Embed Size (px)

Citation preview

AUTOMOBILES & AUTO COMPONENTS SECTOR

Automobiles & Auto Components : Global Scenario

Automobiles & Auto Components : Indian Scenario

Automobiles & Auto Components : Tamil Nadu Scenario

Government Support

Investment Opportunities

CONTENTS

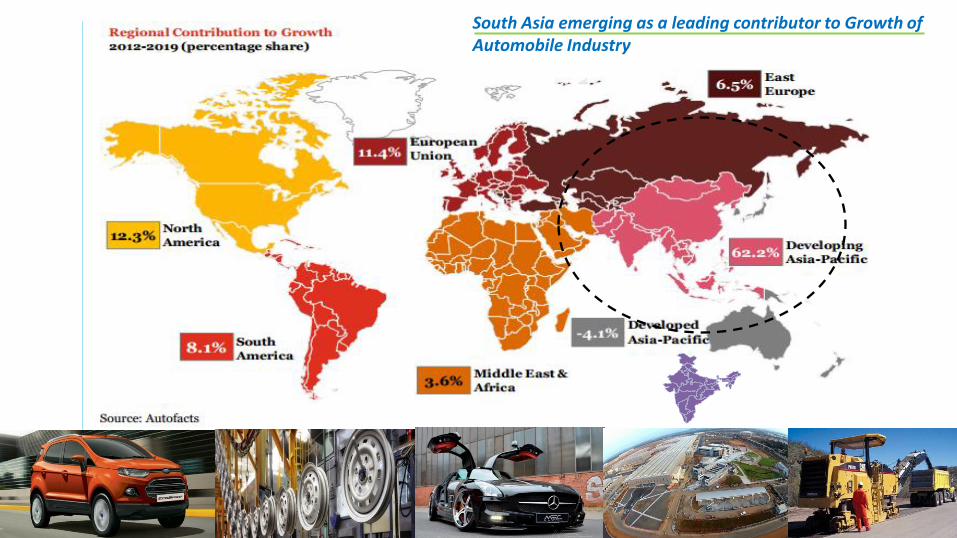

South Asia emerging as a leading contributor to Growth of Automobile Industry

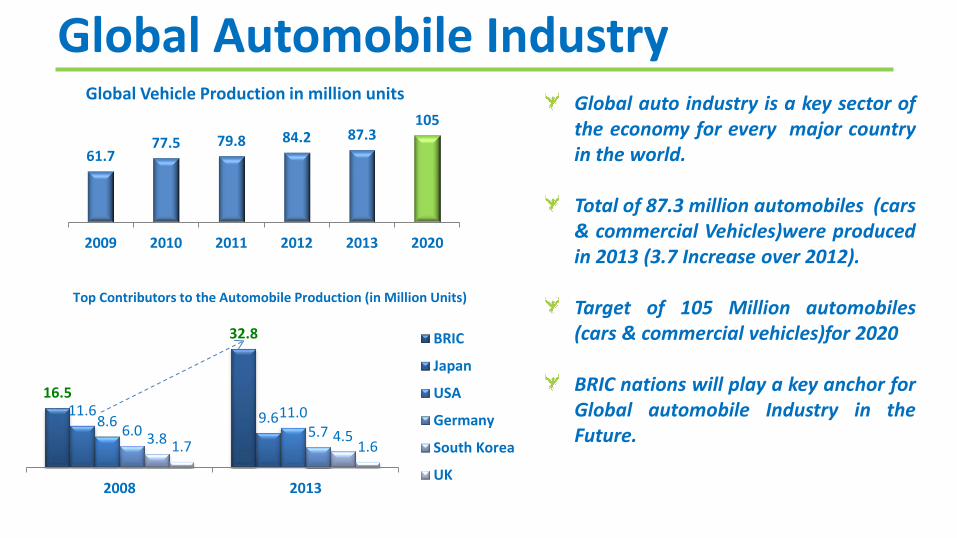

Global Automobile Industry

61.7 77.5 79.8 84.2 87.3

105

2009 2010 2011 2012 2013 2020

Global Vehicle Production in million units

16.5

32.8

11.6 9.6 8.6 11.0

6.0 5.7 3.8 4.5 1.7 1.6

2008 2013

Top Contributors to the Automobile Production (in Million Units)

BRIC

Japan

USA

Germany

South Korea

UK

Source: OICA, IHS automotive

Global auto industry is a key sector of the economy for every major country in the world. Total of 87.3 million automobiles (cars & commercial Vehicles)were produced in 2013 (3.7 Increase over 2012). Target of 105 Million automobiles (cars & commercial vehicles)for 2020 BRIC nations will play a key anchor for Global automobile Industry in the Future.

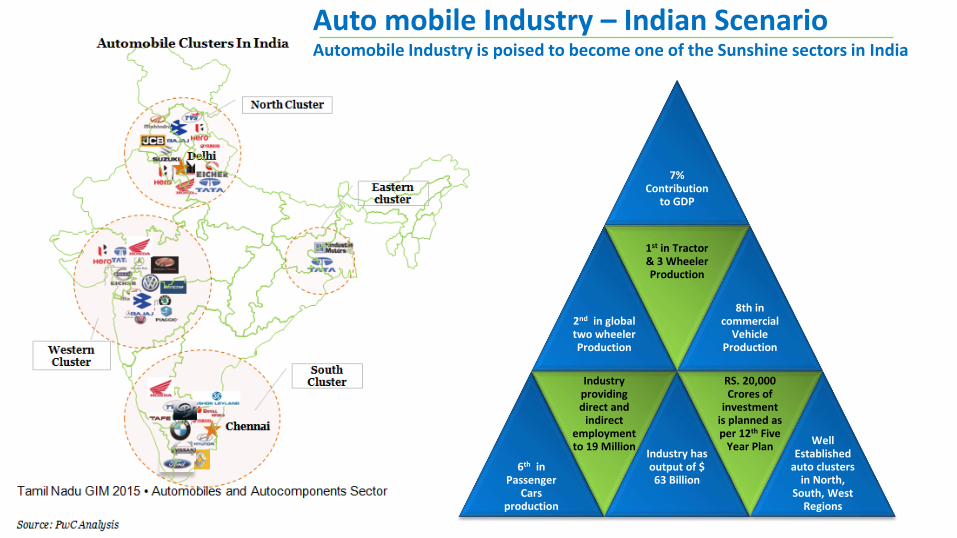

7% Contribution

to GDP

2nd in global two wheeler Production

1st in Tractor & 3 Wheeler Production

8th in commercial

Vehicle Production

6th in Passenger

Cars production

Industry providing direct and

indirect employment to 19 Million

Industry has output of $ 63 Billion

RS. 20,000 Crores of

investment is planned as per 12th Five

Year Plan Well

Established auto clusters

in North, South, West

Regions

Auto mobile Industry – Indian Scenario Automobile Industry is poised to become one of the Sunshine sectors in India

