Embed Size (px)

Citation preview

Azerbaijan Life Insurance & Bancassurance Market

Highlights

Tatiana Savelyeva

Azerbaijan International Insurance ForumJuly 3, 2015

2

About Qala Life Insurance

• “Qala Life” is one of the first Life Insurance companies of Azerbaijan which received the license for life insurance operations, including compulsory life insurance. Currently – one of the three life insurers. Only life insurance, no non-life operations in the group

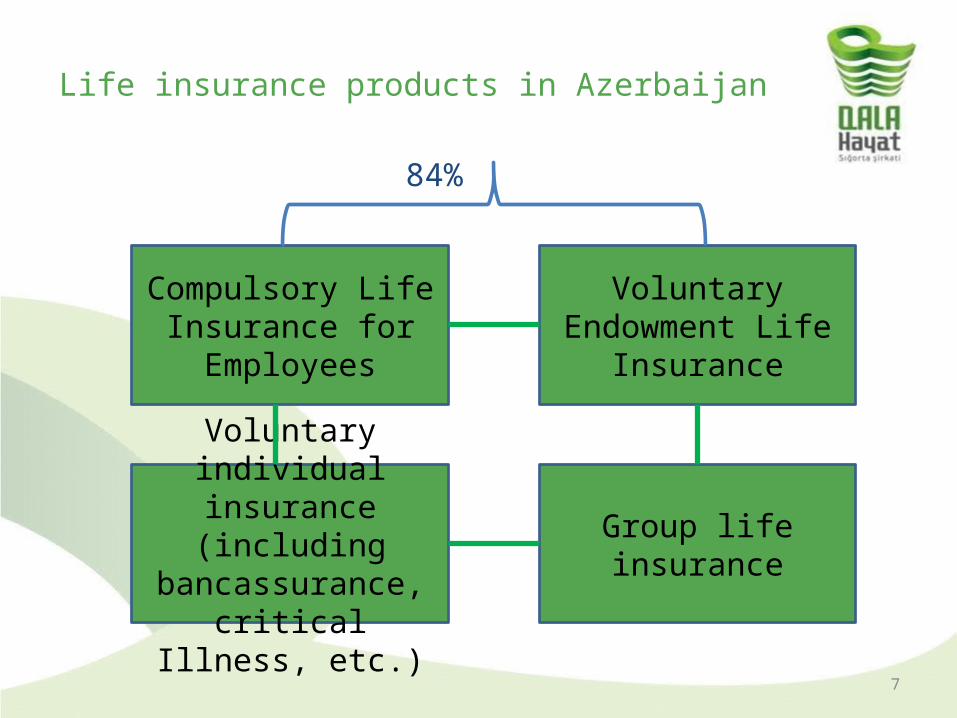

• Products include compulsory life insurance and voluntary life insurance (corporate endowment, credit life insurance, group and personal term life).

• “AzRe” is the founder of “Qala Həyat” Insurance Company. “AzRe Reinsurance” OJSC, being the first and the only reinsurer in Azerbaijan, has one of the largest authorized capital among insurance organizations in the country. Combined capital for AzRe and Qala Həyat constitutes over 47,5 mln AZN, 7,5 mln AZN of which is for Qala Həyat.

