Embed Size (px)

Citation preview

A fairer, simpler and more efficient taxation system

5 yeAr reform plAn

June 2012

AustrAliAn cApitAl territory

A fairer, simpler and more efficient taxation system >>> 5 year reform plan

© Australian Capital Territory, Canberra 2012

ISBN 978-0-642-60581-8

This work is copyright. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced by any process without written permission from the Territory Records Office, Shared Services, Treasury Directorate, ACT Government. GPO Box 158, Canberra City ACT 2601.

Published by Publishing Services for the:

l Treasury Directorate, ACT Government

Enquiries about this publication should be directed to:

Treasury DirectorateGPO Box 158Canberra City, ACT 2601

www.treasury.act.gov.au

Publication No 12/0715

http://www.act.gov.au

Telephone Canberra Connect 132 281

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 1

treasurer’s message 2

executive summary 3

Why is reform necessary? 8

summary of reform 10

reform is fiscally responsible 12

the reform includes targeted support measures 13

reform measures 14

impact of reform 16Households 16

Businesses 18

first Home Buyers 19

renters 19

rental Investors 20

older Canberrans 21

Distribution of reform impacts 22abolishing Duty on Insurance 22

payroll Tax 22

phasing out Duty on Conveyances 23

Improving progressivity of residential land Tax 23

Utilities network facilities Tax 27

residential General rates 28

Distributional Impacts on pensioners 32

individual tax reform measures 33removing Duty on Insurance 34

abolishing Conveyance Duty 36

reducing payroll Tax 39

Improving the progressivity of residential land Tax 41

abolishing Commercial land Tax 46

residential General rates 47

Commercial General rates 49

Utilities (network facilities) Tax (UnfT) 50

expanding assistance to Households 51

Abbreviations 56

Glossary 57

find out more 59

contents

2 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

The aCT has a modern, thriving economy with high quality services and infrastructure. However, our future prosperity depends on being able to fund the services and infrastructure the Canberra community deserves and expects.

The aCT’s taxation system allows the Government to support those in need, to function effectively, and to make investments for the benefit of current and future generations.

However, our taxation system has become outdated, and is in need of reform. The Commonwealth’s tax review (the Henry review) and the aCT Taxation review (the Quinlan review) both concluded that the aCT’s taxation system – similar to other states and territories – is inefficient and unsustainable. Both reviews also outlined a plan for reform.

The aCT Government’s vision is to create a tax system that is fairer, simpler and more efficient, and that is sustainable for the long term.

We will reduce taxes for those on lower incomes, make taxes simpler to understand and administer, and reduce distortions on household spending and business activity.

further, we will continue to provide appropriate and targeted assistance and financial support to those who need it.

Taxation reform is difficult for a number of reasons. Changing taxes means changing how people share the costs of our society’s functioning. It would be easy to wait for joint national action on reform. However, this could be a very long wait and it increases the likelihood of sharp adjustments to services or tax policy settings in the future, which could harm the social and economic wellbeing of the Territory. Delaying reform also reduces the potential benefits to the Territory’s economy from a simpler and more efficient system.

This plan is the first stage of what will be a long-term process. reform needs to be phased in to avoid distortions in the market.

Together, the reform measures announced in this first stage make a substantial improvement in the Territory’s taxation system. The benefits of these reforms are economy wide – the costs and benefits are spread across the whole community.

The Taxation reform plan will support economic growth, make the Territory’s taxes sustainable in the long run and allow the Government to maintain and enhance the high standard of living our community enjoys.

Andrew Barr mlATreasurer

June 2012

treasurer’s message

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 3

BackgroundThe need for the reform of State and Territory taxes was highlighted in the Commonwealth’s Australia Future Tax System (afTS) report.

The subsequent review of the Territory’s taxation system commissioned by the aCT Government reaffirmed the afTS’ finding regarding the efficacy of some of the major taxes. The aCT Taxation review concluded that there are risks to the long term sustainability of revenues for the Territory – a number of major taxes are unfair, have high economic efficiency costs, are highly volatile, and as such are unsustainable.

The aCT’s taxation system is not unique in relying on such taxes; all State and Territory jurisdictions need to resort to those taxes given their circumstances. The aCT, however, has a unique opportunity to commence structural reform.

The relatively higher socio-economic status provides capacity to cushion the transition costs of reform. The Territory, due to its combined state and local government functions, also has access to a base for what is considered a highly efficient tax – a broad based tax on land.

The review highlighted the necessity for the reform to be over a long time frame. It suggested that measures and steps could be taken that combined will lead to structural change over time.

taxation reform planThe Government in its response, released along with the review report, reaffirmed its commitment to the reform of the Territory’s taxation system, and commenced a process of further consultation with the community and business. The 2012-13 Budget includes a package of measures to commence reform.

Approaching the reform

The measures in the package are not developed as annual initiatives; they represent a 5 year Taxation reform plan. The plan sets the broad direction for reform, and makes some measured changes to the taxation system.

for this plan, General rates is adopted as the revenue replacement base. This is the base identified in afTS and the aCT Taxation review as the most efficient taxation base available.

The plan improves the overall fairness of the taxation system.

executive summary

4 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

Duty on conveyances is considered a highly unfair tax. a small number of households contribute disproportionately to the funding of services, at a time when their circumstances may necessitate a move. The plan commences a phase out of duty on conveyances for both the residential and commercial sectors.

The plan makes the taxation system simpler, by combining some of the taxes. Commercial land Tax will be combined with the commercial General rates system.

The reform measures combined are aimed at improving the economic efficiency of the taxation system.

By the end of the forward estimates period, the share of transaction taxes will reduce from 29 per cent of the total taxation to 23 per cent. The share of efficient taxes will increase from 29 per cent to 38 per cent.

The excess economic burden is estimated to reduce by around $169 million cumulatively over the next five years.

By the end of the first 5 year reform plan, the Territory’s taxation system will be fairer, simpler, and more efficient.

The reform plan is fiscally responsible.

revenue foregone from abolishing or phasing out of unfair and inefficient taxes is replaced annually through more efficient taxes. This ensures that while the tax settings are adjusted, the capacity for priority services is preserved.

The plan is socially equitable.

revenue replacement is also accompanied by improving the progressivity of the overall system. Tax brackets based on land values and increasing marginal tax rates are being introduced.

The impacts of revenue replacement measures on lower value properties are relatively lower – in fact, close to a quarter of dwellings will be subject to lower General rates. Impacts on pensioners and households on statutory incomes are further ameliorated through significantly increasing the General rates rebate cap.

The plan is designed to support key policy objectives.

The progressivity of the residential land Tax system is being improved to reduce rental pressures for median priced dwellings. a more efficiently working housing market from the phase-out of conveyance and land Tax reform will be more attractive to investment in rental accommodation, and improve rental affordability.

The phase-out of conveyance duty on commercial transactions, changes to landholder provisions, and the treatment of wholesale unit trusts should make the aCT relatively more attractive for commercial investment.

a simplified tax system for businesses and the extension of the tax-free threshold for payroll Tax should support business and jobs growth.

The plan is measured and designed to minimise distortions.

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 5

In general, taxes change behaviour. Changes in taxation settings, even when improving the efficiency of the system, can have adverse effects. The annual adjustment measures in the plan are deliberately kept small so as not to distort markets or decisions by households or businesses.

Cumulatively, however, the adjustments represent a significant change. By the end of five years, conveyance duty on a block of land would reduce by up to 45 per cent. for a home valued at $450,000 the tax will reduce by around 35 per cent.

While the general direction of reform is set, the plan provides opportunity for a community conversation to continue for the future reform.

reform measuresThe key reform measures are:

l Duty on insurance policies will be abolished over the next five years. The tax on general insurance and life insurance policies will be reduced by 20 per cent every year from 2012-13.

l a phase out of duty on conveyances will commence. The marginal tax rates will be adjusted every year to progressively reduce the duty. The changes will apply to both the residential and commercial sectors.

l revenue replacement will be through the General rates for both the residential and commercial sectors. The progressivity of the General rates system is being improved to make the revenue substitution more equitable.

l Commercial land Tax is being abolished and substituted by an increase in commercial General rates on a revenue and cost neutral basis.

l residential land Tax is being made more progressive to reduce the tax burden for properties below the median price.

l The tax-free threshold for payroll Tax is being increased to $1.75 million.

l motor vehicle registrations will be based on environmental performance of the vehicles. This reform will commence in future years once the Green Vehicle rating guide has been completed.

l a number of legislative amendments are included to improve the functioning and operations of various taxes. Significant amendments relate to:

– align more closely to landholder provisions in the Duties Act 1999 with new South Wales (nSW).

– The treatment of wholesale unit trusts.

– abolishing duty on subleases.

6 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

targeted Assistance measures

The plan includes a number of targeted support measures to ameliorate the impact of reform, or to improve access.

l The cap for General rates rebate will be increased from $481 in 2011-12 to $565 in 2012-13, an increase of 17 per cent. pre 1997 pensioners subject to uncapped rebate, will receive a 50 per cent rebate on any rates increase.

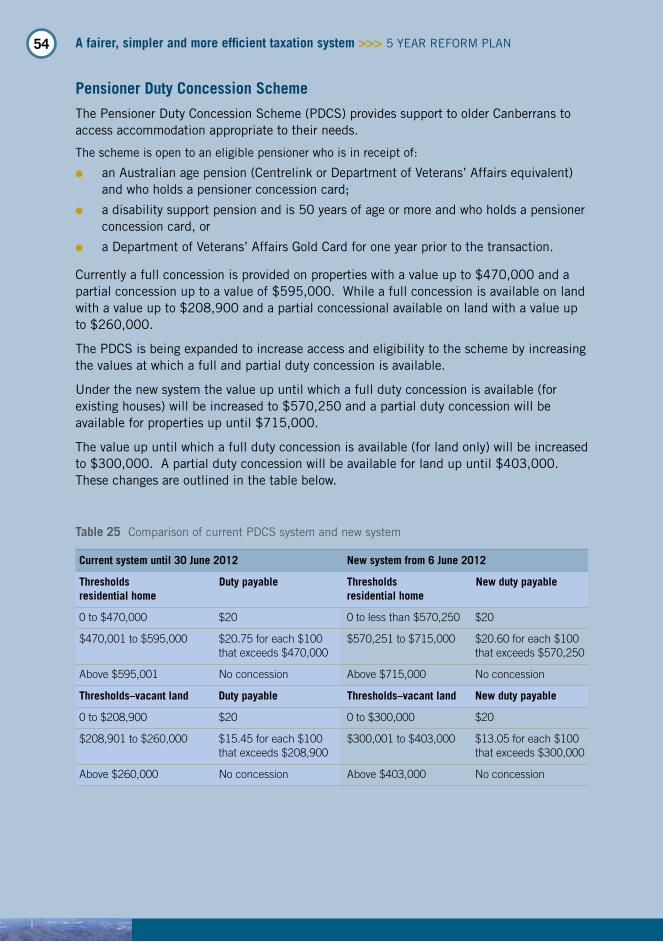

l The pensioner Duty Concession Scheme (pDCS) is being extended by three years. The property value thresholds are being increased with a full concession available up to a value of $570,250 (the 75th percentile value) and a partial concession up to $715,000 (the 90th percentile).

l The income threshold for the Home Buyer Concession Scheme (HBCS) is being increased by 25 per cent to $150,000. The eligibility will be limited to new dwellings, land purchased for a first home, or significantly renovated dwellings.

l The rates Deferral Scheme (rDS) is being extended to non pensioners. The option will be available to people over 65, whether working or retired, with below average incomes and the unimproved land value above $390,000 (the 80th percentile). Households need to have at least 75 per cent equity in the dwelling to be able to defer the tax as a charge on the dwelling.

l The Duty Deferral Scheme (DDS) will be available to those eligible for HBCS or first Home owners Grant (fHoG).

