Embed Size (px)

Citation preview

Head Office:706/708 Sharda Chambers,New Marine Lines, Mumbai 400020T: +91 22 2200 7318/0607/6360

PuneHotel Swaroop, 4th Floor,Lane No.10, Prabhat Road,Erandawane, Pune 411 004T: +91 020 2566 6932/6060 1005/3292 6341

Bengaluru101, Money Chambers,1st Floor, #6 K.H. Road,Shanthinagar, Bengaluru 560027T: +91 080 4110 5357

DelhiA-4, Westend, Rao Tula Ram Marg, New Delhi 110021T: +91 011 4905 7624

vakils

www.bkkhareco.com

Will the budgetput economic growth

into high gear?

B. K. Khare & Co.Chartered Accountants

BUDGET2016FOR PRIVATE CIRCULATION

B. K. Khare & Co.Chartered Accountants

BUDGET ANALYSIS 2016

This publication is a service to our clients based on a quick appreciation of the budget proposals and must not be regarded as professional advice, authoritative opinion or the sole basis for your decisions. This publication does not constitute an offer or solicitation. For Private Circulation only.

BUDGET ANALYSIS 2016

[02]

Contents

Editorial 03

A Tribute to Mr. B. K. Khare 08

Medley of Budget Poems by Mr. B. K. Khare 09

Bio Sketch by Mr. B. K. Khare 12

If I were the Finance Minister 15

Union Budget 2016 17

Direct Taxes 37

Indirect Taxes 75

B. K. Khare & Co.Chartered Accountants

[03]

Dear Esteemed Reader,

The economic environment in which the Finance Minister rose to present Budget 2016 is challenging both in terms of domestic and global slowdown. A truant monsoon, stressed balance sheets of Corporates, Banks unable to lend, a moribund infrastructure sector, no growth in jobs, weak global demand and stagnating exports – are some of the factors which negatively impacted the domestic economy. The Economic survey states that a percentage point decrease in the world growth rate impacts domestic growth rate by 0.42 percentage. Despite these constraints, the IMF has hailed India as a ‘bright spot’ and our economy is expected to grow at 7.6% per annum in F16 (F15 7.2%). Someone has rightly likened the current economic situation to that prevailing in the second half of the first NDA government term under Atal Behari Vajpayee – GDP growth slackened, Banks were burdened with bad loans, rural economy was distressed and investments came to a grinding to a halt. There were also two positives then and now in the form of a current account surplus and a reined inflation.

The present Budget furthers the theme of consumption driven growth revival and is focussed on high level of public expenditure to stimulate demand with most of it directed towards the rural economy. This has, of course, invited comments of having a political intent with elections in five agrarian States in the offing. MNREGA, rural infrastructure – particularly irrigation, electrification and roads and supporting the ‘Make in India’ mission with a staggering spend in infrastructure (mainly on roads and highways) are the key priorities addressed in the expenditure outlay. The ` 25,000 crore allocated for Bank recapitalisation has been generally regarded as insufficient with the FM clarifying that there will be more allocations made in this direction in the coming years, if required. At the same time, the FM has walked the path of FRBM and boldly stuck to the target of 3.5% fiscal deficit. The number does seem ambitious given the underlying assumptions made in nominal GDP growth (11%), tax and non-tax revenues (to grow by 11.2%) being optimistic

and the full impact of the Pay Commission recommendations not being reflected in the expenditures. The Economic Survey expects real GDP growth to remain almost unchanged at 7-7.75% (8% being achieved in a few years) and this coupled with low inflation makes the nominal GDP growth at 11% a stiff target. The increase in non-tax revenue by ` 37,000 crores on the back of spectrum auctions and disinvestment also seem difficult to achieve given the actual realisations in 2015-16. The Gross Tax receipts are estimated to increase by ` 1.71 lakh crores despite missing the direct tax target by nearly ` 46,000 crores this fiscal. The Budget therefore allows very little room for slippage in both revenues and expenditure which also presupposes that Gods will be kind blessing us with good rains and soft oil prices.

The FM announced that he would be moving away from the distinction between plan and non-plan expenditure which is in keeping with the recommendation of the Rangarajan committee and that the FRBM will also be reviewed by an expert committee to be set up for this purpose.

The tax collections as a percentage of GDP continue to hover around 10% and this ratio seems unchanged for many decades despite the economic boom in India. Moreover the buoyancy in direct tax collections is missing and the share of direct tax collection in total tax revenues also needs a healthy improvement. The desired scenario of direct tax collections constituting the larger proportion of tax revenues, of which personal income tax would comprise a lion’s share is far removed from the prevailing situation. Direct tax revenues today are 55% of total tax revenues with indirect taxes accounting for the balance 45%. The composition of tax revenue is now thus very similar to that of some OECD countries.

The latest available numbers for AY 2014-15 show the total number of assessees as 2.57 crores as compared to 3.41 crores in the immediate previous year. Of this, the number of assessees who file a taxable income of less than ` 5 lacs is 1.97 crores which is more than 76% of the total number of assessees. There are only

BUDGET ANALYSIS 2016

[04]

83,000 tax payers (0.32%) returning an income of more than ` 1 crore who contribute to more than 60% of the personal income tax collection and this is the abysmal statistic in a country which is supposed to have the largest number of millionaires after USA and China. It is an eye-opener on the tax evasion that still prevails in the country and perhaps the reason why the Government has targeted the rich in the tax proposals and why it finds it difficult to raise the exemption limit to ` 5 lakhs which would then leave only a very small number (about 60 lacs) of individual tax payers!

In this background, we can perhaps understand the quandary of the FM and his yielding to the temptation of announcing a special scheme called Income Declaration Scheme, 2016, which he was at pains to clarify is not an amnesty scheme. An opportunity has been given to declare undisclosed income by paying tax and penalty cumulatively of a mere 45% which is less than reasonable to say the least. The presumptive tax net is also proposed to be widened by extending the scheme to professionals and increasing the eligible turnover for business from ` 1 crore to ` 2 crores.

On the individual taxation front, the most debated and controversial proposal is to tax the withdrawal of monies from Provident Fund account for employees, though prospectively, for contributions made after 1 April 2016. This has justifiably raised a furore as this is a fundamental move from EEE to EET without any forewarning. The House Rent deduction has been increased to ` 60,000 from the present ` 24,000 and a small relief to ` 5,000 under section 87A for small tax payers. In the Robin hood spirit, it is proposed to levy an additional surcharge of 3% (taking the surcharge from 12% to 15%) on high tax payers returning income of more than ` 1 crore and tax at a flat rate of 10% on dividend earned in excess of ` 10 lacs.

The FM had declared his intention last year of moving to a corporate tax rate of 25% over a period of 5 years but presently, no reduction is proposed in the rate except a reduction of 1% for

small companies (turnover less than ` 5 crores). An incentive to start-ups is also proposed by way of 100% deduction of profits from 3 out of 5 years which are set-up in April 2016 to March 2019. A phasing out of deduction as indicated earlier in moving towards simplication and certainty has also been announced for among others- accelerated depreciation, R&D and SEZs. Notable amongst the proposals for financial companies is the 5% deduction from income for sticky loan to NBFCs as currently available to Banks and the pass through status for securitisation trusts including those of Asset Reconstruction Companies. A first in the world measure proposed in this Budget is the debut of ‘Google tax’. Foreign digital companies such as Google, Twitter etc will now have to pay a 6% tax on their income from online advertisements in India. This new tax has been called the ‘Equalisation Levy’ on e-commerce companies earning revenues on B2B transactions in the country but who do not have a Permanent establishment in India. There has been an exponential growth in online goods and services in India and since these transactions take place in cyberspace, there is difficulty of locating the transaction and the identity of the taxpayer and therefore taxing these transactions seemed logical.

In our view, the measures to reform tax administration that have been announced in this Budget are path breaking and a boon for all taxpayers. There will be more and more reliance on technology to reduce the interface between the tax payer and tax collector which is the root cause of all tax payer woes. Even assessments will not require personal attendance except in exceptional circumstances. The recent trend of levying penalty and collecting taxes on additions made in assessments in quick succession was becoming backbreaking and imposing a great strain on resources and the financial burden placed almost made it impossible to wait for relief at the appellate stage. A slew of measures in this direction including a requirement to pay a mere 15% of the demand before filing and pendency of first appeal, calibrating the penalties imposable and giving an option to settle disputes through

B. K. Khare & Co.Chartered Accountants

[05]

a new dispute resolution mechanism – The Direct Tax Dispute Resolution Scheme, 2016, are all very welcome and much awaited measures which will restore the faith of the taxpayer in the fairness of administration. The FM also announced that the rules for determining the place of effective management (POEM) and GAAR have both been deferred by a year.

The Modi sarkar is committed to implementation of GAAR from 1 April 2017. It is only hoped that the GAAR proposals are less draconian and carry enough safeguards to prevent undue hardship to the assessee lest this exercise does not suffer the same fate as its earlier avatar.

It was quite surprising to find GST being conspicuously absent in the Budget speech except for a solitary reference as a passing policy intent. For a tax reform which has the potential to be the single-biggest reform India has seen since Independence, it was felt GST was not given its due. To be fair to the FM, he is finding it difficult to push this reform past the last mile i.e. the Rajya Sabha where the Government does not have the numbers.

The FM has identified nine pillars inter-alia agriculture and farmer’s welfare, rural sector with emphasis on rural employment, infrastructure and investment, governance and ease of doing business, that will ‘Transform India’ to the next level. Several proposals on the indirect taxes have been made in the Finance Bill to achieve this objective, few of which are highlighted below:

YY Krishi Kalyan Cess @ 0.5% levied on all taxable services thereby raising the effective rate of tax on services to 15%

YY Service tax exemption for construction of affordable housing up to 60 sq. m. under state and central housing schemes

YY Existing exemption has been removed thereby widening the tax base such as –

Yy Services provided by a senior advocate to an advocate or firm of advocates

Yy A person represented on an arbitral tribunal to an arbitral tribunal

Yy Assignment by the Government of the right to use the radio frequency spectrum and subsequent transfer thereof shall be deemed to be a declared service and hence liable to service tax

YY Indirect Tax Dispute Resolution Scheme proposed whereunder an assessee can put to an end to disputed cases pending before Commissioner (A) by paying disputed tax along with interest and penalty @ 25% of penalty ordered by the adjudicating authority

YY Simplification of provisions relating to reversal of CENVAT credit on inputs/input services used in or in relation to the manufacture of exempted products removed and provision of exempted services

YY Reduction in the rate of interest payable in case of delay in payment of service tax, excise and customs duty

YY Provisions relating to distribution of credit by Input Service Distribution has been extended to outsourced manufacturers also

YY Transactions involving supply of Information Technology Software on a media on which affixing of RSP is obligatory has been exempted from service tax

YY Number of excise returns to be filed by assessee is proposed to be reduced from 27 to 13 (12 monthly returns and an annual return)

YY Infrastructure Cess upto 4% of the assessable value has been levied on specified vehicles

YY Clean Environment Cess (formerly known as Clean Energy Cess) enhanced from ` 200 PMT to ` 400

Two broad areas stand out that failed to receive adequate attention in the budget. The first of these relates to exports. We often forget that the structure of the Indian economy has undergone a metamorphosis in recent times. The economy is no longer insulated as used to be. It is now very much affected by international trends. Unlike

BUDGET ANALYSIS 2016

[06]

in the past, foreign trade – that is imports and exports put together – add upto nearly 42% of the GDP. Examined in this context, the decline exports witnessed in the current year, month after month, is a cause of considerable concern, because even the success of the Make in India campaign will at least partly depend upon the buoyancy of our exports. Unfortunately, for January 2016, they stood at $ 21 billion, as compared to $ 24.39 billion a year ago, and $ 26.75 billion, two years ago. The decline is alarming and currently India is being outperformed by countries like Bangladesh and Vietnam. One critical problem which the country currently faces therefore relates to the revival of the demand for Indian exports. The Business Standard has suggested the setting up of a high level inter-ministerial group to suggest how the competitiveness of Indian exports could be improved. The problem, point out many observers, is that Indian exporters are largely small, and thus do not reap economies of scale, like their counterparts in other countries.

