Embed Size (px)

Citation preview

1

BANKERS’ ERRORS IN SCREENING NEW FIRMS

Jean Bonnet *, Sylvie Cieply

** and Marcus Dejardin

***

* University of Caen, CREM-CAEN, UMR CNRS 6211, Faculty of Economics and Business Administration,

19, rue Claude Bloch, 14032 Caen, France, [email protected]

**

University of Caen, CREM-CAEN, UMR CNRS 6211, Institut Banque-Assurance,

19 rue Claude Bloch, 14032 Caen, France, [email protected]

*** Université Catholique de Louvain and University of Namur, CERPE, Faculty of Economics, Social Sciences

and Business Administration,

8, Rempart de la Vierge, 5000 Namur, Belgium, [email protected]

Draft version: February 23, 2012

Abstract:

Bankers are making errors when screening new firms. Two types can be distinguished. Both

are based on informational asymmetries. The first error corresponds to credit rationing “à la

Stiglitz and Weiss” (1981) and consists in not financing good risks. The second error “à la De

Meza and Webb” (1987) relates to firms receiving credit although they should have not. How

much reliable are these classics? Challenging theories through the exploitation of a very rich

dataset on new French firms from the late Twentieth Century, we show that the Stiglitz and

Weiss constraint is not highly spread. The imperfection of the credit market described by De

Meza and Webb appears more realistic. In addition, we identify factors influencing the

decision of bankers to grant credit and explaining the errors they make. Our results make a

plea for bankers’ risk assessment to be fed by systematic multivariate analysis of the actual

outcomes obtained by starters.

Key words:

Credit Rationing, Over Financing, Informational Asymmetries, Errors, Bankers.

JEL Classification:

M13, D82, G21

2

1. Introduction

Banks do exist because they screen and monitor borrowers more efficiently than other

investors would (Goodhart, 1989, Bhattacharya and Thakor, 1993, Allen and Santomero,

1998, Fama, 1985). Banks are superior to non financial agents because they are specialized in

gathering private information and treating it (Freixas and Rochet, 1999). By granting bigger

loans than private non financial agents would be able to, they reduce transaction costs

(Benston and Smith, 1976) and limit free-riding problems (Diamond, 1984, Bhattacharya,

Boot and Thakor, 2004). Banks are superior to other financial institutions too because they

manage money and deposit accounts, and consequently they own highly strategic information

on firms’ receipts and expenditures and on the way firms develop themselves or not (Ruhle,

1997, Diamond and Rajan, 2001).

Despite all these comparative advantages of banks, relationships between bankers and

firms are not perfect. Banks indeed suffer from informational asymmetries and agency

problems (Freixas and Rochet, 1999). In this context, prices cannot clear the market and (non-

walrassian) equilibrium arises with a fringe of unsatisfied agents.

For Keynes (1930), the unsatisfied agents are borrowers. Stiglitz and Weiss (1981)

propose an explanation for it. In their model, entrepreneurs launch projects. By assumption,

they all require the same external finance, and projects have the same mean return but differ

in their risk. The individual characteristics of entrepreneurs are privileged information owned

by entrepreneurs and very imperfectly shared with outside investors. In this model, bankers

only know the distribution of entrepreneurs’ characteristics. Consequently, the risk of projects

cannot be easily and perfectly accessed. Bankers may not be able to differentiate adequately

between high risk and low risks firms and projects. Moreover, once loans have been granted,

borrowers may not be able to perfectly monitor firms. In all these cases, increasing the interest

rate may be disastrous. A rise in interest rate would drive the “best” firms (lower risks) to

refuse loans proposals they would consider as too costly (adverse selection). Additionally, it

may incite firms to launch riskier projects, leading to an excessively risky portfolio (moral

hazard). Ultimately, because of these informational imperfections, bankers may prefer simply

not to lend credit and equilibrium on the credit market may arise with rationing1.

De Meza and Webb (1987) contest this result. Like in Stiglitz and Weiss (1981), all

projects require the same initial investments and the same level of external finance. Bankers

are assumed to have no prior information on entrepreneurs’ characteristics too. In contrast to

Stiglitz and Weiss (1981) however, De Meza and Webb (1987) consider that the mean return

of projects varies across firms. In their model, entrepreneurs differ from each other in

expected return and not in risk. This change in hypotheses has serious consequence. De Meza

and Webb (1987) find neither credit rationing nor under-investment but, on the contrary, over-

financing and over-investment; too many entrepreneurial projects are financed2. More

recently, De Meza and Webb (2000) show that even a credit-rationing equilibrium may

involve excessive lending. Their model combines the assumption that entrepreneurs differ in

intrinsic quality (and not only in risk) with the moral hazard problem described by Stiglitz and

Weiss. In this model, rationing occurs as a result of moral hazard and coexists with over-

investment due to heterogeneous agents. Whether banks randomly screen customers, the

result may be more lending than the optimal situation under full information3.

1 The consequence of this market failure is under-investment (Hubbard, 1998, Jaffee and Stiglitz, 1990) and

appropriate policy is to subsidize lending. 2 Here, appropriate policy is no more to subsidize lending but to tax it.

3 In this case, “subsidizing inactivity and taxing lending may yield a Pareto improvement” (De Meza and Webb,

2000, p. 218).

3

In the two polar cases described above (credit rationing and over-financing), bankers

do not succeed in perfectly discriminating “good” firms and/or projects; the imperfection of

information leads bankers to make errors in the screening of applicants for credit. This error

can be either a lack of credit (“error à la Stiglitz and Weiss”) or an excessive offer of credit

(“error à la De Meza, Webb”), these two cases being potentially observed simultaneously on

the credit market for different agents.

The objective of this paper is to collect some evidence to identify what kind of error is

the most prevalent in the credit market for new firms. In both popular and academic presses,

there is the widespread idea that entrepreneurial activity is hampered by a limited access to

banking loans. The financing of new firms is so supposed to be a perfect field to apply the

Stiglitz and Weiss model whilst any consensus on the existence of credit rationing does not

come into view by surveying empirical studies. For instance, Evans and Jovanovic (1989),

Evans and Leighton (1989), Holtz-Eakin, Joulfaian and Rosen (1994a and 1994b) and

Johansson (2000) derive from a significant positive relationship between entrepreneur’s

wealth and the probability to become self-employed that start-ups suffer from capital gap. But

this interpretation is criticized by Cressy (1996) who supports the idea that the correlation

between financial capital and the survival of new firms is spurious and that the treatment of

endogeneity between the determinants of banking loans and those of entrepreneurial activity

stresses mainly the role of human capital4. A report by OECD (2006) supports as well the idea

that “in a number of high income OECD countries, there is little evidence of an overall

scarcity of financing for SMEs” (p. 11). Berger and Udell (1998) adopt an intermediate

position: they argue that while the macro effects of credit rationing may be small, there is

evidence to suggest that when credit is rationed for some firms it may be more readily

available to others.

Better understanding of errors made by bankers when they screen new firms may have

policy implications. Many policymakers believe that new firms have inadequate access to

banking loans as a result of market imperfections. In response, significant resources are being

channeled into the financing of new firms. For example, support programs help bankers to

finance new firms based on collateral programs and/or co-financing devices. However, if

these imperfections lead to an excessive supply of loans (and not to a lack of loans), these

solutions may be totally inappropriate.

We address these issues using a firm level qualitative data source produced by the

French National Institute of Statistics and Economic Studies (INSEE). The dataset relates to

the situation in France, during the mid-nineties. It builds on an original survey that was

carried out on a cohort of new firms set up, or taken over, during the first half of 1994.