6

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 7

the impacts of reformThere will be an improvement in the overall economic efficiency from a net decrease in excess economic burden. By the last year, the annual net benefit will reach around $57 million. Cumulatively, over the five years, the economic benefit is estimated at around $169 million.

The budget’s reliance on relatively inefficient taxes will reduce. The share of inefficient taxes will reduce from 71 per cent to 62 per cent by 2015-16.

average savings per household from the abolition of duty on insurance will be $34 in 2012-13 increasing to $171 based on the current premiums.

In 2012-13, phasing out duty on conveyances will reduce the duty by 2 per cent for $1 million transaction, and by 13 per cent for a $0.2 million transaction. These benefits will increase to 14 per cent and 45 per cent by the last year.

from 2012-13, residential land Tax will reduce for around 74 per cent of the properties by an average of $208. for some suburbs, the decrease will be up to 16 per cent of the current land Tax payable, which should reduce pressures on rents. around 12 per cent of the properties will have an average increase of $602, and up to 14 per cent of the current rent payable.

residential General rates will increase by $122 on average. around 24 per cent of the properties will have a rates reduction. on average, General rates will decrease for the bottom two property value quintiles.

reforms to payroll Tax will result in 115 businesses in the Territory no longer having to pay this tax. on average, all businesses with a payroll above $1.75 million will receive a benefit of around $17,125.

8 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

some of the major taxes have high economic costs

5

10

15

20

25

0

30

35

40

45

50

Conveyance Duty

General Rates

Land Tax

Payroll Tax

General Insurance

5

10

15

20

25

0

Vola

tilit

y (%

)

30

Land Tax

General Rates

Gambling Tax

Payroll Tax

Conveyance Duty

General Insurance

some taxes are highly volatile and unreliable

chart 1 economic cost of major taxes

Total compliance, administration, and economic efficiency cost per dollar of tax is:

l around 43 cents for duty insurance;

l around 38 cents for duty on conveyances; and

l around 36 cents for payroll Tax.

Combined, these taxes comprise around 60 per cent of total taxation.

Conveyance duty stands out as the most volatile and unpredictable tax.

chart 2 Volatility of major taxes

Why is reform necessary?

Cen

ts p

er d

olla

r

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 9

0

0–4

5–9

10–1

4

15–1

9

20–2

4

25–2

9

30–3

4

35–3

9

40–4

4

65–6

9

70–7

4

75–7

9

80–8

4

85+

45–4

9

50–5

4

55–5

9

60–6

4

Age categories (years)

5

10

15

20

25

exp

endi

ture

per

cap

ita

($’0

00

) 30

some of the major taxes are unfairl Conveyance duty raises around one quarter of the taxation revenue from

around 9 per cent of the people whose circumstances may necessitate a move to different accommodation.

l rising conveyance duty discourages people from moving to accommodation that meets their needs.

unfair, inefficient and volatile taxes are unsustainablel With an unsustainable revenue base, delivery of priority services to the

community is at risk. l expenditure on services for the aged is considerably higher than

the average, reaching close to $25,000 per person for people aged 80 years and over.

l a taxation system reliant upon unfair and inefficient taxes cannot support priority services for an ageing population.

chart 4 aCT Government spending per capita by age

2004 20052003 2006 2007 2008 2009 2010 2011

DutyTurnover

Trend (Duty)Trend (Turnover)

50

100

150

200

0

Inde

x =

mar

ch 2

00

3

250

chart 3 number of transactions and conveyance duty on median price

Why is reform necessary?

10 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

A fairer taxation system

5.0

effe

ctiv

e co

nvey

ance

dut

y ra

te (

%)

4.0

3.0

2.0

1.0

0

200 800 1,2000

property value ($’000)

Current system until 5 June 2012

New system from 1 July 2016

6.0

7.0

400 600 1,000 1,400

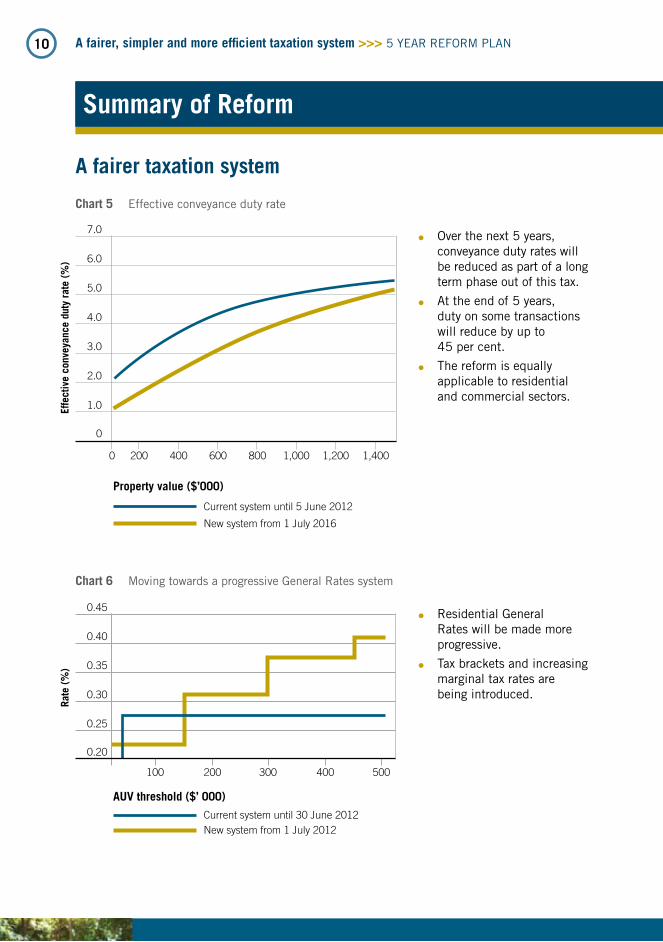

summary of reform

chart 5 effective conveyance duty rate

l over the next 5 years, conveyance duty rates will be reduced as part of a long term phase out of this tax.

l at the end of 5 years, duty on some transactions will reduce by up to 45 per cent.

l The reform is equally applicable to residential and commercial sectors.

rate

(%

)

100

AuV threshold ($’ 000)

200 400 500

0.45

0.40

0.35

0.30

0.25

0.20

300

Current system until 30 June 2012New system from 1 July 2012

chart 6 moving towards a progressive General rates system

l residential General rates will be made more progressive.

l Tax brackets and increasing marginal tax rates are being introduced.

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 11

0

200 400 600 8000

AuV ($’ 000) Current system until 30 June 2012New system from 1 July 2012

700500100 300

summary of reform

A simpler taxation system

abolish duty on general insurance

abolish duty on life insurance

phase out conveyance duty

abolish Commercial land Tax

reduce payroll Tax

abolish duty on transfer of subleases

align more closely with nSW wholesale unit trusts provisions

Increased General rates – Commercial

Increased General rates – residential with enhanced concessions

adjustment to Utilities (network facilities) Tax to reflect land value appreciation

replAce reVenue throuGh

A more efficient taxation system

effe

ctiv

e la

nd ta

x ra

te (

%)

2.0

1.5

1.0

0.5

chart 7 moving towards a more progressive land Tax system

l residential land Tax is being made more progressive.

l Tax rate reduces for land values up to $400,000 to encourage investment in affordable rental accommodation.

l The share of inefficient taxes will reduce and the share of more efficient taxes will progressively increase over the next five years.

l The aCT Taxation reforms will increase the overall economic efficiency of the aCT’s taxation system by an estimated $14.5 million in the first year of reform, increasing to $57 million in 2016-17.

2011–12

2015–16

62%

71%

38%

29%

efficient taxes

Inefficient taxes

summary of reform

12 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

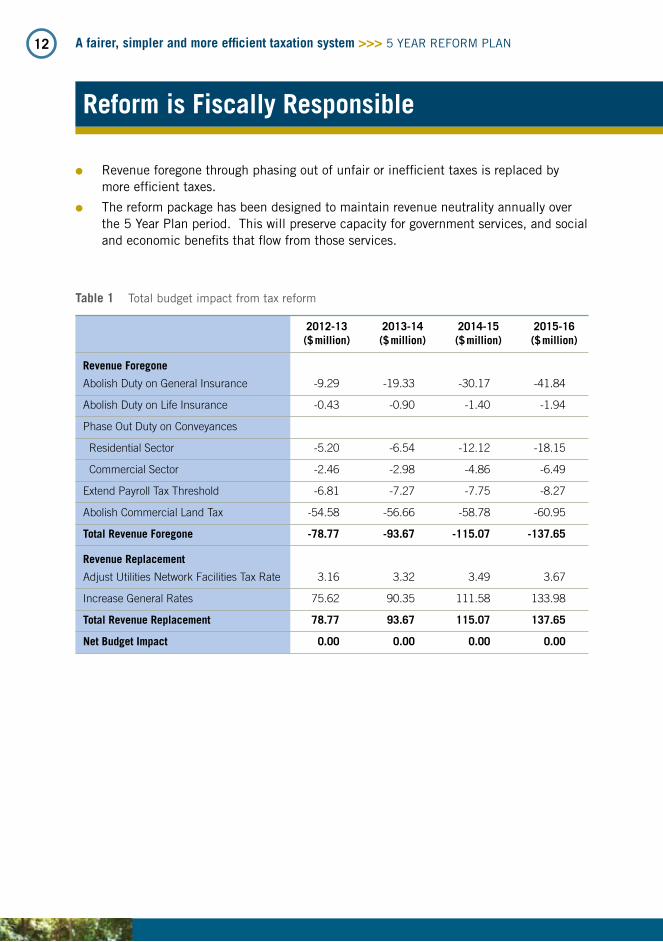

l revenue foregone through phasing out of unfair or inefficient taxes is replaced by more efficient taxes.

