Embed Size (px)

Citation preview

Report prepared for

US Confectionery Industry Export Program

Australian Confectionery Market

Prepared by

ERU Consulting Group July 2002

Table of Contents 1 Executive Summary..............................................................................................................................1

1.1 Australian Profile .........................................................................................................................1 1.2 The Australian Confectionery Industry........................................................................................1 1.3 Distribution ..................................................................................................................................2 1.4 Trade ............................................................................................................................................2 1.5 Laws and Regulations ..................................................................................................................3 1.6 Customs and Tariffs .....................................................................................................................3 1.7 Conclusion ...................................................................................................................................3

2 Introduction ..........................................................................................................................................5 3 Geography ............................................................................................................................................6

3.1 Climate.........................................................................................................................................7 4 Economy...............................................................................................................................................8

4.1 Trade ............................................................................................................................................8 4.2 Foreign Exchange ......................................................................................................................11 4.3 Domestic Environment ..............................................................................................................11 4.4 Micro Economic Reforms..........................................................................................................12

5 Demographics.....................................................................................................................................13 5.1 Today .........................................................................................................................................13 5.2 Tomorrow ..................................................................................................................................16

6 Infrastructure ......................................................................................................................................18 6.1 Transportation ............................................................................................................................18

7 Industry Profile ...................................................................................................................................21 7.1 History .......................................................................................................................................22 7.2 Chocolate Confectionery ...........................................................................................................23 7.3 Sugar Confectionery ..................................................................................................................25 7.4 Gum ...........................................................................................................................................25 7.5 Industry Characteristics .............................................................................................................26 7.6 Industry Attractiveness ..............................................................................................................28 7.7 Major Players .............................................................................................................................30 7.8 Marketing Strategies of Industry................................................................................................32 7.9 Imports .......................................................................................................................................33

8 Production...........................................................................................................................................37 8.1 Production Trends and Outlook .................................................................................................38

9 Consumption.......................................................................................................................................39 9.1 Competitors in the Snack Category ...........................................................................................40 9.2 Consumer Behaviour .................................................................................................................40 9.3 Demand Determinants ...............................................................................................................41

10 Distribution.........................................................................................................................................43 10.1 Grocery Channel ........................................................................................................................44 10.2 Route Distribution......................................................................................................................44 10.3 Independent Wholesalers ...........................................................................................................45

11 Trade...................................................................................................................................................46 11.1 Confectionery Retail Channels ..................................................................................................46 11.2 Confectionery Retail Trends ......................................................................................................46 11.3 The Australian Grocery Sector ..................................................................................................47 11.4 The Australian Route Trade.......................................................................................................50

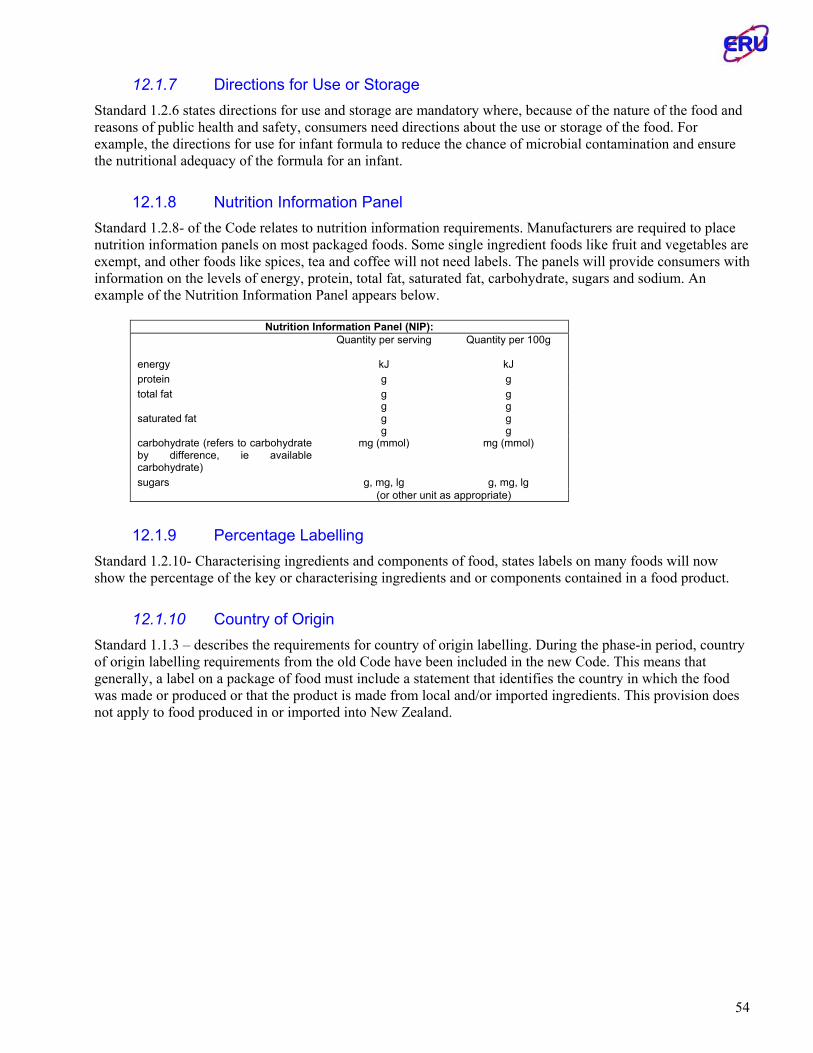

12 Laws and Regulations.........................................................................................................................52 12.1 Food Labelling ...........................................................................................................................52 12.2 Food Additives...........................................................................................................................55 12.3 Processing Aids..........................................................................................................................56 12.4 GM Foods ..................................................................................................................................56

13 Customs and Tariffs............................................................................................................................57

13.1 Import Documentation ...............................................................................................................57 13.2 Customs Valuation System ........................................................................................................58 13.3 Taxation .....................................................................................................................................58 13.4 Rules of Origin...........................................................................................................................58 13.5 Assistance ..................................................................................................................................59 13.6 Government Initiatives...............................................................................................................59 13.7 Imported Food Program.............................................................................................................60

14 Opportunities for US Confectionery...................................................................................................61 14.1 Adult Confectionery...................................................................................................................61 14.2 Children’s and Novelty Confectionery ......................................................................................61 14.3 Packaging Innovations ...............................................................................................................61 14.4 Functional Confectionery...........................................................................................................61 14.5 New Seasonal Opportunities - Halloween .................................................................................62 14.6 Chewing Gum ............................................................................................................................62 14.7 US Product Banner ....................................................................................................................62 14.8 Australia as an Export Base .......................................................................................................62

15 Conclusion ..........................................................................................................................................63 15.1 Barriers and Facilitators to Market Entry ..................................................................................63 15.2 Importance of Distribution.........................................................................................................63 15.3 Branding and Marketing ............................................................................................................64

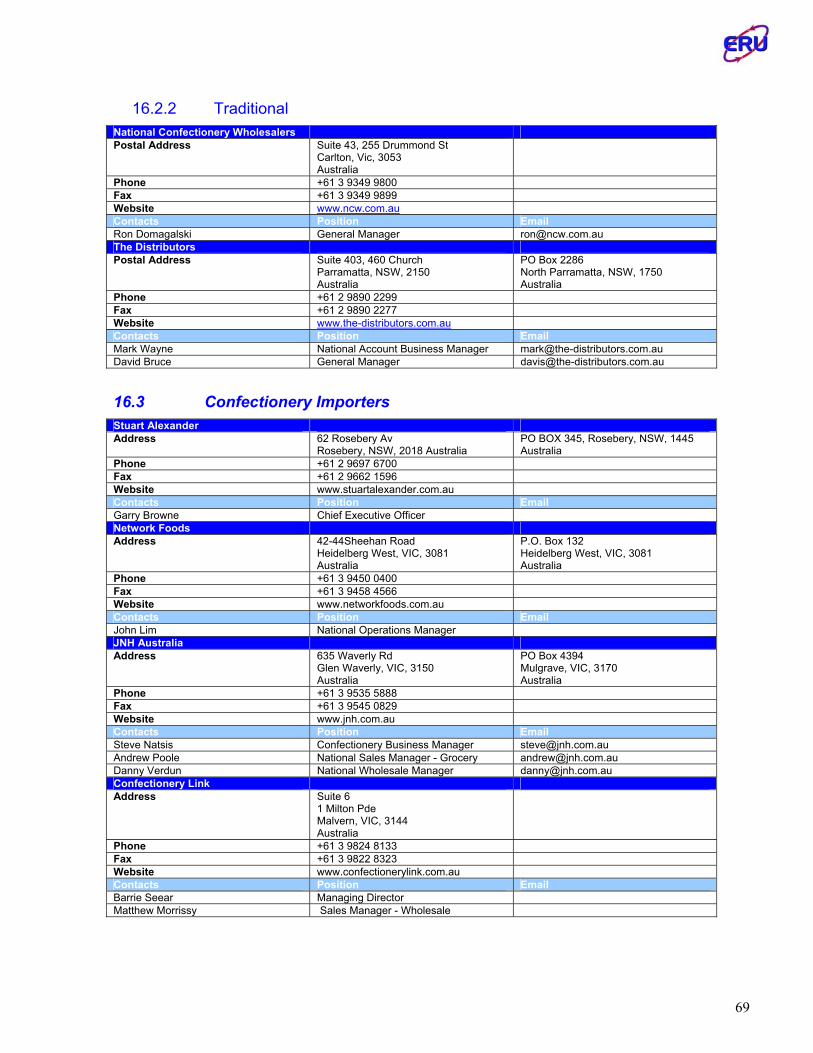

16 Contacts ..............................................................................................................................................65 16.1 Trade ..........................................................................................................................................65 16.2 Distributors ................................................................................................................................68 16.3 Confectionery Importers ............................................................................................................69 16.4 Government Bodies and Industry Associations .........................................................................70

ERU Consulting Group

25-27 Garden Road, Donvale, Victoria, 3111.

