Embed Size (px)

Citation preview

Awareness of Mutual Fund Investment among investors of Mehsana city

Management Research Project - II

Submitted

In the partial fulfillment of the Degree of

Master of Business Administration

Semester-IV

By

Name Roll No.

Pancholi Jalpa 11044311056

Parmar Kashmira 11044311062

Parmar Payal 11044311065

Parmar Viraj 11044311066

Prajapati Jayshree 11044311117

Rabari Hetal 11044311122

Under the Guidance of:

Prof. (Dr.) Mahendra Sharma Prof. & Head,

V. M. Patel Institute of Management.

&

Jayesh D. Patel Assistant Professor,

V. M. Patel Institute of Management.

Dipesh Dasani Assistant Professor,

V. M. Patel Institute of Management.

Submitted To: V. M. Patel Institute of Management

(April-2013)

ii

CERTIFICATE BY THE GUIDE

This is to certify that the contents of this report entitled “Awarenessof Mutual Fund

Investment among investors of Mehsanacity.”submitted to V. M. Patel Institute of

Management for the Award of Master of Business Administration (MBA Sem-IV) is original

research work carried out by him/her/them under my supervision. This report has not been

submitted either partly or fully to any other University or Institute for award of any degree or

diploma.

Name Exam No.

Pancholi Jalpa 11044311056

Parmar Kashmira 11044311062

Parmar Payal 11044311065

Parmar Viraj 11044311066

Prajapati Jayshree 11044311117

Rabari Hetal 11044311122

Professor & Head,

V. M. Patel Institute of Management,

Ganpat University.

Kherva.

Date: 22/04/2013

Place: Kherva

iii

CANDIDATE’S STATEMENT

We hereby declare that the work incorporated in this report entitled “Awarenessof Mutual Fund Investment among investors of Mehsana city.” in partial fulfilment of the requirements for the award of Master of Business Administration (Sem.-IV) is the outcome of original study undertaken by us and it has not been submitted earlier to any other University or Institution for the award of any Degree or Diploma. Name Exam No. Sign.

Pancholi Jalpa 11044311056

Parmar Kashmira 11044311062

Parmar Payal 11044311065

Parmar Viraj 11044311066

Prajapati Jayshree 11044311117

Rabari Hetal 11044311122

Date: 22/04/2013

Place: Kherva

iv

PREFACE

“Experience is the best teacher.”- This saying plays a guiding role in our lives and also in Management Research Project those are an integral part of the M.B.A. Today’s age is an age of management. Management is the backbone of any organization or

any activity done. The real success of management lies in applying the professional

management techniques in all managerial activities. As we move into an era of intense

competition and high performance expectations, it is important that we develop the winning

edge.

Practical study is eminent, and plays vital role for the students of management, because

classroom coaching and theoretical study alone are not enough. To survive in this highly

competitive world, practicality outweighs theoretic. Students are supposed to learn the

various principles of business administration conceptually but accuracy and efficiency in

their implementation is possible only through exposure to practical environment.

In this report we have tried to analyze one of the lending industry that is mutual fund

industry and tried to find out industry’s awareness and preference through primary survey.

The project has given us a very good exposure to know the industry and to understand the

working of industry.

Date: - 22/04/2013

Place : - Kherva

v

ACKNOWLEDGMENT

We have been able to prepare our report successfully and we acknowledge a special thanks to

all those people without whose support it was impossible to make the project report.

We would hereby take this opportunity to show our gratitude towards all our mentors for

what we have learnt during our MRP-II project. A good response, feedback and co-operation

given by whole staff helped out in gaining knowledge and solving our queries.

The successful completion of this project could not have been possible without the co-

operation and support of our faculty guide and investors who have given complete

information for the project.

We feel immense pleasure to thank Prof. (Dr.) Mahendra Sharma, Principal, V.M.Patel

institute of management, Ganpat University, Kherva. For making available all facilities in

fulfilling the requirements for the research work.

We forward our appreciation to respected coordinator of the V.M.Patel institute of

management form Prof. Jayesh Patel & Dipesh Dasani.

vi

EXECUTIVE SUMMARY

Starting out as an industry with a single player, the UTI, in 1963, the mutual fund industry in

India has come a long way since then. Today, close to 30 players, offering over 460 schemes,

dot the industry landscape. The industry has gained enormously in size as reflected in its

assets under management which now stand at a whopping Rs.1,75,918 cr., as on July 31,

2005 from Rs.1,00,000 crore in early 2000.

Further, the emergence of Mehsana city a major investment destination has done a world of

good to the mutual fund industry in an India as it is witnessing entry of many big names in

the global investment management business. The entry of major global players like Morgan

Stanley, Principal, Sunlife, and Fidelity, while Vanguard is mulling over its India debut,

augurs well for the industry as not only these global investment management firms bring with

them the expertise gained internationally but also bring the best international practices in

terms of performances and investor services which will benefit the industry and will go a

long way in helping it catch up with its counter parts in developed markets like the US and

the UK.

vii

TABLE OF CONTENTS

Sr No. PARTICULARS PAGE No.

Certificate by the Guide II

Candidate’s Statement III

Preface IV

Acknowledgments V

Executives summary VI

1 Introduction of Mutual Fund 1

1.1 What is Mutual Fund? 2

1.2 Concept of Mutual Fund 4

1.3 History of the Mutual Fund Industry 5

1.4 Global scenario 8

1.5 Organisation of Mutual Fund 9

1.6 Process of Mutual Fund 11

1.7 How to invest in Mutual Fund? 12

1.8 Regulatory Of mutual fund in India 13

1.9 Types of Mutual Fund schemes 14

1.10 Procedure for registering a Mutual fund with SEBI 17

1.11 SEBI registered Mutual Fund Companies 18

1.12 Pointers to measure Mutual Fund performance 20

1.13 How to reduce risk while investing? 21

1.14 Advantages of Mutual fund 23

1.15 Disadvantages 24

2 Literature Review 26

3 Research Methodology 29

viii

4 Data analysis & interpretation 32

4.1 Chi-Square Test 33

4.2 Anova Test 34

5 Findings 115

6 Recommendations 117

7 Conclusion 119

8 Limitations of the study 121

9 Bibliography 123

Annexure 125

1

Chapter:-1

Introduction

2

1.1 WHAT IS A MUTUAL FUND?

Mutual fund is an investment company that pools money from shareholders and invests in a

variety of securities, such as stocks, bonds and money market instruments. Most open-end

Mutual funds stand ready to buy back (redeem) its shares at their current net asset value, which

depends on the total market value of the fund's investment portfolio at the time of redemption.

Most open-end Mutual funds continuously offer new shares to investors. Also known as an open-

end investment company, to differentiate it from a closed-end investment company. Mutual funds

invest pooled cash of many investors to meet the fund's stated investment objective. Mutual

funds stand ready to sell and redeem their shares at any time at the fund's current net

asset value: total fund assets divided by shares outstanding.

Figure 1.1: Investment Flow

3

In Simple Words, Mutual fund is a mechanism for pooling the resources by issuing units to the

investors and investing funds in securities in accordance with objectives as disclosed in offer

document.

Investments in securities are spread across a wide cross-section of industries and sectors and thus

the risk is reduced. Diversification reduces the risk because all stocks may not move in the same

direction in the same proportion at the same time. Mutual fund issues units to the investors in

accordance with quantum of money invested by them.

Investors of Mutual funds are known as unit holders. The profits or losses are shared by the

investors in proportion to their investments. The Mutual funds normally come out with a number

of schemes with different investment objectives which are launched from time to time.

In India, A Mutual fund is required to be registered with Securities and Exchange Board of India

(SEBI) which regulates securities markets before it can collect funds from the public. In Short, a

Mutual fund is a common pool of money in to which investors with common investment

objective place their contributions that are to be invested in accordance with the stated

investment objective of the scheme.

The investment manager would invest the money collected from the investor in to assets that are

defined/ permitted by the stated objective of the scheme. For example, an equity fund would

invest equity and equity related instruments and a debt fund would invest in bonds, debentures,

gilts etc. Mutual fund is a suitable investment for the common man as it offers an opportunity to

invest in a diversified, professionally managed basket of securities at a relatively low cost

4

1.2 CONCEPT OF THE MUTUAL FUND

A Mutual Fund is a trust that pools the savings of a number of investors who share a common

financial goal. The money thus collected is then invested in capital market instruments such as

shares, debentures and other securities. The income earned through these investments and the

capital appreciations realized are shared by its unit holders in proportion to the number of units

owned by them. Thus a Mutual Fund is the most suitable investment for the common man as it

offers an opportunity to invest in a diversified, professionally managed basket of securities at a

relatively low cost. The flow chart below describes broadly the working of a mutual fund:

Figure 1.2 Working of mutual fund

5

1.3 HISTORY OF THE MUTUAL FUND INDUSTRY

The mutual fund industry in India started in 1963 with the formation of Unit Trust of India, at

the initiative of the Government of India and Reserve Bank. The history of mutual funds in

India can be broadly divided into four distinct phases

Figure 1.3 Phase of mutual fund industry in India

Phase - 1964-87

Unit Trust of India (UTI) was established on 1963 by an Act of Parliament. It was set up by

the Reserve Bank of India and functioned under the Regulatory and administrative control of

the Reserve Bank of India. In 1978 UTI was de- linked from the RBI and the Industrial

Development Bank of India (IDBI) took over the regulatory and administrative control in

place of RBI. The first scheme launched by UTI was Unit Scheme 1964. At the end of 1988

UTI had Rs.6,700crores of assets under management.

