Embed Size (px)

Citation preview

26th Annual HealthSciences Tax ConferenceASC 740 update: accounting for income taxesfor exempt organizations

December 7, 2016

Page 2

Disclaimer

► EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US.

► This presentation is © 2016 Ernst & Young LLP. All rights reserved. No part of this document may be reproduced, transmitted or otherwise distributed in any form or by any means, electronic or mechanical, including by photocopying, facsimile transmission, recording, rekeying, or using any information storage and retrieval system, without written permission from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material herein is prohibited and is in violation of US and international law. Ernst & Young LLP expressly disclaims any liability in connection with use of this presentation or its contents by any third party.

► Views expressed in this presentation are those of the speakers and do not necessarily represent the views of Ernst & Young LLP.

► This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any taxpayer because it does not take into account any specific taxpayer’s facts and circumstances.

► These slides are for educational purposes only and are not intended, and should not be relied upon, as accounting advice.

ASC 740 update: accounting for income taxes for exempt organizations

Page 3

Presenters

► Terence M. KennedyErnst & Young LLPCleveland, [email protected]+1 216 583 1504

► Raymond LeeErnst & Young LLPAustin, [email protected]+ 1 512 473 3446

► Jocelyne C. MillerErnst & Young LLPSan Diego, [email protected] +1 858 535 7360

ASC 740 update: accounting for income taxes for exempt organizations

Page 4

Agenda

► Accounting for income taxes of exempt organizations► Uncertain tax positions► Deferred taxes and valuation allowances► Affordable Care Act (ACA) tax exposures► Recent accounting pronouncements► Regulator focus on audited financial statements► Error corrections versus changes in accounting estimates► Income tax-related financial statement concerns► Tax provision best practices► Questions?

ASC 740 update: accounting for income taxes for exempt organizations

Page 5

Accounting for income taxes of exempt organizations

ASC 740 update: accounting for income taxes for exempt organizations

Page 6

Accounting Standards Codification (ASC) Topic 740

► ASC 740 addresses financial accounting and reporting for the effects of income taxes that result from an entity’s activities during the current and preceding years.► Exempt organizations:

► May have a tax provision for significant unrelated business income activities (federal and state income tax) or significant income subject to tax outside of the US

► Need to evaluate and document continued qualification for tax exemption

► Taxable subsidiaries and unrelated business income activities:► ASC 740 applies► Financial statement impact depending on materiality

ASC 740 update: accounting for income taxes for exempt organizations

Page 7

Evaluate and document qualification for exempt status

► Exemption only effective while the requirements are met► Current documentation

► Internal Revenue Service (IRS) Select Check review of (501(c)(3) organizations except under group exemptions)

► Missed filings of smaller organizations — three in a row► IRS or state notices

► Activities — as described to IRS► Exempt activities► Any political activities► Significant lobbying activities► Private inurement — private benefit► Substantial unrelated activities ► 501(r) compliance

ASC 740 update: accounting for income taxes for exempt organizations

Page 8

Unrelated business income

► Unrelated business income► New revenue sources and businesses

► Who has the details about how these are operated?► Recurring revenue activities

► Are the activities still operated in ways that are substantially related to tax-exempt purposes?

► Has the scope expanded? ► Do rents still meet the exemption requirements?

