Embed Size (px)

Citation preview

Auditing: A Journal of Practice & Theory American Accounting AssociationVol. 33, No. 4 DOI: 10.2308/ajpt-50783November 2014pp. 119–166

Client-Auditor Supply Chain Relationships,Audit Quality, and Audit Pricing

Karla M. Johnstone, Chan Li, and Shuqing Luo

SUMMARY: We investigate the association between auditors’ supply chain knowledge

and companies’ audit quality and audit pricing. Auditor supply chain knowledge is a

specialized understanding of information and processes regarding accounting and

auditing issues that relates to both a supplier and its major customer, regardless of

industry commonalities, that is particularly useful for understanding complexities

associated with the revenue cycle. We find that auditors’ supply chain knowledge at

the city level is associated with higher audit quality and lower audit fees, compared to

companies employing auditors with supply chain knowledge at the national level or

employing auditors without supply chain knowledge. Such effects are stronger for

supplier companies that derive a high proportion of revenue from their major customers,

and when the revenue cycle for the supplier companies is more important. We obtain

these results while controlling for the usual determinants of audit quality and fees, along

with auditors’ industry specialization.

Keywords: audit pricing; audit quality; supply chain relationships; industry expertise.

INTRODUCTION

Supply chain relationships between suppliers and their major customers are of strategic

importance in the modern economy, and prior research has investigated the effects of these

relationships on partners within the supply chain. However, little is known about how otherconstituents in capital markets, such as auditors, might be affected by, or might respond to, supply

Karla M. Johnstone is a Professor at the University of Wisconsin–Madison, Chan Li is anAssociate Professor at the University of Pittsburgh, and Shuqing Luo is an Assistant Professor atthe National University of Singapore.

We thank participants at research workshops at National University of Singapore, The University of Auckland, TheUniversity of Melbourne, The University of Kansas, and University of Wisconsin–Madison for comments on drafts ofthis paper. We especially appreciate the comments of Jean Bedard, Steven Cahan, Mark DeFond, David Emanuel, DavidHay, W. Robert Knechel, Brian Mayhew, Vic Naiker, Jay Thibodeau, and Terry Warfield. Karla M. Johnstoneacknowledges support through her professorship with EY, as well as the Andersen Center for Financial Reporting at theUniversity of Wisconsin–Madison. We thank the AAA’s Auditing Section for acknowledging this manuscript with the‘‘Best Paper Award’’ for the 2012 Midyear Meeting. Finally, we thank two anonymous reviewers and our editor forexcellent suggestions and positive feedback throughout the review process.

Editor’s note: Accepted by W. Robert Knechel.

Submitted: April 2013Accepted: April 2014

Published Online: April 2014

119

chain relationships. In this study, we investigate whether audit firms’ supply chain knowledge is

associated with differential audit quality and audit pricing. We define auditor supply chain

knowledge as specialized understanding of information and processes regarding accounting and

auditing issues that relates to both a supplier and its major customer, regardless of industry

commonalities, that is particularly useful for understanding complexities associated with the

revenue cycle.

We examine audit quality and pricing implications of auditor supply chain knowledge for

several reasons. First, supply chain relationships are quite common. About 35 percent of Big 4

clients covered in Audit Analytics report having major customer relationships, and there are wealth

transfer and interdependence implications among supply chain partners (e.g., Hertzel, Li, Officer,

and Rodgers 2008). However, most prior studies focus exclusively on financial performance and

operational strategy implications for upstream suppliers or downstream major customers in the

same supply chain relationship (e.g., Baiman and Rajan 2002a; Baiman and Rajan 2002b; Kulp,

Lee, and Ofek 2004). Related issues that have received limited attention are (1) how a company’s

supply chain relationships may affect other constituents in capital markets, such as audit firms,

when they provide audit services to both suppliers and their major customers, and (2) whether the

knowledge derived from such integrated supply chain audit services is associated with higher audit

quality.1

Second, supply chain partners may use earnings management to influence the perception of

their respective supplier or customer partners about their own financial performance, and such

earnings management activity adversely affects the duration of supply chain relationships (Raman

and Shahrur 2008). The supply chain knowledge that an auditor brings may help improve audit

quality and the assurance regarding the reliability of the financial statements of the respective

supply chain partners. However, prior research has not addressed whether auditor supply chain

knowledge is associated with audit quality as proxied by the extent of earnings management in

financial statements of supply chain partners.

Third, while we predict a positive association between auditor supply chain knowledge and

audit quality, it is unclear whether that association leads to fee premia or discounts reflecting

production efficiencies. Auditors with supply chain knowledge may charge a fee premium reflecting

a differentiation strategy in which that knowledge is valued by supply chain partners. On the other

hand, there may be efficiencies for an audit firm in completing the audit engagement for both a

supplier and its major customer(s), thereby yielding a fee discount reflecting such efficiencies.

We advance the literature on the development and transfer of knowledge at the individual and

audit-firm levels (e.g., Libby and Luft 1993; Bonner and Walker 1994; Solomon, Shields, and

Whittington 1999; Thibodeau 2003) by introducing the concept of knowledge redundancy in the

context of auditor supply chain knowledge. Sivakumar and Roy (2004) develop a model explaining

the distribution of private and common knowledge among supply chain partners. We adapt their

model to explain the implications of supply chain knowledge redundancy with respect to common

knowledge available to the supply chain partners and their auditors.

To examine the audit quality and pricing implications of auditor supply chain knowledge, we

use a sample of 4,569 supplier company years, of which about 11 percent employ an auditor with

supply chain knowledge at the city level and about 21 percent of which employ an auditor with

supply chain knowledge at the national level, but not at the city level. We measure auditors’ supply

1 New research is beginning to examine how supply chain relationships affect other constituents. Luo and Nagarajan(2014) and Guan, Wong, and Zhang (2014) examine how analysts benefit from the information shared withinmembers of a supply chain relationship when analysts issue forecasts for both a supplier and one or more of thesupplier’s major customers. Both of these papers find that analysts gain an information advantage and issue moreaccurate earnings forecasts for the supplier when analysts follow both of the supply chain partners.

120 Johnstone, Li, and Luo

Auditing: A Journal of Practice & TheoryNovember 2014

chain knowledge by calculating the number of supplier companies employing the same auditor (at

the city level or national level, respectively) as their major customers, divided by the total number

of supplier companies audited by that audit firm (at the city level or national level, respectively). We

separately examine auditor supply chain knowledge at the city level and at the national level

because we expect supply chain knowledge transfer to be more pronounced within a local audit

office. We focus our sample on supplier companies rather than customer companies because by

construction, supplier companies in our sample are much more dependent on major customers than

vice versa.2

The results show that auditor supply chain knowledge at the city level (but not at the national

level) is associated with higher audit quality for supplier companies, as indicated by lower

discretionary accruals, a lower likelihood of having a restatement, and a lower likelihood of

managing earnings to meet or beat analysts’ forecasts, compared to companies employing an

auditor without supply chain knowledge. Further, we also find that such supply chain knowledge at

the city level (but not at the national level) is associated with lower audit fees paid by supplier

companies compared to those paid by companies employing an auditor without supply chain

knowledge. In addition, we find that these results only hold in situations in which the customer is

highly important to the supplier company, and when the revenue cycle of the supplier company in

the audit engagement is more important, i.e., sales and accounts receivable accounts comprise a

higher percentage of total assets for the supplier company. We obtain these results while controlling

for the usual determinants of audit quality and fees, along with auditors’ industry specialization at

the national and city levels.

We conduct several sensitivity analyses to control for potential selection bias, the effects of

potential omitted variables on the association between auditors’ supply chain knowledge and audit

quality and audit pricing, and the simultaneity of such effects. The main conclusions remain

unchanged. These results contribute to research on audit quality differentiation and audit pricing.

Demand for quality-differentiated audits has long been documented (e.g., Watts and Zimmerman

1986; Simunic and Stein 1987). However, prior literature generally finds that audit firms

differentiate themselves from competitors via either brand name or industry specialization. We

report evidence on a new dimension of auditor knowledge acquisition and transfer and document

evidence consistent with audit firms providing value-added, quality-differentiated services via

supply chain specialization.

Our study also contributes to the supply chain literature that illustrates the importance of the

information shared between supply chain partners. For example, the exchange of detailed customer

demand and inventory information within the supply chain is associated with reduced total supply

chain costs (Chen 1998; Cachon and Fisher 2000) and improved efficiency in the use of resources

(Matsumura and Schloetzer 2014). We extend this literature by exploring how supplier companies

benefit both in terms of enhanced audit quality and more competitively priced auditing services

when they purchase auditing services from the same audit firm as their major customer, but only

when that auditor conducts the two audits out of the same city office.

