Embed Size (px)

Citation preview

Behavioural biases : overconfidence and optimism and their influence on corporate dividend policy

Paulina Krawczyk Supervisor: Profesor Philip Valta

Bachelor Thesis Bachelor in Business Administration

December 2015

L’auteur de ce projet est le seul responsable de son contenu, qui n’engage en rien la responsabilité de l’Université ou celle du professeur chargé de sa supervision. Par ailleurs, l'auteur atteste que le contenu est de sa propre rédaction, en dehors des citations parfaitement identifiées, empruntées à d'autres sources.

� Paulina Krawczyk GSEM1

Table of contest:

Executive Summary 3 Introduction 4 Can we assume that managers are fully rational? 5

Biases 6

Section I: Overconfidence 9 Definition 9

CEO’s overconfidence 9

Measures of overconfidence – solutions 10

Malmendier and Tate’s approach 10

Ben - Davids approach 12

Section II: Optimism 14 Definition 14

Optimistic CEOs 14

Campbell optimism measures 15

Otto’s approach 17

Section III: Overconfidence, optimism and dividend policy 19 Dividend policy 19

Dividend policy and overconfidence 22

Dividend policy and optimism 22

Conclusion 24 References 25

� Paulina Krawczyk GSEM2

Executive Summary

The goal of my Bachelor Thesis is to show how behavioural biases might influence corporate financial decision. I concentrate in my project on the two most quoted and most robust biases: optimism and overconfidence and on their influence on the dividend policy.

The work is divided in five parts. The first part is an introduction, where I describe the development of cognitive psychology and its influence on the world of finance and economics. I also ask if we should assume that the CEO, whose goal is to maximise firm’s profit is always fully rational and does not suffer from behavioural distortions. At the end of the section I give a definition of bias.

The second part covers overconfidence, in particular the overconfidence of CEOs. The idea in this section is to first explain overconfidence from a psychological point of view and then show how one might measure that irrational behaviour in economics and finance. Assessment of psychological treats is not an evident task, especially in a corporate setting, where both internal and external factors have an impact on the CEO’s decisions. However I present two evolution methods than help link irrational behaviour to corporate decision-making.

In the next section I proceed similarly with the optimism bias: I start with a description of optimistic CEOs and then propose an explanation for the gap between rational and irrational decisions. Then I suggest that overconfidence and optimism bias may have the same influence on corporate decision making.

The fourth section applies the presented bias measure methodology on dividend policy.

In conclusion I sum up my work and ask open questions about the development of behavioural finance and its impact on corporate decision-making.

� Paulina Krawczyk GSEM3

Introduction

The theory of efficient markets assumes that agents behave in a rational way. That theory is widely approved in economics, finance, psychology, political science and as well in philosophy. Described by Adam Smith in the Wealth of Nation (1776), the theory considers that in the decision making process agents take into consideration available information, probabilities and potential costs in order to chose the self-determined best action. That’s the classical XVIII century theory, which gave a solid base for the development of economics studies.

The theory was questioned 200 years later. Researchers started to ask themselves how we can say that individuals make choices in their own interest and what it means precisely. In XX century the attractions of the rational choice approach, its empirical failings in psychology and economics have promoted an intense interest in new approaches. A wide range of alternative models were suggested. They are called “real life models” and complete the classical theory of rational decision making. Let’s take the example of two great researchers: Kaheman and Tversky who established the Prospect Theory (1979) – theory which helped to develop new field of study of behavioural economics and behavioural finance. According to Kaheman and Tversky agents do not behave in a rational way and they systematically violate the Expected Utility Theory. They tend to overweight small probabilities and underweight large probabilities. Individuals make decisions by comparing alternatives and prefer avoiding losses over acquiring gains. The other example which is often used to question rational decision making is an experience called Allais Paradox (1953), which explains how people violate the Independence Axiom. Also related is Robin’s Calibration Theorem (1997), which describes agent’s attitude over small and large stakes. There are many more examples which talk about the divergence from the classical rational theory and introduce cognitive psychology into the world of economics and finance.

The new behavioural financial concepts grow beginning 2000, when the dot-com bubble seems to be in its blow-off phase. Financial analysts and economists started to realise that the agent’s behaviour is far away from being rational. They introduce into their analysis the concepts of anchoring, hindsight bias, confirmation bias, overconfidence and herd behaviour. Researchers begin to realise that introducing the aspects of cognitive psychology into asset pricing models is something essential. They follow the hypothesis by empirical studies. Firstly, Hersh Shefrin (1994) introduces the name of “noise traders” for agents making cognitive errors. Mair Statman (2008) explains an behavioural asset pricing model in which expected returns are high not only when the objective risk is high, but also when the subjective risk is high. Fama and French (2004) summarise the theory and review the empirical studies of the CAMP. They conclude that CAMP fails to fully explain the relation

� Paulina Krawczyk GSEM4

between risk and return, which invalids most of its applications. Behavioural finance takes its place in the asset pricing modelling.

In this paper I am going to investigate behavioural finance in the field of corporate finance.

Is it important to consider cognitive aspects of CEO’s in their decision-making or can we assume that they are fully rational and they only need to face the irrational investor’s decision? What are the biases? How shall we measure cognitive treats? What are their influences on corporate manager’s decisions? Does it influence only certain decisions, like investment cash-flow? I would like to answer these questions by investigating managerial overconfidence and optimism biases and at the end look at their influence on dividend policy.

Can we assume that managers are fully rational? Even though we perceive the CEO’s role in measuring a company’s performance as crucial, when the performance is poor, we rarely blame the CEO. Usually we look for an explanation in market conditions, political policy or economic bubbles. As far as the CEO is concerned we do believe that they behave in a rational way and their goal is to maximise the company’s profit, given their leadership position and compensation. What is more in companies there exist many mechanisms designed to keep CEOs focused on value maximisation, like paying them with a stock options or saddling them with debt. Nowadays, researchers and analysists tend to relate corporate decisions to personal characteristics of the top decision maker inside the firm, instead of looking at the firm – its characteristics or environmental characteristics. One of the first ones who took into consideration manager’s irrationality was Roll (1986). He was studying corporate takeovers and found that economists should abandon the hypothesis of manager’s rationality. According to him there is no evidence to indicate that every individual behaves as if they were rational economic agents. He claims that market prices reflect rational behaviour because of averages: in actuality the market is characterised by grossly irrational individual behaviour that cancels out in the aggregate, leaving at the end a small behavioural component, a rational core, that all individuals have in common. On the example of takeovers he suggested that economists should stop disregarding psychological studies and started to analyse managerial biases. When managers think about taking over another firm, they conduct a valuation analysis of that firm and they take synergies into consideration. Roll suggests that if they are overconfident, they will be too quick to launch a bid when their valuations exceeds the market price of the target. It leads to excessive trading. Also in the case of takeovers the arbitrage strategies are complicated to implant as the managerial decisions concern assets, also human assets which are difficult to make an arbitrage with. What is more the hypothesis that irrational managers will learn from bad decisions is not valid, as the takeovers do not happen very often. We need to add as well a tournament mechanism in the company. That assumption could be generalised. During the CEO’s cadence some of the decisions are taken

� Paulina Krawczyk GSEM5

only once, like large investment decisions or choosing investment partners. In fact major decisions are not repeated often, which means that executives do not have the possibility to learn from bad decisions.

