Embed Size (px)

Citation preview

3 -/3-/d

4 REPORT TO THE CONGRESS"Ccou

Examination Of Financial Statements~,eanama Canal Company And

. ,ll1anal Zone Government" Fiscal Years 1969 And 1968 8-114839

BY THE COMPTROLLER GENERALOF THE UNITED STATES

ARCH 13,19 70zaX>,L, a 3s

COMPTROLLER GENERAL 6'FrtHE UNITED STATES

WASHINGTON., D.C. 20548

B-114839

To the President of the Senate and the

Speaker of the House of Representatives

This is our report on the examination of financial

statements of the Panama Canal Company for the fiscal

years ended June 30, 1969, and June 30, 1968, which is re-

quired by the Government Corporation Control Act

(31 U.S.C. 841), and on the examination of financial state-

ments of the Canal Zone Government for fiscal years 1969

and 1968.

Copies of this report are being sent to the Director,

Bureau of the Budget; the Secretary of the Army; and the

President of the Panama Canal Company.

Comptroller General

of the United States

ContentsPage

DIGEST 1

CHAPTER

1 INTRODUCTION 3

2 COMMENTS ON DEPRECIATION, ACCOUNTS RECEIV-

ABLE, AND ADMINISTRATIVE EXPENSES -10Depreciation not recorded on certain

fixed assets 10

Accounts receivable from the Republicof Panama 12

Certain costs not included in CanalZone Government results of operations 14

3 SCOPE OF EXAMINATION 16

4 OPINIONS OF FINANCIAL STATEMENTS 17

ScheduleFINANCIAL STATEMENTS

Panama Canal Company:Comparative statement of

financial conditionJune 30, 1969 and 1968 1 21

Comparative statement ofrevenue and expenses,fiscal years endedJune 30, 1969 and 1968 2 22

Statement of changes inequity of the U.S. Gov-ernment:

Fiscal year endedJune 30, 1969 3a 23

Fiscal year endedJune 30, 1968 3b 24

PagKeSchedule

Comparative statement offixed assets, June 30,1969 and 1968 4 25

Comparative statement ofsource and applicationof funds for fiscalyears ended June 30,1969 and 1968 5 26

Notes to financial state-ments 27

Canal Zone Government:Comparative statement offinancial condition,June 30, 1969 and 1968 6 31

Statement of changes inequity of the U.S. Gov-ernment:June 30, 1969 7a 32June 30, 1968 7b 33

Statement of operations:Fiscal year endedJune 30, 1969 8a 34

Fiscal year endedJune 30, 1968 8b 35

Comparative statement offixed assets, June 30,1969 and 1968 9 36

Notes to financial state-ments 37

ABBREVIATIONS

AID Agency for International Development

IDAAN Instituto de Acueductos y AlcantarilladosNacionales

GAO General Accounting Office

COMPTROLLER GENERAL'S EXAMINATION OF FINANCIAL STATEMENTS,REPORT TO THE CONGRESS FISCAL YEARS 1969 AND 1968

Panama Canal Company and Canal ZoneGovernment B-114839

DIGEST

WHY THE EXAMINATION WAS MADE

The Government Corporation Control Act requires the Comptroller Generalto audit the Panama Canal Company's annual financial statements and tosubmit a report on the audit to the Congress. Because the Company andthe Canal Zone Government--the independent agency of the United Statescharged with the civil government of the Canal Zone--are closely re-lated in mission, organization, and operation of the Canal enterpriseas a whole, the General Accounting Office (GAO) also audits the annualfinancial statements of the Canal Zone Government.

FINDi'NGS AND CONCLUSIONS

In GAO's opinion the financial statements accompanying the report, sub-ject to certain qualifications as summarized below, present fairly thefinancial position of the Panama Canal Company and the Canal Zone Gov-ernment at June 30, 1969 and 1968, the results of their operations forthe years then ended, and the sources and application of funds of theCompany for the years then ended, in conformity with principles andstandards of accounting prescribed for executive agencies by theComptroller General. (See p. 17.)

The GAO opinions are qualified because:

--The Company's policy of not depreciating or amortizing the cost ofcertain assets, results in an understatement of the cost of opera-tions of over $3 million annually. (See p. 10.)

--Certain accounts receivable from the Republic of Panama, outstand-ing since January 1, 1961, and amounting to about $2.2 million, areclassified as current assets. (See p. 12.)

--A decision to discontinue allocating a portion of the Company'sgeneral and administrative expenses to the Canal Zone Governmentfor administrative support services results in less than full dis-closure of the cost of operating the Canal Zone Government. (Seep. 14.)

RECOMMENDATIONS OR SUGGESTIONS

None.

A GENCY ACTIONS AND UNRESOLVED ISSUES

The Company continues to believe that it cannot legally amortize or de-preciate the cost of certain assets without legislation authorizing itto do so and that the accounting treatment is necessarily founded onthis construction of law.

GAO does not believe a change in legislation is necessary to permit theCompany to provide for depreciation or amortization of these assets forthe purpose of including the costs relative thereto in its financialstatements. GAO believes that the cost of the limited special-purposeland assets consisting of excavations, embankments, fills, and relatedfacilities should be depreciated or amortized. (See p. 11.)

The Company and the Canal Zone Government believe that, since the Re-public of Panama acknowledges the validity of the accounts receivableand has historically liquidated all delinquent accounts, these receiv-ables are collectible. (See p. 14.)

The President of the Panama Canal Company notified GAO on November 13,1969, that a letter had been sent to the Bureau of the Budget on Octo-ber 23, 1969, requesting that provision be made in the fiscal year 1971budget to permit resumption of the Company's assessment against the Ca-nal Zone Government for administrative support. Provision was not madein the fiscal year 1971 budget request for resumption of the Company'sassessment against the Canal Zone Government for administrative support.GAO was notified by a Bureau of the Budget official that the appropri-ation committees would be informed of this fact. (See p. 15.)

MATTERS FOR CONSIDERATION BY THE CONGRESS

This report is submitted to the Congress as required by the GovernmentCorporation Control Act to disclose the results of the audit.

2

CHAPTER I

INTRODUCTION

The General Accounting Office has made an examinationof the financial statements of the Panama Canal Company andthe Canal Zone Government for the fiscal years ended June 30,1969 and 1968. The scope of our examination is describedon page 16 of this report.

The Company was created as a wholly owned GovernmentCorporation by the act of June 29, 1948 (62 Stat. 1075).This act was amended by the act of September 26, 1950(64 Stat. 1038), effective July 1, 1951,which vested in theCompany the functions pertaining to the waterway and the re-lated supporting business activities and which created theCanal Zone Government, as an independent agency of theUnited States, to perform the funct1ions normally associatedwith civil government--including health, sanitation, andprotection of the Canal Zone. The enterprise as a whole isieferred to throughout this report as the Canal organization.'

The functions of the Company pertaining to the waterwayinclude transit operations and the maintenance of the Canaland locks. Supporting service activities include harborterminal and vessel repair operations; a steamship servicebetween New Orleans, Louisiana, and Cristobal, Canal Zone;a railroad across the Isthmus of Panama; electric power,communication, and water systems; and-many other servicesessential to employee welfare such as retail stores, restau-rants, and housing. In addition, under the terms of an in-teragency agreement, the Company acts as an agent in admin-istering various functions for the Canal Zone Government.These functions include services such as legal and person-nel matters; budget and accounting operations; and advance-ment of funds for the monthly operations, constructioncosts, and changes in the working capital accounts of theCanal Zone Government.

The management of the Company is vested in a board ofdirectors; the management of the Canal Zone Government isvested in the Governor of the Canal Zone. Both organiza-tions are subject to the supervision of the President of

3

the United States. This surpervision has been delegated tothe Secretary of the Army who is designated as the solestockholder of the Company and the personal representativeof the President of the United States in matters concerning,the activities of the Canal Zone Government.

