Embed Size (px)

Citation preview

Autonomous Vehicles and InsuranceThe Technology, New Mobility Models and Potential Industry Impact

Trusted Choice Company Partner MeetingOctober 17, 2018Private and Confidential

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Agenda

2

Autonomous Vehicle Technology Update2

New Mobility Models: Islands of Autonomy3

Potential Impact on Insurance4

Introduction and Market Update1

Introduction and Market Update

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

In the Beginning . . .

Fall 2012 Summer 2015 Fall 2015 Summer 2017 Fall 2017

4

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 5

Changes in Transportation are Impacting Insurance

Source(s): Company websites, Reuters, TechCrunch and press releases

Zipcar is founded. By 2003, Zipcar reaches

5,000 users

1999 201620142009 2012 2013

Uber is founded. Google begins autonomous

vehicle project

2015

Lyft is founded. By 2013, Lyft was averaging

30,000 rides per week

2017

Google rebrands its self-driving car initiative as “Waymo”

Intel acquires Mobileye, an autonomous driving technology company. Nvidia partners with

Volvo on self-driving cars

Tesla releases Autopilot 2.0 self-driving vehicle

software

20112010

Tesla announces partnership with Direct

Line, a UK insurer

2018

BMW partners with Swiss Re to develop

vehicle-specific insurance ratings

Autonomous Vehicle Technology Update

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 7

Model Phases and Adoption Estimates

Phase 1 – Driver Assistance

Source(s): NHTSA, SAE

2018

Vehicle Make / Model

Sales by Specific ADAS

Adoption

Total Vehicle Sales broken

down by Phased

Adoption

Phase 2 – Partial Automation(Tesla Autopilot, Mercedes Drive Pilot, Cadillac Super Cruise, Etc…)

Rear Camera (RC)

Phase 3/4 – High Automation

2019 2020 2021 2022 2023 2024 - 2033

Rear Parking Sensors (RPS)Lane Detection Warning (LDW)

Blind Spot Detection (BSD)

Forward Collision Warning (FCW)

Adaptive Cruise Control (ACC)

Autonomy Description:

• Equivalent to SAE Level 1 Autonomy

• Vehicle is controlled by driver but features assist driver performance

• Similar to SAE Level 2 Autonomy• Vehicle has limited automated

functions; driver must be engaged

• Combination of SAE Level 3 and 4• Vehicle has full automated

functions; driver may override

Phase 5 – Full Automation• Equivalent to SAE Level 5• Vehicle has full automated functions

in all situations

Lane Keep Assist (LKA)Automatic Emergency Braking (AEB)

Cross Traffic Alert (CTA)

Active System

Passive System

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 8

AV Launch Timeline

2017: A8 with AI traffic jam pilot (SAE level 3) to handle traffic upto 37.3mph

2017: Self-driving features to be made available in new E-Class

2018: Launch of fully AV in the Phoenix area in partnership with FCA

2021: Partnered with Bosch to develop fully AV and launch a driverless taxi service

2024: Announced in 2014 that JLR was 10 yrs from a fully AV

2017: Launch 2018 Cadillac CT6 with Super Cruise

2020: Next gen of Leaf to have autonomous features

2020: Lexus to self-drive on highways,RoboTaxi for Olympics

2021: Plans to introduce self driving car in its i Next series

2021: Plans to mass produce AVs and partner with ride sharing companies

2020: Expected launch year of Google’s self-driving car

20202017-19 2021-302015-16

Fully autonomous models

Semi-autonomous models

Key:

2015: Tesla Auto Pilot available

2030: Investing $1.7b to launch AV on highways (2020) and in city streets (2030)

2019-21: Partnered with Uber to provide 24,000 XC90 SUV with AV technology

2021: Expects to launch full AV for commercial ride sharing

2016: Uber begins pilot of self-driving vehicle in Pittsburgh

2016: NuTonomy begins pilot of self-driving vehicle in Singapore

2020: Expected launch of level 4 Audi’s self-driving car

2019: Plan to launch car with full self-driving capabilities

2020: Launch of fully AV fleet commercially to compete with Uber and Lyft

2021: Plans to launch fully AVs (the Sedric) electric cars, vans, and trucks

Source(s): CB Insights, The WSJ, Autonews.com, Topgear.com, Driverlessfuture.com, Business Insider, Wired, The Guardian, Slashgear, Drive, Huffington Post, Motoring.com, The Verge, IEEE, CNBC

