Embed Size (px)

DESCRIPTION

Automobile Industry in India. Its past, present and future

Citation preview

PRESENTED BY:

AMIT KUMAR

ASHISH RANJAN

CHANRASHEKHAR

CHANDRAMANI

SHWETA KUMARI

YASHASVI GOJA

AUTOMOBILE INDUSTRY

The Indian Automobile Industry manufactures over 11 million vehicles and exports about 1.5 million each year.

The dominant products of the industry are two-wheelers with a market share of over 75% and passenger cars with a market share of about 16%.

Commercial vehicles and three-wheelers share about 9% of the market between them. About 91% of the vehicles sold are used by households and only about 9% for commercial purposes.

The industry has a turnover of more than USD $35 billion and provides direct and indirect employment to over 13 million people.

OVERVIEW

The supply chain is similar to the supply chain of the automotive industry in Europe and America.

Interestingly, the level of trade exports in this sector in India has been medium and imports have been low. However, this is rapidly changing and both exports and imports are increasing.

With a high cost of developing production facilities, limited accessibility to new technology, and increasing competition, the barriers to enter the Indian Automotive sector are high.

India has a well-developed tax structure. The power to levy taxes and duties is distributed among the three tiers of Government. The cost structure of the industry is fairly traditional, but the profitability of motor vehicle manufacturers has been rising over the past five years.

Tata Motors is leading the commercial vehicle segment with a market share of about 64%. Maruti Suzuki is leading the passenger vehicle segment with a market share of 46%. Hyundai Motor India Limited and Mahindra and Mahindra are focusing expanding their footprint in the overseas market. Hero MotoCorp is occupying over 41% and sharing 26% of the two-wheeler market in India with Bajaj Auto. Bajaj Auto in itself is occupying about 58% of the three-wheeler market.

Over the past few years, the industry has been volatile. Currently, India's increasing per capita disposable income which is expected to rise by 106% by 2015 and growth in exports is playing a major role in the rise and competitiveness of the industry.

The level of technology change in the Motor vehicle Industry has been high but, the rate of change in technology has been medium. Investment in the technology by the producers has been high.

The key to success in the industry is to improve labour productivity, labour flexibility, and capital efficiency. Having quality manpower, infrastructure improvements, and raw material availability also play a major role. Access to latest and most efficient technology and techniques will bring competitive advantage to the major players.

The role of Industry is and will primarily be in designing and manufacturing products of world-class quality establishing cost competitiveness and improving productivity in labour and in capital. With a combined effort, the Indian Automotive industry will emerge as the destination of choice in the world for design and manufacturing of automobiles .

The Indian market offers endless possibilities for investors.

The first car ran on India's roads in 1897. Until the 1930s, cars were imported directly, but in very small numbers.

Embryonic automotive industry emerged in India in the 1940s. Mahindra & Mahindra was established by two brothers as a trading company in 1945, and began assembly of Jeep CJ-3A utility vehicles under license from Willys. The company soon branched out into the manufacture of light commercial vehicles (LCVs) and agricultural tractors.

Following the independence, in 1947, the Government of India and the private sector launched efforts to create an automotive component manufacturing industry to supply to the automobile industry. However, the growth was relatively slow in the 1950s and 1960s due to nationalisation and the license raj which hampered the Indian private sector.

HISTORY

After 1970 the automotive industry started to grow, but the growth was mainly driven by tractors, commercial vehicles and scooters. Cars were still a major luxury. Japanese manufacturers entered the Indian market ultimately leading to the establishment of Maruti Udyog.

In the 1980, a number of Japanese manufacturers launched joint-ventures for building motorcycles and light commercial-vehicles. It was at this time that the Indian government chose Suzuki for its joint-venture to manufacture small cars.

Following the economic liberalisation in 1991 and the gradual weakening of the license raj, a number of Indian and multi-national car companies launched operations. Since then, automotive component and automobile manufacturing growth has accelerated to meet domestic and export demands.

Economic liberalization in India in 1991, the Indian automotive industry has demonstrated sustained growth as a result of increased competitiveness and relaxed restrictions.

Several Indian automobile manufacturers such as Tata Motors, Maruti Suzuki and Mahindra and Mahindra, expanded their domestic and international operations. India's robust economic growth led to the further expansion of its domestic automobile market which has attracted significant India-specific investment by multinational automobile manufacturers.

