Embed Size (px)

Citation preview

Austria

Transfer Pricing Overview Presented by Clemens Nowotny (LeitnerLeitner)

Agenda

Austrian Transfer Pricing Rules

Selected Highlights from Austrian TPG 2010

Documentation Requirements

Compliance and Transfer Pricing Audits

Advance Pricing Agreement

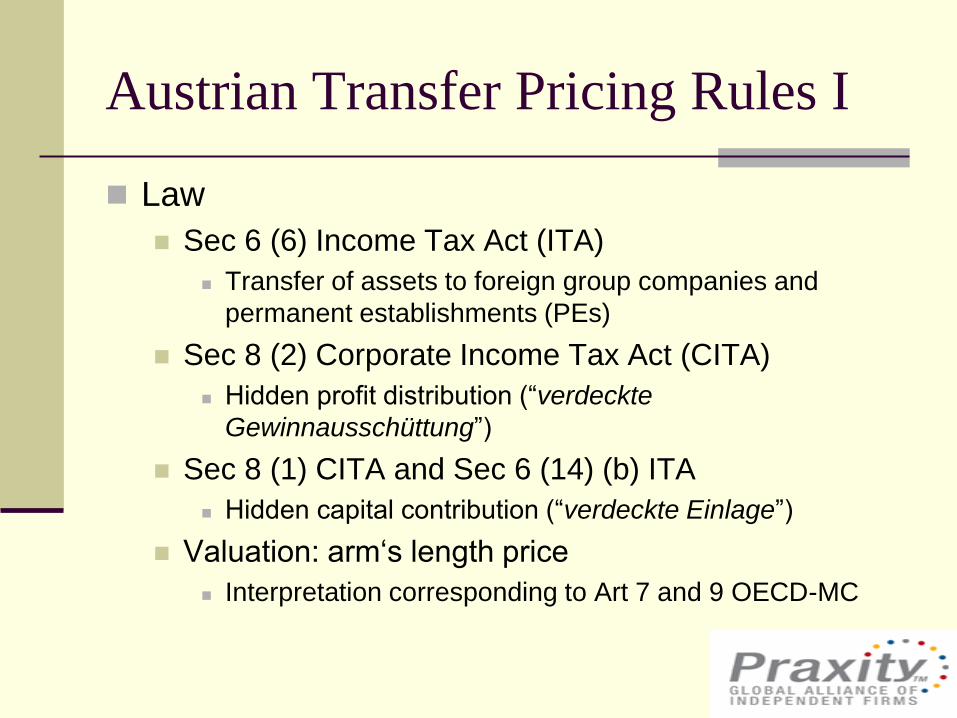

Austrian Transfer Pricing Rules I

Law

Sec 6 (6) Income Tax Act (ITA)

Transfer of assets to foreign group companies and

permanent establishments (PEs)

Sec 8 (2) Corporate Income Tax Act (CITA)

Hidden profit distribution (“verdeckte

Gewinnausschüttung”)

Sec 8 (1) CITA and Sec 6 (14) (b) ITA

Hidden capital contribution (“verdeckte Einlage”)

