Embed Size (px)

DESCRIPTION

Strategic Management Accounting Document

Citation preview

TEMBABA 382T--Managerial Accounting

Syllabus

Spring 2004

Professor: Robert G. MayOffice: CBA 3.412APhone: (512) 471-5155FAX: (512) 471-3904E-Mail: [email protected] Meeting Times: Per the course summary

BA 382T Syllabus 2

Course Information

Overview Any organization’s long-term competitive success is critically dependent on (1) the quality of information about its products, services, processes, organizational units, suppliers, and customers, (2) its ability to act [rationally] on that information, and (3) its ability to control its performance consistent with that information. The term managerial accounting refers to the set of information concepts, models and systems that provide this information and control for managers. This course will introduce the student to the modern concepts of managerial accounting. The main objectives are to:

Consider the cost and performance information necessary for long-term success in various competitive environments.

Develop a framework for utilizing information generated by managerial information systems for tactical and strategic decisions.

Consider the current and emerging practices in cost management. Evaluate the many methods developed by firms for decentralizing

and controlling large organizations.

Topics The following key topics will be emphasized:

Designing managerial information systems to support an organization’s strategy.

The limitations of traditional costing systems. Activity-based costing and activity-based management. Management of capacity costs. Revenue-cost behavior and cost-volume-profit analysis. Relevant costs and relevant revenues in business decisions. Performance evaluation Decentralization and transfer pricing. Management control and control systems.

Teaching Materials

Teaching materials include a mix of case studies, articles, and a textbook.

The textbook is Managerial Accounting, by Ronald W. Hilton, Fifth Edition, McGraw Hill, 2002.

Additional teaching materials will be distributed at least ten days prior to the relevant class session.

Class Organization

In this class, we will follow a modified case-method style, which I have found to be most effective for executives who must learn technical content and apply it in a managerial context. The modified case method relies heavily on class participation, but with more guidance through specific

BA 382T Syllabus 3

questions than the pure case method.

Students will be active participants in case discussions, providing summaries of issues, analyses, and recommendations. This involves the preparation of the case and reading assignments before class and the active sharing of your insights during class. My role is primarily to facilitate your analysis and discussion. Note that many of the managerial problems we will address through cases will not have clear-cut or "correct" solutions; do not let this discourage you.

To prepare for class, you must read the assigned readings carefully and understand the accounting techniques described in them. You must also attempt to answer all of the case questions in your own way in advance so that you will be prepared for class discussion and will “learn by doing.” This is essential when specific technical knowledge has a bearing on solutions to managerial decisions. Do not obsessively pursue the right answer or format your preparations to look nice. Such pursuits will waste your time and contribute nothing.

Policy on Scholastic Dishonesty

The McCombs School of Business has no tolerance for acts of scholastic dishonesty. The responsibilities of both students and faculty with regard to the Honor System have been described to you by the Executive MBA staff. You have embarked on a first-class MBA experience and an MBA degree will be awarded to you individually upon completion. One of the faculty’s responsibilities is to assess the achievements of each member of the class and ensure that all who receive credit, a particular grade and/or the degree itself have accomplished what such recognition implies. These standards are essential not only to the maintenance of the academic integrity of the program but also its brand equity, an important part of its value to all graduates.

Academic integrity requires that all work graded in the course, including cases and examinations, be done and submitted individually, except work explicitly described as group assignments.

You should not ask other members of the class specifically what they wrote for a part of an assignment, share electronic versions of your write-ups and analyses or have one group member type the solution and share the document, electronic or otherwise, with the other members. Doing so is not only an act of academic dishonesty, but significantly reduces the learning experience in the course.