► Debt financing► Alternative and foreign investments

► Often pass-through — character and revenue

ASC 740 update: accounting for income taxes for exempt organizations

Page 9

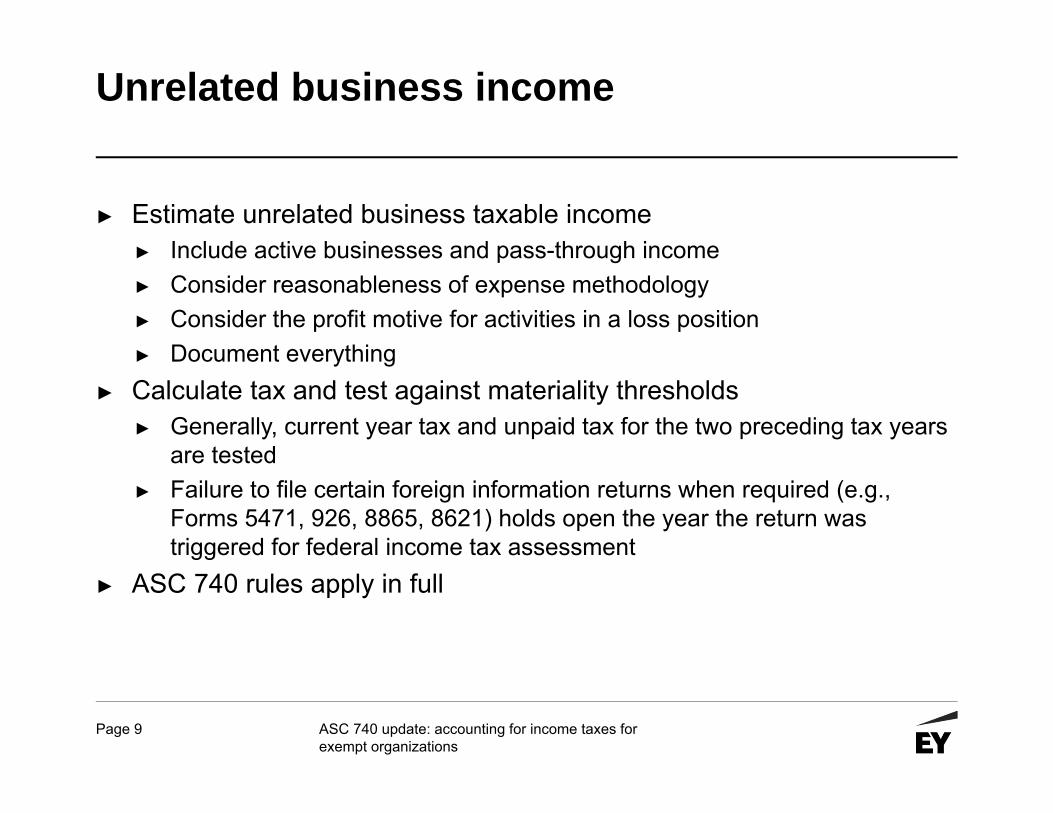

Unrelated business income

► Estimate unrelated business taxable income► Include active businesses and pass-through income► Consider reasonableness of expense methodology► Consider the profit motive for activities in a loss position► Document everything

► Calculate tax and test against materiality thresholds► Generally, current year tax and unpaid tax for the two preceding tax years

are tested► Failure to file certain foreign information returns when required (e.g.,

Forms 5471, 926, 8865, 8621) holds open the year the return was triggered for federal income tax assessment

► ASC 740 rules apply in full

ASC 740 update: accounting for income taxes for exempt organizations

Page 10

Taxable subsidiary income tax calculations

► Taxable subsidiaries► Consolidated groups► Tax-sharing agreements► Sufficient documentation supporting tax calculations► Determination of tax years open for federal income tax

assessment

ASC 740 update: accounting for income taxes for exempt organizations

Page 11

Non-income tax considerations

► Indirect taxes ► Property► Sales and use► Medical device excise tax► Private foundation tax — lapsed public charity (including

compliance with Section 509(a)(3) reporting requirements)► Other non-income taxes

► Tax-exempt financing► Compliance requirements

► Compensation reporting► State filing requirements

► Penalties — financial and effect on statute of limitations

ASC 740 update: accounting for income taxes for exempt organizations

Page 12

Uncertain tax positions

ASC 740 update: accounting for income taxes for exempt organizations

Page 13

Accounting for uncertainty in income taxes

► Benefit recognition model► Tax position must meet minimum recognition threshold before

being recognized in financial statements

► ASC Topic 450 is not applicable to income taxes► Applies to all companies, including non-public entities► Determination that exempt status is highly certain► Review of less-than-highly certain positions