At the beginning managerial and economical press which was supposed to study the role of CEOs focused on the directly observable characteristics, like age, sex or education, as those variables could affect corporate decisions. Nowadays most of the researchers follow Roll’s hypothesis and consider in their empirical studies behavioural biases, which make the mangers behave irrationally, because even if companies have mechanisms to keep managers focused on value maximisation, CEOs tend to think they are proceeding correctly and if they are wrong it is difficult to change their mind. That is why the development in the study of CEO’s behavioural biases is so essential.

Biases Cognitive biases, or beliefs, are described as a type of error in thinking that occurs when people are processing and interpreting information in the world around them. They often originate from an attempt to simplify information processing, like a rule of thumb that helps agents to make sense of the world and reach decisions with relative speed. What is the reason of biases? It is psychologically proved that heuristic or mental shortcuts can often lead to such errors. What is more social pressure, individual motivations, emotions and limits on the mind’s ability to process information can also contribute to cognitive biases. They can often lead to bad judgments and as follow wrong decision-making. However we should not always consider them as bad. Psychologists argue that many of them may serve an adoptive purpose – they allow us to reach decisions quickly, which might be very helpful when one is forced to make decisions under pressure. Relevant examples of bias for this paper include:

Representativeness: Is described as a situation in which agents take decisions based on stereotypes and prejudice. The problem was investigated by Kahmen and Tversky (1974) and refers to the problem of underweighting of base rates of some situations or characteristics, which were generated by already existed model or situation:

”Many of the probabilistic questions with which people are concerned belong to one of the following types: What is the probability that object A belongs to class B? What is the probability that event A originate from process B? What is the probability that process B will generate event A? In answering such questions, people typically rely on the representativeness heuristic, in which probabilities are evaluated by the degree to which A is representative of B, that is, by the degree to which A resembles B. For example, when A is highly representative of B, the probability that A originates from B is judged to be high. On the other hand, if A is not similar to B, the probability that A originates from B is judged to be low.”

� Paulina Krawczyk GSEM6

Availability Heuristic: it refers to the problem when decision is taken in an “easy and quick way”, when agents take into consideration only readily available information (usually relying on memories), without investigating other alternatives or procedures. Again the problem is described by Tversky and Kahneman (1974):

"There are situations in which people assess the frequency of a class or the probability of an event by the ease with which instances or occurrences can be brought to mind. For example, one may assess the risk of heart attack among middle-aged people by recalling such occurrences among one's acquaintances. Similarly, one may evaluate the probability that a given business venture will fail by imagining various difficulties it could encounter. This judgmental heuristic is called availability. Availability is a useful clue for assessing frequency or probability, because instances of large classes are usually reached better and faster than instances of less frequent classes. However, availability is affected by factors other than frequency and probability. Consequently, the reliance on availability leads predictable biases."

The problem has been followed by the researches and for example Chiodo (2002) found that overestimation of the subjective probabilities can cause overreaction and under reaction of expectations and, subsequently, asset pricing.

Anchoring: is a heuristic in which decisions are made based on an “anchor”, which means that agents start their decisions with some initial, possibly arbitrary, value and then they adjust to it. Tversky and Kahneman conducted an experiment in which subjects were asked to estimate the percentage of United Nations’ countries that are African. Before giving a guess, they were asked to generate a random number between 0-100. As it appeared later their guessed were affected by the generated number. Agents how gave number 10, estimated to probability at 25%, and whose compared to 60, gave the estimation at 45%.

In psychology the biases problem is well known and described, but when the psychological theories came into financial literature, they were met with scepticism. Some scientists argued that behaviourists use psychological literature to find support for their assumptions which will make their arguments matter, without using empirical studies; that for instance they use contradicting biases, like optimism and pessimism to support the same argument in their research. It is not surprising that the demand for empirical studies has emerged. The empirical studies have for goal to identify which exact bias, if any, influences decision-making and in which way. They have to deal with many challenges, because it is not obvious how to measure the gap between rationality and irrationality, especially when we consider corporate decision making. Campbell (2000) discusses the “technical” problem of empirical research, arguing that behavioural models cannot be tested using aggregate consumption or market portfolios, because rational utility maximisation neither consumes aggregate consumption, nor holds a market portfolio. As stated previously, Roll (1986) claimed population might be considered as grossly irrational individuals. The idea of measuring behavioural biases will be

� Paulina Krawczyk GSEM7

to treat each decision and individual separately to measure the distortions. As a result testing behavioural models is difficult without detailed information on the individual trading information of market participants. That sort of information is confidential and difficult to get. The other problem in empirical studies might be time scale: can we measure the CEO’s biased decisions over one year and assume that the next year they will be rational, since CEO is learning from his mistakes? The effect of learning is often muted by errors of application: when a bias is explained, agents often understand it, but then immediately proceed to violate it again in a specific application. Finally, there is a difficulty to link the biased CEO’s decisions with the changes in corporate decisions, like investment cash-flow, the behaviour towards shareholders or the financial preferences. The key question is: how and which biases influence CEO’s decisions, and which kinds of decision?

As psychologists use the psychological tests to evaluate biases – like cognitive reflection test – in corporate finance some interesting, solutions have been proposed as well. In future sections I will present how researchers suggested to deal with the numerical measures of behavioural biases. I will focus on overconfidence and optimism as these two are mostly quoted. They are as well robust and strong and have been measured on many samples. Since these biases are very individual there is a little risk that they will be unbiased through learning (Baker and Wurgler 2013). Furthermore I will be investigating their influence on the dividend policy.