The Governor of the Canal Zone, who is appointed for aterm of 4 years by the President of the United States withthe advice and consent of the Senate, is the administrativehead of the Canal Zone Government and the President of theCompany. An organization chart of the Canal organizationis presented at the end of this chapter.

The Canal organization is designed to be operationallyself-sustaining. The Company uses its revenues from transitand supporting service operations to finance its operatingand capital expenditures. Funds appropriated by the Con-gress are used to repay the Company for cash advanced tocover the operating and capital expenditures of the CanalZone Government. However, pursuant to section 62g, title 2of the Canal Zone Code, the Company uses its revenues toreimburse the U.S. Treasury for the net cost of operatingthe Canal Zone Government--the amount by which the cost ofoperating the Canal Zone Government, including depreciationof fixed assets, exceeds its revenues.

The photographs at the end of this chapter furnishedby the Panama Canal Company illustrate some of the activi-ties carried out by the Canal organization.

4

S

O ~~ mt·n nC03 aO

C! -4 I

MM~~~~~~~~~~~~~'I~~~~

rfl ~~~~~~~~~~~~~~~-M MO~ m

o 1 I

I Mm Bcm 2O I *

r~~~~~~~F <M

oo

rn Ip ~ I oI __ aI I t, -

- o· . ,, ·

rn8 ,z U

MZ 0

N a-TInZ

-- ~~~ ~ ~ m 0i0~~~~

C> -4~~~~~~~~~~~~~~~~~~~~~~~~~~~~~-rn~~~~~~~~~~~-

OZ --IZC) mm ~ ~ ~ ~ ~ ~ ~ ~ ~. 4 >

mm ~~~~~~~~~~~~~- "44 - i

>rn- 4

rn 0 ~~~~~~~~~~~~~~~~~~~~~~C 44 2

C-

n m co~~~~~~~~mC

z M~~~~~~~~~~~~~C

M, -< 0

C~~~~~~~~~~~~~MC

> r X M

M n~~~~~~~~C)

M ~ ~ ~ '0M

c, ar

z r

M 0 ~ ~ ~ ~ 0

rn o :

C o

r0~~~~~~

U, -4 ~ ~ ~ ~ -4

zm~~~;a> ~ ~oz n o~~z

0-4

-4 Ifa ll , .> -

411o r

L-L~~~~~~~~~~-

9

ma

z ro

o mm m

rm>

0

zo

r &I '

g >

im 9

O 0

Z00~~~~~~~~~~~~~~~~~~~~&

( Z-

0 10

z

m0

m m1 m

m

>>~~~~~~~~~~~~~~ -4 ~ ~ ~ ~ ~ ~ ~ ~ ~ N?1m m 0na'i

m - in

0inm~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

mmr

0

r --

>~ (A ) 0

lo)~

X cn r m:::~

~~(1 ~~~~

(r 0 2

C)I

mI m

-i -jm~e,·_

Mxl :-.-io

zunmO

P , 0

oO~ ~~~~~~bT ) ·

ow

>rr

>(fl

z

zI

M'1

m >

0>

-i 'n~~~~~~~~~~~~~~~~~~~~~~~~~~,

RflI

N 3"

01

z -t

m

Z r,

0zV

o 'i

ml

F>r x '

> F

0-4

(jj

m r~~~~oU) N~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~.

0r G;I

mX;um>M

tn M>r

>v

rfl cnri

wt ij' 0

m 27m "0

, z-0i

Fmr-

Ch

r0F zrnI

mz

mm

rzma-II

>U>

ri 0

0 Zmm

Min

z.

>00 m

a,

0G

>

0

0

m

oc

mzz

000M>11

m

I-I

-na

iom(A

I40

H.

.r

-11

co r

cn l

LooTC

CHAPTER 2

COMMENTS ON DEPRECIATION, ACCOUNTS RECEIVABLE, AND

ADMINISTRATIVE EXPENSES

DEPRECIATION NOT RECORDED ON CERTAIN FIXED ASSETS

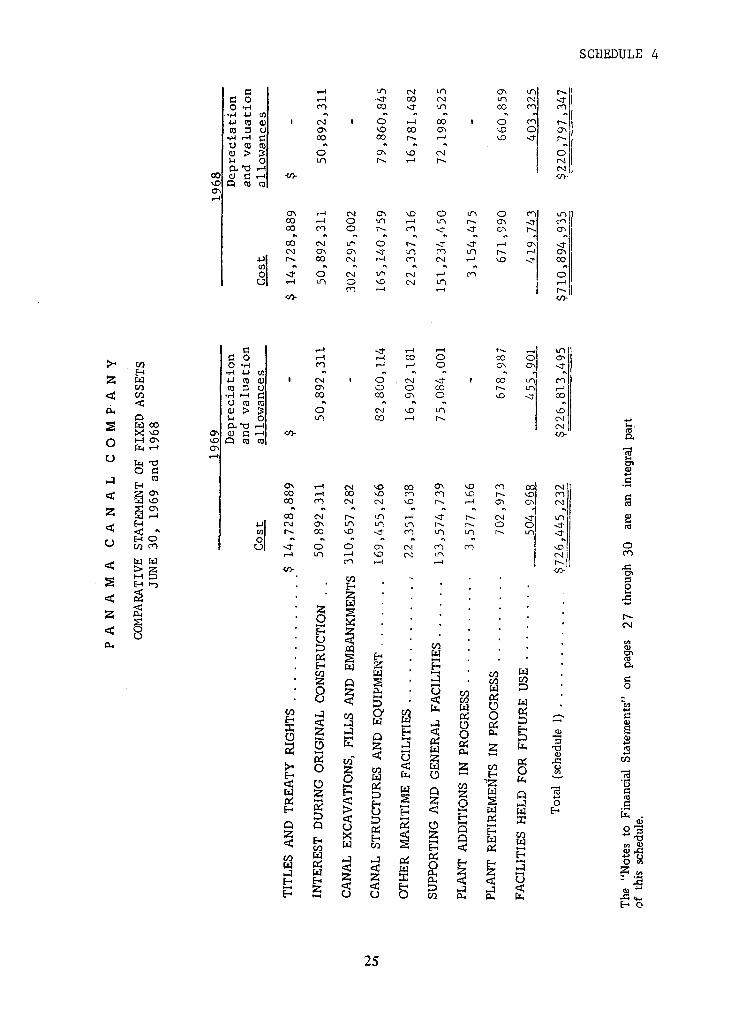

As stated in note 2 to the Company's financial state-ments, the Company interprets the Canal Zone Code as not re-quiring the depreciation or amortization of certain canalconstruction costs relating to titles; treaty rights; exca-vations of channels, harbors, and basins; and other workstotaling $325 million at June 30, 1969, and $317 million atJune 30, 1968. The note further states that, if these as-sets were depreciated at 1 percent a year, there would be acharge against operations of $3.3 million and $3.2 millionin fiscal years ended June 30, 1969 and 1968, respectively.The Company believes that it cannot legally amortize or de-preciate the cost of these assets without legislation autho-rizing it to do so and that the accounting treatment is nec-essarily founded on this construction of the law.

The Company submitted legislation for the considerationof the Eighty-third, Eighty-fourth, Eighty-eighth, Eighty-ninth, Ninetieth, and Ninety-first Congresses, which wouldhave amended the Canal Zone Code to require the Company toamortize, prospectively, at the rate of 1 percent a yearthose fixed assets of the Company that are classified as non-depreciable. The legislation submitted to the Eighty-third,Eighty-fourth, and Eighty-eighth Congresses was introducedas House Bill 9665, 5733, and 7900, respectively, but wasnot acted upon, and the legislation submitted to the Eighty-ninth Congress was not introduced. The Company informed usthat the Bureau of the Budget did not recommend the intro-duction of the legislation to the Ninetieth and Ninety-firstCongresses because of the Department of State's views thatthe introduction of such legislation should be deferredpending the outcome of treaty negotiations with the Republicof Panama.