In February 2009, monthly sales of passenger cars in India exceeded 100,000 units and has since grown rapidly to a record monthly high of 182,992 units in October 2009.

From 2003 to 2010, car sales in India have progressed at a CAGR of 13.7%, and with only 10% of Indian households owning a car in 2009

SIAM is the apex industry body representing all the vehicle manufacturers, home-grown and international, in India.

This class consists of units mainly engaged in manufacturing motor vehicles or motor vehicle engines.

The primary activities of this industry are: Motor cars manufacturing Motor vehicle engine manufacturing

The major products and services in this industry are: Passenger motor vehicle manufacturing segment (Passenger Cars, Utility Vehicles & Multi Purpose Vehicles) Commercial Vehicles (Medium & Heavy and Light Commercial Vehicles) Two Wheelers Three Wheelers.

Supply Chain of Automobile Industry: The supply chain of automotive industry in India is very similar to the supply chain of the automotive industry in Europe and America. The orders of the industry arise from the bottom of the supply chain i. e., from the consumers and goes through the automakers and climbs up until the third tier suppliers.

INDUSTRY DEFINATION

Supply Chain of Automobile Industry: The supply chain of automotive industry in India is now very similar to the supply chain of the automotive industry in Europe and America.

The orders of the industry arise from the bottom of the supply chain i.e, from the consumers and goes through the automakers and climbs up until the third tier suppliers.

Main components of achieving this supply chain system are:

Third Tier Suppliers.

Second Tier Suppliers.

First Tier Suppliers.

CHANGES IN INDIAN AUTOMOBILE INDUSTRY SUPPLY CHAIN SYSTEM:

Third Tier Suppliers: These companies provide basic products like rubber, glass, steel, plastic and aluminium to the second tier suppliers.

Second Tier Suppliers: These companies design vehicle systems or bodies for First Tier Suppliers and OEMs. They work on designs provided by the first tier suppliers or OEMs. They also provide engineering resources for detailed designs. Some of their services may include welding, fabrication, shearing, bending etc.

First Tier Suppliers: These companies provide major systems directly to assemblers. These companies have global coverage to follow their customers to various locations around the world. They design and innovate to provide "black-box" solutions for the requirements of their customers. Black-box solutions are solutions created by suppliers using their own technology to meet the performance and interface requirements set by assemblers.

Role of each of the contributors to the supply chain are discussed below:-

First tier suppliers are responsible not only for the assembly of parts into complete units like dashboard, brakes-axle-suspension, seats, or cockpit but also for the management of second-tier suppliers.

Automakers/Vehicle Manufacturers/Original Equipment Manufacturers (OEMs): After researching consumers' wants and needs, automakers begin designing models which are tailored to consumers' demands. The design process normally takes five years. These companies have manufacturing units where engines are manufactured and parts supplied by first tier suppliers and second tier suppliers are assembled. Automakers are the key to the supply chain of the automotive industry. Examples of these companies are Tata Motors, Maruti Suzuki, Toyota, and Honda. Innovation, design capability and branding are the main focus of these companies.

Dealers: Once the vehicles are ready they are shipped to the regional branch and from there, to the authorised dealers of the companies. The dealers then sell the vehicles to the end customers.

Parts and Accessory: These companies provide products like tires, windshields, and air bags etc. to automakers and dealers or directly to customers.

Service Providers: Some of the services to the customers include servicing of vehicles, repairing parts, or financing of vehicles. Many dealers provide these services but, customers can also choose to go to independent service providers.

YearCar

Production % Change Commercial % Change

Total Vehicles Prodn.