Interestingly, this survey gathers information on both demands for credit by entrepreneurs and

supply of credit by bankers. It was no longer the case for following surveys on more recent

cohorts of new firms.

The main result is to show that credit rationing and over financing may coexist. It was

the case on the French credit market for new firms in the mid-nineties. Accordingly, the De

Meza and Webb model (2000) appears to be more appropriate than the Stiglitz and Weiss one

(1981). Even a credit-rationing equilibrium may involve excessive lending. Additionally, our

results allow identifying the determining characteristics of entrepreneurs and firms according

to their group (the credit rationing group and the excessive lending group). This is important

as they may be subject to different public policies.

4 “Provision of finance is demand-driven, with banks supplying funds elastically and business request governing

take-up. Firms self-select for funds on the basis of the human capital endowments of the proprietors with ‘better’

business more likely to borrow. A reason why others have seemingly identified start-up debt-gaps may be the

failure to test a sufficiently rich empirical model” (Cressy, 1996, p. 1253).

4

The remaining of the paper is structured as follows. Section 2 presents the data.

Section 3 introduces the empirical strategy that we designed to test new firms access to credit

and bankers’ errors. Statistical and econometric results are presented in section 4. The paper

ends with a discussion of the findings.

2. Data

We rely on the SINE data5 produced by the French National Institute of Statistics and

Economic Studies (INSEE). These data give information on the financing policy of young

firms when they are created and, where applicable, their financial problems in the following

two years. Additionally, they allow the characterization of the entrepreneur, his/her track

record, and the context. The SINE dataset does not refer to the general entrepreneurial

intention in the French population but to entrepreneurial projects that are concretized in new

firms. As a consequence, entrepreneurial intentions that are aborted due to financial

constraints are not reported. The point is of importance as the firm financing conditions are

considered.

The first-wave survey (SINE 94-1) was conducted in 1994 among a sample of 30 778

firms which had been set up or taken over during the first half of 1994, and survived at least

for one month. The sample6 is representative of the total population which was of 96 407 new

firms belonging to the private productive sector, active in the fields of industry, building,

trade and services. A second-wave survey (SINE 94-2), carried out in 1997, gives information

about the status of the same firms three years after their start: are they closed down or still

running. In the following research and for the sake of consistency, we consider only new

firms that have been active in the same field over the entire period, i.e. without change of

(branch of) activity during the period; with unvarying legal status; and set up by individuals in

the Metropolitan France, meaning that firm subsidiaries and French overseas department are

excluded. Finally we consider only new firms with banking relationships, i.e. new firms that

have asked for banking loans, at their start. We remain with a sample of 8 855 units,

representing 22 760 new firms.

3. Empirical strategy

Our empirical strategy entails two steps. First, we identify and classify bankers’ errors

by distinguishing whether they can be derived from Stiglitz-Weiss or De Meza-Webb way of

modeling credit market imperfections. Second, econometric analyses are performed to deliver

information on factors associated with access to credit, and to identify the determinants of

bankers’ errors.

To define the new firm situation regarding the credit market, we first use information

indicating whether banks were granting credit or not to the start-up (acceptance versus

refusal). We then identify bankers’ errors derived from the theoretical literature. The error “à

la Stiglitz and Weiss” (SW error) corresponds to the case of new firms that are denied credit

although they are successful in developing their project. Success is proxied by the fact that the

firm is still alive three years after the start. The error “à la De Meza and Webb” (DMW error)

refers to new firms that receive credit although they fail in developing their project; failure

being here proxied by the fact that the firm ceases activities during the three years period after

5 SINE stands for “Système d'information sur les nouvelles entreprises”.

6 It is a compulsory survey which obtained a 98.8 % rate of reply. The sample was built by randomly drawing

out samples from 416 (2x8x26) elementary strata: origin (start-up or takeover: 2 modalities), branch (8

modalities) and localization (22 French regions plus 4 overseas départements). The exploitation of the database

involves the use of a weight variable (the reverse of the draw rate per branch, per region and per origin).

5

the start. As a final point, we consider as good firms, all firms still alive after three years. It

means that we include those firms whose survival does not depend on access to credit. The

other firms, i.e. all dead firms whatever they ask and obtain, or are denied credit, are

considered as bad firms.

Our econometric modeling strategy is summarized in Table 1, where are crossed

respectively the resulting decision of the screening process by bankers, expressed in terms of

erroneous or non-erroneous decision, and the ex post observed quality of firms, i.e. are they

still alive or did they die during the three years period after the start.

Table 1: Econometric modeling strategy

Ex post quality of firm

Ex ante discrimination

of bankers

Good

Firms still alive after three

years

Bad

Firms died during the

three years period after

the start

Total

Errors Firms ask for credit and are

denied it (a): SW error

Firms ask for credit and

obtain it (c): DMW error

Errors

(a+c)

Model 4

a vs. b

Model 1 (b+c) vs. (a+d)

Model 5

c vs. d

Model 3

(a+c) vs (b+d)

Non Errors Firms ask for credit and

obtain it (b)

Firms ask for credit and

are denied it (d)

Non errors

(b+d)

Total Still alive firms

(a+b) Model 2

(a+b) vs. (c+d)

Dead firms

(c+d)

The first model (Model 1) looks for factors used to screen applicants for credit. The

model is logistic. The binary output variable corresponds to bankers’ decision. This variable is

equal to 1 when loan is granted and zero when credit is denied. We look for determinants of

the likelihood that banks will grant a loan to a start-up. This model is tested on the global

sample that concerns all firms, whatever their status may be (still alive three years after their

start, or closed down). Exogenous variables concern the characteristics of firms and those of

entrepreneurs.

The relationship between firm survival and access to credit is not trivial: when a firm

is not indebted, the risk to default is automatically reduced. To assess the impact of obtaining

credit on firm survival, another logistic model (Model 2) is tested with the status of firms

(alive or closed down) as the binary endogenous variable (equal to 1 when firms are still alive

three years after their start; 0, otherwise) and the access to credit among exogenous variables.

The third logistic model (Model 3) looks for the determinants of errors whatever these

errors may be (SW error or DMW error). We identify consequently the variables which can

be more frequently associated with errors. In this new logistic model, the endogenous variable

is equal to 1 if bankers make an error and zero otherwise.

With the estimation of two additional logistic models (Models 4 and 5), we identify

variables which are associated, first, with SW error; and, second, with DMW error. The

endogenous variable for these models is equal to 1 if bankers make a SW (a DMW) error and

zero otherwise. Estimations are respectively run on the sub-population of firms still alive

three years after their start, and on the sub-sample of dead firms.

All estimated models include several control variables characterizing the new firm and

its context: origin, branch of industry, financial public aid, start-up size, initial investment.

The other variables which have been retained describe the entrepreneur. They comprise the

entrepreneur’s human capital measured through his or her previous status, previous

occupation, level of diploma, skills acquired during previous activity, length of the experience

in the same branch of activity, size of the firm in which it was acquired, the main motive for

the business to be set-up, the present managing experience, and the number of new firms set

6

up before. We also control for the entrepreneur’s social capital linked to entrepreneurship and

business ownership (family antecedents, or friends), and other individual characteristics

(gender, age and nationality).

4. Results

4.1. Descriptive statistics

On a population of 66 873 new firms set up in 1994, only 22 760 asked indeed for

credit at the beginning of activity; meaning that only a third of new firms ask for credit at

their start. And, out of these 22 760, only 2 801 firms are denied banking loans. The rate of

loan refusals is therefore only 12.31%.