� Paulina Krawczyk GSEM8

Section I: Overconfidence

Definition What does overconfidence mean? In the psychological literature the expression: “better than average” is used. We might take as an example an experiment of Svenson (1981) who asked subjects about their driving competences. The majority of subjects believed they were more skilful and less risky than average – 82% of a sample of students placed themselves among the top 30% safest drivers. However overconfidence may be regarded not only as a “better than average” effect. After reading papers from the Psyching database with the keyword “overconfidence” (365 results), Moore and Healy (2007) distinguished three different definitions of overconfidence. The first one is the overestimation of one’s ability, performance, level of control, or chance of success. The second one is when people believe themselves better than others, they rank themselves better than median. It is called over placement. The last way to look at the overconfidence is to examine subjects with numerical answers and look if they are excessively regarding the accuracy of answer. That experiment shows that subjects very often give to their answers the confidence intervals which are too narrow, it leads to overvaluation of the correctness of theirs answers. Usually most of the researchers do not take into consideration the difference between these definitions.

CEO’s overconfidence Taking into consideration psychological papers, I may assume how the overconfident CEO will be behaving. If we look at the “better than average” effect, I will expect that overconfident CEO will be sure of his abilities of management and will find himself better than other average managers in the company. They might assume that they have better skills in picking investment policies or merger targets and that their decisions are usually correct. When we look at the overestimation of expected payoffs we might consider that overconfidence CEO’s will be expecting higher outcome of his investment decisions. There is also a probability that overconfident CEO will be picking more risky and challenging projects, as they under valuate the expected variance. And if we examine the CEO’s confidence intervals we might identify that they are too narrow as they are too assured of their decision-making. These are only my hypothesis given the overconfidence explanation; however some of them are proved by the empirical research and some of the researchers proposed smart results to these problems. To respond these questions fist of all we need to establish how to measure overconfidence and than investigate which CEO’s decisions it influences.

� Paulina Krawczyk GSEM9

Measures of overconfidence – solutions In behavioural finance the most demanding problem is to measure a derivation between rational (none biased) behaviour, and irrational (biased) behaviour. The first idea which comes to mind is to use in such a research psychological questionnaires, which is not a bad solution and it is quite often used in searches. However, using psychological survey requires a lot of time, because to measure the biases one needs at least 5-7 years time’s intervals (that is based on a mean of few researchers, used in my paper). What is more, considering time’s intervals we are facing a problem of tournament in the companies, when the CEO changes, one needs to start a survey from the beginning. Even is psychological tests might take lots of time, they are quite efficient in terms of eliminating company’s characteristics. Psychological surveys are usually very personal and they only concentrate on the individual treats. That eliminates in the survey the characteristics of company, which might influence CEO’s decisions – like corporate culture, financial preferences or shareholders influence’s. On the other hand these surveys should be created in such a way to exclude CEO’s environmental aspects, like family’s history, education or financial status, as these are the variables which could impact CEO’s overconfidence. As the cognitive questionnaires are concerned the numerical answers tests are very efficient to measure the biases. These are the tests which help to measure the confidence intervals which I had already described. Further I will present an example of a survey lead by Ben-Davis (2007) to measure overconfidence. That survey is robust as it helps to eliminate other biases which could correlate with overconfidence, like optimism.

The other solution, than cognitive tests will be to use numerical surveys, which success will depend on the precision of measure of bias. As it was already mentioned in the introduction, working on real data in behavioural finance is very challenging. We need detailed information on personal trading actions, which are usually confidential. Nonetheless, some researchers came up with some clever approaches. I will start this paragraph with Malmendier and Tate (2005) approach. They argued that CEO’s characteristics lead to distortions in corporate investment polices. What is very intriguing and revolutionary they looked at the detailed information on the stock ownership and set of option package to define overconfidence bias.

Malmendier and Tate’s approach Stock options, which give a recipient the right to buy a share of stock at a pre-specified exercise price for a pre-specified term, have emerged as the largest component of compensation for US executives (Hall and Liebman 1998, Hall and Murphy 2002). They are interesting as a form of compensation since they provide a direct link between an executive and a company’s stock performance. However executive stock–options differ in critical ways from the standard “priced” options formulas, which are freely tradable and traders may hedge the risk of option by short-selling. Executive options face the problem of under-diversification

� Paulina Krawczyk GSEM10

and are not tradable and, furthermore, the sale of executive stock-options may be restricted. These are the mechanisms put on the CEO to engage risk-seeking behaviour.

Malmendier and Tate (2005) use an analysis of execution of stock options to evaluate the overconfidence bias. They study a sample of 477 large publicly traded US companies from 1980-1994, which had to as well appear at least four times at one of the Forbes lists. Their set of data provides them with detailed information on the stock ownership and options package and they obtain the CEO’s portfolio picture. To investigate the CEO’s transactions on his personal account and on corporate account, they supplied the data set with extra items, like investment on capital expenditures, cash-flow as earnings before extraordinary items, capital as property. To have a final sample, they supplement the data with personal information about executives (their education background, employment experience). I assume that they use these variables to show a more detailed picture of CEO.

They say that rational CEOs should exercise in-the-money options or sell stock on a pre-committed schedule, as it helps to avoid sending negative signals to the market. What is more executive stock-options as said before face the under diversification problem and the human capital is invested, which confirms that they should be exercised before expiation or when it exceeds some level of in-the-money. Looking at the data they notice that some of executives do exactly the opposite, they keep or even buy more company stock-options instead of selling it, which shows that they overestimate the company’s performance under their executive period (1 type of overconfidence according to Moole and Haely definition). That helped them to define three measures of overconfidence, or proxies based on “delta”: Holder 67, Longholder and Net Buyer.

Holder 67 refers to the CEO who keeps the stock-options after the vesting period and when their stock-option exceeds 67% in-the-money. Vesting is a period over which executive has the ability to realise his right to exercise stock-options — in most cases it is 5 years. Malmendier and Tate use the Hall and Murphy (2002) framework to decide a reasonable benchmark for the percentage in-the-money at above which executive should exercise options and they fix it at 67%. Holder 67 is constructed as follow: they are looking at the CEOs who had 67% in-the-money during the vesting period. They identify the CEO and look if they wasted the possibility of executing the option during or after the vesting period. If the CEO failed to exercise the option they are investigating if they subsequently exhibit the same behaviour at least one more time during their tenure as CEO. If that is right the CEO is classified as an overconfident. From the subsample of firms (337 observations), 58 CEOs were classified as overconfident using the Holder 67 measure.

