Embed Size (px)

Citation preview

Award of 3.4 GHz andAward of 3.4 GHz and10 GHz Licences10 GHz Licences

Fixed Wireless Access Consultative Committee25th October 2000

Steve JonesRadiocommunications Agency

Introduction

James KinsleyWS Atkins

Management Consultants

Overview

Today…….Today…….Today…….Today…….

Overview of Progress to Date…. Markets/Revenue Technical/Costs Financial/Valuation Economic

Overview of Progress to Date…. Markets/Revenue Technical/Costs Financial/Valuation Economic

2

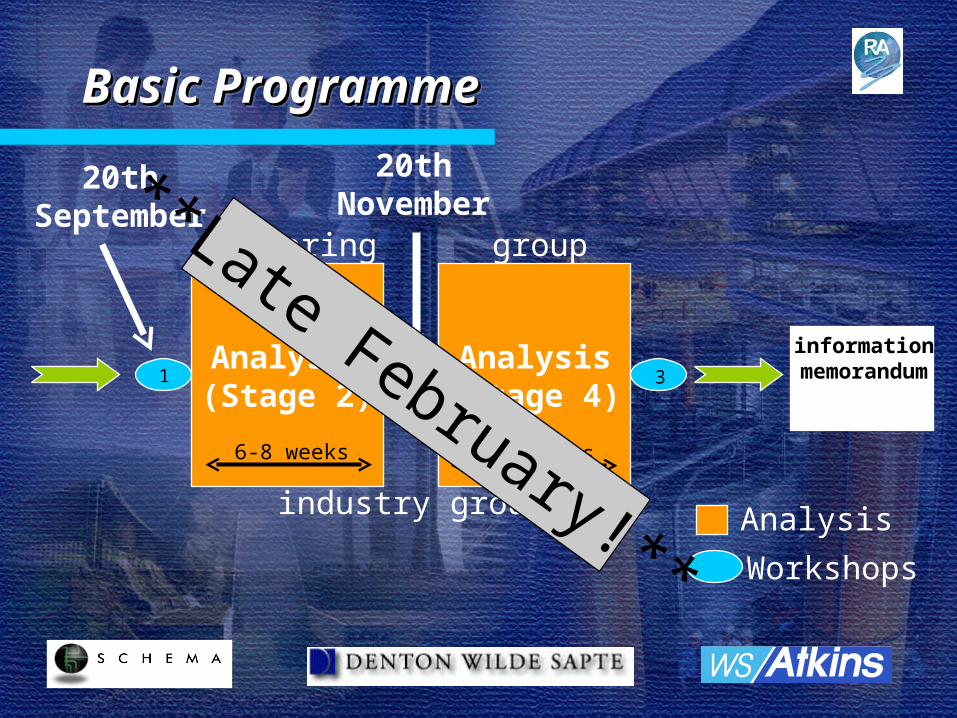

20thNovember

Basic ProgrammeBasic ProgrammeBasic ProgrammeBasic Programme

Analysis(Stage 2)

Analysis(Stage 4)

Workshops

informationmemorandum

20thSeptember

steering group

industry group

6-8 weeks 4-6 weeks

**Late February!**

1 3

Analysis

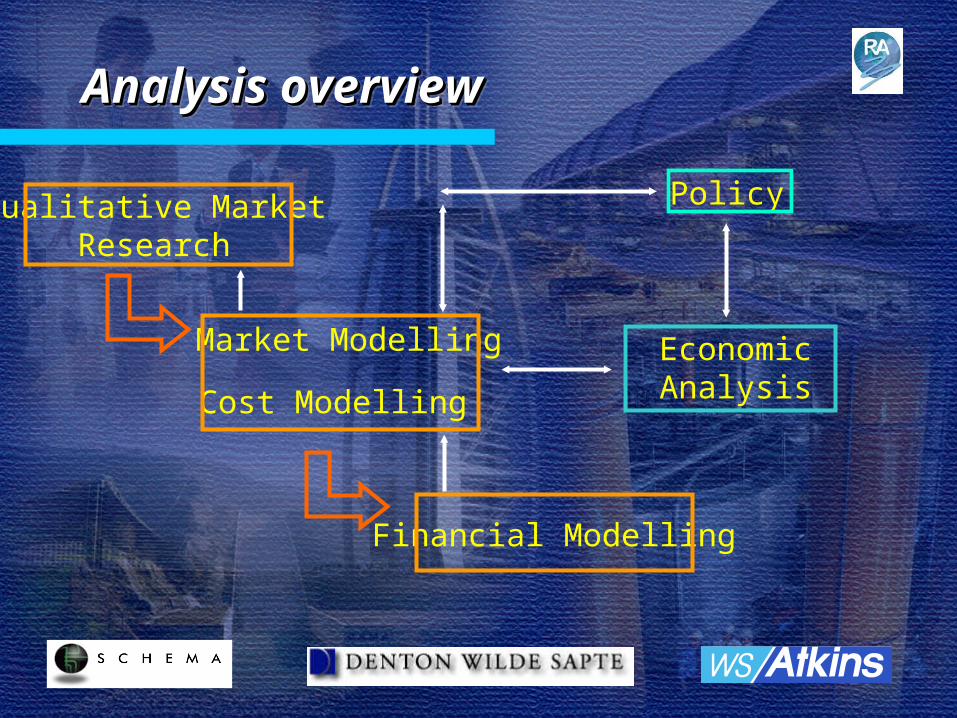

Analysis overviewAnalysis overviewAnalysis overviewAnalysis overview

Qualitative MarketResearch

Cost Modelling

Market Modelling

Financial Modelling

EconomicAnalysis

Policy

Bérangère Mira-SmithWS Atkins

Management Consultants

Qualitative Market Research

Purpose of the QMRPurpose of the QMRPurpose of the QMRPurpose of the QMR

Consult with industry to:– Gather market intelligence– Test the assumptions made by the team– Inform the modelling exercise

Consult with industry to:– Gather market intelligence– Test the assumptions made by the team– Inform the modelling exercise

Progress to dateProgress to dateProgress to dateProgress to date

Contacted 30 companies 13 companies have been interviewed so

far, including:– Operators

BT, Firstmark, NTL, Atlantic, Tele2, Energis, FORMUS.

– Consultants

Albera Networks– Manufacturers

Lucent, Ericsson, Airspan, Harris Microwave, European Antennas

Contacted 30 companies 13 companies have been interviewed so

far, including:– Operators

BT, Firstmark, NTL, Atlantic, Tele2, Energis, FORMUS.

– Consultants

Albera Networks– Manufacturers

Lucent, Ericsson, Airspan, Harris Microwave, European Antennas

Looking forwardLooking forwardLooking forwardLooking forward

We are planning to carry out further interviews in Stage 2

Interview players in the banking world

We are planning to carry out further interviews in Stage 2

Interview players in the banking world

Industry Views:Industry Views:Services and target market Services and target market Industry Views:Industry Views:Services and target market Services and target market

Operators are planning to provide:– Always On link to the Internet– Voice telephony

Market share expectations 10-15% The principal target markets are:

– SMEs– SOHOs– Residential market

Operators are planning to provide:– Always On link to the Internet– Voice telephony

Market share expectations 10-15% The principal target markets are:

– SMEs– SOHOs– Residential market

Industry Views:Industry Views:Overview of Access TechnologiesOverview of Access TechnologiesIndustry Views:Industry Views:Overview of Access TechnologiesOverview of Access Technologies