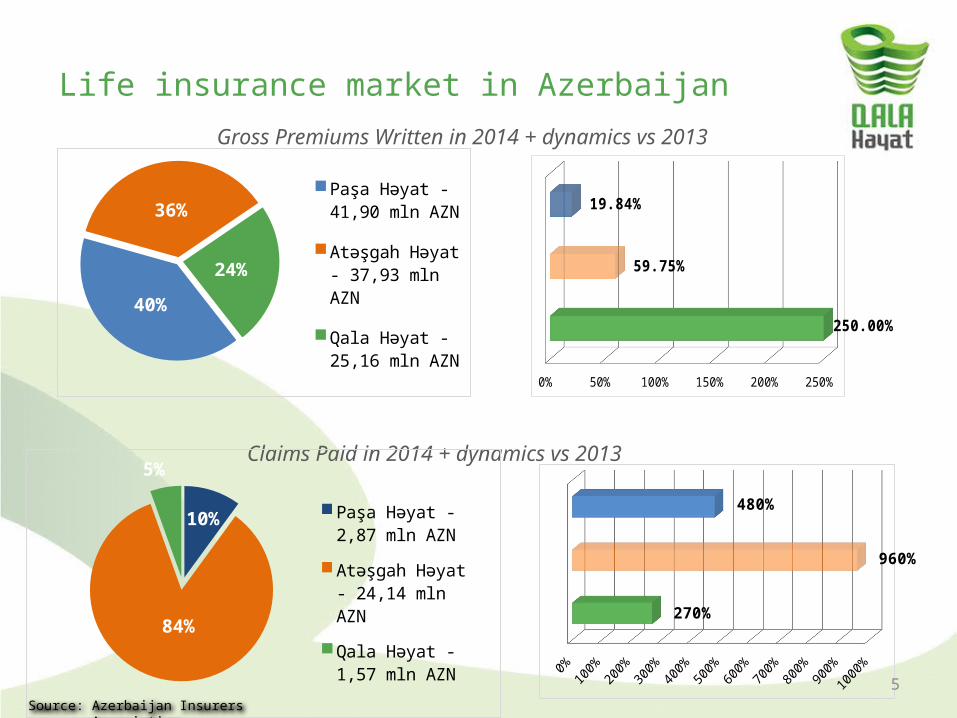

• Gross written premium in 2014 was 25,16 mln AZN, including 7,13 mln AZN for compulsory insurance. Growth against 2013 was 2,5 times, and 14,2% for compulsory line.

3

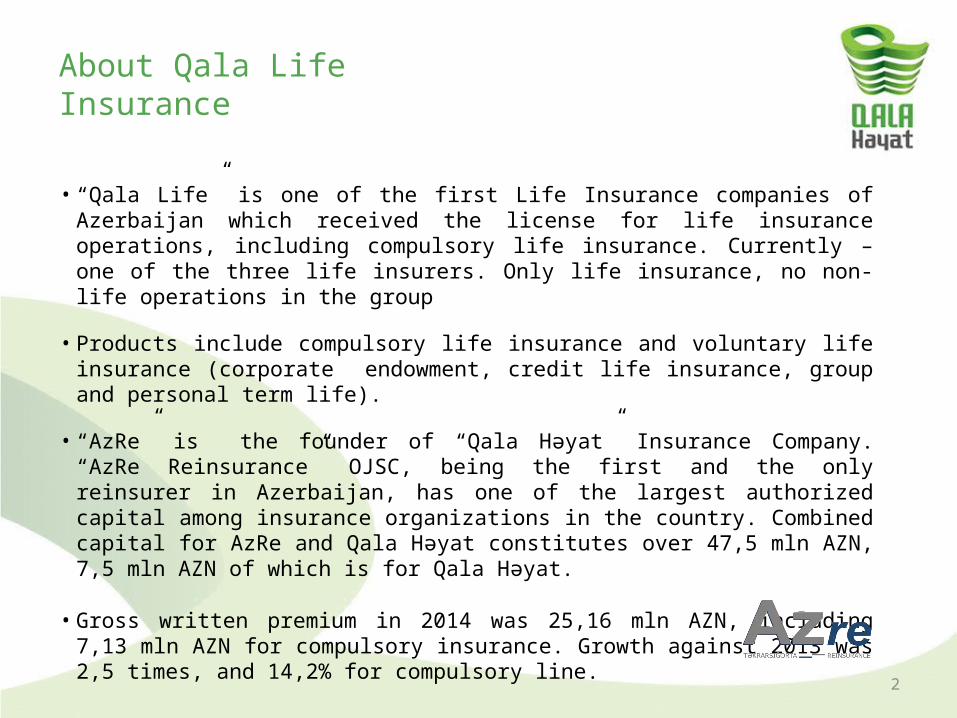

Bancassurance at Qala Life

Consumer credit life insurance7 banks, 4 of which already use online point-of-sale system

Life insurance for card holders, auto credit life insurance – not commonly offered at the market

Mortgage life insurance20 banks, 15 of which already use online point-of-sale system

Credit life only, developing products for bancassurance channel not linked to credits