l The reform package has been designed to maintain revenue neutrality annually over the 5 year plan period. This will preserve capacity for government services, and social and economic benefits that flow from those services.

table 1 Total budget impact from tax reform

2012-13 2013-14 2014-15 2015-16 ($ million) ($ million) ($ million) ($ million)

revenue foregone

Abolish Duty on General Insurance -9.29 -19.33 -30.17 -41.84

Abolish Duty on Life Insurance -0.43 -0.90 -1.40 -1.94

Phase Out Duty on Conveyances

Residential Sector -5.20 -6.54 -12.12 -18.15

Commercial Sector -2.46 -2.98 -4.86 -6.49

Extend Payroll Tax Threshold -6.81 -7.27 -7.75 -8.27

Abolish Commercial Land Tax -54.58 -56.66 -58.78 -60.95

total revenue foregone -78.77 -93.67 -115.07 -137.65

revenue replacement

Adjust Utilities Network Facilities Tax Rate 3.16 3.32 3.49 3.67

Increase General Rates 75.62 90.35 111.58 133.98

total revenue replacement 78.77 93.67 115.07 137.65

net Budget impact 0.00 0.00 0.00 0.00

reform is fiscally responsible

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 13

General rates rebate for pensioners

l The cap on General rates rebate for pensioners, veterans and concession card holders is being increased by 17 per cent, from $481 in 2011-12 to $565 in 2012-13.

l The pre-1997 pensioners will continue to receive 50 per cent rebate on any increase in their General rates.

pensioner Duty concession scheme (pDcs)

l pDCS is being extended by three years.

l The Scheme’s criteria are also being extended. properties up to the 75th percentile value ($570,250) will receive full concession. The concession will progressively reduce by 90th percentile value ($715,000).

General rates Deferral scheme

l Currently, pensioners are able to defer their General rates. rates deferral options will be available to non-pensioners above 65 years, whether working or retired.

l The eligibility will be on the basis of income, land value, and equity tests.

l This will support ageing in place by providing a choice to households with high value properties, but relatively low incomes to defer their rates as a charge against the property.

Duty Deferral scheme

l During the phase out period of the conveyance duty, deferral option will be available to eligible households.

l The deferral will be available to purchasers eligible for the HBCS or the fHoG scheme, and property value below the median.

the reform includes targeted support measures

14 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

Taxation reform will take place over the next 20 years. reform will be implemented in five year periods. The first 5 year tranche of reform will commence 6 June 2012.

Abolish Duty on insurance

l over the next five years, duty on insurance is being abolished.

l The tax rate at which insurance duty is levied will be reduced by 20 per cent every year.

Abolish Duty on conveyances

l Duty on conveyances is being abolished over the next 20 years. The conveyance duty rate will be progressively reduced over the next five years.

l These decreases form the first steps towards the long-term reform of abolishing duty on conveyances.

Abolish commercial land tax

l land Tax on commercial properties is being abolished and placed on commercial general rates, combining and simplifying the taxes paid on commercial properties.

General rates

l General rates will be used as the base on which to replace revenue lost as a result of abolishing inefficient taxes.

l The system will be made more progressive to ensure the system is fair and equitable.

extend payroll tax thresholds

l The payroll Tax threshold is being increased from $1.5 million to $1.75 million.

increasing the utilities network facilities (unft) tax

l The UnfT rate will be increased to $921 per kilometre to reflect recent growth in average unimproved land values.

legislative measures

Duties Act (land rent scheme)

l legislative changes clarify that the dutiable value of a land rent lease has the same value as a normal crown lease.

l This will ensure that the leases are treated in the same manner as other crown leases and attract the appropriate duty as intended under the scheme.

reform measures

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 15

short-term subleases

l Duty will not be payable on transfers of subleases with a term less than 30 years.

l This will remove a nuisance tax on the aCT business community and streamline the asset transfer process and reduce regulatory and compliance burdens on aCT businesses.

Wholesale unit trusts

l Wholesale unit trust schemes are used by national and international investors. Simplifying landholder provisions will improve the aCT’s attractiveness to large wholesale investors, increase our investment competitiveness and more closely align the aCT with nSW.

l These changes will more closely align the aCT provisions to nSW, reduce the administrative burden on trust companies and simplify compliance in landholder provisions.

land rent scheme

l recent legislative amendments to the land rent Scheme will help improve its operation and further reduce barriers to entry in the aCT residential property market.

– Community Housing Canberra will now be able to access the scheme at the 2 per cent discount rate.

– Households whose circumstances change will be able to immediately move from the 4 per cent to the 2 per cent rate.

l other changes will help streamline existing processes and reduce the administrative burden on the aCT revenue office.

rates and land tax Amendment

l amendments have been made to the rates and land Tax acts to charge rates and land Tax on common areas within a Community Title Scheme at a more appropriate level. Currently the common area is charged Commercial General rates, due to the fact it is not specifically classified as either residential or rural.

l Under the amendments, if all the leases within a Community Title Scheme are residential, then the common area will be charged residential General rates.

reform measures

16 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

There are economy wide benefits from the reform measures in the package. Because the tax reforms are a package of actions, it would be wrong to judge the social impact of each action in isolation. The social impact needs to be assessed as a package.

over the next 5 years, the share of duties on insurance policies and conveyances, payroll Tax, and narrow land Tax will reduce from 71 per cent to 62 per cent. These taxes have economic burden of 35 to 45 cents for every dollar raised in revenue.

The share of the more efficient broad based land Taxes will increase from 29 per cent to 38 per cent.

The improved sustainability and stability of the revenues will ensure the sustainability of the priority services such as health, education, emergency services, child protection, and services to the disabled and the aged.

householdsThe reform of the aCT’s tax system will help ensure that education, health and other services to the community can continue to be adequately funded.

There are wide social benefits from some of the reform measures. However, the reform will affect individuals and households in different ways, depending upon a range of factors and their circumstances. Those include:

l their housing tenure, whether they are homeowners or renters;

l the value of home owners’ home and land;

l whether they are eligible for concessions; or

l whether they are employed in private enterprises subject to payroll Tax.

The 2003 Canberra bushfires highlighted home underinsurance of between 25 per cent and 30 per cent. The aBS data indicates around 32 per cent of households with incomes up to $30,000 have no insurance.

impact of reform

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 17

In 2009-10, on average, Canberra households paid $171 in annual insurance taxes. By 1 July 2017, these taxes will be eliminated. The reduced cost of insurance should allow more households to insure.

Working families will be more able to afford to buy insurance against mishaps which diminish their capacity to work.

The cost of disability income insurance premiums will decline by 9 per cent because the tax on disability insurance is being phased-out.

While concessions are available for first home buyers and those re-entering the market, conveyance duty is an impediment to moving house if circumstances change.

The Government has acknowledged that reform to conveyance duty needs to occur over a long period of time. However, over the next five years, there will be quite significant benefits for households as well as businesses.

for a block of land valued at $200,000, the duty will reduce by 46 per cent. for a dwelling price of $450,000, the duty will decrease by 35 per cent. Commercial property transactions will receive the same benefits under the reform.

all of these benefits will have some offsetting costs including higher UnfT and higher General rates. The exact cost impact will depend on individual householder circumstances. Impacts by suburbs, districts, property values and incomes (as relevant) are provided in the following sections.

The taxation system has a range of concessions and rebates. Those will remain available, and in some cases are being enhanced.

impact of reform

18 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

BusinessesBusinesses will benefit from lower cost pressures because of reduced payroll Tax and the abolition of insurance taxes.

The extension of the payroll Tax free threshold from $1.5 million to $1.75 million from 1 July 2012 will result in the aCT having the lowest payroll taxes in australia for businesses with yearly payrolls up to $4.7 million.

Businesses with a payroll of $2 million, employing around 30 full-time workers, will pay $17,125 less payroll Tax each year. larger businesses will also benefit. from this one measure, cost of doing business in the aCT is expected to fall by $6.8 million in 2012-13. The savings for business will grow each year thereafter.

The abolition of insurance taxes will reduce business costs by $4.6 million in 2012-13. It will continue to substantially reduce business costs until it is fully phased out in 2016-17.

The construction sector, in particular, will benefit from the targeting of the HBCS towards new houses only.

The reform will simplify tax matters for business.

The commercial component of land Tax will be transferred over to the General rates framework, eliminating the need for businesses to pay separate land Taxes.

Duty will no longer be payable on transfers of subleases with a term less than 30 years, a clear nuisance tax on aCT businesses. This will streamline the asset transfer process and reduce business compliance burdens.

Wholesale unit trust schemes are used by national and international investors. provisions affecting wholesale unit trusts have been aligned more closely with those applying in nSW.

impact of reform

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 19

The duty liability threshold has been raised to 50 per cent of landholder property and will reduce the reporting burden. Simplifying landholder provisions will improve the aCT’s attractiveness to large wholesale investors and increase our investment competitiveness.

Business will contribute towards paying for these benefits with increases in Commercial General rates and the UnfT.

first home Buyerseligible first home buyers will have access to a full exemption of conveyance duty for new homes worth up to $385,000. This compares to a maximum concession for homes worth up to $375,000 currently (for both new and established homes).

In addition, the income threshold (at which first home buyer concessions cut out) will be more generous, rising from $120,000 presently to $150,000. The income threshold is even higher for first home buyers with children.

over time, conveyance duty on all homes will be abolished. This will benefit all other first home owners who are not eligible for the current concessional arrangements.

more progressive land Tax on rental homes will encourage the building of more lower-cost homes. That will reduce cost pressures on all lower-cost homes, both rental and owner occupied. That, in turn, will benefit many first home buyers.

rentersmore progressive land Tax on rental homes will encourage the building of more low cost rental homes. This will be of most benefit to renters seeking low-cost stand alone accommodation.

Some renters are unable to access the first home market. The new benefits for first home buyers will encourage some renters into a first home purchase by making first homes more affordable.

more first home buyers and more low-cost homes are expected to reduce pressures on demand for public housing.

impact of reform

20 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

rental investorsoverall, the reform is expected to encourage investment in rental accommodation.

The phasing-out of conveyance duty will lower after-tax costs for rental investors, whether they are aCT residents or live outside the aCT. This is because the ‘loss’ of tax deductibility is worth less than the gain to investors from no longer paying conveyance duty. aCT conveyance duty will continue to be a tax deductible loss until it is eventually phased out.

a more efficient housing market will be relatively more attractive for investors.

rental investors will also benefit from lower cost pressures from the phasing-out of insurance taxes by 1 July 2016.

finally, rental investors will benefit from lower land Tax on low cost rental housing, although more up-market rental housing will face higher land Tax.

impact of reform

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 21

older canberransmany older Canberrans will benefit from the Targeted assistance measures included in the Taxation reform package. Those include:

l the pensioner Duty Concession Scheme;

l General rates rebate;

l General rates Deferral; and

l Duty Deferral Scheme.