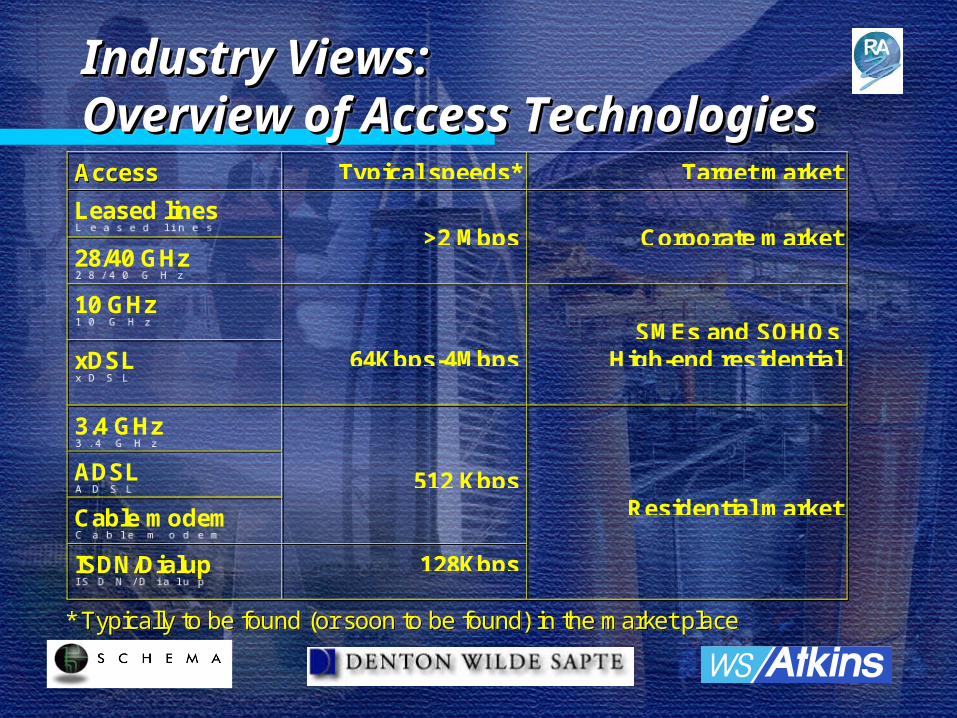

Access Typical speeds* Target market

Leased lines

28/40 GHz>2 Mbps Corporate market

10 GHz

xDSL 64Kbps-4MbpsSMEs and SOHOs

High-end residential

3.4 GHz

ADSL

Cable modem

512 Kbps

ISDN/Dialup 128Kbps

Residential market

* Typically to be found (or soon to be found) in the market place

Access Typical speeds* Target market

Leased lines

28/40 GHz>2 Mbps Corporate market

10 GHz

xDSL 64Kbps-4MbpsSMEs and SOHOs

High-end residential

3.4 GHz

ADSL

Cable modem

512 Kbps

ISDN/Dialup 128Kbps

Residential market

* Typically to be found (or soon to be found) in the market place

Industry Views:Industry Views:Location of target marketLocation of target marketIndustry Views:Industry Views:Location of target marketLocation of target market

Prime location is suburban areas of cities, towns and business parks:– strong competition in city centres (fibre,

copper and in July 2001 ULL) – need to target densely populated areas to

achieve base station “fill factor” and adequate return

No business case to roll out in rural areas

Prime location is suburban areas of cities, towns and business parks:– strong competition in city centres (fibre,

copper and in July 2001 ULL) – need to target densely populated areas to

achieve base station “fill factor” and adequate return

No business case to roll out in rural areas

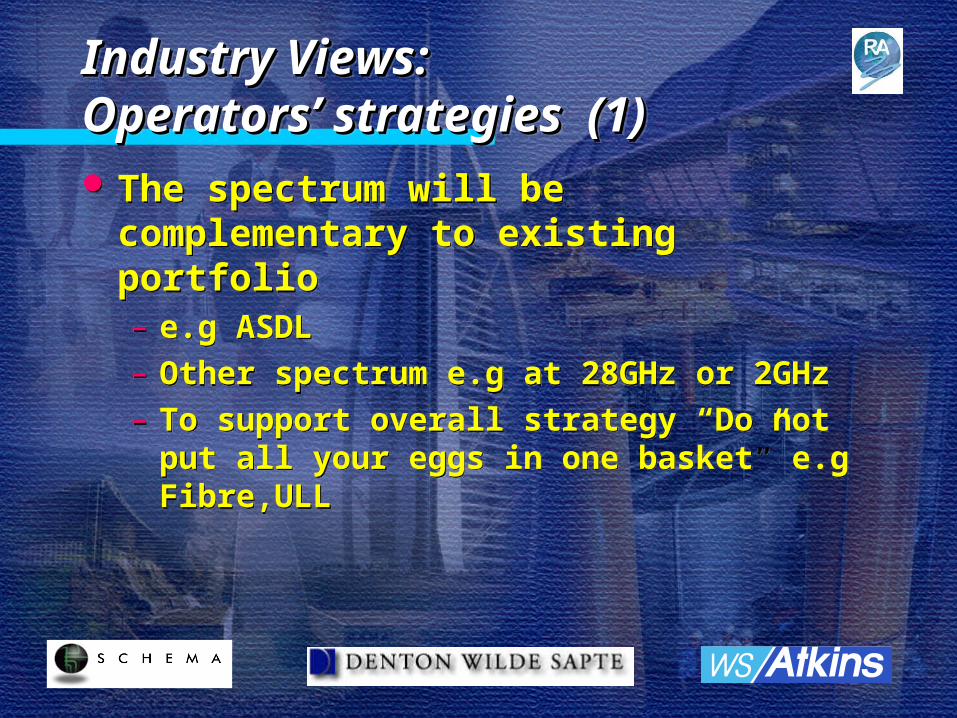

Industry Views:Industry Views:Operators’ strategies (1)Operators’ strategies (1)Industry Views:Industry Views:Operators’ strategies (1)Operators’ strategies (1) The spectrum will be complementary to

existing portfolio– e.g ASDL– Other spectrum e.g at 28GHz or 2GHz– To support overall strategy “Do not put all

your eggs in one basket” e.g Fibre,ULL

The spectrum will be complementary to existing portfolio– e.g ASDL– Other spectrum e.g at 28GHz or 2GHz– To support overall strategy “Do not put all

your eggs in one basket” e.g Fibre,ULL

Industry Views:Industry Views:Operators’ strategies (2)Operators’ strategies (2)Industry Views:Industry Views:Operators’ strategies (2)Operators’ strategies (2)

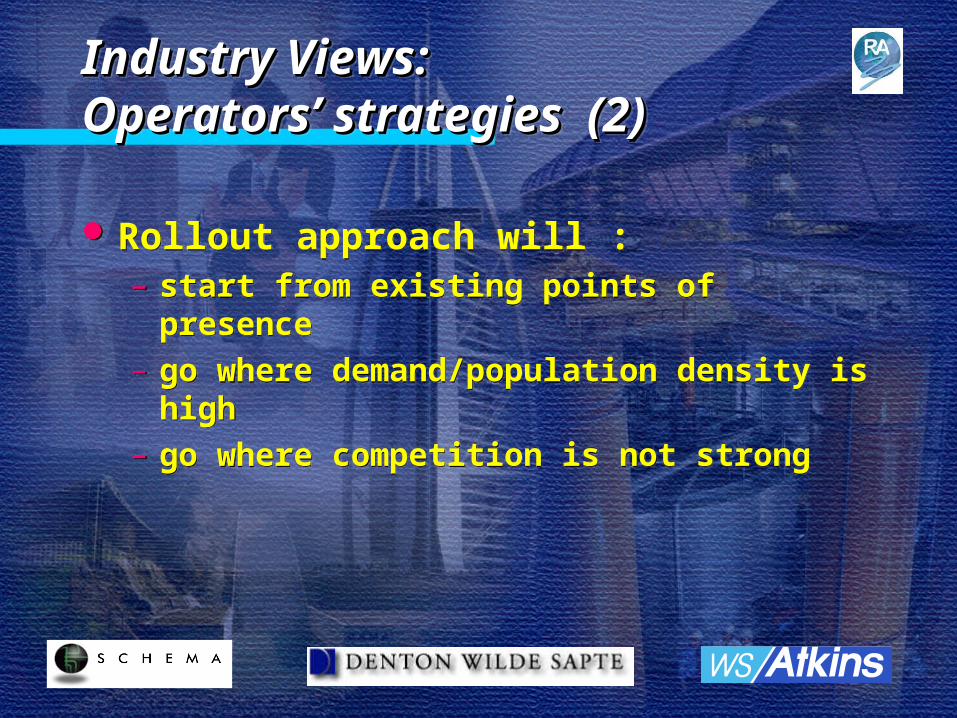

Rollout approach will :– start from existing points of presence– go where demand/population density is high– go where competition is not strong

Rollout approach will :– start from existing points of presence– go where demand/population density is high– go where competition is not strong

Industry View:Industry View:Regulatory & licensing matters (1)Regulatory & licensing matters (1)Industry View:Industry View:Regulatory & licensing matters (1)Regulatory & licensing matters (1)