Life risks only

4

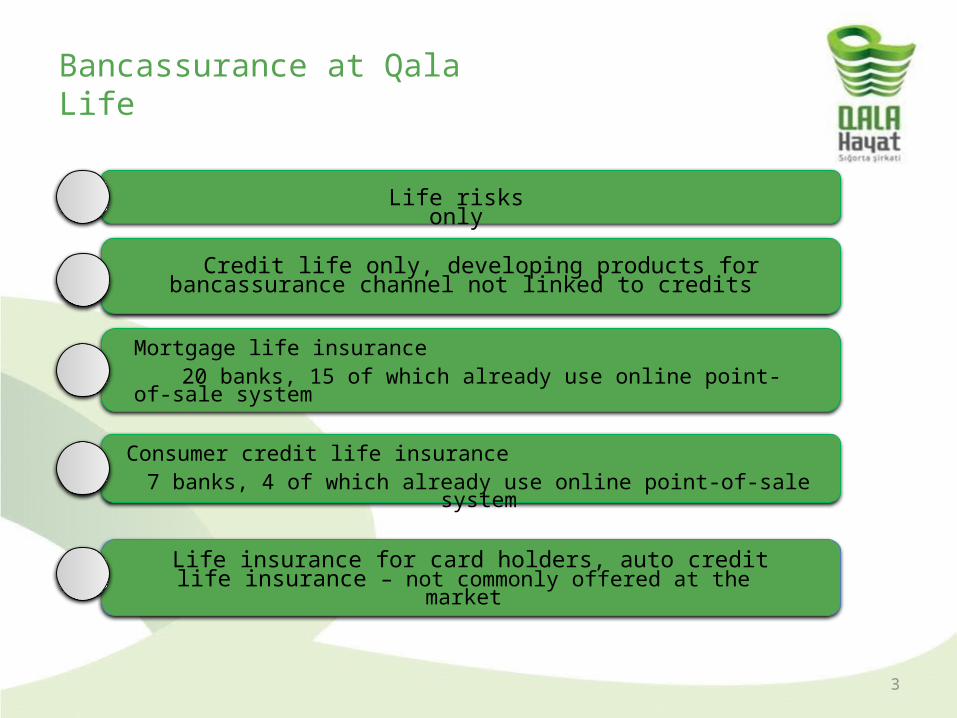

Major players in Life / Bancassurance market in Azerbaijan

•3 life insurance companies

•25 non-life insurance companies

•45 Commercial banks

•157 Non-banking credit organizations, incl. 104 credit unions

•State pension fund

5

Life insurance market in Azerbaijan

40%

36%

24%

Paşa Həyat - 41,90 mln AZN

Atəşgah Həyat - 37,93 mln AZN

Qala Həyat - 25,16 mln AZN

0% 50% 100% 150% 200% 250%

250.00%

59.75%

19.84%

Gross Premiums Written in 2014 + dynamics vs 2013

Claims Paid in 2014 + dynamics vs 2013

270%

960%

480%10%

84%

5%Paşa Həyat - 2,87 mln AZN

Atəşgah Həyat - 24,14 mln AZN

Qala Həyat - 1,57 mln AZN

Source: Azerbaijan Insurers Association

6

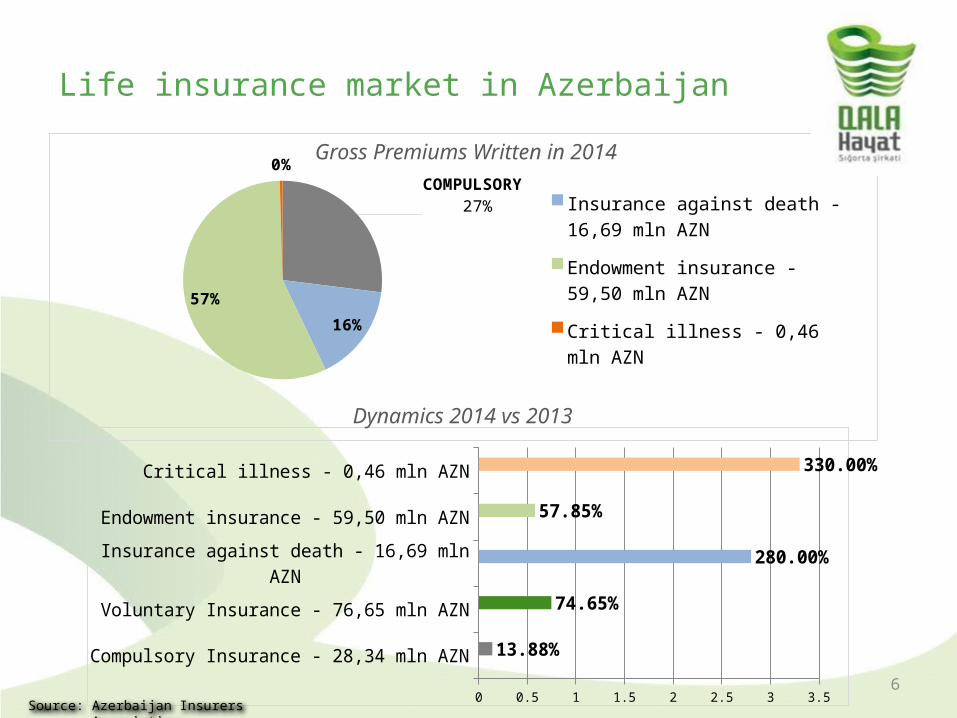

COMPULSORY 27%

16%

57%

0%

Insurance against death - 16,69 mln AZN

Endowment insurance - 59,50 mln AZN

Critical illness - 0,46 mln AZN

Life insurance market in Azerbaijan

Compulsory Insurance - 28,34 mln AZN

Voluntary Insurance - 76,65 mln AZN

Insurance against death - 16,69 mln AZN

Endowment insurance - 59,50 mln AZN

Critical illness - 0,46 mln AZN

0 0.5 1 1.5 2 2.5 3 3.5

13.88%

74.65%

280.00%

57.85%

330.00%

Gross Premiums Written in 2014

