Embed Size (px)

Citation preview

Australian Economic Outlook

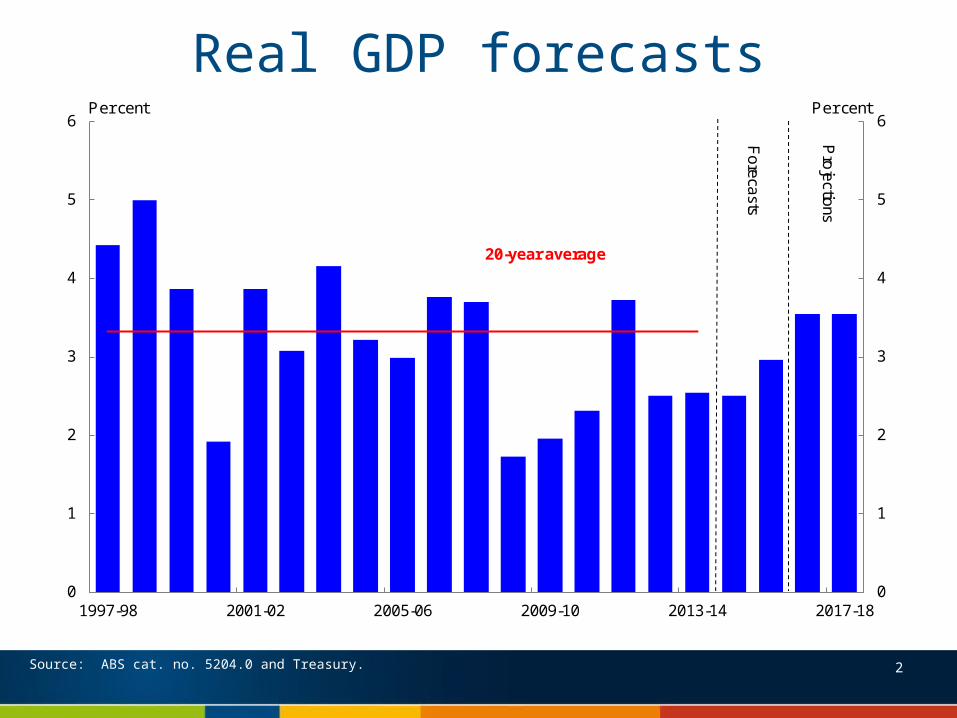

Real GDP forecasts

Source: ABS cat. no. 5204.0 and Treasury.

0

1

2

3

4

5

6

0

1

2

3

4

5

6

1997-98 2001-02 2005-06 2009-10 2013-14 2017-18

Per cent

Fo

reca

sts

Pro

jectio

ns

20-year average

Per cent

2

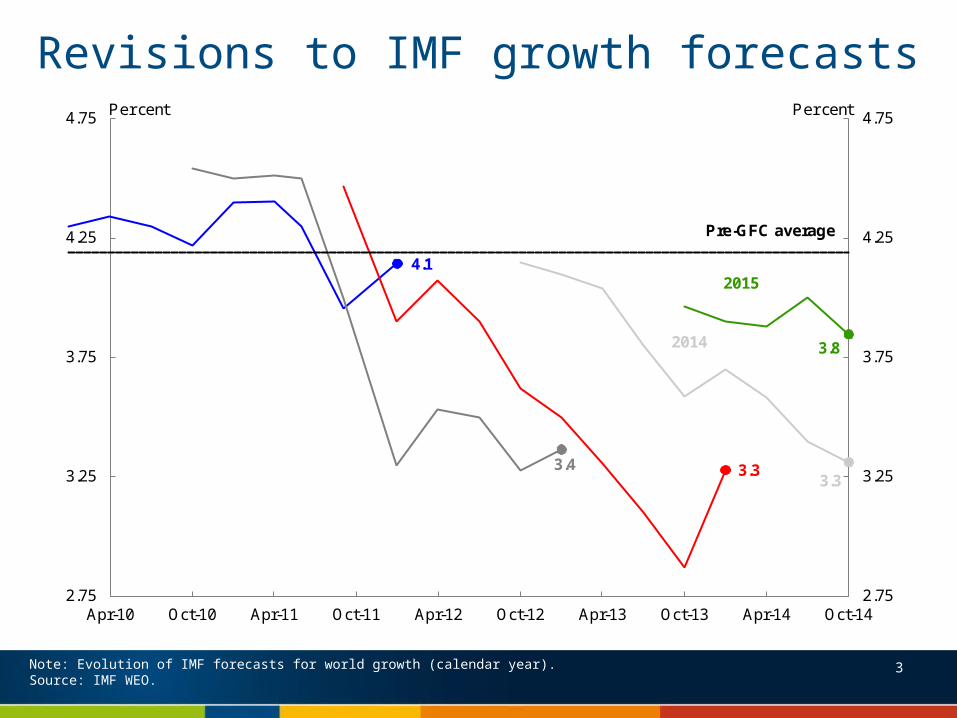

Revisions to IMF growth forecasts

Note: Evolution of IMF forecasts for world growth (calendar year). Source: IMF WEO.

4.1

3.4 3.33.3

3.8

2.75

3.25

3.75

4.25

4.75

2.75

3.25

3.75

4.25

4.75

Apr-10 Oct-10 Apr-11 Oct-11 Apr-12 Oct-12 Apr-13 Oct-13 Apr-14 Oct-14

Per centPer cent

Pre-GFC average

2014

2015

3

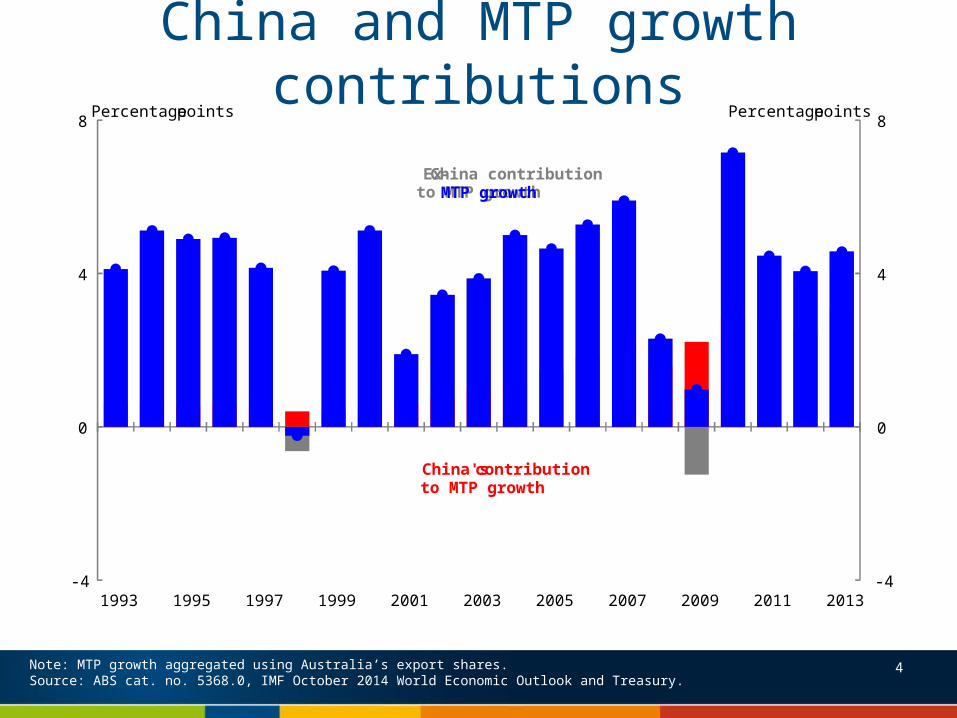

China and MTP growth contributions

Note: MTP growth aggregated using Australia’s export shares.Source: ABS cat. no. 5368.0, IMF October 2014 World Economic Outlook and Treasury.

