Embed Size (px)

Citation preview

1© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

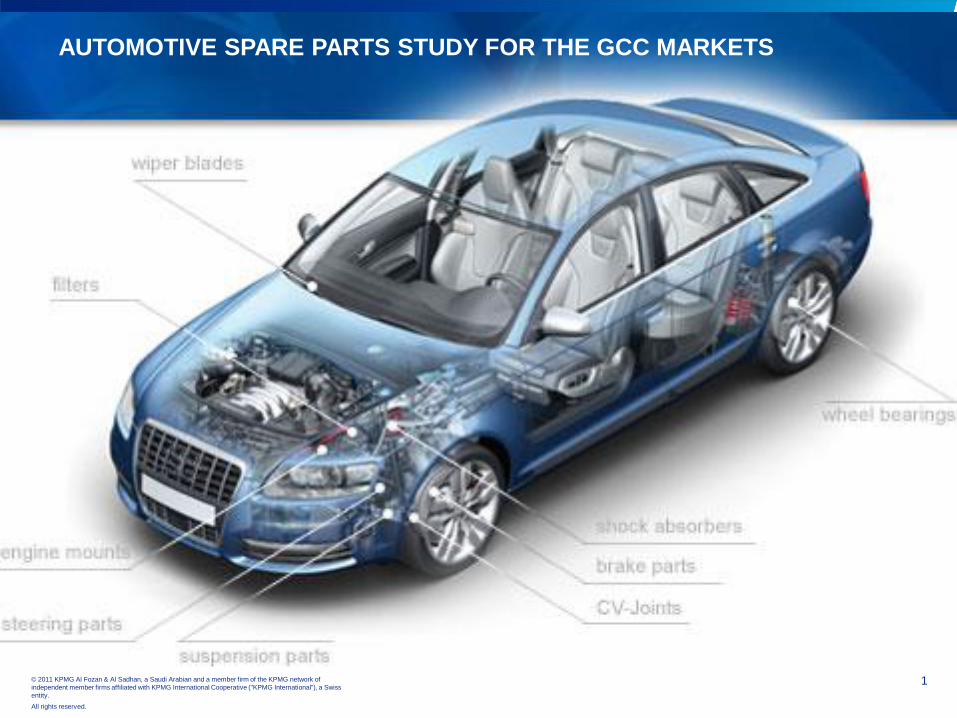

AUTOMOTIVE SPARE PARTS STUDY FOR THE GCC MARKETS

2© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

Kuwait

Oman

Qatar

United Arab Emirates Saudi Arabia

Bahrain

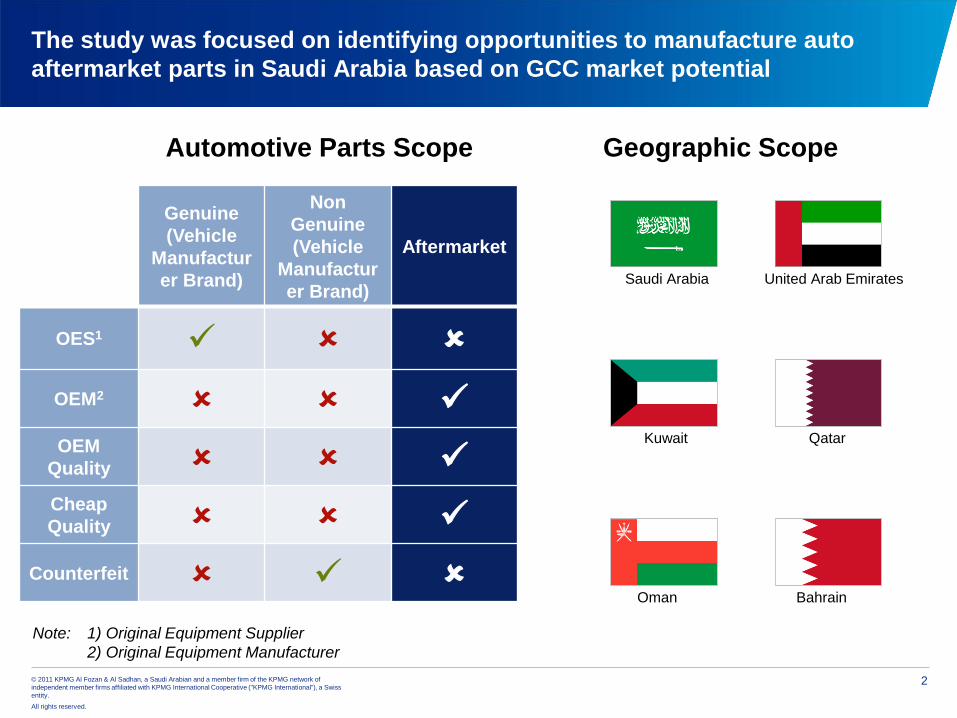

The study was focused on identifying opportunities to manufacture auto

aftermarket parts in Saudi Arabia based on GCC market potential

Genuine

(Vehicle

Manufactur

er Brand)

Non

Genuine

(Vehicle

Manufactur

er Brand)

Aftermarket

OES1

OEM2

OEM

Quality

Cheap

Quality

Counterfeit

Note: 1) Original Equipment Supplier

2) Original Equipment Manufacturer

Automotive Parts Scope Geographic Scope

3© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

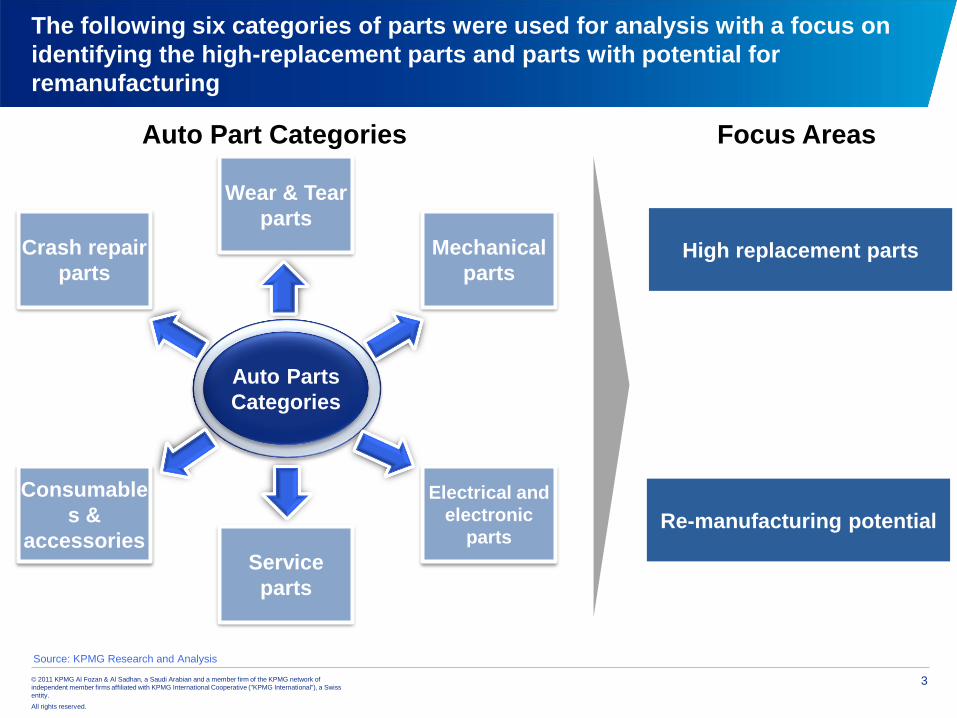

The following six categories of parts were used for analysis with a focus on

identifying the high-replacement parts and parts with potential for

remanufacturing

Auto Parts

Categories

Wear & Tear

parts

Mechanical

parts

Crash repair

parts

Consumable

s &

accessories

Electrical and

electronic

parts

Service

parts

Source: KPMG Research and Analysis

Auto Part Categories Focus Areas

High replacement parts

Re-manufacturing potential

4© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

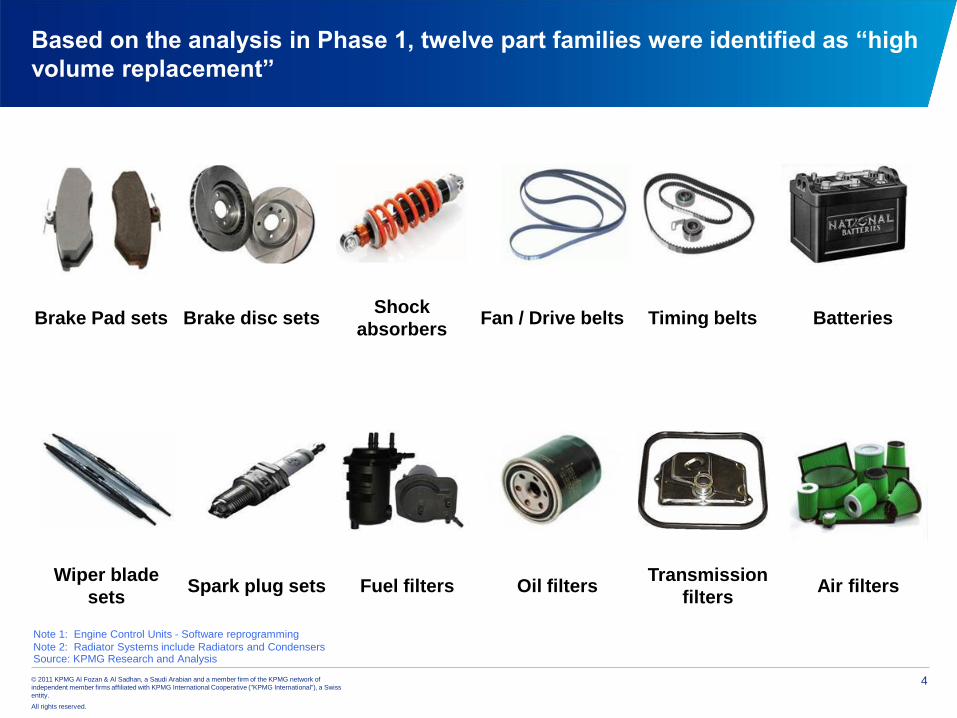

Based on the analysis in Phase 1, twelve part families were identified as “high

volume replacement”

Source: KPMG Research and Analysis

Note 1: Engine Control Units - Software reprogramming

Note 2: Radiator Systems include Radiators and Condensers

Brake Pad sets Brake disc sets Fan / Drive belts Timing belts BatteriesShock

absorbers

Wiper blade

setsSpark plug sets Oil filters

Transmission

filtersAir filtersFuel filters

5© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

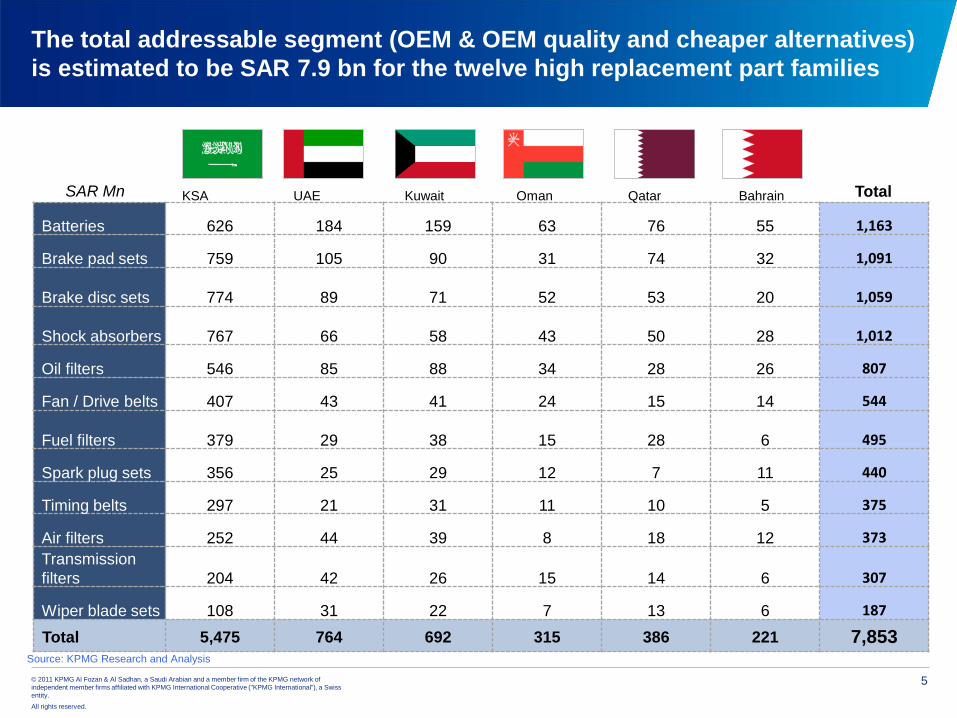

The total addressable segment (OEM & OEM quality and cheaper alternatives)

is estimated to be SAR 7.9 bn for the twelve high replacement part families

Batteries 626 184 159 63 76 55 1,163

Brake pad sets 759 105 90 31 74 32 1,091

Brake disc sets 774 89 71 52 53 20 1,059

Shock absorbers 767 66 58 43 50 28 1,012

Oil filters 546 85 88 34 28 26 807

Fan / Drive belts 407 43 41 24 15 14 544

Fuel filters 379 29 38 15 28 6 495

Spark plug sets 356 25 29 12 7 11 440

Timing belts 297 21 31 11 10 5 375

Air filters 252 44 39 8 18 12 373

Transmission

filters 204 42 26 15 14 6 307

Wiper blade sets 108 31 22 7 13 6 187

Total 5,475 764 692 315 386 221 7,853Source: KPMG Research and Analysis

Kuwait Bahrain Oman Qatar UAEKSASAR Mn Total

6© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

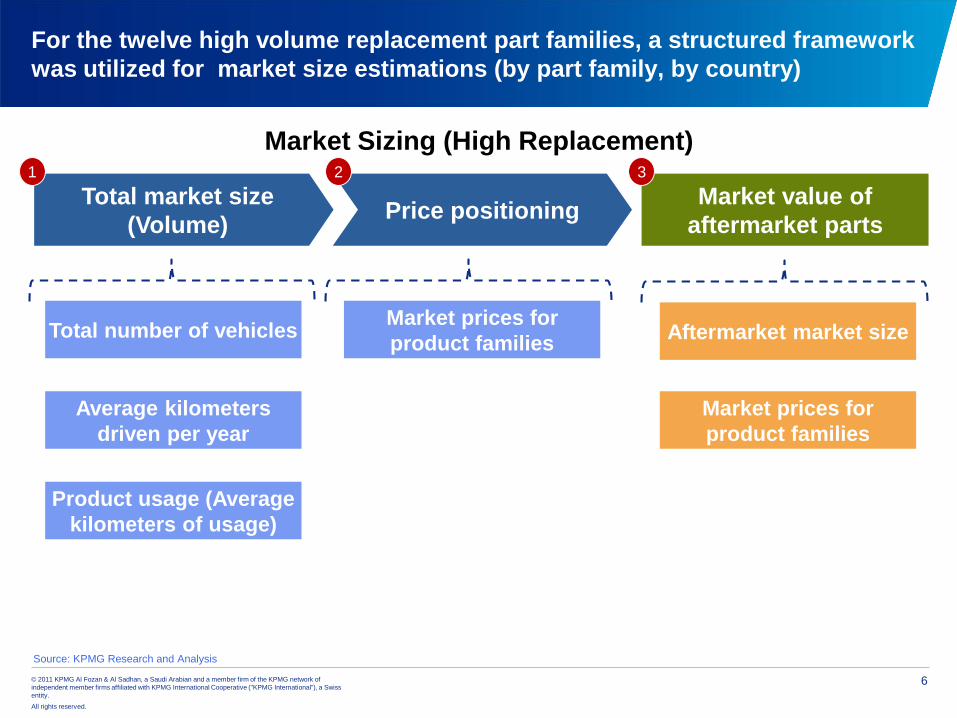

Market Sizing (High Replacement)