The remainder of the study proceeds as follows. The second section provides background

information and hypotheses. The third section describes the sample and method. The fourth section

reports empirical results and discusses additional analyses. The fifth section concludes.

2 For example, in our sample, the mean (median) supplier sales dependence on major customer companies is 21.0(16.0) percent (calculated as total sales made to a major customer, divided by total sales of the supplier in the year).The mean supplier dependence on the major customer is comparable to 19.23 percent reported in Fee, Hadlock, andThomas (2006). In contrast, the mean (median) customer purchasing dependence on supplier companies is just 3.2(2.1) percent (calculated as the purchases of a major customer from the supplier, divided by total purchases of themajor customer in the year).

Client-Auditor Supply Chain Relationships, Audit Quality, and Audit Pricing 121

Auditing: A Journal of Practice & TheoryNovember 2014

BACKGROUND AND HYPOTHESES

The Importance of Supply Chain Relationships

A company’s strategic interactions with supply chain partners can have important performance

implications. Major customers influence suppliers’ revenue and earnings realization (e.g., Baiman

and Rajan 2002a; Baiman and Rajan 2002b; Kulp et al. 2004; Hertzel et al. 2008). When a major

customer expects growth, that demand for products and services positively affects the supplier’s

revenue. Similarly, when a major customer experiences financial distress, the customer may take

actions (e.g., decrease purchases, delay or stop payment, or default on long-term contracts) that

reduce the supplier’s revenue and, thus, have negative consequences for the supplier’s financial

performance (Hertzel et al. 2008).

Suppliers can also affect their customers’ expenses and resulting financial performance. For

example, a major customer with a trusted relationship with a supplier will benefit from a dependable

supply source and improved effectiveness of inventory management and operational efficiency,

each of which reduces costs and improves earnings (Gavirneni, Kapuscinski, and Tayur 1999; Lee,

So, and Tang 2000; Fee and Thomas 2004). Alternatively, when a supplier experiences a raw

material shortage or price increase, these adverse events negatively affect a major customer’s

production efficiency, inventory management, and product delivery (Gavirneni et al. 1999; Lee et

al. 2000; Fee and Thomas 2004).

Given the strategic importance of supply chain relationships to company performance, Raman

and Shahrur (2008) document the role of supply chain relationships in financial reporting decisions.

They argue that because the value of supply chain relationships to the suppliers/customers depends

on each company’s future prospects, supply chain partners may use earnings management to inflate

earnings in order to favorably influence the perception of suppliers/customers and their willingness

to undertake continuing relationship-specific investment. Other studies also find that companies

manage earnings to influence other terms of trade with suppliers/customers, such as input/output

prices and terms of trade credit. For example, customers are willing to pay higher prices if they

perceive that their suppliers have superior ability to honor explicit or implicit commitments, which

is likely to be the case for more profitable suppliers (e.g., Bowen, DuCharme, and Shores 1995;

Burgstahler and Dichev 1997).

The Development and Transfer of Auditor Supply Chain Knowledge

From an auditing perspective, supply chain relationships are important to suppliers because

they affect the suppliers’ revenue cycle. The revenue cycle is one of the most important transaction

cycles in any audit (Johnstone, Gramling, and Rittenberg 2013). Improper revenue recognition

practices are the most frequent cause of financial misstatements. In fact, 50–60 percent of the fraud

cases involve overstating revenues (Committee of Sponsoring Organizations of the Treadway

Commission [COSO] 1999, 2010).

By providing integrated supply chain auditing services, we predict that both individual auditors

and audit firms develop knowledge that is useful in understanding the supply chain partners and

assessing their respective risks. Such an effect would be consistent with knowledge gains due to

industry specialization (e.g., Craswell, Francis, and Taylor 1995; Mayhew and Wilkins 2003;

Balsam, Krishnan, and Yang 2003; Reichelt and Wang 2010). However, the nature of this

knowledge is likely different from that captured in studies on industry specialization, since supplier

and customer companies are generally in different industries. Our discussions with audit

practitioners suggest that supply chain knowledge relates to a deep understanding of the risks

inherent in the revenue cycle of supplier companies in their respective industries. In situations in

which there is no audit team overlap between the two engagements, one partner with whom we

122 Johnstone, Li, and Luo

Auditing: A Journal of Practice & TheoryNovember 2014

spoke explained that if a particularly complex issue arose, then consulting the other engagement

team was helpful, particularly in auditing revenue cycle accounts. The partner explained that since

customer incentive payments are often one of the more challenging issues, being able to more fully

understand both sides of the agreement would be important, since revenue recognition is one of the

highest restatement areas. That partner also described a situation in which he served on the

engagement of a major customer whose supplier was also audited by his firm. In that situation, one

client was on the wholesale side and the other on the retail side. He noted that the audit firm has

significant internal knowledge leadership that is gathered from these clients that is shared at an

aggregate basis and that is cleansed of specific client information.

Based on this discussion, we define auditor supply chain knowledge as specialized

understanding of information and processes regarding accounting and auditing issues that relates

to both a supplier and its major customer, regardless of industry commonalities, that is particularly

useful for understanding the complexities associated with the revenue cycle. Supply chain

knowledge exists at both the individual auditor level and at the organizational level through audit

firm knowledge leadership, knowledge management systems, and personal communication

networks. While it is logical to expect that there may be some overlap of auditor industry

knowledge and auditor supply chain knowledge, supply chain knowledge differs in that it can

develop across clients regardless of industry membership, and that it is likely more specialized,

focusing especially on accounting and auditing issues concerning revenue cycle accounts. Further,

it is logical to expect that auditor supply chain knowledge differs from nontransferrable client-

specific knowledge because it is aggregated across clients in a way that ensures client

confidentiality.

The Development of Supply Chain Knowledge at an Individual Level

A variety of factors play a role in the development of supply chain knowledge over the course

of an auditor’s career. Underlying audit task knowledge develops early, including both explicit and

tacit knowledge, and is an important determinant of audit task performance (Libby and Luft 1993).

As the auditor specializes in certain industries, industry expertise grows (Bonner and Walker 1994;

Solomon et al. 1999; Thibodeau 2003). Over time, the auditor establishes personal and professional

contacts in the business community, which enables networking across individuals and organizations

through repeated interactions (Borgatti and Cross 2003). These interactions may yield

enhancements in the acquisition of supply chain knowledge (e.g., relating to accounts receivable,

revenue, and associated contracting complexities). As the auditor gains further experience, the

likelihood increases that the auditor will work on both engagements in a supply chain partnership,

or will have close colleagues within the audit firm that do so. It also increases the likelihood of an

individual auditor working on one client in the supply chain relationship and then transferring to

also working on the other client in the relationship. Ultimately, over time and with experience, the

auditor develops an understanding of commonalities and shared risks/opportunities among supply

chain partners, which constitutes individual auditor-level supply chain knowledge.

The Transfer of Supply Chain Knowledge at an Organizational Level

In addition to developing supply chain knowledge at the individual level, audit firms face the

organizational challenge of ensuring effective transfer of such knowledge among and between

engagement teams. A significant body of the management literature is devoted to knowledge

transfer and organizational learning (e.g., Borgatti and Cross 2003; van Wijk, Jansen, and Lyles

2008). An important construct in that literature is that of knowledge redundancy, which is defined

as ‘‘the degree of overlap in the knowledge base between two or more social actors’’ (Rindfleisch

and Moorman 2001). Knowledge redundancy has been used to understand how individuals and

Client-Auditor Supply Chain Relationships, Audit Quality, and Audit Pricing 123

Auditing: A Journal of Practice & TheoryNovember 2014

organizations manage interpersonal and interorganizational communication of knowledge,

processes, and ideas. Sivakumar and Roy (2004) extend the knowledge redundancy literature

into the supply chain domain, arguing that while in some contexts knowledge redundancy may be

viewed as wasteful, in the supply chain domain it is essential for superior performance of the

partners because they cannot operate effectively unless they have in-depth knowledge of their

supply chain partner. Suppliers and major customers will find it in their mutual best interests to

share knowledge, ideas, and processes with one another to achieve maximum performance. As an

example from our sample, Apache Corporation is in the crude petroleum and natural gas industry

(SIC 1311) and its supplier is OIL States International Inc., which is in the oil and gas field

machinery and equipment industry (SIC 3533). The same audit firm conducts both engagements out

of the Houston, TX office. When the auditor audits both Apache and OIL States, we expect that

knowledge redundancy between the three parties will be enhanced, which should be beneficial from

an auditing perspective.