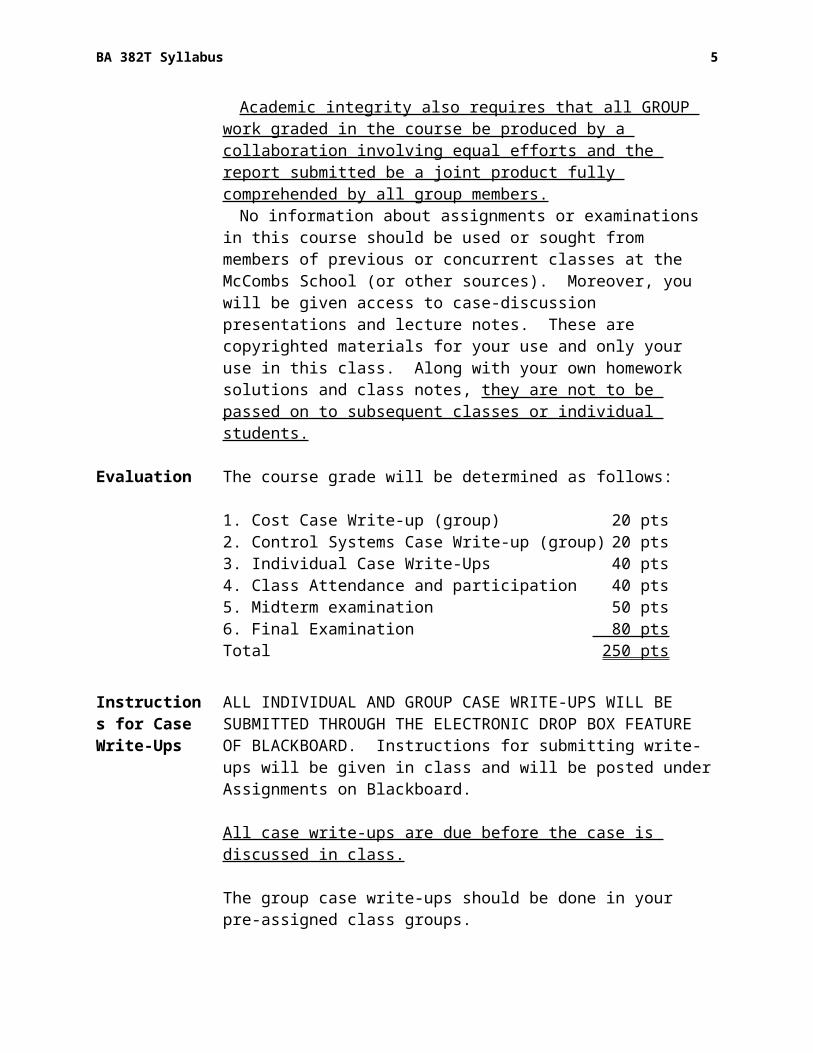

Academic integrity also requires that all GROUP work graded in the course be produced by a collaboration involving equal efforts and the report submitted be a joint product fully comprehended by all group members.

No information about assignments or examinations in this course should be used or sought from members of previous or concurrent classes at the McCombs School (or other sources). Moreover, you will be given access to case-discussion presentations and lecture notes. These are copyrighted

BA 382T Syllabus 4

materials for your use and only your use in this class. Along with your own homework solutions and class notes, they are not to be passed on to subsequent classes or individual students.

Evaluation The course grade will be determined as follows:

1. Cost Case Write-up (group) 20 pts2. Control Systems Case Write-up (group) 20 pts3. Individual Case Write-Ups 40 pts4. Class Attendance and participation 40 pts5. Midterm examination 50 pts6. Final Examination 80 ptsTotal 250 pts

Instructions for Case Write-Ups

ALL INDIVIDUAL AND GROUP CASE WRITE-UPS WILL BE SUBMITTED THROUGH THE ELECTRONIC DROP BOX FEATURE OF BLACKBOARD. Instructions for submitting write-ups will be given in class and will be posted under Assignments on Blackboard.

All case write-ups are due before the case is discussed in class.

The group case write-ups should be done in your pre-assigned class groups.

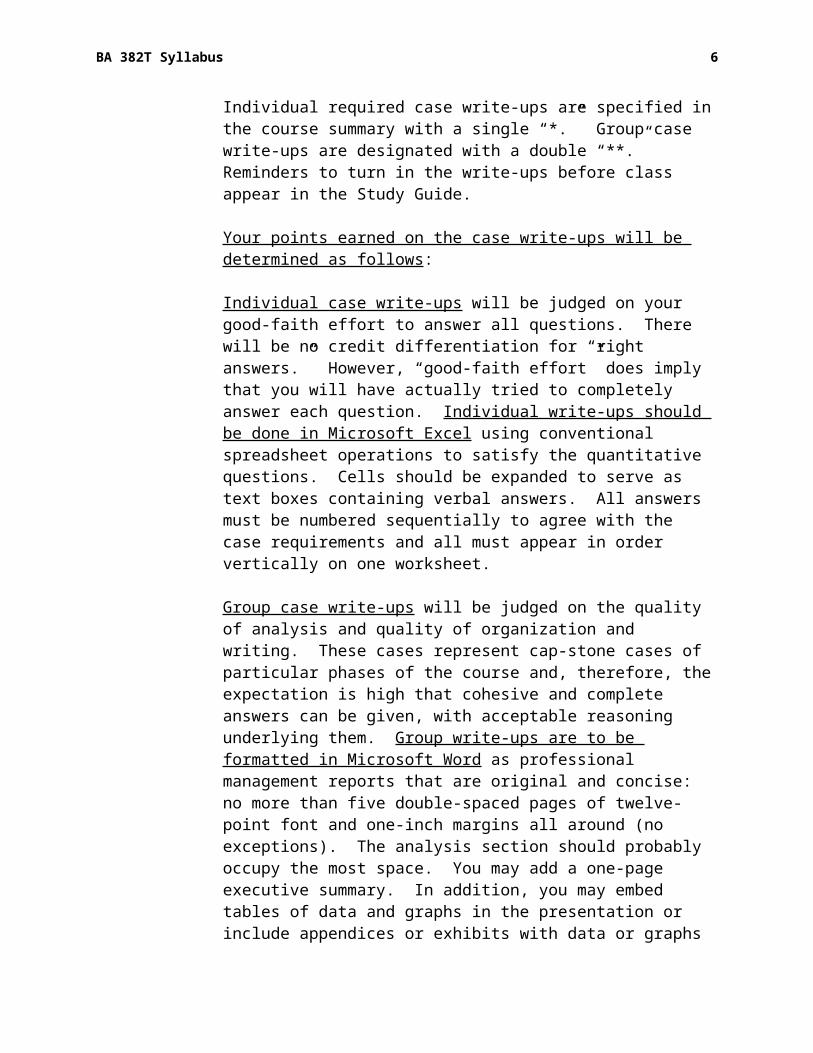

Individual required case write-ups are specified in the course summary with a single “*.” Group case write-ups are designated with a double “**.” Reminders to turn in the write-ups before class appear in the Study Guide.