In general these measures support ageing in place.

The pensioner Duty Concession Scheme (pDCS) provides concessions on conveyance duty to help eligible pensioners move to accommodation more suited to their needs, such as from a house to a townhouse. The concessional duty of $20 for pensioners will be extended to include a broader range of properties: up to $570,250 for land and improvements and $300,000 for land alone.

The rates Deferral Scheme (rDS) allows pensioners to defer payments of their General rates, on which a relatively low rate of simple interest is charged. This is being expanded to allow people above 65 years satisfying income, assets and equity criteria to defer their rates.

The cap on General rates rebate in the first year will increase from a maximum of $481 to $565. Capped rebate recipients will receive a rebate with a maximum value of 38 per cent of the average General rates bill. Uncapped recipients will continue to receive a 50 per cent rebate.

older Canberrans with more assets will specifically benefit from a number of the other reforms. With home, contents and car assets to protect, the phasing-out of insurance duties will provide many older Canberrans with significant savings. In addition, the phasing-out of conveyance duty will result in lower financial penalties for those wishing to downsize their housing needs in retirement.

impact of reform

22 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

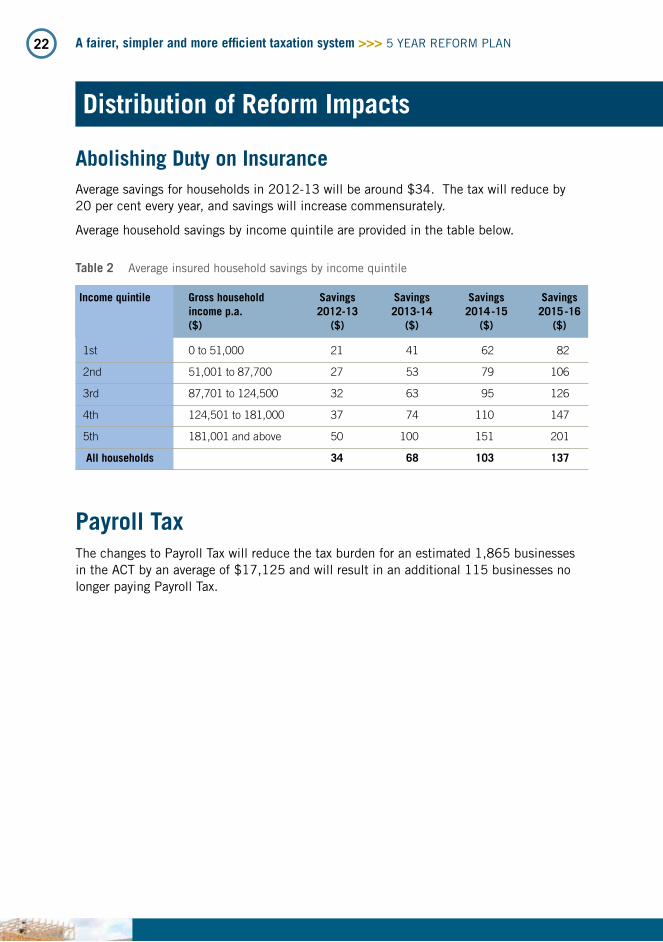

Abolishing Duty on insurance average savings for households in 2012-13 will be around $34. The tax will reduce by 20 per cent every year, and savings will increase commensurately.

average household savings by income quintile are provided in the table below.

Distribution of reform impacts

income quintile Gross household savings savings savings savings income p.a. 2012-13 2013-14 2014 -15 2015 -16 ($) ($) ($) ($) ($)

table 2 average insured household savings by income quintile

1st 0 to 51,000 21 41 62 82

2nd 51,001 to 87,700 27 53 79 106

3rd 87,701 to 124,500 32 63 95 126

4th 124,501 to 181,000 37 74 110 147

5th 181,001 and above 50 100 151 201

All households 34 68 103 137

payroll taxThe changes to payroll Tax will reduce the tax burden for an estimated 1,865 businesses in the aCT by an average of $17,125 and will result in an additional 115 businesses no longer paying payroll Tax.

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 23

phasing out Duty on conveyances The changes to duty on conveyances will reduce the tax payable on properties with a value up to $1.2 million in 2012-13, increasing to $3.6 million in 2016 -17.

In 2012-13 homebuyers will save around 12 per cent on a property valued at $500,000, increasing to 34 per cent in 2016 -17.

property value Duty payable Duty payable savings Duty payable savings current 2012-13 2016 -17 ($’000) ($) ($) (%) ($) (%)

table 3 Impact on property values of phasing out conveyance duty

200 5,500 4,800 13 2,960 46

300 9,500 8,550 10 5,460 43

400 15,000 13,300 11 9,460 37

500 20,500 18,050 12 13,460 34

600 26,250 23,550 10 18,460 30

700 32,000 29,050 9 23,460 27

800 37,750 35,050 7 29,210 23

900 43,500 41,550 5 35,710 18

1,000 49,250 48,050 2 42,210 14

improving progressivity of residential land taxThe adjustments to marginal tax rates will result in the effective tax rate reducing for properties in the first four land value quintiles.

The maximum benefit will be for properties in the fourth land value quintile, which should reduce rental pressures for standalone dwellings around the median property value. for unimproved value of $270,000, the decrease in tax will be around $400.

land Tax will increase for properties with unimproved values in the highest quintile.

land median current land new land Average percentage current new value tax tax change change effective tax effective quintile ($) ($) ($) ($) (%) rate (%) tax (%)

table 4 Impact by land value quintile from changes to land Tax

1st 0 to 92,000 370 364 -6 -1 0.61 0.60

2nd 92,001 to 142,000 832 750 -82 -10 0.70 0.64

3rd 142,001 to 229,000 1,482 1,257 -225 -15 0.81 0.69

4th 229,001 to 320,000 2,567 2,170 -398 -16 0.93 0.79

5th 320,001 and above 5,330 5,655 325 3 1.10 1.15

Distribution of reform impacts

24 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

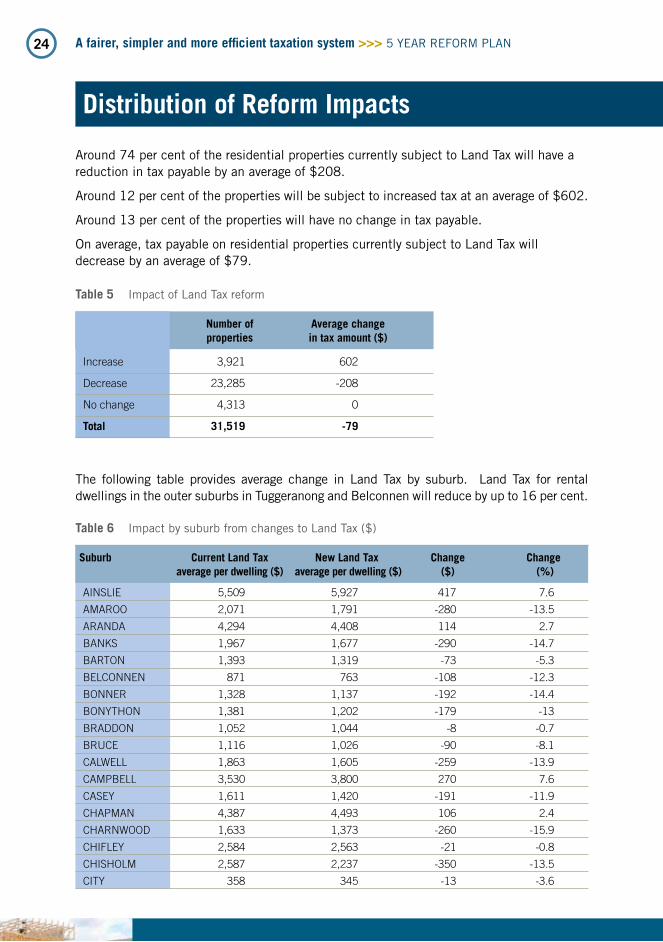

around 74 per cent of the residential properties currently subject to land Tax will have a reduction in tax payable by an average of $208.

around 12 per cent of the properties will be subject to increased tax at an average of $602.

around 13 per cent of the properties will have no change in tax payable.

on average, tax payable on residential properties currently subject to land Tax will decrease by an average of $79.

number of Average change properties in tax amount ($)

table 5 Impact of land Tax reform

Increase 3,921 602

Decrease 23,285 -208

No change 4,313 0

total 31,519 -79

The following table provides average change in land Tax by suburb. land Tax for rental dwellings in the outer suburbs in Tuggeranong and Belconnen will reduce by up to 16 per cent.

table 6 Impact by suburb from changes to land Tax ($)

AINSLIE 5,509 5,927 417 7.6

AMAROO 2,071 1,791 -280 -13.5

ARANDA 4,294 4,408 114 2.7

BANKS 1,967 1,677 -290 -14.7

BARTON 1,393 1,319 -73 -5.3

BELCONNEN 871 763 -108 -12.3

BONNER 1,328 1,137 -192 -14.4

BONYTHON 1,381 1,202 -179 -13

BRADDON 1,052 1,044 -8 -0.7

BRUCE 1,116 1,026 -90 -8.1

CALWELL 1,863 1,605 -259 -13.9

CAMPBELL 3,530 3,800 270 7.6

CASEY 1,611 1,420 -191 -11.9

CHAPMAN 4,387 4,493 106 2.4

CHARNWOOD 1,633 1,373 -260 -15.9

CHIFLEY 2,584 2,563 -21 -0.8

CHISHOLM 2,587 2,237 -350 -13.5

CITY 358 345 -13 -3.6

suburb current land tax new land tax change change average per dwelling ($) average per dwelling ($) ($) (%)

Distribution of reform impacts

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 25

table 6 Impact by suburb from changes to land Tax ($) [ConTInUeD]