Auditing standards demand client confidentiality.3 However, it is important to note that

specialized knowledge in a particular field is allowed to transfer among different client

engagements (McAllister and Cripe 2008).4 Audit firm knowledge leadership, knowledge

management systems, and informal knowledge sharing via personal networks enable the capture

and dissemination of broad insights for companies up and down the supply chain. We expect supply

chain-relevant knowledge will help auditors to make more informed judgments and more accurate

risk assessments, especially with regard to the revenue cycle on the audits of the supplier

companies, thus producing a higher-quality audit.

Sivakumar and Roy (2004) develop a model explaining the distribution of private and common

knowledge among supply chain partners. In Figure 1, we adapt their model to explain the implications

of supply chain knowledge redundancy with respect to common knowledge available to the supply

chain partners and their auditors. Each of the scenarios in Figure 1 depicts the knowledge possessed

by only the supplier (denoted Ksupplier), the knowledge possessed by only the customer (denoted

Kcustomer), the common knowledge shared between the supplier and auditor (denoted KC-S, A), the

common knowledge shared between the customer and auditor (denoted KC-C, A), and finally the

common knowledge of all three parties (denoted KC-S, C, A). Following the introduction of our

hypotheses, we discuss the various panels in Figure 1, including implications for differences in the

application of supply chain-relevant knowledge at the city versus national levels, and in situations in

which the supplier is more versus less reliant on the major customer or when the revenue cycle is

more versus less important to the supplier.

3 The AICPA’s (1992) confidentiality rules compel the individual auditor not to reveal private information about eitherpartner in the supply chain relationship to the other client. However, it is routine practice for engagement teams todiscuss information about clients both audited by their firm. One partner that we contacted told us that individualauditors generally do not to talk with other teams about specific client matters that would not otherwise be publiclyknown. That said, he noted that situations do arise when it is appropriate to share knowledge that could benefit theindividual office or the audit firm. Such situations tend to relate to particular accounting or auditing issues, not toconfidential client information. He noted that such communications are usually informal and verbal, which is due tothe need to delicately address a potential issue without compromising confidentiality.

4 McAllister and Cripe (2008, 53) provide a comprehensive discussion of the benefits and risks of knowledge transferacross client engagements. Of most relevance, the authors state, ‘‘paragraph 30 of Rule 301 allows auditors to provide‘knowledge and expertise resulting in a special competence in a particular field’ to clients without violating theconfidence of another client as long as details associated with a particular engagement are not disclosed. Thisindicates that auditors are allowed to apply technical knowledge and experience acquired during current auditengagements to future audit engagements.’’

124 Johnstone, Li, and Luo

Auditing: A Journal of Practice & TheoryNovember 2014

Hypotheses Concerning Supply Chain Knowledge, Audit Quality, and Audit Pricing

As discussed earlier, supply chain-relevant knowledge should help auditors to make more

informed judgments and more accurate risk assessments, especially with regard to the revenue cycle

on the audits of the supplier companies, thus producing a higher-quality audit. Our first set of

hypotheses involves expectations comparing audit quality and audit pricing of supplier companies

audited by auditors with supply chain knowledge (at either the city or the national levels) to those

without such knowledge. Hereafter, we refer to an audit firm that provides audit services to both a

supplier and its major customer out of one office location as a ‘‘supply chain auditor at the city

level’’ and we refer to an audit firm that provides audit services to both a supplier and its major

customer out of two separate audit office locations as a ‘‘supply chain auditor at the national level.’’

H1a: Supplier companies audited by a supply chain auditor receive higher audit quality

compared to supplier companies audited by a non-supply chain auditor.

H1b: Supplier companies audited by supply chain auditors at the national level receive higher

audit quality compared to supplier companies audited by non-supply chain auditors.

As an example from our sample relating to H1a, the same audit firm audits Micron Technology

Inc. and its supplier, Netlogic Microsystems, Inc., both out of the San Jose, CA office. H1a predicts

higher audit quality for Netlogic Microsystems compared to a supplier-customer pair audited by

FIGURE 1Implications of Supply Chain Auditing Knowledge Redundancy

Note: Ksupplier denotes supplier knowledge; Kcustomer denotes customer knowledge; Kc denotes common knowledge withsubscript denoting supplier (S), customer (C), or auditor (A); dashed boarder denotes entire domain of auditorknowledge.

Client-Auditor Supply Chain Relationships, Audit Quality, and Audit Pricing 125

Auditing: A Journal of Practice & TheoryNovember 2014

different audit firms. As an example from our sample relating to H1b, the same audit firm audits

Barnes & Noble Inc. and its supplier, Source Interlink Inc., but out of different offices (Chicago, IL

and New York, NY, respectively). H1b predicts higher audit quality for Source Interlink compared

to a supplier-customer pair audited by different audit firms.

While H1a and H1b predict that supply chain knowledge can be leveraged by auditors at both

the city and national levels, we expect that the effect should be more pronounced at the city level.

Figure 1, Scenarios A and B depict knowledge sharing for city-level versus national-level auditor

supply chain knowledge. When different auditor offices conduct the audits for a supplier and its

major customer, these audits are typically conducted by different audit teams with different audit

partners. At the national level, it is less likely that auditors from different offices have information

communication concerning the related companies in their client portfolio. In such circumstances,

the information advantages and the knowledge that auditors build by providing supply chain

auditing services is likely to be less. In contrast, it is likely that informal communication concerning

these parties within the same city office may help auditors assess the business risk of supplier

companies. In situations in which an individual auditor is involved in the audit of both the supplier

company and the customer company, that individual knowledge is naturally retained. For example,

it would not be unusual to find overlap among members of an audit engagement team on both a

supplier client and a major customer client, especially when the supplier and major customer are

audited by the same city office of the audit firm. The result is that KC-S, C, A in Scenario A is larger

than KC-S, C, A in Scenario B. Thus, our next hypothesis is:

H1c: Supplier companies audited by supply chain auditors at the city level receive higher

audit quality compared to supplier companies audited by supply chain auditors at the

national level.

Continuing prior examples, H1c predicts higher audit quality for Netlogic Microsystems (same

city-level auditor) compared to Source Interlink (same national-level auditor).

Regarding audit pricing, Raman and Shahrur (2008) document an earnings management

motivation in financial reporting for supply chain partners. They argue that because the value of

supply chain relationships to the suppliers/customers depends on each company’s future prospects,

supply chain partners may use earnings management to favorably influence the perception of their

supply chain partner. This motivation creates both a demand for, and supply of, quality and fee

differentiated audit services (e.g., Copley and Doucet 1993; Copley, Doucet, and Gaver 1994).

In addition to a risk-based argument, if supplier companies place value on auditors’ supply

chain knowledge and resulting higher audit quality, auditors with supply chain knowledge may be

able to charge a fee premium reflecting this differentiation strategy. For example, the audit

committee of a supplier company may find it appealing during the bidding process to know that

members of the audit engagement team have experience auditing the company’s major customer,

especially when the supplier and major customer are audited by the same city office of the audit

firm, which may then translate to the auditor being able to negotiate a relatively higher audit fee

than cases if members of the audit engagement team had no such relevant experience.5 One partner

with whom we spoke stated his strategy in these cases is to highlight supplier experience during the

proposal process when he thinks it will be beneficial to demonstrating additional knowledge, and

when the potential client has not indicated concern about the auditor’s relationship with the major

customer.

5 If the audit committee members were uncomfortable with the potential for the supplier’s private information leakageby the auditor with supply chain knowledge, even if it were indirect, to the major customer, then presumably the auditcommittee members simply would not hire the auditor with such knowledge in the first place.

126 Johnstone, Li, and Luo

Auditing: A Journal of Practice & TheoryNovember 2014

A competing argument is that the auditor’s supply chain knowledge and resulting synergies

could yield audit production efficiencies. Production efficiencies associated with auditor supply

chain knowledge would enable the auditor to offer a fee discount reflecting such efficiencies; such

synergies would of course be most pronounced when the supplier and the major customer are

audited by the same city office of the audit firm. One partner with whom we spoke articulated the

process by which this might occur, stating that when there is supply chain knowledge the audit firm,

as a whole, would generally have greater experience, which could lead to efficiencies. He noted that

if both clients were in the same office (even if the audit teams may not directly overlap) there would

be experience in the office and/or an ability to consult on tough issues that otherwise may take

additional time to resolve independently without such consultation. Prior research shows an

association between audit production efficiencies and audit pricing. For example, Gist (1994)

provides empirical evidence that audit firms with a more structured audit approach charge lower

audit fees, although that study acknowledges that without data on audit hours (a direct measure of

audit effort) a definitive link between audit firm structure and production efficiencies is unavailable.