The other big opportunity the country appears to have missed out on relates to tapping of non-tax revenues for growth. The sale of spectrum, it is pointed out, could easily be expedited but has not received the attention it deserves, at least so far. However even more than that, in a country where the informal economy is large and more than 50% of the GDP emanates from the cash economy, much more could have been done to tap resources. Attractive bonds of various kinds could still be raised, so as to reduce pressure of raising revenues through taxes. Many people might still be happy to contribute to infrastructure growth, with low rates of interest provided they are not harassed with regard to the source of their earnings. A lot of non–tax revenues could similarly be raised from non-residents and the diaspora settled abroad. The release of the fiscal pressure would enable the Government to do more for its own honest taxpayers, many of whom diligently pay their own share of taxes year after year.

On its part, the Government has devoted significant attention to the social sector and

promote stimulus in the economy by allocating funds for infrastructure. Some of the key initiatives announced in this regard would include:

YY Giving a statutory backing to AADHAR platform to ensure benefits reach the deserving

YY Provide legal framework for dispute resolution and re-negotiations in PPP projects and public utility contracts

YY ‘Pradhan Mantri Krishi Sinchai Yojana’ to be implemented in mission mode. 28.5 lakh hectares will be brought under irrigation

YY To reduce the burden of loan repayment on farmers, a provision of ` 15,000 crore has been made in the BE 2016-17 towards interest Subvention

YY District Level Committees under Chairmanship of senior most Lok Sabha MP from the district for monitoring and implementation of designated Central Sector and Centrally Sponsored Schemes

YY New health protection scheme will provide health cover up to ` 1 lakh per family. For senior citizens an additional top-up package up to ` 30,000 will be provided

YY ‘National Dialysis Services Programme’ to be started under National Health Mission through PPP mode

YY ‘Stand Up India Scheme’ to facilitate at least two projects per bank branch. This will benefit at least 2.5 lakh entrepreneurs

YY 62 new Navodaya Vidyalayas will be opened

YY Regulatory architecture to be provided to ten public and ten private institutions to emerge as world-class Teaching and Research Institutions

YY GoI will pay contribution of 8.33% for of all new employees enrolling in EPFO for the first three years of their employment

YY To approve nearly 10,000 kms of National Highways in 2016-17

B. K. Khare & Co.Chartered Accountants

[07]

YY Amendments to be made in Motor Vehicles Act to open up the road transport sector in the passenger segment

YY Action plan for revival of unserved and underserved airports to be drawn up in partnership with State Governments

Overall, we feel that it has been a commendable exercise on the part of the FM, doing a tight-rope walk between inclusive growth, public spending, mopping up tax collections, providing stimulus to demand, tax reforms, controlling inflation and reining fiscal discipline. An unenviable job that he has, the FM has shown tremendous teflon-coated resolve to chart the Indian economy on a dynamic growth path and cleanse the system from the scourge of black-money, even if it meant good-riddance of defaulters in the short run. In doing so, he is doing a yeoman service to the current milieu. He is also sparing future generations from a rot that eats India from within. By and large, the reactions to the Budget have been encouraging (especially after the fine print has been combed and recombed). Perhaps, the one from Jim Rogers, the noted Global Investment Guru sums it up succinctly – while welcoming the rightful steps taken to deregulate agriculture and striving to reform the tax bureaucracy, he has exhorted the FM to do more in areas such as ushering land-holding reforms and liberalizing markets further, so as to make India a favoured destination for investments and a better place

to do business in. Firmly placing hope and trust on the Indian story, he says if ever the FM opens the doors to the Indian capital markets fully, he would be the first person to walk in. May the tribe increase!

Mr. B. K. Khare, eminent Chartered Accountant, founder of our firm & my beloved father, left us for the heavenly abode in November 2015, leaving behind a rich legacy and a proud tradition which we dutifully continue as a token of our tribute to the legend, we have collated poems from his erudite & rich collection of Budgetary analysis of yore.

Our detailed analysis of the Direct and Indirect tax proposals is preceded, as in the past, by our analysis of the state of the economy and the economic survey. We trust you will find the publication a useful read.

Sincerely,

Padmini Khare KaickerManaging Partner

B. K. Khare & Co.Chartered Accountants

Date: 1 March 2016

BUDGET ANALYSIS 2016

[08]

A TribuTe To Mr. b. K. KhAre

Mr. B. K. Khare, the founder of our firm made his mark, in his chosen field of taxation, a subject he became passionately fond of.

Mr. B. K. Khare pioneered the practice of commenting on the Budget which he circulated in the form of a cyclostyled booklet, with the tax administrators and teachers as the readers in mind. He was interested in sharing his point of view with the people who mattered, influencing and administering taxation in all its aspects, including teaching, administering and interpreting the income-tax law. Apart from commenting on the taxation laws, he did have many a suggestion, some of them novel, to make to the Finance Minister which he penned under the heading “If I were the Finance Minister....” A blend of imagination, gumption and expertise were applied in coming up with these suggestions which as someone not claiming to be an economist, were unique.

He was a great advocate of the principle of taxing book profits and we are happy to note that the present thinking of simplification, rationalization and doing away with ad-hoc exemptions is in line with his thinking although the ICDS proposed to be enacted detracts from this position.

With a heart which always went out to the underprivileged and the belief that questioned economic inequality, he expressed this sentiment poetically which then became a regular feature in the Budget commentary booklet that was printed.

After leading a fulfilling life of 89 years he passed away peacefully on 15th November. He leaves behind a legacy for us to be proud of and the indelible mark of his personality, style and thinking will be missed by his loyal readers.

“The old order changeth, yielding place to the new” in the inexorable march of time and life but as a tribute to Mr. Khare who eagerly looked forward to pour this thinking in print on paper, we have reproduced snippets from his poems and suggestions and a small bio-sketch which he had penned for a professional journal.

B. K. Khare & Co.Chartered Accountants

[09]

Medley of Budget Poems by Mr. Khare

I am born every year – at times twice a yearLike a phoenix in the whirlwind of time My birthday is on 28th February – 29th February in the leap year Precise timing of my birth depends upon stars Sometimes at 11.00 A.M. sometimes in the evening I represent two sides – receipt and expenditure I am different from family or business budget where expenditure is determined by incomeI do the impossible balancing; I try to reconcile the irreconcilable, Incompatible with compatible and compatible with incompatible My resources are unlimited and the needs and wants are limited I am a mystic and keep everybody guessing except a very few privileged No distinction between capital and revenue I can borrow limitlessly – no matter I borrow even to pay interest and for meeting day to day expenditure I do not worry but at the same time I worry I also do not worry for funding in the name of productive expenditure To create plenty for all Alas! It becomes unproductive What else can happen when my creator has unlimited access to use me as he likes; What with the Mint working overtime.

In my not too distant birthday I will use my powers to destroy the evils and promote goodness and rekindle the man with the right springs to create a just and orderly society.

Sadly, transient parliaments cannot change: the moorings fastened on the constitutionA few wise ones do wade their way through the murk trying their best to do some good. But for all the oppressed and silenced, there is now a chance of better governance. This year, let power of state yield to gandhigiri instead of dadagiri.

What is your vision of India A question I get asked around The Ides of March As histograms and diagnostics of fiscal India Are in the air like pollen In this season A metaphor with another use As there is also heard the buzz of our revenue-gatherers With their sting in proportion to The sweetness of the honey they gather in.

birTh oF A buGDeT

(2002-2003)

GooD GoVerNANCe MAY

hAVe A ChANCe (2009-2010)

BUDGET ANALYSIS 2016

[10]

An aside here about visions. Of what use is a vision The more literal minded of my friends might ask. For that I may use a standard rhetorical feint And throw Indian philosophy at my unsuspecting interlocutors.For in philosophe Indienne Reality is a matter of modulation From an idea to a thing is but Six degrees of separation. Each vision has a place in the emporium of reality Contradictions are but subtleties of understanding. Perhaps it is this cultivated ease with antinomies That helps us live with prosperity and object deprivation Cheek by jowl in such close proximity.

What will it be like 20 years hence? Prediction is a dangerous game Although 20 years seems a safe distance away!

To speak less in jest India will grow rapidly The question is if this will benefit The poorer sections. As even plenty does not promise the Well-being of all As the image of mountainous stocks of food grains Locked in warehouses As people go hungry testify.As Amartyada says Even here democratic IndiaHas prevented faminesBetter than ChinaAs the public airing of grievances makes All voices heard sooner or later.

Farmers commit suicidetrapped in debt beyond redemption, modest it may be economy is shining thriving and glittering, scorching sun is burning down on corpses of the farmers on homeless and bare footed on those wandering in the wilderness foraging for work regardless, of rural guarantee scheme,

A ViSioNArY reCKoNiNG (2006-2007)

B. K. Khare & Co.Chartered Accountants

[11]

the mule of lower middle class harbingers of the unalterable values pride of India bending backwards in their efforts, zealously guarding the values hedged in dollar a day fence witnessing gloom all around’ the cattle like unorganized labour and the forgotten and unemployed the mute sufferers economy is shining.