% Change

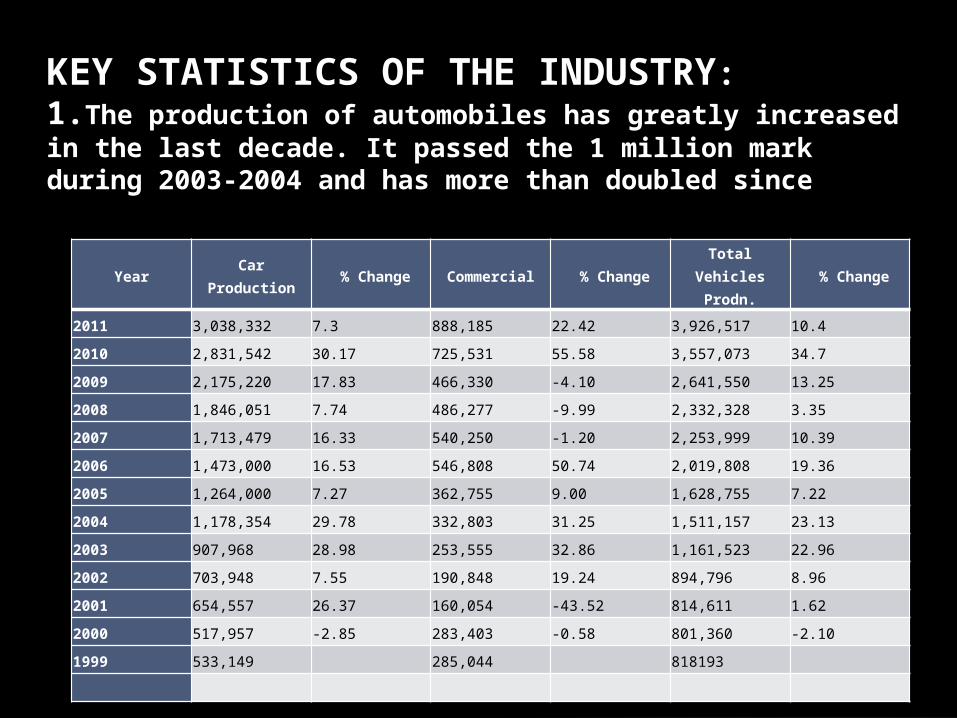

2011 3,038,332 7.3 888,185 22.42 3,926,517 10.4

2010 2,831,542 30.17 725,531 55.58 3,557,073 34.7

2009 2,175,220 17.83 466,330 -4.10 2,641,550 13.25

2008 1,846,051 7.74 486,277 -9.99 2,332,328 3.35

2007 1,713,479 16.33 540,250 -1.20 2,253,999 10.39

2006 1,473,000 16.53 546,808 50.74 2,019,808 19.36

2005 1,264,000 7.27 362,755 9.00 1,628,755 7.22

2004 1,178,354 29.78 332,803 31.25 1,511,157 23.13

2003 907,968 28.98 253,555 32.86 1,161,523 22.96

2002 703,948 7.55 190,848 19.24 894,796 8.96

2001 654,557 26.37 160,054 -43.52 814,611 1.62

2000 517,957 -2.85 283,403 -0.58 801,360 -2.10

1999 533,149 285,044 818193

KEY STATISTICS OF THE INDUSTRY:1.The production of automobiles has greatly increased in the last decade. It passed the 1 million mark during 2003-2004 and has more than doubled since