Dopuch, Gupta, Simunic, and Stein (2003, 52) utilize empirical data on audit firm effort and pricing

and show that inefficiencies in audit production hours are associated with reductions in audit firm

realization rates, and they also note that ‘‘efficient production could also lead to fee discounting.’’More recently however, Knechel, Rouse, and Schelleman (2009) report that audit fees are not very

sensitive to audit efficiency, so the results with respect to audit production models are mixed.

Based on these two competing arguments, it remains an empirical question as to whether

providing audit services to supply chain partners is associated with higher or lower audit fees. As

such, we formulate the following research question:

RQ: Do supplier companies audited by supply chain auditors at the national or city level pay

higher or lower audit fees compared to companies audited by non-supply chain auditors?

Hypotheses Concerning Supply Chain Knowledge and Supplier Reliance and SupplierRevenue Cycle Importance

Supplier reliance on a major customer varies across supplier-customer pairs, and the importance

of revenue cycle accounts also varies across individual suppliers. Comparing Scenarios C and D in

Figure 1 helps to explain knowledge redundancy implications when the supplier and customer have

asymmetric overlap of private versus common knowledge. Asymmetric overlap occurs when one

party in the supply chain relationship has greater private knowledge than the other party. Scenario C

represents a situation in which the supplier’s reliance on the customer is higher in terms of the

percentage of revenue they earn through transactions with the customer, or for which the revenue

cycle is relatively more important to the supplier, whereas Scenario D represents a situation in which

the supplier’s reliance is lower or the revenue cycle is relatively less important. Comparing Scenarios

C and D illustrates that when a supplier company is more dependent on the sales made to its major

customer, or when the revenue cycle accounts of the supplier companies are the primary accounts

affected by the supplier-customer relationship, the common knowledge available to an auditor with

integrated supply chain knowledge is greater than when a supplier company is less dependent on its

major customer. Sivakumar and Roy (2004, 245) illustrate the extreme example of supply chain

dependence as one in which a supplier’s only source of revenue is manufacturing steering wheels for

Ford Motor Company. The authors note ‘‘Clearly, such a supplier can be expected to be efficient and

to be almost as internalized and domesticated as a company department . . . knowledge redundancy

will be at a maximum between the supplier and Ford.’’Finally, based on insights gained from comparing Scenarios C and D in Figure 1, we predict

that the associations that we observe relevant to H1 and the research question will be stronger in

two situations: (1) for supplier companies that derive a high proportion of their total revenue from

Client-Auditor Supply Chain Relationships, Audit Quality, and Audit Pricing 127

Auditing: A Journal of Practice & TheoryNovember 2014

sales to their major customers, and (2) when the revenue cycle in the audit engagement for supplier

companies is more important.

H2a: The association between audit quality and auditor supply chain knowledge at the

national or city level is stronger for supplier companies (1) that derive a greater

proportion of their total revenue from sales to their major customers, and (2) when the

revenue cycle in the audit engagement for the supplier companies is more important.

H2b: The association between audit fees and auditor supply chain knowledge at the national

level or city level is stronger for supplier companies (1) that derive a greater proportion

of their total revenue from sales to their major customers, and (2) when the revenue

cycle in the audit engagement for the supplier companies is more important.

SAMPLE AND METHOD

Sample

To determine whether a supplier and its major customer employ the same audit firm in a given

fiscal year, we require identification of each party in a company’s supply chain relationships and the

identity of the auditors of these companies. SFAS No. 14 (FASB 1976) requires companies to

report financial information for any industry segment that comprises more than 10 percent of the

company’s consolidated yearly sales, assets, or profit. In addition, companies must disclose the

name of any customer representing more than 10 percent of the total sales of the company. We

obtain this information from the Compustat customer segment file, a subset of the Compustat

segment database that records the identity of, and sales to, a company’s major customers based on

the company’s 10-K.6

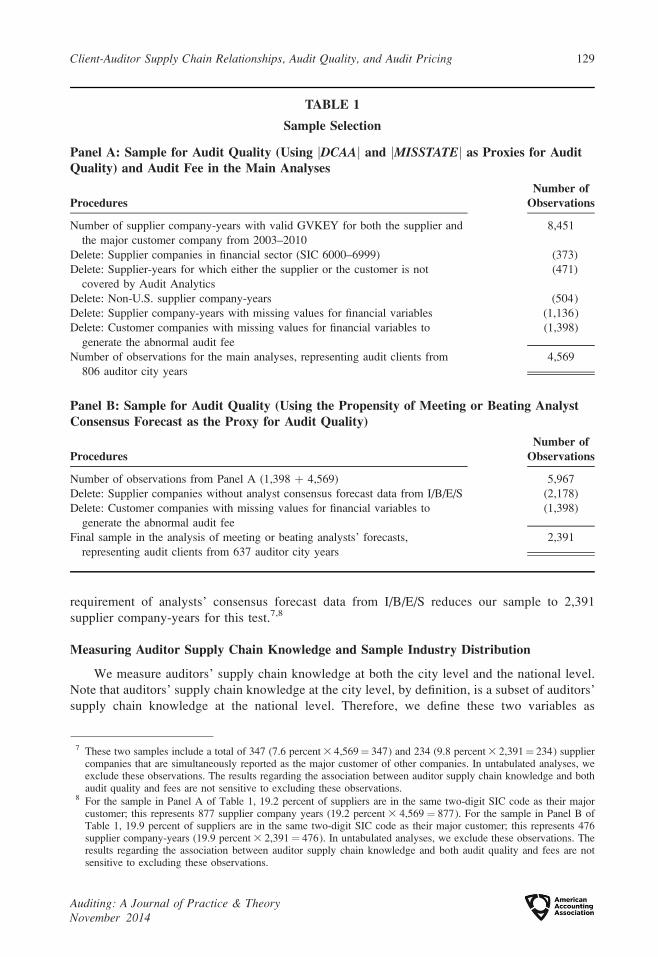

Table 1 shows the sample selection process. We begin with all supplier-major customer

relationships reported in the Compustat customer segment file during the period January 1, 2003

to December 31, 2010. We start in 2003 to avoid issues associated with the collapse of Arthur

Andersen in 2002. We use an algorithm similar to that in Fee and Thomas (2004) that compares

the number and order of the letters for the customer names with the historical company names

listed in the CRSP company name file and retain a list of 8,451 supplier company-years with a

valid GVKEY for both the supplier and its major customer. When a supplier company discloses

more than one major customer, we retain in our sample the customer to whom the supplier makes

the greatest amount of sales. As noted previously, we focus our sample on supplier companies

rather than customer companies because suppliers are much more dependent on the sales made to

major customers than vice versa. We then delete 373 supplier-years in the financial sector (e.g.,

Francis, Reichelt, and Wang 2005; Reichelt and Wang 2010), 471 supplier-years with either the

supplier or the major customer not covered by Audit Analytics, and 504 supplier companies not

headquartered in the U.S. We eliminate 1,136 (1,398) suppliers (major customers) with missing

financial data from Compustat. We require data on major customers because we include the

abnormal audit fee of the major customer as one of the control variables in the regression

analyses. This yields a sample of 4,569 supplier company-year observations. In analyzing audit

quality, we also examine the propensity of companies’ meeting or beating analysts’ earnings

forecasts within one penny of earnings per share (Reichelt and Wang 2010). The additional

6 Therefore, all customer companies included in our sample meet this requirement, i.e., customer companies that makeless than 10 percent of the total sales to the supplier company will not be included in our sample.

128 Johnstone, Li, and Luo

Auditing: A Journal of Practice & TheoryNovember 2014

requirement of analysts’ consensus forecast data from I/B/E/S reduces our sample to 2,391

supplier company-years for this test.7,8

Measuring Auditor Supply Chain Knowledge and Sample Industry Distribution

We measure auditors’ supply chain knowledge at both the city level and the national level.