Table 2 describes the distribution of new firms with credit demand among different

cases bound to both the status of firms three years after their start (still alive or died) and the

errors of bankers (SW errors or DMW errors). Errors concern 35.49% of the sample. SW

errors only concern 5.02% of the total sample, and 14.15% of all errors made by bankers.

Most of errors are thus DMW errors. DMW errors concern 30.47% of the total sample and

85.85% of errors made by bankers. Bankers appear to grant too much credit taking into

account the final risk of default among new firms.

Table 2: Distribution of new firms with credit demand

Ex post quality of firm Good Bad Total

Ex ante discrimination

of bankers

Errors SW error DMW error Errors

1 143 6 935 8 078

5,02%*/14,15%**/8,08% 30,47%*/85,85%**/80,71% 35,49%*/100%**/35,49%***

Non Errors Non error Non error Non error

13 024 1 658 14 682

57,22%*/88,71%**/91,92%*** 7,28%*/11,29%**/19,29%*** 64,51%*/100%**/64,51%***

Total 14 167

62,25%*/62.25%**/100%***

8 593

37,75%*/37,75%**/100%***

22 760

100%*, **, ***

Lecture of the table: * % of the cell in the total sample, **% of the cell in the line, ***% of the cell in the column

7

4.2. Bankers’ decision to grant credit to new firms

Model 1 (see Table 3) identifies factors that influence the decision of bankers to grant

credit to new firms or not. The factors that influence positively the acceptance of credit

demand are, among firms’ characteristics, to buy out an existing firm rather than to start an

ex-nihilo new firm, to belong to some sectors where customers are individuals rather than

firms (Agriculture and Food Industry, Construction, Catering, Households Services), to

receive public aid and to benefit from a high financial capital (more than 100 000 kF) to start.

Among entrepreneurs’ characteristics, the factors that make it likely to receive a bank loan are

some status of the owner-manager before the start-up (being craftsman or skilled worker) and

an experience close to this new venture. On the contrary, the factors that negatively influence

the acceptance for credit demand are: to work in the branch of activity services for firms, to

have two employees or more, a low level of financial capital (less than 100 000 kF), to be a

foreigner, to be a man, to be formerly unemployed or without activity as to be workers and

executives, to be a graduate (bachelor or undergraduate), to be incited to create a firm because

of unemployment and not to benefit from an entrepreneurial environment.

We also confirm the role of financial capital to increase access to credit for new firms.

Public aid produces quite the same impact on the likelihood of firms to get access to credit.

The role of human capital, in particular the status of entrepreneur, i.e. his professional and

academic background, is more ambiguous: being graduated makes new firms’ access to credit

decrease whereas past experiences in the same field play a positive role in access to credit.

We must notice that the access of new firms to credit is an important factor, which

contributes to firms’ survival (Model 2; see Table 4). On the global population (22 760 firms),

14 157 firms are still alive after four years whereas 8 593 closed down. The decision of

bankers is an important determinant of the likelihood of firms to survive or not more than four

years. Refusals of credit to new firms by bankers indeed negatively influence the likelihood of

firms to survive as does belonging to the Catering branch of activity and employing more than

five persons. A short life span of the firm is related to entrepreneurs under 35 years old or

from 45 to 50 years old; with a professional status of middle management executive; long

term or short-term unemployed, without activity, without any degree and with an experience

which is not strictly in the same sector. On the contrary, we notice that high equity when they

start (more than 100 kf) and the allowance of public aid play, as banking loans, a positive role

in the probability of survival of new firms.

