Embed Size (px)

Citation preview

Avoiding the Loss of a Gain: Retaining Top Managers

in an Acquisition

Caren Siehl and Dayle Smith*

The turnover of management following a merger or acquisition is a signifrmnt, yet understudied, human resource issue. W propose that the relevant HR question is not merely how to retain top managers, but 4equal importance, whether or not top manage- ment retention should be an obpctive. W present a model that integrates the retention process w*th the uverall integration strategy being pursued by the acquiring firm. The model prompts a disnwsion of those factors that influence the decision 0s to whether the top management of the acquired firm should be retained. We conclude by ident&ing appropriate HR tactics for managing the retention process.

The importance of managing the challenges of human resource issues during mergers and other forms of restructuring has k n the subject of recent research (e.g., Buono & Bowditch, 1989; Pritclqett, 1988). Al- though it has been argued that the wave of merger and acquisition (m & a) activity is now over, a quid look at the number of mergers in the last two years indicates that interest in managing human resource issues is still warranted. In 1989 and the first three quarters of 1990, over 6,276 mergers totaling over $368,650 million transpired. If we assume that restructuring will make an even greater impact as firms try to recover from the excessive debts taken on during the last decade of rampant m & a activity, then we can also assume that the management issues and strategies associated with downsizing, diversification, restructuring, and m & a’s are still of primary importance.

One major focus of the work on mergers has been on coping with the problems associated with the “merger syndrome” (Marks, 1982; Marks & Mirvis, 1985,1986). The merger syndrome is described as the stress, anxiety, and powerlessness which people experience as a result of being involved in a merger or acquisition. Employees suffering from the “mer ger syndrome” antiapate the worst due to the fear and uncertainty of what the merger holds in store for them. For example, according to Dan

The authors wish to thank David Bowen, Art Bell, and the reviewers for their comments on earlier versions of this manuscript.

Human Resource Management, Summer, 1990, Vol. 29, Number 2, Pp. 167-185 8 1991 by John Wdey & Sons, Inc. CCC 0090-4&48/91 /O20167-19$04.00

M. Dressel, Vice President of Human Resources and Organizational Services for Baxter-Travenol Labs, Inc., his people problems were mag- nified by 30,000 to 60,000 when his company acquired American Hospi- tal Supply Corporation due to merger syndrome-related issues (Ulrich, LaFasto, & Ruca, 1989). A second major human resource concern for Dressel, but one which has not been well-studied, was the retention of the top management of the acquired firm. As Dressel stated:

. . . our lives will be complicated in that we will be installing programs and concurrently attempting to minimize the defection of senior employees. (Ulrich, LaFasto, & Rucci, 1989)

The HR issue of whether to attempt to retain the top managers of the acquired firm can have significant consequences for the success or failure of a merger. Unfortunately, the guidelines which have evolved around this HR issue are in conflict. Two guidelines, which have been generically used by firms during mergers, have been offered:

1. Keep as many top managers as possible from the acquired company since they represent a key asset, and involve them heavily in key decisions about post-merger integration.

2. Quickly replace the management of the acquired company or be prepared to do so at any time in the near future.

Such conflicting principles would make it appear that the “right“ HR strategy for top management retention differs case by case. While a few studies have looked at the retention of personnel after the merger, the focus of this work has been on a concern for minimizing the upheaval commonly associated with acquisition activity. This literature has stud- ied the career development of managers after a merger (Gaertner, 1986) or post-fact0 retention of the acquired firm’s managers (Baytos, 1986; Hayes & Hoag, 1974). Current research has failed to investigate the importance of integrating pre-acquisition deasion making regarding re- tention into the overall acquisition strategy of the acquiring firm. We would argue that neglecting this aspect of acquisition strategy may jeop- ardize the potential to maximize acquisition performance, particularly if performance is contingent upon acquired managerial talent-either short- or long-term.

The central question is not merely how to retain top managers, but more important, whether or not top management retention should be an objective. We will argue that careful attention to the retention process is critical and that this process should be linked to the overall integration strategy being pursued by the acquiring firm. We will begin by examin- ing four common acquisition integration strategies. Then we will discuss the factors influencing the decision as to whether the top management of the acquired firm should be retained. Finally, we will identify the most appropriate HR tactics for managing the retention process.

168 I Human Resource Management, Summer 1990

ACQUISITION INTEGRATION STRATEGY AS A DETERMINANT OF RETENTION

Acquisition strategy, in general, involves evaluating and formulating the strategy for selecting the acquisition target, and determining the degree of acquisition integration (Baytos, 1986; Bradley & Kom, 1981). We use the term integration to refer to the overall approach taken by an acquiring company to incorporate the acquired firm. A variety of de- grees of integration are possible. Thus, it is possible for the acquiring company to selectiveiy retain parts of the acquired company while di- vesting others, to maintain the acquired organization as a semi-autono- mous subsidmy, or to absorb the acquired company completely. All of these options represent different levels of acquisition integra-

tion. We emphasize acquisition integration because the desired end point regarding the degree of integration is critical in determining the appropriate activities at every phase of the acquisition process. The ini- tial acquisition integration strategy has a significant impact on the out- come of the acquisition (Allen, Oliver, & Schwallier, 1981; Jemison & Sitkin, 1986; Mirvis, 1985).

The Langclage of Mergers and Acquisitions Our analysis of strategies for acquisition integration proceeds from

the following commonplace observation about mergers and acquisitions: the language used to describe these phenomena is rife with the language of interpersonal relationships. Employees tend to use interpersonal met- aphors to capture their impressions and to share their feelings (Hirsh, 1987; Hirsh & Andrews, 1982). The literature often refers to mergers and acquisitions as corporate "marriages." The pre-acquisition phase has been described as a "courtship period; the post-acquisition phase is said to begin with a "honeymoon." The acquired company is sometimes called the "bride"-and not uncommonly, the "reluctant bride." How did the two parties meet? In many situations, the acquiring company was a "white knight" who rode to the rescue, saving the maiden in distress from a "shark," "raider," or some other peril. On the other hand, if things go badly, employees of the acquired company may feel that their company has been "raped." The use of such metaphors has been shown to impact the way that employees process information in organizations, generally, and during the acquisition experience, more specifically (Lakoff &Johnson, 1980; Pondy, 1982; Smith & Larson, 1986).