The Budget is like the libretto of an opera That will be sung on the stage of the unfolding financial year. It will choreograph the dance of money Its ups and downs, full of the Sturm und Drang Of our economic lives. The libretto will be sung into an existence Mellifluous and hectic By the sopranos, the counter tenors – The industrialists, the investors – The prima donnas – The policy-making politicians. The febrile tale of money Will be told through various markers Like the wavering exchange rates, inflation rate Heart stopping news that will then lead We all hope in good Bollywood fashion To the Happy Ending The Holy Grail of low inflation And High Growth. But the economy swaggers and sometimes staggers along Like a scriptless drama quite beyond the control of the Sutradhar. The pundits say the fundamentals are strong There is nothing that can stop in the long term The Great Indian Economic Miracle.

In this Leap Year, Will our Finance Minister take the leap Of the imagination and empathy and financial wizardry That will bottle the genie of inflation And liberate the economic genius of our great Nation? In my long career I have witnessed the coming of age of our economy In the 1950’s there was darkness even at noon. While now even the nights are neon-lit!

DeFiCiTS ShiNiNG

(2007-2008)

ThiS Too WiLL PASS

(2012-2013)

BUDGET ANALYSIS 2016

[12]

Reminiscences as a pRofessionalIT was said by someone that unless a man feels he has a good enough memory, he should never venture to lie. I am not quite sure that I have a very fine memory for events, and I should prefer, as I ordinarily do, to stick to the truth, when I get to reminiscing about my days as a professional. I promise you that there shall be no purple patches in what I shall write about my professional life.

My birthday did not begin with the water birds and the birds of the winged trees flying my name. Oliver Goldsmith’s Vicar of Wakefield has this sentence in its preface: ‘I was ever of opinion that the honest man who married and brought up a large family did more service than he who continued single and only talked of population.’ My father was an honest, virtuous man, with immense faith in values that no longer seem to compel respect, with no greed or envy; I mention these facts here since my parents have been an enduring influence on my life.

I and my brothers broke the age-old tradition of vedic and priestly family tradition. Perhaps my father must have realised that the wealthy, material city like Bombay must have brainwashed us and we might not stand up to the test of a Spartan, which is a bye-product of a dedicated vedic scholar. He always impressed on us that if you digested poverty, it was your best friend, but if you fumed and fretted about it, you were the poorest of the poor in the world. What is more, though I had a personal inclination to become a Sanskrit scholar, my father persuaded me to take the career of a Chartered Accountant. I was greatly influenced by my school Sanskrit teacher, who taught me Sitatyagah, a canto of a great epic, Raghuvansh, written by the peerless, inimitable Kalidasa, which impressed me the most and even today the stanzas are ringing in my ears. Of couse, our great Prime Minister also assures us that like Sitamai, he has or he will come unscathed from the ordeal, without actually going through the fires, which Sitamai went through. I do not know even today what

would have been the right thing for me; but, then again, it is futile to speculate as I had immense faith in my father, my Guru.

I was articled to late K. M. Vartak, a well-known Chartered Accountant of his time and I became a full-fledged professional in the year 1955. I have done not too badly as a professional. When I say this, I am reminded of some words of William Hazlitt, who, no doubt, uttered them in a different context. He said, ‘I make me happy, but wanting that have wanted everything.’ He meant to convey a certain meaning that he intended to, but a great man’s words, like the aphorisms you find in the Gita, are many-splendored things and have several layers of meaning. It seems to me that his words also suggest that man may think that his needs are limited but, when he labours to see that they are satisfied, his needs expand further and he perseveres to fulfil them and a chain reaction sets in and he becomes more and more self-centred. Hazlitt himself says elsewhere, ‘The least pain in our little finger gives us more concern and uneasiness than the destruction of millions of our fellow beings.’

I know that I must avoid the criticism – I mean, your criticism – which Queen Victoria made of the great Gladstone. She said that Gladstone ‘speaks to me as if I was a public meeting.’ My idea is not to suggest that I have a great fund of wisdom to impart to others. On the contrary, I do not pretend that I do not have the failings of the next man. I have no ambition but to share some of my thoughts with you thoughts that cross my mind, when I think of my professional life.

No doubt, when year after year. I was going through the travails of my profession, I had noticed the agonisingly slow pace of wingless, crawling hours. When I started my practice sometime in April 1955, I was on an unchartered sea. Even at the noon, I saw darkness. Opportunities were far and few between and could hardly inform the many who ventured for the first time in the money world. The opportunities grew only with the commencement of industrialisation of India in post sixties. I never lost my courage and with His Grace slowly, steadily but surely I could find

B. K. Khare & Co.Chartered Accountants

[13]

my foot. I chanted with Shelley, ‘If winter comes, can the spring be far behind.’

What I suddenly find is that nearly four decades of professional life have whizzed past me and they stretch before me like a vista, with their moments of unhappiness, moments of hope, moments of achievement and moments of truth.

The first ever early shock I got from the profession was in connection with the audit of a public limited company quoted on the stock exchange and from this shock I have not recovered even to this day. Good faith sometimes makes all, including perhaps Accountants, almost blind. Having discovered that the accounts were a can of worms, I could not certain myself. I was confused and confounded and was at my wits’ end. The qualified report was inescapable. The earlier report given by me was a clean one and hence the predicament. The type of discrepancies I found must have informed the accounts of even the earlier year/s. All sorts of advices were given to me including ignoring my findings; all sorts of influences were extended on me, however, I stuck to my guns in the belief that I have not consciously signed the unworthy accounts of the earlier year, the initial year of the audit. I gave a thumping qualified report and I sought and got the guidance of late B. N. Pardiwala, a very kind person so as to ensure that I did not get imbalanced and crossed the rubicon of auditor’s discipline. I have learnt one thing that the test checks based upon comparative results over the years is no insurance against the dangerous accounts and there is no substitute for intelligent, though selective, routine audit. This was almost a solitary audit then which came to my lot by quirk of fate.

Entry in the tax field was also difficult. But after all waiting is the name of the game. To begin with, I found tax work satisfying, particularly it gave me immense pleasure to argue before the Income Tax Appellate Tribunal. I did reasonably well. For the first time, I propounded the theory that an assessee could claim 100% deduction in case of capital expenditure on scientific research as also investment allowance and form the following

year he can claim depreciation; in all a total deduction at 225%. It was quite a sensational decision then. However, the Madras Special Bench of the Tribunal poured cold water on my theory in that the Bench came to the contrary conclusion. I could persuade the Bombay Bench, which consisted of A. Krishnamoorthi and Nair, when the Madras Bench decision was cited against me to refer to the larger Special Bench, the Bench asked me to show cause why Madras decision required reconsideration at the hands of the larger Special Bench. There and then I could succeed in persuading the Tribunal that Madras Special Bench was not the last word on the subject. The larger Special Bench was constituted in Bombay which upheld my interpretation of the law. I earned the sobriquet of 225, which I did not mind as long as the profession did not call me 420, though it is not perhaps impossible of being dubbed so by the Tax Official! Of course, the Supreme Court has debunked this theory and it thundered that nobody could claim deduction of any expenditure under more than one Section unless the law clearly laid down so and no on the specious plea that such claim for double deduction was not prohibited by the Act.

I feel that I contributed to the development of law modestly though. For example, I again could persuade the Tribunal that initial contribution to Superannuation Fund is to be allowed in his entirety and not in conformity with the Circular of the CBDT which allows initial contribution being scaled down to 80% and being allowed over a period of five years. Submission was simple that what Section 36(1)(iv) gave, the subordinate rule making authority could not deny it. I need not elongate the list.

However, of late, realisation has come that the tax practice only hovers round the distribution of wealth between the State and the subject, without contributing in the process of creation of wealth. I think success of the profession does not depend upon the attesting work nor by doing other regulatory work. To much emphasis on tax practice for the last 40 years has drained the Accountant of his accounting expertise and his

BUDGET ANALYSIS 2016

[14]

tools have become blunted. I sincerely believe that the accountant’s initiative will be hijacked by computer scientists and we will be related to only doing regulatory and statutory work. Given a chance, I will first become an Engineer and then a C.A. This cocktail will go very well as after all the finance and financial figures are reflex of physical inputs and outputs and unless one has the firm grip on these physical factors, one shall not become a good accountant either in the regulatory field or activist in the process of creation of wealth. I am not unware that even without a formal technical background, yet, a trained, experienced and intelligent mind could pick up proper signals.

Our Institute should permit now the mixed conglomeration of Accountants, Engineers, Scientists, actuaries, computer-men and the management experts. Through this synergy, the profession can play a big role and at as a catalyst for creation of wealth. The new economic freedom that has lately dawned on India will tremendously increase the professional opportunities and the limitation, if any, will be our own shortcomings. Despite all these platitudes, it is rather too late for me to play an effective part in this ‘Yagna’ of regenerating Modern India without the vice of prosperous and affluent society. In the meantime, I will continue fiddling with the Department.

As I look back at the past, I find myriad men and isms, ideas and philosophies crowing in on me and I’ll admit to having been influenced by some of them and a shade affected by some others. But I have never held radical views. I believe, with

Franklin D. Roosevelt, that a radical is a man with both feet firmly planted in the air. I have always admired men, who have contributed to the growth of our national wealth. I also believe that our national wealth should be used for promotion of the welfare of our countrymen. I pay homage to the Mahatma, who, unconditionally, thought that the trusteeship principle should apply to the holding and use of our national wealth.

What a miracle if you give more, you get more! My wife is trying to teach me, though I am not sufficiently learning, that wants are limited and resources are unlimited, debunking the whole premises of economic theory and practice. Similarly, she is trying to impress on me that every investment is an expenditure and every expenditure is an investment. Ultimately, it is an attitude of mind. Sometimes, I wonder why there should be want in the world. Has not science and technology advanced enough to unleash the productive forces which will generate unlimited wealth on this Planet which will go round more than needed? But, then, life from life may disappear! The material but the value-based Society perhaps may be the answer.

I will end this write-up, harking back to my father’s remark, ‘My son, still he died’, when I peevishly told him that the neighbour who died yesterday was a millionaire. I think that sums up the philosophy of life.

B. K. KhareChartered Accountant

B. K. Khare & Co.Chartered Accountants

[15]

if i weRe the finance ministeR…For a long time, Mr. B. K. Khare, the visionary that he was, used to run a column titled ‘If I were the Finance Minister’ as part of our Budget Analysis & Presentations. In fact, the origins could be traced, based on material available in our library, from Union Budget 1992-93 and perhaps even before. A man of razor sharp wit, he used to remark of his subjunctive stumper, in a humorous way, saying “My prescription for raising additional revenue will continue to be more or less the same as hitherto as long as I have no opportunity to give it a concrete shape. It will continue to be in the wilderness in the meantime crying for notice”. Some of his ahead-of-the-times thoughts do still ‘cry for notice’, radical yet relevant to this time.