CONDER 1,835 1,581 -255 -13.9

COOK 2,527 2,409 -118 -4.7

CRACE 1,565 1,326 -239 -15.3

CURTIN 3,532 3,676 144 4.1

DEAKIN 5,275 5,849 574 10.9

DICKSON 2,856 2,902 46 1.6

DOWNER 3,624 3,622 -2 -0.1

DUFFY 2,843 2,698 -145 -5.1

DUNLOP 1,754 1,491 -263 -15

EVATT 2,234 1,916 -318 -14.2

FADDEN 3,097 2,853 -245 -7.9

FARRER 3,339 3,305 -35 -1

FISHER 2,993 2,773 -220 -7.3

FLOREY 1,977 1,722 -255 -12.9

FLYNN 2,561 2,186 -375 -14.6

FORDE 1,828 1,594 -235 -12.8

FORREST 3,663 4,188 525 14.3

FRANKLIN 1,380 1,169 -211 -15.3

FRASER 2,203 1,878 -325 -14.8

GARRAN 2,534 2,673 139 5.5

GILMORE 2,069 1,765 -304 -14.7

GIRALANG 2,418 2,070 -348 -14.4

GORDON 1,561 1,343 -218 -14

GOWRIE 2,363 1,976 -387 -16.4

GREENWAY 1,017 893 -124 -12.2

GRIFFITH 1,865 1,961 96 5.1

GUNGAHLIN 1,541 1,310 -231 -15

HACKETT 3,176 3,221 45 1.4

HALL 6,191 6,763 571 9.2

HARRISON 2,036 1,720 -316 -15.5

HAWKER 1,693 1,575 -118 -6.9

HIGGINS 2,565 2,196 -369 -14.4

HOLDER 2,356 2,147 -209 -8.9

HOLT 1,321 1,119 -201 -15.2

HUGHES 3,157 3,247 90 2.9

ISAACS 3,277 3,206 -71 -2.2

ISABELLA PLAINS 1,565 1,337 -229 -14.6

KALEEN 2,768 2,497 -271 -9.8

KAMBAH 2,183 1,901 -282 -12.9

KINGSTON 1,260 1,158 -103 -8.1

suburb current land tax new land tax change change average per dwelling ($) average per dwelling ($) ($) (%)

Distribution of reform impacts

26 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

table 6 Impact by suburb from changes to land Tax ($) [ConTInUeD]

LATHAM 2,111 1,760 -351 -16.6

LYNEHAM 1,239 1,213 -27 -2.1

LYONS 2,224 2,241 17 0.8

MACARTHUR 2,468 2,154 -314 -12.7

MACGREGOR 1,605 1,356 -249 -15.5

MACQUARIE 2,420 2,264 -156 -6.4

MAWSON 1,927 1,905 -22 -1.1

MCKELLAR 2,646 2,342 -304 -11.5

MELBA 2,029 1,757 -273 -13.4

MONASH 1,739 1,517 -221 -12.7

NARRABUNDAH 3,548 3,749 201 5.7

NGUNNAWAL 1,374 1,198 -177 -12.9

NICHOLLS 2,109 1,876 -233 -11.1

OAKS ESTATE 882 763 -119 -13.5

O’CONNOR 4,021 4,299 278 6.9

O’MALLEY 7,001 7,835 833 11.9

OXLEY 2,054 1,829 -225 -11

PAGE 2,472 2,240 -231 -9.4

PALMERSTON 1,635 1,402 -234 -14.3

PEARCE 2,874 2,916 42 1.5

PHILLIP 1,033 907 -127 -12.3

PIALLIGO 5,814 6,277 464 8

RED HILL 6,245 7,034 788 12.6

REID 2,515 2,721 206 8.2

RICHARDSON 2,085 1,747 -338 -16.2

RIVETT 2,772 2,473 -299 -10.8

SCULLIN 2,001 1,717 -284 -14.2

SPENCE 2,416 2,050 -367 -15.2

STIRLING 2,005 1,870 -135 -6.7

THARWA 1,889 1,601 -288 -15.3

THEODORE 1,778 1,511 -267 -15

TORRENS 3,497 3,486 -11 -0.3

TURNER 1,459 1,500 41 2.8

WANNIASSA 2,557 2,274 -283 -11.1

WARAMANGA 2,865 2,670 -196 -6.8

WATSON 1,705 1,658 -47 -2.8

WEETANGERA 3,442 3,403 -39 -1.1

WESTON 2,722 2,569 -153 -5.6

YARRALUMLA 6,707 7,511 804 12

Distribution of reform impacts

suburb current land tax new land tax change change average per dwelling ($) average per dwelling ($) ($) (%)

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 27

utilities network facilities taxThe Utilities network facilities Tax (UnfT) rates are being adjusted to reflect growth in land values. The impact of adjustment by income quintile, assuming that utilities passed on the tax to consumers, is provided in the table below.

income quintile Gross household Average increase income p.a. in price p.a. ($) ($)

table 7 Impact in price by income quintile

1st 0 to 51,000 16.17

2nd 51,001 to 87,700 17.73

3rd 87,701 to 124,500 19.63

4th 124,501 to 181,000 18.81

5th 181,001 and above 26.22

All households 22.19

Distribution of reform impacts

28 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

table 8 Change in General rates by aUV quintile

AuV AuV (2012-13) Average General Average General Differencequintile ($) rates (2011-12) ($) rates (2012-13) ($) ($)

1st 0 to 156,000 778 775 -3

2nd 156,001 to 250,000 1,079 1,074 -5

3rd 250,001 to 300,000 1,257 1,279 22

4th 300,001 to 390,000 1,421 1,488 67

5th 390,001 and above 2,036 2,378 342

All properties 1,276 1,399 123

Distribution of reform impacts

changes in General rates

The 24th percentile of properties (AUV of $180,000) will have no

change in rates. Lower value properites will have a rate cut.

chart 8 Cumulative changes in General rates, 2012-13

AuV

perc

entil

e (%

)

The 50th percentile, or median, of properties (AUV of $273,000) will incur an additional $40 in

general rates.

The 80th percentile of properties (AUVof $390,000) will incur an additional $160 in general rates.

residential General ratesGeneral rates will be reformed, with about 24 per cent of properties having a decrease in rates. for all but the most expensive land value quintiles, General rates will fall or rise by less than $67 a year on average. The increase only represents revenue replacement, but does not reflect the benefits to households from reduced taxes on insurance, conveyance duty or payroll Tax.

The increase in General rates is not uniform across all properties. Comparing 2012-13 General rates without reform to 2012-13 General rates with reform shows that around 24 per cent of the properties will have a decrease in their General rates payable.

Table 8 below provides the change in rates by average Unimproved Value (aUV) quintile.

100

40

20

60

80

-$50 $50-0 $100 $150 $300$250$200

100

30

50

70

90

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 29

table 9 General rates impact by suburb

AINSLIE 1,800 2,190 390

AMAROO 1,116 1,195 79

ARANDA 1,607 1,871 264

BANKS 1,132 1,199 67

BARTON 1,115 1,216 102

BELCONNEN 800 842 42

BONNER 1,015 1,013 -2

BONYTHON 1,049 1,095 46

BRADDON 933 1,008 75

BRUCE 1,011 1,066 54

CALWELL 1,144 1,222 78

CAMPBELL 1,842 2,222 380

CASEY 1,017 1,026 9

CHAPMAN 1,650 1,908 258

CHARNWOOD 1,051 1,107 56

CHIFLEY 1,370 1,518 148

CHISHOLM 1,238 1,339 101

CITY 662 686 23

CONDER 1,144 1,207 64

COOK 1,278 1,454 176

CRACE 1,006 1,038 31

CURTIN 1,603 1,889 286

DEAKIN 2,218 2,774 557

DICKSON 1,385 1,607 222

DOWNER 1,464 1,657 192

DUFFY 1,310 1,465 156

DUNLOP 1,068 1,091 23

EVATT 1,225 1,304 79

FADDEN 1,344 1,497 152

FARRER 1,600 1,856 257

FISHER 1,269 1,417 148

The following table provides average change in General rates by suburb.

District General rates General rates Difference (2011-12) ($) (2012-13) ($) ($)

Distribution of reform impacts

30 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

table 9 General rates impact by suburb [ConTInUeD]

District General rates General rates Difference (2011-12) ($) (2012-13) ($) ($)

Distribution of reform impacts

FLOREY 1,184 1,299 114

FLYNN 1,234 1,325 91

FORDE 1,118 1,146 28

FORREST 2,684 3,530 846

FRANKLIN 1,014 1,049 35

FRASER 1,205 1,291 86

GARRAN 1,612 1,934 322

GILMORE 1,185 1,261 76

GIRALANG 1,217 1,302 85

GORDON 1,084 1,140 56

GOWRIE 1,156 1,234 77

GREENWAY 873 907 34

GRIFFITH 1,598 1,897 298

GUNGAHLIN 997 1,060 63

HACKETT 1,507 1,757 250

HALL 1,832 2,207 375

HARRISON 1,092 1,149 57

HAWKER 1,377 1,593 215

HIGGINS 1,213 1,319 105

HOLDER 1,240 1,375 134

HOLT 1,016 1,075 59

HUGHES 1,638 1,952 313

ISAACS 1,432 1,643 212

ISABELLA PLAINS 1,050 1,113 62

KALEEN 1,294 1,403 109

KAMBAH 1,190 1,284 94

KINGSTON 1,008 1,027 20

LATHAM 1,142 1,216 74

LYNEHAM 1,137 1,155 17

LYONS 1,346 1,519 174

MACARTHUR 1,263 1,377 114

MACGREGOR 1,059 1,078 19

MACQUARIE 1,266 1,418 151

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 31

table 9 General rates impact by suburb [ConTInUeD]

District General rates General rates Difference (2011-12) ($) (2012-13) ($) ($)