Given that so much of the literature makes use of interpersonal meta- phors and that employees and top management use this type of Ian- guage in descriiing their experiences, we propose using the language of interpersonal relationships to describe four different strategies for ac- quisition integration. Through an analysis of each of these strategies, we can explore the influence that each strategy has on the retention of top managers of the acquired firm.

Siehl and Smith Retaining Top Managen I 169

ACQUISITION INTEGRATION STRATEGIES

Acquiring firms tend to make acquisitions pursuing one of four basic acquisition strategies (Siehl, Ledford, Silverman, & Fay, 1988; Siehl, Smith, & Omura, 1990):

1. Pillage and Plunder

Otherwise known as "asset stripping," this strategy results in a policy of taking the most valuable assets of the acquired company as quickly as possible and incorporating them into the acquiring firm. There tends to be little concern over the impact of the acquisition on employees and little of the old organization remains after the acquisition is complete. A fairly common strategy in the last few years, Pillage and Plunder is seen most frequently in corporate raiding and turnaround situations. In the corporate raider case, the raider announces that if the takeover attempt is successful, the acquired company will be broken up and the assets sold. Raiders reason that the companies are undervalued and, hence, are worth more to the shareholders "dead than alive." In the turn- around situation, the acquiring company may need to take decisive action in order to preserve any value of the acquired company. This strategy may involve closing unprofitable plants, laying off excess man- agement, staff, and employees, or abandoning obsolete product lines. In either case, employees in the acquired firm are likely to feel that their company has been "pillaged." A strategy such as this was implemented during Texaco's takeover of Getty Oil. Because the goal of the acquisition was to obtain oil reserves (a critical concern due to the much depleted reserves of Texaco), Getty represented a target whereby Texaco could acquire the reserves, strip assets, and sell off the rest of the company (Coll, 1987). T. Boone Pickens, of Mesa Petroleum, used this strategy often in the oil industry, justifying that the raid was necessary to force management to take actions which the market would value more highly, thus allowing shareholders to maximize their earnings.

2. One Night Stand

This strategy involves the development of an intense financial, but otherwise generally superficial, relationship between the acquired and the acquiring firms. The guiding principle is to avoid becoming overly involved in the acquisition. The goal is to keep the acquired company only as long as it performs; if it stops performing, divest it and find another firm with the potential for stronger performance.

This strategy is commonly used by conglomerates. Top management is concerned with managing a portfolio of assets, rather than any partic- ular business. Indeed, the top management of the acquiring firm may

170 1 Human Resource Management, Summer 1990

not know enough about most of the businesses it owns to manage them successfully without the help of experienced managers h m the ac- quired companies. Integration between the firms is minimal. The con- glomerate usually manages by the "numbers"; it often has no other choice. Financial performance is of paramount importance and the factor upon which major decisions rest. The One Night Stand strategy is best exemplified in #he acquisitions by R. J. Reynolds of Nabism and the Philip Moms purchase of General Foods, as well as Beatrice's m y acquisitions during the early 1980's. The overall goal is continued high financial performance of the acquisition portfolio.

3. CourtshiplJust Friends

This strategy involves a great deal of platonic relationship-building, but does not end in maniage. The objective is not a complete merger of the two organizations, but rather a complementary, dependable work- ing relationship. For exampie, a medical speaalties firm may acquire other product-related subsidiaries with complementary product lines. The companies remain basically independent but certain functions and the overall mission of the firms may be integrated. The firms can have operational as well as cultural differences. As in other friendships, re- sentments may at times develop on either side resulting in conflict and tension. Nevertheless, the relationship may continue and even flourish for an indefinite period of time if it is properly nurtured. A good exam- ple of the Courtship/Just Friends strategy was demonstrated by men- tieth Century-Fox Film Corporation when they acquired three com- panies (Coca-Cola Bottling Midwest, Aspen Skiing Corporation, and Pebble Beach Corporation). The company pursued these diverse targets to minimize the risks inherent in their own core business. Fox manage- ment let the companies run themselves, functioning as an inves- todowner in the first three years of the acquisitions with input on strate- gic decisions. Gradually, Fox learned the businesses and began to make suggestions for operations. The strategy pursued and the relationship that Fox built with its acquisitions decreased initial tensions enabling the firms to work togephef (Ferguson dr Doig, 1989).

The Courtship strategy involves a major attempt at achieving a stable working relationship between the firms. In the case where the Court- ship is with a distinctly diffexvnt type of firm (such as firms from differ ent industries, with diffenmt cultures, different top management styles),

Tl~ese acquisitions were eventually sold or liquidated. However, the logic for the acquisition and the aquisition strategy were considered successful in the industry.

Siehl and Smith Retaining Top Managers I 171

the efforts of maintaining stable working relationships between the or- ganizations can be quite difficult and time consuming. Such mergers require a high degree of autonomy (because the acquired firm is differ- ent), but also require a high degree of interdependence (because of the potential for synergies). In the long run, the tensions between these two needs are never really resolved.

Most of the suggestions and recommendations in the organizational literature on improving the acquisition process assume that this strategy, or the Love and Mamage Strategy described below, is being pursued. The objective of these recommendations is to help firms both reduce acquisition integration problems and to work through those problems which remain in an amicable fashion.