On MiniMuM AlternAte tAxAtiOnMr. Khare’s words were: “I have a dream that one day meaning of income, profits and gains will be the same both for the businessman and for the taxman.” We suggested that the Accounting Standards, unanimously evolved, should be made as part of the Companies Act so that the Accounting standards are as much binding on the corporates as on the auditor, not excluding revenue authorities. It was high time for convergence for evolving uniform principles which will inform all the legislation so that income, profits and gains will not mean different things to different authorities who are entrusted with administering relevant enactments. We are entitled to believe that if what is suggested in the matter of corporate taxation is accepted, statute book will become lean and trim, and therefore, healthy. Several man-hours in the form of human energy could be saved, which could be utilized for productive purposes. A situation like zero tax company will never arise.

That Proposal, This Day

In the recent past, we see some effort towards convergence in the form of ICDS being brought in by the CBDT. However, as Mr. Khare put it, by not

resorting to two different sets of accounts, one for audit and one for tax, we could save precious man-hours and litigation too.

On rAtiOnAlizAtiOn Of tAx exeMptiOnsMr. Khare had, way back in 2005-06, suggested ‘wholesale abolition’ of Chapter VI-A (deductions), various tax concessions bestowed on profits derived from new industrial undertaking and infra projects and the likes. He felt that economic growth of the society was not brought about only through tax breaks, especially in the era of rational and reasonable levels of taxation coupled with congenial atmosphere and business friendly environment of the tax administration. On the contrary, more often than not, such provisions for such incentive deductions brought about distortions, he passionately argued.

That Proposal, This Day

As if paying heed to the departed legend, the present Government has embarked on the phased withdrawal of deductions and exemptions in a phased manner. And this Budget 2016 carries the noble effort forward.

On tAxing AgriculturAl incOMeMr. Khare was particularly sympathetic to the plight of the poor farmer. However, he felt strongly that the story was different in case of farmers who have become agricultural lords and there was no reason why their income was not taxed. He used to lament that the farm lobby of capitalistic farmers was taking advantage of the unfortunate farmers at large who for generations craved for a better life.

That Proposal, This Day

Income-tax continues to be in the Union List, which excludes agricultural income, which falls under the State List and States don’t (read can’t) tax agricultural income. The fact is that the rural rich, wherever they exist, are extremely powerful,

BUDGET ANALYSIS 2016

[16]

much beyond the collective might of political will. So on this count, status quo continues and agricultural income continues to be exempt, as it has been since independence.

On cArry fOrwArd Of Business lOss in cAse Of discOntinued BusinessIf, for any reason, a loss-spewing business is discontinued or abandoned, such loss is not to be allowed for being set-off in the next year against the assessee’s income from other business. Mr. Khare was an ardent believer that there was no sense in this prescription. It should not be the legislative intention that loss-making business should be continued to be carried on by incurring further losses only for being set-off against the profit from any other business. He further felt that the carried forward business loss ought to be set-off against any taxable income (barring speculation one) and not necessarily restricted to business income, of the following year. For that matter, loss under any head other than business ought to be eligible for setting off against any taxable income (speculation excluded) of the following year. He was convinced that the basic tenet was that income, profits and gains are made only when the capital is kept intact.

That Proposal, This Day

Section 72 continues to prohibit carry forward of business loss in case of discontinued business, notwithstanding the counter logic which has been so lucidly expounded by Mr. Khare. Perhaps with changed business scenarios likely to emerge in the immediate future (esp. given the fancied and rampant proliferation of start-ups and volatile economic headwinds), the Government of that day might be forced to rethink on this issue - soon.

On the ‘tOBin’ tAxDrawing inspiration from the Nobel Laureate, Prof. James Tobin, Mr. Khare had suggested that in order to blunt the pernicious effect of flow of

funds world over, some fee could be levied on the spot and speculative forex transactions, in concert with the international community. Another unconventional measure to widen the tax base suggested by Mr. Khare was to impose a moderate levy on the amount of cheques cleared through the Clearing Houses.

That Proposal, This Day

An attempt in this direction has already been made through the levy of securities transaction tax w.e.f. 2004. A simple yet powerful tool for raising significant tax revenue, raising tax based on the amount of cheques cleared has not yet been attempted by the Finance Minister, albeit the banking cash transaction tax was briefly toyed with. However, considering that the BCTT created more problems than solving some, this tax was withdrawn in 2009.

On levy Of ecO tAxMuch before the Governments felt compelled to act (such as the recent odd-even rule in Delhi or shut down of a city as in Beijing), Mr. Khare mooted the idea of an ‘Eco levy’ on those who pollute the atmosphere on some criteria.

That Proposal, This Day

An Eco-tax is an attempt (in the right direction) to make the private parties feel the social burden of their actions. We feel that it is simply a matter of time before the Government is compelled to take drastic step such as the Eco-tax so passionately put forth by Mr. Khare. Other countries have already done so, in some form or other. For instance, the Netherlands, Portugal, Canada, Spain and Finland have introduced differentiations into their car registration taxes to encourage car buyers to opt for the cleanest car models.

B. K. Khare & Co.Chartered Accountants

[17]

Please check thoroughly. Vakils will not be responsible for errors not noted on this proof. Please check thoroughly. Vakils will not be responsible for errors not noted on this proof.Shailesh Shailesh

UNION BUDGET 2016

1. THE INDIAN MY’ST(O)RY’ - WORK-IN-PROGRESS

And Miles to go before I sleep,

And Miles to go before I sleep

The present Government was elected in May 2014 on the promise of ushering in achche din. Nearly two years have gone by, but the nation still waits for those happy days to arrive. As we shall see in the next section, it is not as if this government is without any achievement to its credit. Very briefly, nearly 3 years ago, the twin deficits relating to the fiscal and the current account, had almost spun out of control. Since then the consolidation of the fiscal deficit is according to plan and the current account deficit stands at a healthy 1.4%. Inflation both measured either by WPI or CPI is under control, with the former being in negative territory. Overall, the economy is said to be growing at about 7.6%. Much has been done to rationalize subsidies, and foreign exchange reserves stand at a figure of about US$ 350 billion.

Even so, large sections of the population are disenchanted. Two successive droughts have impoverished farmers; as a consequence, large sections of the rural population are in distress. Corporates balance-sheets reveal heavy indebtedness and idle capacity. Public sector banks cannot lend because they carry too many stressed assets. As a result the gross capital formation as percentage of the GDP has declined and because of slowing down of the world economy, India’s exports have declined throughout the current year. The rupee has declined to ` 68 to the dollar as the country finds itself out performed in export markets, by much smaller countries like Bangladesh and Vietnam. 10 lakh people join the workforce every month and when they find all avenues for employment blocked, they launch agitations to seek reservations for their communities in government jobs.

Last year this time the Economic Survey pointed out that the economy was close to hitting a sweet spot with a long term growth potential ranging from 8% to 10% per annum. Clearly, this is unlikely to be realized till some of the current challenges are surmounted.

Some of these are fiscal in nature: Funds of the order of about .07% of GDP, for example, are required to implement the recommendations of the Seventh Pay Commission and OROP. Likewise, large funds are required again to recapitalize banks so that they can start lending again. Clearly, ` 25,000 indicated in Finance Budget speech is not going to be enough. Overall, all these requirements are bound to affect the fiscal deficit sooner or later, unless the Government finds innovative ways of generating non- tax revenues, perhaps through sale of spectrum or disinvestment of shares in public sector undertakings.

The political and social challenges the Government faces are even greater: a hostile opposition has stymied attempts to make land acquisition for projects easier. The Government is also facing a nightmare in getting the GST bill through the Rajya Sabha. Ironically, as a columnist in the Business Standard pointed out recently, every reform the economy requires is opposed by some powerful vested interest. Labour reforms at the Centre cannot be considered because they do not go down well with a small but well-entrenched labour aristocracy to be found in the formal manufacturing sector of the economy. They will not allow an exit policy, so that a new manufacturer, finds himself in the middle of a chakravyuh, a military formation that allows the enemy to enter a certain area, but not leave it. Agricultural reform that will free farmers to sell their produce wherever they get the best price is obstructed by traders who block the amendment of the laws relating to the marketing of agricultural produce. Divestment of government ownership of banks and other loss-making PSUs is opposed by trade unions who have vested interest in governmental ownership.

So, the list goes on and on. And yet the sweet spot the Finance Minister talked about last year is

BUDGET ANALYSIS 2016

[18]

Please check thoroughly. Vakils will not be responsible for errors not noted on this proof. Please check thoroughly. Vakils will not be responsible for errors not noted on this proof.Shailesh Shailesh

so beckoningly close, if only the Government can master the skills required to forge a wide ranging coalition that supports its reforms agenda.

Clearly, a lot hard work lies ahead in finding support for these reforms which the country badly needs: for the millions of our young countrymen who deserve a better future, the Government must not lose focus when other controversies rage. These are generated essentially to make the Government lose focus on its economic policies. One is reminded of Robert Frost’s lovely lines:

The woods are lovely, dark and deep,But I have promises to keep,

And miles to go before I sleep,And miles to go before I sleep.

The present budget therefore comes at a very critical juncture: we look at the economy in three parts. In the first instance, we analyze the year that was. We move then to bring out the highlights of this year’s Economic Survey and then finally we see how far the Government has gone in tackling the problems that confront it.

2. THE YEAR THAT WAS – BUDGET TO BUDGET - A QUICK RECAP

Despite the doubts raised by many observers, India today is the fastest growing economy in the world. During FY 16, it is expected to grow at 7.6% per annum in real terms, estimates the Central Statistical Organisation (CSSO). The corresponding figure for the earlier year is 7.2%. Considering that the country has suffered successive droughts during the last two years, the overall economic growth has been impressive.

This is despite the many legacy problems which this Government inherited:

YY By the time, it came to power, investor confidence in the economy had eroded because of retrospective taxation.

YY With the fiscal deficit (4.4% of GDP) and the current account deficit (4.8% in 2012-13) almost spinning out of control, public finances were in a mess.

YY In tandem, NPAs of public sector banks were growing at an alarming pace; and inflation (WPI at 7.4% in 2012-13; 6% in 2013-14), and particularly food inflation (CPI at 9.5% in 2013-14), refused to be tamed.

YY To cap this depressing scenario were the problems of policy paralysis which afflicted large parts of the bureaucracy and stalled projects which brought further investment to a grinding halt.

Now the situation is very different: Thanks to the crash in oil and commodity prices and restraint exercised by the Government in its spending programmes, the situation has changed. The gross fiscal deficit has come down to 3.9% and is slated to reduce further. CAD is healthy at 1.4%. Inflation as measured by WPI, is currently in negative territory, and, in CPI terms, stands at 5.61% (as on December 2015).