Phases Of Mutual Fund

Industry In India

Phase I

Phase II

Phase III

Phase IV

6

Second Phase - 1987-1993 (Entry of Public Sector Funds)

1987 marked the entry of non- UTI, public sector mutual funds set up by public sector banks

and Life Insurance Corporation of India (LIC) and General Insurance Corporation of India

(GIC). SBI Mutual Fund was the first non- UTI Mutual Fund established in June 1987

followed by Can bank Mutual Fund (Dec 87), Punjab National Bank Mutual Fund (Aug 89),

Indian Bank Mutual Fund (Nov 89), Bank of India (Jun 90), Bank of Baroda Mutual Fund

(Oct 92). LIC established its mutual fund in June 1989 while GIC had set up its mutual fund

in December 1990.At the end of 1993, the mutual fund industry had assets under management

of Rs.47, 004 cr.

Third Phase - 1993-2003 (Entry of Private Sector Funds)

With the entry of private sector funds in 1993, a new era started in the Indian mutual fund

industry, giving the Indian investors a wider choice of fund families. Also, 1993 was the year

in which the first Mutual Fund Regulations came into being, under which all mutual funds,

except UTI were to be registered and governed. The erstwhile Kothari Pioneer (now merged

with Franklin Templeton) was the first private sector mutual fund registered in July 1993.

The 1993 SEBI (Mutual Fund) Regulations were substituted by a more comprehensive and

revised Mutual Fund Regulations in 1996. The industry now functions under the SEBI

(Mutual Fund) Regulations 1996.

The number of mutual fund houses went on increasing, with many foreign mutual funds

setting up funds in India and also the industry has witnessed several mergers and acquisitions.

As at the end of January 2003, there were 33 mutual funds with total assets of Rs.

1,21,805crores. The Unit Trust of India with Rs.44,541crores of assets under management

was way ahead of other mutual funds.

Fourth Phase - since February 2003

In February 2003, following the repeal of the Unit Trust of India Act 1963 UTI was

bifurcated into two separate entities. One is the Specified Undertaking of the Unit Trust of

India with assets under management of Rs.29,835crores as at the end of January 2003,

7

representing broadly, the assets of US 64 scheme, assured return and certain other schemes.

The Specified Undertaking of Unit Trust of India, functioning under an administrator and

under the rules framed by Government of India and does not come under the purview of the

Mutual Fund Regulations.

The second is the UTI Mutual Fund Ltd, sponsored by SBI, PNB, BOB and LIC. It is

registered with SEBI and functions under the Mutual Fund Regulations. With the bifurcation

of the erstwhile UTI which had in March 2000 more than Rs.76,000crores of assets under

management and with the setting up of a UTI Mutual Fund, conforming to the SEBI Mutual

Fund Regulations, and with recent mergers taking place among different private sector funds,

the mutual fund industry has entered its current phase of consolidation and growth. As at the

end of September, 2004, there were 29 funds, which manage assets of Rs.153108 crores under

421 schemes.

The graph indicates the growth of assets over the years.

Chart 1.1: Growth in Assets under management

8

1.4 GLOBAL SCENARIO:

The money market fund segment has a total corpus of $1.48 trillion in the US against a corpus

of $100 million in India.

Out of the top 10 mutual funds worldwide, eight are bank sponsored. Only Fidelity and

capital are non-bank mutual funds in this group.

In the US the total number of schemes is higher than that of the listed companies while in

India we have just 277 schemes.

Internationally, mutual funds are allowed to go short. In India fund managers do not have

such leeway.

In the US about 9.7 million households will manage their asset on- line by the year 2003, such

a facility is not yet of avail in India.

On-line trading is great idea to reduce management expenses from the current 2% of total

assets to about 0.75% of the total asset.

72% of the core customer base of mutual funds in the top 50-broking firms in the US where

expected to trade on line by-2003.

9

1.5 ORGANISATION OF MUTUAL FUND:

Figure 1.4: Flow of SEBI to Investors

10

THE STRUCTURE CONSISTS OF

Sponsor

Sponsor is the person who acting alone or in combination with another body corporate

establishes a mutual fund. Sponsor must contribute at least 40% of the net worth of the

Investment managed and meet the eligibility criteria prescribed under the Securities and

Exchange Board of India (Mutual Fund) Regulations, 1996. The sponsor is not responsible or

liable for any loss or shortfall resulting from the operation of the Schemes beyond the initial

contribution made by it towards setting up of the Mutual Fund.

Trust

The Mutual Fund is constituted as a trust in accordance with the provisions of the Indian Trusts

Act, 1882 by the Sponsor. The trust deed is registered under the Indian Registration Act, 1908.

Trustee

Trustee is usually a company (corporate body) or a Board of Trustees (body of individuals). The

main responsibility of the Trustee is to safeguard the interest of the unit holders and ensure that

the AMC functions in the interest of investors and in accordance with the Securities and

Exchange Board of India (Mutual Funds) Regulations, 1996, the provisions of the Trust Deed

and the Offer Documents of the respective Schemes. At least 2/3rd directors of the Trustee are

independent directors who are not associated with the Sponsor in any manner.

Asset Management Company (AMC)

The AMC is appointed by the Trustee as the Investment Manager of the Mutual Fund. The AMC

is required to be approved by the Securities and Exchange Board of India (SEBI) to act as an

asset management company of the Mutual Fund. At least 50% of the directors of the AMC are

independent directors who are not associated with the Sponsor in any manner. The AMC must

have a net worth of at least 10 cores at all times.

Registrar and transfer agent

The AMC if so authorized by the Trust Deed appoints the Registrar and Transfer Agent to the

Mutual Fund. The Registrar processes the application form, redemption requests and dispatches

account statements to the unit holders. The Registrar and Transfer agent also handles

communications with investors and updates investor records.

11

1.6 PROCESS OF MUTUAL FUND

Figure 1.5: Process of mutual fund

In the above graph shows how Mutual Fund works and how investor earns money by investing in

the Mutual Fund. Investors put their saving as an investment in Mutual Fund. The Fund Manager

who is a person who takes the decisions where the money should be invested in securities

according to the scheme’s objective. Securities include Equities, Debentures, Govt. Securities,

Bonds, and Commercial Paper etc. These Securities generates returns to the Fund Manager. The

Fund Manager passes back return to the investor.

12

1.7 HOW TO INVEST IN MUTUAL FUND?

Mutual funds normally come out with an advertisement in newspapers publishing the date of

launch of the new schemes. Investors can also contact the agents and distributors of mutual funds

who are spread all over the country for necessary information and application forms. Forms can

be deposited with mutual funds through the agents and distributors who provide such services.

Now days, the post offices and banks also distribute the units of mutual funds. However, the

investors may please note that the mutual funds schemes being marketed by banks and post

offices should not be taken as their own schemes and no assurance of returns is given by them.

The only role of banks and post offices is to help in. distribution of mutual funds schemes to the

investors. Investors should not be carried away by commission/gifts given by agents/distributors

for investing in a particular scheme. On the other hand they must consider the track record of the

mutual fund and should take objective decision.

• One time investment

The amount that has to be invested in onetime is known as Onetime Investment. The investor has

to pay the whole amount at once. The minimum amount is Rs. 5000 and maximum is as per the

investor’s Choice. This investment is generally preferred for the business man who is able to pay

at one time.

• Systematic investment plan (SIP)

The amount that has to be invested through same monthly installment is known as Systematic

Investment Plan. The investor has to pay the minimum amount Rs.1000 monthly for all equity

and balanced schemes like that for 6months. And Rs.500 monthly for Tax Saver scheme like that

for 12 months. The minimum amount that the investor has to invest is Rs6000 and maximum as

per their choice. This type of investment is generally preferred for the salaried people.

13

1.8 REGULATORY OF MUTUAL FUND IN INDIA

• SEBI

The capital market regulates the mutual funds in India. SEBI requires all mutual funds to be

registered with them. SEBI issues guidelines for all mutual funds operations-investment,

accounts, expenses etc. Recently, it has been decided that Money Market Mutual Funds of

registered mutual funds will be regulated by SEBI through (Mutual Fund) Regulations 1996.

• RBI

RBI, a supervisor of the Banks owned Mutual Funds-As banks in India come under the

regulatory Jurisdiction of RBI, banks owned funds to be under supervision of RBI and SEBI.

RBI has supervisory responsibility over all entities that operate in the money markets.

• Ministry of finance (MOF)

Ministry of Finance ultimately supervises both the RBI and the SEBI and plays the role of

apex authority for any major disputes over SEBI guidelines.

• Company low board

Registrar of companies is called Company Low Board. AMCs of Mutual Funds are

companies registered under the companies Act 1956 and therefore answerable to regulatory

authorities empowered by the Companies Act.

• Stock exchange

Stock Exchanges are Self-regulatory organizations supervised by SEBI. Many closed ended

funds of AMCs are listed as stock exchanges and are traded like shares.

• Office of the public trustee

Mutual Fund being public trust is governed y the Indian Trust Act 1882. The Board of trustee

or the Trustees Company is accountable to the office of public trustee, which in turn reports

to the Charity commissioner.

14

1.9TYPES OF MUTUAL FUND SCHEMES

1. By structure

1.1. Open – Ended Schemes.

1.2. Close – Ended Schemes.

1.3. Interval Schemes.

2. By investment objective

2.1. Growth Schemes.

2.2. Income Schemes.

2.3. Balanced Schemes.

3. Other schemes

3.1. Tax Saving Schemes.

3.2. Special Schemes.

3.3. Index Schemes.

3.4. Sector Specific Schemes.

1.1 Open – ended schemes

The units offered by these schemes are available for sale and repurchase on any business day at

NAV based prices. Hence, the unit capital of the schemes keeps changing each day. Such

schemes thus offer very high liquidity to investors and are becoming increasingly popular in

India. Please note that an open-ended fund is NOT obliged to keep selling/issuing new units at all

times, and may stop issuing further subscription to new investors. On the other hand, an open-

ended fund rarely denies to its investor the facility to redeem existing units.

1.2 Closed – ended schemes

The unit capital of a close-ended product is fixed as it makes a one-time sale of fixed number of

units. These schemes are launched with an initial public offer (IPO) with a stated maturity period

after which the units are fully redeemed at NAV linked prices. In the interim, investors can buy

or sell units on the stock exchanges where they are listed. Unlike open-ended schemes, the unit

15

capital in closed-ended schemes usually remains unchanged. After an initial closed period, the

scheme may offer direct repurchase facility to the investors. Closed-ended schemes are usually

more illiquid as compared to open-ended schemes and hence trade at a discount to the NAV. This

discount tends towards the NAV closer to the maturity date of the scheme.

