Embed Size (px)

Citation preview

Avoiding Corporate Successor

Liability in Asset Sales Mitigating Risk Through Due Diligence, Contractual Provisions,

Reps and Warranties Insurance, and More

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

THURSDAY, NOVEMBER 20, 2014

Presenting a live 90-minute webinar with interactive Q&A

Thomas O. Bean, Partner, Verrill Dana, Boston

Craig Carpenter, Vice President and Associate General Counsel, Ingram Micro,

Santa Ana, Calif.

Leib Orlanski, Partner, K&L Gates, Los Angeles

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-888-450-9970 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can

address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

For CLE purposes, please let us know how many people are listening at your

location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of

attendees at your location

• Click the SEND button beside the box

If you have purchased Strafford CLE processing services, you must confirm your

participation by completing and submitting an Official Record of Attendance (CLE

Form).

You may obtain your CLE form by going to the program page and selecting the

appropriate form in the PROGRAM MATERIALS box at the top right corner.

If you'd like to purchase CLE credit processing, it is available for a fee. For

additional information about CLE credit processing, go to our website or call us at

1-800-926-7926 ext. 35.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

© Copyright 2014 by K&L Gates LLP. All rights reserved.

November 20, 2014

Avoiding Successor Liability in

Asset Purchase Acquisitions

Presented by: Leib Orlanski, K&L Gates

Craig Carpenter, Ingram Micro

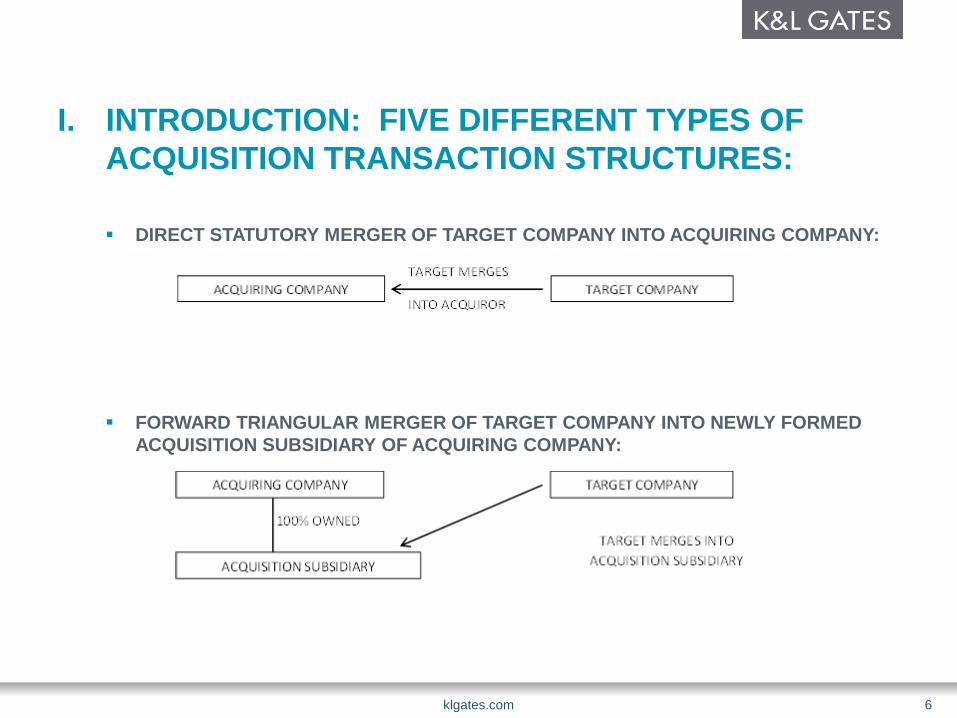

I. INTRODUCTION: FIVE DIFFERENT TYPES OF

ACQUISITION TRANSACTION STRUCTURES:

DIRECT STATUTORY MERGER OF TARGET COMPANY INTO ACQUIRING COMPANY:

FORWARD TRIANGULAR MERGER OF TARGET COMPANY INTO NEWLY FORMED

ACQUISITION SUBSIDIARY OF ACQUIRING COMPANY:

klgates.com 6

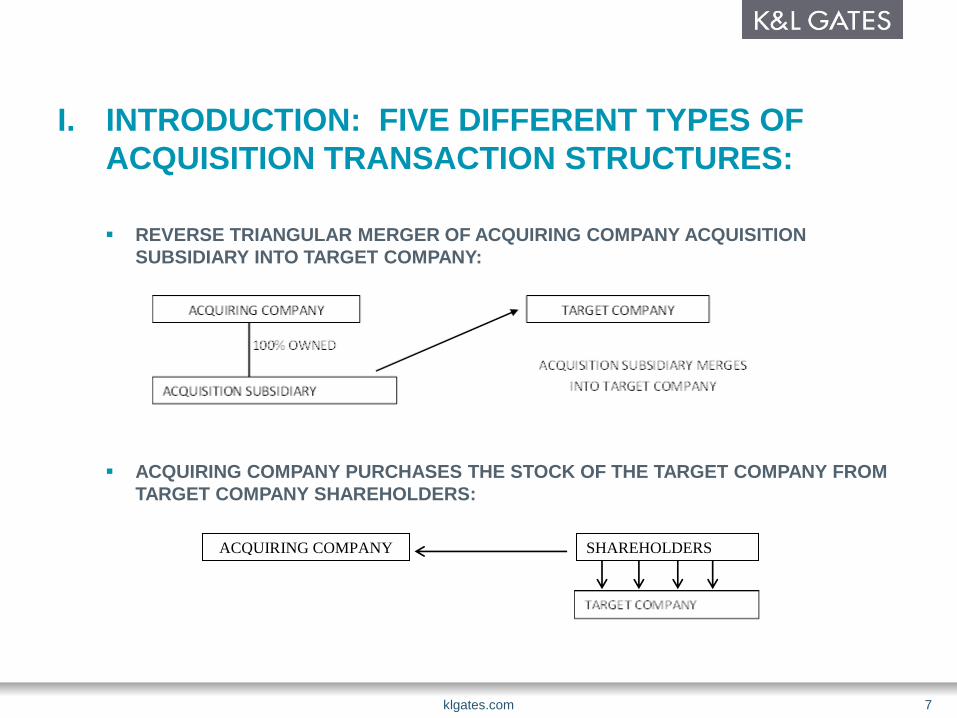

I. INTRODUCTION: FIVE DIFFERENT TYPES OF

ACQUISITION TRANSACTION STRUCTURES:

REVERSE TRIANGULAR MERGER OF ACQUIRING COMPANY ACQUISITION

SUBSIDIARY INTO TARGET COMPANY:

ACQUIRING COMPANY PURCHASES THE STOCK OF THE TARGET COMPANY FROM

TARGET COMPANY SHAREHOLDERS:

klgates.com 7

ACQUIRING COMPANY SHAREHOLDERS

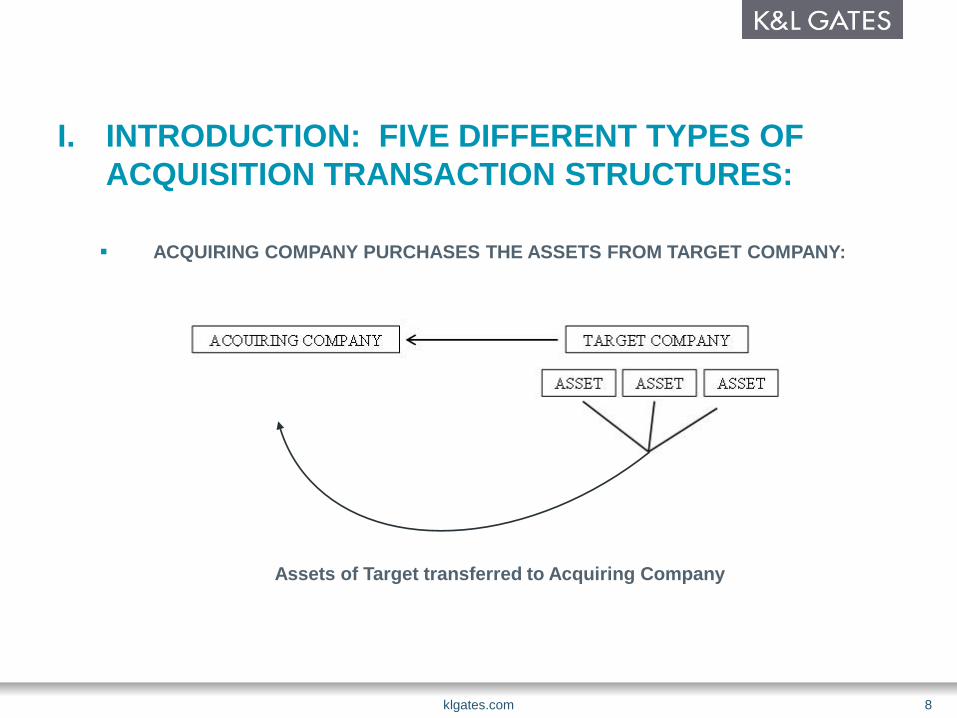

I. INTRODUCTION: FIVE DIFFERENT TYPES OF

ACQUISITION TRANSACTION STRUCTURES:

ACQUIRING COMPANY PURCHASES THE ASSETS FROM TARGET COMPANY:

Assets of Target transferred to Acquiring Company

klgates.com 8

II. PROS/CONS OF ASSET ACQUISITION V. STOCK

ACQUISITION

LIABILITY PROTECTION AFFORDED BY ASSET SALE

Ability to specifically identify specific liabilities assumed by acquiring company and

exclude named liabilities.

Example

“Buyer will not assume debt owed to X”

Example

“Buyer will not assume the obligation to repair shipped parts to XYZ customer”

Example

“Buyer will not assume consulting contract with Finagle Consulting”

Ability to insulate buyer from unknown and contingent liabilities not identified such as, for

example, delinquent taxes, trade creditors, former employees, lawsuits not yet filed.

klgates.com 9

II. PROS/CONS OF ASSET ACQUISITION V. STOCK

ACQUISITION

ABILITY TO STEP-UP BASIS FOR TAX DEPRECIATION PURPOSES

Old Basis of assets stepped-up to purchase price of assets.

Purchase price can be allocated to assets which have shorter (i.e. faster) depreciation

lives - machinery and equipment 3-5 year life v. goodwill 15 year life.

DIFFERENCES IN REPS AND WARRANTIES IN ASSET SALE V. STOCK

SALE

No reps and warranties as to capital structure of target in asset sale needed.

No reps and warranties as to authorization to do business or in good standing in foreign

jurisdictions.

klgates.com 10

II. PROS/CONS OF ASSET ACQUISITION V. STOCK

ACQUISITION

DIFFICULTY IN ITEMIZING NUMEROUS ASSETS TRANSFERRED IN ASSET

SALE

All assets, machinery, raw materials, copyrights, logos, business names, trade secrets,

must be itemized, identified and specifically transferred via a bill of sale.

All contracts must be identified and transferred.

Because in some states (e.g., New York) sales tax may be payable on some of the

tangible assets being transferred to the buyer, it is necessary to allocate a portion of the

purchase price to each itemized assets in order to avoid paying a sales tax on all

assets.

Since only assets being sold, business permits, licenses, qualifications, (ISO

certifications) need to be re-applied for by new owner.

klgates.com 11

II. PROS/CONS OF ASSET ACQUISITION V. STOCK

ACQUISITION

NECESSITY OF OBTAINING THIRD PARTY CONSENTS UNDER NON-

ASSIGNMENT CLAUSES OF EXISTING CONTRACTS.

Leases

I.P. licenses

Material contracts with customers and suppliers

Governmental contracts (e.g., Defense Dept. contracts)

U.S. Patent and Trademark Office forms for patent assignment

klgates.com 12

III. Successor Liability in Asset Sales

13

Thomas O. Bean, Partner [email protected] One Boston Pl. – Ste. 1600 Boston, MA 02108 (617) 309-2600

The Principal Virtues Of An Asset Sale For A Buyer:

• In an asset acquisition, a Buyer can “cherry pick” the assets it wishes to buy.

• More importantly, a Buyer can by express language limit or avoid assuming the target’s liabilities, both known and unknown.

• If only it were is so easy. A Buyer should not take complete comfort in the protective contractual language of an asset purchase agreement.

14

A Buyer Can Still be Saddled with Target Liabilities Notwithstanding Express Limiting Language In The Acquisition Agreement

• Successor Liability Common Law Doctrines

• Statutorily Imposed Liabilities on Successors

Important: Applicable case law and statutes can vary significantly from state to state.