ASC 740 update: accounting for income taxes for exempt organizations

Page 14

Uncertain tax positionsPresentation

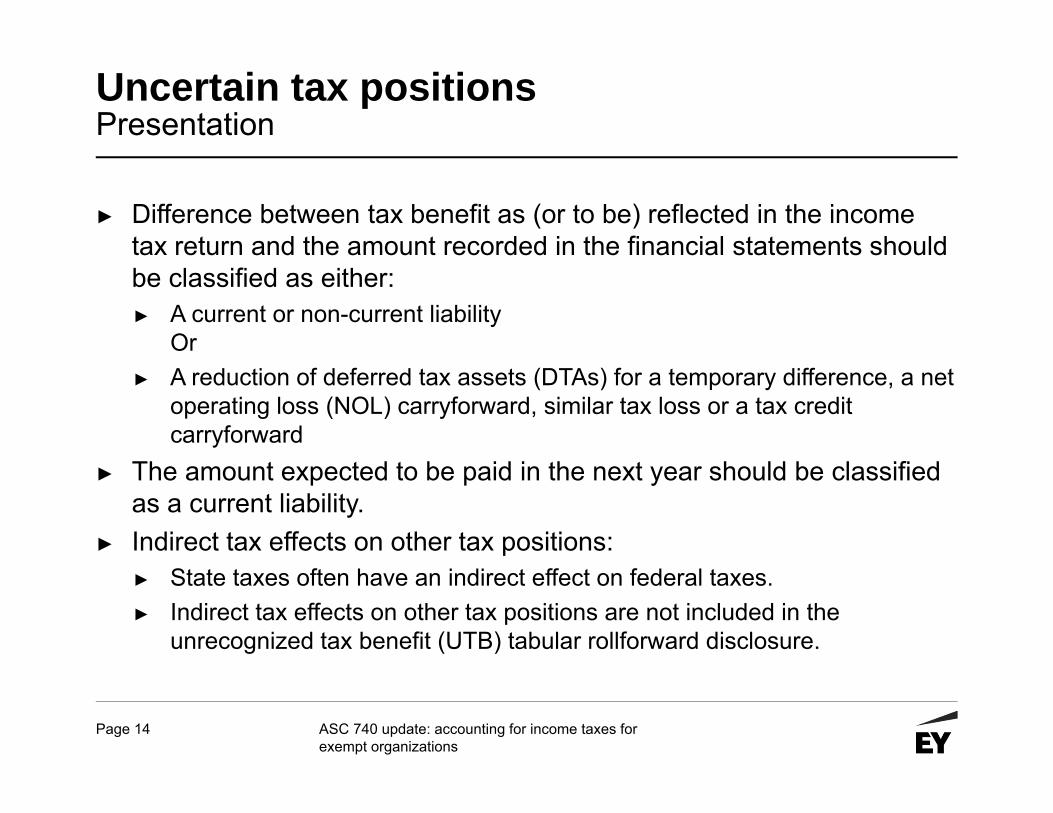

► Difference between tax benefit as (or to be) reflected in the income tax return and the amount recorded in the financial statements should be classified as either:► A current or non-current liability

Or ► A reduction of deferred tax assets (DTAs) for a temporary difference, a net

operating loss (NOL) carryforward, similar tax loss or a tax credit carryforward

► The amount expected to be paid in the next year should be classified as a current liability.

► Indirect tax effects on other tax positions:► State taxes often have an indirect effect on federal taxes. ► Indirect tax effects on other tax positions are not included in the

unrecognized tax benefit (UTB) tabular rollforward disclosure.