Dynamics 2014 vs 2013

Source: Azerbaijan Insurers Association

7

Compulsory Life Insurance for

Employees

Voluntary Endowment Life Insurance

Voluntary individual insurance (including

bancassurance, critical Illness, etc.)

Group life insurance

Life insurance products in Azerbaijan

84%

8

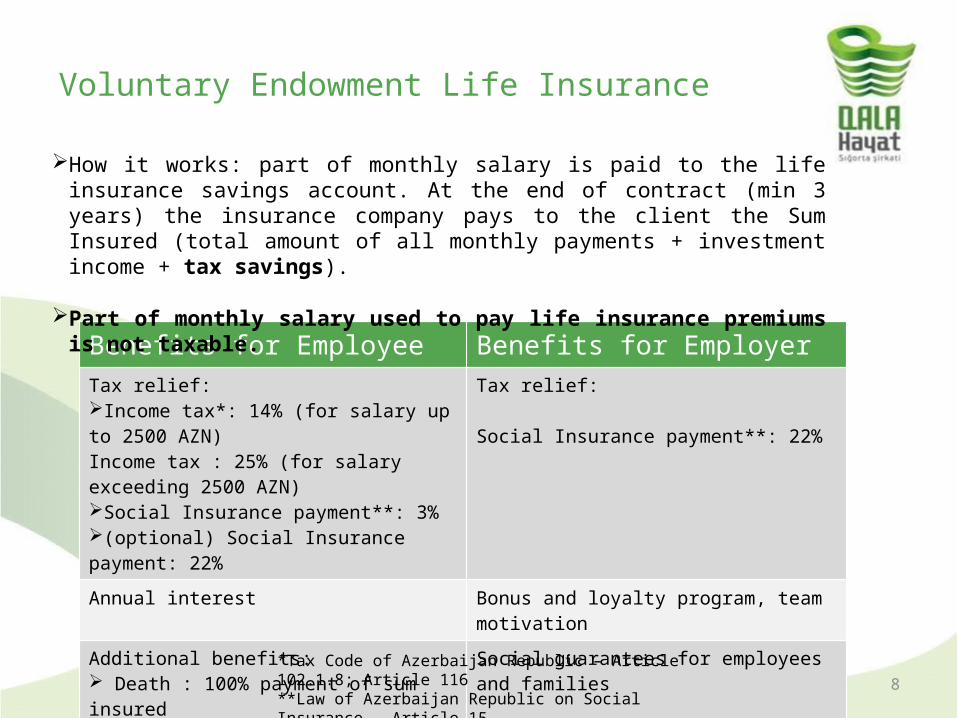

Voluntary Endowment Life Insurance

Benefits for Employee Benefits for EmployerTax relief:Income tax*: 14% (for salary up to 2500 AZN)Income tax : 25% (for salary exceeding 2500 AZN)Social Insurance payment**: 3%(optional) Social Insurance payment: 22%

Tax relief:

Social Insurance payment**: 22%

Annual interest Bonus and loyalty program, team motivation

Additional benefits: Death : 100% payment of sum insuredDisability : 0 to 100% payment of sum insured

Social guarantees for employees and families

*Tax Code of Azerbaijan Republic – Article 102.1.8; Article 116**Law of Azerbaijan Republic on Social Insurance – Article 15

How it works: part of monthly salary is paid to the life insurance savings account. At the end of contract (min 3 years) the insurance company pays to the client the Sum Insured (total amount of all monthly payments + investment income + tax savings).