Company announcements to date indicate that autonomous vehicles are being developed aggressively with plans to launch post-2020

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 9

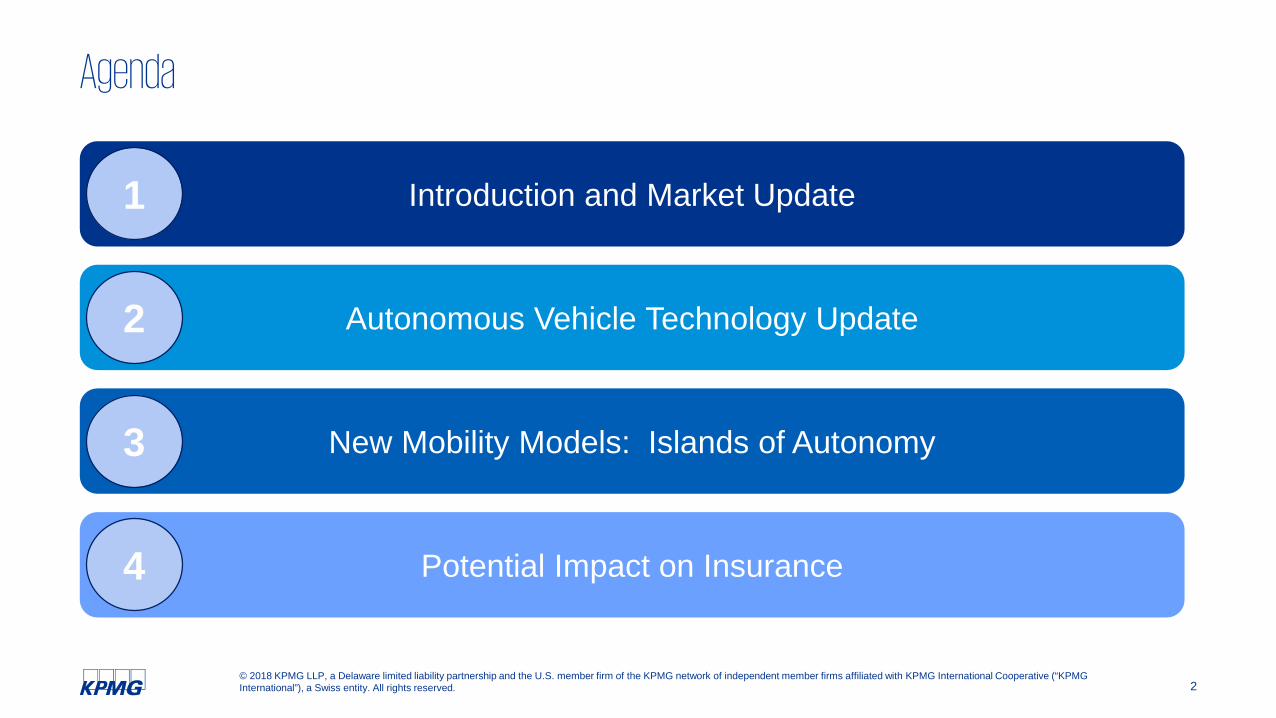

Loss Effects of Autonomy Already HappeningAutonomy is making vehicles safer, with results being realized today. Crash avoidance features which underpin self-driving technology are already improving the safety profile of vehicles

Note: (1) IIHS Study analyzes police-reported rear-end crashes in 22 states during 2010-2014 involving Acura, Honda, Mercedes-Benz, Subaru and Volvo vehicles with forward collision warning (“warning”) and autonomous emergency breaking (“autobrake”) vs. the same models without the optional technology; (2) ‘City Safety’ represents Volvo’s low-speed autobrake system. The test was conducted by comparing two Volvo models with City Safety vs. other vehicles without front crash prevention technology Source: IIHS’s research papers ‘Effectiveness of Forward Collision Warning Systems with and without Autonomous Emergency Braking in Reducing Police-Reported Crash Rates’ and ‘Effectiveness of Volvo’s City Safety Low-Speed Autonomous Emergency Braking System in Reducing Police-Reported Crash Rates’ and IIHS’s Status Report, Vol. 51, No.1, January 2016

According to recent IIHS findings, more than 700,000 police-reported rear-end crashes(1) in 2013 could have been avoided if the vehicles were equipped with auto break technology.