10

LL w

w

-I-<ctn~

I-s

(n-Ji

0 wm

Iii

-OW

U

U 0

U2 iz-<

I-JI

Zw

(LL

CO

J (n E

W

an~

LI)W

0)C

OwU

0 - Ir

0 4W

i a~~~~~~~~~~~~~~~~(

: U) LL

9

uo o

zwU ww L

Ir -W

X zt< W4

U mZ

< wgW U

cz xuU)0 < 5 ~-

0 wO

9~~~~~~~~~~~~

The Company has retained this proposed legislation inits legislative program because of the continued suggestionsfrom the Senate Appropriations Committee that the Companysubmit and make every effort to obtain enactment of theproposal.

The Company stated that it considers it inadvisableunder the circumstances to provide for depreciation ofthese assets solely for the purpose of changing the meansof disclosing the cost thereof:

"*** since to do so would compromise the Congressas to:

"(a) what the effective date of depreciation oramortization should be; that is, the date in ser-vice, the date of reorganization, or prospectively,

"(b) the appropriate rate to be used, and,

"(c) any other alternatives to which the Congressmight care to address legislation."

As has been stated in our reports on the examinationof the financial statements of the Panama Canal Company forfiscal years 1963 through 1967 (B-114839, April 17, 1964;B-114839, April 21, 1966; and B-114839, February 6, 1968),we do not believe that a change in legislation is necessaryto permit the Company to provide for depreciation or amor-tization of these assets for the purpose of including thecosts relative thereto in its financial statements.

It is our view that the assets in question--excavations,embankments, fills, and related facilities--are limited-purpose land assets whose utility diminishes or terminatesas the utility of the canal diminishes or is terminated andthat their cost should be depreciated or amortized. Theseassets were constructed for the special purpose of enablingthe passage of ships through the canal. When this purposeceases, the utility of the assets will presumably alsocease. The assets involved thus do not add permanent valueto the land but rather have value of a terminable nature.

ACCOUNTS RECEIVABLE FROMTHE REPUBLIC OF PANAMA

As shown in its statements of financial condition, theCompany has classified as current assets accounts receivabledue from the Republic of Panama in the amounts of $2,608,655and $2,835,970 as of June 30, 1969 and 1968, respectively.These amounts include $1,864,283 which has been outstandingsince January 1, 1961, of which $1,686,348 is for potablewater services provided in calendar years 1959 and 1960.

In accordance with a February 1963 loan agreement be-tween the Agency for International Development (AID) and theInstituto de Acueductos y Alcantarillados Nacionales (IDAAN),an agency for the Republic of Panama, for the extension ofthe water supply and sewerage system in Panama City, theborrower, IDAAN, is to keep up to date with respect to pay-ments to the Company for water supplied; that is, the in-voices presented to IDAAN for water are to be settled within90 days of the invoice date. The loan agreement providesthat noncompliance by IDAAN with this requirement could, atAID's option, result in the suspension of loan disbursementsby AID. Subsequent loan agreements between AID and IDAAN,entered into in July 1965, January 1967, July 1967, and May1969 for the construction or improvement of water and sewer-age facilities in Panama City and Colon, included similarprovisions requiring IDAAN to keep up to date on the amountsdue the Panama Canal Company for water services.

At June 30, 1969, the amounts due the Company from theRepublic of Panama included $535,409 for water processingcharges applicable to the period February through June 1969,subsequently paid by November 1969. At June 30, 1968, theamounts due the Company included $788,369 for water process-ing charges applicable to the period November 1967 throughJune 1968, subsequently paid by November 1968.

No specific arrangements, however, were made with IDAANfor the payment of the receivables of $1,686,348 due fromthe Republic of Panama since January 1, 1961; this debt hadbeen incurred prior to the establishment of IDAAN and wasnot considered an obligation of that agency.

12

During fiscal years 1969 and 1968, the rates chargedthe Republic of Panama per unit of water (100 cubic feet)were 7.5 cents for the first 100,000 units supplied eachmonth and 7 cents for water supplied each month in excess of100,000 units. These rates, which were established in April1960 as part of a program initiated by the President of theUnited States to improve relations with the Republic, repre-sent a reduction of about 20 percent from the rates previ-ously charged. In June 1960, the Panamanian Governmentexpressed a willingness to accept the reduced rate but alsoexpressed the view that further reductions should be consid-ered.

In addition, the statement of financial condition forthe Canal Zone Government shows accounts receivable due fromthe Republic of Panama in the amounts of $1,931,008 and$1,682,456 asof June 30, 1969 and 1968, respectively, whichare also classified as current assets. These amounts arepayable to the U.S. Treasury, when collected, and are there-fore included in the current liabilities of the Canal ZoneGovernment at those dates.

The amounts due the Canal Zone Government include$1,868,735 and $1,620,784 at June 30, 1969 and 1968, respec-tively, for the care of Panamanian nationals at a Canal Zonehospital for the treatment of Hansen's disease (Palo SecoHospital). Of these amounts, $317,879 has been outstandingsince January 1, 1961. Payments were made by the Republicfor bills rendered for the 18-month period ended June 30,1962. However, no payments have been made for the chargesfor services provided for fiscal years 1963 through 1969,which have averaged about $222,000 a year.

The Palo Seco Hospital was established pursuant to theTaft Agreement, December 3, 1904, between the United Statesand the Republic of Panama, which stated that the UnitedStates would accept for treatment such persons as the Repub-lic might request, provided the Republic paid to the UnitedStates a reasonable daily charge for each patient admitted.In accordance with an agreement between officials of thePanama Canal and the Comptroller General of the Republic ofPanama, effective January 1, 1950, the principle was estab-lished for billing the Republic of Panama on the basis ofthe actual operating costs of the hospital. The average

13

costs per patient-day for fiscal years 1969 and 1968 were$9.54 and $8.06, respectively.

We were informed by officials of the Canal organizationthat no new patients had been admitted since May 1962. AtJune 30, 1969, the hospital had 71 patients, of whom 68 weredesignated as the responsibility of the Republic of Panama.At June 30, 1968, there were 80 patients, of whom 77 weredesignated as the responsibility of Panama.

As we pointed out in our report on the examination ofthe Company's financial statements for fiscal years 1967 and1966 (B-114839, February 6, 1968), various collection effortsmade by the Canal organization during fiscal year 1964 ledto a November 1964 proposal by the Republic to settle thedebt by issuance of Panamanian bonds of 30 years' maturity.However, the Department of State termed this offer "unaccep-table"; and in subsequent consideration of the matter, U.S.officials concluded that, in lieu of the proposal for accept-ing Panama bonds, the settlement of the outstanding debtshould be part of the overall negotiations to establish anew relationship between the United States and the Republic.The Canal organization has subsequently limited its collec-tion effort to notifying the State Department and the U.S.Embassy in Panama monthly of the status of the amounts duefrom the Republic.

In a letter dated September 25, 1969, the Comptrollerof the Panama Canal Company informed us that:

"In the Company's view, these amounts arecollectible. Historically, the Republic of Panamahas liquidated all delinquent accounts, and theRepublic of Panama acknowledges the validity ofthis debt."

CERTAIN COSTS NOT INCLUDED IN CANAL ZONEGOVERNMENT RESULTS OF OPERATIONS

As stated in the notes to the financial statements ofthe Company and the Canal Zone Government in fiscal year1968, the Company discontinued its practice of allocating aportion of its general and administrative expenses to the

14

Canal Zone Government for administrative support services.This accounting change precluded the need for the CanalZone Government to request a supplemental appropriation forfiscal year 1968 and enabled it to request a lower supple-mental appropriation for fiscal year 1969.

