beneficiaries

A global offer of standardised products- Censydiam- ASI*Connect- Brand Value Creator- Brand*Shout- Ideal Customer

Experience- WAO!Optimiser

(Wallet Allocation Optimiser)

Common Information Systems- Harmony- Symphony- iStaff- iTime- iQuote

PRODUCTS INTEGRATION SIMPLIFICATION HUBs & GMUs TRAINING

INFORMATION SYSTEMS

22

GLOBALISATION OF OPERATING SYSTEMS:

BETTER GLOBAL AND LOCAL PERFORMANCE

Hubs

Data processing andInternational projectmanagementcentres in Bulgaria, Roumania, Argentina, Malaysia, Tunisia, Chile:- 872 employees

GMUs

Expert modellingcentres based on specialist activities, located in Argentina, Brazil, China, France, Japan, Malaysia, South Africa, UK, US: - 193 employees

2013 Full Year Results – 27 February 2014 22

THE IPSOS DIFFERENCE: 6 SPECIALISATIONS, 86 COUNTRIES

COUNTRY MANAGERS’ ACCOUNTABILITY…

� Entrepreneurial autonomy

� Management of teams

� Innovation

� Local activation

� Closeness to clients

� Sensitive to local needs

…IN COMPLIANCE WITH

THE VALUES AND RULES

OF THE GROUP

� Information Systems Business Intelligence

� WSBLs, specialised business lines

� Global services

� International clients

� Integrated production

� Monitoring of Quality

� Around 50% of Ipsos’ turnover comes from local business

The Ipsos leadership team is multicultural and motivated by the same values

2013 Full Year Results – 27 February 2014 23

A GLOBAL NETWORK WITH STRONG ROOTS IN COUNTRIES

LOYALTY AND STRENGTHENING OF OUR TEAM

Judith Passingham

CEO Ipsos Interactive

Services (online, mobile)

Peter Braun

CEO Germany

Jim Meyer

CEO Ipsos

ASI NA

Francesc Costa

CEO Spain

Hamish Munro

CEO Australia

Yannick Carriou

CEO MCT & ASI

Jeremy McNamara

COO Operations

Ralf Ganzenmueller

CEO Loyalty

Neville

Rademeyer

Global CIO

Miranda Cheung

CEO Singapore

& Malaysia

New talent joined key activities and markets Support for and development of our leaders

David Parma

President P&G Org.

Marketing US

Dmitry Shoulgin

CEO CEE

Kerstin Wegener

Head of Client

Relationship Prog.

David Somers

CEO PanAfrica

Tim Swift

CEO Nigeria

Virginia Weil

Global Head of

Product Testing

� Sept. 2012: launch of Ipsos Partnership Fund (IPF)