Constructing Longholder measure Malmedier and Tate targeted the expiration date of option, rather than looking at vesting period. The CEO was classified as an overconfident if they were

� Paulina Krawczyk GSEM11

holding the option till the last year of its duration. In this subsample of 661 CEOs, 85 were considered as overconfident.

In the last measure called Net Buyer, they looked at the CEOs’ tendency to purchase additional stock-options despite their high exposure to company risk. Of 158 CEOs used in a subsample, 97 of them were considered as Net Buyers.

The rationale behind these behavioural measures is that the overconfident executive perceives a firm’s stock as under value by the market and is less likely to exercise stock-options, than a rational executive. Furthermore, overconfident CEOs believe in a good performance of company under their tenure. Malmendier and Tate also looked at some alternatives which could explain the late exercising of stock-options and they excluded: inside information, signalling, risk aversion and corporate governance, which strengthen the interpretation of their measures as proxies for overconfidence.

I am using the example of Malmendier and Tate’s approach to present a link between stock-options exercising and overconfidence. Their solution for empirical studies is nowadays used to show the relations between overconfidence and corporate polices. However Malmendier and Tate’s solution does not exclude other biases which might make agents behave the same way. For example agents who are optimistic might also overestimate the performance of the company. That is why overconfidence and optimism in their research are considered very close and similar to each other.

Their insight into stock-options exercises as an assumption of overconfidence is interesting and is coherent with the Hall and Murphy framework. However access to that sort of data is difficult and the bias can not be measured for every firm.

As mentioned above the other possibility to measure overconfidence will be to run an empirical, “numerical answer” survey. I will use now a different approach to identify a behavioural bias.

Ben - Davids approach Ben-Davids (2007) says that overconfidence is an overestimation of one’s beliefs or underestimation of variance of risky processes. These two definitions of overconfidence help to investigate the bias by focusing on the confidence intervals and by looking at the variance of predicted results. In his research he was using a data collected by Duke University between March 2001 and June 2009, which was investigating each quarter around 2000-3000 financial officers. The aggregate results of data are accessible on www.cfosurvay.org. The question asked in the survey was as following:

“On the next year, I expect the S&P 500 return will be:

� Paulina Krawczyk GSEM12

a). There is 1 in 10 chance the actual return will be less than …%

b). I expect the return to be ….%

c). There is 1 in 10 chance that actual return will be grater than … %”

He also used a double-siring procedure to separate the long and short term overconfidence (ST - based on the one-year return and LT - based on the 10 year return). Given the responses he measures the confidence intervals of given predictions (10% and 90%) into probability distribution. Looking at the probability distribution, if it is a wide one, we may assume the subjective uncertainty and a narrow one, may reflect a subjective confidence. In addition, we can calculate the variance of distribution - if the predicted variance distribution is bigger than the real variance distribution, we can assume that the agent is overconfident.

Ben-Davids went further than Malmendier and Tate’s in his research. He tried to separate optimism and overconfidence bias, which very often go together. Agents, who sees their company’s future in bright colours, might feel as well more confident in their decision-making. To eliminate optimism form the overconfidence he asked one more question in his survey:

“a). Rate your optimism about the US economy on a scale from 0-100, with 0 being the least optimistic and 100 being the most optimistic.

b), Rate your optimism about the financial prospects for your company on a scale from 0-100, with 0 being the least optimistic and 100 being the most optimistic. “

These questions helped him to specify the optimism about the US economy and optimism about the firm performance. Then, as in the first question, he compares the predictions with the reality. As Malmendire and Tate he also excludes some other variables which could influence the executives predictions, like past market and firm performance and personal characteristics. These variables are included in his final sample.

Ben-Davids’ approach is also different because it is based on the predictions, which goes well with the theory that overconfidence causes the overestimation of expected returns. An advantage in his approach is the fact that he eliminates (by asking more specific questions) the optimism bias from the overconfidence, so it makes his research more robust. However making a survey requires lots of time and the data is not easy to be collected.

Ben-Davids and Malmendier and Tates measures of overconfidence will be used furthermore in this paper to elaborate the influence of biases on the dividend policy. Now we will have a look at optimism, how it is defined, and what is the idea to measure it.

� Paulina Krawczyk GSEM13

Section II: Optimism

Definition Wenstein (1980) defines optimism as the unrealistic tendency of individuals to underestimate the likelihood they will experience adverse events, such as skin cancer or a car accident. He calls it a positive illusion. Taylor and Brown (1988) describe optimism as unrealistically positive self-evaluation, exaggerated perception of control. They believe that it is maintained through interpretation and retrieval of information, cognitive drift, acknowledging pockets of incompetence (i.e. accepting a lack of talent in certain areas of life while maintaining belief in a general competence) and negative self-schemata which enable people to simply avoid situations in which they lack talent – in other words they construct a self enhancing world in which to live. Optimism bias is especially pronounced when the problem is perceived infrequently, for example becoming bankrupt or experiencing a nervous breakdown (Griffin and Murray, 2008). On the other hand when the event is frequent the optimism bias perceived is relatively prevalent. There exist two approaches in psychology to asses optimism bias. In first one participants are explicitly instructed to rate the likelihood of experiencing some adverse event. The direct approach demonstrates that some agents feel less likely to experience some adverse events. The second method, which is indirect agents are asked the same question, plus one additional question. They are asked to estimate the likelihood that other individuals will experience some adverse events at the end a difference is calculated between the two estimations. The indirect method is more often used and gives more robust results.

The psychological studies on optimism bias made optimism an interesting subject of study for corporate finance. On the subject of managerial optimism, Heaton (2002) states: “managers are more optimistic when they systematically overestimate the probability of good firm performance and underestimate the probability of bad firm performance”. March and Shapira (1987) say that managers are more optimistic about the outcomes they can control and Gilson (1989) shows that agents are more optimistic about the outcomes to which they are highly committed. That implies that managers will generally be highly optimistic about the firm’s success, because their wealth and reputation depend on it. As in the previous section, I will make a hypothesis about how optimism might influence corporate managers decisions, then I will demonstrate Campbell’s and Otto’s approaches to measure optimism bias.