Your points earned on the case write-ups will be determined as follows:

Individual case write-ups will be judged on your good-faith effort to answer all questions. There will be no credit differentiation for “right answers.” However, “good-faith effort” does imply that you will have actually tried to completely answer each question. Individual write-ups should be done in Microsoft Excel using conventional spreadsheet operations to satisfy the quantitative questions. Cells should be expanded to serve as text boxes containing verbal answers. All answers must be numbered sequentially to agree with the case requirements and all must appear in order vertically on one worksheet.

Group case write-ups will be judged on the quality of analysis and quality of organization and writing. These cases represent cap-stone cases of particular phases of the course and, therefore, the expectation is high that cohesive and complete answers can be given, with acceptable reasoning underlying them. Group write-ups are to be formatted in Microsoft Word as professional management reports that are original and concise: no more than five double-spaced pages of twelve-point font and one-inch margins all around (no

BA 382T Syllabus 5

exceptions). The analysis section should probably occupy the most space. You may add a one-page executive summary. In addition, you may embed tables of data and graphs in the presentation or include appendices or exhibits with data or graphs (in which case they should not require significant separate analysis by the reader).

Midterm Exam In-class, four hours (or less)

Final Exam In-class, four hours (or less)

BA 382T Syllabus 6

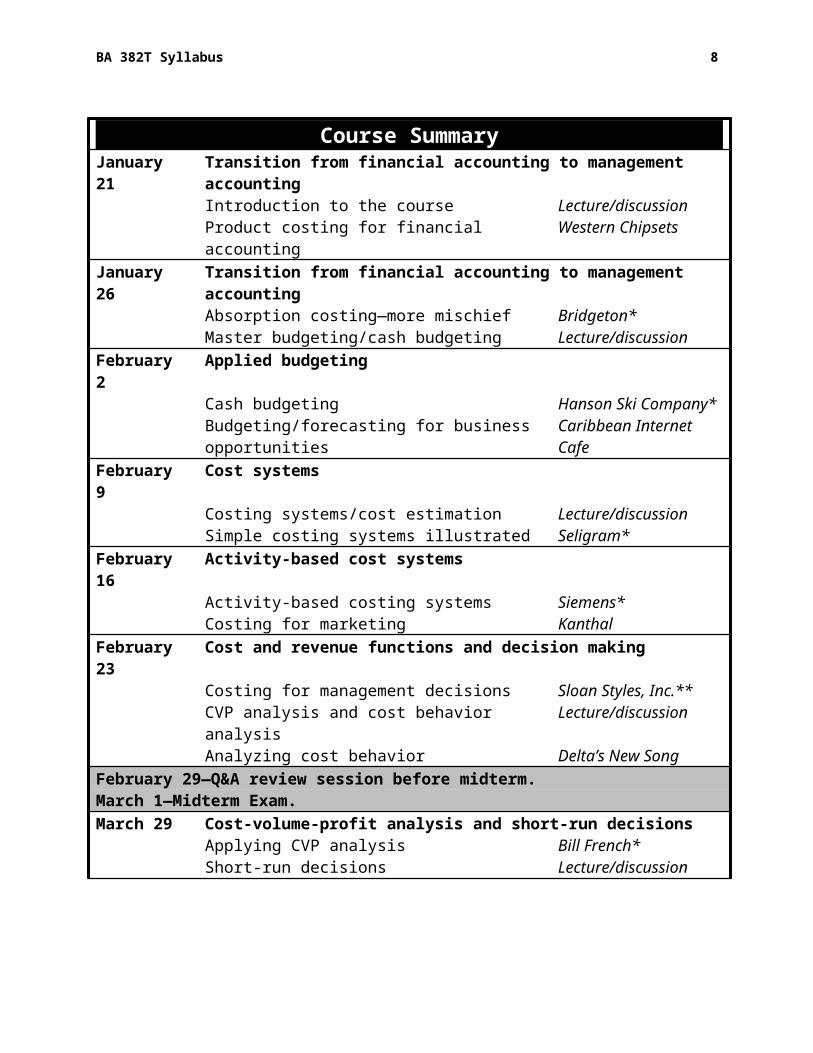

Course SummaryJanuary 21 Transition from financial accounting to management accounting

Introduction to the course Lecture/discussionProduct costing for financial accounting Western Chipsets

January 26 Transition from financial accounting to management accountingAbsorption costing—more mischief Bridgeton*Master budgeting/cash budgeting Lecture/discussion

February 2 Applied budgetingCash budgeting Hanson Ski Company*Budgeting/forecasting for business opportunities Caribbean Internet Cafe

February 9 Cost systemsCosting systems/cost estimation Lecture/discussionSimple costing systems illustrated Seligram*

February 16 Activity-based cost systemsActivity-based costing systems Siemens*Costing for marketing Kanthal

February 23 Cost and revenue functions and decision makingCosting for management decisions Sloan Styles, Inc.**CVP analysis and cost behavior analysis Lecture/discussionAnalyzing cost behavior Delta’s New Song

February 29—Q&A review session before midterm.March 1—Midterm Exam.March 29 Cost-volume-profit analysis and short-run decisions