Note that auditors’ supply chain knowledge at the city level, by definition, is a subset of auditors’

supply chain knowledge at the national level. Therefore, we define these two variables as

TABLE 1

Sample Selection

Panel A: Sample for Audit Quality (Using jDCAAj and jMISSTATEj as Proxies for AuditQuality) and Audit Fee in the Main Analyses

ProceduresNumber of

Observations

Number of supplier company-years with valid GVKEY for both the supplier and

the major customer company from 2003–2010

8,451

Delete: Supplier companies in financial sector (SIC 6000–6999) (373)

Delete: Supplier-years for which either the supplier or the customer is not

covered by Audit Analytics

(471)

Delete: Non-U.S. supplier company-years (504)

Delete: Supplier company-years with missing values for financial variables (1,136)

Delete: Customer companies with missing values for financial variables to

generate the abnormal audit fee

(1,398)

Number of observations for the main analyses, representing audit clients from

806 auditor city years

4,569

Panel B: Sample for Audit Quality (Using the Propensity of Meeting or Beating AnalystConsensus Forecast as the Proxy for Audit Quality)

ProceduresNumber of

Observations

Number of observations from Panel A (1,398 þ 4,569) 5,967

Delete: Supplier companies without analyst consensus forecast data from I/B/E/S (2,178)

Delete: Customer companies with missing values for financial variables to

generate the abnormal audit fee

(1,398)

Final sample in the analysis of meeting or beating analysts’ forecasts,

representing audit clients from 637 auditor city years

2,391

7 These two samples include a total of 347 (7.6 percent 3 4,569¼ 347) and 234 (9.8 percent 3 2,391¼ 234) suppliercompanies that are simultaneously reported as the major customer of other companies. In untabulated analyses, weexclude these observations. The results regarding the association between auditor supply chain knowledge and bothaudit quality and fees are not sensitive to excluding these observations.

8 For the sample in Panel A of Table 1, 19.2 percent of suppliers are in the same two-digit SIC code as their majorcustomer; this represents 877 supplier company years (19.2 percent 3 4,569 ¼ 877). For the sample in Panel B ofTable 1, 19.9 percent of suppliers are in the same two-digit SIC code as their major customer; this represents 476supplier company-years (19.9 percent 3 2,391¼ 476). In untabulated analyses, we exclude these observations. Theresults regarding the association between auditor supply chain knowledge and both audit quality and fees are notsensitive to excluding these observations.

Client-Auditor Supply Chain Relationships, Audit Quality, and Audit Pricing 129

Auditing: A Journal of Practice & TheoryNovember 2014

orthogonal to each other. In particular, CHAIN_CITY is a ratio measure of auditors’ supply chain

knowledge at the city level, and it is defined as the number of supplier companies (i.e., companies

that have reported having major customer relationships in Compustat with both the supplier and

the major customer being covered in Audit Analytics) employing the same city-office auditor as

their major customers, divided by the total number of supplier companies from the same auditor

city in the year. For example, assume that Audit Firm X in City A has ten client companies that

have major customer relationships. Further assume that Audit Firm X also audits two of these

supplier companies’ major customers out of the City A office. In this example, CHAIN_CITYequals 20 percent. CHAIN_CITY equals 0 if Audit Firm X does not audit any of the supplier

companies’ major customers out of the City A office. CHAIN_NATION is a ratio measure of

auditors’ supply chain knowledge at the national level, and it is defined as the number of supplier

companies employing the same auditor (but not from the same city) as their major customers,

divided by the total number of supplier companies that the audit firm audits at the national level.

For example, assume that Audit Firm X has 100 client companies that have major customer

relationships nationwide. Further assume that Audit Firm X also audits two of these supplier

companies’ major customers, but that the supplier and customer companies are audited out of

different city offices. In this example, CHAIN_NATION equals 2 percent. Appendix A provides

further illustrations of the calculation of these variables using examples from the sample; our

calculations reflect the convention in the industry specialization literature regarding the use of

relative market share to measure the underlying construct (e.g., Craswell et al. 1995; Balsam et al.

2003).

Table 2 shows that about 11 percent of supplier companies (509/4,569) employ an auditor with

city-level supply chain knowledge, 21 percent (979/4,569) employ an auditor with national-level

TABLE 2

Industry Distribution of Sample Companies

Fama-French’s 12 Industries

CHAIN_CITY . 0 CHAIN_NATION . 0CHAIN_CITY ¼ 0 andCHAIN_NATION ¼ 0

n Percent n Percent n Percent

Consumer nondurables 19 3.7% 120 12.3% 413 13.4%

Consumer durables 7 1.4% 48 4.9% 165 5.4%

Manufacturing 64 12.6% 150 15.3% 473 15.4%

Energy and coal extraction and

products

31 6.1% 35 3.6% 244 7.9%

Chemicals and allied products 11 2.2% 29 3.0% 126 4.1%

Business equipment 200 39.3% 250 25.5% 878 28.5%

Telephone and television

transmission

11 2.2% 28 2.9% 41 1.3%

Utilities 21 4.1% 14 1.4% 48 1.6%

Wholesale, retail, and some

services

10 2.0% 39 4.0% 107 3.5%

Healthcare, medical equipment,

and drugs

86 16.9% 137 14.0% 312 10.1%

Others 49 9.6% 129 13.2% 274 8.9%

Total 509 100% 979 100% 3,081 100%

130 Johnstone, Li, and Luo

Auditing: A Journal of Practice & TheoryNovember 2014

supply chain knowledge, with the remainder employing an auditor with neither type of supply chain

knowledge. Industry distribution is relatively similar across these groups, with manufacturing,

business equipment, and the healthcare/medical equipment/drug sectors having the largest

representation.

Research Design

We first consider the association between auditor supply chain knowledge at either the city or

national level and three common proxies for audit quality (H1a and H1b). The first proxy is the

absolute value of discretionary accruals jDACCj (e.g., Frankel, Johnson, and Nelson 2002; Reichelt

and Wang 2010), which is calculated based on the cross-sectional modified Jones (1991) model

where expected accruals are estimated from the change in revenue, adjusted by the change in

accounts receivable, the level of property, plant, and equipment, and the prior year’s operating

performance by industry at the two-digit SIC code level in year t. jDACCj represents the amount of

unexpected accruals and is the amount of earnings that have been potentially distorted through

managerial discretion in earnings management. See Appendix B for an illustration of the calculation

of jDACCj. See Appendix C for variable definitions.

The second proxy for audit quality is the existence of a restatement, RESTATE (e.g., Palmrose

and Scholz 2004; Francis, Michas, and Yu 2012). This variable equals 1 if a company’s financial

reports for year t are subsequently restated in future periods, and 0 otherwise. The third proxy for

audit quality relates to the existence of aggressive earnings management. Following Reichelt and

Wang (2010), we use the propensity that a company meets or just beats analysts’ earnings forecasts

as a proxy for clients’ aggressive earnings management behavior. MEET equals 1 if earnings

exactly meet or beat the latest analyst earnings forecast by one cent per share in year t, and equals 0

otherwise.9 H1a and H1b predict a negative association between these three audit quality proxies

and CHAIN_CITY and CHAIN_NATION, respectively. Our research question explores the

association between auditor supply chain knowledge and audit fees and, accordingly, we make

no directional prediction between the natural log of audit fees, logAUDITFEE, and either

CHAIN_CITY or CHAIN_NATION.

We include various control variables in the models. A particularly important control variable is

auditor industry specialization. Prior studies find that industry specialist auditors are associated with

better earnings quality and that they charge higher audit fees (e.g., Balsam et al. 2003; Francis et al.

2005; Reichelt and Wang 2010). Following prior research, we control for industry specialization at

the national level only (IND_NATION), the city level (IND_CITY), and at both the national and the

city levels (JOINT_IND).

Other control variables follow prior research in terms of measurement and directional predictions;

when divergent results in prior research exist we make nondirectional predictions (e.g., Frankel et al.

2002; Ashbaugh, LaFond, and Mayhew 2003; Francis et al. 2005; Reichelt and Wang 2010). For the

audit quality models, we control for whether the auditor is a Big 4 auditor (BIG_4), total accruals

(TACC),10 company size (logAT), operating cash flows (CFO), cash flow volatility (STD_CFO),

financial condition (LEVERAGE, ROA, and LOSS), company growth as measured by market-to-book

value, sales growth, and research and development expenses (MB, SALE_GROWTH, and

RD_RATIO), whether the company is in a litigious industry (LITIGATION), the likelihood of

9 As we discussed earlier, auditors’ supply chain knowledge is important for the revenue cycle in the audit engagement.Thus, as a sensitivity test we also use the likelihood that companies meet or beat analyst consensus revenue forecastsas an alternative proxy for audit quality. Our results remain essentially the same.

10 Following prior studies, we include the absolute value of TACC rather than unsigned TACC as a control variable whenwe use the absolute value of discretionary accruals as the measure for audit quality (e.g., Reichelt and Wang 2010).