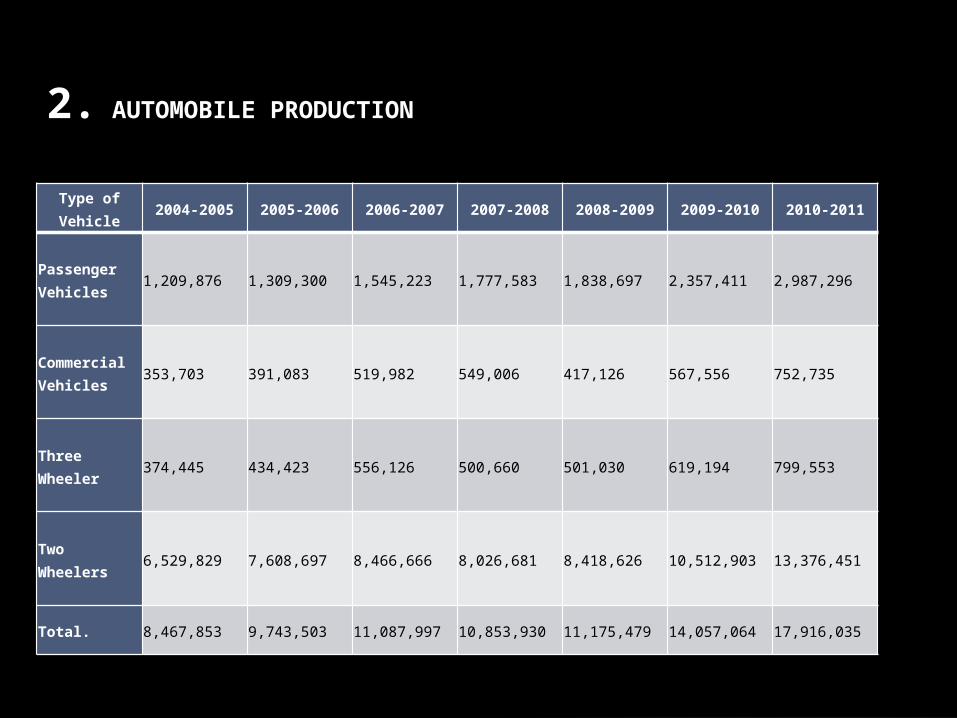

Type of Vehicle

2004-2005 2005-2006 2006-2007 2007-2008 2008-2009 2009-2010 2010-2011

Passenger Vehicles

1,209,876 1,309,300 1,545,223 1,777,583 1,838,697 2,357,411 2,987,296

Commercial Vehicles

353,703 391,083 519,982 549,006 417,126 567,556 752,735

Three Wheeler

374,445 434,423 556,126 500,660 501,030 619,194 799,553

Two Wheelers

6,529,829 7,608,697 8,466,666 8,026,681 8,418,626 10,512,903 13,376,451

Total. 8,467,853 9,743,503 11,087,997 10,853,930 11,175,479 14,057,064 17,916,035

2. AUTOMOBILE PRODUCTION

Year 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009

Motor Vehicle Production[

8,467,853 9,743,503 11,087,997 10,853,930 11,175,479

Industry Revenue USD Million[

24,379 26,969 30,507 32,383 33,342*

Exports (Units)[ 629,544 806,222 1,011,529 1,238,333 1,530,660

Exports (Revenue)

1,915 2,231 2,552 3,008 3,718*

3.YEAR WISE GROWTH OVERALL

The automotive industry of India is categorised into passenger cars, two-wheelers, commercial vehicles and three-wheelers, with two-wheelers dominating the market.

More than 75% of the vehicles sold are two-wheelers. Nearly 59% of these two-wheelers sold were motorcycles and about 12% were scooters. Mopeds occupy a small portion in the two-wheeler market however; electric two-wheelers are yet to penetrate.

The passenger vehicles are further categorised into passenger cars, utility vehicles and multi-purpose vehicles. All sedan, hatchback, station wagon and sports cars fall under passenger cars.

PRODUCT AND SERVICE SEGMENTATION:

Multi-purpose vehicles or people-carriers are similar in shape to a van and are taller than a sedan, hatchback or a station wagon, and are designed for maximum interior room.

Utility vehicles are designed for specific tasks. The passenger vehicles manufacturing account for about 15% of the market in India.

Commercial vehicles are categorised into heavy, medium and light. They account for about 5% of the market. Three-wheelers are categorised into passenger carriers and goods carriers. Three-wheelers account for about 4% of the market in India.

Many services were introduced by automobile company are :