ASC 740 update: accounting for income taxes for exempt organizations

Page 15

Uncertain tax positionsPresentation — Accounting Standards Update (ASU) 2013-11

► Assume tax position is disallowed at the reporting date► If net settlement of a net operating loss, similar tax loss or tax credit

carryforward and an unrecognized tax benefit is required or expected, present liability associated with uncertain tax benefit as a reduction to related DTA for net operating loss, similar tax loss or tax credit carryforward

► If net settlement is not required or expected, present uncertain tax benefit as a liability; not combined with DTA

► Not expected to change DTA realizability assessment► Does not change disclosure requirements of uncertain tax positions

ASC 740 update: accounting for income taxes for exempt organizations

Page 16

Uncertain tax positionsDocumentation

► Nature and extent of documentation required may vary based upon the character of the uncertain income tax position

► Distinguish between “highly certain” tax positions and tax positions for which greater uncertainty is present► Highly certain tax positions are based on clear and unambiguous

tax law► Clearly meets more-likely-than-not recognition standard and there is a

greater than 50% likelihood that 100% of benefit will be sustained

ASC 740 update: accounting for income taxes for exempt organizations

Page 17

Deferred taxes and valuation allowances

ASC 740 update: accounting for income taxes for exempt organizations

Page 18

Evaluating the need for a valuation allowance

► DTAs represent future tax deductions (or tax carryforwards and tax credits)

► Reduced by a valuation allowance (VA) if it is more likely than not (>50%) that some portion, or all, of the DTAs will not be realized► Evaluation is made on a gross basis — common pitfall► Based on weight of all available evidence► Depends on sufficient taxable income

► Consider four sources of income► VAs address the realizability of DTAs, not their existence — common

pitfall► Consider presentation of valuation allowance

(current and non-current)

ASC 740 update: accounting for income taxes for exempt organizations

Page 19

Evaluation of positive and negative evidence

► Weight given to evidence should be commensurate with the ability to objectively verify the evidence.

► Examples of positive and negative evidence include:

Negative evidence Positive evidenceCumulative pretax losses in recent history (generally three years) or projections of cumulative pretax losses — common pitfall

Existing contracts or firm sales backlog

History of carryforwards expiring unused Strong earnings history, exclusive of loss that created the future deductible amount, coupled with evidence that the loss is an aberration

Brief carryback or carryforward periods Implemented cost reduction plans that can be objectively verified (however, consider any effects on revenues)

ASC 740 update: accounting for income taxes for exempt organizations

Page 20

Cumulative losses in recent years

► Calculation► Cumulative pretax income or loss for three years (current year and

two preceding years)► Annual calculation — common pitfall► Exclude only the cumulative effect of accounting changes

► Not an “on/off” switch► Does not, in itself, result in a conclusion of the realizability of

deferred tax assets — common pitfall ► Quantitative considerations► Qualitative considerations

► Significant piece of negative evidence that is often difficult to overcome

ASC 740 update: accounting for income taxes for exempt organizations

Page 21

Releasing a valuation allowance

► What framework do I apply when determining whether to release a valuation allowance?► Same framework ► Change in circumstance causes change in judgment about

realization in future years► Key considerations

► Extent of positive and negative evidence that exists► Ability to rely on future projections of income

► Return to profitability► Not an “on/off” switch► No quarterly rolling reversal

ASC 740 update: accounting for income taxes for exempt organizations

Page 22

Recap of common pitfalls

► Is the timing of reversal of deferred tax losses (DTLs) considered?► “Naked tax credits” resulting from indefinite-lived intangible assets

► Does a tax planning strategy result in a projection of future taxable income?

► Are DTAs recognized based on projections of future taxable income when the company is in a cumulative loss position, has a going concern opinion or has recently emerged from bankruptcy?

► Is the company considering a rolling reversal of a valuation allowance upon sustained profitability?

► Has a cumulative loss been considered a bright line or “on/off” switch requiring a valuation allowance?

► Is the valuation allowance presented appropriately on the balance sheet (current vs. non-current)?