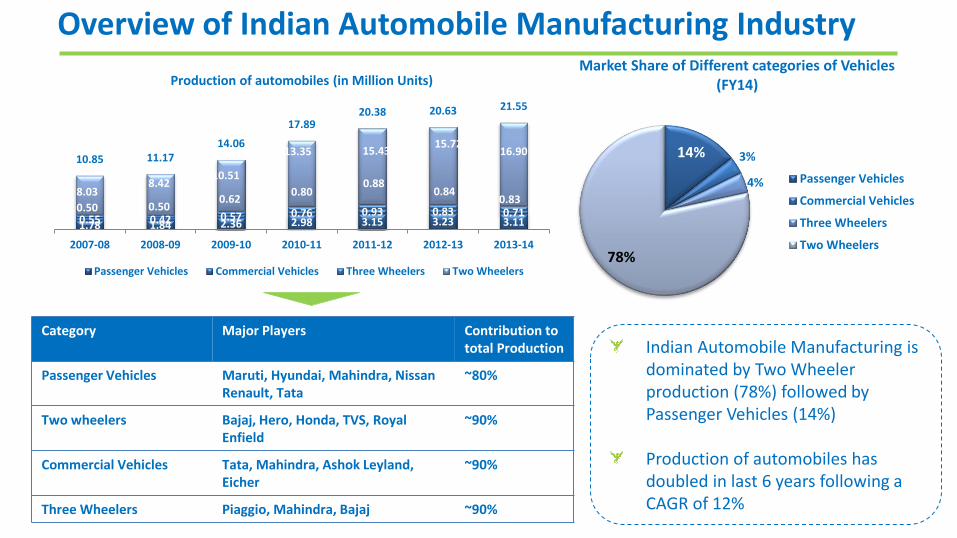

1.78 1.84 2.36 2.98 3.15 3.23 3.11 0.55 0.42 0.57 0.76 0.93 0.83 0.71 0.50 0.50 0.62

0.80 0.88

0.84 0.83

8.03 8.42

10.51

13.35 15.43 15.72

16.90 10.85 11.17

14.06

17.89 20.38 20.63 21.55

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

Production of automobiles (in Million Units)

Passenger Vehicles Commercial Vehicles Three Wheelers Two Wheelers

Category Major Players Contribution to total Production

Passenger Vehicles Maruti, Hyundai, Mahindra, Nissan Renault, Tata

~80%

Two wheelers Bajaj, Hero, Honda, TVS, Royal Enfield

~90%

Commercial Vehicles Tata, Mahindra, Ashok Leyland, Eicher

~90%

Three Wheelers Piaggio, Mahindra, Bajaj ~90%

14% 3%

4%

78%

Market Share of Different categories of Vehicles (FY14)

Passenger Vehicles

Commercial Vehicles

Three Wheelers

Two Wheelers

Indian Automobile Manufacturing is dominated by Two Wheeler production (78%) followed by Passenger Vehicles (14%) Production of automobiles has doubled in last 6 years following a CAGR of 12%

Overview of Indian Automobile Manufacturing Industry

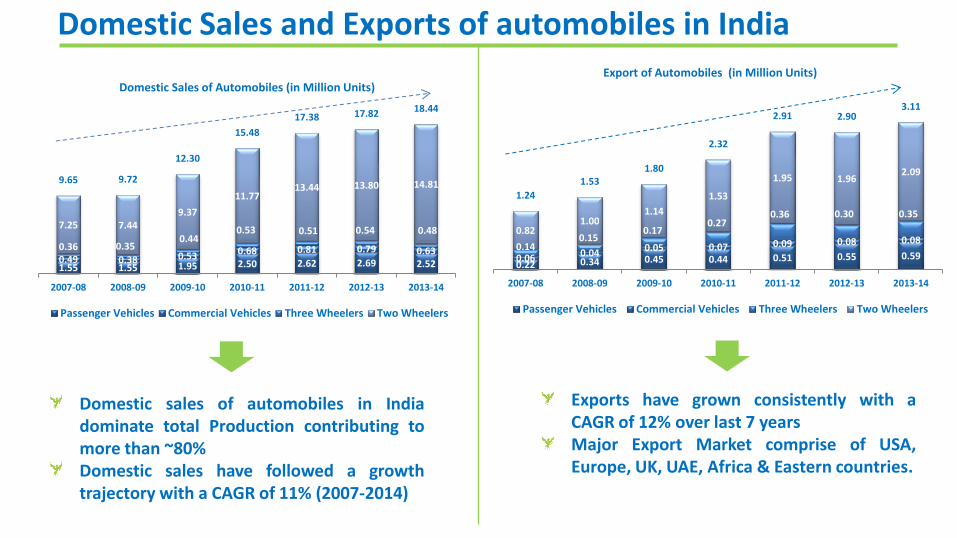

1.55 1.55 1.95 2.50 2.62 2.69 2.52 0.49 0.38 0.53 0.68 0.81 0.79 0.63 0.36 0.35 0.44

0.53 0.51 0.54 0.48 7.25 7.44

9.37

11.77 13.44 13.80 14.81 9.65 9.72

12.30

15.48

17.38 17.82 18.44

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

Domestic Sales of Automobiles (in Million Units)

Passenger Vehicles Commercial Vehicles Three Wheelers Two Wheelers

0.22 0.34 0.45 0.44 0.51 0.55 0.59 0.06 0.04 0.05 0.07 0.09 0.08 0.08 0.14

0.15 0.17

0.27 0.36 0.30 0.35

0.82 1.00

1.14

1.53

1.95 1.96 2.09

1.24

1.53 1.80

2.32

2.91 2.90 3.11

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

Export of Automobiles (in Million Units)

Passenger Vehicles Commercial Vehicles Three Wheelers Two Wheelers

Domestic sales of automobiles in India dominate total Production contributing to more than ~80% Domestic sales have followed a growth trajectory with a CAGR of 11% (2007-2014)

Exports have grown consistently with a CAGR of 12% over last 7 years Major Export Market comprise of USA, Europe, UK, UAE, Africa & Eastern countries.