Most operators would prefer a national licence

Regional licences would be wasteful The amount of spectrum can only really

support one licence holder Licence duration needs to be 15-20 years

Most operators would prefer a national licence

Regional licences would be wasteful The amount of spectrum can only really

support one licence holder Licence duration needs to be 15-20 years

Industry View:Industry View:Regulatory & licensing matters (2)Regulatory & licensing matters (2)Industry View:Industry View:Regulatory & licensing matters (2)Regulatory & licensing matters (2)

Some licence clauses would be acceptable, e.g.:– “Use It or Lose It” – Rollout clauses with deadlines & penalties– No backhaul on band

Service clauses would make the licence unattractive

Some licence clauses would be acceptable, e.g.:– “Use It or Lose It” – Rollout clauses with deadlines & penalties– No backhaul on band

Service clauses would make the licence unattractive

Industry Views:Industry Views:Auction vs Comp. SelectionAuction vs Comp. SelectionIndustry Views:Industry Views:Auction vs Comp. SelectionAuction vs Comp. Selection

Comparative selection is the preferred award mechanism– auctions are clear cut, but take money out of

the industry– comparative selection has the means to

ensure that the licence will be used

Comparative selection is the preferred award mechanism– auctions are clear cut, but take money out of

the industry– comparative selection has the means to

ensure that the licence will be used

Nick BladesSchema

Market Modelling

Market & Revenue ModelMarket & Revenue ModelMarket & Revenue ModelMarket & Revenue Model

Objectives– addressable market sizing based on three

geographic areas• cities : nine UK cities modelled as one whole

• regional : remaining UK

• coverage assumptions consistent with cost model

– revenues generated• telephony, Internet access & value added

• strategies : new venture vs existing operator

Objectives– addressable market sizing based on three

geographic areas• cities : nine UK cities modelled as one whole

• regional : remaining UK

• coverage assumptions consistent with cost model

– revenues generated• telephony, Internet access & value added

• strategies : new venture vs existing operator

ScenariosScenariosScenariosScenarios

Cities– 9 demographic profiles

– cities have cost structures which differ from those in regions

– level of competition in access is markedly different to that in regions

Cities– 9 demographic profiles

– cities have cost structures which differ from those in regions

– level of competition in access is markedly different to that in regions

Regions– n x demographic profile

• modelled as one for Stage 2

– lower subscriber density

– lower competition in access

– significant backhaul costs

Regions– n x demographic profile

• modelled as one for Stage 2

– lower subscriber density

– lower competition in access

– significant backhaul costs

Geo-demographicsGeo-demographicsGeo-demographicsGeo-demographics

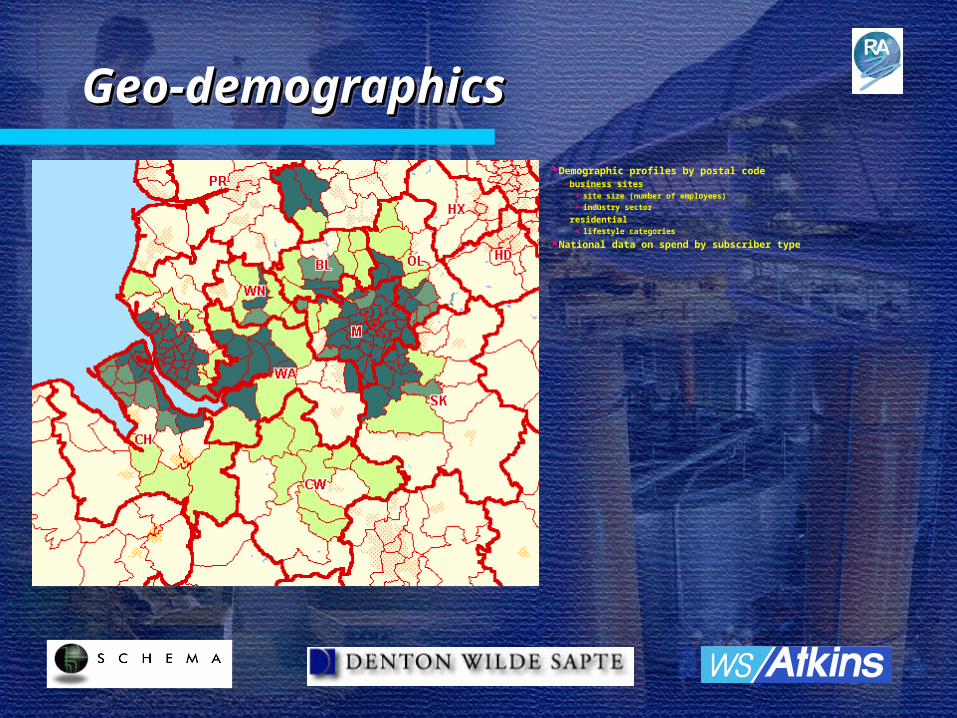

Demographic profiles by postal code– business sites

• site size (number of employees)

• industry sector

– residential

• lifestyle categories

National data on spend by subscriber type

Model OutputsModel OutputsModel OutputsModel Outputs

Series of revenue forecasts– city, regional, whole UK licence

Consistent assumptions with cost model Opex

– interconnect, other CoGS (e.g. CPE & installation)– marketing, SG&A costs

Subscriber forecast for input into cost model

Series of revenue forecasts– city, regional, whole UK licence

Consistent assumptions with cost model Opex

– interconnect, other CoGS (e.g. CPE & installation)– marketing, SG&A costs

Subscriber forecast for input into cost model

Market for Broadband ServicesMarket for Broadband ServicesMarket for Broadband ServicesMarket for Broadband Services

Schema forecasts a supply shortfall of 3 million by 2010

FWA model predicts a reduction in this shortfall

Schema forecasts a supply shortfall of 3 million by 2010

FWA model predicts a reduction in this shortfall

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Subscribers

Demand

Supply

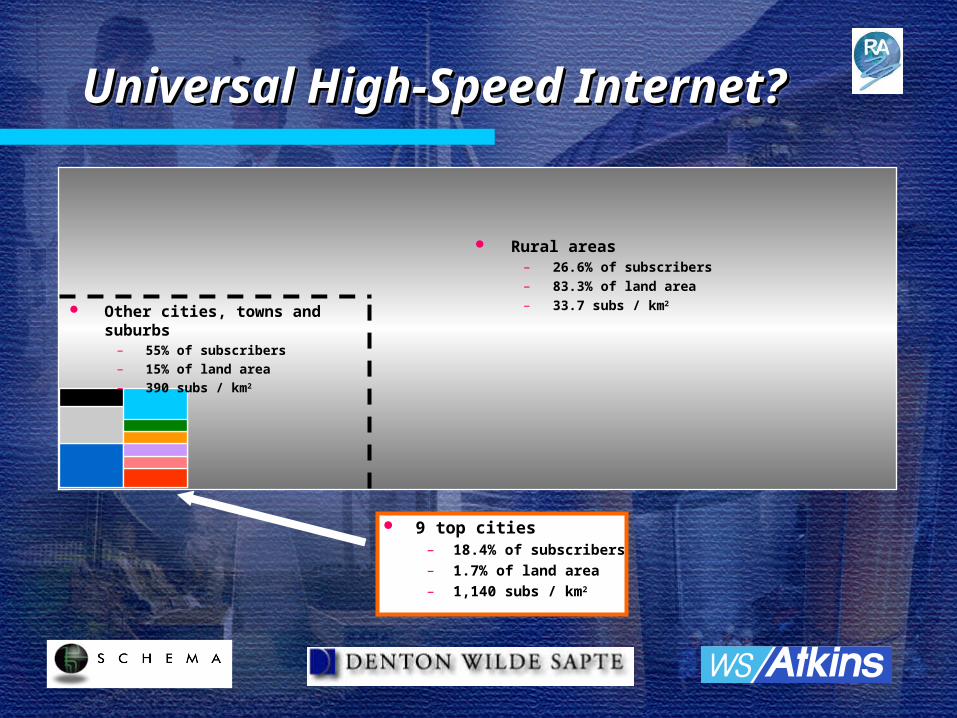

Universal High-Speed Internet?Universal High-Speed Internet?Universal High-Speed Internet?Universal High-Speed Internet?