Australia.

Phone +61 3 9842 7671 Fax +61 3 9842 8904

Email: [email protected]

1 Executive Summary

1.1 Australian Profile Australia is an island continent in the southern hemisphere roughly the same land mass of the United States. The climate varies from tropical monsoon in the north, and continental in the centre of the country, to temperate in the south. The estimated population of Australia in 2001 was 19.6 million people, with an estimated growth rate of 1.5 to 2% over the next ten years. Soil and climatic conditions have resulted in a heavy concentration of the population residing on the eastern sea border, with 78% of the population residing in New South Wales, Victoria and Queensland. Australia is also heavily urbanised with 70% of people residing in the state’s capital cities National gross domestic product in 2000-01 was A$641.4 billion (US$365.6 bn) which equates to a per capita GDP of A$33,281 (US$18,970). The Australian economy seems to have been relatively immune to the latest global downturn, experiencing a growth rate of around 4% in 2001. Australian trade for 2001 had a total value of A$303.8 billion (US$173.2 bn), exports accounting for A$153.7 billion (US$87.6 bn) and imports accounting for A$150.1 billion (US$85.6 bn), resulting in a surplus of A$3.6 billion (US$2.1 bn). Major trading partners with Australia include; Japan, United States, China, the Republic of Korea and New Zealand. Currently the AUD/USD exchange rate is 57 US cents. Australia has a relatively sophisticated transport infrastructure for all transport mediums, with the dominant mode of freight transport being road, rail plays an important part in transporting bulk freight long distances.

1.2 The Australian Confectionery Industry In 2001, the retail sales value of confectionery in Australia was A$2.53 billion (US$1.44 bn). This represented a 7% increase on the previous year. Chocolate accounts for around 60% of the total confectionery market with the major segments being chocolate bars (43%), blocks (27%), boxed assortments (12%), children’s novelties (7%) and seasonal (mainly Easter moulded – 11%). Sugar confectionery and gum, is estimated at A$838 million (US$477.7 m), accounted for 41% of the confectionery market. The chocolate confectionery business has a seasonal bias towards the colder months of the year and special gift occasions such as Easter, Christmas, Mother's Day and Valentines Day. In Australia, the confectionery market is in a mature phase of its life cycle with long-term volume growth limited to population growth (2-3%). There are some 85 firms producing confectionery in Australia however, the overall confectionery market is dominated by the resident multinational producers Cadbury Schweppes (36%), Nestlé Confectionery (22%) and Mars Confectionery (18%). Total confectionery imports accounted for around A$205 million (US$116.9 m) in 2001. This translates to a retail sales value of around A$420 million (US$239.4 m), some 17% of the national market. Major import suppliers come from New Zealand, United Kingdom, Belgium, Italy, Switzerland, United States and China. There are five different types of confectionery importers who operate in the Australian market;

1. Domicile manufacturers importing from overseas parent/related subsidiaries 2. Supermarkets importing directly 3. Specialised importing agents of international brands 4. Sales/marketing offices of overseas producers 5. Small niche/bulk confectionery import agents

1

Per capita consumption of confectionery is around 10.1 kgs per annum. In 2001, Australians consumed 4kg of sugar products, and 6.1kg of chocolate. In Australia, nine out of ten people consume confectionery regularly, 80% of which consume from both chocolate and sugar confectionery. Most consumers enjoy at least 2 or 3 different confectionery brands per week with heavy chocolate consumers eating on average 7 different brands each week. Confectionery accounts for about 43% of the Australian snack food market. Australians are the fourth largest consumers overall of processed snacking foods. The average Australian household spend is A$800 pa (US$456) on snack foods. However, compared to overseas consumers, Australians eat a wider variety of snack goods.

1.3 Distribution Two broad distribution channels exist in the Australian confectionery market; grocery and traditional. The grocery channel accounts for 61% of confectionery sales with traditional (route) accounting for 39%. Over recent years, more confectionery is being sold through grocery at the expense of route. Confectionery distribution to grocery accounts is direct, with product being dispatched from the manufacturers warehouse to the retailers distribution centre. The past five years has seen the end of State buying functions with the chains’ National office dominant in the purchase decision. Independent wholesalers, who in most cases are aligned to one of two trade groups, supply the route channel. The Distributors accounting for around 60% of route and National Confectionery Wholesalers (NCW) with 32%. Until recently, the independent wholesalers have solely supplied the growing Convenience sector. An emerging trend is the move of some Convenience chains to mirror grocery distribution.

1.4 Trade The grocery sector is highly concentrated and this concentration has been further exacerbated in late 2001 with the exit of the number three supermarket chain, Franklins, from the Australian market. This development leaves the big two, Coles Supermarkets and Woolworths with 70% of the national grocery retail market. Early in 2001, German based Aldi Supermarkets entered the Australian market. Unlike the US market that leans more to ‘every-day pricing’ in grocery, Australia tends to follow the European approach of heavy promotion. Over the last 15 years, the retail chains have earned more and more of their gross margin directly from suppliers. The net result is the margins earned at store level are about 14% very low by world standards. It is estimated that the total trade spend is about A$4 billion (US$2.3 bn), and averages 15% of supplier turnover. On a spend per capita basis it is A$205 p.a (US$ 117). Co-op charges average about 6% at present. Price promotions are endemic in this channel. On average over 70% of all volumes are sold into the chains on a discount. The amount sold out to the consumer would be far less, maybe 25% to 30%. The preference of Australian grocery is to deal directly with the supplier (manufacturer or importer). National confectionery buyers regularly attend the major trade shows around the world (ISM, All Candy etc). The route trade accounts for about A$4 billion (US$2.3 bn) in retail sales with confectionery a considerable contributor at 40% gross margin and 8% of sales. Total route trade confectionery sales in 2001 was A$1 billion (US$ 570 m). Over half of this is chocolate confectionery (56%), sugar confectionery accounted for 34% and gum accounts for the remaining 10%. Once dominated by small family owned corner stores (Ma and Pa stores), this group has been eroded by the emergence of gas and convenience outlets which offer a greater and more competitive proposition to consumers over extended hours and convenient access.

2

Other route channels are also growing, notably vending, cinema and fundraising. A number of companies have also enjoyed some success exploiting non-traditional sales opportunities (hardware stores, hotel liquor outlets, event ‘presence’ sales and on-line bulk sales).

1.5 Laws and Regulations In Australia the production and sale of processed foods are regulated at both Federal and State Government levels. Federal involvement principally arises through its responsibility for developing the Australian Food Standards Code, the setting of imports and export standards, and the inspection of exports and imports. State and local governments are responsible for enforcement of the Code. In the latter half of 1996 the Australian food regulating body joined forces with New Zealand, forming the Australia New Zealand Food Authority (ANZFA). By 2001, the process of developing ‘streamlined’ joint standards was completed, enabling harmonisation of food regulations between both countries. The new Code replaces existing food standards codes and food regulations operating in both Australia and New Zealand in approximately December 2002. Comprehensive labelling requirements are included in Part 1 of the Code. The Code also sets levels for food additives, processing aids, vitamin and mineral nutrients, and the purity of these substances, in foods. No novel, irradiated or genetically modified food is permitted for sale in Australia and New Zealand unless they have passed a pre-market safety assessment by ANZFA.

1.6 Customs and Tariffs All goods imported into Australia must be cleared by customs. Importers are responsible for obtaining a formal customs clearance for consignments of goods above set value limits. Goods entering the country attract customs duties and/or GST levies (10%). The relevant tariff rate for confectionery is 5% but this is reduced to 3% for developing countries and zero for under developed countries. No industry-specific subsidies or grants are available to this industry. The Australian Quarantine and Inspection Service (AQIS) and the Australia New Zealand Food Authority (ANZFA) jointly run the Imported Food Program (IFP), with ANZFA advising on food risk assessment policy and AQIS having operational responsibility for inspection and sampling. AQIS officers carry out inspections of food, and standards applied are set down in the Australian Food Standards Code (FSC). Food imported into Australia falls into one of three inspection categories, which determine the frequency of freight inspections. The three categories are risk, active surveillance and random surveillance. On the whole confectionery products are generally classified as low risk and are therefore subject to random inspections.

1.7 Conclusion US culture is readily accepted in Australia. With few exceptions, US licensed products sell well. Hollywood movies and American music dominate the local scene. The Australian palate, however, is different. From a confectionery standpoint, it is closer to the taste and preferences of Britain. This is particularly true of chocolate. US chocolate is coarser, bittersweet and not well received in Australia. Sour tasting sugar candy is also markedly less developed as a segment when compared with the US. However there are several identified opportunities for US confectionery including;

• Adult Confectionery • Children’s and Novelty Confectionery • Packaging Innovations • Functional Products • New Seasonal Opportunities – Halloween • Chewing Gum • US Product Banner • Australia as an Export Base

3

In developing a market entry strategy, US manufacturers should bear in mind the relatively small total market size, extent of confectionery manufacturer and brand concentration, price competitive nature of the market and the high levels of concentration of retail trade outlets. Advertising and promotional commitment is fundamental to facilitate broad based consumer trial. To obtain a substantial share of the Australian confectionery market, a wide distribution network is essential because of the impulse nature of confectionery purchase decisions. The fact that grocery retail (and for that matter, route retail) is highly concentrated, this allows fairy straightforward access to the entirety of the national market. Operational model options include; to operate either through an appointed local agent, or alternatively, establish their own local sales and marketing office. Smaller firms may consider forming a network with other manufacturers in order to share the costs associated with market entry, perhaps through a cross-branded strategy. Niche product specialists can take advantage of either direct supply or through a number of specialised local import agents.