Domestic Sales and Exports of automobiles in India

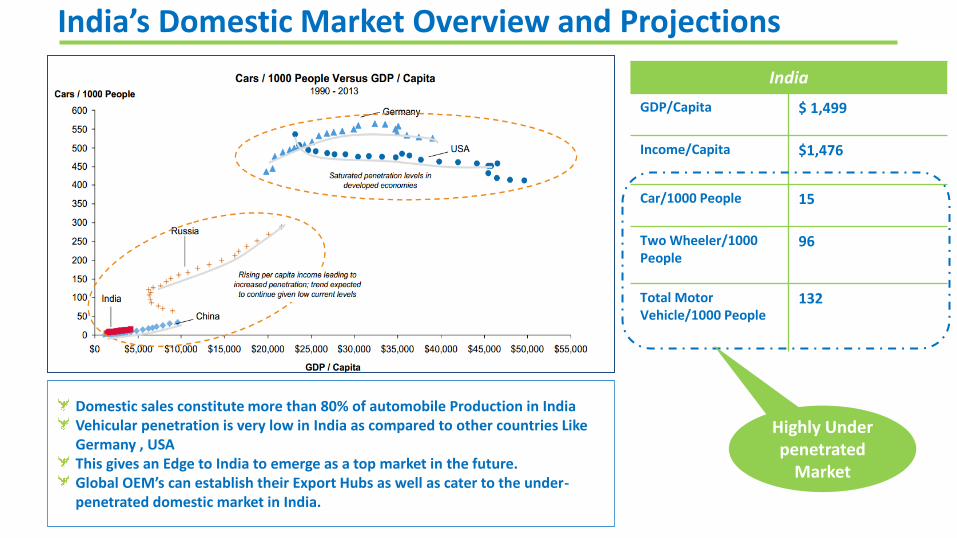

Domestic sales constitute more than 80% of automobile Production in India Vehicular penetration is very low in India as compared to other countries Like Germany , USA This gives an Edge to India to emerge as a top market in the future. Global OEM’s can establish their Export Hubs as well as cater to the under-penetrated domestic market in India.

India

GDP/Capita $ 1,499

Income/Capita $1,476

Car/1000 People 15

Two Wheeler/1000 People

96

Total Motor Vehicle/1000 People

132

Highly Under penetrated

Market

India’s Domestic Market Overview and Projections

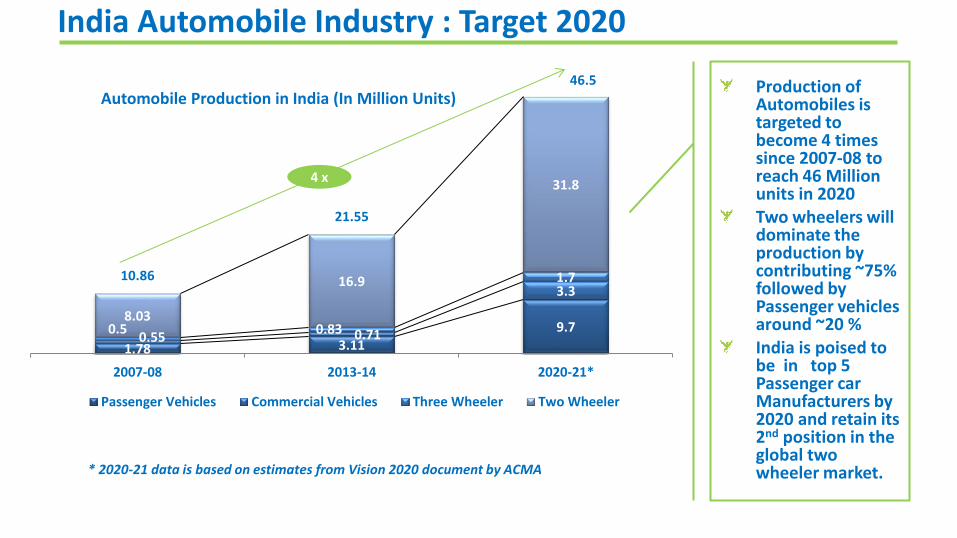

1.78 3.11 9.7

0.55 0.71

3.3

0.5 0.83

1.7

8.03

16.9

31.8

10.86

21.55

46.5

2007-08 2013-14 2020-21*

Automobile Production in India (In Million Units)

Passenger Vehicles Commercial Vehicles Three Wheeler Two Wheeler

4 x

Production of Automobiles is targeted to become 4 times since 2007-08 to reach 46 Million units in 2020 Two wheelers will dominate the production by contributing ~75% followed by Passenger vehicles around ~20 % India is poised to be in top 5 Passenger car Manufacturers by 2020 and retain its 2nd position in the global two wheeler market. * 2020-21 data is based on estimates from Vision 2020 document by ACMA

India Automobile Industry : Target 2020

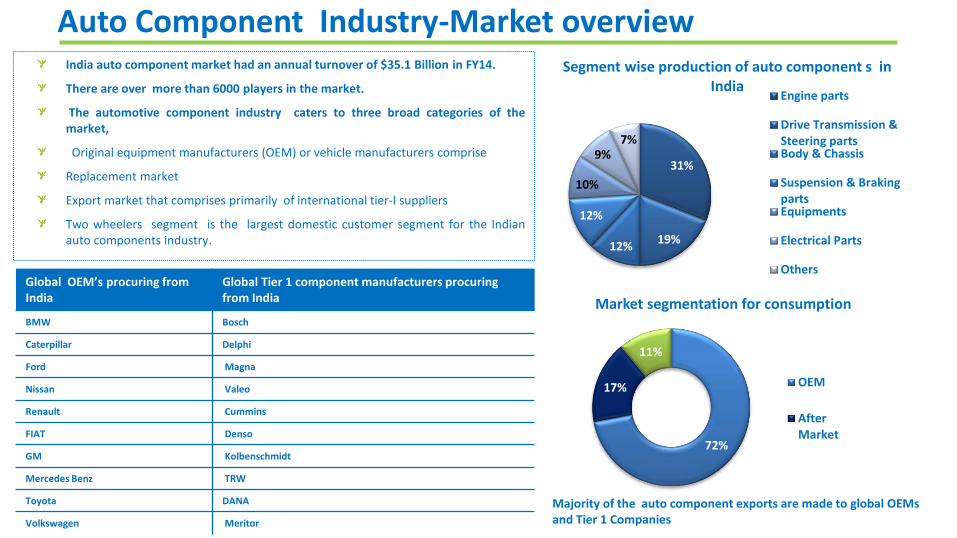

31%

19% 12%

12%

10%

9% 7%

Segment wise production of auto component s in India

Engine parts

Drive Transmission &Steering partsBody & Chassis

Suspension & BrakingpartsEquipments

Electrical Parts

Others

72%

17%

11%

Market segmentation for consumption

OEM

AfterMarket

Majority of the auto component exports are made to global OEMs and Tier 1 Companies

India auto component market had an annual turnover of $35.1 Billion in FY14.

There are over more than 6000 players in the market.

The automotive component industry caters to three broad categories of the market,

Original equipment manufacturers (OEM) or vehicle manufacturers comprise

Replacement market

Export market that comprises primarily of international tier-I suppliers

Two wheelers segment is the largest domestic customer segment for the Indian auto components industry.