Valuation: arm„s length price

Interpretation corresponding to Art 7 and 9 OECD-MC

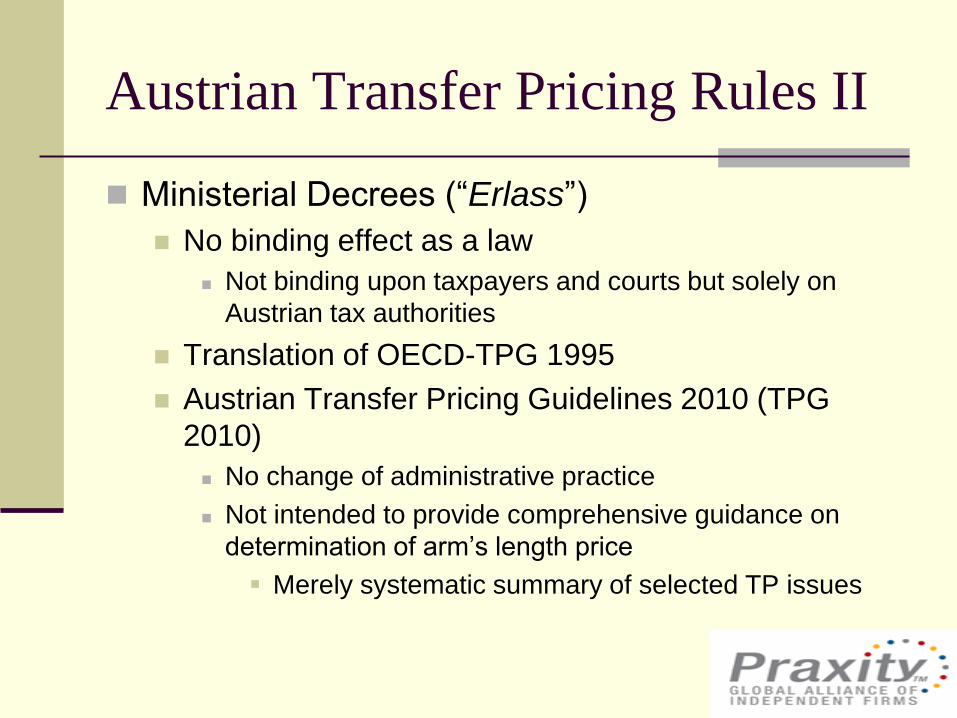

Austrian Transfer Pricing Rules II

Ministerial Decrees (“Erlass”)

No binding effect as a law

Not binding upon taxpayers and courts but solely on

Austrian tax authorities

Translation of OECD-TPG 1995

Austrian Transfer Pricing Guidelines 2010 (TPG

2010)

No change of administrative practice

Not intended to provide comprehensive guidance on

determination of arm‟s length price

Merely systematic summary of selected TP issues

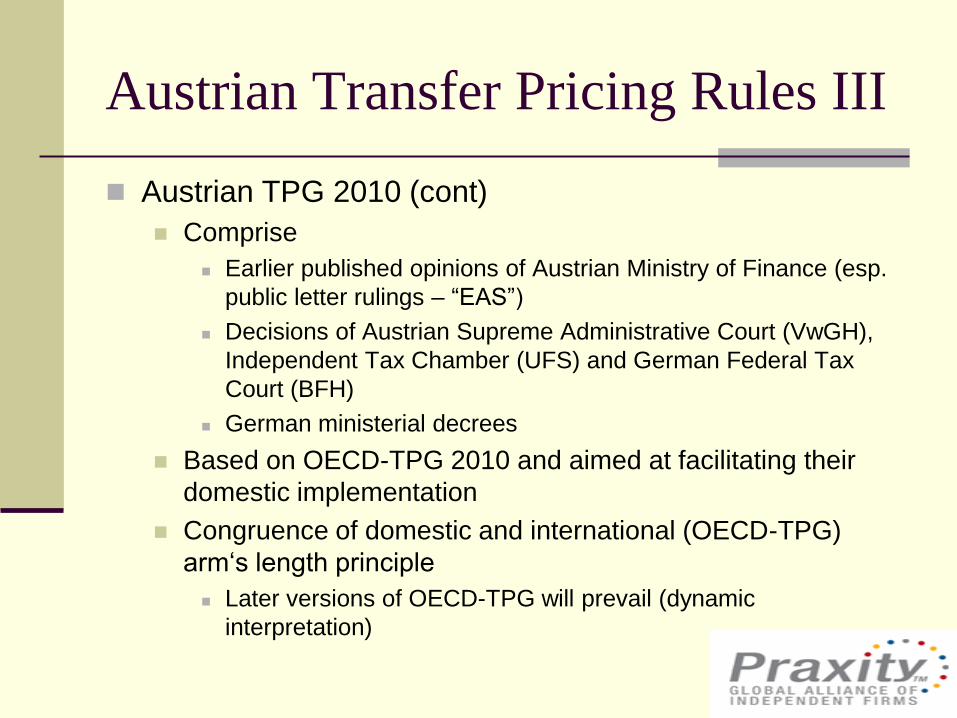

Austrian Transfer Pricing Rules III

Austrian TPG 2010 (cont)