4

2 Introduction This report has been prepared for the National Confectioners Association under a research engagement conducted by ERU Consulting Group for the US Confectionery Industry Export Program (USCIEP). The primary purpose of the research program was to provide US confectionery manufacturers and marketers with the market information necessary for making informed decisions regarding market opportunities in Australia for their products. In addition the research provides contact information, which will enable interested parties to immediately begin inquiries with appropriate distributors. Research findings will be shared with all interested US confectionery manufacturers and other interested parties. Based on the above considerations, the objective of the research has been specified: "to develop qualitative and quantitative intelligence on the Australian Confectionery Market, its distribution

channels and to produce alternative market entry strategies and a market contact base" The research engagement was commissioned on 10 May, 2002, the background research and trade interviews where conducted during May - June 2002 with the bulk of the report being written in late June. The scope of the engagement requirements has been reflected in the section headings of this report. A wide range of confectionery industry published information sources were reviewed during the research engagement and was supplemented by direct market and industry surveys consisting of interviews with manufacturers, importers/exporters, wholesalers, distributors, retailers from all categories and industry trade organisations involving some 40 persons covering major Australian capital cities. The report that follows has involved the collation and analysis of these different data and information sources into a composite and integrated market analysis. A detailed list of key industry contacts has been provided in chapter 16, laws and regulations in relation to the importation of confectionery into Australia and a selection of relevant reports and documents have been included on the CD Rom version of this report, these provide valuable information about the specifics of food regulations and import laws. Note: All currency conversions contained within this report were calculated based on an exchange rate of A$1:US$0.75.

5

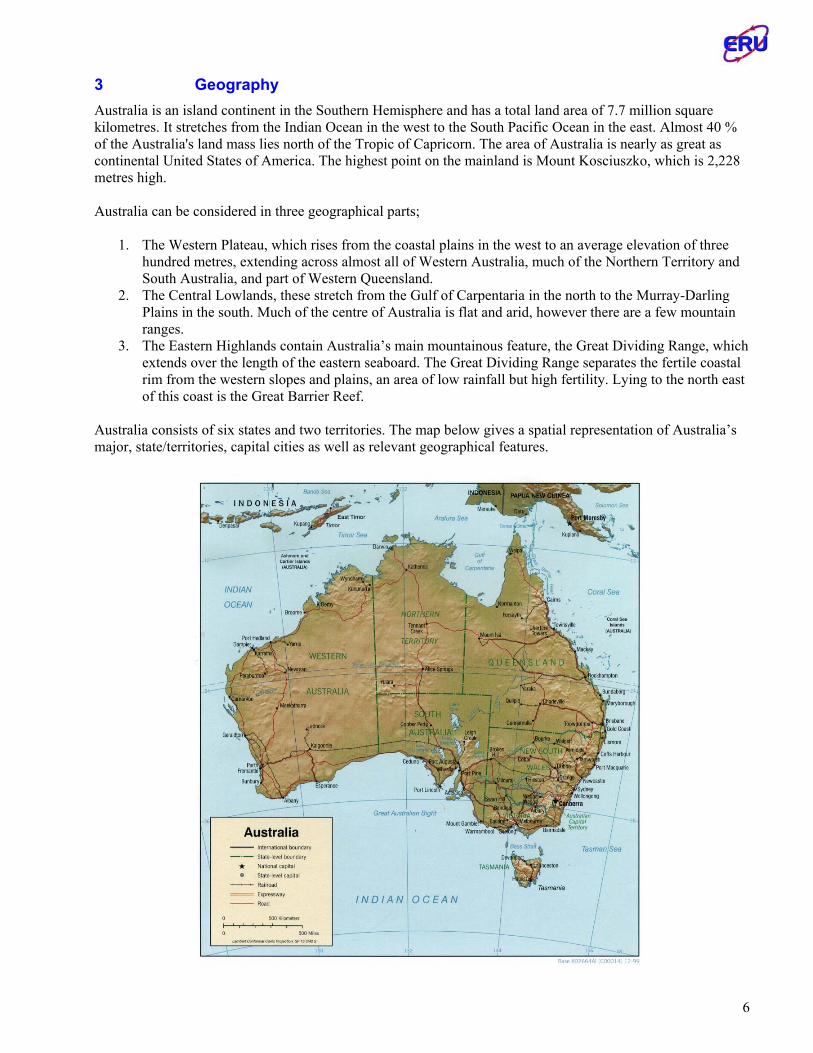

3 Geography Australia is an island continent in the Southern Hemisphere and has a total land area of 7.7 million square kilometres. It stretches from the Indian Ocean in the west to the South Pacific Ocean in the east. Almost 40 % of the Australia's land mass lies north of the Tropic of Capricorn. The area of Australia is nearly as great as continental United States of America. The highest point on the mainland is Mount Kosciuszko, which is 2,228 metres high. Australia can be considered in three geographical parts;

1. The Western Plateau, which rises from the coastal plains in the west to an average elevation of three hundred metres, extending across almost all of Western Australia, much of the Northern Territory and South Australia, and part of Western Queensland.

2. The Central Lowlands, these stretch from the Gulf of Carpentaria in the north to the Murray-Darling Plains in the south. Much of the centre of Australia is flat and arid, however there are a few mountain ranges.

3. The Eastern Highlands contain Australia’s main mountainous feature, the Great Dividing Range, which extends over the length of the eastern seaboard. The Great Dividing Range separates the fertile coastal rim from the western slopes and plains, an area of low rainfall but high fertility. Lying to the north east of this coast is the Great Barrier Reef.

Australia consists of six states and two territories. The map below gives a spatial representation of Australia’s major, state/territories, capital cities as well as relevant geographical features.

6

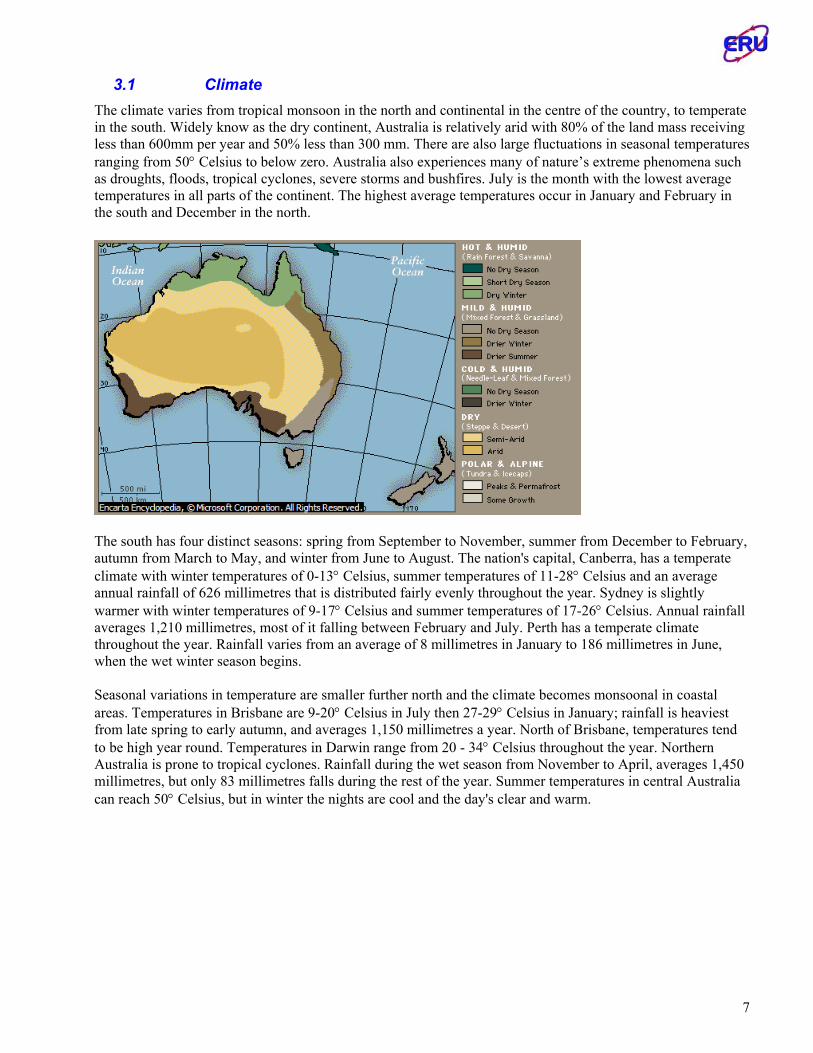

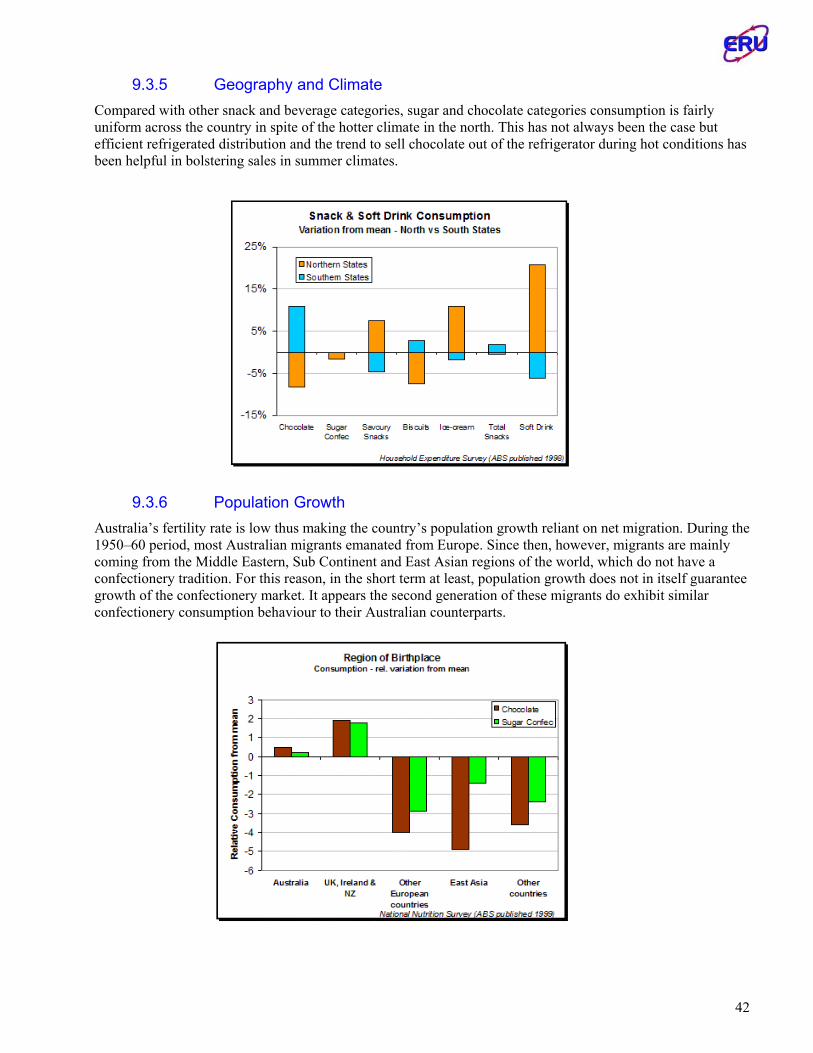

3.1 Climate The climate varies from tropical monsoon in the north and continental in the centre of the country, to temperate in the south. Widely know as the dry continent, Australia is relatively arid with 80% of the land mass receiving less than 600mm per year and 50% less than 300 mm. There are also large fluctuations in seasonal temperatures ranging from 50° Celsius to below zero. Australia also experiences many of nature’s extreme phenomena such as droughts, floods, tropical cyclones, severe storms and bushfires. July is the month with the lowest average temperatures in all parts of the continent. The highest average temperatures occur in January and February in the south and December in the north.