23%

39%41%

6%

42%

47%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Warning Only Warning Plus Autobrake City Safety

All Rear-end Strikes Rear-end Strikes with Injuries

Perc

ent D

ecre

ase

Vehicles With Front Crash Prevention Technology(1,2)

New Mobility Models: Islands of Autonomy

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The Trillion Dollar Question – When are Autonomous Vehicles Coming?

11

Knowing when is important . . .

. . . but so is where.

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

What are Islands of Autonomy?

12

“Cities with distinct metropolitan centers economically and socially linked to surrounding areas”

High density of ridersFrequent vehicle

observations of the streets

Source: Information in “New Mobility Models: Islands of Autonomy” is from KPMG LLP’s 2017 white paper, “Islands of Autonomy”

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Islands of Autonomy . . . a New Transportation Ecosystem

New transportation market(s) 150-plus island markets

Potential (massive) decline in sedan salesThe islands will transform the car market, most heavily impacting the sedan class. Self-driving vehicles and mobility services provide options that have significant potential to reduce consumer desire to own cars, particularly sedans

Trip mission focusNo one-size-fits-all vehicle – each island will need a unique mix of vehicles to meet consumer needs

13

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Chicago – A Half-Sun

14

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Atlanta – A Star

15

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

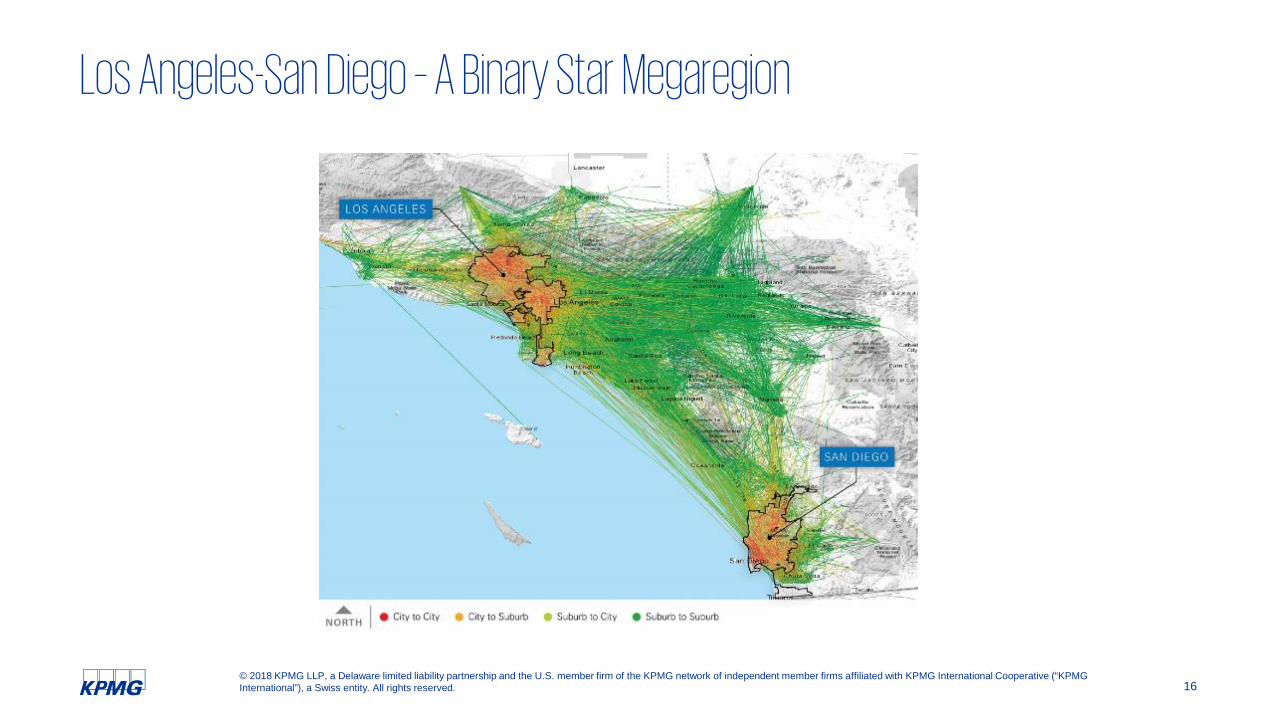

Los Angeles-San Diego – A Binary Star Megaregion

16

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Different Islands . . . Distinct Transportation Requirements

17

Chicago“A half-sun”

Atlanta“A star”

Los Angeles-San Diego“A binary star megaregion”

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 18

AV-MaaS and Potential Vehicle Sales Impact

Potential Impact on Insurance

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The ‘Chaotic Middle’ BeginsWe anticipate a ‘chaotic middle’ over the next 5-10 years, during which business models and the competitive landscape are transformed

New technologies and application

Decline in accident loss frequency

Risk shift

Asymmetric info

New ownership models

New entrants and competitor actions

Regulatory requirements and mandates

Adop

tion

of A

uton

omy

Time

C h A o T I c M I D d L e

Use

of M

obili

ty o

n D

eman

d

20

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Accident Frequency Could Fall DramaticallyThe KPMG Actuarial Team estimates by 2050 a potential reduction in accident frequency of almost 90% through additive benefits from technology improvements and car stock conversion

Source: KPMG LLP – “The Chaotic Middle: Autonomous Vehicles and Disruption in Automobile Insurance” – June 2017

Updated Baseline Scenario - Accident Frequency Projection

-

0.010

0.020

0.030

0.040

0.050Av

erag

e In

cide

nts

Per V

ehic

le

21

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Cost of Future Accidents is UncertainThe severity of future accidents has several competing factors at play affecting the cost of the claim. While increased severity appears to be winning the current “battle” with frequency benefits due to improved safety technology, many market participants believe that over time there will be a 'tipping point' where costs plateau and eventually drop

Source: KPMG LLP – “The Chaotic Middle: Autonomous Vehicles and Disruption in Automobile Insurance” – June 2017

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Cos

t Per

Acc

iden

t ($)

$39,424

Automated driving benefits (faster reaction time)