MAWSON 1,241 1,353 111

MCKELLAR 1,233 1,356 124

MELBA 1,210 1,314 105

MONASH 1,157 1,240 82

NARRABUNDAH 1,607 1,891 283

NGUNNAWAL 976 1,015 39

NICHOLLS 1,234 1,349 115

OAKS ESTATE 957 997 40

O’CONNOR 1,706 2,039 334

O’MALLEY 2,052 2,566 514

OXLEY 1,197 1,298 101

PAGE 1,165 1,267 102

PALMERSTON 1,064 1,128 64

PEARCE 1,449 1,643 194

PHILLIP 858 890 32

PIALLIGO 1,999 2,365 366

RED HILL 2,646 3,408 762

REID 1,686 2,064 378

RICHARDSON 1,136 1,207 71

RIVETT 1,253 1,375 122

SCULLIN 1,149 1,237 88

SPENCE 1,195 1,282 87

STIRLING 1,296 1,411 115

THARWA 1,073 1,086 13

THEODORE 1,106 1,177 71

TORRENS 1,520 1,729 209

TURNER 1,104 1,241 137

WANNIASSA 1,268 1,379 111

WARAMANGA 1,276 1,430 154

WATSON 1,192 1,316 124

WEETANGERA 1,517 1,772 255

WESTON 1,307 1,447 140

YARRALUMLA 2,331 2,879 548

Distribution of reform impacts

32 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

Distribution of reform impacts

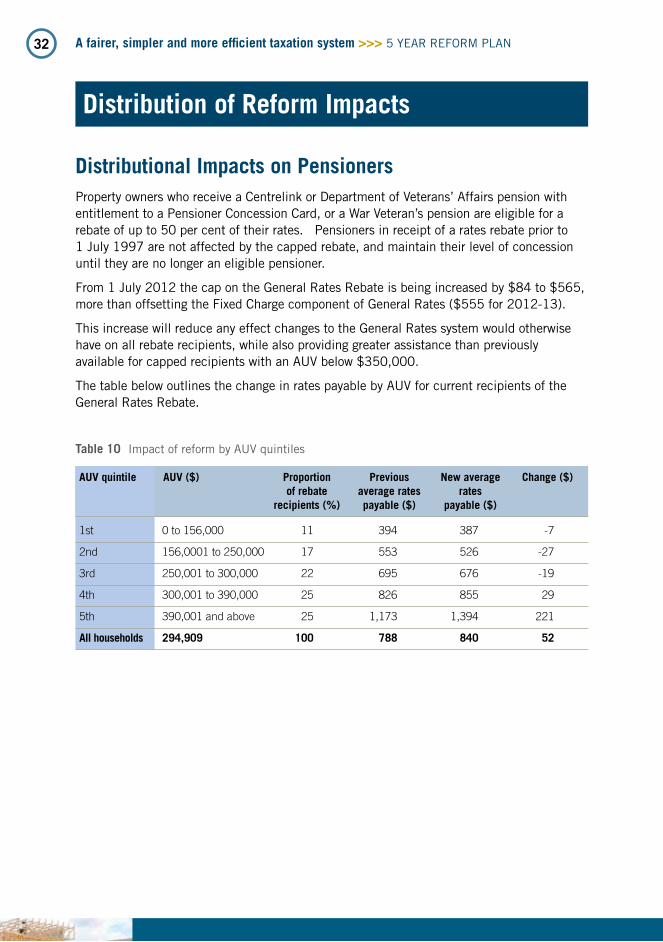

table 10 Impact of reform by aUV quintiles

AuV quintile AuV ($) proportion previous new average change ($) of rebate average rates rates recipients (%) payable ($) payable ($)

1st 0 to 156,000 11 394 387 -7

2nd 156,0001 to 250,000 17 553 526 -27

3rd 250,001 to 300,000 22 695 676 -19

4th 300,001 to 390,000 25 826 855 29

5th 390,001 and above 25 1,173 1,394 221

All households 294,909 100 788 840 52

Distributional impacts on pensionersproperty owners who receive a Centrelink or Department of Veterans’ affairs pension with entitlement to a pensioner Concession Card, or a War Veteran’s pension are eligible for a rebate of up to 50 per cent of their rates. pensioners in receipt of a rates rebate prior to 1 July 1997 are not affected by the capped rebate, and maintain their level of concession until they are no longer an eligible pensioner.

from 1 July 2012 the cap on the General rates rebate is being increased by $84 to $565, more than offsetting the fixed Charge component of General rates ($555 for 2012-13).

This increase will reduce any effect changes to the General rates system would otherwise have on all rebate recipients, while also providing greater assistance than previously available for capped recipients with an aUV below $350,000.

The table below outlines the change in rates payable by aUV for current recipients of the General rates rebate.

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 33

removing Duty on Insurance

abolishing Conveyance Duty

reducing payroll Tax

Improving the progressivity of residential land Tax

abolishing Commercial land Tax

residential General rates

Commercial General rates

Utilities (network facilities) Tax (UnfT)

expanding assistance to Households

individual tax reform measures

34 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

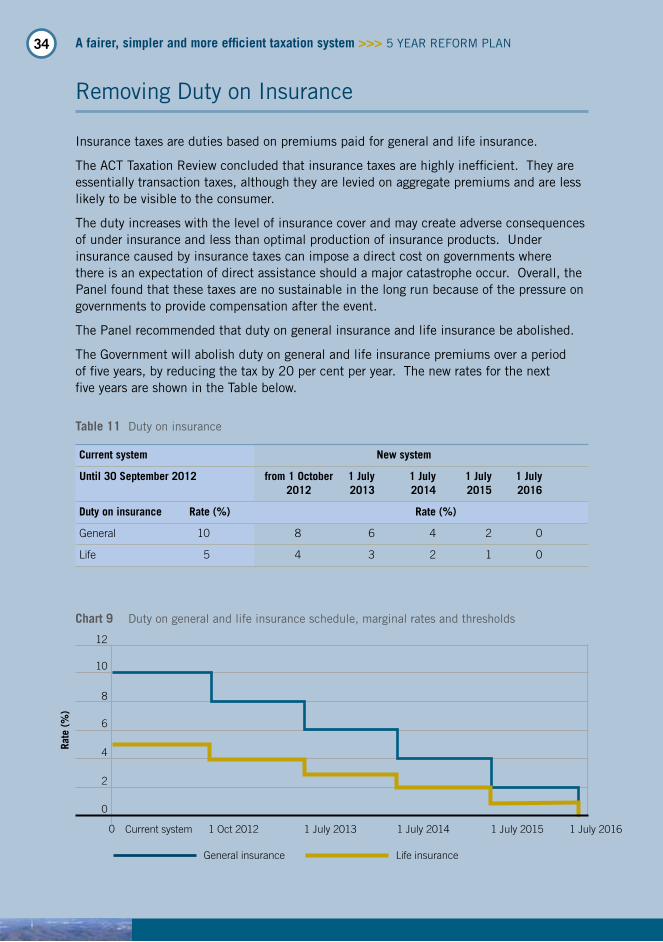

removing Duty on Insurance

Insurance taxes are duties based on premiums paid for general and life insurance.

The aCT Taxation review concluded that insurance taxes are highly inefficient. They are essentially transaction taxes, although they are levied on aggregate premiums and are less likely to be visible to the consumer.

The duty increases with the level of insurance cover and may create adverse consequences of under insurance and less than optimal production of insurance products. Under insurance caused by insurance taxes can impose a direct cost on governments where there is an expectation of direct assistance should a major catastrophe occur. overall, the panel found that these taxes are no sustainable in the long run because of the pressure on governments to provide compensation after the event.

The panel recommended that duty on general insurance and life insurance be abolished.

The Government will abolish duty on general and life insurance premiums over a period of five years, by reducing the tax by 20 per cent per year. The new rates for the next five years are shown in the Table below.

table 11 Duty on insurance

current system new system

until 30 september 2012 from 1 october 1 July 1 July 1 July 1 July 2012 2013 2014 2015 2016

Duty on insurance rate (%) rate (%)

General 10 8 6 4 2 0

Life 5 4 3 2 1 0

chart 9 Duty on general and life insurance schedule, marginal rates and thresholds

rate

(%

)

12

8

4

2

0

General insurance Life insurance

6

10

0 1 Oct 2012 1 July 2013 1 July 2014 1 July 2015 1 July 2016Current system

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 35

To provide Insurance Companies with sufficient time to adapt to these changes, the reduced rates will come into effect from 1 october 2012.

impact on householdsabolishing duty on insurance will reduce the cost of general and life insurance policies for all households and businesses in the aCT.

The savings for aCT households depends on whether they insure and how much they insure. around 68 per cent of aCT households earning up to $51,000 gross annual household income have an insurance policy, compared with almost 100 per cent of the highest income bracket. for average households which insure, the savings will eventually reach $103 per year for those with the lowest income (up to $51,000 per annum), to a maximum of $251 per annum for households in the highest income bracket.

table 12 Insurance tax burden by household income

income Gross household Duty on insurance for households with households with noquintile income p.a ($) those with insurance ($) insurance (%) insurance (%)

1st 0 to 51,000 103 68.4 31.6

2nd 51,001 to 87,700 132 85.5 14.5

3rd 87,701 to 124,500 158 92.3 7.7

4th 124,501 to 181,000 184 93.8 6.2

5th 181,001 and above 251 99.6 0.4

All households 171 87.9 12.1

source Treasury Directorate, australian Bureau of Statistics, 2010 Household Expenditure Survey, Australia: Summary of Results 2009-10, Cat. no. 6530.0, aBS, Canberra and unpublished data from the australian prudential regulation authority, apra; Department of Human Services, Sydney.

Households and businesses with insurance will save 2 per cent on insurance in the first year, increasing to 10 per cent in the final year of reform. for example, an aCT household paying $2,500 per year in insurance will save $50 in the first year of reform, increasing to $250 in the fifth year when insurance duty is abolished.

The savings on a variety of different premium amounts is shown below.

table 13 Savings on insurance premiums

Annual premium paid ($) 2012-13 ($) 2013-14 ($) 2014-15 ($) 2015-16 ($) 2016-17 ($)

1,500 -30 -60 -90 -120 -150

2,000 -40 -80 -120 -160 -200

2,500 -50 -100 -150 -200 -250

3,000 -60 -120 -180 -240 -300

The Independent Competition and regulatory Commission will be tasked with monitoring in the future to ensure that consumers receive the full benefits of the savings.

36 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

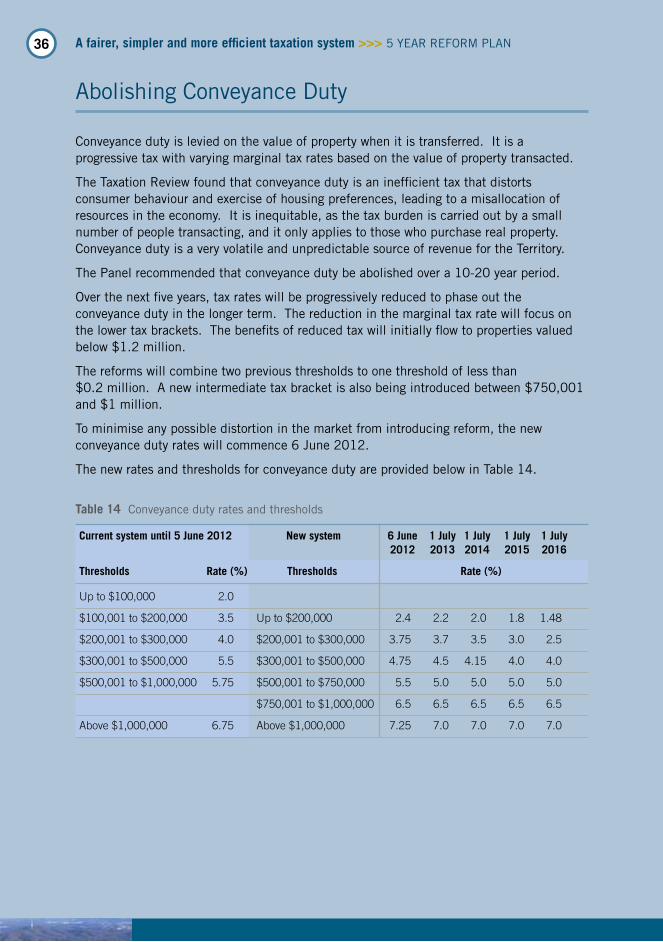

abolishing Conveyance Duty

Conveyance duty is levied on the value of property when it is transferred. It is a progressive tax with varying marginal tax rates based on the value of property transacted.