Comprise

Earlier published opinions of Austrian Ministry of Finance (esp.

public letter rulings – “EAS”)

Decisions of Austrian Supreme Administrative Court (VwGH),

Independent Tax Chamber (UFS) and German Federal Tax

Court (BFH)

German ministerial decrees

Based on OECD-TPG 2010 and aimed at facilitating their

domestic implementation

Congruence of domestic and international (OECD-TPG)

arm„s length principle

Later versions of OECD-TPG will prevail (dynamic

interpretation)

Austrian Transfer Pricing Rules IV

Austrian TPG 2010 (cont)

Primarily aimed at avoiding “unjustified” profit

transfers to foreign jurisdictions (abuse of law)

But: any statement referring to outbound transaction also

to be applied to corresponding inbound transaction et

vice versa

5 Chapters

Multinational group structures

Multinational PE structures

TP documentation requirements

TP audits by tax authorities

Tax planning via intermediate companies

Selected Highlights I

Austria follows OECD-TPG 2010 to large extent

Selected controversial issues in Austrian TPG

2010 and administrative practice

Dynamic interpretation (slide 5)

TP adjustment to median (slide 19)

Use of databases and comparability

Profit margin for routine services

Intra-group financing services

Shareholder costs

Business Restructurings

Selected Highlights II

Use of databases

“Unrestricted“ comparability required (para 66 AT TPG 2010)

5 comparability factors according to OECD-TPG

In case of limited comparability

Database search unusable

Relevance for “rough control calculation” only (para 65 AT TPG 2010)

Excessive requirement

No need for database search in case of unrestricted comparability

In practice not available – implications for tax audits?

Multiple-year data accepted to enhance reliability

Qualitative screening mandatory

Use of interquartile range

“Common international practice” (para 67 AT TPG 2010)

Not to enhance comparability in case of limited comparability of data

(German decree on documentation requirements, 2005)

Selected Highlights III

Profit margin for routine services

C+ appropriate except if direct comparables are available (CUP)

Cost base: direct and indirect cost

Markup for routine services between 5% and 15% (para 77 AT TPG

2010)

No safe harbour rule but approximate guidance

Not every markup within range considered arm‟s length

Markup to be determined on a case by case basis

EU-JTPF: arm‟s length mark up between 3% and 10% (regularly

around 5%)

In specific circumstances charging at cost acceptable

Services not part of core business of enterprise and mere ancillary

service provision towards related party with continuing transactions

(maintaining customer relationship)