ASC 740 update: accounting for income taxes for exempt organizations

Page 23

Key takeaways

► Must consider all sources of income in assessing realizability

► Determination of whether a company is, or is not, in a cumulative loss position does not, in itself, result in a conclusion as to the realizability of deferred tax assets

► Avoid common valuation allowance pitfalls

ASC 740 update: accounting for income taxes for exempt organizations

Page 24

Affordable Care Act tax exposures

ASC 740 update: accounting for income taxes for exempt organizations

Page 25

Affordable Care Act (ACA) considerations

► The employer mandate was generally effective on January 1, 2015.

► There are significant excise tax penalties for ACA failures.► A company may need to recognize an accrual for the

resulting loss contingency.► Employers should account for uncertainties resulting from

a lack of clarity in the provisions of the employer mandate (e.g., certain aspects of the definition of a full-time employee) under the loss contingencies accounting guidance (ASC 450).

ASC 740 update: accounting for income taxes for exempt organizations

Page 26

ACA considerations

► Key questions:► Have all potential full-time employees been identified? How have

they been identified?► Is there a system in place to appropriately track hours of service?

Is this system compliant with ACA rules?► Was the population of contingent workers, interns, transfers,

international assignees, etc. reviewed under the “common law” definition of “employee”?► Form 1099 workers may be considered employees for the ACA.► Do any potential employee categories signal a risk under the ACA?

► Is the coverage offered considered “affordable” and does it provide minimum value?

► Has the company taken any steps to mitigate the risks associated with contingent workers?

ASC 740 update: accounting for income taxes for exempt organizations

Page 27

ACA considerations

► The ACA imposes a nondeductible fee on each covered entity engaged in the business of providing health insurance for US health risks.► A covered entity is generally any entity with net premiums written for

health insurance for US health risks during the fee year that is:► A health insurance issuer within the meaning of Internal Revenue Code (IRC)

Section 9832(b)(2) ► A health maintenance organization within the meaning of IRC

Section 9832(b)(3) ► An insurance company subject to tax under Subchapter L or that would be so

subject to tax but for being exempt under IRC Section 501(a) ► An insurer that provides health insurance under Medicare Advantage, Medicare

Part D or Medicaid ► A non-fully insured, multiple-employer welfare arrangement

► The permanent nondeductible fee can be a material item.

ASC 740 update: accounting for income taxes for exempt organizations

Page 28

Recent accounting pronouncements

ASC 740 update: accounting for income taxes for exempt organizations

Page 29

Revenue recognition

ASC 740 update: accounting for income taxes for exempt organizations

Page 30

Revenue recognitionAmerican Institute of Certified Pubic Accountants (AICPA) health care task force implementation issues

ASC 740 update: accounting for income taxes for exempt organizations

► Third-party settlements

► Continuing Care Retirement Community (CCRC) performance obligations

► Significant financing component

► Disclosures ► Contract costs

► Self-pay► Portfolio

approach

Identified by Revenue

Recognition Industry Task

Force

Submitted to Revenue

Recognition Working Group

Submitted to The Financial

Reporting Executive Committee

Made available for

public comment

Included in Accounting Guide on Revenue

Recognition

Page 31

Revenue recognitionAICPA health care task force implementation issues

► Comment period for working drafts of revenue recognition implementation issues ended on September 1, 2016

► No significant external comments received► Other informal comments received:

► If an entity selects the modified retrospective approach, how does it account for changes in the year of adoption to the prior year allowance for doubtful accounts (through bad debt or revenue)?

► In determining if the entity meets the criteria in the paper for implicit price concessions (i.e., that it is not probable that it will collect substantially all of the billed amount), does it evaluate the entire billed amount (insured and self-pay portions) or only the self-pay portion?

► How are multiple portfolios for a single contract and performance obligation handled?

