Embed Size (px)

Citation preview

AUDITING PROBLEMS

FIRST SET OF PROBLEMS

PROBLEM NO. 1

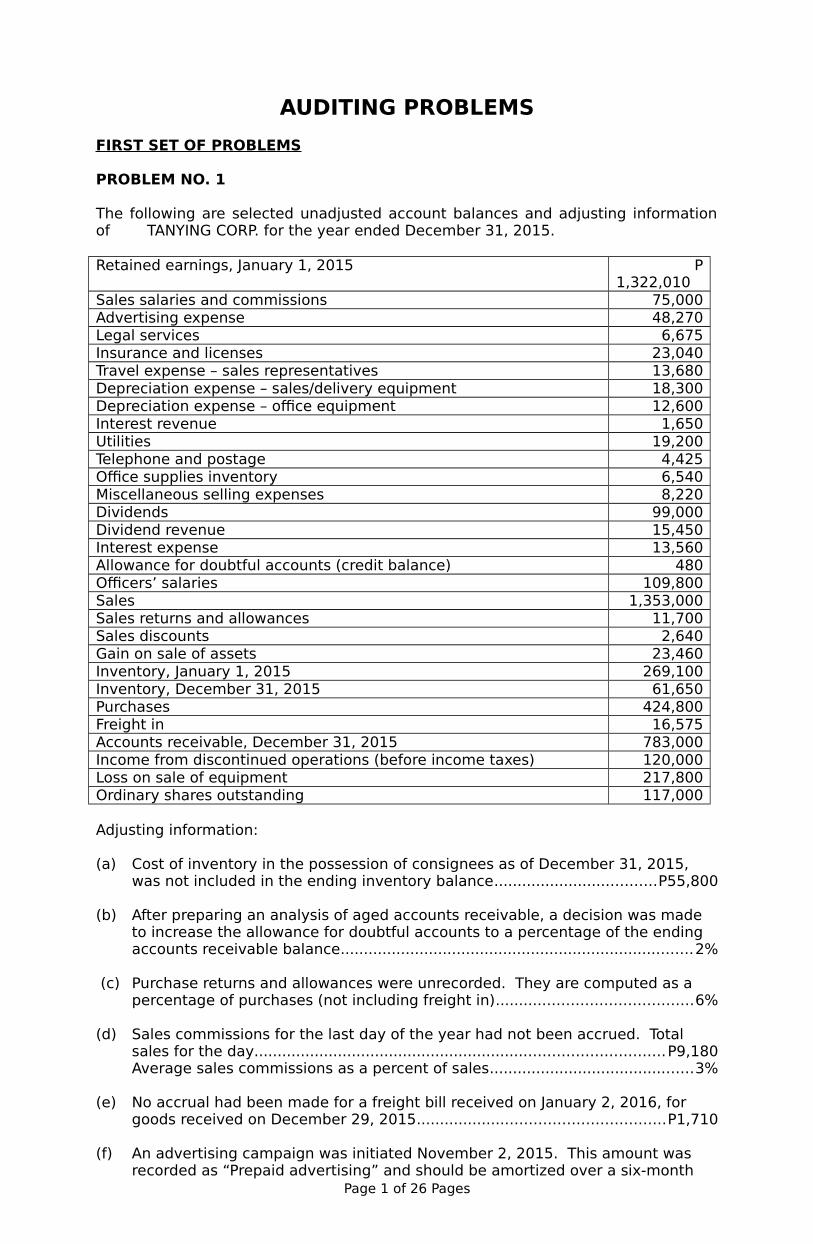

The following are selected unadjusted account balances and adjusting informationof TANYING CORP. for the year ended December 31, 2015.

Retained earnings, January 1, 2015 P1,322,010

Sales salaries and commissions 75,000Advertising expense 48,270Legal services 6,675Insurance and licenses 23,040Travel expense – sales representatives 13,680Depreciation expense – sales/delivery equipment 18,300Depreciation expense – office equipment 12,600Interest revenue 1,650Utilities 19,200Telephone and postage 4,425Office supplies inventory 6,540Miscellaneous selling expenses 8,220Dividends 99,000Dividend revenue 15,450Interest expense 13,560Allowance for doubtful accounts (credit balance) 480Officers’ salaries 109,800Sales 1,353,000Sales returns and allowances 11,700Sales discounts 2,640Gain on sale of assets 23,460Inventory, January 1, 2015 269,100Inventory, December 31, 2015 61,650Purchases 424,800Freight in 16,575Accounts receivable, December 31, 2015 783,000Income from discontinued operations (before income taxes) 120,000Loss on sale of equipment 217,800Ordinary shares outstanding 117,000

Adjusting information:

(a) Cost of inventory in the possession of consignees as of December 31, 2015,was not included in the ending inventory balance...................................P55,800

(b) After preparing an analysis of aged accounts receivable, a decision was madeto increase the allowance for doubtful accounts to a percentage of the endingaccounts receivable balance............................................................................2%

(c) Purchase returns and allowances were unrecorded. They are computed as apercentage of purchases (not including freight in)..........................................6%

(d) Sales commissions for the last day of the year had not been accrued. Totalsales for the day........................................................................................P9,180Average sales commissions as a percent of sales............................................3%

(e) No accrual had been made for a freight bill received on January 2, 2016, for goods received on December 29, 2015.....................................................P1,710

(f) An advertising campaign was initiated November 2, 2015. This amount was recorded as “Prepaid advertising” and should be amortized over a six-month

Page 1 of 26 Pages

AUDITING PROBLEMS

period. No amortization was recorded......................................................P5,454

Freight charges paid on sold merchandise were netted against sales. Freightcharges on sales during 2015..................................................................P10,500

(g) Interest earned but not accrued.................................................................P1,680

(h) Depreciation expense on a new forklift purchased March 1, 2015, had not been recognized. (Assume all equipment will have no salvage value and thestraight-line method is used. Depreciation is calculated to the nearest month.)Purchase price..........................................................................................P23,400Estimated life in years......................................................................................10

(i) A “real” account is debited upon the receipt of office supplies. Office supplieson hand at

year-end.....................................................................................................P3,675

(j) Income tax rate (on all items)........................................................................30%

Compute the adjusted balances of the following:

1. Net salesA. P1,363,500 B. P1,349,160 C. P1,353,000 D. P1,342,500

2. Cost of goods available for saleA. P684,900 B. P824,697 C. P686,697 D. P779,913

3. Inventory, December 31, 2015A. P61,500 B. P61,350 C. P56,250 D. P117,450

4. Distribution costsA. P181,649 B. P167,513 C. P178,013 D. P176,453

5. Administrative expensesA. P207,345 B. P193,785 C. P194,265 D. P194,595

6. Allowance for doubtful accountsA. P15,660 B. P16,140 C. P15,180 D. P480

7. Total incomeA. P817,143 B. P811,653 C. P779,913 D. P822,153

8. Income from continuing operations before taxesA. P231,360 B. P436,795 C. P218,995 D. P239,695

9. Office supplies inventoryA. P6,540 B. P3,675 C. P2,865 D. P 0

10. Net income A. P237,296 B. P210,299 C. P250,289 D. P216,296

-----------------------------oooOOOooo-----------------------------

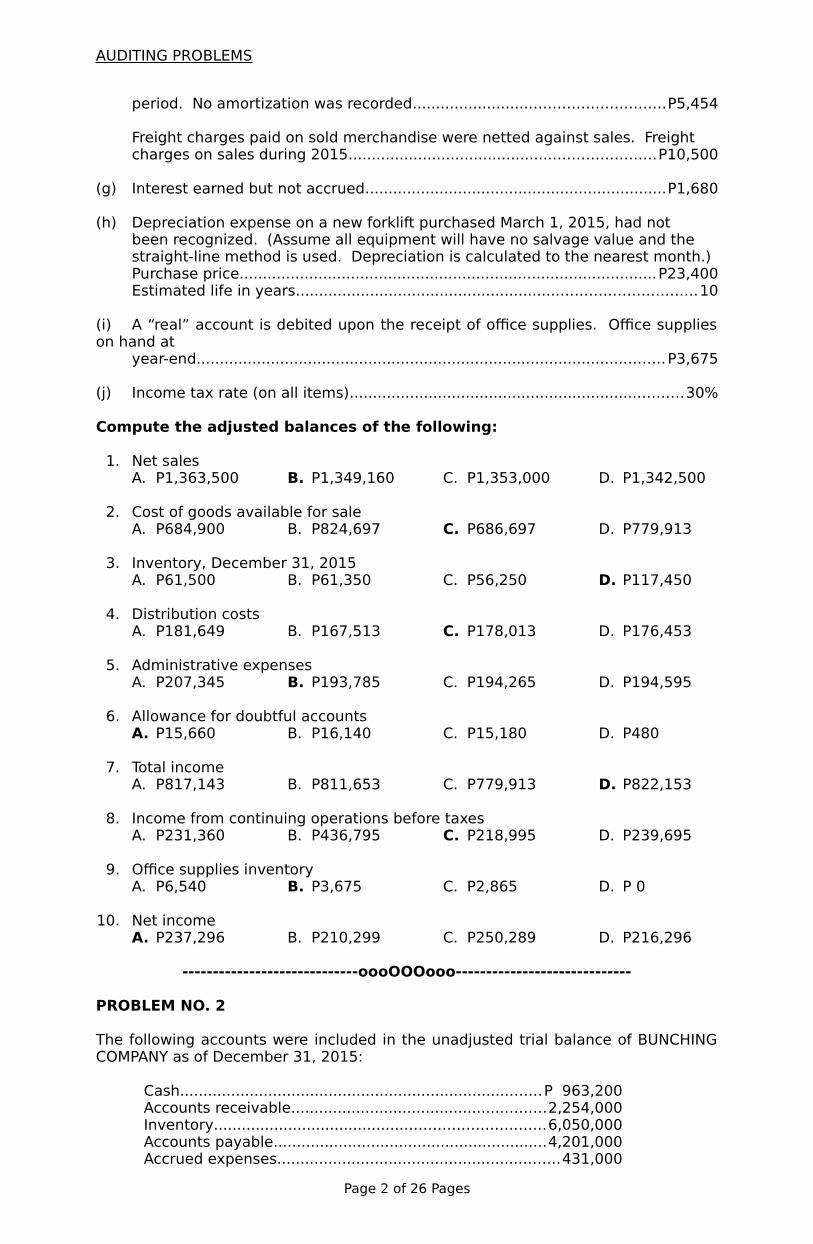

PROBLEM NO. 2

The following accounts were included in the unadjusted trial balance of BUNCHINGCOMPANY as of December 31, 2015:

Cash..............................................................................P 963,200Accounts receivable.......................................................2,254,000Inventory.......................................................................6,050,000Accounts payable...........................................................4,201,000Accrued expenses.............................................................431,000

Page 2 of 26 Pages

AUDITING PROBLEMS

During your audit, you noted that Bunching Company held its cash books open afteryear-end. In addition, your audit revealed the following:

1. Receipts for January 2016 of P654,600 were recorded in the December 2015cash receipts book. The receipts of P360,100 represent cash sales and P294,500represent collections from customers, net of 5% cash discounts.

2. Accounts payable of P372,400 was paid in January 2016. The payments, onwhich discounts of P12,400 were taken, were included in the December 2015check register.

3. Merchandise inventory is valued at P6,050,000 prior to any adjustments. Thefollowing information has been found relating to certain inventory transactions:

a. The invoice for goods costing P175,000 was received and recorded as apurchase on December 31, 2015. The related goods, shipped FOBdestination, were received on January 4, 2016, and thus were not included inthe physical inventory.

b. A P182,000 shipment of goods to a customer on December 30, 2015, termsFOB destination, are not included in the year-end inventory. The goods costP130,000 and were delivered to the customer on January 3, 2016. The salewas properly recorded in 2016.

c. Goods costing P637,500 were shipped on December 31, 2015, and weredelivered to the customer on January 3, 2016. The terms of the invoice wereFOB shipping point. The goods were included in the 2015 ending inventoryeven though the sale was recorded in 2015.

d. Goods costing P217,500 were received from a vendor on January 4, 2016.The related invoice was received and recorded on January 6, 2016. Thegoods were shipped on December 31, 2015, terms FOB shipping point.

e. Goods valued at P275,000 are on consignment with a customer. These goodsare not included in the inventory figure.

f. Goods valued at P612,800 are on consignment from a vendor. These goodsare not included in the physical inventory.

Based on the above and the result of your audit, determine the adjusted balances ofthe following as of December 31, 2015:

11. Cash A. P963,200 B. P681,000 C. P668,600 D. P693,400

12. Accounts receivableA. P2,908,600 B. P2,564,000 C. P2,254,000 D. P2,548,500

13. InventoryA. P6,035,000 B. P6,080,000 C. P5,860,000 D. P5,010,000

14. Accounts payableA. P4,790,900 B. P4,615,900 C. P4,573,000 D. P4,603,500

15. Current ratioA. 2.00 B. 1.83 C. 1.84 D. 2.01

-----------------------------oooOOOooo-----------------------------

PROBLEM NO. 3

The following are independent situations:

Page 3 of 26 Pages

AUDITING PROBLEMS

The Machinery account of PAKO COMPANY contains the following entries during theyear:

Date Item Debit Credit2015

Jan. 1 Balance P1,800,000June 30 Purchased four new machines 1,080,000

Installation cost of new machines 48,000Sept.30 Proceeds from sale of old machine, cost

P150,000; accumulated depreciation, P105,000 P 66,000Oct. 31 Repairs of machinery 75,000Dec. 1 Cash paid for trade-in of old machines—cost,

P90,000; accumulated depreciation, P36,000. Cash price of new machine, P270,000 225,000

Dec.31 Balance 3,162,000Total P3,228,000 P3,228,000

16. What is the correct balance of the Machinery account on December 31, 2015?A. P3,162,000 B. P3,057,000 C. P3,048,000 D. P2,958,000

17. Assuming depreciation is recorded on a monthly basis at 10% a year, howmuch was the depreciation charge for 2015?A. P234,150 B. P300,000 C. P316,200 D. P227,400

On June 30, 2015, the GENLUNA COPPER MINES, INC. purchased a copper mine forP14,580,000. The estimated capacity of the mine was 1,620,000 tons. GenlunaCopper Mines expects to extract 15,000 tons of ore a month with an estimatedselling price of P50 per ton. Production started immediately after some newmachines costing P1,800,000 were bought on June 30, 2015. These new machineshad an estimated useful life of 15 years with a scrap value of 10% of cost after theore estimate has been extracted from the property, at which time the machines willalready be useless. Genluna’s books show the following expenses for 2015:

Depletion expense..................................P1,215,000Depreciation—Machinery.............................120,000

18. Recorded depletion expense wasA. Overstated by P270,000.B. Understated by P270,000.C. Overstated by P405,000D. Understated by P405,000.

19. Recorded depreciation expense wasA. Understated by P60,000.B. Overstated by P60,000.C. Understated by P30,000.D. Overstated by P30,000.

BULKAN COMPANY purchased a machine for P300,000 on January 1, 2012, with thefollowing additional items paid or incurred:

Separation pay for laborer laid off upon acquisition of new machine......P3,600Loss on sale of machine replaced..............................................................3,900Transportation in.......................................................................................3,000Installation cost.......................................................................................12,000

The new machine is estimated to have a useful life of 10 years and a residual valueof P12,000.

Page 4 of 26 Pages

AUDITING PROBLEMS

On January 1, 2015, new parts which cost P37,800 were added to the machine so asto reduce its fuel consumption, but with no change in its estimated life or residualvalue.

20. The annual depreciation charge on the machine for 2015 wasA. P34,080 B. P35,494 C. P36,450 D. P35,700

-----------------------------oooOOOooo-----------------------------

PROBLEM NO. 4

Presented below are unrelated situations.

1. HARLINGTON COMPANY buys and sells securities expecting to earn profits onshort-term differences in price. During 2016, Harlington Company purchased thefollowing trading securities:

Fair ValueSecurity Cost Dec. 31, 2016

A P 585,000 P 675,000B 900,000 486,000C 1,980,000 2,034,000

Before any adjustments related to these trading securities, Harlington Companyhad net income of P2,700,000.

21. What is Harlington’s net income after making any necessary trading securityadjustments?A. P2,430,000 B. P2,286,000 C. P2,934,000 D. P2,700,000

22. What would Harlington’s net income be if the fair value of security B wereP855,000?A. P2,601,000 B. P2,799,000 C. P2,700,000 D. P2,655,000

2. LABADA CO.’s portfolio of trading securities includes the following on December31, 2015:

Cost Fair Value15,000 ordinary shares of Camias Co. P1,431,000 P1,251,00030,000 ordinary shares of Ganda Co. 1,638,000 1,710,000

P3,069,000 P2,961,000

All of the above securities have been purchased in 2015. In 2016, Labada Co.completed the following securities transactions:

Mar. 1 Sold 15,000 shares of Camias Co. ordinary shares at P93, less brokeragecommission of P13,500.