Part of monthly salary used to pay life insurance premiums is not taxable.

9

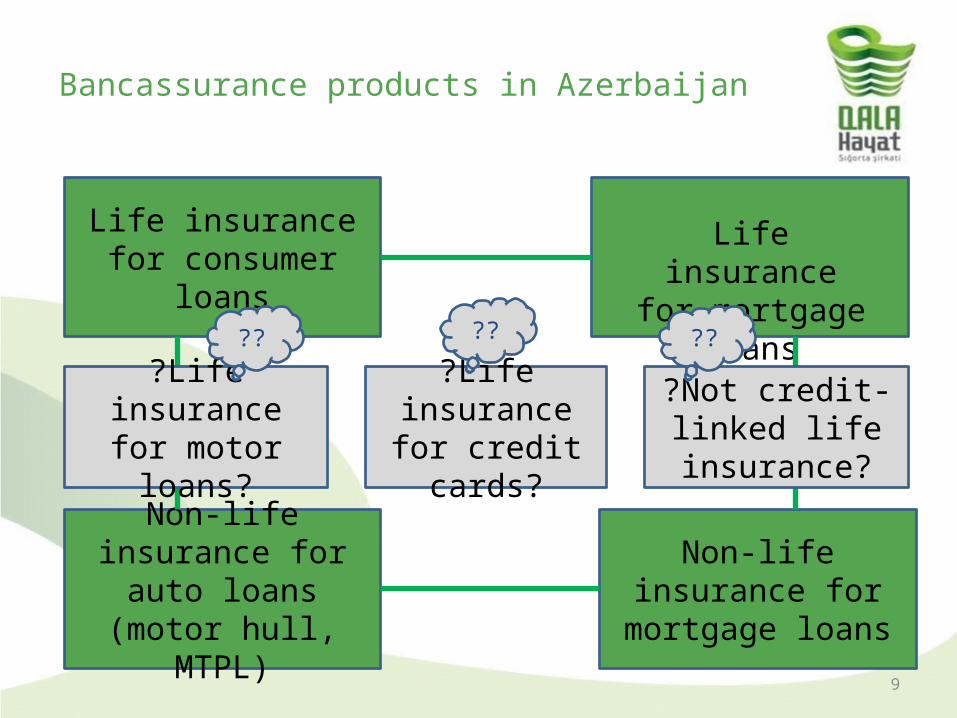

Life insurance for consumer loans

Non-life insurance for auto loans (motor hull,

MTPL)

Non-life insurance for mortgage loans

Bancassurance products in Azerbaijan

Life insurance for mortgage loans

?Life insurance for motor loans?

??

?Life insurance for credit cards?

??

?Not credit-linked life insurance?

??

