Embed Size (px)

Citation preview

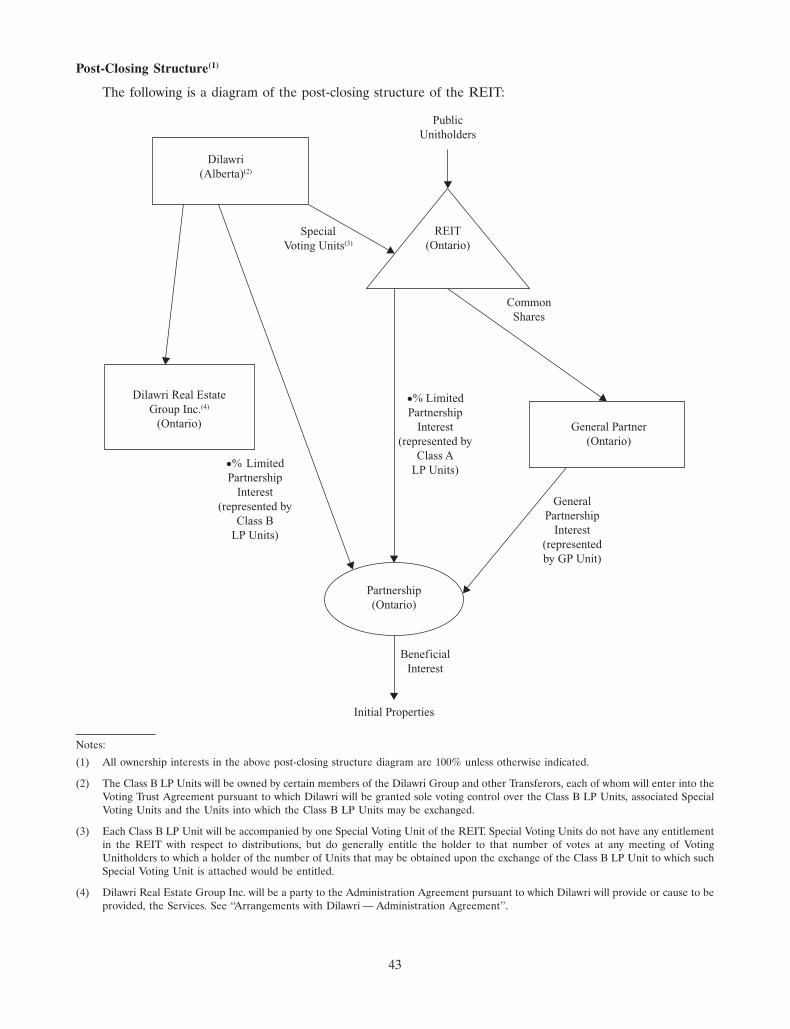

3JUN201506580802

No securities regulatory authority has expressed an opinion about these securities and it is an offence to claim otherwise. This prospectus constitutes apublic offering of these securities only in those jurisdictions where they may be lawfully offered for sale and therein only by persons permitted to sell suchsecurities. These securities have not been, and will not be, registered under the United States Securities Act of 1933, as amended (the ‘‘U.S. SecuritiesAct’’), or the securities laws of any state of the United States and may not be offered, sold or delivered, directly or indirectly, in the United States (as suchterm is defined in Regulation S under the U.S. Securities Act) (the ‘‘United States’’) except pursuant to an exemption from the registration requirements ofthe U.S. Securities Act and applicable state securities laws. This prospectus does not constitute an offer to sell or solicitation of an offer to buy any of thesesecurities in the United States. See ‘‘Plan of Distribution’’.

PRELIMINARY PROSPECTUSInitial Public Offering June 9, 2015

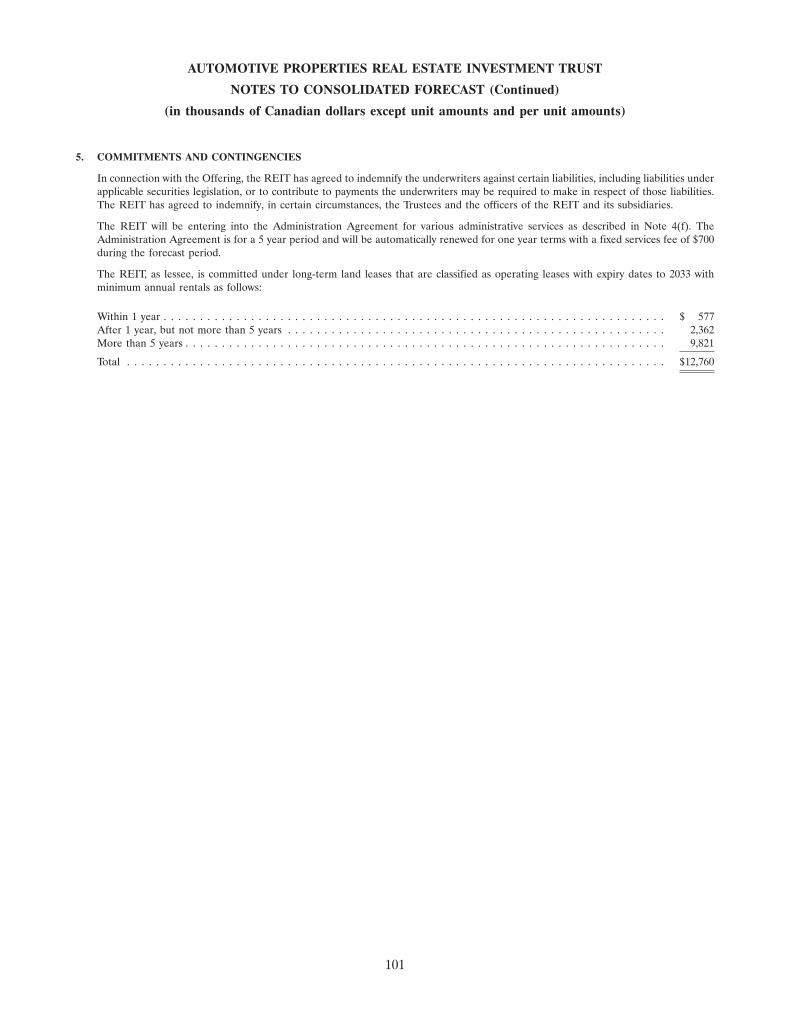

AUTOMOTIVE PROPERTIES REAL ESTATE INVESTMENT TRUST$ �

� Units

This prospectus qualifies the distribution to the public (the ‘‘Offering’’) of � units (the ‘‘Units’’) of Automotive Properties RealEstate Investment Trust (the ‘‘REIT’’), an unincorporated, open-ended real estate investment trust established under, andgoverned by, the laws of the Province of Ontario, at a price of $10.00 per Unit (the ‘‘Offering Price’’). The REIT has been formedto own primarily income-producing automotive dealership properties located in Canada.

893353 Alberta Inc. (‘‘Dilawri’’) has taken the initiative in creating the REIT in order to establish a growth-oriented real estateentity that is expected to benefit from its relationship with the Dilawri Group (as defined herein), while retaining a significanteconomic interest in the Initial Properties (as defined below). In connection with the completion of the Offering and relatedtransactions (the ‘‘Closing’’), the REIT will indirectly acquire, through Automotive Properties Limited Partnership(the ‘‘Partnership’’), all of the property interests currently directly or indirectly held by the Transferors (as defined herein) in26 commercial properties (collectively, the ‘‘Initial Properties’’) located in Ontario, Saskatchewan, Alberta and British Columbiatotaling approximately 958,000 square feet of gross leasable area (‘‘GLA’’). Out of the 26 Initial Properties, 24 are exclusivelyoccupied by the Dilawri Group for use as automotive dealerships or, in one case, an automotive repair facility, while the other twoproperties are jointly occupied by the Dilawri Group (for use as automotive dealerships) and one or more third parties (for use asautomotive dealerships or complementary uses, including restaurants). The Initial Properties represent all of the REIT-SuitableProperties (as defined herein) currently owned by the Dilawri Group. As part of the Closing, the REIT will enter into leases withthe applicable members of the Dilawri Group pertaining to the entirety of each Initial Property, including the two properties thatare partially occupied by third parties, and the applicable members of the Dilawri Group will sublease the applicable portions ofthose two properties to such third parties. Consequently, the Dilawri Group will be the REIT’s only tenant at Closing and its mostsignificant tenant for the foreseeable future, with members of the Dilawri Group occupying 87% of the REIT’s GLA on Closingand third parties occupying the remainder pursuant to sublease arrangements with the Dilawri Group. The rent from the portionsof the Initial Properties occupied by the Dilawri Group will represent approximately 88% of the REIT’s Cash NOI (as definedherein) over the Forecast Period (as defined herein), with the portions of the Initial Properties occupied by third party tenantspursuant to sublease arrangements accounting for the remainder. On Closing, the initial terms of the leases with the Dilawri Groupwill range from 11 to 19 years, with a Cash NOI weighted average lease term of 15 years. See ‘‘Acquisition of the Initial Properties’’and ‘‘Assets of the REIT’’.

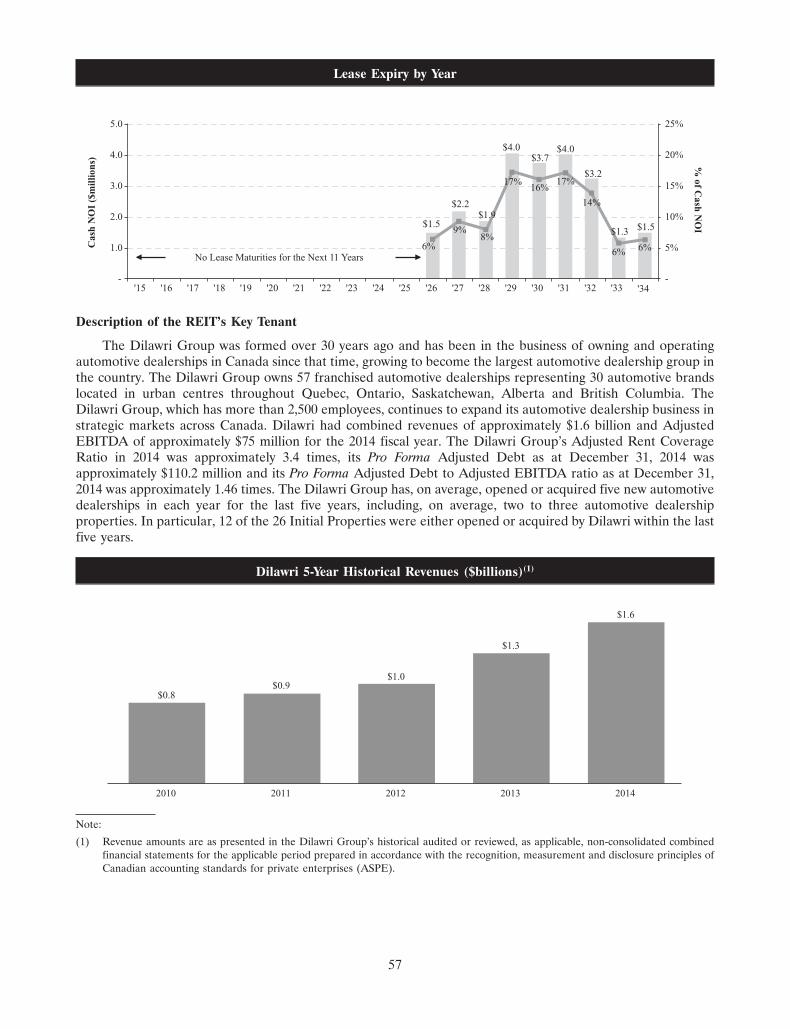

The Dilawri Group was formed over 30 years ago and has been in the business of owning and operating automotive dealerships inCanada since that time, growing to become the largest automotive dealership group in the country. The Dilawri Group owns57 franchised automotive dealerships representing 30 automotive brands located in urban centres throughout Quebec, Ontario,Saskatchewan, Alberta and British Columbia. The Dilawri Group, which has more than 2,500 employees, continues to expand itsautomotive dealership business in strategic markets across Canada. Dilawri had combined revenues of approximately $1.6 billionand Adjusted EBITDA (as defined herein) of approximately $75 million for the 2014 fiscal year. The Dilawri Group has, onaverage, opened or acquired five new automotive dealerships in each year for the last five years, including, on average, two to threeautomotive dealership properties. In particular, 12 of the 26 Initial Properties were either opened or acquired by Dilawri within thelast five years.

(continued on next page)

A copy of this preliminary prospectus has been filed with the securities regulatory authorities in each of the provinces of Canada, but has not yet becomefinal for the purpose of the sale of securities. Information contained in this preliminary prospectus may not be complete and may have to be amended. Thesecurities may not be sold until a receipt for the prospectus is obtained from the securities regulatory authorities.