8

Table 3. Model 1: Factors affecting the decision of bankers to grant credit

Variable

Reference modality

Estimation std Wald Pr > Khi 2

Intercept 2.3051 0.1193 373.4784 <.0001

Origin Start-up Buy out 0.6486 0.0560 133.9453 <.0001

Branch of Activity

Trade

Agriculture and food industry 1.1236 0.1744 41.5163 <.0001

Industry 0.1202 0.0847 2.0163 0.1556

Transportation 0.4003 0.0806 24.6877 <.0001

Construction 0.1782 0.0968 3.3865 0.0657

Catering 0.5336 0.0783 46.4981 <.0001

Household services 0.8635 0.0870 98.4238 <.0001

Services to firms -0.2360 0.0727 10.5501 0.0012

Public financial aid Non obtained Obtained 0.7361 0.0567 168.5946 <.0001

Initial size of the firm

No employee

1 employee -0.1026 0.0598 2.9456 0.0861

2 – 5 employees -0.1823 0.0646 7.9616 0.0048

+ 5 employees -1.0140 0.1094 85.9699 <.0001

Total amount of money invested at the beginning

7623 - 15244 euros

Less than 1525 euros -1.0184 0.0875 135.4209 <.0001

1525 – 3811 euros -0.5136 0.0775 43.8970 <.0001

3812 – 7622 euros -0.1836 0.0693 7.0185 0.0081

15245– 38112 euros 0.2857 0.0648 19.4462 <.0001

38113 – 76225 euros 0.7012 0.0860 66.5384 <.0001

76226 – 152450 euros 1.0278 0.1142 81.0397 <.0001

+ 152450 euros 2.5393 0.2314 120.4475 <.0001

Nationality

French

European foreigner -0.3061 0.1207 6.4277 0.0112

Non European foreigner -1.3153 0.0974 182.3957 <.0001

Gender Woman Man -0.2517 0.0555 20.5342 <.0001

Age of the entrepreneur

30 – 35 years old

- 25 years old 0.1834 0.0917 3.9942 0.0457

25 – 30 years old 0.2562 0.0729 12.3535 0.0004

35 – 40 years old 0.0826 0.0717 1.3280 0.2492

40 – 45 years old 0.3164 0.0768 16.9694 <.0001

45 – 50 years old 0.1395 0.0830 2.8265 0.0927

+ 50 years old 0.1972 0.0962 4.2006 0.0404

Previous professional status Employee

Craftsman 0.3535 0.1004 12.4024 0.0004

Manager -0.1512 0.1211 1.5604 0.2116

Supervisor worker 0.2188 0.1091 4.0221 0.0449

Middle management position -0.1820 0.0899 4.0954 0.0430

Executive -0.1371 0.0785 3.0477 0.0809

Worker -0.1543 0.0714 4.6656 0.0308

Student -0.0691 0.0907 0.5808 0.4460

Previous occupation of the entrepreneur

Labor force

Short term unemployed -0.8298 0.0664 156.1301 <.0001

Long term unemployed -1.1112 0.0747 221.3827 <.0001

Non-working -0.6861 0.1129 36.9500 <.0001

Level of diploma

Intermediate level

No diploma 0.00707 0.0750 0.0089 0.9248

Secondary school diploma -0.1539 0.0638 5.8200 0.0158

Till two years at university -0.2095 0.0787 7.0827 0.0078

From three years and more at university -0.0471 0.0894 0.2770 0.5987

Experience in the same branch of activity

No experience

Close vocational experience 0.2536 0.0695 13.3078 0.0003

Different experience -0.2088 0.0825 6.4021 0.0114

Close experience for the partner -0.2131 0.1256 2.8805 0.0897

Length of the experience

More than 10 years

No experience -0.3583 0.1559 5.2792 0.0216

3 years experience -0.4205 0.0822 26.1526 <.0001

3 – 10 years experience -0.1406 0.0678 4.3015 0.0381

Size of the firm in which the experience was acquired

Between 4 and 9 employees

Less than 3 employees 0.00640 0.0767 0.0070 0.9335

Between 10 and 49 employees 0.1576 0.0806 3.8234 0.0505

Between 50 and 99 employees -0.4706 0.1160 16.4645 <.0001

Between 100 and 199 employees 0.2734 0.1506 3.2929 0.0696

Between 200 and 499 employees -0.5882 0.1446 16.5503 <.0001

More than 500 employees -0.3006 0.1172 6.5796 0.0103

Entrepreneurship "milieu" Family or friends No -0.1479 0.0496 8.9099 0.0028

Main motivation to set up his firm

Taste for entrepreneurship

Start for new idea -0.0911 0.0848 1.1538 0.2828

Catch an opportunity 0.0553 0.0596 0.8628 0.3529

Start for necessity -0.4806 0.0637 56.8594 <.0001

Example of the surrounding 0.0137 0.1221 0.0125 0.9110

Present exercise of entrepreneur role No Yes -0.2057 0.0807 6.4916 0.0108

Previous setting up of new firms

No

1 start up -0.3912 0.0735 28.3205 <.0001

2 or 3 start ups -0.5120 0.1085 22.2685 <.0001

+ 4 start ups -0.7590 0.1895 16.0411 <.0001

9

Table 4. Model 2: Factors affecting the survival of new firms

Variable

Reference modality

Estimation std Wald Pr > Khi 2

Intercept 0.3950 0.0802 24.2707 <.0001

Bank loan asked accepted Denial of credit -0.6756 0.0460 216.0252 <.0001

Origin Start-up Buy out 0.6767 0.0356 361.3093 <.0001

Branch of Activity

Trade

Agriculture and food industry 0.1979 0.0834 5.6328 0.0176

Industry 0.3497 0.0623 31.5000 <.0001

Transportation 0.4978 0.0585 72.3142 <.0001

Construction 0.6319 0.0724 76.1305 <.0001

Catering -0.3257 0.0460 50.1399 <.0001

Household services 0.6119 0.0532 132.1264 <.0001

Services to firms -0.0498 0.0561 0.7868 0.3751

Public financial aid Non obtained Obtained 0.1471 0.0403 13.2992 0.0003

Initial size of the firm No employee

1 employee 0.0295 0.0400 0.5436 0.4609

2 – 5 employees -0.0422 0.0425 0.9841 0.3212

+ 5 employees -0.3301 0.0826 15.9769 <.0001

Total amount of money invested at the beginning

7623 - 15245 euros

Less than 1525 euros -0.0423 0.0741 0.3257 0.5682

1525 – 3811 euros 0.0659 0.0600 1.2086 0.2716

3812 – 7622 euros 0.0728 0.0509 2.0473 0.1525

15245– 38112 euros 0.3500 0.0443 62.4807 <.0001

38113 – 76225 euros 0.7367 0.0539 187.1441 <.0001

76226 – 152450 euros 0.9104 0.0643 200.4301 <.0001

+ 152450 euros 1.2156 0.0836 211.3771 <.0001

Nationality French

European foreigner 0.3345 0.0927 13.0136 0.0003

Non European foreigner -0.1037 0.0898 1.3326 0.2483

Gender Woman Man 0.0843 0.0363 5.3951 0.0202

Age of the entrepreneur 30 – 35 years old

- 25 years old -0.5509 0.0642 73.5986 <.0001

25 – 30 years old -0.2507 0.0500 25.0993 <.0001

35 – 40 years old -0.0873 0.0505 2.9907 0.0837

40 – 45 years old -0.1012 0.0524 3.7313 0.0534

45 – 50 years old -0.1786 0.0567 9.9143 0.0016

+ 50 years old -0.1235 0.0675 3.3473 0.0673

Previous professional status Employee

Craftsman 0.0623 0.0620 1.0100 0.3149

Manager 0.1772 0.0899 3.8896 0.0486

Supervisor worker 0.4160 0.0717 33.6759 <.0001

Middle management position -0.0486 0.0651 0.5559 0.4559

Executive 0.2454 0.0543 20.4434 <.0001

Worker 0.2322 0.0490 22.4341 <.0001

Student -0.1082 0.0653 2.7513 0.0972

Previous occupation of the entrepreneur

Labor force

Short term unemployed -0.2714 0.0456 35.4986 <.0001

Long term unemployed -0.3533 0.0533 43.9530 <.0001

Non-working -0.6923 0.0776 79.5783 <.0001

Level of diploma

Intermediate level

No diploma -0.3076 0.0520 35.0441 <.0001

Secondary school diploma 0.1046 0.0435 5.7763 0.0162

Till two years at university 0.1511 0.0547 7.6419 0.0057

From three years and more at university 0.6733 0.0661 103.7856 <.0001

Experience in the same branch of activity

No experience

Close vocational experience -0.4646 0.0466 99.3689 <.0001

Different experience -0.8670 0.0559 240.5805 <.0001

Close experience for the partner -0.8467 0.0827 104.8190 <.0001

Length of the experience More than 10 years

No experience -0.4188 0.1141 13.4595 0.0002

3 years experience -0.2338 0.0579 16.3128 <.0001

3 – 10 years experience -0.1384 0.0460 9.0539 0.0026

Size of the firm in which the experience was acquired

Between 4 and 9 employees

Less than 3 employees -0.00345 0.0508 0.0046 0.9458

Between 10 and 49 employees -0.2045 0.0550 13.8224 0.0002

Between 50 and 99 employees -0.2677 0.0895 8.9479 0.0028

Between 100 and 199 employees -0.0439 0.1058 0.1720 0.6784

Between 200 and 499 employees -0.1486 0.1168 1.6197 0.2031

More than 500 employees -0.3360 0.0824 16.6229 <.0001

Entrepreneurship "milieu" Family or friends No 0.0753 0.0350 4.6426 0.0312

Main motivation to set up his firm

Taste for entrepreneurship

Start for new idea -0.0706 0.0602 1.3757 0.2408

Catch an opportunity 0.1240 0.0384 10.4460 0.0012

Start for necessity -0.2156 0.0481 20.0836 <.0001

Example of the surrounding -0.1850 0.0824 5.0415 0.0247

Present exercise of entrepreneur role No Yes 0.0897 0.0568 2.4935 0.1143

Previous setting up of new firms

No

1 start up -0.0351 0.0531 0.4362 0.5090

2 or 3 start ups -0.6696 0.0750 79.7467 <.0001

+ 4 start ups 0.2013 0.1519 1.7575 0.1849

10

4.3. Errors made by bankers when they screen new firms

As shown by estimation of Model 3 (see Table 5), errors are positively linked with the

allowance of public aid to new firms. Errors are more frequent when entrepreneurs are

European ones, when they are over 50 years old, when they were executives or without

activity, when they are undergraduate, without experience or with an experience of less than

three years, when their motivation to create a firm is to escape unemployment and when they

created several firms in the past. On the contrary, errors are less frequent when firms survive,

when they are denied credit at birth, when they are takeovers, from several sectors

(Agriculture and Food Industry, Building, Transportation, Hotels/Restaurant, Services), when

the size (number of employees and total equity to start) is rather high, when entrepreneurs are

non European ones, when they are men, supervisor workers before starting the new firm and

unemployed for a short term.