4. Love and Marriage

This strategy is by far the most intense and the most difficult strategy to implement due to the amount of time involved and the requisite major changes in both firms which affect large numbers of people. The focus is on creating one from two with the guiding principles being mutual respect, reciprocity, and mutual problem solving. This strategy seeks a true merger of cultures, personnel, and operations. It is the focus of most of the acquisition integration literature. In the Love and Mamage type of integration, the acquiring firm seeks to fully consoli- date the acquired firm.

Much more effort toward integration is required if the Love and Mar- riage strategy is to be employed. At the same time, with proper lead- ership, this process can be successfully managed quite effectively. A classic example illustrates this strategy. In 1985, Baxter Travenol Labora- tories Inc. acquired American Hospital Supply corporation. Although initial resistance to the merger existed, the firms integrated fully, re- designing the organizational structure and HR systems to accommodate the best of each. This integration successfully created one of the largest distributors of hospital supplies under the name of Baxter International (Ulrich, LaFasto, & Rucci, 1989). All four strategies presented above vary along a number of HR di-

mensions including the degree of interaction between employees of the two firms, amount of participation, types of communication, style of management, degree of human orientation, and the retention of top management. The literature which addresses many of these HR issues is abundant (e.g., Bastien, 1987; Buono & Bowditch, 1989; Marks, 1982). However, the decision-making process of the acquiring firm regarding top management retention has not been studied extensively. We will next discuss the impact of the four acquisition integration strategies described above on the acquiring firm’s decision-making process relative to the retention of the top managers from the acquired firm.

172 1 Human Resource Management, Summer 1990

TOP MANAGEMENT RETENTION: WHO SHOULD STAY, WHO SHOULD GO?

When planning the acquisition, the acquiring firm's chosen integra- tion strategy should determine what needs, if any, the firm will have for acquired personnel. Of course, it should be noted that the strategy an organization pursues (and the choices it makes regarding acquired per- sonnel) may not be the one that it ends up employing throughout the transition period. Firms need to take time out to make assessments, reevaluate needs, and make adaptations to the strategy as necessary. It is possible that after gaining more information about the acquired firm, the acquiring firm could learn that the acquired firm does not have the management depth to do what needs to be done. Thus, the set of ac- quired managerial competencies may change the acquisition strategy being pursued. For example, AT&T started with a love and marriage strategy with NCR. Due to NCR's reticence, AT&T ended up with a more aggressive strategy.

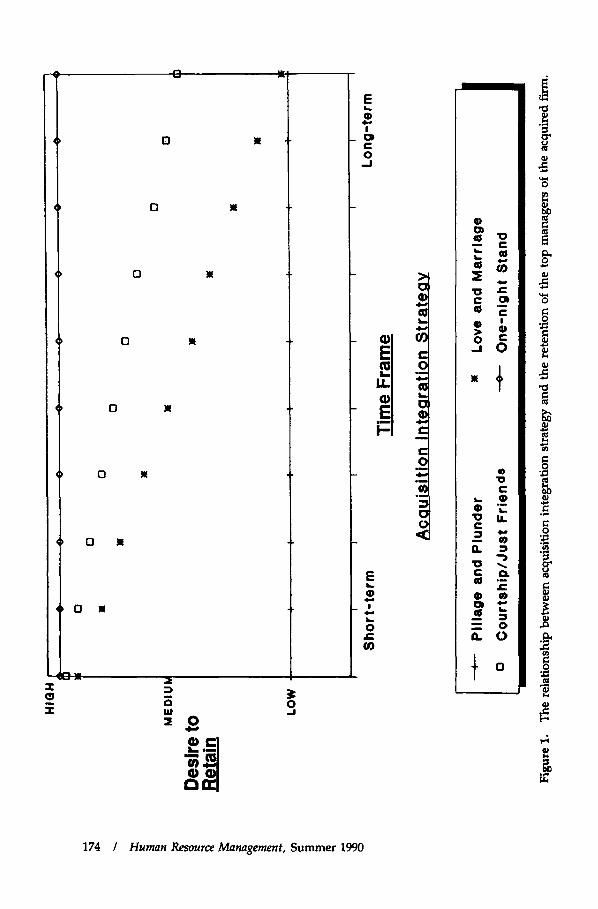

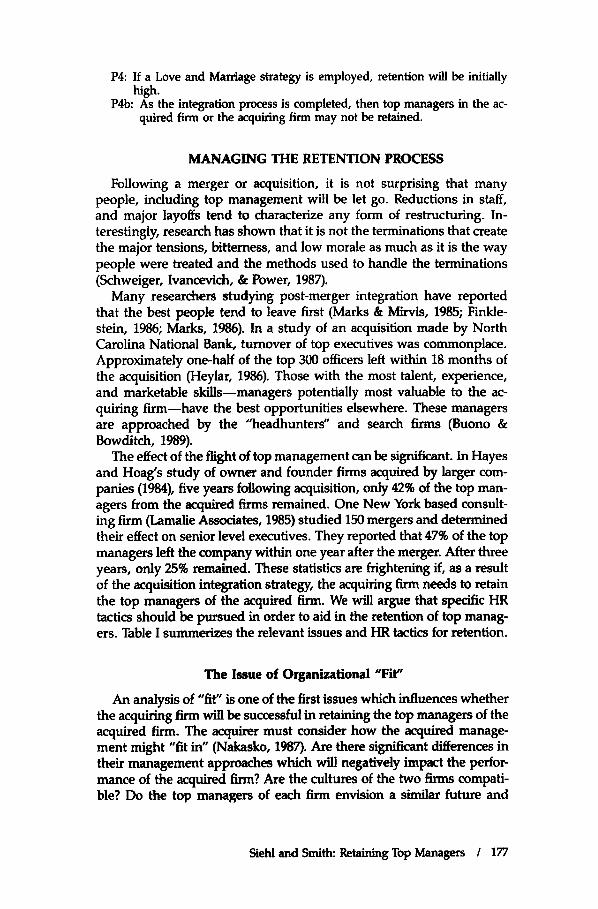

Based on the strategy pursued, and keeping in mind the adaptations the firm might make, top management retention should vary as a conse- quence of the acquisition integration strategy. Figure 1 presents the rela- tionship between the acquisition integration strategy, the desire to retain the top managers of the acquired firm, and time. In the following, we will discuss those factors that influence the decision to attempt to retain the top managers of the acquired firm.