15

A. Common Law Liabilities 1. DeFacto Merger

• This doctrine was initially based on the notion that while a transaction may have been documented as an asset purchase, the practical result may look like a merger. For example, the selling company disappears and the Seller’s stockholders may hold significant equity stakes in the Buyer. Over time, public policy considerations also crept in. Courts have sometimes determined that disadvantaged plaintiffs should not be left without a remedy.

16

1. DeFacto Merger (Cont’d)

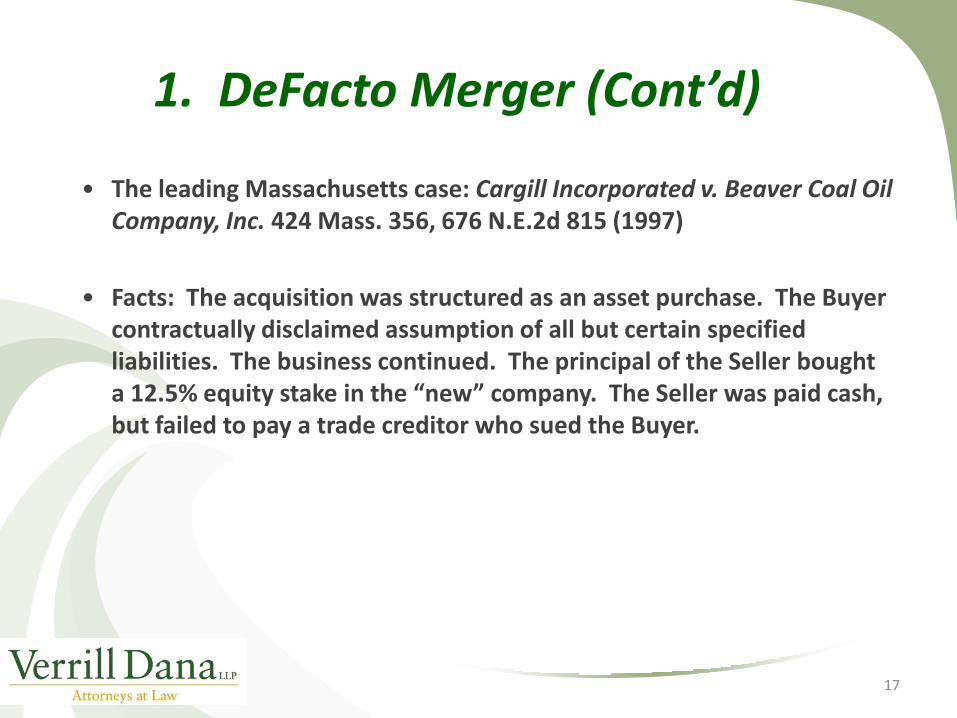

• The leading Massachusetts case: Cargill Incorporated v. Beaver Coal Oil Company, Inc. 424 Mass. 356, 676 N.E.2d 815 (1997)

• Facts: The acquisition was structured as an asset purchase. The Buyer contractually disclaimed assumption of all but certain specified liabilities. The business continued. The principal of the Seller bought a 12.5% equity stake in the “new” company. The Seller was paid cash, but failed to pay a trade creditor who sued the Buyer.