4

-4

0

4

8

-4

0

4

8

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Percentage points

China's contribution to MTP growth

Ex-China contribution to MTP growth

Percentage points

MTP growth

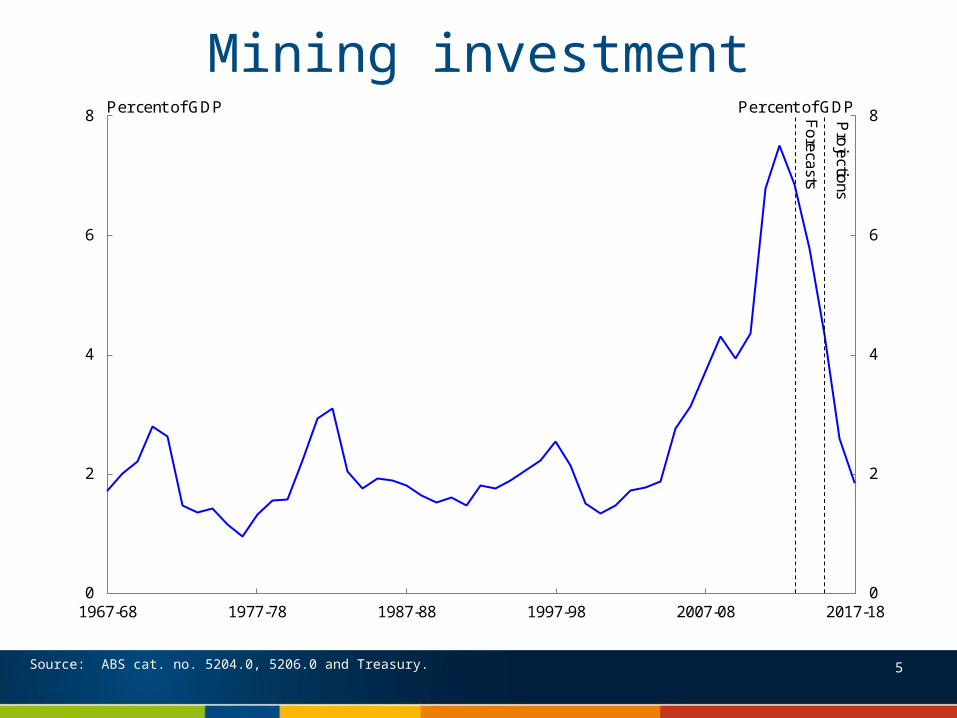

Mining investment

Source: ABS cat. no. 5204.0, 5206.0 and Treasury.

0

2

4

6

8

0

2

4

6

8

1967-68 1977-78 1987-88 1997-98 2007-08 2017-18

Per cent of GDPPer cent of GDP Fo

reca

sts

Pro

jectio

ns

5

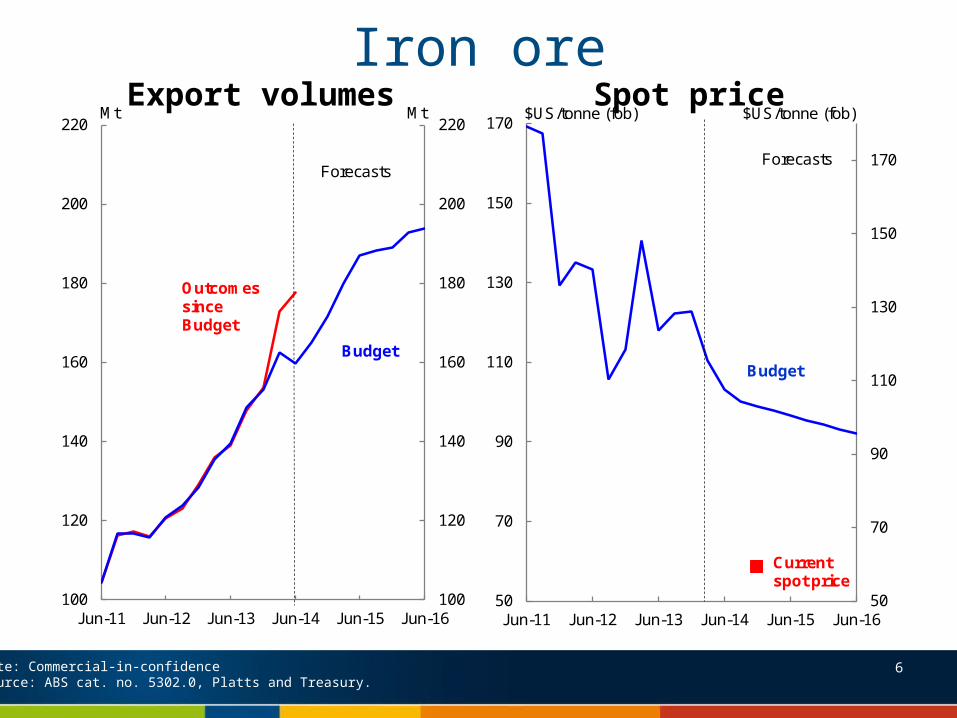

Iron oreExport volumes Spot price

6Note: Commercial-in-confidence Source: ABS cat. no. 5302.0, Platts and Treasury.

100

120

140

160

180

200

220

100

120

140

160

180

200

220

Jun-11 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16

MtMt

OutcomessinceBudget

Budget

Forecasts

50

70

90

110

130

150

170

50

70

90

110

130

150

170

Jun-11 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16

$US/tonne (fob) $US/tonne (fob)

Current spot price

Forecasts

Budget

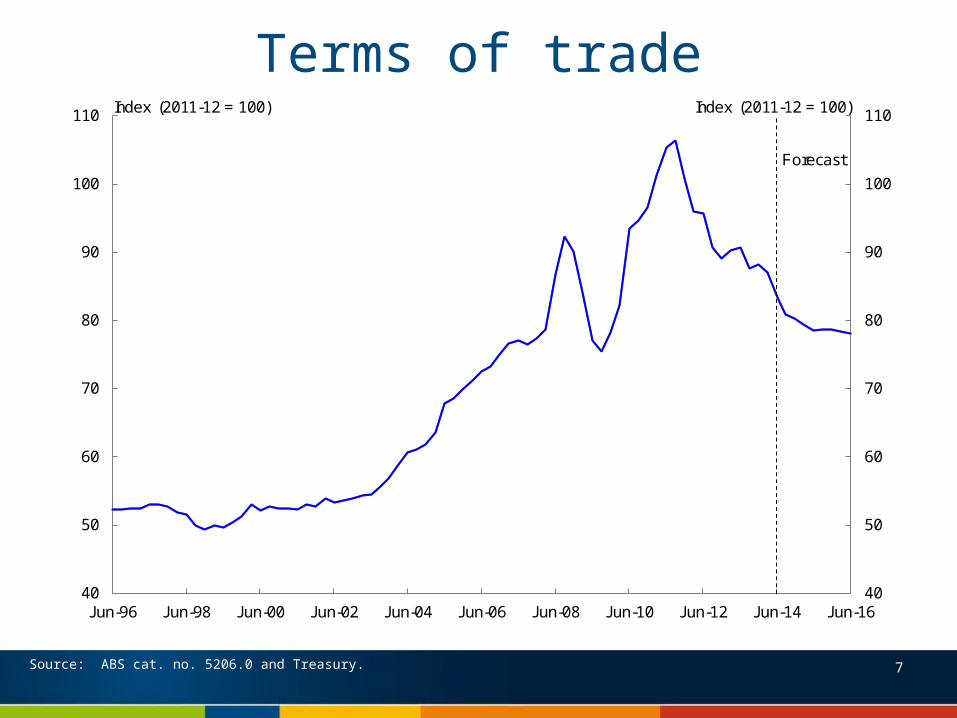

Terms of trade

40

50

60

70

80

90

100

110

40

50

60

70

80

90

100

110

Jun-96 Jun-98 Jun-00 Jun-02 Jun-04 Jun-06 Jun-08 Jun-10 Jun-12 Jun-14 Jun-16

Index (2011-12 = 100)Index (2011-12 = 100)

Forecast

7Source: ABS cat. no. 5206.0 and Treasury.