Total number of vehicles

Product usage (Average

kilometers of usage)

Average kilometers

driven per year

Market prices for

product families

For the twelve high volume replacement part families, a structured framework

was utilized for market size estimations (by part family, by country)

Price positioningTotal market size

(Volume)

Market value of

aftermarket parts

Source: KPMG Research and Analysis

1 2

Aftermarket market size

Market prices for

product families

3

7© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

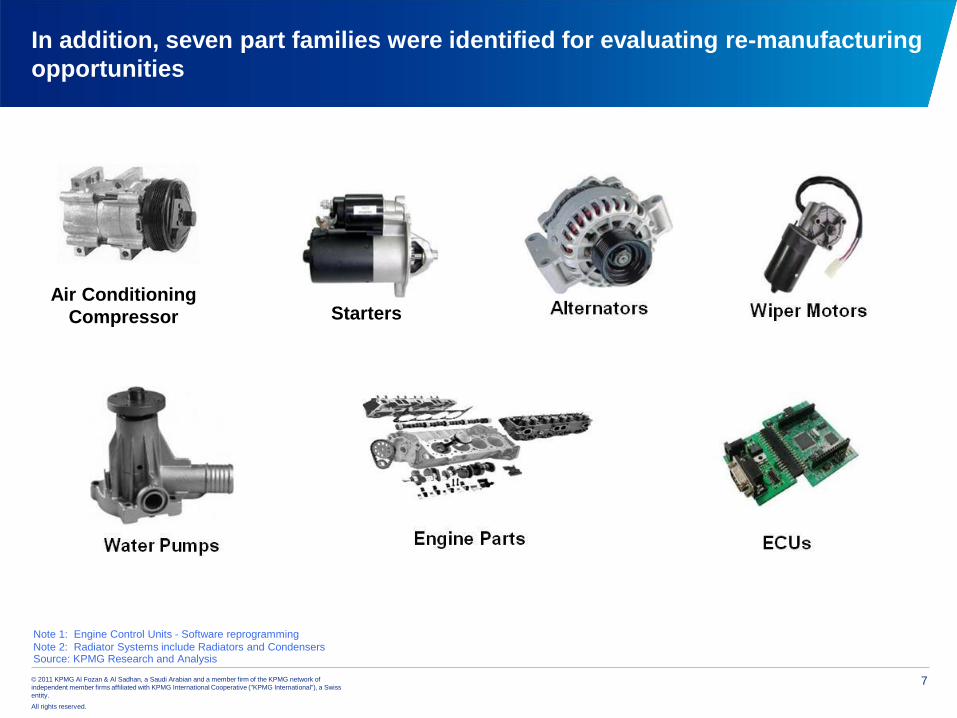

In addition, seven part families were identified for evaluating re-manufacturing

opportunities

Source: KPMG Research and Analysis

Note 1: Engine Control Units - Software reprogramming

Note 2: Radiator Systems include Radiators and Condensers

Air Conditioning

Compressor Starters

8© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

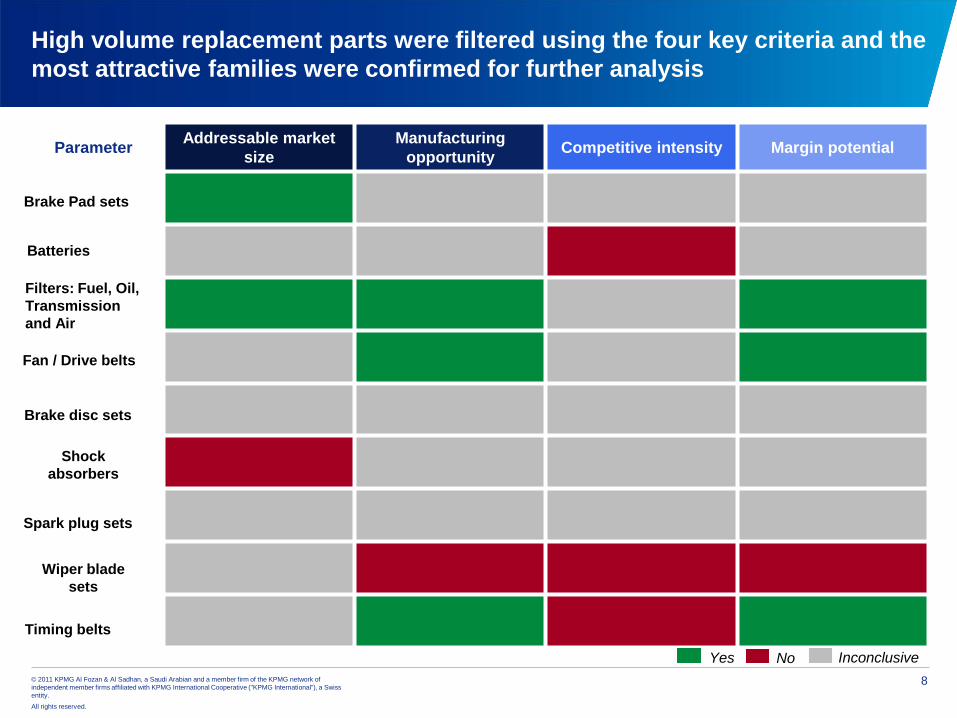

ParameterAddressable market

size

Manufacturing

opportunityCompetitive intensity Margin potential

Brake Pad sets

Batteries

Filters: Fuel, Oil,

Transmission

and Air

Fan / Drive belts

Brake disc sets

Shock

absorbers

Wiper blade

sets

Spark plug sets

Timing belts

High volume replacement parts were filtered using the four key criteria and the

most attractive families were confirmed for further analysis

Yes InconclusiveNo

9© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

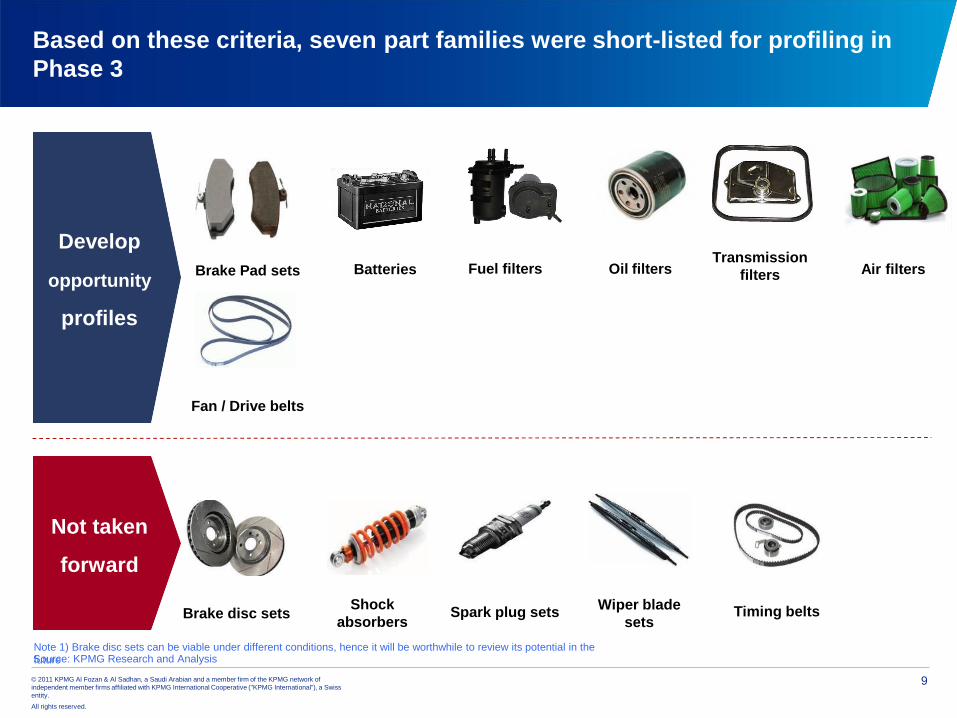

Based on these criteria, seven part families were short-listed for profiling in

Phase 3

Develop

opportunity

profiles

Not taken

forward

Brake Pad sets

Brake disc setsShock

absorbers

Fan / Drive belts

Batteries

Wiper blade

setsSpark plug sets

Fuel filters Oil filtersTransmission

filters Air filters

Timing belts

Note 1) Brake disc sets can be viable under different conditions, hence it will be worthwhile to review its potential in the

futureSource: KPMG Research and Analysis

10© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

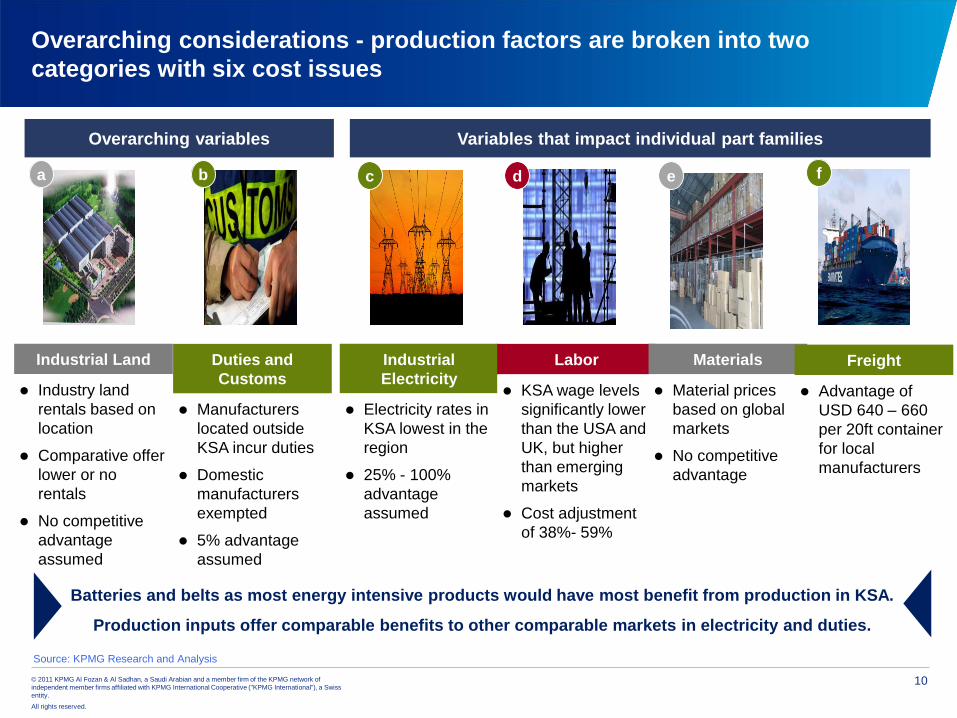

Overarching considerations - production factors are broken into two

categories with six cost issues

Overarching variables Variables that impact individual part families

fa b c d e

Source: KPMG Research and Analysis

Industrial Land

Industry land

rentals based on

location

Comparative offer

lower or no

rentals

No competitive

advantage

assumed

Duties and

Customs

Manufacturers

located outside

KSA incur duties

Domestic

manufacturers

exempted

5% advantage

assumed

Industrial

Electricity

Electricity rates in

KSA lowest in the

region

25% - 100%

advantage

assumed

Labor

KSA wage levels

significantly lower

than the USA and

UK, but higher

than emerging

markets

Cost adjustment

of 38%- 59%

Materials

Material prices

based on global

markets

No competitive

advantage

Freight

Advantage of

USD 640 – 660

per 20ft container

for local

manufacturers

Batteries and belts as most energy intensive products would have most benefit from production in KSA.

Production inputs offer comparable benefits to other comparable markets in electricity and duties.

11© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

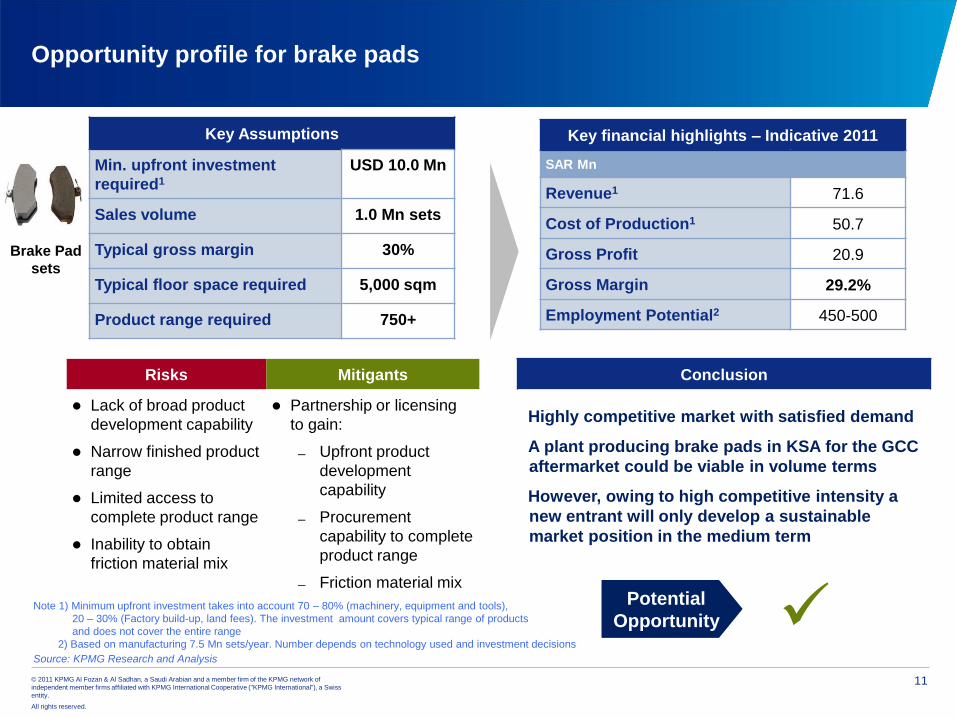

Opportunity profile for brake pads

Source: KPMG Research and Analysis

Risks Mitigants

Lack of broad product

development capability

Narrow finished product

range

Limited access to

complete product range

Inability to obtain

friction material mix

Partnership or licensing

to gain:

Upfront product

development

capability

Procurement

capability to complete

product range

Friction material mix

Key financial highlights – Indicative 2011

SAR Mn

Revenue1 71.6

Cost of Production1 50.7

Gross Profit 20.9

Gross Margin 29.2%

Employment Potential2 450-500

Key Assumptions

Min. upfront investment

required1

USD 10.0 Mn

Sales volume 1.0 Mn sets

Typical gross margin 30%

Typical floor space required 5,000 sqm

Product range required 750+

Conclusion

Highly competitive market with satisfied demand

A plant producing brake pads in KSA for the GCC

aftermarket could be viable in volume terms

However, owing to high competitive intensity a

new entrant will only develop a sustainable

market position in the medium term

Brake Pad

sets

Potential

Opportunity Note 1) Minimum upfront investment takes into account 70 – 80% (machinery, equipment and tools),

20 – 30% (Factory build-up, land fees). The investment amount covers typical range of products

and does not cover the entire range

2) Based on manufacturing 7.5 Mn sets/year. Number depends on technology used and investment decisions

12© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

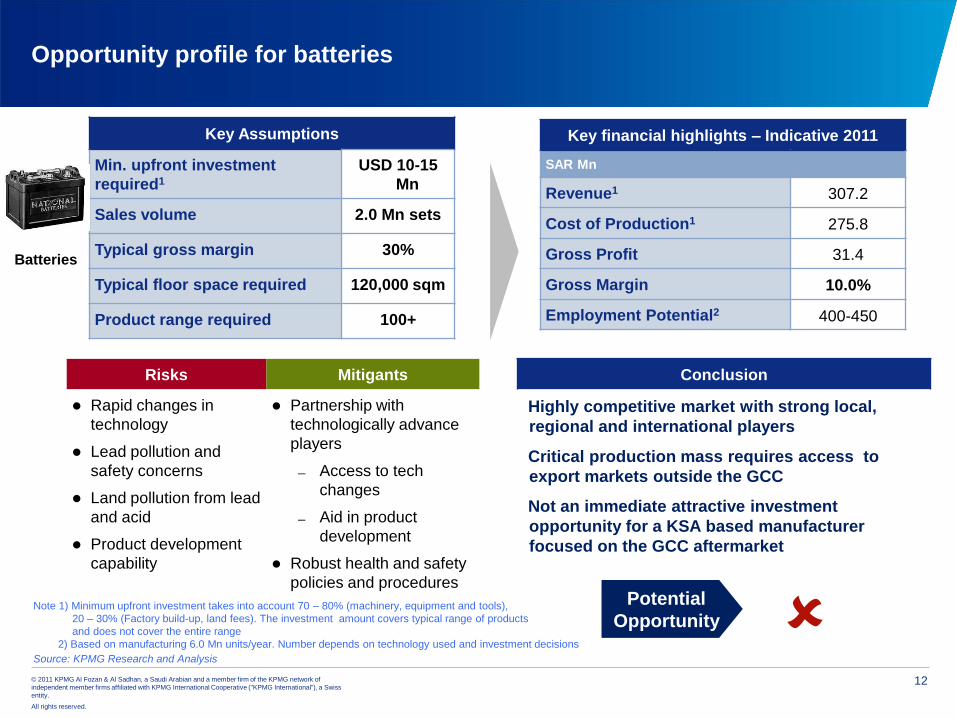

Opportunity profile for batteries

Source: KPMG Research and Analysis

Risks Mitigants

Rapid changes in

technology

Lead pollution and

safety concerns

Land pollution from lead

and acid

Product development

capability

Partnership with

technologically advance

players

Access to tech

changes

Aid in product

development

Robust health and safety

policies and procedures

Key financial highlights – Indicative 2011

SAR Mn

Revenue1 307.2

Cost of Production1 275.8

Gross Profit 31.4

Gross Margin 10.0%

Employment Potential2 400-450

Key Assumptions

Min. upfront investment

required1

USD 10-15

Mn

Sales volume 2.0 Mn sets

Typical gross margin 30%

Typical floor space required 120,000 sqm

Product range required 100+

Conclusion

Highly competitive market with strong local,

regional and international players

Critical production mass requires access to

export markets outside the GCC

Not an immediate attractive investment

opportunity for a KSA based manufacturer

focused on the GCC aftermarket

Batteries

Potential

Opportunity Note 1) Minimum upfront investment takes into account 70 – 80% (machinery, equipment and tools),

20 – 30% (Factory build-up, land fees). The investment amount covers typical range of products

and does not cover the entire range

2) Based on manufacturing 6.0 Mn units/year. Number depends on technology used and investment decisions

13© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

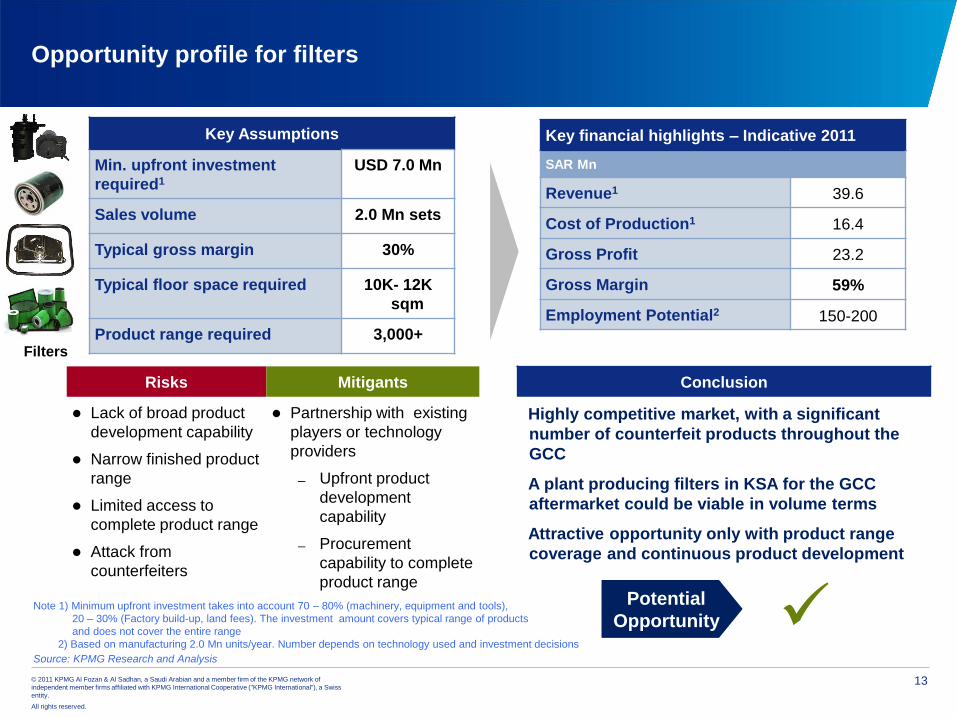

Opportunity profile for filters

Source: KPMG Research and Analysis

Risks Mitigants

Lack of broad product

development capability

Narrow finished product

range

Limited access to

complete product range

Attack from

counterfeiters

Partnership with existing

players or technology

providers

Upfront product

development

capability

Procurement

capability to complete

product range

Key financial highlights – Indicative 2011

SAR Mn

Revenue1 39.6

Cost of Production1 16.4

Gross Profit 23.2

Gross Margin 59%

Employment Potential2 150-200

Key Assumptions

Min. upfront investment

required1

USD 7.0 Mn

Sales volume 2.0 Mn sets

Typical gross margin 30%

Typical floor space required 10K- 12K

sqm

Product range required 3,000+

Conclusion

Highly competitive market, with a significant

number of counterfeit products throughout the

GCC

A plant producing filters in KSA for the GCC

aftermarket could be viable in volume terms

Attractive opportunity only with product range

coverage and continuous product development

Filters

Potential

Opportunity Note 1) Minimum upfront investment takes into account 70 – 80% (machinery, equipment and tools),

20 – 30% (Factory build-up, land fees). The investment amount covers typical range of products

and does not cover the entire range

2) Based on manufacturing 2.0 Mn units/year. Number depends on technology used and investment decisions

14© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

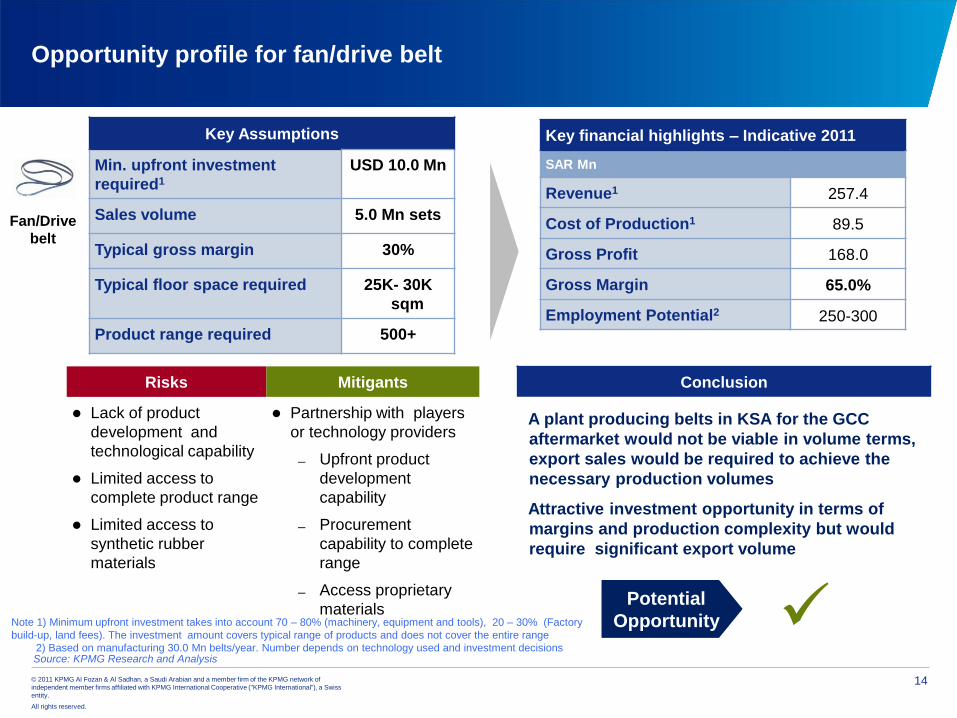

Opportunity profile for fan/drive belt

Source: KPMG Research and Analysis

Risks Mitigants

Lack of product

development and

technological capability

Limited access to

complete product range

Limited access to

synthetic rubber

materials

Partnership with players

or technology providers

Upfront product

development

capability

Procurement

capability to complete

range

Access proprietary

materials

Key financial highlights – Indicative 2011

SAR Mn

Revenue1 257.4

Cost of Production1 89.5

Gross Profit 168.0

Gross Margin 65.0%

Employment Potential2 250-300

Key Assumptions

Min. upfront investment

required1

USD 10.0 Mn

Sales volume 5.0 Mn sets

Typical gross margin 30%

Typical floor space required 25K- 30K

sqm

Product range required 500+

Conclusion

A plant producing belts in KSA for the GCC

aftermarket would not be viable in volume terms,

export sales would be required to achieve the

necessary production volumes

Attractive investment opportunity in terms of

margins and production complexity but would

require significant export volume

Fan/Drive

belt

Potential

Opportunity Note 1) Minimum upfront investment takes into account 70 – 80% (machinery, equipment and tools), 20 – 30% (Factory

build-up, land fees). The investment amount covers typical range of products and does not cover the entire range

2) Based on manufacturing 30.0 Mn belts/year. Number depends on technology used and investment decisions

15© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

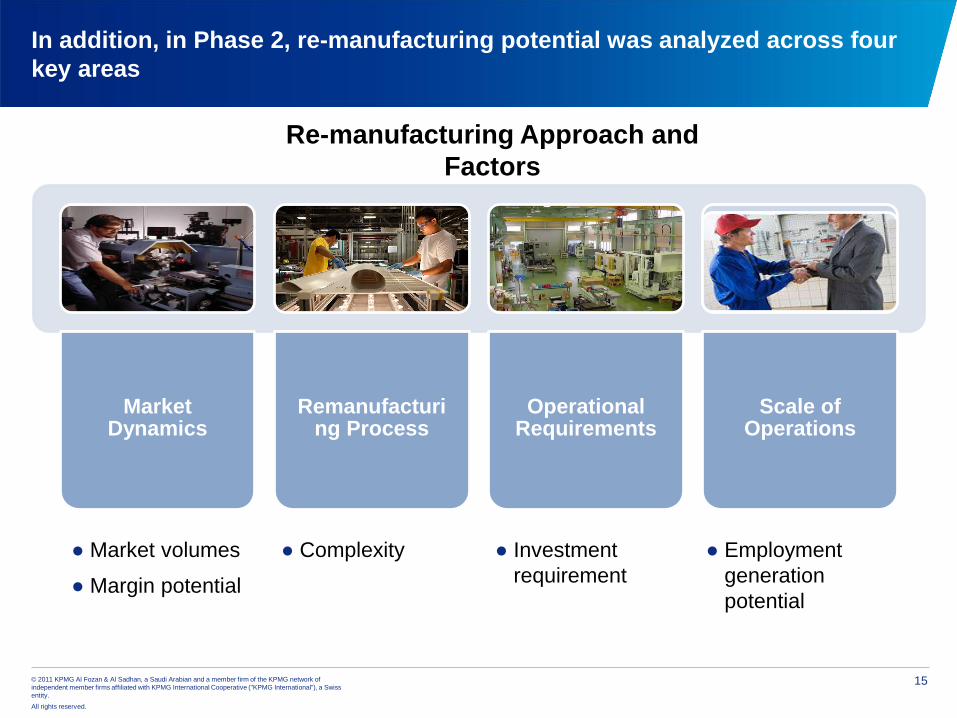

In addition, in Phase 2, re-manufacturing potential was analyzed across four

key areas

Re-manufacturing Approach and

Factors

Market Dynamics

Remanufacturing Process

Operational Requirements

Scale of Operations

● Market volumes

● Margin potential

● Complexity ● Investment

requirement

● Employment

generation

potential

16© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

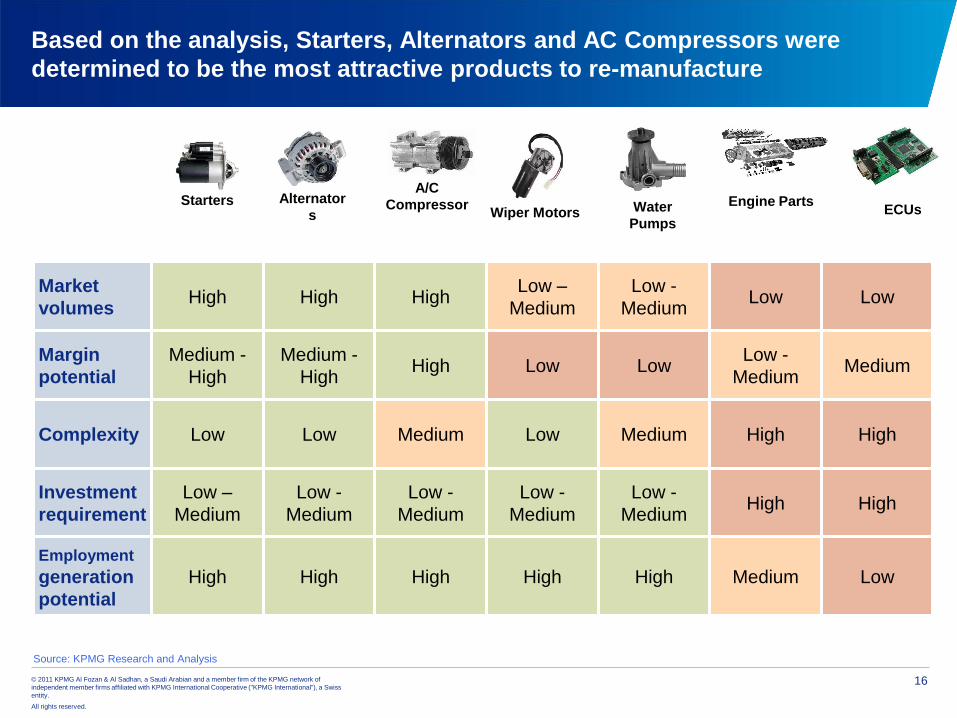

Based on the analysis, Starters, Alternators and AC Compressors were

determined to be the most attractive products to re-manufacture

Alternator

sWater

PumpsWiper Motors ECUs

Engine PartsA/C

CompressorStarters

Market

volumesHigh High High

Low –

Medium

Low -

MediumLow Low

Margin

potential

Medium -

High

Medium -

HighHigh Low Low

Low -

MediumMedium

Complexity Low Low Medium Low Medium High High

Investment

requirement

Low –

Medium

Low -

Medium

Low -

Medium

Low -

Medium

Low -

MediumHigh High

Employment

generation

potential

High High High High High Medium Low

Source: KPMG Research and Analysis

17© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

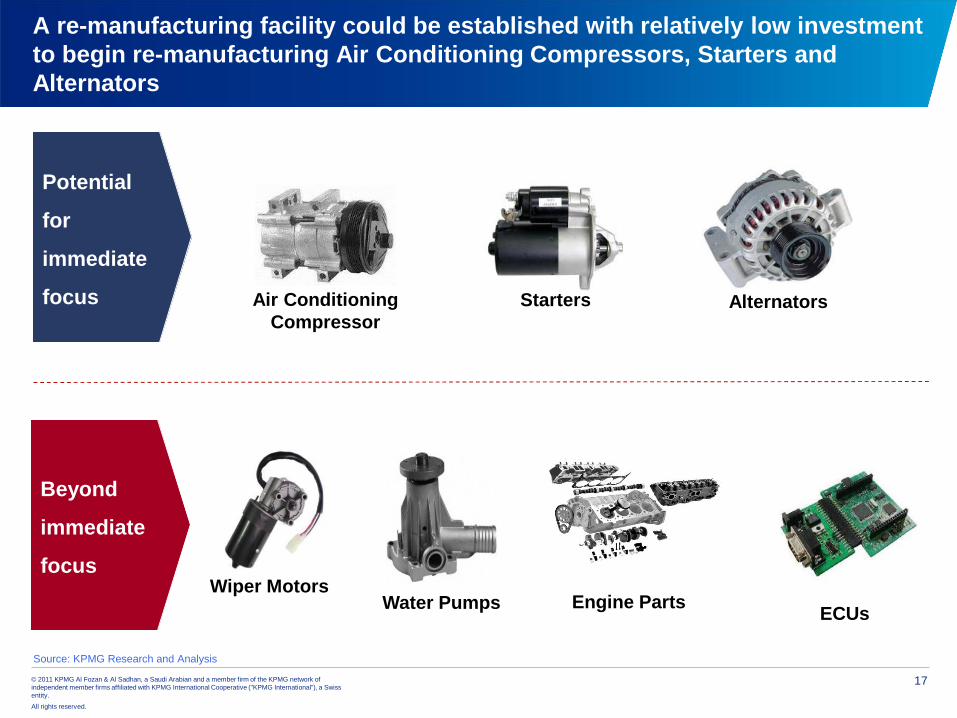

A re-manufacturing facility could be established with relatively low investment

to begin re-manufacturing Air Conditioning Compressors, Starters and

Alternators

Potential

for

immediate

focus

Beyond

immediate

focus

Alternators

Water PumpsWiper Motors

ECUsEngine Parts

Air Conditioning

Compressor

Starters

Source: KPMG Research and Analysis

18© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

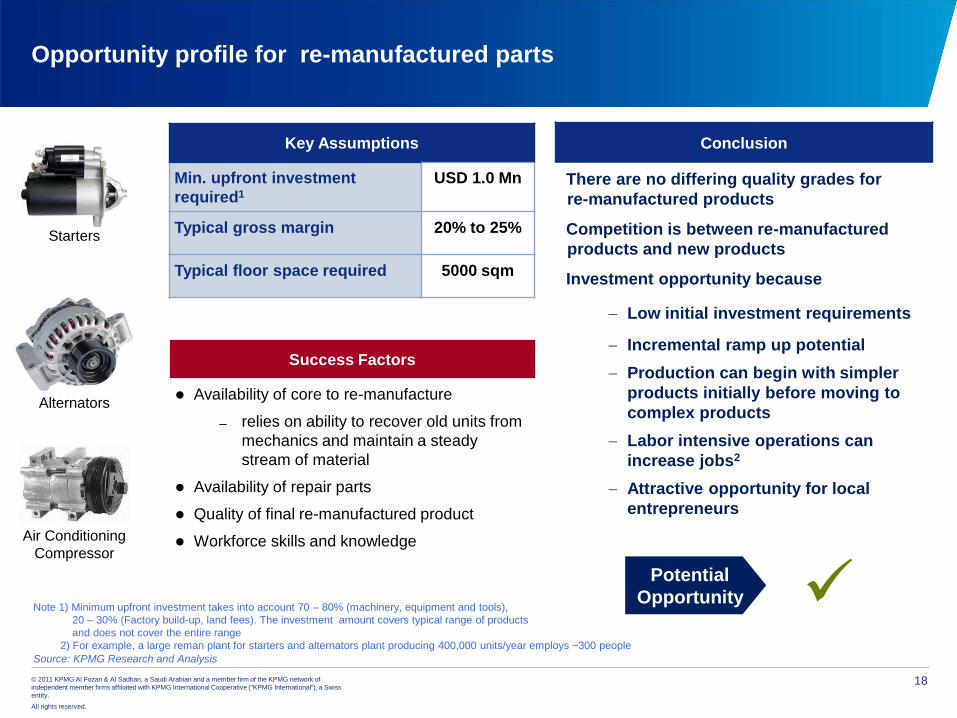

Opportunity profile for re-manufactured parts

Source: KPMG Research and Analysis

Key Assumptions

Min. upfront investment

required1

USD 1.0 Mn

Typical gross margin 20% to 25%

Typical floor space required 5000 sqm

Conclusion

There are no differing quality grades for

re-manufactured products

Competition is between re-manufactured

products and new products

Investment opportunity because

Low initial investment requirements

Incremental ramp up potential

Production can begin with simpler

products initially before moving to

complex products

Labor intensive operations can

increase jobs2

Attractive opportunity for local

entrepreneurs

Success Factors

Availability of core to re-manufacture

relies on ability to recover old units from

mechanics and maintain a steady

stream of material

Availability of repair parts

Quality of final re-manufactured product

Workforce skills and knowledge

Alternators

Air Conditioning

Compressor

Starters

Potential

Opportunity Note 1) Minimum upfront investment takes into account 70 – 80% (machinery, equipment and tools),

20 – 30% (Factory build-up, land fees). The investment amount covers typical range of products

and does not cover the entire range

2) For example, a large reman plant for starters and alternators plant producing 400,000 units/year employs ~300 people

19© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

Based on opportunity profiling, five areas present opportunities to be

pursued further

Opportunity Product Range Required Critical Success Factors Assessment Summary

750+

• Access to friction

material

• Partnership with a

technology provider

Attractive opportunity both

in volume and margins

3000+• Partnership with a

technology provider

Attractive opportunity as

minimal volumes required

for viability

100+

• Higher exports

• Access to technology

provider

Opportunity becomes

attractive if significant

export markets are

accessible

500+

• Higher exports

• Access to synthetic

rubber (needs

partnership with a

technology provider)

Attractive opportunity due

to high margins

Not applicable• Potential help during

initial setup only

Attractive opportunity due

high potential for

employment and low initial

investment

Brake pads

Filters

Fan / Drive Belts

Re-manufactured

Parts1

Note 1) Remanufactrured parts include Starters, Alternators and AC Compressors

Batteries

20© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

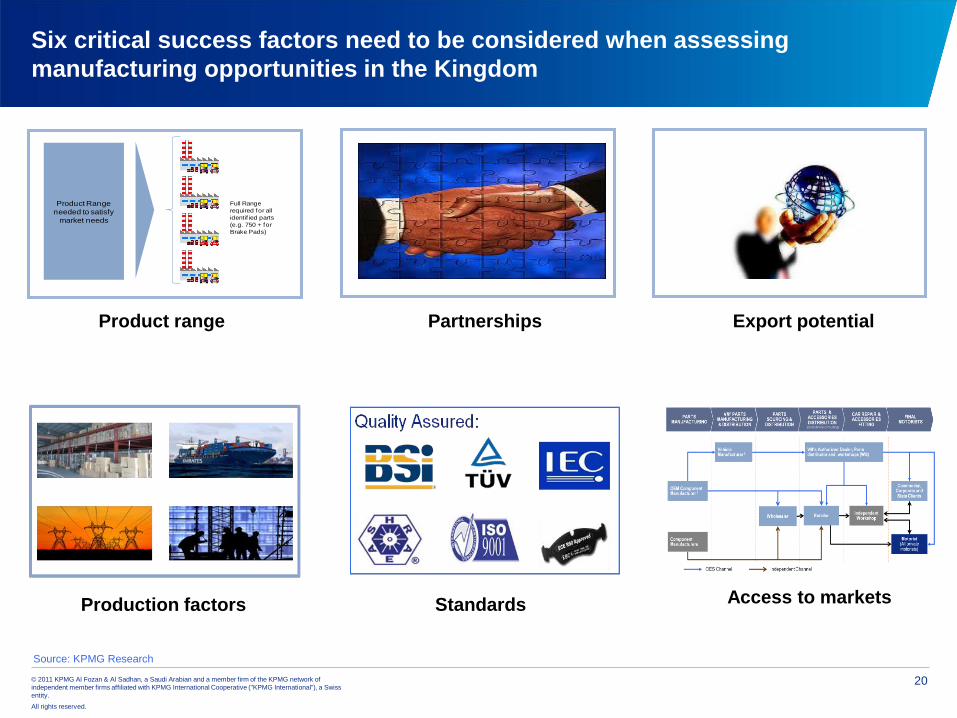

Six critical success factors need to be considered when assessing

manufacturing opportunities in the Kingdom

Source: KPMG Research

Product Range

needed to satisfy

market needs

Full Range

required for all

identif ied parts

(e.g. 750 + for

Brake Pads)

Product range Partnerships Export potential

Production factors Standards Access to markets

21© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

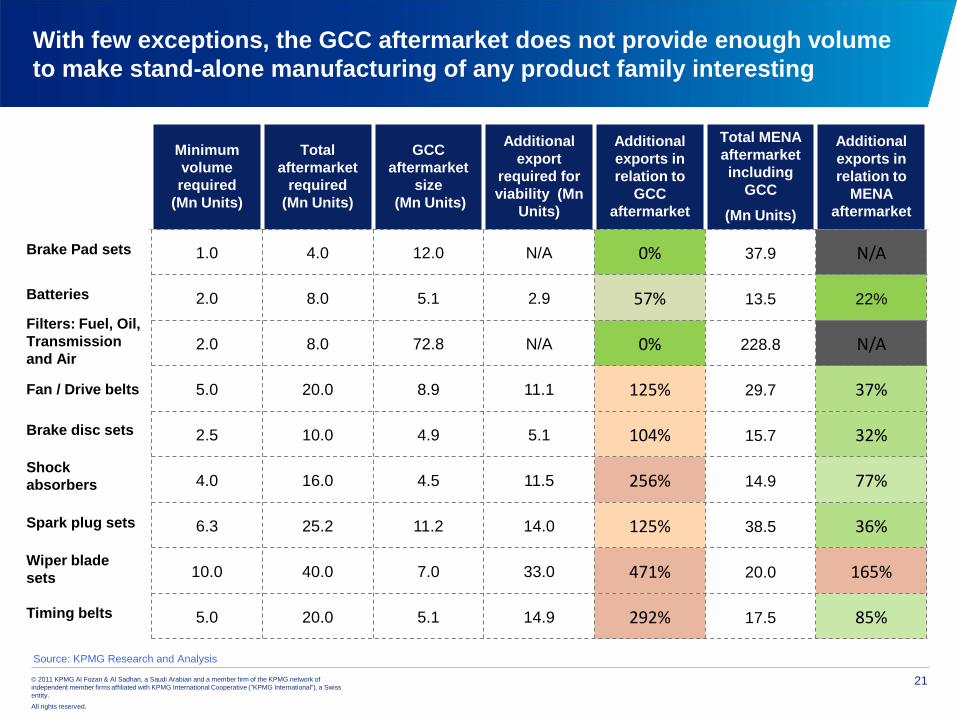

With few exceptions, the GCC aftermarket does not provide enough volume

to make stand-alone manufacturing of any product family interesting

Source: KPMG Research and Analysis

Minimum

volume

required

(Mn Units)

Total

aftermarket

required

(Mn Units)

GCC

aftermarket

size

(Mn Units)

Additional

export

required for

viability (Mn

Units)

Additional

exports in

relation to

GCC

aftermarket

Total MENA

aftermarket

including

GCC

(Mn Units)

Additional

exports in

relation to

MENA

aftermarket

1.0 4.0 12.0 N/A 0% 37.9 N/A

2.0 8.0 5.1 2.9 57% 13.5 22%

2.0 8.0 72.8 N/A 0% 228.8 N/A

5.0 20.0 8.9 11.1 125% 29.7 37%

2.5 10.0 4.9 5.1 104% 15.7 32%

4.0 16.0 4.5 11.5 256% 14.9 77%

6.3 25.2 11.2 14.0 125% 38.5 36%

10.0 40.0 7.0 33.0 471% 20.0 165%

5.0 20.0 5.1 14.9 292% 17.5 85%

Brake Pad sets

Batteries

Filters: Fuel, Oil,

Transmission

and Air

Fan / Drive belts

Brake disc sets

Shock

absorbers

Wiper blade

sets

Spark plug sets

Timing belts

22© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

After considering higher export assumptions, three additional products

become potentially attractive

Source: KPMG Research and Analysis

Brake disc sets Spark plugsBatteries

(additional plants)

23© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

DRAFT

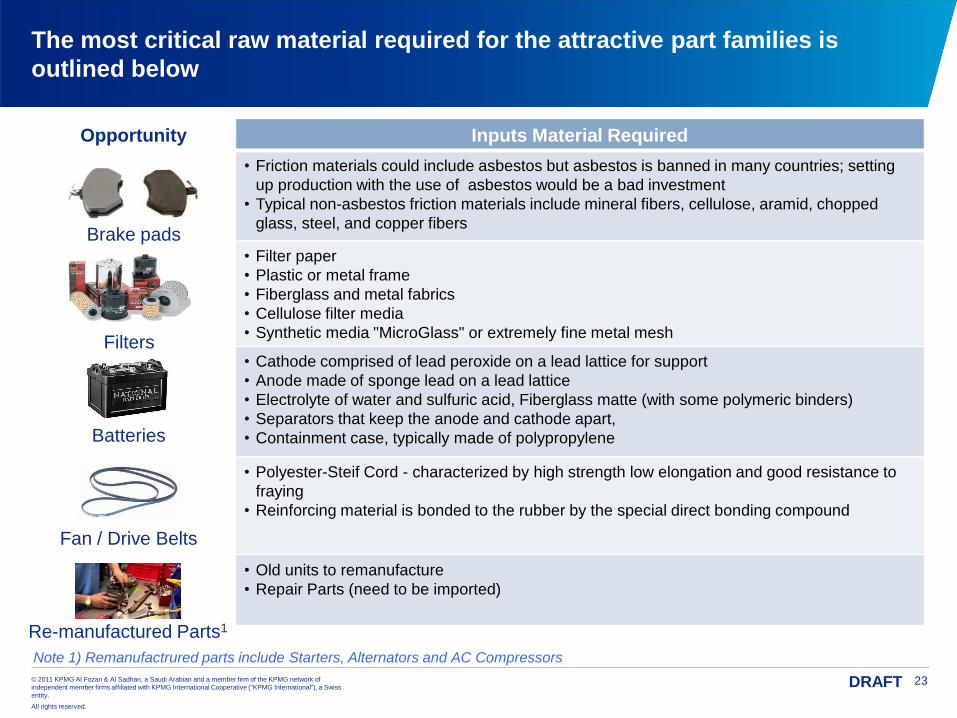

The most critical raw material required for the attractive part families is

outlined below

Opportunity Inputs Material Required

• Friction materials could include asbestos but asbestos is banned in many countries; setting

up production with the use of asbestos would be a bad investment

• Typical non-asbestos friction materials include mineral fibers, cellulose, aramid, chopped

glass, steel, and copper fibers

• Filter paper

• Plastic or metal frame

• Fiberglass and metal fabrics

• Cellulose filter media

• Synthetic media "MicroGlass" or extremely fine metal mesh

• Cathode comprised of lead peroxide on a lead lattice for support

• Anode made of sponge lead on a lead lattice

• Electrolyte of water and sulfuric acid, Fiberglass matte (with some polymeric binders)

