Embed Size (px)

Citation preview

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/researchdisclosures or call +1 (877) 291-2683 US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

21 January 2013

Asia Pacific/Australia

Equity Research

Macro

Australian ESG/SRI SOCIALLY RESPONSIBLE INVESTING

Banks down, REITS up, RIO down to BB

■ Key stock calls. We have taken key calls from our sector analysts, strategy

team, quant team, and HOLT Best in Class stocks, and overlaid an ESG

view. Our key ESG long calls are BXB (strategy), CRZ, MMS (also HOLT),

TAH, (sector analysts), AUT, ILU, PRU (quant) and FLT, HGG (HOLT Best

in Class). Our key short calls are TWE (sector analyst) and EGP (Quant).

■ MSCI IVA rating upgrades for REITS: New poster child for AAA rating.

CFX (AA), CQR (BB), GMG (AA), IOF (AAA), WDC (BBB) and WRT (BB) all

have managed an upgrade to their MSCI IVA ratings. REITS now dominate the

MSCI IVA AAA rated stocks in Australian (CPA, DXS, GPT, IOF, LLC, SGP).

■ No AAA rated Australian banks post MSCI IVA rating downgrades.

ANZ (AA), BOQ (BB), CBA (AA), NAB (A) and WBC (AA), all have suffered

MSCI IVA rating downgrades amid litigation concerns. No Australian banks

are rated AAA now, with ANZ, CBA and WBC the highest rated at AA.

■ Resource companies mixed bag: AWC (A), BHP (A), RIO (BB), WHC (B)

all suffered downgrades in their MSCI IVA ratings. BTU (B), GBG (BB),

MGX (BB), OZL (BBB), PNA (A) and WSA (BBB) had an MSCI IVA rating

upgrade. Resource companies that still have an MSCI IVA rating in the A

zone include: BHP (A), CTX (A), GRY (A), ORG (AA), PNA (A), PAN (AA),

STO (A) and WPL (AA).

■ RIO at risk with BB rating: RIO has had its MSCI IVA rating downgraded

from BBB to BB. With many of its peers rated at A (including BHP), a rating

of BB risks RIO being excluded from some investors’ universe. Or

conversely, it risks other BB or lower MSCI IVA rated companies being

squeezed from some investors’ consideration (NCM, OSH also BB rated).

Figure 1: Key stock calls with an ESG overlay Ticker Company name Actual

share

price ($)

Target

Price

($)

Rating MSCI

ESG

Rating

View on

MSCI

rating

Market

cap

($mn)

AUT.AX Aurora Oil & Gas 3.43 4.10 OUTPERFORM B Positive 1,615

BXB.AX Brambles Limited 7.80 7.90 OUTPERFORM AAA Neutral 12,762

CRZ.AX carsales.com.au 8.66 8.80 OUTPERFORM B Positive 2,042

FLT.AX Flight Centre 28.27 26.35 OUTPERFORM B Positive 2,832

ILU.AX Iluka Resources 9.70 11.00 OUTPERFORM BBB Positive 4,061

MMS.AX McMillan Shakespeare 13.60 14.85 OUTPERFORM B Positive 1,014

PRU.AX Perseus Mining 1.96 3.20 OUTPERFORM B Positive 895

TAH.AX Tabcorp Holdings 3.04 3.30 OUTPERFORM AAA Neutral 2,231

EGP.AX Echo Entertainment 3.55 3.30 UNDERPERFORM BB Neutral 2,931

TWE.AX Treasury Wine 4.73 3.50 UNDERPERFORM B Neutral 3,061 Source: MSCI IVA ratings, Company data, Credit Suisse estimates

Research Analysts

Sandra McCullagh

61 2 8205 4729

21 January 2013

Australian ESG/SRI 2

Analyst changed views on ESG Target Price impacts

■ ESG embedded into analysts’ Target Prices. At Credit Suisse Australia, we have

developed a methodology for embedding Environment, Social, and Governance (ESG)

issues into how analysts’ view on stocks. This includes assessing an explicit impact on

target prices from ESG issues. This is expressed as a percentage impact off an

unaffected target price. For example, let’s consider a stock that would normally have a

$10 target price, if there were no ESG concerns. If the analysts has a view that ESG

concerns have a 10% downside impact to the target price, this would result in a $9

target price, -10% as the ESG impact is included in the target price.

■ We published our first view of the impact on analysts’ target prices on 2 July 2012 in

our note “$21.4bn in ESG concerns on Australian stocks”, with subsequent notes

on 24 October “ESG changes in stocks calls and analyst views”. The following is

a commentary on recent changes to the percentage impact on individual stock target

prices (refer Figure 2).

Figure 2: Recent analysts changes to ESG impact on target prices Ticker Company name Actual

share

price ($)

Target

Price

($)

Rating ESG TP

impact -

updated

ESG TP

impact -

prior

Change in

ESG TP

impact

ESG TP Impact Comment

APN.AX APN News & Media 0.32 0.23 UNDERPERFORM -3.0% -3.0% Independent Chairman has reduced governance risk, however APN does not

have a majority of independent Directors and major shareholder INM retains

considerable influence over the company.

BSE.AX Base Resources Ltd 0.36 0.80 OUTPERFORM -68.0% -13.0% -55.0% The Kenyan Government has passed a regulation that says every mineral right

shall have a local equity participation amounting to at least 35% but is silent on

whether it applies to existing leases and if there is any compensation. Until we

have more clarity, we value BSE at a sharp 60% discount to our DCF as, in

addition to potential dilution, there is a risk project funding can no longer be

unlocked and the project stalls. This discount is in addition to increasing our

WACC by 2% to adjust for country risk.

FXJ.AX Fairfax Media 0.54 0.40 UNDERPERFORM -3.0% -3.0% Gina Rinehart has been vocal in her opposition to parts of the company’s

strategic direction and the company’s Board composition. Increased influence of

a major shareholder may also pose problems in relation to editorial independence.

KGD.AX Kula Gold 0.34 0.55 OUTPERFORM 0.0% -25.0% 25.0% TP set using a bear case scenario that assumes a heavily discounted capital

raising. As such ESG issues are now largely inherent in our bear case capital

raising scenario, that include, but are not limited to, geopolitcal risk in PNG.

NWS.AX News Corporation 26.33 27.00 NEUTRAL -10.0% -17.2% 7.2% NWS has been faced with significant governance issues; most recently the

phone hacking controversy and the failed takeover of BSkyB. The considerable

influence that Rupert Murdoch and the Murdoch family exert over the company

through its dual class share structure raises the risk of further governance issues

in the future as well as inhibiting the rights of minority shareholders.

PRT.AX Prime Media Group 0.95 0.86 NEUTRAL -3.0% -3.0% While we have seen no indication that Chairman and major shareholder Paul

Ramsay will try to exert undue influence on the compay, the lack of

independence on the Board is a cause for concern.

REA.AX REA Group 19.24 19.76 OUTPERFORM -5.0% -5.0% NWS owns over half the shares in REA and has effective Board control,

resulting in a low free float and reduced liquidity in addition to higher risks to

minority shareholders.

SGN.AX STW Communications Group 1.18 1.24 OUTPERFORM -2.0% -2.0% While WPP to date has not looked to exert undue influence on the company, as

SGN expands internationally it is possible that its interests may conflict with

those of WPP. Additionally, given that the company is increasingly investing in

South East Asia where ESG risks may be more prevalent and harder to

measure, this is something that we will be keeping our eye on.

SWM.AX Seven West Media Ltd 2.03 1.80 OUTPERFORM -5.0% -5.0% The lack of independence on the board and large influence of major shareholder

Kerry Stokes increases the risk to minority shareholders and their interests.

TEN.AX Ten Network Holdings 0.35 0.27 OUTPERFORM -5.0% -5.0% Chairman and substantial shareholder Lachlan Murdoch has previously shown his

willingness to exert his influence over the company by taking over as Interim

CEO prior to the commencement of James Warburton’s employment.

Additionally, less than half of TEN’s Board is independent, lessening the likelihood

of the Board resisting attempts to influence the company by major shareholders.

TME.AX Trade Me Group Ltd 3.21 3.70 NEUTRAL -3.0% -3.0% The board is not fully independent and there is a risk that minority shareholders'

wishes could be ignored by majority shareholder FXJ.

Source: Company data, Credit Suisse estimates

■ Media stocks initiation: Our analysts have assumed coverage of the media sector

stocks. Our key piece, Australian ESG/SRI - ESG in the Media Sector, published

on 27 November 2012, covers the ESG issues for the Media sector in detail. The key

target price impacts for Media centre around Governance concern. The largest

21 January 2013

Australian ESG/SRI 3

downside impact is -10% for NWS, which is based on historic share price impact from

News of the World scandals. All other stocks’ downsides are then considered relative

to NWS, with a 5% target price downsides for SWM, TEN and REA, 3% downside for

APN, FXJ, PRT and TME and 2% downside for SGN.

■ KGD Target Price based off discounted capital raising: We have based our KGD

target price off a Bear Case of a heavily discounted capital raising. Therefore any ESG

concerns are captured as part of the capital raising and is not separated out, removing

the previous 25% downside on the target price for ESG issues associated with PNG.

■ Resource stocks and asbestos liabilities continue to dominate: The stocks with

10% or more Target Price downside impact from ESG issues are dominated by

resources stocks (refer Figure 3). Interestingly, the stocks with the highest negative

target price impacts from ESG all are rather lowly rated by MSCI IVA (range is BBB to

CCC). CSR, at -39% target price impact from ESG concerns, is BB rated; ERA, with -

36% target price impact is BB rated; BTU; with -18% target price impact is B rated;

JHX with -18% target price impact is BB rated; and NSW, at -10% target price impact

is CCC rated.

Figure 3: Stocks with >-10% ESG downside impact Ticker Company name Actual

share

price ($)

Target

Price

($)

Rating MSCI

ESG

Rating

View on

MSCI rating

TP rating

risk %

Mcap

($mn)

ESG

Impact

($mn)

ESG comment

BSE.AX Base Resources Ltd 0.36 0.80 OUTPERFORM -68.0% 199 423- The Kenyan Government has passed a regulation that says every

mineral right shall have a local equity participation amounting to at

least 35% but is silent on whether it applies to existing leases and if

there is any compensation. Until we have more clarity, we value

BSE at a sharp 60% discount to our DCF as, in addition to

potential dilution, there is a risk project funding can no longer be

unlocked and the project stalls. This discount is in addition to

increasing our WACC by 2% to adjust for country risk.