� 147 IPF members still present (out of 156), as of 31/01/2014

2013 Full Year Results – 27 February 2014 24

CLIENTS: COMMITMENT AND TRUST

25

���� Consequence of a long-term commitment, close relationship and dedicated

resources

���� Covering a wide spread of industries

Finance

4 PRP clients

CPG

9 IGP clients 13 PRP clients

Pharma

2 IGP clients 6 PRP clients

Media/tech

3 IGP clients 1 PRP clients

Automotive

1 IGP client5 PRP clients

Energy

1 PRP client

THE 16 PARTNERING CLIENTS ACCOUNT FOR ~25% OF IPSOS BUSINESS IN 2013

� +6% vs 2012

� 6 clients grew more than 10%

STRONG PERFORMANCE IN KEY MARKETS

� Emerging countries: +8.1%

� UK, US and Germany: +6.5%

2013 Full Year Results – 27 February 2014 25

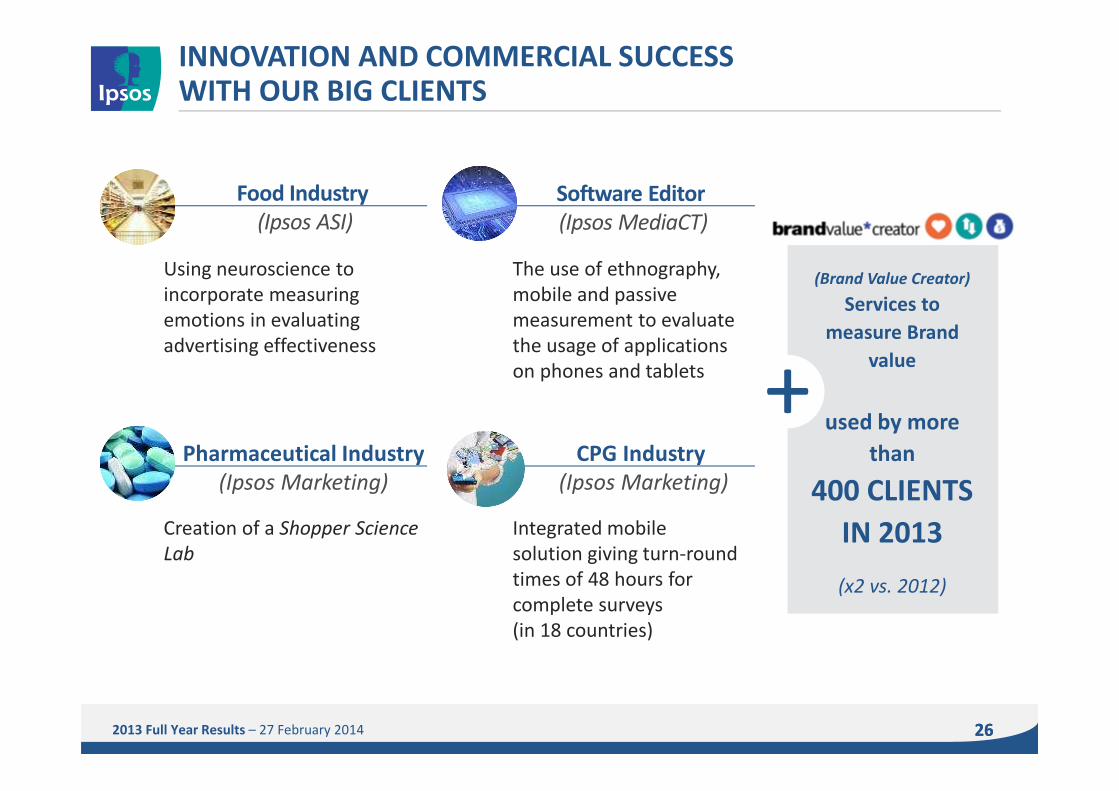

CPG Industry

(Ipsos Marketing)

26

Using neuroscience to

incorporate measuring

emotions in evaluating

advertising effectiveness

Creation of a Shopper Science

Lab

Integrated mobile

solution giving turn-round

times of 48 hours for

complete surveys

(in 18 countries)

(Brand Value Creator)

Services to

measure Brand

value

used by more

than

400 CLIENTS

IN 2013

(x2 vs. 2012)

Pharmaceutical Industry

(Ipsos Marketing)

+

The use of ethnography,

mobile and passive

measurement to evaluate

the usage of applications

on phones and tablets

Software Editor

(Ipsos MediaCT)

Food Industry

(Ipsos ASI)

2013 Full Year Results – 27 February 2014

INNOVATION AND COMMERCIAL SUCCESSWITH OUR BIG CLIENTS

26

NEW SERVICES, NEW OPPORTUNITIES

2013 Full Year Results – 27 February 2014 27

Source: Internal estimates Ipsos – 2012/2013 change

Mobile

SocialMedia

(Web listening andCommunities) Big Data

Analytics

Neuro-sciences

New Services enriching Ipsos’ offer

5.4% of Group turnover

+202%+44%

+73%

+170%Ethnography

+45%

US: IPSOS, AN AMERICAN STORY

SynovateLoyalty,Marketing,PublicAffairs

LEVERAGING CLIENTS’ GLOBALISATION

28

*Esomar 2013: The figures refer to the size of the market in 2012, incl. Advisory services ** 2011 only includes 1Q

