Embed Size (px)

Citation preview

Audit Committee Charter Status: Approved Date: 2014-03-14 File Reference:

1

Audit & Risk Committee Charter

Status: Approved Custodian: Executive Office Date approved: 2014-03-14 Implementation date: 2014-03-17 Decision number: SAQA 04103/14 Due for review: 2015-03-13 File Number:

Audit Committee Charter Status: Approved Date: 2014-03-14 File Reference:

2

TABLE OF CONTENTS

1. INTRODUCTION ............................................................................................................. 3

2. PURPOSE AND OBJECTIVES ....................................................................................... 3

3. COMPOSITION ............................................................................................................... 4

4. MEETINGS ...................................................................................................................... 5

4.1. Chairperson .......................................................................................................... 5

4.2. Frequency ............................................................................................................. 5

4.3. Attendance ............................................................................................................ 5

4.4. Quorum ................................................................................................................. 6

4.5. Agenda and Minutes ............................................................................................. 6

5. DUTIES ........................................................................................................................... 7

5.1. The Committee shall: ............................................................................................ 7

5.2. Integrated reporting ............................................................................................... 7

5.3. Combined assurance ............................................................................................ 8

5.4. Governance and risk management ....................................................................... 8

5.5. Internal control ...................................................................................................... 9

5.6. Internal Audit ......................................................................................................... 9

5.7. External audit ...................................................................................................... 10

5.8. Fraud .................................................................................................................. 10

5.9. Compliance with laws and regulations ................................................................ 11

5.10. Compliance with the Code of Ethics ................................................................... 11

6. REPORTING ................................................................................................................. 11

7. OTHER .......................................................................................................................... 12

8. AUTHORITY .................................................................................................................. 12

Appendix A: Annual Work Plan of the Audit and Risk Committee

Audit Committee Charter Status: Approved Date: 2014-03-14 File Reference:

3

THE AUDIT AND RISK COMMITTEE CHARTER

1. INTRODUCTION

The Audit and Risk Committee is constituted as a statutory committee in respect of its statutory duties in terms of sections 76 (4)(d) and 77 of the Public Finance Management Act, 1999 and a committee of the Board in respect of all other duties assigned to it by the Board. The duties and responsibilities of the members of the Committee who are Board members are in addition to those as members of the Board. The deliberations of the Committee do not reduce the individual and collective responsibilities of Board members in regard to their fiduciary duties and responsibilities, and they must continue to exercise due care and judgment in accordance with their statutory obligations. The Committee does not assume the functions of management, which remain the responsibility of the Directors and other members of senior management. The Committee has an independent role, operating as an overseer and maker of recommendations to the Board for its consideration and final approval.

2. PURPOSE AND OBJECTIVES

The Committee’s members are appointed by the Board to assist them in fulfilling their fiduciary duties, as well as to advise them about discharging their duties with regard to the operation of adequate systems and financial controls, corporate accountability, and the associated risks in terms of management assurance and financial reporting. The purpose of the Committee is to assist the Board with oversight of:

• The implementation of an effective policy and plan for risk management that will

enhance the Organisation’s ability to achieve its strategic objectives; • The comprehensive, timely and relevant disclosure regarding risk; • The performance of the internal and external audit functions; • Management's responsibilities to ensure that there is in place an effective system of

controls, designed to reasonably : • Safeguard the assets and income of SAQA. • Monitor the operation of adequate systems, including the deliverables as included

in the Annual Performance Plan. • Maintain compliance with the governance frameworks, ethical standards, policies,

plans and procedures, and with laws and regulations. • The review of financial information and ensuring of the integrity of the annual

financial statements.

Audit Committee Charter Status: Approved Date: 2014-03-14 File Reference:

4

3. COMPOSITION

The Board appoints the committee consisting of six members of whom two are non-executive Board members and three are non Board members independent of management. The names of members must be disclosed in the Annual Integrated Report. The members should have the necessary financial expertise in order to properly assist and advise the Committee in the execution of its duties and responsibilities. The Committee may call on expert advice at SAQA's cost in accordance with the SAQA Rules of Procedure. All members of the committee must be suitably skilled and experienced. They must collectively have sufficient qualifications and experience to fulfill their duties including an understanding of the following:

• Financial and sustainability reporting • Internal financial controls • External audit process • Internal audit process • Corporate law • Risk management • Sustainability issues • Information technology governance as it relates to integrated reporting and in

accordance with SAQA’s IT Charter and Governance Framework • Governance processes within SAQA