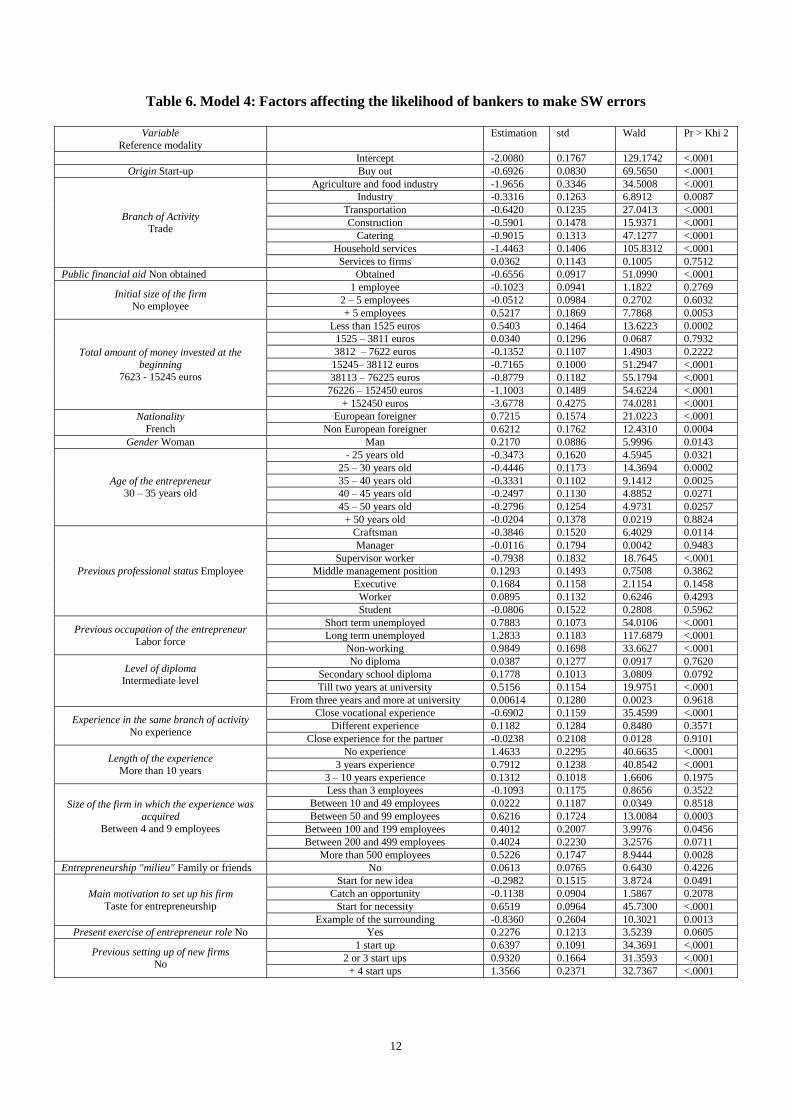

By testing the Model 4 (see Table 6), we identify factors affecting the likelihood of

SW errors. On the population of firms which are still alive three years after their start (14 167

firms), the SW error concerns 1 143 firms. SW Errors are positively linked with a high

number of employees (more than five) and a small amount of equity at the beginning of firms’

life (less than 10 kF). This error is more frequent when the entrepreneurs are not French,

when they are men, when they are unemployed (short and long term) or without any activity,

when they are undergraduate, when their experience is inferior to 3 years, when the desire to

start a new firm is bound to unemployment or when they created more than, at least, one firm

in the past. SW errors are negatively linked with buyouts, all sectors except services to firms,

the allowance of public aid, high equity at the beginning, a past experience of entrepreneurs as

craftsmen or supervisor workers, a close experience before starting and a motive to create a

new firm based on new idea and in an entrepreneurial context.

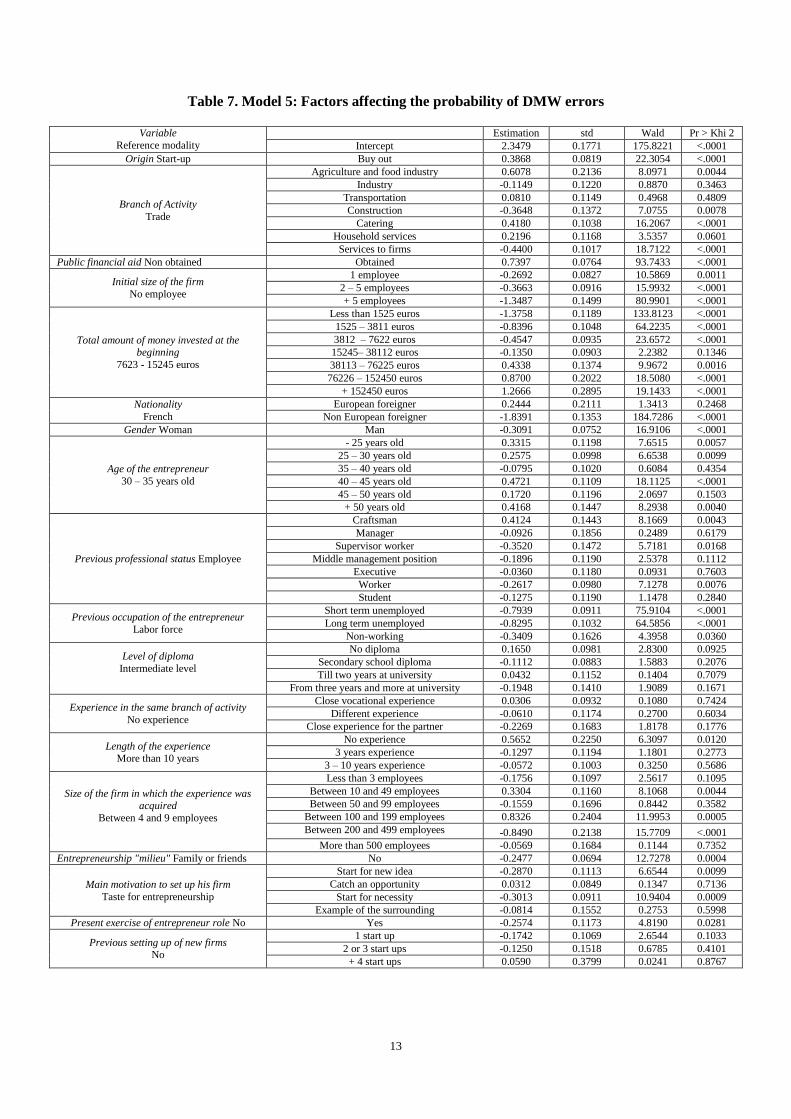

By testing the Model 5 (see Table 7), we identify factors affecting the frequency of

DMW errors. On the population of firms which did not survive in the three years after they

start (8 593 firms), the DMW errors concern 6 935 firms. DMW errors are positively linked

with buyouts, some sectors (Agriculture and food industry, Hotels and restaurants, … ), public

aid, high equity at the beginning of firms’ life (more than 250 kF) and past experience of

entrepreneurs as craftsmen. Public aids in this case are a source of inefficiency on the credit

market. Buyouts or high equity are interpreted as signal of quality that can finally hide the

reality of high risks to bankers. DMW Errors are negatively linked to other sectors (transport,

services to firms) and to a small amount of equity at the beginning of firms’ life (less than 50

kF). DMW errors decrease when firm employs at least one employee, when the entrepreneur

is non European, when they are men rather than women, supervisor workers, executives, or

skilled and unskilled workers, when they are unemployed (short and long term) or without

any activity, with diploma (A-level or postgraduate) and when their motive to create is based

on escaping unemployment.