Global OEM’s procuring from India

Global Tier 1 component manufacturers procuring from India

BMW Bosch

Caterpillar Delphi

Ford Magna

Nissan Valeo

Renault Cummins

FIAT Denso

GM Kolbenschmidt

Mercedes Benz TRW

Toyota DANA

Volkswagen Meritor

Auto Component Industry-Market overview

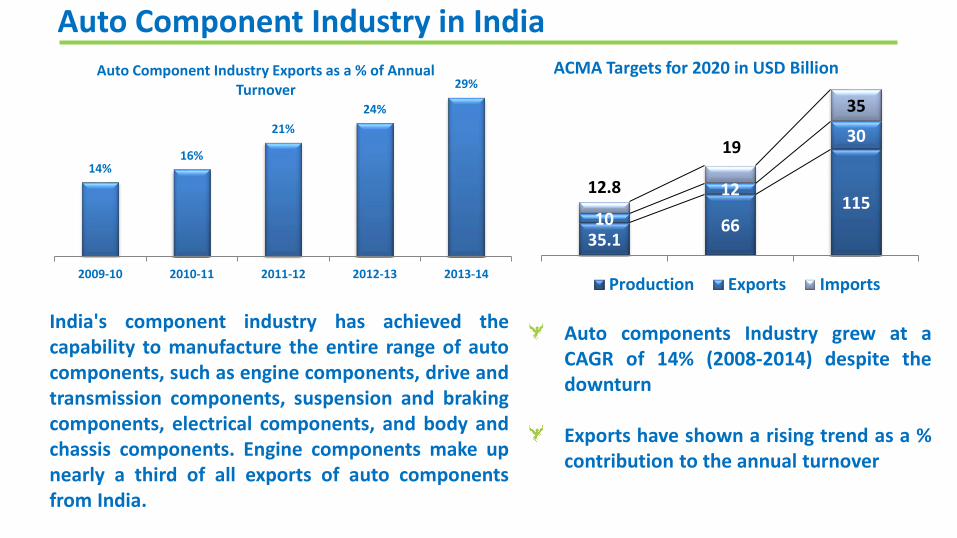

Auto components Industry grew at a CAGR of 14% (2008-2014) despite the downturn Exports have shown a rising trend as a % contribution to the annual turnover

14% 16%

21%

24%

29%

2009-10 2010-11 2011-12 2012-13 2013-14

Auto Component Industry Exports as a % of Annual Turnover

35.1 66

115 10

12

30

12.8

19

35

2013-14 2015-16 2020-21

ACMA Targets for 2020 in USD Billion

Production Exports Imports

India's component industry has achieved the capability to manufacture the entire range of auto components, such as engine components, drive and transmission components, suspension and braking components, electrical components, and body and chassis components. Engine components make up nearly a third of all exports of auto components from India.

Auto Component Industry in India

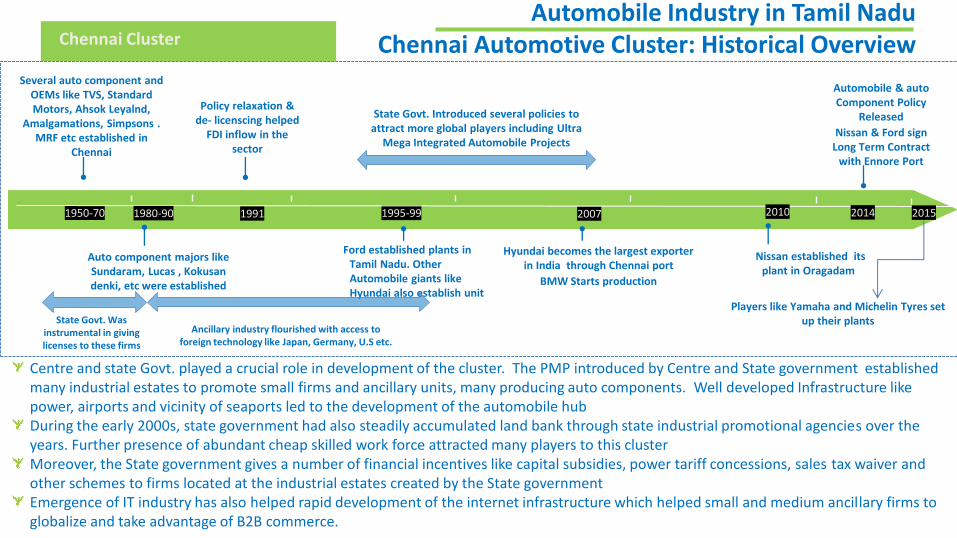

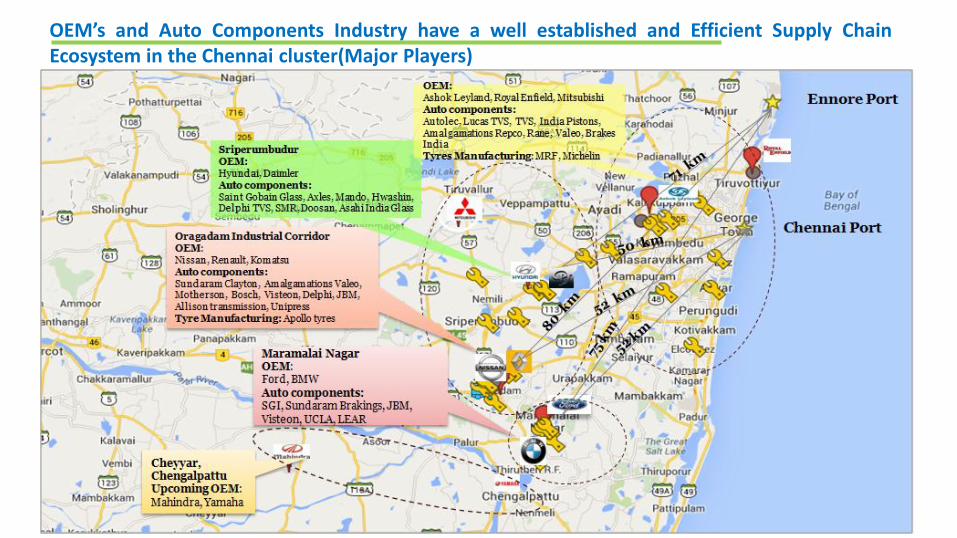

Chennai Cluster

Centre and state Govt. played a crucial role in development of the cluster. The PMP introduced by Centre and State government established many industrial estates to promote small firms and ancillary units, many producing auto components. Well developed Infrastructure like power, airports and vicinity of seaports led to the development of the automobile hub During the early 2000s, state government had also steadily accumulated land bank through state industrial promotional agencies over the years. Further presence of abundant cheap skilled work force attracted many players to this cluster Moreover, the State government gives a number of financial incentives like capital subsidies, power tariff concessions, sales tax waiver and other schemes to firms located at the industrial estates created by the State government Emergence of IT industry has also helped rapid development of the internet infrastructure which helped small and medium ancillary firms to globalize and take advantage of B2B commerce.