Members must keep up to date with developments affecting the required skill set. Committee members must express opinions, exercise judgment and make decisions impartially, and may not be:

• involved in the day-to-day management of SAQA’s business or have been so involved at any time during the previous financial year;

• a prescribed officer, or full-time employee, of SAQA or have been such an officer or employee at any time during the previous three financial years; or

• a material supplier or customer of SAQA, such that a reasonable and informed third party would conclude in the circumstances that the integrity, impartiality or objectivity of that member is compromised by that relationship; and

• not be related to any person who falls within any of the criteria set out above.

The Board appoints the members of the Committee and the chairperson for the term of the Board subject to periodic review, and may remove any member from the Committee for good reason. Committee members shall not be eligible to serve on the Committee once they are deemed to be no longer able to act independently. Neither the appointment nor the duties of the Committee reduce the functions and duties of the Board or the directors.

Audit Committee Charter Status: Approved Date: 2014-03-14 File Reference:

5

The Chairperson of the Board shall not be a member of the Committee. The performance of the Committee and the individual members will be assessed by annual performance assessment or appraisal. New members receive an induction programme that allows them to function effectively. Committee members are required to obtain an ongoing understanding of SAQA, its business and products, an understanding of the industry sector, and knowledge of its risks and controls. The members of the Committee will be remunerated for the services at the level approved from time to time by the Minister, through the Board (treasury guidelines).

4. MEETINGS

4.1. Chairperson

The Chairperson should possess the characteristics mentioned in paragraph 3 above as well as strong leadership qualities, objectivity, and the ability to promote effective working relations among Committee members and with others such as management and internal and external auditors.

4.2. Frequency

The Committee must hold sufficient meetings to fulfill its statutory duties and fully discharge all aspects of the charter, subject to a minimum of three meetings per annum. The Committee Chairperson will formally report to the Board on the activities of the Committee at relevant Board meetings. Additional Committee meetings may be held, with the approval of the Chairperson, at the request of a member or the external auditors, the internal auditors, or at the request of the Board or of management. At least annually, the Committee shall meet separately with management, and the external and internal auditors.

4.3. Attendance

If the appointed Chairperson of the Committee is absent from a meeting, the members present shall elect one of their members, not being a Board member, to act as Chairperson. The following will normally be in attendance at Committee meetings by invitation only:

Audit Committee Charter Status: Approved Date: 2014-03-14 File Reference:

6

• Chief Executive Officer • Chief Financial Officer • Representatives from the internal auditors (including the person responsible for

signing the internal audit reports) • Representatives from the external auditors (including the person responsible for

the audit, i.e. the designated auditor); and • Other assurance providers as required (e.g. risk, legal counsel, forensics and

governance) • Any other assurance providers (e.g. senior executives and professional advisers)

as deemed appropriate by the Committee, may also be in attendance as required by invitation only.

The Chairperson of the Committee may invite the Chairperson of the Board and any other Board member to attend all or part of a Committee meeting, even though they are not members of the Committee. The Committee will have the authority to exclude any conflicted member or other attendee from meetings for the duration of a specific meeting or item under discussion if it believes there is sufficient reason or justification for doing so. A person designated by the Chief Executive Officer will act as the secretary to the Committee.

4.4. Quorum

A quorum for Committee meetings will comprise fifty percent plus 1 of the members. Individuals in attendance at Committee meetings by invitation may participate in discussions but do not form part of the quorum for Committee meetings and may not vote on any matter.

4.5. Agenda and Minutes

The Committee must establish a plan for each year to ensure that all relevant matters are covered by the agendas of the meetings planned for the year. From this plan, the number, timing and length of meetings and the agendas can be determined. The annual plan should ensure proper coverage of the matters laid out in the Committee Charter: the more critical matters will need to be attended to each year while other matters may be dealt with on a rotation basis over a three-year period. The Committee Annual Plan is a guideline to assist in planning effective meetings, and is not intended to be a comprehensive checklist. Normally four meetings are held each year, concentrating on the following:

• Pre-audit planning (normally in March) • Post-audit review (normally in June) • Consideration of Strategic Plan and Budget (normally in August)

Audit Committee Charter Status: Approved Date: 2014-03-14 File Reference:

7

• Other Matters (normally in November) The Annual Plan is attached as Appendix A. The agenda shall be circulated with supporting documentation at least five working days prior to each meeting to the members of the Committee and where applicable, other invited attendees. The minutes shall be completed as soon as reasonably practicable after the meeting and sent to the Chairperson of the meeting for comment.