Even so, the country’s most sympathetic supporters, admit that there are some facts which are worrying and there is something that is not quite right: the economy just does not pass the small test of an economy that is doing well. Although the CSSO estimates a YOY manufacturing growth of 9.5%, top lines of many corporates do not reflect this trend. The share of gross capital formation (GCFC) which is a proxy for investment, continues to languish at 29.4%, whereas just five years ago in 2011-12 this figure stood at 33.6%. During FY 2014-15, because of a drought, agricultural output shrank by 0.2%; currently, it is expected to grow by 1.1% YOY. The question to be asked is if we are in the midst of a recovery, how far is it really sustainable when current investment continues to be so depressed?

Truth to speak, of the four Keynesian engines- private consumption(C), private investment (I), Government spending (G) and net exports (X) that comprise the GDP of a modern economy, only two are firing- private consumption and government spending.

Private investment refuses to pick up because public sector banks, saddled with stressed assets of over ` 7 lakh crores, are unable to lend;

B. K. Khare & Co.Chartered Accountants

[19]

Please check thoroughly. Vakils will not be responsible for errors not noted on this proof. Please check thoroughly. Vakils will not be responsible for errors not noted on this proof.Shailesh Shailesh

corporates, on the other hand suffer, from heavy indebtedness.

Exports in the first half of the current fiscal year declined by 1.1% YOY, because of slack global demand. For January 2016 they stood at US$ 21 billion, as compared to US$ 24.39 billion a year ago, and US$ 26.75 billion two years ago. The decline is alarming and currently India is being outperformed by countries like Bangladesh and Vietnam. The fall in exports is likely to result in a negative impact on the ‘Make in India’ campaign of the present government; in turn, this would lead to a failure to generate new employment.

Some real out of the box thinking will thus be needed to spur both exports as well as investments. To boost exports, suggests the Business Standard, the Ministry itself should play a more proactive role in solving problems, particularly in speeding shipments at our ports. A high level inter-ministerial group could also be set-up to suggest how the competitiveness of Indian exports could be improved.

Increasing private investment, however is an altogether different proposition. Public sector banks (PSBs) will have to clean up their balance sheets. They may have to depend upon public issues to raise funds required by them for their recapitalization needs. Government may not be able to help much because it may be constrained by its requirement to meet stiff fiscal targets during the next few years. It also has a huge responsibility to implement OROP as well the recommendations of the Seventh Pay Commission. But which investor would like to risk investing his hard earned money in PSBs when their recent performance has been so poor?

An alternative way to spur investments may be to give taxpayers further tax breaks when they make long term investments needed by the economy. Reducing and rationalizing tax rates so as to leave more money with taxpayers, a measure already being contemplated by the FM, may also help.

There really is no option for the Government except to find ways of making all the four engines of the economy fire. Let us not forget that 10 lakh persons are joining the work force every month. The economy has to grow rapidly to absorb them. In fact as the Red Queen warned Alice in Alice Through the Looking Glass and What Alice Found There, in our country, “... it takes all the running you can do, to keep in the same place.” Demands of reservations in the private sector and all manner of social unrest we witness today are ominous warnings of times to come unless the country can get its act together.