1.3 Interval schemes

These schemes combine the features of open-ended and closed-ended schemes. They may be

traded on the stock exchange or may be open for sale or redemption during pre-determined

intervals at NAV based prices.

2.1 Growth schemes

These schemes, also commonly called Equity Schemes, seek to invest a majority of their funds in

equities and a small portion in money market instruments. Such schemes have the potential to

deliver superior returns over the long term. However, because they invest in equities, these

schemes are exposed to fluctuations in value especially in the short term.

2.2Income schemes

These schemes, also commonly called Debt Schemes, invest in debt securities such as corporate

bonds, debentures and government securities. The prices of these schemes tend to be more stable

compared with equity schemes and most of the returns to the investors are generated through

dividends or steady capital appreciation. These schemes are ideal for conservative investors or

those not in a position to take higher equity risks, such as retired individuals. However, as

compared to the money market schemes they do have a higher price fluctuation risk and

compared to a Gilt fund they have a higher credit risk.

2.3Balanced schemes

These schemes are commonly known as Hybrid schemes. These schemes invest in both equities

as well as debt. By investing in a mix of this nature, balanced schemes seek to attain the objective

of income and moderate capital appreciation and are ideal for investors with a conservative, long-

term orientation.

3.1 Tax saving schemes

Investors are being encouraged to invest in equity markets through Equity Linked Savings

Scheme (“ELSS”) by offering them a tax rebate. Units purchased cannot be assigned /

16

transferred/ pledged / redeemed / switched – out until completion of 3 years from the date of

allotment of the respective Units.

The Scheme is subject to Securities & Exchange Board of India (Mutual Funds) Regulations,

1996 and the notifications issued by the Ministry of Finance (Department of Economic Affairs),

Government of India regarding ELSS.

Subject to such conditions and limitations, as prescribed under Section 88 of the Income-tax Act,

1961.

3.2 Index schemes

The primary purpose of an Index is to serve as a measure of the performance of the market as a

whole, or a specific sector of the market. An Index also serves as a relevant benchmark to

evaluate the performance of mutual funds. Some investors are interested in investing in the

market in general rather than investing in any specific fund. Such investors are happy to receive

the returns posted by the markets. As it is not practical to invest in each and every stock in the

market in proportion to its size, these investors are comfortable investing in a fund that they

believe is a good representative of the entire market. Index Funds are launched and managed for

such investors.

3.3Sector specific schemes

Sector Specific Schemes generally invests money in some specified sectors for example: “Real

Estate” Specialized real estate funds would invest in real estates directly, or may fund real estate

developers or lend to them directly or buy shares of housing finance companies or may even buy

their securitized assets.

17

1.10 WHAT IS THE PROCEDURE FOR REGISTERING A MUTUAL FUND

WITH SEBI?

An applicant proposing to sponsor a Mutual fund in India must submit an application in Form A

along with a fee of Rs.25, 000. The application is examined and once the sponsor satisfies certain

conditions such as being in the financial services business and possessing positive net worth for

the last five years, having net profit in three out of the last five years and possessing the general

reputation of fairness and integrity in all business transactions, it is required to complete the

remaining formalities for setting up a Mutual fund.

These include inter alia, executing the trust deed and investment management agreement, setting

up a trustee company/board of trustees comprising two- thirds independent trustees,

incorporating the asset management company (AMC), contributing to at least 40% of the net

worth of the AMC and appointing a custodian. Upon satisfying these conditions, the registration

certificate is issued subject to the payment of registration fees of Rs.25.00 lacs for details; see the

SEBI (Mutual funds) Regulations, 1996.

18

1.11 SEBI REGISTERED MUTUAL FUND

1. FORTIS Mutual fund

2. Alliance Capital Mutual fund,

3. AIG Global Investment Group Mutual fund

4. Benchmark Mutual fund,

5. Baroda Pioneer Mutual fund

6. Birla Mutual fund

7. Bharti AXA Mutual fund

8. CanaraRobeco Mutual fund

9. CRB Mutual fund (Suspended)

10. DBS Chola Mutual fund,

11. Deutsche Mutual fund

12. DSP Blackrock Mutual fund,

13. Edelweiss Mutual fund

14. Escorts Mutual fund,

15. Franklin Templeton Mutual fund

16. Fidelity Mutual fund

17. Goldman Sachs Mutual fund

18. HDFC Mutual fund,

19. HSBC Mutual fund,

20. ICICI Securities Fund,

21. IL & FS Mutual fund,

22. ING Mutual fund,

19

23. ICICI Prudential Mutual fund

24. IDFC Mutual fund,

25. JM Financial Mutual fund

26. JP Morgan Mutual fund

27. Kotak Mahindra Mutual fund,

29. LIC Mutual fund

31. Morgan Stanley Mutual fund

32. Mirae Asset Mutual fund

33. Principal Mutual fund

34. Quantum Mutual fund,

35. Reliance Mutual fund

36. Religare AEGON Mutual fund

37. Sahara Mutual fund,

38. SBI Mutual fund

39. Shriram Mutual fund

40. Sundaram BNP Paribas Mutual fund,

41. Taurus Mutual fund

42. Tata Mutual fund,

43. UTI Mutual fund

20

1.12 POINTERS TO MEASURE MUTUAL FUND PERFORMANCE

MEASURES DESCRIPTION IDEAL RANGE

STANDARD

DEVIATION

Standard Deviation allows evaluating the volatility of the

fund. The standard deviation of a fund measures this risk

by measuring the degree to which the fund fluctuates in

relation to its mean return.

Should be near to it’s

mean return.

BETA Beta is a fairly commonly used measure of risk. It

basically indicates the level of volatility associated with

the fund as compared to the benchmark.

Beta > 1 = high risky

Beta = 1 = Average

Beta <1 = Low Risky

R-SQUARE R- square measures the correlation of a fund’s movement

to that of an index. R-squared describes the level of

association between the fund's volatility and market risk.

R-squared values

range between 0 and 1,

where 0 represents no

correlation and 1

represents full

correlation.

ALPHA Alpha is the difference between the returns one would

expect from a fund, given its beta, and the return it

actually produces. It also measures the unsystematic risk.

Alpha is positive =

returns of stock are

better then market

returns.

Alpha is negative =

returns of stock are

worst then market.

Alpha is zero = returns

are same as market.

SHARPE

RATIO Sharpe Ratio= Fund return in excess of risk free return/

Standard deviation of Fund. Sharpe ratios are ideal for

comparing funds that have a mixed asset classes.

The higher the Sharpe

ratio, the better a funds

returns relative to the

amount of risk taken.

21

1.13 HOW TO REDUCE RISK WHILE INVESTING?

Any kind of investment we make is subject to risk. In fact we get return on our investment purely and

solely because at the very beginning we take the risk of parting with our funds, for getting higher

value back at a later date. Partition itself is a risk.

Well known economist and Nobel Prize recipient William Sharpe tried to segregate the total risk

faced in any kind of investment into two parts - systematic (Systemic) risk and unsystematic

(Unsystematic) risk.

Systematic risk is that risk which exists in the system. Some of the biggest examples of systematic

risk are inflation, recession, war, political situation etc.

Inflation erodes returns generated from all investments e.g. If return from fixed deposit is 8 per cent

and if inflation is 6 per cent then real rate of return from fixed deposit is reduced by 6 per cent.

Similarly if returns generated from equity market is 18 per cent and inflation is still 6 per cent then

equity returns will be lesser by the rate of inflation. Since inflation exists in the system there is no

way one can stay away from the risk of inflation.

Economic cycles, war and political situations have effects on all forms of investments. Also these

exist in the system and there is no way to stay away from them. It is like learning to walk.

Anyone who wants to learn to walk has to first fall; you cannot learn to walk without falling.

Similarly anyone who wants to invest has to first face systematic risk; there can never make any kind

of investment without systematic risk.

Another form of risk is unsystematic risk. This risk does not exist in the system and hence is not

applicable to all forms of investment. Unsystematic risk is associated with particular form of

investment.

22

Suppose we invest in stock market and the market falls, then only our investment in equity gets

affected OR if we have placed a fixed deposit in particular bank and bank goes bankrupt, than we

only lose money placed in that bank.

While there is no way to keep away from risk, we can always reduce the impact of risk.

Diversification helps in reducing the impact of unsystematic risk. If our investment is distributed

across various asset classes the impact of unsystematic risk is reduced.

If we have placed fixed deposit in several banks, then even if one of the banks goes bankrupt our

entire fixed deposit investment is not lost.

Similarly if our equity investment is in Tata Motors, HLL, Infosys, adverse news about Infosys will

only impact investment in Infosys, all other stocks will not have any impact.

To reduce the impact of systematic risk, we should invest regularly. By investing regularly we

average out the impact of risk.

Mutual fund, as an investment vehicle gives us benefit of both diversification and averaging.

Portfolio of mutual funds consists of multiple securities and hence adverse news about single security

will have nominal impact on overall portfolio.

By systematically investing in mutual fund we get benefit of rupee cost averaging.

23

1.14 ADVANTAGES OF MUTUAL FUNDS

Figure 1.6 Advantages of mutual fund

Professional Management

The major advantage of investing in a mutual fund is that you get a professional money manager to

manage your investments for a small fee. You can leave the investment decisions to him and only

have to monitor the performance of the fund at regular intervals.

Diversification

Considered the essential tool in risk management, mutual funds make it possible for even small

investors to diversify their portfolio. A mutual fund can effectively diversify its portfolio because of

the large corpus. However, a small investor cannot have a well-diversified portfolio because it calls

for large investment. For example, a modest portfolio of 10 bluechip stocks calls for a few a few

thousands.