5. DUTIES

In seeking to satisfy the broad objectives set out above, the Committee shall address its duties as outlined below.

5.1. The Committee shall: • Receive and deal appropriately with any concerns or complaints, whether from

within or outside SAQA, or on its own initiative, relating to � the accounting practices and internal audit of SAQA � the content or auditing of SAQA’s financial statements � the internal financial controls of SAQA or � any related matter

• Make submissions to the Board on any matter concerning SAQA’s accounting

policies, financial control, records and reporting.

5.2. Integrated reporting

The committee must oversee integrated reporting and in particular must:

• Have regard to all factors and risks that may impact on the integrity of the annual integrated report, including factors that may predispose management to present a misleading picture, significant judgments and reporting decisions made. It must also have regard to any evidence that brings into question previously published information.

• Comment in the annual integrated report on the financial statements, the accounting policies and practices and the effectiveness of the internal financial controls.

• Review the annual integrated report and disclosure of sustainability issues and performance information in the report to ensure that it is reliable and does not conflict with the financial information.

• Recommend to the Board whether or not to engage an external assurance provider on material sustainability issues.

• Review and consider the audit report and annual financial statements; • Recommend to the Board whether or not it should adopt the annual financial

statements;

Audit Committee Charter Status: Approved Date: 2014-03-14 File Reference:

8

• Consider the impact of any unusual or abnormal transactions necessary for a proper understanding of SAQA's operations;

• Consider the impact of any material litigation and claims; • Review the going concern status of SAQA and minute it as such; • Consider the adequacy of disclosure of significant or unusual commitments or

contingencies; and • After considering all the above matters recommend the annual integrated report

for approval by the Board.

5.3. Combined assurance

The Committee must monitor that a combined assurance Framework and an annual Combined Assurance Plan is applied to provide a coordinated approach to all assurance activities, and in particular the committee must:

• Oversee that the combined assurance received is appropriate to address all the

significant risks facing the Board; • Monitor the relationship between the external assurance providers and the

Organisation; • Evaluate the suitability of the expertise and experience of the Director: Finance

and Administration and recommend to the Board if any changes are necessary.

5.4. Governance and risk management

• Oversee the development and annual review of a policy and plan for risk management including fraud and IT risks, to recommend for approval to the Board;

• Monitor implementation of the policy and plan for risk management taking place by means of risk management systems and processes;

• Make recommendations to the Board concerning the levels of tolerance and appetite, and monitoring that risks are managed within the levels of tolerance and appetite as approved by the Board;

• Oversee that the risk management plan is widely disseminated throughout the Organisation and integrated in the day-to-day activities of the Organisation;

• Oversee that risk management assessments are performed on a continuous basis;

• Oversee that frameworks and methodologies are implemented to increase the possibility of anticipating unpredictable risks;

• Oversee that management considers and implements appropriate risk responses;

• Oversee that continuous risk monitoring by management takes place. • Oversee the risk areas of operations to be covered in the scope of the internal

and external audits; • Oversee compliance by management of good governance principles. • Express the Committee’s formal opinion to the Board on the effectiveness of the

system and process of risk management; and • Review reporting concerning risk management that is to be included in the

integrated report for it being timely, comprehensive and relevant.

Audit Committee Charter Status: Approved Date: 2014-03-14 File Reference:

9

5.5. Internal control

In terms of internal control, the Committee shall:

• Oversee the effectiveness and completeness of the internal control environment; • Review management's and the internal auditor's reports on the effectiveness of

the systems for internal financial control, financial reporting and risk management;

• Review the response of management to reported weaknesses in internal, operating and financial controls; and management information systems and the safeguarding of assets, and the proposed remedial action. Major differences of opinion between the internal and external audit and management are to be specifically brought to the attention of the Committee; and

• In liaison with the external auditors, internal auditors and senior management, consider whether there were any material breakdowns in internal controls such as to warrant inclusion in the corporate governance statement in the integrated report.