The south has four distinct seasons: spring from September to November, summer from December to February, autumn from March to May, and winter from June to August. The nation's capital, Canberra, has a temperate climate with winter temperatures of 0-13° Celsius, summer temperatures of 11-28° Celsius and an average annual rainfall of 626 millimetres that is distributed fairly evenly throughout the year. Sydney is slightly warmer with winter temperatures of 9-17° Celsius and summer temperatures of 17-26° Celsius. Annual rainfall averages 1,210 millimetres, most of it falling between February and July. Perth has a temperate climate throughout the year. Rainfall varies from an average of 8 millimetres in January to 186 millimetres in June, when the wet winter season begins. Seasonal variations in temperature are smaller further north and the climate becomes monsoonal in coastal areas. Temperatures in Brisbane are 9-20° Celsius in July then 27-29° Celsius in January; rainfall is heaviest from late spring to early autumn, and averages 1,150 millimetres a year. North of Brisbane, temperatures tend to be high year round. Temperatures in Darwin range from 20 - 34° Celsius throughout the year. Northern Australia is prone to tropical cyclones. Rainfall during the wet season from November to April, averages 1,450 millimetres, but only 83 millimetres falls during the rest of the year. Summer temperatures in central Australia can reach 50° Celsius, but in winter the nights are cool and the day's clear and warm.

7

4 Economy “Australia is the lucky country; yet its recent performance is more than a one-year wonder. Over the past ten years, Australia has enjoyed the fastest growth rate of any big developed economy. A series of reforms over the past two decades--from financial deregulation and reduced import barriers to the overhaul of taxes and labour relations--has made the economy much more competitive. Good policy has counted for more than good luck.” The Economist 6/04/2002

Australia is a market based economy and a member of the OECD. Gross domestic product (GDP) in 2000-01 was A$641.4 billion (US$365.5 bn) which equates to a per capita GDP of A$33,281 (US$18,970). Australia is one of the few industrialized economies that has been relatively unaffected by the latest global downturn, experiencing a growth rate of around 4% in 2001. That is not to say that it has not been unaffected. Export growth in 2000 was in the order of 25-30% in 2001 it was only 9%. This resilience has been due broadly to three factors. Firstly the Australian dollar has been weak which has made manufacturers highly competitive and has boosted exports. Second demand has been propped up by a boom in the housing sector. Finally, Australia has been relatively immune to the crash in the IT sector, which accounts for 15% of GDP compared to 45% in the US. Assuming that the global economy growth improves in the later part of 2002 market analysts expect to see growth sustained at a robust pace of 3.75 - 4% over the next financial year. The most critical domestic issue is the timing and the extent of the swing in activity from housing to business investment. Recent business surveys do indicate there is a significant recovery in business investment intentions but firmer evidence of a global recovery is needed before these are realized. Private consumption is set to remain strong with the improving labour market and lagged effects of increases in household wealth offsetting the impact of rising interest rates.

4.1 Trade The total value of trade in goods and services in 2001 was A$303.8 billion (US$173.2 bn), a 5% increase on the previous year, which is slightly lower than the five year average growth of 8%. Exports grew by 8% to A$153.7 billion (US$87.6 bn), the result of a 1% increase in export volumes and a 7% rise in prices received for exports. Imports increased by 1% to A$150.1 billion (US$85.6 bn), a result of a 6% increase in prices and a 4% decrease in volume. This result put the trade balance in a surplus of A$3.6 billion (US$2.1 bn), a turnaround of A$9.7 billion (US$5.5 bn) from it’s 2000 deficit of A$6.1 billion (US$3.5 bn). Merchandise trade recorded a surplus of A$4.8 billion (US$2.7 bn) while the trade in services recorded a deficit of A$1.2 billion (US$680 m) for 2001.

Australian Exports 2001

47%

8%17%

8%

20%

Primary Products Simply Transformed ManufacturersElaborately Transformed Manufacturers Other MerchandiseServices

Source: Australian Department of Foreign Affairs and Trade

8

Australian exports for the last five years have been growing at an average annual rate of 9% fuelled by the low value of the Australian dollar and the strong domestic economy. Nearly half of all exports are primary products, manufactured goods account for 25% simply transformed manufactures (STM) and elaborately transformed manufactures (ETM), services account for a further 20% and other merchandise accounts for 8%. The growth in exports during 2001 was a result of exports of primary products increasing by 12%, manufacturing exports growing by 8%, other merchandise exports growing by 18% and a fall in service exports of 2%. The chart on the previous shows a category breakdown of Australian exports.

Australian Imports 2001

12%8%

56%

1%

23%

Primary Products Simply Transformed ManufacturersElaborately Transformed Manufacturers Other MerchandiseServices

Source: Australian Department of Foreign Affairs and Trade During the last five years imports have been growing at an average rate of 9% pa. Nearly two thirds of Australian imports are manufactured goods, followed by services accounting for 23% and the remainder is made up of other merchandise trade. Major category changes to imports for 2001 included a 4% increase in manufacturing imports, a 21% increase in other merchandise imports and a 4% increase in service imports. The chart above shows a category breakdown of Australian imports.

4.1.1 Merchandise Trade In terms of global merchandise trade Australia is a small player accounting for 1.1% of global merchandise trade in 2000. Given this, Australia is predominantly a price taker (must except the market price) except for a few commodities of which it is a major global producer. Merchandise trade for 2001 was A$240.3 billion an increase of 6% on the previous year. Exports accounted for A$122.5 billion an 11% rise and imports accounted for A$117.7 billion an increase of 1%. Australia’s top five export categories include;

1. Coal at A$12.5 billion (10% of exports). 2. Crude Petroleum at A$ 6.5 billion (5% of exports). 3. Iron Ore at A$5.2 billion (4% of exports). 4. Non-monetary gold at A$5.2 billion (4% of exports). 5. Aluminium at A$4.7 billion (4% of exports).

Australia’s top five imports categories include;

1. Passenger Motor Vehicles at A$8.7 billion (7% of imports). 2. Crude Petroleum at A$7.7 billion (7% of imports).. 3. Telecommunications Equipment at A$5 billion (4% of imports). 4. Computers at A$4.8 billion (4% of imports). 5. Medicaments (including veterinary) at A$3.6 billion (3% of imports).

9

4.1.2 Distribution of Trade Members of the Asian Pacific Economic Community remain Australia’s largest regional trading group representing A$170.6 billion, 71% of total trade. Australia’s trade is spread across the following regions.

• North Asia accounts for A$85.1 billion or 35% of total trade. Exports account for A$50.4 billion and imports were A$34.7 billion leaving a surplus of A$15.7 billion.

• South East Asia accounts for A$32.9 billion or 14% of total trade. Exports account for A$15.4 billion and imports were A$17.5 billion leaving a deficit of A$2.1 billion.

• European Union accounts for A$41.2 billion or 17% of total trade. Exports account for A$14.7 billion and imports were A$26.5 billion leaving a deficit of A$11.7 billion.

• The Americas accounts for A$40 billion or 17% of total trade. Exports account for A$15.2 billion and imports were A$24.8 billion leaving a deficit of A$9.6 billion.

• Oceania accounts for A$16.1 billion or 7% of total trade. Exports account for A$9.7 billion and imports were A$6.4 billion leaving a surplus of A$3.3 billion.

Australian Trade 2001

40%

15%19%

19%

7%

North Asia South East Asia European Union Americas Oceania

Source: Australian Department of Foreign Affairs and Trade Australia’s top five individual trading partners are as follows;

1. Japan accounted for A$39 billion in trade during 2001 representing 16% of total trade. 2. United States accounted for A$33.3 billion in trade during 2001 representing 14% of total trade. 3. China accounted for A$17.9 billion in trade during 2001 representing 7% of total trade. 4. Republic of Korea accounted for A$14.2 billion in trade during 2001 representing 6% of total trade. 5. New Zealand accounted for A$11.9 billion in trade during 2001 representing 5% of total trade.

4.1.3 Trade Priorities Australia has a strong interest in the removal of barriers to investment and trade with the government’s stated priorities being:

• Domestic reform. • Improving bilateral relations. • Improving the regional framework for trade. • Strengthening the international trading system. • Promoting exports.

10

4.2 Foreign Exchange The AUD/USD exchange rate is currently around 57 US cents to A$1. Recently the Australian dollar has been appreciating which is a result of reducing risk aversion, some weakening of the US dollar and an improvement in fundaments (commodity prices, interest rate differentials and relative equity market returns). Further appreciation is expected with the rate topping 57 – 60 US cents in early 2003. However these gains will be progressively eroded as the US economy growth accelerates and as interest rate differentials and relative equity returns advantages are reduced. As the US economy improves so will the pace of capital inflows into the US, which will result in a depreciation of the Australian dollar to around the 55 US cents at the end of 2003.