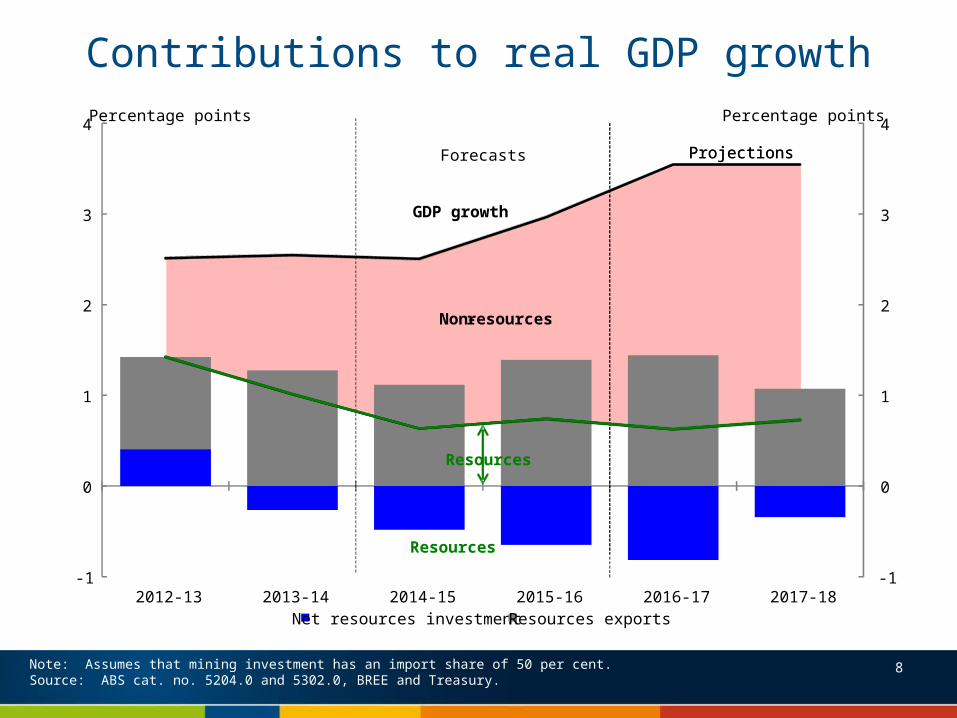

Non-resources

GDP growth

Contributions to real GDP growth

Note: Assumes that mining investment has an import share of 50 per cent.Source: ABS cat. no. 5204.0 and 5302.0, BREE and Treasury.

8

-1

0

1

2

3

4

-1

0

1

2

3

4

2012-13 2013-14 2014-15 2015-16 2016-17 2017-18

Percentage pointsPercentage points

Net resources investment Resources exports

ProjectionsForecasts Projections

Resources

Resources

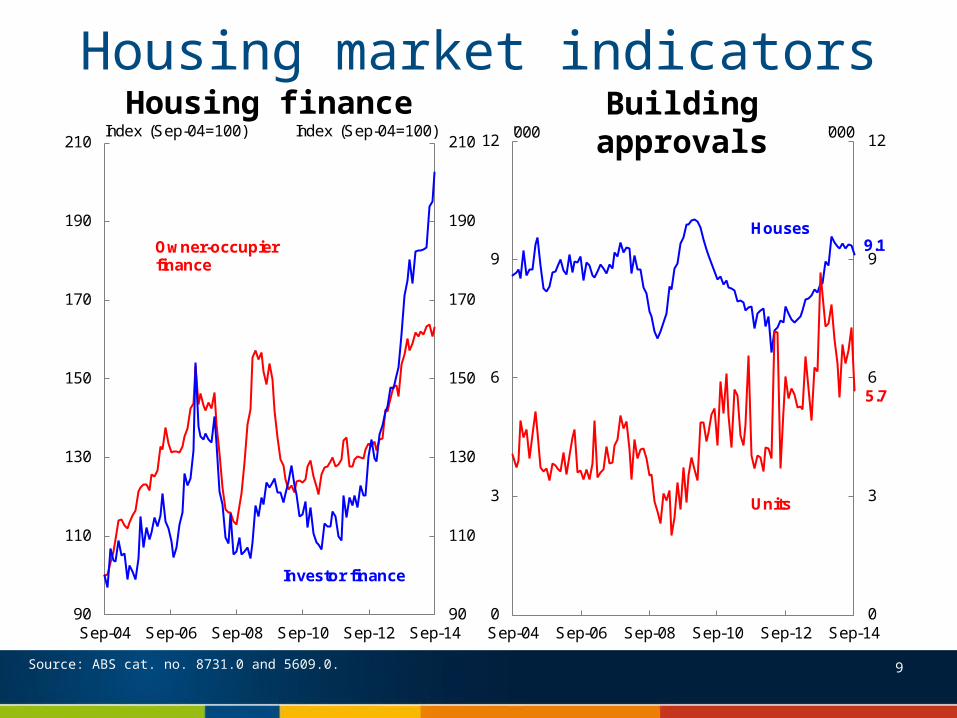

Housing market indicatorsBuilding approvals

Source: ABS cat. no. 8731.0 and 5609.0.

Housing finance

9.1

5.7

0

3

6

9

12

0

3

6

9

12

Sep-04 Sep-06 Sep-08 Sep-10 Sep-12 Sep-14

'000 '000

Houses

Units

90

110

130

150

170

190

210

90

110

130

150

170

190

210

Sep-04 Sep-06 Sep-08 Sep-10 Sep-12 Sep-14

Index (Sep-04=100) Index (Sep-04=100)

Owner-occupier finance

Investor finance

9

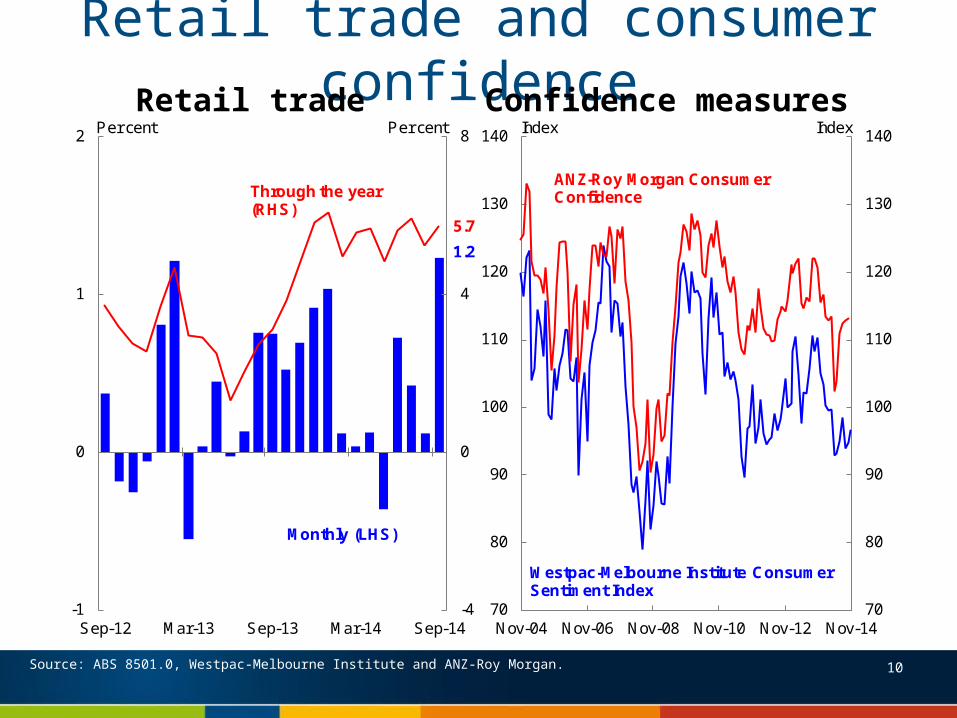

Source: ABS 8501.0, Westpac-Melbourne Institute and ANZ-Roy Morgan.