Applying CVP analysis Bill French*Short-run decisions Lecture/discussion

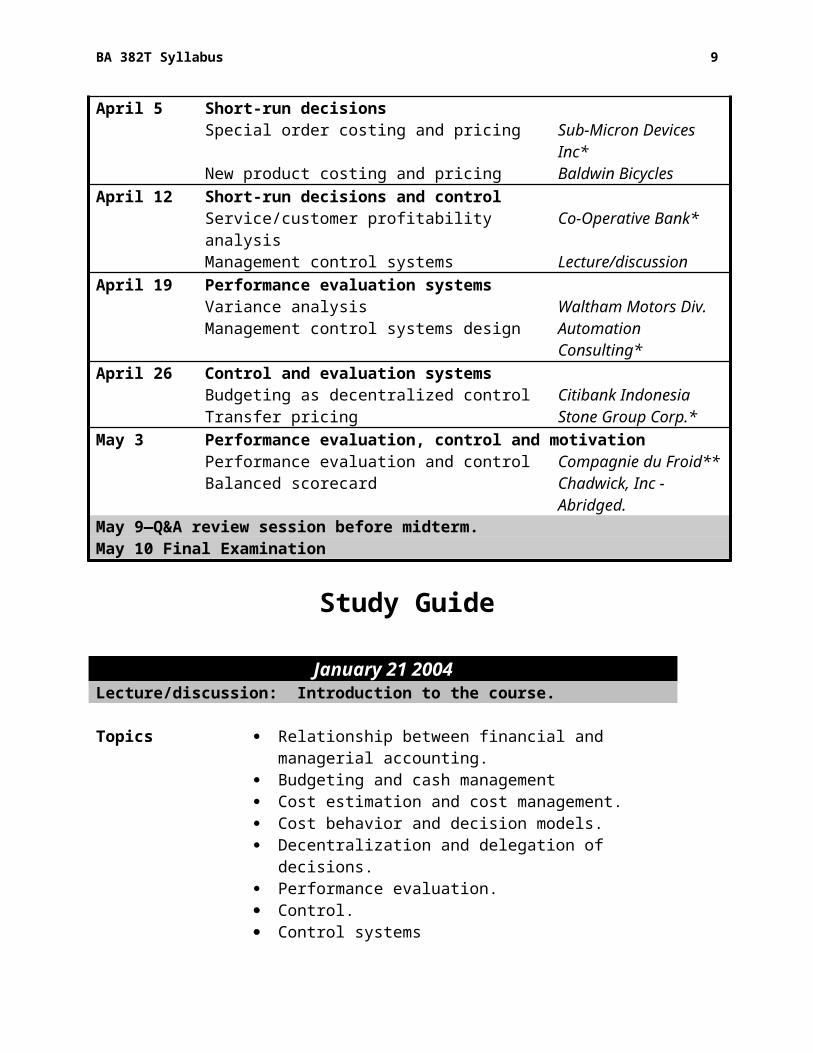

April 5 Short-run decisionsSpecial order costing and pricing Sub-Micron Devices Inc*New product costing and pricing Baldwin Bicycles

April 12 Short-run decisions and controlService/customer profitability analysis Co-Operative Bank*Management control systems Lecture/discussion

April 19 Performance evaluation systemsVariance analysis Waltham Motors Div.Management control systems design Automation Consulting*

April 26 Control and evaluation systemsBudgeting as decentralized control Citibank IndonesiaTransfer pricing Stone Group Corp.*

May 3 Performance evaluation, control and motivationPerformance evaluation and control Compagnie du Froid**Balanced scorecard Chadwick, Inc -Abridged.

May 9—Q&A review session before midterm.May 10 Final Examination

BA 382T Syllabus 7

Study Guide

January 21 2004Lecture/discussion: Introduction to the course.

Topics Relationship between financial and managerial accounting. Budgeting and cash management Cost estimation and cost management. Cost behavior and decision models. Decentralization and delegation of decisions. Performance evaluation. Control. Control systems