Expensive components

Inexpensive transportation pods and parts

Inflation and marginal expense increases

$15,723

‘Tipping point’ with autonomous car stock

Updated Baseline Scenario - Accident Severity

22

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

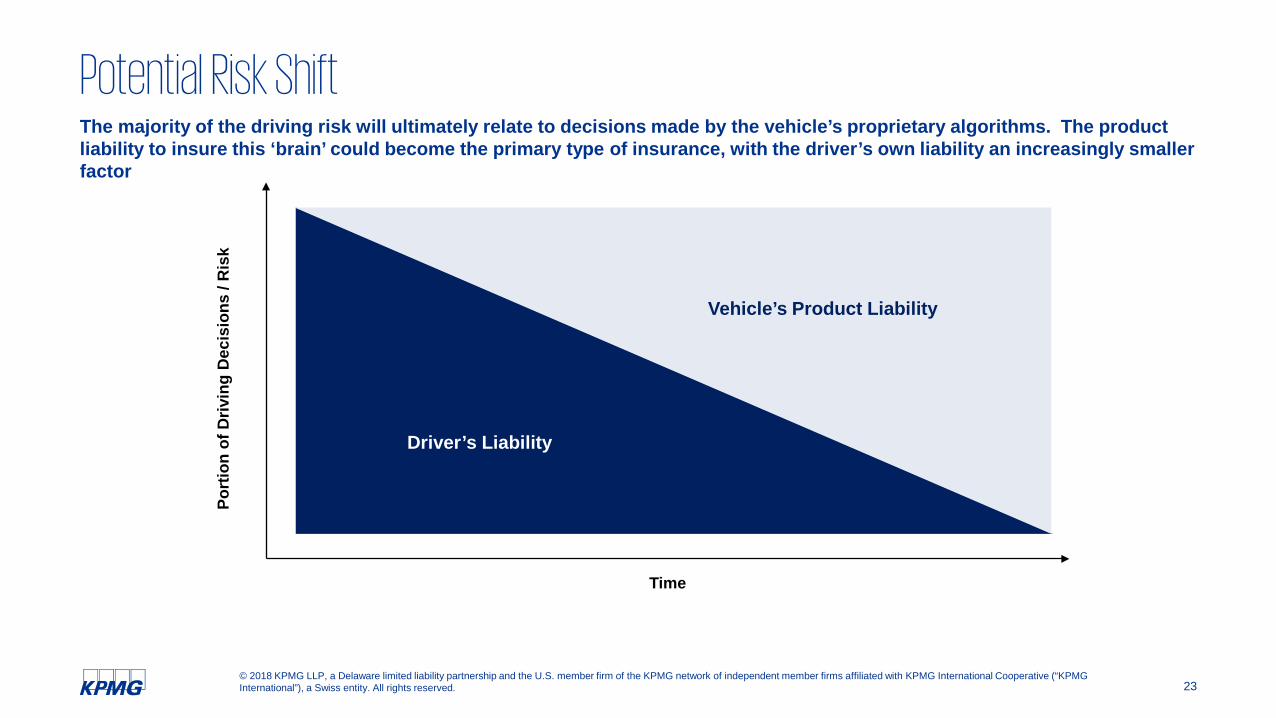

Potential Risk ShiftThe majority of the driving risk will ultimately relate to decisions made by the vehicle’s proprietary algorithms. The product liability to insure this ‘brain’ could become the primary type of insurance, with the driver’s own liability an increasingly smaller factor