Optimistic CEOs Since optimistic CEOs tend to overestimate a probability of positive events I will assume that optimistic CEOs will have a tendency to think that the projects they choose will be very profitable or they might think that the mergers will bring positive effects. We can note that these assumptions are very similar to the ones about overconfidence. Can we say that

� Paulina Krawczyk GSEM14

optimism and overconfidence have the same effects? Is there any difference between optimism and overconfidence? The main difference is that overconfidence will be making changes in variance - it causes the underestimation of variance, and optimism causes overestimation of the mean. However the effects of both biases will be similar and we can easily consider both biases causing the same results. Ben-David (2007) finds that: “In particular, it is plausible that managers who exhibit overconfidence are also optimistic about the future of their firms. Alternatively, it is possible that managers who anticipate a bright future for their firm feel more confident.” I find the Ben-Davids statement very wise, further I will write about Otto’s paper, where he shows a correlation between optimism and confidence. Most of the researches use overconfidence and optimism alternatively and they establish similar measures for both biases. A very good example of how overconfidence and optimism are so close to each other is a paper by Colin Campbell (2010), where he uses Malmenier’s and Tate’s overconfidence proxies to establish an optimism measure.

Campbell optimism measures Campbell (2010) investigates a relation between optimism and forced turnover. He asks if optimistic CEOs are more likely to be fired. To examine that problem he tests that hypothesis using CEOs in the ExecuComp database between 1992 and 2005 and uses Malmendier’s and Tate’s overconfidence proxies modified to infer a hight or low optimism level. They draw three optimism measures.

1. Optimism measure based on stock option holding/exercise decision

The first measure is based on the overconfidence measures of Malmendier and Tate. Campbell proceeds in a similar way to Malmendier and Tate, looking at the stock option exercise decisions. He takes as a given 67% money's cutoff for a full sample of CEOs to indicate optimistic CEOs. Then he identifies high and low optimistic measures. To define high optimism he looks at the CEOs who hold stock options that are more than 100% in the money. To complete the hight optimism he defines low optimism as the CEOs who exercise stock options that are less than 30% in the money and do not hold any other exercisable options that are greater than 30% in the money. Given both definitions of high and low optimism he calls moderate optimism CEOs who hold or exercise options between 30-100% in the money. Having three definitions of optimism he classifies the CEOs.

His approach is very similar to Malmendier’s who also defined three measures of overconfidence. Since keeping options more than 67% into money is not rational Campbell assumes that sort of behaviour is due to optimistic bias. However in his research he lays out some potential concerns about the stock exercise measure. First, CEO options decisions might depend on the expectations of their board of directors pressure. Second, CEOs might have

� Paulina Krawczyk GSEM15

inside information. However later Campbell creates a model which is robust and these concerns are not valid anymore.

2. Optimism based on net stock purchases

Net stock purchases equal purchases minus sales, both in units of shares. Campbell calls a CEO highly optimistic if in a given year their net purchases are in the top quantile of distribution of net purchases by all CEOs and those purchases increase their ownership of firm stock by at least 10%. The CEOs are classified as low optimistic if they are in a bottom quantile of net stock distribution. CEOs in between low and high net purchases are classified as moderately optimistic. In this measure of optimism we may be concerned that the buy or sell stock decisions might depend on the inside information or on the board of directors or even on the CEO’s personal taxes information. The idea will be to construct a model to take into consideration those matters.

3. Optimism Measures based on firm investment level.

This kind of measure helps avoid personal decisions, because it does not depend on managerial compensations and incentives. Return on investment is defined as a profit made on the sale of a security or other asset divided by amount of the year’s investment, expressed in an annual percentage rate. Highly optimistic CEOs are classified if they are placed in the top quantile of firms sorted on industry-adjusted investment rates for two consecutive years. Already Malmendier and Tate (2005) showed that there exists a link between behavioural biases and investment decisions, however that sort of measure is a subject of criticism, as investment decisions might depend on many external factors, such as the market situation, interest rates or internal — company — factors like cash flow.

Campbell’s results show that in most cases the percentage of each sort of optimism measures in average is about 33%. We might conclude that if a CEO is hight optimistic according to option holding exercise, they will also be optimistic according to investment rate indicator. That means the the bias will be visible in the CEO’s stock option exercises and in his investment policy at the same moment.

Campbell’s measures are very coherent with Malmendier’s and Tate’s approach. Obviously robustness of those proxies will depend on the way one constructs the model to investigate an implication between optimism and a managerial decisions.

The other measure of optimism I want to present in my paper is based on the earnings forecasts. Using that kind of measure we will assume that the CEOs overestimate perceived earnings. The empirical research is proposed by Otto in his paper CEO optimism and incentive compensation, 2012.

� Paulina Krawczyk GSEM16

Otto’s approach Otto (2012) investigates the relation between optimism and CEO compensations. He assumes that the more optimistic the CEO is, the higher their compensation will be. To measure optimism bias, he uses an approach similar to Campbell’s, Malmendier’s and Tate’s. He also establishes another approach based on the earnings forecasts, called EPS Forecasts.

Earnings forecasts are very powerful. Even small deviations can send a stock higher or lower. If a company exceeds its consensus estimates, it is usually rewarded with an increase in stock price. If the company sometimes falls under the consensus or only meets expectations, the share price might fall. In the short term the difference between earnings forecasts and real numbers might be one of the factors which influence share prices.

Companies release earnings forecasts each year, around 70 % of these forecasts are available in the Execucomp database. Otto starts his analysis with all company-issued EPS forecasts announced on Execucomp between 1996 and 2005. Than he compares the forecasts with the ex post realised EPS. “If the forecast was issued in the form of an EPS range (62% of all forecasts), then the dummy variable takes the value one if the lower bound of the range exceeds the EPS that were eventually realised. If the forecast was a point estimate (38% of all forecasts), then the dummy variable takes the value one if this point estimate exceeds the ex post realised EPS.“ (Otto, CEO optimism and incentive compensation, 2012). Otto introduces two more variables in his paper: HighForecast and WidthForecast. HighForecast is a dummy variable which is zero if all EPS forecasts are lower than realised EPS. That means that a higher value of HighForecast will imply a higher value of optimism. ForecastWidth measures that average the width of the EPS ranges that are forecast by CEOs. By calculating the confidence intervals of forecast we may assume that whether the CEO is confident about their forecasts or not. What is more interesting, he calculates the correlation between ForecastWidth and HighForecast. The correlation coefficient implies a positive relation between optimism and confidence. That means the more optimistic CEOs are also more confident in their earnings forecasts.

Otto’s approach is similar to Ben-Davids’ approach for optimism which is also based on predictions. I find that the advantage of Otto’s approach is that each CEO wants to give the predictions witch will be very close to the real EPS, because as mentioned before even small derivations between predictions and real EPS might influence share prices. That is why executives do not see any resort to manipulate the forecasts. Furthermore, large amounts of EPS forecasts are available in open databases, like the Execucomp database.