1. Maintaince servicing.

2. Vehicle Insurance.

3. Vehicle finance schemes.

4. Test drive.

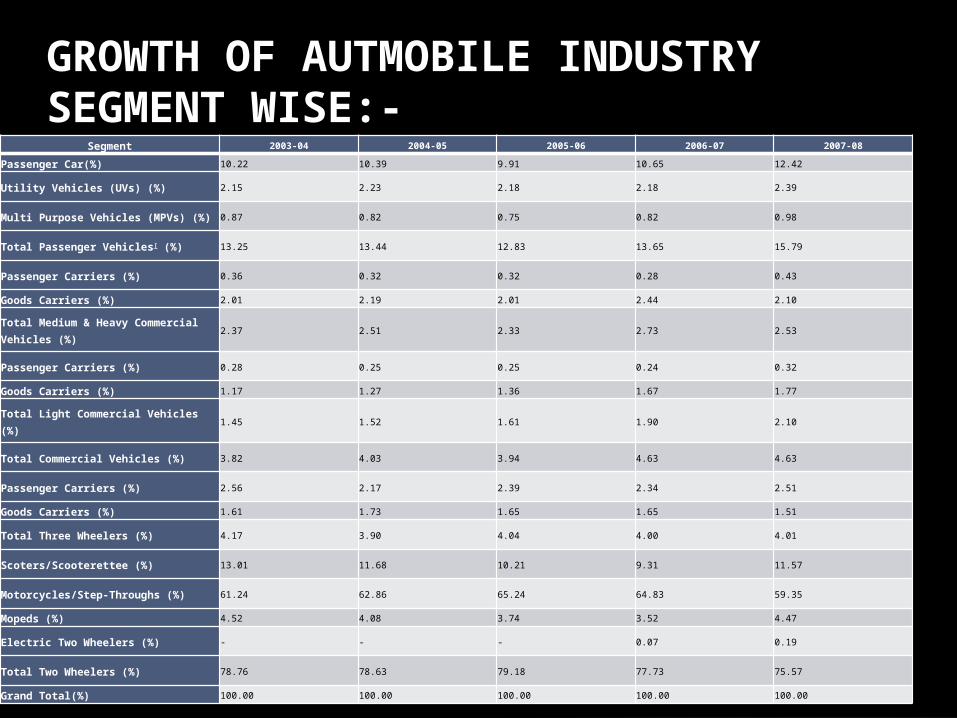

GROWTH OF AUTMOBILE INDUSTRY SEGMENT WISE:-

Segment 2003-04 2004-05 2005-06 2006-07 2007-08

Passenger Car(%) 10.22 10.39 9.91 10.65 12.42

Utility Vehicles (UVs) (%) 2.15 2.23 2.18 2.18 2.39

Multi Purpose Vehicles (MPVs) (%) 0.87 0.82 0.75 0.82 0.98

Total Passenger Vehicles[ (%) 13.25 13.44 12.83 13.65 15.79

Passenger Carriers (%) 0.36 0.32 0.32 0.28 0.43

Goods Carriers (%) 2.01 2.19 2.01 2.44 2.10

Total Medium & Heavy Commercial Vehicles (%)

2.37 2.51 2.33 2.73 2.53

Passenger Carriers (%) 0.28 0.25 0.25 0.24 0.32

Goods Carriers (%) 1.17 1.27 1.36 1.67 1.77

Total Light Commercial Vehicles (%) 1.45 1.52 1.61 1.90 2.10

Total Commercial Vehicles (%) 3.82 4.03 3.94 4.63 4.63

Passenger Carriers (%) 2.56 2.17 2.39 2.34 2.51

Goods Carriers (%) 1.61 1.73 1.65 1.65 1.51

Total Three Wheelers (%) 4.17 3.90 4.04 4.00 4.01

Scoters/Scooterettee (%) 13.01 11.68 10.21 9.31 11.57

Motorcycles/Step-Throughs (%) 61.24 62.86 65.24 64.83 59.35

Mopeds (%) 4.52 4.08 3.74 3.52 4.47

Electric Two Wheelers (%) - - - 0.07 0.19

Total Two Wheelers (%) 78.76 78.63 79.18 77.73 75.57

Grand Total(%) 100.00 100.00 100.00 100.00 100.00

The level of volatility is medium.

Over the past few years, the Motor Vehicle Manufacturing industry has become more volatile. This has been the result of fluctuations in metal prices and fuel prices, as well as changes in legislation and assistance packages.

India's increasing per capita disposable income and growth in exports is playing a major role in the rise and the competitiveness of the industry.

According to the Economic Times of India, economic liberalization – allowing unrestricted Foreign Direct Investment (FDI) and removing foreign currency neutralisation and export obligations – has been also been one of the key to India's automotive volatility.

INDIAN AUTOMOBILE INDUSTRY VOLATILTY:-

The Indian Automotive Industry after de-licensing in July 1991 has grown at a spectacular rate on an average of 17% for last few years.

The industry has attained a turnover of USD $35.8 billion, (INR 165,000 crores) and an investment of USD 10.9 billion.

The industry has provided direct and indirect employment to 13.1 million people. Automobile industry is currently contributing about 5% of the total GDP of India.

The projected size in 2016 of the Indian automotive industry varies between $122 billion and $159 billion including USD 35 billion in exports. This translates into a contribution of 10% to 11% towards India's GDP by 2016, which is more than double the current contribution.