• Separators that keep the anode and cathode apart,

• Containment case, typically made of polypropylene

• Polyester-Steif Cord - characterized by high strength low elongation and good resistance to

fraying

• Reinforcing material is bonded to the rubber by the special direct bonding compound

• Old units to remanufacture

• Repair Parts (need to be imported)

Brake pads

Filters

Fan / Drive Belts

Re-manufactured Parts1

Note 1) Remanufactrured parts include Starters, Alternators and AC Compressors

Batteries

24© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

DRAFT

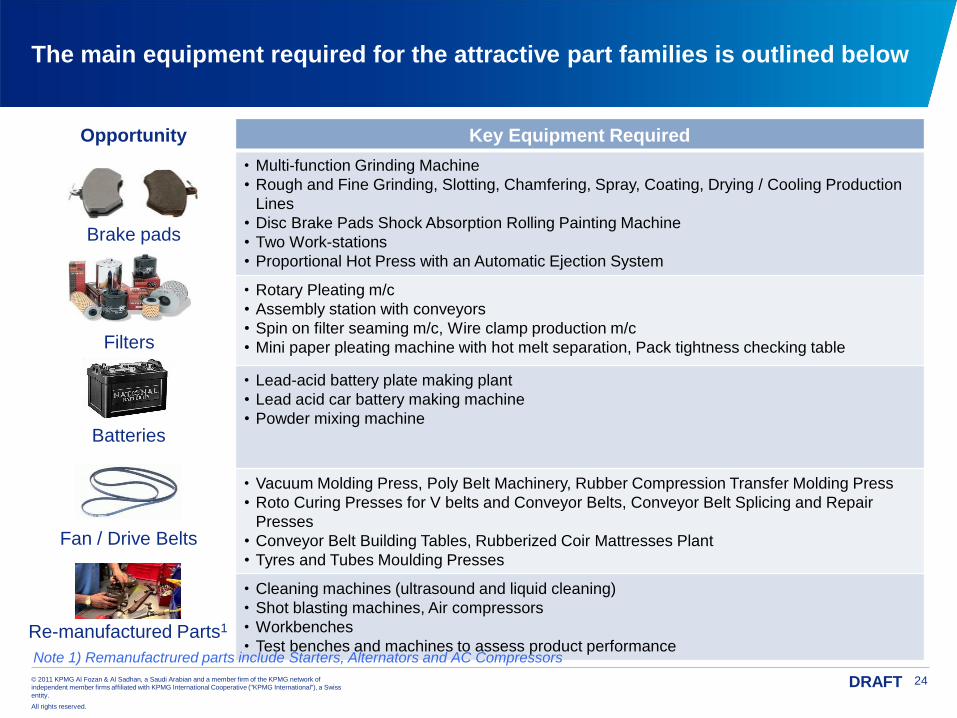

The main equipment required for the attractive part families is outlined below

Opportunity Key Equipment Required

• Multi-function Grinding Machine

• Rough and Fine Grinding, Slotting, Chamfering, Spray, Coating, Drying / Cooling Production

Lines

• Disc Brake Pads Shock Absorption Rolling Painting Machine

• Two Work-stations

• Proportional Hot Press with an Automatic Ejection System

• Rotary Pleating m/c

• Assembly station with conveyors

• Spin on filter seaming m/c, Wire clamp production m/c

• Mini paper pleating machine with hot melt separation, Pack tightness checking table

• Lead-acid battery plate making plant

• Lead acid car battery making machine

• Powder mixing machine

• Vacuum Molding Press, Poly Belt Machinery, Rubber Compression Transfer Molding Press

• Roto Curing Presses for V belts and Conveyor Belts, Conveyor Belt Splicing and Repair

Presses

• Conveyor Belt Building Tables, Rubberized Coir Mattresses Plant

• Tyres and Tubes Moulding Presses

• Cleaning machines (ultrasound and liquid cleaning)• Shot blasting machines, Air compressors• Workbenches• Test benches and machines to assess product performance

Brake pads

Filters

Fan / Drive Belts

Re-manufactured Parts1

Note 1) Remanufactrured parts include Starters, Alternators and AC Compressors

Batteries

25© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

DRAFT

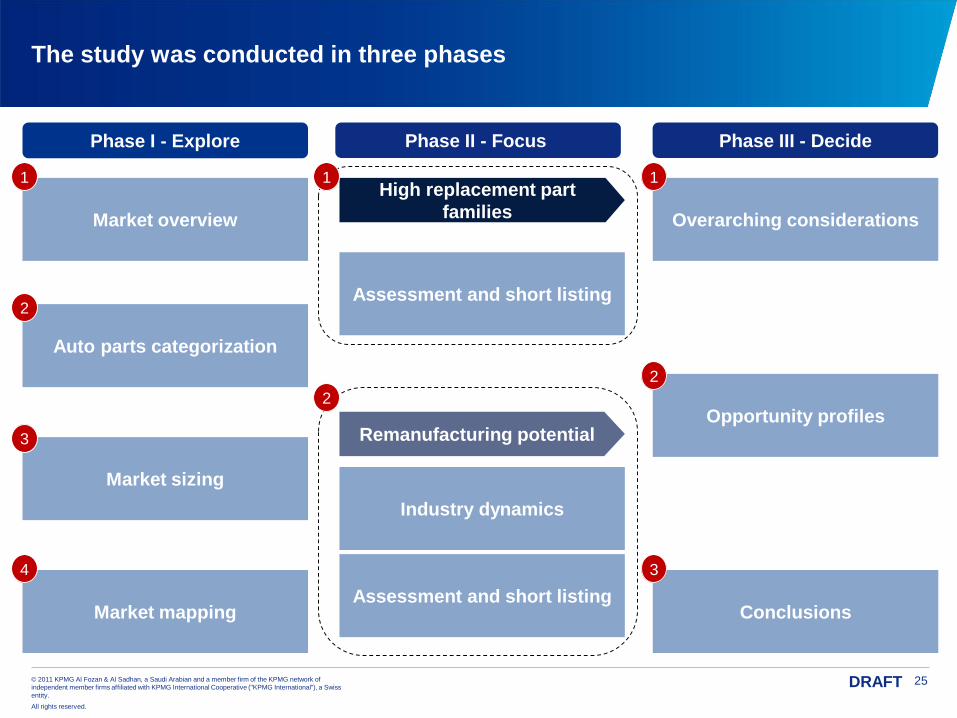

The study was conducted in three phases

Auto parts categorization

Market overview

Market sizing

Market mapping

Phase I - Explore Phase III - DecidePhase II - Focus

Assessment and short listing

High replacement part

families

Remanufacturing potential

Assessment and short listing

Industry dynamics

Opportunity profiles

Overarching considerations

Conclusions

1

2

3

4

1

2

3

1

2

26© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

DRAFT

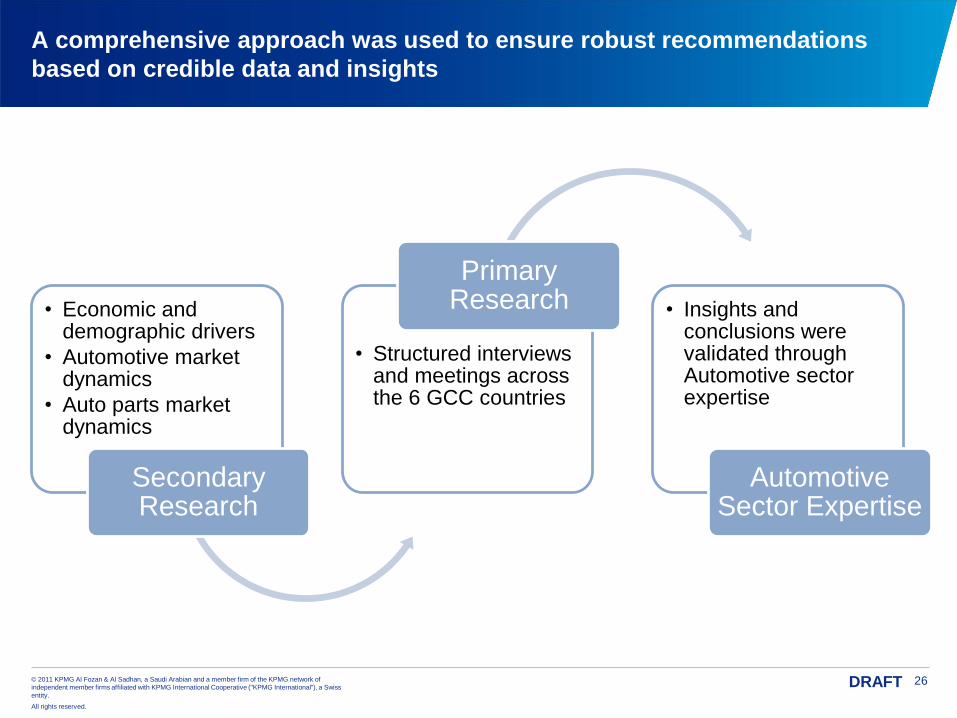

A comprehensive approach was used to ensure robust recommendations

based on credible data and insights

• Economic and demographic drivers

• Automotive market dynamics

• Auto parts market dynamics

Secondary Research

• Structured interviews and meetings across the 6 GCC countries

Primary Research • Insights and

conclusions were validated through Automotive sector expertise

Automotive Sector Expertise

27© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

DRAFT

25

15

54 4 4

26

22

17

1011 11

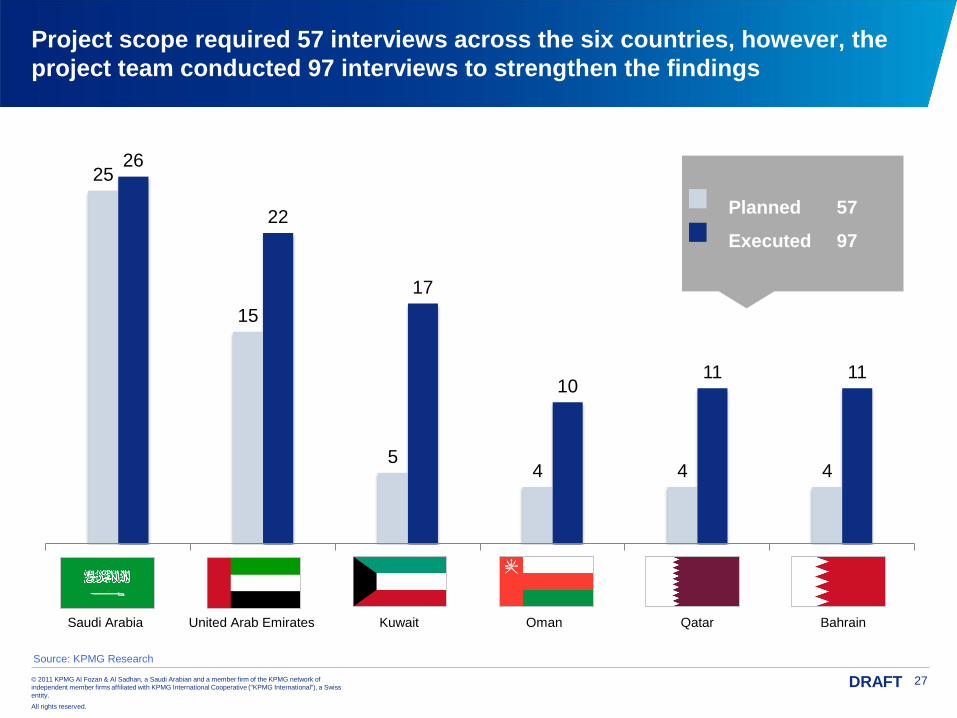

Project scope required 57 interviews across the six countries, however, the

project team conducted 97 interviews to strengthen the findings

Kuwait Bahrain Oman Qatar United Arab Emirates Saudi Arabia

Planned 57

Executed 97

Source: KPMG Research

28© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

DRAFT

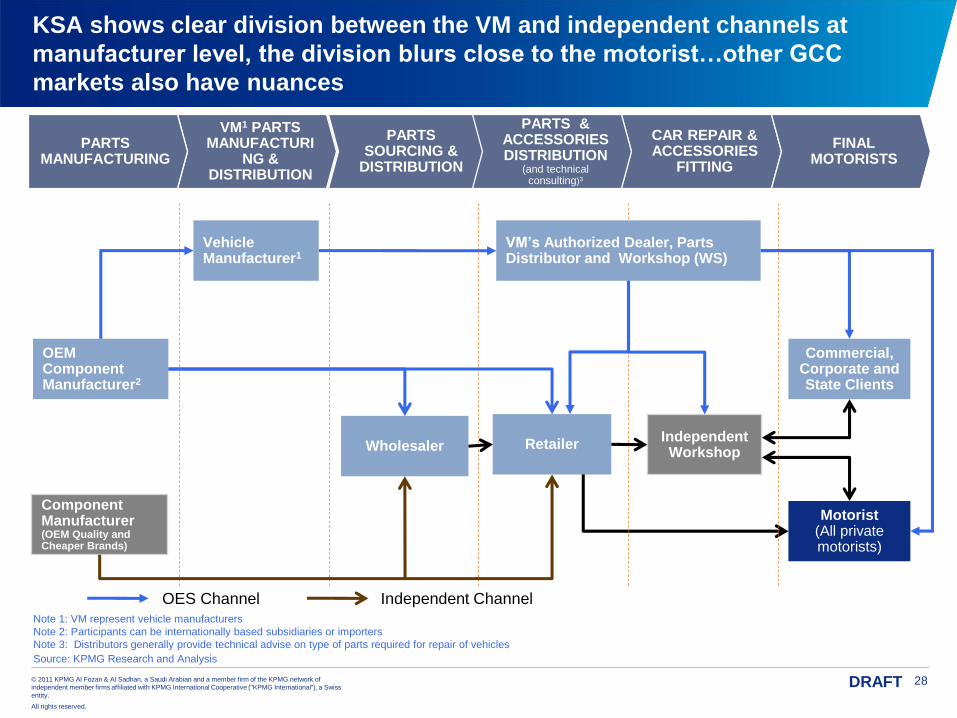

KSA shows clear division between the VM and independent channels at

manufacturer level, the division blurs close to the motorist…other GCC

markets also have nuances

OEM Component Manufacturer2

Vehicle Manufacturer1

Wholesaler RetailerIndependent Workshop

Commercial, Corporate and State Clients

Motorist (All private motorists)