This accounting change, which was disclosed in the justi-fication submitted to the Congress for the Canal Zone Govern-ment's fiscal year 1969 supplemental operating expense appro-priation, also resulted in a net reduction of $750,000 inthe reported cost of operating the Canal Zone Government foreach of the fiscal years 1969 and 1968. However, since thenet cost of the Canal Zone Government is absorbed by theCompany, the accounting change had no effect on the net re-sults of the Company's operations for these years.

The President of the Panama Canal Company notified uson November 13, 1969, that a letter had been sent to theBureau of the Budget on October 23, 1969, requesting thatprovision be made in the fiscal year 1971 budget to permitresumption of the Company's assessment against the CanalZone Government for administrative support. Provision wasnot made in the fiscal year 1971 budget request for resump-tion of the Company's assessment against the Canal ZoneGovernment for administrative support. We were notified bya Bureau of the Budget official that the appropriation com-mittees would be informed of this fact.

Notwithstanding disclosure to the Congress throughthe appropriation process, we do not concur in the account-ing change because it does not result in the full disclo-sure of the cost of operating the Canal Zone Government.

15

CHAPTER 3

SCOPE OF EXAMINATION

Our examination, which was made in the Canal Zone, wasdirected to the Company's statements of financial conditionas of June 30, 1969 and 1968, and the related comparativestatements of revenue and expenses and the source and appli-cation of funds for the fiscal years then ended.

Inasmuch as the Company (1) is required to assume thenet cost of the Canal Zone Government as an operating ex-pense and (2) acts as agent for the Canal Zone Government inadvancing funds for its monthly operations, construction,and other activities and in collecting its revenue; we alsoexamined the Canal Zone Government's statements of financialcondition as of June 30, 1969 and 1968, and its relatedstatements of operation for fiscal years 1969 and 1968.

In our examination we gave consideration to the finan-cial audit work performed by the Company's internal auditors.Because of the extent of coverage and adequacy of the inter-nal auditors' work, we were able to limit the extent of ourown tests of the Canal organization's accounting records.

Our examination was made in accordance with generallyaccepted auditing standards and included such tests of theaccounting records and such other auditing procedures as weconsidered necessary in the circumstances and in view ofthe financial audit work performed by the Company's inter-nal auditors.

16

CHAPTER 4

OPINIONS OF FINANCIAL STATEMENTS

PANAMA CANAL COMPANY

In our opinion, subject to the comments on pages 10and 11 of this report concerning the Company's depreciationpolicy with respect to certain canal construction costs andto the comments on pages 12 through 14 concerning accountsreceivable due from the Republic of Panama, the accompany-ing financial statements (schedules 1 through 5) presentfairly the financial position of the Panama Canal Companyat June 30, 1969 and 1968, and the results of its operationsand the source and application of its funds for the fiscalyears then ended, in conformity with the principles andstandards of accounting prescribed for executive agenciesby the Comptroller General of the United States.

CANAL ZONE GOVERNMENT

In our opinion, subject to our comments on pages 14 and15 of this report regarding the exclusion of certain costsand to our comments on pages 12 through 14 concerning ac-counts receivable due from the Republic of Panama, the ac-companying financial statements (schedules 6 through 9) pre-sent fairly the financial position of the Canal Zone Govern-ment at June 30, 1969 and 1968, and the results of its op-erations for the fiscal years then ended, in conformity withthe principles and standards of accounting prescribed forexecutive agencies by the Comptroller General of the UnitedStates.

17

FINANCIAL STATEMENTS

19,

SCHEDULE 1

I ..

. , v r4 , 0

*J 0 0 000. 0 0 . 0. e0 0 0

v{on

C0 l1: 4II NNE 0 0N-

or

A a r ,e * 0 0 _

o i.Q . r.0

1 :M:1... .

,* _

.. . . .. . ...

* 0.

N0 N -,. i

* *

n c 00X . 0 , 4

, .0- - L >e

w o c .

O . r< O. r O . 0 ON N e O

Cr-. 44 r..O0 6 04 0.0 0 4 N O I 0 4 0

· ~~~~0 44

m O ,M~~~~~~~~~~~~~~~.

444.40000000..0444.c4 41 0 04

4/04. 041 0

ooo o · · b~2

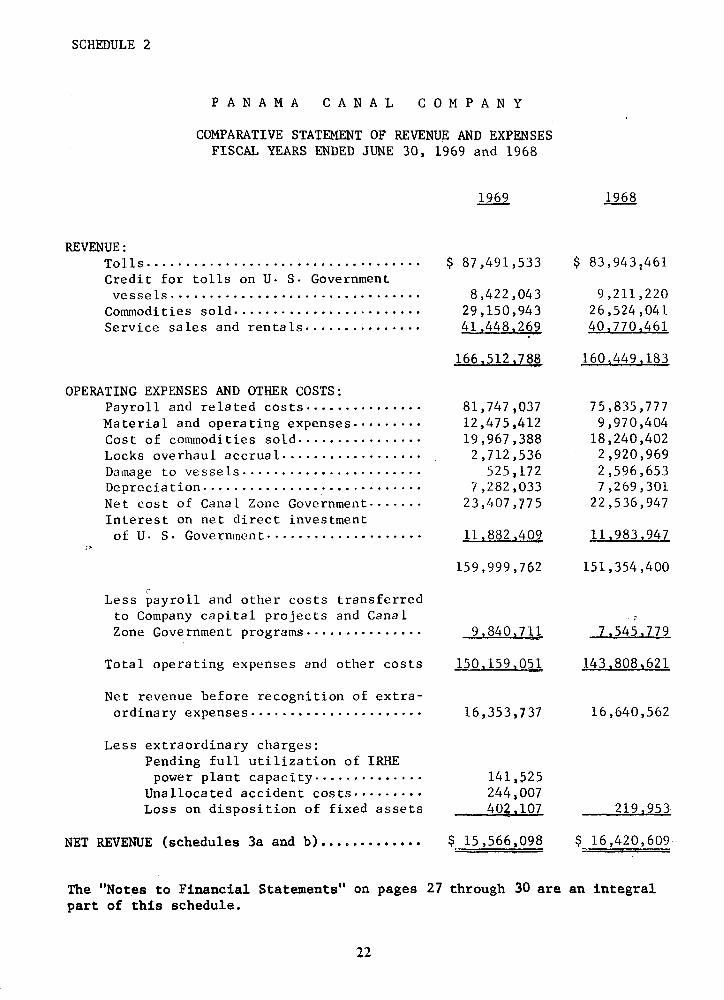

SCHEDULE 2

PANAMA CANAL C O M P A N Y

COMPARATIVE STATEMENT OF REVENUE AND EXPENSESFISCAL YEARS ENDED JUNE 30, 1969 and 1968

1969 1968

REVENUE:Tolls ................................... $ 87,491,533 $ 83,9432461Credit for tolls on U. S. Governmentvessels ................................ 8,422,043 9,211,220

Commodities sold ... ........ .. ...... 29,150,943 26,524,041Service sales and rentals ............... 41,448,269 40,770,461

166,512,78?8 160.449,183

OPERATING EXPENSES AND OTHER COSTS:Payroll and related costs .......... ..... 81,747,037 75,835,777

Material and operating expenses ......... 12,475,412 9,970,404Cost of commodities sold ................ 19,967,388 18,240,402Locks overhaul accrual ................ 2,712,536 2,920,969Damage to vessels ....................... . 525,172 2,596,653Depreciation ............................ 7,282,033 7,269,301Net cost of Canal Zone Government ....... 23,407,775 22,536,947Interest on net direct investmentof U. S. Government .................... 11,882,409 11,983.947

159,999,762 151,354,400

Less payroll and other costs transferredto Company capital projects and Canal ,Zone Government programs ............... _9,840,711 7,545,779

Total operating expenses and other costs 150,159,051 143,808,621

Net revenue before recognition of extra-ordinary expenses ................ ... 16,353,737 16,640,562

Less extraordinary charges:Pending full utilization of IRHEpower plant capacity .............. 141,525

Unallocated accident costs ......... 244,007Loss on disposition of fixed assets 40g.107 219,953

NET REVENUE (schedules 3a and b)............. $ 15,566,098 $ 16,420,609

The "Notes to Financial Statements" on pages 27 through 30 are an integralpart of this schedule.