Agency costs

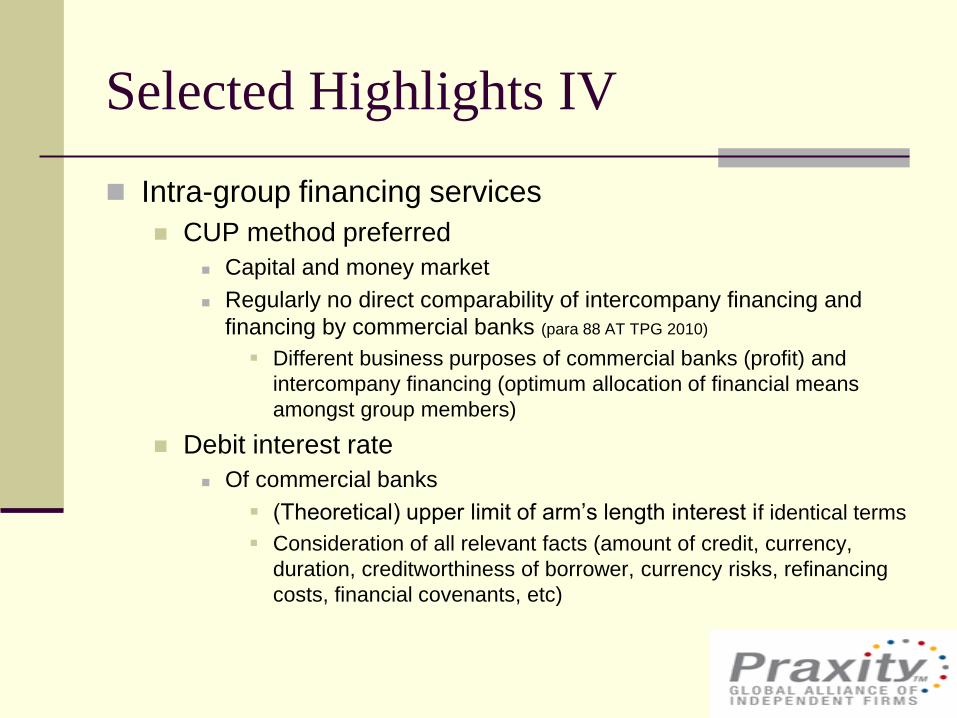

Selected Highlights IV

Intra-group financing services

CUP method preferred

Capital and money market

Regularly no direct comparability of intercompany financing and

financing by commercial banks (para 88 AT TPG 2010)

Different business purposes of commercial banks (profit) and

intercompany financing (optimum allocation of financial means

amongst group members)

Debit interest rate

Of commercial banks

(Theoretical) upper limit of arm‟s length interest if identical terms

Consideration of all relevant facts (amount of credit, currency,

duration, creditworthiness of borrower, currency risks, refinancing

costs, financial covenants, etc)

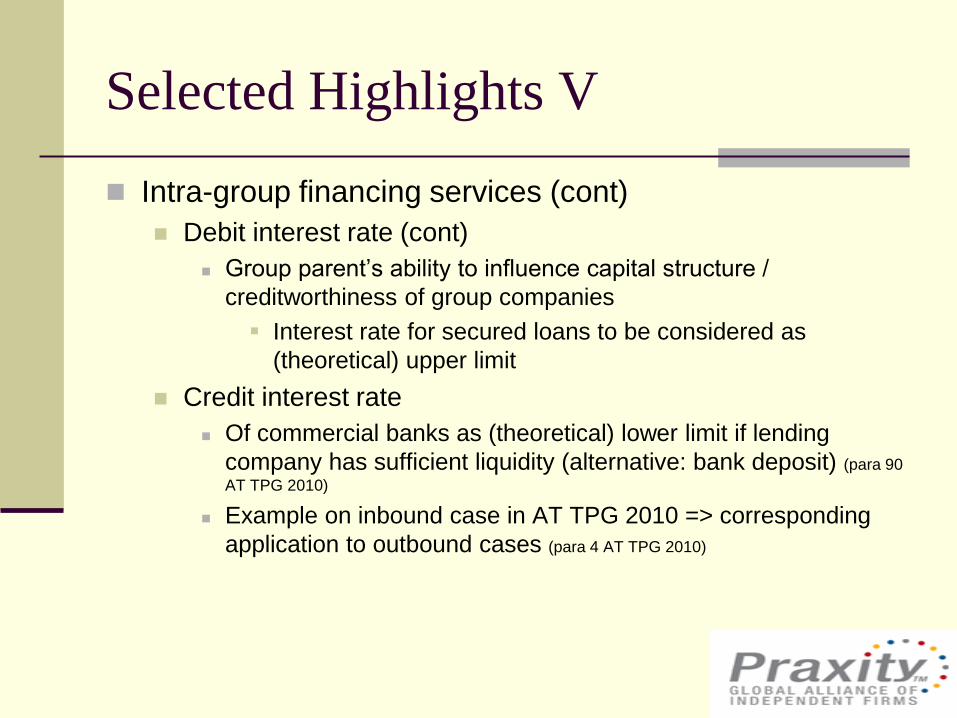

Selected Highlights V

Intra-group financing services (cont)