Component Manufacturer (OEM Quality and Cheaper Brands)

OES Channel Independent Channel

VM’s Authorized Dealer, Parts Distributor and Workshop (WS)

VM1 PARTS MANUFACTURI

NG & DISTRIBUTION

PARTS MANUFACTURING

PARTS SOURCING &

DISTRIBUTION

PARTS & ACCESSORIES DISTRIBUTION

(and technical consulting)3

CAR REPAIR & ACCESSORIES

FITTING

FINAL MOTORISTS

Note 1: VM represent vehicle manufacturers

Note 2: Participants can be internationally based subsidiaries or importers

Note 3: Distributors generally provide technical advise on type of parts required for repair of vehicles

Source: KPMG Research and Analysis

29© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

DRAFT

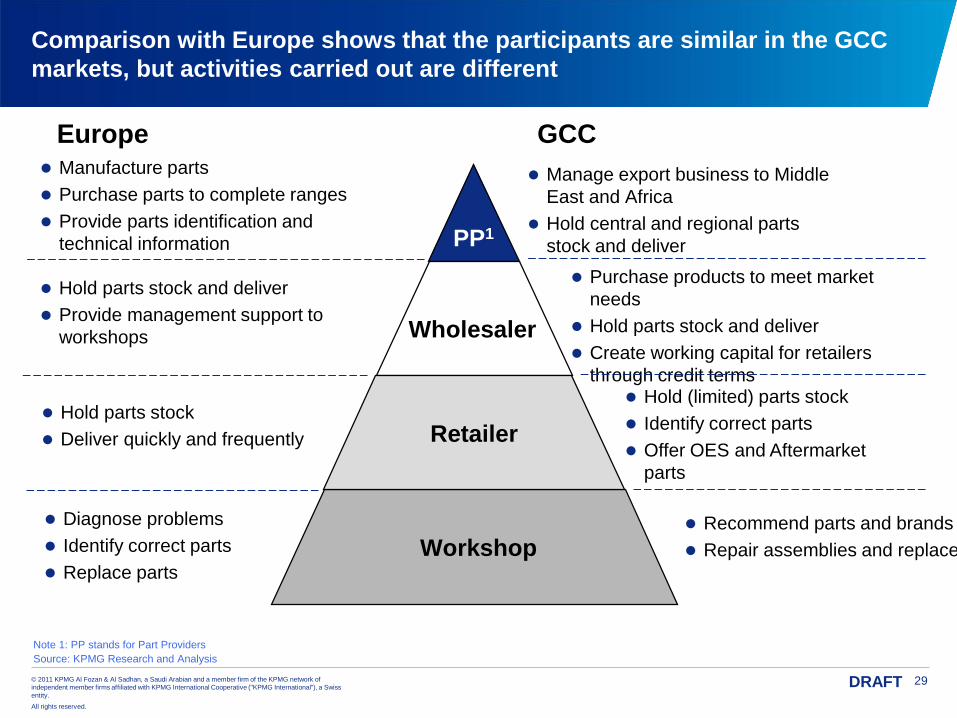

Comparison with Europe shows that the participants are similar in the GCC

markets, but activities carried out are different

Recommend parts and brands

Repair assemblies and replace

PP1

Workshop

Retailer

Wholesaler

Diagnose problems

Identify correct parts

Replace parts

Hold parts stock

Deliver quickly and frequently

Hold (limited) parts stock

Identify correct parts

Offer OES and Aftermarket

parts

Hold parts stock and deliver

Provide management support to

workshops

Purchase products to meet market

needs

Hold parts stock and deliver

Create working capital for retailers

through credit terms

Manufacture parts

Purchase parts to complete ranges

Provide parts identification and

technical information

Manage export business to Middle

East and Africa

Hold central and regional parts

stock and deliver

Europe GCC

Note 1: PP stands for Part Providers

Source: KPMG Research and Analysis

30© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

DRAFT

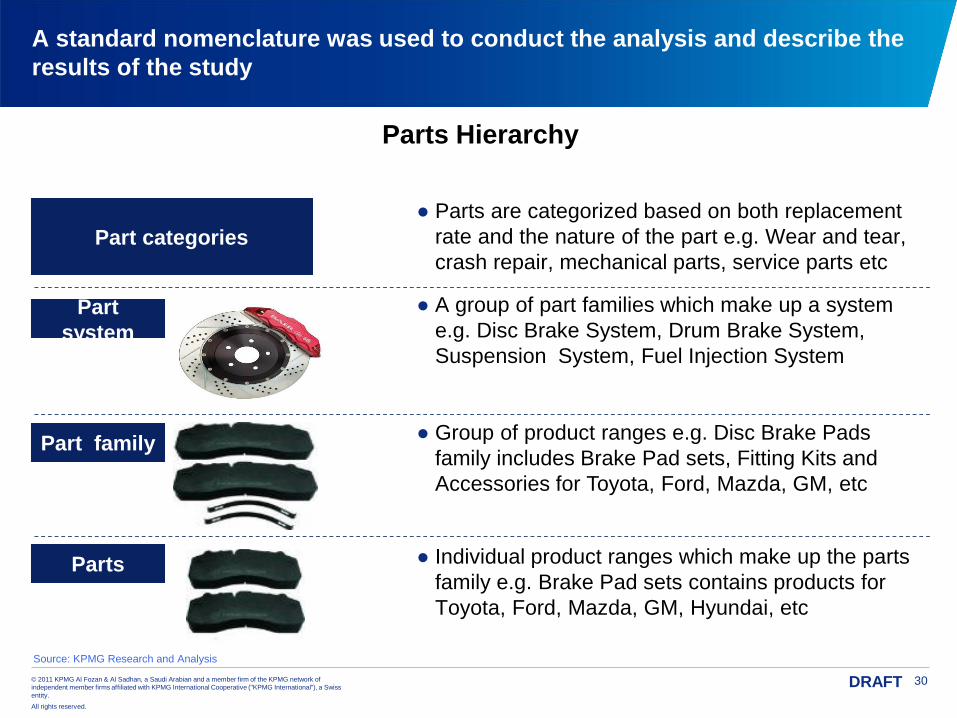

A standard nomenclature was used to conduct the analysis and describe the

results of the study

● A group of part families which make up a system

e.g. Disc Brake System, Drum Brake System,

Suspension System, Fuel Injection System

● Group of product ranges e.g. Disc Brake Pads

family includes Brake Pad sets, Fitting Kits and

Accessories for Toyota, Ford, Mazda, GM, etc

● Individual product ranges which make up the parts

family e.g. Brake Pad sets contains products for

Toyota, Ford, Mazda, GM, Hyundai, etc

Parts Hierarchy

Source: KPMG Research and Analysis

Part

system

Part family

Parts

Part categories

● Parts are categorized based on both replacement

rate and the nature of the part e.g. Wear and tear,

crash repair, mechanical parts, service parts etc

31© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

DRAFT

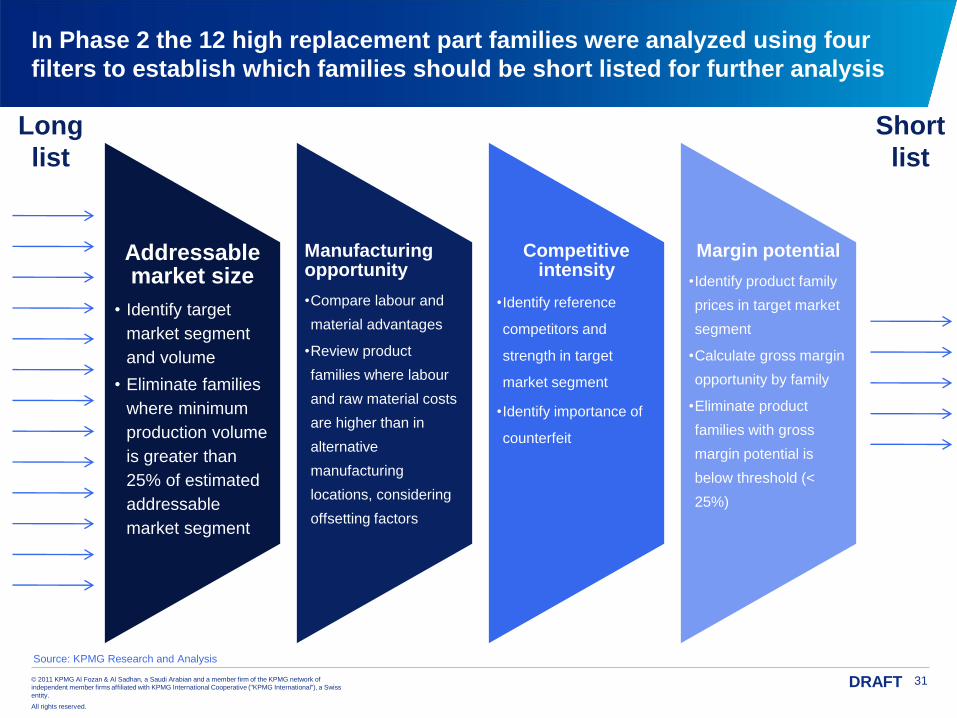

In Phase 2 the 12 high replacement part families were analyzed using four

filters to establish which families should be short listed for further analysis

Addressable market size

• Identify target

market segment

and volume

• Eliminate families

where minimum

production volume

is greater than

25% of estimated

addressable

market segment

Manufacturing opportunity

•Compare labour and

material advantages

•Review product

families where labour

and raw material costs

are higher than in

alternative

manufacturing

locations, considering

offsetting factors

Competitive intensity

•Identify reference

competitors and

strength in target

market segment

•Identify importance of

counterfeit

Margin potential

•Identify product family

prices in target market

segment

•Calculate gross margin

opportunity by family

•Eliminate product

families with gross

margin potential is

below threshold (<

25%)

Long

list

Short

list

Source: KPMG Research and Analysis

32© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

DRAFT

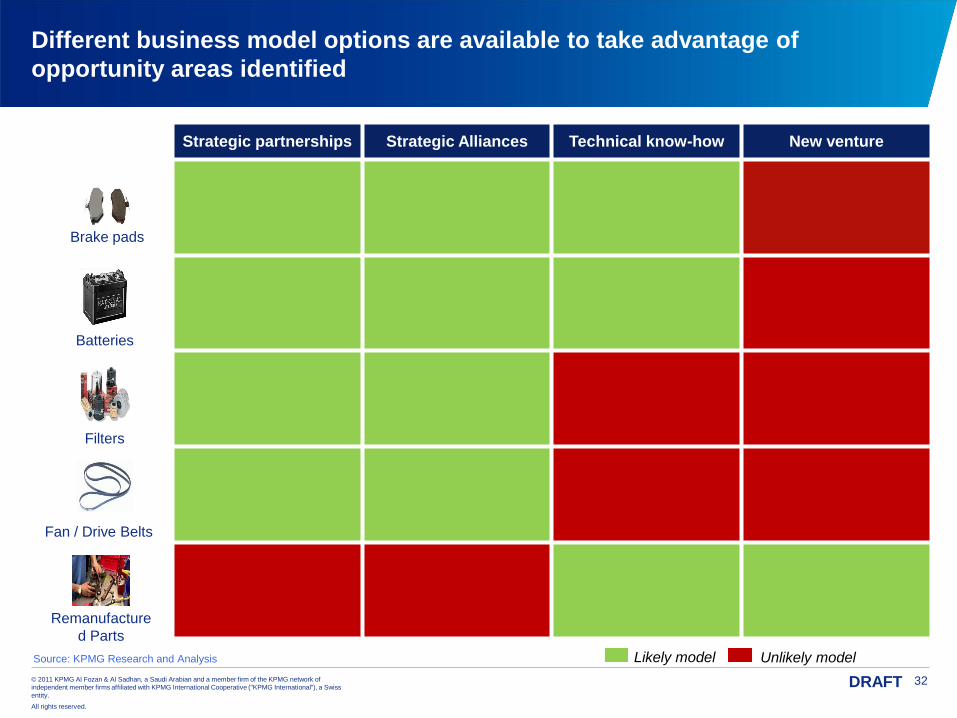

Different business model options are available to take advantage of

opportunity areas identified

Strategic partnerships Strategic Alliances Technical know-how New venture

Source: KPMG Research and Analysis

Fan / Drive Belts

Batteries

Filters

Brake pads

Remanufacture

d Parts

Unlikely modelLikely model

33© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

DRAFT

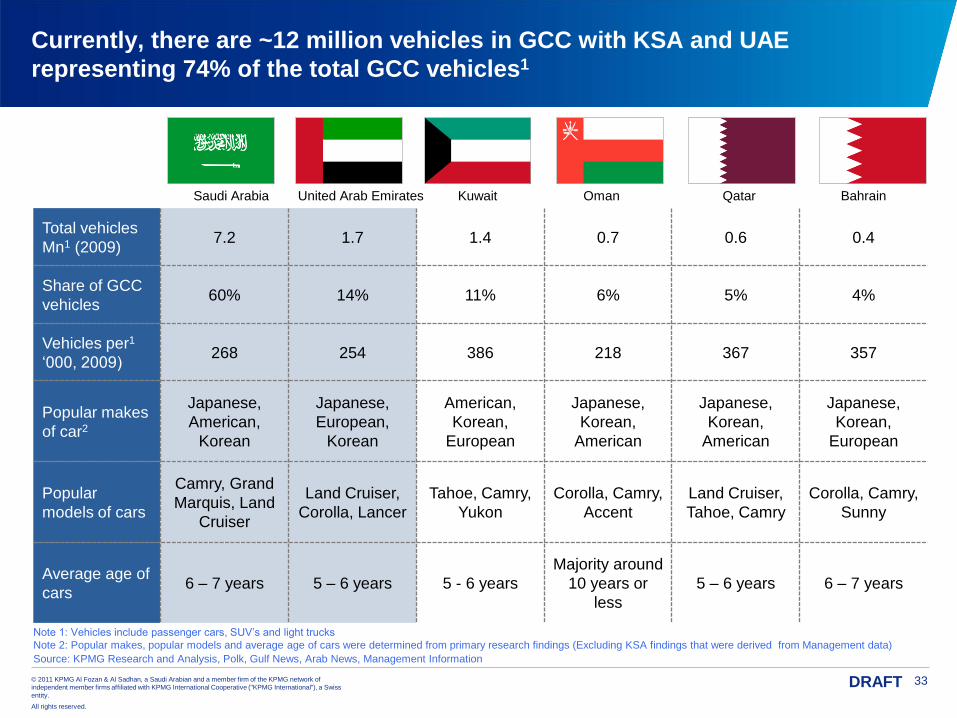

Total vehicles

Mn1 (2009)7.2 1.7 1.4 0.7 0.6 0.4

Share of GCC

vehicles60% 14% 11% 6% 5% 4%

Vehicles per1

‘000, 2009)268 254 386 218 367 357

Popular makes

of car2

Japanese,

American,

Korean

Japanese,

European,

Korean

American,

Korean,

European

Japanese,

Korean,

American

Japanese,

Korean,

American

Japanese,

Korean,

European

Popular

models of cars

Camry, Grand

Marquis, Land

Cruiser

Land Cruiser,

Corolla, Lancer

Tahoe, Camry,

Yukon

Corolla, Camry,

Accent

Land Cruiser,

Tahoe, Camry

Corolla, Camry,

Sunny

Average age of

cars6 – 7 years 5 – 6 years 5 - 6 years

Majority around

10 years or

less

5 – 6 years 6 – 7 years

Currently, there are ~12 million vehicles in GCC with KSA and UAE

representing 74% of the total GCC vehicles1

Note 1: Vehicles include passenger cars, SUV’s and light trucks

Note 2: Popular makes, popular models and average age of cars were determined from primary research findings (Excluding KSA findings that were derived from Management data)