Having established solutions to measure cognitive treats, let us focus on how they might influence corporate decisions. Many researchers connect overconfidence or optimism with managerial decisions, like investment judgements, mergers and acquisitions choices or

� Paulina Krawczyk GSEM17

financing policies. I would like to ask in next section if these two biases should be taken into consideration during the analysis of dividend polices, if they impact the dividend distribution and can explain the variations in dividend payouts.

� Paulina Krawczyk GSEM18

Section III: Overconfidence, optimism and dividend policy

Dividend policy What makes a dividend policy such a complicated decision to make by the CEOs?

First of all, dividends payment may be executed in different ways: shareholders can be paid in cash, they might be given extra shares or even properties as dividend payment. The choice of payment is already complicated, as dividends in cash are highly taxed, but they are still mostly preferred by shareholders. There is also the crucial question of how much they should be paid, since the total amount of money is significative. As Allen and Michaely, 2003 say: “For example, in 1999 corporations spent more than $350b on dividends and repurchases and over $400b on liquidating dividends in the form of cash spent on mergers and acquisitions”.

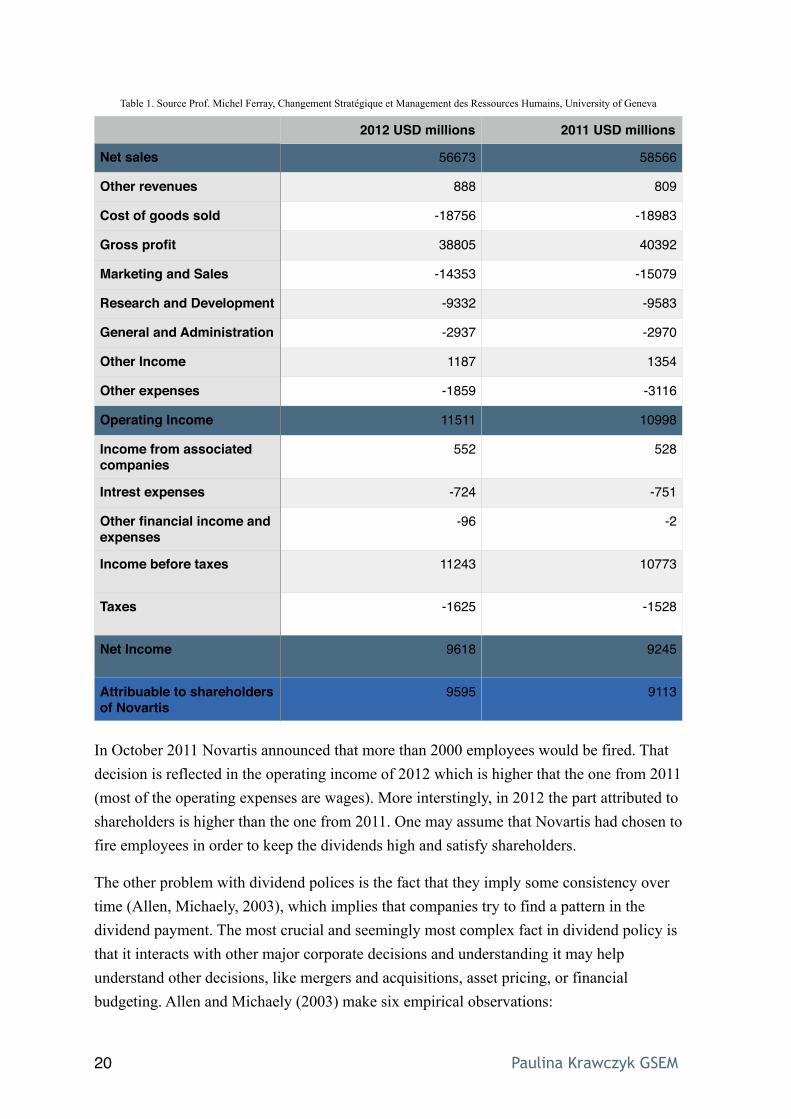

Dividend payments also touch the problem of equity and social responsibility. Let us have a look at the consolidated income statements of Novartis for 2012 and 2011.

� Paulina Krawczyk GSEM19

In October 2011 Novartis announced that more than 2000 employees would be fired. That decision is reflected in the operating income of 2012 which is higher that the one from 2011 (most of the operating expenses are wages). More interstingly, in 2012 the part attributed to shareholders is higher than the one from 2011. One may assume that Novartis had chosen to fire employees in order to keep the dividends high and satisfy shareholders.

The other problem with dividend polices is the fact that they imply some consistency over time (Allen, Michaely, 2003), which implies that companies try to find a pattern in the dividend payment. The most crucial and seemingly most complex fact in dividend policy is that it interacts with other major corporate decisions and understanding it may help understand other decisions, like mergers and acquisitions, asset pricing, or financial budgeting. Allen and Michaely (2003) make six empirical observations:

Table 1. Source Prof. Michel Ferray, Changement Stratégique et Management des Ressources Humains, University of Geneva

2012 USD millions 2011 USD millions

Net sales 56673 58566

Other revenues 888 809

Cost of goods sold -18756 -18983

Gross profit 38805 40392

Marketing and Sales -14353 -15079

Research and Development -9332 -9583

General and Administration -2937 -2970

Other Income 1187 1354

Other expenses -1859 -3116

Operating Income 11511 10998

Income from associated companies

552 528

Intrest expenses -724 -751

Other financial income and expenses

-96 -2

Income before taxes 11243 10773

Taxes -1625 -1528

Net Income 9618 9245

Attribuable to shareholders of Novartis

9595 9113

� Paulina Krawczyk GSEM20

“(1) Large, established corporations typically pay out a significant percentage of their earnings in the form of dividends and repurchases.

(2) Historically, dividends have been the predominant form of payout. Share re-purchases were relatively unimportant until the mid-1980s, but since then have become an important form of payment.

(3) Among firms traded on organised exchanges in the USA, the proportion of dividend-paying firms has been steadily declining. Since the beginning of the 1980s, most firms have initiated their cash payment to shareholders in the form of repurchases rather than dividends.

(4) Individuals in high tax brackets receive large amounts in cash dividends and pay substantial amounts of taxes on these dividends.

(5) Corporations smooth dividends relative to earnings. Repurchases are more volatile than dividends.

(6) The market reacts positively to announcements of repurchase and dividend increases, and negatively to announcements of dividend decreases.”

What is more important, Allen and Michaely define the corporate decisions which should be taken into consideration, while fixing a dividend payments.