Opportunity to gain exposure to a

unique real estate asset class

Automotive dealership properties

benefit from strong underlying

fundamentals

Portfolio of high-quality and

strategically located automotive

dealership properties

Significant growth opportunities

Strong national tenant with

significant alignment of interests

Excellent leasing profile

Compelling valuation and

conservative financial metrics

Experienced executive management

and strong independent board

Growth • Long-term leases with contractual rent escalations

> Cash NOI weighted average term to maturity of 15 years, with no lease expiries prior to 2026

> 1.5% contractual annual rent increase = 2.4% AFFO increase

• Third party acquisitions

> Leading platform to consolidate fragmented market

• Dilawri Group pipeline acquisitions

> Strong track record of developing automotive dealerships – three properties already in pipeline

> Right of first offer on all REIT-suitable properties

Portfolio of high-quality and strategically located automotive dealership properties

26 initial properties, with 42 rental buildings with

958,000 sq. ft. of GLA on 88 acres

Forecast Cash NOI $23.4 million

Average age of 8 years

958,000 square feetof GLA

REGINA

CALGARY

GVA

16% of Cash NOI

21% of Cash NOIGTA

48% of Cash NOI

15% of Cash NOI

26 automotive brands

Canada’s largest automotive group with 2014 revenues of approximately

$1.6 billion

Strong national tenant

AcuraAston MartinAudiBentleyBMWBuickCadillacChevroletChrysler

DodgeFIATFordGMCHondaHyundaiInfinitiJeepKIA

MazdaMINIMitsubishiNissan PorscheRAMToyotaVolkswagen

(continued from cover)

On Closing, it is expected that Dilawri will have an approximate � % effective interest in the REIT through the ownership,direction or control of all of the Class B limited partnership units of the Partnership (‘‘Class B LP Units’’) which are economicallyequivalent to, and exchangeable for, Units (or an approximate � % effective interest in the REIT if the Over-Allotment Option(as defined below) is exercised in full). See ‘‘Retained Interest’’. Dilawri has advised the REIT that it is the current intention of theDilawri Organization (as defined herein) to retain a significant interest in the REIT for the foreseeable future.

The primary objectives of the REIT are to: (a) provide holders of Units (‘‘Unitholders’’) with stable, predictable and growingmonthly cash distributions on a tax-efficient basis; (b) enhance the value of the REIT’s assets in order to maximize long-termUnitholder value; and (c) expand the REIT’s asset base while also increasing the REIT’s adjusted funds from operations (‘‘AFFO’’)per Unit, including through accretive acquisitions. The REIT initially intends to make monthly cash distributions of $ � perUnit to Unitholders, which are estimated to be approximately 90% of the REIT’s AFFO, on an annual basis, during the periodfrom July 1, 2015 to June 30, 2016 (the ‘‘Forecast Period’’). See ‘‘Non-IFRS Measures’’ and ‘‘Distribution Policy’’. The REITintends to pay monthly cash distributions, initially expected to provide Unitholders with an annual yield ranging fromapproximately 7.5% to 8.0% based on an AFFO payout ratio of approximately 90%.

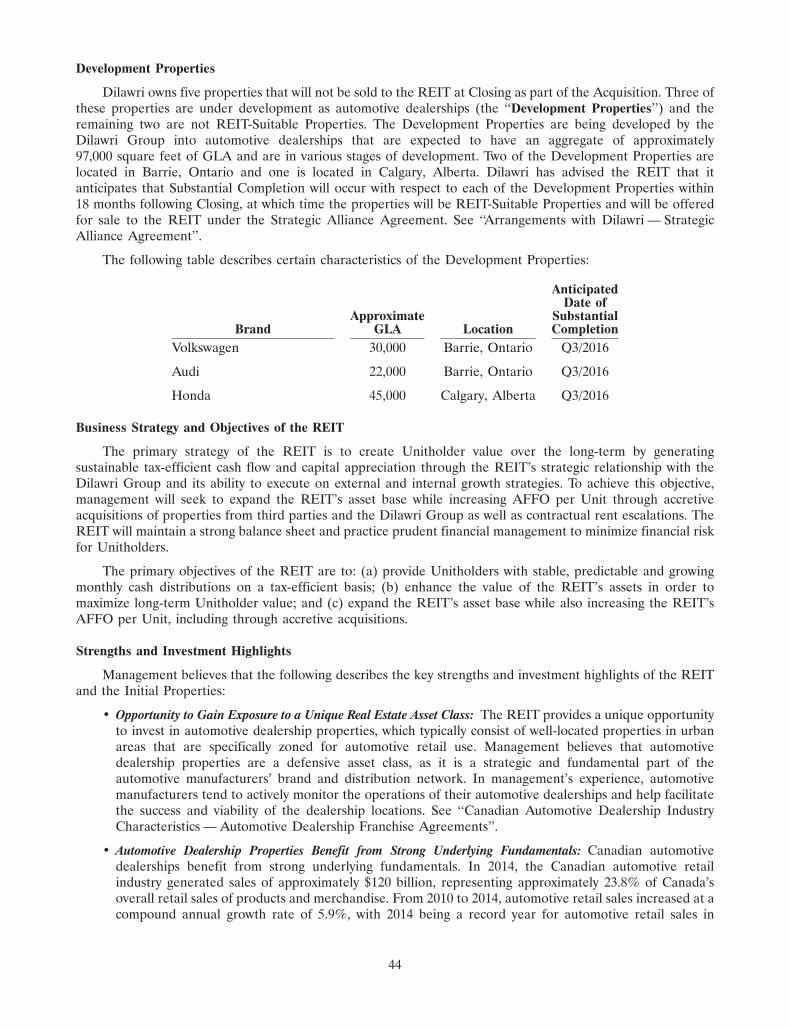

The primary strategy of the REIT is to create Unitholder value over the long-term by generating sustainable tax-efficient cash flowand capital appreciation through the REIT’s strategic relationship with the Dilawri Group and its ability to execute on external andinternal growth strategies. To achieve this objective, management will seek to expand the REIT’s asset base while increasing AFFOper Unit through accretive acquisitions of properties from third parties and the Dilawri Group as well as contractual rentescalations. Although the REIT expects that the majority of its acquisitions will be from third party vendors, the REIT also intendsto pursue acquisitions from the Dilawri Group pursuant to a strategic alliance agreement with Dilawri (the ‘‘Strategic AllianceAgreement’’) to be entered into on Closing. Under the terms of the Strategic Alliance Agreement, any property that is acquired,developed, redeveloped, refurbished or repositioned by a member of the Dilawri Group following Closing, including theDevelopment Properties (as defined herein) that is, in each case, determined by Dilawri, acting reasonably, to be a REIT-SuitableProperty must be offered for sale to the REIT within 90 days of the acquisition of such REIT-Suitable Property by the DilawriGroup or upon Substantial Completion (as defined herein) of such property, as applicable. The Dilawri Group currently has threeproperties under development that will be offered to the REIT upon Substantial Completion and which will have an aggregate ofapproximately 97,000 square feet of GLA. In addition, the REIT will have a right of first offer to purchase any REIT-SuitableProperty owned by a member of the Dilawri Group that it decides to sell. See ‘‘Growth Strategies of the REIT’’ and ‘‘Arrangementswith Dilawri — Strategic Alliance Agreement’’.

The REIT will be externally administered on a cost-recovery basis by Dilawri pursuant to the Administration Agreement(as defined herein). The REIT’s President and Chief Executive Officer and the Chief Financial Officer are currently employees ofa Subsidiary of Dilawri whose services will be provided to the REIT pursuant to the Administration Agreement. The President andChief Executive Officer of the REIT is a new employee of such Dilawri Subsidiary specifically recruited by Dilawri for this role.The President and Chief Executive Officer and the Chief Financial Officer will be supported by Dilawri personnel with experiencein property acquisitions and dispositions, development and finance. If and as requested by the REIT, Dilawri will provide, or causeto be provided, other support services, including certain administrative services, to the REIT, on a cost-recovery basis, pursuant tothe Administration Agreement. See ‘‘Arrangements with Dilawri — Administration Agreement’’.

Price: $10.00 per UnitPrice to the Underwriters’ Net Proceeds to

Public(1) Fee the REIT(2)

Per Unit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $10.00 $0.60 $9.40Total Offering(3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $� $� $�

Notes:

(1) The price of the Units was established by negotiation among the REIT, Dilawri and the Underwriters (as defined below) and has been determined, inpart, based on the forecasted net earnings and the resulting calculation of AFFO for the Forecast Period. See ‘‘Financial Forecast’’.

(2) Before deducting the REIT’s expenses of the Offering, estimated to be $ � , which, together with the Underwriters’ fee, will be paid from theproceeds of the Offering.

(3) The REIT has granted the Underwriters an option (the ‘‘Over-Allotment Option’’), exercisable in whole or in part at any one time up to 30 days afterClosing, to purchase up to an additional � Units at the Offering Price, solely to cover the Underwriters’ over-allocation position, if any, and formarket stabilization purposes. If the Over-Allotment Option is exercised in full, the total ‘‘Price to the Public’’, ‘‘Underwriters’ Fee’’ and ‘‘Net Proceedsto the REIT’’, before deducting the expenses of the Offering, will be $ � , $ � and $ � , respectively. This prospectus also qualifies the grantof the Over-Allotment Option and the Units issuable upon the exercise of the Over-Allotment Option. A purchaser who acquires Units forming part ofthe Underwriters’ over-allocation position acquires those Units under this prospectus, regardless of whether the over-allocation position is ultimatelyfilled through the exercise of the Over-Allotment Option or secondary market purchases. See ‘‘Plan of Distribution’’.

(continued from cover)

The following table sets out the number of Units that may be issued to the Underwriters pursuant to the Over-Allotment Option.

Maximum Sizeor Number of

Underwriters’ Position Securities Available Exercise Period Exercise Price

Over-Allotment Option . . . . . . . . . . . . . . . Option to acquire up to Exercisable at any one time up to $10.00 per Unit� Units 30 days after Closing

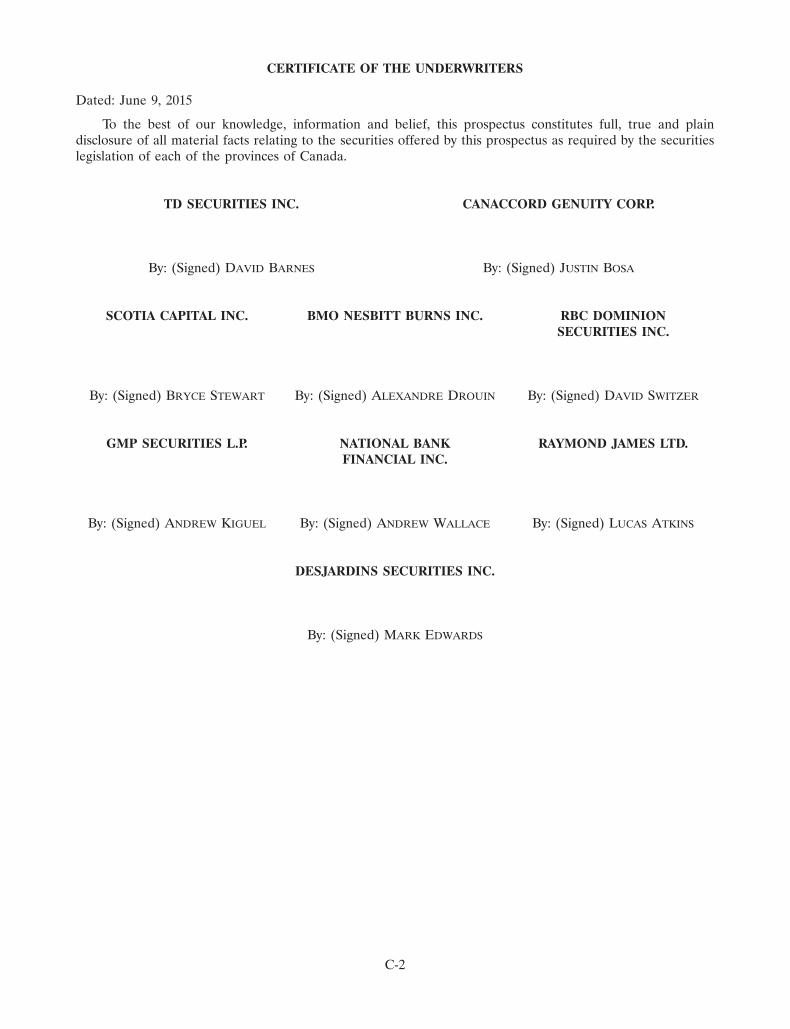

TD Securities Inc. (‘‘TDSI’’), Canaccord Genuity Corp. (‘‘CG’’ and, together with TDSI, the ‘‘Lead Underwriters’’), ScotiaCapital Inc. (‘‘SCI’’), BMO Nesbitt Burns Inc. (‘‘BMONB’’), RBC Dominion Securities Inc. (‘‘RBCDS’’), GMP Securities L.P.,National Bank Financial Inc., Raymond James Ltd. and Desjardins Securities Inc. (and, together with the Lead Underwriters, the‘‘Underwriters’’), as principals, conditionally offer the Units qualified under this prospectus, subject to prior sale, if, as and whenissued by the REIT and accepted by the Underwriters in accordance with the conditions contained in the underwriting agreementbetween the REIT, Dilawri and the Underwriters referred to under ‘‘Plan of Distribution’’ and subject to the approval of certainlegal matters on behalf of the REIT by Torys LLP and on behalf of the Underwriters by Blake, Cassels & Graydon LLP.