9 top cities– 18.4% of subscribers

– 1.7% of land area

– 1,140 subs / km2

Other cities, towns and suburbs– 55% of subscribers– 15% of land area– 390 subs / km2

Rural areas– 26.6% of subscribers– 83.3% of land area– 33.7 subs / km2

Next StepsNext StepsNext StepsNext Steps

In Stage 4– evaluate cities individually– generate revenues by regions if required– test sensitivities

• in concert with cost model– rollout plans– market share assumptions– price competition

• impact on subscribers, revenues & profits– feed into socio-economic benefit analysis

In Stage 4– evaluate cities individually– generate revenues by regions if required– test sensitivities

• in concert with cost model– rollout plans– market share assumptions– price competition

• impact on subscribers, revenues & profits– feed into socio-economic benefit analysis

Abdul LadakWS Atkins Telecommunications

Infrastructure RolloutCost Model

ProgressProgressProgressProgress

Technical ReviewConsultations with IndustryCost Model - First PassCoverage and PropagationSpectrum and CapacityImplementation

Technical ReviewConsultations with IndustryCost Model - First PassCoverage and PropagationSpectrum and CapacityImplementation

Cost Model StructureCost Model StructureCost Model StructureCost Model Structure

Cost Model

NationalCityRegionalBuild InfrastructureLease InfrastructureBackhaul Options

Scenarios

EnterpriseSOHOResidential

Markets

ServicesData RatesQoSAvailability

Demands

AllocationRe-useCondition

Spectrum

ModulationMutiplexingStandards

Technologies

HardwareSitesInstallat ionCommissioning

System

Optical FibreTransportSwitchingBuildLeaseInterconnect

Infrastructure

CoverageCo-ordinationCo-locat ionInterferenceCapacityTraff icBER and QoS

Planning & Design

LicencingService LevelsNetwork ManagementPerformanceBillingSecurity & Disaster

Operations

INFLUENCINGFACTORS

COSTS

OUTPUTS

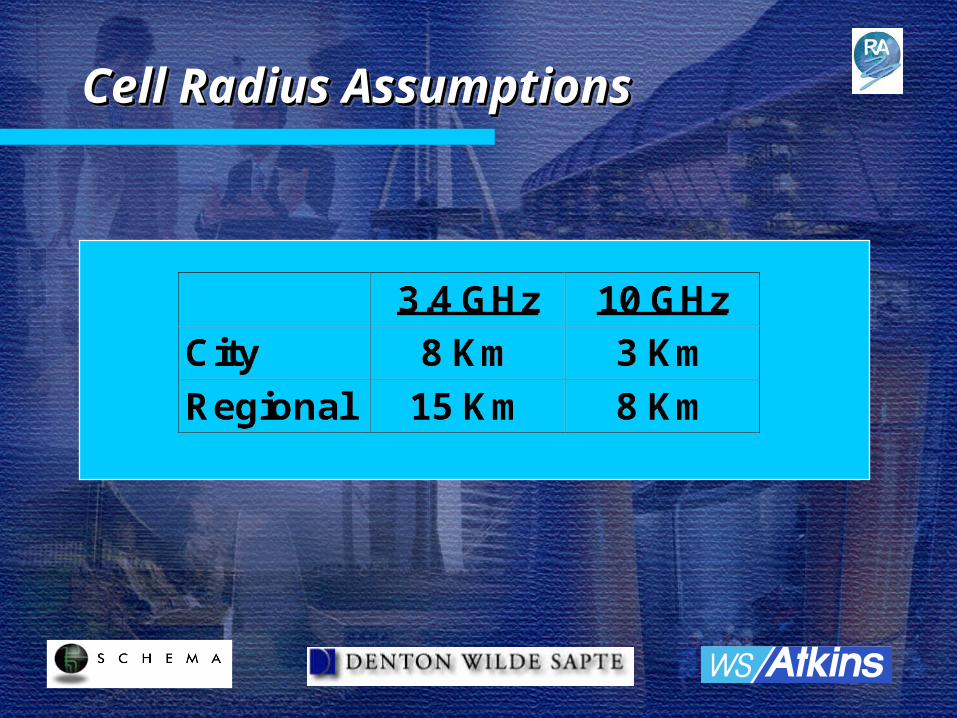

Cell Radius AssumptionsCell Radius AssumptionsCell Radius AssumptionsCell Radius Assumptions

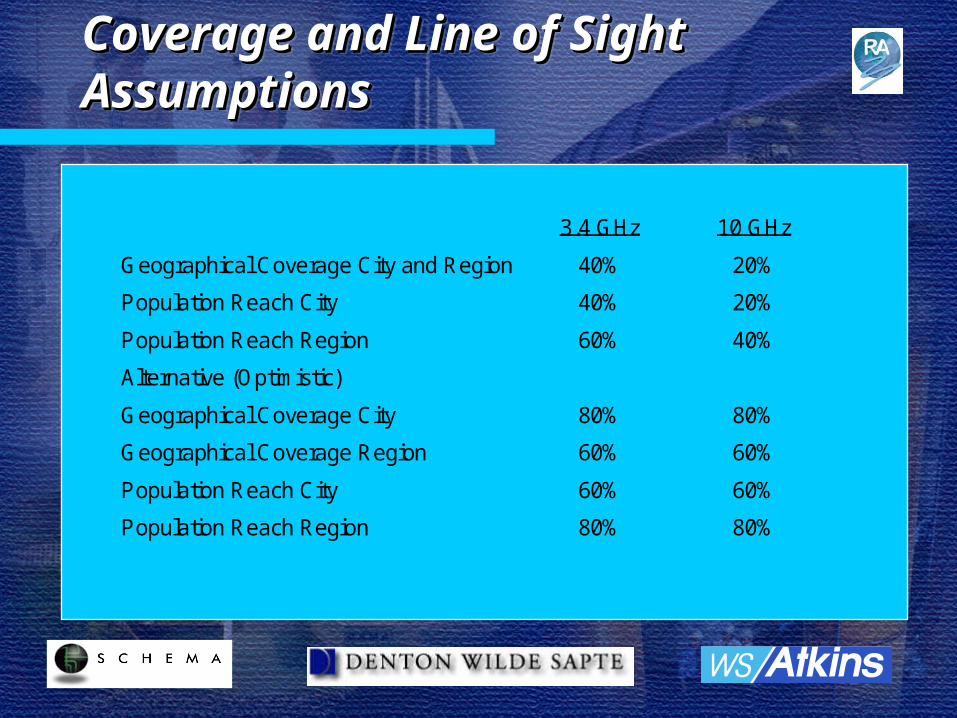

Coverage and Line of Sight Coverage and Line of Sight AssumptionsAssumptionsCoverage and Line of Sight Coverage and Line of Sight AssumptionsAssumptions

3.4 GHz 10 GHz

Geographical Coverage City and Region 40% 20%

Population Reach City 40% 20%

Population Reach Region 60% 40%

Alternative (Optimistic)

Geographical Coverage City 80% 80%

Geographical Coverage Region 60% 60%

Population Reach City 60% 60%

Population Reach Region 80% 80%

Propagation IndicationsPropagation IndicationsPropagation IndicationsPropagation Indications

Extensive engineering Even more so at 10 GHz Propagation modelling essential Selective subscriber targeting

Extensive engineering Even more so at 10 GHz Propagation modelling essential Selective subscriber targeting