April 1 Bought 1,800 ordinary shares of Waston, Inc. at P135 plus commission,taxes, and other transaction costs of P4,950.

The Labada Co. portfolio of trading securities appeared as follows on December31, 2016:

Cost Fair Value30,000 ordinary shares of Ganda Co. P1,638,000 P1,740,000 1

1,800 ordinary shares of Waston, Inc. 247,950 225,000 2

P1,885,950 P1,965,0001 Net of P19,500 estimated transaction costs that would be incurred on the sale of the securities.2 Net of P4,500 estimated transaction costs that would be incurred on the sale of the securities.

23. What amount of unrealized gain on these securities should be reported in the2016 income statement?

Page 5 of 26 Pages

AUDITING PROBLEMS

A. P31,050 B. P79,050 C. P84,000 D. P36,000

24. What is the gain on the sale of Camias Co. ordinary shares on March 1, 2016?A. P144,000 B. P27,000 C. P130,500 D. P13,500

25. What amount should be reported as trading securities in Labada’s statement offinancial position on December 31, 2016?A. P1,965,000 B. P1,989,000 C. P1,885,950 D. P1,909,950

-----------------------------oooOOOooo-----------------------------

PROBLEM NO. 5

On January 1, 2014, SAMSON MFG. CO. began construction of a building to be usedas its office headquarters. The building was completed on June 30, 2015.

Expenditures on the project were as follows:

January 3, 2014 P2,500,000March 31, 2014 3,000,000June 30, 2014 4,000,000October 31, 2014 3,000,000January 31, 2015 1,500,000March 31, 2015 2,500,000May 31, 2015 3,000,000

On January 3, 2014, the company obtained a P5 million construction loan with a10% interest rate. The loan was outstanding all of 2014 and 2015. The company’sother interest-bearing debts included a long-term note of P25 million with an 8%interest rate, and a mortgage of P15 million on another building with an interestrate of 6%. Both debts were outstanding during all of 2014 and 2015. Thecompany’s fiscal year-end is December 31.

26. What is the amount of capitalizable interest in 2014?A. P3,400,000 B. P1,043,750 C. P663,125 D. P500,000

27. What is the amount of capitalizable interest in 2015?A. P630,625 B. P654,663 C. P361,707 D. P799,663

28. What amount of interest should be expensed in 2014?A. P2,736,875 B. P2,356,250 C. P2,900,000 D. P 0

29. What amount of interest should be expensed in 2015?A. P2,769,375 B. P3,038,293 C. P2,600,337 D. P2,745,337

30. What is the total cost of the building (including the interest capitalized in 2014and 2015)?A. P24,600,000 B. P20,817,788 C. P20,905,457 D. P20,630,625

-----------------------------oooOOOooo-----------------------------

PROBLEM NO. 6

At the beginning of year 1, an entity grants to a senior executive 30,000 shareoptions. The grant is conditional upon the executive remaining in the entity’semploy until the end of year 3.

The share options can be exercised if the entity’s share price increases from P20 atthe beginning of year 1 to above P30 at the end of year 3. If the share price isabove P30 at the end of year 3, the share options can be exercised at any timeduring the next five years, i.e., by the end of year 8.

Page 6 of 26 Pages

AUDITING PROBLEMS

The entity estimates the fair value of the share options on grant date to be P5 peroption. This estimate takes into account the following market condition:

The possibility that the share price will exceed P30 at the end of year 3, i.e., theshare options become exercisable; andThe possibility that the share price will not exceed P30 at the end of year 3, i.e.,the share options will be forfeited.

The following actual events occurred in years 1 to 3:

Year 1

The share price has increased to P24.The entity’s estimate of the fair value of the options is P4 at the end of year 1.This takes into account whether the market condition will be satisfied by the endof year 3.

Year 2

The share price has decreased to P22. However, the entity remains optimisticthat the share price target will be met by the end of year 3.The estimated fair value of the share options is P3. Again, this estimate takesinto account the market condition noted above.

Year 3

The share price only reaches P28 by the end of year 3.The estimated fair value of the share options is zero, as the market condition hasnot been satisfied.

Based on the preceding information, determine the following:

31. Compensation expense for year 1A. P30,000 B. P40,000 C. P50,000 D. P60,000

32. Compensation expense for year 2A. P30,000 B. P40,000 C. P50,000 D. P60,000

33. Compensation expense for year 3A. P 0 B. P30,000 C. P40,000 D. P50,000

34. Share options outstanding at the end of year 2A. P70,000 B. P80,000 C. P90,000 D. P100,000

35. Cumulative compensation expense for the three-year periodA. P 0 B. P70,000 C. P100,000 D. P150,000

-----------------------------oooOOOooo-----------------------------

PROBLEM NO. 7

The following independent situations relate to the audit of shareholders’ equity.Answer the questions at the end of each situation.

BRANDY CO. was organized at the beginning of the current year. The followingshareholders’ equity accounts are included in the entity’s year-end trial balance.

Preference share capital, P100 par, authorized 100,000 shares,issued and outstanding, 66,000 shares P6,600,000

Preference share capital subscribed, 6,000 shares 600,000Share premium – preference 240,000Subscriptions receivable – preference 360,000

Page 7 of 26 Pages

AUDITING PROBLEMS

Ordinary share capital, P10 par value, authorized 200,000 shares,issued and outstanding, 72,000 shares 720,000

Ordinary share capital subscribed, 72,000 shares 720,000Share premium – ordinary 2,850,000Subscriptions receivable – ordinary 1,080,000

The following current year transactions relate to Brandy Co.’s shareholders’ equity:

Immediately after Brandy Co. was organized, it received subscriptions to 60,000preference shares. Subscriptions to ordinary shares were also received on thesame date.

During the year, subscriptions were received for an additional 12,000 preferenceshares at a price of P120 per share.

Cash payments were received from subscribers at frequent intervals for severalmonths after subscription. The company’s policy is to issue share certificatesonly upon full payment of the share subscription.

Also during the current year, Brandy Co. issued 24,000 ordinary shares inexchange for a tract of land with a fair value of P690,000.

36. What is the total subscription price of the ordinary shares originallysubscribed?A. P4,290,000 B. P3,840,000 C. P3,600,000 D. P4,050,000

37. How much was collected from the subscribers of preference shares?A. P1,440,000 B. P5,640,000 C. P7,440,000 D. P7,080,000

38. The company’s statement of financial position at the end of the current yearshould report contributed capital of

Preference OrdinaryA. P7,440,000 P4,290,000B. 7,080,000 3,210,000C. 6,480,000 2,490,000D. 6,840,000 360,000

The following shareholders’ equity accounts are included in the statement offinancial position of CONDESSA CO. on December 31, 2014.

Preference share capital, 8%, P100 par (200,000 shares authorized,60,000 shares issued and outstanding) P6,000,000

Ordinary share capital, P5 par (2,000,000 shares authorized,600,000 shares issued and outstanding) 3,000,000

Share premium 3,750,000Retained earnings 3,500,000Total P16,250,000

During 2015, Condessa took part in the following transactions concerning equity.

1. Paid the annual 2014 P8 per share dividend on preference shares and a P2 pershare dividend on ordinary shares. These dividends had been declared onDecember 31, 2014.

2. Purchased 81,000 shares of its own outstanding ordinary shares for P40 pershare.

3. Reissued 21,000 treasury shares for land valued at P900,000.

4. Issued 15,000 preference shares at P105 per share.

Page 8 of 26 Pages

AUDITING PROBLEMS

5. Declared a 10% stock dividend on the outstanding ordinary shares when theshares are selling for P45 per share.

6. Issued the stock dividend.

7. Declared the annual 2015 P8 per share dividend on preference shares and theP2 per share dividend on ordinary shares. These dividends are payable in2016.

8. Reported net income of P9,900,000 for the current year.

39. What is the retained earnings balance (before appropriation for treasuryshares) on December 31, 2015?A. P9,182,000 B. P718,000 C. P6,782,000 D. P11,000,000

40. What amount should be reported as total shareholders’ equity on December31, 2015?A. P25,997,000 B. P23,597,000 C. P21,197,000 D. P14,415,000

-----------------------------oooOOOooo-----------------------------

PROBLEM NO. 8

The following independent situations relate to the audit of intangible assets.Answer the questions at the end of each situation.