Port

ion

of D

rivin

g D

ecis

ions

/ R

isk

Driver’s Liability

Vehicle’s Product Liability

Time

23

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

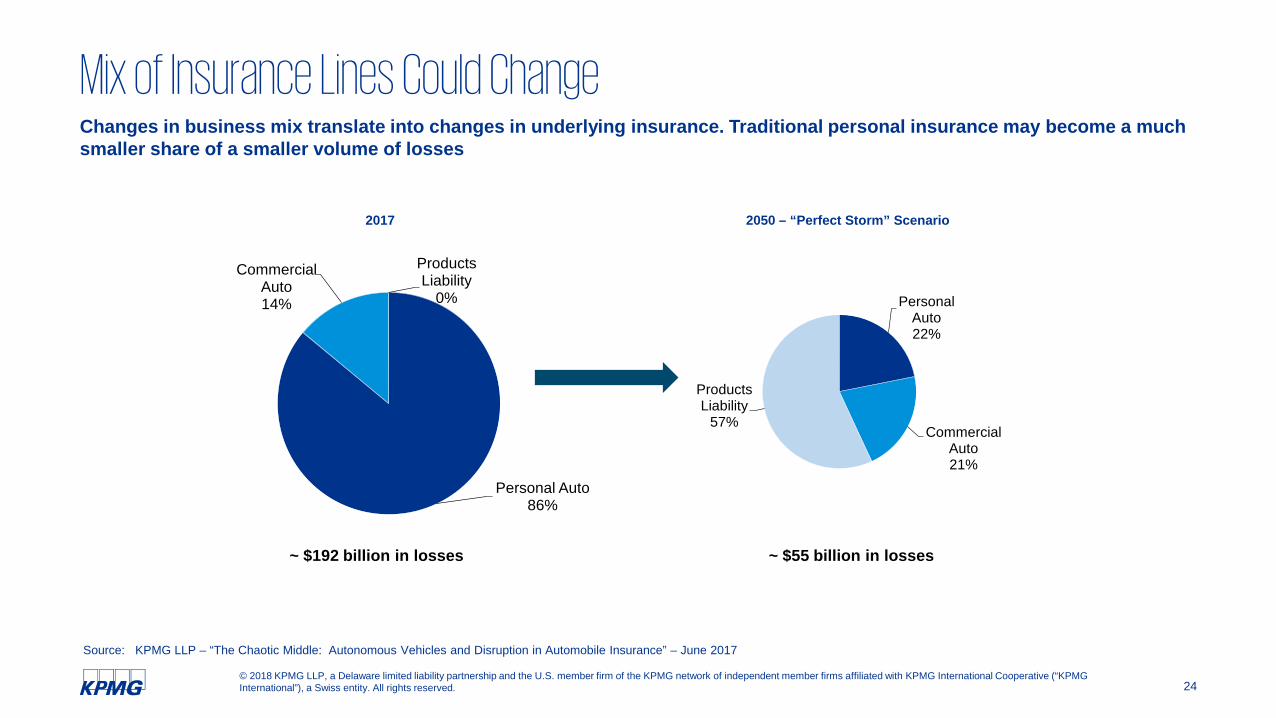

Mix of Insurance Lines Could ChangeChanges in business mix translate into changes in underlying insurance. Traditional personal insurance may become a much smaller share of a smaller volume of losses

24

Personal Auto86%

Commercial Auto14%

Products Liability

0%

~ $192 billion in losses

2017 2050 – “Perfect Storm” Scenario

~ $55 billion in losses

Personal Auto22%

Commercial Auto21%

Products Liability

57%

Source: KPMG LLP – “The Chaotic Middle: Autonomous Vehicles and Disruption in Automobile Insurance” – June 2017