In connection with this distribution, the Underwriters have been granted the Over-Allotment Option and may, subject to applicablelaw, over-allocate or effect transactions which stabilize or maintain the market price of the Units at levels other than those whichotherwise might prevail on the open market. The Underwriters may offer the Units at a price lower than that stated above. See‘‘Plan of Distribution’’.

Subscriptions will be received subject to rejection or allocation in whole or in part and the Underwriters reserve the right to closethe subscription books at any time without notice. Closing is expected to occur on � , 2015 or such other date as the REIT andthe Lead Underwriters may agree, but in any event no later than � , 2015. Registrations and transfers of Units will be effectedelectronically through the non-certificated inventory system administered by CDS Clearing and Depository Services Inc. Beneficialowners of Units will not, except in certain limited circumstances, be entitled to receive physical certificates evidencing theirownership of Units. See ‘‘Declaration of Trust and Description of REIT Units — Non-Certificated Inventory System’’ and ‘‘Plan ofDistribution’’.

There is no market through which the Units may be sold and purchasers may not be able to resell Units purchased under thisprospectus. This may affect the pricing of the Units in the secondary market, the transparency and availability of trading prices, theliquidity of the Units and the extent of issuer regulation. See ‘‘Risk Factors’’.

A return on a purchaser’s investment in Units is not comparable to the return on an investment in a fixed income security. Therecovery of the initial investment in Units by an investor is at risk, and the anticipated return on an investment is based on manyperformance assumptions. Although the REIT intends to make distributions of available cash to Unitholders in accordance with itsdistribution policy, these cash distributions are not guaranteed and may be reduced or suspended at the discretion of the trustees ofthe REIT (the ‘‘Trustees’’). The ability of the REIT to make distributions and the actual amount distributed on Units will dependon numerous factors, including the financial performance of the REIT’s properties, debt covenants and other contractualobligations, working capital requirements and future capital requirements, all of which are subject to a number of risks. In addition,the market value of the Units may decline if the REIT is unable to meet its cash distribution and AFFO targets in the future, andthat decline may be significant. It is important for a person making an investment in Units to consider the particular risk factorsthat may affect the REIT, its business and the real estate industry, and therefore the stability of distributions to Unitholders. Aprospective purchaser should therefore review this document in its entirety and carefully consider the risk factors described under‘‘Risk Factors’’ before purchasing Units.

The after-tax return from an investment in Units to an investor subject to Canadian federal income tax will depend, in part, on thecomposition for income tax purposes of distributions made by the REIT, portions of which may be fully or partially taxable or mayconstitute tax deferred returns of capital (i.e., returns that initially are non-taxable but which reduce the adjusted cost base of aholder’s Units). The REIT estimates that approximately 100% of the monthly cash distributions to be made by the REIT toUnitholders will be tax-deferred in 2015. That composition may change over time, thus affecting the after-tax return toUnitholders. See ‘‘Certain Canadian Federal Income Tax Considerations’’.

SCI, BMONB and RBCDS are affiliates of Canadian chartered banks that are expected to provide the REIT with the CreditFacilities (as defined herein) at Closing. Consequently, the REIT may be considered a ‘‘connected issuer’’ of each of SCI, BMONBand RBCDS under applicable Canadian securities laws. See ‘‘Debt Strategy and Indebtedness’’ and ‘‘Plan of Distribution’’.

The REIT is not a trust company and is not registered under applicable legislation governing trust companies as it does not carryon or intend to carry on the business of a trust company. The Units are not ‘‘deposits’’ within the meaning of the Canada DepositInsurance Corporation Act and are not insured under the provisions of that statute or any other legislation.

On Closing, one right will be issued and attached to each outstanding Unit pursuant to the Unitholders’ rights plan of the REIT.See ‘‘Unitholders’ Rights Plan’’.

The principal, registered and head office of the REIT is located at 133 King Street East, Suite 300, Toronto, Ontario, M5C 1G6.

TABLE OF CONTENTS

Page Page

GLOSSARY . . . . . . . . . . . . . . . . . . . . . . . . 8 THE PARTNERSHIP . . . . . . . . . . . . . . . . . 127

ABOUT THIS PROSPECTUS . . . . . . . . . . 17 DISTRIBUTION POLICY . . . . . . . . . . . . . 130

MEANING OF CERTAIN REFERENCES . 18 UNITHOLDERS’ RIGHTS PLAN . . . . . . . 131

MARKET AND INDUSTRY DATA . . . . . . 18 CERTAIN CANADIAN FEDERALINCOME TAX CONSIDERATIONS . . . . 135FORWARD-LOOKING STATEMENTS . . . 18

NON-IFRS MEASURES . . . . . . . . . . . . . . 20 PLAN OF DISTRIBUTION . . . . . . . . . . . . 142

ELIGIBILITY FOR INVESTMENT . . . . . . 21 PRIOR ISSUANCES . . . . . . . . . . . . . . . . . 144

PROSPECTUS SUMMARY . . . . . . . . . . . . 22 USE OF PROCEEDS . . . . . . . . . . . . . . . . 145THE OFFERING . . . . . . . . . . . . . . . . . . . 39 RISK FACTORS . . . . . . . . . . . . . . . . . . . . 145THE REIT . . . . . . . . . . . . . . . . . . . . . . . . 42

MATERIAL CONTRACTS . . . . . . . . . . . . 164GROWTH STRATEGIES OF THE REIT . . 46

INTERESTS OF MANAGEMENT ANDCANADIAN AUTOMOTIVE OTHERS IN MATERIAL

DEALERSHIP INDUSTRY TRANSACTIONS . . . . . . . . . . . . . . . . . . 165CHARACTERISTICS . . . . . . . . . . . . . . . 48

PROMOTER . . . . . . . . . . . . . . . . . . . . . . . 165ASSETS OF THE REIT . . . . . . . . . . . . . . . 55

PRINCIPAL UNITHOLDER . . . . . . . . . . . 165ACQUISITION OF THE INITIALPROPERTIES . . . . . . . . . . . . . . . . . . . . 75 MANAGEMENT’S DISCUSSION AND

ANALYSIS OF FINANCIALASSESSMENTS AND VALUATIONS OFCONDITION AND RESULTS OFTHE INITIAL PROPERTIES . . . . . . . . . 76OPERATIONS OF THE THIRD PARTY

RETAINED INTEREST . . . . . . . . . . . . . . . 79 TENANT PORTFOLIO . . . . . . . . . . . . . 165

DEBT STRATEGY AND INDEBTEDNESS 82 LEGAL PROCEEDINGS ANDREGULATORY ACTIONS . . . . . . . . . . . 172ARRANGEMENTS WITH DILAWRI . . . . 86

LEGAL MATTERS . . . . . . . . . . . . . . . . . . 172CAPITALIZATION OF THE REIT . . . . . . 91

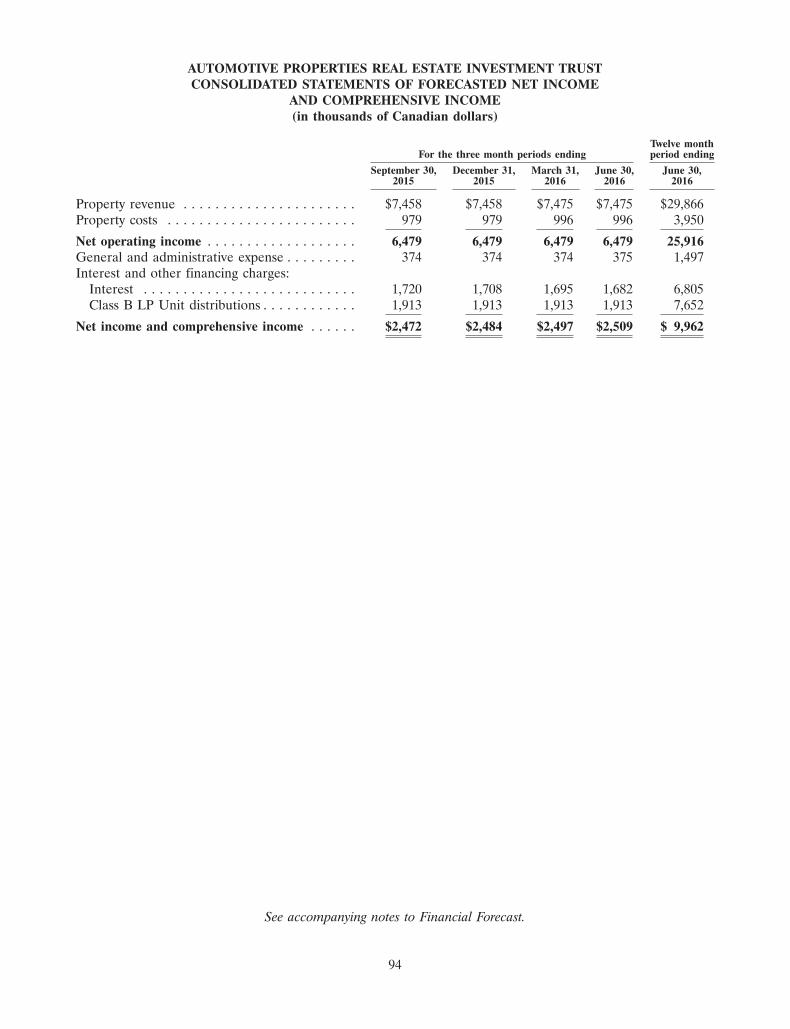

EXPERTS . . . . . . . . . . . . . . . . . . . . . . . . . 172FINANCIAL FORECAST . . . . . . . . . . . . . 92

REPORT ON CONSOLIDATED AUDITORS AND TRANSFER AGENTFINANCIAL FORECAST . . . . . . . . . . . . 93 AND REGISTRAR . . . . . . . . . . . . . . . . 173