CABOOM LABORATORIES holds a valuable patent (No. 112170) on a device thatprevents certain types of air pollution. Caboom does not manufacture or sell theproducts and processes it develops; it conducts research and develops productswhich it patents, and then assigns the patents to manufacturers on a royalty basis.The history of Patent No. 112170 is as follows:

Date A c t i v i t y Cost

2005-2006 Research conducted to develop device P1,259,100Jan. 2007 Design and construction of a prototype 262,800Mar. 2007 Testing of models 126,000Jan. 2008 Legal and other fees to process patent application; patent granted

June 2008 186,150Nov. 2009 Engineering activity necessary to advance the design of the device

to the manufacturing stage 244,500April 2011 Research aimed at modifying the design of the patented device 129,000May 2015 Legal fees paid in a successful patent infringement suit against a

competitor 102,000

Caboom assumed a useful life of 17 years when it received the initial device patent.On January 1, 2013, it revised its useful life estimate downward to 5 remainingyears. Amortization is computed for a full year if the cost is incurred prior to July 1and no amortization for the year if the cost is incurred after June 30. Caboom’sreporting date is December 31, 2015.

Compute the carrying value of Patent No. 112170 on each of the following dates:

41. December 31, 2008A. P180,675 B. P186,150 C. P293,788 D. P175,200

42. December 31, 2012A. P223,200 B. P52,560 C. P131,400 D. P122,640

43. December 31, 2015A. P120,560 B. P78,840 C. P52,560 D. P98,550

Page 9 of 26 Pages

AUDITING PROBLEMS

BARTOLO COMPANY has provided information on intangible assets as follows:

A patent was purchased from Valenzuela Company for P4,000,000 on January 1,2014. Bartolo estimates the remaining useful life of the patent to be 10 years.The patent was carried in Valenzuela’s accounting records at a net book value ofP4,000,000 when Valenzuela sold it to Bartolo.

During 2015, a franchise was purchased from Delco Company for P960,000. Thecontract which runs for 10 years provides that 5% of revenue from the franchisemust be paid to Delco. Revenue from the franchise for 2015 was P5,000,000.Bartolo takes a full year amortization in the year of purchase.

The following research and development costs were incurred by Bartolo in 2015:Materials and equipment P284,000Personnel 378,000Indirect costs 204,000

P866,000

Bartolo estimates that these costs will be recouped by December 31, 2018. Thematerials and equipment purchased have no alternative uses.

On January 1, 2015, because of recent events in the field, Bartolo estimates thatthe remaining life of the patent purchased on January 1, 2014 is only 5 yearsfrom January 1, 2015.

44. What is the total carrying value of Bartolo’s intangible assets on December 31,2015?A. P3,744,000 B. P4,864,000 C. P2,880,000 D. P3,681,500

45. As a result of the facts above, compute the total amount of charges againstincome for the year ended December 31, 2015?A. P2,428,000 B. P1,932,000 C. P1,648,000 D. P1,116,000

-----------------------------oooOOOooo-----------------------------

PROBLEM NO. 9

The following are two (2) unrelated situations. Answer the questions at the end ofeach situation.

1. The December 31 year-end financial statements of SAMOA COMPANY containedthe following errors:

Dec. 31, 2014 Dec. 31, 2015

Ending inventory P48,000 understated P40,500 overstatedDepreciation expense P11,500 understated -------

An insurance premium of P330,000 was prepaid in 2014 covering the years 2014,2015, and 2016. The entire amount was charged to expense in 2014. In addition,on December 31, 2015, a fully depreciated machinery was sold for P75,000 cash,but the sale was not recorded until 2016. There were no other errors during 2014and 2015, and no corrections have been made for any of the errors. Ignore incometax effects.

46. What is the total effect of the errors on Samoa’s 2015 net income?A. P123,500 overstatementB. P27,500 overstatementC. P192,500 understatementD. P177,500 understatement

Page 10 of 26 Pages

AUDITING PROBLEMS

47. What is the total effect of the errors on the amount of Samoa’s working capitalat December 31, 2015?A. P75,500 overstatementB. P40,500 overstatementC. P225,500 understatementD. P144,500 understatement

48. What is the total effect of the errors on the balance of Samoa’s retainedearnings at December 31, 2015?A. P156,000 understatementB. P87,000 overstatementC. P133,000 understatementD. P85,000 understatement

2. CHILE CO. reported pretax incomes of P505,000 and P387,000 for the yearsended December 31, 2014 and 2015, respectively. However, the auditor noted thatthe following errors had been made:

a. Sales for 2014 included amounts of P191,000 which had been received in cashduring 2014, but for which the related goods were shipped in 2015. Title did notpass to the buyer until 2015.

b. The inventory on December 31, 2014, was understated by P43,200.

c. The company’s accountant, in recording interest expense for both 2014 and2015 on bonds payable, made the following entry on an annual basis:

Interest expense 75,000Cash 75,000

The bonds have a face value of P1,250,000 and pay a nominal interest rate of6%. They were issued at a discount of P75,000 on January 1, 2014, to yield aneffective interest rate of 7%.

d. Ordinary repairs to equipment had been erroneously charged to the Equipmentaccount during 2014 and 2015. Repairs of P42,500 and P47,000 had beenincurred in 2014 and 2015, respectively. In determining depreciation charges,Chile applies a rate of 10% to the balance in the Equipment account at the endof the year.

49. What is the corrected pretax income for 2014?A. P303,200 B. P225,300 C. P311,700 D. P307,450

50. What is the corrected pretax income for 2015?A. P480,042 B. P484,292 C. P575,392 D. P488,992

-----------------------------oooOOOooo-----------------------------

PROBLEM NO. 10

The following are two (2) unrelated situations. Answer the questions at the end ofeach situation.

OMEGA COMPANY sells its products in expensive, reusable containers. Thecustomer is charged a deposit for each container delivered and receives a refund foreach container returned within two years after the year of delivery. Omegaaccounts for the containers not returned within the time limit as being sold at thedeposit amount. Information for 2015 is as follows:

Containers held by customers atDecember 31, 2014,from deliveries in: 2013 85,000

2014 240,000 325,000

Page 11 of 26 Pages

AUDITING PROBLEMS

Containers delivered in 2015 430,000Containers returned in 2015from deliveries in: 2013 57,500

2014 140,0002015 157,000 354,500

51. How much revenue from container sales should be recognized for 2015?A. P127,500 B. P267,500 C. P27,500 D. P85,000

52. What is the total amount of Omega Company’s liability for returnablecontainers at December 31, 2015?A. P373,000 B. P400,500 C. P267,500 D. P430,000

DP, INC., a dealer of household appliances, sells washing machines at an averageprice of P8,100. The company also offers to each customer a separate 3-yearwarranty contract for P810 that requires the company to provide periodicmaintenance services and to replace defective parts. During 2015, DP sold 300washing machines and 270 warranty contracts for cash. The company estimatesthat the warranty costs are P180 for parts and P360 for labor.

Assume sales occurred on December 31, 2015. DP’s policy is to recognize incomefrom the warranties on a straight-line basis. In 2016, DP incurred actual costsrelative to 2015 warranty sales of P18,000 for parts and P36,000 for labor.

53. What liability relative to these transactions would appear on the December 31,2015, statement of financial position and how would it be classified?

Current NoncurrentA. P145,800 P72,900B. P72,900 P72,900C. P72,900 P145,800D. P 0 P218,700

54. What amount of warranty expense would be shown on the income statementfor the year ended December 31, 2015?A. P18,000 B. P 0 C. P 36,000 D. P54,000

55. What liability relative to the 2015 warranties would appear on the December31, 2016, statement of financial position and how would it be classified?