Source: KPMG Research and Analysis, Polk, Gulf News, Arab News, Management Information

Kuwait Oman Qatar United Arab Emirates Saudi Arabia Bahrain

34© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

DRAFT

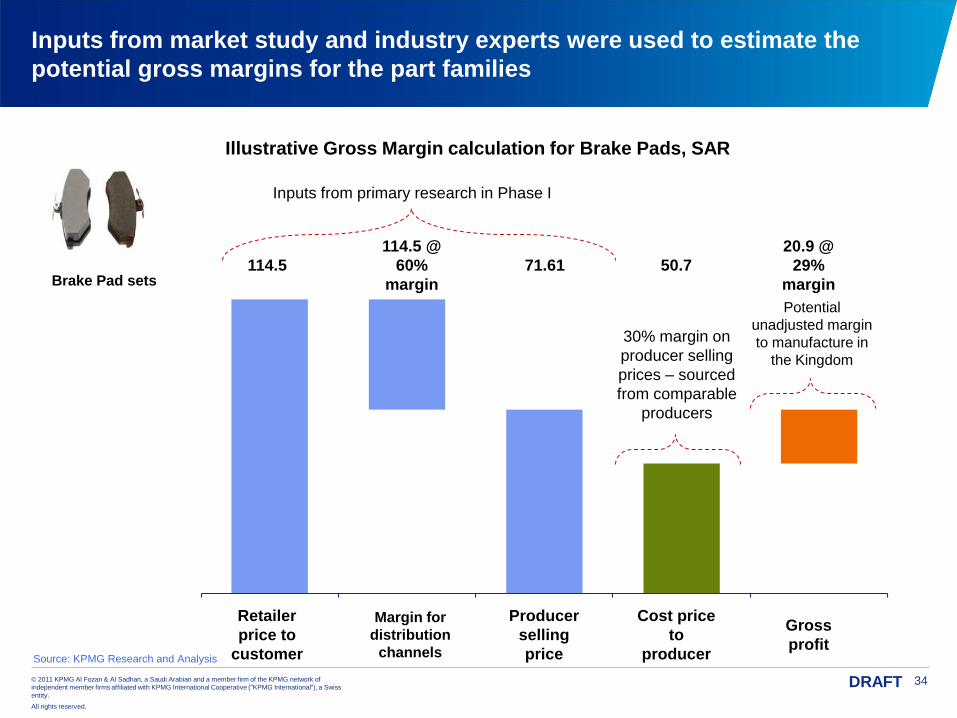

Inputs from market study and industry experts were used to estimate the

potential gross margins for the part families

Retailer

price to

customer

114.5

Margin for

distribution

channels

114.5 @

60%

margin

Producer

selling

price

71.61

Cost price

to

producer

50.7

Gross

profit

20.9 @

29%

margin

Inputs from primary research in Phase I

30% margin on

producer selling

prices – sourced

from comparable

producers

Potential

unadjusted margin

to manufacture in

the Kingdom

Source: KPMG Research and Analysis

Illustrative Gross Margin calculation for Brake Pads, SAR

Brake Pad sets

35© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

DRAFT

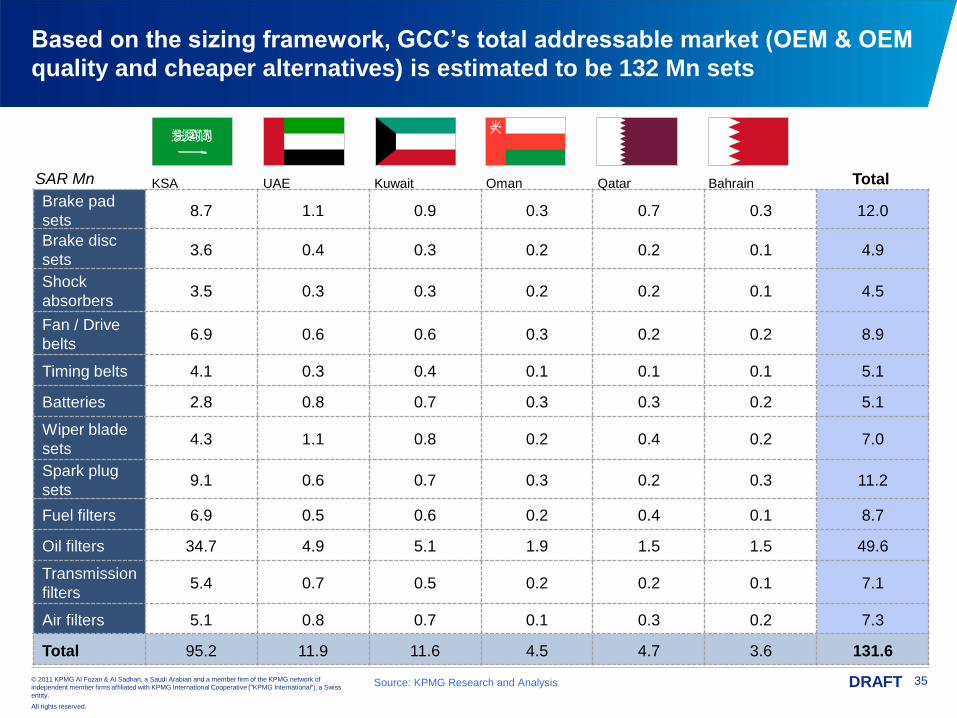

Based on the sizing framework, GCC’s total addressable market (OEM & OEM

quality and cheaper alternatives) is estimated to be 132 Mn sets

Brake pad

sets8.7 1.1 0.9 0.3 0.7 0.3 12.0

Brake disc

sets3.6 0.4 0.3 0.2 0.2 0.1 4.9

Shock

absorbers3.5 0.3 0.3 0.2 0.2 0.1 4.5

Fan / Drive

belts6.9 0.6 0.6 0.3 0.2 0.2 8.9

Timing belts 4.1 0.3 0.4 0.1 0.1 0.1 5.1

Batteries 2.8 0.8 0.7 0.3 0.3 0.2 5.1

Wiper blade

sets4.3 1.1 0.8 0.2 0.4 0.2 7.0

Spark plug

sets9.1 0.6 0.7 0.3 0.2 0.3 11.2

Fuel filters 6.9 0.5 0.6 0.2 0.4 0.1 8.7

Oil filters 34.7 4.9 5.1 1.9 1.5 1.5 49.6

Transmission

filters5.4 0.7 0.5 0.2 0.2 0.1 7.1

Air filters 5.1 0.8 0.7 0.1 0.3 0.2 7.3

Total 95.2 11.9 11.6 4.5 4.7 3.6 131.6

Source: KPMG Research and Analysis

Kuwait Bahrain Oman Qatar UAEKSA TotalSAR Mn

36© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

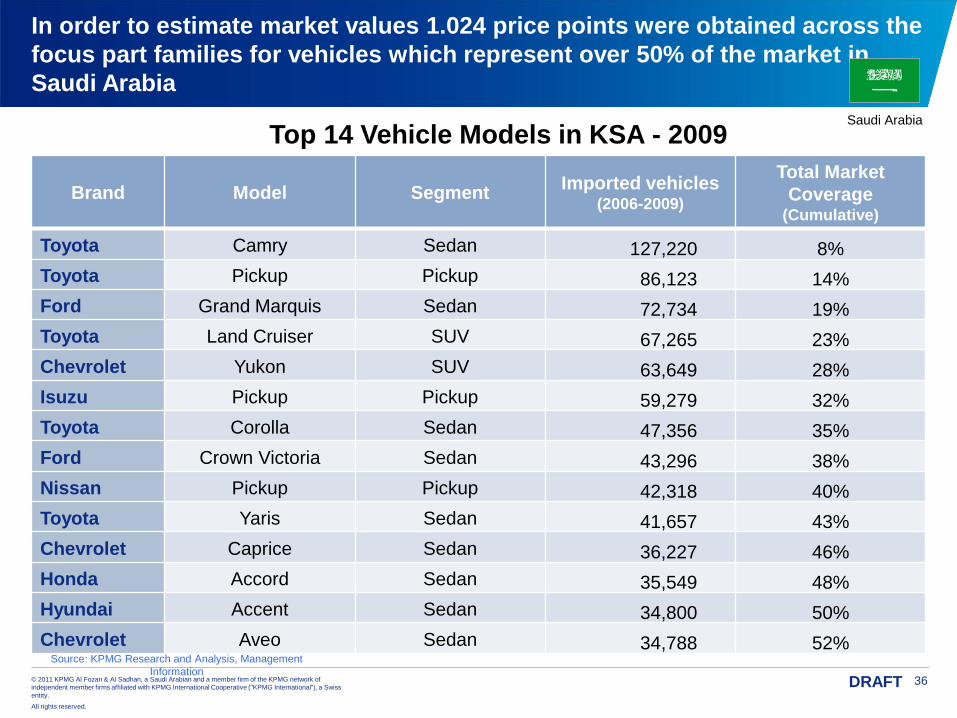

DRAFT

Brand Model SegmentImported vehicles

(2006-2009)

Total Market

Coverage (Cumulative)

Toyota Camry Sedan 127,220 8%

Toyota Pickup Pickup 86,123 14%

Ford Grand Marquis Sedan 72,734 19%

Toyota Land Cruiser SUV 67,265 23%

Chevrolet Yukon SUV 63,649 28%

Isuzu Pickup Pickup 59,279 32%

Toyota Corolla Sedan 47,356 35%

Ford Crown Victoria Sedan 43,296 38%

Nissan Pickup Pickup 42,318 40%

Toyota Yaris Sedan 41,657 43%

Chevrolet Caprice Sedan 36,227 46%

Honda Accord Sedan 35,549 48%

Hyundai Accent Sedan 34,800 50%

Chevrolet Aveo Sedan 34,788 52%

In order to estimate market values 1.024 price points were obtained across the

focus part families for vehicles which represent over 50% of the market in

Saudi Arabia

Top 14 Vehicle Models in KSA - 2009Saudi Arabia

Source: KPMG Research and Analysis, Management

Information

37© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

DRAFT

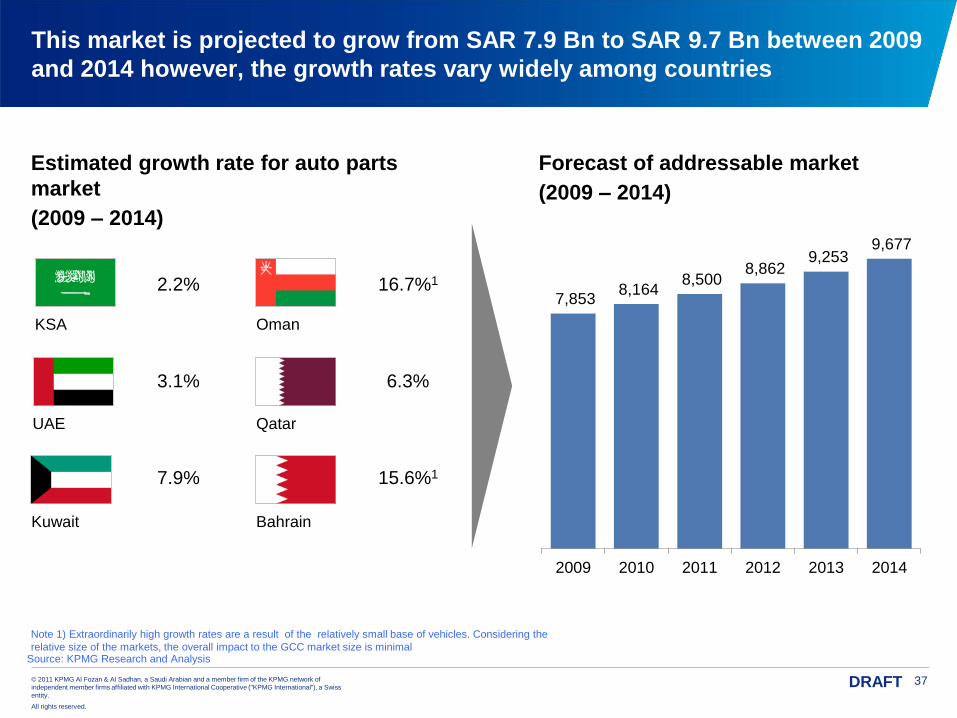

This market is projected to grow from SAR 7.9 Bn to SAR 9.7 Bn between 2009

and 2014 however, the growth rates vary widely among countries

Estimated growth rate for auto parts

market

(2009 – 2014)

Source: KPMG Research and Analysis

2.2%

3.1%

7.9%

16.7%1

6.3%

15.6%1

Kuwait Bahrain

Oman

Qatar UAE

KSA

7,853 8,164

8,500 8,862

9,253 9,677

2009 2010 2011 2012 2013 2014

Forecast of addressable market

(2009 – 2014)

Note 1) Extraordinarily high growth rates are a result of the relatively small base of vehicles. Considering the

relative size of the markets, the overall impact to the GCC market size is minimal

38© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

DRAFT

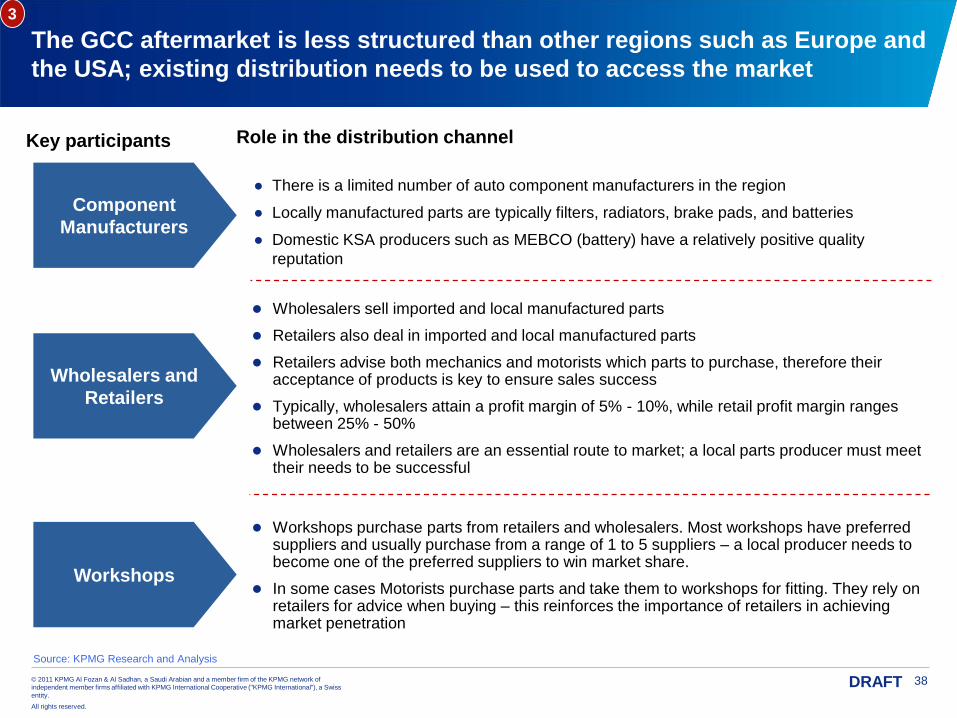

The GCC aftermarket is less structured than other regions such as Europe and

the USA; existing distribution needs to be used to access the market

● There is a limited number of auto component manufacturers in the region

● Locally manufactured parts are typically filters, radiators, brake pads, and batteries

● Domestic KSA producers such as MEBCO (battery) have a relatively positive quality

reputation

Wholesalers sell imported and local manufactured parts

Retailers also deal in imported and local manufactured parts

Retailers advise both mechanics and motorists which parts to purchase, therefore their acceptance of products is key to ensure sales success

Typically, wholesalers attain a profit margin of 5% - 10%, while retail profit margin ranges between 25% - 50%

Wholesalers and retailers are an essential route to market; a local parts producer must meet their needs to be successful

Workshops purchase parts from retailers and wholesalers. Most workshops have preferred suppliers and usually purchase from a range of 1 to 5 suppliers – a local producer needs to become one of the preferred suppliers to win market share.