Spectrum 3.4 GHzSpectrum 3.4 GHzSpectrum 3.4 GHzSpectrum 3.4 GHz

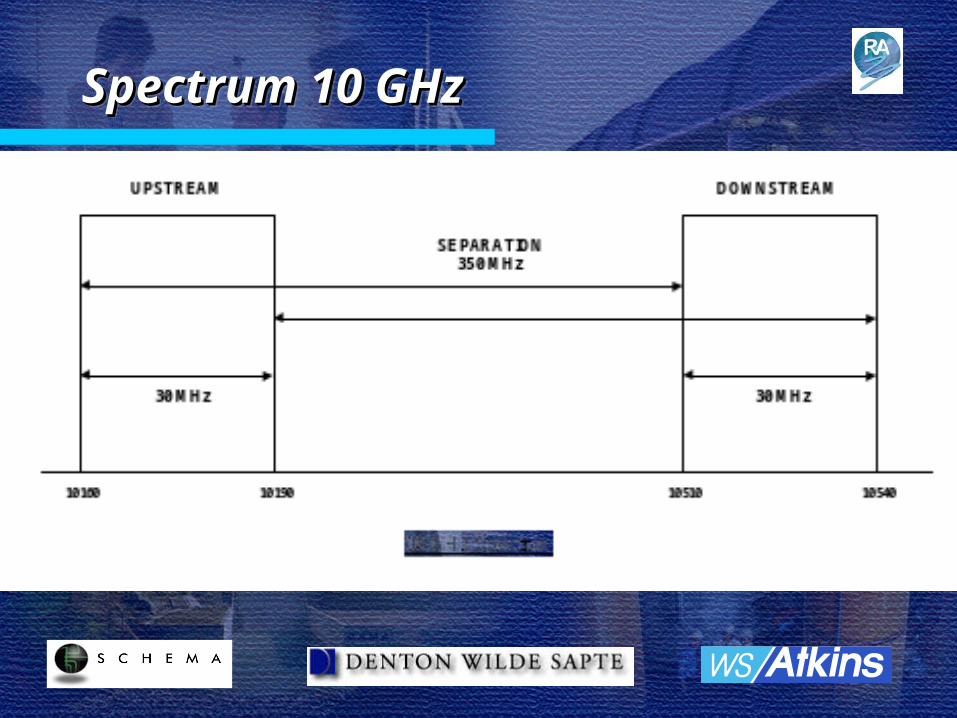

Spectrum 10 GHzSpectrum 10 GHzSpectrum 10 GHzSpectrum 10 GHz

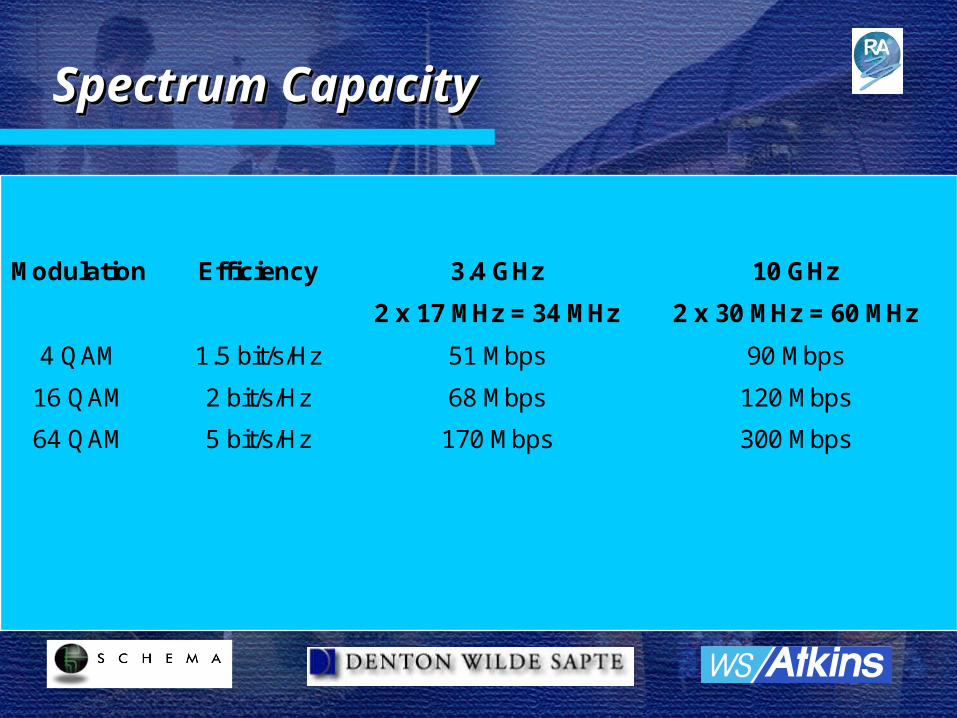

Spectrum CapacitySpectrum CapacitySpectrum CapacitySpectrum Capacity

Modulation Efficiency 3.4 GHz

2 x 17 MHz = 34 MHz

10 GHz

2 x 30 MHz = 60 MHz

4 QAM 1.5 bit/s/Hz 51 Mbps 90 Mbps

16 QAM 2 bit/s/Hz 68 Mbps 120 Mbps

64 QAM 5 bit/s/Hz 170 Mbps 300 Mbps

Cell Structure and Spectrum Cell Structure and Spectrum ReuseReuseCell Structure and Spectrum Cell Structure and Spectrum ReuseReuse

F2

F1

F1

F2 F2

F1

F1

F2

F2

F1

F1

F2 F2

F1

F1

F2

F3

F1

F1

F3 F2

F4

F4

F2

F1

F3

F3

F1 F4

F2

F2

F4

Whole spectrum used in each cellFrequency Reuse = 100%

Half spectrum used in each cellFrequency Reuse = 50 %

F1 = f1, f5 - 1.75 MHz each (up and down)A

BA

F2 = f4, f8 - 1.75 MHz each (up and down)

F1 = f1, f3, f5, f7 - 1.75 MHz each (up and down)B

F2 = f2, f4, f6, f8 - 1.75 MHz each (up and down)

F3 = f3, f7 - 1.75 MHz each (up and down)

Controlled and Co-ordinated by: Tx Power, Back to Front Ratio, Antenna Downtilt

F3 = f2, f6 - 1.75 MHz each (up and down)

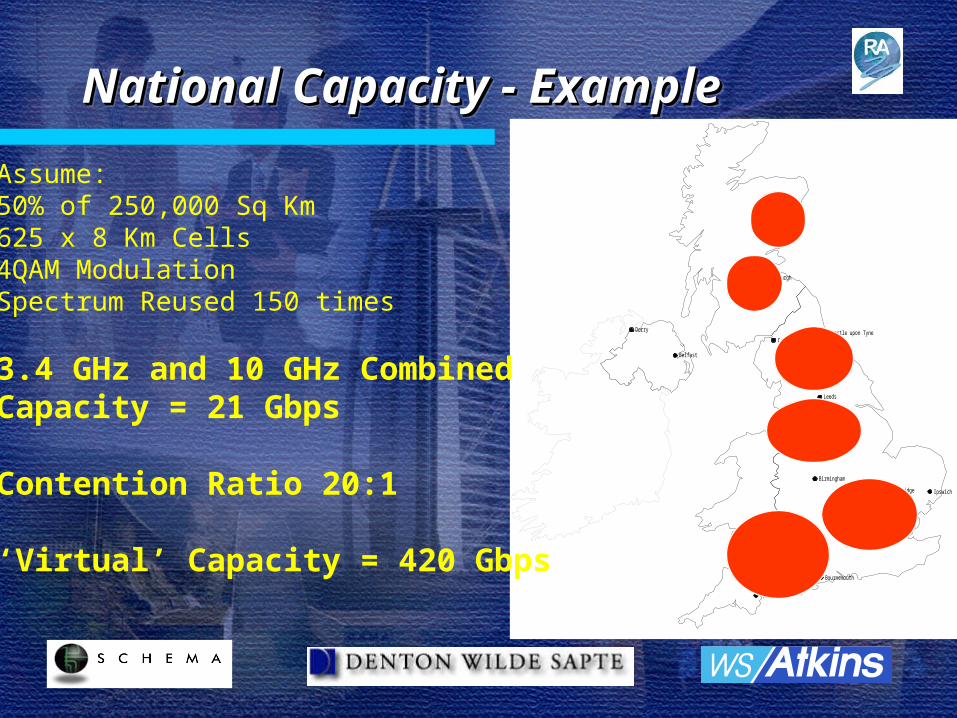

National Capacity - ExampleNational Capacity - ExampleNational Capacity - ExampleNational Capacity - Example

London

Cambridge

Derry

Belfast

Edinburgh

Cardiff

Liverpool

Manchester

Birmingham

Glasgow

Swansea

Newcastle upon Tyne

Oxford

Aberdeen

Carlisle

Bournemouth

Torbay

Leeds

Sheffield

Ipswich

Assume:50% of 250,000 Sq Km625 x 8 Km Cells4QAM ModulationSpectrum Reused 150 times