Convenient Administration

Mutual funds offer tailor-made solutions like systematic investment plans and systematic withdrawal

plans to investors, which is very convenient to investors. Investors also do not have to worry about

investment decisions, they do not have to deal with brokerage or depository, etc. for buying or selling

of securities. Mutual funds also offer specialized schemes like retirement plans, children’s plans,

industry specific schemes, etc. to suit personal preference of investors. These schemes also help small

investors with asset allocation of their corpus. It also saves a lot of paper work.

Regulation

Tex Benefit

Professional Mngt

Variety

Diversification

Affordability

24

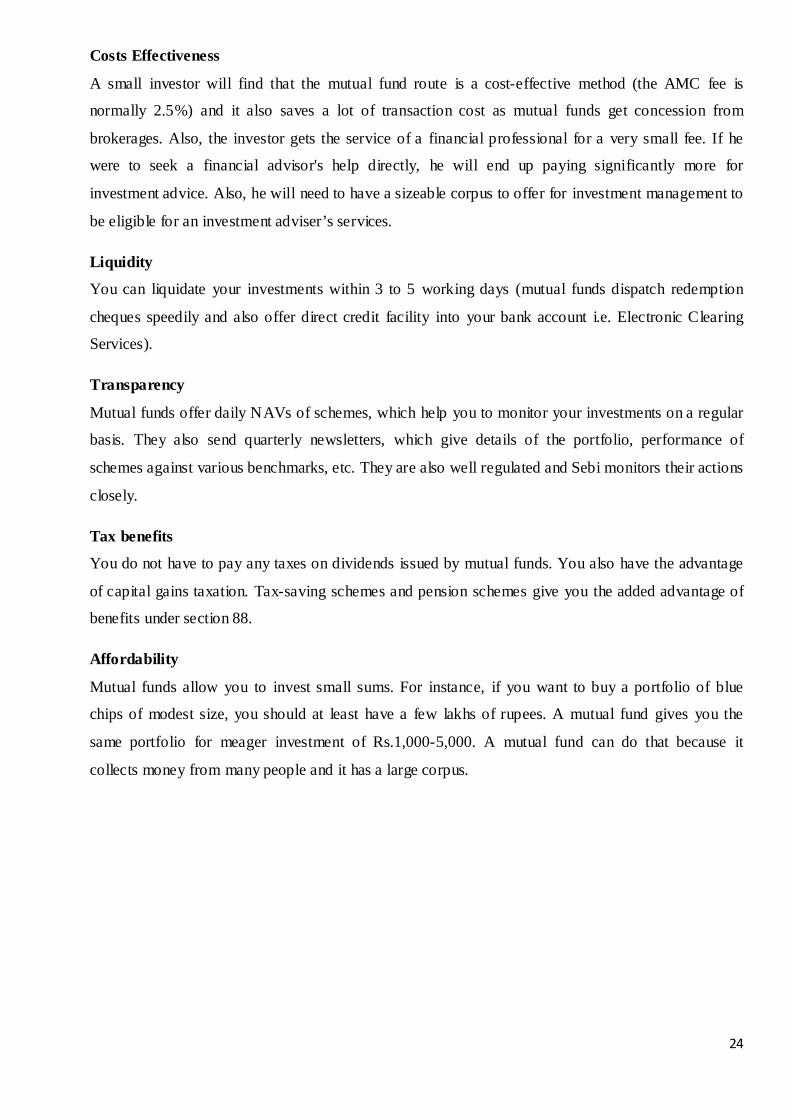

Costs Effectiveness

A small investor will find that the mutual fund route is a cost-effective method (the AMC fee is

normally 2.5%) and it also saves a lot of transaction cost as mutual funds get concession from

brokerages. Also, the investor gets the service of a financial professional for a very small fee. If he

were to seek a financial advisor's help directly, he will end up paying significantly more for

investment advice. Also, he will need to have a sizeable corpus to offer for investment management to

be eligible for an investment adviser’s services.

Liquidity

You can liquidate your investments within 3 to 5 working days (mutual funds dispatch redemption

cheques speedily and also offer direct credit facility into your bank account i.e. Electronic Clearing

Services).

Transparency

Mutual funds offer daily NAVs of schemes, which help you to monitor your investments on a regular

basis. They also send quarterly newsletters, which give details of the portfolio, performance of

schemes against various benchmarks, etc. They are also well regulated and Sebi monitors their actions

closely.

Tax benefits

You do not have to pay any taxes on dividends issued by mutual funds. You also have the advantage

of capital gains taxation. Tax-saving schemes and pension schemes give you the added advantage of

benefits under section 88.

Affordability

Mutual funds allow you to invest small sums. For instance, if you want to buy a portfolio of blue

chips of modest size, you should at least have a few lakhs of rupees. A mutual fund gives you the

same portfolio for meager investment of Rs.1,000-5,000. A mutual fund can do that because it

collects money from many people and it has a large corpus.

25

1.15 DISADVANTAGES OF MUTUAL FUNDS

Professional Management-

Did you notice how we qualified the advantage of professional management with the word

"theoretically"? Many investors debate over whether or not the so-called professionals are any better

than you or I at picking stocks. Management is by no means infallible, and, even if the fund loses

money, the manager still takes his/her cut. We'll talk about this in detail in a later section.

Costs

Mutual funds don't exist solely to make your life easier--all funds are in it for a profit. The Mutual

fund industry is masterful at burying costs under layers of jargon. These costs are so complicated that

in this tutorial we have devoted an entire section to the subject.

Dilution

It's possible to have too much diversification (this is explained in our article entitled "Are You Over-

Diversified?"). Because funds have small holdings in so many different companies, high returns from

a few investments often don't make much difference on the overall return. Dilution is also the result of

a successful fund getting too big. When money pours into funds that have had strong success, the

manager often has trouble finding a good investment for all the new money.

Taxes

When making decisions about your money, fund managers don't consider your personal tax situation.

For example, when a fund manager sells a security, a capital-gain tax is triggered, which affects how

profitable the individual is from the sale. It might have been more advantageous for the individual to

defer the capital gains liability.

Equity funds

If selected in the right manner and in the right proportion, have the ability to play an important role in

achieving most long-term objectives of investors in different segments. While the selection process

becomes much easier if you get advice from professionals, it is equally important to know certain

aspects of equity investing yourself to do justice to your hard earned money.

26

Chapter: - 2

Literature Review

27

LITERATURE REVIEW

Literature on mutual fund performance evaluation is enormous. A few research studies that have

influenced the preparation of this paper substantially are discussed in this section.

Sharpe, William F. (1966) suggested a measure for the evaluation of portfolio performance. Drawing

on results obtained in the field of portfolio analysis, economist Jack L. Treynor has suggested a new

predictor of mutual fund performance, one that differs from virtually all those used previously by

incorporating the volatility of a fund's return in a simple yet meaningful manner.

Michael C. Jensen (1967) derived a risk-adjusted measure of portfolio performance (Jensen’s alpha)

that estimates how much a manager’s forecasting ability contributes to fund’s returns.

As indicated by Statman (2000), the e SDAR of a fund portfolio is the excess return of the portfolio

over the return of the benchmark index, where the portfolio is leveraged to have the benchmark

index’s standard deviation.

S.Narayan Rao, evaluated performance of Indian mutual funds in a bear market through relative

performance index, risk-return analysis, Treynor’s ratio, Sharpe’s ratio, Sharpe’s measure , Jensen’s

measure, and Fama’s measure. The study used 269 open-ended schemes (out of total schemes of 433)

for computing relative performance index. Then after excluding funds whose returns are less than

risk-free returns, 58 schemes are finally used for further analysis. The results of performance

measures suggest that most of mutual fund schemes in the sample of 58 were able to satisfy investor’s

expectations by giving excess returns over expected returns based on both premium for systematic

risk and total risk. Bijan Roy, et. al., conducted an empirical study on conditional performance of

Indian mutual funds. This paper uses a technique called conditional performance evaluation on a

sample of eighty-nine Indian mutual fund schemes .This paper measures the performance of various

mutual funds with both unconditional and conditional form of CAPM, Treynor- Mazuy model and

Henriksson-Merton model. The effect of incorporating lagged information variables into the

evaluation of mutual fund managers’ performance is examined in the Indian context. The results

suggest that the use of conditioning lagged information variables improves the performance of mutual

fund schemes, causing alphas to shift towards right and reducing the number of negative timing

coefficients. Mishra, et al., (2002) measured mutual fund performance using lower partial moment. In

this paper, measures of evaluating portfolio performance based on lower partial moment are

developed. Risk from the lower partial moment is measured by taking into account only those states

in which return is below a pre-specified “target rate” like risk-free rate. KshamaFernandes(2003)

28

evaluated index fund implementation in India. In this paper, tracking error of index funds in India is

measured.

The consistency and level of tracking errors obtained by some well-run index fund suggests that it is

possible to attain low levels of tracking error under Indian conditions. At the same time, there do

seem to be periods where certain index funds appear to depart from the discipline of indexation. K.

Pendaraki et al. studied construction of mutual fund portfolios, developed a multi-criteria

methodology and applied it to the Greek market of equity mutual funds. The methodology is based on

the combination of discrete and continuous multi-criteria decision aid methods for mutual fund

selection and composition. UTADIS multi-criteria decision aid method is employed in order to

develop mutual fund’s performance models. Goal programming model is employed to determine

proportion of selected mutual funds in the final

portfolios.

ZakriY.Bello (2005) matched a sample of socially responsible stock mutual funds matched

to randomly selected conventional funds of similar net assets to investigate differences in

characteristics of assets held, degree of portfolio diversification and variable effects of diversification

on investment performance. The study found that socially responsible funds do not differ significantly

from conventional funds in terms of any of these attributes. Moreover, the effect of diversification on

investment performance is not different between the two groups. Both groups underperformed the

Domini 400 Social Index and S & P 500 during the study period.