CSR.AX CSR 2.09 1.40 UNDERPERFORM BB Neutral -39.0% 1,058 676- Our CSR val'v captures the impact from its asbestos liability

(reduces our SOTP val'n by $0.72). The 39% reduction in val's is

high on a relative basis given current depressed (trough cycle)

earnings. We ascribe a nominal impact from the carbon tax effective

1 July 2012.

ERA.AX Energy Resources of

Australia

1.34 1.65 NEUTRAL BB Negative -36.0% 694 390- Key risk is that the Ranger underground mine does not proceed due

to environmental concerns - we currently value it at 75% but also

have a high discount rate - 13% in nominal terms.

JHX.AX James Hardie Industries SE 9.58 9.20 NEUTRAL BB Neutral -18.0% 4,440 975- Our JHX val'v is reduced by A$1.42/share (18.0%) due to the

asbestos liability. Our valuation captures a nominal impact from

carbon (>1%) effective 1 July 2012. MSCI ascribes a 33% weighting

to carbon which we believe is overstated.

BTU.AX Bathurst Resources 0.42 0.60 OUTPERFORM B Neutral -18.0% 289 64- We risk Escarpment and Deep Creek at 50% to account for the

Appeals hearing outcome. The hearing will commence 29 Oct 2012.

TIG.AX Tigers Realm Coal 0.16 0.17 NEUTRAL -17.0% 43 9- We risk the Ammam project at 25% and use a WACC of 11% to

account for ESG impacts of operating in Russia and in a difficult

area

SMR.AX Stanmore Coal 0.21 0.20 NEUTRAL -15.0% 44 8- 10% of our project risk weighting on the Range and Mackenzie

reflects approval risks

SPN.AX SP AusNet 1.13 1.07 NEUTRAL BB Neutral -13.2% 3,805 576- We have reduced our Target Price for SPN to account for risks

associated with pending bushfire litigation and a long-term reduction

in Debt Risk Premiums in regulated WACCs

KAR.AX Karoon Gas 5.49 7.65 OUTPERFORM B Positive -11.7% 1,216 161- We apply a 25% risk weighting on a $/boe to KAR's Brazil/Peru

assets to account for country risk.

MDL.AX Mineral Deposits Ltd. 3.58 6.50 OUTPERFORM BBB Positive -11.0% 314 39- We include country specific risk of 2% to reflect concerns on

corruption and instability in Senegal

BND.AX Bandanna Energy Limited 0.32 0.50 OUTPERFORM -10.0% 166 18- Around 55% of the Springsure Creek project area is located on

strategic cropping land. We see 10% downside risk relating to

regulatory hurdles.

CAB.AX Cabcharge Australia 4.61 5.40 NEUTRAL BBB Negative -10.0% 555 62- For CAB, outside of the consumer services ESG risk factors we

include in our base valuation downside to reflect 1) follow on

litigation as a result of the ACCC settlement for anticompetitive NWS.AX News Corporation 26.33 27.00 NEUTRAL CCC Neutral -10.0% 63,586 7,065- NWS has been faced with significant governance issues; most

recently the phone hacking controversy and the failed takeover of

BSkyB. The considerable influence that Rupert Murdoch and the

Murdoch family exert over the company through its dual class share

structure raises the risk of further governance issues in the future as

well as inhibiting the rights of minority shareholders. Source: MSCI IVA, Company data, Credit Suisse estimates

21 January 2013

Australian ESG/SRI 4

MSCI IVA changes and analysts’ outlook

■ Analyst outlook on MSCI IVA ratings: At Credit Suisse Australia, we use the MSCI

IVA rating system as part of analysts’ assessment of ESG issues for individual stocks.

These ratings range from AAA (top rated) to CCC (lowest rating). Our analysts have

overlaid a forward looking view on the MSCI IVA ratings, based on their views of the

stocks and events that may have happened since the MSCI IVA rating was set. This

provides a ‘Positive’, ‘Neutral’ or ‘Negative’ outlook on the MSCI IVA rating.

■ We published our view on the analysts’ outlook for MSCI IVA ratings on 27 September

2012 in our note “ESG overlay on key stock calls” and updated that on 24 October,

“ESG changes in stocks calls and analyst views”. The following are changes to

the MSCI ratings and analysts’ views since the last note was published. Figure 4

shows the MSCI rating changes in the end of December 2012.

Figure 4: MSCI IVA rating changes—October–December 2012

ENV SOC GOVOVERALLENV SOC GOVOVERALL

ANZ.AX Australia and New Zealand Bank 25/10/2012 DOWN 8.10 5.90 6.00 AA 8.50 6.80 8.40 AAA

APA.AX APA Group 10/10/2012 DOWN 4.60 8.50 7.00 A 5.60 7.90 7.00 AA

AWC.AX Alumina Limited 28/12/2012 DOWN 4.40 4.90 5.70 A 4.50 7.30 6.60 AA

BHP.AX BHP Billiton 28/12/2012 DOWN 4.70 4.20 6.50 A 4.90 5.90 8.20 AA

BOQ.AX Bank of Queensland 25/10/2012 DOWN 3.20 3.40 7.40 BB 3.50 5.30 9.80 BBB

BTU.AX Bathurst Resources 28/12/2012 UP 0.50 2.50 5.70 B 1.40 3.40 3.80 CCC

CBA.AX Commonwealth Bank Australia 25/10/2012 DOWN 8.40 5.60 5.50 AA 8.70 6.10 10.00 AAA

CFX.AX CFS Retail Property Trust 10/10/2012 UP 6.90 9.20 7.00 AA 5.20 5.00 7.00 A

COH.AX Cochlear 28/12/2012 DOWN 5.80 4.30 4.40 BB 4.30 5.50 4.90 BBB

CQR.AX Charter Hall Retail REIT 10/10/2012 UP 4.30 5.70 7.00 BB 0.70 5.00 7.00 B

CSL.AX CSL Ltd 10/10/2012 DOWN 3.60 4.20 7.00 BBB 5.00 6.10 7.00 AA

ENV.AX Envestra 10/10/2012 DOWN 1.50 7.80 7.00 BB 3.80 7.30 7.00 BBB

FLT.AX Flight Centre 25/10/2012 DOWN 4.90 7.10 7.00 B 4.80 9.20 7.00 BB

GBG.AX Gindalbie Metals Ltd 28/12/2012 UP 2.60 6.90 7.00 BB 1.60 6.40 7.00 B

GMG.AX Goodman Group 10/10/2012 UP 9.00 3.40 7.00 AA 5.50 5.00 7.00 A

GNC.AX Graincorp 10/12/2012 UP 2.50 4.90 7.00 BB 0.60 5.40 7.00 B

IOF.AX Investa Office Fund 10/10/2012 UP 9.10 4.80 7.00 AAA 6.20 5.00 7.00 AA

IVC.AX Invocare Group 10/12/2012 UP 6.00 5.70 10.00 AAA 9.30 6.40 7.00 A

MGX.AX Mount Gibson Iron 28/12/2012 UP 3.40 5.70 7.00 BB 1.60 5.00 7.00 B

NAB.AX National Australia Bank 25/10/2012 DOWN 9.20 4.40 4.90 A 7.10 6.40 7.00 AA

NVT.AX Navitas Ltd 10/12/2012 UP 3.00 3.80 10.00 BBB 2.90 4.60 7.00 BB

OZL.AX OZ Minerals 28/12/2012 UP 2.70 6.00 4.80 BBB 2.60 3.70 5.20 BB

PNA.AX PanAust 28/12/2012 UP 3.10 5.60 5.70 A 4.10 4.40 4.90 BBB

RIO.AX Rio Tinto 28/12/2012 DOWN 2.50 3.40 5.80 BB 4.10 4.70 5.30 BBB

WBC.AX Westpac 25/10/2012 DOWN 8.80 5.70 5.50 AA 9.10 5.40 10.00 AAA

WDC.AX Westfield 10/10/2012 UP 4.80 8.20 7.00 BBB 2.80 4.40 7.00 BB

WHC.AX Whitehaven Coal 28/12/2012 DOWN 0.90 3.10 5.30 B 1.60 5.60 5.00 BB

WRT.AX Westfield Retail Trust 10/10/2012 UP 5.10 4.10 7.00 BB 2.00 5.00 7.00 B

WSA.AX Western Areas NL 28/12/2012 UP 4.10 4.40 4.30 BBB 2.60 5.30 3.50 BB

Company NameOverall Rating

revision date

Overall

Rating

Change

Current Prior

Source: MSCI IVA rating, Credit Suisse estimates

■ REITS up: CFX (AA), CQR (BB), GMG (AA), IOF (AAA), WDC (BBB) and WRT (BB),

all have managed an upgrade to their MSCI IVA ratings. REITS now dominate the

MSCI IVA AAA rated stocks (CPA, DXS, GPT, IOF, LLC, SGP). CFX has been

upgraded to AA as its portfolio has one of the lowest energy intensities. CQR was

upgraded to BB due to improvements in the waste management practices. GMG was

upgraded to AA, with industry leading certification of green building standards. An

21 January 2013

Australian ESG/SRI 5

improvement in product quality through improved tenant engagement would lift this

company to AAA rating. IOF was upgraded to AAA with one of the highest level of

green certification and improvements in energy efficiency rating. WDC was upgraded

to BBB on significantly improved service quality (e.g. online real-time resolution of

issues). WRT was upgraded to BB on increased green opportunities (from

refurbishments). We retain our Neutral outlook on all these upgraded REITs.

■ Banks down: ANZ (AA), BOQ (BB), CBA (AA), NAB (A) and WBC (AA), all have

suffered MSCI IVA rating downgrades. No Australian banks are rated AAA, post this

downgrade, with ANZ, CBA and WBC the highest rated at AA. ANZ and WBC, while

acknowledged as leaders in ESG, were downgraded due to a class action on fees. We

have a Positive outlook on the AA rating for WBC, as we believe the issue of the class

action of fees is not material. ANZ and NAB also have concerns about the dominance

of residential mortgage lending with concerns on mortgage stress. We now have a

Neutral outlook on ANZ’s MSCI IVA rating, post the downgrade. CBA’s downgrade to

AA also mentioned the litigation around the collapse of Storm Financial, and we retain

our Neutral outlook on this rating. We have a Negative outlook on the A rating for

NAB, as we factor in shareholder class action on CDOs. BOQ was downgraded to a

quite low BB, on concerns of a lack of an environmental financing strategy,

involvement in the litigation around fees and the collapse of Storm Financial. We move

to a Neutral outlook on this rating, down from our Positive view of BOQ’s

environmental credentials, which are overshadowed by litigation issues.