22

SCHEDULE 3a

PANAMA CANAL COMPANY

STATEMENT OF CHANGES IN EQUITY OF THE U. S. GOVERNMENTFISCAL YEAR ENDED JUNE 30, 1969

RetainedNet Direct Investment revenue,

Non-interest- non-interest-Interest-bearing bearing bearinR

EQUITY AT JUNE 30, 1968 ............. $321,736,896 $18,051,630 $165,479,742Additions:

Net revenue (schedule 2) ........ 15,566,098Reactivations:Concrete block enclosure,Building 10, N.S.R.F. ......... 8,720Various pieces of equipment fromNavy Ship Repair Facilities .... 180,122Adjust value of Drydock No. 1,Balboa, previously reactivated. 90.766

322.016,504 18.051.630 181.045.840.

Reduction:Capital repayment ............... 5.000,000

EQUITY AT JUNE 30, 1969 (schedule 1) $317,016,504 $18,051.630 $181,045,840

The "Notes to Financial Statements" on pages 27 through 30 are an integralpart of this schedule.

23

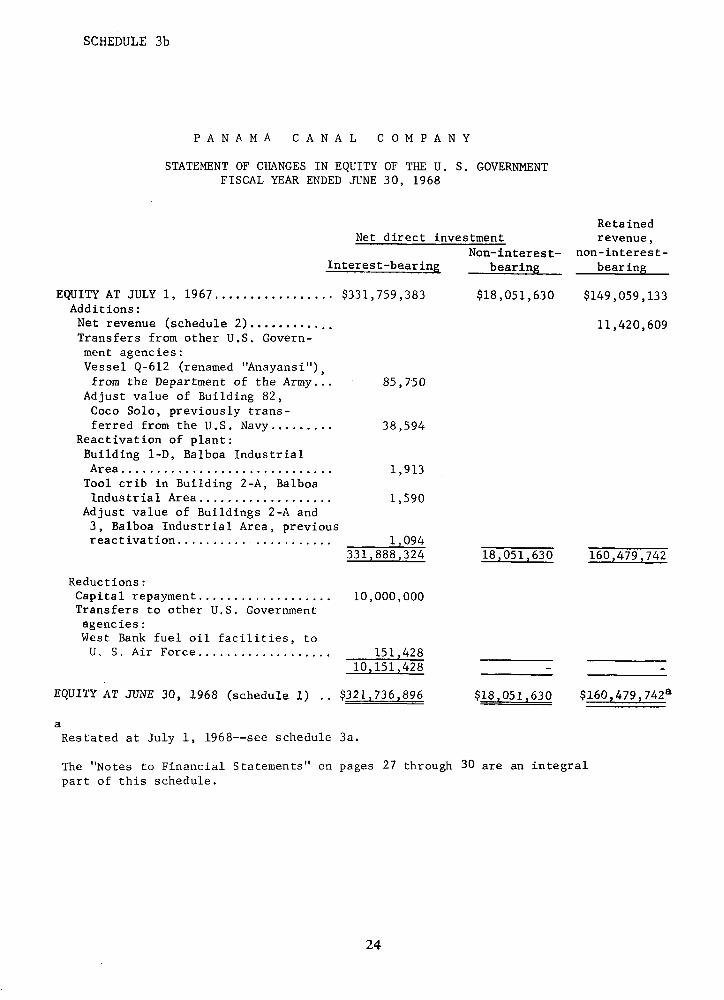

SCHEDULE 3b

PANAMA CANAL COMPANY

STATEMENT OF CHANGES IN EQUITY OF THE U. S. GOVERNMENTFISCAL YEAR ENDED JUNE 30, 1968

RetainedNet direct investment revenue,

Non-interest- non-interest-Interest-bearing bearing bearing

EQUITY AT JULY 1, 1967 ................. $331,759,383 $18,051,630 $149,059,133Additions:Net revenue (schedule 2) ............ 11,420,609Transfers from other U.S. Govern-ment agencies:Vessel Q-612 (renamed "Anayansi"),from the Department of the Army... 85,750

Adjust value of Building 82,Coco Solo, previously trans-ferred from the U.S. Navy ......... 38,594

Reactivation of plant:Building l-D, Balboa IndustrialArea .............................. 1,913Tool crib in Building 2-A, BalboaIndustrial Area ................... 1,590

Adjust value of Buildings 2-A and3, Balboa Industrial Area, previousreactivation ..... ................. 1,094

331,888,324 18,051,630 160,479,742

Reductions:Capital repayment ................... 10,000,000Transfers to other U.S. Governmentagencies:West Bank fuel oil facilities, toU, S. Air Force ................... 151,428

10,151,428 - -

EQUITY AT JUNE 30, 1968 (schedule 1) .. $321,736,896 $18,051,630 $160,479,742a

aRestated at July 1, 1968--see schedule 3a.

The "Notes to Financial Statements" on pages 27 through 30 are an integralpart of this schedule.

24

SCHEDULE 4

5. 0 _t ..Zr co cli ul) c1i Ito0 -04 0 C o o.. 0, V -4 CO I

t a) I Co I O 00 1 0

,) > 3 O0 CN .0 Nq O .£4 Q Ln r- -4 X IN

O O

00 Q) Z O

-4

oo - N o ' 0 , coa\o z3 <l\ -. o 00 -4 0 V M Ln4 a, a'

00 N t 0 rl ON - ,-4

0O I ^ cI

0 0 O- co 0. CI I O 0-4 -4 'A 0 O I

Z w - c S N N ri )to C~0c a C) c Co o c0

Z cv *,I- cs CO a C I 0 CO O \r

¢ w I .,O O C0 x4v O ·o a) r

o I4 '..0u ccu4 C

0Q h O 00 0 t C

4 Ca ON -4 N \0 CO) a\ '.0 m Nico 1-4 CO 0 ( m '.0 1- ':.0, I

S0co CN N r.0 1*- -4 ac O JN Ua

¢Oo V Cl h Co 1

,-4 LfN 4 '.0 N0 L J*nN

'" ' 0

Z) 0

Co H-' Z -

Z C

Z Z H ~ c z; I 0 Z

E- 0

SCHEDULE 5

PANAMA CANAL COMPANY

COMPARATIVE STATEMENT OF SOURCE AND APPLICATION OF FUNDSJUNE 30, 1969 AND 1968

SOURCE OF FUNDS 1969 1968From Operations:Revenues (schedule 2) ............................... $166,512,788 $160,449,183Less operating expenses and extraordinary charges... 150,946,690 144,028,574

Net revenue ..................................... 15,566,098 16,420,609Add transactions not requiring expenditure of funds:Provision for depreciation ........................ 7,282,033 7,269,301Provision for canal locks overhaul ................ 2,712,536 2,920,969Other............................................. 653,091 365,574

Total funds from operations ..................... 26,213,758 26,976,453

Proceeds from disposition of fixed assets ............. 89,370 71,451Adjustment to alien cash relief liability ............. 128,000 196,025Net change in working capital other than cash ......... - 3,399,675

Total ............................................ $ 26,431,128 $ 30,643,604

APPLICATION OF FUNDSCapital expenditures .................................. $ 17,075,906 $ 13,651,717Canal locks overhaul expenditures ..................... 1,438,898 2,851,478Capital repayment ..................................... 5,000,000 10,000,000Net change in working capital other than cash ......... 146,494Increase in cash ...................................... 2,769,830 4,140,409

Total ........................................... $ 26,431,128 $ 30,643,604

The "Notes to Financial Statements" on pages 27 through 30 are an integral part ofthis schedule.