17

1. DeFacto Merger (Cont’d)

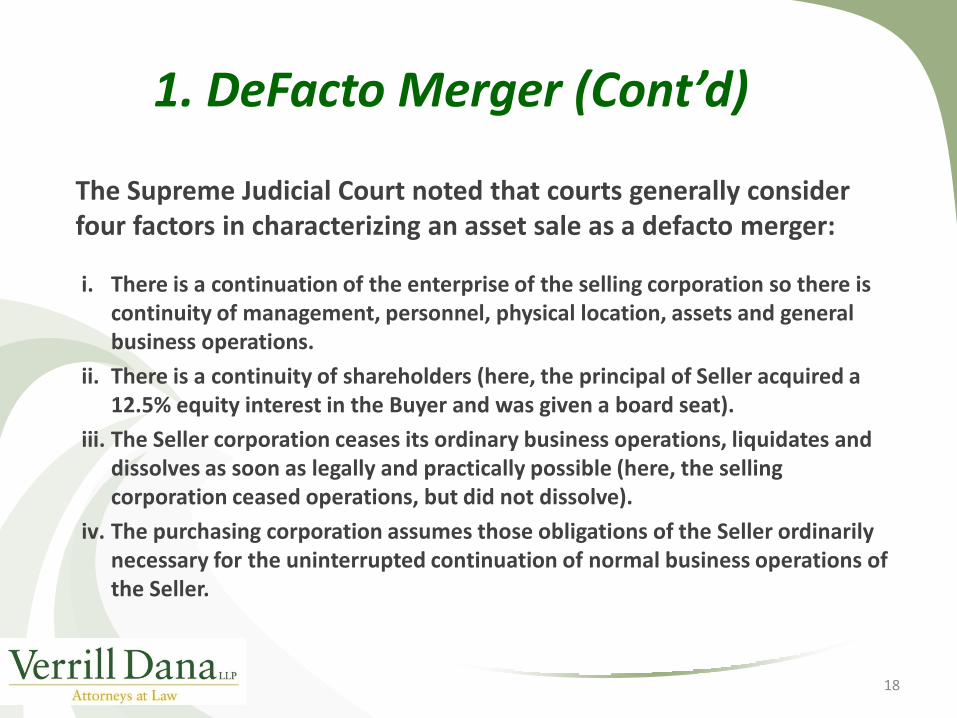

The Supreme Judicial Court noted that courts generally consider four factors in characterizing an asset sale as a defacto merger:

i. There is a continuation of the enterprise of the selling corporation so there is continuity of management, personnel, physical location, assets and general business operations.

ii. There is a continuity of shareholders (here, the principal of Seller acquired a 12.5% equity interest in the Buyer and was given a board seat).

iii. The Seller corporation ceases its ordinary business operations, liquidates and dissolves as soon as legally and practically possible (here, the selling corporation ceased operations, but did not dissolve).

iv. The purchasing corporation assumes those obligations of the Seller ordinarily necessary for the uninterrupted continuation of normal business operations of the Seller.

18

1. DeFacto Merger (Cont’d)

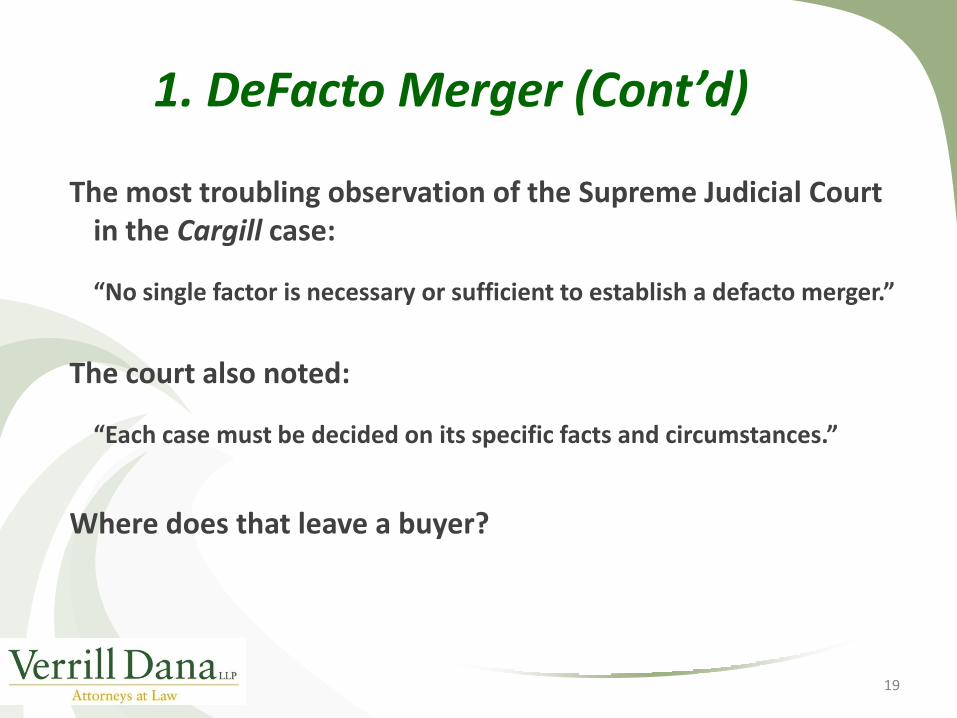

The most troubling observation of the Supreme Judicial Court in the Cargill case:

“No single factor is necessary or sufficient to establish a defacto merger.”