10

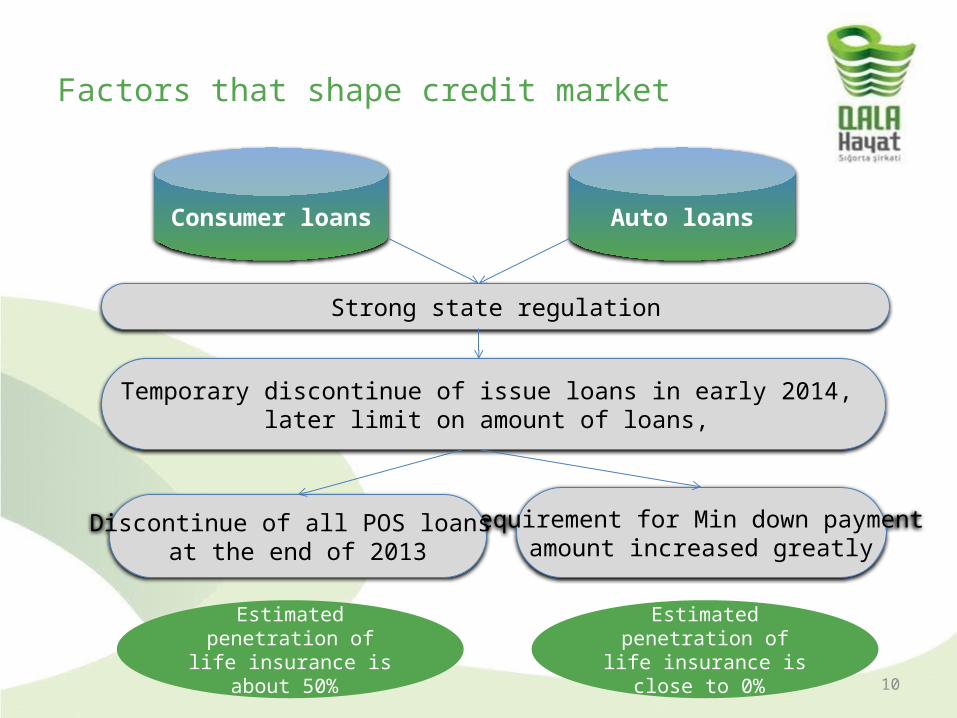

Factors that shape credit market

Consumer loans Auto loans

Strong state regulation

Temporary discontinue of issue loans in early 2014, later limit on amount of loans,

Requirement for Min down payment amount increased greatly

Discontinue of all POS loans at the end of 2013

Estimated penetration of life insurance is close to 0%

Estimated penetration of life insurance is about 50%

11

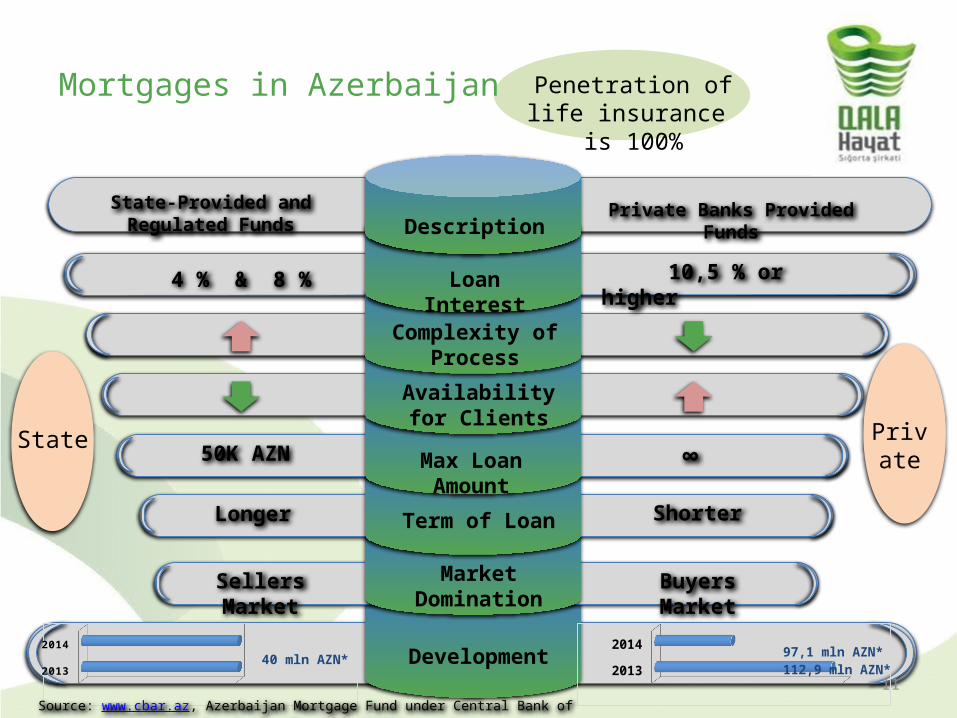

Development2013

201440 mln AZN*

2013

2014 97,1 mln AZN* 112,9 mln AZN*

State-Provided and Regulated Funds

10,5 % or higher 4 % & 8 %

Availability for Clients

Complexity of Process

Loan Interest

Description

State

Private Banks Provided Funds

Max Loan Amount50K AZN

Term of LoanLonger Shorter

Private∞

Market Domination

Sellers Market Buyers Market

Mortgages in Azerbaijan Penetration of life insurance is

100%

Source: www.cbar.az, Azerbaijan Mortgage Fund under Central Bank of Azerbaijan Republic (AMF)