Retail trade and consumer confidenceRetail trade Confidence measures

70

80

90

100

110

120

130

140

70

80

90

100

110

120

130

140

Nov-04 Nov-06 Nov-08 Nov-10 Nov-12 Nov-14

Index Index

ANZ-Roy Morgan Consumer Confidence

Westpac-Melbourne Institute ConsumerSentiment Index

10

1.2

5.7

-4

0

4

8

-1

0

1

2

Sep-12 Mar-13 Sep-13 Mar-14 Sep-14

Per cent Per cent

Monthly (LHS)

Through the year (RHS)

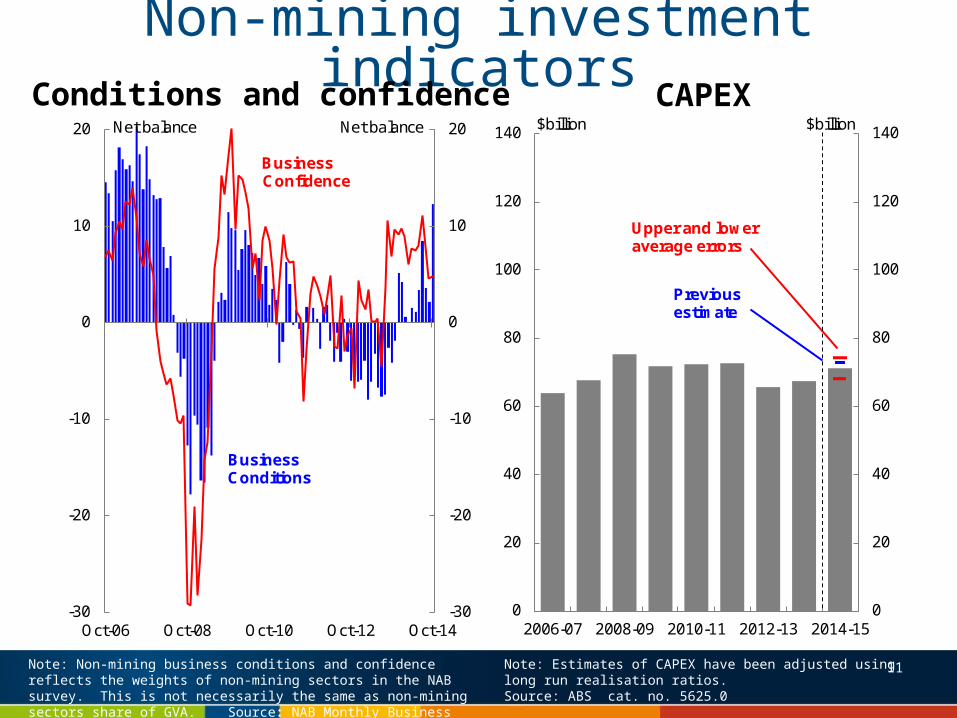

Non-mining investment indicators

Note: Non-mining business conditions and confidence reflects the weights of non-mining sectors in the NAB survey. This is not necessarily the same as non-mining sectors share of GVA. Source: NAB Monthly Business Survey.

Note: Estimates of CAPEX have been adjusted using long run realisation ratios. Source: ABS cat. no. 5625.0

-30

-20

-10

0

10

20

-30

-20

-10

0

10

20

Oct-06 Oct-08 Oct-10 Oct-12 Oct-14

Business Confidence

Business Conditions

Net balance Net balance

Conditions and confidence CAPEX

11

0

20

40

60

80

100

120

140

0

20

40

60

80

100

120

140

2006-07 2008-09 2010-11 2012-13 2014-15

$billion$billion

Upper and lower average errors

Previous estimate

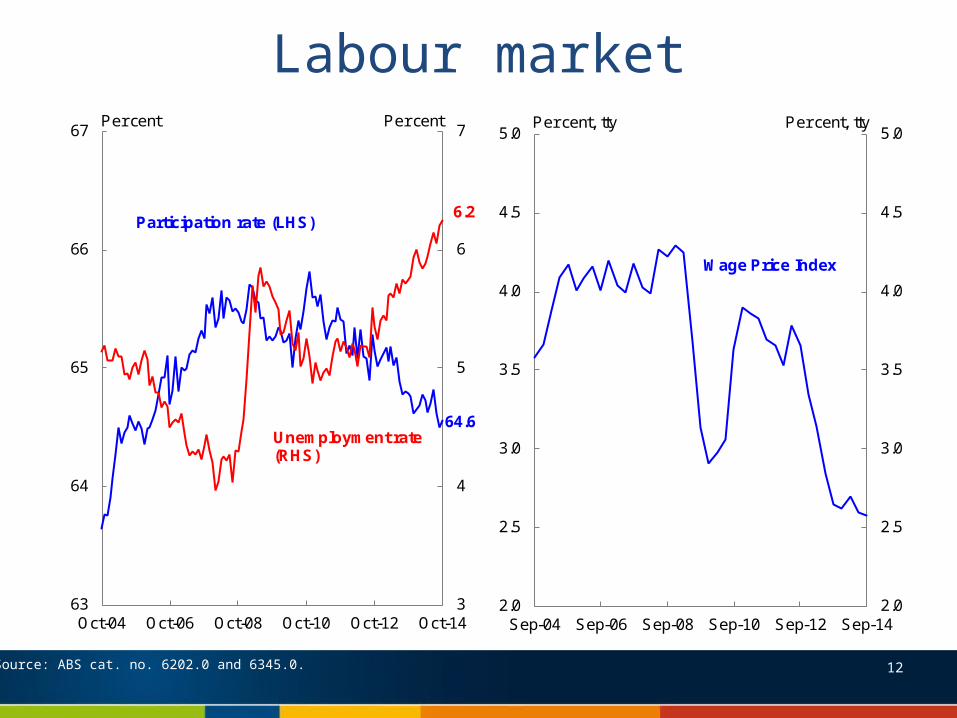

Labour market

Source: ABS cat. no. 6202.0 and 6345.0.

64.6

6.2

3

4

5

6

7

63

64

65

66

67

Oct-04 Oct-06 Oct-08 Oct-10 Oct-12 Oct-14

Per cent Per cent

Unemployment rate(RHS)

Participation rate (LHS)

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Sep-04 Sep-06 Sep-08 Sep-10 Sep-12 Sep-14