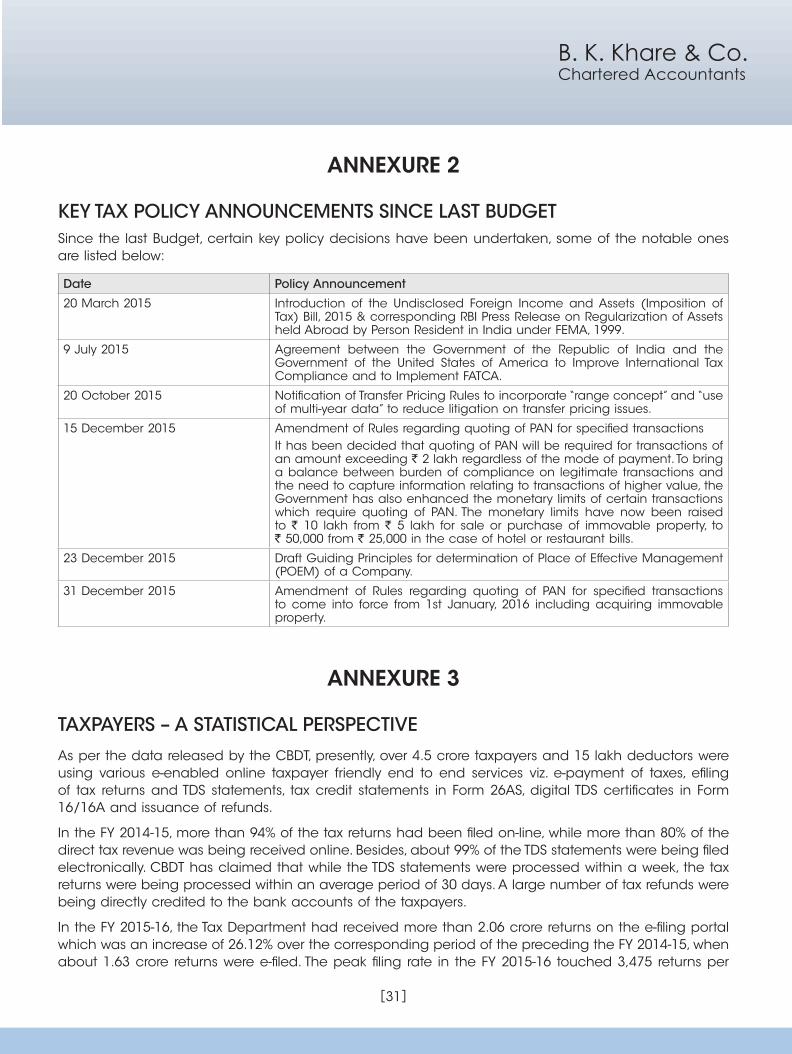

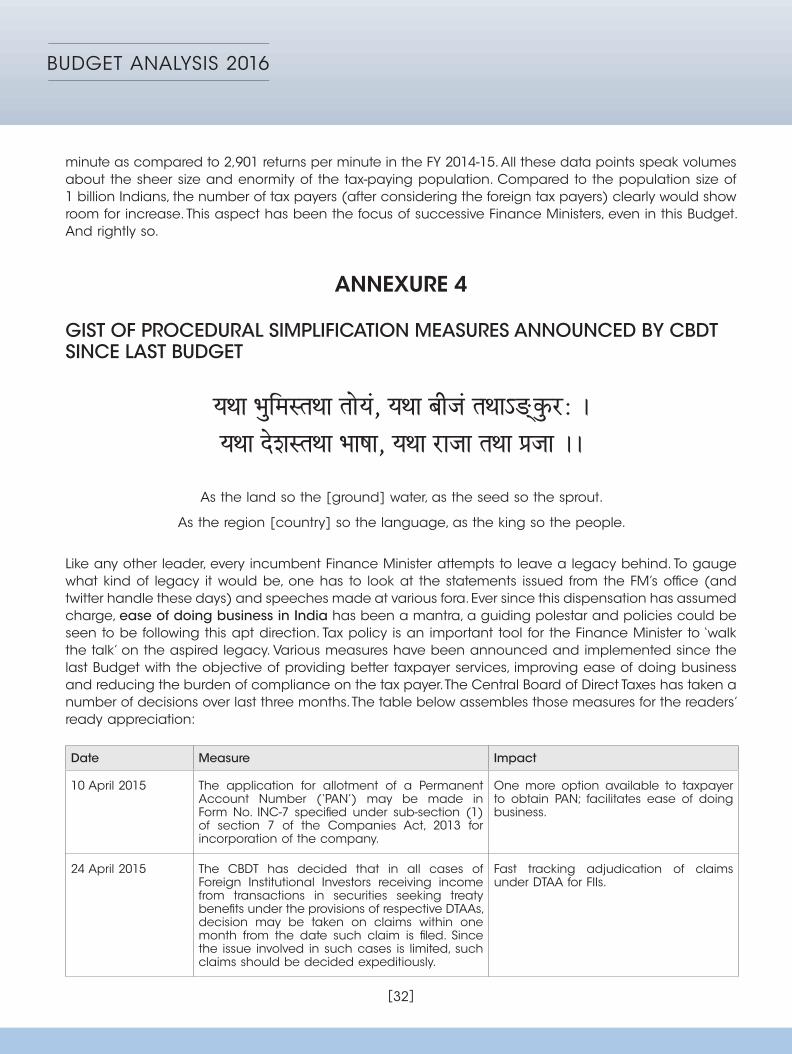

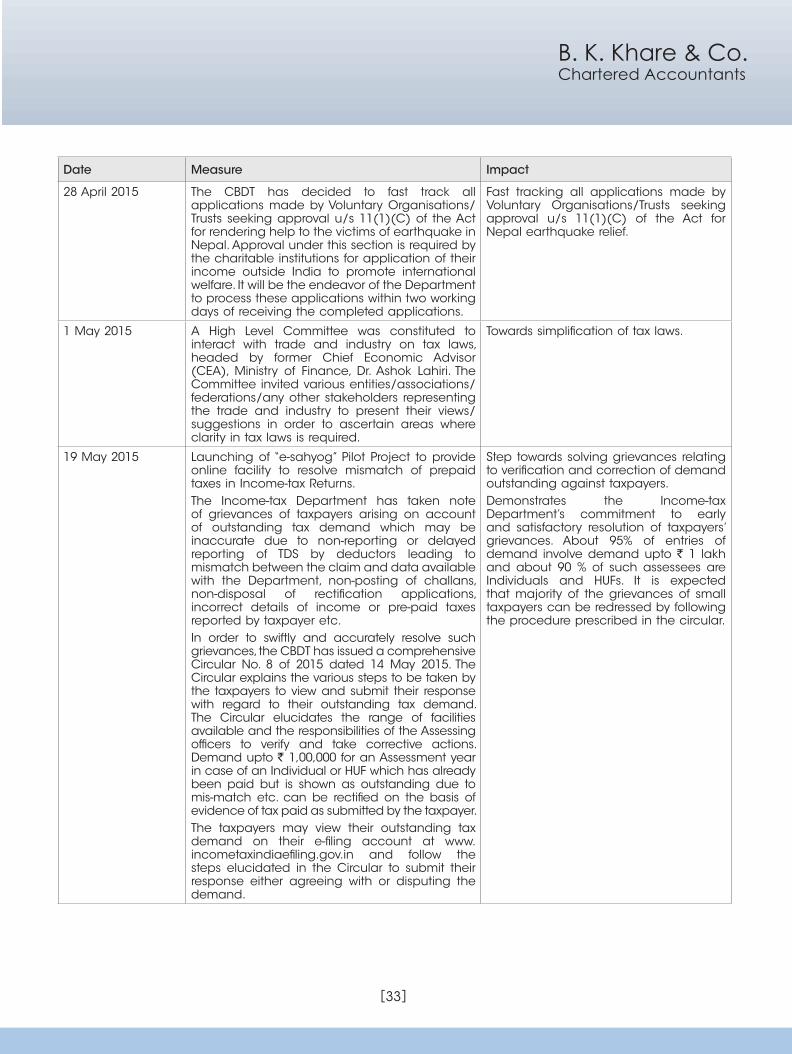

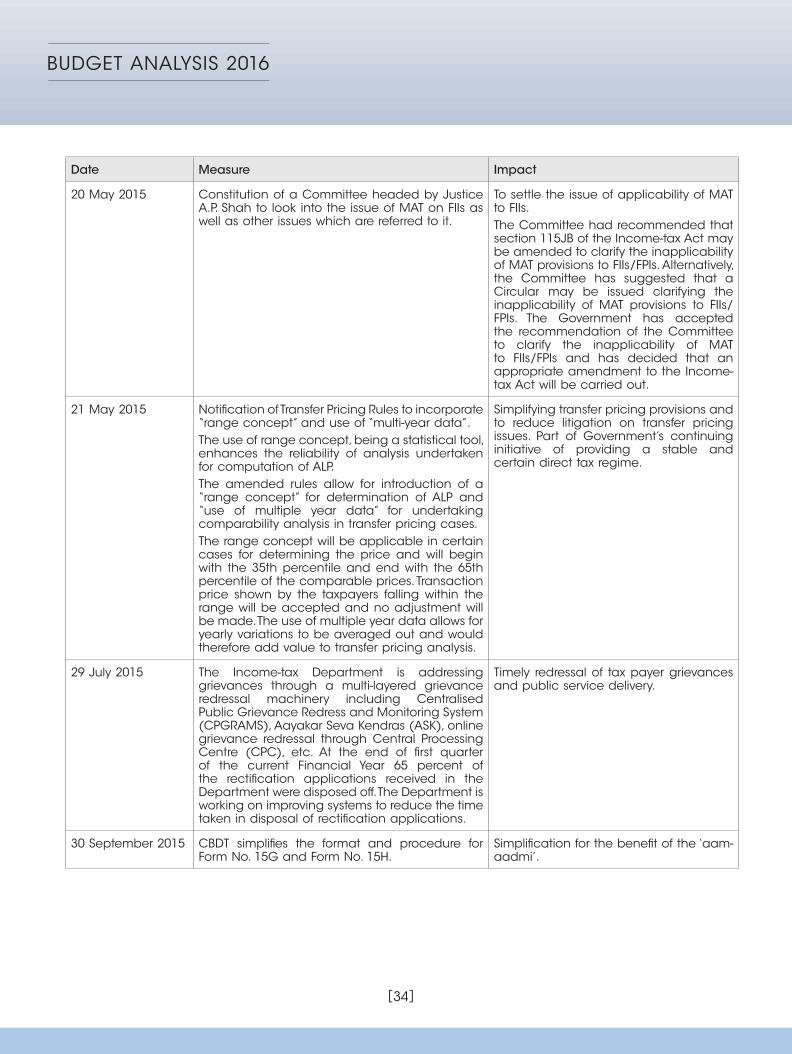

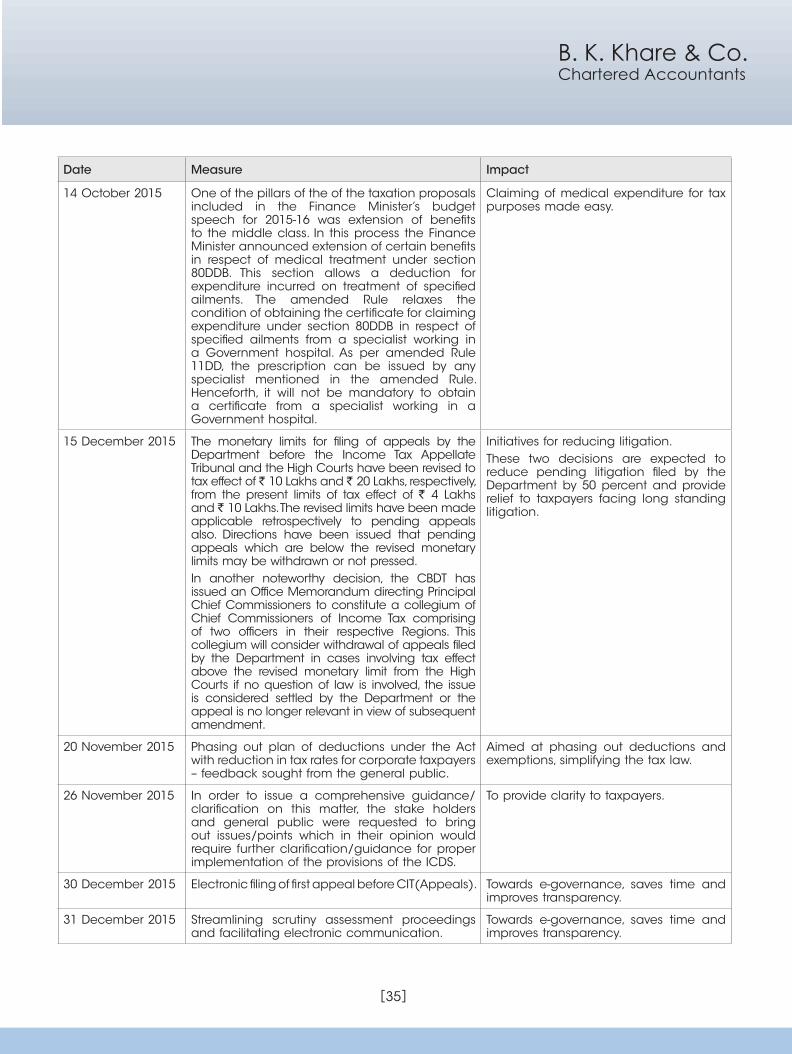

A list of important macro-economic initiatives taken by the Government in the current year and their current status may be seen in the Annexure 1. In Annexure 2, we have listed out key tax policy initiatives announced since the last Budget. Annexure 3 offers a statistical glimpse of certain interesting aspects relating to the tax base, based on data published by the CBDT. A gist of Key Circulars & Notifications issued by CBDT since last Budget has been collated for the reader’s ready reference, in Annexure 4.

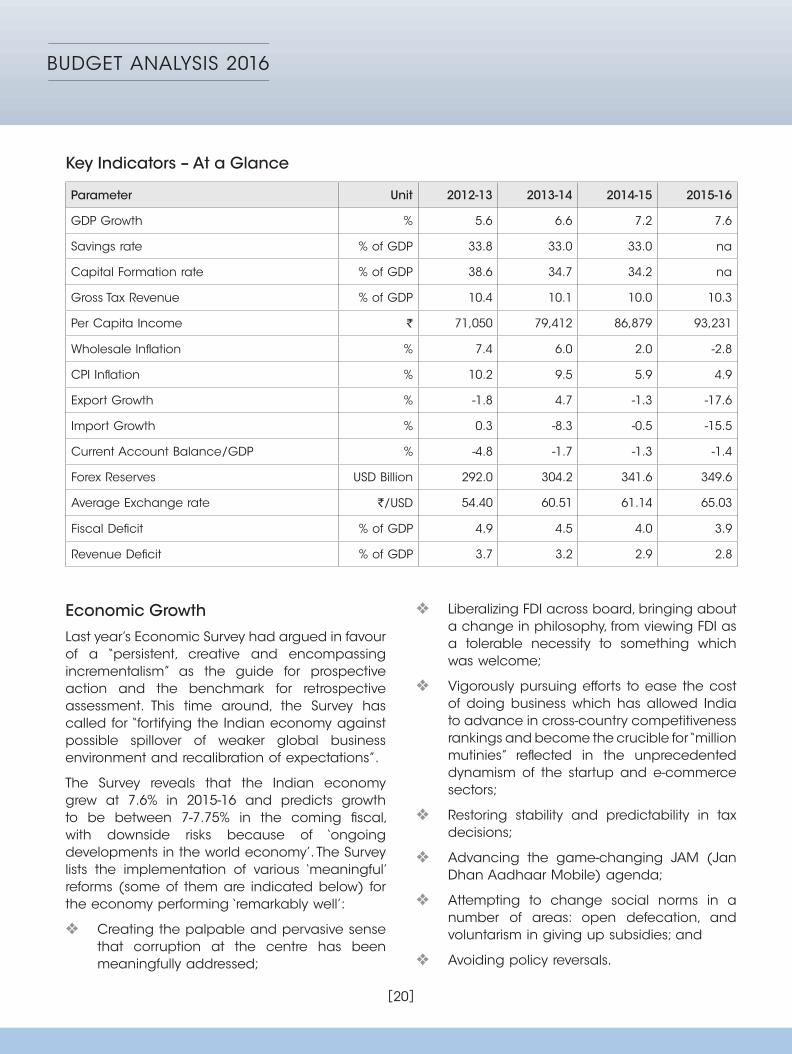

3. ECONOMIC SURVEY 2016 – HIGHLIGHTS

The Survey does recognize the reality that global macro-economic landscape is currently chartering a rough and uncertain terrain characterized by weak growth of world output. The situation has been exacerbated by; (i) declining prices of a number of commodities, with reduction in crude oil prices being the most visible of them, (ii) turbulent financial markets (more so equity markets), and (iii) volatile exchange rates. The Survey notes that despite global headwinds and a truant monsoon, India registered robust growth of 7.2% in 2014-15 and 7.6% in 2015-16, thus becoming the fastest growing major economy in the world.

BUDGET ANALYSIS 2016

[20]

Please check thoroughly. Vakils will not be responsible for errors not noted on this proof. Please check thoroughly. Vakils will not be responsible for errors not noted on this proof.Shailesh Shailesh

Key Indicators – At a Glance

Parameter Unit 2012-13 2013-14 2014-15 2015-16

GDP Growth % 5.6 6.6 7.2 7.6

Savings rate % of GDP 33.8 33.0 33.0 na

Capital Formation rate % of GDP 38.6 34.7 34.2 na

Gross Tax Revenue % of GDP 10.4 10.1 10.0 10.3

Per Capita Income ` 71,050 79,412 86,879 93,231

Wholesale Inflation % 7.4 6.0 2.0 -2.8

CPI Inflation % 10.2 9.5 5.9 4.9

Export Growth % -1.8 4.7 -1.3 -17.6

Import Growth % 0.3 -8.3 -0.5 -15.5

Current Account Balance/GDP % -4.8 -1.7 -1.3 -1.4

Forex Reserves USD Billion 292.0 304.2 341.6 349.6

Average Exchange rate `/USD 54.40 60.51 61.14 65.03

Fiscal Deficit % of GDP 4.9 4.5 4.0 3.9

Revenue Deficit % of GDP 3.7 3.2 2.9 2.8

Economic Growth

Last year’s Economic Survey had argued in favour of a “persistent, creative and encompassing incrementalism” as the guide for prospective action and the benchmark for retrospective assessment. This time around, the Survey has called for “fortifying the Indian economy against possible spillover of weaker global business environment and recalibration of expectations”.