29

Chapter:-3 Research Methodology

30

RESEARCH PROPOSAL

Main Objective:

“Awareness of Mutual Fund among Investors of Mehsana City”

The Indian mutual fund industry is a very large industry consisting of number of investors. In this era

of competition different investor’s have different investment objectives. As the human behavior is

unpredictable, this study helps in finding out the necessary facts regarding investors’ opinion and

perceptions regarding mutual fund investment. The main objectives of the study are:

1. To study the growth of mutual fund industry in India.

2. To analyze the investors awareness and perception regarding investing in mutual funds.

3. To find out the investors opinion regarding major deficiencies in the working of the mutual fund

industry

4. To find out the suggestions from the investors that can help in plugging out these deficiencies

31

Research Methodology

3.1 Research Design

Descriptive study

Descriptive studies are under taken in many circumstances. When the researcher is interested in

knowing the characteristics of certain group such as age, gender, occupation, educational level or

income, a descriptive study may be necessary. Other cases when a descriptive study could be taken up

are when researcher is interested in knowing the proportion of people in a given population who are

investing in mutual fund a particular manner or determining the relationship between two or more

variables. The objective of such a study is to answer the “who, what, when, where and how” of the

subject under investigation.

3.2 Population Definition

The target population was the investors and non- investors of Mehsana city.

3.3 Sampling Frame

In these of type research study we cannot use sampling frame.

3.4 Sampling Size

This research consists of the 280 sample size for undergone this research project.

3.5 Sampling Method

In these research study we use convince non-probability sampling method for fill the Questionnaire.

3.6 Approach

Survey approach using questionnaire.

3.7 Measure Used

For conducting this research we are used structure questionnaire in which we are used the different

scales for collecting the information.

3.8 Area of the study

The research has been conducted in Mehsana city.

32

Chapter:-4 Data Analysis & Interpretation

33

Chi-Square Test:- 1. BASED ON GENDER (Q-)

Ho: There is no significant difference between gender and preference of investment.

H1: There is significant difference between gender and preference of investment.

Test Statistics Gender Where do you prefer to invest your money?

Chi-Square 11.200a 213.250b df 1 4 Asymp. Sig. .001 .000

INTERPRETATION:

The significant level is less than 0.05 so that alternative hypothesis is accepted and the null hypothesis is rejected. Therefore we can say that there is no significantly difference between gender and preference of investment.

34

ANOVA TEST:-

4.1BASED ON AGE

4.1.1

Ho: There is no significant difference between age and aware of the mutual fund investment.

H1: There is significant difference between age and aware of the mutual fund investment.

ANOVA I am aware of the Mutual Fund Investment.

Sum of Squares df Mean Square F Sig.

Between Groups 2.069 2 1.035 .767 .465 Within Groups 373.642 277 1.349

Total 375.711 279

Descriptive

I am aware of the Mutual Fund Investment.

N Mean Std. Deviation Std. Error

18-25 27 3.44 1.086 .209 26-35 155 3.15 1.155 .093 above 36 98 3.16 1.190 .120 Total 280 3.18 1.160 .069

35

Post Hoc Tests

Multiple Comparisons I am aware of the Mutual Fund Investment. LSD

(I) Age (J) Age Mean Difference

(I-J) Std. Error Sig.

18-25 26-35 .296 .242 .223

above 36 .281 .252 .266

26-35 18-25 -.296 .242 .223

above 36 -.015 .150 .921

above 36 18-25 -.281 .252 .266

26-35 .015 .150 .921

INTERPRETATION:

The significant level is 0.465 which is greater than 0.05 so that alternative hypothesis is rejected and the null hypothesis is accepted. Therefore we can say that there is no significantly difference between age and the mutual investment fund.

36

4.1.2

Ho: There is no significant difference between age and mutual fund safe.

H1: There is significant difference between age and mutual fund safe.

Descriptive Mutual Fund is safe

N Mean Std.

Deviation Std. Error

18-25 27 3.70 1.203 .232 26-35 155 3.68 .979 .079 above 36 98 3.71 1.075 .109 Total 280 3.70 1.032 .062

ANOVA

Mutual Fund is safe

Sum of Squares Df Mean Square F Sig.

Between Groups .057 2 .029 .027 .974

Within Groups 297.139 277 1.073

Total 297.196 279

37

Post Hoc Tests

Multiple Comparisons Mutual Fund is safe LSD

(I) Age (J) Age Mean Difference

(I-J) Std. Error Sig.

18-25 26-35 .020 .216 .927

above 36 -.011 .225 .963 26-35 18-25 -.020 .216 .927

above 36 -.030 .134 .820

above 36 18-25 .011 .225 .963 26-35 .030 .134 .820

Interpretation:

The significant level is 0.974 which is greater than 0.05 so that alternative hypothesis is rejected and the null hypothesis is accepted. Therefore we can say that there is no significantly difference between age and mutual fund safe.

38

4.1.3

Ho: There is no significant difference between age and return on mutual fund.

H1: There is significant difference between age and return on mutual fund.

Descriptive Mutual Fund gives better return than Bank Deposit.

N Mean Std. Deviation Std. Error

18-25 27 3.37 1.115 .214 26-35 155 3.22 1.130 .091 above 36 98 3.20 1.201 .121 Total 280 3.23 1.151 .069

ANOVA Mutual Fund gives better return than Bank Deposit.

Sum of Squares df Mean Square F Sig.

Between Groups .615 2 .307 .231 .794 Within Groups 368.757 277 1.331

Total 369.371 279

39

Post Hoc Tests

Multiple Comparisons Mutual Fund gives better return than Bank Deposit. LSD

(I) Age (J) Age Mean Difference

(I-J) Std. Error Sig.

18-25 26-35 .151 .241 .531

above 36 .166 .251 .508 26-35 18-25 -.151 .241 .531

above 36 .015 .149 .918

above 36 18-25 -.166 .251 .508 26-35 -.015 .149 .918

INTERPRETATION:

The significant level is 0.794 which is greater than 0.05 so that alternative hypothesis is rejected

and the null hypothesis is accepted. Therefore we can say that there is no significantly difference

between age and return on mutual fund.

40

4.1.4

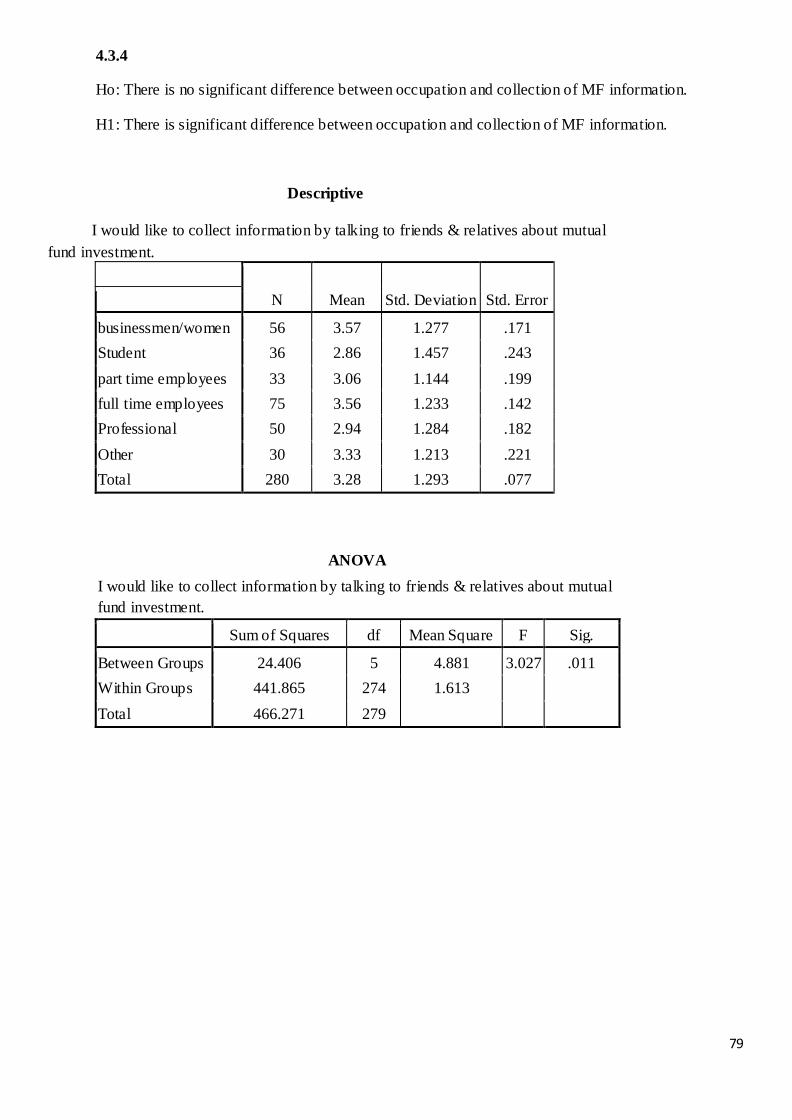

Ho: There is no significant difference between age and collection of mutual fund information.

H1: There is significant difference between age and collection of mutual fund information.

Descriptive I would like to collect information by talking to friends & relatives about mutual fund investment.

N Mean Std. Deviation Std. Error

18-25 27 3.26 1.289 .248 26-35 155 3.30 1.311 .105 above 36 98 3.24 1.277 .129 Total 280 3.28 1.293 .077

ANOVA I would like to collect information by talking to friends & relatives about mutual fund investment. Sum of

Squares df Mean Square F Sig.

Between Groups .215 2 .108 .064 .938 Within Groups 466.056 277 1.683

Total 466.271 279

41

Post Hoc Tests

Multiple Comparisons I would like to collect information by talking to friends & relatives about mutual fund investment. LSD

(I) Age (J) Age Mean Difference

(I-J) Std. Error Sig.