INDIAN AUTOMOBILE MARKET CHARACTERSTICS:-

Determinants of demand for this industry include vehicle prices (which are determined largely by wage, material and equipment costs) and exchange rates, preferences, the running cost of a vehicle (mainly determined by the price of petrol), income, interest rates, scrapping rates, and product innovation.

Exchange Rate: Movement in the value of Rupee determines the attractiveness of Indian products overseas and the price of import for domestic consumption.

Affordability: Movement in income determine the affordability of new motor vehicles. Allowing unrestricted Foreign Direct Investment (FDI) led to increase in competition in the domestic market hence, making better vehicles available at affordable prices.

INDIAN AUTOMBILE INDUSTRY DEMAND DETERMINANTS:-

Product Innovation is an important determinant as it allows better models to be available each year and also encourages manufacturing of environmental friendly cars.

Demographics: It is evident that high population of India has been one of the major reasons for large size of automobile industry in India. Factors that may be augment demand include rising population and an increasing proportion of young persons in the population that will be more inclined to use and replace cars. Also, increase in people with lesser dependency on traditional single family income structure is likely to add value to vehicle demand.

Infrastructure: Longer-term determinants of demand include development in Indian's infrastructure. India needs about $500 billion to repair its infrastructure such as ports, roads, and power units. These investments have been made with an aim to generate long-term cash flow from automobile, power, and telecom industries.

The Indian automotive industry embarked a new journey in 1991 with de-licensing of the sector and subsequent opening up for 100% foreign direct investment (FDI).

Since then almost all global majors have set up their facilities in Indian taking the level of production from 2 million in 1991 to over 10 million in recent years.

The exports in automotive sector have grown on an average compound annual growth rate of 30% per year for the last seven years. The export earnings from this sector are over USD 6 billion.

Even with this rapid growth, the Indian automotive industry's contribution in global terms is very low. This is evident from the fact that even thought passenger and commercial vehicles have crossed the production figures of 2.3 million in the year 2008, yet India's share is about 3.28% of world production of 70.53 million passenger and commercial vehicles. India's automotive exports constitute only about 0.3% of global automotive trade.

INDIAN AUTOMOBILE INDUSTRY INTERNATIONAL MARKET STATUS:

The automobile industry has defined its target in the Automotive Mission Plan as To emerge as the destination of choice in the world for design and manufacture of automobiles with output reaching a level of USD 145 billion accounting more than 10% of GDP and providing additional employment to 25 million people by 2016.

In order to achieve these goals the following key recommendations have been made in the Automotive Mission Plan to the Indian Government and Industry:-

Manufacturing and export of small cars, multi-utility vehicles, two- and three-wheelers, tractors, components to be promoted Care to be taken of negative like and rules of the country with current negotiation of Free Trade Agreement and Regional Trade agreement with countries like Thailand, Singapore, Malaysia, China, Korea, Egypt, Gulf etc.

INDIAN AUTOMOBILE INDUSTRY TRYING FOR:-

Trying to adapt a Attractive Tariff Policy which may follow attractive investment. Specific measures will be taken for expansion of domestic market. Incremental investment of USD 35 to 40 billion to Automotive Industry during the next 10 years.

National level Automotive Institute for training on automobile at International Training Institutes (ITIs) and Automotive Training Institute (ATIs) to be set up.

An Auto Design Centre to be established at National Institute of Design, Ahmadabad. National Automotive Testing and R&D Implementation Project (NATRIP) to act as Centre of Excellence for Technical Design Data.

The profitability of motor vehicle manufacturers has been rising over the past five years, mainly due to rising demand and growth of Indian middle class and industry is trying to continue it by focusing on this segment.

In tune with international standards to reduce vehicular pollution, the central government unveiled the standards titled 'India 2000' in 2000 with later upgraded guidelines as 'Bharat Stage'.

These standards are quite similar to the more stringent European standards and have been traditionally implemented in a phased manner, with the latest upgrade getting implemented in 13 cities and later, in the rest of the nation.

Delhi(NCR), Mumbai, Kolkata, Chennai, Bangalore, Hyderabad, Ahmedabad, Pune, Surat, Kanpur, Lucknow, Solapur, and Agra are the 13 cities where Bharat Stage IV has been imposed while the rest of the nation is still under Bharat Stage III.