The court also noted:

“Each case must be decided on its specific facts and circumstances.”

Where does that leave a buyer?

19

1. DeFacto Merger (Cont’d)

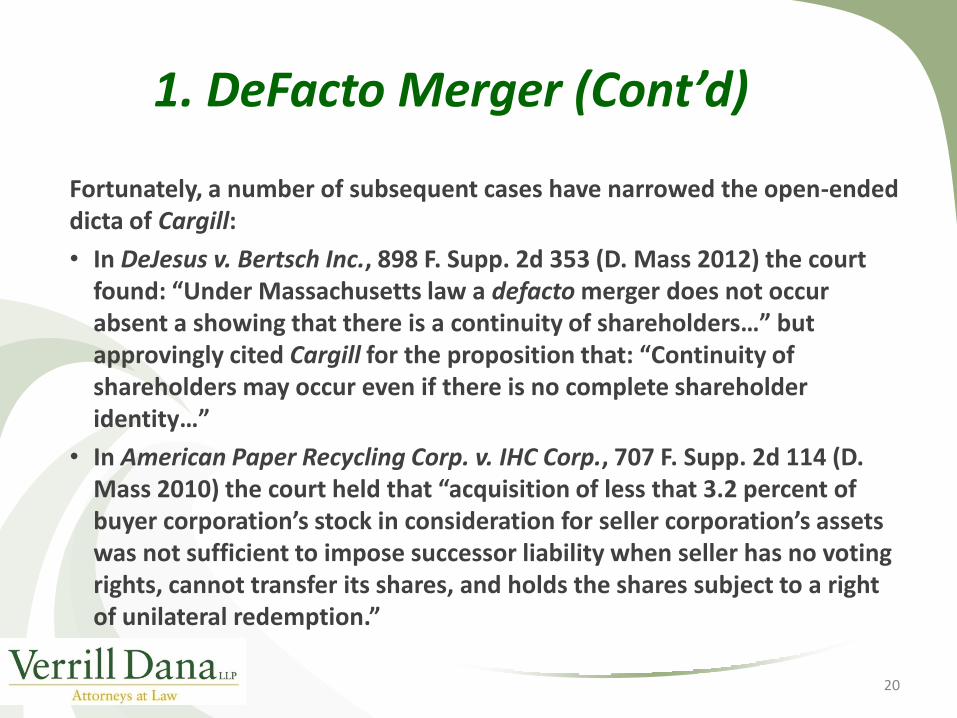

Fortunately, a number of subsequent cases have narrowed the open-ended dicta of Cargill:

• In DeJesus v. Bertsch Inc., 898 F. Supp. 2d 353 (D. Mass 2012) the court found: “Under Massachusetts law a defacto merger does not occur absent a showing that there is a continuity of shareholders…” but approvingly cited Cargill for the proposition that: “Continuity of shareholders may occur even if there is no complete shareholder identity…”

• In American Paper Recycling Corp. v. IHC Corp., 707 F. Supp. 2d 114 (D. Mass 2010) the court held that “acquisition of less that 3.2 percent of buyer corporation’s stock in consideration for seller corporation’s assets was not sufficient to impose successor liability when seller has no voting rights, cannot transfer its shares, and holds the shares subject to a right of unilateral redemption.”

20

2. Mere Continuation Morphs Into Continuation of Enterprise

• This doctrine was initially limited to instances where Newco was merely an alter ego of Oldco and where there was substantial identity between the stockholders, directors and officers of seller and buyer.

• Courts then found other principal factors:

i. Continuity of operations and the outward appearance of the enterprise

ii. The prompt dissolution of the predecessor following the asset transfer

iii. Assumption of liabilities and obligations necessary to operate the business

• However, in Turner v. Bituminous Casualty Co., 397 Mich 406, 244 N.W.2d 873 (1976) the Michigan Supreme Court found the continuing stockholder requirement unnecessary for a tort claimant.