We would predict that with the Pillage and Plunder strategy, in most cases, attempts to retain the top management of the acquired firm are inappropriate. Turnover should be high. The acquiring firm may want to terminate acquired top managers as quickly as possible for several rea- sons. Acquired top managers may not be perceived to have been effec- tive. This is likely to be true when the acquisition is part of a turnaround situation. Alternatively, the rationale for the merger may have been the acquisition of key assets of the acquired firm such as distribution chan- nels or other resources, nof the top management team. For example, in the Texaco acquisition described above, the goal was to obtain the oil reserves. Other corporate assets, including management, were not re- quired to meet the acquirer's purpose. In another case an insurance firm seeking to expand its product line acquired another insurance firm which offered more diverse products. The acquirer sold a significant portion of the acquired firm and, thus, had no need for the acquired top management (Siehl, Smith, & Omura, 1990).

A major challenge in this situation is how to assess the quality of top management and lower level operating managers. There may be some good people near the top but the key will be identifymg them and then convincing them to stay during this period of turmoil. Although the top managers may not be needed, the retention of operating managers may be critical to either turning the firm around or selling off the business.

Siehl and Smith: Retaining Top Managers I 173

HlQ

H

ME

DlU

l

Des

lre to

R

etai

n.

LOW

0

0

Y

w 0

x

0

Y

0

0

0

0

w w

Sh

ort

-ter

m

Tim

e Fr

ame

Aca

u isi

tion

lnte

ara t

ion

St r

ateq

y

Long

-ter

m

+ P

illag

e an

d P

lun

der

0

Co

urt

ship

/Ju

st

Fri

end

s

)I

Love

an

d M

arri

age

+ O

ne-

nig

ht

Sta

nd

Figu

re 1

. Th

e re

latio

nshi

p be

twee

n ac

quisi

tion

inte

grat

ion

stra

tegy

and

the

rete

ntio

n of

the

top

man

ager

s of

the

acqu

ired

firm

.

When pursuing a One-Night Stand strategy, on the other hand, the acquiring firm should give serious thought to the need for the expertise of the top management team of the acquired firm. In this situation, the acquiring firm is not likeiy to have the experience, skills, talent, or in- terest in managing the day-today operations of the acquired firm. As an example, in the Beatrice acquisition of Esmark in 1984, the experience needed to run the divisions of Esmark (Playtex clothing, Avis Rent-A- Car, and Hunt-Wesson Foods) was lacking within Beatrice. In spite of this need for the top management of the acquired firm, turnover was high among Esmark executives. Several reasons explain this turnover. First, once Beatrice & b a n James Dutt took over, the management style became much harsher. The Chicago Tribune captured this style in a cartoon caption attributed to Dutt, “All those opposed, signify by saying ’I quit’.” In addition, Beatrice’s top executives failed to communicate in a supportive way to Esmark executives. The talent they needed the most were the same people to whom they showed the least care and respect. Consequently, Esmark top managers had no motivation to stay. Without Esmark’s top management team and their experience in running these profitable divisions, Beatrice was forced to divest these companies (Hirsch, 1988).

With Courtship/Just Friends, the goal is to develop a good, solid working relationship with the acquired firm and its top management team. Therefore, we would predict that retention needs would be ini- tially high. In the long term, the desire to retain the top management may be moderated by the need to further integrate the two firms, thus causing the top management team to be redundant. hitially, the firms must work together and capitalize on the expertise and experience of the managers from both firms. Cooperation is paramount for success. Should more collaboration lead to further integration, redundancies in management would lead to layoffs. Such is the case when Johnson & Johnson merged four of their subsidiary critical care firms. AU four firms sold different product lines well known under their brand name (Jelco catheters, Dinamaps, etc.). As subsidiary firms, these companies, when originally acquired, enjoyed the autonomy and independence afforded to them by J & J. The CourtshiplJust Friends strategy played a para- mount role. But as J & J corporate determined that the financial syn- ergies would be far greater by further merging these four firms, redun- dancies were evident. As collaboration increased between the sales force, product managers, and top executives from the four firms, it was clear that layoffs had to occur to avoid overlap and to streamline. To J & J’s credit, many of the redundant employees had opportunities at other J & J companies.

With Love and Marriage, we find an interesting paradox. This strat- egy calls for integration at all levels of the two firms with a concern for blending both employees and operations. Because of this, it is critical to carefully manage the human resource issues and to assure a good fit

Siehl and Smith: Retaining Top Managers I 175

between the two firms while minimizing the amount of friction and the destructive threats normally associated with mergers. The transition team charged with implementing the acquisition strategy will need par- ticipation and assistance from both companies. At the same time, the amount of redundancy will necessitate layoffs and mass firings. Insecu- rity, fear, stress and rumors run rampant. Even the employees and man- agers in the acquiring firm may have concerns or doubts about their own job security, given the overall goals of this integration strategy.

The problem or paradox for the acquiring firm in this situation is that in order to achieve a smooth integration process, in the short-term, the need to keep the top management team of the acquired firm is high. In the 1982 Allied-Bendix merger, this short-term integration was accom- plished through Chairman Hennessy's announcement to keep Bendix executives and to commit to them that they were to be a part of building the combined company (Hirsh, 1988).

However, in the long term, the desire to retain the acquired execu- tives is expected to be low because of the need to streamline and reduce duplicative effort. It is possible that the redundancies could come from either the acquired or acquiring firm with managers from either firm being at risk. This might mitigate the turnover of talented top managers of the acquired firm. Redundancy develops even in an effective use of the Love and Marriage strategy. In the Baxter Travenol acquisition of American Hospital Supply described above, insecurity and fears loomed daily in the early days of the transition. To successfully consolidate operations, top management was needed from both firms. Eventually, the need to streamline prevailed. In this case, however, a system for choosing the best people from both companies was used and the top jobs were filled with managers from both firms.