18-25 26-35 -.044 .270 .871

above 36 .014 .282 .959

26-35 18-25 .044 .270 .871 above 36 .058 .167 .728

above 36 18-25 -.014 .282 .959

26-35 -.058 .167 .728

INTERPRETATION:

The significant level is 0.938 which is greater than 0.05 so that alternative hypothesis is rejected

and the null hypothesis is accepted. Therefore we can say that there is no significantly difference

between age and collection of mutual fund investment.

42

4.1.5

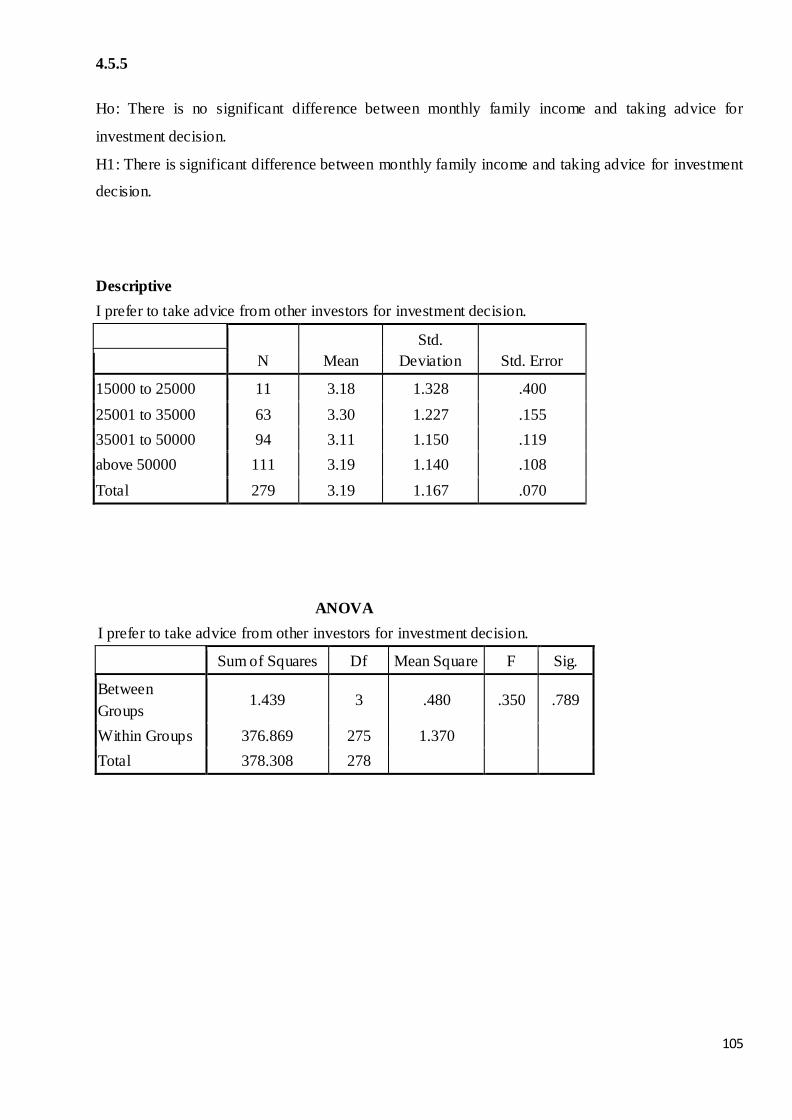

Ho: There is no significant difference between age and taking advice for investment decision.

H1: There is significant difference between age and taking advice for investment decision.

Descriptive I prefer to take advice from other investors for investment decision.

N Mean Std. Deviation Std. Error

18-25 27 3.30 1.137 .219 26-35 155 3.15 1.157 .093 above 36 98 3.21 1.195 .121 Total 280 3.19 1.165 .070

ANOVA I prefer to take advice from other investors for investment decision.

Sum of Squares Df Mean Square F Sig.

Between Groups

.554 2 .277 .203 .816

Within Groups 378.414 277 1.366

Total 378.968 279

43

Post Hoc Tests Multiple Comparisons I prefer to take advice from other investors for investment decision. LSD

(I) Age (J) Age Mean Difference

(I-J) Std. Error Sig.

18-25 26-35 .141 .244 .562

above 36 .082 .254 .747

26-35 18-25 -.141 .244 .562

above 36 -.059 .151 .694 above 36 18-25 -.082 .254 .747

26-35 .059 .151 .694

INTERPRETATION:

The significant level is 0.816 which is greater than 0.05 so that alternative hypothesis is rejected

and the null hypothesis is accepted. Therefore we can say that there is no significantly difference

between age and taking advice for investment decision.

44

4.1.6

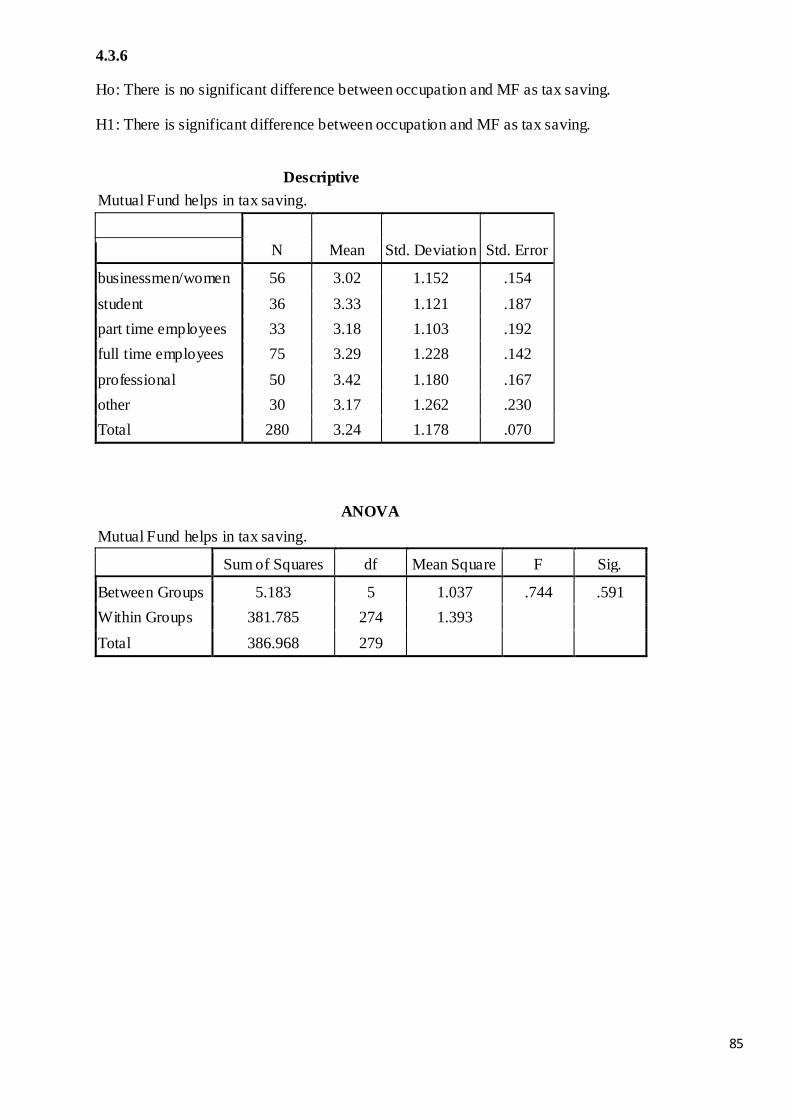

Ho: There is no significant difference between age and mutual fund in tax saving.

H1: There is significant difference between age and mutual fund in tax saving.

Descriptive

Mutual Fund helps in tax saving.

N Mean Std. Deviation Std. Error

18-25 27 2.89 1.281 .247 26-35 155 3.28 1.188 .095 above 36 98 3.27 1.127 .114 Total 280 3.24 1.178 .070

ANOVA Mutual Fund helps in tax saving.

Sum of Squares df Mean Square F Sig.

Between Groups

3.689 2 1.845 1.333 .265

Within Groups 383.278 277 1.384

Total 386.968 279

45

Post Hoc Tests

Multiple Comparisons Mutual Fund helps in tax saving. LSD

(I) Age

Mean Difference (I-J) Std. Error Sig.

18-25 26-35 -.395 .245 .108

above 36 -.376 .256 .142

26-35 18-25 .395 .245 .108 above 36 .019 .152 .903

above 36 18-25 .376 .256 .142

26-35 -.019 .152 .903

INTERPRETATION:

The significant level is 0.265 which is greater than 0.05 so that alternative hypothesis is rejected

and the null hypothesis is accepted. Therefore we can say that there is no significantly difference

between age and mutual fund in tax saving.

46

4.1.7

Ho: There is no significant difference between age and mutual fund liquidity.

H1: There is significant difference between age and mutual fund liquidity.

Descriptive Mutual Fund provides better liquidity than other investment option.

N Mean Std. Deviation Std. Error

18-25 27 3.30 1.137 .219 26-35 155 3.15 1.157 .093 above 36 98 3.21 1.195 .121 Total 280 3.19 1.165 .070

ANOVA Mutual Fund provides better liquidity than other investment option.

Sum of Squares df Mean Square F Sig.

Between Groups .554 2 .277 .203 .816

Within Groups 378.414 277 1.366

Total 378.968 279

47

Post Hoc Tests

Multiple Comparisons Mutual Fund provides better liquidity than other investment option. LSD

(I) Age (J) Age Mean Difference

(I-J) Std. Error Sig.

18-25 26-35 .141 .244 .562

above 36 .082 .254 .747

26-35 18-25 -.141 .244 .562 above 36 -.059 .151 .694

above 36 18-25 -.082 .254 .747

26-35 .059 .151 .694

INTERPRETATION:

The significant level is 0.816 which is greater than 0.05 so that alternative hypothesis is rejected and

the null hypothesis is accepted. Therefore we can say that there is no significantly difference between

age and mutual fund liquidity.

48

4.1.8

Ho: There is no significant difference between age and mutual fund is diversification of portfolio.

H1: There is significant difference between age and mutual fund is diversification of portfolio.