Made available for

public comment

► Self-pay► Portfolio

approach

ASC 740 update: accounting for income taxes for exempt organizations

Page 32

Revenue recognitionAICPA health care task force implementation issues

► RRWG discussed third-party settlement working draft this week

► RRWG disagreed with conclusions reached in CCRC performance obligations working draft

► Third-party settlements

► CCRC performance obligations

► Significant financing component

Submitted to Revenue

Recognition Working Group

(RRWG)

ASC 740 update: accounting for income taxes for exempt organizations

Page 33

Revenue recognitionAICPA health care task force implementation issues

► Task force is addressing:► What constitutes a contract asset vs. a receivable?► What types of health care services represent a single

performance obligation (or a bundle of goods or services, or a series of distinct goods or services, that are substantially the same and have the same pattern of transfer) vs. multiple performance obligations?

► Are health care entities required (or should be they be required) to quantitatively disclose the amount of implicit price concessions?

► Disclosures

Identified by Revenue

Recognition Industry

Task Force

ASC 740 update: accounting for income taxes for exempt organizations

Page 34

Leases

ASC 740 update: accounting for income taxes for exempt organizations

Page 35

LeasesOverview

► FASB issued final standard in February 2016► Key changes to today’s US Generally Accepted Accounting Principles

(GAAP) guidance include: ► Lessees will recognize assets and liabilities for most leases.► New presentation and disclosure requirements for lessees have been

introduced.► Real estate-specific guidance was eliminated► Leases will be classified using criteria similar to today’s guidance.

► Effective for public business entities, certain not-for-profit entities and employee benefit plans for annual and interim periods beginning after December 15, 2018► Early adoption permitted

ASC 740 update: accounting for income taxes for exempt organizations

Page 36

LeasesLease classification

► Lessees and lessors will classify leases using criteria similar to today’s guidance but without bright lines. ► Today’s real estate-specific guidance was eliminated. ► Today’s additional lessor classification criteria was changed.► Today’s non-performance default covenant guidance was eliminated.

► Lessees will classify most leases as either: ► Finance — similar to today’s capital leases ► Operating — similar to today’s operating leases

► For leases with a lease term of 12 months or less, lessees would be able to make an accounting policy election to use a short-term lease exemption► Do not recognize lease assets or liabilities► Recognize lease expense on a straight-line basis

► Lessors will classify all leases as sales-type, direct financing or operating

ASC 740 update: accounting for income taxes for exempt organizations

Page 37

Presentation of financial statements of not-for-profit entities

ASC 740 update: accounting for income taxes for exempt organizations

Page 38

Presentation of financial statements of not-for-profit entities

► The Financial Accounting Standards Board (FASB) issued guidance that will change certain financial statement requirements for not-for-profit (NFP) entities.

► NFPs will be required to:► Present two classes of net assets (without donor restrictions and with

donor restrictions)► Classify the underwater portion of endowments within net assets with

donor restrictions ► NFPs may continue to use either the direct or indirect method of

reporting operating cash flows but will no longer be required to present a reconciliation if the direct method is used.

ASC 740 update: accounting for income taxes for exempt organizations

Page 39

Presentation of financial statements of not-for-profit entities

► NFPs also will be required to:► Net external and direct internal investment expenses against investment

return► Report expenses by their natural and functional classification► Provide more information about their available resources and liquidity

► Effective for annual periods beginning after December 15, 2017, and interim periods thereafter

ASC 740 update: accounting for income taxes for exempt organizations

Page 40

Presentation of financial statements of not-for-profit entities

► What should NFPs do to prepare?► Consider how the presentation guidance for net investment returns may

affect financial performance reporting measures► Consider their plans to implement and communicate these changes to

their governing boards and other key stakeholders in conjunction with those of other accounting standards effective in a similar time frame

► Monitor the FASB’s activities in the second phase of this project

ASC 740 update: accounting for income taxes for exempt organizations

Page 41

FASB’s proposed changes to income tax disclosure requirements

ASC 740 update: accounting for income taxes for exempt organizations

Page 42

FASB’s proposed changes to income tax disclosure requirements

► Aim is to make income tax disclosures more effective► Exposure draft issued July 26, 2016, with comments due