If the top managers abandon ship rather than assist in the integration effort or if they take a wait-and-see attitude, numerous problems of coordination will result. Unfortunately, for many acquiring firms, the early assessment of human resource needs in terms of acquisition strat- egy is often neglected. A failure to consider this in the negotiating stage of the deal may very well contribute to major integration problems or even spell failure for the acquiring firm.

Assessing acquisition strategy, then, will help firms to determine their management retention needs. We present the following testable propo- sitions regarding the relationship between the acquisition strategy and the retention of the top managers of the acquired firm:

P1: If the acquirer pursues a Pillage and Plunder strategy, then frequently top managers will not be retained, but key operating managers may be retained.

P2: If the acquirer pursues a One-Night-Stand strategy, then top managers will tend to be retained.

P3: If the acquirer pursues Courtship/Just Friends strategy, retention will be initially high with possible turnover in the future.

176 I Human Resource Management, Summer 1990

P4: If a Love and Marriage strategy is employed, retention will be initially

P4b: As the integration process is completed, then top managers in the ac- high.

quired firm or the acquiring firm may not be retained.

MANAGING THE RETENTION PROCESS Following a merger or acquisition, it is not surprising that many

people, including top management will be let go. Reductions in staff, and major layoffs tend to characterize any form of restructuring. In- terestingly, research has shown that it is not the terminations that create the major tensions, bitterness, and low morale as much as it is the way people were treated and the methods used to handle the terminations (Schweiger, Ivancevich, & Power, 1987).

Many researchers studying post-merger integration have reported that the best people tend to leave first (Marks & Mirvis, 1985; Finkle- stein, 1986; Marks, 1986). In a study of an acquisition made by North Carolina National Bank, turnover of top executives was commonplace. Approximately one-half of the top 300 officers left within 18 months of the acquisition (Heylar, 1986). Those with the most talent, experience, and marketable skills-managers potentially most valuable to the ac- quiring firm-have the best opportunities elsewhere. These managers are approached by the Yheadhunters” and search firms (Buono & Bowditch, 1989).

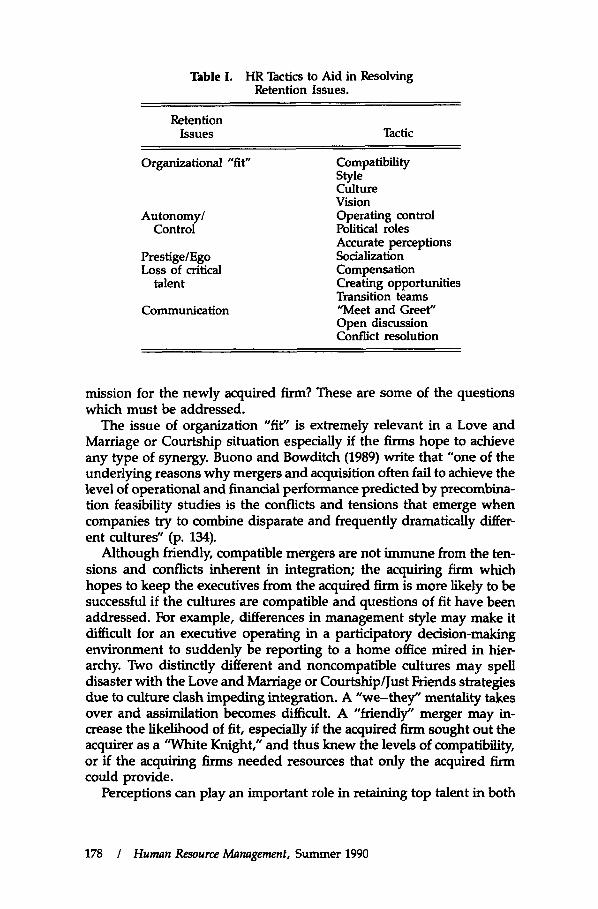

The effect of the flight of top management can be significant. In Hayes and Hoag’s study of owner and founder firms acquired by larger com- panies (1984), five years following acquisition, only 42% of the top man- agers from the acquired firms remained. One New York based consult- ing firm (Lamalie Associates, 1985) studied 150 mergers and determined their effect on senior level executives. They reported that 47% of the top managers left the company within one year after the merger. After three years, only 25% remained. These statistics are frightening if, as a result of the acquisition integration strategy, the acquiring firm needs to retain the top managers of the acquired firm. We will argue that speafic HR tactics should be pursued in order to aid in the retention of top manag- ers. Table I summerizes the relevant issues and HR tactics for retention.

The Issue of Organizational “Fit”

An analysis of “fit” is one of the first issues which influences whether the acquiring firm will be successful in retaining the top managers of the acquired firm. The acquirer must consider how the acquired manage- ment might “fit in” (Nakasko, 1987). Are there significant differences in their management approaches which will negatively impact the perfor- mance of the acquired firm? Are the cultures of the two firms compati- ble? Do the top managers of each firm envision a similar future and

Siehl and Smitlx Retaining Top Managers / 177

Table I. HR Tactics to Aid in Resolving Retention Issues.

Retention issues Tactic

Organizational "fit"

Autonomy/ Control

Pres tige/Ego Loss of critical

talent

Communication

Compatibility Style Culture Vision Operating control Political roles Accurate perceptions Sodalition Compensation Creating opportunities Transition teams "Meet and Greet" Open discussion Conflict resolution

mission for the newly acquired firm? These are some of the questions which must be addressed.