4.3 Domestic Environment The Australian economy is set for robust growth during the next two years in respect to other economies around the globe. Analysts are predicting that consumer demand will continue to grow until the latter half of 2002 and early 2003 when the downturn in housing occurs as a result of the ending of the governments’ first home buyer scheme and increasing interest rates. Australian businesses’ balance sheets are in a healthy position given the solid growth in profits over the last year. Growth in household consumption is expected to remain strong, fuelled by increased household wealth and low debt servicing.

4.3.1 Fiscal Management "Monetary and fiscal policies have a medium-term orientation, with emphasis on price stability and a sound budgetary position …The fiscal policy framework aims at maintaining a balanced budget, on average, over the business cycle." Steven Hess, Moody’s 9/01/2002

The federal budget for 2001-02 has an estimated deficit of A$3 billion, which is largely a result of higher expenditure on defence, border protection and the first home buyers scheme. Prospects for 2002-03 bring the budget back into a surplus of A$2.1 billion. Recently sound fiscal management and monetary policy has left government finances in a healthy position. Since 1997 the government’s net debt has fallen from A$82.9 billion to A$39.3 billion. This brings Australia’s debt position well below the OECD average. Although the most recent budget is more about delivering election promises than sound fiscal management. Expenditure is relatively unchanged from the previous year at A$170.2 billion. Revenues are expected to grow by 1.8% in real terms during 2002-03 to A$169.6 billion.

4.3.2 Labour Market Despite the strong Australian economy, employment growth has remained sluggish over 2001. Heightened uncertainty surrounding the events of September 11 has delayed employment recovery, although strong activity during the latter half of 2001 is now flowing through and producing substantial employment opportunities. This is evidenced through unemployment dropping to 6.3% and an increase in the number of advertised positions. Further gains are expected in future quarters and unemployment is expected to stabilise at 6% by 2003. Due to the weak labour market in 2001 wage pressures were contained. However as employment grows, there are likely to be some pressures on wages.

4.3.3 Inflation The Reserve Bank of Australia (RBA) has set tight inflation targets for the Australian economy between 2-3%. Inflation has picked up in 2001 at about 3.5% due largely to a pass-through of a weaker currency. Inflation is forecast at 2.5% for 2002 as a result of increases in import prices and a strengthening Australian currency, coupled with moderate unit labour costs. The RBA’s official cash rates are currently 4.75%, with the bank signalling that it intends to restore rates to more neutral levels, which analysts believe are around 5.5%.

11

4.4 Micro Economic Reforms The Australian government has put in place many structural reforms in the last decade to improve the competitiveness and performance of the Australian economy. Some of the major reforms include;

• The restructuring of the labour market away from centralised wage fixing to enterprise bargaining. This has resulted in a more flexible and productive workforce.

• Reductions in tariffs and other microeconomic reforms have helped grow Australia’s export base through creating greater competitiveness and opening up new business opportunities.

• Australia introduced a new taxation system in July 2000 the Goods and Services Tax (GST), which lowered income tax, wholesale sales tax and thus reducing the complexity of the old system.

• Deregulation of the banking, communications and energy sectors, opening up these markets to greater competition.

• Strong corporate regulation and insolvency regimes which are business orientated.

12

5 Demographics

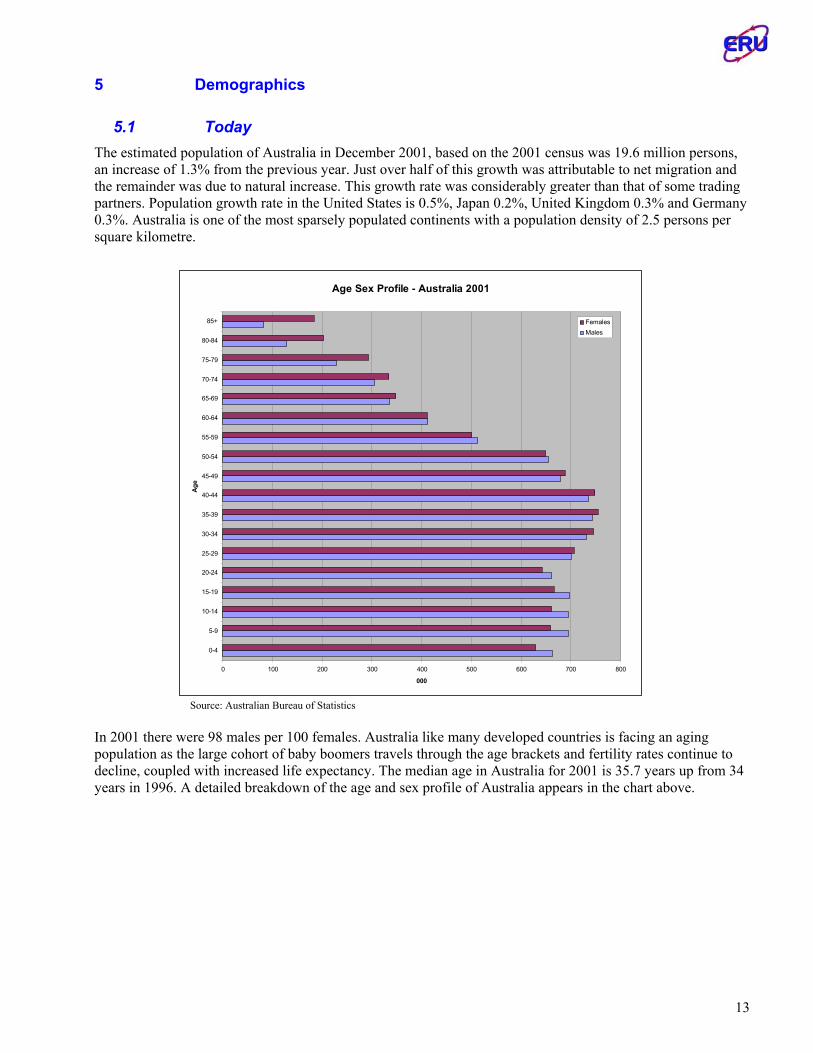

5.1 Today The estimated population of Australia in December 2001, based on the 2001 census was 19.6 million persons, an increase of 1.3% from the previous year. Just over half of this growth was attributable to net migration and the remainder was due to natural increase. This growth rate was considerably greater than that of some trading partners. Population growth rate in the United States is 0.5%, Japan 0.2%, United Kingdom 0.3% and Germany 0.3%. Australia is one of the most sparsely populated continents with a population density of 2.5 persons per square kilometre.

Age Sex Profile - Australia 2001

0 100 200 300 400 500 600 700 800

0-4

5-9

10-14

15-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

70-74

75-79

80-84

85+

Age

000

FemalesMales

Source: Australian Bureau of Statistics In 2001 there were 98 males per 100 females. Australia like many developed countries is facing an aging population as the large cohort of baby boomers travels through the age brackets and fertility rates continue to decline, coupled with increased life expectancy. The median age in Australia for 2001 is 35.7 years up from 34 years in 1996. A detailed breakdown of the age and sex profile of Australia appears in the chart above.

13

Soil and climatic conditions have been controlling factors in the concentration of population in the well-watered, fertile coastal regions of the east, southeast, and southwest. The largest populated of these regions is the south east and east. Within these coastal regions population is concentrated in urban centres particularly capital cities. To put this in perspective the most densely populated 1% of the continent contains 84% of the population. The map below shows the spatial distribution of Australia’s population.

The majority of Australia’s population (78%) resides in three states, New South Wales, Victoria and Queensland, all located on Australia’s south eastern sea border. The largest of these, New South Wales, accounts for one third of the nation’s population. The table below indicates the geographical spread of Australia’s population by states and territories.

State Population % of Population Median Age millions

New South Wales 6.6 34% 35.7 Victoria 4.9 25% 35.5 Queensland 3.7 19% 34.9 South Australia 1.5 8% 37.4 Western Australia 1.9 10% 34.5 Tasmania 0.5 3% 37.0 Northern Territory 0.2 1% 29.3 Australian Capital Territory 0.3 2% 32.9 Total 19.6 100%

Source: Australian Bureau of Statistics

14

With more than 70% of Australians live in the metropolitan areas of the capital cities of the six states, the country is highly urbanized. Less than 14% of the population live in rural areas. By far the largest two cities are Sydney and Melbourne, the state capitals of New South Wales and Victoria, together accounting for 39% of the population. The table below outlines the geographical spread of Australia’s population by major capital cities and principle metropolitan centres.

Population 2001 % of Population % of States Population

millions New South Wales Sydney 4.1 20.9% 62%

Newcastle 0.5 2.6% 8% Wollongong 0.3 1.5% 5%

Victoria Melbourne 3.5 17.9% 71%

Geelong 0.2 1.0% 4% Queensland Brisbane 1.7 8.7% 46%

Gold Coast 0.4 2.0% 11% South Australia Adelaide 1.1 5.6% 73% Western Australia Perth 1.4 7.1% 74% Tasmania Hobart 0.2 1.0% 40%

Launceston 0.1 0.5% 20% Northern Territory Darwin 0.1 0.5% 50% Australian Capital Territory Canberra 0.3 1.5% 100%

Total 13.9 70.9% Source: Australian Bureau of Statistics

Australia is a tolerant and inclusive society, a nation built by people from diverse backgrounds. Cultural diversity is a cornerstone in the national identity. Net migration plays an important part in the make up of Australia’s population and in the last five years net migration has added half a million people to Australia’s population (3% of total population). Most of the population of Australia is of European descent, Australian aborigines account for about 1% of the total population. Before World War II (1939-1945) the population was almost entirely of British origin, but since then more than 2 million continental Europeans have migrated to Australia. In the 1970s, after the removal of the White Australia Policy, tens of thousands of Southeast Asians were admitted to the country, mainly as refugees. The table below gives a breakdown of the Australian population by their region of birth.