September 30, 2016► Any final issued guidance would be applied prospectively► Proposal would:

► Require entities to make additional disclosures related to foreign earnings

► Change the disclosure requirements related to uncertain tax positions

► Broaden the applicability of certain income tax disclosure requirements by replacing the term “public entity” with “public business entity” throughout ASC 740

ASC 740 update: accounting for income taxes for exempt organizations

Page 43

FASB’s proposed changes to income tax disclosure requirements

► A public business entity (PBE) is a business entity that:► Is required by the US Securities and Exchange Commission (SEC) to file

or furnish audited financial statements to the SEC► Is required by the Securities Exchange Act of 1934 (the Act) to file or

furnish audited financial statements with a regulatory agency other than the SEC

► Is required to file or furnish audited financial statements with a foreign or domestic regulatory agency for purposes of issuing securities

► Has issued, or is a conduit bond obligor for, securities that are traded, listed or quoted on an exchange or over-the-counter market

► Has issued securities that are not subject to transfer restriction, is required to issue US GAAP financial statements and makes them publicly available on a periodic basis

► Neither a not-for-profit entity nor an employee benefit plan is a business entity.

ASC 740 update: accounting for income taxes for exempt organizations

Page 44

FASB’s proposed changes to income tax disclosure requirements

► Other income tax topics► Valuation allowances — PBEs to provide an explanation of the

nature and amounts of valuation allowances recorded or released during the reporting period

► Tax carryforwards — PBEs to disclose:► Gross carryforward amount and related deferred tax asset before

valuation allowance to be disaggregated by federal, state and foreign jurisdiction and broken out by year

► Report total amount of unrecognized tax benefits that offset the deferred tax asset attributable to carryforwards► Non-PBEs would be required to disclose the gross amounts of federal,

state and foreign carryforwards and their expiration dates

► Government assistance — All entities to describe certain legally enforceable agreements with a government

ASC 740 update: accounting for income taxes for exempt organizations

Page 45

FASB’s proposed changes to income tax disclosure requirements

► Changes in tax laws — All entities to disclose information about an enacted change in tax law if it is probable that the change will affect the entity in a future period

► Tax rate reconciliations — PBEs to disclose:► Reconciliation between the amount computed by multiplying

pretax income (loss) by the applicable statutory federal income tax rate and the total income tax expense (benefit) from continuing operations

► Individual reconciling items that amount to more than 5% of the amount computed by multiplying the income before tax by the applicable statutory federal income tax rate

► A qualitative description of items causing significant changes in the rate year over year

ASC 740 update: accounting for income taxes for exempt organizations

Page 46

Regulator focus on audited financial statements

ASC 740 update: accounting for income taxes for exempt organizations

Page 47

Regulator focus Realizability of deferred tax assets

► How evidence was weighted ► Cumulative losses► Consideration of the four sources of taxable income,

including the prominence of each source and the material uncertainties, assumptions or limitations associated with each source

► Timing and reason for changes in valuation allowance► Consistency of assumptions► Consistency of accounting with management discussion

and analysis disclosures

ASC 740 update: accounting for income taxes for exempt organizations

Page 48

Error corrections versus changes in accounting estimates

ASC 740 update: accounting for income taxes for exempt organizations

Page 49

Return-to-provision adjustments Change in estimate or correction of an error?

► A temporary difference is defined as:► A difference between the tax basis of an asset or liability

(computed in accordance with ASC 740) and its reported amount in the financial statements

► In preparing its tax return, a company may identify a difference between the tax basis used to compute a temporary difference and the tax basis used for the tax return.

► Differences may also arise related to income taxes payable, tax credit carryforwards or other income tax accounts.