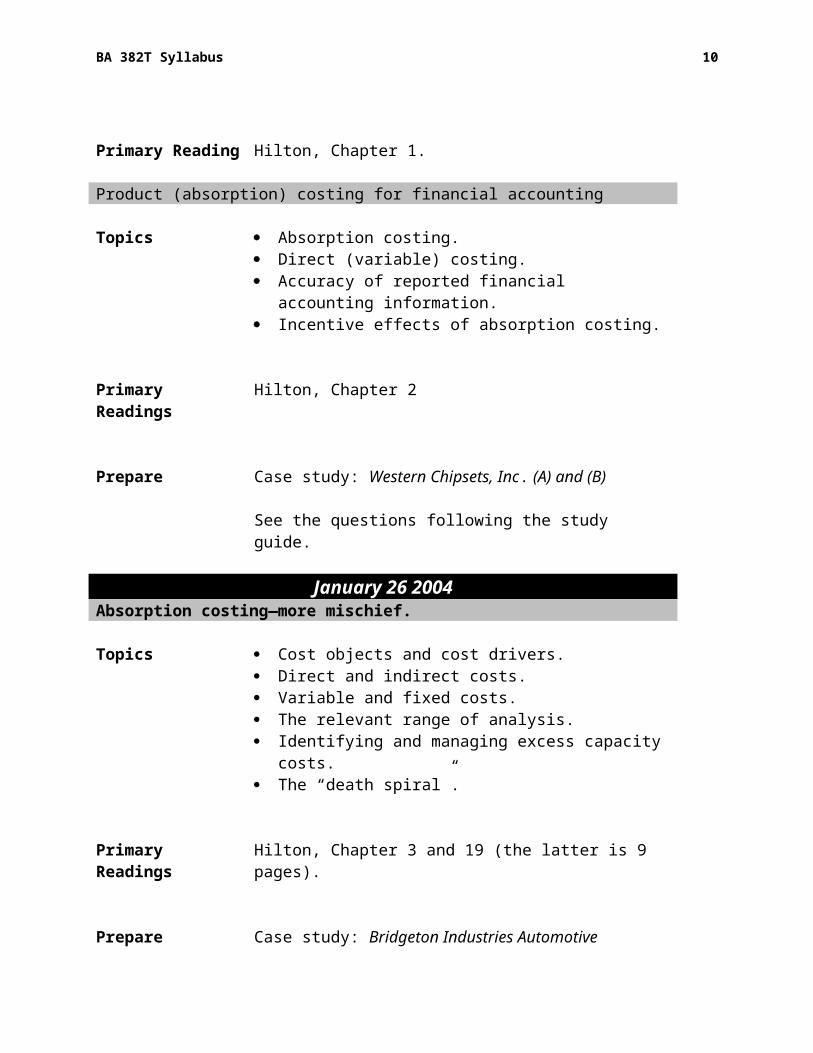

Primary Reading Hilton, Chapter 1.

Product (absorption) costing for financial accounting

Topics Absorption costing. Direct (variable) costing. Accuracy of reported financial accounting information. Incentive effects of absorption costing.

Primary Readings Hilton, Chapter 2

Prepare Case study: Western Chipsets, Inc. (A) and (B)

See the questions following the study guide.

January 26 2004Absorption costing—more mischief.

Topics Cost objects and cost drivers. Direct and indirect costs. Variable and fixed costs. The relevant range of analysis. Identifying and managing excess capacity costs. The “death spiral”.

Primary Readings Hilton, Chapter 3 and 19 (the latter is 9 pages).

BA 382T Syllabus 8

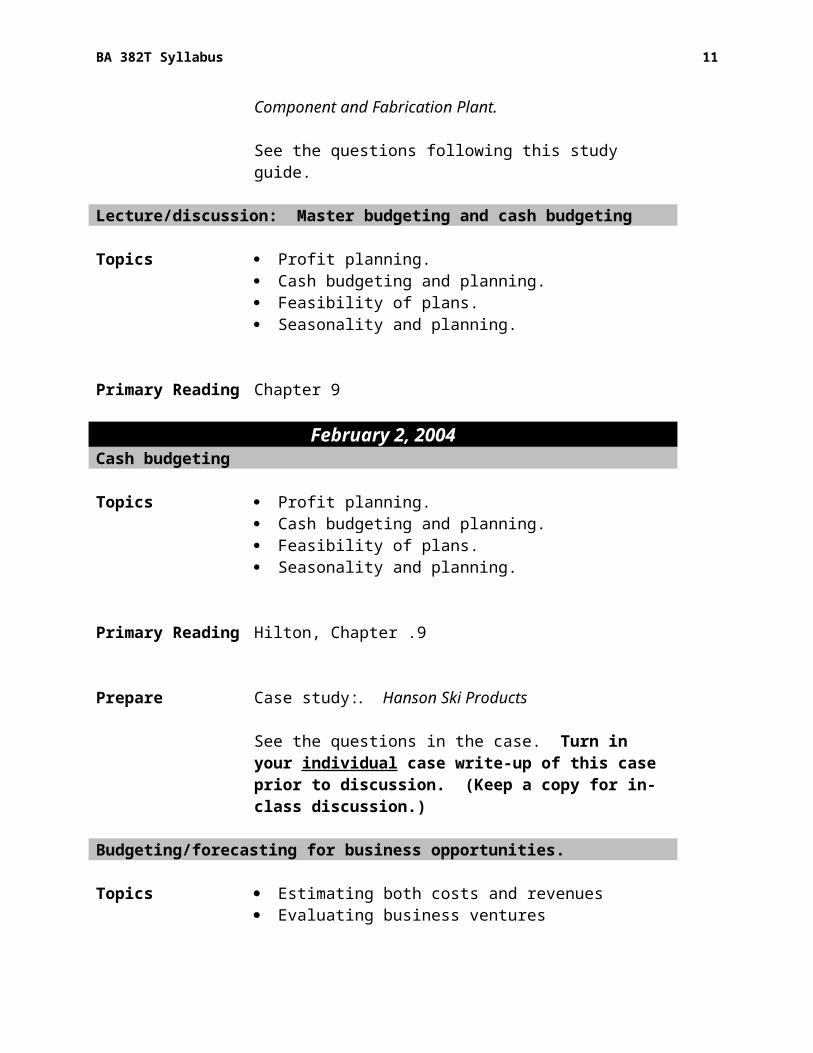

Prepare Case study: Bridgeton Industries Automotive Component and Fabrication Plant.

See the questions following this study guide.

Lecture/discussion: Master budgeting and cash budgeting

Topics Profit planning. Cash budgeting and planning. Feasibility of plans. Seasonality and planning.

Primary Reading Chapter 9

February 2, 2004Cash budgeting

Topics Profit planning. Cash budgeting and planning. Feasibility of plans. Seasonality and planning.

Primary Reading Hilton, Chapter .9

Prepare Case study:. Hanson Ski Products

See the questions in the case. Turn in your individual case write-up of this case prior to discussion. (Keep a copy for in-class discussion.)

Budgeting/forecasting for business opportunities.

Topics Estimating both costs and revenues Evaluating business ventures

Primary Reading Hilton, Chapter 7.