FORECAST NON-IFRS PURCHASERS’ STATUTORY RIGHTS . . . 173RECONCILIATION . . . . . . . . . . . . . . . . 102

INDEX TO FINANCIAL STATEMENTS . . F-1TRUSTEES AND MANAGEMENT OF

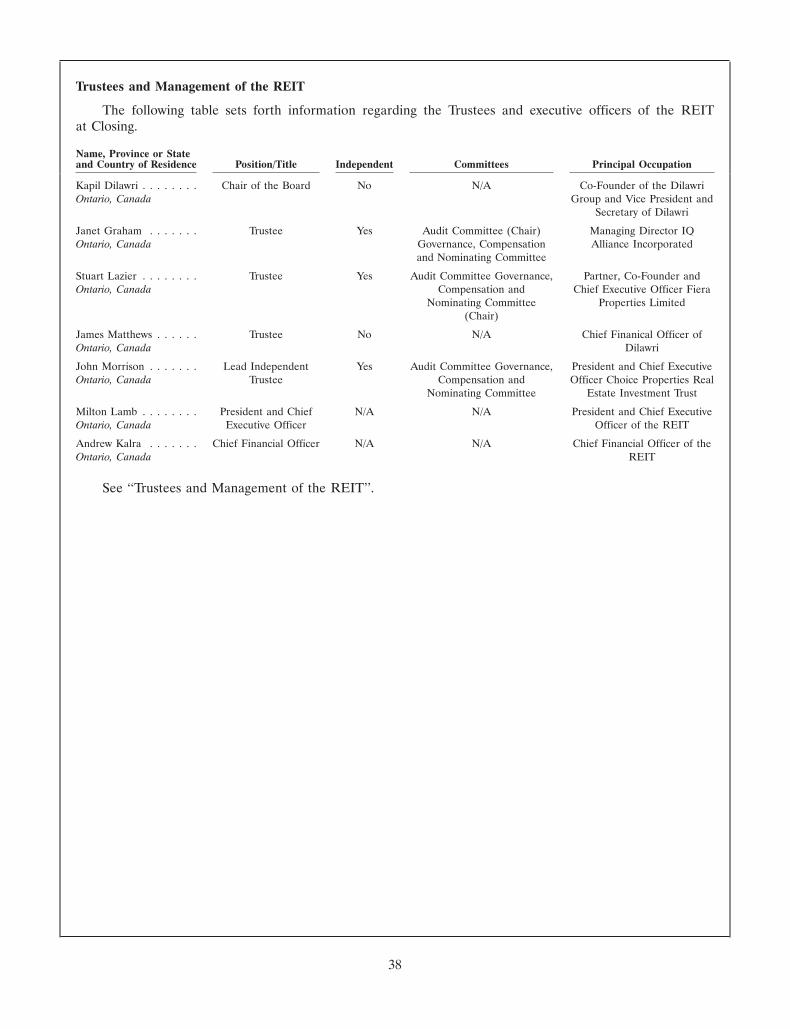

THE REIT . . . . . . . . . . . . . . . . . . . . . . . 103 APPENDIX A — BOARD MANDATE . . . . A-1

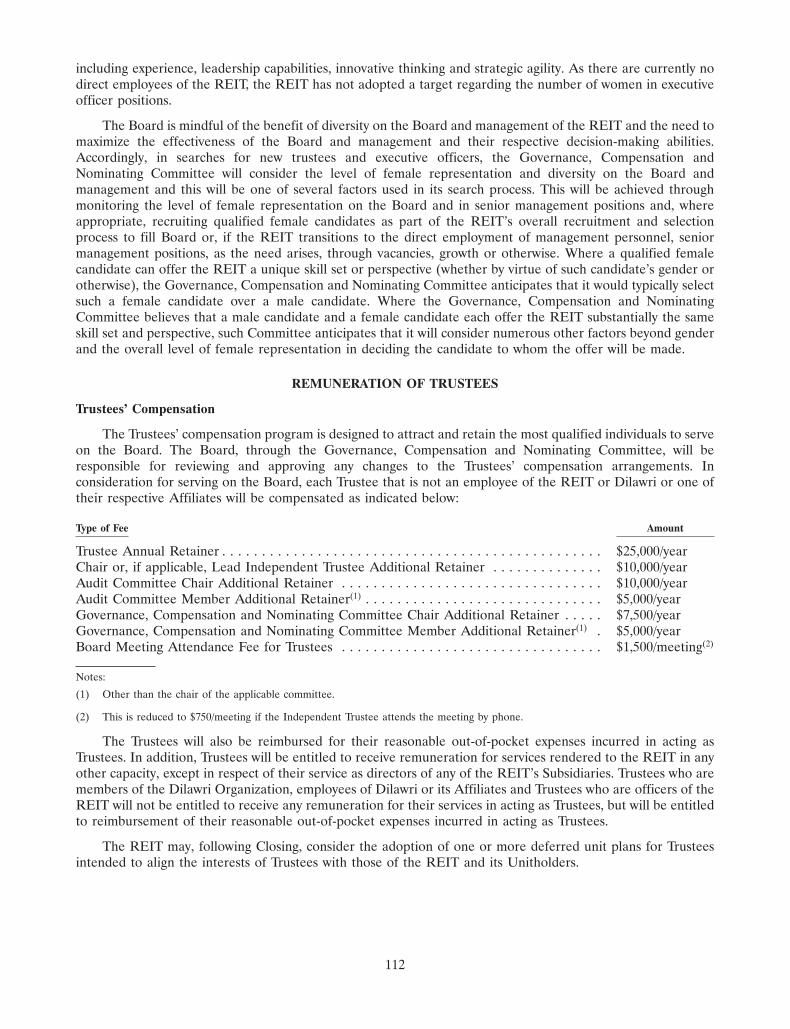

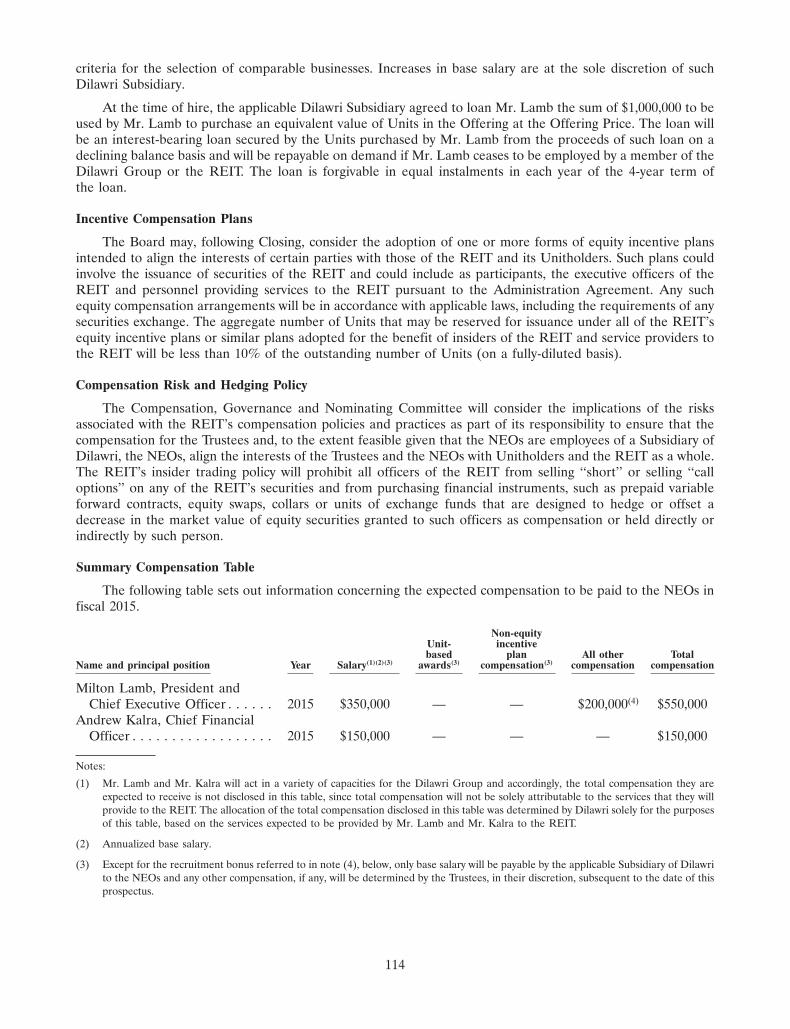

REMUNERATION OF TRUSTEES . . . . . . 112 APPENDIX B — AUDIT COMMITTEECHARTER . . . . . . . . . . . . . . . . . . . . . . . B-1EXECUTIVE COMPENSATION . . . . . . . . 113

CERTIFICATE OF THE REIT AND THEINVESTMENT GUIDELINES ANDPROMOTER . . . . . . . . . . . . . . . . . . . . . C-1OPERATING POLICIES . . . . . . . . . . . . 115

DECLARATION OF TRUST AND CERTIFICATE OF THEDESCRIPTION OF REIT UNITS . . . . . . 118 UNDERWRITERS . . . . . . . . . . . . . . . . . C-2

7

GLOSSARY

‘‘Acquired Issuer’’ has the meaning given to that term under ‘‘Investment Guidelines and Operating Policies —Investment Guidelines’’.

‘‘Acquiring Person’’ has the meaning given to that term under ‘‘Unitholders’ Rights Plan — Acquiring Person’’.

‘‘Acquisition’’ has the meaning given to that term under ‘‘About This Prospectus’’.

‘‘Acquisition ROFO’’ has the meaning given to that term under ‘‘Arrangements with Dilawri — Strategic AllianceAgreement’’.

‘‘Adjusted EBITDA’’ means the earnings of the Dilawri Group before interest, taxes, depreciation andamortization and adding back thereto employee bonus payments and bonus payments made to the shareholdersof Dilawri, all as reflected in the audited or reviewed, as applicable, non-consolidated combined financialstatements of the Dilawri Group prepared in accordance with the recognition, measurement and disclosureprinciples of Canadian accounting standards for private enterprises (ASPE).

‘‘Adjusted Rent Coverage Ratio’’ is calculated by Dilawri as Adjusted EBITDA for the 2014 fiscal year adding backto that amount the sum of distributions estimated to be received by the Dilawri Group during the ForecastPeriod on the Class B LP Units to be issued to it in the Acquisition and rent paid by the Dilawri Group in 2014to third parties. That resultant figure is divided by the rent paid by the Dilawri Group in the 2014 fiscal year onits properties, including inter-company rents paid on the Initial Properties.

‘‘Administration Agreement’’ means the administration agreement among the REIT, the Partnership, Dilawri anda Subsidiary of Dilawri to be entered into at Closing pursuant to which Dilawri will provide, or cause to beprovided, the Services, as described under ‘‘Arrangements with Dilawri — Administration Agreement’’.

‘‘Advance Notice Provision’’ has the meaning given to that term under ‘‘Declaration of Trust and Description ofREIT Units — Nomination of Trustees’’.

‘‘Affiliate’’ has the meaning given to that term in National Instrument 45-106 — Prospectus and RegistrationExemptions, subject to the term ‘‘issuer’’ in such instrument being ascribed the same meaning as the term‘‘person’’ in such instrument.

‘‘AFFO’’ has the meaning given to that term under ‘‘Non-IFRS Measures’’.

‘‘Agincourt Mazda’’ means the Initial Property municipally known as 5500 Finch Avenue East in Toronto, Ontario.

‘‘Annuitant’’ has the meaning given to that term under ‘‘Eligibility for Investment’’.

‘‘Appraisal’’ means the estimate of the fair market value of the Initial Properties provided by the Appraiser, asdescribed under ‘‘Assessments and Valuations of the Initial Properties — Independent Valuations’’.

‘‘Appraiser’’ means Cushman & Wakefield Ltd.

‘‘Audi Sales Downtown Vancouver’’ means the Initial Property municipally known as 1788 West 2nd Avenue inVancouver, British Columbia.

‘‘BCA Reports’’ means the building condition assessment reports prepared for all but one of the Initial Properties,as described under ‘‘Assessments and Valuations of the Initial Properties — Building Condition Assessments’’.

‘‘BMONB’’ means BMO Nesbitt Burns Inc.

‘‘Board’’ means the board of trustees of the REIT.

‘‘Bolton Toyota’’ means the Initial Property municipally known as 12050 Albion Vaughan Road in Bolton, Ontario.

‘‘Burrard Acura’’ means the Initial Property municipally known as 730 Terminal Avenue in Vancouver, BritishColumbia.

‘‘Calgary BMW’’ means the Initial Property municipally known as 34 Heritage Meadows Road S.E. in Calgary,Alberta.

8

‘‘Calgary Honda’’ means the Initial Property municipally known as 11700 Lake Fraser Drive S.E. in Calgary,Alberta.

‘‘Capital Lease Obligation’’ of any person means the obligation of such person, as lessee, to pay rent or otherpayment amounts under a lease of real or personal property which is required to be classified and accounted foras a finance lease or a liability on a consolidated balance sheet of such person in accordance with IFRS.

‘‘Cash NOI’’ has the meaning given to that term under ‘‘Non-IFRS Measures’’.

‘‘CBCA’’ means the Canada Business Corporation Act, as amended.

‘‘CCA’’ has the meaning given to that term under ‘‘Certain Canadian Federal Income Tax Considerations —Status of the REIT — Qualification as a ‘‘Real Estate Investment Trust’’ ’’.

‘‘CDS’’ means CDS Clearing and Depository Services Inc.

‘‘CG’’ means Canaccord Genuity Corp.

‘‘CICA’’ means the Canadian Institute of Chartered Accountants.

‘‘Class A LP Preferred Distribution’’ has the meaning given to that term under ‘‘The Partnership —Distributions’’.

‘‘Class A LP Units’’ means, collectively, the Class A limited partnership units of the Partnership.

‘‘Class B LP Units’’ means, collectively, the Class B limited partnership units of the Partnership, and ‘‘Class BLP Unit’’ means any one of them.

‘‘Closing’’ means the closing of the Offering and the Acquisition and other related transactions, the materialterms of which are described in this prospectus.

‘‘Closing Date’’ means � , 2015, or such other date as the REIT and the Lead Underwriters may agree, but inany event no later than � , 2015.

‘‘Closing Market Price’’ has the meaning given to that term under ‘‘Declaration of Trust and Description of REITUnits — Redemption Right’’.

‘‘Code of Conduct’’ has the meaning given to that term under ‘‘Trustees and Management of the REIT — Trusteesand Executive Officers’’.

‘‘Competing Permitted Bid’’ has the meaning given to that term under ‘‘Unitholders’ Rights Plan — Permitted BidRequirements’’.

‘‘Contribution Agreement’’ means the agreement to be entered into on or before Closing pursuant to which theREIT will indirectly acquire the Initial Properties, as described under ‘‘Acquisition of the Initial Properties —Contribution Agreement’’.

‘‘Contribution Agreement Cap’’ has the meaning given to that term under ‘‘Acquisition of the Initial Properties —Contribution Agreement’’.

‘‘Control’’ means the possession by any person, of the ownership, control or direction, directly or indirectly, of50% or more of the outstanding voting securities of a person, or in the case of a limited partnership, thepossession by any person of the ownership, control or direction, directly or indirectly, of 50% or more of theoutstanding voting securities of the general partner; and each of ‘‘Controlled by’’ or ‘‘Controlling’’ has acorresponding meaning.

‘‘CRA’’ means the Canada Revenue Agency.

‘‘Credit Facilities’’ means, collectively, Loan Facility 1, Loan Facility 2 and Loan Facility 3.

‘‘Declaration of Trust’’ means the declaration of trust of the REIT dated as of June 1, 2015, as it will be amendedand restated on or prior to Closing, as described under ‘‘Declaration of Trust and Description of REIT Units’’.

‘‘Demand Distribution’’ has the meaning given to that term under ‘‘Retained Interest — Registration Rights’’.

9

‘‘Demand Registration Right’’ has the meaning given to that term under ‘‘Retained Interest — RegistrationRights’’.