ASC 740 update: accounting for income taxes for exempt organizations

Page 50

Change in accounting estimate

► Results from new information► Accounted for in the period of change or the period

of change and future periods if the change affects multiple periods► No retrospective adjustment or restatement

► May require disclosure depending on materiality and whether the change is expected to affect future periods

ASC 740 update: accounting for income taxes for exempt organizations

Page 51

Correction of an error

► Examples include:► A change from an accounting principle that is not generally

accepted to one that is generally accepted► Corrections of mistakes in the application of US GAAP► Corrections of mathematical mistakes► Oversight or misuse of facts that existed at the time the financial

statements were prepared

► Requires restatement of prior period financial statements (if material) or correction in current period if immaterial

► Determine if there are deficiencies in internal control

ASC 740 update: accounting for income taxes for exempt organizations

Page 52

Key takeaways

► A change related to a prior period that did not result from new information is an error and requires additional consideration under ASC 250.

► Refer to Ernst & Young LLP Financial Reporting Developments: Guide on accounting for income taxes, accounting changes and error corrections for additional information.

ASC 740 update: accounting for income taxes for exempt organizations

Page 53

Income tax-related financial restatement concerns

ASC 740 update: accounting for income taxes for exempt organizations

Page 54

Income tax-related financial restatement concerns

► General causes:► Application of tax technical rules

► Tax basis ► Intraperiod tax allocation

► Interim periods► Accounting for outside basis differences► Realizability of deferred tax assets

► Tax planning strategies► Deferred tax liabilities as source of income

Income tax errors continue to be a leading cause of restatements.

ASC 740 update: accounting for income taxes for exempt organizations

Page 55

Income tax-related financial restatement concerns Realizability of DTAs

► Same framework► Establishing a valuation allowance for the first time► Determining whether a valuation allowance continues to

be necessary

► Have all four sources of taxable income been considered?► Future reversals of existing taxable temporary differences

► Evaluate DTAs on a gross basis ► Consider the timing of reversal of existing taxable temporary

differences ► Common pitfall — DTAs evaluated on a net basis► Common pitfall — Naked credits are used as a source of taxable

income

ASC 740 update: accounting for income taxes for exempt organizations

Page 56

Tax provision best practices

ASC 740 update: accounting for income taxes for exempt organizations

Page 57

Tax provision best practices

► Accelerate work during quarters and interim:► Evaluate and record return-to-provision adjustments► Prove out deferred tax assets and liabilities, current taxes payable and

receivable► Prepare analysis before filing tax return to identify errors in the return

► Document and analyze state tax rates, including apportionment changes and the impact on deferred taxes, and foreign tax rates for changes

► Document outside basis differences, including indefinite reinvestment assertions and prepare outside basis difference calculations (consider previously taxed income and unrecaptured Subpart F income)

► Document valuation allowance considerations (four sources of taxable income) and prepare position paper

► Document uncertain tax positions► Consider tool to improve efficiency and accuracy of computations

ASC 740 update: accounting for income taxes for exempt organizations

Page 58

Tax provision best practices

► Institute regular meetings with external auditors regarding contemporaneous issues (significant transactions, changes in business, etc.)

► Annually challenge prior year processes to identify areas for improvement► Simplify, standardize and add controls to existing Excel templates► Address technical issues early and prepare white papers for consideration by

management and external audit► Implement standardized global procedures► Consider the tax provision process a year-round area of continued focus► Identify a third party to assist with preparation or review of the provision (pre-

audit review) or co-source/outsource to free up internal time for review► Obtain assistance researching and documenting issues or preparing white

papers on tax accounting positions

ASC 740 update: accounting for income taxes for exempt organizations

Page 59

Questions?

ASC 740 update: accounting for income taxes for exempt organizations

EY | Assurance | Tax | Transactions | AdvisoryAbout EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US.

© 2016 Ernst & Young LLP.All Rights Reserved.

BSC # 1608-2011220

ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.