■ Resource companies mixed bag: AWC (A), BHP (A), RIO (BB), WHC (B), all have

suffered downgrades in their MSCI IVA ratings. BTU (B), GBG (BB), MGX (BB), OZL

(BBB), PNA (A) and WSA (BBB), all have managed an upgrade in their MSCI IVA rating.

■ WPL, ORG and PAN are top rated resource companies: Resource companies that

still have an MSCI IVA rating in the A zone include BHP (A), CTX (A), GRY (A), ORG

(AA), PNA (A), PAN (AA), STO (A) and WPL (AA)

■ BHP down to AA on industrial unrest concerns: For BHP, despite industry’s

leading practices for health and safety, concerns around industrial unrest has seen a

downgrade in BHP’s MSCI IVA rating from AA to A. We move to a Neutral outlook

(from Negative) on the MSCI IVA rating.

■ RIO at risk with BB rating: RIO has had its MSCI IVA rating downgraded from BBB

to BB. Despite a top rating for Corporate Governance, RIO’s rating suffers from its

growth in countries with political risks or areas or significant environmental concerns

and community opposition. RIO also scores lowly on labour management compared to

peers, due to layoffs and a view that there is a combative stance at some of its

operations. With many of its peers rated at A (including BHP), a rating of BB risks RIO

being excluded from some investors’ universe. Or conversely, it risks other BB or less

MSCI IVA rated companies being squeezed out from some investors consideration. In

Figure 5, we list all resource and energy companies (by market cap) in our coverage

universe that have a BB or less MSCI IVA rating (including NCM and OSH).

■ Comparison of BHP and RIO: We have also graphed the relative ratings by MSCI

IVA for BHP and RIO (refer Figure 6). Despite its high Governance score relative to

BHP, it lags behind BHP and the sector average especially on labour management,

toxic emissions and waste and biodiversity/land use. RIO still uses riverine tailings

disposal methods compared to BHP which has stated its opposition to controversial

tailings disposal methods (riverine and deep sea).

■ AWC down to A on emissions concerns: AWC’s MSCI IVA rating was downgraded

from AA to A, as it faces rates low compared to peers on its emissions with average

four year emissions cited at six times the average of peers. Its decision to sign an

energy off-take agreement with MGK’s brown coal Loy Yang generator until 2036 for

21 January 2013

Australian ESG/SRI 6

its Portland and Point Henry refineries is cited as a concern in its quest to reduce its

overall emissions. We note that Victoria, where these operas are based, is dominated

by brown coal generation. For AWC, we move to a Neutral outlook (from Negative) on

the MSCI IVA rating, post the downgrade.

Figure 5: Other BB and below MSCI IVA resource and energy stocks

Ticker Company name Actual

share

price ($)

Target

Price

($)

Rating MSCI

ESG

Rating

View on

MSCI

rating

Market

cap

RIO.AX Rio Tinto 66.45 75.00 OUTPERFORM BB Neutral 108,850

NCM.AX Newcrest Mining 23.25 30.00 OUTPERFORM BB Neutral 17,807

OSH.AX Oil Search 7.14 8.00 NEUTRAL BB Neutral 10,017

AUT.AX Aurora Oil & Gas 3.43 4.10 OUTPERFORM B Positive 1,615

AGO.AX Atlas Iron 1.54 RESTRICTED B 1,401

SFR.AX Sandfire Resources NL 8.47 8.00 UNDERPERFORM B Positive 1,300

AQA.AX Aquila Resources 3.15 2.75 NEUTRAL B Positive 1,297

KAR.AX Karoon Gas 5.49 7.65 OUTPERFORM B Positive 1,216

EVN.AX Evolution Mining Limited 1.615 1.85 NEUTRAL B Positive 1,144

IGO.AX Independence Group NL 4.48 5.20 NEUTRAL BB Neutral 1,043

PRU.AX Perseus Mining 1.955 3.20 OUTPERFORM B Positive 895

MGX.AX Mount Gibson Iron 0.82 0.90 OUTPERFORM BB Neutral 894

ERA.AX Energy Resources of Australia 1.34 1.65 NEUTRAL BB Negative 694

MBN.AX Mirabela Nickel 0.55 0.65 NEUTRAL BB Neutral 507

GBG.AX Gindalbie Metals Ltd 0.295 0.37 NEUTRAL BB Neutral 414 Source: MSCI IVA ratings, Company data, Credit Suisse estimates

Figure 6: BHP versus RIO MSCI IVA ratings

0 2 4 6 8 10

Carbon emissions

Biodiversity & land use

Toxic emissions and waste

Labour management

Health & safety

Corruption and instability

Corporate Governance

Average

RIO

BHP

Source: MSCI IVA

■ WHC downgraded on emissions, social and labour concerns: WHC was

downgraded from BB to B, on combined concerns of emissions, social impact of its

mining operations and industrial unrest. Its NSW operations are believed to have

fugitive emissions three times the level of Queensland operations. We retain our

Neutral outlook on WHC’s MSCI IVA rating.

■ Some safety improvements drive Resource upgrades: BTU has been upgraded to B

(from the lowest CCC rating) as it shows commitment to mitigating some of the concerns

of its Buller Coal development in New Zealand. GBG has been upgraded to BB as it

improved its safety record (almost halved its LTIR to 0.66 in 2012). For BTU and GBG,

we move to a Neutral outlook (from Positive) on the MSCI IVA rating. Post the upgrade,

21 January 2013

Australian ESG/SRI 7

MGX was upgraded to BB (from B) on improved environmental systems that are

consistent across its sites. OZL was upgraded to BBB on its improved health and safety

with a substantial drop in LTIR (down to 1.5 in 2011 from 4.38 in 2010), but concerns

remain on a spike in recordable safety incidents (18.24 in 2011 from 12.36 in 2009).

PNA was upgraded to A (from BBB) with improvements in its health and safety as well

as improved processes for toxic waste and emissions (95% water recycling in 2011).

WSA was upgraded to BBB from BB, on improved health and safety (LTIR down to 1.5

from 4.2) and an improved management plan for threatened species and waste.

■ IVC takes a AAA rating: IVC has been upgraded from A to AAA, but we caution there

are only five peers in the comparison set. This could see a fall in the rating if more peers

are added or if any peer shows a marked improvement, given the relativity across peer

group system used by MSCVI IVA. However we retain our AAA rating on IVC.

■ GNC upgraded to BB: Graincorp was recently upgraded to a 'BB' rating from 'B'

following the initiation of programs to improve energy consumption efficiency.

According to MSCI IVA, GNC's rating is being dragged by relatively weak carbon

emission and water stress programmes. However, these are offset by a strong

presence of operations in developed economies reducing its exposure to poor labour

standard risks. We are currently Restricted on GNC.

■ APA, ENV down on environmental concerns: APA has been downgraded to A,

based on lack of evidence of emissions reduction strategies (as costs are passed

through) and below average safety performance (LTIR rate twice the industry

average). ENV has been downgraded to BB (from BBB) due to concerns on a lack of

environmental management and carbon emission reduction plans. We believe

improved disclosure at ENV should lift this rating. In the meantime, we retain our

Neutral outlook for the MSCI IVA ratings for both these stocks.

■ COH, CSL down: COH has been downgraded to BB from BBB with on-going concerns

about the transparency of its payments to doctors. CSL has been downgraded two

notches to BBB (from AA), based on concerns about product quality with a recent Class

1 recall. We believe that CSL can reverse this rating downgrade, but in the meantime,

we retain our Neutral outlook on the MSCI IVA ratings for both these stocks.

■ NVT upgraded to BBB: NVT has been upgraded to BBB (from BB) with a view that it

has relatively strong human capital and customer service processes. Post this

upgrade, we move our outlook to Neutral (from Positive).

■ FLT downgraded to B: FLT has been downgraded to B on concerns that it does not

have energy efficiency and water conservation programs in place. We believe this is

harsh given the type of operation that FLT is, with MSCI IVA comparing FLT’s retail

operations against hotels that have a far greater exposure to energy and water use.

We retain our Positive outlook on the MSCI IVA rating.

■ Summary of analyst MSCI rating outlook comments: In Figure 7, we detail the

analysts’ comment on the latest MSCI rating for recent MSCI IVA rating changes.

21 January 2013

Australian ESG/SRI 8

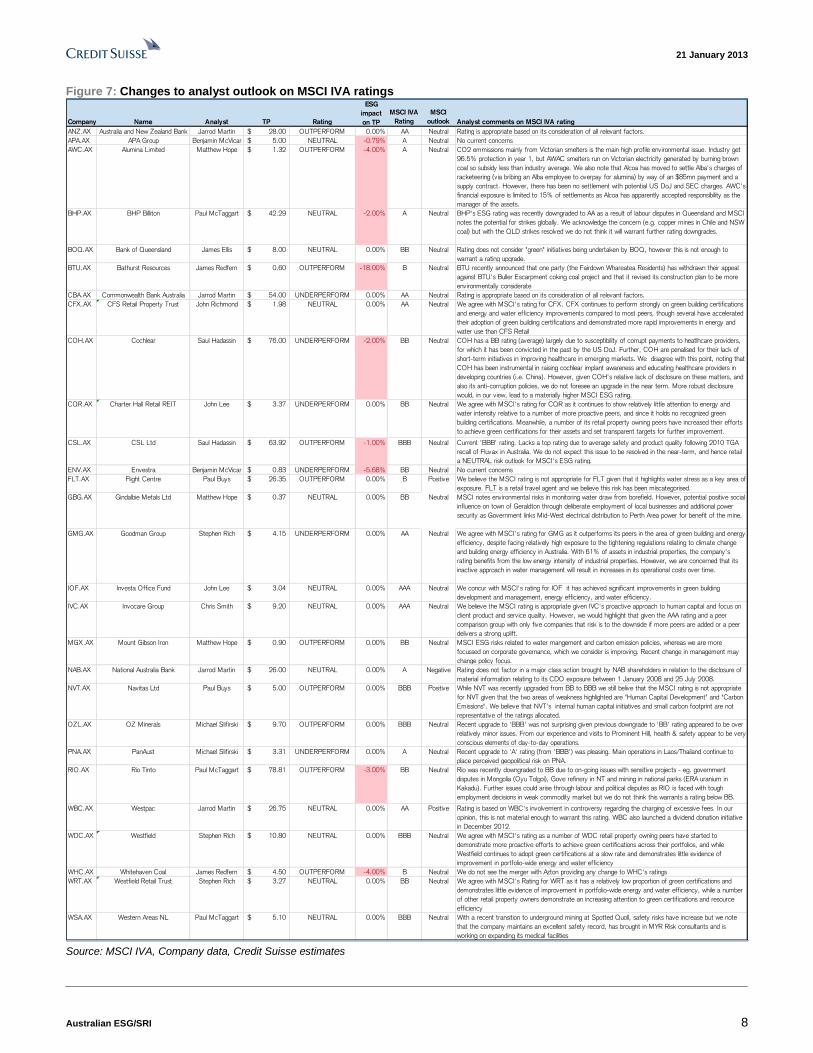

Figure 7: Changes to analyst outlook on MSCI IVA ratings

Company Name Analyst TP Rating

ESG

impact

on TP

MSCI IVA

Rating

MSCI

outlook Analyst comments on MSCI IVA rating

ANZ.AX Australia and New Zealand Bank Jarrod Martin 28.00$ OUTPERFORM 0.00% AA Neutral Rating is appropriate based on its consideration of all relevant factors.