Population 2000 % of Population millions

Oceania and Antarctica 15.1 78.6% Europe and former USSR 2.4 12.5% Middle East and North Africa 0.2 1.0% Southeast Asia 0.6 3.1% Northeast Asia 0.3 1.6% Southern Asia 0.2 1.0% The Americas 0.2 1.0% Other Africa 0.2 1.0%

Total 19.2 Source: Australian Bureau of Statistics

15

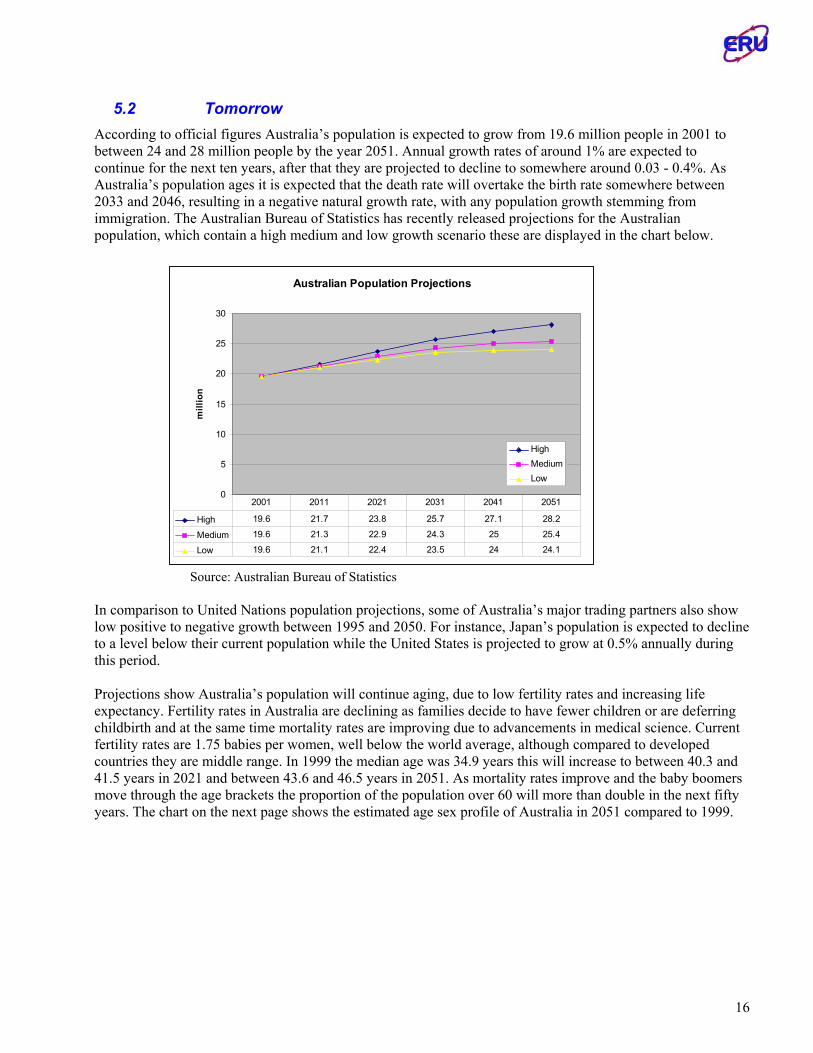

5.2 Tomorrow According to official figures Australia’s population is expected to grow from 19.6 million people in 2001 to between 24 and 28 million people by the year 2051. Annual growth rates of around 1% are expected to continue for the next ten years, after that they are projected to decline to somewhere around 0.03 - 0.4%. As Australia’s population ages it is expected that the death rate will overtake the birth rate somewhere between 2033 and 2046, resulting in a negative natural growth rate, with any population growth stemming from immigration. The Australian Bureau of Statistics has recently released projections for the Australian population, which contain a high medium and low growth scenario these are displayed in the chart below.

Australian Population Projections

0

5

10

15

20

25

30

mill

ion

HighMediumLow

High 19.6 21.7 23.8 25.7 27.1 28.2

Medium 19.6 21.3 22.9 24.3 25 25.4

Low 19.6 21.1 22.4 23.5 24 24.1

2001 2011 2021 2031 2041 2051

Source: Australian Bureau of Statistics In comparison to United Nations population projections, some of Australia’s major trading partners also show low positive to negative growth between 1995 and 2050. For instance, Japan’s population is expected to decline to a level below their current population while the United States is projected to grow at 0.5% annually during this period. Projections show Australia’s population will continue aging, due to low fertility rates and increasing life expectancy. Fertility rates in Australia are declining as families decide to have fewer children or are deferring childbirth and at the same time mortality rates are improving due to advancements in medical science. Current fertility rates are 1.75 babies per women, well below the world average, although compared to developed countries they are middle range. In 1999 the median age was 34.9 years this will increase to between 40.3 and 41.5 years in 2021 and between 43.6 and 46.5 years in 2051. As mortality rates improve and the baby boomers move through the age brackets the proportion of the population over 60 will more than double in the next fifty years. The chart on the next page shows the estimated age sex profile of Australia in 2051 compared to 1999.

16

Source: Australian Bureau of Statistics In terms of the near future the table below estimates the age profile of the population in 2011.

Age 2001 % of Population 2011 % of Population millions millions 0-14 years 4 20% 3.8 18% 15-64 years 13.1 67% 14.5 68% 65 plus 2.5 13% 3.0 14%

Source: Australian Bureau of Statistics All state populations are expected to grow over the next fifty years, with the exception of Tasmania and South Australia. However, they are all growing at different rates and the outcome will be a noticeably different population distribution. The major changes expected are that Queensland will overtake Victoria in terms of population size and ACT and the Northern Territory will overtake Tasmania. The major factor contributing to the changes in population distribution relate to internal migration, in 1999-2000 some 367,390 people moved between states and territories. Australia has a planned migration program which supports skilled migration and future net migration is expected to remain constant at 90,000 persons per year with the same age-gender profile in the near future. Net migration can have a large impact on population size overtime though the impact will tend to vary between states and territories. However, such impacts tend to have little effect on the age structure of the population. Currently the majority of migrants settle in NSW (43%) and other dominant states including Victoria (23%), Queensland (16%) and Western Australia (14%). It is also expected that the three largest states will continue to receive the majority of migrants.

17

6 Infrastructure

6.1 Transportation Australia is a large continent with a very concentrated population living in capital cities separated by vast distances. The chart below provides details of distances between Australian capital cities.

Distances Between Australian Capital Cities (km’s) CITY Adelaide Brisbane Darwin Hobart Melbourne Perth Sydney Adelaide 1,618 2,620 976 641 2,114 1,162 Brisbane 1,618 2,849 1,995 1,380 3,605 750 Darwin 2,620 2,849 3,747 3,132 2,648 3,151 Hobart 976 1,995 3,747 615 3,212 1,039 Melbourne 641 1,380 3,132 615 2,699 705 Perth 2,114 3,605 2,648 3,212 2,699 3,274 Sydney 1,162 750 3,151 1,320 705 3,274

The dominant medium of transport of freight is road, though rail plays an important part in transporting bulk freight long distances. Australia’s transport system has developed to serve primary production and mining for domestic and international markets, the manufacturing and tourism sectors as well as to meet the needs of a community separated by vast distances. Australia has relatively sophisticated transport infrastructure for all transport modes, which service the needs of the urban centres and a more basic infrastructure services rural areas where lower levels of demand exist.

6.1.1 Rail The structure of the rail industry in Australia has been under going tremendous change over the last five years as State and Federal Governments privatise their industry holdings. Australia’s rail network comprises of 40,000 kilometres of private and government broad, standard and narrow gauge track, including 4,150 km of sugar cane railways in Queensland. The mainline rail system comprises 8,000 km of standard gauge and 1,680 km of narrow gauge (link between Brisbane and Cairns). The Australian rail system also includes 270 km of tram networks in Melbourne, Adelaide, Sydney and the Snowy Mountains. The rail network is responsible for carrying one third of all domestic freight, some 535 million tonnes or 139.7 billion tonne kilometres in 2000-2001. The rail network is an integral part of the distribution process for intrastate and interstate freight and a range of regional produce and bulk export commodities. The map below details the national rail network.

18

6.1.2 Sea Australia has some of the world’s finest natural harbours and as a result coastal and transoceanic shipping are vital to the Australian economy. Some 70 ports serve the state capitals as well as industrial and mining centres. Major ports include Melbourne, Sydney, Port Dampier, Newcastle, Port Kembla, Gladstone, Hay Point, Weipa, Brisbane, Port Adelaide, Geelong and Fremantle. In 1999-2000 some 620.8 million tonnes of cargo moved across Australian wharves up 6% on the previous year. The majority of this is exports (74%), imports account for 9%, coastal cargo loaded and discharged account for 8% each. Major sea ports are shown on the map on the previous page and a detailed map of sea ports is provided below as well.

Coastal freight movement accounted for 102.1 million tonnes of cargo through Australian ports in 1999-2000. Coastal freight movement accounts for just under one third of all freight movements within Australia. This represents 108.9 billion tonne kilometres. The major freight items are bulk movements of natural resources.

19

6.1.3 Road Australia has approximately 865,000 km of roads, about half of which are paved. Highways are limited to the more densely populated areas. Some 10 million motor vehicles (more than one vehicle for every two persons) are registered.

6.1.4 Air A comprehensive network of airline services, including some 440 airports link major cities and even remote settlements around Australia. Domestic airlines (Qantas and Virgin Blue) carry over 10 million passengers annually. Because of the long distances between cities and the country's ideal flying conditions, Australians are especially air-minded. Qantas International Airline, operates services to many world capitals, and numerous international airlines operate to Australia.