‘‘Development Properties’’ means, collectively, two properties located in Barrie, Ontario and one property locatedin Calgary, Alberta, in which the Dilawri Group currently holds 100% interests and which are underdevelopment as automotive dealerships and which, upon Substantial Completion, will be REIT-SuitableProperties having an aggregate of approximately 97,000 square feet of GLA.

‘‘Dilawri’’ means 893353 Alberta Inc., an entity formed pursuant to the Business Corporations Act (Alberta) onSeptember 20, 2000, that indirectly owns (or co-owns, in two cases) the Initial Properties.

‘‘Dilawri Acura’’ means the Initial Property municipally known as 1921 1st Avenue in Regina, Saskatchewan.

‘‘Dilawri BMW’’ means the Initial Property municipally known as 1919 1st Avenue in Regina, Saskatchewan.

‘‘Dilawri Dealership Properties’’ has the meaning given to that term under ‘‘About This Prospectus’’.

‘‘Dilawri Group’’ means Dilawri and its Affiliates, other than any shareholder of Dilawri or any other person thatControls Dilawri.

‘‘Dilawri Leases’’ and ‘‘Dilawri Lease’’ have the meanings given to them under ‘‘Assets of the REIT — Descriptionof the Material Terms of the Dilawri Leases’’.

‘‘Dilawri Mitsubishi’’ means the Initial Property municipally known as 1750 6th Avenue in Regina, Saskatchewan.

‘‘Dilawri Nissan Infiniti’’ means the Initial Property municipally known as 1775 5th Avenue in Regina,Saskatchewan.

‘‘Dilawri Organization’’ means, collectively, (i) Dilawri, any person Controlled by Dilawri or under commonControl with Dilawri or any other member of the Dilawri Organization; (ii) any persons who are beneficiaries ofa discretionary trust that Controls Dilawri on the Closing Date or any of such beneficiaries’ respective spouses,sons, daughters, sons-in-law, daughters-in-law, parents and siblings, or their respective spouses, sons, daughters,sons-in-law and daughters-in-law; and (iii) any trust, the majority of the trustees or beneficiaries of which are anyone or more members of the Dilawri Organization and/or any person Controlled by any one or more membersof the Dilawri Organization.

‘‘Dilawri Tenant’’ has the meaning given to that term under ‘‘Assets of the REIT — Description of the MaterialTerms of the Dilawri Leases’’.

‘‘Distinctive Collection’’ means the Initial Property municipally known as 150 Glendeer Circle S.E. in Calgary,Alberta.

‘‘Distribution Date’’ means, in respect of a calendar month, on or about the 15th day of the following calendarmonth or such other date as the Trustees so determine in their discretion.

‘‘Dixie Auto Mall’’ means the Initial Property municipally known as 5500 Dixie Road, 5505, 5515, 5525 and5500 Ambler Drive, and 1465, 1475, 1485 and 1495 Aerowood Drive in Mississauga, Ontario.

‘‘Dixie Industrial Property’’ has the meaning given to that term under ‘‘About This Prospectus’’.

‘‘DRIP’’ means a distribution reinvestment plan of the REIT, if any.

‘‘Equivalent Securities’’ means exchangeable securities attached to Special Voting Units, as more particularlydescribed under ‘‘Unitholders’ Rights Plan — Permitted Bid Requirements’’.

‘‘Exchange Agreement’’ means the agreement to be entered into at Closing pursuant to which the holders ofClass B LP Units will be granted, among other things, the right to require the REIT to exchange each Class BLP Unit held thereby for one Unit (subject to certain anti-dilution adjustments) as described under ‘‘RetainedInterest — Exchange Rights’’.

‘‘Exempt Plans’’ has the meaning given to that term under ‘‘Eligibility for Investment’’.

‘‘FFO’’ has the meaning given to that term under ‘‘Non-IFRS Measures’’.

10

‘‘Financial Forecast’’ means the financial forecast of the REIT contained under ‘‘Financial Forecast’’.

‘‘Flip-in Event’’ has the meaning given to that term under ‘‘Unitholders’ Rights Plan — Rights Exercise Privilege’’.

‘‘Floorplan Debt’’ means revolving debt provided to the Dilawri Group to finance its vehicle inventory.

‘‘Forecast Period’’ means the forecast period contemplated under ‘‘Financial Forecast’’, being the period fromJuly 1, 2015 to June 30, 2016.

‘‘Frost Chevrolet Buick GMC Cadillac’’ means the Initial Property municipally known as 150 Bovaird Drive Westin Brampton, Ontario.

‘‘GBV’’ means, at any time, the greater of (A) the book value of the assets of the REIT and its consolidatedsubsidiaries, as shown on its then most recent consolidated balance sheet, less the amount of any receivablereflecting interest rate subsidies on any debt assumed by the REIT; and (B) the historical cost of the investmentproperties, plus (i) the carrying value of cash and cash equivalents, (ii) the carrying value of mortgagesreceivable; and (iii) the historical cost of other assets and investments used in operations.

‘‘General Partner’’ has the meaning given to that term under ‘‘The Partnership — General’’.

‘‘GLA’’ means gross leasable area.

‘‘GP Interest’’ has the meaning given to that term under ‘‘The Partnership — Partnership Units’’.

‘‘GP Unit’’ means a unit representing the GP Interest in the Partnership.

‘‘Grandfathered Person’’ has the meaning given to that term under ‘‘Unitholders’ Rights Plan — AcquiringPerson’’.

‘‘GTA’’ means the greater Toronto area.

‘‘GVA’’ means the greater Vancouver area.

‘‘Holder’’ has the meaning given to that term under ‘‘Certain Canadian Federal Income Tax Considerations’’.

‘‘Honda Used Car and Regina Collision Centre’’ means the Initial Property municipally known as 815 BroadStreet in Regina, Saskatchewan.

‘‘Hyundai Gallery’’ means the Initial Property municipally known as 11770 Lake Fraser Drive S.E. in Calgary,Alberta.

‘‘IAS 39’’ has the meaning given to that term under ‘‘Management’s Discussion and Analysis of FinancialCondition and Results of Operations of the Third Party Tenant Portfolio’’.

‘‘IASB’’ has the meaning given to that term under ‘‘Management’s Discussion and Analysis of FinancialCondition and Results of Operations of the Third Party Tenant Portfolio’’.

‘‘IFRS’’ means International Financial Reporting Standards as issued by the International Accounting StandardsBoard and as adopted by the CICA in Part I of The Canadian Institute of Chartered Accountants Handbook —Accounting, as amended from time to time.

‘‘IFRS 15’’ has the meaning given to that term under ‘‘Management’s Discussion and Analysis of FinancialCondition and Results of Operations of the Third Party Tenant Portfolio’’.

‘‘Indebtedness’’ of any person means (without duplication) (i) any obligation of such person for borrowed money(including, for greater certainty, the full principal amount of convertible debt, notwithstanding its presentationunder IFRS), (ii) any obligation of such person incurred in connection with the acquisition of property, assets orbusinesses, (iii) any obligation of such person issued or assumed as the deferred purchase price of property,(iv) any Capital Lease Obligation of such person, and (v) any obligations of the type referred to in clauses (i)through (iv) of another person, the payment of which such person has guaranteed or for which such person isresponsible or liable; provided that, (A) for the purpose of clauses (i) through (v) (except in respect ofconvertible debt, as described above), an obligation will constitute Indebtedness of such person only to theextent that it would appear as a liability on the consolidated balance sheet of such person in accordance withIFRS, (B) obligations referred to in clauses (i) through (iii) exclude trade accounts payable, distributions

11

payable to Unitholders or holders of other securities excluded from the definition of Indebtedness pursuant toclause (C) below, accrued liabilities arising in the ordinary course of business which are not overdue or which arebeing contested in good faith, deferred revenues, intangible liabilities, deferred income taxes, deferred financingcosts, tenant deposits and indebtedness with respect to the unpaid balance of installment receipts where suchindebtedness has a term not in excess of 12 months, and (C) Units, Class A LP Units, Class B LP Units,exchangeable securities and other equity securities that constitute debt under IFRS do not constituteIndebtedness.

‘‘Independent Trustee’’ means a Trustee who is ‘‘independent’’ pursuant to National Instrument 58-101 —Disclosure of Corporate Governance Practices.

‘‘Independent Unitholders’’ has the meaning given to that term under ‘‘Unitholders’ Rights Plan — Permitted BidRequirements’’.

‘‘Infiniti Vancouver’’ means the Initial Property municipally known as 1718 West 3rd Avenue in Vancouver, BritishColumbia.

‘‘Initial Properties’’ means the portfolio of 26 commercial properties located in Ontario, Saskatchewan, Albertaand British Columbia totaling approximately 958,000 square feet of GLA that the REIT will indirectly acquirethrough the Partnership on Closing, but does not include the Dixie Industrial Property, and ‘‘Initial Property’’means any one of them.

‘‘Issued Securities’’ has the meaning given to that term under ‘‘Retained Interest — Pre-Emptive Rights’’, and‘‘Issued Security’’ means any one of them.

‘‘Langley Acura’’ means the Initial Property municipally known as 20257 Langley Bypass in Langley, BritishColumbia.

‘‘Lead Independent Trustee’’ refers to the Independent Trustee who is responsible for ensuring the appropriateleadership for the Independent Trustees, as further described under ‘‘Trustees and Management of the REIT —Trustees and Executive Officers’’.

‘‘Lead Underwriters’’ means, collectively, TDSI and CG.

‘‘Limited Partners’’ and ‘‘Limited Partner’’ have the meanings given to them under ‘‘The Partnership —General’’.

‘‘Limited Partnership Agreement’’ means the amended and restated limited partnership agreement governing thePartnership to be dated as of the Closing Date.

‘‘Loan Facility 1’’ has the meaning given to that term under ‘‘Debt Strategy and Indebtedness — Composition ofIndebtedness’’.

‘‘Loan Facility 2’’ has the meaning given to that term under ‘‘Debt Strategy and Indebtedness — Composition ofIndebtedness’’.

‘‘Loan Facility 3’’ has the meaning given to that term under ‘‘Debt Strategy and Indebtedness — Composition ofIndebtedness’’.

‘‘Lock-up Period’’ has the meaning given to that term under ‘‘Prospectus Summary — The Offering’’.

‘‘LRE’’ has the meaning given to that term under ‘‘Risk Factors — Risk Factors Related to the Offering andStructure of the REIT — Tax-Related Risk Factors’’.

‘‘Market Price’’ has the meaning given to that term under ‘‘Declaration of Trust and Description of REIT Units —Redemption Right’’.

‘‘Markham Acura’’ means the Initial Property municipally known as 5201 Highway 7 East in Markham, Ontario.

‘‘Markham Honda and Ford’’ means the Initial Property municipally known as 8210 Kennedy Road and8220 Kennedy Road in Markham, Ontario.

12

‘‘MD&A’’ has the meaning given to that term under ‘‘Management’s Discussion and Analysis of FinancialCondition and Results of Operations of the Third Party Tenant Portfolio’’.

‘‘Meadowvale Honda’’ means the Initial Property municipally known as 2210 Battleford Road in Mississauga,Ontario.

‘‘Monthly Limit’’ means the monthly limit on the total amount payable in cash by the REIT in respect of Unitstendered for redemption in a calendar month as described under ‘‘Declaration of Trust and Description of REITUnits — Redemption Right’’.

‘‘NCI’’ means the non-certificated inventory system administered by CDS.

‘‘NEOs’’ means the REIT’s named executive officers for the purposes of National Instrument 51-102 —Continuous Disclosure Obligations, as more particularly described under ‘‘Executive Compensation’’.

‘‘NI 52-110’’ has the meaning given to that term under ‘‘Trustees and Management of the REIT — Committees ofthe Board’’.

‘‘NOI’’ has the meaning given to that term under ‘‘Non-IFRS Measures’’.

‘‘Nominating Unitholder’’ has the meaning given to that term under ‘‘Declaration of Trust and Description ofREIT Units — Nomination of Trustees’’.

‘‘Non-Residents’’ means (i) non-residents of Canada, (ii) partnerships that are not Canadian partnerships, or(iii) a combination of non-residents and such partnerships (all within the meaning of the Tax Act).

‘‘Non-Revolving Facility 1’’ has the meaning given to that term under ‘‘Debt Strategy and Indebtedness —Composition of Indebtedness’’.

‘‘Non-Revolving Facility 2’’ has the meaning given to that term under ‘‘Debt Strategy and Indebtedness —Composition of Indebtedness’’.

‘‘Non-Revolving Credit Facilities’’ has the meaning given to that term under ‘‘Debt Strategy and Indebtedness —Composition of Indebtedness’’.

‘‘North Vancouver Nissan Infiniti’’ means the Initial Property municipally known as 819 Automall Drive in NorthVancouver, British Columbia.

‘‘Notice Date’’ has the meaning given to that term under ‘‘Declaration of Trust and Description of REIT Units —Nomination of Trustees’’.

‘‘Oakville Honda’’ means the Initial Property municipally known as 500 Iroquois Shore Road in Oakville, Ontario.

‘‘OBCA’’ means the Business Corporations Act (Ontario), as amended.

‘‘OEM’’ means original equipment manufacturer.

‘‘Offering’’ means the offering of Units pursuant to this prospectus.