3.4 GHz and 10 GHz CombinedCapacity = 21 Gbps

Contention Ratio 20:1

‘Virtual’ Capacity = 420 Gbps

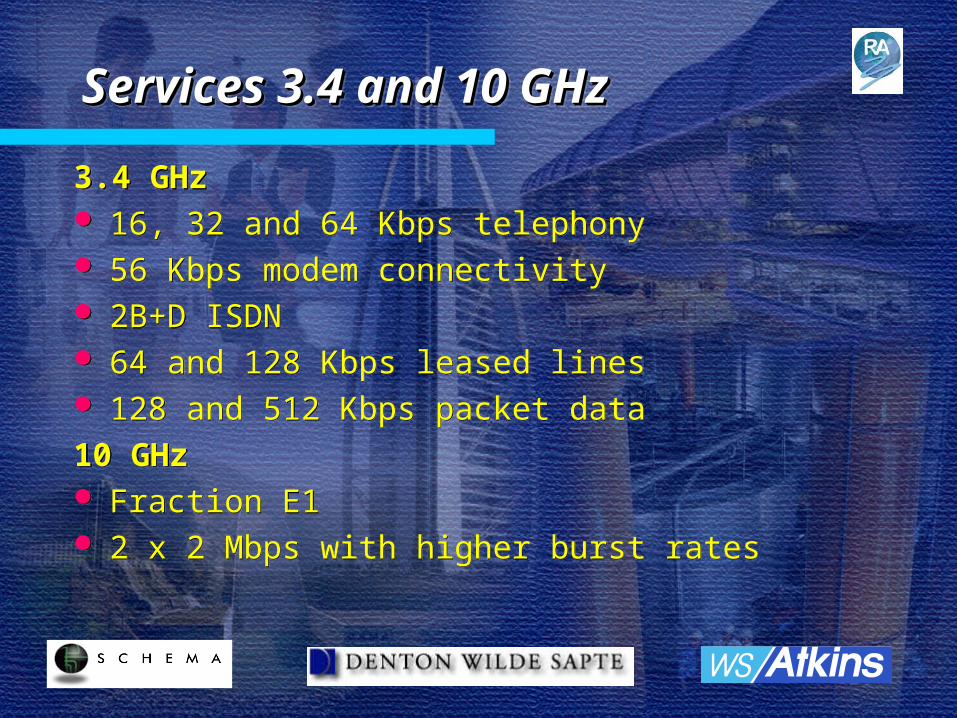

Services 3.4 and 10 GHzServices 3.4 and 10 GHzServices 3.4 and 10 GHzServices 3.4 and 10 GHz

3.4 GHz 16, 32 and 64 Kbps telephony 56 Kbps modem connectivity 2B+D ISDN 64 and 128 Kbps leased lines 128 and 512 Kbps packet data

10 GHz Fraction E1 2 x 2 Mbps with higher burst rates

3.4 GHz 16, 32 and 64 Kbps telephony 56 Kbps modem connectivity 2B+D ISDN 64 and 128 Kbps leased lines 128 and 512 Kbps packet data

10 GHz Fraction E1 2 x 2 Mbps with higher burst rates

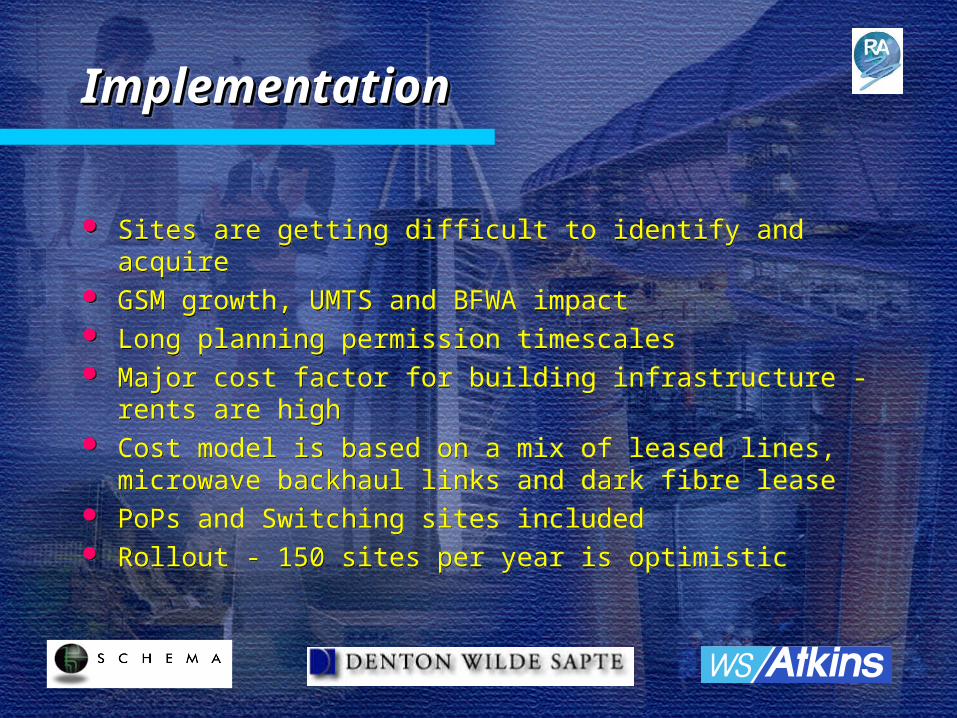

ImplementationImplementationImplementationImplementation

Sites are getting difficult to identify and acquire GSM growth, UMTS and BFWA impact Long planning permission timescales Major cost factor for building infrastructure - rents are high Cost model is based on a mix of leased lines, microwave

backhaul links and dark fibre lease PoPs and Switching sites included Rollout - 150 sites per year is optimistic

Sites are getting difficult to identify and acquire GSM growth, UMTS and BFWA impact Long planning permission timescales Major cost factor for building infrastructure - rents are high Cost model is based on a mix of leased lines, microwave

backhaul links and dark fibre lease PoPs and Switching sites included Rollout - 150 sites per year is optimistic

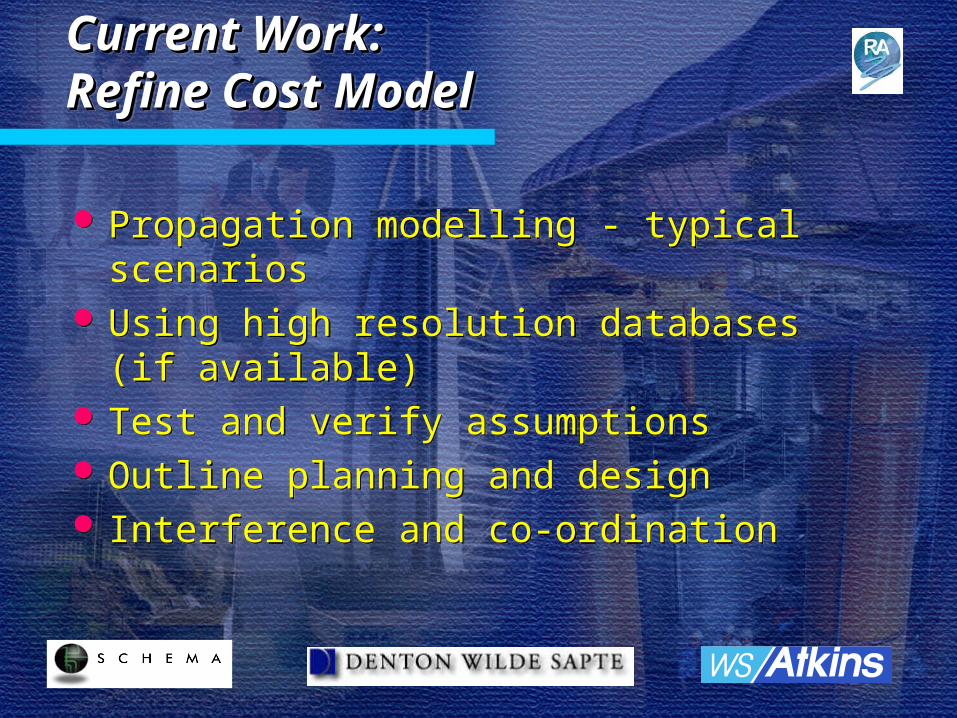

Current Work: Current Work: Refine Cost ModelRefine Cost ModelCurrent Work: Current Work: Refine Cost ModelRefine Cost Model

Propagation modelling - typical scenarios Using high resolution databases (if available) Test and verify assumptions Outline planning and design Interference and co-ordination

Propagation modelling - typical scenarios Using high resolution databases (if available) Test and verify assumptions Outline planning and design Interference and co-ordination

Saule ZhonkebayevaWS Atkins

Management Consultants

Financial Modelling

Purpose of the financial modelPurpose of the financial modelPurpose of the financial modelPurpose of the financial model