26

NOTES TO FINANCIAL STATEMENTS

1. Inventories. Inventories of operating materials and sup-

plies are stated principally at standard cost. Inven-tories of merchandise for sale in warehouses are statedat average cost on a line-item basis; and inventories ofmerchandise for sale in retail outlets are stated at av-erage cost using the retail method for valuation.

The operating materials and supplies included inactivestock (items having no issues during the past 12 or moremonths) valued at $2.5 million and $2.4 million at the

end of fiscal years 1968 and 1969, respectively. Thisstock consists primarily of items having a use cycle in

excess of 12 months and stand-by items which have no re-curring demand but which must be available immediately

in an emergency. The Company is now reviewing and clas-sifying this stock either into the above categories oras excess.

2. Fixed assets. Fixed assets generally are stated at costor, if acquired from another Government agency, at orig-inal cost to such agency. Valuation allowances have

been established in accordance with sections 62 and 412of title 2 of the Canal Zone Code. These allowances con-sist of: (a) $50.9 million for interest during originalconstruction; (b) $14.3 million and $14.1 million as of

June 30, 1969, and 1968, respectively, to reduce to us-able value the cost of fixed assets transferred to theCompany from The Panama Canal (agency) at July 1, 1951;and (c) $72.8 million and $82.7 million as of June 30,1969, and June 30, 1968, respectively, of defense facil-ities and suspended construction projects, the latter be-ing principally the partial construction of a third set

of locks abandoned in the early part of World War II.Although all valuation allowances established under au-

thority of the Canal Zone Code are carried in the booksof account, both the cost and corresponding valuation al-lowances of defense facilities and suspended constructionprojects, 2(c) above, have been excluded from the state-ment of financial condition.

Because of historical practice and interpretation of theCanal Zone Code, depreciation or amortization allowanceshave not been provided on titles, treaty rights, and

27

excavation of channels, harbors, basins, and other workscosting $325 million at June 30, 1969, and $317 millionat June 30, 1968. If these assets were depreciated atthe rate of 1 percent a year, there would be a chargeagainst operations of $3.3 million and $3.2 million asof June 30, 1969,and 1968, respectively. Depreciationallowances on all other fixed assets are accumulated ona straight-line basis.

3. Liabilities. Certain liabilities and offsetting receiv-ables in the amount of $690,000 that were applicable topayroll transactions of the Canal Zone Government are ex-cluded from the Company's fiscal year 1969 accounts.The June 30, 1968, balances have been restated to facili-tate comparison.

Effective with fiscal year 1968, the basis for computingthe liability for "Relief Payments to Former Employees"was changed from a projection of experienced attritionfrom deaths to an actuarial basis. The adjustment re-sulted in an increase of $3.2 million in the fiscal year1968 liabilities. Because this increase was establishedby an offsetting charge to a deferred expense accountwhich was amortized against annual operations in theamount of the cash outlay for the year, the change hadno effect on net income.

4. Equity of the U.S. Government. The net direct interest-bearing investment was established in accordance withsection 62 of title 2 of the Canal Zone Code. Interestthereon is paid at a rate established annually by theSecretary of the Treasury.

The rates for 1968 and 1969 were 3.668 and 3.687 percent,respectively. The net direct non-interest-bearing in-vestment consists of the costs of the Thatcher FerryBridge constructed in accordance with the act of July 23,1956 (70 Stat. 596). The act of August 25, 1959 (73 Stat.428) amended section 71 of title 2 of the Canal ZoneCode to provide the Company with authority to borrowfunds from the U.S. Treasury not to exceed $10 millionoutstanding at any time at interest rates to be deter-mined by the Secretary of the Treasury.

28

The non-interest-bearing retained revenue of the U.S.Government at June 30, 1968, was increased by $5 millionto reflect the reversal of a fiscal year 1968 provisionfor the stabilization of canal slide hazards which didnot materialize to the extent initially estimated. Thecost of stabilization work done during fiscal years 1968and 1969 was charged to operations during the 2 fiscalyears in the amounts of $337,000 and $827,000, respec-tively.

5. Contingent and other liabilities. The Company is contin-gently liable with respect to certain pending suits andclaims. In addition, the Company has outstanding at alltimes certain liabilities of indeterminable amounts,which are recognized in the accounts on an as-paid basis.These liabilities include, principally, commitments forconstruction work, supplies and services, and death anddisability benefits payable under provisions of the Fed-eral Employees' Compensation Act.

The maximum liability which could result from outstand-ing claims and lawsuits is estimated to be $30.4 millionat June 30, 1969. Commitments under uncompleted construc-tion contracts and unfilled purchase orders amounted to$13.3 million at June 30, 1969, and $7.9 million atJune 30, 1968.

The Company held negotiable U.S. Government securitiesand Republic of Panama securities in the face amount of$2,535,000 and $2,515,000 at June 30, 1969,and 1968, re-spectively, which were deposited by customers and Panama-nian insurance firms to guarantee contract performanceand payment of tolls and other charges. In addition, theCompany held on behalf of the Canal Zone Government, ne-gotiable securities in the face amount of $673,000 and$633,000 as of June 30, 1969, and 1968, respectively, toguarantee payment of possible judgments against insurancecompanies operating in the Canal Zone.

Effective May 9, 1969, the Company entered into a 25-yearcontract with Instituto de Recursos Hidraulicos y Electri-ficacion, an autonomous agency of the Republic of Panama,for the purchase of electric power to be produced by theagency. As of June 30, 1969, the Company's total

29

minimum liability over the remaining period of the con-tract amounted to about $37 million.

Under provisions of a lease agreement with U.S. ArmyForces Southern Command, the Company is also liable foran indefinite period in the amount of $690,000 a yearfor minimum annual usage of electrical energy producedby the power barge "Sturgis".

6. Other. Effective with fiscal year 1968, the annual as-sessment to the Canal Zone Government of $750,000 forgeneral and administrative support performed by the Pan-ama Canal Company was discontinued. This was followedin fiscal year 1969 by transfer from the Canal Zone Gov-ernment to the Panama Canal Company of the responsibilityfor the cost and an equivalent amount of revenue associ-ated with retail sales of Canal Zone Government pharma-cies. These changes in accounting treatment had no ef-fect upon the net results of the Company's operations.

30

SCHEDULE 6

N '0_ 0-I 0' G' a 01 G | ' 0

O GIi.~iI -4 ,_ 1 r I r 01 A 4'00'0I '^I" ~ j Ch __

O0000 8 Y 1

r- 0 ., '4 *,

0°' OO o

* n *, --**

.0

*3 C >

0.14 !4 !1 !1i

z 014 5. o% (144_ 4%,,

P1 !!44 l0. .4'

- G0 14. 0 P - co( - O

o (C C44444.

,C 0 T, . .

0 .0 .41 .0 4 . .. 0 .! . . .