Automobile Industry in Tamil Nadu Chennai Automotive Cluster: Historical Overview

1950-70 1991 1995-99 2007 1980-90 2010 2014 2015

Several auto component and OEMs like TVS, Standard Motors, Ahsok Leyalnd,

Amalgamations, Simpsons . MRF etc established in

Chennai

Ford established plants in Tamil Nadu. Other Automobile giants like Hyundai also establish unit

State Govt. Introduced several policies to attract more global players including Ultra

Mega Integrated Automobile Projects

Policy relaxation & de- licenscing helped

FDI inflow in the sector

State Govt. Was instrumental in giving licenses to these firms

Hyundai becomes the largest exporter in India through Chennai port

BMW Starts production

Auto component majors like Sundaram, Lucas , Kokusan denki, etc were established

Nissan established its plant in Oragadam

Ancillary industry flourished with access to foreign technology like Japan, Germany, U.S etc.

Automobile & auto Component Policy

Released

Nissan & Ford sign Long Term Contract

with Ennore Port

Players like Yamaha and Michelin Tyres set up their plants

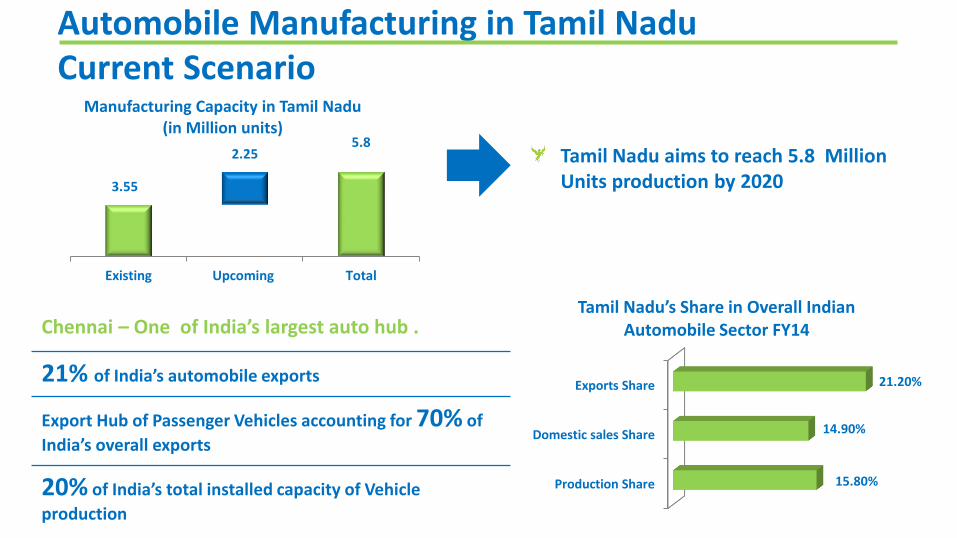

3.55

5.8 2.25

Existing Upcoming Total

Manufacturing Capacity in Tamil Nadu (in Million units)

Tamil Nadu aims to reach 5.8 Million Units production by 2020

Chennai – One of India’s largest auto hub .

21% of India’s automobile exports

Export Hub of Passenger Vehicles accounting for 70% of

India’s overall exports

20% of India’s total installed capacity of Vehicle

production

Production Share

Domestic sales Share

Exports Share

15.80%

14.90%

21.20%

Tamil Nadu’s Share in Overall Indian Automobile Sector FY14

Automobile Manufacturing in Tamil Nadu Current Scenario

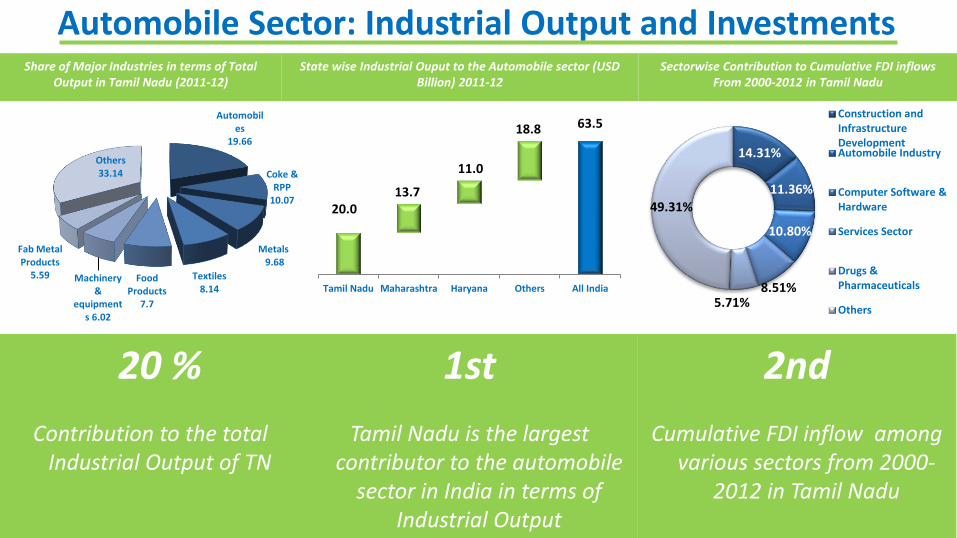

20.0

63.5

13.7

11.0

18.8

Tamil Nadu Maharashtra Haryana Others All India

14.31%

11.36%

10.80%

8.51% 5.71%

49.31%

Construction andInfrastructureDevelopmentAutomobile Industry

Computer Software &Hardware

Services Sector

Drugs &Pharmaceuticals

Others

Automobiles

19.66

Coke & RPP

10.07

Metals 9.68

Textiles 8.14

Food Products

7.7

Machinery &

equipments 6.02

Fab Metal Products

5.59

Others 33.14

20 %

Contribution to the total Industrial Output of TN

1st

Tamil Nadu is the largest contributor to the automobile

sector in India in terms of Industrial Output

2nd

Cumulative FDI inflow among various sectors from 2000-

2012 in Tamil Nadu

Share of Major Industries in terms of Total Output in Tamil Nadu (2011-12)