12

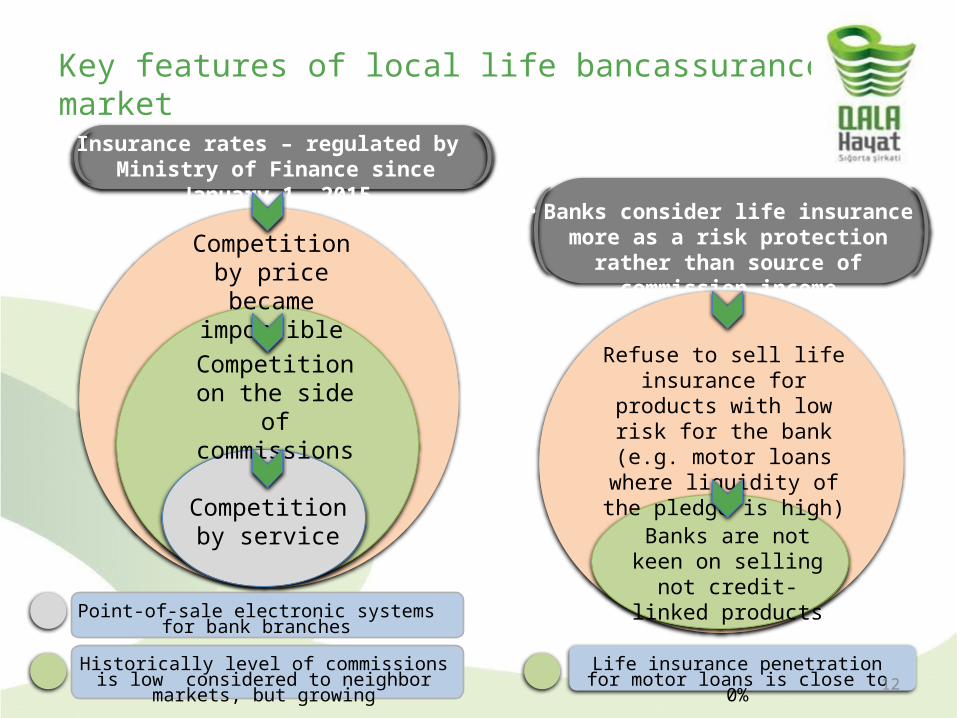

Insurance rates – regulated by Ministry of Finance since January 1, 2015

Point-of-sale electronic systems for bank branches

Historically level of commissions is low considered to neighbor markets, but growing

Competition by price became impossible

Competition on the side of

commissions

Competition by service

• Banks consider life insurance more as a risk protection rather than source of

commission income

Refuse to sell life insurance for products with low risk for the bank (e.g. motor

loans where liquidity of the pledge is high)