5.6. Internal Audit

In terms of the internal audit, the Committee shall:

• Assess the performance of the outsourced internal audit service provider and appoint or remove such;

• Review and recommend the internal audit charter for approval by the Board ; • Approve the scope and plan of the internal audit function, taking into account the

audit plan of the external auditor. • Oversee that the internal audit function is adequately resourced and has

appropriate standing within SAQA; • Ensure that the internal auditor has direct access to the Committee Chairperson

and, where there is conflict, the Board Chairperson; • Receive a report on and review the results of the internal auditor's work on a

periodic basis, ensuring the plan is followed and that the internal audit is not being utilised to undertake unauthorised work;

• Review and monitor management's responsiveness to the internal auditor's findings and recommendations;

• Monitor and assess the role and effectiveness of the internal audit function in the overall context of the risk management system;

• Review the intention, direction and effectiveness of the internal audit service provider; and

• Meet separately with the auditor, without management, at least once a year. • Approve the internal audit fees

Audit Committee Charter Status: Approved Date: 2014-03-14 File Reference:

10

5.7. External audit

In terms of the external audit, the Committee shall:

• Discuss with the external auditor, before the audit commences, the nature and scope of the audit;

• Review and monitor management’s responsiveness to the external auditor’s findings and recommendations;

• Review and discuss with the external auditor: • the findings of their work; • any major issues that arose during the course of the audit that have

subsequently been resolved, and those that have been left unresolved; • key accounting and audit judgments; • levels of errors identified during the audit; • errors that have remained unadjusted;

• Review the audit representation letters before submission to the Board, giving particular consideration to matters that relate to non-standard issues;

• Assess at the end of the audit cycle, the quality and effectiveness of the audit process by: • reviewing whether the auditor has met the agreed audit plan, and

understanding the reasons for the changes, including changes in perceived audit risks and the work undertaken by the external auditors to address those risks;

• reviewing and approving the fees charged by the external auditor; • considering the robustness and perceptiveness of the auditors in their

handling of the key accounting and auditing judgments identified and in responding to questions from the Committee, and in their commentary, where appropriate, on the systems of internal control;

• obtaining feedback about the conduct of the audit from key people involved; and

• reviewing the content of the external auditor's management letter in order to assess whether it is based on proper understanding of SAQA's business, and establishing whether recommendations have been acted upon and, if not, reasons for this.

• Encourage co-operation with the internal auditor • Meet separately with the auditor, without management, at least once year.

5.8. Fraud • Assess, monitor and influence the tone at the top and reinforce a zero-tolerance

policy for fraud; • Evaluate management’s process and procedures for:

• The identification and mitigation of fraud risk, including the measures implementation by management designed to help detect and prevent fraud;

• Screening potential employees, including monitoring whether or not background checks are performed;

• Making significant estimates used in the financial reporting process; and • The processing of manual journal entries and reporting cycle closing process;

Audit Committee Charter Status: Approved Date: 2014-03-14 File Reference:

11

• Provide oversight to management’s internal controls and contemplate the potential for management override of, or inappropriate influence over, those controls;

• Compare the reasonableness of financial results with prior or forecast results and consider quarterly analysis of cash reserves;

• Monitor the whistleblower process; and • Provide other insight into and guidance on implementing or strengthening fraud

prevention and detection measures. Should a report, whether from the internal auditor or from any other source implicate the accounting officer or Board in transactions related to fraud, corruption, or gross negligence, the Chairperson of the Committee, after investigation and consultation with the Audit and Risk Committee must promptly and in writing report this to the Minister of Higher Education and Training and to National Treasury, and inform the Board.

5.9. Compliance with laws and regulations • Review the effectiveness of the system for monitoring compliance with laws and

regulations (in particular the Public Finance Management Act and the Regulations made there under) and the results of management’s investigation and follow-up (including disciplinary action) of any fraudulent acts or accounting irregularities.

• Obtain regular updates from management regarding compliance matters, where necessary.

• Be satisfied that all regulatory compliance matters have been considered in the preparation of the financial statements.

• Review the findings of any examinations by regulatory agencies. • Oversee the governance processes including those relating to information

technology.

5.10. Compliance with the Code of Ethics • Oversee that the Code is in writing and that arrangements are made for all Board

members and employees to be aware of it. • Evaluate whether management is setting the appropriate “tone at the top” by

communicating the importance of the Code. • Review the process for monitoring compliance with the code. • Obtain regular updates from management regarding compliance.