Prepare Case study: Caribbean Internet Café.

See the questions following the study guide.

BA 382T Syllabus 9

February 9 2004Lecture/discussion: Costing systems/cost estimation.

Topics Cost estimation and cost management. Two-stage structure of costing systems. Selection of Cost Drivers. Failure of traditional costing systems.

Primary Readings Hilton, Chapter 3

John K. Shank and Vijay Govindarajan, “The Perils of Cost Allocation Based on Production Volumes,” Accounting Horizons, December 1988, pp. 71-79.

Simple costing systems illustrated.

Topics Cost estimation and cost management. Two-stage structure of costing systems. Selection of Cost Drivers. Failure of traditional costing systems.

Primary Readings Same as above

Prepare Case study: Seligram, Inc.: Electronic Testing Operations.

See the questions following the study guide. Turn in your individual case write-up of this case prior to discussion. (Keep a copy for in-class discussion.)

February 16 2004Activity based costing systems.

Topics Activity-based costing. Activity drivers. Cost drivers. Differences from and advantages over “traditional” costing

systems. Hierarchy of activities. Designing activity-based-costing systems.

Primary Readings Hilton, Chapter 5.

BA 382T Syllabus 10

Prepare Case study: Siemens Electric Motor Works (A).

See the questions following the study guide. Turn in your individual case write-up of this case prior to discussion. (Keep a copy for in-class discussion.)

Costing for marketing.

Topics Analysis of General, Selling, and Administrative expenses. Customer profitability analysis.

Primary Readings Rick Brooks, “Unequal Treatment: Alienating Customers Isn’t Always a Bad Idea, Many Firms Discover,” The Wall Street Journal, January 1, 1999, p. A1+.

Werner Reinartz and V. Kumar. “The Mismanagement of Customer Loyalty,” Harvard Business Review, July 2002, pp. 86-94.

Prepare Case study: Kanthal (A).

See the questions following the study guide.

February 23 2004Costing for management decisions.

Topics The business value chain. Managing the profitability of products and channels.

Primary Reading Gary Cokins, “Measuring Costs Across the Supply Chain” Cost Engineering, October 2001, pp. 25-31.

Prepare Case study: Sloan Styles, Inc.

See the questions in the case. Turn in your group case write-up of this case prior to discussion. (Keep a copy for in-class discussion.)

Lecture/Discussion: Cost-volume-profit analysis and cost behavior analysis

Topics Variable and fixed costs.

BA 382T Syllabus 11

The break-even point. Introduction to cost-volume-profit (CVP) analysis. CVP Analysis with income taxes. CVP Analysis with multiple products. Estimating cost behavior patterns.

Primary Reading Hilton, Chapter 8.

Analyzing cost behavior

Topics Variable and fixed costs. Engineering method of estimate The high-low data analysis method Regression analysis

Primary Reading Hilton, Chapters 7 & 8.

Prepare Case study: Delta’s New Song

See the questions in the case.

Expectations for the midterm exam

Topics All of the above

March 29, 2004Applying cost-volume-profit analysis

Topics Variable and fixed costs. The break-even point. Introduction to cost-volume-profit (CVP) analysis. CVP Analysis with income taxes. CVP Analysis with multiple products. Analysis with constrained capacity. Analysis with uncertainty.

Primary Reading Hilton, Chapters 7 & 8.

Prepare Case study:. Bill French, Accountant

See the questions in the case. Turn in your individual case

BA 382T Syllabus 12

write-up of this case prior to discussion. (Keep a copy for in-class discussion.)

Lecture/Discussion: Short run decisions.

Topics Marginal costing. Relevant costs Avoidable costs Flexible budgets

Primary Reading Hilton, Chapter 14.

April 5, 2004Special order costing and pricing.

Topics Quantifying effects of decisions. Relevant costs and revenues. Appropriate costing and pricing. Issues in accepting special orders. Implications for existing sales, costs and revenues.

Primary Reading Hilton, Chapter 14.

Prepare Case study:. Sub-Micron Devices

See the questions following the study guide. Turn in your individual case write-up of this case prior to discussion. (Keep a copy for in-class discussion.)

New product line costing and pricing.

Topics Quantifying effects of decisions. Relevant costs and revenues. Appropriate costing and pricing. Issues in accepting major customer relationship. Implications for existing sales, costs and revenues.

Primary Reading Hilton, Chapter 14.

Prepare Case study:. Baldwin Bicycles

BA 382T Syllabus 13

See the questions in the case.

April 12, 2004Service/customer profitability analysis

Topics Relevant costs and revenues. Appropriate costing and pricing. Product-line contribution to profitability. Customer contribution to profitability. Strategy for customer profitability.

Primary Reading Hilton, Chapter 14 (review), Chapter 12.

Prepare Case study:. Co-Operative Bank

See the questions following the study guide. Turn in your individual case write-up of this case prior to discussion. (Keep a copy for in-class discussion.)

Lecture/Discussion: Management control systems

Topics Standard Costing. Flexible Budgets. Responsibility Accounting. Decentralization. Controlling investment centers. Financial controls versus management controls. Balanced scorecards.

Primary Reading Skim Hilton, Chapters 10-13.

April 19, 2004Variance analysis

Topics Responsibility accounting. Cost analysis. Variance calculation. Variance analysis.

Primary Reading Hilton, Chapter 10 and 11.

BA 382T Syllabus 14

Prepare Case study:. Waltham Motors Div.