for Synovate

3rd largest research company in the US

Size of the market* $13,756M

Ipsos revenue 2013 $575M

2013 Full Year Results – 27 February 2014

1st

office

1996 1998 2000 2001 20132002 2003 2005 2008 2010 2011**

ASIAdvertising

MonroeMendelsohnMediaCT OTX

Digital,Social listening,Communities

1,690

NPDPanels,Marketing

ForwardResearchAnimal Health& NutritionResearch

MarketingMetricsLoyalty

UnderstandingUnlimitedQualitative

Angus Reid (CA)Marketing

AC NielsenVantisModelling 23

offices

� Clients

o We have international programmes with 17 of our top 20 US clients

� New services: +54.2%

o Mobile (+193%)

o Communities and social listening (+30%)

o Marketing Mix Modelling (MMA) (+25%)

o Customer Journey (+40%)

� Partnerships of excellence

o Ivy League: Duke, Yale

o Thomson Reuters

UK: IPSOS MORI, A BRITISH STORY

29

INNOVATION AT ITS HEART

� Clients

o We have international programmes with 10 of our top 20 UK clients

� New services: +68.7%

o Mobile (x6)

o Ethnography (+41%)

o Evaluation (x30)

o Workshops (+148%)

� Partnerships of excellence

o Thought Leadership: 30 events in 2013, 1,500 clients

o Among the Top 100 brands in the UK

2nd largest research company in the UK

Size of the market* £5,076M

Ipsos revenue 2013 £161M

** 2011 only includes 1Q

for Synovate

2013 Full Year Results – 27 February 2014

** 2005 only includes 1Q

for MORI*Esomar 2013: The figures refer to the size of the market in 2012, incl. Advisory services

Research

in Focus

Synovate

1991 2000 20132005**

7offices

1,079

RSL

MORI

2011***

PANAFRICA: NEW BOUNDARIES

IPSOS REVENUE 2013: €21M

MARKET SHARE: 25%

ORGANIC GROWTH: +20%

EMPLOYEES: 499

Ipsos, in the TOP 3 of market research companies:

A story that begins

with a Nigerian start-up (2010)

then the acquisition of Synovate (2011)

Tanzania (1)

Uganda (1)

Zambia (1)

Kenya (1)

Mozambique (3)

Nigeria (2)

LARGEST RESEARCH COMPANY IN PANAFRICA

Ghana (1)

Ivory Coast (1)

QUALIFIED TEAMS

2013 Full Year Results – 27 February 2014 30

We have regional programmes with 6 of our top 10 Pan African clients

SOUTH AFRICA: AN ALREADY SOPHISTICATED MARKET

CLIENTS� + 10% with PartneRing clients

� + 31% with PRP clients

� We have regional programmes with 6 of our top 10 South African clients

PEOPLE� Establishment of a Graduate School to support young graduates

joining Ipsos (10 in 2013)� Employees= 294

SERVICES� Innovation and Forecasting (+32.4%)

� Leading supplier in Automotive research

� Important EFM offer (Enterprise Feedback Management), with own web-based

reporting platform (+15%)

� Largest Mystery Shopping supplier in Africa using latest mobile technology (+7%)

SUPPORTING GROWTHIN AFRICA

2ND LARGEST RESEARCH COMPANY IN SOUTH AFRICA

PARTNERSHIP� Partnership with the South African Sunday Times

SIZE OF THE MARKET*: $249MIPSOS REVENUE 2013: ZAR251M ($26M)ORGANIC GROWTH: +8.5%

2013 Full Year Results – 27 February 2014 31

*Esomar 2013: The figures refer to the size of the market in 2012, incl. Advisory services

2014OUTLOOK

2014 OUTLOOK

Accelerate

Keep implementing

Grow new services

Manage our talent

Balance global/local relationships

Increase margins, dividends

global platforms, solutions, services

building on science and technology

and reward people, reflecting their contribution

the generation of cash flow and deleverage the company

2013 Full Year Results – 27 February 2014 33

organic growth of at least 3%

Nobody’s

Unpredictable