:0 0 i 4

0:

0'.... '"

e0 '0 . . 6

3

s ~~~~~U Y ~~~~~~~f ·E~~~~

·· PUI 10 IIYLI I~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~a

(41 .-(00 0

31% ~

SCHEDULE 7a

CANAL ZONE GOVERNMENT

STATEMENT OF CHANGES IN EQUITY OF THE U. S. GOVERNMENT

FISCAL YEAR ENDED JUNE 30, 1969

Operating Capital InvestedTotal funds funds capital

EQUITY AT JUNE 30, 1968:Unobligated funds .................................. $ 6,080,943 $ 111 $ 6,080,832Obligated funds .................................... 3,366,822 265,738 3,101,084Invested capital:

Fixed assets, net ............................. 53,690,052 $53,690,052Inventories ................................... 298,164 298.164

63.435,981 265,849 9.181,916 53,988,216

INCREASES IN EQUITY:

Appropriations by the Congress ..................... 38,769500 38,569,500 200,000

DECREASES IN EQUITY:Net cost of Canal Zone Government (schedule 8a):

Accrued operating expenses .................... 38,044,873 38,044,873Depreciation ...... ...................... 1,920,253 1,920,253Plant adjustments, net ........................ 128,086 128,086Increase in liabilities for:

Employees' accrued leave .................... 287,451 287,451Employees' repatriation ..................... 365 200 365,200

40,745,863 38,044,873 2,700,990Less recovery of costs ........................ 17,338,088 17.338.088

23,407,775 20.706,785 2,700,990Other decreases:

Recovery of costs coverable into U. S. Treasury:From regular operations ..................... 17,338,088 17,338,088From disposition of fixed assets ............ 8,151 8,151

Unobligated operating funds withdrawn by U. S.Treasury, net of restorations amounting to$25,554.96 ............................ ...... 329,611 329,611

17,675,850 17,667,699 8,151

Less increase in liabilities for employees'accrued leave and repatriation, not coverableinto U. S. Treasury until funds have beenappropriated therefor......... ............... 652.651 652,651

17,023,199 17.667,699 (644.500)

40.430.974 38.374,484 2.056.490

TRANSFERS BETWEEN FUNDS:Capital expenditures............................ (5,142,131) 5,142,131Removal costs of plant retirements ................. (7,543) 7,543Increase in inventories ............................ (62,620) 62,620

(62,620) (5.149,674) 5,212,294

Total increase or (decrease).................. (1,661,474) 132,396 (4,949,674) 3,155,804

EQUITY AT JUNE 30, 1969:Unobligated funds .................................. 2,658,179 2,658,179Obligated funds ......... ...................... 1,972,308 398,245 1,574,063Invested capital:

Fixed assets, net ............................. 56,783,235 56,783,235Inventories ............ ....................... 360,785 360,785

TOTAL (schedule 6) ..................................... $ 39824 $ 4,232,242 $57,144,020

The "Notes to Financial Statements" on page 37 are an integral part of this schedule.

32

SCHEDULE 7b

CANAL ZONE GOVERNMENT

STATEMENT OF CHANGES IN EQUITY OF THE U. S. GOVERNMENTFISCAL YEAR ENDED JUNE 30, 1968

Operating Capital InvestedTotal funds funds capital

EQUITY AT JUNE 30, 1967:Unobligated funds ...................................... $ 6,875,415 $ 6,875,415Obligated funds ....................................... 1,396,750 $ 360,950 1,035,800Invested capital:

Fixed assets, net .................................. 52,582,505 $52,582,505Inventories ........................................ 334828 334.828

61,189,498 360,950 7.911,215 52,917.333

INCREASES IN EQUITY:Appropriations by the Congress ....................... 40,500,000 .36000,000 4,500,000

DECREASES IN EQUITY:Net cost of Canal Zone Government (schedule 8b):

Accrued operating expenses ......................... 35,693,506 35,693,506Depreciation ....................................... 1,900,956 1,900,956Plant adjustments, net ............................. 196,819 196,819Increase in liabilities for:

Employees' accrued leave ......................... 472,116 472,116Employees' repatriation ........................ 120,800 _ _120800

38,384,197 35,693,506 2,690,691Less recovery of costs ............................ 15,847,250 15,847,250

22,536,947 19,846,256 2,690,691

Other decreases:Recovery of costs coverable into U. S. Treasury:

From regular operations .......................... 15,847,250 15,847,250From disposition of fixed assets ................. 23,977 23,977

Unobligated operating funds withdrawn by U. S.Treasury, net of restorations amounting to $22,521 438,259 438,259

16,309,486 16,285,509 23,977

Less increase in liabilities for employees' accruedleave and repatriation, not coverable into U. S.Treasury until funds have been appropriatedtherefor .......................................... 592.916 592.916

15,716,570 16,285,509 (568,939)

38,253,517 36.131.765 2,121,752

TRANSFERS BETWEEN-FUNDS:Capital expenditures.................................... (3.165,576) 3,165,576Removal costs of plant retirements ...................... (63,723) 63,723Decrease in inventories ................................. 36664 (36,664)

36,664 (3,229,299) 3,192,635

Total increase or (decrease) ....................... 2,246,483 (95,101) 1,270,701 1.070,883

EQUITY AT JUNE 30, 1968:Unobligated funds ....................................... 6,080,943 111 6,080,832Obligated funds ......................................... 3,366,822 265,738 3,101,084Invested capital:

Fixed assets, net .................................. 53,690,052 53,690,052Inventories .............................. 298164 298,164

TOTAL (schedule 6) .......................................... 3,435,98 $1 $265.849 $ 9 181 916 $53,988,216

The "Notes to Financial Statements" on page 37 are an integral part of this schedule.

33

SCHEDULE 8a

2 t0t..0 0.,.t00 s40 00.01 .0.0.. -01....l1--a: nO- ~ o.(.0....0..l0! .0.0 .0.0 040 ..I .4.00 .-I.0(..00 0 0 0 0 I .-.. 4... ....... .01 ...........

0~ ~~~~ ~~ ~ ~ ~ S~ 0io, oI' -

~ 0 ( 0 00~0 .4. 400 0 .0 ,:0~~ ~ ~ , ,g

'-5 ,., ,¢..*,,¢..,4: ,4 -~·N ·,.¢. ~ ~.,

5 < ~~ ~~~~~~ ~ 40o .. 0 .00

" I I O

6... . . . . .. .. .o . : ;o 0 4 0. ;N 0 ,.; .......0

............ ,. ....-..... -

.0.0.......... ; 0 :.5 : 0 ; : - -:%:. "

~~j(. . ..... . . . . ...... :, 00- 0:

........ , ~ : ..... n., ,

"., o o

0. ~ ~ ~ ~ Ia a1n : o

000.4~ N'0 0. 0. .0 rq 0.4 00 4 0 0 00 0 4 - 40nn~~~~~~Nnr~~~~~~~~~~ I1 ZNI

00 0.00.00000 .0000 00004 000000.00 (N 04 .00((N-.'N 0 4,-- 00..4i~ 000. 34

V~~~~~~~~~~~~

0-. 14440

,,, R m-trr~~~~~~~~~ocm~~~ N~

rnr~~~~~~~~o~~~~m.0 00 2( r ~ ~ ~ 0 0om .>000('4 ~~u~so- N~~~-4:0. 4:40(20 aOO ~ n~

=hr~~~~~~~U0.. 0. 0 00 .0

F ~ ~ ~ ~ ~ ~ ~ (0 0. . 0 0 : 6 00 :. -- 4~ ~r o

(200 . . .020.00- .-. *020 0 ~~~~~0 0 0 0 0 0 0 (0: - 0 .