11

Table 5. Model 3: Factors affecting the likelihood of bankers to make errors

Variable

Reference modality

Estimation std Wald Pr > Khi 2

Intercept 2.2010 0.1193 340.4779 <.0001

Status of the firm closed down Still alive -4.0704 0.0477 7287.0029 <.0001

Bank loan asked accepted Denial of credit -0.8890 0.0613 210.0244 <.0001

Origin Start-up Buy out -0.1355 0.0509 7.0725 0.0078

Branch of Activity Trade

Agriculture and food industry -0.2874 0.1201 5.7290 0.0167

Industry -0.1239 0.0876 2.0010 0.1572

Transportation -0.1792 0.0834 4.6122 0.0317

Construction -0.4066 0.1021 15.8629 <.0001

Catering 0.0265 0.0660 0.1609 0.6883

Household services -0.4694 0.0749 39.2621 <.0001

Services to firms -0.1686 0.0791 4.5422 0.0331

Public financial aid Non obtained Obtained 0.1208 0.0564 4.5917 0.0321

Initial size of the firm No employee

1 employee -0.2053 0.0573 12.8582 0.0003

2 – 5 employees -0.2693 0.0602 20.0026 <.0001

+ 5 employees -0.7059 0.1142 38.2191 <.0001

Total amount of money invested at the

beginning

7623 - 15245 euros

Less than 1525 euros -0.7256 0.1013 51.261 <.0001

1525 – 3811 euros -0.4545 0.0851 28.5362 <.0001

3812 – 7622 euros -0.287 0.0735 15 <.0001

15245– 38112 euros -0.3158 0.0643 24.0875 <.0001

38113 – 76225 euros -0.264 0.0764 11.9216 0.0006

76226 – 152450 euros -0.3179 0.0909 12.2205 0.0005

+ 152450 euros -0.9084 0.1157 61.6601 <.0001

Nationality

French

European foreigner 0.5772 0.1248 21.3885 <.0001

Non European foreigner -0.962 0.1178 66.7172 <.0001

Gender Woman Man -0.101 0.052 3.7735 0.0521

Age of the entrepreneur 30 – 35 years old

- 25 years old 0.0512 0.0908 0.3179 0.5728

25 – 30 years old -0.0482 0.0711 0.4587 0.4982

35 – 40 years old -0.1262 0.0718 3.0901 0.0788

40 – 45 years old 0.0872 0.0743 1.3779 0.2405

45 – 50 years old 0.012 0.0802 0.0225 0.8807

+ 50 years old 0.2945 0.0951 9.5924 0.002

Previous professional status Employee

Craftsman -0.0639 0.0896 0.5094 0.4754

Manager 0.24 0.124 3.7416 0.0531

Supervisor worker -0.3421 0.1025 11.1423 0.0008

Middle management position -0.1077 0.0913 1.3923 0.238

Executive 0.1573 0.0769 4.1806 0.0409

Worker -0.1121 0.0703 2.5426 0.1108

Student -0.1314 0.0907 2.0956 0.1477

Previous occupation of the entrepreneur

Labor force

Short term unemployed -0.1486 0.0643 5.3462 0.0208

Long term unemployed 0.1129 0.0752 2.2559 0.1331

Non-working 0.2993 0.1095 7.4651 0.0063

Level of diploma Intermediate level

No diploma -0.00212 0.0727 0.0009 0.9767

Secondary school diploma -0.0428 0.0623 0.4707 0.4927

Till two years at university 0.1752 0.0782 5.0238 0.025

From three years and more at university 0.0966 0.0887 1.1862 0.2761

Experience in the same branch of activity

No experience

Close vocational experience -0.2407 0.0672 12.8213 0.0003

Different experience 0.1525 0.0788 3.7453 0.053

Close experience for the partner 0.0353 0.1181 0.0892 0.7652

Length of the experience

More than 10 years

No experience 0.97 0.1626 35.5887 <.0001

3 years experience 0.2592 0.0822 9.9518 0.0016

3 – 10 years experience 0.099 0.0653 2.2962 0.1297

Size of the firm in which the experience was

acquired

Between 4 and 9 employees

Less than 3 employees -0.1784 0.0726 6.0352 0.014

Between 10 and 49 employees 0.2054 0.0775 7.0218 0.0081

Between 50 and 99 employees 0.2554 0.1234 4.2817 0.0385

Between 100 and 199 employees 0.6614 0.1466 20.3554 <.0001

Between 200 and 499 employees -0.3904 0.169 5.3388 0.0209

More than 500 employees 0.1449 0.1155 1.5742 0.2096

Entrepreneurship "milieu" Family or friends No -0.079 0.0497 2.5274 0.1119

Main motivation to set up his firm

Taste for entrepreneurship

Start for new idea -0.384 0.0847 20.5393 <.0001

Catch an opportunity 0.0773 0.0542 2.0319 0.154

Start for necessity 0.162 0.069 5.508 0.0189

Example of the surrounding -0.2141 0.1161 3.4028 0.0651

Present exercise of entrepreneur role No Yes 0.0567 0.0808 0.4921 0.483

Previous setting up of new firms No

1 start up 0.2481 0.0745 11.0855 0.0009

2 or 3 start ups 0.345 0.1078 10.2357 0.0014

+ 4 start ups 1.1797 0.1871 39.7596 <.0001

12

Table 6. Model 4: Factors affecting the likelihood of bankers to make SW errors

Variable

Reference modality

Estimation std Wald Pr > Khi 2

Intercept -2.0080 0.1767 129.1742 <.0001

Origin Start-up Buy out -0.6926 0.0830 69.5650 <.0001

Branch of Activity Trade

Agriculture and food industry -1.9656 0.3346 34.5008 <.0001

Industry -0.3316 0.1263 6.8912 0.0087

Transportation -0.6420 0.1235 27.0413 <.0001

Construction -0.5901 0.1478 15.9371 <.0001

Catering -0.9015 0.1313 47.1277 <.0001

Household services -1.4463 0.1406 105.8312 <.0001

Services to firms 0.0362 0.1143 0.1005 0.7512

Public financial aid Non obtained Obtained -0.6556 0.0917 51.0990 <.0001

Initial size of the firm No employee

1 employee -0.1023 0.0941 1.1822 0.2769

2 – 5 employees -0.0512 0.0984 0.2702 0.6032

+ 5 employees 0.5217 0.1869 7.7868 0.0053

Total amount of money invested at the

beginning

7623 - 15245 euros

Less than 1525 euros 0.5403 0.1464 13.6223 0.0002

1525 – 3811 euros 0.0340 0.1296 0.0687 0.7932

3812 – 7622 euros -0.1352 0.1107 1.4903 0.2222

15245– 38112 euros -0.7165 0.1000 51.2947 <.0001

38113 – 76225 euros -0.8779 0.1182 55.1794 <.0001

76226 – 152450 euros -1.1003 0.1489 54.6224 <.0001

+ 152450 euros -3.6778 0.4275 74.0281 <.0001

Nationality French

European foreigner 0.7215 0.1574 21.0223 <.0001

Non European foreigner 0.6212 0.1762 12.4310 0.0004

Gender Woman Man 0.2170 0.0886 5.9996 0.0143

Age of the entrepreneur 30 – 35 years old

- 25 years old -0.3473 0.1620 4.5945 0.0321

25 – 30 years old -0.4446 0.1173 14.3694 0.0002

35 – 40 years old -0.3331 0.1102 9.1412 0.0025

40 – 45 years old -0.2497 0.1130 4.8852 0.0271

45 – 50 years old -0.2796 0.1254 4.9731 0.0257

+ 50 years old -0.0204 0.1378 0.0219 0.8824

Previous professional status Employee

Craftsman -0.3846 0.1520 6.4029 0.0114

Manager -0.0116 0.1794 0.0042 0.9483

Supervisor worker -0.7938 0.1832 18.7645 <.0001

Middle management position 0.1293 0.1493 0.7508 0.3862

Executive 0.1684 0.1158 2.1154 0.1458

Worker 0.0895 0.1132 0.6246 0.4293

Student -0.0806 0.1522 0.2808 0.5962

Previous occupation of the entrepreneur

Labor force

Short term unemployed 0.7883 0.1073 54.0106 <.0001