APA.AX APA Group Benjamin McVicar 5.00$ NEUTRAL -0.79% A Neutral No current concerns

AWC.AX Alumina Limited Matthew Hope 1.32$ OUTPERFORM -4.00% A Neutral CO2 emmissions mainly from Victorian smelters is the main high profile environmental issue. Industry get

96.5% protection in year 1, but AWAC smelters run on Victorian electricity generated by burning brown

coal so subsidy less than industry average. We also note that Alcoa has moved to settle Alba's charges of

racketeering (via bribing an Alba employee to overpay for alumina) by way of an $85mn payment and a

supply contract. However, there has been no settlement with potential US DoJ and SEC charges. AWC's

financial exposure is limited to 15% of settlements as Alcoa has apparently accepted responsibility as the

manager of the assets.

BHP.AX BHP Billiton Paul McTaggart 42.29$ NEUTRAL -2.00% A Neutral BHP's ESG rating was recently downgraded to AA as a result of labour disputes in Queensland and MSCI

notes the potential for strikes globally. We acknowledge the concern (e.g. copper mines in Chile and NSW

coal) but with the QLD strikes resolved we do not think it will warrant further rating downgrades.

BOQ.AX Bank of Queensland James Ellis 8.00$ NEUTRAL 0.00% BB Neutral Rating does not consider "green" initiatives being undertaken by BOQ, however this is not enough to

warrant a rating upgrade.

BTU.AX Bathurst Resources James Redfern 0.60$ OUTPERFORM -18.00% B Neutral BTU recently announced that one party (the Fairdown Whareatea Residents) has withdrawn their appeal

against BTU's Buller Escarpment coking coal project and that it revised its construction plan to be more

environmentally considerate

CBA.AX Commonwealth Bank Australia Jarrod Martin 54.00$ UNDERPERFORM 0.00% AA Neutral Rating is appropriate based on its consideration of all relevant factors.

CFX.AX CFS Retail Property Trust John Richmond 1.98$ NEUTRAL 0.00% AA Neutral We agree with MSCI's rating for CFX. CFX continues to perform strongly on green building certifications

and energy and water efficiency improvements compared to most peers, though several have accelerated

their adoption of green building certifications and demonstrated more rapid improvements in energy and

water use than CFS Retail

COH.AX Cochlear Saul Hadassin 76.00$ UNDERPERFORM -2.00% BB Neutral COH has a BB rating (average) largely due to susceptibility of corrupt payments to heatlhcare providers,

for which it has been convicted in the past by the US DoJ. Further, COH are penalised for their lack of

short-term initiatives in improving healthcare in emerging markets. We disagree with this point, noting that

COH has been instrumental in raising cochlear implant awareness and educating healthcare providers in

developing countries (i.e. China). However, given COH's relative lack of disclosure on these matters, and

also its anti-corruption policies, we do not foresee an upgrade in the near term. More robust disclosure

would, in our view, lead to a materially higher MSCI ESG rating.

CQR.AX Charter Hall Retail REIT John Lee 3.37$ UNDERPERFORM 0.00% BB Neutral We agree with MSCI's rating for CQR as it continues to show relatively little attention to energy and

water intensity relative to a number of more proactive peers, and since it holds no recognized green

building certifications. Meanwhile, a number of its retail property owning peers have increased their efforts

to achieve green certifications for their assets and set transparent targets for further improvement.

CSL.AX CSL Ltd Saul Hadassin 63.92$ OUTPERFORM -1.00% BBB Neutral Current 'BBB' rating. Lacks a top rating due to average safety and product quality following 2010 TGA

recall of Fluvax in Australia. We do not expect this issue to be resolved in the near-term, and hence retail

a NEUTRAL risk outlook for MSCI's ESG rating.

ENV.AX Envestra Benjamin McVicar 0.83$ UNDERPERFORM -5.68% BB Neutral No current concerns

FLT.AX Flight Centre Paul Buys 26.35$ OUTPERFORM 0.00% B Positive We believe the MSCI rating is not appropriate for FLT given that it highlights water stress as a key area of

exposure. FLT is a retail travel agent and we believe this risk has been miscategorised.

GBG.AX Gindalbie Metals Ltd Matthew Hope 0.37$ NEUTRAL 0.00% BB Neutral MSCI notes environmental risks in monitoring water draw from borefield. However, potential positive social

influence on town of Geraldton through deliberate employment of local businesses and additional power

security as Government links Mid-West electrical distribution to Perth Area power for benefit of the mine.

GMG.AX Goodman Group Stephen Rich 4.15$ UNDERPERFORM 0.00% AA Neutral We agree with MSCI's rating for GMG as it outperforms its peers in the area of green building and energy

efficiency, despite facing relatively high exposure to the tightening regulations relating to climate change

and building energy efficiency in Australia. With 61% of assets in industrial properties, the company's

rating benefits from the low energy intensity of industrial properties. However, we are concerned that its

inactive approach in water management will result in increases in its operational costs over time.

IOF.AX Investa Office Fund John Lee 3.04$ NEUTRAL 0.00% AAA Neutral We concur with MSCI's rating for IOF it has achieved significant improvements in green building

development and management, energy efficiency, and water efficiency.

IVC.AX Invocare Group Chris Smith 9.20$ NEUTRAL 0.00% AAA Neutral We believe the MSCI rating is appropriate given IVC's proactive approach to human capital and focus on

client product and service quality. However, we would highlight that given the AAA rating and a peer

comparison group with only five companies that risk is to the downside if more peers are added or a peer

delivers a strong uplift.

MGX.AX Mount Gibson Iron Matthew Hope 0.90$ OUTPERFORM 0.00% BB Neutral MSCI ESG risks related to water mangement and carbon emission policies, whereas we are more

focussed on corporate governance, which we consider is improving. Recent change in management may

change policy focus.

NAB.AX National Australia Bank Jarrod Martin 26.00$ NEUTRAL 0.00% A Negative Rating does not factor in a major class action brought by NAB shareholders in relation to the disclosure of

material information relating to its CDO exposure between 1 January 2008 and 25 July 2008.

NVT.AX Navitas Ltd Paul Buys 5.00$ OUTPERFORM 0.00% BBB Positive While NVT was recently upgraded from BB to BBB we still belive that the MSCI rating is not appropriate

for NVT given that the two areas of weakness highlighted are "Human Capital Development" and "Carbon

Emissions". We believe that NVT's internal human capital initiatives and small carbon footprint are not

representative of the ratings allocated.

OZL.AX OZ Minerals Michael Slifirski 9.70$ OUTPERFORM 0.00% BBB Neutral Recent upgrade to 'BBB' was not surprising given previous downgrade to 'BB' rating appeared to be over

relatively minor issues. From our experience and visits to Prominent Hill, health & safety appear to be very

conscious elements of day-to-day operations.

PNA.AX PanAust Michael Slifirski 3.31$ UNDERPERFORM 0.00% A Neutral Recent upgrade to 'A' rating (from 'BBB') was pleasing. Main operations in Laos/Thailand continue to

place perceived geopolitical risk on PNA.

RIO.AX Rio Tinto Paul McTaggart 78.81$ OUTPERFORM -3.00% BB Neutral Rio was recently downgraded to BB due to on-going issues with sensitive projects - eg. government

disputes in Mongolia (Oyu Tolgoi), Gove refinery in NT and mining in national parks (ERA uranium in

Kakadu). Further issues could arise through labour and political disputes as RIO is faced with tough

employment decisions in weak commodity market but we do not think this warrants a rating below BB.

WBC.AX Westpac Jarrod Martin 26.75$ NEUTRAL 0.00% AA Positive Rating is based on WBC's involvement in controversy regarding the charging of excessive fees. In our

opinion, this is not material enough to warrant this rating. WBC also launched a dividend donation initiative

in December 2012.

WDC.AX Westfield Stephen Rich 10.80$ NEUTRAL 0.00% BBB Neutral We agree with MSCI's rating as a number of WDC retail property owning peers have started to

demonstrate more proactive efforts to achieve green certifications across their portfolios, and while

Westfield continues to adopt green certifications at a slow rate and demonstrates little evidence of

improvement in portfolio-wide energy and water efficiency

WHC.AX Whitehaven Coal James Redfern 4.50$ OUTPERFORM -4.00% B Neutral We do not see the merger with Azton providing any change to WHC's ratings

WRT.AX Westfield Retail Trust Stephen Rich 3.27$ NEUTRAL 0.00% BB Neutral We agree with MSCI's Rating for WRT as it has a relatively low proportion of green certifications and

demonstrates little evidence of improvement in portfolio-wide energy and water efficiency, while a number

of other retail property owners demonstrate an increasing attention to green certifications and resource

efficiency

WSA.AX Western Areas NL Paul McTaggart 5.10$ NEUTRAL 0.00% BBB Neutral With a recent transition to underground mining at Spotted Quoll, safety risks have increase but we note

that the company maintains an excellent safety record, has brought in MYR Risk consultants and is

working on expanding its medical facilities Source: MSCI IVA, Company data, Credit Suisse estimates

21 January 2013

Australian ESG/SRI 9

Key stock calls with an ESG overlay

Figure 8: ESG overlay on key stock calls Ticker Company name Actual

share

price ($)

Target

Price

($)

Rating MSCI

ESG

Rating

View on

MSCI

rating

Market

cap

($mn) Key call criteria

AUT.AX Aurora Oil & Gas 3.43 4.10 OUTPERFORM B Positive 1,615 Quant call on quality plus Positive MSCI IVA outlook

BXB.AX Brambles Limited 7.80 7.90 OUTPERFORM AAA Neutral 12,762 AAA rated (MSCI IVA) and Strategy sector and Quant call