Debit interest rate (cont)

Group parent‟s ability to influence capital structure /

creditworthiness of group companies

Interest rate for secured loans to be considered as

(theoretical) upper limit

Credit interest rate

Of commercial banks as (theoretical) lower limit if lending

company has sufficient liquidity (alternative: bank deposit) (para 90

AT TPG 2010)

Example on inbound case in AT TPG 2010 => corresponding

application to outbound cases (para 4 AT TPG 2010)

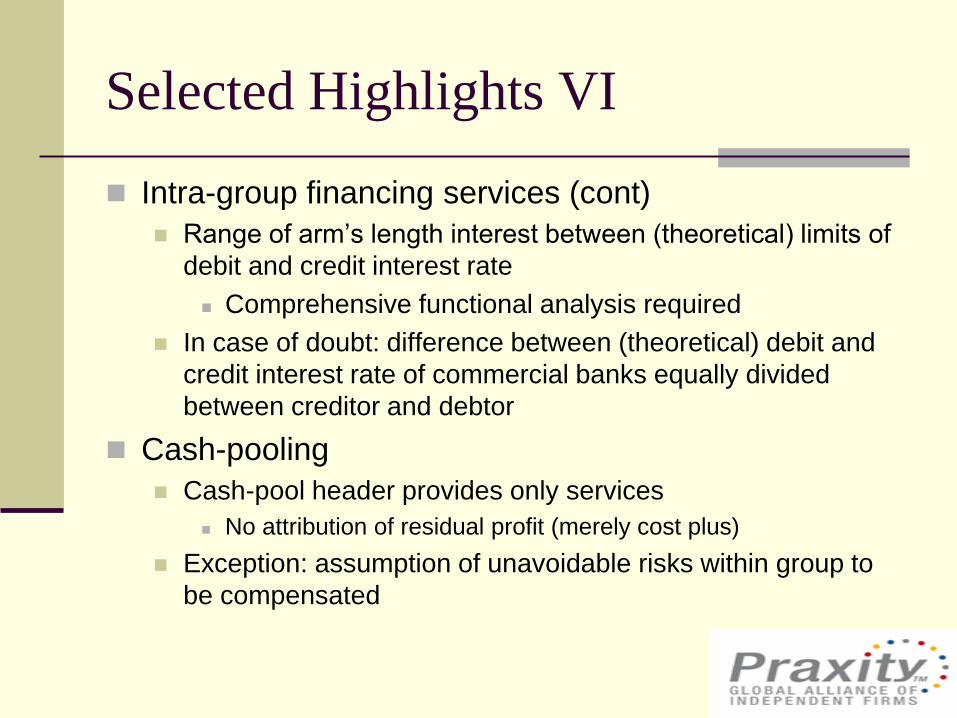

Selected Highlights VI

Intra-group financing services (cont)

Range of arm‟s length interest between (theoretical) limits of

debit and credit interest rate

Comprehensive functional analysis required

In case of doubt: difference between (theoretical) debit and

credit interest rate of commercial banks equally divided

between creditor and debtor

Cash-pooling

Cash-pool header provides only services

No attribution of residual profit (merely cost plus)