The issue of organization "fit" is extremely relevant in a Love and Marriage or Courtship situation especially if the firms hope to achieve any type of synergy. Buono and Bowditch (1989) write that "one of the underlying reasons why mergers and acquisition often fail to achieve the level of operational and financial performance predicted by precombina- tion feasibility studies is the conflicts and tensions that emerge when companies try to combine disparate and frequently dramatically differ ent cultures" (p. 134).

Although friendly, compatible mergers are not immune from the ten- sions and conflicts inherent in integration; the acquiring firm which hopes to keep the executives from the acquired firm is more likely to be successful if the cultures are compatible and questions of fit have been addressed. For example, differences in management style may make it difficult for an executive operating in a participatory decision-making environment to suddenly be reporting to a home office mired in hier- archy. Two distinctly different and noncompatible cultures may spell disaster with the Love and Marriage or Courtship/Just Friends strategies due to culture clash impeding integration. A "we-they" mentality takes over and assimilation becomes difficult. A "friendly" merger may in- crease the likelihood of fit, especially if the acquired firm sought out the acquirer as a "White Knight," and thus knew the levels of compatibility, or if the acquiring firms needed resources that only the acquired firm could provide.

Perceptions can play an important role in retaining top talent in both

178 I Human Resource Management, Summer 1990

the long- and short-term. For example, in one company which was taken over by a company pursuing a One-Night-Stand strategy, an executive noted, ". . . I had the option of staying but from what I understood (the other company) was not an ideal place to work even in terms of report- ing relationships. . . eventually we believed there would be demo- tions . . . I didn't stay around to find out." (Smith, 1986).

The Issue of Autonomy

Numerous studies have identified "autonomy" as a factor of central concern to top managers following a merger (Baytos, 1986; Bradley & Korn, 1981; Buono & Bowditch, 1988; Hayes & Hoag, 1974; Marks, 1982). Having decision-making authority and control can be particularly impor- tant to newly-acquired executives. Even in a Courtship or One-Night- Stand situation, where autonomy is espoused (by the acquiring finn) to be important, problems and surprises can arise. In a Courtship situa- tion, the reality of one president was summarized as the following:

Less than a year after Northwest industries, Inc., played White Knight to Micro- dot, Inc., rescuing the company from a hostile takeover attempt by General Cable Corp., Rudolph Eberstadt, Jr. left the presidency of h4icrodot, a company he helped to found and headed for 16 years. Eberstadt's departure sent shock waves through the business community, particularly since he and Northwest president Ben W. Heineman appeared to get along well. AIthough Eberstadt's reasons for leaving were varied, when asked to sum them up in one sentence, he responded, "I just wasn't used to having a boss.'' (Business &k Oct. 30, 1978)

In organizations where executives have stayed, the managers re- ported that they felt they had a satisfactory degree of autonomy (Hayes & Hoag, 1974). That is, the executives in the acquired firm had day-to- day operating authority to manage the business. Allowing the acquired top managers this degree of freedom may be critical in terms of long- term retention. The parent firm may retain tight financial and budgetary control but must relinquish enough operating control to encourage long- er term executive retention in the One-Night-Stand and Courtship situa- tions. The key for the acquirer is to balance what is perceived to be the necessary degree of control with allowing the acquired top manage- ment team to run their own show.

A feeling of autonomy can also be achieved through the creation of political roles for the acquired firm's top management, such as a seat on the board of directors of the parent firm. Perception is important here as well. Does the management of the acquired firm understand the acquir- ing firm's philosophy regarding autonomy? Have the executives of other acquisitions enjoyed high amounts of control and visible political roles? Does the acquirer communicate confidence in the acquired's abilities to perform? What is the level of decentralization in the parent h? How flexible are reporting relationships? How people-oriented is the ac-

Siehl and Smith Retaining Tap Managers / 179

quirer? With the Love & Marriage strategy, even short-term retention may be problematic if the responses to questions such as these are not shared with the top management of the acquired firm.

The Issue of Prestige/Ego

A loss of prestige is often related to the issue of autonomy. By main- taining the company as an independent subsidiary and allowing name recognition to go on unencumbered, egos are massaged, and prestige is safeguarded. How sensitive is the acquirer to previous status and role differences?

This issue of status can be understood in an analysis of the Illinois Central Industries takeover of PET Inc. in 1978. Although this was a hostile takeover, the chairman of Illinois Central understood the concept of status and ego. In addition to committing to let known brand names (e.g., Midas mufflers, PET dairy foods) continue-symbolically impor- tant to PET executives-the chairman also allowed acquired personnel to maintain their status and prestige by keeping corporate headquarters intact in St. Louis and traveling to their home base when doing corporate planning. Paul Hirsch (1988), in an article on “happy endings to merg- ers,’’ describes these behaviors taken by the acquiring firm as “minimal strutting.”

Socializing acquired managers into the parent firm and dealing with feelings of the loss of ego, disillusionment, and misplaced loyalty pre- sent challenges to managing the retention process as well. Executives may experience a feeling of failure depending upon how the acquirer chooses to socialize the acquired managers (Mirvis, 1985). The loss of ego can lead to resentment and can trickle down through the ranks. Misplaced loyalties can result in similar problems. Anticipating this and managing these concerns as early as possible can go a long way to easing the transition and increasing both short-term and long-term retention. A failure to consider this aspect of the transition can result in the loss of the best people and often the ones needed to make the merger work.

The Issue of the Loss of Talent

Avoiding the loss of valuable talent is a key concern of many ac- quirers. This factor is critical in the One-Night-Stand, Courtship, and perhaps even Love & Marriage strategies. Those managers with the skills and competence to make a real difference to the acquirer are an asset in and of themselves. Since these managers have the record to go elsewhere, acquiring firms need to give serious thought as to how to increase the likelihood that they will stay, even for a short time to aid in the transition and/or in training successors. Even when an executive has a ”golden parachute,” he or she may not want to stop working. After the merger between Texaco and Getty, one executive from Getty Oil stated,

180 I Human Resource Management, Summer 1990

"I had a golden parachute, so financially I came out very well, as well as I would have if I were 10 years older. . . but I wasn't ready to quit working . . . there was a great void." (Smith, 1986).