The Survey reveals that the Indian economy grew at 7.6% in 2015-16 and predicts growth to be between 7-7.75% in the coming fiscal, with downside risks because of ‘ongoing developments in the world economy’. The Survey lists the implementation of various ‘meaningful’ reforms (some of them are indicated below) for the economy performing ‘remarkably well’:

YY Creating the palpable and pervasive sense that corruption at the centre has been meaningfully addressed;

YY Liberalizing FDI across board, bringing about a change in philosophy, from viewing FDI as a tolerable necessity to something which was welcome;

YY Vigorously pursuing efforts to ease the cost of doing business which has allowed India to advance in cross-country competitiveness rankings and become the crucible for “million mutinies” reflected in the unprecedented dynamism of the startup and e-commerce sectors;

YY Restoring stability and predictability in tax decisions;

YY Advancing the game-changing JAM (Jan Dhan Aadhaar Mobile) agenda;

YY Attempting to change social norms in a number of areas: open defecation, and voluntarism in giving up subsidies; and

YY Avoiding policy reversals.

B. K. Khare & Co.Chartered Accountants

[21]

Please check thoroughly. Vakils will not be responsible for errors not noted on this proof. Please check thoroughly. Vakils will not be responsible for errors not noted on this proof.Shailesh Shailesh

The Survey remarks that the fiscal sector registered three striking successes: ongoing fiscal consolidation, improved indirect tax collection efficiency; and an improvement in the quality of spending at all levels of government.

Demand-side Story

The recent growth revival in India is predominantly consumption-driven. Three visible changes are taking place in aggregate demand. First, with improving growth in private consumption, its contribution to GDP growth is getting aligned to its GDP share. Second, aided by the growth in capital goods, the growth of fixed capital formation (also known as fixed investment and which reflects addition to the productive capacity in the economy) has picked up. A robust growth in valuables has been recorded during the current year. Third, the substantial erosion of global demand for Indian output, manifest in loss of Indian Exports, acts as a drag on domestic growth. It is from this angle that India’s achievement of being able to sustain its growth at a fairly high level, primarily on the strength of her domestic absorption, becomes noteworthy.

Supply-side Report Card

The Gross Value Added (GVA), which broadly reflects the supply or production side of the economy, registered an increase in the growth rate from 5.4% in 2012-13 to 7.1% in 2014-15. In the current year, the growth in GVA is likely to increase to 7.3%.

Talking of sectoral growth, agriculture (which includes forestry and fishing) contracted by 0.2% in 2014-15 but is expected to recover by 1.1% in the coming fiscal. Industry grew at 5.9% in 2014-15 [expected to grow 7.3% in 2015-16] whereas services expanded by 10.3% in the same period [expected to grow 9.2% in 2015-16]. Growth in the agriculture sector in 2015-16 has continued to be lower than the average of last decade, mainly on account of it being the second successive year of lower than – normal

monsoon rains. Growth in the service sector moderated slightly, but still remains robust; while the acceleration in manufacturing growth compensated for it.

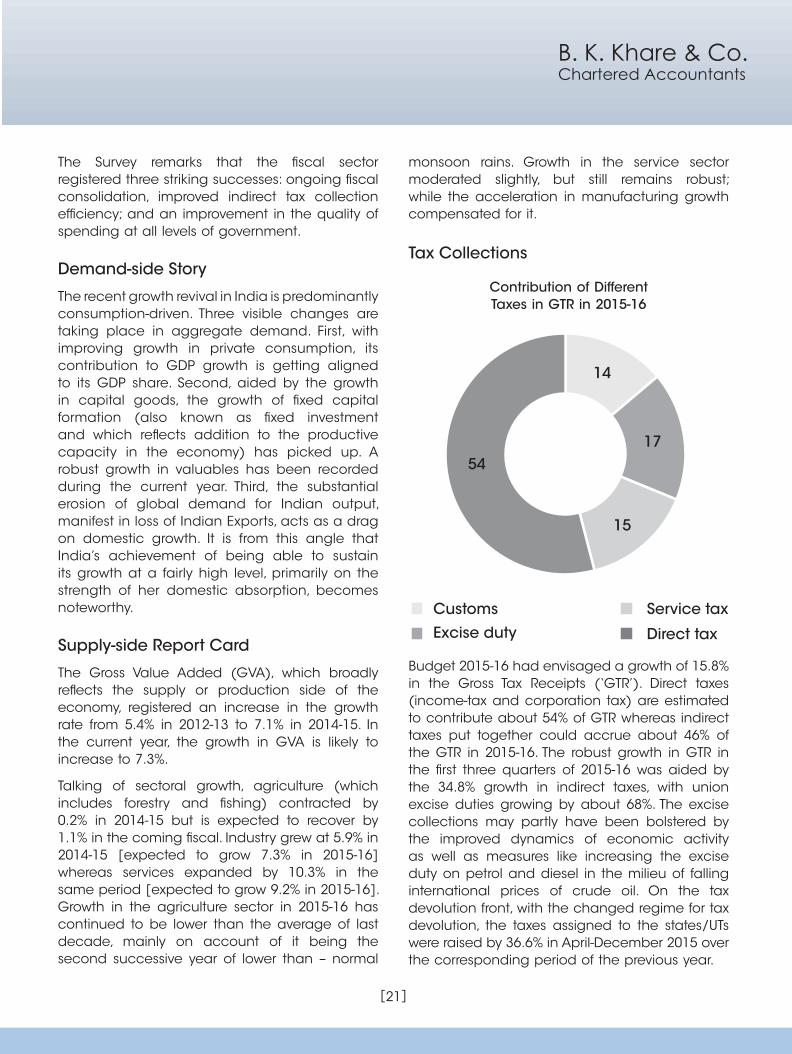

Tax Collections

Contribution of Different Taxes in GTR in 2015-16

Customs Service tax

14

17

15

54

Excise duty Direct tax

Budget 2015-16 had envisaged a growth of 15.8% in the Gross Tax Receipts (‘GTR’). Direct taxes (income-tax and corporation tax) are estimated to contribute about 54% of GTR whereas indirect taxes put together could accrue about 46% of the GTR in 2015-16. The robust growth in GTR in the first three quarters of 2015-16 was aided by the 34.8% growth in indirect taxes, with union excise duties growing by about 68%. The excise collections may partly have been bolstered by the improved dynamics of economic activity as well as measures like increasing the excise duty on petrol and diesel in the milieu of falling international prices of crude oil. On the tax devolution front, with the changed regime for tax devolution, the taxes assigned to the states/UTs were raised by 36.6% in April-December 2015 over the corresponding period of the previous year.

BUDGET ANALYSIS 2016

[22]

Please check thoroughly. Vakils will not be responsible for errors not noted on this proof. Please check thoroughly. Vakils will not be responsible for errors not noted on this proof.Shailesh Shailesh

Concern Factors

To its credit, the Survey does highlight certain disappointments which could stifle India’s full supply potential – approval for the game-changing GST bills has proved elusive so far; the disinvestment program fell short of targets, including that of achieving strategic sales; and the next stage of subsidy rationalization is a work-in-progress. Critically, corporate and bank balance sheets remain stressed, affecting the prospects for reviving private investment, a key engine of long term growth.

The Survey pays due attention to the problems in the banking system that have been growing for some time. Stressed assets (non performing loans plus restructured assets) have been rising ever since 2010, impinging on capital positions, even as the strictures of Basel III loom ever closer on the horizon. It notes that the Banks have responded by limiting the flow of credit to the real economy so as to conserve capital, while investors have responded by pushing down bank valuations, especially over the past year. The shares of many banks now trade well below their book value. This balance sheet vulnerability is in some ways a mirror and derivative of similar frailties in the corporate sector, especially the large business houses that borrowed heavily during the boom years to invest in infrastructure and commodity-related businesses, such as steel. Corporate profits are low while debts are rising, forcing firms to cut investment to preserve cash flow. This situation is not sustainable; a decisive solution is needed. But finding one is difficult.

In sum, the Survey does note that for now but not indefinitely, the ‘sweet spot’ for India is still beckoningly there.

Forecast

The Survey notes that foreign demand is likely to be weak, forcing India – in the short run – to find and activate domestic sources of demand to prevent growth momentum from weakening. At the very least, a tail risk event (the Survey portends a major currency readjustment in Asia) would require the

Indian monetary and fiscal policy not to add to the deflationary impulses from abroad. The consolation would be that weaker oil and commodity prices would help keep inflation in check.

The Survey pins its hopes on two factors that could boost consumption. If and to the extent that the Seventh Pay Commission is implemented, increased spending from higher wages and allowances of government workers will start flowing through the economy. If, in addition, the monsoon returns to normal, agricultural incomes will improve. Against this, the disappearance of much of last year’s oil windfall would work to reduce consumption growth. Current prospects suggest that oil prices (Indian crude basket) might average US$ 35 per barrel in next fiscal year compared with US$ 45 per barrel in 2015-16. The resulting income gain would amount roughly equivalent to 1% point of GDP. But the Survey cautions that this would be half the size of last year’s gain, so consumption growth would be slow on this account next year.

Indian fortunes intertwined with Global Growth

The Survey recognizes the fact that reflecting India’s growing globalization, the correlation between India’s growth rate and that of the world has risen sharply to reasonably high levels. India’s contribution to global growth in PPP terms increased from an average of 8.3% during the period 2001 to 2007 to 14.4% in 2014. During the 1990s, the US’s contribution to the global GDP growth in PPP terms was, on an average, around 16% points higher than India’s. The picture changed dramatically in 2013 and 2014 when India’s contribution was higher than that of the US by 2.2 and 2.7% points respectively. While it sounds ‘too good to be true’ that India has indeed surpassed the US in certain growth parameter, however, what is undeniable is the fact that India’s real contribution to global growth is here to stay and will only increase in the short to mid-term.

A 1% point decrease in the world growth rate is now associated with a 0.42% decrease in

B. K. Khare & Co.Chartered Accountants

[23]

Please check thoroughly. Vakils will not be responsible for errors not noted on this proof. Please check thoroughly. Vakils will not be responsible for errors not noted on this proof.Shailesh Shailesh

Indian growth rates. Accordingly, if the world economy remains weak, India’s growth will face considerable headwinds. For example, if the world continues to grow at close to 3 percent over the next few years rather than returning to the buoyant 4-4.5% recorded during 2003-2011, India’s medium-term growth trajectory could well remain closer to 7-7.5%, notwithstanding the government’s reform initiatives, rather than rise to the 8-10% that its long-run potential suggests.