‘‘Offering Price’’ means $10.00, being the price per Unit sold pursuant to the Offering.

‘‘Officer’s Certificate’’ has the meaning given to that term under ‘‘Certain Canadian Federal Income TaxConsiderations’’.

‘‘Over-Allotment Option’’ means the option granted to the Underwriters by the REIT, exercisable in whole or inpart and at any one time up to 30 days after Closing, to purchase up to an additional � Units at the OfferingPrice, solely to cover the Underwriters’ over-allocation position, if any, and for market stabilization purposes, asdescribed under ‘‘Plan of Distribution — General’’.

‘‘Partnership’’ means Automotive Properties Limited Partnership, a limited partnership to be formed under theLimited Partnership Act (Ontario).

‘‘Permitted Bid’’ has the meaning given to that term under ‘‘Unitholders’ Rights Plan — Permitted BidRequirements’’.

13

‘‘Phase I ESA Report’’ has the meaning given to that term under ‘‘Assessments and Valuations of the InitialProperties — Environmental Site Assessments’’.

‘‘Phase II ESA’’ has the meaning given to that term under ‘‘Assessments and Valuations of the Initial Properties —Environmental Site Assessments’’.

‘‘Piggy-Back Distribution’’ has the meaning given to that term under ‘‘Retained Interest — Registration Rights’’.

‘‘Piggy-Back Registration Right’’ has the meaning given to that term under ‘‘Retained Interest — RegistrationRights’’.

‘‘Porsche Centre Vancouver’’ means the Initial Property municipally known as 688 Terminal Avenue in Vancouver,British Columbia.

‘‘Pro Forma Adjusted Debt’’ is calculated by Dilawri as the Dilawri Group’s total debt reflected in its auditednon-consolidated combined financial statements as at December 31, 2014 prepared in accordance with therecognition, measurement and disclosure principles of Canadian accounting standards for private enterprises(ASPE) excluding Floorplan Debt, less debt related to the Initial Properties to be repaid by the applicablemember of the Dilawri Group in connection with the Acquisition.

‘‘RBCDS’’ means RBC Dominion Securities Inc.

‘‘REALpac’’ has the meaning given to that term under ‘‘Non-IFRS Measures’’.

‘‘Redemption Date’’ has the meaning given to that term under ‘‘Declaration of Trust and Description of REITUnits — Redemption Right’’.

‘‘Redemption Price’’ has the meaning given to that term under ‘‘Declaration of Trust and Description of REITUnits — Redemption Right’’.

‘‘Regina Honda’’ means the Initial Property municipally known as 789 Broad Street in Regina, Saskatchewan.

‘‘Regina Hyundai’’ means the Initial Property municipally known as 444 Broad Street in Regina, Saskatchewan.

‘‘Reimbursement Distribution Amount’’ has the meaning given to that term under ‘‘The Partnership —Distributions’’.

‘‘REIT’’ means Automotive Properties Real Estate Investment Trust and references in this prospectus to the‘‘REIT’’ should be interpreted as described under ‘‘Meaning of Certain References’’.

‘‘REIT Exception’’ means the exclusion from the definition of ‘‘SIFT trust’’ in the Tax Act for a trust qualifying as a‘‘real estate investment trust’’ under the Tax Act, as more particularly described under ‘‘Certain CanadianFederal Income Tax Considerations — Status of the REIT — Qualification as a ‘‘Real Estate Investment Trust’’‘.

‘‘REIT-Suitable Property’’ means any income-producing property in Canada or the United States which the REITwould be permitted to acquire or invest in within the terms set out in the ‘‘Investment Guidelines and OperatingPolicies’’ of the REIT’s Declaration of Trust and which property is ready for use on a long-term basis, or is beingused on a long-term basis, primarily as an automotive dealership or automotive repair facility, or, in the case of adisposition of an income-producing property by a member of the Dilawri Group to which the Sale ROFOapplies, is being ‘‘sold’’ for use on a long-term basis, primarily as an automotive dealership or automotive repairfacility.

‘‘Related Party’’ means, with respect to any person, a person who is a ‘‘related party’’ as that term is defined inMultilateral Instrument 61-101 — Protection of Minority Security Holders in Special Transactions, as amendedfrom time to time.

‘‘Report Package’’ has the meaning given to that term under ‘‘Assets of the REIT — Description of the MaterialTerms of the Dilawri Leases’’.

‘‘Revolving Facility 1’’ has the meaning given to that term under ‘‘Debt Strategy and Indebtedness — Compositionof Indebtedness’’.

14

‘‘Revolving Facility 2’’ has the meaning given to that term under ‘‘Debt Strategy and Indebtedness — Compositionof Indebtedness’’.

‘‘Revolving Credit Facilities’’ has the meaning given to that term under ‘‘Debt Strategy and Indebtedness —Composition of Indebtedness’’.

‘‘Right’’ means a right issued and attached to a Voting Unit pursuant to the Rights Plan.

‘‘Rights Plan’’ means the Unitholders’ Rights Plan to be adopted by the Board on Closing.

‘‘RRIF’’ has the meaning given to that term under ‘‘Eligibility for Investment’’.

‘‘RRSP’’ has the meaning given to that term under ‘‘Eligibility for Investment’’.

‘‘Sale ROFO’’ has the meaning given to that term under ‘‘Arrangements with Dilawri — Strategic AllianceAgreement’’.

‘‘SCI’’ means Scotia Capital Inc.

‘‘SEDAR’’ means the System for Electronic Documents Analysis and Retrieval at www.sedar.com.

‘‘Selected Amount’’ has the meaning given to that term under ‘‘The Partnership — Distributions’’.

‘‘Separation Time’’ has the meaning given to that term under ‘‘Unitholders’ Rights Plan — Rights ExercisePrivilege’’.

‘‘Services’’ means the services to be provided to the REIT pursuant to the Administration Agreement, asdescribed under ‘‘Arrangements with Dilawri — Administration Agreement’’.

‘‘SIFT Rules’’ means the rules applicable to SIFT trusts and SIFT partnerships in the Tax Act, as described under‘‘Certain Canadian Federal Income Tax Considerations — Status of the REIT — Qualification as a ‘‘Real EstateInvestment Trust’’‘.

‘‘Special Voting Units’’ means, collectively, special voting units of the REIT, and ‘‘Special Voting Unit’’ means anyone of them.

‘‘Strategic Alliance Agreement’’ means the strategic alliance agreement between the REIT and Dilawri to beentered into at Closing, as described under ‘‘Arrangements with Dilawri — Strategic Alliance Agreement’’.

‘‘Subsidiary’’ has the meaning given to that term in National Instrument 45-106 — Prospectus and RegistrationExemptions, subject to the term ‘‘issuer’’ in such instrument being ascribed the same meaning as the term‘‘person’’ in such instrument.

‘‘Subsidiary Notes’’ means promissory notes of the Partnership, a trust all of the units of which, or a corporation allof the shares of which, are owned directly or indirectly by the REIT or another entity that would be consolidatedwith the REIT under IFRS, having a maturity date and interest rate determined by the Trustees at the timeof issuance.

‘‘Substantial Completion’’ means, in respect of any development, redevelopment, refurbishment or repositioningproject, the completion of such project so that it is ready for use or is being used for the purposes intended,including receipt of necessary certificates of occupancy, but subject to the completion of ‘‘punch list’’ items, andin respect of which the tenant is in occupancy and paying rent.

‘‘Tangible Net Worth’’ means the aggregate of stated capital and retained earnings, less goodwill, incorporationand prepaid expenses, deferred costs and other assets normally regarded as intangible under generally acceptedaccounting principles in Canada.

‘‘Tax Act’’ means the Income Tax Act (Canada) and the regulations thereunder.

‘‘Tax Proposals’’ has the meaning given to that term under ‘‘Certain Canadian Federal Income TaxConsiderations’’.

‘‘TDSI’’ means TD Securities Inc.

15

‘‘Tenant Change of Control’’ means the acquisition (directly or indirectly) of the Control of a Dilawri Tenant byany person other than any one or more members of the Dilawri Organization, the REIT or any Affiliate of theREIT, provided that a Tenant Change of Control will be deemed not to occur if such Tenant Change of Controlresults from a change in the ownership, control or direction of publicly held or traded securities.

‘‘Termination Notice’’ has the meaning given to that term under ‘‘Assets of the REIT — Description of theMaterial Terms of the Dilawri Leases — Right to Cease Operation’’.

‘‘TFSA’’ has the meaning given to that term under ‘‘Eligibility for Investment’’.

‘‘Third Party Tenant Portfolio’’ has the meaning given to that term under ‘‘About This Prospectus’’.

‘‘Transferor Notes’’ means the promissory note(s) to be issued by the Partnership to the Transferors pursuant tothe Contribution Agreement.

‘‘Transferors’’ means, collectively, Dilawri, any member of the Dilawri Group and other entities the interests inwhich are jointly owned by Dilawri and a third party that directly or indirectly own the leasehold and freeholdinterests, as applicable, in the Initial Properties and which will be parties to the Contribution Agreement, and‘‘Transferor’’ means any one of them.

‘‘Triple 7 Chrysler’’ means the Initial Property municipally known as 700 Broad Street in Regina, Saskatchewan.

‘‘Trustees’’ means the trustees from time to time of the REIT, and ‘‘Trustee’’ means any one of them.

‘‘TSX’’ means the Toronto Stock Exchange.

‘‘UCC’’ has the meaning given to that term under ‘‘Certain Canadian Federal Income Tax Considerations —Taxation of the Partnership’’.

‘‘Underwriters’’ means, collectively, TDSI, CG, SCI, BMONB, RBCDS, GMP Securities L.P., National BankFinancial Inc., Raymond James Ltd. and Desjardins Securities Inc., as described under ‘‘Plan of Distribution’’.

‘‘Underwriting Agreement’’ means the underwriting agreement to be entered into among the REIT, Dilawri andthe Underwriters, as described under ‘‘Plan of Distribution’’.

‘‘United States’’ means the United States as such term is defined in Regulation S under the U.S. Securities Act.

‘‘Unitholders’’ means holders of Units, and ‘‘Unitholder’’ means any one of them.

‘‘Unit Ownership Guidelines’’ has the meaning given to that term under ‘‘Remuneration of Trustees — TrusteeUnit Ownership Guidelines’’.

‘‘Units’’ means trust units in the capital of the REIT, other than Special Voting Units, and ‘‘Unit’’ means any oneof them.

‘‘U.S. Securities Act’’ means the United States Securities Act of 1933, as amended.

‘‘Underwriter’s Certificate’’ has the meaning given to that term under ‘‘Certain Canadian Federal Income TaxConsiderations’’.

‘‘Vacant Premises’’ has the meaning given to that term under ‘‘Assets of the REIT — Description of the MaterialTerms of the Dilawri Leases — Right to Cease Operation’’.

‘‘Voting Trust Agreement’’ has the meaning given to that term under ‘‘Retained Interest — General’’.

‘‘Voting Unitholders’’ means, collectively, holders of Voting Units, and ‘‘Voting Unitholder’’ means any oneof them.

‘‘Voting Units’’ means, collectively, the Units and the Special Voting Units, and ‘‘Voting Unit’’ means any oneof them.

16

ABOUT THIS PROSPECTUS

An investor should rely only on the information contained in this prospectus and is not entitled to rely onparts of the information contained in this prospectus to the exclusion of others. The REIT has not, and theUnderwriters and Dilawri have not, authorized anyone to provide investors with additional or differentinformation. The REIT is not, and the Underwriters are not, offering to sell the Units in any jurisdictions wherethe offer or sale of such Units is not permitted. The information contained in this prospectus is accurate only asof the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of the Units.The REIT’s business, financial condition, results of operations and prospects may have changed since the date ofthis prospectus.

For investors outside Canada, none of the REIT, Dilawri or any of the Underwriters has done anything thatwould permit the Offering or the possession or distribution of this prospectus in any jurisdiction where action forthat purpose is required, other than in Canada. Investors are required to inform themselves about, and toobserve any restrictions relating to, the Offering and the possession or distribution of this prospectus.

This prospectus includes a summary description of certain material agreements of the REIT. See ‘‘MaterialContracts’’. The summary description discloses all attributes material to an investor in Units but is not completeand is qualified by reference to the terms of the material agreements, which will be filed with the Canadiansecurities regulatory authorities and available on SEDAR. Investors are encouraged to read the full text of suchmaterial agreements.

Any graphs and tables demonstrating the historical performance of the Initial Properties contained in thisprospectus are intended only to illustrate past performance and are not necessarily indicative of futureperformance.

All references in this prospectus to ‘‘AFFO per Unit’’ refer to AFFO per Unit on a fully-diluted basis,assuming all Class B LP Units were exchanged for Units at the beginning of the applicable period.