In some cases Motorists purchase parts and take them to workshops for fitting. They rely on retailers for advice when buying – this reinforces the importance of retailers in achieving market penetration

Role in the distribution channel

Source: KPMG Research and Analysis

Workshops

Wholesalers and

Retailers

Component

Manufacturers

3

Key participants

39© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

DRAFT

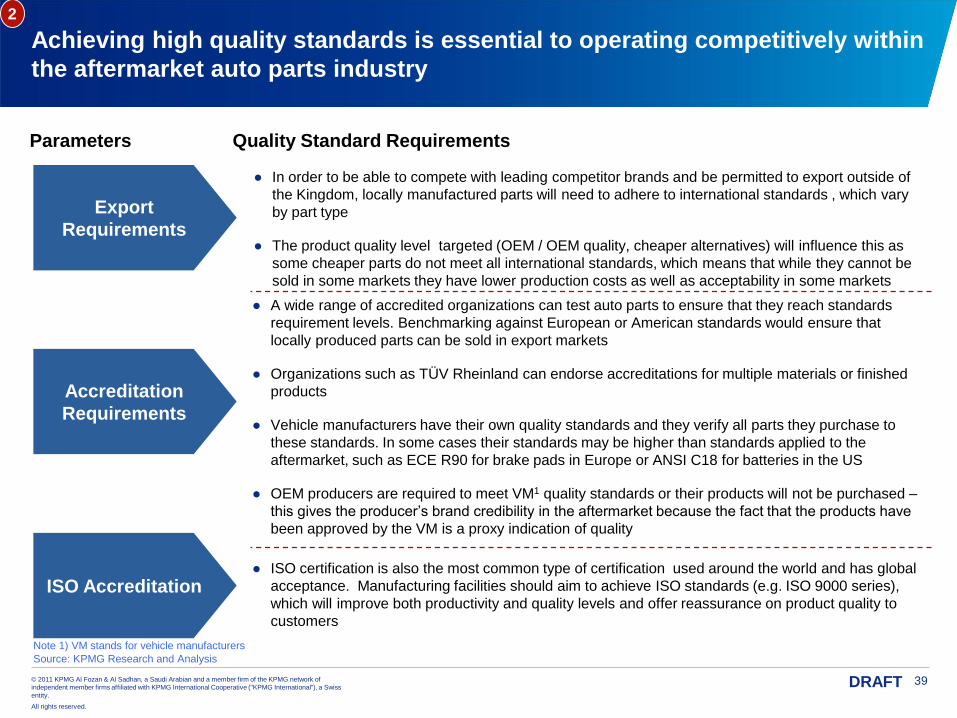

Achieving high quality standards is essential to operating competitively within

the aftermarket auto parts industry

● In order to be able to compete with leading competitor brands and be permitted to export outside of

the Kingdom, locally manufactured parts will need to adhere to international standards , which vary

by part type

● The product quality level targeted (OEM / OEM quality, cheaper alternatives) will influence this as

some cheaper parts do not meet all international standards, which means that while they cannot be

sold in some markets they have lower production costs as well as acceptability in some markets

● A wide range of accredited organizations can test auto parts to ensure that they reach standards

requirement levels. Benchmarking against European or American standards would ensure that

locally produced parts can be sold in export markets

● Organizations such as TÜV Rheinland can endorse accreditations for multiple materials or finished

products

● Vehicle manufacturers have their own quality standards and they verify all parts they purchase to

these standards. In some cases their standards may be higher than standards applied to the

aftermarket, such as ECE R90 for brake pads in Europe or ANSI C18 for batteries in the US

● OEM producers are required to meet VM1 quality standards or their products will not be purchased –

this gives the producer’s brand credibility in the aftermarket because the fact that the products have

been approved by the VM is a proxy indication of quality

ISO Accreditation

Accreditation

Requirements

Export

Requirements

● ISO certification is also the most common type of certification used around the world and has global

acceptance. Manufacturing facilities should aim to achieve ISO standards (e.g. ISO 9000 series),

which will improve both productivity and quality levels and offer reassurance on product quality to

customers

Quality Standard RequirementsParameters

Source: KPMG Research and Analysis

Note 1) VM stands for vehicle manufacturers

2

40© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

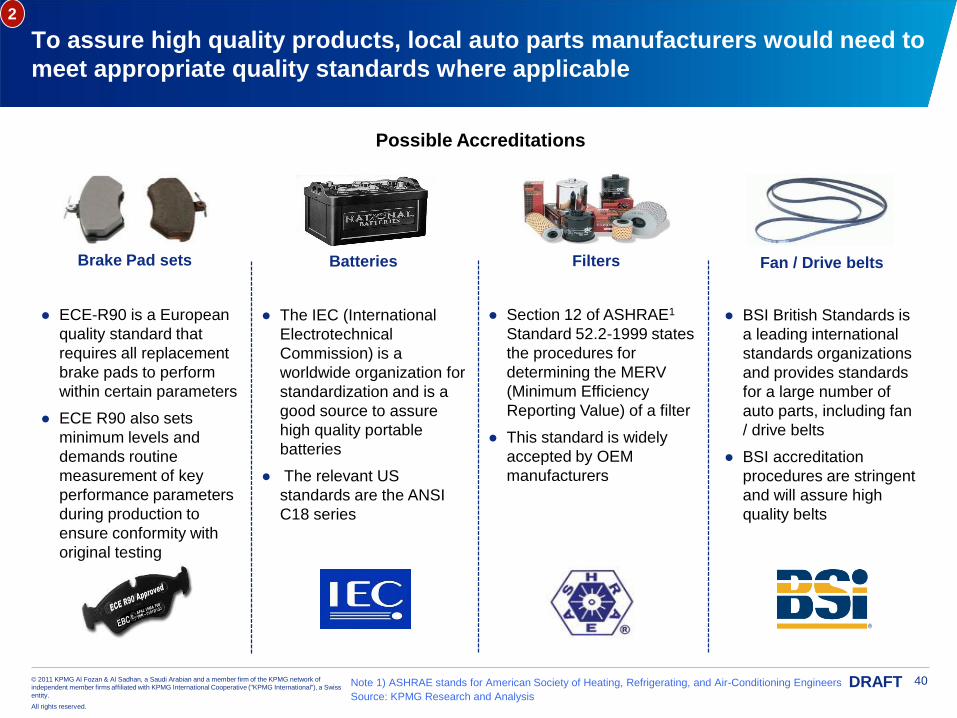

DRAFT

Fan / Drive beltsBatteries FiltersBrake Pad sets

● ECE-R90 is a European

quality standard that

requires all replacement

brake pads to perform

within certain parameters

● ECE R90 also sets

minimum levels and

demands routine

measurement of key

performance parameters

during production to

ensure conformity with

original testing

● The IEC (International

Electrotechnical

Commission) is a

worldwide organization for

standardization and is a

good source to assure

high quality portable

batteries

● The relevant US

standards are the ANSI

C18 series

● Section 12 of ASHRAE1

Standard 52.2-1999 states

the procedures for

determining the MERV

(Minimum Efficiency

Reporting Value) of a filter

● This standard is widely

accepted by OEM

manufacturers

● BSI British Standards is

a leading international

standards organizations

and provides standards

for a large number of

auto parts, including fan

/ drive belts

● BSI accreditation

procedures are stringent

and will assure high

quality belts

Possible Accreditations

2

To assure high quality products, local auto parts manufacturers would need to

meet appropriate quality standards where applicable

Source: KPMG Research and Analysis

Note 1) ASHRAE stands for American Society of Heating, Refrigerating, and Air-Conditioning Engineers

41© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

DRAFT

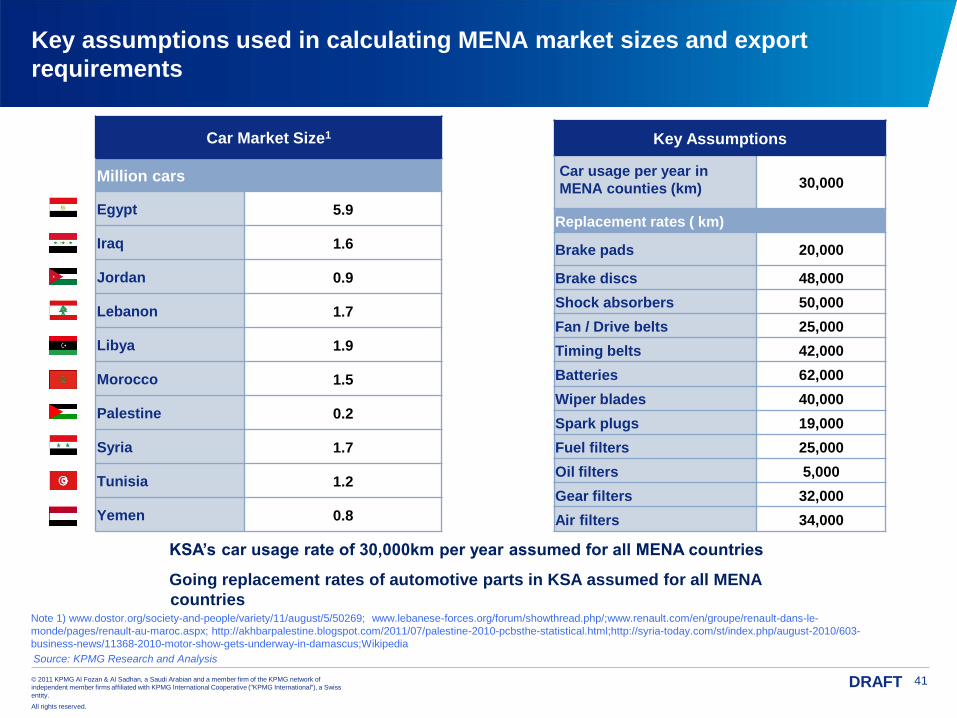

Key assumptions used in calculating MENA market sizes and export

requirements

KSA’s car usage rate of 30,000km per year assumed for all MENA countries

Going replacement rates of automotive parts in KSA assumed for all MENA

countries

Car Market Size1

Million cars

Egypt 5.9

Iraq 1.6

Jordan 0.9

Lebanon 1.7

Libya 1.9

Morocco 1.5

Palestine 0.2

Syria 1.7

Tunisia 1.2

Yemen 0.8

Source: KPMG Research and Analysis

Note 1) www.dostor.org/society-and-people/variety/11/august/5/50269; www.lebanese-forces.org/forum/showthread.php/;www.renault.com/en/groupe/renault-dans-le-

monde/pages/renault-au-maroc.aspx; http://akhbarpalestine.blogspot.com/2011/07/palestine-2010-pcbsthe-statistical.html;http://syria-today.com/st/index.php/august-2010/603-

business-news/11368-2010-motor-show-gets-underway-in-damascus;Wikipedia

Key Assumptions

Car usage per year in

MENA counties (km) 30,000

Replacement rates ( km)

Brake pads 20,000

Brake discs 48,000

Shock absorbers 50,000

Fan / Drive belts 25,000

Timing belts 42,000

Batteries 62,000

Wiper blades 40,000

Spark plugs 19,000

Fuel filters 25,000

Oil filters 5,000

Gear filters 32,000

Air filters 34,000

42© 2011 KPMG Al Fozan & Al Sadhan, a Saudi Arabian and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss

entity.

All rights reserved.

DRAFT

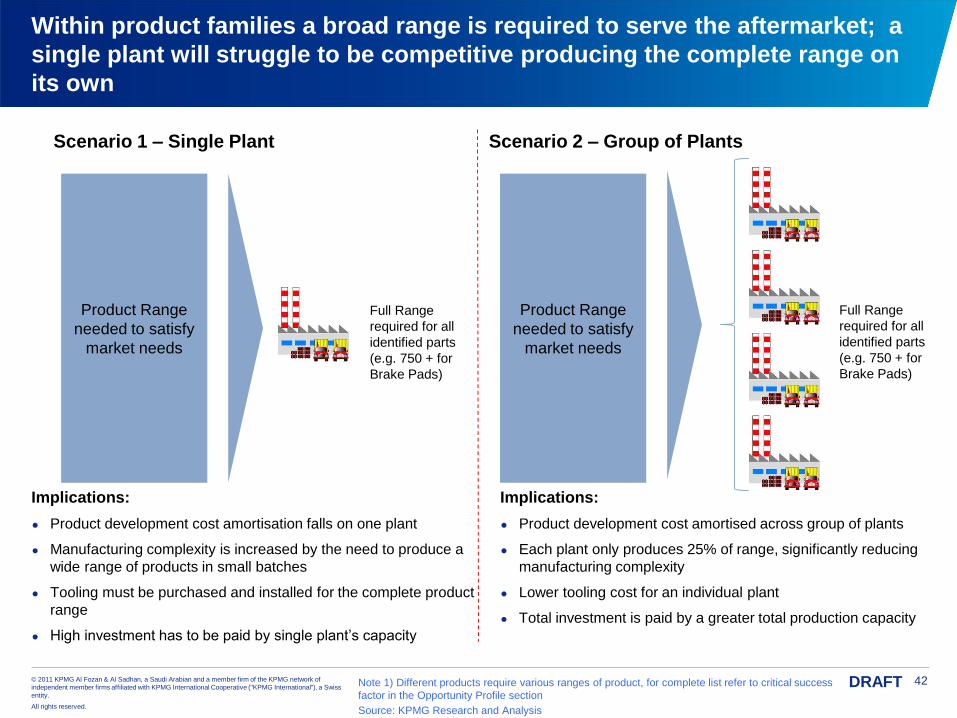

Within product families a broad range is required to serve the aftermarket; a

single plant will struggle to be competitive producing the complete range on

its own

Product Range

needed to satisfy

market needs

Full Range

required for all

identified parts

(e.g. 750 + for

Brake Pads)

Product Range

needed to satisfy

market needs

Implications:

● Product development cost amortisation falls on one plant

● Manufacturing complexity is increased by the need to produce a

wide range of products in small batches

● Tooling must be purchased and installed for the complete product

range

● High investment has to be paid by single plant’s capacity

Implications:

● Product development cost amortised across group of plants

● Each plant only produces 25% of range, significantly reducing

manufacturing complexity

● Lower tooling cost for an individual plant

● Total investment is paid by a greater total production capacity

Scenario 1 – Single Plant Scenario 2 – Group of Plants

Source: KPMG Research and Analysis

Full Range

required for all

identified parts

(e.g. 750 + for

Brake Pads)

Note 1) Different products require various ranges of product, for complete list refer to critical success

factor in the Opportunity Profile section