Perhaps it may not be out of place to predict that as India (and Indians) grows rapidly, it may not be long before one could say ‘if India gets sick, the world will need treatment’ (to paraphrase Mr. Palkhivala differently).

India-China Dance - Genuine Anxiety or Misplaced Optimism?

The Survey notes that India’s long run potential growth rate is around 8-10% whereas China would grow about 5%. Interestingly, the Survey observes that India is not rich enough despite its uncontestably vibrant political institutions whereas China is too rich notwithstanding its weak democratic institutions. The Survey notes that the Chinese economy is faced with concerns of rebalancing investment and consumption activities. In this backdrop, the Indian economy stands out ‘as a haven of macro-economic stability, resilience and optimism’.

Here, a word of caution would be in place. Die-hard (nationalistic) optimism could well spill into misplaced jingoism, which would pull wool over one’s myopic eyes; however, it may not sustain (unless focus is maintained) till the evils which were pushed under the carpet, come home to roost. The policy framers must set aim just as Arjuna did when aiming at the game parrot amidst the branches and leaves, not for a moment losing focus. India has potential, no doubt. India needs to make more progress on agricultural productivity, change mindsets, be more trade-enabled, have efficient infrastructure (roads, ports, connectivity etc). If India is to take its rightful place amongst the comity of nations,

it must unleash and harness the full potential in terms of the ‘3Ds’ as our Prime Minister puts it – Democracy, Demography and Demand. Otherwise, we run the risk of remaining, as Mr. T. N. Ninan has very nicely put it, in his book ‘The Turn of the Tortoise’, ‘a premature power’ which has taken large strides in the past quarter century and has become a leading economy, but it continues to have more poor people than any other country and a level of per capita income that puts it in the lowest quartile in a global country listing.

4. THE VITAL PUSH AHEAD - LET A THOUSAND FLOWERS BLOOM

Does the budget of 2016 go far enough in addressing the important and critical problems that the economy currently faces? To be sure, the FM has travelled that extra mile to reassure farmers that the country cares for them. He has allocated ` 35,984 crores to agriculture and farmer welfare and has promised grants in aid of 2.87 lakhs to gram panchayats and municipalities. 89 critical irrigation projects are being fast tracked and ` 1,700 crores has been allocated to them to increase the acreage under irrigation. Hopefully, the unified agricultural marketing scheme which twelve states have accepted will provide farmers the necessary platform to realize better value for their products. Considering that more than 60% of our population is engaged in agriculture, these outlays are perhaps necessary, especially as the rural economy has been through two droughts and many farmers have had to commit suicide because of indebtedness. Similarly, the many other rural welfare measures which have been taken are also welcome. These relate to sanitation, provision of cooking gas to poor families etc.

The current budget and the Economic Survey have both emphasized that the Government will adhere to its fiscal deficit target of 3.5% for the coming year. The CAD will range from 1% to 1.5%. These are welcome developments because the country needs to be in a strong position tomorrow to repay what it has borrowed today. The Government realizes that the current debt

BUDGET ANALYSIS 2016

[24]

Please check thoroughly. Vakils will not be responsible for errors not noted on this proof. Please check thoroughly. Vakils will not be responsible for errors not noted on this proof.Shailesh Shailesh

to GDP ratio at 67% is high and needs to be brought down. By adhering to certain discipline in its spending the Government would also be establishing credibility internationally with other international actors who deal with it.

With the slowing down of the world economy, India’s exports will continue to be adversely impacted. This is because unlike in the past, imports and exports taken together, are now of the order of 42% of the GDP. Currently, quite apart from the decline in international demand, the existing problems also relate to our exports not being able to match competition coming from smaller countries who have been able increase their market share. If the long term potential growth rate (8%-10%) of the Indian economy has to be realized, the country will have to increase its share of the world trade from 3% to 15%. This is one area where perhaps the Government could perhaps have done much more.

There are two other themes that emerge from the current economic situation in which the country currently finds itself. First of all it is interesting to note that both India and China are outliers in to the general relationship which economists have been able to perceive between democracy and economic development. Overall, the more democratic a country, the greater are the chances of its government being able to launch really successful programmes of economic development. By this logic, China should have been much less, and India, much more successful than what either of them has been so far. In India’s case, one mistake which the state committed in the past was to assume

too much responsibility (under socialist regimes) for making things happen. The government has now enunciated its new philosophy in its “Make in India” campaign in which it has clarified that it will only act as a facilitator and in the words of Mao allow entrepreneurs to take the initiative. It will thus “let a thousand flowers bloom.”

Were the Government really to do this, it would be left playing the role of a regulator or a facilitator. We would then in the long run end up with a leaner bureaucracy and it would become much easier for the country to absorb such expenditure as that which will arise from implementing the recommendations of the seventh pay commission.

It now remains for us to take stock and conclude our analysis. Over the long term we give ourselves less credit as a nation than what we perhaps deserve. Indeed as the statistical portion of the Economic Survey brings out, since 1950-51 per capita incomes have gone up 10.28 times in real terms despite the fact that the population has since then almost quadrupled. Similarly GDP has risen 38.27 times in real terms and per capita availability of food grains and pulses has gone up from 394 grams to 491.2 grams per capita per day. Babies born today will in all probability live up to the year 2083; at least 73% of them will be able to read and write.

These are not small achievements but the question really is could the country have done much better? Indeed that is what it seeks to do now. A billion people hope that the Government succeeds in its mission of ushering in happy days for the nation.

B. K. Khare & Co.Chartered Accountants

[25]

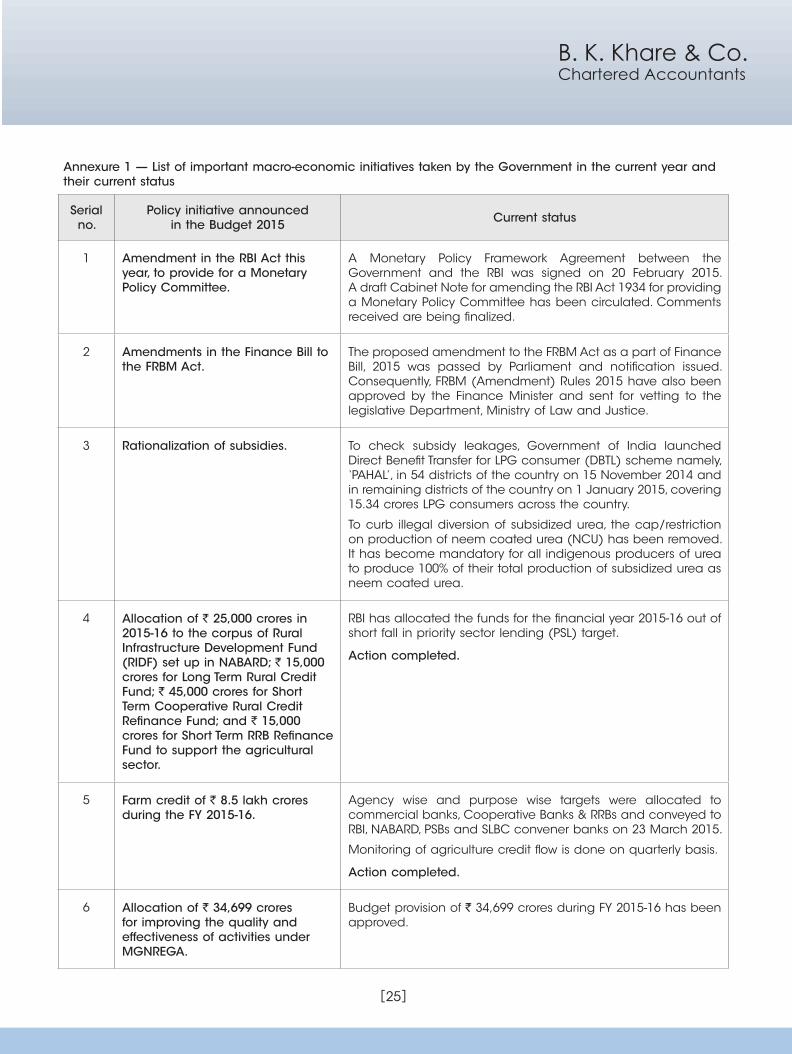

Annexure 1 — List of important macro-economic initiatives taken by the Government in the current year and their current status

Serial no.

Policy initiative announced in the Budget 2015 Current status

1 Amendment in the RBI Act this year, to provide for a Monetary Policy Committee.

A Monetary Policy Framework Agreement between the Government and the RBI was signed on 20 February 2015. A draft Cabinet Note for amending the RBI Act 1934 for providing a Monetary Policy Committee has been circulated. Comments received are being finalized.

2 Amendments in the Finance Bill to the FRBM Act.

The proposed amendment to the FRBM Act as a part of Finance Bill, 2015 was passed by Parliament and notification issued. Consequently, FRBM (Amendment) Rules 2015 have also been approved by the Finance Minister and sent for vetting to the legislative Department, Ministry of Law and Justice.

3 Rationalization of subsidies. To check subsidy leakages, Government of India launched Direct Benefit Transfer for LPG consumer (DBTL) scheme namely, ‘PAHAL’, in 54 districts of the country on 15 November 2014 and in remaining districts of the country on 1 January 2015, covering 15.34 crores LPG consumers across the country.

To curb illegal diversion of subsidized urea, the cap/restriction on production of neem coated urea (NCU) has been removed. It has become mandatory for all indigenous producers of urea to produce 100% of their total production of subsidized urea as neem coated urea.

4 Allocation of ` 25,000 crores in 2015-16 to the corpus of Rural Infrastructure Development Fund (RIDF) set up in NABARD; ` 15,000 crores for Long Term Rural Credit Fund; ` 45,000 crores for Short Term Cooperative Rural Credit Refinance Fund; and ` 15,000 crores for Short Term RRB Refinance Fund to support the agricultural sector.

RBI has allocated the funds for the financial year 2015-16 out of short fall in priority sector lending (PSL) target.

Action completed.

5 Farm credit of ` 8.5 lakh crores during the FY 2015-16.

Agency wise and purpose wise targets were allocated to commercial banks, Cooperative Banks & RRBs and conveyed to RBI, NABARD, PSBs and SLBC convener banks on 23 March 2015.

Monitoring of agriculture credit flow is done on quarterly basis.

Action completed.

6 Allocation of ` 34,699 crores for improving the quality and effectiveness of activities under MGNREGA.

Budget provision of ` 34,699 crores during FY 2015-16 has been approved.

Revised Annexure 1.indd 25 3/2/2016 8:25:45 PM

BUDGET ANALYSIS 2016

[26]

Serial no.

Policy initiative announced in the Budget 2015 Current status

7 Creation of a unified national agriculture market.