20

7 Industry Profile The retail sales value (RSV) of confectionery in Australia was A$2.53 billion (US$1.44 bn) in 2001, up 7% on the previous year. Sales growth, averaging around 5% per annum throughout the 1990’s reflects both the number of new brands and product launches along with the continued high levels of advertising and promotional activity. Over A$110 million (estimate) (US$62.7 m) was spent on consumer advertising and promotion in 2001 supporting key brands. With some 5,000 different confectionery products and packs available in the market place, the Australian confectionery market place remains intensively competitive. Virtually every major global player is represented along with around 80 smaller producers. In Australia, as in other Western economies, the confectionery market is in a mature phase of its life cycle. Long-term volume growth is therefore limited to around 2-3% per annum, largely reflecting population growth. The confectionery market is divided into three main segments: chocolate confectionery, sugar confectionery and gum, with the largest, chocolate, having four distinct product segments: chocolate bars, chocolate blocks, boxed chocolate and other chocolate. The latter segment largely comprises novelty and seasonal items including Easter Eggs. The overall confectionery market is dominated by the resident multinational producers; Cadbury Schweppes (36%), Nestlé Confectionery (22%) and Mars Confectionery (18%). Shares for major categories are detailed below: Within individual market segments, the respective shares held by the companies vary considerably, with Cadbury more dominant in chocolate compared to Nestlé who dominates the sugar segment.

Australian Confectionery Market 2001 Retail Sales Value $2.53 billion

Chocolate confectionery

Sugar confectionery Gum

RSV $ $1490 million $838 million $201 million RSV % 59% 33% 8% Market shares

Cadbury 54% Nestlé 32% Wrigley 97% Mars 19% Mars (inclu. Kenman) 17% Others 3% Nestlé

17% Cadbury (inclu Chupa Chups, Trebor)

11%

Ferrero 2% Ferrero 3% House, generics 1% House, generics 11% Others 7% Others 26%

Source: Confectionery Manufacturers of Australasia (CMA)

21

7.1 History The formalisation of the Australian confectionery industry started when James Stedman set up a small factory in 1874. In 1918 the James Stedman Henderson Company established Sweetacres, in New South Wales. MacRobertsons commenced manufacturing in Victoria around 1900, followed by Hoadley. Nestlé began its food operations in 1908, manufacturing a variety of food products including chocolate products. The Allen's brand dates back to 1891 and Life Savers to 1921. Cadbury Fry Pascall began their Australian operations in 1928. Mars products were introduced in the late 1950s, when they were made, sold and distributed by MacRobertson. In the following three decades, the industry underwent major rationalisation, beginning with Cadbury's takeover of MacRobertson in 1967. In 1968, Hoadley acquired Stedman only to be acquired itself by Rowntree three years later. In 1979 Mars ceased its long standing manufacturing license with Mackintosh, establishing its own manufacturing plant in Ballarat, Victoria. Acquisitions both in Australia and overseas continued in the final two decades of the 20th century. The key corporate changes impacting on Australia include: Nestlé's acquisition of local firms Life Savers (1985) and Allen's (1985) and globally, the UK based Rowntree Mackintosh (1988). Nestlé Confectionery Ltd was established in 1991 bringing all its confectionery brands under the one banner group. Cadbury's acquisition of Beatrice Australia Limited (Red Tulip, Europe Strength Foods, Van Camp, James and Molly Bushell Confectionery) in 1987. Phillip Morris' acquisition of Jacobs Suchard (1990) and Terry's (1993) placing them under its Kraft Food operation. Mars acquisition of Kenman Kandy in 1997, the latter operating with considerable autonomy, marketing under its own company name. By century’s end, the combined national market share held by global giants Cadbury Schweppes, Nestlé and Mars accounted for around 75%. Yet, in spite of the extensive concentration of the industry since the 1950’s, the number of domestic confectionery manufacturers has doubled to around 140 firms, testimony to the plethora of niche opportunities characteristic of confectionery markets in industrialised countries.

22

7.2 Chocolate Confectionery In 2001, the top ten chocolate brands accounted for approximately 70% of sales. Cadbury has the major share in this sector at 54%, followed by Mars at 19% and Nestlé at 17%. However, within each of the chocolate segments, company shares vary considerably.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

RSV $A Millions

1999 2000 2001

Chocolate Segment Sales 1999-2001

SEASONAL

CHILDRENS

ASSORTMENTS

BARS

MOULDED

Source: CMA In sales terms, ($ Value), chocolate accounts for around three-fifths of the total confectionery market with the major segments being chocolate bars (43%), blocks (27%), boxed assortments (12%), children’s novelties (7%) and seasonal (mainly Easter moulded – 11%).

7.2.1 Chocolate Bars With retail sales of A$636 million (US$362.5 m), chocolate bars are the largest chocolate sub-segment experiencing 6% growth over the past three years. Bars account for about 40% of chocolate sales and benefit from the highest level of advertising expenditure within the confectionery category. Competition is intense in this market with about 75% of sales made on impulse. The top selling bars in order are Mars Bar, Kit Kat and Cadburys Cherry Ripe. Mars has the highest market share in this segment at around 38% with three of its brands (Mars Bar, Snickers and M&M’s) in the top five. Cadbury, with major brands Cherry Ripe, Crunchie, Picnic and Time Out in the top eight has 32% share. Nestlé has the third highest share at 25%. Nestlé's Kit Kat is the second best seller in this segment, while its bars, Violet Crumble and Smarties, also rank in the top ten.

7.2.2 Chocolate Blocks The chocolate block market, estimated at A$415 million (US$236.6 m) in 2001, is dominated by Cadbury, with a 74% market share. Cadbury dominate the block category producing the eight top selling products in this segment, with Cadbury Dairy Milk being the top selling brand over the entire confectionery market. Its major competitor, Nestlé, has a 16% market share and is market leader in the dark and white chocolate segments with Nestlé Milky Bar and Nestlé Club, its most popular brands. Suchard's market share of 3% comes from Toblerone, Milka and Cote D'or products.

23

In recent years Nestle has attempted to gain market share in this segment through extending some of their current bar lines into block format, some examples of these include Smarties, Violet Crumble, Milky Bar and Rolo.

7.2.3 Boxed Chocolates The boxed chocolate market estimated at A$159 million (US$90.6 m) in 2001, is again dominated by Cadbury with a share around 38%, Lindt at 19% and Ferrero at 13%. In 1999, faced with sustained unfavourable US exchange rates, Russell Stover (Whitmans) exited the Australian market following a peak share of 22% in 1998. This was a regrettable development given that in a short space of time, Whitman’s had significantly expanded this segment through its heavy advertising and promotional activity. Being largely purchased as a gift item, boxed chocolate sales are highly seasonal, with 90% of sales around Valentines Day, Easter, Mother's Day and Christmas. Unlike other confectionery products that compete against each other or food substitutes, boxed chocolates compete against flowers, wine and compact discs as presents. The market for boxed chocolates is very price sensitive and retailers and manufacturers regularly cut prices to boost sales. The top sellers in this segment, in order, are Cadbury Roses, Favourites (Cadbury mini-bar twist wraps), Ferrero Rocher, Milk Tray (Cadbury) and Celebrations (Mars mini-bar twist wraps). Imported products from Ferrero, Nestlé (Baci) and Stuart Alexander (Guylian) are taking small but increasingly significant shares of the Australian market. About 70% of boxed chocolate sales are through grocery outlets. A number of assortment lines are now being successfully sold in impulse ‘counter-top’ packs of one, two or three items. Ferrero started this trend but have been followed by Lindor Balls (Lindt).

7.2.4 Other Chocolate Other chocolate, including Easter Eggs, other seasonal lines, and chocolate food products such as milk modifiers, totalled A$275 million (US$156.8 m) in 2001. Cadbury, Ferrero and Nestlé dominate this market with a 50%, 27% and 20.5% share respectively. In the Easter market, Cadbury's dominates with 70% market share. A major segment of The children’s category is children's lines (A$100 million). Over the past three years, growth in the children’s chocolate category has been spectacular, largely as a result of the very successful entry of Cadbury’s Yowie. This novel product incorporates a plastic indigenous animal within a chocolate shell and is further augmented by books, web site and various merchandising devices. Cadbury is the clear market leader in this category associated with Yowie number one brand followed by its Freddo Frog brand, which celebrated its 70th birthday in 2000. Other Cadbury brands include Caramello Koala, Curly Wurly and Furry Friends brands. Nestlé’s Smarties and Milky Bar products are also major brands. Ferrero's Kinder Surprise, the second most popular brand in 1996 is now sixth owing to some sales displacement from Yowies. Cadbury has also been successful in marketing its Crème Eggs, formerly an Easter-only line, all year round.

24

7.3 Sugar Confectionery In 2001 sugar confectionery and gum sales, estimated at A$838 million (US$477.7 m), accounted for 41% of the confectionery market. Products in this segment comprise sugar bags and packs (including pick and mix) candy rolls and medicated products. The chart below is the most recent breakdown of sugar confectionery product segments

Source: Nestle , varies slightly with AC Nielson data used elsewhere in this report.

he sugar segment is more fragmented than chocolate with the two largest companies accounting for half the

estlé's leading brands are Allen's Minties, Fantales, Kool Mints, Snakes Alive, Lifesavers, Jaffas, Butter

ugar-free brands were launched in the late 1990’s by both majors, Cadbury with Zeros and Nestlé with Zones)

7.4 Gum Th million (US$114.6 m) in 2001, accounts for 8% of confectionery sales

nd

rigley’s have been successful in several rather large direct mail campaigns containing product samples to

Sugar Confectionery Segment Sales 1995-98

289

118

69

92

108

268 271

251

131124

112

93

128124119

109116

76

86

84

0

50

100

150

200

250

300

1995 1996 1997 1998

RSV

$AU

S m

ill.