CRZ.AX carsales.com.au 8.66 8.80 OUTPERFORM B Positive 2,042 Positive MSCI IVA rating outlook plus Analyst key Long call

FLT.AX Flight Centre 28.27 26.35 OUTPERFORM B Positive 2,832 HOLT Best in Class plus positive MSCI IVA outlook

ILU.AX Iluka Resources 9.70 11.00 OUTPERFORM BBB Positive 4,061 Quant call on quality plus Positive MSCI IVA outlook

MMS.AX McMillan Shakespeare 13.60 14.85 OUTPERFORM B Positive 1,014 Analyst Long call /HOLT Best in Class plus positive MSCI IVA outlook

PRU.AX Perseus Mining 1.96 3.20 OUTPERFORM B Positive 895 Quant call on quality plus Positive MSCI IVA outlook

TAH.AX Tabcorp Holdings 3.04 3.30 OUTPERFORM AAA Neutral 2,231 AAA rated (MSCI IVA), Quant and Analyst key Long call

EGP.AX Echo Entertainment 3.55 3.30 UNDERPERFORM BB Neutral 2,931 Low MSCI IVA Rating plus low Quant quality

TWE.AX Treasury Wine 4.73 3.50 UNDERPERFORM B Neutral 3,061 Low MSCI IVA Rating plus Analyst key Short call (paired with TAH) Source: MSCI IVA ratings, Company data, Credit Suisse estimates

■ ESG overlay on key stocks call: At Credit Suisse Australia, we have taken key calls

from our sector analysts, strategy team, quant team and HOLT Best in Class stocks

and overlaid those with our ESG views of AAA rated (MSCI IVA) or analysts’ Positive

outlook on the MSCI IVA rating:

o Our analysts long/short key stock calls: Best ideas from sector analysts.

o Our Quant call on quality stocks (earnings certainty and ROE)

o Our Strategy call on Global Industrials, A-REITS, Utilities and

Infrastructure.

o Our HOLT® Best in Class (refer to appendix for a further details).

■ Key calls: In Figure 8, we have listed our key stocks calls. Our key long calls are

BXB (strategy), CRZ, MMS (also HOLT), TAH, (sector analysts), AUT, ILU, PRU

(quant) and FLT, HGG (HOLT Best in Class). Our key short calls are TWE (sector

analyst) and EGP (Quant). The 12-month underperformance is impacted by significant

underperformance of UILU and PRU. Equally, three year outperformance has been

positively impacted by stellar performance by AUT, ILU, and MMS over that period.

Figure 9: Performance of key ESG stock calls Ticker Company name Actual

share

price ($)

Target

Price

($)

Rating MSCI

ESG

Rating

View on

MSCI

rating

Market

cap

($mn)

1 month total

return

6 months total

return

12 months

total return

3 year

performance

AUT.AX Aurora Oil & Gas 3.43 4.10 OUTPERFORM B Positive 1,615 -5.2% 2.1% 5.2% 971.9%

BXB.AX Brambles Limited 7.80 7.90 OUTPERFORM AAA Neutral 12,762 4.3% 28.5% 10.5% 28.1%

CRZ.AX carsales.com.au 8.66 8.80 OUTPERFORM B Positive 2,042 18.3% 46.0% 82.9% 90.0%

FLT.AX Flight Centre 28.27 26.35 OUTPERFORM B Positive 2,832 7.9% 40.9% 55.9% 60.3%

ILU.AX Iluka Resources 9.70 11.00 OUTPERFORM BBB Positive 4,061 10.2% 16.4% -42.2% 221.8%

MMS.AX McMillan Shakespeare 13.60 14.85 OUTPERFORM B Positive 1,014 0.4% 21.3% 61.4% 280.6%

PRU.AX Perseus Mining 1.96 3.20 OUTPERFORM B Positive 895 -7.3% -10.3% -32.6% 9.2%

TAH.AX Tabcorp Holdings 3.04 3.30 OUTPERFORM AAA Neutral 2,231 1.3% 0.3% 13.9% 13.9%

EGP.AX Echo Entertainment 3.55 3.30 UNDERPERFORM BB Neutral 2,931 3.8% -14.3% 4.9% N/A

TWE.AX Treasury Wine 4.73 3.50 UNDERPERFORM B Neutral 3,061 1.1% 8.4% 35.4% N/A

Market cap weighted average 19,067 4.4% 16.0% 5.1% 82.8%

All ords 3.6% 15.7% 11.6% 0.6% Source: MSCI IVA, Company data, Credit Suisse estimates

■ ESG stock call outperformance of short term: Overall the current key stock calls

with an ESG overlay have outperformed over a one and six month time-frame (refer

Figure 9).

■ Key call of BXB—fits our Global Industrials Strategy call and Quant Quality call:

For BXB, our Strategy team has a preference for Global Industrials over Domestic

Cyclicals and prefers BXB. BXB is AAA rated (MSCI IVA) with an analyst

21 January 2013

Australian ESG/SRI 10

OUTPERFORM call. We continue to believe Brambles is the highest quality name in

the Australian Transport universe. While the business is considered by some to be

expensive, trading at a 30% premium to market on a P/E basis, we believe the growth

prospects and operating characteristics continue to justify such a multiple. The

business is highly leveraged to an FMCG volume and pricing recovery in Western

markets, particularly the US where we are starting to see tentative signs of pricing

increases. In addition, the business continues to expand in emerging markets like

China and EMEA, where we see the growth accelerating. Finally, the business

continues to earn very high margins and returns on capital, helped by reasonably high

barriers to entry and longstanding relationships with customers. With respect to its

ESG credentials, BXB continues to improve its sourcing of sustainable lumbar for its

CHEP business, with 94% of lumber coming from certified sources (up from 91%),

with a target of 100% certified sourcing (independently verified) by 2015. Its CHEP

business is also working on a carbon neutral pallet for customers.

■ TAH is an analyst Long call with an AAA MSCI IVA rating: TAH has the top AAA

MSCI IVA rating. Our analyst has selected it as a key ‘Long’ call based on a

preference for the less risky domestic wagering businesses, with TAH representing

better value than TTS. Wagering revenue growth reached 7% in the June quarter and

variable contribution margin increased sequentially to 36.4% from 36.1%. Customer

growth and market share were solid in FY12. Strong growth in fixed odds, sports bets

and on-line bets which attract lower taxes and fees continue to lift margins. These

trends are likely to continue for a few years. The Victorian license refund claim has

been lodged. The payment could be as high as A$686mn before a partial tax

assessment. This is not in our valuation.

■ CRZ favoured in media: CRZ is well positioned in the digital media space. It is the

dominant player in online auto classifieds. Relative to real estate and employment, car

sales are less volatile, the auto display ad market is larger and there is greater volume

upside from new cars. While its MSCI rating is a low B rating, we see upside on

improved disclosure and therefore have a Positive analyst outlook on the MSCI rating.

■ MMS added to key analyst call and HOLT Best in Class: MMS is a key call from

our Small Cap analysts, as well as screening as a HOLT Best in Class stock. Our

analysts like the high growth profile with an attractive set of earnings drivers and

relatively low correlation to broader economic conditions. We believe these attributes

provide ample support for the stock’s valuation metrics. While MMS scores a low B

rating under the MSCI IVA ratings, our analysts have a Positive outlook on this rating.

The view is that the low Labour Management score of 0.6 does not reflect MMS’

proactive approach to human capital and rigorous internal/external audit and focus on

risk management.

■ FLT screens for HOLT Best in Class: FLT has an OUTPERFORM rating by our

analyst and a Positive outlook on the MSCI IVA B rating. Our analyst considers FLT,

which is a retail travel agent with shop-front operations that have low energy/water

requirements, is being harshly judged on water and energy strategies in a peer group

of large tourist operations. FLT is in a small group of mid-small caps stocks that

have provided FY13 guidance and offers relative earnings certainty. While

domestic leisure travel growth is likely to slow somewhat from previous periods,

FLT stands to benefit from continued growth in the corporate market (40% of Total

Transactional value) through market share gains and strong performance in its US

and UK businesses which are gaining scale. On this basis and considering FLT’s

strong net cash balance sheet, we believe valuation remains attractive.

■ Favour AUT, ILU and PRU for our Quant theme of quality: AUT, ILU and PRU are

stocks we highlight based on our Quant preference for quality stocks (earnings

certainty and ROE). These stocks have a Positive analyst outlook on the MSCI IVA

rating and an Outperform analyst call.

21 January 2013

Australian ESG/SRI 11

o AUT growth in FY13 of ~160%: As AUT ramps up production from its Eagle

Ford shale operations, its EPS growth is expected to be 80-160% over the

coming 12-24 months. We have a Positive view on AUT’s MSCI IVA rating of

B, as improved disclosure on environmental issues should lift the rating.

o ILU growth in FY13 volumes: We see ILU as undervalued, based on

our forecast mineral sands prices, which are lower than spot. Sales

volumes were low in 2012, but should increase in FY13. Operations

remain cash positive and high margin. Despite our recent commodity

price downgrades, ILU remains profitable because every tonne sold has

+60% EBITDA margin, but sales volumes in 2012 have been low and

erratic. We believe destocking of zircon is complete, and sales will

increase. Sales of titanium dioxide feedstock should also increase,

although pricing will contract to compete for market share.

o PRU growth in FY13: PRU is our favoured pick among junior gold

exposures. It is leveraged to gold price, Tengrela approval and primarily

Edikan ramp-up to 8Mtpa. If Edikan reaches the guided to 8Mtpa by mid-

2013, the current share price is supported by Edikan NPV alone. Edikan

mine review is a key datapoint in de-risking production and earnings profile.

■ TWE—short call and a low MSCI IVA rating: Our Analyst has a key ‘Short’ call on

TWE (paired with a Long call on TAH) combined with a weak B ESG rating under the

MSCI IVA system. We continue to regard the stock as expensive relative to the

market, intrinsic value, and its peers. 2H12 overheads were much lower than modelled

and we question if such a low level of costs can be maintained in North America and

Asia. TWE is trading on around 22x and 17x FY13E and FY14E P/E, respectively. For

FY13, management expects constant currency EBIT to grow less than the historical

two-year CAGR (16%) due to rising IT costs, rising grape costs and distributor de-

stocking. For FY14E, management expects above trend growth. Optimistically, we

assume that the 20% increase in inventory value is a 20% increase in inventory

volume despite rising grape prices. Assume all high end wine can be sold and this

drives a 100 bp improvement in gross margin.