See the questions in the case.

Management control systems design

Topics Performance measurement. Responsibility centers. Growth and creativity—incentives versus constraints. Control systems. Levers of control.

Primary Reading Hilton, Chapter 12.

Robert Simons, “Control in an Age of Empowerment,” Harvard Business Review OnPoint, 2000.

Prepare Case study:. Automation Consulting

See the questions following the study guide. Turn in your individual case write-up of this case prior to discussion. (Keep a copy for in-class discussion.)

April 26, 2004Budgeting as decentralized control

Topics Budgeting in global organizations. International issues in managerial accounting.

Primary Reading Review Hilton, Chapters 9 and 11.

Prepare Case study:. Citibank Indonesia

See the questions following the study guide.

Transfer pricing

Topics Decentralization. Optimal decisions for the organization as a whole.

BA 382T Syllabus 15

Transfer prices for managing decentralization.

Primary Reading Hilton, Chapter 13.

Prepare Case study:. Stone Group Corp.

See the questions following the study guide. Turn in your individual case write-up of this case prior to discussion. (Keep a copy for in-class discussion.)

May 3, 2004Performance evaluation and control

Topics Variance investigation for cost management and control. Transfer pricing Problems in performance evaluation

Primary Reading Review Hilton, Chapter 13.

Prepare Case study:. Compagnie du Froid

See the questions following the study guide.Turn in your group case write-up of this case prior to discussion. (Keep a copy for in-class discussion.)

Balanced scorecard

Topics Management controls versus financial controls. Balanced scorecard.

Primary Reading Robert Kaplan and David Norton, “The Balanced Scorecard – Measures that Drive Performance,” Harvard Business Review OnPoint, 2000.

Robert Kaplan and David Norton, “Putting the Balanced Scorecard to Work,” Harvard Business Review OnPoint, 2000.

Prepare Case study:. Chadwick, Inc -Abridged

See the questions following the study guide.

BA 382T Syllabus 16

Questions for Case AnalysisWestern Chpsets (A) and (B)

1. (A)—come up with as many potential solutions to the problem of making up an approximate $2 million profit short-fall as you can. Comment on their probable feasibility.

2. (B)—analyze the solution put forth by the controller and show how it generates over $9 million in additional profit without the sale of one unit more than expected in December.

Bridgeton Industries Automotive Component and Fabrication Plant.

1. The overhead allocation rate used in the 1987 model-year strategy study at the ACF was 435% of direct labor cost. Calculate the overhead allocation rate using the 1987 model year budget. Why do you get different numbers?

2. Calculate the overhead allocation rate for each of the model years, 1988 through 1990. Are the changes since 1987 in overhead allocation rates significant? Why have these changes occurred?

3. Consider two products in the same product line:

Product 1 Product 2

Expected selling price $ 62 $ 54

Standard material cost 16 27

Standard labor cost 6 3

Calculate the expected gross margins as a percentage of selling price on each product based on the 1988 and 1990 model year budgets assuming selling price and material and labor cost do not change from standard.

4. Are the product costs reported by the cost system appropriate for use in the strategic analysis?

5. Assume that the selling prices, volumes, and material costs for the 1991 model year will not change for fuel tanks and doors produced by the ACF of Bridgeton Industries. Assume also that if manifolds are produced, their selling prices, volume, and material costs will not change either.

a) Prepare an estimated model year budget for the ACF in 1991,

i) if no additional products are dropped;

ii) if the manifold line is dropped.

Explain any additional assumptions you make in preparing your estimated model-year budgets.

b) What will be the overhead allocation rate under the two scenarios?

BA 382T Syllabus 17

6. Would you outsource manifolds from the ACF in 1991? Why or why not? What other information would you want before reaching a final decision?

Caribbean Internet Café

1. Prepare revenue and cost estimates for the Internet Café proposal using the information in the case for each of the three forecasting scenarios. Support your estimates of revenues and costs with appropriate back-up calculations.

2. Prepare an analysis of annual net income and net cash flows from your estimates.

3. Does your analysis imply a clear “go” or “no go” decision? Why or why not?

4. How would you resolve the decision situation? What’s your “call.”

Seligram, Inc.: Electronic Testing Operations.

1. What caused the existing system at ETO to fail?

2. Calculate the reported costs of the five components described as computed by

a. the existing system;

b. the system proposed by the accounting manager;

c. the system proposed by the consultant.

3. Which system is preferable? Why?

4. Would you recommend any changes to the system you prefer? Why?

5. Would you treat the new machine as a separate cost center or as part of the main test room?

Siemens Electric Motor Works (A).

1. Calculate the cost of the five orders in Exhibit 4 under the traditional and new cost systems. Hint: First calculate the revised cost of processing an order and handling a special component.

2. Calculate traditional and revised costs for each order if 1 unit, 10 units, 20 units, or 100 units are ordered. Graph the product costs against volume ordered.

3. Does the new cost system support the strategy of the firm in ways that the traditional system cannot? Is Mr. Karl-Heinz Lottes overestimating the value of the new cost system?

Kanthal (A).

1. Why have selling and administrative costs not traditionally been traced to individual products and customers?

2. Evaluate the approach taken at Kanthal to compute the profit of individual orderlines, including assigning S&A costs to each customer order. How were the costs of customer orders and of producing non-stocked items estimated?