Exception: assumption of unavoidable risks within group to

be compensated

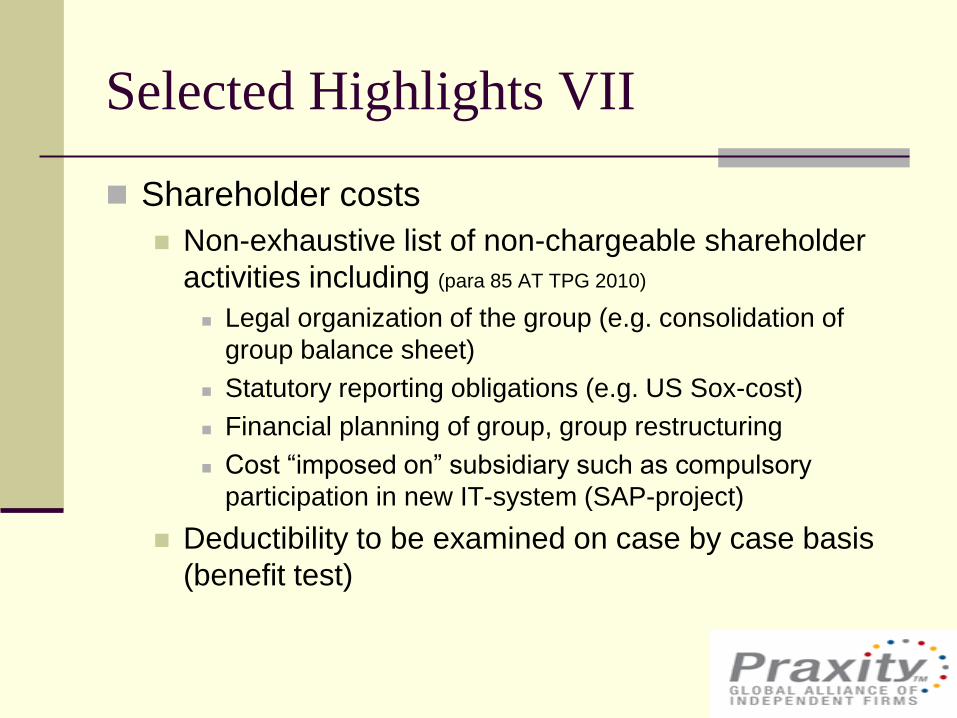

Selected Highlights VII

Shareholder costs

Non-exhaustive list of non-chargeable shareholder

activities including (para 85 AT TPG 2010)

Legal organization of the group (e.g. consolidation of

group balance sheet)

Statutory reporting obligations (e.g. US Sox-cost)

Financial planning of group, group restructuring

Cost “imposed on” subsidiary such as compulsory

participation in new IT-system (SAP-project)

Deductibility to be examined on case by case basis

(benefit test)

Selected Highlights VIII

Business Restructurings

AT TPG 2010 generally follow Chapter IX. OECD-TPG

Relocation of functions (“downsizing”): assumed transfer and

taxation of business opportunity

Third party not willing to give up business opportunity without

compensation (para 136 AT TPG 2010)

Basis for compensation of unsubstantiated business opportunity (resp

“profit potential”) in OECD-TPG 2010 and Austrian domestic tax law?

Conversion of AT sub from fully-fledged distributor into limited-risk

distributor or commissionaire (para 176 AT TPG 2010)

Austrian finance authorities: AT sub qualifies as dependent agent

according to Art 5 (5) OECD-MC

Economic interpretation of “authority to conclude contracts” (para

175 AT TPG 2010)

Application of “two-taxpayer-approach” (OECD-AOA)

TP Documentation Requirements I

No specific legislation on TP documentation requirements

Austrian TPG 2010

General provisions on bookkeeping and record keeping (Sec 124

and 131 Federal Fiscal Code [FFC]) and enhanced obligation to

cooperate in cross-border transactions (Sec 138 FFC)

supposed to serve as legal basis for obligatory TP-documentation (paras 302 et seq AT TPG 2010)

Interpretation of FFC according to Chapter V. OECD-TPG?

Chapter V. OECD TPG 2010 itself does not provide sufficient guidance

on form, content and structure of documentation

Austrian Supreme Administrative Court confirms obligation to document

transfer prices (VwGH 8.7.2009, 2007/15/0036)

EU-TPD according to EU-JTPF (master file +

country-specific appendices) accepted

TP Documentation Requirements II

Content of documentation

Underlying facts (general company information, controlled

transactions, analysis of functions and risks, etc)

Analysis of TP (selected method, arm's length analysis)

No statutory submission deadlines

Public letter ruling No 3198 (24.1.2011)

Obligatory documentation to be prepared until filing of tax

return (at the latest)

Submission upon request of tax authorities (usually during tax

audit) without delay

No specific penalties if documentation missing or

inappropriate

Compliance and TP Audits I

Cooperation obligation of taxpayers relating to TP?