EGP—low MSCI IVA rating and low Quant screening on quality: Our analyst

has an UNDERPERFORM rating on EGP. The value of EGP’s Sydney asset,

Star, is a function of its monopolistic license position in NSW. If Crown is

successful in securing a second casino license for Barangaroo, it will emerge as a

competitor to Star post the end of its NSW license exclusivity in 2019. EGP will

end up sharing the Sydney VIP market with Crown, This could imply downside

risks to our current longer term VIP forecasts for Star. There may be no value left

in EGP’s Queensland casino portfolio. It appears EGP may spend about $1.25bn

in capex (double the original Project Icon) to refurbish its QLD casinos. Funding

remain a concern. EGP will either need to raise equity or seek a partner to

execute this project: FY14–FY18 development horizon. We value EGP at our core

DCF-based target price of A$3.30, equating to about 7.9x FY14 EV/EBITDA.

CWN’s domestic casinos are trading on 8.7x FY14 EV/EBITDA. With the

uncertainty around QLD and CWN’s inside running on a new Sydney casino

licence, the takeover premium built into EGP has deflated.

21 January 2013

Australian ESG/SRI 12

Appendix Links to recent ESG research:

■ Australian ESG/SRI - ESG in the Media Sector: Our views on ESG issues in the

Media sector in Australia – 27 November

■ ESG changes in stocks calls and analyst views: An update on key ESG stock

calls, MSCI IVA rating changes and ESG Target Price impact changes – 24 October

2012.

■ “ESG overlay on key stock calls”: Our view on the analysts’ outlook for MSCI IVA

ratings on 27 September 2012..

■ “$21.4bn in ESG concerns on Australian stocks”: Our first view of the impact on

analysts’ Target Prices - 2 July 2012.

21 January 2013

Australian ESG/SRI 13

MSCI IVA ratings

■ MSCI IVA identifies and analyses key ESG issues by looking at the risks inherent in

each sector. Through an in-depth comparison against sector peers, MSCI generates

‘best-in-class’ company risk ratings and reveals ESG-driven investment risks or

opportunities that may not be captured by conventional analysis. To get a full picture

of corporate ESG practices, MSCI researches a wide and extensive range of ESG

data points, and then applies a three-phased analysis methodology. The first step is to

identify the key issues for each industry. Step 2 is to evaluate the stock’s risk exposure

and risk management. Lastly, they rate each company against its global sector peers.

■ Figure 10 shows the breakdown into 31 separate features, all of which aggregate to

give an overall score, on an ‘AAA’ to ‘CCC’ scale relative to the performance of

industry peers. It should be noted that MSCI sector-adjust their ratings by applying a

weighting on certain factors for some sectors they deem them relevant to and others

they do not. For example, Carbon Emissions may make up an important part of the

environmental characteristics for an energy company but would be almost entirely

irrelevant when looked at from a telecom company’s standpoint. In this way, all

constituents may be compared relatively against each other, in a sector-neutral

manner.

Figure 10: ESG factors—relevance by sector

Enviro

nm

enta

l key

issu

es

Car

bon E

mis

sions

Upsr

eam

Car

bon E

mis

sions

Energ

y E

ffic

iency

Insu

ring C

limat

e C

han

ge R

isk

Wat

er

Str

ess

Bio

divers

ity a

nd L

and U

se

Raw

Mat

eria

l Sourc

ing

Fin

anci

al E

nviro

nm

enta

l Im

pac

ts

Toxi

c R

ele

ases

Pac

kagin

g M

ateria

ls &

Was

te

E-W

aste

Opport

uniti

es

in E

nv.

Tech

nolo

gie

s

Opport

uniti

es

in G

reen B

uild

ing

Opport

uniti

es

in R

enew

able

Energ

y

Soci

al k

ey

issu

es

Lab

or

- O

pera

tional

Heal

th &

Saf

ety

Lab

or

- S

upply

Chai

n

Raw

Mat

eria

l Sourc

ing -

Soci

al

Pro

duct

and S

erv

ices

Qual

ity

Pro

duct

Saf

ety

- C

hem

ical

s

Pro

duct

Saf

ety

- F

inan

cial

Priv

acy

& D

ata

Secu

rity

Resp

onsi

ble

Inve

stin

g

Insu

ring H

eal

th a

nd D

em

ogra

phic

Ris

k

Opport

uniti

es

in N

utr

ition a

nd H

eal

th

Acc

ess

to C

om

munic

atio

ns

Acc

ess

to F

inan

ce

Acc

ess

to H

eal

thca

re

Gove

rnan

ce-r

ela

ted k

ey

issu

es

Corr

uptio

n a

nd Inst

abilit

y

Fin

anci

al S

yste

m Inst

abilit

y

Corp

ora

te G

ove

rnan

ce

Energy X X X X X X X X

Materials X X X X X X X X X X X X X

Industrials X X X X X X X X X

Consumer X X X X X X X X X X X X X X X X X X X

Health Care X X X X X X

Financials X X X X X X X X X X X X X X X

Technology X X X X X X X X X X X X

Telecoms X X X X X

Utilities X X X X X Source: MSCI ESG Research

21 January 2013

Australian ESG/SRI 14

Explanation of HOLT® methodology

■ HOLT CFROI: HOLT is an advanced corporate performance, valuation and strategic

analysis framework for the benefit of Credit Suisse and its clients. Corporate

performance is calculated in terms of our CFROI® metric. This provides a unique

perspective on valuation issues that result from strategic decisions driven by corporate

management. We believe the HOLT methodology helps identify valuation insights

about a company quickly and easily, saving time and wasted effort, in our view.

■ HOLT’s default model initially uses consensus estimates to drive CFROI

forecasts, before proprietary algorithms determine the “rate of fade” towards the long

run average (the rate of this fade is a function of the level and volatility of returns and

the rate of growth).

■ Simply stated, we take accounting information, convert it to cash, and then

value that cash. This brings valuation back to basics at a time when differing / revised

accounting practices are moving further away from commercial realities. From our

perspective, a company’s ability to deliver strong, sustainable and preferably

increasing free cash flows is what matters. It is sustainable free cash that ultimately

should drive the share price, longer term. Our approach takes away all the accounting

anomalies and those so-called (and seemingly consistent) one-offs where

accountability is not taken by many.

■ HOLT stock rankings: To do so, we leverage Credit Suisse’s proprietary cash flow return

on investment (CFROI) valuation framework HOLT. We establish a ranking system to

select stocks according to factors of the value creation of its operations, its forecast and

price momentum and its overall valuation according to the HOLT framework.

■ Best in class stocks: The HOLT scorecard is used across wide range of other areas

of our research. However, here we use it to focus in on the more highly rated stocks in

the IVA framework to see if we can enhance performance with an overlay of the

scorecard. We have focused on all stocks rated A and above in MSCI World to ensure

we have a sufficiently broad universe to then select stocks that are ranked in the top

two quintiles across the universe in each of the three factors—operations, momentum

and valuation. These represent the stocks we term “Best in class”.

21 January 2013

Australian ESG/SRI 15

Figure 11: Current HOLT Australian Best in Class/Worse in Class stocks

ID Company Score Operations Momentum Valuation

HOLTfolio

Theme

BEST IN CLASS

BPT BEACH ENERGY LIMITED 4.00 3.60 3.87 4.54 Best in Class

FLT FLIGHT CENTRE LIMITED 4.18 4.39 4.09 4.05 Best in Class

FMG FORTESCUE METALS GROUP LIMITED 3.88 4.44 3.66 3.54 Best in Class

MMS MCMILLAN SHAKESPEARE LTD 4.28 4.85 4.18 3.82 Best in Class

MND MONADELPHOUS GROUP LIMITED 4.34 4.98 4.14 3.89 Best in Class

RMD RESMED INC 4.04 3.72 4.66 3.75 Best in Class

RSG RESOLUTE MINING LIMITED 4.24 4.71 3.44 4.57 Best in Class

SUN SUNCORP GROUP LIMITED 3.78 3.54 4.08 3.73 Best in Class

SUL SUPER RETAIL GROUP LIMITED 3.74 3.52 4.40 3.32 Best in Class

WORST IN CLASS

AWC ALUMINA LIMITED 1.97 1.61 2.56 1.76 Worst in Class

AHD AMALGAMATED HOLDINGS LIMITED 2.10 1.44 2.62 2.24 Worst in Class

AQA AQUILA RESOURCES LIMITED 1.58 1.00 2.39 1.36 Worst in Class

BLD BORAL LIMITED 2.21 1.64 2.67 2.31 Worst in Class

KAR KAROON GAS AUSTRALIA LIMITED 1.47 1.42 1.77 1.22 Worst in Class

LYC LYNAS CORPORATION LIMITED 1.16 1.03 1.03 1.42 Worst in Class

MSB MESOBLAST LTD 1.56 1.07 2.12 1.51 Worst in Class

QAN QANTAS AIRWAYS LIMITED 1.90 1.38 2.39 1.92 Worst in Class

QBE QBE INSURANCE GROUP LIMITED 1.93 1.48 1.65 2.66 Worst in Class

SDL SUNDANCE RESOURCES LIMITED 1.57 1.00 2.59 1.12 Worst in Class

WHC WHITEHAVEN COAL LIMITED 1.60 1.07 1.28 2.46 Worst in Class Source: Company data, Credit Suisse estimates

■ HOLT contacts: For further information on this report or for other HOLT related

matters, please contact:

Scott Chessum

+613 9280 1662

Peter Jabour

+613 9280 1702

21 January 2013

Australian ESG/SRI 16

■ ESG views embedded in our research: We include our analyst’s view on the impact

of ESG issues on their target price, plus an outlook on the MSCI IVA rating for their

stocks (refer example in Figure 12).