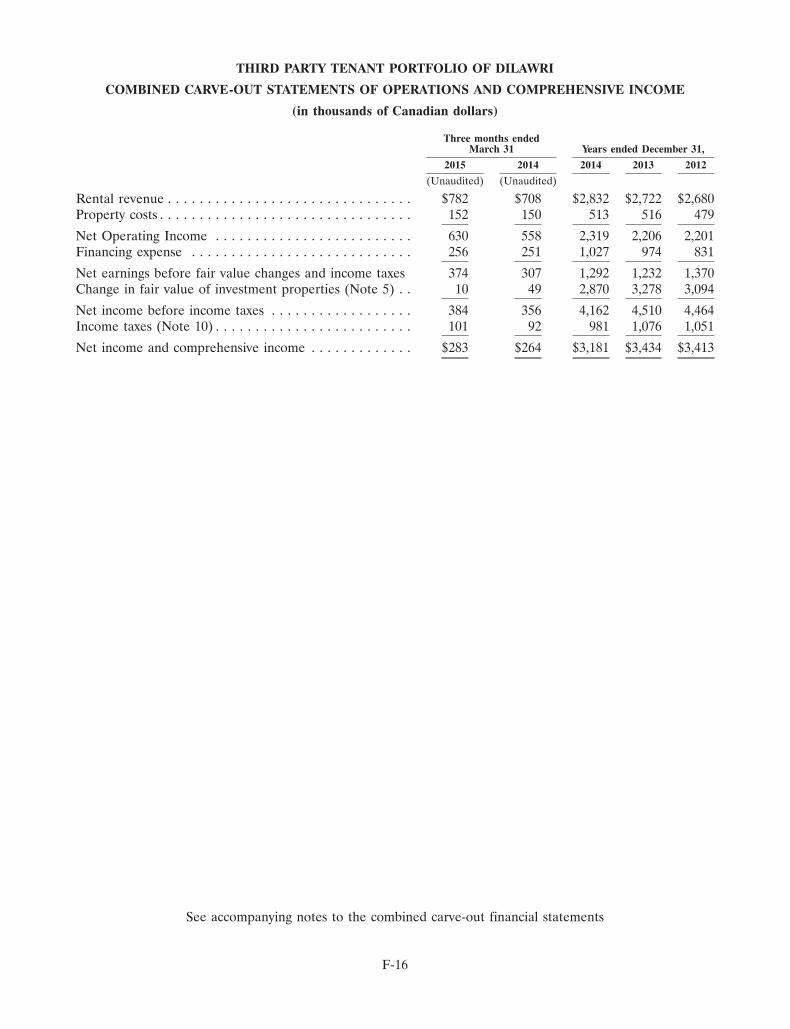

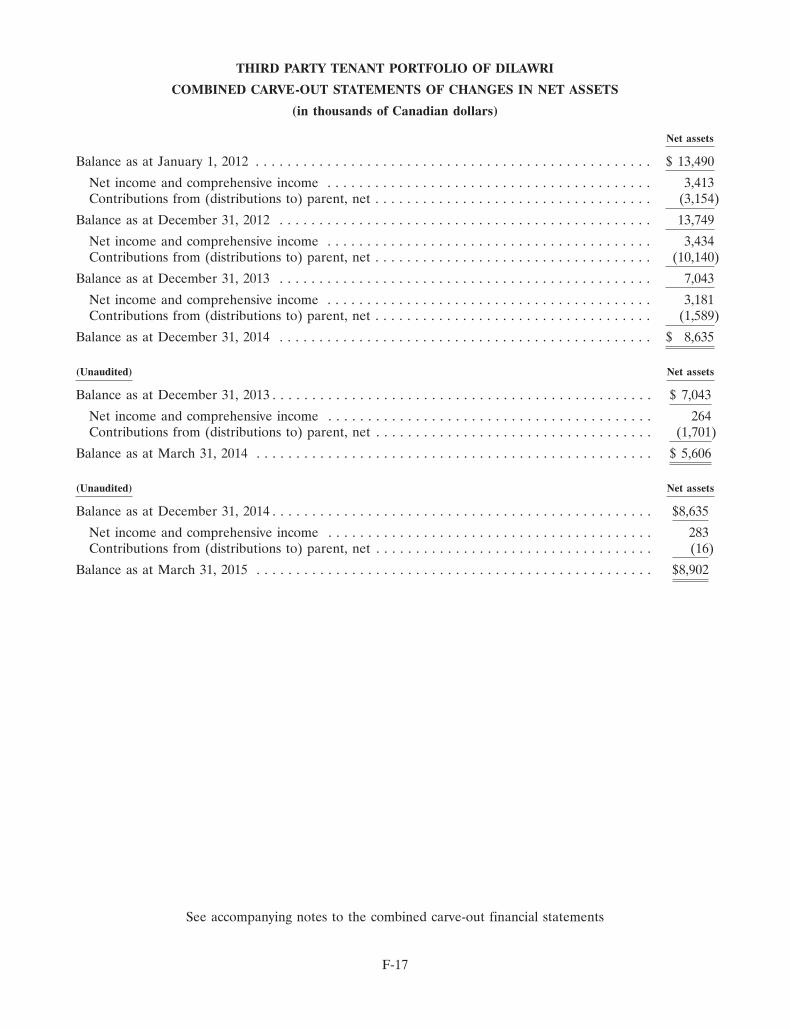

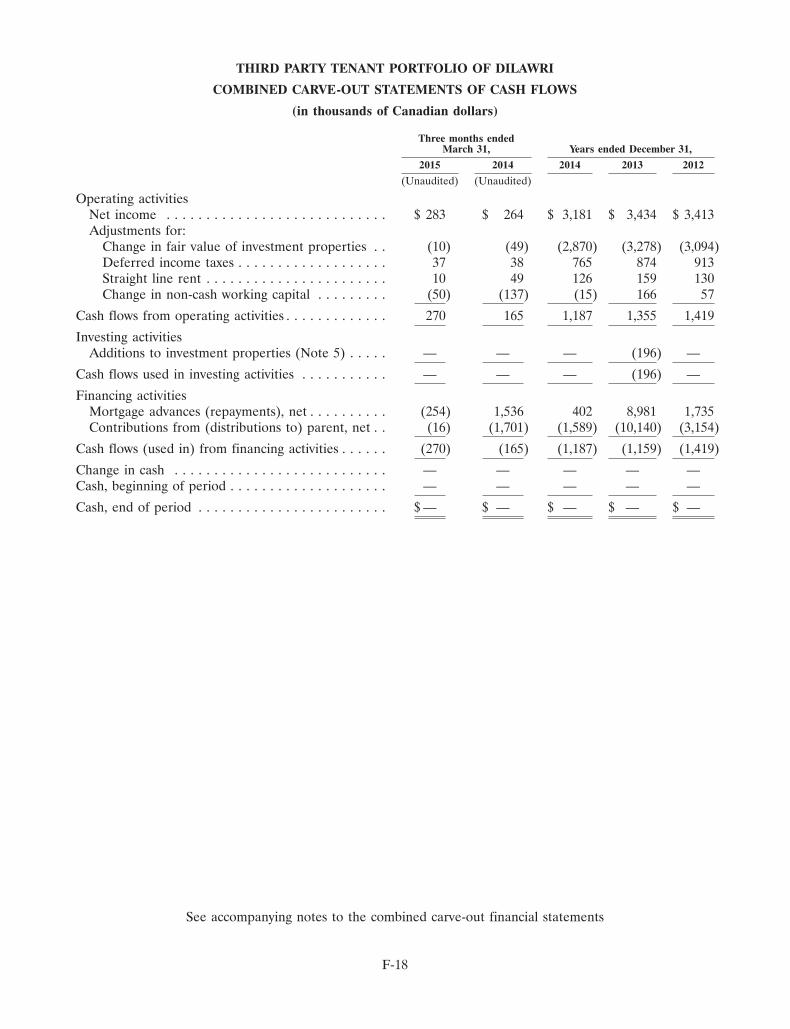

This prospectus includes historical combined carve-out financial statements only in respect of the portionsof the Initial Properties to be acquired by the REIT on Closing which are currently leased by third party tenants(collectively, the ‘‘Third Party Tenant Portfolio’’). See ‘‘Index to Financial Statements’’. The remainder of theInitial Properties (the ‘‘Dilawri Dealership Properties’’) have historically been used by the Dilawri Group inconjunction with its automotive dealership business. Under applicable securities laws, only the Third PartyTenant Portfolio is considered a business to be acquired by the REIT on Closing; whereas the propertiescomprising the Dilawri Dealership Properties are instead considered assets that the REIT will acquire onClosing. In accordance with applicable securities laws, the REIT is required to include only historical financialstatements in this prospectus that relate to the proposed acquisition of a business, provided that this prospectusotherwise contains full, true and plain disclosure of all material facts relating to the Units. Accordingly, thisprospectus contains historical audited and unaudited combined carve-out financial statements only in respect ofthe Third Party Tenant Portfolio, but does not include historical audited or unaudited combined carve-outfinancial statements in respect of the Dilawri Dealership Properties.

Applicable securities laws require the REIT to include pro forma financial statements in this prospectus inrespect of the Third Party Tenant Portfolio giving effect to, among other things, the Offering and the acquisitionby the REIT of the Initial Properties (the ‘‘Acquisition’’), only if such pro forma financial statements arenecessary for this prospectus to contain full, true and plain disclosure of all material facts relating to the Units.As evidenced by their execution of the certificates attached to this prospectus, the REIT, Dilawri and theUnderwriters do not believe that such pro forma financial statements are necessary for such purpose, and,accordingly, no such statements are included. The REIT, Dilawri and the Underwriters made theirdetermination on the basis that: (i) the Third Party Tenant Portfolio is expected to indirectly represent less than12% of the REIT’s Cash NOI during the Forecast Period; and (ii) the Financial Forecast included in thisprospectus, together with the audited schedule of assets to be acquired and liabilities to be assumed as at June 1,2015 and the other information in this prospectus relating to the Initial Properties, provides investors withmeaningful material information about the REIT and its business following Closing.

Three of the Initial Properties are undergoing redevelopment or substantial renovation work by the DilawriGroup (see ‘‘Assets of the REIT — Description of the Initial Properties’’). In this prospectus, reference is made

17

to the Initial Properties totaling approximately 958,000 square feet of GLA. This figure is, and all calculations ofor reference to GLA are, based on the ‘‘as completed’’ GLA for these three Initial Properties as the base rentpayable in respect of these properties under the applicable Dilawri Leases has been determined on an ‘‘ascompleted’’ basis.

The Dixie Auto Mall currently includes an industrial property with approximately 53,000 square feet ofGLA on approximately 4.5 acres of land (the ‘‘Dixie Industrial Property’’) which is not included as part of theInitial Properties as it is not an asset over which the REIT will have control. See ‘‘Assets of the REIT —Description of the Initial Properties’’.

MEANING OF CERTAIN REFERENCES

Unless otherwise indicated, the disclosure in this prospectus assumes that: (i) the transactions describedunder ‘‘Acquisition of the Initial Properties’’ have been completed; and (ii) the Over-Allotment Option is notexercised. All references to dollars or ‘‘$’’ are to Canadian dollars.

Unless the context otherwise requires or as otherwise provided herein, all references to the ‘‘REIT’’ in thisprospectus refer to the REIT and its Subsidiaries, including the Partnership, on a consolidated basis.

References to ‘‘management’’ in this prospectus means the REIT’s President and Chief Executive Officer,Chief Financial Officer and other persons who, following Closing, will be acting in the capacities of the REIT’sofficers whether pursuant to the Administration Agreement or otherwise. Any statements in this prospectusmade by or on behalf of management are made in such persons’ capacities as officers of the REIT and not intheir personal capacities.

Numerous terms used in this prospectus are defined under ‘‘Glossary’’.

MARKET AND INDUSTRY DATA

This prospectus includes market and industry data and forecasts that were obtained from third partysources, including industry publications and publicly available information, as well as industry data prepared bymanagement on the basis of its knowledge of the automotive dealership industry in which the REIT will operate(including management’s estimates and assumptions relating to that industry based on that knowledge).Management’s knowledge of the automotive dealership industry in Canada has been developed through itsexperience and participation in the industry. Management believes that its industry data is accurate and that itsestimates and assumptions are reasonable, but there can be no assurance as to the accuracy or completeness ofthis data. Third party sources, which include Statistics Canada, DesRosiers Automotive Consultants Inc.,PricewaterhouseCoopers LLP, McKinsey & Company Inc., public company disclosure, and other publiclyavailable information, generally state that the information contained therein has been obtained from sourcesbelieved to be reliable, but there can be no assurance as to the accuracy or completeness of includedinformation. Although management believes it to be reliable, none of the REIT, Dilawri or the Underwriters hasindependently verified any of the data from third party sources referred to in this prospectus, ascertained theunderlying economic assumptions relied upon by such sources, or analyzed or verified the underlying studies orsurveys relied upon or referred to by third party sources. In this prospectus, references to ‘‘the Canadianautomotive retail industry’’ include new cars, used cars, other motor vehicle dealers, and parts/accessories/tirestores as published by Statistics Canada.