“(i) Taxes If dividends are taxed more heavily than capital gains, and investors cannot use dynamic trading strategies to avoid this higher taxation, then minimising dividends is optimal

(ii) Asymmetric information If managers know more about the true worth of their firm, dividends can be used to convey that information to the market, despite the costs associated with paying those dividends (However, we note that with asymmetric information, dividends can also be viewed as bad news. Firms that pay dividends are the ones that have no positive NPV projects in which to invest).

(iii) Incomplete contracts If contracts are incomplete or are not fully enforceable, equity holders may, under some circumstances, use dividends to discipline managers or to expropriate wealth from debt holders.

(iv) Institutional constraints If various institutions avoid investing in non or low- dividend-paying stocks because of legal restrictions, management may find that it is optimal to pay dividends despite the tax burden it imposes on individual investors.

(v) Transaction costs If dividend payments minimise transaction costs to equity- holders (either direct transaction costs or the effort of self control), then positive dividend payout may be optimal.” (Handbook of Economics of Finance, chapter 7).

� Paulina Krawczyk GSEM21

Taxes, or transaction cost should be taken into consideration while realising dividend. However can we consider that executives do not behave rationally and consider behavioural biases like overconfidence and optimism, which could influence dividends payments? In the next section I would like to show how both biases might influence dividend payments and the CEO’s preferences about the dividend policy.

Dividend policy and overconfidence Ben-David, Graham, Harvey (2007) test how miscalibrated (irrational) CEOs take financing decisions. They showed that miscalibrated managers think that investors underestimate the value of project and therefore they believe that their firms’ equity is undervalued by market. For an overconfident CEO external securities to finance projects seem very expensive, thought they will prefer to use internal cash to finance them. All of that will influence dividend policy. Since internal cash is used to pay investment projects, there will be less of it to finance dividend payments and therefore overconfident CEOs are less likely to pay dividends because they hoard cash for future investments.

Deshmukh and Goel (2013) go even further in their analysis. They model a dividend distribution as a trade off between minimising the cost of retaining excess cash in the firm and minimising the expected cost of external financing for future investment. According to it a CEO should be worried about the cost of external financing as shareholder interests are taken into consideration. Deshmukh and Goel investigate the differences in dividend payments by rational and irrational CEOs and take into consideration growth opportunities, cash flow and firm size. Their results show that dividends paid by overconfident CEOs are smaller in companies with a higher growth rate than those paid by overconfident CEOs in companies with a smaller growth rate. Moreover, the positive relation between dividend payments and cash flow is stronger for overconfident CEOs. If current cash-flows are hight an overconfident will increase the dividend payment. They explain that it is caused by the strong perception of current cash-flows, which influence a stronger prediction of future cash-flows. They also study the effect of asymmetric information on the overconfident CEOs’ dividend payments. It seems that there should be a negative relation between asymmetric information and dividend payment, however they conclude that the strength of the effect does not appear to depend on the overconfidence bias.

Dividend policy and optimism While most papers concentrate on the dividend amount payments and relation with behavioural biases, professor Christa H.S Bouwman decided to look closer into the market reaction on dividend announcements, in the case of investors who don’t know which manager is rational and which one is not. Her main prediction is that: “the market reacts more positively to a given dividend change by an optimistic manager.” Her assumption implies that when rational and irrational managers announce the same dividend change, the market will look more assuredly into the dividend change announced by optimistic manager. On the other

� Paulina Krawczyk GSEM22

hand, her assumption does not imply that optimistic managers will pay higher dividends than rational ones. In her study she investigates only positive dividend changes.

Her empirical research is very interesting. The prior question, which need to be studied carefully is to determine the announcement day. It needs to include the same type of dividend change and avoid announcements which took place around confounding events. First, she takes all the dividend announcements in the CRSP (Center in Research in Security Prices). Then, to define final sample she uses the following criteria:

“a). the firm paid an ordinary quarterly cash dividend in U.S dollars, in a current and previous quarter

b). Other distribution events (stock splits, mergers, stock dividends, rights offerings, etc.) were not declared between the declaration of the previous dividend and four days after the declaration of the current dividend.

c). There were no ex-distribution dates between the ex-distribution dates of the previous and current dividends. “ Than the market reaction is measured using the modified market model (Brawn and Warner, 1985), where daily returns for each sample firm are calculated by deducting the equal- or value-weighted index return from firm’s return. She is summing the returns over three days and gets the Cumulative Abnormal Returns.

To measure optimism bias Bouwman used Malmendier’s and Tate’s observation sample and their proxies. For each observation she associate the CRSP dividend observation and calculates the Cumulative Abnormal Returns. Her results are as follow: “the coefficients on the optimism measures suggest that, ceteris paribus, the three-day cumulative abnormal returns are 0.7% to 1.7% higher when an optimistic CEO announces a dividend increase than

when her rational counterpart announces such an increase.”

� Paulina Krawczyk GSEM23

Conclusion The goal of my Bachelor Thesis was to show the impact of behavioural biases on the corporate financial decisions. Since behavioural finance literature sees its peak performance since 2000, there appeared interesting solutions to run empirical studies. Malmendier’s and Tate’s suggest to look at the stock-option execution to find if executives suffer of overconfidence or optimism biases. Ben-Davids asks in his survey numerical questions, which help him to estimate confidence intervals and measure overconfidence biases. Campbell suggests three different measures of optimism: based on stock-options exercise, based on net purchases and on the firm’s investment level. Finally, Otto looks at the EPS forecasts to decide it an executive is optimistic about future firm performance. These solutions are revolutionary in a world of corporate finance and they might help complete financial decisions analyses. As shown in the final example, behavioural biases might influence dividend policy. However, we need to mention that other studies proved that overconfidence and optimism influence as well: mergers and acquisitions (Malmendier and Tates 2008 or Schneider and Spalt, 2010), investment polices (Malmendier and Tates 2005), capital structure (Hackbarth, 2009) or IPO prices (Ljungqvist and Wilhelm, 2005).

The subject of behavioural biases is very comprehensive, some might still say that it is very subjective. However, I think that the period when behavioural finance was not considered serious has passed and now it occupies financial press and has been introduced as a course in top Business Universities. That is very crucial, because as with every new developing area of study there are some open questions, which still needs to be resolved.

In my introduction I pointed out some other biases than optimism and overconfidence. It would be interesting to investigate an influence of representativeness or availability heuristics on corporate decisions.