6. REPORTING

• The Committee shall prepare a report for inclusion in the annual financial statements, including whether or not it adopted formal terms of reference and if so, whether or not it satisfied its responsibilities in compliance therewith.. Such a report must be in accordance with the format approved by the Committee annually.

• The Committee shall prepare a report on the effectiveness of the internal control system;

• Review the expertise, resources and experience of the Organisation’s finance function, and disclose the results of the review in the integrated report; and

Audit Committee Charter Status: Approved Date: 2014-03-14 File Reference:

12

• The Committee shall report to the Board after each meeting on its activities and critical issues, including compliance with the charter.

7. OTHER

The Committee has other responsibilities which are to:

• Monitor issues raised by, amongst others: • other committees, and • management;

• Perform other oversight functions as determined by the Board; • If necessary, institute special investigations and, if appropriate, hire special counsel

or experts to assist in accordance with the SAQA Rules of Procedure; and • Review the Committee Charter annually.

8. AUTHORITY In terms of its authority:

• The Committee acts in terms of its statutory duties and the delegated authority of the Board as recorded in the Committee Charter. It has the power to investigate any activity within its terms of reference;

• The Committee will have access to SAQA's records, facilities and any other information and resources necessary to discharge its duties and responsibilities. It must safeguard all the information supplied to it within the ambit of the law.; and

• The Committee may form, and delegate authority to, subcommittees and may delegate authority to one or more designated members of the Committee.

Annual Work Plan of the Audit and Risk Committee Status: Approved Date: 2014-03-14

File Reference:

APPENDIX A ___________________________________________________________________

Annual Work Plan of the Audit and Risk Committee

Annual Work Plan of the Audit and Risk Committee Status: Approved Date: 2014-03-14

File Reference: 2

Content:

1.INTRODUCTION…………………………………………………………………………….3

2.PURPOSE………………………………………………………………………………..…..3

3.WORK PLAN………………………………………………………………………………...3

1.General ................................................................................................................ 3

2.Integrated Reporting .......................................................................................... 3

3.Combined Assurance ........................................................................................ 4

4.Risk Management: ............................................................................................. 4

5.Internal Control .................................................................................................. 5

6.Internal Audit ...................................................................................................... 6

7.External Audit ..................................................................................................... 6

8.Fraud ................................................................................................................... 7

9.Compliance with Laws and Regulations .......................................................... 8

10.Compliance with the Code of Ethics .............................................................. 8

11.Reporting .......................................................................................................... 8

12.Other Responsibilities: .................................................................................... 9

Annual Work Plan of the Audit and Risk Committee Status: Approved Date: 2014-03-14

File Reference: 3

ANNUAL WORK PLAN FOR THE AUDIT AND RISK COMMITTEE

1. INTRODUCTION According to paragraph 4.5 of the Charter of the Audit and Risk Committee, the Committee must establish a plan for each year to ensure that all relevant matters are covered by the agendas of the meetings planned for the year. From this plan, the number, timing and length of meetings and the agendas can be determined.

2. PURPOSE The purpose of the Committee annual plan is to ensure proper coverage of the matters laid out in the Committee Charter. The Annual Plan is a guideline to assist in planning effective meetings, and is not intended to be a comprehensive checklist. Normally four meetings are held each year, concentrating on the following:

• Meeting 1: March Pre-audit planning • Meeting 2: June Review of the Annual Integrated Report and the

post-audit review • Meeting 3: August Consideration of Strategic Plan and Budget • Meeting 4: November Other Matters

3. WORK PLAN

DUTIES OF THE AUDIT AND RISK COMMITTEE

MEETING 1 2 3 4

1. General The Committee shall 1.1 Receive and deal appropriately with any concerns or

complaints, whether from within or outside SAQA, or on its own initiative, relating to

• the accounting practices and internal audit of SAQA • the content or auditing of SAQA’s financial statements • the internal financial controls of SAQA or any related matter

As required

1.2 Make submissions to the Board on any matter concerning SAQA’s accounting policies, financial control, records and reporting

As required

2. Integrated Reporting The committee must oversee integrated reporting and in particular must: • Have regard to all factors and risks that may impact on the

integrity of the annual integrated report, including factors that

Annual Work Plan of the Audit and Risk Committee Status: Approved Date: 2014-03-14

File Reference: 4

DUTIES OF THE AUDIT AND RISK COMMITTEE

MEETING 1 2 3 4

may predispose management to present a misleading picture, significant judgments and reporting decisions made. It must also have regard to any evidence that brings into question previously published information.