Current NoncurrentA. P145,800 P72,900B. P72,900 P72,900C. P72,900 P145,800D. P145,800 P 0

-----------------------------oooOOOooo-----------------------------

PROBLEM NO. 11

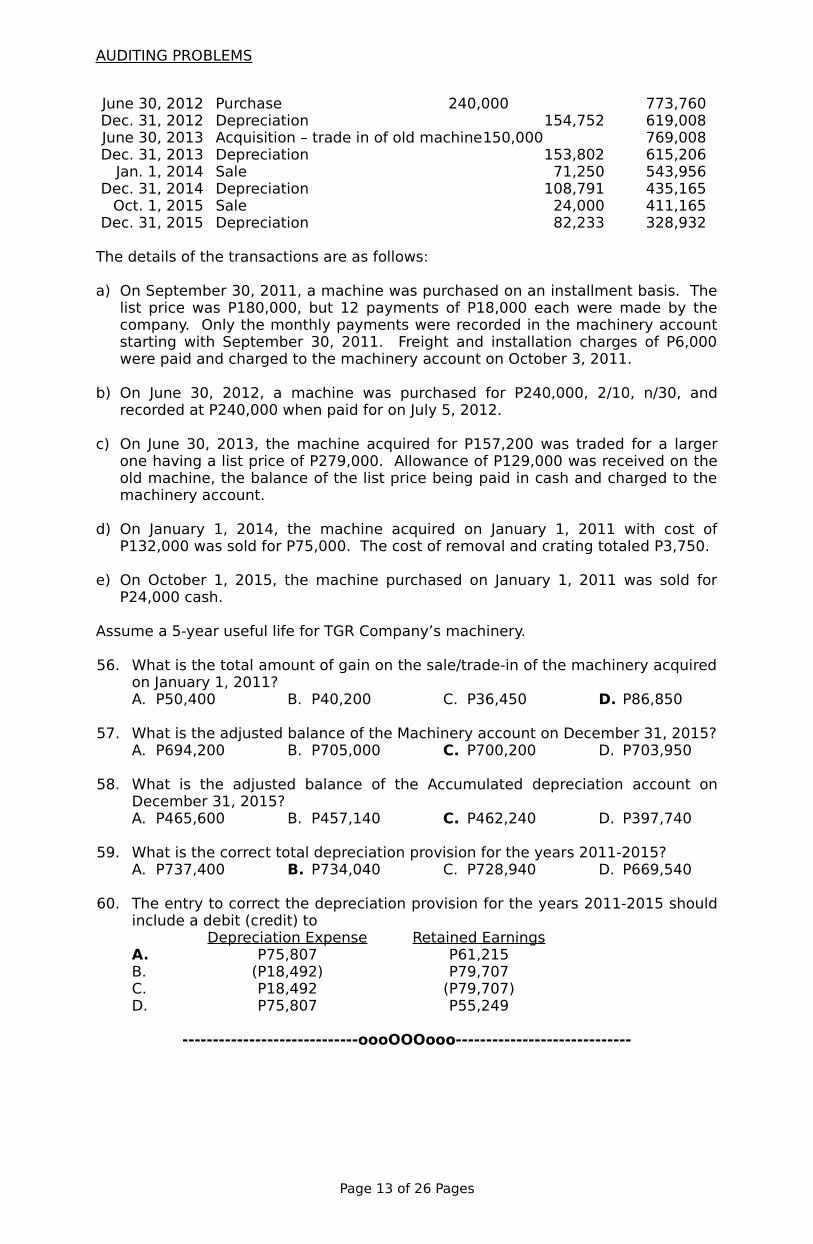

The TGR Company commenced operations on January 1, 2011. The company’smachinery account is shown below.

Date Particulars Debit Credit BalanceJan. 1, 2011 Purchase P157,200

120,000132,000 P409,200

Sept. 30, 2011 Purchase on installmentPayments from Sept. to Dec. 72,000 481,200

Oct. 3, 2011 Freight and installation 6,000 487,200Dec. 31, 2011 Depreciation P97,440 389,760

2012 Installment payments for acquisitionon Sept. 30, 2011 144,000 533,760

Page 12 of 26 Pages

AUDITING PROBLEMS

June 30, 2012 Purchase 240,000 773,760Dec. 31, 2012 Depreciation 154,752 619,008June 30, 2013 Acquisition – trade in of old machine150,000 769,008Dec. 31, 2013 Depreciation 153,802 615,206

Jan. 1, 2014 Sale 71,250 543,956Dec. 31, 2014 Depreciation 108,791 435,165

Oct. 1, 2015 Sale 24,000 411,165Dec. 31, 2015 Depreciation 82,233 328,932

The details of the transactions are as follows:

a) On September 30, 2011, a machine was purchased on an installment basis. Thelist price was P180,000, but 12 payments of P18,000 each were made by thecompany. Only the monthly payments were recorded in the machinery accountstarting with September 30, 2011. Freight and installation charges of P6,000were paid and charged to the machinery account on October 3, 2011.

b) On June 30, 2012, a machine was purchased for P240,000, 2/10, n/30, andrecorded at P240,000 when paid for on July 5, 2012.

c) On June 30, 2013, the machine acquired for P157,200 was traded for a largerone having a list price of P279,000. Allowance of P129,000 was received on theold machine, the balance of the list price being paid in cash and charged to themachinery account.

d) On January 1, 2014, the machine acquired on January 1, 2011 with cost ofP132,000 was sold for P75,000. The cost of removal and crating totaled P3,750.

e) On October 1, 2015, the machine purchased on January 1, 2011 was sold for

P24,000 cash.

Assume a 5-year useful life for TGR Company’s machinery.

56. What is the total amount of gain on the sale/trade-in of the machinery acquiredon January 1, 2011?A. P50,400 B. P40,200 C. P36,450 D. P86,850

57. What is the adjusted balance of the Machinery account on December 31, 2015?A. P694,200 B. P705,000 C. P700,200 D. P703,950

58. What is the adjusted balance of the Accumulated depreciation account onDecember 31, 2015?A. P465,600 B. P457,140 C. P462,240 D. P397,740

59. What is the correct total depreciation provision for the years 2011-2015?A. P737,400 B. P734,040 C. P728,940 D. P669,540

60. The entry to correct the depreciation provision for the years 2011-2015 shouldinclude a debit (credit) to

Depreciation Expense Retained EarningsA. P75,807 P61,215B. (P18,492) P79,707C. P18,492 (P79,707)D. P75,807 P55,249

-----------------------------oooOOOooo-----------------------------

Page 13 of 26 Pages

AUDITING PROBLEMS

SECOND SET OF PROBLEMS

PROBLEM NO. 1

You have been assigned to audit the financial statements of AYALA MERCHANTSCORPORATION for the year 2015. The company is a dealer of appliances and hasseveral branches in Metro Manila. Its main office is located in Makati City. You weregiven by the company controller the unadjusted balances of the items to beincluded in the company’s statement of financial position and statement of incomeas of and for the year ended December 31, 2015. Audit findings are as follows:

I. AUDIT OF CASH

A cash count was conducted by your staff on January 7, 2016. The petty cashfund of P60,000 maintained by the company on an imprest basis relected abalance of P22,750. Unreplenished expenses totaled P37,250 of which P9,510pertains to January 2016.

You were furnished a copy of the company’s bank reconciliation statement withChartered Bank as follows:

Balance per bank P277,994Add: Deposit in transit 248,836

Bank debit memos 712,750Returned check 63,000

Less: Outstanding checks (174,580)Book error (72,000)

Balance per books P1,056,000

Your review of the reconciliation statement disclosed the following:

1. Postdated checks totaling P107,400 were included as part of the deposit intransit. These represent collections from various customers whose accountshave been outstanding for less than three months. These checks wereactually deposited on January 8, 2016.

2. Included in the deposit in transit is a check from a customer for P63,000 whichwas returned by the bank on December 27, 2015 for insufficiency of funds.This account has been outstanding for over six months. The check wasreplaced by the customer on January 15, 2016.

3. The bank debited the account of Ayala Merchants for P710,000 as payment ofnotes payable including interest of P10,000 due on December 26, 2015. Thiswas not recorded as of year-end.

4. A check was cleared by the bank as P30,900 but was recorded by thebookkeeper as P102,900. This was in payment of accounts payable.

5. Bank service charges totaling P2,750 were not recorded.

II. AUDIT OF ACCOUNTS RECEIVABLE AND ALLOWANCE FOR DOUBTFUL ACCOUNTS

It is the company’s policy to provide allowance for doubtful accounts as follows:

Less than 3 months P2,500,960 1%3 to 6 months 843,200 5%Over 6 months 274,500 10%

Page 14 of 26 Pages

AUDITING PROBLEMS

Total P3,618,660

An analysis of the accounts receivable schedule showed that several longoutstanding accounts for more than a year totaling P152,460 should be written-off.

III. AUDIT OF MARKETABLE SECURITIES – TRADING

The company’s equity portfolio as of year-end showed the following:

Total Market ValueShares Cost per Share

Bacnotan Cement 7,000 P108,500 P16.00Fil-Estate 10,000 195,000 19.75Ionics 2,400 49,200 24.00La Tondena 2,000 67,000 26.00Selecta 8,000 31,600 1.20Union Bank 1,600 50,880 27.50

P502,180

The securities are listed in the stock exchange. The company follows the fairvalue accounting.