One tactic that some acquiring firms have found helpful is tied to compensation. Although the executives may have "golden parachutes," the acquiring firm should develop "silver seatbelts" or "golden hand- cuffs" to make it more attractive for the executive to stay. In effect, this option negates the parachute and creates an opportunity for the top manager that would be difficult to refuse. This tactic makes it attractive for the acquired management to stay or next to impossible for them to leave. Stock options, financial incentives, valuable career opportunities, executive perks, and overall attractive compensation packages tied to short-term or long-term retention make it more likely that the acquirer can retain desired personnel.

Another tactic is to demonstrate that continued opportunities exist for talented managers. This demonstration can aid in shaping percep- tions and expectations. In the Lamalie study, for example, it was found that 38% of the executives said the merger created new capeer oppor- tunities while only 25% said there was a decrease. Thirty-four percent noted little or no effect. These percentages are a reflection of the acquisi- tion integration strategy. For example, in a conglomerate acquisition of smaller companies, many opportunities for top-performing managers may exist in the parent firm or other subsidiaries. In Johnson & Johnson and Procter & Gamble, for example, often times, top executives from the new subsidiary are brought inside or offered positions in other Subsidi- aries. The opportunity to work for a larger organization in a different environment presents a unique learning experience. Also, the oppor- tunity to learn a new business presents yet another challenge.

Other strategies will provide unique opportunities, such as being a member of a transition team. Transition teams provide a useful tactic in keeping the best people and maximizing the integration process. Suc- cess is dependent upon the cooperative efforts of employees from both firms who are members of the transition team. The key, of course, is to provide the incentive for the best and brightest to stay and to be a part of the transition tern. As an example, one acquired VP of Human Re- sources at Saga Corp. (a restaurant services company) noted that he had hoped his company would stay independent but following hAarriott's acquisition and the implementation of a Love and Marriage strategy, he decided to stay to help during the transition. Although he subsequently left the company, he commented that "I found the process has been a real learning experience." The treasurer of another firm stated that he would have liked the opportunity to "clean up the combined companies into an absolute gem." He said that, "I still think that over the long run, we could have given the shareholders more value and given me pe- rsonally the opportunity to participate in actomplishing that." (Smith, 1986).

Siehl and Smith: Retaining Top Managers I 181

The Issue of Communication

A last issue for retention deals with the communication that occurs before, during, and after the merger. Needless to say, if the strategy is to retain top managers, communication of this goal is paramount. Usually, tactics in communicating are tied closely to assurances that talented top managers don’t need to leave (e.g., attractive benefits for staying). The first tactic could be called “Meet and Greet.’’ This tactic involves the acquiring firm making an effort to communicate up front about its needs, intentions, and integration plans. Failing to do this increases uncertainty and insecurity.

Second, the firm must be committed to open discussion. Indecision and lack of communication send mixed signals to acquired personnel and the acquirer risks losing the best managers. For example, Buono and Bowditch (1989) describe what happened in the Steel Co. acquisition of Petro. The acquiring firm wanted the expertise of the technical experts, engineers, and scientists of Petro. In fact, the expertise was a major reason for the acquisition. Terminations and layoffs of other personnel, however, sent mixed messages to the very people Steel Co. hoped to keep. The most talented left the company voluntarily to avoid being fired. Thus, the acquirer bought the firm, but without the experts that made the firm desirable in the first place.

Resolving conflicts and negotiating expectations are also communica- tion tactics necessary to retain target managers. Negative feelings from specific incidents can result in voluntary turnover, as evidenced in one bank merger where one-half of the top officers left the company (Heylar, 1986).

CONCLUSION

The purpose of this article has been to investigate a critical HR issue which arises as a result of a merger or acquisition. We have discussed the importance of framing decisions about the retention of top management from the acquired firm in the context of the acquisition integration strat- egy being pursued by the acquiring firm. We have argued that the an- swer to the question of whether the acquiring firm should attempt to retain the acquired top management is directly linked to the choice of integration strategy. The major problem facing most acquiring firms, however, is that the determination of who stays or who goes is done almost exclusively post-fact0 or after the deal has been made (Hayes & Hoag, 1974). Both the acquiring firm and the executives in the acquired firm tend to be reactive in making decisions rather than proactively managing the process before the transition begins (Siehl, Smith, & Omura, 1990). This failure to match the desire for executive retention with the integration strategy and to plan accordingly can lead to subop- timal outcomes for the merger.

182 I Human Resource Management, Summer 1990

We have also discussed how specific HR tactics can be helpful in resolving common retention issues. The acquiring firm must plan how to manage the retention process and to implement those tactics which will lead to the desired duration of retention. Without this level of atten- tion to such an important HR issue, the acquiring firm is likely to lose what may be a critical asset of the acquired firm-the top managers.

Our argument that the deasion to retain top management based on acquisition strategy has several implications for senior managers facing a merger or acquisition. First, the senior executive should assess &/her own risk or vulnerability following the acquisition. What strategy is the firm pursuing? What are the firm's likely retention needs? Corporate staff positions, redundancies in job responsibilities, talent and/or exper- tise that would no longer be required put the executive at more risk, Thus, if the firm pursues a Pillage and Plunder strategy, a manager's best position is to prepare for the termination by working out the best severance package/parachute during negotiation (for a full discussion of executive options, see Hirsch, 1987 and Siehl, Smith, & Omura, 1990). The executive who oversees a function that generates revenues, has political clout, and/or is needed to make the post-merger integration work is at less risk for termination when the strategies of the One Night Stand, Courtship/Just Friends and, initially, Love and Marriage are being pursued. All managers affected by the merger must assess the strategy, evaluate options, and reassess the process during the transi- tion.