State wise Industrial Ouput to the Automobile sector (USD Billion) 2011-12

Sectorwise Contribution to Cumulative FDI inflows From 2000-2012 in Tamil Nadu

Automobile Sector: Industrial Output and Investments

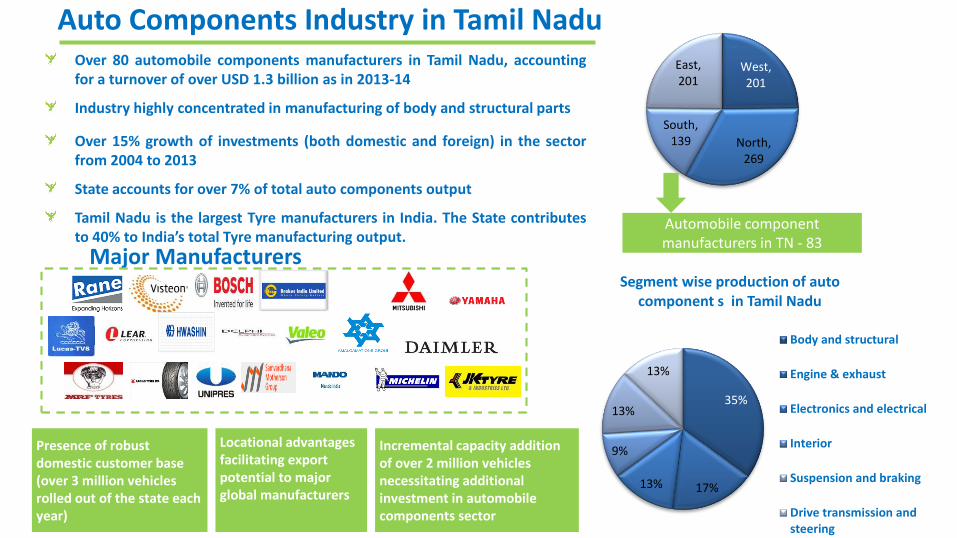

Over 80 automobile components manufacturers in Tamil Nadu, accounting for a turnover of over USD 1.3 billion as in 2013-14

Industry highly concentrated in manufacturing of body and structural parts

Over 15% growth of investments (both domestic and foreign) in the sector from 2004 to 2013

State accounts for over 7% of total auto components output

Tamil Nadu is the largest Tyre manufacturers in India. The State contributes to 40% to India’s total Tyre manufacturing output. Major Manufacturers

35%

17% 13%

9%

13%

13%

Segment wise production of auto component s in Tamil Nadu

Body and structural

Engine & exhaust

Electronics and electrical

Interior

Suspension and braking

Drive transmission andsteering

West, 201

North, 269

South, 139

East, 201

Automobile component manufacturers in TN - 83

Incremental capacity addition of over 2 million vehicles necessitating additional investment in automobile components sector

Locational advantages facilitating export potential to major global manufacturers

Presence of robust domestic customer base (over 3 million vehicles rolled out of the state each year)

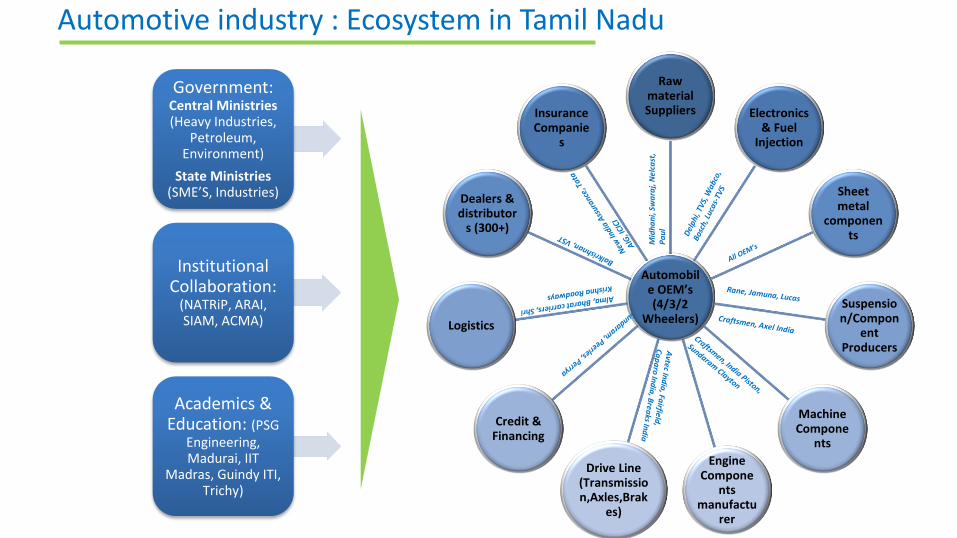

Auto Components Industry in Tamil Nadu

Automobile OEM’s (4/3/2

Wheelers)

Raw material Suppliers Electronics

& Fuel Injection

Sheet metal

components

Suspension/Compon

ent Producers

Machine Compone

nts

Engine Compone

nts manufactu

rer

Drive Line (Transmission,Axles,Brak

es)

Credit & Financing

Logistics

Dealers & distributor

s (300+)

Insurance Companie

s

Mid

ha

ni,

Sw

ara

j, N

elca

st,

Pa

ul

Government: Central Ministries (Heavy Industries,

Petroleum, Environment)

State Ministries (SME’S, Industries)

Institutional Collaboration:

(NATRiP, ARAI, SIAM, ACMA)

Academics & Education: (PSG

Engineering, Madurai, IIT

Madras, Guindy ITI, Trichy)

Automotive industry : Ecosystem in Tamil Nadu

Global Automotive Research Centre (GARC)- Chennai by NATRiP

NATRiP is one the largest R&D infrastructure in the country for the automotive sector. GARC is one the seven test centres of NATRiP which is present in Chennai.

GARC is situated in the SIPCOT industrial growth centre at Oragadam near Chennai . GARC performs testing of full range of automobile , agriculture tractors and construction equipment vehicles.

Facilities at the centre

Infotronics Lab (Centre of

Excellence)

Passive Safety Lab(Centre of

Excellence

EMC Lab (Centre of Excellence)

Powertrain Lab Fatigue Lab

Homologation Tracks

Component Lab Material Lab Certification Lab

Asia’s largest R&D and vehicle design center - Mahindra Research Valley, Chennai

Daimler R&D center for vehicle design

Ashok Leyland R&D and Technical Centre

Visteon R&D centre

Renault & Nissan R&D centre

Hyundai vehicle development

Ford technical support centre

State of the art National Automobile Testing and R&D centre

Other Research and Development Centres

OEM’s and Auto Components Industry have a well established and Efficient Supply Chain Ecosystem in the Chennai cluster(Major Players)