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 25

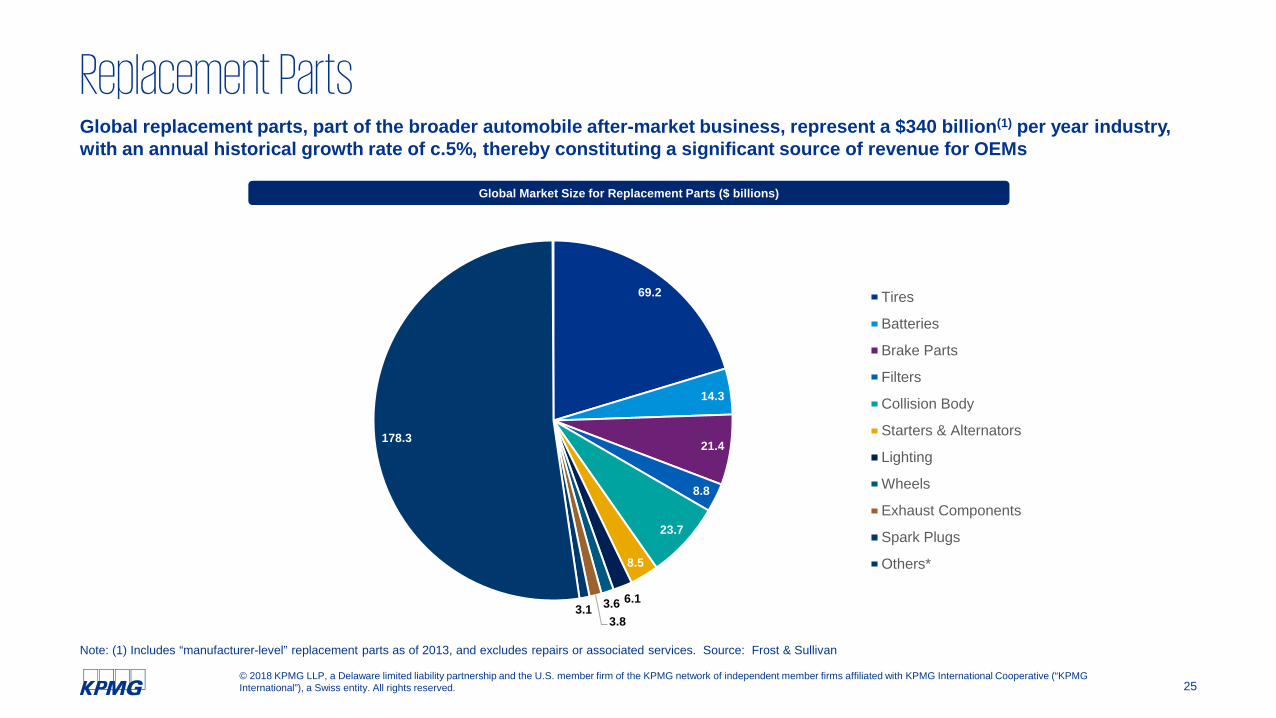

Note: (1) Includes “manufacturer-level” replacement parts as of 2013, and excludes repairs or associated services. Source: Frost & Sullivan

69.2

14.3

21.4

8.8

23.7

8.5

6.13.63.8

3.1

178.3

Tires

Batteries

Brake Parts

Filters

Collision Body

Starters & Alternators

Lighting

Wheels

Exhaust Components

Spark Plugs

Others*

Global Market Size for Replacement Parts ($ billions)

Replacement PartsGlobal replacement parts, part of the broader automobile after-market business, represent a $340 billion(1) per year industry, with an annual historical growth rate of c.5%, thereby constituting a significant source of revenue for OEMs

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26

Note: (1) Does not contemplate fully autonomous vehicles; and (2) Property damage losses are estimates and are based on KPMG LLP’s Updated Baseline Scenario. Source: KPMG LLP actuarial analysis

2017 – Total Estimated PD Losses(2)

2050 Potential PD Losses – Status Quo(1)

2050 Potential PD Losses –Autonomous Vehicles Proliferation(2)

$117.7 B

$230.8 B

$38.8 B

96% increase

67% decrease

Parts Business at RiskThe frequency and severity trends directly impact demand for parts related to accidents and the property damage (“PD”) arising from them

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 27

Entity Scenario A Scenario B Scenario C Scenario D

Provide driving and vehicle data to insurers

Become distributor of insurance for a selected set of carriers

Act as an insurance company with many functions outsourced

Become a fully integrated insurance company

Strategic Angle Telemetry data Brand, customerconnectivity Product advantage Product advantage

Revenue Model Licensing fees Commissions Underwriting profit and investment income

Underwriting profit and investment income

License data from OEMsto underwrite policies

Form alliances with OEMs

Serve as third-party administrators - for example, current insurers could process the claims of the OEMs