Client-Auditor Supply Chain Relationships, Audit Quality, and Audit Pricing 131

Auditing: A Journal of Practice & TheoryNovember 2014

bankruptcy (ALTMAN), and auditor tenure (logAUDITOR_TENURE). We expect BIG_4, CFO, and

ROA to be positively associated with audit quality (i.e., negatively associated with jDACCj,RESTATE, or MEET), and TACC, STD_CFO, LEVERAGE, LOSS, MB, SALE_GROWTH,

RD_RATIO, and ALTMAN to be negatively associated with audit quality (i.e., positively associated

with jDACCj, RESTATE, or MEET). We make no directional predictions for logAT or LITIGATION

or logAUDITOR_TENURE due to variation in results in prior studies (e.g., Ashbaugh et al. 2003;

Knechel and Vanstraelen 2007; Reichelt and Wang 2010).

In the audit fee models, we control for whether the auditor is a Big 4 auditor (BIG_4), whether

the company’s year-end is in the busy season (BUSY_SEASON), company size (logAT), long term

debt (LONG_DEBT), current liabilities (CURRENT_LIABILITY), inventory ratio (INVT_RATIO), a

modified auditor opinion (MODIFIED_OPN), financial risk (ROA and LOSS), volatility

(STD_CFO), growth (SALE_GROWTH and RD_RATIO), restructuring (RESTRUCTURE), special

items (SPECIAL_ITEM), foreign transactions (FOREIGN), complexity (NUM_SEG), and auditor

tenure (logAUDITOR_TENURE). We expect ROA to be negatively associated with audit fees, and

the other variables to be positively associated with audit fees.

Finally, because characteristics of suppliers’ major customers may potentially affect supplier

companies’ audit quality and audit fees, we control for such characteristics. To manage the number

of independent variables, we include a variable representing the abnormal audit fee paid by major

customer companies (ABN_CU_logFEE). ABN_CU_logFEE is the residual value from the audit fee

model presented in Appendix D. We make no directional prediction for the association between

ABN_CU_logFEE and audit quality, and expect a positive association between ABN_CU_logFEE

and audit fees.

Below are the regression models that we use to examine the association between auditor supply

chain knowledge and audit quality. Because CHAIN_CITY and CHAIN_NATION are defined at the

auditor-office-year and auditor-year level, respectively, we adjust the standard errors for the

coefficient estimates in the regression analyses by clustering the observations at the supplier-company

level.

jDACCtj ; ðRESTATEtÞ ; ðMEETtÞ ¼ b0 þ b1CHAIN CITYt þ b2CHAIN NATIONt

þ b3IND NATIONt þ b4IND CITYt þ b5JOINT INDt

þ b6BIG 4t þ b7jTACCtjðTACCtÞ þ b8logATt þ b9CFOt

þ b10STD CFOt þ b11LEVERAGEt þ b12ROAt

þ b13LOSSt þ b14MBt þ b15SALE GROWTHt

þ b16RD RATIOt þ b17LITIGATIONt þ b18ALTMANt

þ b19logAUDITOR TENUREt þ b20ABN CU logFEEt

þ fixed industryþ fixed year þ et

ð1Þ

logðAUDITFEEtÞ ¼ b0 þ b1CHAIN CITYt þ b2CHAIN NATIONt þ b3IND NATIONt

þ b4IND CITYt þ b5JOINT INDt þ b6BIG 4t þ b7BUSY SEASONt

þ b8logATt þ b9LONG DEBTt þ b10CURRENT LIABILITYt

þ b11INVT RATIOt þ b12MODIFIED OPNt þ b13ROAt þ b14LOSSt

þ b15STD CFOt þ b16SALE GROWTHt þ b17RESTRUCTUREt

þ b18SPECIAL ITEMt þ b19FOREIGNt þ b20NUM SEGt

þ b21RD RATIOt þ b22logAUDITOR TENUREt þ b23ABN CU logFEEt

þ fixed industryþ fixed year þ et

ð2Þ

132 Johnstone, Li, and Luo

Auditing: A Journal of Practice & TheoryNovember 2014

RESULTS

Descriptive Statistics

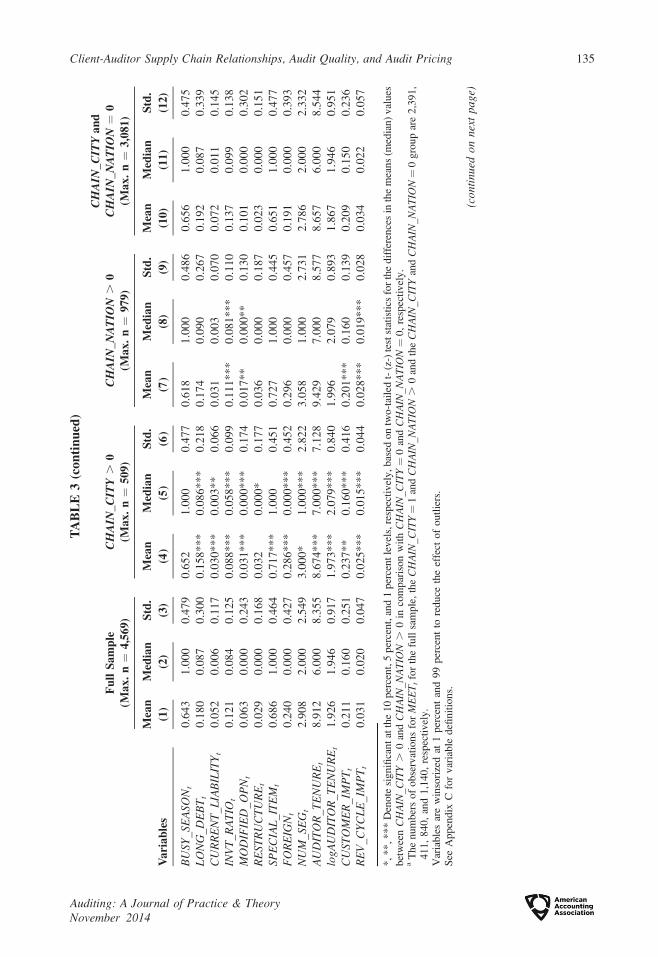

Table 3, Panel A reports descriptive statistics for for the full sample, as well as the three

subsamples of companies, i.e., CHAIN_CITY . 0, CHAIN_NATION . 0, and CHAIN_CITY and

CHAIN_NATION ¼ 0. Using the full sample, the mean jDACCj is 0.097, 15.8 percent of the

companies restated their financial statements (RESTATE), and 12.5 percent of companies have met

or just beat analyst forecasts by one cent (MEET). The mean (median) of logAUDITFEE is 13.130

(13.158), which is equivalent to an unlogged mean (median) value of $1.29 million ($573,000).

Univariate comparisons at the city level show that, compared with companies for which

CHAIN_CITY and CHAIN_NATION ¼ 0, those companies for which CHAIN_CITY . 0 have

marginally lower discretionary accruals (jDACCj; p ¼ 0.08), a lower likelihood of restatement

(RESTATE; p ¼ 0.045), a marginally lower likelihood of meeting or beating the latest analyst

earnings forecast by one cent (MEET; p ¼ 0.08), and no significant difference in audit fees. In

addition, companies for which CHAIN_NATION . 0 also have a marginally lower likelihood of

restatement (RESTATE; p ¼ 0.08) compared with companies for which CHAIN_CITY and

CHAIN_NATION ¼ 0. However, the differences in jDACCj, MEET, and logAUDITFEE between

these two groups are insignificant. When comparing companies for which CHAIN_CITY . 0 to

those companies for which CHAIN_NATION . 0 (untabulated), we find the former companies have

marginally lower discretionary accruals (p¼ 0.06), and lower audit fees (p¼ 0.02) compared to the

latter companies.

The Pearson/Spearman correlation matrix in Table 3, Panel B reveals that jDACCj is negatively

associated with both CHAIN_CITY (p , 0.01) and IND_CITY (p¼ 0.02). RESTATE is negatively

associated with both logAUDITFEE (p , 0.01) and CHAIN_CITY (p¼ 0.04). MEET is positively

associated with logAUDITFEE (p , 0.01). Due to the large number of control variables across

various models, we do not tabulate those correlations. While several correlations among

independent variables exceed 0.35, the highest variance influence factor (VIF) is only 4.60

(2.31) in the model of audit quality using discretionary accruals as the measure and audit fee,

respectively, suggesting multicollinearity is unlikely to be problematic.

Regarding correlations between auditor supply chain knowledge and industry specialization,

the results reveal that CHAIN_CITY is positively associated with both CHAIN_NATION (p , 0.01)

and JOINT_IND (p , 0.01), and is negatively associated with IND_CITY (p , 0.01).

CHAIN_NATION is positively associated with IND_NATION (p , 0.01), IND_CITY (p ,

0.01), and JOINT_IND (p , 0.01). While statistically significant, the correlations between proxies

for auditor supply chain knowledge and industry specialization range from�0.09 to 0.15, so these

constructs appear to be related but distinct.