IV. AUDIT OF NOTES RECEIVABLE

The note receivable amounting to P1,300,000 represents a loan granted to asubsidiary. This is covered by a promissory note with interest at 15% per annumdated November 1, 2015. No interest has been accrued on the note as ofDecember 31, 2015.

V. AUDIT OF PREPAYMENTS

Prepaid expenses account consists of the following:

Prepaid advertising P 640,000Prepaid insurance 490,000Prepaid rent 420,000Unused office supplies 361,000

P1,911,000

Ayala Merchants renewed its contract with an advertising agency for the annualpromotion as well as the regular advertisement of its products. It paid a total ofP640,000, P100,000 of which is for the Christmas promotion while the balance isfor the regular promotion and which will run for one year starting on August 1,2015. Payment was made on July 20, 2015, and the total amount was reflectedas prepaid advertising.

The company leases the main office and store in Makati City at a monthly rentalof P140,000. On November 5, 2015, a check for P420,000 was issued inpayment of three-month rental as per renewal contract which was effective onNovember 1, 2015. Rental deposit remained at three months and is includedunder other assets.

The company’s delivery equipment is insured with Fortune Insurance Corporationfor a total coverage of P2.4 million. Total payment made on November 16, 2015for the renewal amounted to P490,000 which covers the period from November1, 2015 to November 1, 2016. No adjustment has been made as of December31, 2015.

To take advantage of volume discount ranging from 10% to 20%, the companybuys office and store supplies on a bulk basis. The staff-in-charge boughtsupplies worth P220,000 on June 10, 2015 and included the same in their officesupplies inventory. As at year-end, unused office supplies amount to P102,500.

Page 15 of 26 Pages

AUDITING PROBLEMS

VI. AUDIT OF INVENTORIES

A physical count of inventories was conducted simultaneously in all stores onDecember 29 and 20, 2015. Your review of the list submitted by the accountantdisclosed the following:

1. Some deliveries made in December 2015 have not been invoiced andrecorded as of year-end. These items had a selling price of P146,940 withterm of 15 days. The corresponding cost was already deducted from theending inventory.

2. Goods on consignment to Ayala Merchants totaling P356,000 were includedin the inventory list.

3. Some appliances worth P138,500 were recorded twice in the inventory list.

4. Goods costing P153,800 purchased and paid on December 26 was receivedon January 4, 2016. The goods were shipped by the supplier on December28, FOB shipping point.

VII. AUDIT OF PROPERTY, PLANT AND EQUIPMENT

The company purchased additional equipment worth P268,000 on June 30, 2015.At the date of purchase, it incurred the following additional costs which werecharged to repairs and maintenance account:

Freight-in P30,400Installation cost 13,000 Total P43,400

The above equipment has an estimated useful life of ten years and estimatedsalvage value of P20,000. Depreciation for the above equipment has beenprovided based on original cost.

The company discarded some store equipment on October 1, 2015, realizing nosalvage value. The cost of these equipment amounted to P165,520 with anaccumulated depreciation of P138,620 as of December 31, 2015. Depreciationbooked from October 1, 2015 to year-end was P10,480. No entry was made onthe disposal of the property.

VIII. AUDIT OF ACCRUED EXPENSES

Some expenses for December 2015 were recorded when paid in January 2016.These are as follows:

Electric bills P73,400Commission of sales agents 57,000Telephone charges 42,500Minor repair of delivery equipment 21,340Water bills 18,760 Total P213,000

IX. AUDIT OF LIABILITIES

Ayala Merchants obtained a one-year loan from Chartered Bank amounting toP2.6 million at an interest rate of 16% per annum on October 1, 2015. Accruedinterest on this loan was not taken up at year-end.

X. OTHER AUDIT FINDINGS

A review of the minutes of meeting showed that a 10% cash dividend wasdeclared to shareholders of record as of December 15, 2015, payable on January31, 2016.

Ayala Merchants Corporation

Page 16 of 26 Pages

AUDITING PROBLEMS

UNADJUSTED TRIAL BALANCEDecember 31, 2015

Debit CreditPetty cash fund P 60,000Cash in bank 1,056,000Trading securities 483,640Accounts receivable – trade 3,618,660Allowance for doubtful accounts P 110,360Notes receivable 1,300,000Inventories 7,274,900Prepaid advertising 640,000Prepaid insurance 490,000Prepaid rent 420,000Office supplies inventory 361,000Furniture and fixtures 1,298,400Delivery equipment 2,770,000Accumulated depreciation 1,177,500Other assets 548,000Accounts payable – trade 2,356,320Notes payable 3,300,000Accrued expenses 169,040Bonds payable 5,000,000Discount on bonds payable 500,000Ordinary share capital 5,400,000Retained earnings 792,160Sales 13,078,000Cost of goods sold 8,034,000Operating expenses 3,357,000Other income 1,453,500Other charges 625,280

P32,836,880 P32,836,880

Based on the above information, determine the adjusted balances of the following:(Ignore tax implications.)

1. Petty cash fundA. P37,250 B. P60,000 C. P22,750 D. P32,260

2. Cash in bankA. P522,650 B. P450,650 C. P1,056,000 D. P244,850

3. Trading securitiesA. P403,640 B. P502,180 C. P491,240 D. P472,700

4. Accounts receivableA. P3,936,000 B. P3,618,660 C. P3,783,540 D. P3,613,140

5. Allowance for doubtful accountsA. P110,360 B. P152,640 C. P130,316 D. P88,217

6. Notes and interest receivableA. P1,331,960 B. P1,332,160 C. P1,332,500 D. P1,300,000

7. InventoriesA. P6,934,200 B. P7,274,900 C. P7,290,200 D. P6,780,400

8. Prepaid insuranceA. P449,167 B. P408,333 C. P490,000 D. P428,750

9. Prepaid rentA. P140,000 B. P 0 C. P420,000 D. P280,000

Page 17 of 26 Pages

AUDITING PROBLEMS

10. Prepaid advertisingA. P325,000 B. P640,000 C. P373,334 D. P315,000

11. Office supplies inventoryA. P258,500 B. P117,500 C. P361,000 D. P102,500

12. Total current assetsA. P14,0333,612 B. P13,523,866 C. P13,677,666 D. P13,537,666

13. Property, plant, and equipmentA. P4,068,400 B. P2,905,228 C. P3,946,280 D. P3,902,880

14. Accumulated depreciationA. P1,038,880 B. P1,041,050 C. P1,177,500 D. P1,179,672

15. Accounts payableA. P2,525,360 B. P2,428,320 C. P2,597,360 D. P2,356,320

16. Interest payableA. P104,000 B. P16,178 C. P4,000 D. P27,644

17. Total current liabilitiesA. P6,803,798 B. P6,103,798 C. P6,054,360 D. P5,603,798

18. SalesA. P13,068,440 B. P13,078,000 C. P13,224,940 D. P12,339,500

19. Cost of goods soldA. P8,034,000 B. P8,236,200 C. P8,018,700 D. P8,374,700

20. Operating expensesA. P4,296,514 B. P3,357,000 C. P4,341,514 D. P4,621,514

-----------------------------oooOOOooo-----------------------------

PROBLEM NO. 2

To substantiate the existence of the accounts receivable balances as at December31, 2015 of LUKAS COMPANY, you have decided to send confirmation requests tocustomers. Below is a summary of the confirmation replies together with theexceptions and audit findings. Gross profit on sales is 20%. The company is underthe perpetual inventory method.

Name of Custome

r

BalancePer

Books

CommentsFrom Customers Audit Findings

Concordia

P150,000 P90,000 was returned on December30, 2015. Correct balance as isP60,000.

Returned goods werereceived December 31,2015.

Falcon P30,000 Your CM representing price adjustmentdated December 28, 2015 cancelsthis.

The CM was taken up byLukas Company in 2016.

Lazaro P144,000 You have overpriced us by P150.Correct price should be P300.

The complaint is valid.

Silang P112,500 We received the goods only onJanuary 6, 2016.

Term is shipping point.Shipped in 2015.

Yakal P135,000 Balance was offset by our Decembershipment of your raw materials.

Lukas Company creditedaccounts payable forP135,000 to recordpurchases. Yakal is asupplier.