Examine under what conditions, operators of FWA licences will have a viable business (Stage 2)

Evaluate sensitivity of the return to investors to licence fee (Stage 2)

Assess the sensitivity of the return to investors to other factors such as tariffs, sales volumes, operating costs and capital costs (Stage 4)

Examine under what conditions, operators of FWA licences will have a viable business (Stage 2)

Evaluate sensitivity of the return to investors to licence fee (Stage 2)

Assess the sensitivity of the return to investors to other factors such as tariffs, sales volumes, operating costs and capital costs (Stage 4)

Financial ModellingFinancial ModellingFinancial ModellingFinancial Modelling

MARKET RESEARCH

Sales volume

Sales prices

Debtor days

Creditor days

TECHNICAL ANALYSIS

Stock days

Capital costs

Operating costs

FINANCING

Loan repayment term

Loan interest rates

Interest on cash balance

MARKET RESEARCH

Sales volume

Sales prices

Debtor days

Creditor days

TECHNICAL ANALYSIS

Stock days

Capital costs

Operating costs

FINANCING

Loan repayment term

Loan interest rates

Interest on cash balance

RevenuesRevenues

Working capitalWorking capital FORECAST FINANCIALSTATEMENTS

Profit & loss accountBalance sheetSources & application of fundsCash flow

FORECAST FINANCIALSTATEMENTS

Profit & loss accountBalance sheetSources & application of fundsCash flow

VALUATION MODELVALUATION MODEL

High Level Financial OutcomesHigh Level Financial OutcomesHigh Level Financial OutcomesHigh Level Financial Outcomes

ARPU : Average Revenue Per UserARPU : Average Revenue Per User

High ARPU* Med CPU* Profitable?

High ARPU* Med CPU* Profitable?

New VentureNew Venture

Existing operatorExisting operator

CityCity RegionalRegional NationalNational

CPU : Cost Per UserCPU : Cost Per User

High ARPU* Low CPU* Profitable?

High ARPU* Low CPU* Profitable?

Low ARPU* High CPU* Profitable?

Low ARPU* High CPU* Profitable?

Low ARPU* High CPU* Profitable?

Low ARPU* High CPU* Profitable?

Economies of scale

Profitable?

Economies of scale

Profitable?

Economies of scale

Profitable?

Economies of scale

Profitable?

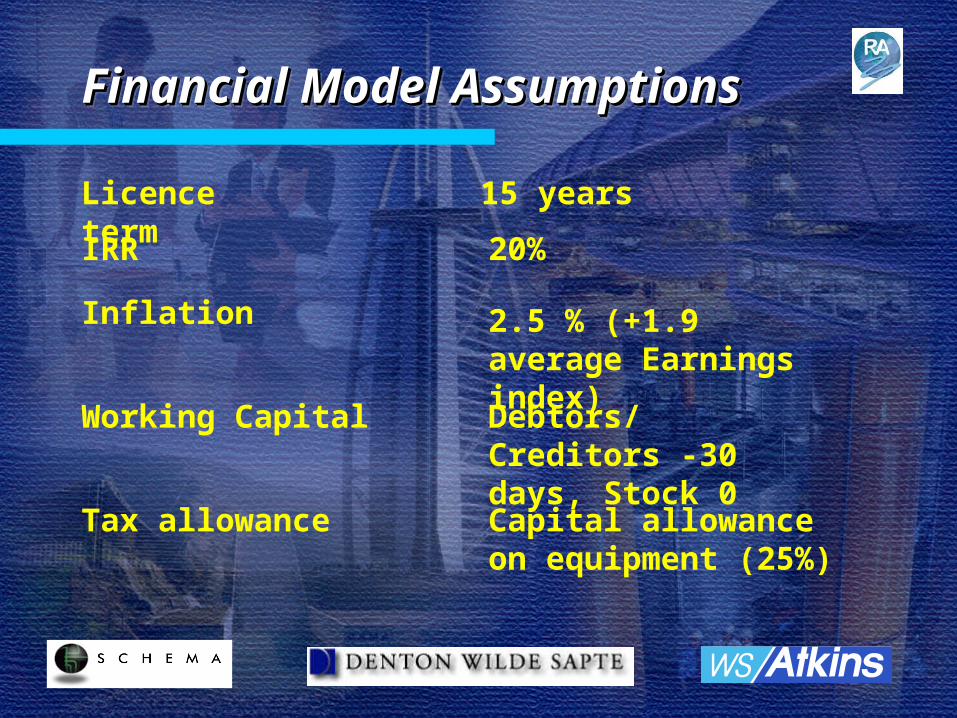

Financial Model AssumptionsFinancial Model AssumptionsFinancial Model AssumptionsFinancial Model Assumptions

Licence term 15 years

Inflation 2.5 % (+1.9 average Earnings index)

Working Capital Debtors/Creditors -30 days, Stock 0

Tax allowance Capital allowance on equipment (25%)

IRR 20%

Financial Model AssumptionsFinancial Model AssumptionsFinancial Model AssumptionsFinancial Model Assumptions

Financing D/E - 60/40IR - 9-10% (incl. banks' margin)Loan term - 10 years

No residual value assumed

Residual Value

Depreciation Straight line :Telecom equipment - 7 yearsIT equipment - 5 yearsFibre - 25 years

Professor Ian JewittBristol University

Economic Analysis

Economic AnalysisEconomic AnalysisEconomic AnalysisEconomic Analysis

Economic value rather than industry profit Industry profit a guide to economic value But an imperfect one

– Industry profit guides business plans– Industry profit guides bidding in e.g.

auctions

Important therefore to understand any divergence between profit and economic value

Economic value rather than industry profit Industry profit a guide to economic value But an imperfect one

– Industry profit guides business plans– Industry profit guides bidding in e.g.

auctions

Important therefore to understand any divergence between profit and economic value

Consumer and Producer SurplusConsumer and Producer SurplusConsumer and Producer SurplusConsumer and Producer Surplus

Q

P

c1

c2

q1 q2

The ObjectiveThe ObjectiveThe ObjectiveThe Objective

EV = CS + PS + a x R– a > 0 ?

Shadow price of funds– estimated in US at 0.3

EV = CS + PS + a x R– a > 0 ?

Shadow price of funds– estimated in US at 0.3

New entry into market with New entry into market with existing suppliersexisting suppliersNew entry into market with New entry into market with existing suppliersexisting suppliers

Consumer surplus on increase in market served

Producer surplus on increase in market served

Cost saving/extra expense on displaced market share

Consumer surplus on increase in market served

Producer surplus on increase in market served

Cost saving/extra expense on displaced market share

New entry into market with New entry into market with existing suppliers (2)existing suppliers (2)New entry into market with New entry into market with existing suppliers (2)existing suppliers (2)

Q

P

c1

c2

q1 q2

initial output level

Relationship Between Economic Relationship Between Economic Value and ProfitValue and ProfitRelationship Between Economic Relationship Between Economic Value and ProfitValue and Profit

EV not therefore generally equal to profitability

How related? …...depends on assumptions of the effect

of increased competition on the market

EV not therefore generally equal to profitability

How related? …...depends on assumptions of the effect

of increased competition on the market

Modelling AssumptionsModelling AssumptionsModelling AssumptionsModelling Assumptions

Demand Conditions– Usual assumptions: OFTEL, KPMG, ...– Linear demand– Constant Unit Costs

Strategic Model– Base model, Cournot competition

Demand Conditions– Usual assumptions: OFTEL, KPMG, ...– Linear demand– Constant Unit Costs