Descriptive Mutual fund provides the diversification of portfolio.

N Mean Std. Deviation Std. Error

18-25 27 3.44 1.251 .241 26-35 155 3.55 1.070 .086 above 36 98 3.51 1.124 .114 Total 280 3.52 1.104 .066

ANOVA

Mutual fund provides the diversification of portfolio.

Sum of Squares df Mean Square F Sig.

Between Groups .281 2 .141 .115 .892

Within Groups 339.544 277 1.226

Total 339.825 279

49

Post Hoc Tests

Multiple Comparisons Mutual fund provides the diversification of portfolio. LSD

(I) Age (J) Age Mean Difference

(I-J) Std. Error Sig.

18-25 26-35 -.104 .231 .653

above 36 -.066 .241 .785

26-35 18-25 .104 .231 .653 above 36 .038 .143 .789

above 36 18-25 .066 .241 .785

26-35 -.038 .143 .789

INTERPRETATION:

The significant level is 0.892 which is greater than 0.05 so that alternative hypothesis is rejected and

the null hypothesis is accepted. Therefore we can say that there is no significantly difference between

age and mutual fund is diversification of portfolio.

50

4.1.9

Ho: There is no significant difference between age and taking information in future.

H1: There is significant difference between age and taking information in future.

ANOVA I am always interested in taking more information about mutual fund investment in future.

Sum of Squares df Mean Square F Sig.

Between Groups

.615 2 .307 .231 .794

Within Groups 368.757 277 1.331

Total 369.371 279

Descriptive I am always interested in taking more information about mutual fund investment in future.

N Mean Std. Deviation Std. Error

18-25 27 3.37 1.115 .214 26-35 155 3.22 1.130 .091 above 36 98 3.20 1.201 .121 Total 280 3.23 1.151 .069

51

Post Hoc Tests Multiple Comparisons I am always interested in taking more information about mutual fund investment in future. LSD

(I) Age (J) Age Mean Difference

(I-J) Std. Error Sig.

18-25 26-35 .151 .241 .531

above 36 .166 .251 .508 26-35 18-25 -.151 .241 .531

above 36 .015 .149 .918

above 36 18-25 -.166 .251 .508 26-35 -.015 .149 .918

INTERPRETATION:

The significant level is 0.794 which is greater than 0.05 so that alternative hypothesis is rejected and the

null hypothesis is accepted. Therefore we can say that there is no significantly difference between age

and taking information in future.

52

4.2BASED ON EDUCATION

4.2.1

Ho= There is no relation between education and awareness of mutual fund.

H1= There is relation between education and awareness of mutual fund.

Descriptive

I am aware of the Mutual Fund Investment.

N Mean Std. Deviation Std. Error

12th std 31 3.29 1.189 .213 Graduation 113 3.19 1.192 .112 post-graduation 89 3.07 1.106 .117 Other 47 3.32 1.181 .172 Total 280 3.18 1.160 .069

ANOVA

I am aware of the Mutual Fund Investment.

Sum of Squares df Mean Square F Sig.

Between Groups 2.418 3 .806 .596 .618 Within Groups 373.293 276 1.353

Total 375.711 279

53

Post- Hoc Tests I am aware of the Mutual Fund Investment. LSD

(I) Education (J) Education Mean Difference (I-

J) Std. Error Sig.

12th Std Graduation .104 .236 .658

post-graduation .223 .243 .359

Other -.029 .269 .915

Graduation 12th Std -.104 .236 .658 post-graduation .118 .165 .473

Other -.133 .202 .510

post-graduation 12th Std -.223 .243 .359 Graduation -.118 .165 .473

Other -.252 .210 .231

other 12th Std .029 .269 .915 Graduation .133 .202 .510

Post-graduation .252 .210 .231

INTERPRETATION:

The significant level is 0.618 which is greater than 0.05 so the alternative hypothesis is rejected

and the null hypothesis is accepted. Therefore we can say that there is a significant difference

between Education and awareness of mutual fund.

54

4.2.2

Ho= There is no relation between education and mutual fund safety.

H1= There is relation between education and mutual fund safety.

Descriptive

Mutual Fund is safe

N Mean Std. Deviation Std. Error

12th Std 31 3.48 1.208 .217 Graduation 113 3.73 .982 .092 post-graduation 89 3.55 1.108 .117 Other 47 4.02 .794 .116 Total 280 3.70 1.032 .062

ANOVA

Mutual Fund is safe

Sum of Squares Df Mean Square F Sig.

Between Groups 8.418 3 2.806 2.682 .047 Within Groups 288.779 276 1.046

Total 297.196 279

55

Post-Hoc Tests

Mutual Fund is safe LSD

(I) Education (J) Education Mean Difference (I-J) Std. Error Sig.

12th Std Graduation -.251 .207 .228

Post-graduation -.067 .213 .755

Other -.537* .237 .024 Graduation 12th Std .251 .207 .228

Post-graduation .184 .145 .206

other -.287 .178 .107 Post-graduation 12th Std .067 .213 .755

Graduation -.184 .145 .206

other -.471* .184 .011 other 12th Std .537* .237 .024

Graduation .287 .178 .107

Post-graduation .471* .184 .011 *. The mean difference is significant at the 0.05 level.

INTERPRETATION:

The significant level is 0.047 which is less than 0.05 so the alternative hypothesis is accepted

and the null hypothesis is rejected. Therefore we can say that there is no significant difference

between Education and awareness of mutual fund.

56

4.2.3

Ho= There is no relation between education and return on mutual fund.

H1= There is relation between education and return on mutual fund.

Descriptive Mutual Fund gives better return than Bank Deposit.

N Mean Std. Deviation Std. Error

12th Std 31 3.48 1.122 .201 Graduation 113 3.23 1.180 .111 Post-graduation 89 3.06 1.101 .117 Other 47 3.38 1.171 .171 Total 280 3.23 1.151 .069

ANOVA Mutual Fund gives better return than Bank Deposit.

Sum of Squares df Mean Square F Sig.

Between Groups 5.786 3 1.929 1.464 .225 Within Groups 363.585 276 1.317

Total 369.371 279

57

Post-Hoc test

Mutual Fund gives better return than Bank Deposit. LSD

(I) Education (J) Education Mean Difference

(I-J) Std. Error Sig.

12th Std Graduation .254 .233 .276

Post-graduation .428 .239 .075

other .101 .266 .704 Graduation 12th Std -.254 .233 .276

Post-graduation .174 .163 .286

other -.153 .199 .443 Post-graduation 12th Std -.428 .239 .075

Graduation -.174 .163 .286

other -.327 .207 .115 Other 12th Std -.101 .266 .704

Graduation .153 .199 .443

Post-graduation .327 .207 .115

INTERPRETATION:

The significant level is 0.225 which is greater than 0.05 so the alternative hypothesis is rejected

and the null hypothesis is accepted. Therefore we can say that there is a significant difference

between Education and return on mutual fund.

58

4.2.4

Ho= There is no relation between education and collection of mutual fund information.

H1= There is relation between education and collection of mutual fund information.

Descriptive

I would like to collect information by talking to friends & relatives about mutual fund investment.

N Mean Std. Deviation Std. Error

12th Std 31 2.94 1.263 .227 Graduation 113 3.24 1.311 .123 Post-graduation 89 3.39 1.302 .138 other 47 3.38 1.243 .181 Total 280 3.28 1.293 .077

ANOVA I would like to collect information by talking to friends & relatives about mutual fund investment. Sum of

Squares df Mean Square F Sig.

Between Groups 5.509 3 1.836 1.100 .350 Within Groups 460.762 276 1.669

Total 466.271 279

59

Post-Hoc Test

I would like to collect information by talking to friends & relatives about mutual fund investment.

(I) Education (J) Education Mean Difference

(I-J) Std. Error Sig.

12th Std Graduation -.303 .262 .248

Post-graduation -.458 .269 .090

other -.447 .299 .136 Graduation 12th Std .303 .262 .248

Post-graduation -.154 .183 .400

other -.144 .224 .521 Post-graduation 12th Std .458 .269 .090

Graduation .154 .183 .400

other .010 .233 .965 other 12th Std .447 .299 .136

Graduation .144 .224 .521

Post-graduation -.010 .233 .965

INTERPRETATION:

The significant level is 0.350 which is greater than 0.05 so the alternative hypothesis is rejected

and the null hypothesis is accepted. Therefore we can say that there is a significant difference

between Education and collection of mutual fund information.

60

4.2.5

Ho= There is no relation between education and taking advice for investment decision.

H1= There is relation between education and taking advice for investment decision.

Descriptive I prefer to take advice from other investors for investment decision.

N Mean Std. Deviation Std. Error

12th Std 31 3.39 1.202 .216 Graduation 113 3.19 1.202 .113 Post-graduation 89 3.10 1.108 .117 other 47 3.21 1.178 .172 Total 280 3.19 1.165 .070

ANOVA

I prefer to take advice from other investors for investment decision.

Sum of Squares df Mean Square F Sig.

Between Groups 1.934 3 .645 .472 .702 Within Groups 377.034 276 1.366

Total 378.968 279

61

Post-Hoc Test I prefer to take advice from other investors for investment decision. LSD

(I) Education (J) Education Mean Difference

(I-J) Std. Error Sig.

12th Std Graduation .192 .237 .418

Post-graduation .286 .244 .242

other .174 .270 .520

Graduation 12th Std -.192 .237 .418 Post-graduation .094 .166 .573

other -.018 .203 .929

Post-graduation 12th Std -.286 .244 .242 Graduation -.094 .166 .573

other -.112 .211 .597

Other 12th Std -.174 .270 .520 Graduation .018 .203 .929

Post-graduation .112 .211 .597

INTERPRETATION:

The significant level is 0.702 which is greater than 0.05 so the alternative hypothesis is rejected

and the null hypothesis is accepted. Therefore we can say that there is a significant difference

between Education and taking advice for investment decision.

62

4.2.6

Ho= There is no relation between education and MF as tax saving.