FORWARD-LOOKING STATEMENTS

Certain statements contained in this prospectus constitute forward-looking information within the meaningof securities laws. Forward-looking information may relate to the REIT’s future outlook and anticipated eventsor results and may include statements regarding the financial position, business strategy, budgets, litigation,projected costs, capital expenditures, financial results, taxes, plans and objectives of or involving the REIT.Particularly, statements regarding future results, performance, achievements, prospects or opportunities for theREIT or the real estate or automotive dealership industry are forward-looking statements. In some cases,forward-looking information can be identified by such terms such as ‘‘may’’, ‘‘might’’, ‘‘will’’, ‘‘could’’, ‘‘should’’,‘‘would’’, ‘‘occur’’, ‘‘expect’’, ‘‘plan’’, ‘‘anticipate’’, ‘‘believe’’, ‘‘intend’’, ‘‘estimate’’, ‘‘predict’’, ‘‘potential’’,

18

‘‘continue’’, ‘‘likely’’, ‘‘schedule’’, ‘‘objectives’’, or the negative thereof or other similar expressions concerningmatters that are not historical facts. Some of the specific forward-looking statements in this prospectus include,but are not limited to, statements with respect to the following:

• the REIT’s relationship with the Dilawri Organization, including in respect of (i) the DilawriOrganization’s retained interest in the REIT and its current intention with respect thereto, (ii) theservices to be provided to the REIT (whether directly or indirectly) by Dilawri pursuant to theAdministration Agreement, (iii) expected transactions to be entered into between Dilawri and the REIT(including the REIT’s acquisition of certain interests in properties held by the Dilawri Group and theDilawri Leases); (iv) Substantial Completion of the Development Properties and occupancy and leasingarrangements relating thereto; and (v) the Strategic Alliance Agreement;

• the REIT’s intention with respect to, and ability to execute, its external and internal growth strategies;

• the forecasted financial results of the REIT, including the assumptions contained in such forecast, for theperiods set out in the ‘‘Financial Forecast’’ section of this prospectus;

• the maintenance by the REIT of a strong balance sheet and prudent financial management and theassociated minimization of financial risk;

• the REIT representing a unique alternative for automotive dealership operators considering a sale orrecapitalization of their business;

• the REIT’s capital expenditure requirements and capital expenditures to be made by the REIT and theDilawri Group;

• the REIT’s distribution policy and the distributions to be paid to Unitholders;

• the distributions to be paid to holders of Partnership units;

• use of the proceeds to be received by the REIT upon the exercise of the Over-Allotment Option,if exercised;

• the REIT’s debt strategy, including the REIT entering into the Credit Facilities;

• the availability and terms of the Credit Facilities, the REIT’s Indebtedness at Closing, hedgingarrangements and the resulting effective fixed interest rates associated with the Credit Facilities;

• the REIT’s access to available sources of debt and/or equity financing;

• future compensation and governance practices by the REIT;

• the expected tax treatment of the REIT and its distributions to Unitholders;

• the REIT’s ability to meet its stated objectives;

• the REIT’s ability to expand its asset base and make accretive acquisitions;

• the percentage of cash distributions to be paid to Unitholders that will be tax deferred in 2015;

• the ability of the REIT to qualify as a ‘‘mutual fund trust’’, as defined in the Tax Act, and as a ‘‘real estateinvestment trust’’, as defined in the SIFT Rules;

• the reduction in the scope of services to be provided to the REIT under the Administration Agreementand the transition by the REIT to directly employing its senior management;

• the REIT being the only publicly listed vehicle in Canada exclusively focused on automotive dealershipproperties; and

• the REIT’s ability to consolidate automotive dealership properties.

The REIT has based these forward-looking statements on factors and assumptions about future events andfinancial trends that it believes may affect its financial condition, results of operations, business strategy andfinancial needs, including that the Canadian economy will remain stable over the next 12 months, that inflationwill remain relatively low, that interest rates will remain stable, that tax laws remain unchanged, that conditions

19

within the automotive dealership real estate industry and the automotive dealership industry generally, includingcompetition for acquisitions, will be consistent with the current climate, that the Canadian capital markets willprovide the REIT with access to equity and/or debt at reasonable rates when required and that the DilawriOrganization will continue its involvement with the REIT.

Although the forward-looking statements contained in this prospectus are based upon assumptions thatmanagement believes are reasonable based on information currently available to management, there can be noassurance that actual results will be consistent with these forward-looking statements. Forward-lookingstatements necessarily involve known and unknown risks and uncertainties, many of which are beyond theREIT’s control, that may cause the REIT’s or the industry’s actual results, performance, achievements,prospects and opportunities in future periods to differ materially from those expressed or implied by suchforward-looking statements. These risks and uncertainties include, among other things, the factors discussedunder ‘‘Risk Factors’’.

The forward-looking statements made in this prospectus relate only to events or information as of the dateon which the statements are made in this prospectus. Except as required by law, the REIT and Dilawriundertake no obligation to update or revise publicly any forward-looking statements, whether as a result of newinformation, future events or otherwise, after the date on which the statements are made or to reflect theoccurrence of unanticipated events.

NON-IFRS MEASURES

Funds from operations (‘‘FFO’’), adjusted funds from operations (‘‘AFFO’’), net operating income (‘‘NOI’’)and cash net operating income (‘‘Cash NOI’’), are key measures of performance used by real estate businesses.However, such measures are not defined by IFRS and do not have standardized meanings prescribed by IFRS.The REIT believes that AFFO is an important measure of economic performance and is indicative of theREIT’s ability to pay distributions, while FFO, NOI and Cash NOI are important measures of operatingperformance and the performance of real estate properties. The IFRS measurement most directly comparableto FFO, AFFO, NOI and Cash NOI is net income.

‘‘FFO’’ is defined consistently with the definition presented in the White Paper on funds from operationsprepared by the Real Property Association of Canada (‘‘REALpac’’). FFO is calculated as net income inaccordance with IFRS, adjusted by removing the impact of (i) fair value adjustments on investment properties;(ii) other fair value adjustments including fair value adjustments on redeemable or exchangeable units; (iii) gainsand losses on the sale of investment properties; (iv) amortization of tenant incentives; and (v) distributions onredeemable or exchangeable units treated as interest expense.

‘‘AFFO’’ is defined as FFO subject to certain adjustments, to (a) remove the impact of: (i) amortization offair value mark-to-market adjustments on debt and amortization of financing costs and indemnity payable inrespect of the Third Party Tenant Portfolio sublease structure; (ii) adjusting for any differences resulting fromrecognizing property rental revenues or expenses (including ground lease rental payments) on a straight-linebasis; (iii) depreciation; and (iv) non-cash compensation incentive plans; and (b) deduct a reserve for normalizedmaintenance capital expenditures, tenant inducements and leasing commissions. Other adjustments may bemade to AFFO as determined by the Trustees in their sole discretion.

‘‘NOI’’ is defined as rental revenue from properties less property operating expenses as presented in thestatement of income prepared in accordance with IFRS. Accordingly, NOI excludes certain expenses included inthe determination of net income such as general and administrative expenses, fair value adjustments andamortization.

‘‘Cash NOI’’ is defined as NOI prior to the effects of straight-line adjustments.

FFO, AFFO, NOI and Cash NOI should not be construed as alternatives to net income or cash flow fromoperating activities determined in accordance with IFRS as indicators of the REIT’s performance. The REIT’smethod of calculating FFO, AFFO, NOI and Cash NOI may differ from other issuers’ methods and, accordingly,may not be comparable to measures used by other issuers. See ‘‘Forecast Non-IFRS Reconciliation’’.

20

ELIGIBILITY FOR INVESTMENT

In the opinion of Torys LLP, counsel to the REIT, and Blake, Cassels & Graydon LLP, counsel to theUnderwriters, based on the current provisions of the Tax Act, provided that on the Closing Date (i) the REITqualifies as a ‘‘mutual fund trust’’ within the meaning of the Tax Act or (ii) the Units are listed on a ‘‘designatedstock exchange’’ as defined in the Tax Act (which currently includes the TSX), the Units will be, on the date ofClosing, qualified investments under the Tax Act for trusts governed by a registered retirement savings plan(‘‘RRSP’’), registered retirement income fund (‘‘RRIF’’), registered disability savings plan, deferred profitsharing plan, tax-free savings account (‘‘TFSA’’) and registered education savings plan, each within the meaningof the Tax Act (collectively, ‘‘Exempt Plans’’).

Notwithstanding that the Units may be qualified investments for a trust governed by a TFSA, RRSP andRRIF, the holder of a TFSA or annuitant of an RRSP or RRIF (each, an ‘‘Annuitant’’), as the case may be, willbe subject to a penalty tax if the Units are a ‘‘prohibited investment’’ (as defined in the Tax Act) for the TFSA,RRSP or RRIF, as the case may be. The Units will not be a prohibited investment unless the Annuitant (i) doesnot deal at arm’s length with the REIT for purposes of the Tax Act, or (ii) has a ‘‘significant interest’’ in theREIT for the purposes of the ‘‘prohibited investment’’ rules in the Tax Act. In addition, Units will not be a‘‘prohibited investment’’ if the Units are ‘‘excluded property’’ as defined in the Tax Act for the purposes of the‘‘prohibited investment’’ rules. Annuitants should consult with their own tax advisors regarding the applicationof the ‘‘prohibited investment’’ rules having regard to their particular circumstances.

Subsidiary Notes received in connection with an in specie redemption of Units by the REIT would not bequalified investments for Exempt Plans, which could give rise to adverse tax consequences to the Exempt Plan orthe annuitant, beneficiary, subscriber or holder thereof. Accordingly, Exempt Plans that own Units shouldconsult with their own tax advisors before deciding to exercise the redemption rights attached to the Units.

For purposes of this ‘‘Eligibility for Investment’’ section, a reference to the REIT is to AutomotiveProperties Real Estate Investment Trust only, and is not a reference to any subsidiary entity.

21

PROSPECTUS SUMMARY

The following is a summary of the principal features of the Offering and should be read together with the moredetailed information and financial data and statements contained elsewhere in this prospectus. Numerous terms usedin this prospectus are defined in the Glossary.

THE REIT

Establishment and Overview

The REIT is a newly formed, unincorporated, open-ended real estate investment trust established pursuantto the Declaration of Trust under, and governed by, the laws of the Province of Ontario. The principal,registered and head office of the REIT is located at 133 King Street East, Suite 300, Toronto, Ontario,M5C 1G6. The REIT has been formed to own primarily income-producing automotive dealership propertieslocated in Canada.

Dilawri has taken the initiative in creating the REIT in order to establish a growth-oriented real estateentity that is expected to benefit from its relationship with the Dilawri Group, while retaining a significanteconomic interest in the Initial Properties. The Dilawri Group was formed over 30 years ago and has been in thebusiness of owning and operating automotive dealerships in Canada since that time, growing to become thelargest automotive dealership group in the country. The Dilawri Group owns 57 franchised automotivedealerships representing 30 automotive brands located in urban centres throughout Quebec, Ontario,Saskatchewan, Alberta and British Columbia. The Dilawri Group, which has more than 2,500 employees,continues to expand its automotive dealership business in strategic markets across Canada. Dilawri hadcombined revenues of approximately $1.6 billion and Adjusted EBITDA of approximately $75 million for the2014 fiscal year. The Dilawri Group has, on average, opened or acquired five new automotive dealerships ineach year for the last five years, including, on average, two to three automotive dealership properties. Inparticular, 12 of the 26 Initial Properties were either opened or acquired by Dilawri within the last five years.

On Closing, the REIT will indirectly acquire all of the Transferors’ interests in the Initial Properties, being aportfolio of 26 commercial properties located in Ontario, Saskatchewan, Alberta and British Columbia totalingapproximately 958,000 square feet of GLA. Out of the 26 Initial Properties, 24 are exclusively occupied by theDilawri Group for use as automotive dealerships or, in one case, an automotive repair facility, while the othertwo properties are jointly occupied by the Dilawri Group (for use as automotive dealerships) and one or morethird parties (for use as automotive dealerships or complementary uses, including restaurants). Interests in twoof the Initial Properties are currently jointly owned by the Dilawri Group and entities unrelated to the DilawriGroup. The Initial Properties represent all of the REIT-Suitable Properties currently owned by theDilawri Group.

As part of the Closing, the REIT will enter into leases with the applicable members of the Dilawri Grouppertaining to the entirety of each Initial Property, including the two properties that are partially occupied bythird parties, and the applicable members of the Dilawri Group will sublease the applicable portions of thosetwo properties to such third parties. Consequently, the Dilawri Group will be the REIT’s only tenant at Closingand its most significant tenant for the foreseeable future, with members of the Dilawri Group occupying 87% ofthe REIT’s GLA on Closing and third parties occupying the remainder pursuant to sublease arrangements withthe Dilawri Group. The rent from the portions of the Initial Properties occupied by the Dilawri Group willrepresent approximately 88% of the REIT’s Cash NOI over the Forecast Period, with the portions of the InitialProperties occupied by third party tenants pursuant to sublease arrangements accounting for the remainder. OnClosing, the initial terms of the Dilawri Leases will range from 11 to 19 years, with a Cash NOI weighted averagelease term of 15 years. See ‘‘Acquisition of the Initial Properties’’ and ‘‘Assets of the REIT’’.