These changes were very effective for indian automobile industry to meet with international standards and and thse standards of international market.

EMMISION NORMS CHANGES

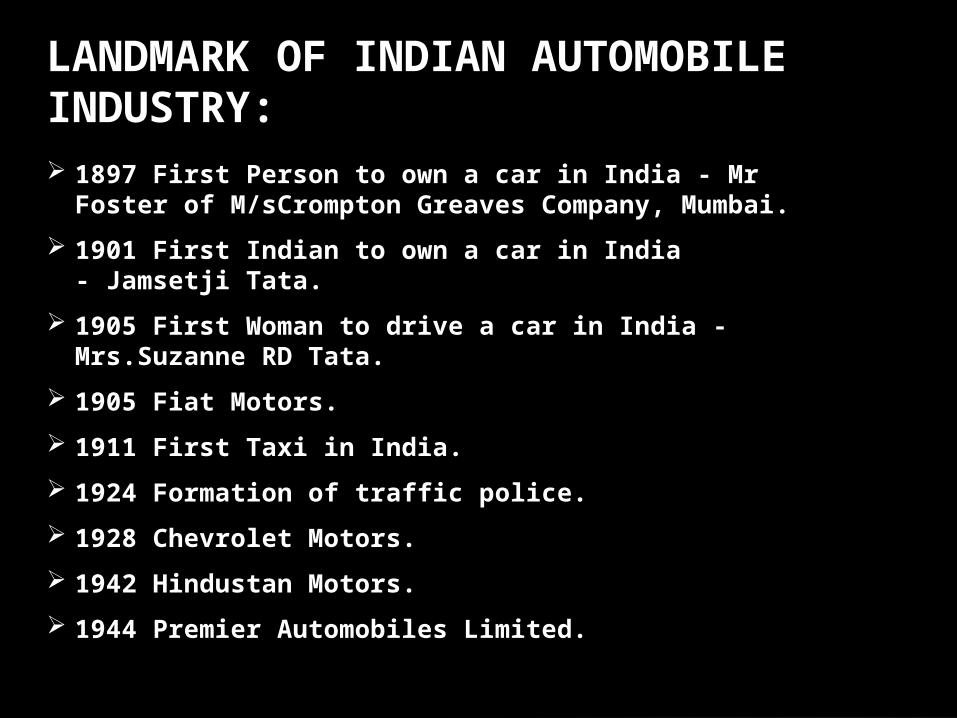

1897 First Person to own a car in India - Mr Foster of M/sCrompton Greaves Company, Mumbai.

1901 First Indian to own a car in India - Jamsetji Tata.

1905 First Woman to drive a car in India - Mrs.Suzanne RD Tata.

1905 Fiat Motors.

1911 First Taxi in India.

1924 Formation of traffic police.

1928 Chevrolet Motors.

1942 Hindustan Motors.

1944 Premier Automobiles Limited.

LANDMARK OF INDIAN AUTOMOBILE INDUSTRY:

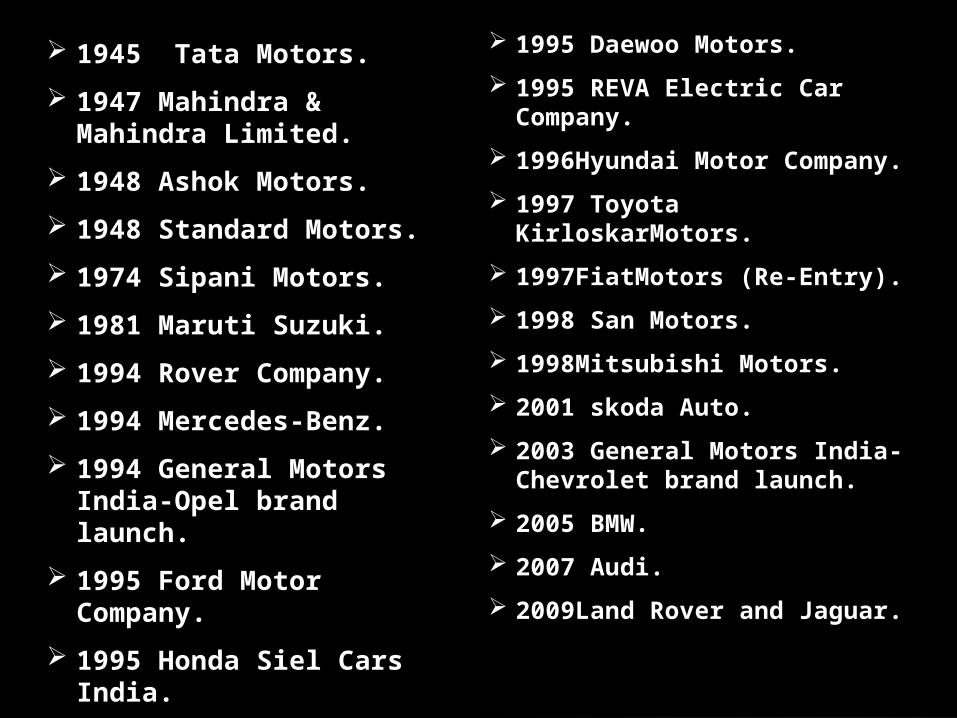

1995 Daewoo Motors.

1995 REVA Electric Car Company.

1996Hyundai Motor Company.

1997 Toyota KirloskarMotors.

1997FiatMotors (Re-Entry).

1998 San Motors.

1998Mitsubishi Motors.

2001 skoda Auto.

2003 General Motors India-Chevrolet brand launch.

2005 BMW.

2007 Audi.

2009Land Rover and Jaguar.

1945 Tata Motors.

1947 Mahindra & Mahindra Limited.

1948 Ashok Motors.

1948 Standard Motors.

1974 Sipani Motors.

1981 Maruti Suzuki.

1994 Rover Company.

1994 Mercedes-Benz.

1994 General Motors India-Opel brand launch.

1995 Ford Motor Company.

1995 Honda Siel Cars India.

Tata Motors: Market Share: Commercial Vehicles 63.94%, Passenger Vehicles 16.45%.

Maruti Suzuki India :Market Share: Passenger Vehicles 46.07%.

Hyundai Motor India :Market Share: Passenger Vehicles 14.15%

Mahindra & Mahindra: Market Share: Commercial Vehicles 10.01%, Passenger Vehicles 6.50%, Three Wheelers 1.31%.

Ashok Leyland: Market Share: Commercial Vehicles 22%.

Hero MotoCorp is occupying over 41% and sharing 26% of the two-wheeler market in India with Bajaj Auto.

Bajaj Auto in itself is occupying about 58% of the three-wheeler market.

INDIAN AUTOBILE INDUSTRY KEY COMPETITORS:-

The government spending on infrastructure in roads and airports and higher GDP growth in the future will benefit the auto sector in general. We expect a slew of launches in the Segment 'B' and Segment 'C' of passenger cars. Utility vehicle segment is expected to grow at around 8% to 9% in the long-term.

In the 2-wheeler segment, motorcycles are expected to witness a flurry of new model launches. Though the market size is expected to grow by 10% to 12%, competitive pressure could keep prices and margins under control. TVS, Honda and Hero Motocorp are poised to benefit from higher demand for ungeared scooters in the urban and rural markets.

FUTURE EXPECTED GROWTH:

Riding the wave of structural changes taking place in the country, the tractor industry registered good growth in FY10 as well as FY11. he strong performance continued in FY11 as well as volumes grew by 20%. While good monsoon is a positive for the sector, given the fact that non-farm incomes have continued to climb up, volumes should still hold up pretty well despite a year or two of poor monsoons. The longer-term picture is impressive in light of poor mechanisation levels in the country’s farm sector and the thrust of the government on improving rural infrastructure.

With an estimated 40% of CVs plying on the roads being 10 years old, demand for HCVs is expected to grow by 7% to 8% over the long term. While the industry is going through cyclical hiccups currently, we expect this factor to weaken in the future on account of strong structural tailwinds. The privatisation of select state transport undertakings bodes well for the bus segment.

End of licensee raj 1991 (DE licensing).

An amazing gear up in competition.

Technological up gradation.

Customer oriented market development.

Increased service facility's.

Development & growth of oil company's with automobile company's in parallel way.

Development & growth of infrastructure company's with automobile company's in indirect way.

Formation of traffic police and increased road safetymeasures

CHANGES WITNESSED:

THANK YOU

DRIVE SAFE