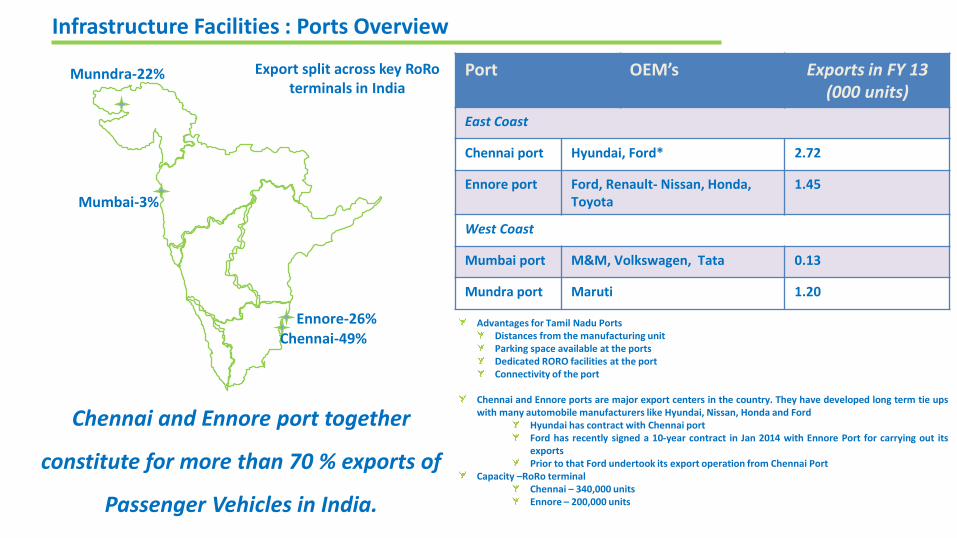

Export split across key RoRo terminals in India

Mumbai-3%

Munndra-22%

Chennai-49% Ennore-26%

Port OEM’s Exports in FY 13 (000 units)

East Coast

Chennai port Hyundai, Ford* 2.72

Ennore port Ford, Renault- Nissan, Honda, Toyota

1.45

West Coast

Mumbai port M&M, Volkswagen, Tata 0.13

Mundra port Maruti 1.20

Advantages for Tamil Nadu Ports Distances from the manufacturing unit Parking space available at the ports Dedicated RORO facilities at the port Connectivity of the port

Chennai and Ennore ports are major export centers in the country. They have developed long term tie ups with many automobile manufacturers like Hyundai, Nissan, Honda and Ford

Hyundai has contract with Chennai port Ford has recently signed a 10-year contract in Jan 2014 with Ennore Port for carrying out its exports Prior to that Ford undertook its export operation from Chennai Port

Capacity –RoRo terminal Chennai – 340,000 units Ennore – 200,000 units

Chennai and Ennore port together

constitute for more than 70 % exports of

Passenger Vehicles in India.