Figure 12: Example of ESG disclosure in Financial Summary for Industrial companies

AGL Energy (AGK) Year ending 30 Jun In AUDmn, unless otherwise stated2011 2012 2013 2014 2015 2011 2012 2013 2014 2015

Share Price: A$15.63 Earnings 06/11A 06/12A 06/13E 06/14E 06/15ERating NEUTRAL c_EPS_SHARESEquiv. FPO (period avg.) mn 456.9 482.3 549.0 555.9 563.3

Target Price A$ 16.10 c_EPS*100EPS (Normalised) c 94.4 99.9 112.5 126.5 141.4

vs Share price % 3.01 EPS_GROWTH*100EPS Growth % 5.9 12.6 12.4 11.8

c_EBITDA_MARGIN*100EBITDA Margin % 11.4 12.1 14.3 14.6 15.1

c_DPS*100DPS c 60.0 61.0 64.0 64.0 65.6

c_PAYOUT*100Payout % 63.6 61.0 56.9 50.6 46.4

FRANKING*100Franking % 51.7 100.0 100.0 100.0 100.0

c_FCF_PS*100Free CFPS c 105.1 76.0 131.9 163.3 166.0

Profit & Loss 06/11A 06/12A 06/13E 06/14E 06/15E c_TAX_RATE*100Effective tax rate % 30.4 29.0 29.0 29.0 29.0

Sales revenue 7,072.5 7,455.6 10,025.2 10,808.8 11,401.8 Valuation

EBITDA 804.5 904.3 1,436.0 1,575.4 1,723.2 c_PE P/E x 16.6 15.6 13.9 12.4 11.1

Depr. & Amort. (148.0) (173.9) (328.6) (361.9) (385.8) c_EBIT_MULTIPLE_CURREV/EBIT x 13.7 15.2 9.8 8.6 7.4

EBIT 656.5 730.4 1,107.5 1,213.5 1,337.4 c_EBITDA_MULTIPLE_CUEV/EBITDA x 11.2 12.3 7.6 6.6 5.8

Associates 0.0 0.0 0.0 0.0 0.0 c_DIV_YIELD*100Dividend Yield % 3.8 3.9 4.1 4.1 4.2

Net interest Exp. (37.4) (51.2) (236.9) (223.0) (215.0) c_FCF_YIELD*100FCF Yield % 6.7 4.9 8.4 10.4 10.6

Other 0.0 0.0 0.0 0.0 0.0 c_PB Price to Book x 1.1 1.2 1.1 1.1 1.0

Profit before tax 619.1 679.2 870.6 990.6 1,122.3 ReturnsIncome tax (188.0) (197.2) (252.8) (287.6) (325.9) c_ROE*100Return on Equity % 6.8 6.8 8.2 8.8 9.3

Profit after tax 431.1 482.0 617.8 703.0 796.5 c_I_NPAT/c_I_SALES*100Profit Margin % 6.1 6.5 6.2 6.5 7.0

Minorities 0.0 0.0 0.0 0.0 0.0 c_I_SALES/c_B_TOT_ASSAsset Turnover x 0.7 0.5 0.7 0.8 0.8

Preferred dividends 0.0 0.0 0.0 0.0 0.0 c_ASSETS/c_EQ_COMMONEquity Multiplier x 1.5 2.1 1.8 1.8 1.7

Associates & Other 0.0 0.0 0.0 0.0 0.0 c_ROA*100Return on Assets % 4.4 3.3 4.5 4.9 5.4

Normalised NPAT 431.1 482.0 617.8 703.0 796.5 c_ROIC*100Return on Invested Cap. % 6.8 5.4 8.0 8.7 9.6

Unusual item after tax 127.6 (367.1) 0.0 0.0 0.0 Gearing

Reported NPAT 558.7 114.9 617.8 703.0 796.5 c_GEARING*100Net Debt to Net debt + Equity % 6.2 25.9 23.1 18.7 13.6

c_NET_DEBT/c_I_EBITDANet Debt to EBITDA x 0.5 2.8 1.6 1.2 0.8

Balance Sheet 06/11A 06/12A 06/13E 06/14E 06/15E c_I_EBITDA/ c_I_NET_INTERESTInt Cover (EBITDA/Net Int.) x 21.5 17.7 6.1 7.1 8.0

Cash & equivalents 753.1 1,812.9 546.8 969.1 1,462.7 c_I_EBIT/ c_I_NET_INTERESTInt Cover (EBIT/Net Int.) x 17.6 14.3 4.7 5.4 6.2

Inventories 127.4 185.4 192.3 207.3 218.7 (c_C_CAPEX/c_I_SALES)*-100Capex to Sales % 8.0 10.2 4.6 4.2 3.7

Receivables 1,272.1 1,531.4 1,510.6 1,628.7 1,718.1 (c_C_CAPEX/c_I_DEPR)*-100Capex to Depreciation % 380.9 437.3 141.0 125.3 109.3

Other current assets 577.8 602.2 602.2 602.2 602.2

Current assets 2,730.4 4,131.9 2,851.9 3,407.3 4,001.6 MSCI IVA (ESG) Rating A

Property, plant & equip. 3,400.9 6,323.5 6,465.8 6,563.9 6,594.8 TP ESG Risk (%): -7.62

Intangibles 3,137.2 3,172.0 3,172.0 3,172.0 3,172.0

Other non-current assets 427.2 1,111.0 1,111.0 1,111.0 1,111.0

Non-current assets 6,965.3 10,606.5 10,748.8 10,846.9 10,877.8

Total assets 9,695.7 14,738.4 13,600.7 14,254.2 14,879.4

Payables 853.1 1,158.4 1,001.0 1,083.5 1,136.6

Interest bearing debt 1,171.2 4,312.0 2,812.0 2,812.0 2,812.0

Other liabilities 1,329.9 2,135.1 2,238.8 2,347.9 2,367.6 MSCI IVA Risk: Neutral

Total liabilities 3,354.2 7,605.5 6,051.8 6,243.4 6,316.2

Net assets 6,341.5 7,132.9 7,548.9 8,010.8 8,563.3

Ordinary equity 6,341.5 7,132.9 7,548.9 8,010.8 8,563.3

Minority interests 0.0 0.0 0.0 0.0 0.0

Preferred capital 0.0 0.0 0.0 0.0 0.0

Total shareholder funds 6,341.5 7,132.9 7,548.9 8,010.8 8,563.3

Net debt 418.1 2,499.1 2,265.2 1,842.9 1,349.3 Source: MSCI IVA Rating

Cashflow 06/11A 06/12A 06/13E 06/14E 06/15E Share Price Performance

EBIT 656.5 730.4 1,107.5 1,213.5 1,337.4

Net interest -39.3 -98.0 -242.5 -228.1 -219.6

Depr & Amort 148.0 173.9 328.6 361.9 385.8

Tax paid -0.7 -180.8 -149.1 -178.5 -306.1

Working capital -219.5 -185.7 -143.5 -50.6 -47.6

Other 24.3 26.7 0.0 0.0 0.0

Operating cashflow 569.3 466.5 900.9 1,118.2 1,149.7

Capex -563.7 -760.4 -463.2 -453.5 -421.5

Capex - expansionary -474.4 -660.5 -286.5 -243.1 -206.6

Capex - maintenance -89.3 -99.9 -176.7 -210.4 -214.9

Acquisitions & Invest -5.0 143.2 0.0 0.0 0.0

Asset sale proceeds 163.9 217.5 0.0 0.0 0.0

Other -14.5 -131.6 -2.0 -1.4 9.4

Investing cashflow -419.3 -531.3 -465.2 -454.9 -412.1

Dividends paid -206.5 -185.8 -294.2 -351.4 -355.8

Equity raised -6.1 879.4 92.4 110.3 111.7

Net borrowings 335.3 431.0 -1,500.0 0.0 0.0

Other 0.0 0.0 0.0 0.0 0.0 1 Month 3 Month 12 Month

Financing cashflow 122.7 1,124.6 -1,701.8 -241.0 -244.1 Absolute 2.0% 6.3% 10.6%

Total cashflow 272.7 1,059.8 -1,266.1 422.3 493.6 Relative -1.3% 1.2% -2.1%

Adjustments 0.0 0.0 0.0 0.0 0.0

Net change in cash 272.7 1,059.8 -1,266.1 422.3 493.6 Source: Reuters 52 week trading range: 13.15-15.98

MSCI IVA Risk Comment: Post the acquisition of the Loy Yang

brown coal generator, AGK’s MSCI IVA rating has been

downgraded to A. We move out Outlook to neutral from

Negative, as a result.

21/01/2013 17:48

AGL Energy is an Australia-based integrated energy retailer. AGL is an integrated

renewable energy company and is a private owner, operator and developer of renewable

generation assets.

Credit Suisse View

TP Risk Comment: We have excluded the NSW coal seam

gas assets from out Target Price due to ESG concerns on

development. Our TP is also impacted (-90cps) by our ESG

concerns around retail energy prices

12.49

12.99

13.49

13.99

14.49

14.99

15.49

15.99

16.49

16.99

10/01/2012 10/03/2012 10/05/2012 10/07/2012 10/09/2012 10/11/2012 10/01/2013

AGK.AX XJO

4.1

4.6

5.1

5.6

6.1

6.6

7.1

7.6

8.1

8.6

Environment Social Governance

Stock Local Sector

Country Global Sector

Source: Company data, Credit Suisse estimates

21 January 2013

Australian ESG/SRI 17

Common ESG concerns by sector

■ In Figure 13, we have summarised some of our key ESG concerns for each sector in

the Australian equities space. For example, the Finance sector is dominated by Social

issues, whereas the resources sector has issues right across the ESG spectrum.

Figure 13: ESG issues by Sector Sector Subsector Issues

Financials Banks Social: regulatory changes arising from social pressures,

Social: pressure to pass on full reserve Bank rates cut to home borrowers

Diversified Financials Social: key man risk for fund managers

Social: regulatory changes to monopoly/dominant market positions

Social: large scale redundancies

Insurance Social: regulatory changes for capital requirements

Resources Coal Environmental: ability to develop new resources

Energy Social: landowner compensation for coal seam gas

Governance: country specific risk

Diversified resources Social: labour disputes

Governance: country specific risk

Other metals Environmental: ability to develop new resources

Governance: country specific risks

Steel Environmental: impact of carbon tax

Social: layoff of staff and viability of domestic production

Industrials Building materials Social: asbestos liability

Chemicals, paper, packaging Environmental: carbon tax impact

Construction Social: OH&S

Governance: bribery and reputation damage

Food and beverage Environmental: emissions and water usage

Gaming Social: potential responsible gaming legislation and employee initiatives

Healthcare Governance: disclosure and family domination

Media Governance: family domination

Retail Social: labour supply chain concerns

Social: gaming and liquor asset concerns

Telcos Social: privacy of data, upside from improving regulation (NBN)