Bags/PacksChewing GumRolls/Pock. packsFunctionalOther

Tmarket: Nestlé with 32%, Mars 17% and Cadbury with 11%. Smaller operators can more easily penetrate this segment because sugar confectionery making is the simplest and least capital intensive. NMenthol, and medicated lines Soothers and Anticol. Cadbury's leading brands are Pascall Marshmallows, Chupa Chups (import agent), Trebor and Pascall Chocolate Eclairs. Other top selling brands include MarsStarburst, Sunrise jellies, Ferrero's Tic Tacs, and Stuart Alexander’s (import agent) Mentos. Sadding to impressive growth in the candy roll segment over the past four years.

e gum market estimated at A$201 with Wrigley’s being the major player led by its major brands Extra, PK, Juicy Fruit, Arrowmint, Freedent, aDoublemint. Other brands in this segment include Stimorol, which is imported by Stuart Alexander and new entrant Fernadale (Gleam, Vapours). In early 2002, Cadbury launched its 24/7 Brand (Trebor) with considerable fanfare though it is too early to judge the long-term impact on its competitors. WAustralian households. Direct mail was a major promotional vehicle for the launch of Airwaves and Xcite products.

25

7.5 Industry Characteristics The Australian confectionery industry and the successful players within it exhibit the following characteristics:

7.5.1 Impulse Buying Some 70% of confectionery products are bought on impulse, ensuring confectionery has one of the widest distribution bases of any consumer product. Even planned purchases tend to be associated with some form of treat, whether for oneself or others. Effective merchandising is paramount in the impulse food sector. Prominent displays, off aisle locations (eg end aisle, check-out) continue to be heavily utilised by the industry. Because confectionery is largely an impulse item, it is well recognised that it competes with other impulse categories, particularly savoury snacks, ice cream, biscuits and cereal/health bars. Category ‘blurring’ has featured, particularly between confectionery and biscuits. Five years ago, Australia’s largest biscuit manufacturer, Arnott’s, reformatted Tim Tams, a perennial favourite chocolate-coated biscuit, into single pack lines to compete alongside traditional chocolate bars. Whilst this line continues to sell, it has faced stiff opposition from ‘confectionery’ biscuit lines, especially Kit Kat (Nestle), Twix (Mars) and Breakaway (Cadbury). Industry commentators note that the consuming public appears resistant paying the higher confectionery price for a standard pantry items such as Tim Tams.

7.5.2 Efficient Selling and Distribution Network: With the high level of impulse purchasing, confectionery has one of the widest distribution networks of any consumer product, ensuring that it is always on hand to satisfy consumer needs. Manufacturers must ensure their product is efficiently distributed and readily available to consumers. Furthermore, the importance of supermarkets continues to grow and therefore strong relationships between confectionery manufacturers and supermarket chains are critical to ensure mass volume sales. Non-traditional distribution networks also extend from vendor selling machines to confectionery fundraising. Smaller producers find the use of school confectionery fundraising a critical source of volume and access to demand that is related more to families and friends supporting children's order sheets, rather than genuine consumer wants. In recent years, this business channel has become a target for the major brand owners with traditional fund-raising specialists such as the local subsidiary of US based World’s Finest Chocolates, being squeezed out of the market.

7.5.3 Strong Brand Names High profile brands with strong consumer loyalty are fundamental to maintaining market share, as well as in generating sales growth in the confectionery industry. A highly successful brand image also gives products a long life cycle. It also explains the dominance of multinationals that bring with them well-known international brands into the market place. Large companies with big promotion budgets are able to maintain strong brand images and introduce new brands. The difficulty of developing new brands and the underlying constraint of low long-term real growth helps to explain the industry's long history of mergers and acquisitions due to the difficulty of developing brand names. The dominance of multi-nationals in the confectionery market is largely due to the ownership of well-known local and international brand names.

26

In Australia the predominance of well-known brand names is evident from the products that hold the greatest market shares. Many of these brands have a long history, and account for the domination of foreign companies in the confectionery industry. For example, seven of the most successful bars in the Australian market are Mars Bar, Kit Kat, Cherry Ripe, Dairy Milk, Roses, Quality Street and Snickers, all launched before 1939. Others such as Pascall dates back to 1866, and Toblerone to 1908. The well known Australian Minties brand dates back to the 1920s.

7.5.4 Effective Media Support, Strong Merchandising In a mature market like confectionery, consumer interest needs to be constantly stimulated through strong merchandising. Advertising and promotional campaigns are also vital to the long-term success of brand images as well as to sales growth. Typically, major brands enjoy considerable promotional support by way of advertising, principally television (TVC’s) and, ‘below the line’ promotional spend with the retail trade. In 2001, the industry invested around A$110 million (US$62.7 m) in advertising with a similar amount below the line. The countervailing power of major confectionery producers to key distribution outlets such as supermarkets is critical to providing them with leverage in negotiating shelf space in supermarkets. Shelf heights and the positioning of end of aisle displays come at a high premium. With continued fragmentation of the traditional commercial television audience base, the industry has turned to other mediums for brand building promotions. In particular, outdoor and transit advertising is increasingly being utilised following the successful example in the soft drinks industry. Sponsorships also continue to enjoy popularity amongst industry marketers. The better known include the 2000 Olympics by Cadbury and the World Soccer Cup by Mars during the early 1990’s.

7.5.5 Product Innovation Whilst established brands are the mainstay of the industry, new innovative products and packaging drive market growth. New products need to be perceived as innovative and not just copycat products of another brand. In Australia, copycat products often fail to gain significant market share. New packaging, such as multi bags, has been an essential part of stimulating sales in supermarkets where there tends to be less impulse buying, or at least where the consumption decision is transferred from the point of purchase to the home. Many of the successful new launches have been line extensions of existing brands; ‘white’ chocolate variants (Kit Kat White, Aero White), teeth whitening and medicated gum lines (Wrigley’s Extra White and Air Waves), new size formats (Kit Kat Chunky), enrobed extruded chocolate (Cadbury Flake to Twirl) and subsequent wafer addition (Twirl to Time-Out), Snickers Light. New packaging size and configuration formats have also enjoyed considerable success evidenced by sales of fun-bag (multi-bag) mini-brands Cadbury’s Favourites and Mars’ Celebrations. Mars have also been successful in sales of single bite-size mini-bars. Licensed products have enjoyed mixed success. Star Wars and Spiderman have enjoyed moderate sales. Hollywood character licensing has yet to succeed with its most recent foray executed by Show Time Foods, which went into receivership in 1999. By contrast, Nestle, following its successful collaboration with Disney in the mid-1990s has sustained its 2001 success with Willie Wonka. It would appear that to succeed in licensed products, the commitment to trade support is even more critical than normal. Successful flavour innovations include sour sugar confectionery (Warheads, Skittles Sour) and all-natural flavours (Sunrise jellies).

27

In recent years, a number of confectionery marketing companies have established, sourcing bulk products from overseas or through local contract manufacturers, repackaging them and selling them under their own brand name. Ferndale has been very successful in the pocket pack counter lines through innovative cardboard packaging and brand positioning. Other new products include the internationally awarded Yowie (Cadbury), with a similar format to Ferrero’s Kinder Surprise featuring indigenous animal plastic novelty. In spite of the importance of bringing new products to the market, failure rates are typically high, reported anywhere between 70% and 90%. Even when success is attained, there are very few modern day examples of enduring brand staying power.

7.5.6 Seasonal Variation in Demand The chocolate confectionery business has a seasonal bias towards the colder months of the year and special gift occasions such as Easter, Christmas, Mother's Day and Valentines Day. Easter is the biggest selling season with sales of A$190 million (US$108.3 m) in 2001. Australian per capita consumption of chocolate Easter products is the highest in the world. For confectionery manufacturers, the later Easter is in the year, the better for sales generally, because the weather tends to be colder. Christmas, the next best sales period, represents less than A$50 million (US$28.5 m)of annual sales in 2001. Valentines Day is a relatively new event in Australia, beginning in the late 1970’s. Valentine sales are approaching A$30 million (US$17.1 m). In the mid-1990’s, the industry collectively funded a programme to develop sales opportunity around Halloween. Retailers were reluctant to join forces with suppliers and consequently, this opportunity remains unfulfilled.

7.5.7 Consumer Value Demand for confectionery is highly price elastic. Value for money is a key part of the purchase decision. Confectionery also faces strong competition from substitutes such as corn chips and biscuits, which increases the importance of competitively pricing and positioning of product lines. Some confectionery products such as Ferrero Rocher, Lindt, Gullyan and Toblerone target specific upper-markets; however in lower volume market segments, promotion as prestige confectionery lines, makes price less important, and a more differentiating feature of a product purchase.

7.6 Industry Attractiveness In spite of the immense power of retailers in the Australian market, promotional costs fundamental to the mass market keep entry barriers moderately high. Thus the Australian confectionery industry is a moderately attractive industry in which to operate. The following sections describe the industry’s attractiveness (utilising Porters Five Forces Model).

7.6.1 New Entrants As a general rule, entry barriers and exit barriers are high. Considerable expenditure is required for purpose-specific machinery. More importantly, it can take many years to establish a confectionery brand in the Australian market. Massive sums are required for advertising and promotion in order to develop brand franchise with the Australian community. Whilst the Australian confectionery market is relatively stable and mature, it is geographically well located to the burgeoning markets of the Asia Pacific Rim. For this reason, there is a likelihood that two new entrants could enter the Australian market in the near future, as a foothold for expansion to these growth markets to the north.

28

One company, US market leader Hershey Foods, has had two forays into the Australian market, in 1987 and 1990. On both occasions they operated through local based importing agents; whilst impressive trial rates were achieved by virtue of an excellent major media campaign, ultimately Australians were unimpressed with the bitter sweet style of the popular US chocolate. Nevertheless, Hershey clearly has the resources to overcome the high entry barriers into the local market, as well as the expertise to reformulate their product to suit the Australian palate. Hershey recently announced its appointment of Network Foods, a major national distribution firm, to act as agent for the Australian market. Similarly, the acquisition of Jacob Suchard, the giant sweets confectioner in 1990 by tobacco multinational, Philip Morris International, could see this company begin local manufacturing and would be complimented by the market power of its sister subsidiary, Kraft Foods. Currently, only a small number of Suchard brands are imported into Australia (eg Toblerone, Milka and more recently, Daim). These brands have an excellent reputation for quality and are positioned at the premium end of the market.