Long term unemployed 1.2833 0.1183 117.6879 <.0001

Non-working 0.9849 0.1698 33.6627 <.0001

Level of diploma Intermediate level

No diploma 0.0387 0.1277 0.0917 0.7620

Secondary school diploma 0.1778 0.1013 3.0809 0.0792

Till two years at university 0.5156 0.1154 19.9751 <.0001

From three years and more at university 0.00614 0.1280 0.0023 0.9618

Experience in the same branch of activity

No experience

Close vocational experience -0.6902 0.1159 35.4599 <.0001

Different experience 0.1182 0.1284 0.8480 0.3571

Close experience for the partner -0.0238 0.2108 0.0128 0.9101

Length of the experience

More than 10 years

No experience 1.4633 0.2295 40.6635 <.0001

3 years experience 0.7912 0.1238 40.8542 <.0001

3 – 10 years experience 0.1312 0.1018 1.6606 0.1975

Size of the firm in which the experience was

acquired

Between 4 and 9 employees

Less than 3 employees -0.1093 0.1175 0.8656 0.3522

Between 10 and 49 employees 0.0222 0.1187 0.0349 0.8518

Between 50 and 99 employees 0.6216 0.1724 13.0084 0.0003

Between 100 and 199 employees 0.4012 0.2007 3.9976 0.0456

Between 200 and 499 employees 0.4024 0.2230 3.2576 0.0711

More than 500 employees 0.5226 0.1747 8.9444 0.0028

Entrepreneurship "milieu" Family or friends No 0.0613 0.0765 0.6430 0.4226

Main motivation to set up his firm

Taste for entrepreneurship

Start for new idea -0.2982 0.1515 3.8724 0.0491

Catch an opportunity -0.1138 0.0904 1.5867 0.2078

Start for necessity 0.6519 0.0964 45.7300 <.0001

Example of the surrounding -0.8360 0.2604 10.3021 0.0013

Present exercise of entrepreneur role No Yes 0.2276 0.1213 3.5239 0.0605

Previous setting up of new firms No

1 start up 0.6397 0.1091 34.3691 <.0001

2 or 3 start ups 0.9320 0.1664 31.3593 <.0001

+ 4 start ups 1.3566 0.2371 32.7367 <.0001

13

Table 7. Model 5: Factors affecting the probability of DMW errors

Variable

Reference modality

Estimation std Wald Pr > Khi 2

Intercept 2.3479 0.1771 175.8221 <.0001

Origin Start-up Buy out 0.3868 0.0819 22.3054 <.0001

Branch of Activity

Trade

Agriculture and food industry 0.6078 0.2136 8.0971 0.0044

Industry -0.1149 0.1220 0.8870 0.3463

Transportation 0.0810 0.1149 0.4968 0.4809

Construction -0.3648 0.1372 7.0755 0.0078

Catering 0.4180 0.1038 16.2067 <.0001

Household services 0.2196 0.1168 3.5357 0.0601

Services to firms -0.4400 0.1017 18.7122 <.0001

Public financial aid Non obtained Obtained 0.7397 0.0764 93.7433 <.0001

Initial size of the firm

No employee

1 employee -0.2692 0.0827 10.5869 0.0011

2 – 5 employees -0.3663 0.0916 15.9932 <.0001

+ 5 employees -1.3487 0.1499 80.9901 <.0001

Total amount of money invested at the beginning

7623 - 15245 euros

Less than 1525 euros -1.3758 0.1189 133.8123 <.0001

1525 – 3811 euros -0.8396 0.1048 64.2235 <.0001

3812 – 7622 euros -0.4547 0.0935 23.6572 <.0001

15245– 38112 euros -0.1350 0.0903 2.2382 0.1346

38113 – 76225 euros 0.4338 0.1374 9.9672 0.0016

76226 – 152450 euros 0.8700 0.2022 18.5080 <.0001

+ 152450 euros 1.2666 0.2895 19.1433 <.0001

Nationality

French

European foreigner 0.2444 0.2111 1.3413 0.2468

Non European foreigner -1.8391 0.1353 184.7286 <.0001

Gender Woman Man -0.3091 0.0752 16.9106 <.0001

Age of the entrepreneur

30 – 35 years old

- 25 years old 0.3315 0.1198 7.6515 0.0057

25 – 30 years old 0.2575 0.0998 6.6538 0.0099

35 – 40 years old -0.0795 0.1020 0.6084 0.4354

40 – 45 years old 0.4721 0.1109 18.1125 <.0001

45 – 50 years old 0.1720 0.1196 2.0697 0.1503

+ 50 years old 0.4168 0.1447 8.2938 0.0040

Previous professional status Employee

Craftsman 0.4124 0.1443 8.1669 0.0043

Manager -0.0926 0.1856 0.2489 0.6179

Supervisor worker -0.3520 0.1472 5.7181 0.0168

Middle management position -0.1896 0.1190 2.5378 0.1112

Executive -0.0360 0.1180 0.0931 0.7603

Worker -0.2617 0.0980 7.1278 0.0076

Student -0.1275 0.1190 1.1478 0.2840

Previous occupation of the entrepreneur

Labor force

Short term unemployed -0.7939 0.0911 75.9104 <.0001

Long term unemployed -0.8295 0.1032 64.5856 <.0001

Non-working -0.3409 0.1626 4.3958 0.0360

Level of diploma

Intermediate level

No diploma 0.1650 0.0981 2.8300 0.0925

Secondary school diploma -0.1112 0.0883 1.5883 0.2076

Till two years at university 0.0432 0.1152 0.1404 0.7079

From three years and more at university -0.1948 0.1410 1.9089 0.1671

Experience in the same branch of activity

No experience

Close vocational experience 0.0306 0.0932 0.1080 0.7424

Different experience -0.0610 0.1174 0.2700 0.6034

Close experience for the partner -0.2269 0.1683 1.8178 0.1776

Length of the experience

More than 10 years

No experience 0.5652 0.2250 6.3097 0.0120

3 years experience -0.1297 0.1194 1.1801 0.2773

3 – 10 years experience -0.0572 0.1003 0.3250 0.5686

Size of the firm in which the experience was acquired

Between 4 and 9 employees

Less than 3 employees -0.1756 0.1097 2.5617 0.1095

Between 10 and 49 employees 0.3304 0.1160 8.1068 0.0044

Between 50 and 99 employees -0.1559 0.1696 0.8442 0.3582

Between 100 and 199 employees 0.8326 0.2404 11.9953 0.0005

Between 200 and 499 employees -0.8490 0.2138 15.7709 <.0001

More than 500 employees -0.0569 0.1684 0.1144 0.7352

Entrepreneurship "milieu" Family or friends No -0.2477 0.0694 12.7278 0.0004

Main motivation to set up his firm

Taste for entrepreneurship

Start for new idea -0.2870 0.1113 6.6544 0.0099

Catch an opportunity 0.0312 0.0849 0.1347 0.7136

Start for necessity -0.3013 0.0911 10.9404 0.0009

Example of the surrounding -0.0814 0.1552 0.2753 0.5998

Present exercise of entrepreneur role No Yes -0.2574 0.1173 4.8190 0.0281

Previous setting up of new firms No

1 start up -0.1742 0.1069 2.6544 0.1033

2 or 3 start ups -0.1250 0.1518 0.6785 0.4101

+ 4 start ups 0.0590 0.3799 0.0241 0.8767

14

5. Discussion and conclusion

Our applied research sought to challenge existing and competing theories about credit

access. Regarding this aim, we first have shown that the constraint described by Stiglitz and

Weiss (1981) was not highly spread among French new firms during the mid-nineties. The

imperfection of the credit market described by DMW is a much more realistic model. Thus, in

a way, we confirm on the French case the result given by Cressy (1996) concerning British

new firms.