Hypothesis Testing

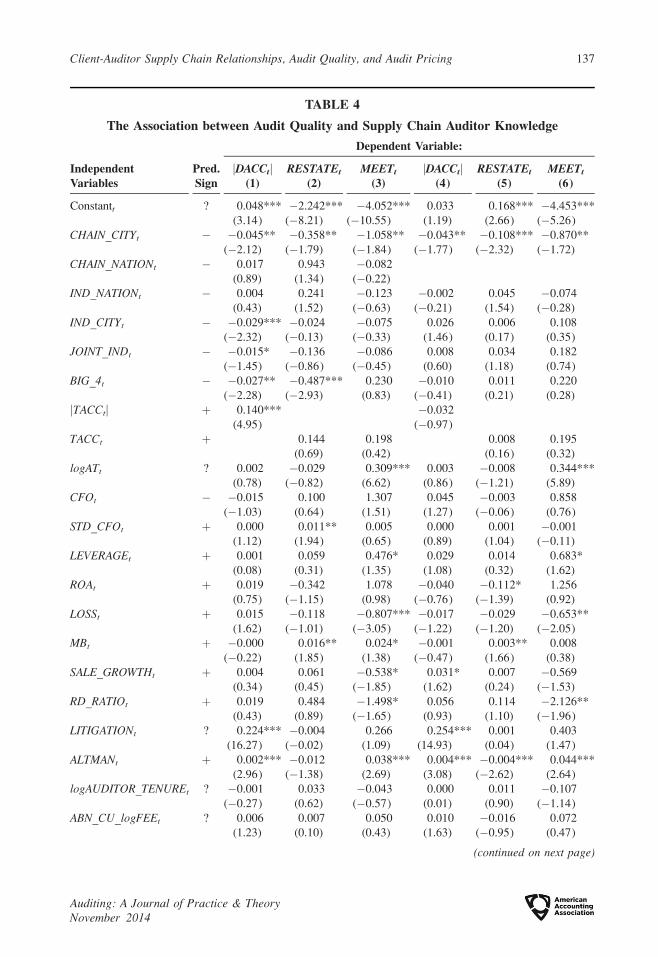

Table 4, Columns (1)–(3) report results relevant to testing H1a and H1b. The results show that

CHAIN_CITY is negatively associated with the level of absolute discretionary accruals (p¼ 0.017),

the likelihood of a restatement (p¼ 0.045), and the likelihood of meeting or just beating analysts’

forecasts for supplier companies (p¼ 0.033). These results support H1a. To put these coefficients

into perspective, these results suggest a decrease of 5.2 percent (�0.045 3 0.112)/0.097) in the total

level of absolute discretionary accruals, a decrease in the probability of a restatement from 21.3

percent to 20.6 percent (representing a 3 percent decrease), and a decrease in the propensity to meet

or beat analyst forecasts from 7.6 percent to 6.8 percent (representing a 10.5 percent decrease),

Client-Auditor Supply Chain Relationships, Audit Quality, and Audit Pricing 133

Auditing: A Journal of Practice & TheoryNovember 2014

TA

BL

E3

Des

crip

tiv

eS

tati

stic

sa

nd

Co

rrel

ati

on

s

Pa

nel

A:

Des

crip

tiv

eS

tati

stic

s

Va

ria

ble

s

Fu

llS

am

ple

(Ma

x.

n¼

4,5

69

)C

HA

IN_

CIT

Y.

0(M

ax

.n¼

50

9)

CH

AIN

_N

AT

ION

.0

(Ma

x.

n¼

97

9)

CH

AIN

_C

ITY

an

dC

HA

IN_

NA

TIO

N¼

0(M

ax

.n¼

3,0

81

)

Mea

nM

edia

nS

td.

Mea

nM

edia

nS

td.

Mea

nM

edia

nS

td.

Mea

nM

edia

nS

td.

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10

)(1

1)

(12

)

jDA

CC

tj0

.09

70

.03

80

.17

60

.09

0*

0.0

36

0.1

71

0.1

05

0.0

39

0.1

91

0.1

01

0.0

45

0.1

68

RE

STA

TE

t0

.15

80

.00

00

.36

50

.13

8*

*0

.00

0*

*0

.38

30

.15

3*

0.0

00

*0

.38

60

.17

80

.00

00

.34

4

ME

ET

ta0

.12

50

.00

00

.33

10

.11

2*

0.0

00

0.3

18

0.1

18

0.0

00

0.3

23

0.1

40

0.0

00

0.3

47

logA

UD

ITF

EE

t1

3.1

30

13

.15

82

.36

41

3.2

26

13

.22

12

.22

31

3.1

90

13

.17

12

.23

41

3.0

55

12

.83

42

.37

5

AU

DIT

FE

Et

(in

mil

lio

n$

)1

.28

70

.57

32

.05

41

.65

7*

**

0.8

09

**

*2

.43

81

.61

2*

**

0.7

83

**

*2

.33

60

.94

20

.37

41

.63

5

IND

_NA

TIO

Nt

0.2

42

0.0

00

0.4

28

0.2

63

***

0.0

00

**

*0

.44

10

.31

1*

*0

.00

0*

*0

.46

30

.19

30

.00

00

.39

5

IND

_CIT

Yt

0.1

05

0.0

00

0.3

06

0.0

82

0.0

00

**

*0

.27

50

.12

3*

**

0.0

00

**

*0

.32

80

.10

10

.00

00

.30

2

JOIN

T_I

ND

t0

.27

80

.00

00

.44

80

.52

0*

**

1.0

00

**

*0

.50

00

.34

7*

**

0.0

00

**

*0

.47

60

.16

10

.00

00

.36

7

BIG

_4t

0.7

59

1.0

00

0.4

28

0.9

66

***

1.0

00

**

*0

.06

40

.97

7*

**

1.0

00

**

*0

.15

10

.75

31

.00

00

.49

7

TA

CC

t�

0.0

23�

0.0

09

0.2

61�

0.0

22

�0

.00

6*

**

0.2

33�

0.0

04

*�

0.0

03

0.2

06�

0.0

36

�0

.01

30

.29

7

logA

Tt

5.5

21

5.4

88

2.0

82

6.3

60

***

6.3

28

**

*1

.87

26

.03

4*

**

5.9

28

**

*1

.79

14

.94

64

.87

12

.14

1

AT

t(i

n1

,00

0m

illi

on

s$

)1

.65

50

.24

14

.31

62

.60

1*

**

0.5

60

5.1

62

2.0

77

**

0.3

75

5.2

23

1.1

03

0.1

30

3.1

86

CF

Ot

0.0

04

0.0

70

0.3

78

0.0

16

**

0.0

69

**

*0

.27

10

.03

8*

0.0

79

**

*0

.25

5�

0.0

20

0.0

65

0.4

61

STD

_CF

Ot

0.3

36

0.3

81

8.1

78

0.1

01

0.3

11

6.1

75

0.7

76

*0

.41

7*

**

9.3

83

0.1

42

0.3

69

7.9

18

LE

VE

RA

GE

t0

.23

10

.15

60

.27

90

.18

7*

**

0.1

22

**

*0

.22

10

.20

10

.13

30

.24

60

.26

30

.18

30

.30

9

RO

At

�0

.07

00

.02

30

.28

1�

0.0

66

**

0.0

20

**

*0

.23

6�

0.0

34

***

0.0

34

**

*0

.21

6�

0.0

94

0.0

19

0.3

24

LO

SSt

0.4

14

0.0

00

0.4

93

0.4

35

0.0

00

0.4

96

0.3

73

***

0.0

00

**

*0

.48

40

.43

20

.00

00

.49

5

MB

t1

.96

21

.84

15

.48

72

.02

22

.09

95

.52

02

.40

82

.05

24

.77

41

.66

61

.64

55

.86

9

SAL

E_G

RO

WT

Ht

0.0

98

0.0

63

0.3

19

0.0

97

0.0

73

**

*0

.33

60

.11

60

.07

40

.29

70

.08

80

.05

40

.32

7

RD

_RA

TIO

t0

.08

30

.02

10

.10

40

.13

6*

**

0.1

40

0.1

16

0.0

90

***

0.0

36

**

*0

.10

30

.06

20

.00

90

.09

3

LIT

IGA

TIO

Nt

0.0

77

0.0

00

0.2

67

0.0

85

**

0.0

00

0.2

79

0.1

01

0.0

00

0.3

02

0.0

59

0.0

00

0.2

36

AL

TM

AN

t6

.25

23

.84

26

.51

86

.73

0*

4.3

83

**

6.6

57

6.0

63

**

3.7

95

**

5.9

74

6.2

27

3.7

32

6.7

97

AB

N_C

U_l

ogF

EE

t0

.39

60

.41

20

.60

20

.41

3*

0.4

20

**

*0

.57

50

.43

90

.41

80

.59

90

.36

50

.40

50

.60

9

(con

tinu

edo

nn

ext

pa

ge)

134 Johnstone, Li, and Luo

Auditing: A Journal of Practice & TheoryNovember 2014

TA

BL

E3

(co

nti

nu

ed)

Va

ria

ble

s

Fu

llS

am

ple

(Ma

x.

n¼

4,5

69

)C

HA

IN_

CIT

Y.