H1= There is relation between education and MF as tax saving.

Descriptive Mutual Fund helps in tax saving.

N Mean Std. Deviation Std. Error

12th Std 31 2.94 1.124 .202 Graduation 113 3.31 1.158 .109 Post-graduation 89 3.45 1.206 .128 Other 47 2.87 1.115 .163 Total 280 3.24 1.178 .070

ANOVA

Mutual Fund helps in tax saving.

Sum of Squares df Mean Square F Sig.

Between Groups 13.681 3 4.560 3.372 .019 Within Groups 373.287 276 1.352

Total 386.968 279

63

Post-Hoc Test

Mutual Fund helps in tax saving. LSD

(I) Education (J) Education Mean Difference

(I-J) Std. Error Sig.

12th Std Graduation -.374 .236 .114

Post-graduation -.514* .243 .035

other .063 .269 .815 Graduation 12th Std .374 .236 .114

Post-graduation -.140 .165 .397

other .437* .202 .031 Post-graduation 12th Std .514* .243 .035

Graduation .140 .165 .397

other .577* .210 .006 other 12th Std -.063 .269 .815

Graduation -.437* .202 .031

Post-graduation -.577* .210 .006 *. The mean difference is significant at the 0.05 level.

INTERPRETATION:

The significant level is 0.019 which is less than 0.05 so the alternative hypothesis is accepted

and the null hypothesis is a rejected. Therefore we can say that there is a significant difference

between Education and MF as tax saving.

64

4.2.7

Ho= There is no relation between education and MF liquidity.

H1= There is relation between education and MF liquidity.

Descriptive

Mutual Fund provides better liquidity than other investment option.

N Mean Std. Deviation Std. Error

12th Std 31 3.39 1.202 .216 Graduation 113 3.19 1.202 .113 Post-graduation 89 3.10 1.108 .117 other 47 3.21 1.178 .172 Total 280 3.19 1.165 .070

ANOVA Mutual Fund provides better liquidity than other investment option.

Sum of Squares df Mean Square F Sig.

Between Groups 1.934 3 .645 .472 .702 Within Groups 377.034 276 1.366

Total 378.968 279

65

Post-Hoc Test

Mutual Fund provides better liquidity than other investment option. LSD

(I) Education (J) Education Mean Difference

(I-J) Std. Error Sig.

12th Std Graduation .192 .237 .418

Post-graduation .286 .244 .242

other .174 .270 .520 Graduation 12th Std -.192 .237 .418

Post-graduation .094 .166 .573

other -.018 .203 .929 Post-graduation 12th Std -.286 .244 .242

Graduation -.094 .166 .573

other -.112 .211 .597 Other 12th Std -.174 .270 .520

Graduation .018 .203 .929

Post-graduation .112 .211 .597

INTERPRETATION:

The significant level is 0.702 which is greater than 0.05 so the alternative hypothesis is rejected

and the null hypothesis is accepted. Therefore we can say that there is a significant difference

between Education and MF liquidity.

66

4.2.8

Ho= There is no relation between education and MF in diversification of portfolio.

H1= There is relation between education and MF in diversification of portfolio.

Descriptive Mutual fund provides the diversification of portfolio.

N Mean Std. Deviation Std. Error

12th Std 31 3.52 1.092 .196 Graduation 113 3.62 1.046 .098 Post-graduation 89 3.28 1.187 .126 other 47 3.77 1.026 .150 Total 280 3.52 1.104 .066

ANOVA Mutual fund provides the diversification of portfolio.

Sum of Squares df Mean Square F Sig.

Between Groups 9.043 3 3.014 2.515 .045 Within Groups 330.782 276 1.198

Total 339.825 279

67

Post-Hoc Test Mutual fund provides the diversification of portfolio. LSD

(I) Education (J) Education

Mean Difference (I-

J) Std. Error Sig.

12th Std Graduation -.103 .222 .642

Post-graduation .235 .228 .304

other -.250 .253 .325 Graduation 12th Std .103 .222 .642

Post-graduation .339* .155 .030

other -.146 .190 .441 Post-graduation 12th Std -.235 .228 .304

Graduation -.339* .155 .030

other -.485* .197 .015 other 12th Std .250 .253 .325

Graduation .146 .190 .441

Post-graduation .485* .197 .015 *. The mean difference is significant at the 0.05 level.

INTERPRETATION:

The significant level is 0.045 which is less than 0.05 so the alternative hypothesis is accepted

and the null hypothesis isrejected. Therefore we can say that there no significant difference

between Education and MF in diversification of portfolio.

68

4.2.9

Ho= There is no relation between education and taking information in future.

H1= There is relation between education and taking information in future.

Descriptive

I am always interested in taking more information about mutual fund investment in future.

N Mean Std. Deviation Std. Error

12th Std 31 3.48 1.122 .201 Graduation 113 3.23 1.180 .111 Post-graduation 89 3.06 1.101 .117 Other 47 3.38 1.171 .171 Total 280 3.23 1.151 .069

ANOVA

I am always interested in taking more information about mutual fund investment in future. Sum of Squares df Mean Square F Sig.

Between Groups 5.786 3 1.929 1.464 .225 Within Groups 363.585 276 1.317

Total 369.371 279

69

Post-Hoc Test

I am always interested in taking more information about mutual fund investment in future.

(I) Education (J) Education

Mean Difference (I-

J) Std. Error Sig.

12th Std Graduation .254 .233 .276

Post-graduation .428 .239 .075

Other .101 .266 .704

Graduation 12th Std -.254 .233 .276 Post-graduation .174 .163 .286

Other -.153 .199 .443

Post-graduation 12th Std -.428 .239 .075 Graduation -.174 .163 .286

Other -.327 .207 .115

other 12th Std -.101 .266 .704 Graduation .153 .199 .443

Post-graduation .327 .207 .115

INTERPRETATION:

The significant level is 0.225 which is greater than 0.05 so the alternative hypothesis is rejected

and the null hypothesis is accepted. Therefore we can say that there is a significant difference

between Education and taking information of mutual fund in future.

70

4.3 OCCUPATION

4.3.1

Ho: There is no significant difference between occupation and awareness of mutual fund.

H1: There is significant difference between occupation and awareness of mutual fund.

Descriptive

I am aware of the Mutual Fund Investment.

N Mean Std. Deviation Std. Error

businessmen/women 56 3.00 1.236 .165 student 36 3.06 1.094 .182 part time employees 33 2.79 1.193 .208 full time employees 75 3.45 1.017 .117 professional 50 3.26 1.209 .171 other 30 3.30 1.208 .221 Total 280 3.18 1.160 .069

ANOVA

I am aware of the Mutual Fund Investment.

Sum of Squares df Mean Square F Sig.

Between Groups 13.800 5 2.760 2.090 .067 Within Groups 361.911 274 1.321

Total 375.711 279

71

Post-Hoc Test I am aware of the Mutual Fund Investment. LSD

(I) occupation (J) occupation Mean Difference

(I-J) Std. Error Sig.

businessmen/women student -.056 .246 .821

part time employees .212 .252 .401

full time employees -.453* .203 .026

professional -.260 .224 .246

other -.300 .260 .250

student businessmen/women .056 .246 .821 part time employees .268 .277 .335

full time employees -.398 .233 .089

professional -.204 .251 .416 other -.244 .284 .390

part time employees businessmen/women -.212 .252 .401

student -.268 .277 .335 full time employees -.665* .240 .006

professional -.472 .258 .068

other -.512 .290 .078 full time employees businessmen/women .453* .203 .026

student .398 .233 .089

part time employees .665* .240 .006 professional .193 .210 .358

other .153 .248 .537

professional businessmen/women .260 .224 .246 student .204 .251 .416

part time employees .472 .258 .068

full time employees -.193 .210 .358 other -.040 .265 .880

other businessmen/women .300 .260 .250

student .244 .284 .390 part time employees .512 .290 .078

full time employees -.153 .248 .537

professional .040 .265 .880 *. The mean difference is significant at the 0.05 level.

72

INTERPRETATION:

The significant level is 0.067 which is greater than 0.05 so the alternative hypothesis is rejected

and the null hypothesis is accepted. Therefore we can say that there is a significant difference

between occupation and awareness of mutual fund.

73

4.3.2

Ho: There is no significant difference between occupation and mutual fund safety.

H1: There is significant difference between occupation and mutual fund safety.

Descriptive Mutual Fund is safe

N Mean Std. Deviation Std. Error

businessmen/women 56 3.68 1.097 .147 student 36 3.53 1.207 .201 part time employees 33 3.64 .994 .173 full time employees 75 3.85 .926 .107 professional 50 3.64 1.005 .142 other 30 3.70 1.055 .193 Total 280 3.70 1.032 .062

ANOVA Mutual Fund is safe

Sum of Squares df Mean Square F Sig.

Between Groups 3.167 5 .633 .590 .707 Within Groups 294.030 274 1.073

Total 297.196 279

74

Post-Hoc Test

Mutual Fund is safe LSD

(I) occupation (J) occupation Mean Difference

(I-J) Std. Error Sig.

businessmen/women student .151 .221 .496

part time employees .042 .227 .853

full time employees -.175 .183 .340

professional .039 .202 .848

other -.021 .234 .927 student businessmen/women -.151 .221 .496

part time employees -.109 .250 .664

full time employees -.326 .210 .122 professional -.112 .226 .621

other -.172 .256 .502

part time employees businessmen/women -.042 .227 .853 student .109 .250 .664

full time employees -.217 .216 .317

professional -.004 .232 .988 other -.064 .261 .808

full time employees businessmen/women .175 .183 .340

student .326 .210 .122 part time employees .217 .216 .317

professional .213 .189 .260

other .153 .224 .494 professional businessmen/women -.039 .202 .848

student .112 .226 .621

part time employees .004 .232 .988 full time employees -.213 .189 .260

other -.060 .239 .802

other businessmen/women .021 .234 .927 student .172 .256 .502