Banks are not keen on selling not credit-linked

products

Life insurance penetration for motor loans is close to 0%

Key features of local life bancassurance market

13

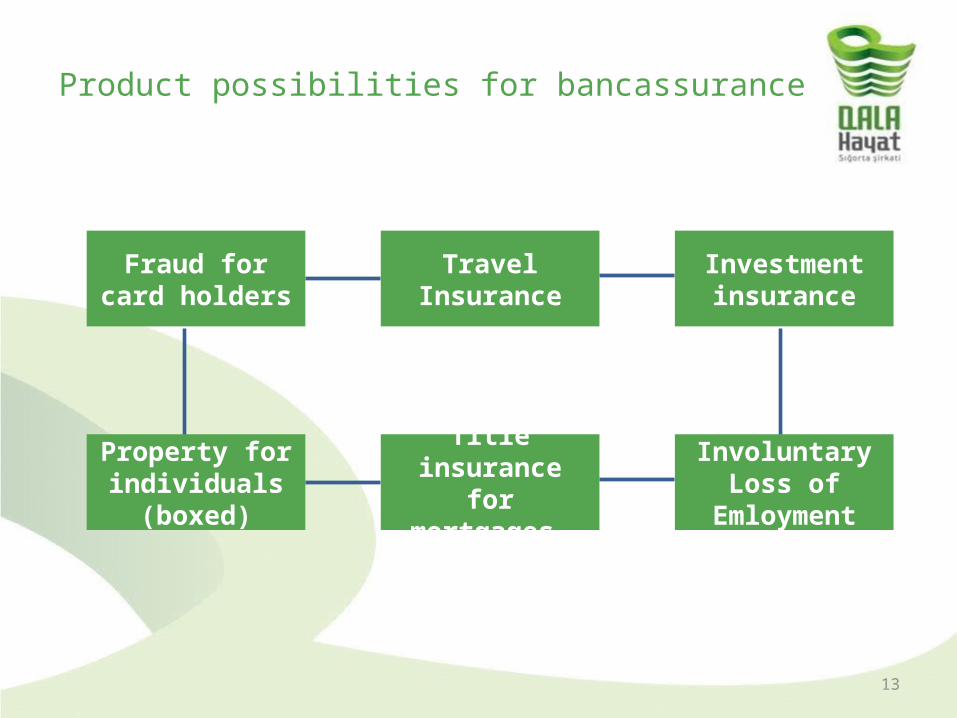

Product possibilities for bancassurance

Fraud for card holders Travel Insurance Investment

insurance

Property for individuals

(boxed)

Title insurance for mortgages

Involuntary Loss of Emloyment

14

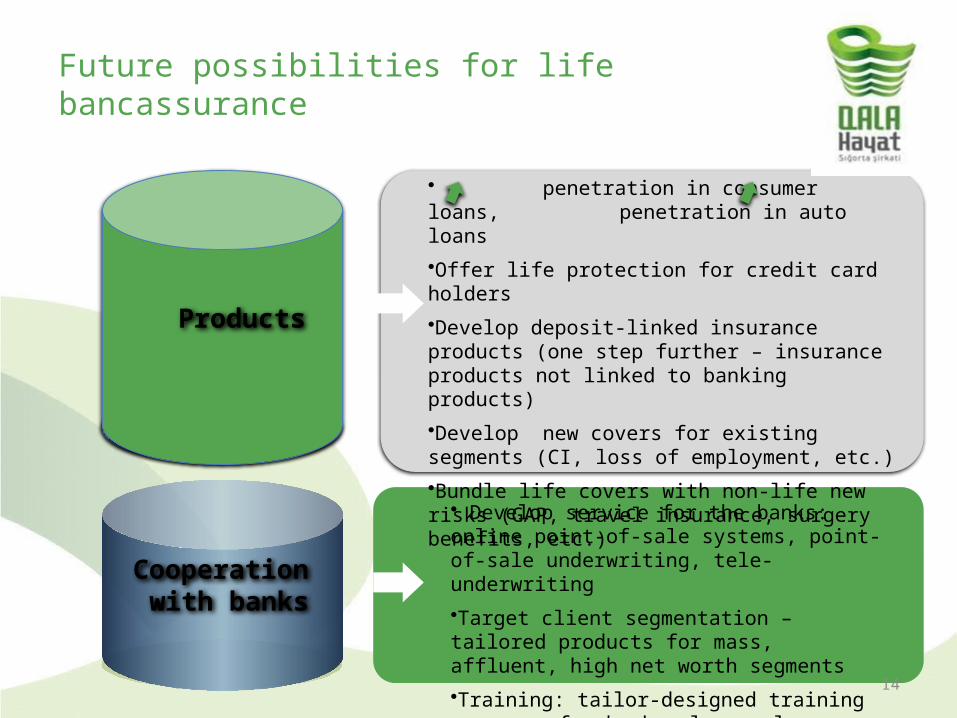

• Develop service for the banks: online point-of-sale systems, point-of-sale underwriting, tele-underwriting

•Target client segmentation – tailored products for mass, affluent, high net worth segments

•Training: tailor-designed training programs for bank sales employees, sales incentive programs

• penetration in consumer loans, penetration in auto loans

•Offer life protection for credit card holders

•Develop deposit-linked insurance products (one step further – insurance products not linked to banking products)

•Develop new covers for existing segments (CI, loss of employment, etc.)

•Bundle life covers with non-life new risks (GAP, travel insurance, surgery benefits, etc.)

Products

Cooperation with banks

Future possibilities for life bancassurance

Tbilisi pr-ti 1058, Bakı, AZ 1122, Azərbaycan, tel/faks: +994 12 404 74 44, +994 12 441 40 [email protected], www.qala.az

Thank you

Tatiana Savelyeva

Member of the Management Board, Head of Underwriting and reinsurance department“Qala Life” Insurance Company OJSCPhone/Fax: (+994 12) 404 77 74, ext.110 Mob: (+994 50) 484 75 95e-mail:[email protected]