• Comment in the annual integrated report on the financial statements, the accounting policies and practices and the effectiveness of the internal financial controls.

• Review the annual integrated report and disclosure of sustainability issues and performance information in the report to ensure that it is reliable and does not conflict with the financial information.

• Recommend to the Board whether or not to engage an external assurance provider on material sustainability issues.

• Review and consider the audit report and annual financial statements;

• Recommend to the Board whether or not it should adopt the annual financial statements;

• • Consider the impact of any unusual or abnormal transactions

necessary for a proper understanding of SAQA's operations; • Consider the impact of any material litigation and claims; • Review the going concern status of SAQA and minute it as

such. • Consider the adequacy of disclosure of significant or unusual

commitments or contingencies. • After considering all the above matters recommend the

annual integrated report for approval by the Board.

� �

3. Combined Assurance The Committee must ensure that a combined assurance model is applied to provide a

coordinated approach to all assurance activities, and in particular the committee must:

3.1 Oversee that the combined assurance received is appropriate to address all the significant risks facing the Board

� �

3.2 Monitor the relationship between the external assurance providers and the Organisation � �

3.4 Evaluate the suitability of the expertise and experience of the Director: Finance and Administration and recommend to the Board if any changes are necessary

� �

4. Governance and Risk Management: The Committee must: 4.1 Oversee the development and annual review of a policy and

plan for risk management including fraud and IT risks, to recommend for approval to the Board.

�

Annual Work Plan of the Audit and Risk Committee Status: Approved Date: 2014-03-14

File Reference: 5

DUTIES OF THE AUDIT AND RISK COMMITTEE

MEETING 1 2 3 4

4.2 Monitor implementation of the policy and plan for risk management taking place by means of risk management systems and processes

� � � �

4.3 Make recommendations to the Board concerning the levels of tolerance and appetite, and monitoring that risks are managed within the levels of tolerance and appetite as approved by the Board.

�

4.4 Oversee that the risk management plan is widely disseminated throughout the Organisation and integrated in the day-to-day activities of the Organisation

� �

4.5 Oversee that risk management assessments are performed on a continuous basis. � �

4.6 Oversee that frameworks and methodologies are implemented to increase the possibility of anticipating unpredictable risks �

4.7 Oversee that management considers and implements appropriate risk responses � � � �

4.8 Ensure that continuous risk monitoring by management takes place

� � � �

4.9 Oversee the risk areas of operations to be covered in the scope of the internal and external audits �

4.10 Oversee compliance by management of good governance principles � � � � 4.11 Express the Committee’s formal opinion to the Board on the

effectiveness of the system and process of risk management �

4.12 Review reporting concerning risk management that is to be included in the integrated report for it being timely, comprehensive and relevant

�

5. Internal Control In terms of internal control, the Committee shall: 5.1 Oversee the effectiveness and completeness of the internal

control environment � � �

5.2 Review management's and the internal auditor's reports on the effectiveness of the systems for internal financial control, financial reporting and risk management

� � � �

5.3 Review the response of management to reported weaknesses in internal, operating and financial controls; and management information systems and the safeguarding of assets, and the proposed remedial action. Major differences of opinion between the internal and external audit and management are to be specifically brought to the attention of the Committee

� � � �

5.4 In liaison with the external auditors, internal auditors and senior management, consider whether there were any material breakdowns in internal controls such as to warrant inclusion in the corporate governance statement in the integrated report

�

Annual Work Plan of the Audit and Risk Committee Status: Approved Date: 2014-03-14

File Reference: 6

DUTIES OF THE AUDIT AND RISK COMMITTEE

MEETING 1 2 3 4

6. Internal Audit In terms of the internal audit, the Committee shall: 6.1 Assess the performance of the outsourced internal audit service

provider and appoint or remove such �

6.2 Review and recommend the internal audit charter for approval by the Board �

6.3 Approve the scope and plan of the internal audit function taking into account the audit plan of the external auditor, and ensure that the internal audit function is adequately resourced and has appropriate standing within SAQA

�

6.4 Ensure that the internal auditor has direct access to the Committee Chairperson and, where there is conflict, the Board Chairperson Receive a report on and review the results of the internal auditor's work on a periodic basis, ensuring the plan is followed and that the internal audit is not being utilised to undertake unauthorised work