Tax authorities ex officio obliged to investigate factual and

legal circumstances relevant for levying taxes (Sec 115 FFC)

However: in case of cross-border transactions enhanced

obligation of taxpayer to cooperate

Implications in case of non-cooperation:

Reduced standard of proof to be applied by tax authorities

Free appraisal of evidence: exceptional and ambiguous facts may

not be accepted (taxation of false facts to detriment of taxpayer)

Conclusion: the greater complexity and unusualness of the

case, the more significance will attach to documentation (para 5.14 OECD-TPG)

Compliance and TP Audits II

Burden of proof that transfer price not arm‟s length

Lies with tax authorities

Qualified counter-evidence required by finance authorities

Mere reference to experience insufficient (VwGH 20.10.2009,

2006/13/0116)

Formal deficiencies of intercompany agreements

Burden of proof de-facto transferred to taxpayer

Case law (VwGH) on contracts concluded between close

relatives applicable on relationship shareholder - corporation

Rebuttable presumption of hidden profit distribution / capital

contribution

Even if TP at arm‟s length (!)

Compliance and TP Audits III

TP adjustment to median if taxpayer„s transfer

price not within arm„s length range (para 49 AT TPG 2010)

No legal basis for adjustment to median –

adjustment to taxpayer‟s most preferential value

within range (?)

Not arm„s length: any point within the range

acceptable

Conclusion: tax authority‟s attempt to prevent

taxpayer from favorable transfer pricing

arrangements

Compliance and TP Audits IV

TP Adjustments

Corresponding adjustment

Based on primary adjustment by other contracting state

Obligatory according to Art 9 (2) OECD-MC (para 322 AT TPG 2010)

Without mutual agreement procedure according to Art 25

(2) OECD-MC (“on short way”)

Only if finance authorities consider primary adjustment

to be justified both in principle and as regards the

amount

Not automatically: taxpayer must document accuracy of

foreign primary adjustment

Procedural problems may occur (statute of limitation)

Compliance and TP Audits V

TP Adjustments (cont)

Secondary Adjustment

May be avoided by posting an account receivable or account

payable (paras 326 et seq AT TPG 2010)

Hidden profit distribution

If no corresponding account payable abroad accepted

25% withholding tax

No relief at source under EC Parent-Subsidiary-Directive in

case of “obvious” hidden profit distributions (refund

procedure)

Reduction of withholding tax rate according to DTT applicable

(relief at source: certificate of residence and proof of

substance of foreign company required)

Hidden capital contribution

If transfer of profit not corrected abroad

Advance Pricing Agreement

Unilateral Advance Ruling (Sec 118 FFC)

Scope: Transfer pricing, reorganizations, group taxation

Written filing required (pre-filing recommended)

Binding effect if identity between alleged and actual facts

Expiration of ruling if underlying tax provisions amended

Fees: EUR 1,500 – 20,000 depending on revenue of

applicant

Bilateral APA

On basis of Art 25 OECD-MC (MAP)

Austria: first bilateral APA concluded at the end of 2011

Questions?

Contact

Dr. Clemens Nowotny

International Tax Partner

T +43 732 70 93 - 359

LeitnerLeitner GmbH

Wirtschaftsprüfer und Steuerberater

Ottensheimer Straße 30

4040 Linz Austria

www.leitnerleitner.com

Contact

CZECH REPUBLIC

Praha

┐

SLOVAKIA

Bratislava

┐

HUNGARY

Budapest

┐

ROMANIA

Bucureşti

┐

AUSTRIA

Salzburg

Linz Vienna

┐

┐

┌

SLOVENIA

Ljubljana

┐

CROATIA Zagreb

┐

BOSNIA AND HERZEGOVINA

Sarajevo

┌

SERBIA

Beograd ┐