The other problem concerns the measures of overconfidence and optimism. As psychological surveys are very precise, they take a lot of time. On the other hand Malmendier’s and Tate’s solution to determine overconfidence or optimism require precise data on stock option exercises, which is difficult to obtain. Do there exist some other ideas to approach the issue of biases measures? Some solution available to everyone, so that the analysis of behavioural biases on corporate decisions making can become something daily?

As behavioural biases touch crucial financial decisions, is there any way to avoid these biases? Can we control the executives, like with the stock-option remuneration, which supposed to keep a CEO focused on the profit maximisation? Is it possible to introduce some sort of regulation to avoid biased decision making?

� Paulina Krawczyk GSEM24

References Allais; 1953; Le comportement de l’homme rationnel devant le risque: critique des postulats et axiomes de l’école Américaine; Econometrica; Vol. 21 (4); pp. 503–546

Allen, Michaely; Payout policy; Handbook of the Economics of Finance, vol. 1; Elsevier; pp. 337-429 (Chapter 7)

Baker, Wurgler; 2013; Behavioral Corporate Finance: An Updated Survey; Handbook of Economics of Finance; Chapter V, Elsevier,

Ben-David, Graham, Harvey; 2007; Managerial Overconfidence and Corporate Polices; National Bureau of Economics Research;

Campbell; 2000; Asset pricing at the millennium; Journal of Finance 55; pp.1515–1567

Chiodo; 2004; Subjective Probabilities: Psychological Theories and Economic Applications; Federal Reserve Bank of St. Louis Review; 86(1); pp. 33-47

Chiodo, Guidolin, Owyang, Shimoji; 2003; Subjective probabilities: Psychological Evidence and Economic Application; Working Paper

Coval, Shumway; 2005; Do Behavioural Biases Affect Prices?; Journal of finance; Vol. IX,No.1;

Deshmukh, Goel, Howe; 2013; CEO overconfidence and dividend policy; Journal of Financial Intermediation; pp. 440-463

Fama, Kenneth; 2004; The capital Asset Pricing Model: Theory and evidence; Journal of Economic Perspectives; vol. 18, no.3; pp. 25-46

Gilson; 1989; Management turnover and Financial Distress; Journal of Financial Economics; Vol. 25; pp. 241-262

Hackbarth; 2009; Determinants of corporate borrowing: A behavioural perspective; Journal of Corporate Finance; Vol. 15; pp. 389-411

Hall, Liebman; 1998; Are CEO’s really paid like bureaucrats?; Quarterly Journal of Economics; pp 653-691

Hall, Murphy; 2000; Optimal exercise prices for executive stock options; American Economic Review; pp 209-2014

Hall, Murphy; 2002; Stock options for undiversifed executives; Journal of Accounting and Economics; pp 3-42

� Paulina Krawczyk GSEM25

Harris, Griffin, Murray; 2008; Testing the limits of optimistic bias: event and person moderators in a multilevel framework; J Pers Soc Psychol; Vol. 95(5); pp. 1225-12237

Heaton; 2002; Managerial Optimism and Corporate Finance; Financial Management; pp. 33-45

Kapla, Klebanov, Sorensen; 2008; Which CEO’s characteristics and abilities matter?; NBER working paper series,

Ljungqvist, Wilhelm; 2005; Does prospect theory explain IPO market behaviour?; Journal of Finance; Vol. 60; pp. 1759-1790

Malmendier, Tate; 2005; CEO Overconfidence and Corporate Investment; The Journal of Finance; Vol. LX, No. 6

Mamendier, Tate; 2005; Does overconfidence affect corporate investment? CEO overconfidence measure revisited; European Financial Management; Vol.11 (5); pp 649-659

Malmendier, Tate; 2008; Who makes acquisitions? CEO Overconfidence and corporate investment; Journal of Finance; Vol. 60; pp. 2661-2700

March, Shapira; 1987; Managerial Plerspectives on Risk and Risk Taking; Management Science; Vol. 33; pp. 1404-1418

Miller, Modigliani; 1961; The Journal of Business; Vol. 34; pp. 411-433

Moore, Healy; 2007; The trouble with overconfidence; Working Papers; Ohio State University;

Oechssler, Roider, Schmitz; 2009; Cognitive abilities and behavioural biases; Journal of Economic Behavior & Organization; Vol. 72; pp. 147–152

Otto; 2014; CEO Optimism and Incentive Compensation; Working Papers; HEC Paris

Oskamp, 1965; Overconfidance in case-study judgements; Journal of consulting psychology studies; Vol. 29, no.3; pp. 261-265

Robin; 1999; Risk Aversion and Expected-Utility Theory: A Calibration Theorem; Working Paper; Department of Economics University of California – Berkeley

Roll; 1986; The Hubris Hypothesis of Corporate Takeovers; The Journal of Business; Vol. 59; No. 2, Part 1; pp. 197-216

� Paulina Krawczyk GSEM26

Schneider, Spalt; 2010; Acquisition as lotteries: Do managerial gambling attitudes influence takeover decision?; Working paper; University of Mannheim

Shefrin, Statman; 1994; Behavioural Capital Asset Pricing; Journal of Finance and Quantitative Analysis; Vol. 29, Issue 3; pp. 323-349

Smith; 1776; Wealth of Nations;

Statman, Kenneth, Fisher, Anginer; 2008; Affects in a Behavioural Asset-Pricing Model; Financial Analyst Journal; Vol. 64 Issue 2

Svenson;1981; Are we all less risky and more skilful than our fellow drivers; Acta Psychological 47, pp. 143-148

Taylor, Brown; 1988; Illusion and well-being. A social psychological perspective on mental health; Psychological Bulletin; Vol. 103; pp. 193-210.

Tversky, Kahneman; 1974; Judgement under Uncertainty: Heuristics and Biases; Science, New Series; Vol. 185; pp. 1124-1131

Weinstein; 1980; Unrealistic optimism about future life events; Journal of Personality and Social Psychology; Vol. 39; pp. 806 – 820.

http://www.cfosurvey.org/2015q3/Q3-2015-US-KeyNumbers.pdf

� Paulina Krawczyk GSEM27

![HIGH PERFORMANCE COMPUTING BACHLOR OF ENGINNERING… · 2018. 8. 26. · HIGH PERFORMANCE COMPUTING BACHLOR OF ENGINNERING[BE COMP] PUNE VIDYARTHI GRIHA’S COLLEGE OF ENGINEERING,](https://img.pdfslide.us/doc/110x75/61026f65a6c021020045cfea/high-performance-computing-bachlor-of-enginnering-2018-8-26-high-performance.jpg)