Per cent, tty Per cent, tty

Wage Price Index

12

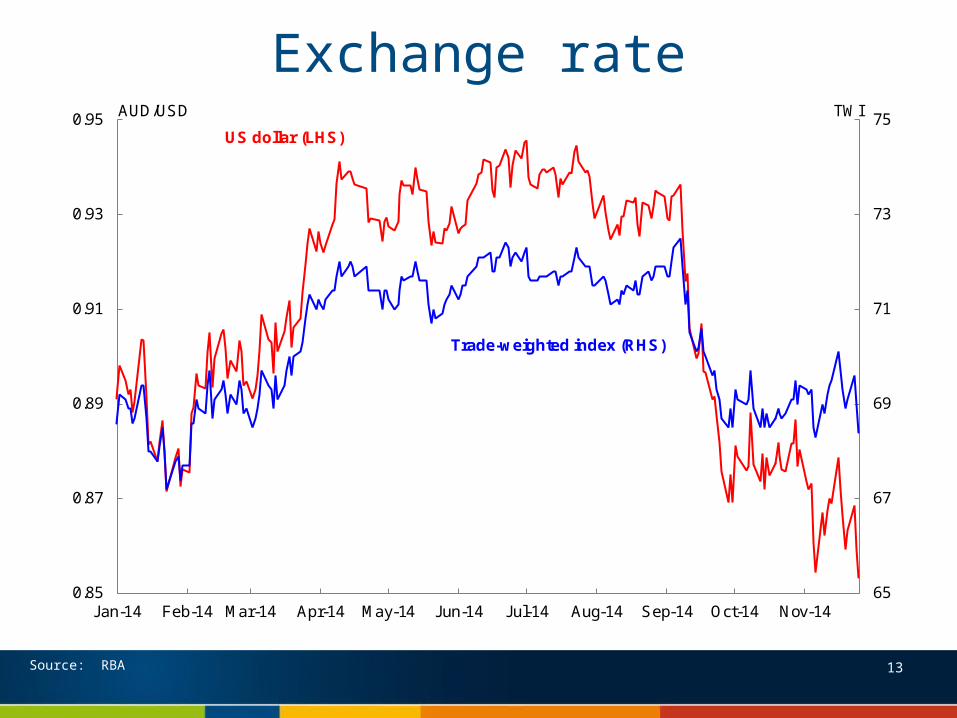

Exchange rate

Source: RBA 13

65

67

69

71

73

75

0.85

0.87

0.89

0.91

0.93

0.95

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14

TWIAUD/USD

US dollar (LHS)

Trade-weighted index (RHS)

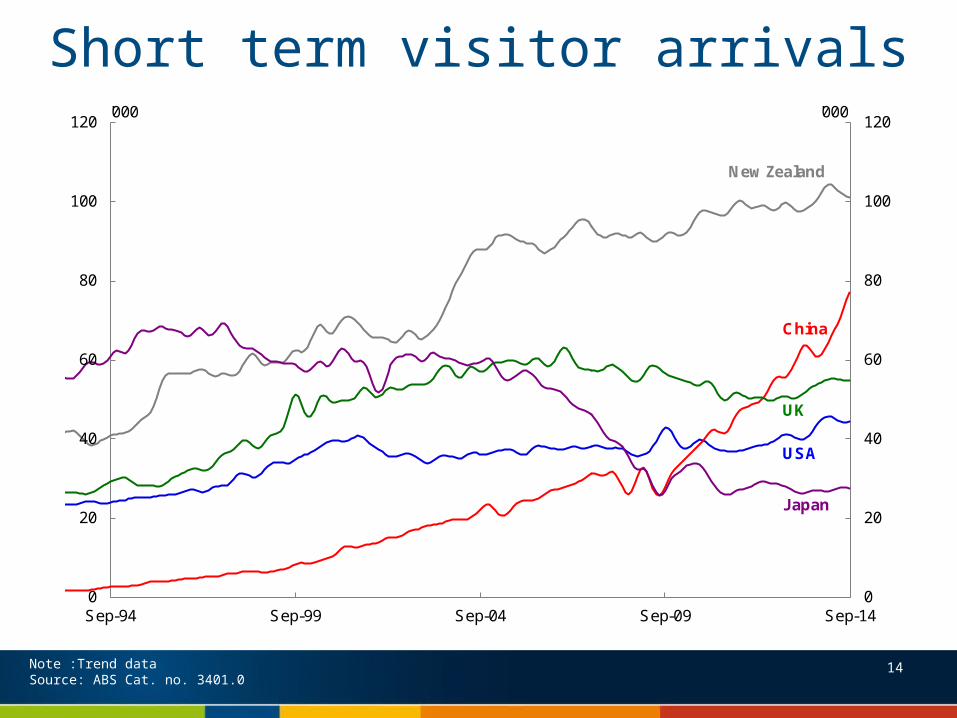

Short term visitor arrivals

Note :Trend dataSource: ABS Cat. no. 3401.0

14

0

20

40

60

80

100

120

0

20

40

60

80

100

120

Sep-94 Sep-99 Sep-04 Sep-09 Sep-14

'000'000

China

New Zealand

UK

Japan

USA

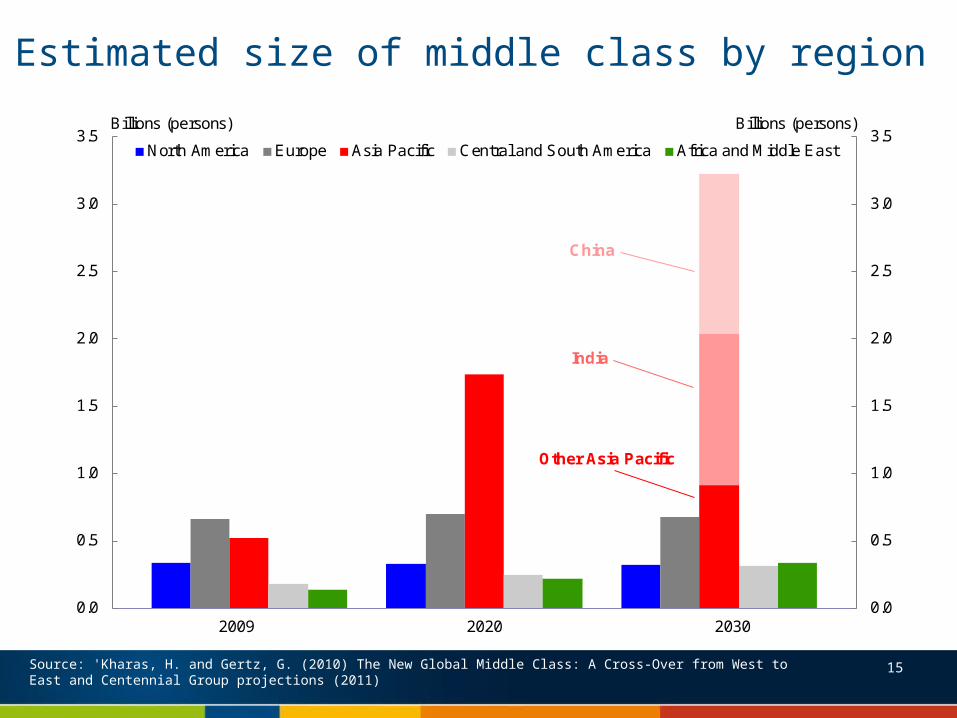

Estimated size of middle class by region

Source: 'Kharas, H. and Gertz, G. (2010) The New Global Middle Class: A Cross-Over from West to East and Centennial Group projections (2011)

2009 2020 20300.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5Billions (persons)Billions (persons)

North America Europe Asia Pacific Central and South America Africa and Middle East

India

China

Other Asia Pacific

15

Other slides

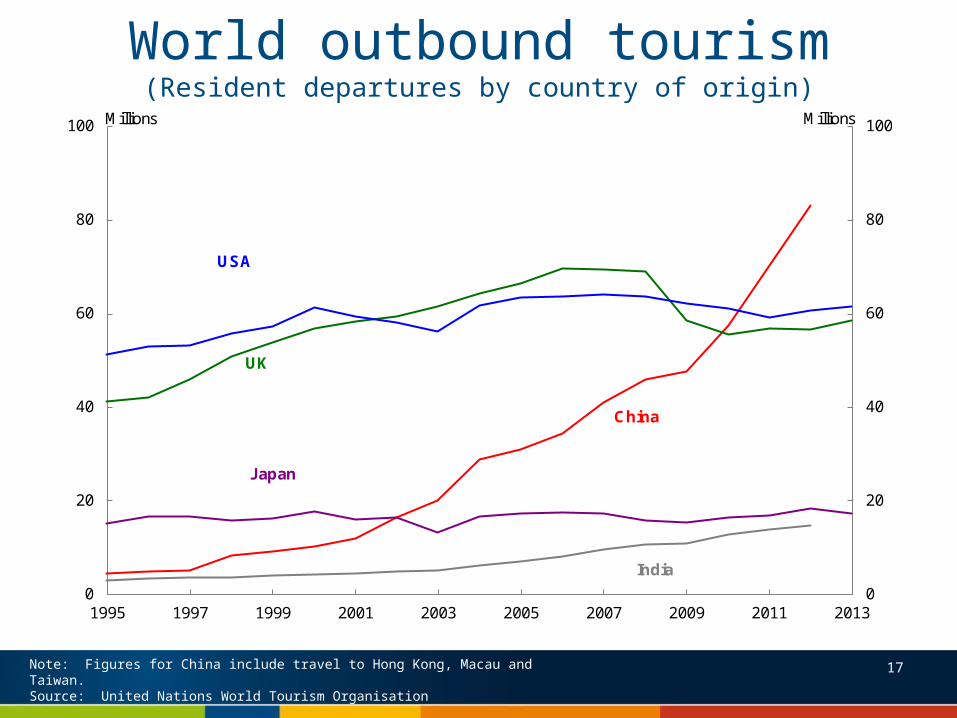

World outbound tourism(Resident departures by country of origin)