�

6.5 Receive a report on and review the results of the internal auditor's work on a periodic basis, ensuring the plan is followed and that the internal audit is not being utilised to undertake unauthorised work

� � � �

6.6 Review and monitor management's responsiveness to the internal auditor's findings and recommendations

� � � �

6.7 Monitor and assess the role and effectiveness of the internal audit function in the overall context of the risk management system

�

6.8 Review the intention, direction and effectiveness of the internal audit service provider �

6.9 Meet separately with the auditor, without management, at least once a year �

6.10 Approve the internal audit fees �

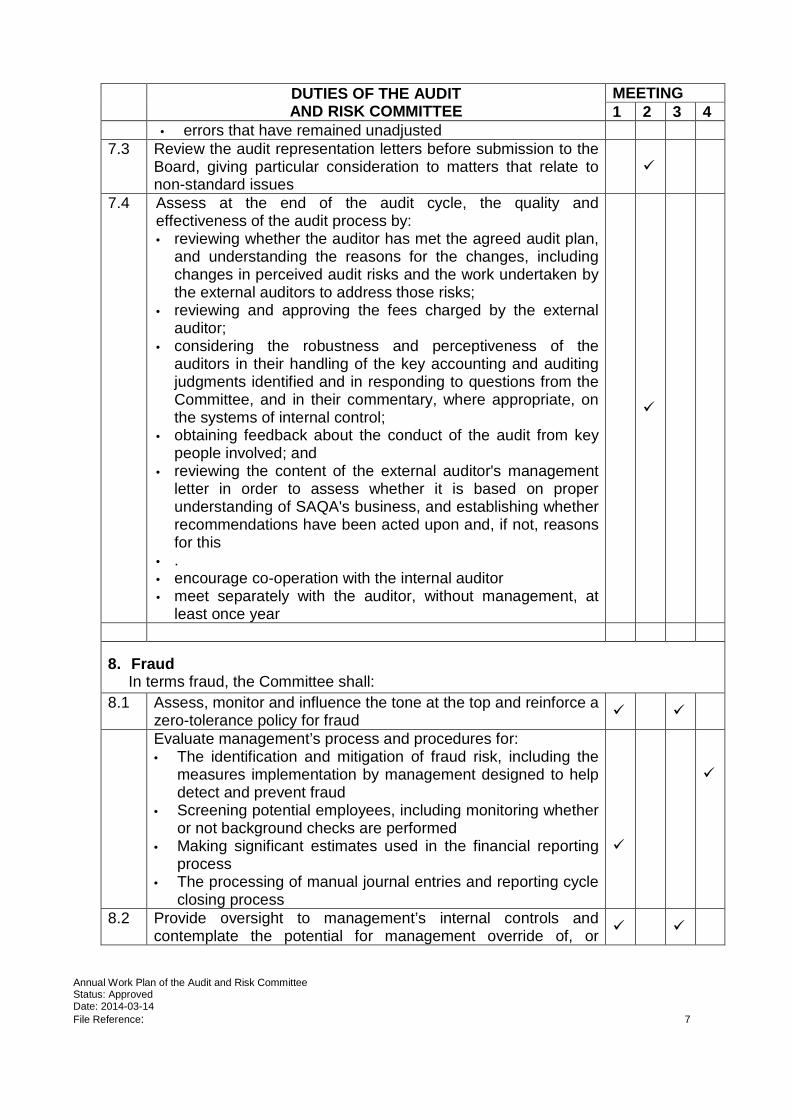

7. External Audit In terms of the external audit, the Committee shall: 7.1 Discuss with the external auditor, before the audit commences,

the nature and scope of the audit �

Review and monitor management’s responsiveness to the external auditor’s findings and recommendations �

7.2 Review and discuss with the external auditor: • the findings of their work; • any major issues that arose during the course of the audit

that have subsequently been resolved, and those that have been left unresolved;

• key accounting and audit judgments; • levels of errors identified during the audit;

�

Annual Work Plan of the Audit and Risk Committee Status: Approved Date: 2014-03-14

File Reference: 7

DUTIES OF THE AUDIT AND RISK COMMITTEE

MEETING 1 2 3 4

• errors that have remained unadjusted 7.3 Review the audit representation letters before submission to the

Board, giving particular consideration to matters that relate to non-standard issues