BA 382T Syllabus 18

3. Consider a product-line with 50% gross margins (after subtracting volume-related expenses from prices). The cost for handling an individual customer order is SEK 750, and the extra cost to handle a production order for a non-stocked item is SEK 2,250.

(a) Compare the operating profits and profit margins of two small orders, both for SEK 2,000. One order is for a stocked item, and the other order is for a non-stocked item.

(b).Compare the operating profits and profit margins for two large customers. Customers A and B both purchased SEK 160,000 worth of products this year. Customer A placed just three orders, for three different non-stocked items. Customer B placed 28 orders — 6 for stocked items, and 22 for non-stocked items.

4. What should Ridderstrale do about the large number of unprofitable customers revealed by the account management system? Should salespersons be allowed to accept an unprofitable order from a customer?

Sub-Micron Devices

1. Compute the cost assigned under the present costing system to one ASIC (application-specific integrated circuit) chip produced for transfer internally to the Systems Division. Show each element of production cost assigned by the system. [Note that one silicon wafer produces 100 ASIC chips.]

2. Calculate the annual incremental contribution to profits of accepting the Western Digital offer.

3. Based on contribution to profits alone, should Sub-Micron accept the offer? Why?

4. What other considerations should enter into this decision and what are their implications for Sub-Micron?

5. On balance, what do you recommend that Sub-Micron do with the Western Digital offer? Explain your position.

6. We can infer from the case that practical capacity of the ASIC production facility is approximately 13,600,000 chips of the internal-transfer (Systems) type (from page 1: 16 million systems-type chips with an 85% yield). Re-compute the cost of an ASIC chip for internal transfer to the Systems Division if an appropriate amount of cost is assigned to excess capacity.

7. Comment on the consequences of taking idle capacity into account, given Sub-Micron’s transfer pricing policy.

The Co-Operative Bank.

1. What were the main characteristics of the costing system used by the Co-Operative Bank before the Project Sabre study was launched? What were the system’s strengths and weaknesses?

2. Evaluate the Co-Operative Bank’s ABC system and its implementation.

BA 382T Syllabus 19

3. Should the Co-Operative Bank phase out Independent Financial Advice / Insurance and Pathfinder products?

4. What does customer profitability add to the product profitability analysis? How can the information on customer profitability be used to improve the bank’s financial condition?

5. What should be done with customers identified as unprofitable?

6. Should the Marketing Manager concentrate on Visa customers?

7. What differences do you see between applying ABC in a service company setting and in a manufacturing company?

Automation Consulting Services.

1. How should the ACS founders deal with the problems that they have identified? Be as specific as possible in making recommendations for each of the four offices.

2. The object of this case is to get us started thinking about what control systems are and how they operate. Relate the problems (and your solutions) of this case to the Hilton text and the reading by Simons.

Citibank Indonesia.

1. How does the Citibank budgeting process work?

2. Is this a participative budgeting process? Is participative budgeting consistent with decentralized planning?

3. What challenge does Mistri face, and what possibilities are available to him?

4. How should Gibson allocate the $4 million increase in profits that he has committed to?

5. How might Citibank discourage Mistri and other country managers from taking actions to meet their short-term goals at the expense of Citibank’s long-term good?

Stone Group Corp.

1. What is a transfer price and what circumstances make it necessary or desirable for a company to establish transfer prices and policies?

2. What are the major options for calculating transfer prices (bases for transfer pricing policy)?

3. What incentives will the alternative transfer prices provide to sell or not to sell the multimeters to the Industrial Controllers Division?

4. Who set the transfer price in this case? If you were in that person’s position, what transfer price would you set? What are your motives?

5. What overall transfer pricing policy, if any, would be best for Stone Group Corp. Defend you r choice.

BA 382T Syllabus 20

Compagnie du Froid, S.A.

1. In evaluating Spain and France, what, if any, adjustments should be made for the transfer pricing information?

a. Justify your position.b. Revise the actual results for the two regions accordingly (if appropriate).

2. After any appropriate adjustment, analyze the overall performance of the three regions according to the criteria (expressed or implied) in Jacques’ profit planning process.

3. After any appropriate adjustment, do a complete variance analysis and evaluate the performance of the Spanish region from a responsibility accounting perspective.

4. Does Jacques Trumen need a policy on transfer pricing? If so, what should it be?

5. What system do you recommend for use by Jacques to evaluate and reward his regional managers? Justify your recommendation.

6. How do you think that temperature-induced variances should be treated in the evaluation and reward system? Justify your recommendation.

Chadwick, Inc. (abridged)

1. How does the balanced scorecard approach differ from other approaches to performance measurement that we have examined and discussed in other cases? What, if anything, distinguishes the balanced scorecard approach from a “measure everything, and you might get what you want” philosophy?

2. Develop a balanced scorecard for Norwalk Pharmaceutical Division of Chadwick, Inc. What parts of the business strategy that John Greenfield sketched out should be included? Are there any parts that should be excluded or cannot be made operational?

3. What are the scorecard measures that you would use to implement your scorecard in the Norwalk Pharmaceutical Division?

4. What are the new measures that need to be developed, and how would you go about developing them?

5. How would you advise John Greenfield on how to “sell” your balanced scorecard to Chadwick management as a basis for evaluating Norwalk?

6. How would a balanced scorecard for Chadwick, Inc. differ from ones developed for its divisions such as Norwalk?

7. Do you anticipate that there might be major conflicts between divisional scorecards and that of the corporation? If so, should those conflicts be resolved and, if so, how should they be resolved?