Page 18 of 26 Pages

AUDITING PROBLEMS

21. If the necessary adjusting journal entry is made regarding the case ofConcordia, the net income willA. Decrease by P18,000. C. Increase by P18,000.B. Decrease by P90,000. D. Increase by P90,000.

22. The effect on 2015 net income of Lukas Company of its failure to record the CMinvolving transaction with Falcon:A. P30,000 over. C. P6,000 over.B. P30,000 under. D. P6,000 under.

23. The overstatement of receivable from Lazaro isA. P96,000 B. P24,000 C. P72,000 D. P48,000

24. The accounts receivable from Silang isA. Correctly stated. C. P112,500 under.B. P112,500 over. D. P225,000 under.

25. The adjusting entry to correct the receivable from Yakal isA. Purchases 135,000

Accounts receivable 135,000B. Accounts payable 135,000

Purchases 135,000C. Accounts receivable 135,000

Accounts payable 135,000D. Accounts payable 135,000

Accounts receivable 135,000-----------------------------oooOOOooo-----------------------------

PROBLEM NO. 3

Palito, CPA, has just accepted an engagement to audit the financial statements ofCrocodile, Inc. for the year ending December 31, 2015. After obtaining anunderstanding of the client’s design of the accounting and internal control systemsand their operation, he then proceeded in performing test of controls related toproduction cycle.

The following questions related to test of controls of the production cycle:

26. Which of the following auditing procedures probably would provide the mostreliable evidence concerning the entity’s assertion of rights and obligationsrelated to inventories:A. Trace the test counts noted during the entity’s physical count to the entity’s

summarization of quantities.B. Inspect agreements to determine whether any inventory is pledged as

collateral or subject to any liens.C. Select the last few shipping documents used before the physical count and

determine whether the shipments were recorded as sales.D. Inspect the open purchase order file for significant commitments that

should be considered for disclosure.

27. Which of the following internal control activities most likely addresses thecompleteness assertion for inventory?A. The work-in-process account is periodically reconciled with subsidiary

inventory records.B. Employees responsible for custody of finished goods do not perform the

receiving functionC. Receiving reports are prenumbered and the numbering sequence is checked

periodically.D. There is a separation of duties between the payroll department and

inventory accounting personnel.

Page 19 of 26 Pages

AUDITING PROBLEMS

28. From the auditor’s point of view, inventory counts are more acceptable prior tothe year-end whenA. Internal control is weak.B. Accurate perpetual inventory records are maintained.C. Inventory is slow moving.D. Significant amounts of inventory are held on a consignment basis.

29. A retailer’s physical count of inventory was higher than that shown by theperpetual records. Which of the following could explain the difference?A. Inventory items had been counted but the tags placed on the items had not

been taken off and added to the inventory accumulation sheets.B. Credit memos for several items returned by customers had not been

recorded.C. No journal entry had been made on the retailer’s books for several items

returned to its suppliers.D. An item purchased FOB shipping point had not arrived at the date of the

inventory count and had not been reflected in the perpetual records.

30. An auditor will usually trace the details of the test counts made during theobservation of physical inventory counts to a final inventory compilation. Thisaudit procedure is undertaken to provide evidence that items physicallypresent and observed by the auditor at the time of the physical inventorycount areA. Owned by the client.B. Not obsolete.C. Physically present at the time of the preparation of the final inventory

schedule.D. Included in the final inventory schedule.

-----------------------------oooOOOooo-----------------------------

PROBLEM NO. 4

A portion of the SPARK COMPANY’s statement of financial position appears asfollows:

December 31, 2015 December 31, 2014Assets:

Cash P353,300 P100,000Notes receivable 0 25,000Inventory ? 199,875

Liabilities:Accounts payable ? 75,000

Spark Company pays for all operating expenses with cash and purchases allinventory on credit. During 2015, cash totaling P471,700 was paid on accountspayable. Operating expenses for 2015 totaled P220,000. All sales are cash sales.The inventory was restocked by purchasing 1,500 units per month and valued byusing periodic FIFO. The unit cost of inventory was P32.60 during January 2015 andincreased P0.10 per month during the year. Spark sells only one product. All salesare made for P50 per unit. The ending inventory for 2014 was valued at P32.50 perunit.

Based on the preceding information, compute the following:

31. Number of units sold during 2015A. 7,066 B. 18,400 C. 4,268 D. 13,400

32. Accounts payable balance at December 31, 2015A. P190,100 B. P50,000 C. P199,100 D. P200,000

33. Inventory quantity on December 31, 2015A. 5,750 B. 2,750 C. 17,084 D. 10,750

Page 20 of 26 Pages

AUDITING PROBLEMS

34. Cost of inventory on December 31, 2015A. P187,450 B. P186,875 C. P192,950 D. P189,660

35. Cost of goods sold for the year ended December 31, 2015A. P609,125 B. P609,700 C. P606,915 D. P603,625

-----------------------------oooOOOooo-----------------------------

PROBLEM NO. 5

A depreciation schedule for semi-trucks of ISIDRO MANUFACTURING COMPANY wasrequested by your auditor soon after December 31, 2015, showing the additions,retirements, depreciation, and other data affecting the income of the company inthe 4-year period 2012 to 2015, inclusive.

The following data were ascertained.Balance of Trucks account, Jan. 1, 2012Truck No. 1 purchased Jan. 1, 2009, cost P180,000Truck No. 2 purchased July 1, 2009, cost 220,000Truck No. 3 purchased Jan. 1, 2011, cost 300,000Truck No. 4 purchased July 1, 2011, cost 240,000Balance, Jan. 1, 2012 P940,000

The Accumulated Depreciation—Trucks account previously adjusted to January 1,2012, and entered in the ledger, had a balance on that date of P302,000(depreciation on the four trucks from the respective dates of purchase, based on a5-year life, no salvage value). No charges had been made against the accountbefore January 1, 2012.

Transactions between January 1, 2012, and December 31, 2015, which wererecorded in the ledger, are as follows.

July 1, 2012 Truck No. 3 was traded for a larger one (No. 5), the agreed purchaseprice of which was P400,000. Isidro Mfg. Co. paid the automobiledealer P220,000 cash on the transaction. The entry was a debit toTrucks and a credit to Cash, P220,000. The transaction has commercialsubstance.

Jan. 1, 2013 Truck No. 1 was sold for P35,000 cash; entry debited Cash and creditedTrucks, P35,000.

July 1, 2014 A new truck (No. 6) was acquired for P420,000 cash and was chargedat that amount to the Trucks account. (Assume truck No. 2 was notretired.)

July 1, 2014 Truck No. 4 was damaged in a wreck to such an extent that it was soldas junk for P7,000 cash. Isidro Mfg. Co. received P25,000 from theinsurance company. The entry made by the bookkeeper was a debit toCash, P32,000, and credits to Miscellaneous Income, P7,000, andTrucks, P25,000.

Entries for depreciation had been made at the close of each year as follows: 2012,P210,000; 2013, P225,000; 2014, P250,500; 2015, P304,000.

36. What is the total depreciation expense for the year ended December 31, 2012?A. P180,000 B. P198,000 C. P172,000 D. P228,000

37. What is the gain (loss) on trade in of Truck #3 on July 1, 2012?A. (P30,000) B. P10,000 C. (P60,000) D. P190,000

38. What is the net book value of the Trucks on December 31, 2015?A. P414,000 B. P348,000 C. P228,500 D. P894,000

Page 21 of 26 Pages

AUDITING PROBLEMS

39. The total depreciation expense recorded for the 4-year period (2012-2015) isoverstated byA. P185,500 B. P265,500 C. P287,500 D. P275,500

40. Assuming that the books have not been closed for 2015, what is the compoundjournal entry on December 31, 2015 to correct the company’s errors for the 4-year period (2012-2015)?A. Accumulated depreciation 629,500

Trucks 480,000Retained earnings 9,500Depreciation expense 140,000

B. Accumulated depreciation 665,500Trucks 480,000Retained earnings 45,500Depreciation expense 140,000

C. Accumulated depreciation 665,500Trucks 480,000Retained earnings 185,500

D. Accumulated depreciation 665,500Trucks 665,500-----------------------------oooOOOooo-----------------------------

PROBLEM NO. 6

The cash account of NUNAL COMPANY shows the following activities:

Date Debit Credit BalanceNov. 30 Balance P345,000Dec. 2 November bank charges P 150 344,850