�

7.4 Assess at the end of the audit cycle, the quality and effectiveness of the audit process by: • reviewing whether the auditor has met the agreed audit plan,

and understanding the reasons for the changes, including changes in perceived audit risks and the work undertaken by the external auditors to address those risks;

• reviewing and approving the fees charged by the external auditor;

• considering the robustness and perceptiveness of the auditors in their handling of the key accounting and auditing judgments identified and in responding to questions from the Committee, and in their commentary, where appropriate, on the systems of internal control;

• obtaining feedback about the conduct of the audit from key people involved; and

• reviewing the content of the external auditor's management letter in order to assess whether it is based on proper understanding of SAQA's business, and establishing whether recommendations have been acted upon and, if not, reasons for this

• . • encourage co-operation with the internal auditor • meet separately with the auditor, without management, at

least once year

�

8. Fraud In terms fraud, the Committee shall: 8.1 Assess, monitor and influence the tone at the top and reinforce a

zero-tolerance policy for fraud � �

Evaluate management’s process and procedures for: • The identification and mitigation of fraud risk, including the

measures implementation by management designed to help detect and prevent fraud

• Screening potential employees, including monitoring whether or not background checks are performed

• Making significant estimates used in the financial reporting process

• The processing of manual journal entries and reporting cycle closing process

�

�

8.2 Provide oversight to management’s internal controls and contemplate the potential for management override of, or

� �

Annual Work Plan of the Audit and Risk Committee Status: Approved Date: 2014-03-14

File Reference: 8

DUTIES OF THE AUDIT AND RISK COMMITTEE

MEETING 1 2 3 4

inappropriate influence over, those controls 8.3 Compare the reasonableness of financial results with prior or

forecast results and consider quarterly analysis of cash reserves � � � �

8.4 Monitor the whistleblower process � 8.5 Provide other insight into and guidance on implementing or

strengthening fraud prevention and detection measures �

Should a report, whether from the internal auditor or from any other source implicate the accounting officer or Board in transactions related to fraud, corruption, or gross negligence, the Chairperson of the Committee must promptly and in writing report this to the Minister of Higher Education and Training and to National Treasury

9. Compliance with Laws and Regulations In respect of compliance with laws and regulations, the Committee shall: 9.1 Review the effectiveness of the system for monitoring

compliance with laws and regulations (in particular the Public Finance Management Act and the Regulations made there under) and the results of management’s investigation and follow-up (including disciplinary action) of any fraudulent acts or accounting irregularities

� �

9.2 Obtain regular updates from management regarding compliance matters, where necessary �

9.3 Be satisfied that all regulatory compliance matters have been considered in the preparation of the financial statements �

9.4 Review the findings of any examinations by regulatory agencies � 9.5 Oversee the governance processes including those relating to

information technology �

10. Compliance with the Code of Ethics In terms of the Code of Ethics, the Committee shall: 10.1 Oversee that the Code is in writing and that arrangements are

made for all Board members and employees to be aware of it �

10.2 Evaluate whether management is setting the appropriate “tone at the top” by communicating the importance of the Code

�

10.3 Review the process for monitoring compliance with the co � 10.4 Obtain regular updates from management regarding compliance �

11. Reporting The Committee shall: 11.1 Prepare a report for inclusion in the annual financial statements,

including whether or not it adopted formal terms of reference and if so, whether or not it satisfied its responsibilities in compliance therewith

�

11.2 Report to the Board after each meeting on its activities and critical issues, including compliance with the charter � � � �

Annual Work Plan of the Audit and Risk Committee Status: Approved Date: 2014-03-14

File Reference: 9

DUTIES OF THE AUDIT AND RISK COMMITTEE

MEETING 1 2 3 4

11.3 Prepare a report on the effectiveness of the internal control system

�

Review the expertise, resources and experience of the Organisation’s finance function, and disclose the results of the review in the integrated report

12. Other Responsibilities: � � � 12.4 Monitor issues raised by, amongst others:

• other committees • management

�

12.5 Perform other oversight functions as determined by the Board � 12.6 If necessary, institute special investigations and, if appropriate,

hire special counsel or experts to assist, in accordance with SAQA’s rules of procedure

�

12.7 Meet separately with management � 12.8 Review the Committee Charter annually � 12.9 Carry a self assessment of the performance of the Committee �

Annual Work Plan of the Audit and Risk Committee Status: Approved Date: 2014-03-14

File Reference: 10