The propositions regarding acquisition strategy and retention needs have not been empirically tested. Anecdotal data indicates that firms pursuing specific strategies face unique problems related to their execu- tive staffing needs. Future research should address the gains and losses achieved by executive retention and termination. Research in this area will broaden our understanding of managing not only merger and ac- quisition activity, but also the downsizing accompanying corporate re- structuring-a phenomenon increasingly familiar in today's competitive environment.

Caren Siehl is currently an assoCiate professor of management at Arizonn State University West after spending two years at INSEAD, the leading business school in Europe. She earned her Ph.D. at Stanford UniPersity. Prior to her academic career, Professor Siehl was involved in executive training and market- ing at IBM. Her research interests focus on organizational culture and the impact of culture on the delivery of customer serwice, the mergerlquisitwn process, and the implementation of joint venture strategy. Her work has ken published in the Academy ofManagement Review, The Academy ofManagement Executive, and Organizational Dynamics.

Dayle Smith is an assistant professor of management at the School of Business Administration, Georgetown University. She received an interdisciplinary PhD.

Siehl and Smith: Retaining Top Manages / 183

in communicationlorganizational behavior from the University of Southern Cal- ifornia. Her research interests focus on managing human resources during merg- ers and acquisitions, organizational culture, and managing the work-family dilemma. Her workhas been published in the Academyof Management Executive, Journal of Staffing and Recruitment, and a forthcoming book by Dow Jones-Irwin.

REFERENCES Allen, M., Oliver, A., & Schwalie, K. (1981). The key to successful acquisitions,

Bastien, D. (1987). Common patterns of behavior and communication in corpo-

Baytos, L. (1986). The HR side of acquisition and divestiture, Human Resource

Bradley, J., & Korn, D. (1981). Acquisition and corporate development. Lexington,

Buono, A., & Bowditch, J. (1989). The human side of mergers and acquisitions. San

Coll, S . (1987). The taking of getty oil. New York Atheneum Press. Finklestein, S. (1986). The acquisition integration process. Proceedings for the

Academy of Management Meetings, Chicago, IL. Gaertner, K. (1986). Colliding cultures: Implications of a merger for managers

careers. Paper presented at the Academy of Management Meetings, Chicago, IL. Hayes, R. H. (1979). The human side of acquisition, Management Review, 8, 41-

46. Hayes, R., & Hoag, R. (1974). Post acquisition retention of top management,

Mergers and Acquisitions, 9, 8-18. Heylar, J. (1986, December 18). In the Merger Mania of Interstate Banking, Style

and Ego are Key. Wall Street Journal. Hirsch, P. (1988, February). Happy endings to mergers. Across the Board, 14-21. Hirsch, P. (1987). Pack your own parachute: How to survive mergers, takeovers and

other corporate disasters. Reading, MA: Addison-Wesley. Hirsch, P., & Andrews, J. (1982). Ambushes, shootouts, and knights of a round-

table: The language of corporate takeovers. In L. Pondy, P. Frost, G. Morgan, & T. Dandridge (Eds.), Organizational symbolism (pp. 145-155). Greenwich, CT: JAI.

Jemison, D., & Sitkin, S. (1986). Acquisitions: The process can be the problem, Harvard Business Review, 64(2), 107-116.

Lakoff, G., & Johnson, M. (1980). Metaphors we live by. Chicago: University of Chicago Press.

Marks, M. (1982). Merging human resources: A review of current research. Mergers and Acquisitions, 17, 38-44.

Marks, M. & Mirvis, P. (1985). Merger syndrome: stress and uncertainty. Mergers and Acquisitions, 82, 38-44.

Marks, M. & Mirvis, P. (1986). The merger syndrome: Management by crisis, Part II. Mergers and Acquisitwns, 70-76.

Merger problems may take years to solve. (1986, May) Management Review,75, 4-5.

Mirvis, P. (1985). Negotiations after the sale: The roots and ramifications of conflict in an acquisition, Journal of Occupational Behavior, 6, 65-84.

Nakasko, P. (1987, January 6). When executives are squeezed by mergers. Sun Jw Mercu y News, p. 8E.

Journal of Business Strategy, 2 , 14-24.

rate mergers and acquisitions, Human Resource Management, 26, 17-33.

Planning, 4, 167-175.

MA: Lexington Books.

Francisco: Jossey-Bass.

184 I Human Resource Management, Summer 1990

Pondy, L. (1982). The role of metaphors and myths in organization and in the facilitation of change. In L. Pondy, P. Frost, G. Morgan, Q T. Dandridge (Eds.), Orgunizational symbolism (pp. 157-166). Greenwich, CT: JAI.

Pritchett, P. (1988). After the merger: Managing the shock waves. Dallas: Dow Jones- Irwin.

Schweiger, D. L., Ivancevich, J. M., & Power, F. R. (1987). Executive actions for managing human resources before and after acquisition, Academy of Manage- ment Executive, I , 127-138.

Siehl, C., Ledford, G., Siverman, R., &Fay, P. (1988, March/April). Preventing culture clashes from botching a merger. Journal of Mergers and Acquisitions, 51- 57.

Siehl, C., Smith, D., & Omura, A. (1990). After the merger: Should executives stay or go? Academy of Mnnagement Executive, 4, 50-59.

Smith, D., & Larson, R. (1986). The meaning of mergers and acquisitions: An interpretive approach. Paper presented at the meetings of the Western Academy of Management, Reno, NV.

Smith, D. (1986). When Cultures Clash A Case Study of the Texaco Takeover of Getty Oil and the Impact of Acculturation on the Acquired Firm. Unpublished doctoral disserfution, University of Southern California.

Ulrich, D., LaFasto, F., and Rucci, T. (1989, July/August). Why Baxter moved quickly to absorb American Hospital, Mergers 6 Acquisitions, 24, 54-59.

Siehl and Smith Retaining Top Managers / 185