The Taxation review found that conveyance duty is an inefficient tax that distorts consumer behaviour and exercise of housing preferences, leading to a misallocation of resources in the economy. It is inequitable, as the tax burden is carried out by a small number of people transacting, and it only applies to those who purchase real property. Conveyance duty is a very volatile and unpredictable source of revenue for the Territory.

The panel recommended that conveyance duty be abolished over a 10-20 year period.

over the next five years, tax rates will be progressively reduced to phase out the conveyance duty in the longer term. The reduction in the marginal tax rate will focus on the lower tax brackets. The benefits of reduced tax will initially flow to properties valued below $1.2 million.

The reforms will combine two previous thresholds to one threshold of less than $0.2 million. a new intermediate tax bracket is also being introduced between $750,001 and $1 million.

To minimise any possible distortion in the market from introducing reform, the new conveyance duty rates will commence 6 June 2012.

The new rates and thresholds for conveyance duty are provided below in Table 14.

current system until 5 June 2012 new system 6 June 1 July 1 July 1 July 1 July 2012 2013 2014 2015 2016

thresholds rate (%) thresholds rate (%)

Up to $100,000 2.0

$100,001 to $200,000 3.5 Up to $200,000 2.4 2.2 2.0 1.8 1.48

$200,001 to $300,000 4.0 $200,001 to $300,000 3.75 3.7 3.5 3.0 2.5

$300,001 to $500,000 5.5 $300,001 to $500,000 4.75 4.5 4.15 4.0 4.0

$500,001 to $1,000,000 5.75 $500,001 to $750,000 5.5 5.0 5.0 5.0 5.0

$750,001 to $1,000,000 6.5 6.5 6.5 6.5 6.5

Above $1,000,000 6.75 Above $1,000,000 7.25 7.0 7.0 7.0 7.0

table 14 Conveyance duty rates and thresholds

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 37m

argi

nal t

ax r

ate

(%)

property value ($’ 000)

8

6

5

3

1

0

Current system until 5 June 2012

New system from 6 June 2012

2

4

7

200 400 1,000800600 1,200

New system from 1 July 2016

0

chart 10 Conveyance duty schedule, marginal rates

5

effe

ctiv

e co

nvey

ance

dut

y ra

te (

%)

4

3

2

1

0

0

6

7

200 800 1,200400 600 1,000 1,400

property value ($’ 000)

Current system until 5 June 2012

New system from 6 June 2012

New system from 1 July 2016

chart 11 Comparison of conveyance duty, average rates

impact on householdsThis reform will mean homebuyers will pay less conveyance duty on properties valued up to $1.2 million (increasing to $3.8 million in 2016). These decreases in conveyance duty payable by homebuyers reflect the phased abolition of stamp duty in the aCT over the next 10 to 20 years.

The following Chart shows the benefits received by households from the reforms at a range of property values.

38 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

$300,000 $400,000 $500,000 $600,000 $700,000

$8,540

$7,790

$7,040

$5,540

$4,040

2011-12 from 1 July 2016

price of the property you buy

chart 12 reduction in conveyance duty over a 5 year period

table 15 Comparison of new conveyance duty with the current system

current system until 5 June 2012 6 June 1 July 1 July 1 July 1 July 2012 2013 2014 2015 2016

property value Duty payable Duty payablethresholds ($) ($) ($)

100,000 2,750 2,400 2,200 2,000 1,800 1,480

200,000 5,500 4,800 4,400 4,000 3,600 2,960

300,000 9,500 8,550 8,100 7,500 6,600 5,460

500,000 20,500 18,050 17,100 15,800 14,600 13,460

750,000 34,875 31,800 29,600 28,300 27,100 25,960

1,000,000 49,250 48,050 45,850 44,550 43,350 42,210

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 39

reducing payroll Tax

payroll Tax is imposed on private sector wages and other forms of employee remuneration.

The review panel noted that views on the efficacy of payroll Tax differ. There is evidence that it reduces employment, creates a welfare loss and provides an inefficient method of raising tax. Its efficiency and equity would depend on the circumstances for States. overall, it performs relatively well.

It was recommended that the aCT retain a form of tax on payroll to maintain a diversified tax system and work towards national harmonisation of the system.

The aCT Government is reducing the tax burden for all businesses located in the aCT and encouraging growth of small to medium sized firms. as a first step, the tax-free threshold will be raised from $1.5 million to $1.75 million. The tax rate will be held constant at 6.85 per cent.

The current system and new rates and thresholds for payroll Tax are provided below. The new system will begin from 1 July 2012.

table 16 payroll Tax rates and thresholds

current system until 30 June 2012 new system from 1 July 2012

threshold rate (%) threshold rate (%)

$1,500,000 6.85 $1,750,000 6.85

chart 13 payroll Tax schedule, marginal rates

mar

gina

l tax

rat

e (%

)

Current system until 30 June 2012

New system from 1 July 2012

8

5

3

1

0

4

7

2

6

1 40 2 3 5

size of payroll ($ million p.a)

40 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

impact on Businessall businesses in the Territory will benefit from paying a reduced amount of payroll Tax. around 115 businesses with payrolls between $1.5 million and $1.75 million will no longer have to pay this tax.

These reforms will make the aCT the most competitive state in the country up until $4.7 million. The Chart shows a comparison between nSW and the aCT (before and after the reforms).

chart 14 Comparison of aCT and nSW payroll Tax

300

100

0

ACT new system from 1 July 2012

ACT current system until 30 June 2012

400

600

200

500

size of payroll ($ million p.a)

tax

paya

ble

($’0

00)

1 80 4 62 3 5 7

NSW

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 41

table 17 residential land Tax rates and thresholds

current system until 30 June 2012 new system from 1 July 2012 Average unimproved value rate (%) rate (%)

Up to $ 75,000 0.60 0.60

From $75,001 to $150,000 0.89 0.70

From $150,001 to $275,000 1.15 0.89

$275,001 and above 1.40 1.80

chart 15 residential land Tax schedule, marginal tax rate

mar

gina

l tax

rat

e (%

)

Current system until 30 June 2012

New system from 1 July 2012

2.0

1.2

0.8

0.2

0

1.0

1.8

0.4

1.4

50 2500 150 200 300

AuV ($’000)

chart 16 Comparison of land Tax, effective tax rates

1.0

0.5

0

New system from 1 July 2012

1.5

2.0

AuV ($’000)

effe

ctiv

e la

nd ta

x ra

te (

%)

0 200

Current system until 30 June 2012

0.6

1.6

100 400 600 800

Improving the progressivity of residential land Tax

land tax is applied to all residential properties that are rented, including boarding houses, multiple dwellings, dual occupancies and granny flats.

for the residential sector, land tax is currently applied to a narrow base of rental properties. a broad based land tax is considered to be efficient. The review panel noted that the aCT is in a unique position among States and Territories to have access to a broad based land tax base in General rates.

The Government is making the residential land tax system fairer and more equitable. It will provide significant savings for properties with a land value below $400,000. The tax burden on properties between $80,000 and $400,000 will decrease.

The new rates will commence 1 July 2012.

42 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

impact on householdsUnder the new residential land Tax rates around 76 per cent of properties will receive an average decrease in land tax of $208.

around 12 per cent of properties will incur an average increase of $602. The land Tax burden of the remaining 12 per cent will be unaffected by the changes.

rented properties valued up to $390,000 will receive a reduction in their total land Tax bill. This will help to improve the supply of affordable stand along properties in the rental market. It will also help reduce the pressure on rental prices in the Territory.

$150,000 $200,000 $250,000 $300,000 $350,000

$273

$143

2011-12 from 1 July 2012

investment property AuV

chart 17 average impact on land Tax for aUV values

$403

$368

$168

The following table shows the changes in land Tax payable for a range of properties up to $350,000. for example, a property with an aUV of $300,000 would receive a benefit of $368 on their annual land Tax charge.

table 18 Changes in land Tax by aUV

AuV ($) previous land tax payable ($) new land tax payable ($) Difference ($)

100,000 673 625 -48

200,000 1,693 1,420 -273

300,000 2,905 2,538 -368

350,000 3,605 3,438 -168

400,000 4,305 4,338 33

450,000 5,005 5,238 233

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 43

around 76 per cent of properties will receive a fall in their average land Tax bill.

table 19 average change in land Tax for suburbs under reform

AINSLIE 5,509 5,927 417 7.6

AMAROO 2,071 1,791 -280 -13.5

ARANDA 4,294 4,408 114 2.7

BANKS 1,967 1,677 -290 -14.7

BARTON 1,393 1,319 -73 -5.3

BELCONNEN 871 763 -108 -12.3

BONNER 1,328 1,137 -192 -14.4

BONYTHON 1,381 1,202 -179 -13

BRADDON 1,052 1,044 -8 -0.7

BRUCE 1,116 1,026 -90 -8.1

CALWELL 1,863 1,605 -259 -13.9

CAMPBELL 3,530 3,800 270 7.6

CASEY 1,611 1,420 -191 -11.9

CHAPMAN 4,387 4,493 106 2.4

CHARNWOOD 1,633 1,373 -260 -15.9

CHIFLEY 2,584 2,563 -21 -0.8

CHISHOLM 2,587 2,237 -350 -13.5

CITY 358 345 -13 -3.6

CONDER 1,835 1,581 -255 -13.9

COOK 2,527 2,409 -118 -4.7

CRACE 1,565 1,326 -239 -15.3

CURTIN 3,532 3,676 144 4.1

DEAKIN 5,275 5,849 574 10.9

DICKSON 2,856 2,902 46 1.6

DOWNER 3,624 3,622 -2 -0.1

DUFFY 2,843 2,698 -145 -5.1

DUNLOP 1,754 1,491 -263 -15

EVATT 2,234 1,916 -318 -14.2

FADDEN 3,097 2,853 -245 -7.9

FARRER 3,339 3,305 -35 -1

FISHER 2,993 2,773 -220 -7.3

FLOREY 1,977 1,722 -255 -12.9

FLYNN 2,561 2,186 -375 -14.6

FORDE 1,828 1,594 -235 -12.8

FORREST 3,663 4,188 525 14.3

FRANKLIN 1,380 1,169 -211 -15.3

FRASER 2,203 1,878 -325 -14.8

GARRAN 2,534 2,673 139 5.5

GILMORE 2,069 1,765 -304 -14.7

GIRALANG 2,418 2,070 -348 -14.4

GORDON 1,561 1,343 -218 -14

suburb current land tax new land tax change ($) change (%) average per dwelling average per dwelling ($) ($)