More originally, by examining factors affecting credit access, we confirm the positive

effect of both financial capital and public aid on access to credit. However, we emphasize the

negative effects of public aid on the quality of bankers’ discrimination. When public aid is

allowed, the likelihood that bankers make errors increases. The screening process used by

bankers is less efficient as soon as firms receive public aid. This result is due to the influence

of financial backing on the frequency of DMW errors. Public aid makes the errors “à la

DMW” increase. On the contrary, we notice that the SW error is negatively bound to public

aids. In this case, the likelihood of credit rationing “à la SW” decreases: firms are less often

excluded from the market of credit when they are eligible for them. We observe the same

effects on access to credit referring to high equity level at the start of the firm. As public aid

and/or relatively high capital contribution improve firms’ financial accounts, bankers are less

severe in their screening process and too optimistic when they assess firms’ risks of default.

The likelihood of errors and the nature of them are dependent on the firms’

characteristics, in particular the circumstances at their start. Financing takeovers is easier than

financing ex nihilo new firms. The global likelihood of bankers’ errors decreases. The effect

on bankers’ errors of this variable is very similar to the effect of financial capital. They both

make the likelihood of DMW errors increase whereas they make the likelihood of SW errors

decrease. On the contrary, when firms belong to the sector of services, their access to credit is

limited but bankers’ errors are less frequent.

The likelihood of errors and the nature of them are dependent on the entrepreneurs’

characteristics too. In particular, human capital (degree and experience) and personal

characteristics play a significant role in access to credit and in the nature of errors made by

bankers. When entrepreneurs are undergraduates, the access of new firms to credit decreases

and, at the same time, bankers’ errors increase. More precisely, we notice the increase in the

SW errors frequency when entrepreneurs are undergraduate. The same effect on errors is

identified when the experience of entrepreneur is inferior to three years before starting a new

firm. A low human capital identified by banks leads new firms to more credit rationing. We

confirm the positive role played by the observed human capital based on diploma and past

experiences. Concerning personal characteristics, we highlight the effect of the nationality of

entrepreneurs and their status on the job market too. As a whole, the screening process of

bankers appears to be more efficient when entrepreneurs are not European and when they are

not unemployed for a long time. In these cases, DMW errors are generally less frequent but

credit rationing (SW errors) is much higher. The screening process of banks is too severe in

comparison with the level of ex post risk and some projects are not financed by banks

although firms finally do not fail.

15

6. References

Allen F, Santomero A., (1998), “The Theory of Financial Intermediation”, Journal of Banking and

Finance, 21, 1461-1485.

Benston G., Smith C., (1976), “A Transaction Cost Approach To the Theory of Financial

Intermediation”, Journal of Finance, 2, 215-231.

Berger A., Udell G., (1998), “The Economics of Small Business Finance: The Roles of Private Equity

and Debt Markets In the Financial Growth Cycle”, Journal of Banking and Finance, 22, 613-673.

Bhattacharya S., Boot A., Thakor A., (2004), Credit, Intermediation and the Macroeconomy, OUP: Oxford.

Bhattacharya S., Thakor A., (1993) “Contemporary Banking Theory”, Journal of Financial

Intermediation, 3, 2-50.

Cressy R., (1996), “Are Business Start-ups Debt-Rationed?” Economic Journal, 438, pp. 1253-1270.

De Meza D.E., Webb D.C., (2006), “Credit Rationing: Something's Gotta Give”, Economica, 73, 563-578.

De Meza D.E., (2002), “Over lending”, The Economic Journal, 112, pp.17-30.

De Meza D.E., Webb, D.C., (1987), “Too Much Investment: a Problem of Asymmetric Information”,

Quarterly Journal of Economics, 102, 281-292.

De Meza D.E., Webb, D.C., (2000), “Does Credit Rationing Imply Insufficient Lending?” Journal of

Public Economics, 78, 215-234.

Diamond D., Rajan R., (2001), “Liquidity Risk, Creation and Financial Fragility: A Theory Of

Banking”, Journal of Political Economy, 2, 287-327.

Diamond D.W., (1984), “Financial Intermediation and Delegated Monitoring “, Journal of Economic

Studies, vol. LI, 393-414.

Evans D. S., Leighton L., (1989), “Some Empirical Aspects of Entrepreneurship”, American

Economic Review, 79 (3), 519-535.

Evans D., Jovanovic B., (1989), “An Estimated Model of Entrepreneurial Choice under Liquidity

Constraints”, Journal of Political Economy, 97(4), 808-827.

Evans D., Leighton L., (1989), “Some Empirical Aspects of Entrepreneurship”, American Economic

Review, 79(3), 519-535.

Fama E.F., (1985), “What’s Different about Banks ?”, Journal of Monetary Economic, 1, pp. 29-39.

Freixas X., Rochet J., (1999), Microeconomics of Banking, MIT Press : Cambridge (Mass.).

Goodhart C.A.E. (1989), Money, Information and Uncertainty, Macmillan: Basingstoke.

Holtz-Eakin D., Joulfaian D., Rosen H., (1994a), “Entrepreneurial Decisions and Liquidity

Constraints”, Rand Journal of Economics, 25(2), 334-347.

Holtz-Eakin, D., Joulfaian, D., Rosen H.S., (1994b), “Sticking It Out: Entrepreneurial Survival and

Liquidity Constraints”, Journal of Political Economy, 102 (1), 53-75.

Hubbard G., (1998), “Capital-Market Imperfections and Investment”, Journal of Economic Literature,

36(1), pp. 193-225.

Jaffee D., Stiglitz J.E., (1990): “Credit rationing” in B.M. Friedman and F.H. Hahn (Eds.): Handbook

of Monetary Economics, vol. II, North Holland, pp. 838-888.

Johansson E., (2000), “Self-employment and Liquidity Constraints: Evidence from Finland”,

Scandinavian Journal of Economics, 102(1), pp. 123-134.

Keynes J.M., (1930), A Treatise on Money, in The Collected Writings of John Maynard Keynes,

Volume VI, The Applied Theory of Money, New York, Cambridge University Press, 1971.

OECD, 2006, The SME Financing Gap: Theory and Evidence, tome I, Paris: OECD,

Ruhle I., (1997), “Why Banks? Microeconomic Foundation of Financial Intermediaries”, Development

and Finance, 3, 10-99.

Stiglitz J.E., Weiss A., (1981), “Credit Rationing In Markets With Imperfect Information”, The

American Economic Review, n°3, pp. 349-410.