Note: Figures for China include travel to Hong Kong, Macau and Taiwan.Source: United Nations World Tourism Organisation

0

20

40

60

80

100

0

20

40

60

80

100

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

China

UK

USA

India

Japan

Millions Millions

17

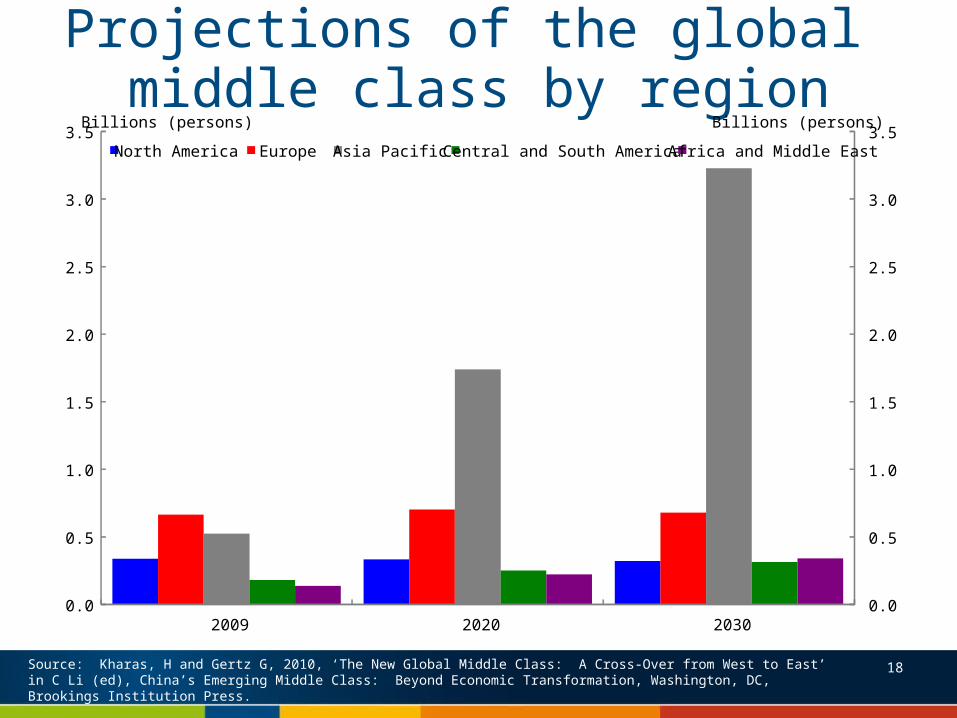

Projections of the global middle class by region

Source: Kharas, H and Gertz G, 2010, ‘The New Global Middle Class: A Cross-Over from West to East’ in C Li (ed), China’s Emerging Middle Class: Beyond Economic Transformation, Washington, DC, Brookings Institution Press.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2009 2020 2030

North America Europe Asia Pacific Central and South America Africa and Middle East

Billions (persons) Billions (persons)