0(M

ax

.n¼

50

9)

CH

AIN

_N

AT

ION

.0

(Ma

x.

n¼

97

9)

CH

AIN

_C

ITY

an

dC

HA

IN_

NA

TIO

N¼

0(M

ax

.n¼

3,0

81

)

Mea

nM

edia

nS

td.

Mea

nM

edia

nS

td.

Mea

nM

edia

nS

td.

Mea

nM

edia

nS

td.

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10

)(1

1)

(12

)

BU

SY_S

EA

SON

t0

.64

31

.00

00

.47

90

.65

21

.00

00

.47

70

.61

81

.00

00

.48

60

.65

61

.00

00

.47

5

LO

NG

_DE

BT

t0

.18

00

.08

70

.30

00

.15

8*

**

0.0

86

**

*0

.21

80

.17

40

.09

00

.26

70

.19

20

.08

70

.33

9

CU

RR

EN

T_L

IAB

ILIT

Yt

0.0

52

0.0

06

0.1

17

0.0

30

**

*0

.00

3*

*0

.06

60

.03

10

.00

30

.07

00

.07

20

.01

10

.14

5

INV

T_R

AT

IOt

0.1

21

0.0

84

0.1

25

0.0

88

**

*0

.05

8*

**

0.0

99

0.1

11

**

*0

.08

1*

**

0.1

10

0.1

37

0.0

99

0.1

38

MO

DIF

IED

_OP

Nt

0.0

63

0.0

00

0.2

43

0.0

31

**

*0

.00

0*

**

0.1

74

0.0

17

**

0.0

00

**

0.1

30

0.1

01

0.0

00

0.3

02

RE

STR

UC

TU

RE

t0

.02

90

.00

00

.16

80

.03

20

.00

0*

0.1

77

0.0

36

0.0

00

0.1

87

0.0

23

0.0

00

0.1

51

SPE

CIA

L_I

TE

Mt

0.6

86

1.0

00

0.4

64

0.7

17

**

*1

.00

00

.45

10

.72

71

.00

00

.44

50

.65

11

.00

00

.47

7

FO

RE

IGN

t0

.24

00

.00

00

.42

70

.28

6*

**

0.0

00

**

*0

.45

20

.29

60

.00

00

.45

70

.19

10

.00

00

.39

3

NU

M_S

EG

t2

.90

82

.00

02

.54

93

.00

0*

1.0

00

**

*2

.82

23

.05

81

.00

02

.73

12

.78

62

.00

02

.33

2

AU

DIT

OR

_TE

NU

RE

t8

.91

26

.00

08

.35

58

.67

4*

**

7.0

00

**

*7

.12

89

.42

97

.00

08

.57

78

.65

76

.00

08

.54

4

logA

UD

ITO

R_T

EN

UR

Et

1.9

26

1.9

46

0.9

17

1.9

73

**

*2

.07

9*

**

0.8

40

1.9

96

2.0

79

0.8

93

1.8

67

1.9

46

0.9

51

CU

STO

ME

R_I

MP

Tt

0.2

11

0.1

60

0.2

51

0.2

37

**

0.1

60

**

*0

.41

60

.20

1*

**

0.1

60

0.1

39

0.2

09

0.1

50

0.2

36

RE

V_C

YC

LE

_IM

PT

t0

.03

10

.02

00

.04

70

.02

5*

**

0.0

15

**

*0

.04

40

.02

8*

**

0.0

19

**

*0

.02

80

.03

40

.02

20

.05

7

*,**,***

Den

ote

signifi

cant

atth

e10

per

cent,

5per

cent,

and

1per

cent

level

s,re

spec

tivel

y,

bas

edon

two-t

aile

dt-

(z-)

test

stat

isti

csfo

rth

edif

fere

nce

sin

the

mea

ns

(med

ian)

val

ues

bet

wee

nC

HA

IN_C

ITY

.0

and

CH

AIN

_NA

TIO

N.

0in

com

par

ison

wit

hC

HA

IN_C

ITY¼

0an

dC

HA

IN_N

AT

ION¼

0,

resp

ecti

vel

y.

aT

he

num

ber

sof

obse

rvat

ions

for

ME

ET

tfo

rth

efu

llsa

mple

,th

eC

HA

IN_C

ITY¼

1an

dC

HA

IN_N

AT

ION

.0

and

the

CH

AIN

_C

ITY

and

CH

AIN

_N

AT

ION¼

0gro

up

are

2,3

91,

411,

840,

and

1,1

40,

resp

ecti

vel

y.

Var

iable

sar

ew

inso

rize

dat

1per

cent

and

99

per

cent

tore

duce

the

effe

ctof

outl

iers

.S

eeA

ppen

dix

Cfo

rvar

iable

defi

nit

ions.

(con

tinu

edo

nn

ext

pa

ge)

Client-Auditor Supply Chain Relationships, Audit Quality, and Audit Pricing 135

Auditing: A Journal of Practice & TheoryNovember 2014

TA

BL

E3

(co

nti

nu

ed)

Pan

elB

:P

ears

on

/Sp

earm

an

Corr

elati

on

Matr

ix(m

ax.

n¼

2,3

91

)

Va

ria

ble

s(1

)(2

)(3

)(4

)(5

)(6

)(7

)(8

)(9

)

(1)jD

AC

Ctj

0.0

30

.02

�0

.06

�0

.03

0.0

9�

0.0

60

.03

0.0

6

(0.0

7)

(0.2

2)

(,0

.01

)(0

.08

)(0

.13

)(,

0.0

1)

(0.0

7)

(,0

.01

)

(2)

RE

STA

TE

t�

0.0

10

.02

�0

.08

�0

.02

0.1

50

.03

�0

.02

0.0

1

(0.7

8)

(0.2

8)

(,0

.01

)(0

.04

)(0

.42

)(0

.07

)(0

.13

)(0

.16

)

(3)

ME

ET

t�

0.0

10

.02

0.1

4�

0.0

2�

0.0

2�

0.0

3�

0.0

3�

0.0

1

(0.5

1)

(0.2

8)

(,0

.01

)(�

0.0

2)

(0.4

2)

(0.0

7)

(0.1

3)

(0.7

1)

(4)

logA

UD

ITF

EE

t�

0.0

1�

0.0

70

.15

0.0

70

.07

0.0

50

.04

0.2

0

(0.9

0)

(,0

.01

)(,

0.0

1)

(0.0

8)

(,0

.01

)(,

0.0

1)

(0.0

6)

(,0

.01

)

(5)

CH

AIN

_CIT

Yt

�0

.05

�0

.01

�0

.01

0.0

80

.33

�0

.01

�0

.06

0.2

0

(,0

.01

)(0

.04

)(0

.08

)(0

.10

)(,

0.0

1)

(0.6

5)

(,0

.01

)(,

0.0

1)

(6)

CH

AIN

_NA

TIO

Nt

�0

.04

0.0

1�

0.0

20

.08

0.2

50

.05

0.0

80

.15

(0.1

2)

(0.5

9)

(0.3

8)

(,0

.01

)(,

0.0

1)

(,0

.01

)(,

0.0

1)

(,0

.01

)

(7)

IND

_NA

TIO

Nt

�0

.03

0.0

30

.01

0.0

40

.02

0.0

5�

0.2

3�

0.4

0

(0.1

6)

(0.0

7)

(0.4

6)

(0.0

3)

(0.3

0)

(,0

.01

)(,

0.0

1)

(,0

.01

)

(8)

IND

_CIT

Yt

�0

.04

�0

.03

0.0

10

.04

�0

.09

0.0

8�

0.2

3�

0.2

7

(0.0

2)

(0.1

3)

(0.5

7)

(0.0

5)

(,0

.01

)(,

0.0

1)

(,0

.01

)(,

0.0

1)

(9)

JOIN

T_I

ND

t0

.02

�0

.07