Transform business model to compete with new entrants

Expand into new products and services

OEM

sIn

sure

rIllustrative Future State Business Models

An OEM’s potential (re)entrance into insurance could take a variety of forms that could evolve to match changes in its core business. There is flexibility to shift business models over time to reflect changes in the marketplace and scale of the autonomous operations / fleet

Insurance Offers Several Business Plays

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 28

Illustrative Process of Buying Automotive Insurance (Personal Lines)

Today

Customer Relationship

Flow of Driving Data

Customer

OEM (Vehicle Manufacturer and

Insurance Company)

The Future

Customer Digital / Agent

OEM (Vehicle Manufacturer)

Driving Data

Insurance Company

Insurance Company

Driving Data

Ultimately, OEMs have the potential to not only control the data, but also the customer relationship, thereby dramatically altering the traditional auto insurance model

Potential Customer Relationship Implications

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

KPMG Contact

NameTitle

OfficeEmail

Joe SchneiderManaging Director, Corporate FinanceCo-Lead – KPMG Autonomous Vehicles and Insurance Task Force

+ 1 312 665 [email protected]

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The information contained in this publication does not constitute a recommendation, offer, or solicitation to buy, sell or hold any security of any issuer. Past performance does not guarantee future results.

Some or all of the services described herein may not be permissible for KPMG audit clients and their affiliates.

The views and opinions expressed herein are those of the speakers and do not necessarily represent the views and opinions of KPMG LLP or its affiliates. KPMG LLP does not necessarily endorse or recommend any commercial products, processes or services described.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

kpmg.com/socialmedia

![Autonomous vehicles[1]](https://img.pdfslide.us/doc/110x75/54bf07bb4a7959cb478b4592/autonomous-vehicles1.jpg)