18

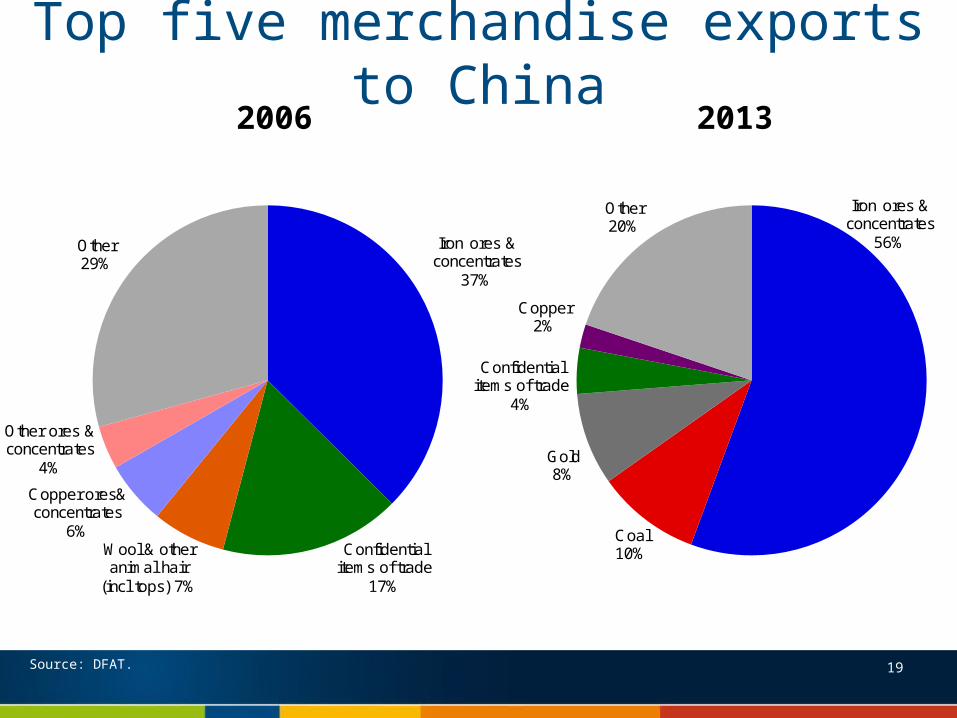

Top five merchandise exports to China2006 2013

Source: DFAT. 19

Iron ores & concentrates

37%

Confidential items of trade

17%

Wool & other animal hair

(incl tops) 7%

Copper ores& concentrates

6%

Other ores & concentrates

4%

Other29%

Iron ores & concentrates

56%

Coal10%

Gold8%

Confidential items of trade

4%

Copper2%

Other20%

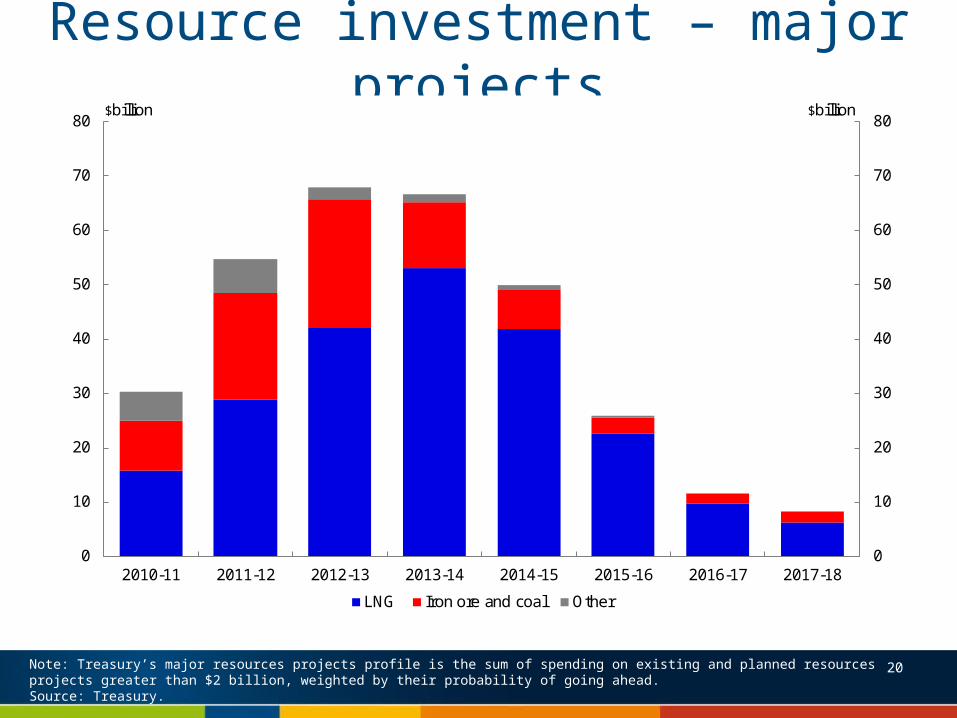

Resource investment – major projects

Note: Treasury’s major resources projects profile is the sum of spending on existing and planned resources projects greater than $2 billion, weighted by their probability of going ahead.Source: Treasury.

0

10

20

30

40

50

60

70

80

0

10

20

30

40

50

60

70

80

2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18

LNG Iron ore and coal Other

$billion $billion

20

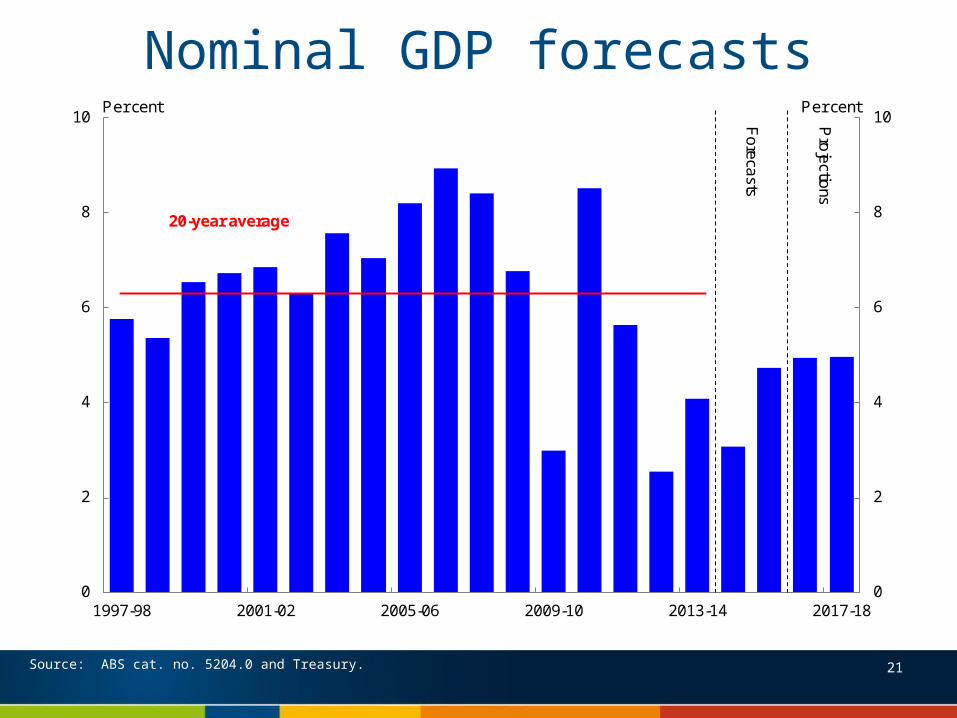

Nominal GDP forecasts

Source: ABS cat. no. 5204.0 and Treasury.

0

2

4

6

8

10

0

2

4

6

8

10

1997-98 2001-02 2005-06 2009-10 2013-14 2017-18

Per cent

Fo

reca

sts

Pro

jectio

ns

20-year average

Per cent

21

Market inflation expectations

22Note: Market inflation expectations are derived from inflation swaps. Expectations are not available for China.Source: Bloomberg

-3

-2

-1

0

1

2

3

4

-3

-2

-1

0

1

2

3

4

Nov 09 Nov 10 Nov 11 Nov 12 Nov 13 Nov 14

Per centPer cent

US Eurozone Japan Australia

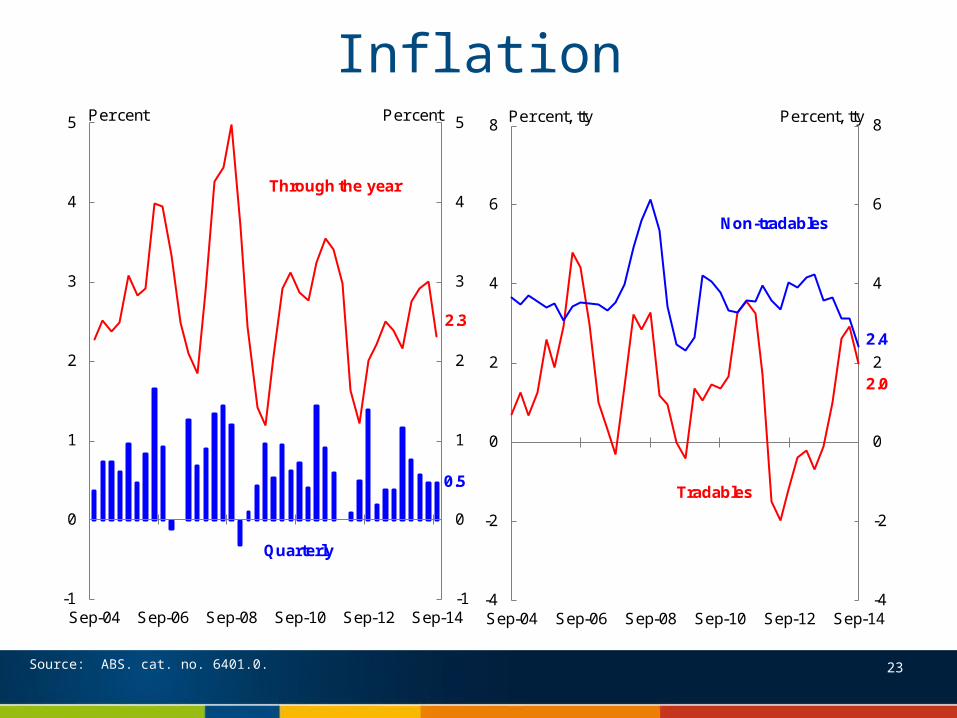

Inflation

Source: ABS. cat. no. 6401.0.