^ ^ ~ ~ ~ 0 0 00 0 4 4 04 0 0 ( 0 1~0.00004. .00 101..0 0 0''' 00 0:0 00 0 .

r ~ ~ ~ . 022000. 000n~ I~ 0-044 0" 4: -0 .00 400( 00( .100 & 40 0 00 4 000 0 4022 2 20 00· 040 0.. 04: - D 0 0 02 0 0( 0 .( 0 0 2 00.00(.( 00 .hQ 0 0( 0 0 0 0 0 0 000 (0 4: 0 40

I ~ ~ ~ ~ 4 000 000 : 00..0 4. 000( 004 00 2 00 0 .r~~ ~ ~ 0 00 .0 . 0 0 000 0 0(4O 04.

o. ~ (.:440022 0 .(00. 004: 0~0 z ~ ~ 0 0 00 0 : 0 00 :4

vr ~ ~ 02( 0 004:4 0 . 00.:440 .8; ~ ~ (0.(.0040 00 .0(0.>(0.

c ~ ~ ~ 04:N0. .000 0 .440400o ~ ~ ~ ~ 00044"40.0. 00 0 01F000

oc ~ ~ ~ . 4.i . 04a n n -U , naccn~~~~~~~~.404

.0~h~r 0 .0 ar l 0O ~ ~~ 04ON- ~ 0 0~o .0J

ao ~ ~~ 0ou~I 0 tna4 j o

" E n , m~~~~N 3

SC

.. o~ .,, -.

~~~~~~~~~~~~~~3 1 ~· - , . . . m

~ . . .,,,,=~ c~: ,,~,~ .... ..

0 00~ rflot'OtOO'0'000

~~~·. .· :-·- ~.H~ . . ~ ........

r o un~t'00 0on mO 0-n0--c-t-rrnn

CO ~ ~ o.00rn got CDI CbooooonI noooO

4~ ~ -- "S,,<,s:, ,4 : ~, ........

3 ~ ~ ~ ,OOt -00 (0,: -tnol On.-'C--N ,- (OO.0 nO 0Co m 0 oh. o 00'--0 0,ocorn 0nOn 000, 000 0.0

-.. 0.0. - . ·".-0 0 . ...............Q ·0-- nC-tao o -0 -. 0 rn 0-fl

0-00- 0 00n0" 0 COBCO- n 0 n C: - :0

O ~ ~ ~ ~~ :D 0':' :l 0,0 0 ' -' ... ...........a· on- n..- n.

~~~~~~~::: ::::: I: ::::::::::::~-0)

0~ ~ ~ ~~' 0. 0~c 0: 0 -Ca 0-rn o t'

":1:::::~! 8

0

on ttO 0-

m0 ; C' '

00.0:nO -- a--0'-4

0 -,

qg l II I I I-t D

4CC-C-fl~ ~ ~ ~ ~~~T 000- 0-r~"Ohi0

I~~~~~~~~~~~~~~~ 0- Ut SdCUC~'0 OtUt0Ut0 000-0 0 CO'00-0'

0 0-~~~~~~~~~~~~~~~,

0*r~

o I C0 "

u w orurr w " a, "~nrO -

I~~~~~~~~~~ ~ ~~~~~~~~~~~ Is 030 00 0.0 COL L K r K ouCrm ooC,~~~~~~~~~~~~~~~.~~~~~~c UtII -'''

'00000 ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ I 00 t 000-0 UO-Uo o 00000000

110 10 00 0O 00 00- .- Ut - 00 '0 -4'C0-~C -0 0- oJ0-C0 -.tt---CO'00

~~rrN ~rWL K NC :j:U~-i 0-3 0- lrY~0 COrlLO i~J ~ iu r no nooamr~r~- oo

II f C n-.-0 K 0-0- 0- 0000~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ P C(0- 00 -ot O'0 Ut -'030- 00-00Ut 000C 0000000- 00- C

It; ~ ~ ~~ m I-0"0'0~~wr n 0 0- 0000O t U -U00- '003- 0 00033' 0003 0

0'0 0- 0 t'0 00 - 0 0 0 0''0 0 0 0-~u 0--0C-0--0-t 000r

r rrN uprr r NN'n rWW ~ 0- U 10

I ~ ~ ~ ~ ~ ,,~Rh~ ·qg ~ ~ o YICK · rucuwf~aRDSw orm

9F

H"0

~" 0 -. 0 l 0 ) MCb 0

rT 0 f. B3 "M< H H

H r·'1nd-~ 0 0 rtn I

En H.. ... . . o oN ~~~~~~ O0::n :3 lbM

* (/2 '~~~~~~0 . 0M P 0 In .4 *- OQZ. 0 E

PO .0 M W.~~ (A .. 0 a) N

.. ~.. . . . . 0>* .~ . .. . . . *

. ... * o o o .o

c~ mo

t~~~~~~~~~~~ N * Hd rmdof

M0,~ ~ ~ ~ ~ 0

M · · r o o .o M nPr o o .o r or o 3 r + p, n ro ; W f

..........l ' - .. ..

~........ . .r :C m oJ< ur~~~~~~~~~~~~~~~~~~~~~~~~ cr~ ~ ~ ~ l c

00 f.- 0 z~~~~~~- ~ -

...... ° ° ° ....' ...

.1-4

............ ~~~. ; ~ ( :~ ': ;

......... ·ot- ·0 CD P- 4-co

o~.C .00 ..ljo.... oO Y oo a, .~~~~DI~ 0''I.v0-j,4-- o'. p-.., *- 0-,H

~..~ '..n 0o 0-, C 0

a,~ ~ ~~~~~~~~~~, 00 W- ..0--IW ON '-.I 4'~ Lo .0 % , 0 i~ %D, , 4 .~ 00 ,,D i.Co c

0H 0% a, 4-W %O a. 0a'CAs

V)~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~N Lr 'J02 4> H.O (J1H 0'

a, NJ0 W ~ o -4 0. J ) o' W "C' O°PIN) 4 0 0

41 W .6 r"LL 0 0 " Oa,., 0 1

oC (0 0- ' o f-a I,-'

Co -JW 41 kp -4 Co --j --i W XI 0, a, Co 41, 00 0 W fOD CT

Ir! " 'T! - · r al " O T· ·o o P) 1 r r

W~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~.

U, H

~~O rMO

ur ·cn z~~~OOD% k O ~ ~41 00~~h,

FN :4~o J ~-":3 C

O D D c , D W 0 -J D ~ I j Cy K) W c , 1 0 0 % -. %D I n 03

a, 0 as 0 F 41Po " > c, roM % -4 0 %D Mrtkq 0 D OD 4 L W-j (AW

r O~~~~~~~m~~~r u m~0:

~~r~~uNN~~r u~~~~~~ WW~~~~6 Hcoo aHD

NOTES TO FINANCIAL STATEMENTS

1. Liabilities. Certain liabilities in the amount of$690,000, formerly reflected as accounts payable due Pan-ama Canal Company, were reclassified in the fiscal year1969 statements as accrued liability for salaries andwages and as accounts payable due other U.S. Governmentagencies. The June 30, 1968, balances have been restatedto facilitate comparison.

2. Contingent and other liabilities. Commitments under un-completed construction contracts and unfilled purchaseorders amounted to $2 million and $3.4 million at June 30,1969 and 1968, respectively. In addition, the Canal ZoneGovernment is liable for an indeterminable amount withrespect to death and disability payments under the Fed-eral Employees' Compensation Act. The maximum liabilitywhich could result from outstanding claims and lawsuitsis estimated to be $1.1 million.

3. Other. Effective with fiscal year 1968, the annual as-sessment to the Canal Zone Government for general andadministrative support performed by the Panama Canal Com-pany was discontinued. Effective with fiscal year 1969,responsibility for the cost and an equivalent amount ofrevenue associated with retail sales at Canal Zone Gov-ernment pharmacies was transferred to the Company. Thesechanges had the effect of reducing the annual appropria-tion of the Canal Zone Government by $1.1 million and thenet cost of operations by $750,000.

U.S. GAO. Wash., D.C.

37