Strategic Model– Base model, Cournot competition

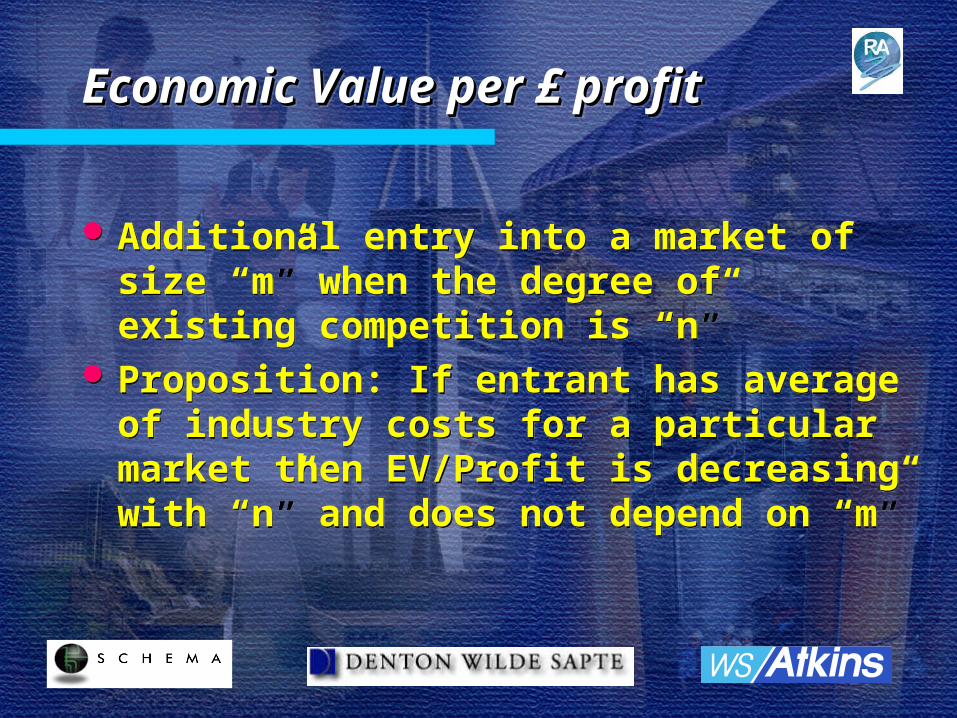

Economic Value per £ profitEconomic Value per £ profitEconomic Value per £ profitEconomic Value per £ profit

Additional entry into a market of size “m” when the degree of existing competition is “n”

Proposition: If entrant has average of industry costs for a particular market then EV/Profit is decreasing with “n” and does not depend on “m”

Additional entry into a market of size “m” when the degree of existing competition is “n”

Proposition: If entrant has average of industry costs for a particular market then EV/Profit is decreasing with “n” and does not depend on “m”

Social versus Private PreferencesSocial versus Private PreferencesSocial versus Private PreferencesSocial versus Private Preferences

Amount of Existing Competition

Size of Market

Private choice

social choice

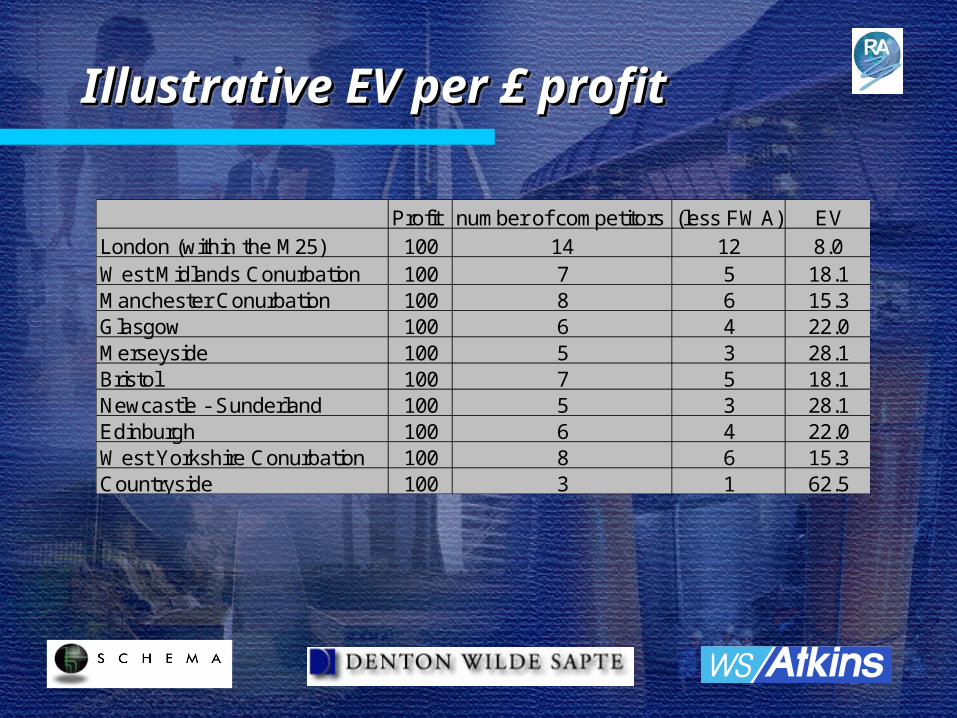

Illustrative EV per £ profitIllustrative EV per £ profitIllustrative EV per £ profitIllustrative EV per £ profit

Profit number of competitors (less FWA) EVLondon (within the M25) 100 14 12 8.0West Midlands Conurbation 100 7 5 18.1Manchester Conurbation 100 8 6 15.3Glasgow 100 6 4 22.0Merseyside 100 5 3 28.1Bristol 100 7 5 18.1Newcastle - Sunderland 100 5 3 28.1Edinburgh 100 6 4 22.0West Yorkshire Conurbation 100 8 6 15.3Countryside 100 3 1 62.5

ConsequencesConsequencesConsequencesConsequences

Roll out to areas less served by current competition a higher social priority than private one

Roll out to areas less served by current competition a higher social priority than private one

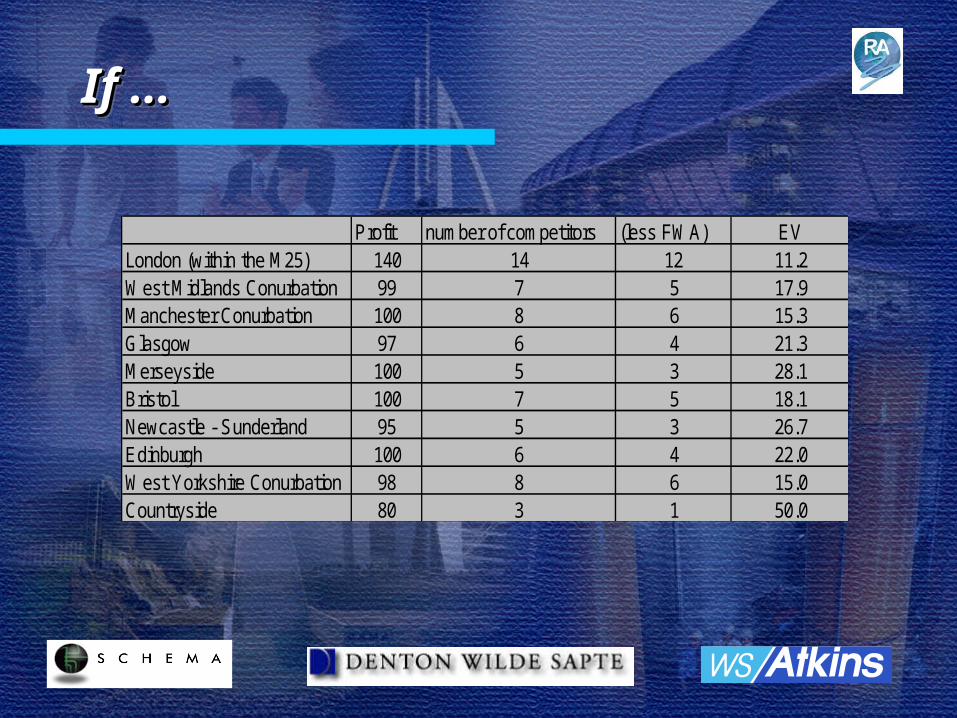

If ... If ... If ... If ...

Profit number of competitors (less FWA) EVLondon (within the M25) 140 14 12 11.2West Midlands Conurbation 99 7 5 17.9Manchester Conurbation 100 8 6 15.3Glasgow 97 6 4 21.3Merseyside 100 5 3 28.1Bristol 100 7 5 18.1Newcastle - Sunderland 95 5 3 26.7Edinburgh 100 6 4 22.0West Yorkshire Conurbation 98 8 6 15.0Countryside 80 3 1 50.0

... then ... then ... then ... then

Profit EVCountryside then London 197 59London then Countryside 207 53

-4.8% 12.2%

discounting later provision at 20%

Other ScenariosOther ScenariosOther ScenariosOther Scenarios

Operating costs of entrants differ from industry average– Differs in different markets

Incumbents and strategic entry deterrence

Operating costs of entrants differ from industry average– Differs in different markets

Incumbents and strategic entry deterrence