0.5

2.3

-1

0

1

2

3

4

5

-1

0

1

2

3

4

5

Sep-04 Sep-06 Sep-08 Sep-10 Sep-12 Sep-14

Quarterly

Through the year

Per cent Per cent

2.0

2.4

-4

-2

0

2

4

6

8

-4

-2

0

2

4

6

8

Sep-04 Sep-06 Sep-08 Sep-10 Sep-12 Sep-14

Non-tradables

Tradables

Per cent, tty Per cent, tty

23

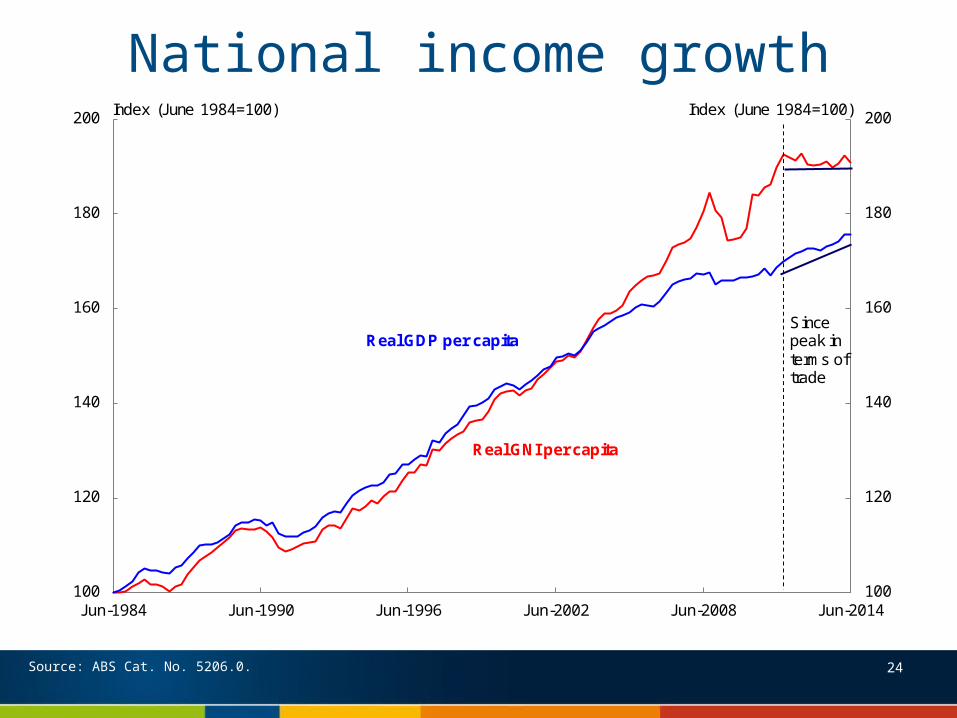

National income growth

100

120

140

160

180

200

100

120

140

160

180

200

Jun-1984 Jun-1990 Jun-1996 Jun-2002 Jun-2008 Jun-2014

Real GDP per capita

Real GNI per capita

Index (June 1984=100) Index (June 1984=100)

Sincepeak in terms of trade

24Source: ABS Cat. No. 5206.0.

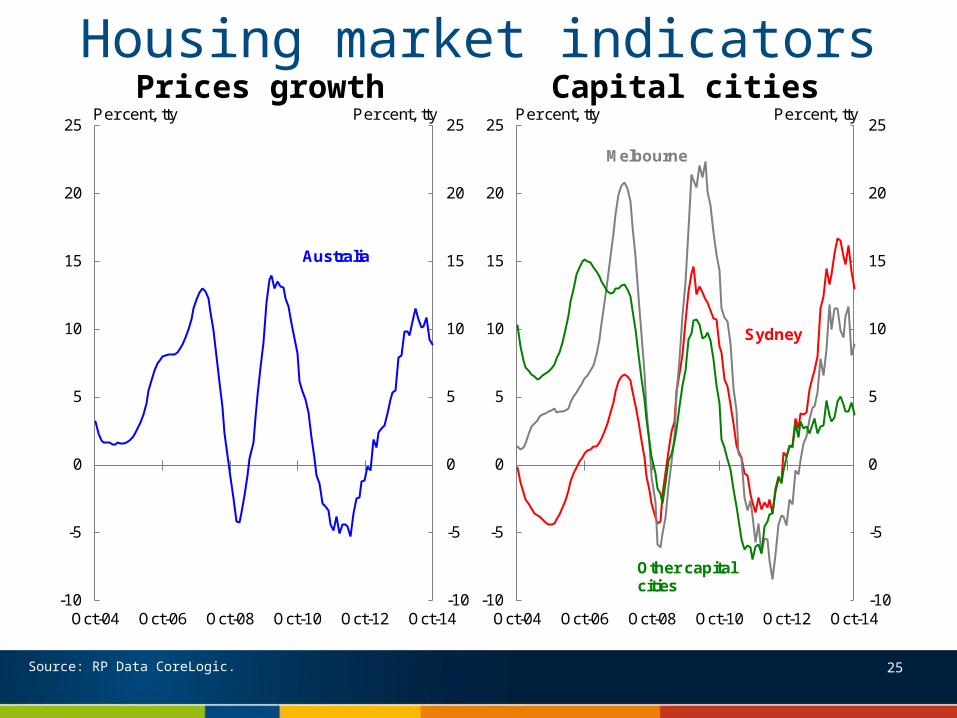

Housing market indicators

Source: RP Data CoreLogic.

-10

-5

0

5

10

15

20

25

-10

-5

0

5

10

15

20

25

Oct-04 Oct-06 Oct-08 Oct-10 Oct-12 Oct-14

Melbourne

Sydney

Other capital cities

Per cent, tty Per cent, tty

-10

-5

0

5

10

15

20

25

-10

-5

0

5

10

15

20

25

Oct-04 Oct-06 Oct-08 Oct-10 Oct-12 Oct-14

Australia

Per cent, tty Per cent, ttyPrices growth Capital cities

25

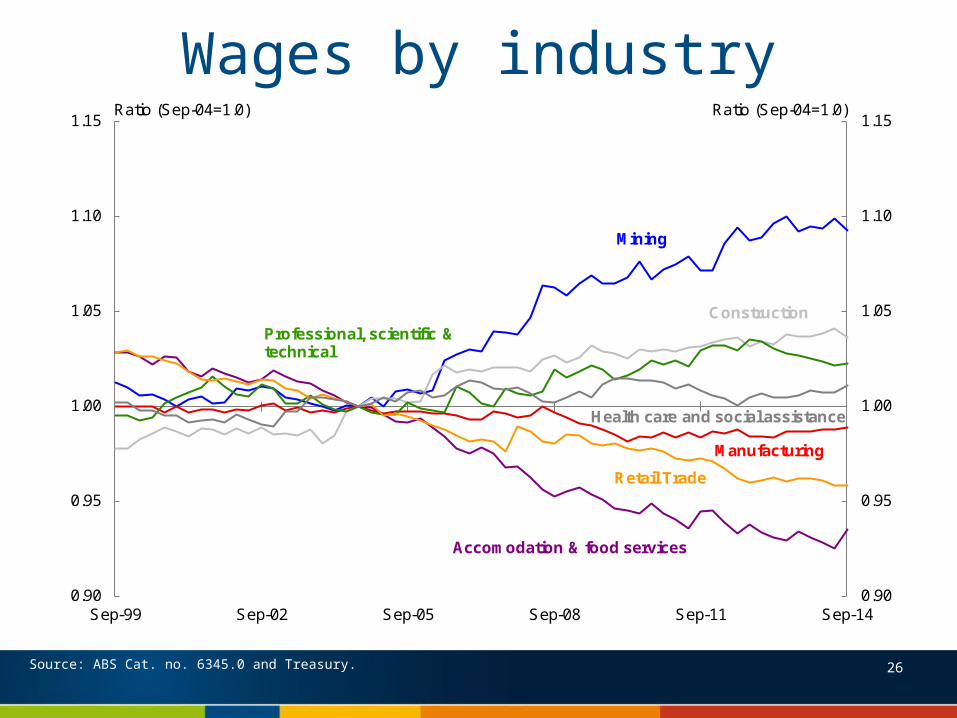

Wages by industry

0.90

0.95

1.00

1.05

1.10

1.15

0.90

0.95

1.00

1.05

1.10

1.15

Sep-99 Sep-02 Sep-05 Sep-08 Sep-11 Sep-14

Mining

ConstructionProfessional, scientific & technical

Health care and social assistance

Manufacturing

Retail Trade

Accomodation & food services

Ratio (Sep-04=1.0) Ratio (Sep-04=1.0)

Source: ABS Cat. no. 6345.0 and Treasury. 26

1

2

3

4

5

6

7

1

2

3

4

5

6

7

Sep-99 Sep-02 Sep-05 Sep-08 Sep-11 Sep-14

Per cent, ttyPer cent, tty

Mining

Total ex. Mining

Source: ABS cat. no. 6345.0 and Treasury.

Wages growth by mining/non-mining

27