4 November bank credit for notesreceivable collected P 30,000 374,850

15 NSF check 3,900 370,95020 Loan proceeds 145,500 516,45021 December bank charges 180 516,27031 Cash receipts book 2,121,900 2,638,17031 Cash disbursements book 1,224,000 1,414,170

CASH BOOKSRECEIPTS PAYMENTS

Date OR No. Amount Check No. AmountDec. 1 110-120 P 33,000 801 P 6,000

2 121-136 63,900 802 9,0003 137-150 60,000 803 3,0004 151-165 168,000 804 9,0005 166-190 117,000 805 36,0008 191-210 198,000 806 57,0009 211-232 264,000 807 78,000

10 233-250 231,000 808 90,00011 251-275 63,000 809 183,00012 276-300 90,000 810 21,00015 301-309 165,000 811 24,00016 310-350 24,000 812 48,00017 351-390 57,000 813 60,00018 391-420 27,000 814 66,00019 421-480 51,000 816 108,00022 481-500 63,000 817 33,00023 501-525 96,000 818 150,00023 - - 819 21,00023 - - 820 12,00026 526-555 222,000 821 9,00028 556-611 15,000 822 36,00028 - - 823 39,000

Page 22 of 26 Pages

AUDITING PROBLEMS

29 612-630 114,000 824 87,00029 - - 825 6,00029 - - 826 33,000

Totals P2,121,900 P1,224,000

BANK STATEMENT

Date Check Charges CreditsDec. 1 792 P 7,500 P 25,500

2 802 9,000 33,0003 - - 63,9004 804 9,000 60,0005 EC 243,000 243,0008 805 36,000 285,0009 CM 16 - 36,000

10 799 21,150 462,00011 DM 57 3.900 231,00012 808 90,000 63,00015 803 3,000 -16 809 183,000 255,00017 DM 61 180 24,00018 813 60,000 57,00019 CM 20 - 145,50022 815 18,000 -23 816 108,000 141,00023 811 24,000 -23 801 6,000 -26 814 66,000 96,00028 818 150,000 222,00028 DM 112 360 -29 821 9,000 15,00029 CM 36 - 36,00029 820 12,000 -

Totals P1,059,090 P2,493,900

Additional information:

1. DMs 61 and 112 are for service charges.2. EC is error corrected.3. DM 57 is for an NSF check.4. CM 20 is for loan proceeds, net of P450 interest charges for 90 days.5. CM 16 is for the correction of an erroneous November bank charge.6. CM 36 is for customers’ notes collected by bank in December.7. Bank balance on December 31 is P1,776,810

Based on the preceding information, determine the following:

41. Outstanding checks at November 30A. P39,150 B. P28,650 C. P21,150 D. P46,650

42. Outstanding checks at December 31A. P459,000 B. P477,000 C. P441,000 D. P487,650

43. Deposit in transit at November 30A. P58,500 B. P145,500 C. P 0 D. P25,500

44. Deposit in transit at December 31A. P114,000 B. P139,500 C. P132,000 D. P 0

45. Adjusted book balance at November 30A. P410,850 B. P345,000 C. P375,000 D. P374,850

46. Adjusted bank receipts for the month of DecemberA. P2,297,400 B. P2,291,400 C. P2,303,400 D. P2,321,400

Page 23 of 26 Pages

AUDITING PROBLEMS

47. Adjusted book disbursements for the month of DecemberA. P1,228,440 B. P1,246,440 C. P1,210,440 D. P1,246,620

48. Adjusted bank balance at December 31A. P1,449,810 B. P1,674,810 C. P1,431,810 D. P1,776,810

49. Unadjusted bank balance at November 30A. P555,060 B. P94,560 C. P1,776,810 D. P342,000

50. The best evidence regarding year-end bank balances is documented in theA. Cutoff bank statements.B. Bank reconciliations.C. Interbank transfer schedule.D. Bank deposit lead schedule.

-----------------------------oooOOOooo-----------------------------

PROBLEM NO. 7

MINA MINING CO. has acquired a tract of mineral land for P50,000,000. Mina Miningestimates that the acquired property will yield 150,000 tons of ore with sufficientmineral content to make mining and processing profitable. It further estimates that7,500 tons of ore will be mined the first and last year and 15,000 tons every year inbetween. (Assume 11 years of mining operations.) The land will have a residualvalue of P1,550,000.

Mina Mining builds necessary structures and sheds on the site at a total cost ofP12,000,000. The company estimates that these structures can be used for 15years but, because they must be dismantled if they are to be moved, they have noresidual value. Mina Mining does not intend to use the buildings elsewhere.

Mining machinery installed at the mine was purchased secondhand at a total cost ofP3,600,000. The machinery cost the former owner P9,000,000 and was 50%depreciated when purchased. Mina Mining estimates that about half of thismachinery will still be useful when the present mineral resources have beenexhausted but that dismantling and removal costs will just about offset its value atthat time. The company does not intend to use the machinery elsewhere. Theremaining machinery will last until about one-half the present estimated mineral orehas been removed and will then be worthless. Cost is to be allocated equallybetween these two classes of machinery.

51. What are the estimated depletion and depreciation charges for the 1st year?Depletion Depreciation

A. P4,845,000 P870,000B. P4,845,000 P780,000C. P2,422,500 P870,000D. P2,422,500 P780,000

52. What are the estimated depletion and depreciation charges for the 5th year?Depletion Depreciation

A. P2,422,500 P1,740,000B. P2,422,500 P1,560,000C. P4,845,000 P1,560,000D. P4,845,000 P1,740,000

53. What are the estimated depletion and depreciation charges for the 6th year?Depletion Depreciation

A. P2,422,500 P1,560,000B. P2,422,500 P1,740,000C. P4,845,000 P1,560,000D. P4,845,000 P1,740,000

54. What are the estimated depletion and depreciation charges for the 7th year?

Page 24 of 26 Pages

AUDITING PROBLEMS

Depletion DepreciationA. P2,422,500 P1,380,000B. P2,422,500 P1,560,000C. P4,845,000 P1,380,000D. P4,845,000 P1,560,000

55. What are the estimated depletion and depreciation charges for the 11th year?Depletion Depreciation

A. P4,845,000 P1,380,000B. P4,845,000 P690,000C. P2,422,500 P1,380,000D. P2,422,500 P690,000

-----------------------------oooOOOooo-----------------------------PROBLEM NO. 8

The HVR Company included the following in its notes receivable as of December 31,2015:

Note receivable from sale of land P2,640,000Note receivable from consultation 3,600,000Note receivable from sale of equipment 4,800,000

The following transactions during 2015 and other information relate to thecompany’s notes receceivable:

a) On January 1, 2015, HVR Company sold a tract of land to Triple X Company. Theland, purchased 10 years ago, was carried on HVR’s books at P1,500,000. HVRreceived a noninterest-bearing note for P2,640,000 from Triple X. The note isdue on December 31, 2016. There was no established exchange price for theland. The prevailing interest rate for this note on January 1, 2015 was 10%.

b) On January 1, 2015, HVR Company received a 5%, P3,600,000 promissory notein exchange for the consultation services rendered. The note will mature onDecember 31, 2017, with interest receivable every December 31. The fair valueof the services rendered is not readily determinable. The prevailing rate ofinterest for a note of this type was 10% on January 1, 2015.

c) On January 1, 2015, HVR Company sold an old equipment with a carryingamount of P4,800,000, receiving P7,200,000 note. The note bears an interestrate of 4% and is to be repaid in 3 annual installments of P2,400,000 (plusinterest on the outstanding balance). HVR received the first payment onDecember 31, 2015. There is no established market value for the equipment.The market interest rate for similar notes was 14% on January 1, 2015.

Note: Round off present value factors to four decimal places and final answers tothe nearest hundred.

56. What amount of consultation fee revenue should be recognized in 2015?A. P3,600,000 B. P2,705,000 C. P4,047,500 D. P3,152,500

57. What amount should be reported as gain on sale of equipment?A. P994,800 B. P2,400,000 C. P1,162,700 D. P1,237,300

58. The amount to be reported as noncurrent notes receivable on December 31,2015 isA. P7,482,200 B. P6,037,300 C. P5,477,500 D. P7,877,600

59. The amount to be reported as current notes receivable on December 31, 2015isA. P4,800,000 B. P2,400,200 C. P4,404,900 D. P7,440,000

Page 25 of 26 Pages

AUDITING PROBLEMS

60. How much interest income should be recognized in 2015?A. P974,200 B. P756,000 C. P1,378,700 D. P1,160,500

--- END OF EXAMINATION ---

Page 26 of 26 Pages