Transport & infrastructure Environment: fuel efficient of fleet

Social: labour productivity

Utilities Environment: ability to develop coal seam gas in NSW

Social: rising electricity prices; landowner compensation for coal seam gas

REITS Environment: upside potential from strong environmental sustainability

Small caps Building Products Environment: carbon impact

Social: labour rights and OH&S

Governance: anti-bribery

Consumer Retail Environment: waste

Social: labour rights and OH&S

Governance: supply chain labour issues

Consumer Services Social: privacy and data security; labour rights and OH&S

Corporate Services Environment: regulation

Social: labour rights and OH&S

Governance: anti-bribery and corruption

IT Services Social: privacy and data security; labour rights and OH&S

Mining services Environment: policy and management systems

Social: labour rights and OH&S

Governance: anti-bribery

Travel Environment: carbon offsetting

Social: privacy and data security

Governance: contracts and anti-competitive regulations

Source: Company data, Credit Suisse estimates

21 January 2013

Australian ESG/SRI 18

Disclosure

Figure 14: Stock list as at 21 January 2013

Ticker Company name

Actual

share

price

Target

Price ($) Rating

TP

rating

risk %

MSCI IVA

rating

Analyst

outlook

on rating

Date of

MSCI IVA

rating Analyst Email contact Phone

ABC.AX Adelaide Brighton 3.29 3.30 NEUTRAL -3.5% CCC Positive 25/05/2012 Andrew Peros [email protected] 61 2 8205 4013

AGK.AX AGL Energy 15.63 16.10 NEUTRAL -7.6% A Neutral 10/07/2012 Benjamin McVicar [email protected] 61 2 8205 4577

AGO.AX Atlas Iron 1.54 RESTRICTED 0.0% B Negative 28/12/2012 Matthew Hope [email protected] 61 2 8205 4669

AIO.AX Asciano Group 4.77 5.95 OUTPERFORM -3.1% BBB Positive 1/03/2012 Nicholas [email protected] 2 8205 4400

ALL.AX Aristocrat Leisure 3.41 3.50 OUTPERFORM 0.0% A Neutral 1/02/2012 Larry Gandler [email protected] 61 3 9280 1855

ALQ.AX ALS Limited 10.95 8.80 UNDERPERFORM 0.0% A Neutral 14/08/2012 Bradley Clibborn [email protected] 61 2 8205 4465

ALZ.AX Australand 3.39 3.35 NEUTRAL 0.0% BBB Neutral 10/10/2012 John Richmond [email protected] 61 2 82054580

AMC.AX Amcor 8.46 7.70 UNDERPERFORM -3.0% A Neutral 10/09/2012 Larry Gandler [email protected] 61 3 9280 1855

AMP.AX AMP 5.21 4.65 NEUTRAL 0.0% A Neutral 11/04/2012 Andrew Adams [email protected] 61 2 8205 4106

AMX.AX Ampella Mining Limited 0.39 1.50 OUTPERFORM 0.0% Michael Slifirski [email protected] 61 3 9280 1845

ANZ.AX Australia and New Zealand Bank25.69 28.00 OUTPERFORM 0.0% AA Neutral 25/10/2012 Jarrod Martin [email protected] 61 2 8205 4334

AOH.AX Altona Mining Limited 0.25 0.46 OUTPERFORM 0.0% Michael Slifirski [email protected] 61 3 9280 1845

APA.AX APA Group 5.70 5.00 NEUTRAL -0.8% A Neutral 10/10/2012 Benjamin McVicar [email protected] 61 2 8205 4577

API.AX Australian Pharmaceutical Ind 0.47 0.60 OUTPERFORM -5.0% Saul Hadassin [email protected] 61 2 8205 4679

APN.AX APN News & Media 0.32 0.23 UNDERPERFORM -3.0% Negative Samantha Carleton [email protected] 2 8205 4148

AQA.AX Aquila Resources 3.15 2.75 NEUTRAL -5.0% B Positive 28/12/2012 Paul McTaggart [email protected] 61 2 8205 4698

AQG.AX Alacer Gold Corp. 4.51 8.25 OUTPERFORM 0.0% Michael Slifirski [email protected] 61 3 9280 1845

AQZ.AX Alliance Aviation Services Limited1.88 2.30 OUTPERFORM 0.0% Paul Buys [email protected] 61 2 8205 4538

ARI.AX Arrium 0.89 0.95 OUTPERFORM 0.0% BBB Neutral 1/12/2011 Michael Slifirski [email protected] 61 3 9280 1845

ARP.AX ARB Corp 11.61 9.80 NEUTRAL 0.0% BBB Neutral 25/05/2012 Paul Buys [email protected] 61 2 8205 4538

ASX.AX ASX 33.42 28.00 UNDERPERFORM 0.0% BB Neutral 25/10/2012 David Bailey [email protected] 61 2 8205 4739

AUB.AX Austbrokers 8.14 7.95 NEUTRAL 0.0% Andrew Adams [email protected] 61 2 8205 4106

AUT.AX Aurora Oil & Gas 3.43 4.10 OUTPERFORM -3.0% B Positive 29/08/2012 James Redfern [email protected] 61 2 8205 4779

AWC.AX Alumina Limited 1.12 1.25 OUTPERFORM -4.0% A Neutral 28/12/2012 Matthew Hope [email protected] 61 2 8205 4669

AWE.AX AWE Ltd 1.20 1.80 OUTPERFORM -0.4% BBB Negative 25/05/2012 James Redfern [email protected] 61 2 8205 4779

AZJ.AX Aurizon 4.04 3.80 NEUTRAL 0.0% Neutral Bradley Clibborn [email protected] 61 2 8205 4465

BBG.AX Billabong International 1.01 1.10 OUTPERFORM 0.0% A 25/09/2012 Grant Saligari [email protected] 61 3 9280 1720

BEN.AX Bendigo and Adelaide Bank 9.03 8.75 NEUTRAL 0.0% BBB Positive 25/10/2012 James Ellis [email protected] 61 2 8205 4531

BHP.AX BHP Billiton 36.54 40.00 NEUTRAL -2.0% A Neutral 28/12/2012 Paul McTaggart [email protected] 61 2 8205 4698

BKN.AX Bradken Limited 5.98 6.60 NEUTRAL 0.0% BBB Neutral 3/05/2012 Paul Buys [email protected] 61 2 8205 4538

BLD.AX Boral 4.86 5.40 OUTPERFORM -1.0% AA Neutral 25/05/2012 Andrew Peros [email protected] 61 2 8205 4013

BLY.AX Boart Longyear Group 1.92 1.85 OUTPERFORM 0.0% AA Neutral 24/04/2012 Emma Alcock [email protected] 61 2 8205 4403

BND.AX Bandanna Energy Limited 0.32 0.50 OUTPERFORM -10.0% James Redfern [email protected] 61 2 8205 4779

BOQ.AX Bank of Queensland 7.99 8.00 NEUTRAL 0.0% BB Neutral 25/10/2012 James Ellis [email protected] 61 2 8205 4531

BRG.AX Breville Group 6.44 7.10 OUTPERFORM 0.0% Paul Buys [email protected] 61 2 8205 4538

BSE.AX Base Resources Ltd 0.36 0.80 OUTPERFORM -68.0% Matthew Hope [email protected] 61 2 8205 4669

BSL.AX BlueScope Steel 3.46 RESTRICTED Michael Slifirski [email protected] 61 3 9280 1845

BTT.AX BT Investment Management 2.80 2.60 NEUTRAL 0.0% David Bailey [email protected] 61 2 8205 4739

BTU.AX Bathurst Resources 0.42 0.60 OUTPERFORM -18.0% B Neutral 28/12/2012 James Redfern [email protected] 61 2 8205 4779

BXB.AX Brambles Limited 7.80 7.90 OUTPERFORM 0.0% AAA Neutral 1/03/2012 Nicholas [email protected] 2 8205 4400

CAB.AX Cabcharge Australia 4.61 5.40 NEUTRAL -10.0% BBB Negative 1/03/2012 Paul Buys [email protected] 61 2 8205 4538

CBA.AX Commonwealth Bank Australia 62.20 54.00 UNDERPERFORM 0.0% AA Neutral 25/10/2012 Jarrod Martin [email protected] 61 2 8205 4334

CCL.AX Coca-Cola Amatil 13.29 13.55 UNDERPERFORM 0.0% A Neutral 8/06/2012 Larry Gandler [email protected] 61 3 9280 1855

CFX.AX CFS Retail Property Trust 1.98 1.98 NEUTRAL 0.0% AA Neutral 10/10/2012 John Richmond [email protected] 61 2 82054580

CGF.AX Challenger Financial Services Group3.75 4.90 OUTPERFORM 0.0% David Bailey [email protected] 61 2 8205 4739

CLO.AX Clough 1.02 1.11 OUTPERFORM 0.0% Paul Buys [email protected] 61 2 8205 4538

COH.AX Cochlear 81.84 76.00 UNDERPERFORM -2.0% BB Neutral 28/12/2012 Saul Hadassin [email protected] 61 2 8205 4679

COK.AX Cockatoo Coal 0.14 0.17 OUTPERFORM 0.0% James Redfern [email protected] 61 2 8205 4779

CPA.AX Commonwealth Property Office Fund1.11 1.10 NEUTRAL 0.0% AAA Neutral 10/10/2012 John Lee [email protected] 61 2 8205 4413

CPU.AX Computershare 10.24 11.15 OUTPERFORM 0.0% BBB Neutral 25/05/2012 David Bailey [email protected] 61 2 8205 4739

CQR.AX Charter Hall Retail REIT 3.72 3.37 UNDERPERFORM 0.0% BB Neutral 10/10/2012 John Lee [email protected] 61 2 8205 4413

CRF.AX Centro Retail Australia 2.28 2.00 UNDERPERFORM 0.0% B Neutral 10/10/2012 Stephen Rich [email protected] 61 2 8205 4617

CRZ.AX carsales.com.au 8.66 8.80 OUTPERFORM 0.0% B Positive 25/05/2012 Samantha Carleton [email protected] 2 8205 4148

CSL.AX CSL Ltd 54.15 60.50 OUTPERFORM -1.0% BBB Neutral 10/10/2012 Saul Hadassin [email protected] 61 2 8205 4679

CSR.AX CSR 2.09 1.40 UNDERPERFORM -39.0% BB Neutral 25/09/2012 Andrew Peros [email protected] 61 2 8205 4013

CTX.AX Caltex Australia 18.94 18.00 UNDERPERFORM -0.2% A Positive 1/04/2012 James Redfern [email protected] 61 2 8205 4779

CWN.AX Crown 11.92 13.10 OUTPERFORM 0.0% AAA Neutral 1/02/2012 Larry Gandler [email protected] 61 3 9280 1855

DJS.AX David Jones 2.37 2.42 UNDERPERFORM 0.0% B Neutral 27/08/2012 Grant Saligari [email protected] 61 3 9280 1720

DMP.AX Domino's Pizza 10.83 9.99 NEUTRAL 0.0% Paul Buys [email protected] 61 2 8205 4538