21

3. Product Line Doctrine

• This doctrine was enunciated by the California Supreme Court in Ray v. Alad Corp., 560 P.2d 3 (Cal. 1977) where the court found: – “A party which acquires a manufacturing business and continues the output

of its line of products under the circumstances here presented assumed strict tort liability for defects in units of the same product line previously manufactured and distributed by the entity from which the business was acquired”.

– The basis for this doctrine is that a customer injured by a defective product would otherwise have no effective remedy.

– The focus is on the defective product and the tort claimant, not deal structure or corporate considerations.

– The product-line exception is a minority rule, but it is of concern if the Buyer (or the injured plaintiff) is in a jurisdiction that recognizes the doctrine.

22

4. Fraudulent Transfers

• Uniform Fraudulent Transfer Act – A transfer is voidable by a creditor if (i) the transfer is made with the actual intent to hinder, delay or defraud a creditor, or (ii) the transfer leaves the debtor insolvent or undercapitalized, and it is not made for reasonably equivalent value.

• Defusing the landmine: – Seller solvency representation – somewhat helpful but not definitive

– Seller solvency certificate – again, somewhat helpful

– Solvency opinion – difficult to obtain, expensive

– Fairness opinion – expensive

– Shopped deal – best evidence of reasonably equivalent value

23

B. Liability Imposed By Statute

Some Federal and State Laws Impose Liabilities that Follow the Acquired Assets:

• Environmental Statutes

• Bulk Transfer Laws

• Labor Liabilities

• Pension-ERISA Liabilities

24

1. Environmental Liabilities

• Federally Imposed (CERCLA): Successor owners may be liable for the cost of cleanup for previous owners’ contamination.

• Exceptions may apply (SBLRBRA): Congress created certain Bona Fide Prospective Purchasers exception to liability; also “innocent purchasers” (but with obligations attached).

• States also impose liability: Many state statutes follow the federal model.

25

1. Environmental Liabilities

To receive the liability protection under CERCLA, commonly known as Superfund, a BFPP must perform

"all appropriate inquiries" prior to acquiring the property, and demonstrate "no affiliation" with a liable party.

This typically means conducting a Phase I environmental assessment that meets federal requirements for “All Appropriate Inquiry.”

26

1. Environmental Liabilities

A BFPP must have purchased the property after January 11, 2002, and satisfy the following obligations:

• compliance with land use restrictions and not impeding the effectiveness or integrity of institutional controls, i.e., not contributing to contamination at any time, stop continuing discharges, and prevent threatened discharges;

• taking “reasonable steps” with respect to hazardous substances affecting a landowner’s property such as installing fences;

27

1. Environmental Liablities

• providing cooperation, assistance and access to those cleaning up the property; and

• complying with information requests and administrative subpoenas.

If the federal government is involved with clean-up at the site, the United States may have a "windfall lien" on a BFPP’s property where an EPA response action increased the fair market value of the property. The amount sought as a windfall lien shall be the lesser of the unrecovered response costs or the increase in fair market value at the property attributable to the Superfund cleanup.

28

2. Bulk Sales Laws

• Most states have eliminated bulk sales laws. Some, however, still have them.

• Confirm that the applicable state no longer has a bulk sales law, or comply with it.

29

IV. DRAFTING TECHNIQUES TO MINIMIZE RISK OF

SUCCESSOR LIABILITY

Specifically and narrowly defined “assumed liabilities” and broadly defined

“excluded liabilities”/liability disclaimers expressly rejecting any continuing

liabilities;

Solid indemnity and survival provisions; and

Obligations to back up the indemnity with trustworthy insurance or, even better,

escrowing a portion of the purchase price.

Other considerations:

Appropriate representations, warranties and covenants of seller (e.g., no

undisclosed liabilities, all consents obtained, good and marketable title/no liens,

solvency, litigation, no violation of law, labor and employment, environmental

matters, insurance policies, fairness opinion)

Deal insurance?

Specific tax matters provisions

Conditions to closing (e.g., require seller to provide clearance from tax authorities

certifying that seller has paid all taxes due)?

klgates.com 30

Leib Orlanski

10100 Santa Monica Blvd.

7th Floor

Los Angeles, CA 90067

310-552-5044

Craig Carpenter

Ingram Micro

klgates.com 31