44 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

table 19 average change in land Tax for suburbs under reform [ConTInUeD]

suburb current land tax new land tax change ($) change (%) average per dwelling average per dwelling ($) ($)

GOWRIE 2,363 1,976 -387 -16.4

GREENWAY 1,017 893 -124 -12.2

GRIFFITH 1,865 1,961 96 5.1

GUNGAHLIN 1,541 1,310 -231 -15

HACKETT 3,176 3,221 45 1.4

HALL 6,191 6,763 571 9.2

HARRISON 2,036 1,720 -316 -15.5

HAWKER 1,693 1,575 -118 -6.9

HIGGINS 2,565 2,196 -369 -14.4

HOLDER 2,356 2,147 -209 -8.9

HOLT 1,321 1,119 -201 -15.2

HUGHES 3,157 3,247 90 2.9

ISAACS 3,277 3,206 -71 -2.2

ISABELLA PLAINS 1,565 1,337 -229 -14.6

KALEEN 2,768 2,497 -271 -9.8

KAMBAH 2,183 1,901 -282 -12.9

KINGSTON 1,260 1,158 -103 -8.1

LATHAM 2,111 1,760 -351 -16.6

LYNEHAM 1,239 1,213 -27 -2.1

LYONS 2,224 2,241 17 0.8

MACARTHUR 2,468 2,154 -314 -12.7

MACGREGOR 1,605 1,356 -249 -15.5

MACQUARIE 2,420 2,264 -156 -6.4

MAWSON 1,927 1,905 -22 -1.1

MCKELLAR 2,646 2,342 -304 -11.5

MELBA 2,029 1,757 -273 -13.4

MONASH 1,739 1,517 -221 -12.7

NARRABUNDAH 3,548 3,749 201 5.7

NGUNNAWAL 1,374 1,198 -177 -12.9

NICHOLLS 2,109 1,876 -233 -11.1

OAKS ESTATE 882 763 -119 -13.5

O’CONNOR 4,021 4,299 278 6.9

O’MALLEY 7,001 7,835 833 11.9

OXLEY 2,054 1,829 -225 -11

PAGE 2,472 2,240 -231 -9.4

PALMERSTON 1,635 1,402 -234 -14.3

PEARCE 2,874 2,916 42 1.5

PHILLIP 1,033 907 -127 -12.3

PIALLIGO 5,814 6,277 464 8

RED HILL 6,245 7,034 788 12.6

REID 2,515 2,721 206 8.2

RICHARDSON 2,085 1,747 -338 -16.2

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 45

table 19 average change in land Tax for suburbs under reform [ConTInUeD]

suburb current land tax new land tax change ($) change (%) average per dwelling average per dwelling ($) ($)

RIVETT 2,772 2,473 -299 -10.8

SCULLIN 2,001 1,717 -284 -14.2

SPENCE 2,416 2,050 -367 -15.2

STIRLING 2,005 1,870 -135 -6.7

THARWA 1,889 1,601 -288 -15.3

THEODORE 1,778 1,511 -267 -15

TORRENS 3,497 3,486 -11 -0.3

TURNER 1,459 1,500 41 2.8

WANNIASSA 2,557 2,274 -283 -11.1

WARAMANGA 2,865 2,670 -196 -6.8

WATSON 1,705 1,658 -47 -2.8

WEETANGERA 3,442 3,403 -39 -1.1

WESTON 2,722 2,569 -153 -5.6

YARRALUMLA 6,707 7,511 804 12

46 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

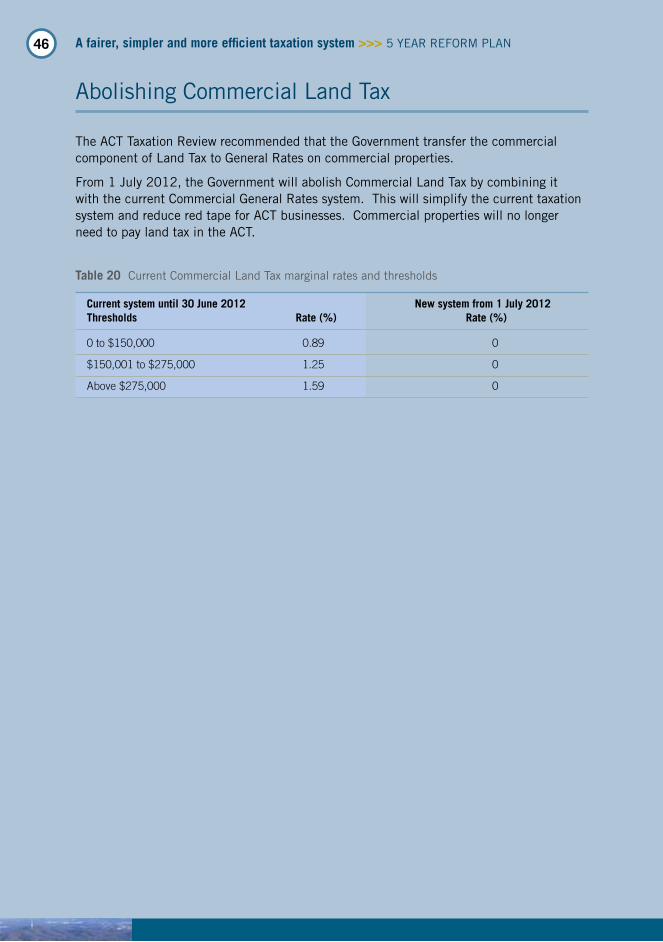

abolishing Commercial land Tax

The aCT Taxation review recommended that the Government transfer the commercial component of land Tax to General rates on commercial properties.

from 1 July 2012, the Government will abolish Commercial land Tax by combining it with the current Commercial General rates system. This will simplify the current taxation system and reduce red tape for aCT businesses. Commercial properties will no longer need to pay land tax in the aCT.

table 20 Current Commercial land Tax marginal rates and thresholds

current system until 30 June 2012 new system from 1 July 2012thresholds rate (%) rate (%)

0 to $150,000 0.89 0

$150,001 to $275,000 1.25 0

Above $275,000 1.59 0

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 47

residential General rates

The aCT Tax review concluded that General rates are an efficient and adequate tax. However, there is considerable scope to improve the rating system, and to establish it as a base for a stable, efficient and fair source of taxation. Improvements could also make the system more coherent to Government’s policy objectives.

effective tax rates are flat, as it is the feature of municipal services cost recovery system. Some progressivity exists because of the land values in the rating formulae.

The aCT Taxation review recommended that General rates be levied through a two-part charge incorporating an element to meet the cost of providing basic city services and a progressive general taxation component contributing to general revenue.

The review panel noted that the aCT is in a unique position among States and Territories to have access to a broad based land tax base in General rates. The Government is adopting General rates as a base for partial revenue replacement.

The progressivity of the General rates system is being improved with the introduction of a number of tax brackets and increasing marginal tax rates.

from 1 July 2012, the new flat fixed charge will be $555 for all households. The current $16,500 aUV threshold is being abolished. four thresholds are being introduced to improve progressivity of the system.

table 21 General rates thresholds and marginal rates

thresholds rate (%)

0 to $150,000 0.2236

$150,001 to $300,000 0.3136

$300,001 to $450,000 0.3736

Above $450,001 0.4136

Fixed charge $555

chart 18 Change in General rates system

rate

(%

)

100

AuV threshold ($’ 000)

200 400 500

0.45

0.40

0.35

0.30

0.25

0.20

300

Current system until 30 June 2012New system from 1 July 2012

48 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

impact on householdsoverall, properties with an aUV below $200,000 will have a decrease in general rates.

around 24 per cent of properties will incur a decrease in rates payable, with 76 per cent incurring an increase. This, however, does not take into account the benefits received by households as a result of other reforms, such as reducing insurance duty.

The increase in rates is not a new charge. General rates on aCT households generally increase each year, in line with increases in the Wage price Index (WpI). However, this plan lowers the General rates bill for almost a quarter of households, and adds modestly to the bill of most other households to accommodate the reduction and removal of other taxes as part of reform measures.

The Government is very mindful of cushioning the impacts of tax reform on lower income households. The aCT Government provides a General rates rebate to eligible households. The maximum rebate available to eligible recipients is being increased from $481 to $565, reflecting the changes to the General rates system.

In addition the current rDS, allowing eligible households to defer payments of their general rates, will be expanded with the introduction of an additional set of standard eligibility criteria on which people can be assessed. The scheme will now be available for those people aged over 65 years; income will be assessed on the lessee’s joint annual income; and an aUV above $390,000 will be introduced. This will help alleviate any additional tax burden incurred as a result of moving to a more progressive General rates system, in which households with a higher aUV will incur an additional increase in General rates.

A fairer, simpler and more efficient taxation system >>> 5 year reform plan 49

Commercial General rates

Commercial General rates will move towards a progressive system. Three thresholds and marginal tax rates are being introduced.

from 1 July 2012, the fixed charge will be $1,213 and the $16,500 aUV threshold will be abolished.

table 22 Commercial General rates

thresholds rating factor fesl rating factor (%) (%)

0 to $150,000 1.9070 0.4093

$150,001 to $275,000 2.2670 0.4093

Above $275,001 2.6070 0.4093

Fixed charge $1,213

These thresholds and tax rates also provide revenue replacement (or transfer) of commercial land Tax. This change will reduce administration costs for business, and simplify the tax system. The transfer is cost neutral for individual businesses.

impact on Businesson average General rates on a commercial property will increase by $1,211 replacing inefficient taxes, such as duty on insurance and conveyance duty. However, most of this revenue replacement is on properties with a value above $560,000. Commercial properties below the average aUV ($129,000) will incur an increase in General rates ranging from $11 to $299.

This table shows the average increase in commercial General rates by aUV decile.

table 23 Commercial General rates payable by aUV decile

AuV deciles AuV current tax neW tax change ($) payable ($) payable ($) ($)

1st 27,046 1,720 1,773 53

2nd 45,189 2,106 2,195 89

3rd 67,787 2,588 2,721 133

4th 94,336 3,153 3,339 186

5th 129,256 3,897 4,151 254

6th 186,333 5,244 5,610 367

7th 329,743 9,002 9,650 649

8th 563,819 15,627 16,736 1,109

9th 973,333 27,218 29,133 1,915

10th 2,300,333 64,779 69,304 4,525

50 A fairer, simpler and more efficient taxation system >>> 5 year reform plan

Utilities network facilities Tax (UnfT)

The Utilities network facilities Tax (UnfT) is applied to the owner of a utility network facility that is installed on, or under land in the aCT.

This includes gas, telecommunication, electricity, water and sewerage network providers.