Infrastructure Facilities : Ports Overview

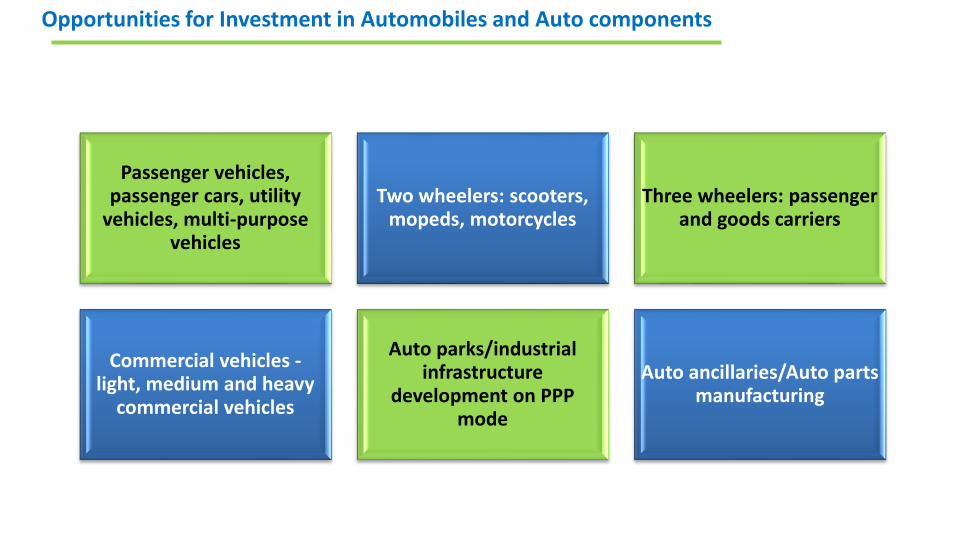

Passenger vehicles, passenger cars, utility

vehicles, multi-purpose vehicles

Two wheelers: scooters, mopeds, motorcycles

Three wheelers: passenger and goods carriers

Commercial vehicles - light, medium and heavy

commercial vehicles

Auto parks/industrial infrastructure

development on PPP mode

Auto ancillaries/Auto parts manufacturing

Opportunities for Investment in Automobiles and Auto components

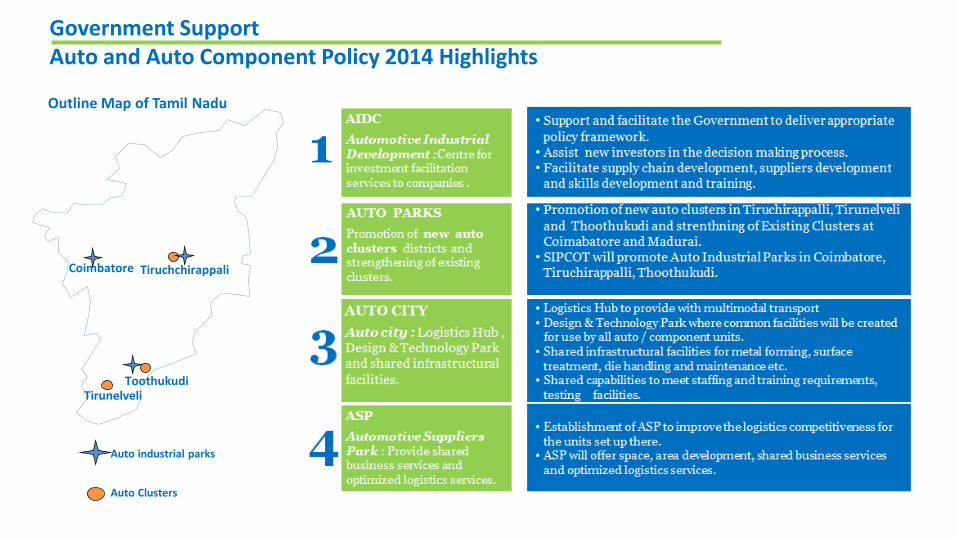

Coimbatore

Toothukudi Tirunelveli

Tiruchchirappali

Auto industrial parks

Auto Clusters

Outline Map of Tamil Nadu

Government Support Auto and Auto Component Policy 2014 Highlights

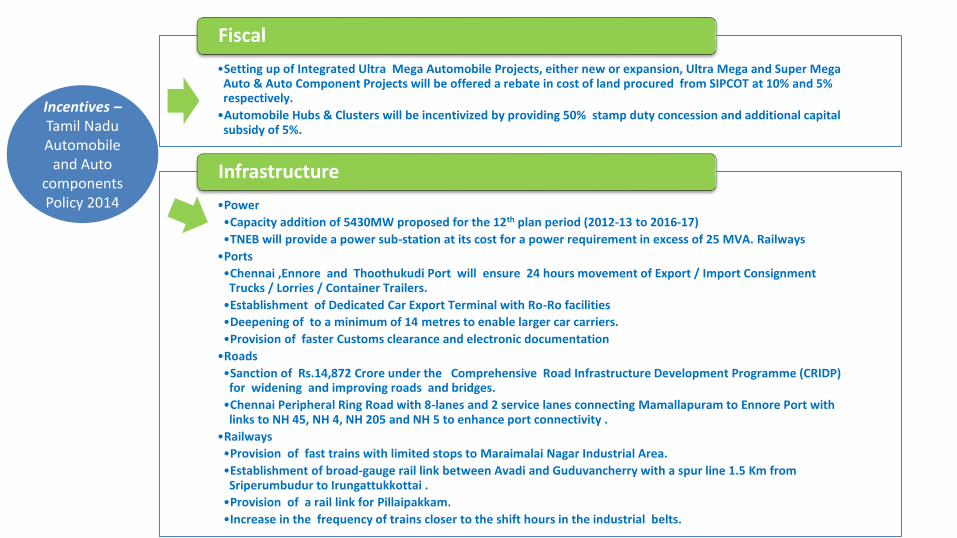

•Setting up of Integrated Ultra Mega Automobile Projects, either new or expansion, Ultra Mega and Super Mega Auto & Auto Component Projects will be offered a rebate in cost of land procured from SIPCOT at 10% and 5% respectively.

•Automobile Hubs & Clusters will be incentivized by providing 50% stamp duty concession and additional capital subsidy of 5%.

Fiscal

•Power

•Capacity addition of 5430MW proposed for the 12th plan period (2012-13 to 2016-17)

•TNEB will provide a power sub-station at its cost for a power requirement in excess of 25 MVA. Railways

•Ports

•Chennai ,Ennore and Thoothukudi Port will ensure 24 hours movement of Export / Import Consignment Trucks / Lorries / Container Trailers.

•Establishment of Dedicated Car Export Terminal with Ro-Ro facilities

•Deepening of to a minimum of 14 metres to enable larger car carriers.

•Provision of faster Customs clearance and electronic documentation

•Roads

•Sanction of Rs.14,872 Crore under the Comprehensive Road Infrastructure Development Programme (CRIDP) for widening and improving roads and bridges.

•Chennai Peripheral Ring Road with 8-lanes and 2 service lanes connecting Mamallapuram to Ennore Port with links to NH 45, NH 4, NH 205 and NH 5 to enhance port connectivity .

•Railways

•Provision of fast trains with limited stops to Maraimalai Nagar Industrial Area.

•Establishment of broad-gauge rail link between Avadi and Guduvancherry with a spur line 1.5 Km from Sriperumbudur to Irungattukkottai .

•Provision of a rail link for Pillaipakkam.

•Increase in the frequency of trains closer to the shift hours in the industrial belts.

Infrastructure

Incentives –Tamil Nadu Automobile

and Auto components Policy 2014

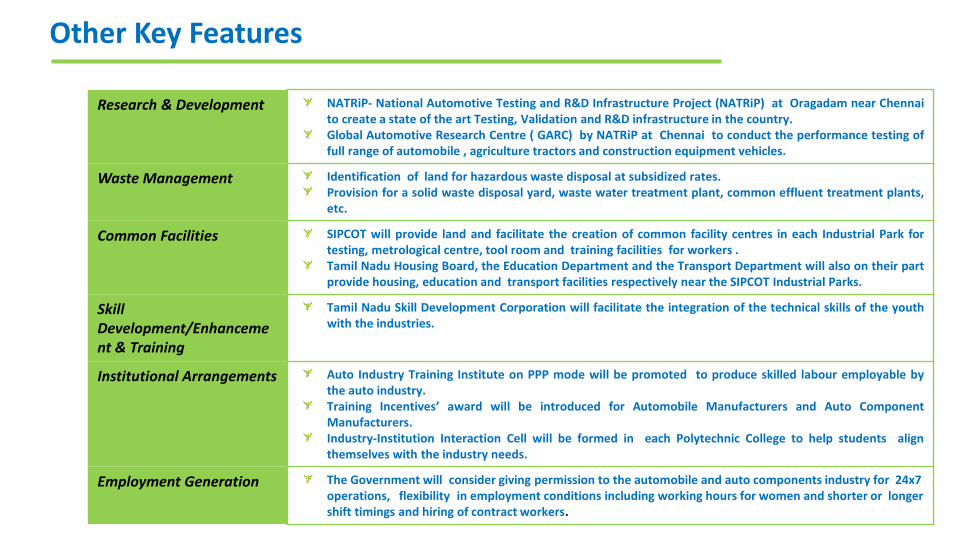

Research & Development NATRiP- National Automotive Testing and R&D Infrastructure Project (NATRiP) at Oragadam near Chennai to create a state of the art Testing, Validation and R&D infrastructure in the country. Global Automotive Research Centre ( GARC) by NATRiP at Chennai to conduct the performance testing of full range of automobile , agriculture tractors and construction equipment vehicles.

Waste Management Identification of land for hazardous waste disposal at subsidized rates. Provision for a solid waste disposal yard, waste water treatment plant, common effluent treatment plants, etc.

Common Facilities SIPCOT will provide land and facilitate the creation of common facility centres in each Industrial Park for testing, metrological centre, tool room and training facilities for workers . Tamil Nadu Housing Board, the Education Department and the Transport Department will also on their part provide housing, education and transport facilities respectively near the SIPCOT Industrial Parks.

Skill Development/Enhancement & Training

Tamil Nadu Skill Development Corporation will facilitate the integration of the technical skills of the youth with the industries.

Institutional Arrangements Auto Industry Training Institute on PPP mode will be promoted to produce skilled labour employable by the auto industry. Training Incentives’ award will be introduced for Automobile Manufacturers and Auto Component Manufacturers. Industry-Institution Interaction Cell will be formed in each Polytechnic College to help students align themselves with the industry needs.

Employment Generation The Government will consider giving permission to the automobile and auto components industry for 24x7 operations, flexibility in employment conditions including working hours for women and shorter or longer shift timings and hiring of contract workers.

Other Key Features

Additional Chief Secretary - Government of Tamil Nadu Industries Department

Phone: 91-44-25671383 Fax: 91-44-25670822Email: [email protected], [email protected]

Nodal agency Tamil Nadu Industrial Guidance and Export Promotion Bureau

19-A, Rukmini Lakshmipathy Road,Egmore, Chennai-600 008Phone: 91-44-2855 3118

Email: [email protected]

Visit us at www.tamilnadugim.com